Embed Size (px)

Citation preview

Completion Report

Program Number: 36383 Loan Number: 2129 December 2009

Cambodia: Small and Medium Enterprise Development Program

CURRENCY EQUIVALENTS

Currency Unit – riel (KR)

At Appraisal At Program Completion (21 September 2004) (31 August 2008)

KR1.00 = $0.00027 $0.00025 $1.00 = KR3,988.50 KR4,199.90

ABBREVIATIONS

ABC – Association of Banks in Cambodia ADB – Asian Development Bank CAS – Cambodian Accounting Standard CIS – credit information system CSDP – Cambodia Small and Medium Enterprise Development Program Danida – Danish International Development Assistance FRT – financial reporting template MEF – Ministry of Economy and Finance MIME – Ministry of Industry, Mines, and Energy MOC – Ministry of Commerce NBC – National Bank of Cambodia NIS – National Institute of Statistics PER – program evaluation report PSC – program steering committee SCSME – subcommittee for small and medium-sized enterprises SMEs – small and medium-sized enterprises SMEDF – small and medium-sized enterprise development framework TA – technical assistance TASF – Technical Assistance Special Fund VAT – value-added tax WTO – World Trade Organization

NOTES

(i) The fiscal year (FY) of the government and its agencies ends on 31 December. (ii) In this report, "$" refers to US dollars.

Vice-President C. Lawrence Greenwood, Jr., Operations 2 Director General A. Thapan, Southeast Asia Department (SERD) Director J. Ahmed, Financial Sector, Public Management and Trade Division, SERD Team leader L. Jovellanos, Senior Economics Officer, SERD Team member F. Barot, Administrative Assistant, SERD

In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area.

