Embed Size (px)

Citation preview

CR Common Practices

FRS 101 “Reduced Disclosure Framework” – A review of application in parent company accounts of IFRS groups

1

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting a Wolters Kluwer Business, 145 London Road, Kingston Upon Thames, Surrey, KT2 6SR

Published on 21 July 2016

Introduction

This report sets out the key findings from our review of the first-time application of FRS 101 “Reduced Disclosure

Framework” by a group of 29 parent companies that prepare consolidated financial statements under IFRS. We

consider a number of points including: how companies informed shareholders of the intention to implement FRS 101;

the format of the primary financial statements; disclosure of the list of exemptions taken; the concept of equivalent

disclosure in the consolidated financial statements; the length of company financial statements under FRS 101; and

changes in accounting policy on adoption.

Further guidance is available in the book CCH Preparing FRS 101 Accounts, on CCH Online (which includes FRS 101

itself and the full suite of IFRSs, along with FRS 101 model accounts) and a summary of measurement differences is

contained in the publication CCH New UK GAAP: An at a glance comparison between new and old UK GAAP and

IFRS.

Key Findings

In light of FRED 65 proposing to remove the requirement to inform shareholders in advance of the use of

disclosure exemptions, we noted there was no consensus as to how companies informed shareholders of the

intent to adopt FRS 101 and the exemptions adopted. Companies used either the AGM notice or previous

financial reports or both, but in 9 cases we found no evidence of the notice.

For the statement of financial position, 11 companies adopt a Companies Act style format with 12 adopting an

IAS 1 style presentation. 6 companies adopt a ‘hybrid’ presentation with a combination of Companies Act and

IAS 1 terminology.

28 out of the 29 companies present a narrative description of the disclosure exemptions taken under FRS

101.

Only three sample companies follow best practice when identifying exemptions by including both IFRS

paragraph references and a full narrative description in respect of all exemptions taken.

16 sample companies make reference to equivalent information being included within the consolidated

financial statements with 10 of these companies referring to equivalent information in respect of specific

exemptions.

Although all companies take advantage of disclosure exemptions following application of FRS 101, the trend

is actually for the company financial statements to be longer this year compared to last year.

14 sample companies restate prior year figures on transition to reflect changes in measurement when moving

from old UK GAAP to FRS 101.

