Embed Size (px)

Citation preview

CHAPTER V

CRITERIA FOR INVESTMENT DECISIONS A N D

RISK MANAGEMENT

Though it is acknowledged to be risky, investing in corporate

securities is now considered to be one of the generally accepted options

of savings management. A large chunk of the savings of the country

finds its way to the stock: markets. Investment in corporate securities

offers income in the form of dividend and interest along with capital

appreciation. Judiciously made investment in shares offers liquidity

also. Investing, however, entails risks, but it can be moderated by

rational and prudent investment decisions. Risk management has

become imperative for investment management. In India, the current

gloomy corporate scenario and the extremely volatile capital markets

have brought risk management to the core of investment decisions.

The more astute and clever investors can take the right investment

decisions to produce the extra reward. In this chapter, an attempt is

made to analyse the criteria for investment decisions and how they are

helpful in countering and reducing risks.

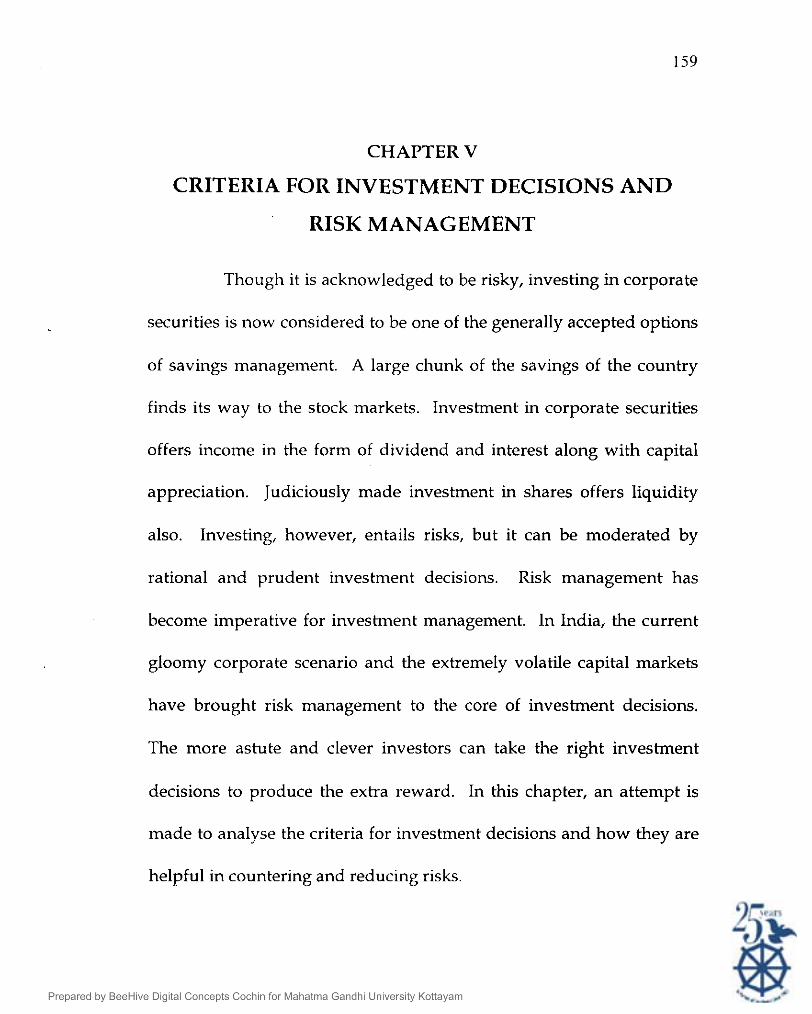

Investment in shares

Table 5.1

Source : Field survey

Investment in shares -(Zonal break-up)

Investment in shares as r No of respondents I/ I

As revealed by table 5.1, 62% of the respondents have

percentage of total

savlngs zone Zone Zone

Zero 9 10 16 35

1 - 25 24 24 96

invested 50% or less of their savings in the capital market. About 12%

Percentage

11.7

32

of the investors kept themselves away from the market without

investing a single rupee in shares. Only 27% of the investors have put

25 - 50 56 j 18.7

more than 75% of their savings in shares. Numerous stock scams and

50 - 75

75 - YO 18 3 27

YO - 100 14 53

Total 150 75 300

political instability frequently haunt the markets. The resulting

11

9

17.6

100

apprehensions and fears of investors are translated into dampened

sentiment in the market. The frequent roller coaster rides of the capital

market further wither investor confidence. While the economy is

craving for funds for its development, the flow of funds from within

the country is blocked by the loss of investor confidence. New

measures are required to improve integrity of the market, enhance its

safety and build investor confidence.

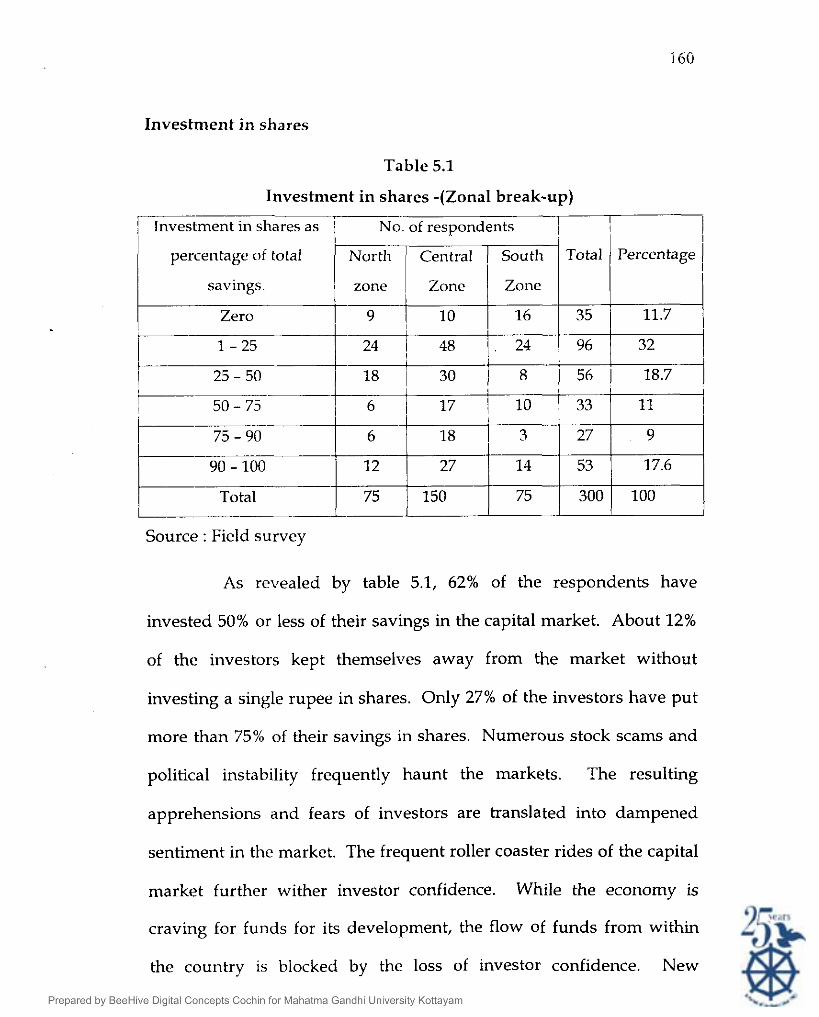

Experience of investors in stock market operations

Experience is of great value, which influences the investment

decisions. Correlation is worked out to find out the relation between

experience of investors and their investment in shares.

Correlntioll betrcreerz experieilce of inzrestors in the stock iilnrket

operntiorzs nild tlzeir ii~oestnrent ill sl~ares

Table-5.2

Investment in shares and experience of investors in

stock market operations

Source : Field Survey

Correlation coefficient (r) = - 0.1395

A very low negative correlation exists between experience in

stock market operations and investment in shares. We can conclude

that increase in experience will not bring additional investment in

shares. That is, the Indian Capital Market is not providing sufficient

support, encouragement and safety to the investors. The experienced

investors are wary of locking up their savings in the stock market.

Investment in Primary Market and Secondary Market

Primary market is the new issues market (NIM), which helps

the corporate sector to raise funds for their new projects, expansions,

modernisation, etc. The NIM deals with new securities, that is

securities, which are offered to the public for the first time. The

secondary market on the other hand, is a market for old securities, that

is, those, which have already been issued and have been granted stock

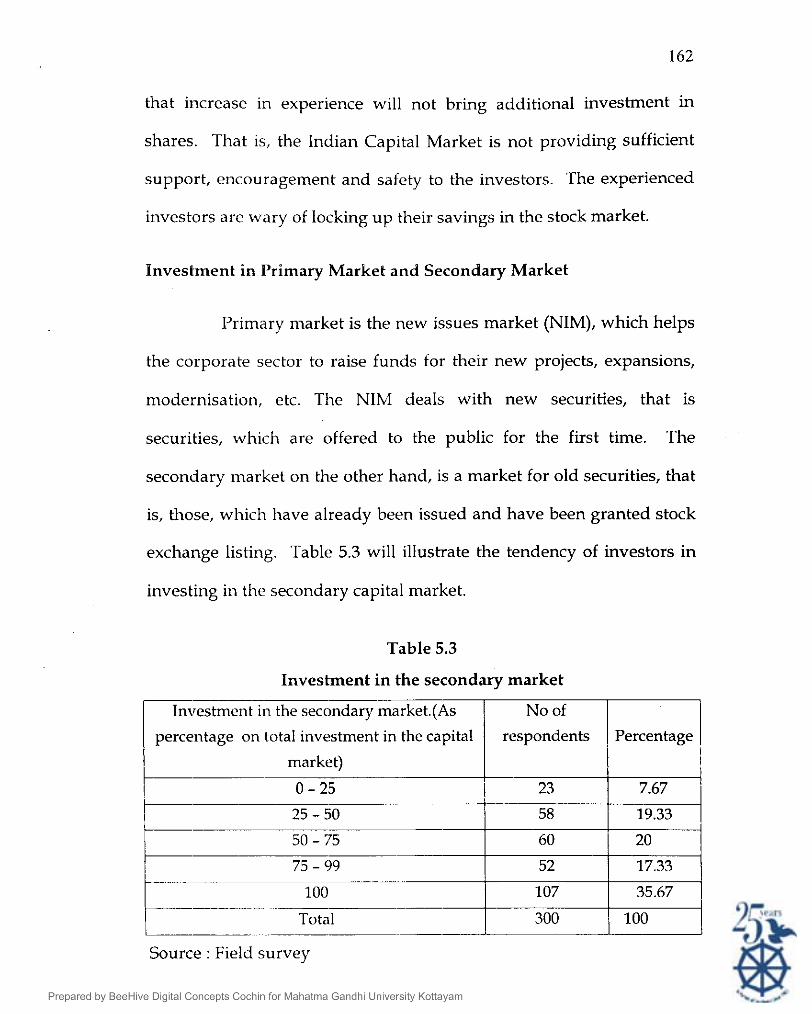

exchange listing. Table 5.3 will illustrate the tendency of investors in

investing in the secondary capital market.