CONTENTS

Page

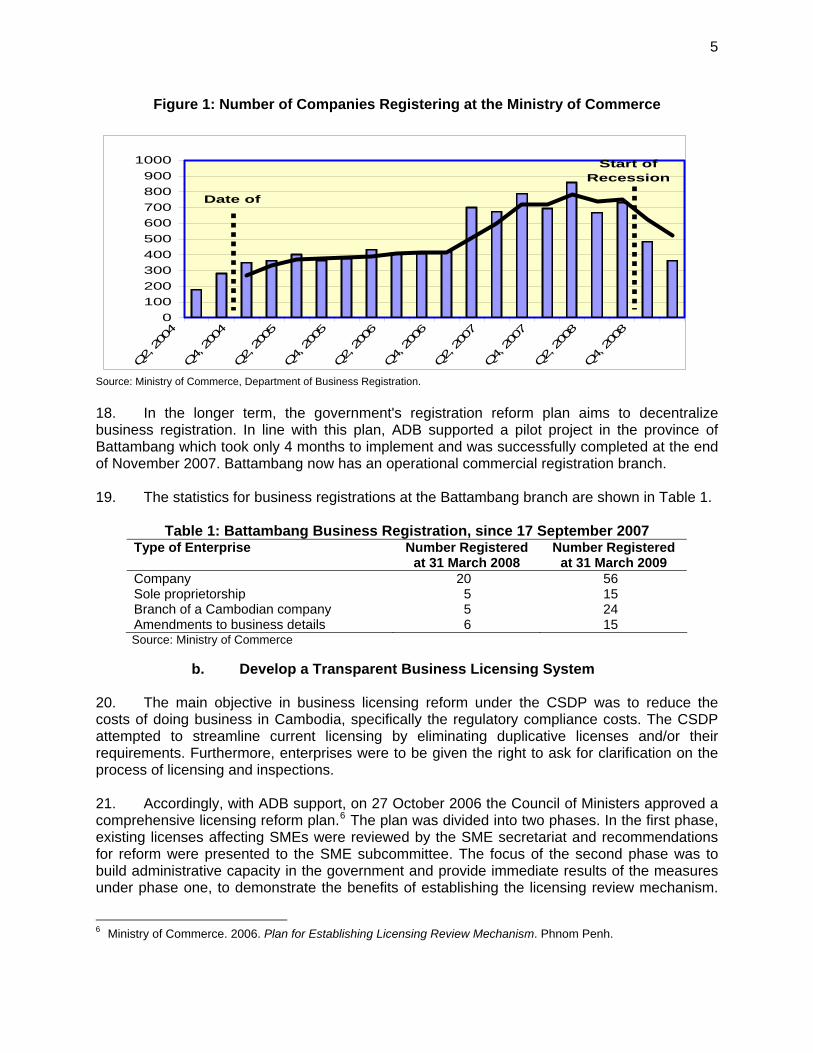

BASIC DATA i I. PROGRAM DESCRIPTION 1 II. EVALUATION OF DESIGN AND IMPLEMENTATION 2

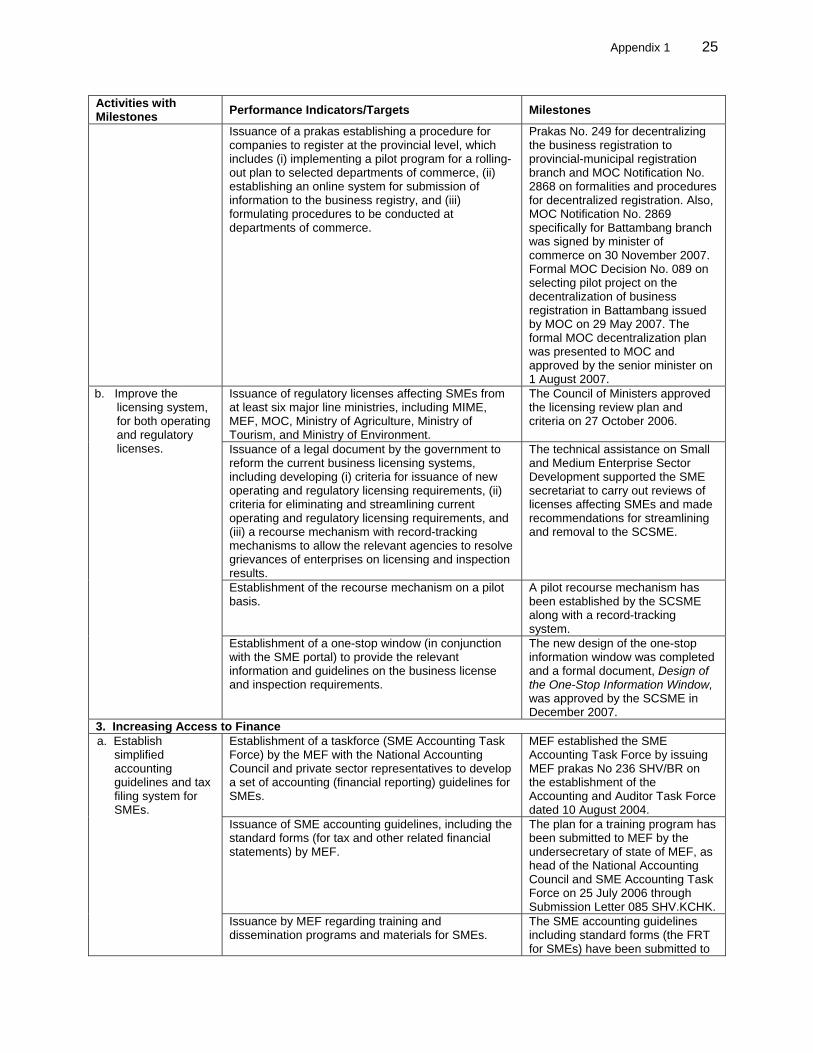

A. Relevance of Design and Formulation 2 B. Program Outputs 3 C. Program Costs and Disbursements 9 D. Program Schedule 9 E. Implementation Arrangements 10 F. Conditions and Covenants 10 G. Related Technical Assistance 11 H. Consultant Recruitment and Procurement 11 I. Performance of Consultants 12 J. Performance of the Borrower and the Executing Agency 12 K. Performance of the Asian Development Bank 12

III. EVALUATION OF PERFORMANCE 13

A. Relevance 13 B. Effectiveness in Achieving Outcome 13 C. Efficiency in Achieving Outcome and Outputs 14 D. Preliminary Assessment of Sustainability 15 E. Impact 15

IV. OVERALL ASSESSMENT AND RECOMMENDATIONS 15

A. Overall Assessment 15 B. Lessons 15 C. Recommendations 16

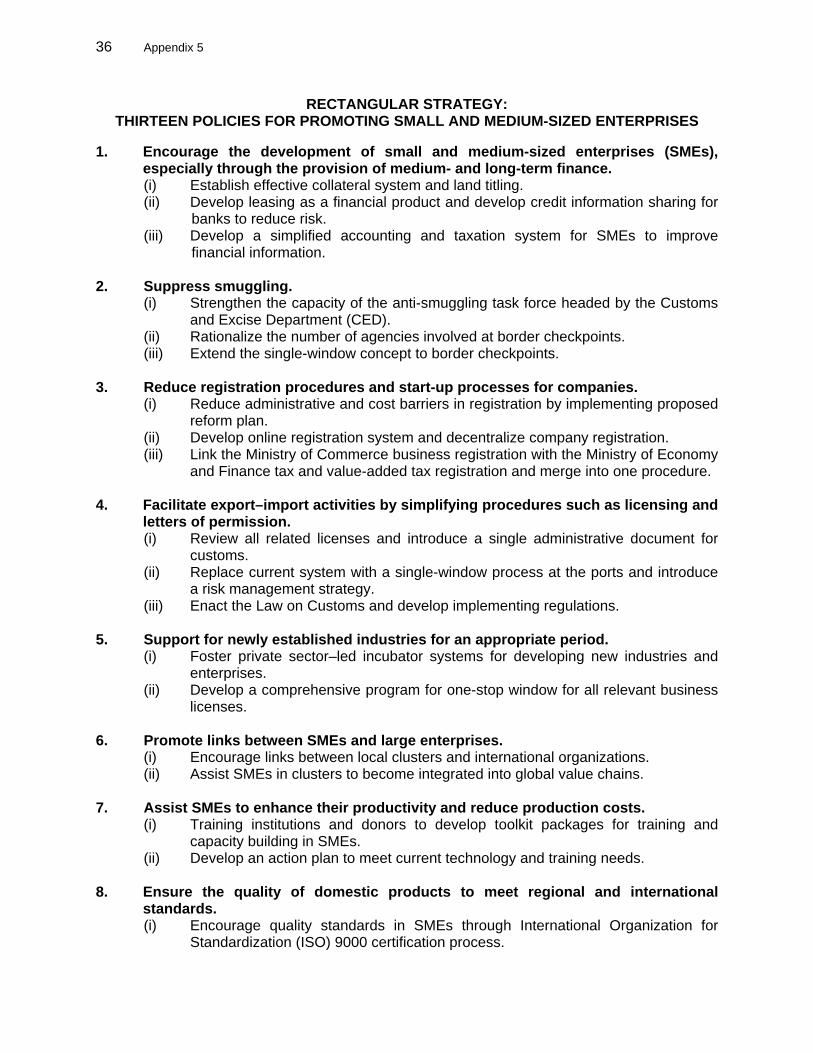

APPENDIXES 1. Design and Monitoring Framework 20 2. Status of Compliance: First Tranche 28 3. Status of Compliance: Second Tranche 29 4. Status of Compliance: Third Tranche 32 5. Rectangular Strategy: Thirteen Policies for Promoting Small and Medium-Sized Enterprises 36 6. Sustainability of Nonlegal and Nonregulatory Measures 38

