Embed Size (px)

Citation preview

5

Activity-BasedCosting Systems

Asfandyar JahangirAzib Hamid

Hassan Mohi-ud-Din.

Asfandyar JahangirAzib Hamid

Hassan Mohi-ud-Din.

TRADITIONAL COSTING SYSTEMS

A single company-wide overhead ratebased on direct labor hours may be

used to allocate overhead to productsin these labor intensive processes.

A single company-wide overhead ratebased on direct labor hours may be

used to allocate overhead to productsin these labor intensive processes.

Traditional cost systems were created whenmanufacturing processes were labor intensive or machine

intensive

Traditional cost systems were created whenmanufacturing processes were labor intensive or machine

intensive

TRADITIONAL COSTING SYSTEMS

Job 1 Job 2

Labor Hours 2 6

In this example, overhead will be allocated to jobs using direct labor hours. If total overhead is $120,

how much will be allocated to each job?

In this example, overhead will be allocated to jobs using direct labor hours. If total overhead is $120,

how much will be allocated to each job?

TRADITIONAL COSTING SYSTEMS

Job 1 Job 2

Labor Hours 2 6

Overhead Allocation

30$ 90$

Overhead Rate = $120 ÷ 8 direct labor hoursOverhead Rate = $15 per direct labor hour

Job 1 = 2 hours × $15 per hour = $30Job 2 = 6 hours × $15 per hour = $90

The company introducesautomated machinery. Totaloverhead rises from $120 to

$420, while the labor timeneeded for Job 2 falls from

6 hours to 1 hour. Nowallocate the $420 overhead

to the two jobs.

TRADITIONAL COSTING SYSTEMS

TRADITIONAL COSTING SYSTEMS

Job 1 Job 2

Labor Hours 2 1

Overhead Allocation

280$ 140$

Overhead Rate = $420 ÷ 3 direct labor hoursOverhead Rate = $140 per direct labor hour

Job 1 = 2 hours × $140 per hour = $280Job 2 = 1 hour × $140 per hour = $140

TRADITIONAL COSTING SYSTEMS

Job 1 Job 2

Labor Hours 2 1

Overhead Allocation

280$ 140$

Is this a reasonable costing method?

Automation benefited only Job 2, but most of the

additional overhead cost was allocated to Job 1.

Clearly, we need to look for another cost driver.

UNDERCOSTING AND OVERCOSTING

Product Undercosting: A product consume a high level of resources but is reported to be a low cost per unit.

Product Overcosting: A product consumes a low level of resources but is reported to be a high cost per unit.

Product Undercosting: A product consume a high level of resources but is reported to be a low cost per unit.

Product Overcosting: A product consumes a low level of resources but is reported to be a high cost per unit.

PRODUCT-COST CROSS-SUBSIDISATION

If a company undercosts one of its products, it will overcost at least one of its other products and vice versa.

Emma James Jessica Matthew Total Average

Entrée $11 $20 $15 $14 $60 $15

Dessert 0 8 4 4 16 4

Drinks 4 14 8 6 32 8

Total $15 $42 $27 $24 $108 $27

If a company undercosts one of its products, it will overcost at least one of its other products and vice versa.

Emma James Jessica Matthew Total Average

Entrée $11 $20 $15 $14 $60 $15

Dessert 0 8 4 4 16 4

Drinks 4 14 8 6 32 8

Total $15 $42 $27 $24 $108 $27

ACTIVITY-BASED COSTING (ABC)

A costing method that identifies the activities performed within the organization as it delivers

its goods and services.

A costing method that identifies the activities performed within the organization as it delivers

its goods and services.

ProductsRequire

Activities

ActivitiesConsume

Resources

PeopleManage

Activities

ACTIVITY-BASED COSTING (ABC)

A costing method that assigns costs to products, based on the number of activities the

organization used in producing them.

A costing method that assigns costs to products, based on the number of activities the

organization used in producing them.