Table 5.3

Source : Field survey

Investment in the secondary market

Investment in the secondary market.(As

percentage on total investment in the capital r market) + No of

respondents Percentage I I

I 0 - 25 1 23 I-P 25 - 5 0 I I 58

7.67

19.33

Seventy three per cent of the investors have directed the major

part (more than 50%) of their inveslent into the secondary market.

This explains their preference to operate in the secondary market rather

than applying for new issues. About 36% of the investors make no

investment in the primary market, as their entire investment is in the

secondary market. This reflects the fading confidence of investors in the

primary market. According to capital market analysts the primary

market is dead. The cause for the debacle is attributable to the low

quality of 1.P.Os (Initial Public Offers) that swamped the capital market

and the unscrupulous promoters who duped the investors by telling

great stories about companies. In the 100 largest issues between 1992

and 1996, 72% of the amount has been lost.' The issue really is of

investors' confidence, which is totally shaken. These days very few

1.P.Os are coming up in the market. These show that immediate

measures are to be taken to review the market.

Debt beats equity in the primaries

Investor interest in equity issues is waning. The trend is

reflected in substantially higher mobilization of funds through debt

issues compared to equity issues during the past few years.

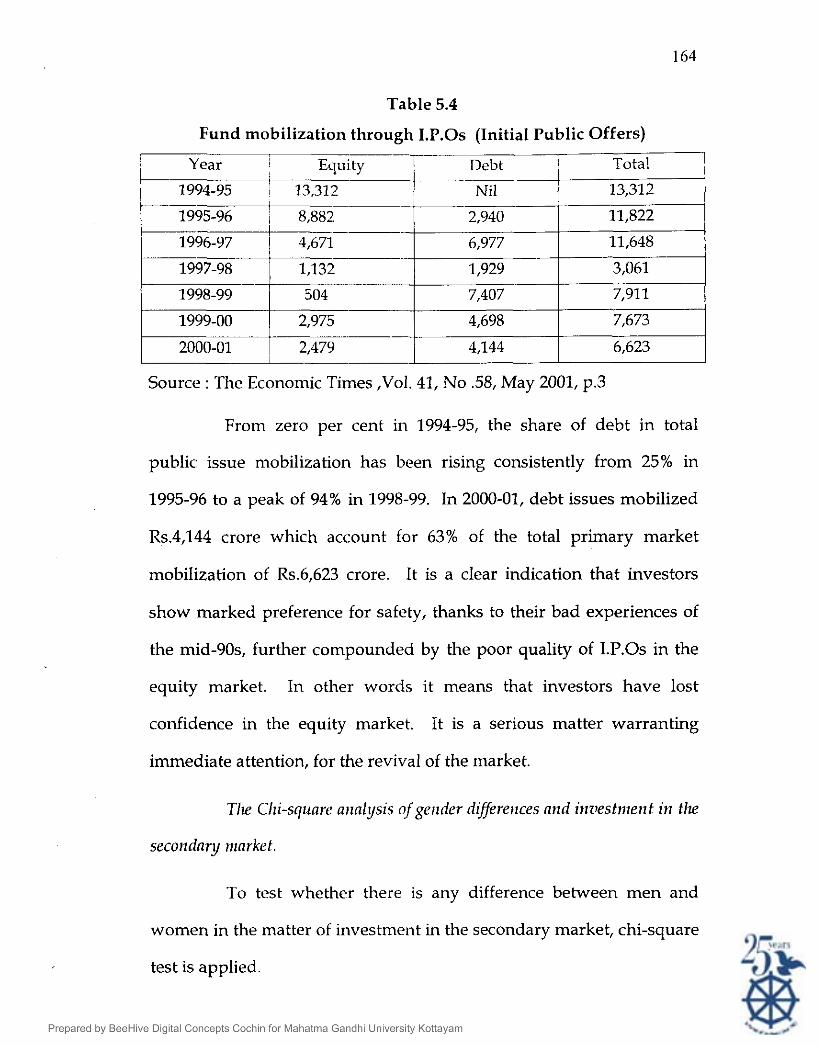

Table 5.4

Fund mobilization through 1.P.Os (Initial Public Offers)

Equity I Debt I Tota! I

1 1994-95 I 13,31Fp ! Nil I 13,312 1

Source : The Economic Times ,Vol. 41, No .58, May 2001, p.3

From zero per cent in 1994-95, the share of debt in total

public issue mobilization has been rising consistently from 25% in

1995-96 to a peak of 94% in 1998-99. In 2000-01, debt issues mobilized

Rs.4,144 crore which account for 63% of the total primary market

mobilization of Rs.6,623 crore. It is a clear indication that investors

show marked preference for safety, thanks to their bad experiences of

the mid-90s, further compounded by the poor quality of I.P.Os in the

equity market. In other words it means that investors have lost

confidence in the equity market. It is a serious matter warranting

immediate attention, for the revival of the market.

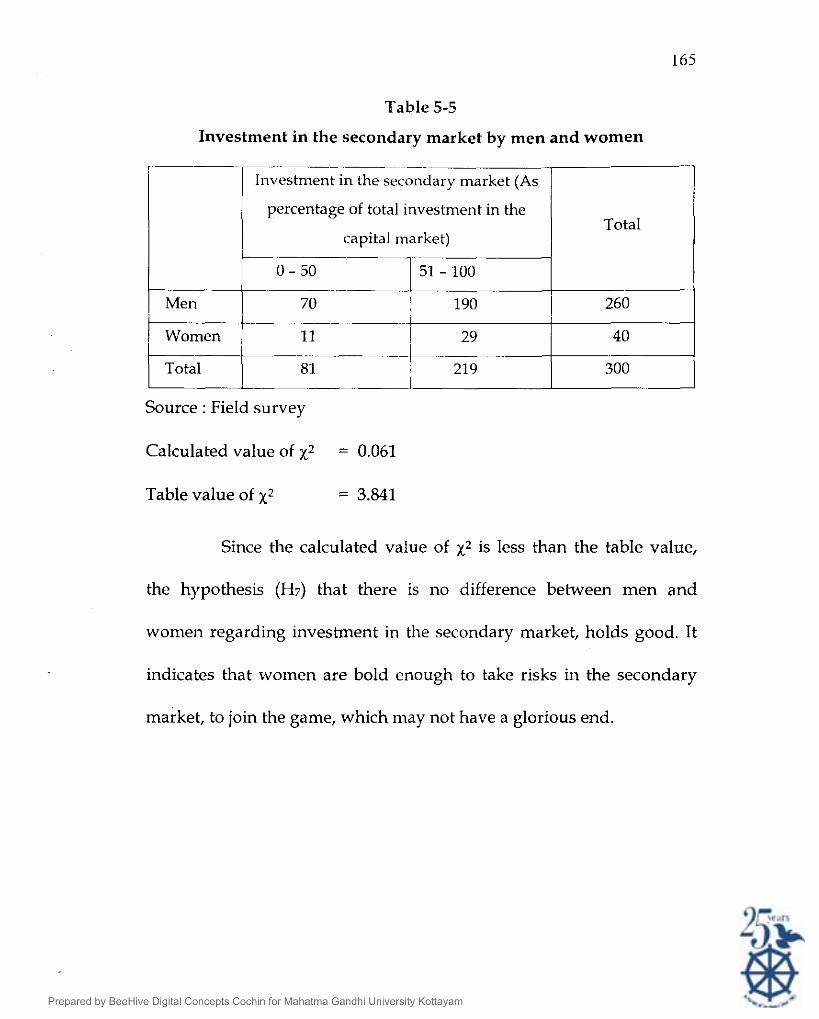

Tlle Chi-square arlnlysis ofgerlder diflerences and inz~estnzent in the

secorldary nlnrket.

To test whether there is any difference between men and

women in the matter of investment in the secondary market, chi-square

test is applied.

Table 5-5

Investment in the secondary market by men and women

in the secondary market (As

Source : Field survey

1 percentage of total investment in the

capital market)

51 - 100

190

k m e n I 29

21 9

Calculated value of ~2 = 0.061

Total

260

40

300

Table value of ~2 = 3.841

Since the calculated value of ~2 is less than the table value,

the hypothesis (H7) that there is no difference between men and

women regarding investment in the secondary market, holds good. It

indicates that women are bold enough to take risks in the secondary

market, to join the game, which may not have a glorious end.

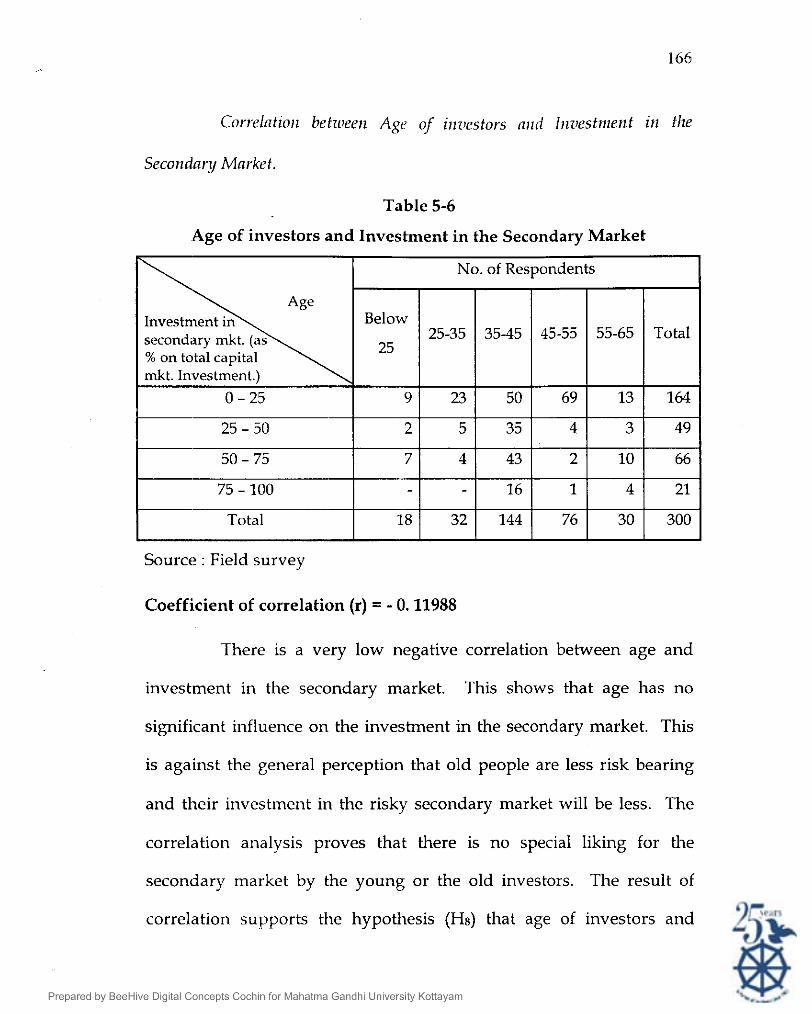

Correlcltioil betroeen Age of illriestors nrrd Inziestnlent in the

Secorzdanj Market.