i

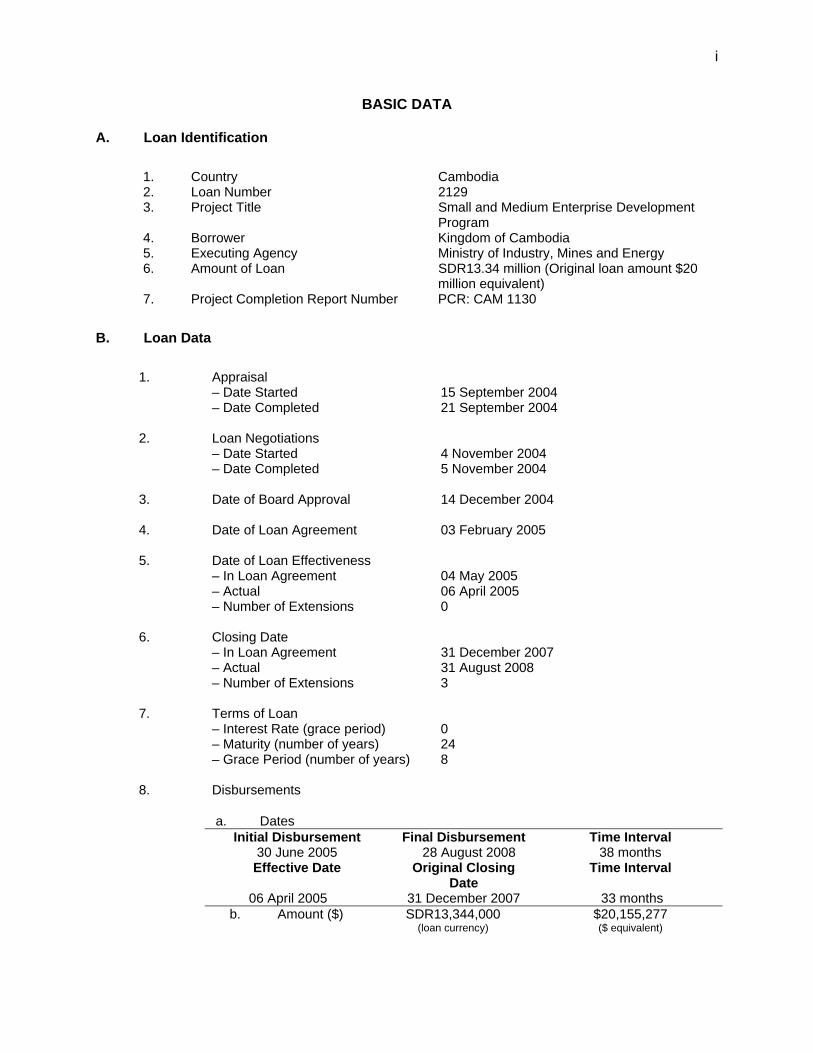

BASIC DATA A. Loan Identification

1. Country Cambodia 2. Loan Number 2129 3. Project Title Small and Medium Enterprise Development

Program 4. Borrower Kingdom of Cambodia 5. Executing Agency Ministry of Industry, Mines and Energy 6. Amount of Loan SDR13.34 million (Original loan amount $20