Lot size Directlabor hours

Processsetups

Designtime

Machinehours

Customercontact

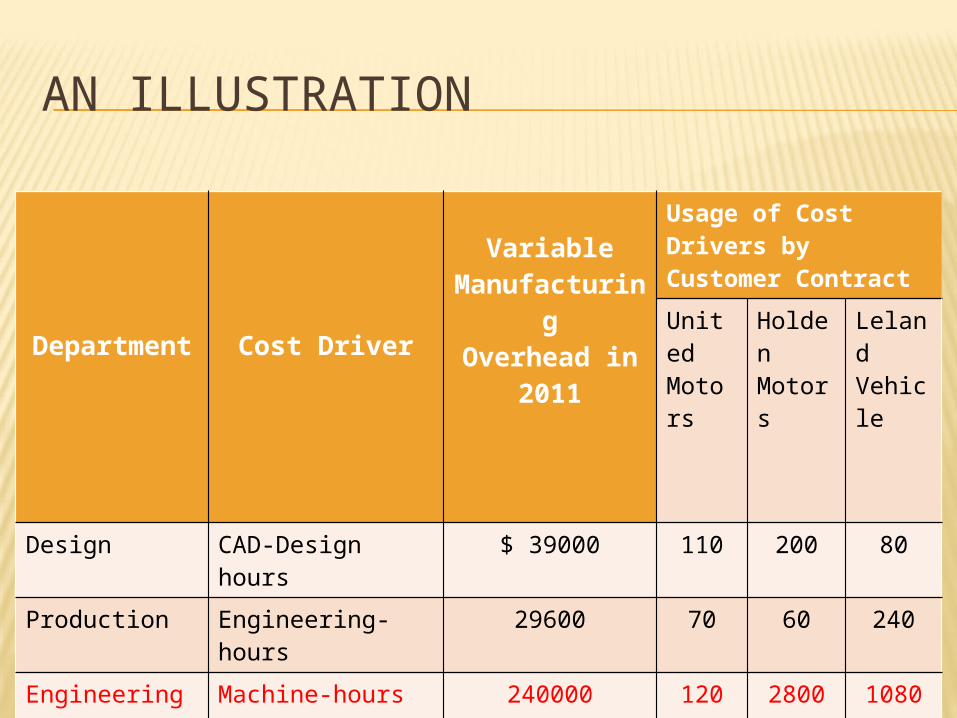

AN ILLUSTRATION

Department

Cost Driver

VariableManufacturi

ngOverhead in

2011

Usage of Cost Drivers by Customer Contract

United Motors

Holden Motors

Leland Vehicle

Design CAD-Design hours

$ 39000 110 200 80

Production Engineering-hours

29600 70 60 240

Engineering Machine-hours 240000 120 2800 1080

Total 308600

AN ILLUSTRATION

Department

Cost Driver

VariableManufacturi

ngOverhead in

2011

Usage of Cost Drivers by Customer Contract

United Motors

Holden Motors

Leland Vehicle

Design CAD-Design hours

$ 39000 110 200 80

Production Engineering-hours

29600 70 60 240

Engineering Machine-hours 240000 120 2800 1080

Total 308600

CONTD….

Actual plant-wide variable MOH rate based on machine hours, $308,600/4,000

$77.15 per machine hour

United Motors

Holden Motors

Leland Vehicle Total

Variable manufacturing overhead, allocated based on machine hours ($77.15 120; $77.15 2,800; $77.15 1,080)