Table 5-6

Age of investors and Investment in the Secondary Market

Source : Field survey

Coefficient of correlation (r) = - 0.11988

I I I I I I I

There is a very low negative correlation between age and

investment in the secondary market. This shows that age has no

significant influence on the investment in the secondary market. This

is against the general perception that old people are less risk bearing

and their investment in the risky secondary market will be less. The

correlation analysis proves that there is no special liking for the

secondary market by the young or the old investors. The result of

correlation supports the hypothesis (Hs) that age of investors and

Total 30 18 300 32 144 76

investment in the secondary market are independent. Hence the

hypothesis H8 holds good

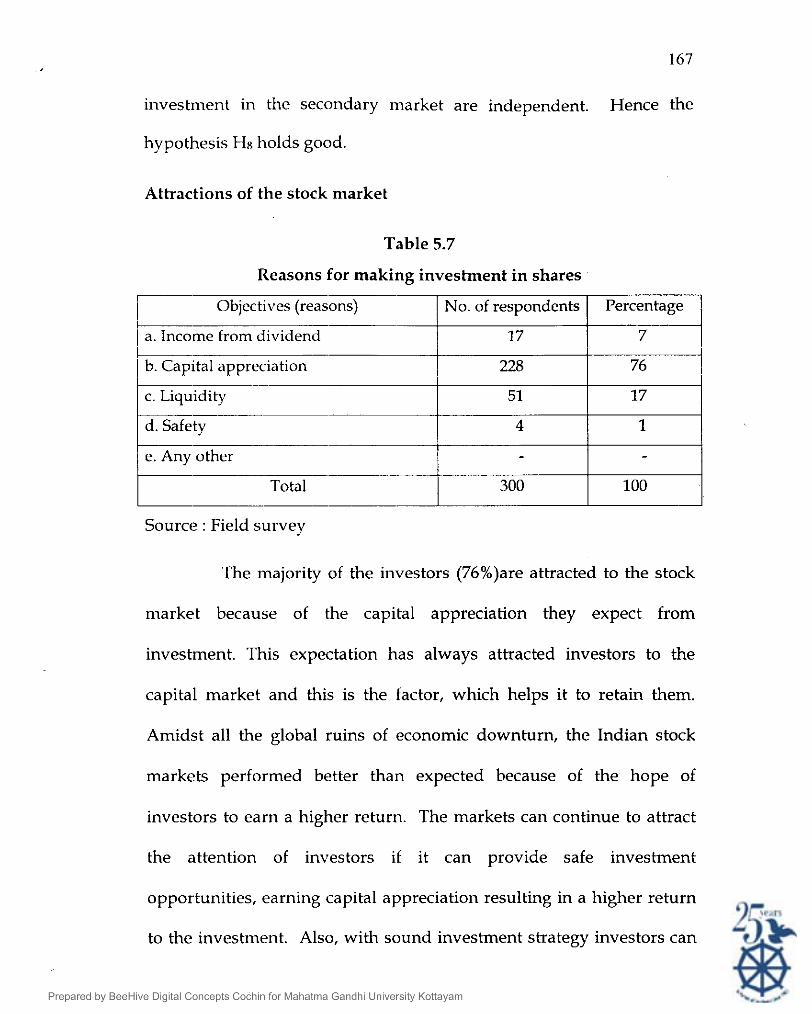

Attractions of the stock market

Table 5.7

Source : Field survey

Reasons for making investment in shares

The majority of the investors (76%)are attracted to the stock

market because of the capital appreciation they expect from

investment. This expectation has always attracted investors to the

capital market and this IS the factor, which helps it to retain them.

Amidst all the global ruins of economic downturn, the Indian stock

markets performed better than expected because of the hope of

investors to earn a higher return. The markets can continue to attract

the attention of investors if it can provide safe investment

opportunities, earning capital appreciation resulting in a higher return

to the investment. Also, with sound investment strategy investors can

Percentage

7

76

17

1

-

100

-- Objectives (reasons)

- a. Income from dividend

-- b. Capital appreciation

c. Liquidity -

d. Safety -

e. Any other -

Total

No. of respondents

17

228

51

4

- 300

earn higher returns for which thev need to spend considerable time

and hard work. If the market fails in fulfilling this expectation held by

76% of the investors, they will shy away from the market.

Liquidity of shares attracts 17% of investors to make

investment in shares. Shares are assumed to be liquid assets. But there

are less liquid shares in the market, which are inactive and transacted

rarely because there are no buyers for them. Investors should be cautious

not to get stuck with an investment, which they can't offload at will.

As per table 5.7, only 7% of the investors consider dividend

from shares as their main objective of investment. In the capital

market, most of the investors do not consider dividend as a major

source of income. Safety is the major objective of investment only for

one percent of the investors.

While making investment, capital appreciation becomes the

most important objective while other factors like safety etc. are least

considered. It is a clear indication that the investors are ready to take

risks to a great extent to attain the main objective of capital

appreciation.

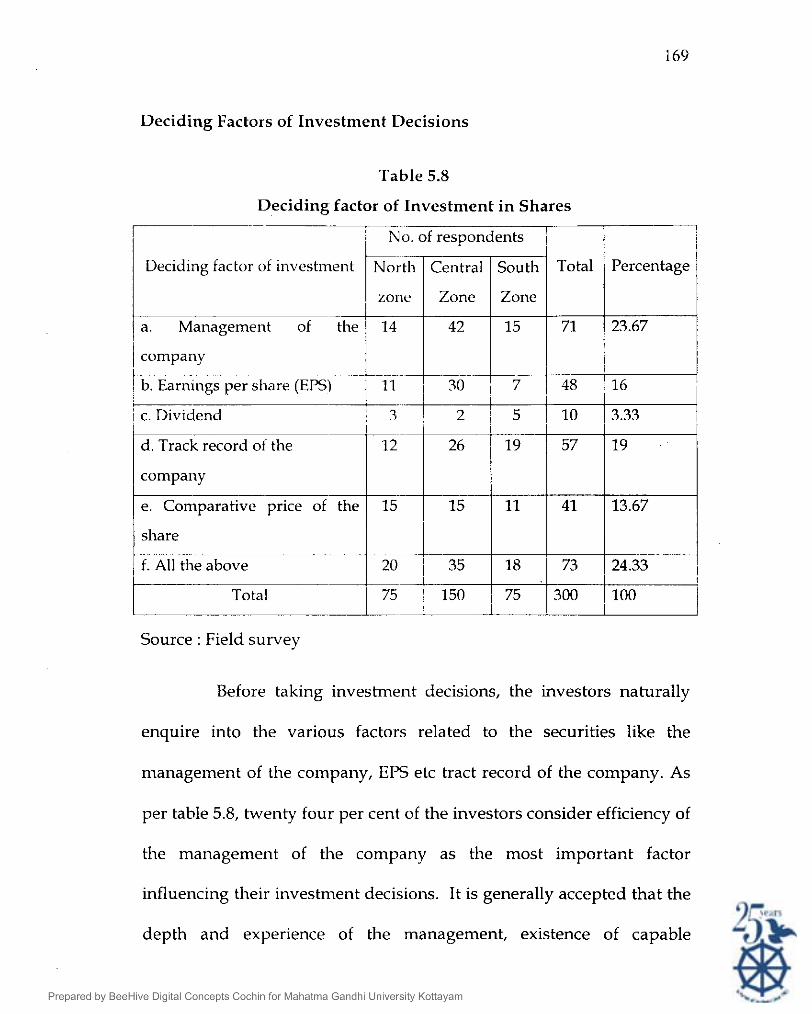

Deciding Factors of Investment Decisions

Table 5.8

Deciding factor of Investment in Shares

Source : Field survey

Before taking investment decisions, the investors naturally

enquire into the various factors related to the securities like the

I

Total

71

48

10

57

41

73

300

-- .- --' .-

i No. of respondents I

I

management of the company, EPS etc tract record of the company. As

Deciding factor of investment

- a. Management of the

Percentage

23.67

16

3.33

19

13.67

24.33

per table 5.8, twenty four per cent of the investors consider efficiency of

i

I

the management of the company as the most important factor

100 i

N ~ F G I zone

14

influencing their investment decisions. It is generally accepted that the

company

b. Earnings per share (EPS) 11 1 30 i 7

depth and experience of the management, existence of capable

Central

Zone

42

I

c. Dividend 3

d. Track record of the f company

e. Comparative price o f h e

I share -

f. All the above

Total 1 75

South

Zone

15

I

2 1 5

26

15

35

19

11

18

150 1 75

managerial personnel and their ability to react effectively to changes

- all these affect a firm's risks and its future income. Being aware of

these, investors look at efficiency of management as the most

important deciding factor of investment. Table 5.8 shows that 19%

investors are influenced by track record of the company in making

their investment decision. For 16% of the investors, earning per share is

the most important deciding factor. All these factors together are taken

into account by 24% of' the investors while making investment

decisions. It is interesting to note that dividend is the deciding factor of

the investment only for 3% of the investors.

Table 5.8 explains that investment decision is influenced by

management of the company, E.P.S, dividend, track record of the

company, price of the share etc. But the question whether these

deciding factors are in turn influenced by the experience of investors in

the stock market operations is to be answered. An effort is made to find

out the deciding factor preferred by the experienced investors and the

freshers to the market and whether with experience the preference for

a particular deciding factor increases or decreases. Hence correlation

has been worked out to find out to what extent these deciding factors

are related to the experience of investors in the stock market.