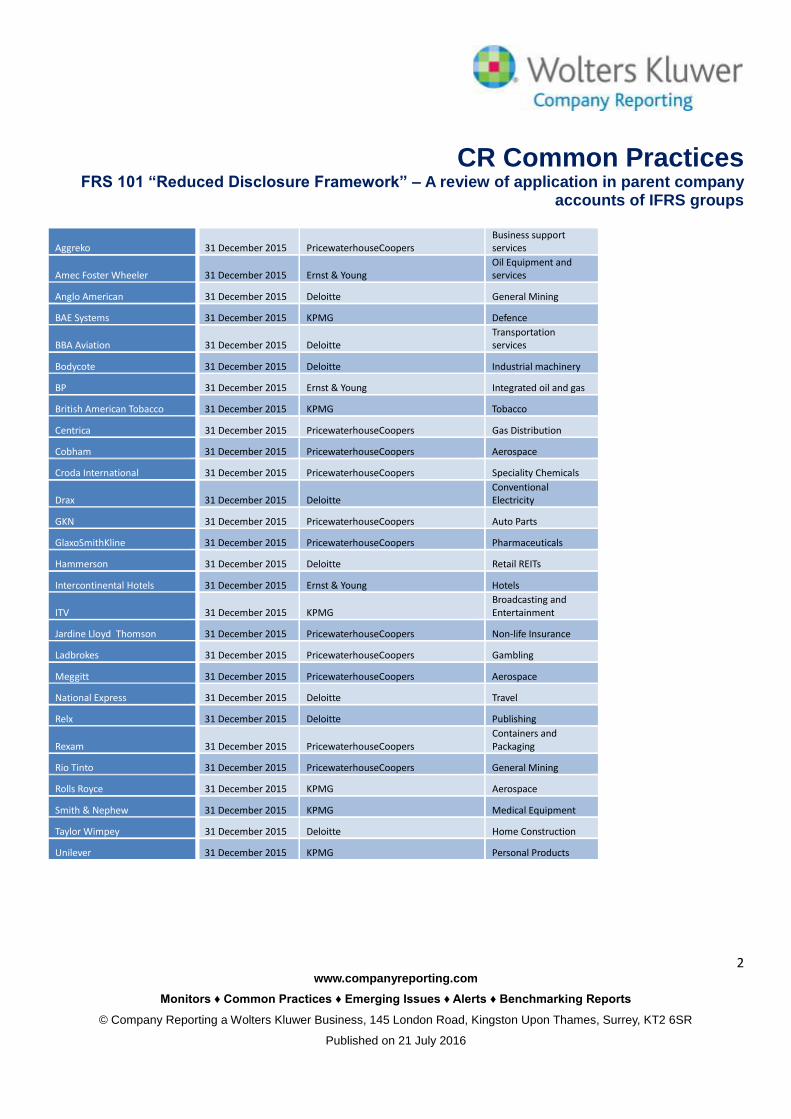

Companies under examination

Our sample consists of the parent company financial statements of 29 UK listed groups. The companies analysed are

all members of the FTSE 350 and are drawn from a range of different industries. A number of companies that are

audited by each of the big four auditors are considered.

Company Period end Auditor Industry Classification

AstraZeneca 31 December 2015 KPMG Pharmaceuticals

CR Common Practices

FRS 101 “Reduced Disclosure Framework” – A review of application in parent company accounts of IFRS groups

2

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting a Wolters Kluwer Business, 145 London Road, Kingston Upon Thames, Surrey, KT2 6SR

Published on 21 July 2016

Aggreko 31 December 2015 PricewaterhouseCoopers Business support services

Amec Foster Wheeler 31 December 2015 Ernst & Young Oil Equipment and services

Anglo American 31 December 2015 Deloitte General Mining

BAE Systems 31 December 2015 KPMG Defence

BBA Aviation 31 December 2015 Deloitte Transportation services

Bodycote 31 December 2015 Deloitte Industrial machinery

BP 31 December 2015 Ernst & Young Integrated oil and gas

British American Tobacco 31 December 2015 KPMG Tobacco

Centrica 31 December 2015 PricewaterhouseCoopers Gas Distribution

Cobham 31 December 2015 PricewaterhouseCoopers Aerospace

Croda International 31 December 2015 PricewaterhouseCoopers Speciality Chemicals

Drax 31 December 2015 Deloitte Conventional Electricity

GKN 31 December 2015 PricewaterhouseCoopers Auto Parts

GlaxoSmithKline 31 December 2015 PricewaterhouseCoopers Pharmaceuticals

Hammerson 31 December 2015 Deloitte Retail REITs

Intercontinental Hotels 31 December 2015 Ernst & Young Hotels

ITV 31 December 2015 KPMG Broadcasting and Entertainment

Jardine Lloyd Thomson 31 December 2015 PricewaterhouseCoopers Non-life Insurance

Ladbrokes 31 December 2015 PricewaterhouseCoopers Gambling

Meggitt 31 December 2015 PricewaterhouseCoopers Aerospace

National Express 31 December 2015 Deloitte Travel

Relx 31 December 2015 Deloitte Publishing

Rexam 31 December 2015 PricewaterhouseCoopers Containers and Packaging

Rio Tinto 31 December 2015 PricewaterhouseCoopers General Mining

Rolls Royce 31 December 2015 KPMG Aerospace

Smith & Nephew 31 December 2015 KPMG Medical Equipment

Taylor Wimpey 31 December 2015 Deloitte Home Construction

Unilever 31 December 2015 KPMG Personal Products

CR Common Practices

FRS 101 “Reduced Disclosure Framework” – A review of application in parent company accounts of IFRS groups

3

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting a Wolters Kluwer Business, 145 London Road, Kingston Upon Thames, Surrey, KT2 6SR

Published on 21 July 2016

Analysis

How does a company qualify to use FRS 101?

In order to apply FRS 101 a company has to meet the definition of a qualifying entity which is “A member of a group

where the parent of that group prepares publicly available consolidated financial statements which are intended to

give a true and fair view and that member is included in the consolidation”. A qualifying entity may be a parent or a

subsidiary but not a consolidated group.

In addition a company must notify its shareholders in writing within a reasonable time frame of its intention to adopt

FRS 101. (The FRC has issued an exposure draft, FRED 65, proposing to remove the need for companies to inform

shareholders in writing. Comments on this FRED are invited until 14 October 2016. It is proposed that the effective

date for this amendment be accounting periods beginning on or after 1 January 2016) It can’t be applied if

shareholders holding in aggregate 5% of the shares object.