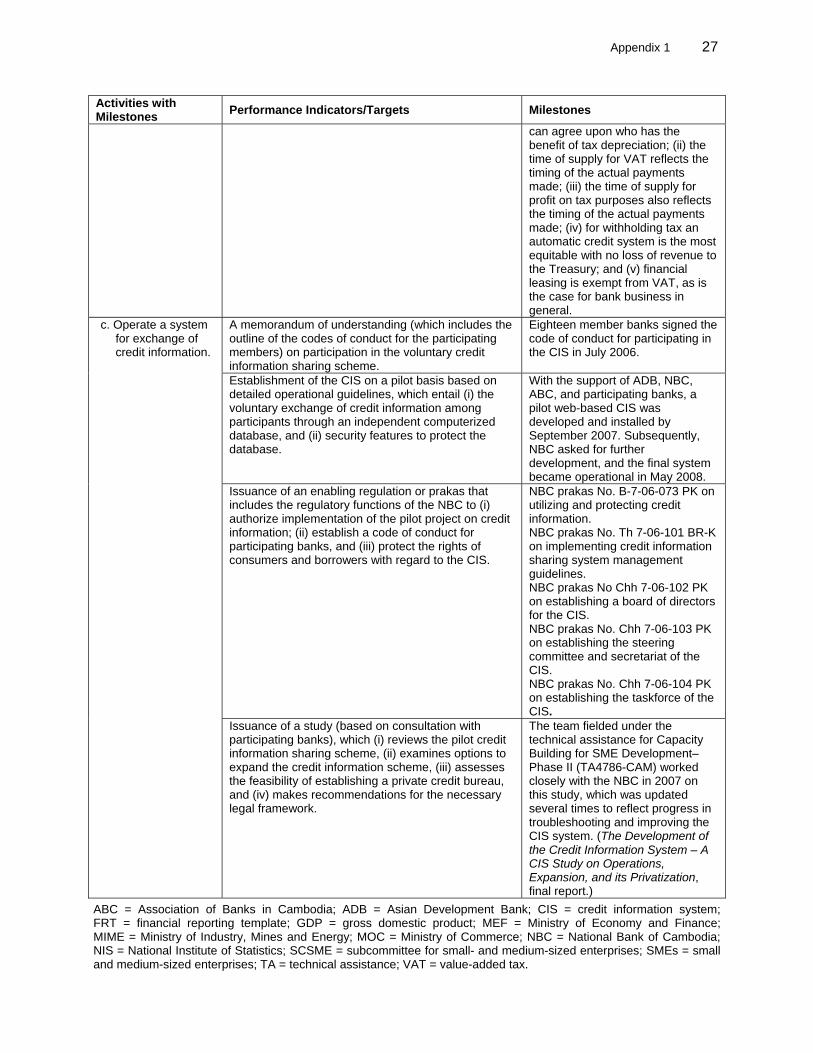

million equivalent) 7. Project Completion Report Number PCR: CAM 1130

B. Loan Data

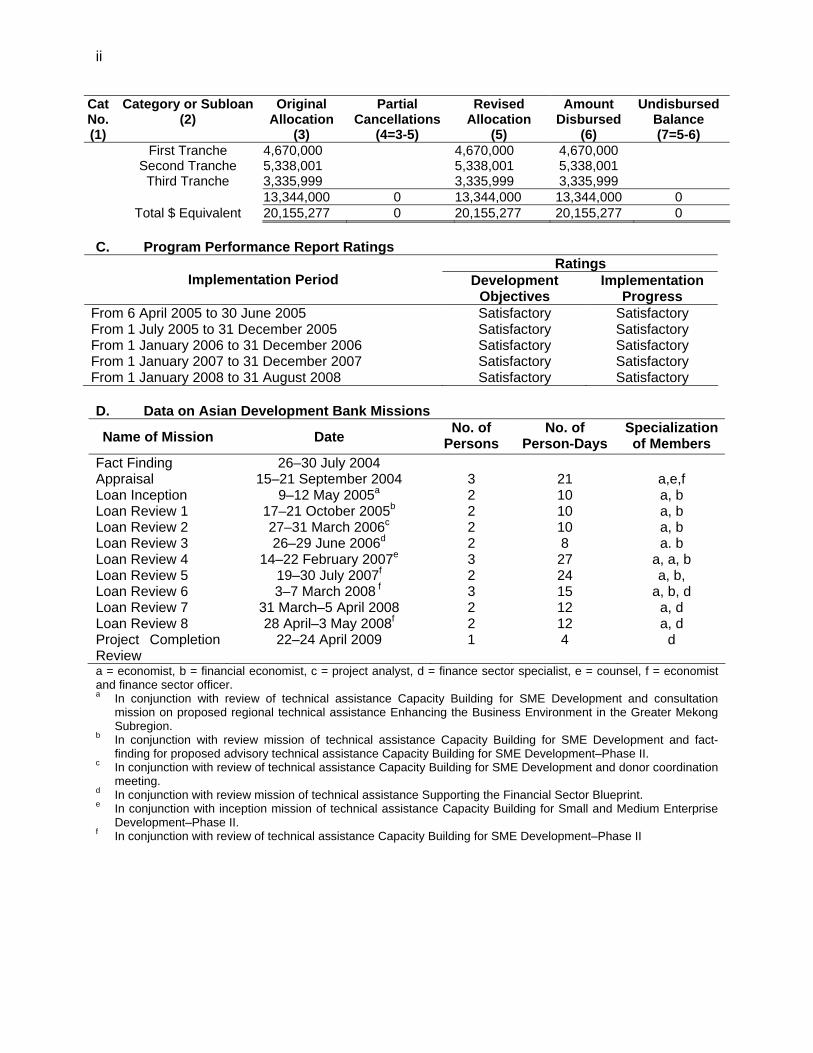

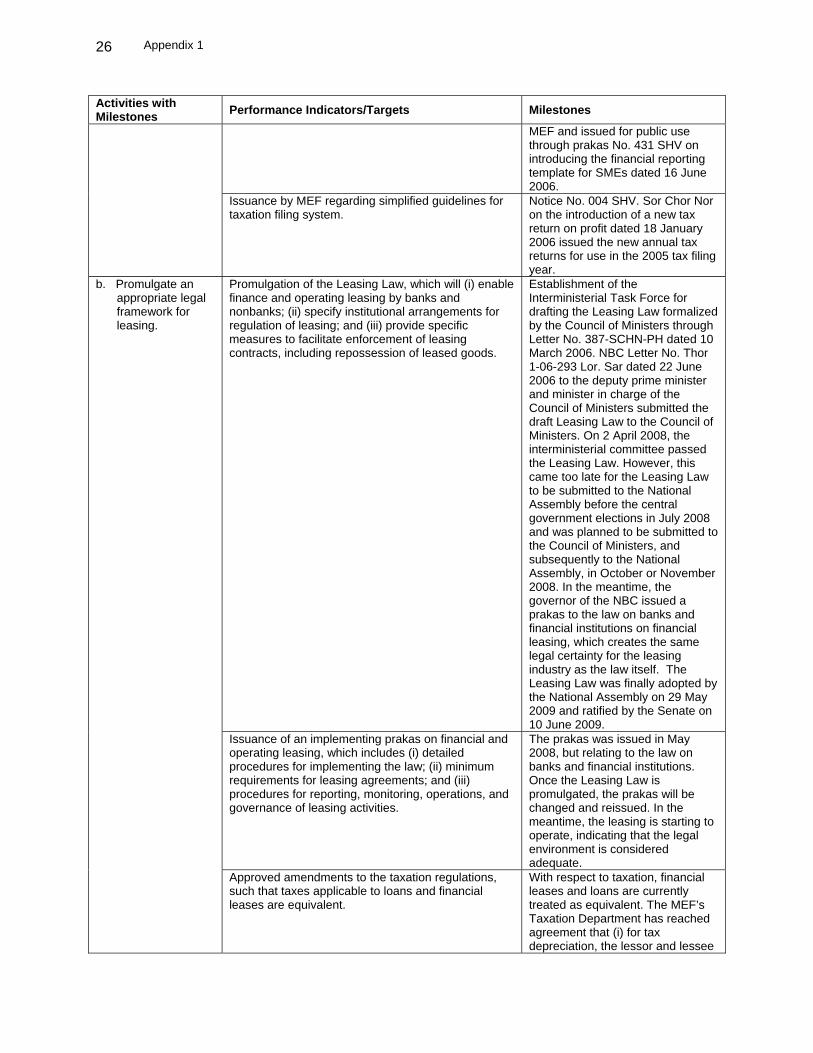

1. Appraisal – Date Started 15 September 2004 – Date Completed 21 September 2004 2. Loan Negotiations – Date Started 4 November 2004 – Date Completed 5 November 2004 3. Date of Board Approval 14 December 2004 4. Date of Loan Agreement 03 February 2005 5. Date of Loan Effectiveness – In Loan Agreement 04 May 2005 – Actual 06 April 2005 – Number of Extensions 0 6. Closing Date – In Loan Agreement 31 December 2007 – Actual 31 August 2008 – Number of Extensions 3 7. Terms of Loan – Interest Rate (grace period) 0 – Maturity (number of years) 24 – Grace Period (number of years) 8 8. Disbursements

a. Dates

Initial Disbursement Final Disbursement Time Interval 30 June 2005 28 August 2008 38 months Effective Date Original Closing