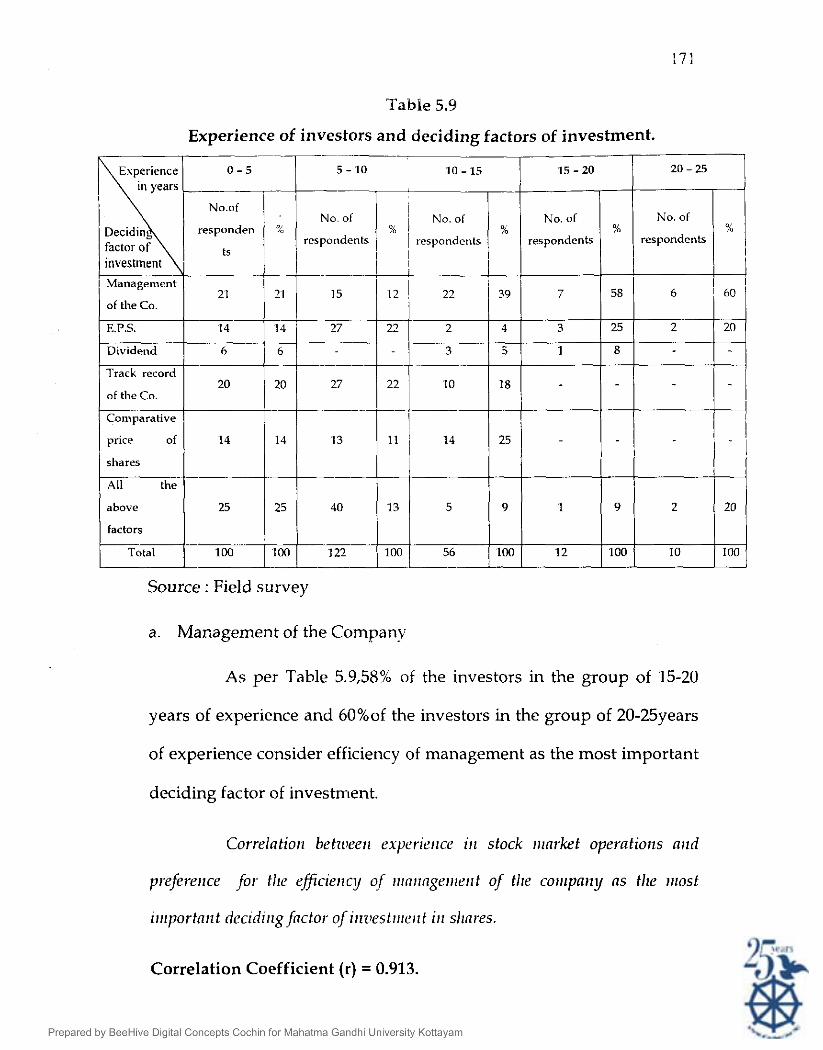

Table 5.9

Source : Field survey

Experience of investors and deciding factors of investment.

responden %

I Management

of the Co.

E.P.S.

Dividend

Track record

of the Co.

Con~parative

price of

shares

All the

a. Management of the Company

above

factors

Total

As per Table 5.9,58% of the investors in the group of 15-20

years of experience and 6O%of the investors in the group of 20-25years

25

1W

of experience consider efficiency of management as the most important

deciding factor of investment.

25

I W

Correlntiorl bekueerl experier~ce I stock rrrnrket operatiorzs nrtd

prefererlce for tlre eficierlcy of rrinringerr~erlt of the corriparly ns the lrlost

40 1 1 3 1 :6 1 9 1 1 1 9 1 ,20 1 2 0 1 122 100 100 12 100 100

Correlation Coefficient (r) = 0.913.

There is almost a perfect positive correlation between

experience and the preference for efficiency of management as the

deciding factor of investment. It proves that those who are experienced

in the stock market operations consider efficiency of management of the

company as a very important factor and with experience, the preference

for this factor increases. This is based on the common belief that the

success of business houses depends on their management and the

business will flourish forever if it is well managed.

b. Earning per share

Correlntion betroeeiz experierzce iiz stock iirnrket operatioizs ntzd the

likiizgfbr the use 0fE.P.S as the factor for ilzuestilzeilt decisiolzs.

Correlation coefficient (r) = 0.286.

A low positive correlation exists between experience in stock

market operations and the preference for E.P.S. as the basis for

investment decision. Thls shows that the experienced investors are

either not aware of the usefulness of E.P.S. for investment decisions or,

are not interested in collecting information related to different

companies for the calculation of E.P.S. But investing requires patience

and hard work to make it successful. As per table 5.9, 25% of the

investors in the group of 15-20yrs experience, prefer E.P.S, as their

deciding factor of investment. It indicates that, even though the liking

for E.I'.S. as the basic factor of investment decisions is not increasing

with experience, it is a widely used investment ratio ,which gives

earnings of a company on a per share basis.

c. Dividend from shares

There are investors who buy shares with the objective of

earning a regular income. Their primary concern is with the

dividends. For such investors dividends play a crucial role in their

investment decisions.

Companies that declare high dividends play a crucial role in

their investment decisions.

Generally, companies that declare high dividends not only

have a poor growth record but also poor growth prospects in the

future. If the bulk of the profits are distributed in the form of

dividends, there may not be any ploughing back of profits for

financing future growth. So growth companies may have a poor

dividend record but their shares are less risky. The investors have to

verify that the declaration of dividend by a company is after setting

apart enough amounts for growth purposes.

Corlrlntioit betroeerz Experience ill Stock Mnrket operntiolzs nild

diz1iderld orz slrnres ns n deciding factor ofii~z~estrizerzt.

Correlation coefficient (r) = - 0.176

There is only a very low negative correlation between

experience and dividend on shares as a deciding factor. Investors from

experience realize that the companies which offer good investment

opportunities have poor dividend records: And with increase in

experience, there is no inc:rease in the application of dividend factor as

a criterion in investment decisions.

d. Track record of the company.

One way to find out whether a company is good or bad is to

look at its past performance. Looking at its track record one can find out

how the company coped with adverse business conditions and whether

the company's management is sufficiently dynamic to warrant

investment.

Correlntion bet~ileen experience of investors in stock market and the

prefereitcefor 'track record ofcon~paities' as basisfor decision making.

Coefficient of correlation (r) = - 0.888.

A very significant negative correlation exists between the

experience of investors and their preference for track record as the

most important factor for investment decision. The track record of

companies is very often traced by the investors who are fresh to the

market. But for experienced investors rather than past records the

future prospects of the company are more important.

e. Price of the shares

Investors can look at various parameters like corporate

fundamentals, commodity prices for commodity based sectors, the

demand and supply situation for secondary or supplier industries and

the economic indicators for the core sectors. But, in a reasonably

efficient market, we believe that, all these filter into the stock price,

which is the reflection of all these. As per table 5.9 twenty-five percent

of the investors in the group having an experience of 10-15 years

consider price of the share as their basic decision making factor.

Correlntior~ bet7oeerl experierlce ofinziestors in the stock nzarket and

prefer~rlce for- 'price' as tlru iilost riilportni~t factor irlflllencing decision on

iirz~estrirei~t iir slrnres.

Correlation coefficient (r) = - 0.588.

The result shows that there is a high negative correlation

between the experience of investors and the preference for 'price' as the

most important deciding factor of investment. The experienced

investors do not find 'price' as a reliable basis for investment decision.

The very premise that stock prices are linked to performance is under

threat. Again, it is a clear indication that our markets are not that

efficient to enable the price to reflect the corporate performance. From

experience investors have realized that, instead of merely comparing the

prices of securities, they should find out whether the price of a share is a

real reflection of the earning capacity and future prospects of the issuer.

f . Considering ail the five factors for investment decisions.

Table 5.8 shows that 24% of the investors consider all these 5

factors (Management of the company, Earnings per share, Dividend,

Track record of the company and Price) together for taking an

investment decision. It is very encouraging as a decision taken based

on all these factors together will naturally be a better one.

Correlntior~ bet7~ee11 experience of itlaestors it1 the stock tliarket and

the preferellcefor. 011 tlzc 5fnctors fog~'t1ler ns hasisfor i~lz~estlilent decisioil.

Correlation coefficient (r) = - 0.5173.

There exists a high negative correlation between experience

and use of all the five factors together for investment decisions. It

indicates that the freshers to the capital market are more interested in

looking at all the factors in tandem for making an investment decision.

With experience, the investors seem to give primary importance to a

single factor.

Type of shares selected by investors

The primary concern of most investors, while investing in

shares is to minimize risk and to maximize return. Their effort in this

venture is reflected in the type of share they select for making

investment. They judge the shares by looking at the volatility, the

income that will be earned or growth prospects. The result of the

response of the respondents to a question as to what type of share they

will choose for investment is disclosed in Table 5.10.

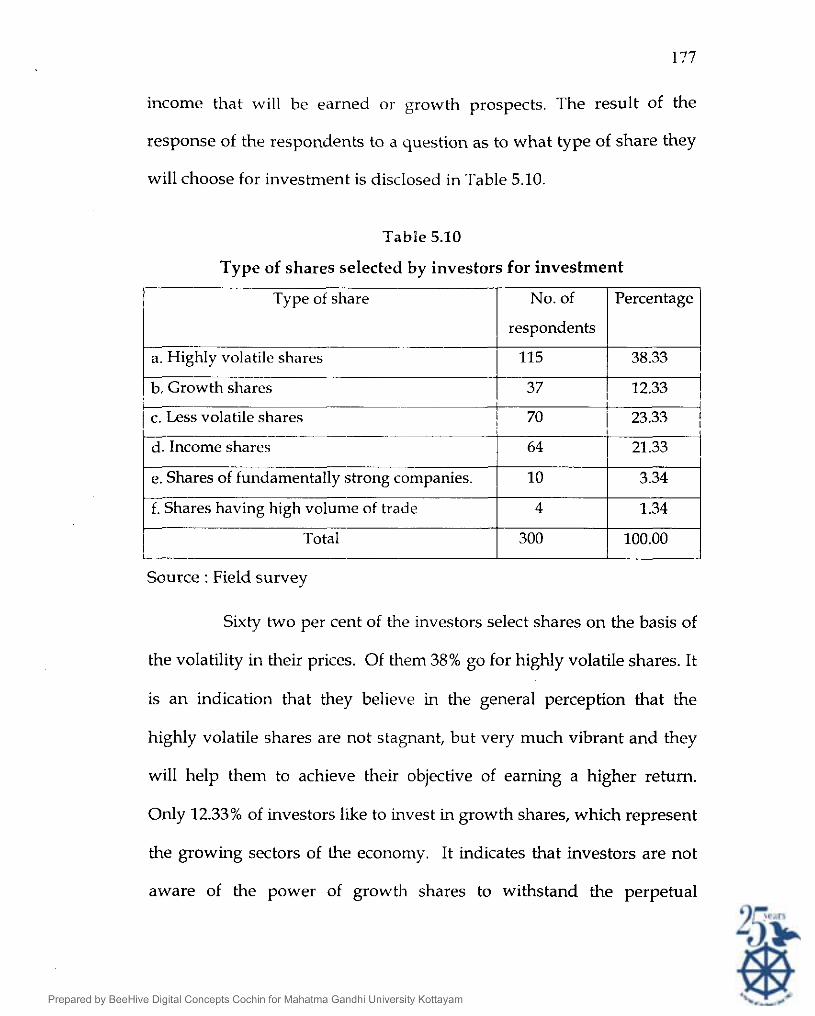

Table 5.10

respondents

a. Highly volatile shares

Type of shares selected by investors for investment

Type of share No. of

t I

~ o t a l I

300 100.00 -

Source : Field survey

Percentage

I I

Sixty two per cent of the investors select shares on the basis of

- b, Growth shares

the volatility in their prices. Of them 38% go for highly volatile shares. It

37 I

is an indication that they believe in the general perception that the

1 12.33 1 -- - c. Less volatile shares 70 1 23.33 1 -- d. Income shares 21.33

- e. Shares of fundamentally strong companies. -- f. Shares having high volume of trade

highly volatile shares are not stagnant, but very much vibrant and they

will help them to achieve their objective of earning a higher return.