To comply fully with FRS 101 an entity must disclose a brief narrative summary of the disclosure exemptions adopted

and identify the consolidated group within which it is included. In addition, a full set of FRS 101 financial statements is

expected to include each of the primary financial statements required by IFRS (other than a cash flow statement which

is one of the optional exemptions), a summary of significant accounting policies and other explanatory notes. There is

a requirement for comparative information although exemptions exist for property, plant and equipment, intangible

assets, investment property, agricultural produce and biological assets.

How did companies notify shareholders?

In order to adopt FRS 101 companies should have informed shareholders in writing of the intent to do so in order to

give them a chance to object to the fact that information is being withheld, although this requirement is likely to be

removed (see note on FRED 65 above). If shareholders holding 5% or more of the share capital in aggregate object

the company cannot apply FRS 101. The document within which this notification is to be given is not specifically

defined.

In an attempt to establish how the sample companies notified shareholders we examined 2015 AGM notices sent to

shareholders and 2014 annual reports:

17 sample companies informed shareholders in either the 2015 AGM notice or the 2014 annual report.

6 companies including GlaxoSmithKline and British American Tobacco made reference to FRS 101 in both

documents.

A further 6 companies including Rio Tinto and GKN made reference to FRS 101 in the AGM notice only.

The remaining 5 companies including Taylor Wimpey and National Express notified shareholders in the 2014

annual report only.

The 2015 interim financial statements were employed by Croda International, ITV and Jardine Lloyd Thomson

as a method of informing shareholders.

CR Common Practices

FRS 101 “Reduced Disclosure Framework” – A review of application in parent company accounts of IFRS groups

4

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting a Wolters Kluwer Business, 145 London Road, Kingston Upon Thames, Surrey, KT2 6SR

Published on 21 July 2016

Based on our review we were unable to determine how the other 9 sample companies informed shareholders

although it should be noted that we did not perform an extensive review of all documentation made available to

shareholders. Our analysis does, however, show that there is no consensus as to how companies informed

shareholders of the disclosure exemptions intended to be adopted under FRS 101.

Primary Financial Statements: what formats did companies adopt?

When presenting primary financial statements under FRS 101 and indeed UK law, companies have a choice to adopt

either IFRS formats as outlined in IAS 1 “Presentation of financial statements” or the Companies Act 2006 formats. As

set out in the 2015 amended FRS 101 (paragraph 81C), it appears that companies should not adopt a halfway house

approach to presentation. The primary financial statements should strictly be fully compliant with one presentation

format or the other.

As parent company accounts, all but one in the sample have taken the exemption given by section 408 of the

Companies Act allowing the individual income statement not to be presented if it included such in group accounts.

Therefore our analysis focussed on the statements of financial position / balance sheet, with the following results:

11 companies adopt Companies Act presentation format including AstraZeneca (See Appendix Extract 1);

12 companies adopt IAS 1 presentation format including BAE Systems (See Appendix Extract 2); and