$9,258

$216,020

$83,322

$308,600

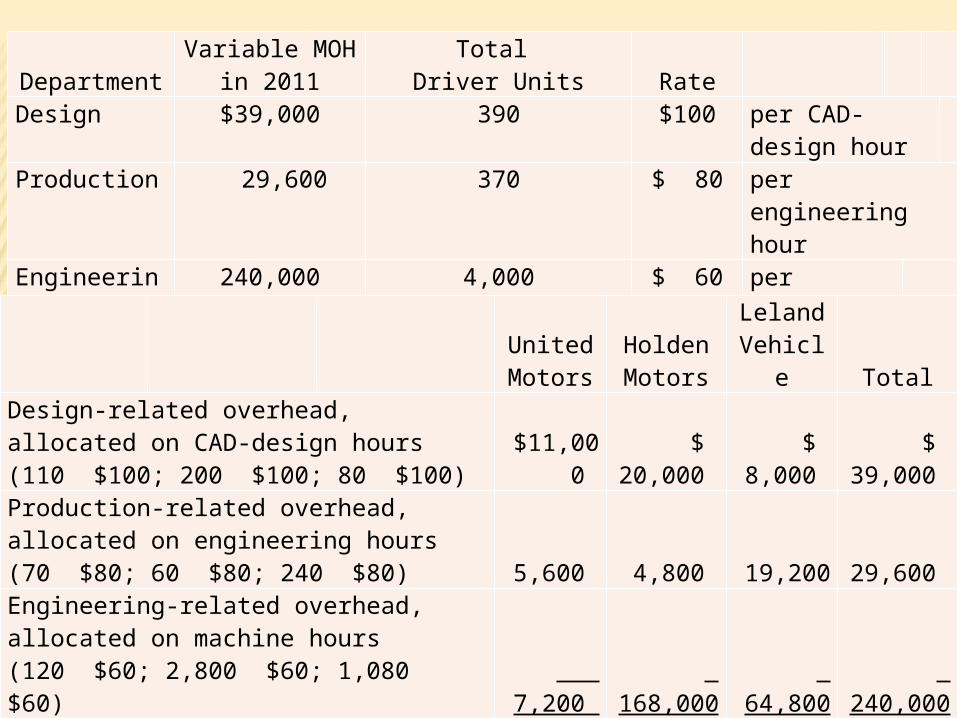

Department

Variable MOH in 2011

Total Driver Units Rate

Design $39,000 390 $100 per CAD-design hour

Production 29,600 370 $ 80 per engineering hour

Engineering 240,000 4,000 $ 60 per machine hour

United Motors

HoldenMotors

Leland Vehicle Total

Design-related overhead, allocated on CAD-design hours (110 $100; 200 $100; 80 $100)

$11,000

$ 20,000

$ 8,000

$ 39,000

Production-related overhead, allocated on engineering hours (70 $80; 60 $80; 240 $80) 5,600 4,800 19,200 29,600 Engineering-related overhead, allocated on machine hours (120 $60; 2,800 $60; 1,080 $60)