Only 12.33% of investors like to invest in growth shares, which represent

the growing sectors of the economy. It indicates that investors are not

aware of the power of growth shares to withstand the perpetual

pressures of depression. Twenty one percent of investors select income

shares as they expect a regular income from their investment.

The selection of shares of fundamentally strong companies

and shares having high volume of trade is by 3. 34% and 1. 34% of the

investors respectively. High volume of trade and fundamentals of a

company are not influencing the investors in Kerala. It is found that

shares of companies having strong fundamentals are capable of

withstanding crises in the stock market. However, the investors have

not realised this factor.

In order to avert risk, the type of share selected by the

beginners in the field of stock market may be different from that of

experienced investors. An effort is made to provide an insight into the

management of risks by experienced and inexperienced investors by

selecting a particular type of share. To achieve that purpose, the

correlation is worked out between experience of investors and the type

of shares selected for investment.

Experience of investors in stock market operations and the type of

shares they prefer to buy.

10-15 15 - 20 20 - 25

No. of NO. o i % NO. of

respondents respondents respondents respondents shares 1. Highly I

26 46 6 50 - 3

25

volatile shares

12 17 5

27 25 2 17 1 10

16 16 10 18 shares

fundamentally 8 6 1 2 1

strong

ror~~panies

I - j trade

I

I -

100 56 100 12 100 10

Source: Field survey

i. Highly volatile shares

As per Table 5.11, 46% of the investors in the group of 10-15

years experience, and 50% of the investors in the group of 15-20 years

of experience prefer to buy highly volatile shares.

Corwlntior~ betrorer~ csjx,r.ie~ice ill stock irlarket operatiotls arid

selectio~i of lliglzly iiolntile slu-rres.

Correlation coefficient (r) = - 0.1456

The correlation is pretty weak which proves that with

increase in experience, there is no corresponding increase or decrease

in the preference for highly volatile shares. From experience, the

investors learn that highly volatile shares are the worst hit when there

is a downturn in the market.

ii. Growth Shares

Growth shares are of such companies, which have a

comparatively higher growth rate than other companies. A growth

company will have a proven record of growth in the past and is likely

to grow in the future also It will have a dynamic and growth-oriented

management. Table 5.11 shows that25% of the investors in the group of

15-20 years of experience like to buy growth shares.

Correlatiorl behoee~l experie~tce I stock 111arket operntiot~s alzd

selectiorz of gro7utli sllnres for iriz~estrriei~t.

Correlation coefficient (r) = - 0.229.

The result shows a low negative correlation between

experience in stock market operations and the selection of growth

shares. Even though growth companies provide excellent investment

opportunities, the result of analysis proves that the experience and

gaining of knowledge do not increase the tendency to buy growth

shares

iii Less Volatile Shares

Correlatiorl betrueerz esperzerzce in share innrket operations nnd t l z

teizdeilcij to buy less z~olntile shares by tlze iizz~esfor.~

Correlation coefficient (r) = - 0.8862

A high degree of negative correlation exists between

experience of investors in share market operations and their preference

for less volatile shares. It is a fact that there is no scope for speculation

in the case of less volatile shares. The result of correlation is indicative

of the general perception that with increase in experience, people tend

to speculate in stocks. Ilence the result supports the hypothesis. (H9)

that with increase in experience people tend to speculate.

iv Income shares

Many investors are keen on receiving a regular income in the

form of dividends. But, on declaring higher dividends, the ploughing

back of profits is constrained and it affects the growth prospects of the

company. So high dividend usually means low capital appreciation.

Correlntioil heizoeerl t/re exyerierlce of irlziestors in the stock iiiarket

nrzd the nppetitefor iiicorrle slrnres

Correlation coefficient (r) = 0.213.

The result of correlation analysis shows that the correlation

between experience of investors and the appetite for income shares is

very low. It is an indication that the investors, from experience come to

know that the declaration of a higher dividend will not have a

permanent impact on capital appreciation which is their main objective

for investment.

Diversion of Funds from the Stock Market

Funds are diverted from the stock market to other avenues of

investment due to many reasons. Data has been analysed to find out to

what extent the diversion of funds from the stock market has taken

place, the reasons for this diversion, and whether the objectives of

investment, type of share selected etc. have any influence on the

diversion of funds from the stock market.

Diversion of funds is a serious problem afflicting the capital

market, which is revealed in table 5.12.

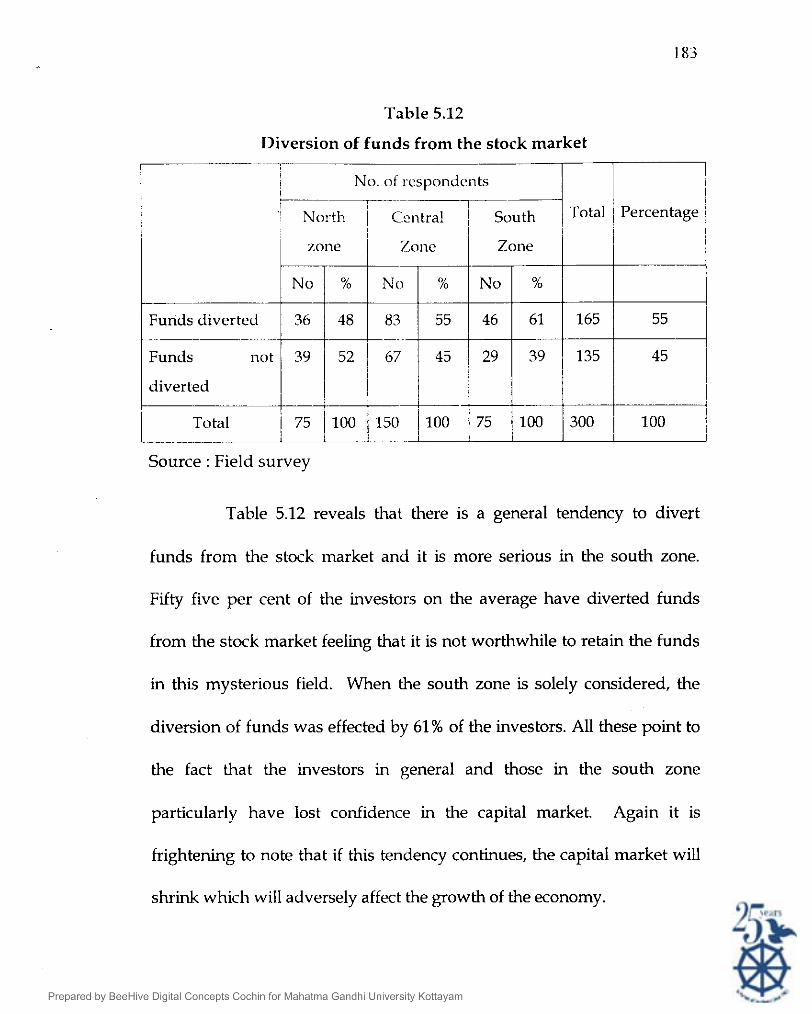

Table 5.12

Diversion of funds from the stock market 7-- - ~

I ! I ! No. o f respondents I I

Zone Zone

No % No '% -

Funds diverted 83 55 46 61 165 55 ..

52 67 45 29 39 135 45

diverted

100 / I 1 I

Source : Field survey

Table 5.12 reveals that there is a general tendency to divert

funds from the stock market and it is more serious in the south zone.

Fifty five per cent of the investors on the average have diverted funds

from the stock market feeling that it is not worthwhile to retain the funds

in this mysterious field. When the south zone is solely considered, the

diversion of funds was effected by 61% of the investors. All these point to

the fact that the investors in general and those in the south zone

particularly have lost confidence in the capital market. Again it is

frightening to note that if this tendency continues, the capital market will

shrink which will adversely affect the growth of the economy.

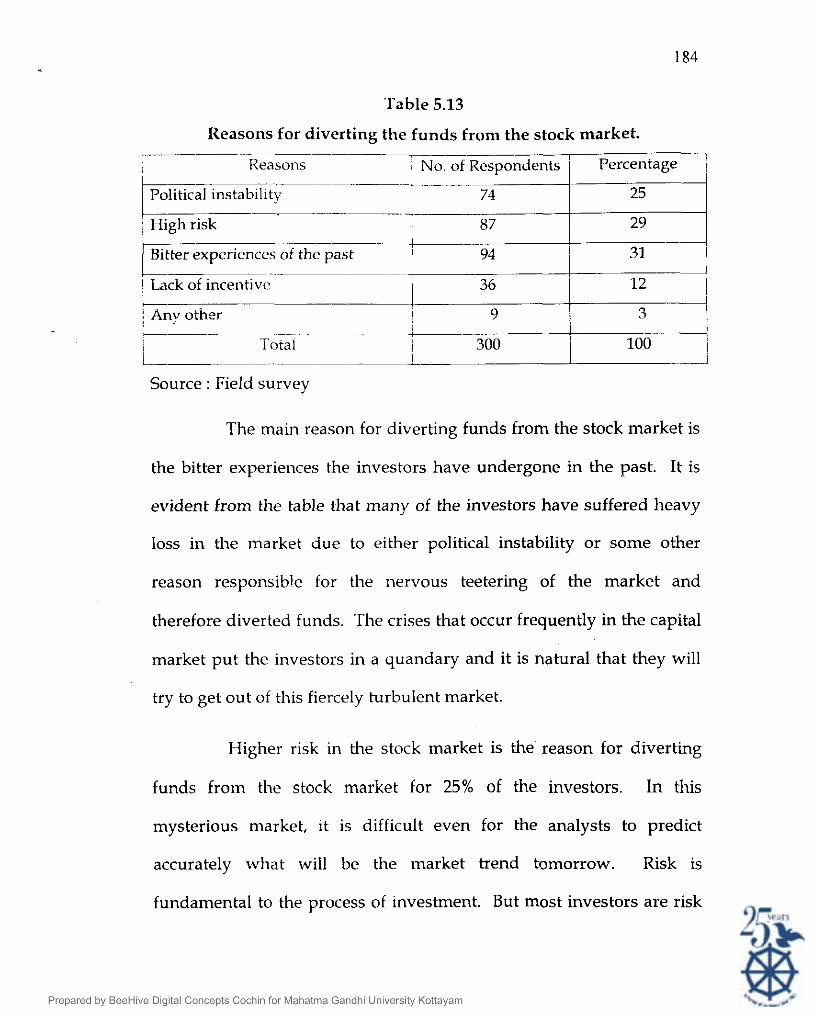

Table 5.13

Reasons for diverting the funds from the stock market. 7- -- --- I Reasons I N o of Respondents / Percentage i

I

of t h e past I 94 31 C- I Lack of incentive + -- ! I i Any other I 9 3 1 I ---- , I Totan 1 I L- - I Source : Field survey

The main reason for diverting funds from the stock market is

the bitter experiences the investors have undergone in the past. It is

evident from the table that many of the investors have suffered heavy

loss in the market due to either political instability or some other

reason responsible for the nervous teetering of the market and

therefore diverted funds. The crises that occur frequently in the capital

market put the investors in a quandary and it is natural that they will

try to get out of this fiercely turbulent market.