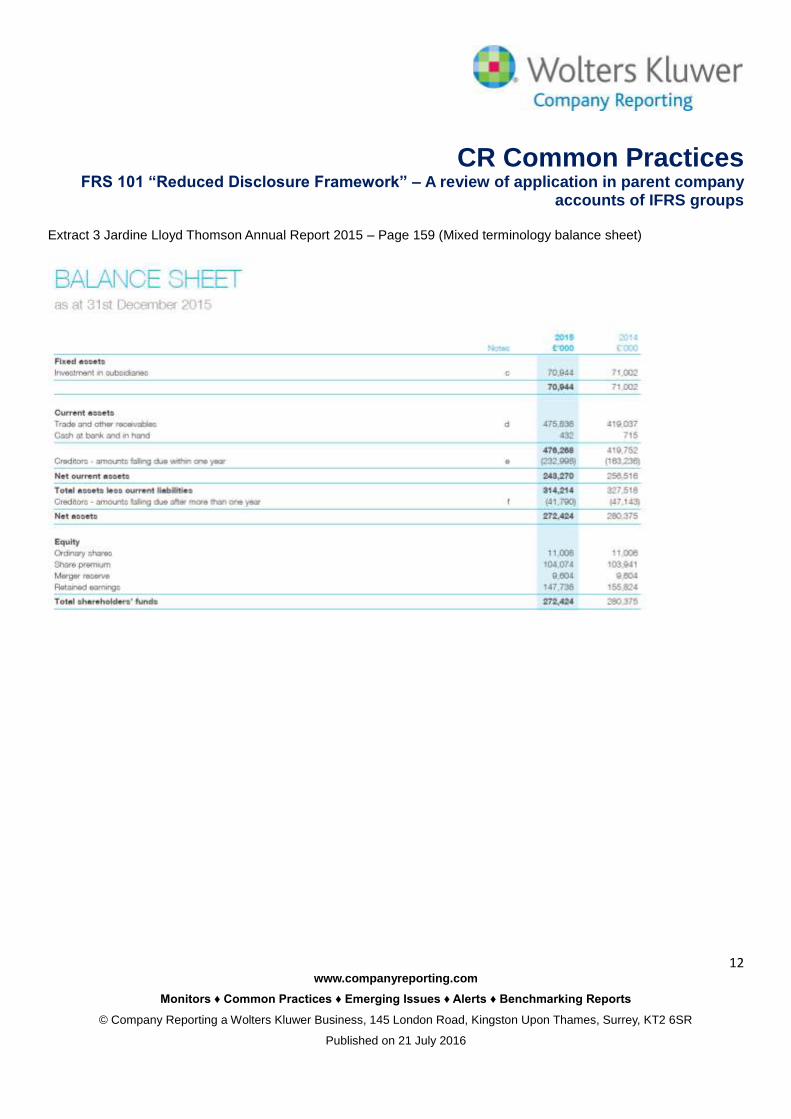

6 companies adopt a hybrid presentation using both Companies Act and IAS 1 terminology including Jardine

Lloyd Thomson (See Appendix Extract 3).

Balance sheet/Statement of financial position

presentation format adopted

Companies

Companies Act 2006 AstraZeneca, Amec Foster Wheeler, Anglo American, BP,

British American Tobacco, Croda International, Drax,

Intercontinental Hotels, National Express, Rio Tinto, and

Smith & Nephew

IAS 1 “Presentation of financial statements” BAE Systems, Centrica, Cobham, GKN, Hammerson,

ITV, Ladbrokes, Relx, Rexam, Rolls Royce, Taylor

Wimpey and Unilever

Hybrid Presentation Aggreko, BBA Aviation, Bodycote, GlaxoSmithKline,

Jardine Lloyd Thomson and Meggitt

Based on this sample there is no strong evidence that one presentation format is generally more popular than the

other. Further, no concrete conclusions can be drawn on whether companies of a particular type or clients of a

particular auditor are more likely to follow one presentation format or the other. All three sample companies audited by

Ernst and Young adopt the Companies Act format but a larger study would have to be performed to arrive at any

concrete conclusions. The lack of a decisive answer in this area is probably not surprising because both options are

equally permissible.

CR Common Practices

FRS 101 “Reduced Disclosure Framework” – A review of application in parent company accounts of IFRS groups

5

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting a Wolters Kluwer Business, 145 London Road, Kingston Upon Thames, Surrey, KT2 6SR

Published on 21 July 2016

It is surprising if not worrying, however, that there are some inconsistencies in terminology and formats. For example,

Company Law terminology such as fixed assets (rather than non-current assets) is used alongside IAS 1 terminology

(property, plant and equipment); or long-term receivables are included in ‘fixed assets’ rather than current assets

(Companies Act). 6 companies in the sample adopt such a ‘hybrid’ presentation and thus strictly their balance sheet

formats do not appear to comply with FRS 101 or the 2015 Regulations (for more information, refer to CCH Preparing

FRS 101 Accounts Section 4.3). It remains to be seen whether such companies fall more clearly into line with either

presentation in future years.

Have companies presented a cash flow statement?

Under old UK GAAP (FRS 1 “Cash flow statements”), companies did not have to present a cash flow statement if the

information was included in the consolidated financial statements. Under FRS 101 companies can also take

advantage of an exemption not to present a statement of cash flows. When doing so specific reference should be

made to the fact that such an exemption is applied.

BP is the only company in the sample to voluntarily present a cash flow statement (the same was true prior to

FRS 101 adoption).

Two companies in the sample, Anglo American and GKN while not presenting a cash flow statement, fail to

make any specific reference to the taking of such an exemption.

As companies did not present cash flow statements last year it is not surprising considering the existence of a

possible exemption under FRS 101 that they again choose not to do so. However under a strict interpretation of FRS

101, companies should clearly disclose that they have taken the exemption.

How detailed is disclosure of the list of exemptions?

To comply fully with FRS 101 an entity must disclose a brief narrative summary of the disclosure exemptions adopted.

The format of this narrative summary is, however, not defined. This section considers the detail that companies give in

respect of common exemptions taken with the aim of identifying our opinion of best practice.

All companies in the sample with the exception of Anglo American disclose a narrative description of

exemptions taken (Anglo American simply states that it takes all exemptions available).