Date Time Interval

06 April 2005 31 December 2007 33 months b. Amount ($) SDR13,344,000

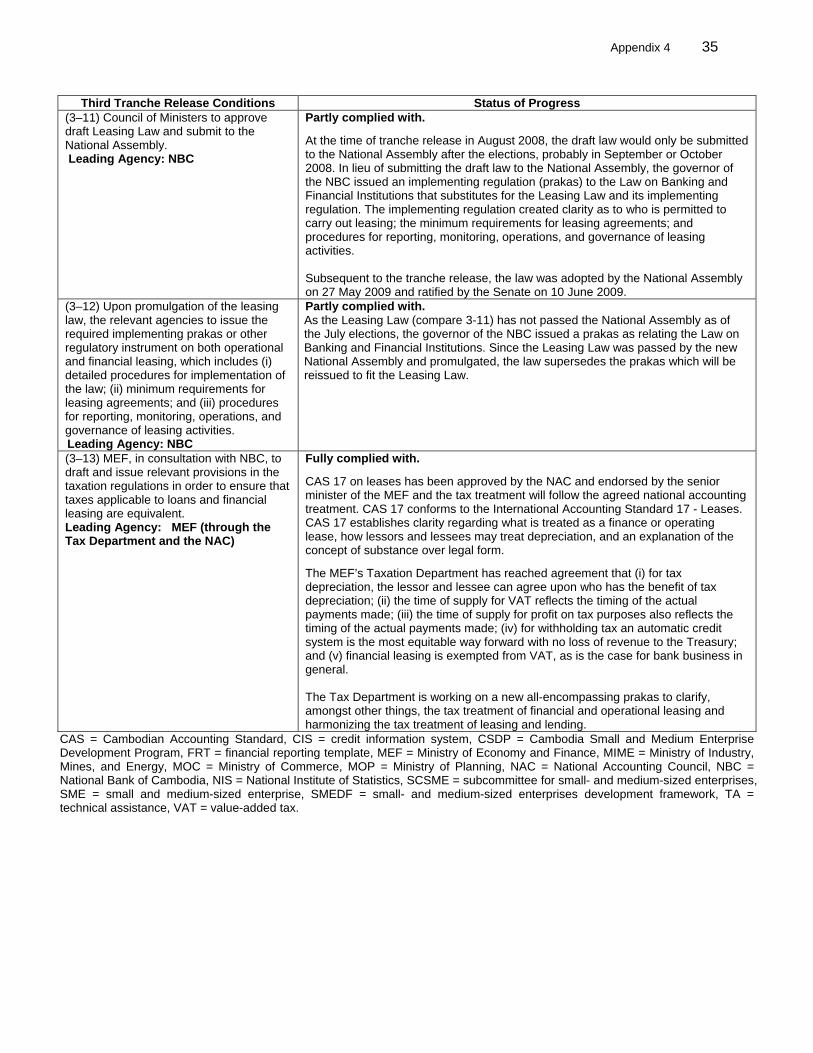

(loan currency) $20,155,277 ($ equivalent)

ii

Cat No. (1)

Category or Subloan (2)

Original Allocation

(3)