Higher risk in the stock market is the reason for diverting

funds from the stock market for 25% of the investors. In this

mysterious market, it is difficult even for the analysts to predict

accurately what will be the market trend tomorrow. Risk is

fundamental to the process of investment. But most investors are risk

averse. It is true that to have a higher return the investors should be

prepared to face greater risks.

Whatever be the reason, it is evident that large amounts are

diverted from the stock market. The stock market is moving nervously

every day, reacting t o the events taking place in and outside the

country. In this context, what is of primary importance is stability in

the market and this is the aspect that has been highlighted by all the

apex chambers

The Clli-square nrlnlysis of diziersiorz o f f t ~ r ~ d s fiDrn the stock nlnrket

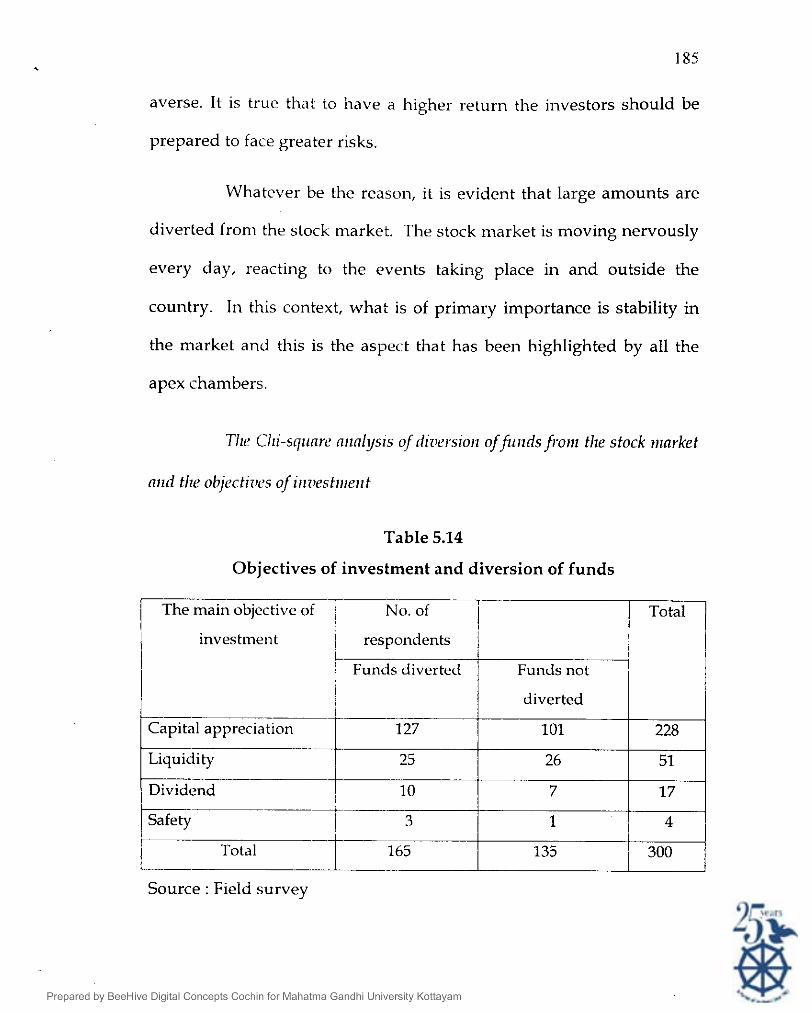

Table 5.14

Objectives of investment and diversion of funds

diverted

127 101 228

Liquidity 25 26 51

Dividend 10 7 17

3 1 4

165 135 I 300 I

Source : Field survey

Total

I

I

The main objective of T No. of I I I investment respondents 1 I I I Funcls diverted

I Funds not

186

Table 5.14 shows that out of 228 investors whose main

objective of investment is capital appreciation, 127 (56%) investors have

directed funds fro111 the stock market. It is interesting to note that 75%

of the investors whose main objective is 'safety', have diverted funds.

To prove whether there is any relation between the objectives

of investment and diversion of funds, chi-square test is applied. The

result of the test is as follows.

Calculated value of ~2 = 2,019

Table value of ~2 = 7.815

The calculated value of ~2 is 2.019 which is lower than the

table value and hence the hypothesis HIO holds good. Hence, it may be

concluded that there is no significant association between the

objectives for which the investment is made and the diversion of funds

from the capital market.

It is evident from the result of the test that even if the

objectives for which the investments are made are not attained, the

investors may not withdraw the amount from the capital market. It is

because of the widespread belief that equities give higher returns than

any other form of investments and they give best access to the

corporate's wealth creation process. Long -term investment in stock

market investing has proven to be the safest and surest path to wealth

187

creation. Also, the Indian stock markets have been able to maintain the

integrity even in the face of extreme circumstances. It emphasises the

fact that in spite of all the ruins of political instability, the Indian capital

market can not- only retain its existing investors but attract more

investors and entice them to invest in shares if it can offer a well

regulated market in terms of investors' safety.

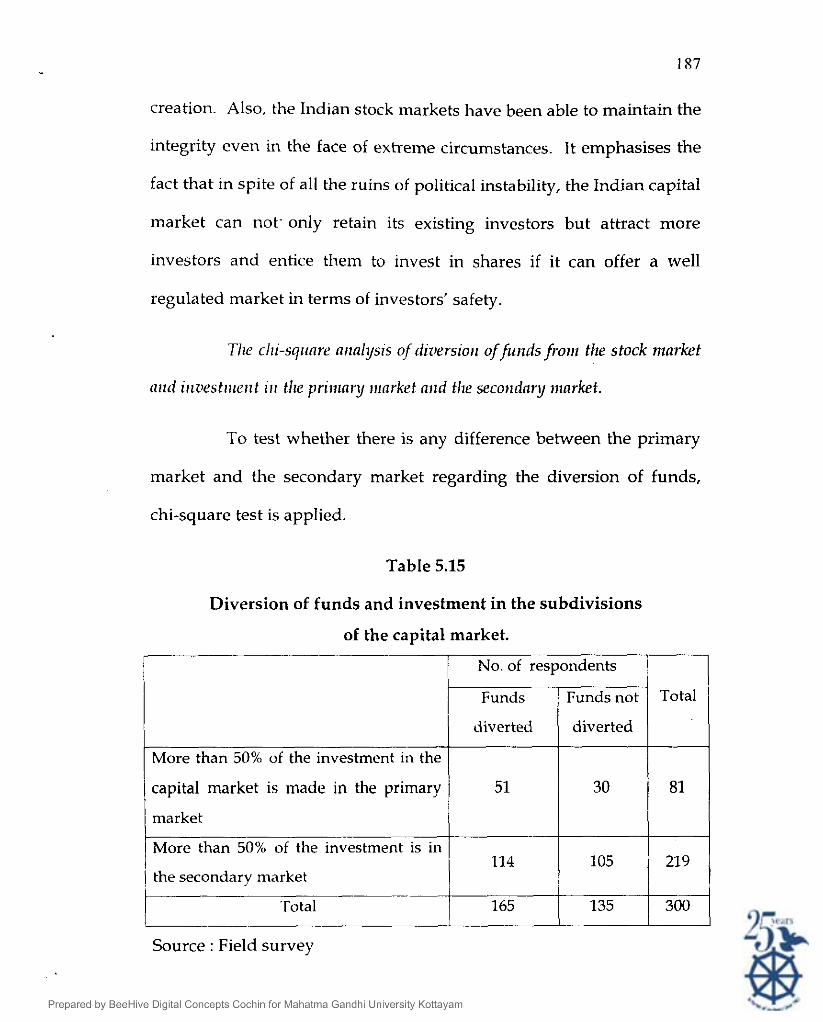

Tlle chi-sqiinre nrzalys~s of diziersioli offuildsfronl the stock nzarket

artd irlz~est~ller~t ill tlle prillmry ~llnrket and t l ~ secot~dnry n~arket.

To test whether there is any difference between the primary

market and the secondary market regarding the diversion of funds,

chi-square test is applied.

Table 5.15

Diversion of funds and investment in the subdivisions

of the capital market. -- / No. of respondents I

1 Funds i Funds not I

diverted diverted

More than 50% of the investment

capital market is made in the primary / 51 1 30 1 81

market I I I More than 50% of the investment is in

the secondary market I I I

114

Total -a-

105

Source : Field survey

135 165

21 9

300

Calculated value of X? = 2.464

Table value of ~2 = 3.841

Since the calculated value of ~2 is less than the table value the

hypothesis (HII) stands good. That is, it is proved that there is no

difference between the primary market and the secondary market in

the matter of diversion of funds. It indicates that the exhaustion of

funds takes place from the entire capital market comprising of the

primary market and secondary market. It is not a specific feature of

any division of the capital market.

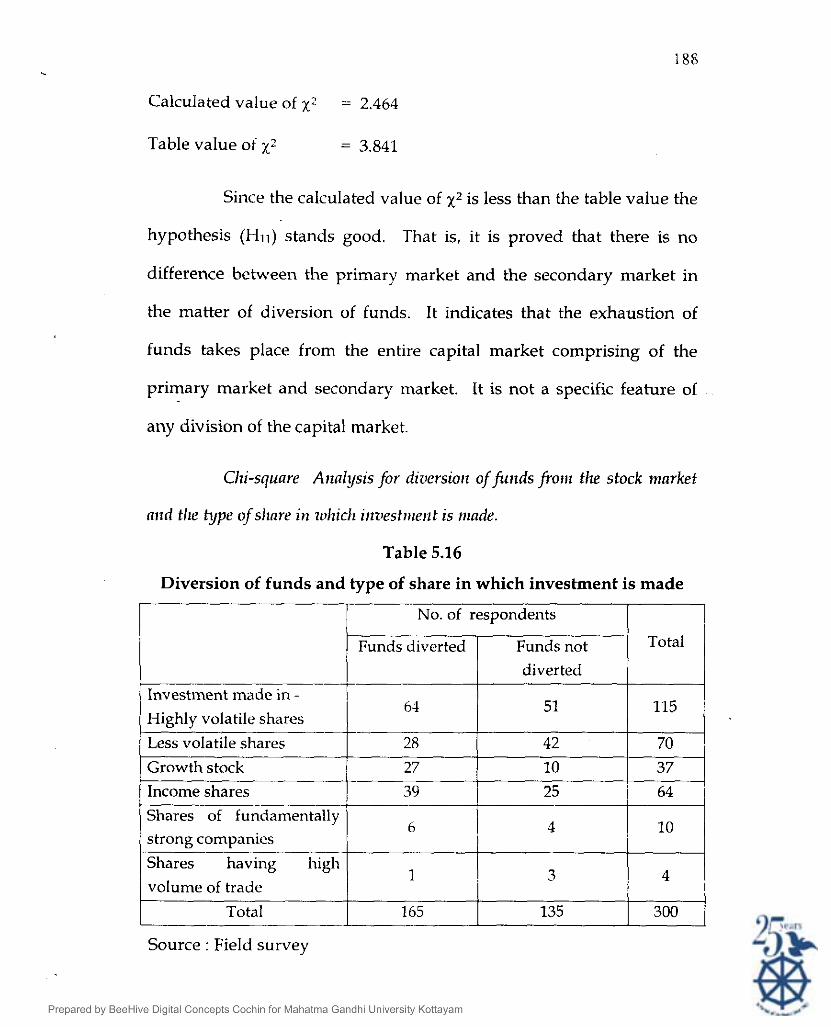

Chi-square Ailalysis for diziersiot~ of funds fro111 tlze stock market

n11d the type of slmre i l l zohic1~1 iizz~estitier~t is nlade.