7,200

168,000

64,800

240,000

Total

$23,800

$192,800

$92,000

$308,600

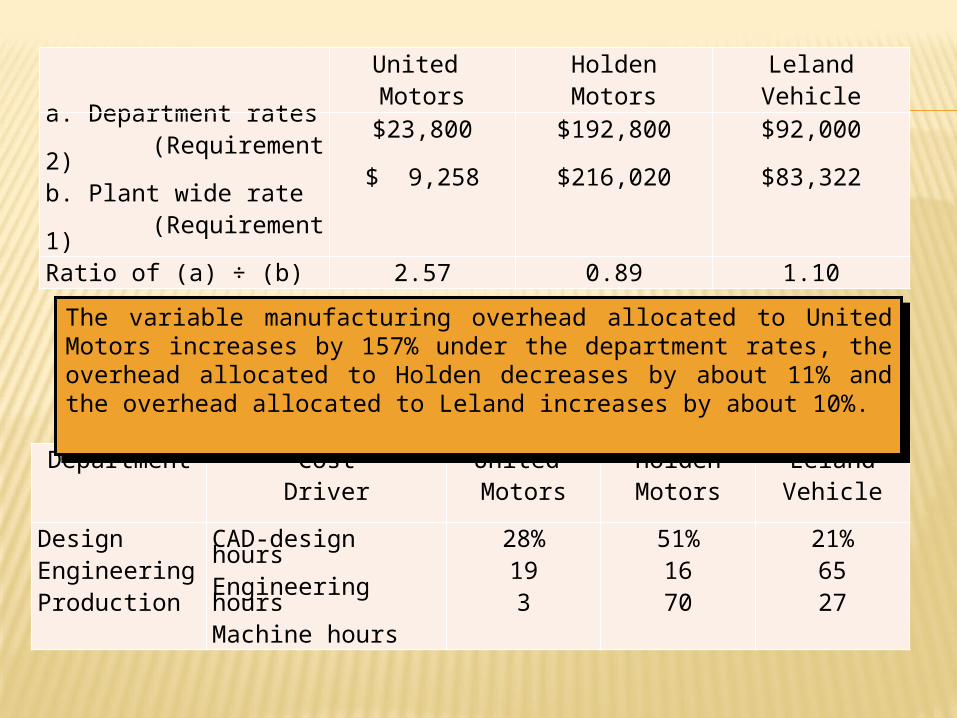

United

MotorsHoldenMotors

LelandVehicle

a. Department rates (Requirement 2)b. Plant wide rate (Requirement 1)

$23,800

$ 9,258

$192,800

$216,020

$92,000

$83,322

Ratio of (a) ÷ (b) 2.57 0.89 1.10

Department Cost

DriverUnited Motors

HoldenMotors

LelandVehicle

DesignEngineeringProduction

CAD-design hoursEngineering hoursMachine hours

28%193

51%1670

21%6527

The variable manufacturing overhead allocated to United Motors increases by 157% under the department rates, the overhead allocated to Holden decreases by about 11% and the overhead allocated to Leland increases by about 10%.

The variable manufacturing overhead allocated to United Motors increases by 157% under the department rates, the overhead allocated to Holden decreases by about 11% and the overhead allocated to Leland increases by about 10%.

COST HIERARCHIESUNIT-LEVEL COST

Cost of activities performed on each individual unit of a product or service e.g., machine operation costs

BATCH-LEVEL COST Cost of activities related to group of units of a product or service rather

than each individual unit of product or service e.g., set up cost

PRODUCT-SUSTAINING COSTCost of activities under taken to support individual products or services regardless

of the number of units or batches e.g., design cost

FACILITY-SUSTAINING COSTCost of activities that cannot be traced to individual products or services but that

support the organization as a whole e.g., general admin cost

ABC– BENEFITS AND LIMITATIONSMore accurate and

informative product costs lead to better pricing decisions.

The activities driving costs are more accurately measured.

Managers gain easier access to the relevant costs.

More accurate and informative product costs lead to better pricing decisions.

The activities driving costs are more accurately measured.

Managers gain easier access to the relevant costs.

An ABC system is very expensiveto develop and implement, and

very time-consuming to maintain.

An ABC system is very expensiveto develop and implement, and

very time-consuming to maintain.

WHERE TO APPLY ABC-YO!!!

1. The Asif Zardari Rule:• Go where the money is!• Look for the areas of large indirect cost/support activities

2. High Complexity Rule:• Look for how different products, processes, customers are!

New Vs Mature products

Custom Vs Standard products

Infrequent Vs Frequent products

Small Vs Irregular products

Low volume Vs High volume

1. The Asif Zardari Rule:• Go where the money is!• Look for the areas of large indirect cost/support activities

2. High Complexity Rule:• Look for how different products, processes, customers are!

New Vs Mature products

Custom Vs Standard products

Infrequent Vs Frequent products

Small Vs Irregular products

Low volume Vs High volume

WHALE CURVE

ABC IN SERVICE AND MERCHANDISING COMPANIES

The process is exactly the same as for manufacturing!

Identify and classify the activities related to the company’s products or services.

Estimate the cost of each activity identified in .

Calculate a cost-driver rate for each activity.

Assign activity costs to products using the relevant cost-driver rates.

Thanks for the Patience

Now its your turn!!