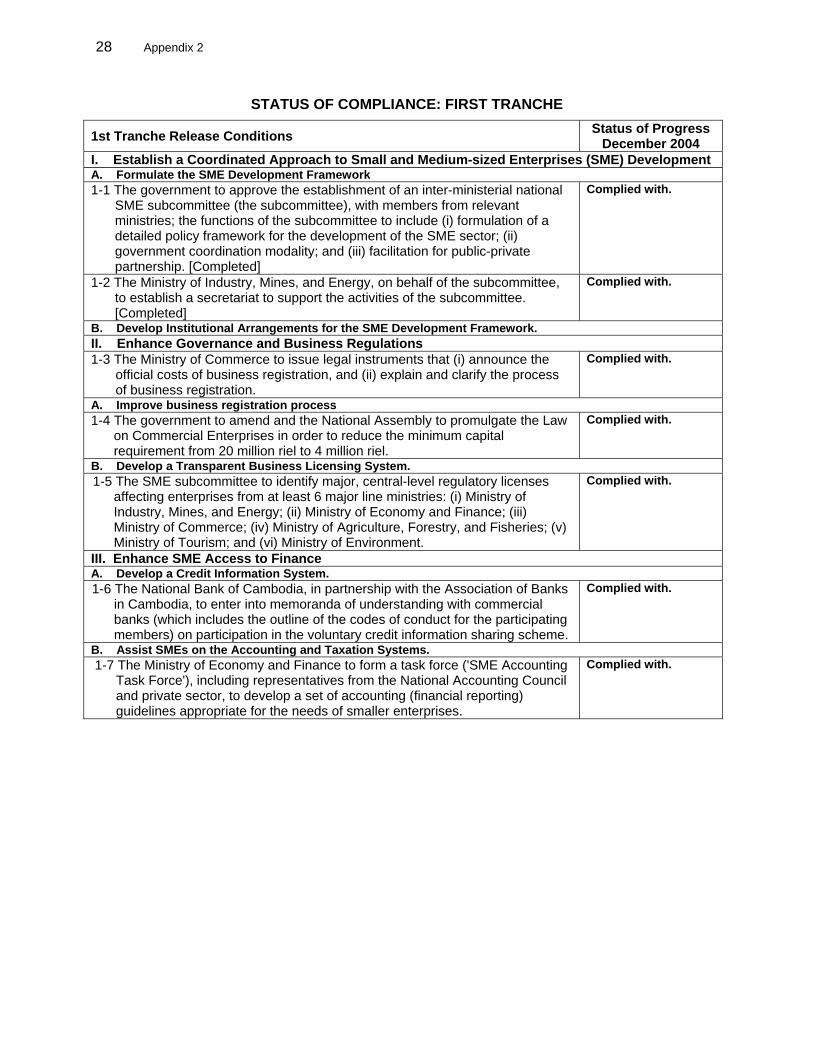

Partial Cancellations

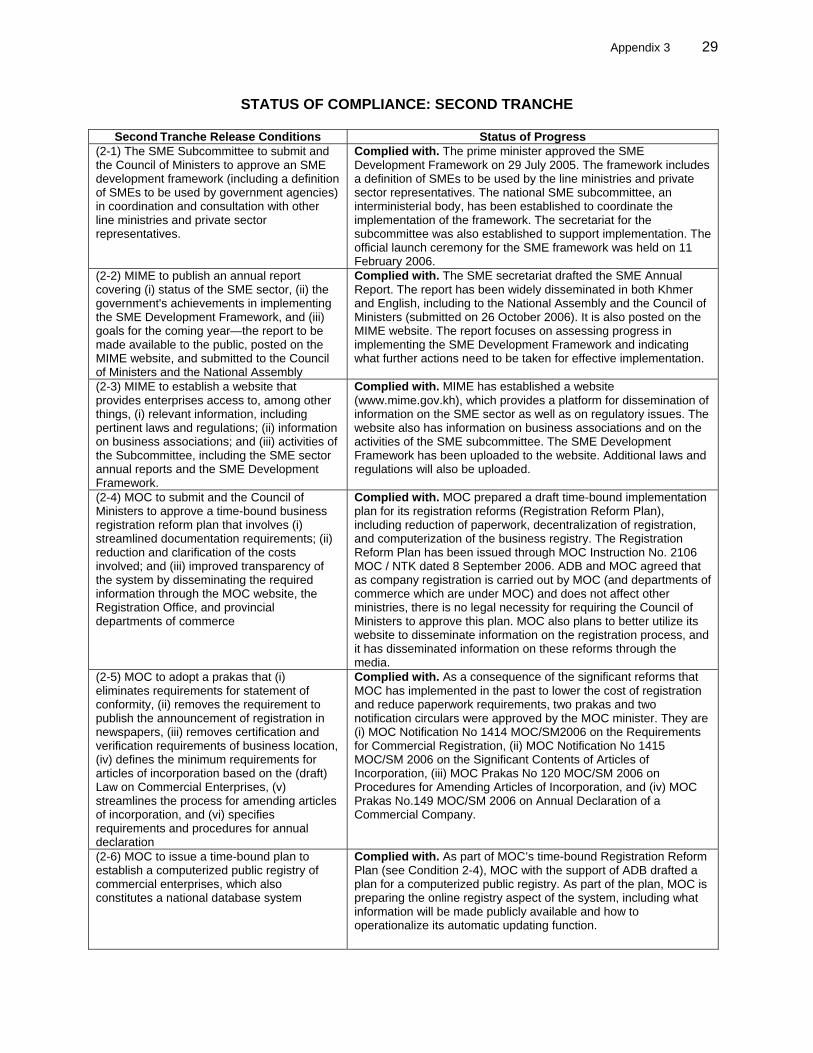

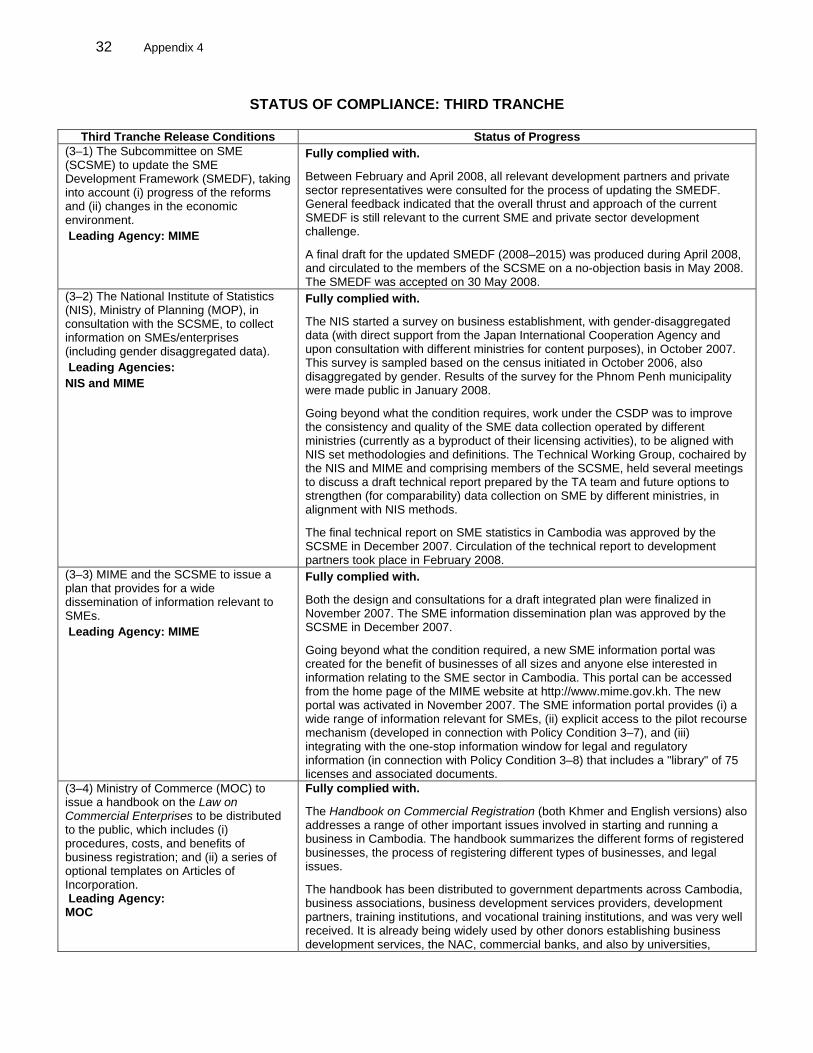

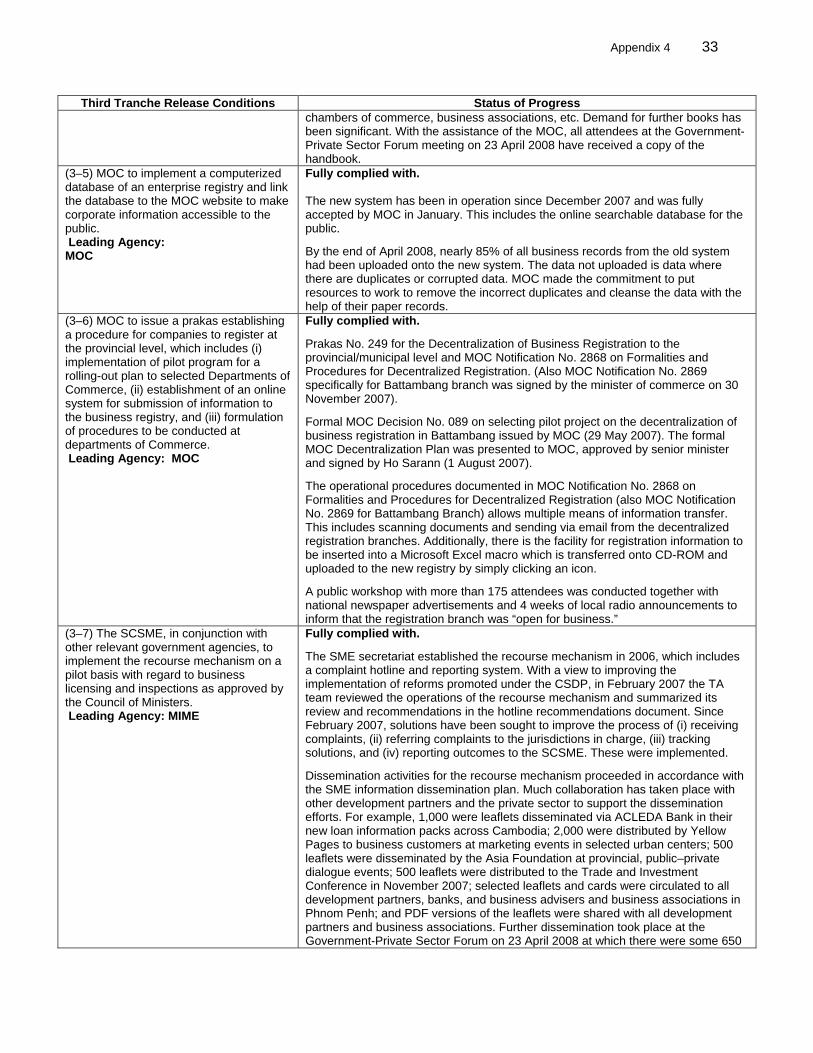

(4=3-5)

Revised Allocation

(5)

Amount Disbursed

(6)

Undisbursed Balance (7=5-6)

First Tranche 4,670,000 4,670,000 4,670,000 Second Tranche 5,338,001 5,338,001 5,338,001 Third Tranche 3,335,999 3,335,999 3,335,999 13,344,000 0 13,344,000 13,344,000 0 Total $ Equivalent 20,155,277 0 20,155,277 20,155,277 0

C. Program Performance Report Ratings

Ratings Implementation Period Development

Objectives Implementation

Progress From 6 April 2005 to 30 June 2005 Satisfactory Satisfactory From 1 July 2005 to 31 December 2005 Satisfactory Satisfactory From 1 January 2006 to 31 December 2006 Satisfactory Satisfactory From 1 January 2007 to 31 December 2007 Satisfactory Satisfactory From 1 January 2008 to 31 August 2008 Satisfactory Satisfactory D. Data on Asian Development Bank Missions

Name of Mission Date No. of Persons

No. of Person-Days

Specialization of Members