Table 5.16

Diversion of funds and type of share in which investment is made

T T I I No. of respondents

Total Funds diverted

I Investment made in - 61

28

27

39

Funds not diverted

I I

Source :: Field survey

51

42

10

high 1

volume of trade

Total -

165

115

70

37

10 of fundamentally

6

25 1 64 !

4

3

135

strong companies I

4

300

I

Table 5.16 reveals that investors in highly volatile shares are

particularly prone to divert funds from the stock market compared to

the investors in less volatile shares. Fifty six percent of the investors in

highly volatile shares and 40% of the investors in the less volatile

shares divert funds from the stock market. The result of the chi-square

test to prove the relation between the type of shares in which

investment is made and diversion of funds is as follows.

Calculated value ~2 = 13.428

Table value of ~2 = 11.07

Since the calculated value of ~2 is higher than the table value,

the hypothesis H 1 2 that there is no association between diversion of

funds from the stock market and the type of share in which investment

is made, is rejected, that is diversion of funds from the stock market

depends very much on the type of share in which investment is made.

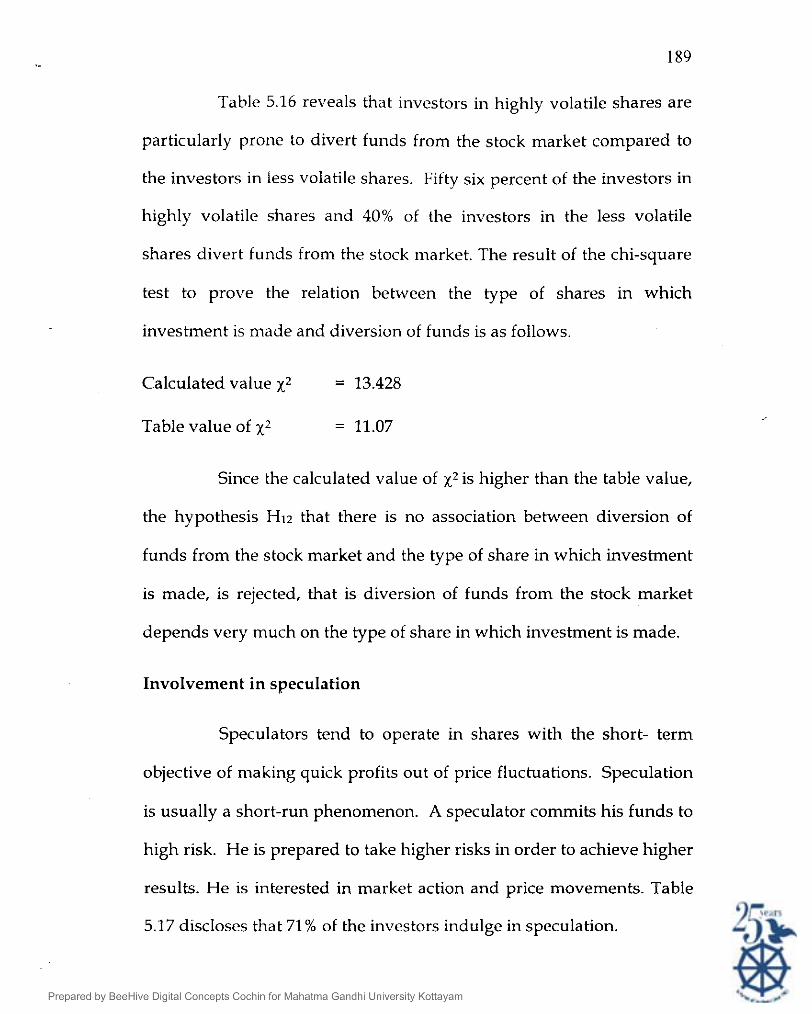

Involvement in speculation

Speculators tend to operate in shares with the short- term

objective of making quick profits out of price fluctuations. Speculation

is usually a short-run phenomenon. A speculator commits his funds to

high risk. He is prepared to take higher risks in order to achieve higher

results. He is interested in market action and price movements. Table

5.17 discloses that 71% of the investors indulge in speculation.

Fable 5.17

Speculative involvement - Zonal break up

No. of respondents

ITZE~I Total (%) 1 I;) 1 zone ('1 1 zone (%) 1 --

Indulge in speculation (76) 102 (68) 54 (72) 213 (71) 1 L- I No speculation

Total

Source : Field survey

Table 5.17 shows that the involvement ,in speculation is

comparatively lesser in the central zone, which is contrary to the general

perception that in the area around the stock exchange the speculation

must be more. Due to the proximity to the stock exchange, the investors

in the central zone are more aware of the complications of speculation.

Table 5.18

Profitability of speculative business.

Percentage of I I I transactions which I No. of respondents I Percentage I

result in profit 4 112 53

Source : Field survey

- Total 213 100

As per table 5.18 fifty three per cent of the investors who

indulge in speculation admit that less than a quarter of their

speculative transactions results in profit. That is 3/4 of the speculative

transactions being them loss. Above 50% of the speculative

transactions result in profit in the case of 23% of the investors who do

speculative business. In other words, most of the speculative

transactions of 77% of the investors result in loss. So the hypothesis

HI^ that most of the speculative business resuslt in loss holds good.

This is a warning to the investors to be cautious and not to go for

quick profit by doing speculative business.

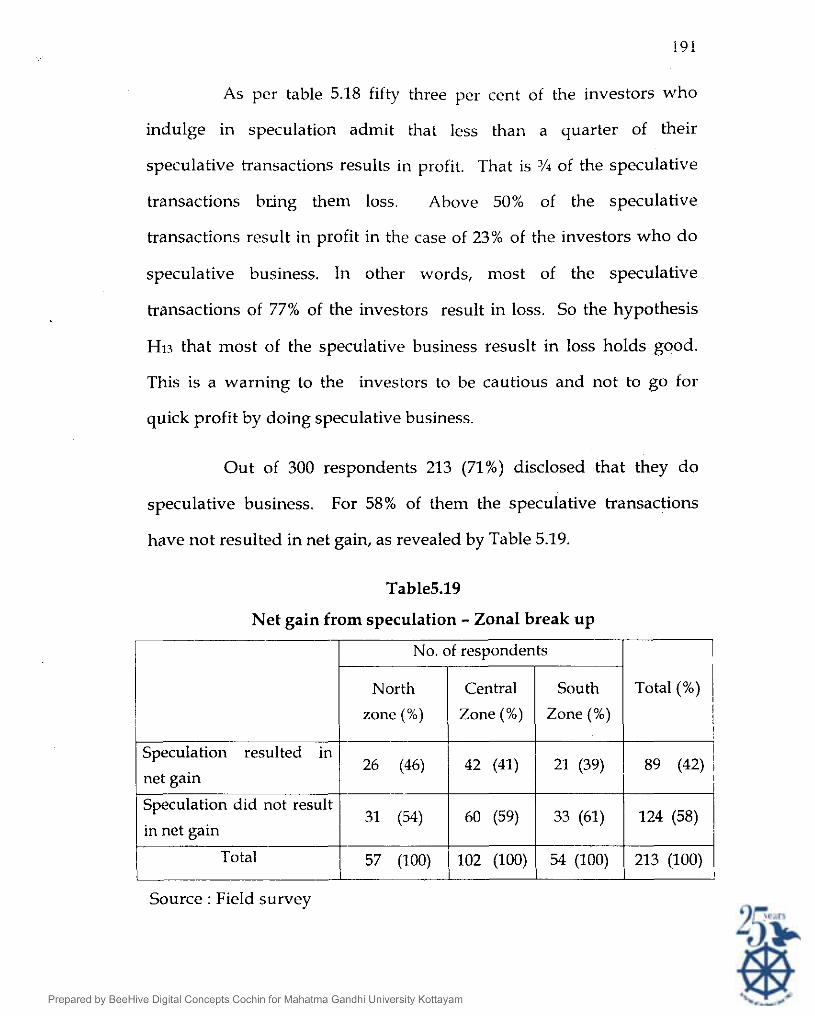

Out of 300 respondents 213 (71%) disclosed that they do

speculative business. For 58% of them the speculative transactions

have not resulted in net gain, as revealed by Table 5.19.

Table5.19

Net gain from speculation - Zonal break up

No. of respondents 1-1 zone (%) Zone (%) Zone (%) Total % ) I 1

Speculation did not result 60 (59) 33 (61) 124 (58) 1

in net gain I

Speculation resulted in 26 (46) 42 (41)

Source : Field survey

I 21 (39) 89 (42)

I I

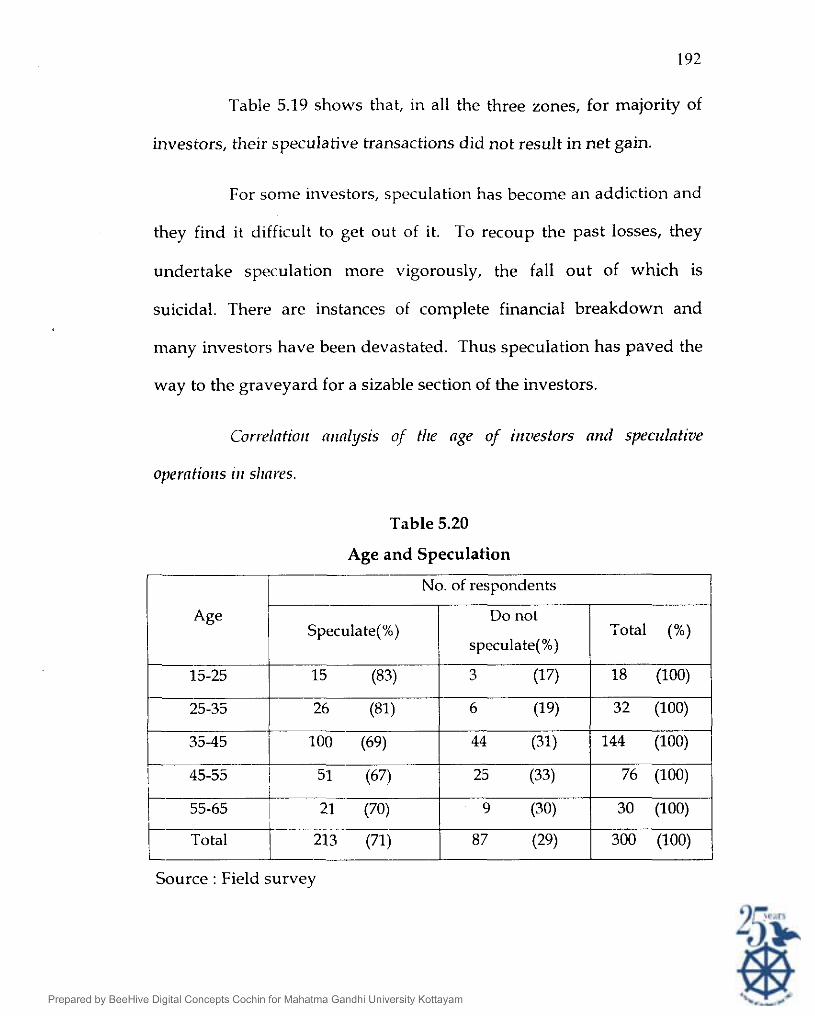

Table 5.19 shows that, in all the three zones, for majority of

investors, their speculative transactions did not result in net gain.