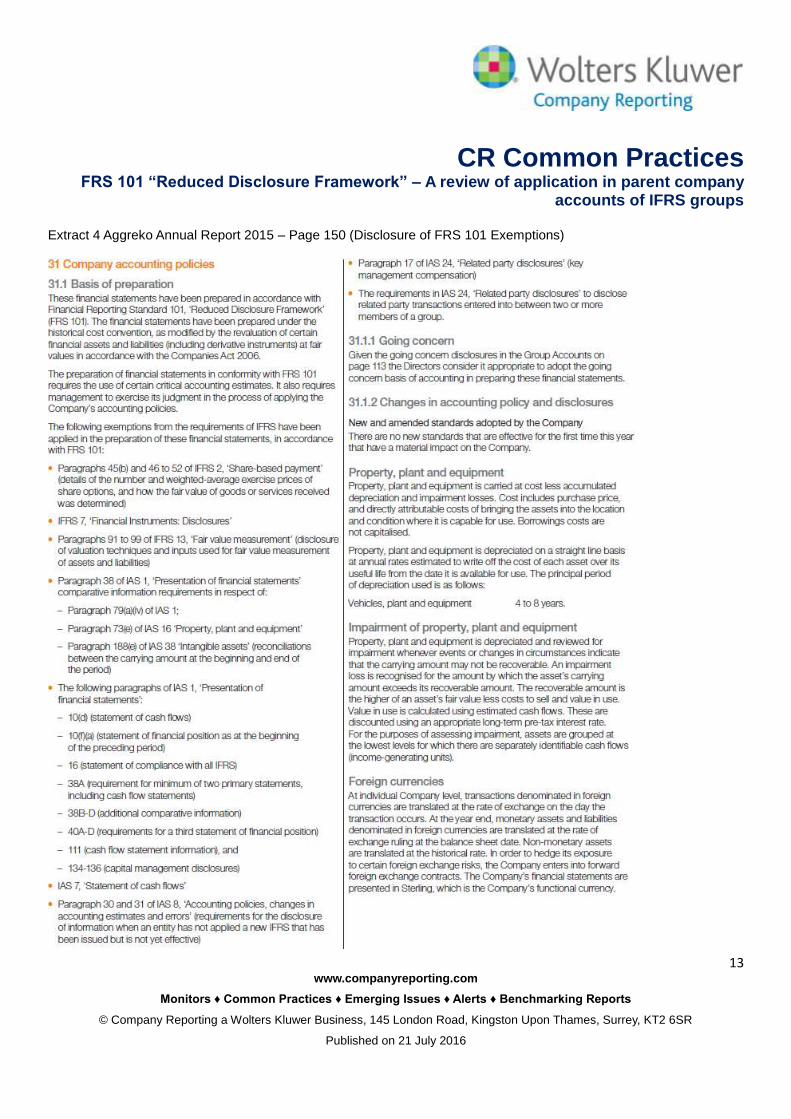

Only 3 companies in the sample, Jardine Lloyd Thomson, Rio Tinto and Aggreko (See Appendix Extract 4)

include both paragraph references and what we consider to be a good level of descriptive detail in respect of

all exemptions taken including those in respect of fair value measurement and share-based payments (best

practice examples all audited by PricewaterhouseCoopers).

19 companies in the sample fall short of best practice as no paragraph references are included in relation to

exemptions taken.

7 companies including Amec Foster Wheeler, Cobham, International Continental Hotels and Rexam when

identifying IAS 1 “Presentation of financial statements” disclosure exemptions present both a description of

the exemption taken and the relevant paragraph of the standard. Meggitt, BAE Systems and

GlaxoSmithKline (See Appendix Extract 5) give a list of paragraphs only.

CR Common Practices

FRS 101 “Reduced Disclosure Framework” – A review of application in parent company accounts of IFRS groups

6

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting a Wolters Kluwer Business, 145 London Road, Kingston Upon Thames, Surrey, KT2 6SR

Published on 21 July 2016

27 companies in the sample identify that exemptions are taken in respect of related party disclosures:

o 8 of these companies including GKN, Bodycote, Drax and National Express give no further detail (5

of which are audited by Deloitte).

o The remaining 19 companies including AstraZeneca, BBA Aviation, Aggreko (See Appendix Extract

4), Amec Foster Wheeler and Cobham give more detail by referring to transactions with wholly owned

subsidiaries or two or more members of the group.