Fact Finding 26–30 July 2004 Appraisal 15–21 September 2004 3 21 a,e,f Loan Inception 9–12 May 2005a 2 10 a, b Loan Review 1 17–21 October 2005b 2 10 a, b Loan Review 2 27–31 March 2006c 2 10 a, b Loan Review 3 26–29 June 2006d 2 8 a. b Loan Review 4 14–22 February 2007e 3 27 a, a, b Loan Review 5 19–30 July 2007f 2 24 a, b, Loan Review 6 3–7 March 2008 f 3 15 a, b, d Loan Review 7 31 March–5 April 2008 2 12 a, d Loan Review 8 28 April–3 May 2008f 2 12 a, d Project Completion Review

22–24 April 2009 1 4 d

a = economist, b = financial economist, c = project analyst, d = finance sector specialist, e = counsel, f = economist and finance sector officer. a In conjunction with review of technical assistance Capacity Building for SME Development and consultation

mission on proposed regional technical assistance Enhancing the Business Environment in the Greater Mekong Subregion.

b In conjunction with review mission of technical assistance Capacity Building for SME Development and fact-finding for proposed advisory technical assistance Capacity Building for SME Development–Phase II.

c In conjunction with review of technical assistance Capacity Building for SME Development and donor coordination meeting.

d In conjunction with review mission of technical assistance Supporting the Financial Sector Blueprint. e In conjunction with inception mission of technical assistance Capacity Building for Small and Medium Enterprise