For some investors, speculation has become an addiction and

they find it difficult to get out of it. To recoup the past losses, they

undertake speculation more vigorously, the fall out of which is

suicidal. There are instances of complete financial breakdown and

many investors have been devastated. Thus speculation has paved the

way to the graveyard for a sizable section of the investors.

Correlntiorr nrznlysis of tllr age of irzzlestors arzd speculative

operntiorzs irz sl~rrres.

Table 5.20

Age and Speculation

I I No. of respondents I

Source : Field survey

Coefficient of correlation (r) = -0.855

There is a strong negative correlation between the age of

investors and the tendency to involve in speculative transactions. As

age increases the investors find it difficult to cope with the risks and

intricacies related to speculation and so they tend to reduce the

involvement in speculative activities. The result of correlation analysis

shows that speculation is a more hazardous activity than investment

and is embraced more by the youngsters. So the hypothesis Hi4 that

youngsters are more involved in speculative transactions than old

people holds good.

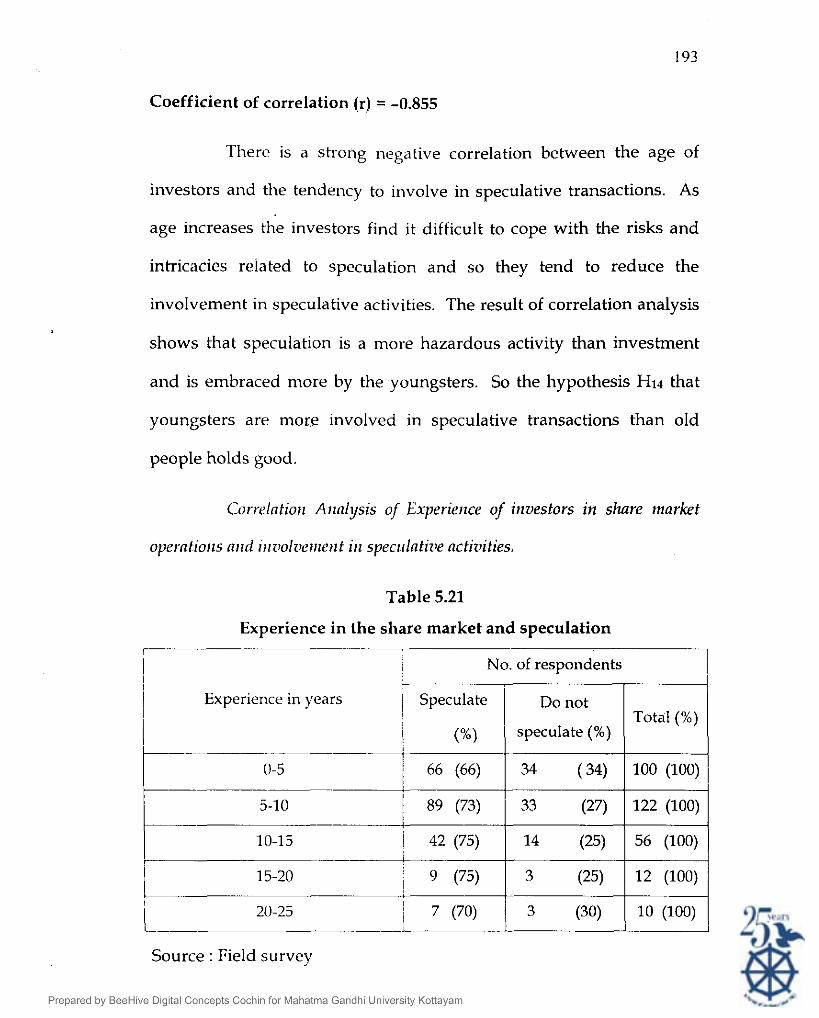

Correlntiorl Arlnlysis of Experience of iilvestors i n slmre ninrket

operntiorls nrld irrr~olz~err~er~t ill spectllntiz~e nctiz~ities.

Table 5.21

Experience in the share market and speculation

No. of respondents I

Source : Field survey

i Experience in years 1 Speculate Do not

1 1 (%) ( speculate (%) Total (%)

Coefficient of correlation (r) = 0.742

The analysis shows that the correlation between experience

of investors in stock market operations and their involvement in

speculative activity is highly positive. It indicates that experience gives

impetus to operators to involve in speculative activities. The result

supports the hypothesis H9 that with experience people tend to

speculate.

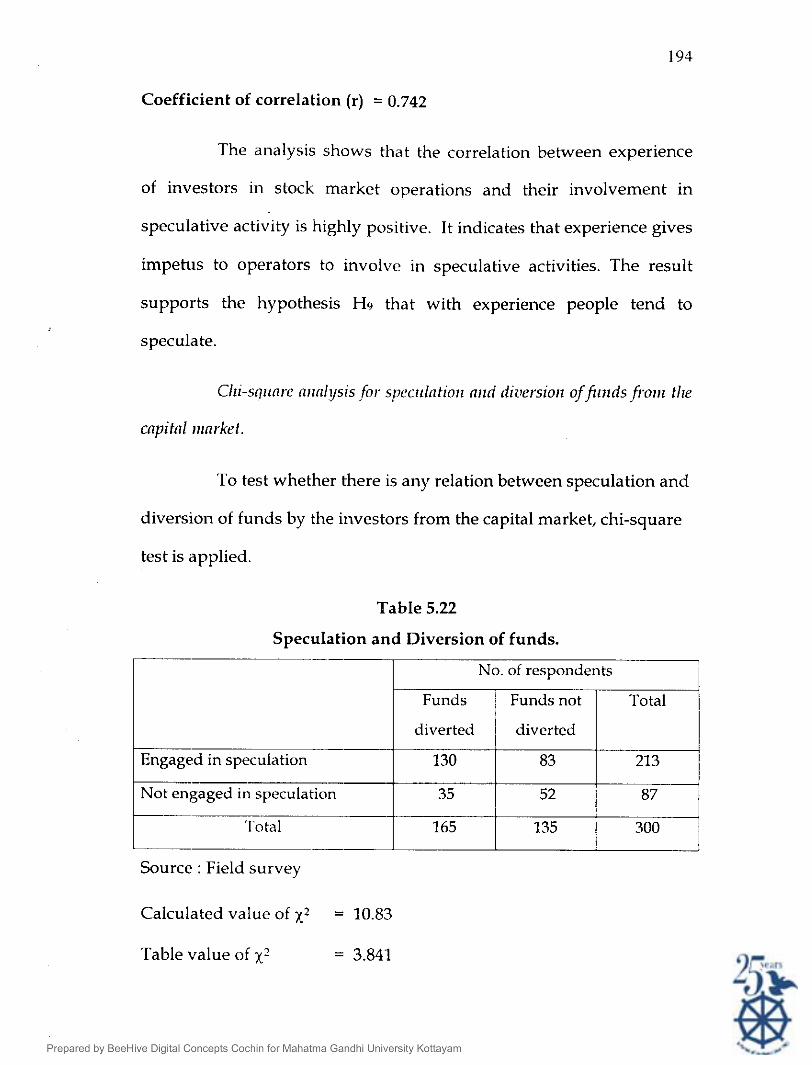

Chi-sqrlnre nr~nlysis for. specr~lntioil nrtd diziersioi~ of f iulds frorr~ tlle

To test whether there is any relation between speculation and

diversion of funds by the investors from the capital market, chi-square

test is applied.

Table 5.22

Speculation and Diversion of funds.

No. of respondents

diverted diverted

- Not engaged in speculation

Total

Source : Field survey

-- I I I

Calculated value of X* = 10.83

Table value of X' = 3.841

Engaged in speculation 130 83 213

The calculated value of X* is greater than the critical value, so

the hypothesis (HIS) is rejected. Hence it is concluded that diversion of

funds from the capital market is verv much dependent on the

involvement in speculative business. Most of the speculative

transactions result in loss which ultimately lead to the diversion of

funds from the stock market.

The prudent investor purchases securities on the genuine

long-term profit expectation. Traditionally, the equity market gives

return over a longer time and in the last few years this aspect has been

totally forgotten. There is predominance of short-term players in the

market, which has changed its colour with every investor coming in for

a quick buck. These short- term players have to realise that speculative

business may result in loss even if they are utmost alert.

The expectation of unrealistic return within too short a

period has encouraged many an investor to involve in speculation at

the cost of even hisjher own capital. The stock markets are notorious

for going up and down sharply in the most unexpected manner. The

position of the investor with short-term gains in mind becomes the

bubble on the whirlpool of speculation which brakes sooner or later.

He finally resorts to transferring the funds to some other avenues of

investment which results in deserting the stock market. This reinforces

the need for the presence of long- term investors who will provide

stability to the market. To retain them in the market, they have to be

educated on making long term investments based on a clear

understanding of the underlying fundamentals. They must

understand that-investing requires caution, patience and hard work

and they must never let greed dominate their decisions.

Despite the risks inherent in common stock, they remain a

popular investment among individual investors. One of the main

reasons for this continuing popularity is the possibility of a spectacular

return. The analysis of data shows that most of the investors in Kerala

invest in corporate securities expecting capital appreciation. It is this

hope, which retains the investors in the capital market. But many of

the investors view the securities market with pre-conceived notions.

Most of their investment decisions are without a clear vision supported

by knowledge and information and quite often they may make

mistakes. After incurring heavy losses they exit the market. It is

evident that new measures are required to fortify confidence in the

investors. Also, investors should not be afraid of the challenges of a

new competitive market place.

Footnotes

1. Manu Bhai Shah, "Primary Market Revival", Tlze Ecoizoii~ic Tiiiles,

April/27,1999.