14 companies in the sample list an exemption in respect of related party key management remuneration

disclosures:

o 11 of these companies including Aggreko (See Appendix Extract 4) Cobham, ITV and Rexam make

specific reference to key management remuneration/compensation.

o The remaining 3 companies Meggitt, BAE Systems and GlaxoSmithKline make no specific statement

instead only referring to IAS 24 “Related party disclosures” paragraph 17.

For a company to simply state that it takes advantage of all disclosure exemptions available is not in our view in line

with FRS 101 so we would hope to see improved disclosure from Anglo American next year. The other companies in

the sample all do what is required by FRS 101 in terms of giving a description of exemptions taken.

To present a list of standard paragraph references without any narrative description falls short of best practice as all

readers of the financial statements are not going to be IFRS experts. Best practice as exhibited by 3 companies,

Jardine Lloyd Thomson, Rio Tinto and Aggreko is to present both paragraph references and a good level of

descriptive detail in respect of all exemptions taken. What really makes these companies stand out from many others

is the fact that they give good descriptive information in respect of fair value measurement and share-based payment

exemptions taken.

To what extent is the concept of equivalence considered when disclosing exemptions taken?

Many of the exemptions that can be taken under FRS 101 are predicated on the fact that equivalent information is

disclosed within the parent companies consolidated financial statements. This section examines to what extent

companies make reference to the concept of equivalence when identifying exemptions taken.

16 companies make reference to equivalent information being included in the consolidated financial

statements in relation to exemptions taken.

The most common exemptions linked to the concept of equivalence are, perhaps unsurprisingly, share-based

payments, financial instruments and fair value disclosures.

Of the above 16, 5 companies including Unilever and Bodycote make a general statement that where

required additional disclosure is given in the group accounts.

Hammerson links all its exemptions to the concept of equivalence including a number not identified in that

way by any other sample company.

The remaining 10 companies mention the concept of equivalence in relation to a subset of exemptions taken.

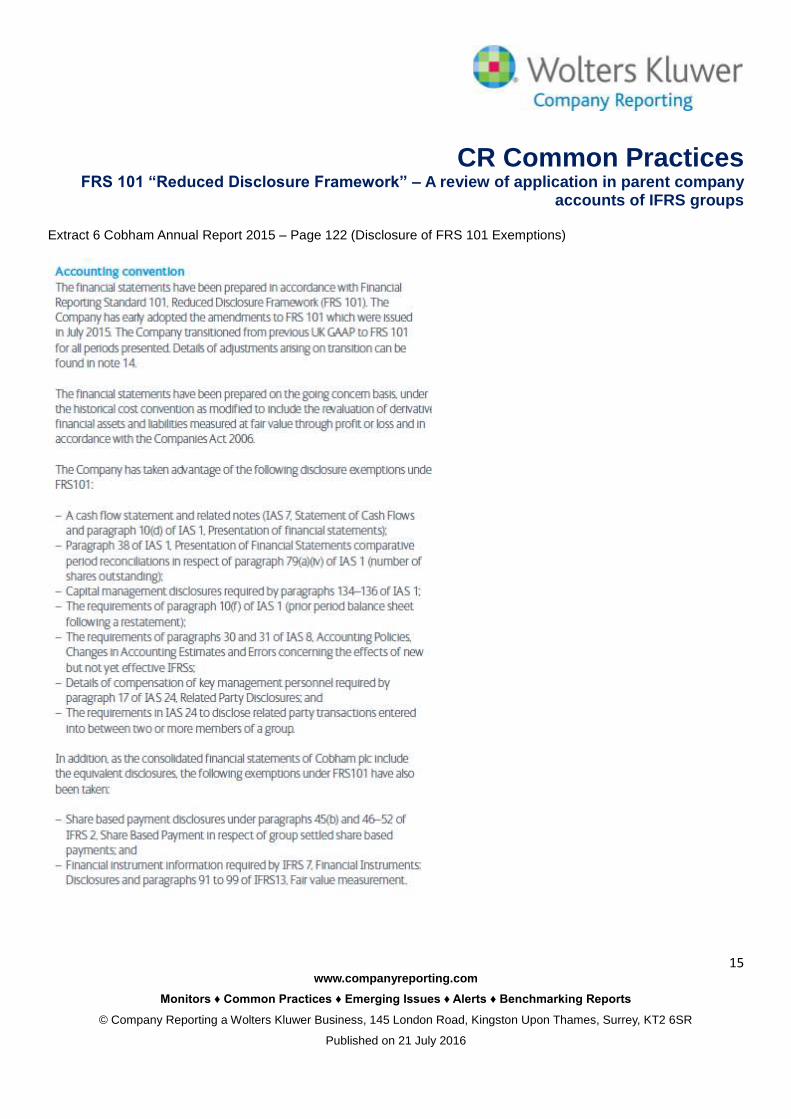

o Of these, 9 including Smith and Nephew, Centrica ,BBA Aviation and Cobham (See Appendix Extract

6) do this by presenting two separate lists of exemptions.

CR Common Practices

FRS 101 “Reduced Disclosure Framework” – A review of application in parent company accounts of IFRS groups

7

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting a Wolters Kluwer Business, 145 London Road, Kingston Upon Thames, Surrey, KT2 6SR

Published on 21 July 2016

o Jardine Lloyd Thomson (See Appendix Extract 7) instead includes a note against the one exemption

that it takes in respect of the concept of equivalence, financial instrument disclosures, in its single list

of exemptions.

Best practice in our view is to refer to the concept of equivalence in respect of defined exemptions. The best way of

doing this, however, is arguably dependent on the number of exemptions to which the concept of equivalence is

attached. If there are a large number of such exemptions then two separate lists is a clearer presentation format. If

there are relatively few exemptions of this type, however, the alternative of including notes alongside specific

exemptions is arguably a more succinct method of presentation.

What is the impact of FRS 101 on the length of company financial statements?

FRS 101 allows companies to limit the level of disclosures that they give. Based on this it would seem sensible to

assume that the current year financial statements prepared under FRS 101 would on average be shorter than the

previous year financial statements that were not prepared under FRS 101. However our findings were as follows:

23 companies actually have longer financial statements than was the case last year.

For a further 5 companies there is no change in length.

Aggreko is the only company where its financial statements are shorter than last year.

It has to be noted that we are not comparing like with like. Each of the companies in the sample previously prepared

their financial statements under old UK GAAP rather than IFRS. The starting point when a company prepares financial

statements under FRS 101 is EU adopted IFRS from which it can then take exemptions, not old UK GAAP. However,

the general trend for such a large majority of financial statements to be longer, particularly for relatively simple parent

companies, could still be considered surprising. A contributory factor to this could be companies giving extra

information on first time adoption of FRS 101. A fairer comparison of the length of financial statements pre and post

FRS 101 adoption may perhaps be made next year.

Is there a relationship between length and number of exemptions?

It would seem sensible that there should be some sort of inverse correlation between the number of exemptions that a

company identifies and the length of its financial statements. We found that there is no strong evidence to support

such a proposition.

The financial statements of only three companies, BP, Jardine Lloyd Thomson and Smith and Nephew

seemed to show longer financial statements due to fewer exemptions taken or vice versa.

Based on the evidence we have to conclude that no relationship exists for our sample of companies but for a wider

sample of different companies this may be an interesting point to analyse in future.

CR Common Practices

FRS 101 “Reduced Disclosure Framework” – A review of application in parent company accounts of IFRS groups

8

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting a Wolters Kluwer Business, 145 London Road, Kingston Upon Thames, Surrey, KT2 6SR

Published on 21 July 2016

Are there significant changes in accounting policy on adoption of FRS 101?

The adoption of FRS 101 is for all of the companies in our sample a change in accounting system from old UK GAAP

to IFRS. As such some changes in accounting measurement and classification would be expected but the areas these

are in and to what extent there is an impact will vary. In our sample we noted that material changes on transition take

place in a comparatively low number of areas on implementation of FRS 101 and only in a minority of companies:

The majority of the companies in the sample recognise no material changes in measurement.

14 companies report material changes in accounting policy.

10 companies including BAE Systems, Rexam and Cobham make changes in respect of defined benefit

pension schemes.

o Group defined benefit schemes could previously be accounted for as defined contribution schemes if

multiple companies were involved. This is no longer the case.

6 companies including Bodycote, Meggitt and Rexam change the treatment of computer software.

o Software costs unless integral to the related hardware are considered to be intangible assets.

8 companies including Unilever, Meggitt and Ladbrokes make changes in relation to deferred tax.

o Deferred tax is now based on differences between the carrying amount of an asset or liability and its

tax base. Additional deferred tax is recognised on the initial recognition of assets and liabilities when

neither accounting profit nor taxable profit is affected.

o In this sample companies recognise deferred tax in respect of retirement benefit assets/obligations,

share-based payments and intangible assets.

4 companies reclassify amounts from current to non-current classifications or vice versa.

Centrica and BBA Aviation reclassify debt financing from part of investments to loans and receivables.

Unilever ends the amortisation of indefinite life intangible assets and now follows a policy of annual

impairment review. An adjustment is made to remove the amortisation charge in respect of indefinite lived

intangible assets.

Based on this sample of parent companies the recognition implications of FRS 101 implementation are limited but this

is likely to be due to the nature of the companies as investment holding companies. Further analysis of a broader

spectrum of companies when their accounts are available would no doubt reveal more changes on transition.

Summary - Conclusion:

Our principal conclusions are that:

In light of FRED 65 proposing to remove the requirement to inform shareholders in advance of the use of

disclosure exemptions, we noted there was no consensus as to how companies informed shareholders of the

intent to adopt FRS 101 and the exemptions adopted. Companies used either the AGM notice or previous

financial reports or both, but in 9 cases we found no evidence of the notice.

For the statement of financial position, 11 companies adopt a Companies Act style format with 12 adopting an IAS

1 style presentation. 6 companies adopt a ‘hybrid’ presentation with a combination of Companies Act and IAS 1

terminology.

CR Common Practices

FRS 101 “Reduced Disclosure Framework” – A review of application in parent company accounts of IFRS groups

9

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting a Wolters Kluwer Business, 145 London Road, Kingston Upon Thames, Surrey, KT2 6SR

Published on 21 July 2016

28 out of the 29 companies present a narrative description of the disclosure exemptions taken under FRS 101.

Only three sample companies follow best practice when identifying exemptions by including both IFRS paragraph

references and a full narrative description in respect of all exemptions taken.

16 sample companies make reference to equivalent information being included within the consolidated financial

statements with 10 of these companies referring to equivalent information in respect of specific exemptions.

Although all companies take advantage of disclosure exemptions following application of FRS 101, the trend is

actually for the company financial statements to be longer this year compared to last year.

14 sample companies restate prior year figures on transition to reflect changes in measurement when moving from

old UK GAAP to FRS 101.

CR Common Practices

FRS 101 “Reduced Disclosure Framework” – A review of application in parent company accounts of IFRS groups

10

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting a Wolters Kluwer Business, 145 London Road, Kingston Upon Thames, Surrey, KT2 6SR

Published on 21 July 2016

Appendix Extracts

Extract 1 AstraZeneca Annual Report 2015 – Page 197 (Companies Act Style Balance Sheet)

CR Common Practices

FRS 101 “Reduced Disclosure Framework” – A review of application in parent company accounts of IFRS groups

11

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting a Wolters Kluwer Business, 145 London Road, Kingston Upon Thames, Surrey, KT2 6SR

Published on 21 July 2016

Extract 2 BAE Systems Annual Report 2015 Page 167 (IAS 1 Style Balance Sheet)

CR Common Practices

FRS 101 “Reduced Disclosure Framework” – A review of application in parent company accounts of IFRS groups

12

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting a Wolters Kluwer Business, 145 London Road, Kingston Upon Thames, Surrey, KT2 6SR

Published on 21 July 2016

Extract 3 Jardine Lloyd Thomson Annual Report 2015 – Page 159 (Mixed terminology balance sheet)

CR Common Practices

FRS 101 “Reduced Disclosure Framework” – A review of application in parent company accounts of IFRS groups

13

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting a Wolters Kluwer Business, 145 London Road, Kingston Upon Thames, Surrey, KT2 6SR

Published on 21 July 2016

Extract 4 Aggreko Annual Report 2015 – Page 150 (Disclosure of FRS 101 Exemptions)

CR Common Practices

FRS 101 “Reduced Disclosure Framework” – A review of application in parent company accounts of IFRS groups

14

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting a Wolters Kluwer Business, 145 London Road, Kingston Upon Thames, Surrey, KT2 6SR

Published on 21 July 2016

Extract 5 GlaxoSmithKline Annual Report 2015 – Page 214 (Disclosure of FRS 101 Exemptions)

CR Common Practices

FRS 101 “Reduced Disclosure Framework” – A review of application in parent company accounts of IFRS groups

15

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting a Wolters Kluwer Business, 145 London Road, Kingston Upon Thames, Surrey, KT2 6SR

Published on 21 July 2016

Extract 6 Cobham Annual Report 2015 – Page 122 (Disclosure of FRS 101 Exemptions)

CR Common Practices

FRS 101 “Reduced Disclosure Framework” – A review of application in parent company accounts of IFRS groups

16

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting a Wolters Kluwer Business, 145 London Road, Kingston Upon Thames, Surrey, KT2 6SR

Published on 21 July 2016

Extract 7 Jardine Lloyd Thomson Annual Report 2015 – Page 161 (Disclosure of FRS 101 Exemptions)