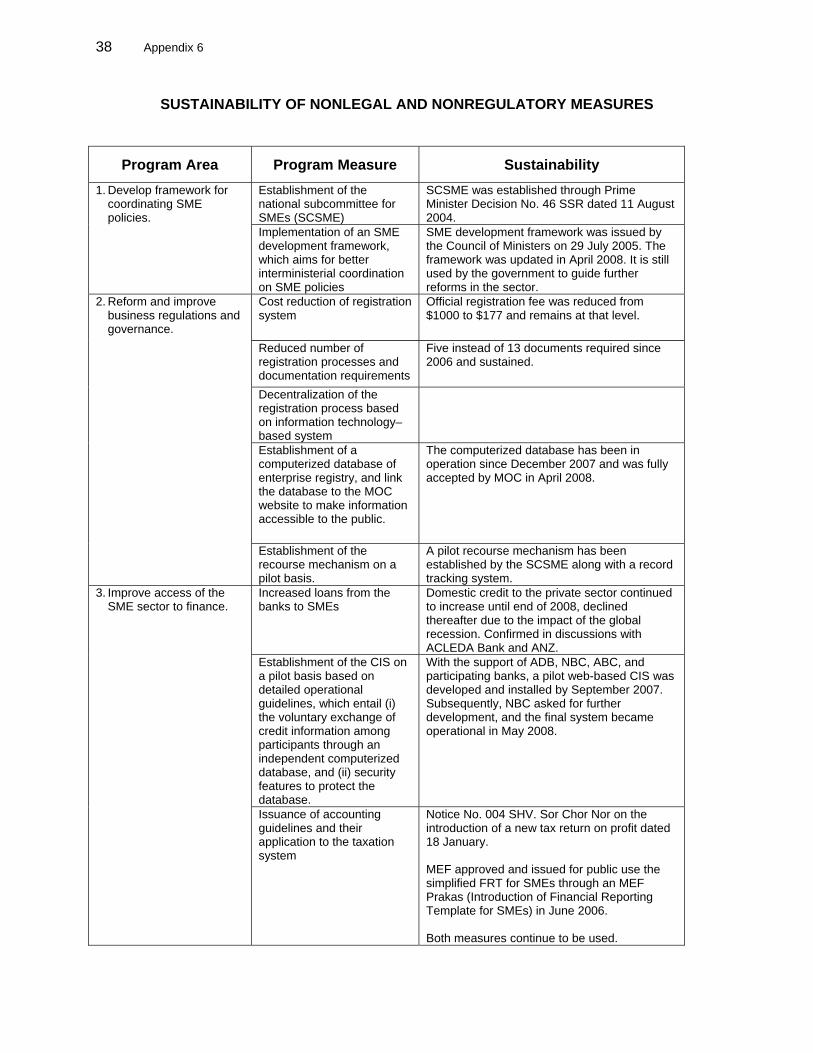

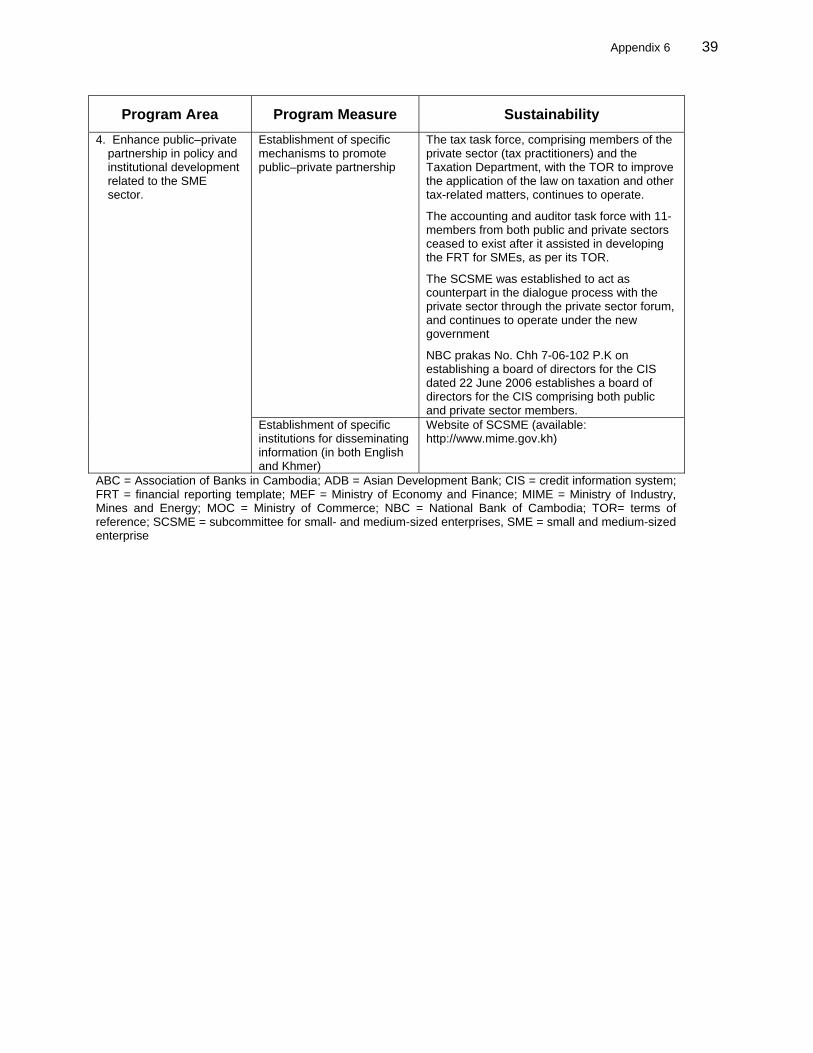

Development–Phase II. f In conjunction with review of technical assistance Capacity Building for SME Development–Phase II

I. PROGRAM DESCRIPTION 1. The Cambodian Small and Medium Enterprise Development Program (CSDP) loan1 of $20 million from the Asian Development Bank's (ADB’s) Special Fund (equivalent to SDR13.34 million) was approved by ADB on 14 December 2004. The loan comprised three tranches to be disbursed as follows: (i) $7 million upon fulfillment of specified first tranche release conditions upon loan effectiveness, (ii) $8 million subject to fulfillment of specified second tranche release conditions approximately 18 months after loan effectiveness, and (iii) $5 million subject to fulfillment of specified third tranche release conditions within 36 months after loan effectiveness. The loan agreement for the CSDP was signed on 3 February 2005 and became effective on 6 April 2005. 2. Economic activity in Cambodia has been dominated by small and medium-sized enterprises (SMEs), which were seen as playing a major role in economic growth and poverty reduction. Through extensive consultation with the government and other stakeholders, the CSDP became the first ADB policy loan to Cambodia designed to lay the foundation for SME development and foster an enabling business environment. Significant legal, institutional, and governance reforms were needed for further effective SME development. First, the costs of doing business were high due to limitations of the regulatory and governance structures. Second, the missing legal structures and institutions led to a high-risk lending environment, which had limited SME access to key resources, particularly finance. Finally, the government lacked an institutional and coordinated framework to facilitate SME development and, in many instances, also lacked the capacity to address SME issues. These factors formed the sector's main barriers to development, reflected by limited growth, informality, and underemployment. 3. The CSDP’s expected outcome was to lay the foundation for the development of a business environment that is conducive to business, especially for SMEs (refer to Appendix 1 for the updated design and monitoring framework). The program was to achieve this outcome through outputs in the following three areas:

(i) Establish an SME development framework: (a) provide a long-term strategic framework for SME development, (b) design an institutional framework to seek better policy coordination and implementation among key government agencies, and (c) promote public–private partnerships and strengthen institutions to effectively implement the development framework.

(ii) Improve governance and regulatory reform related to SMEs: (a) improve the business registration process by enhancing its transparency and reducing costs by eliminating unnecessary requirements, and facilitating decentralization of registration processes; and (b) reform the current business licensing system by reviewing and removing unnecessary licenses and requirements, streamlining the procedures and responsibilities of institutions involved, and establishing a one-stop information window to provide guidelines and information on government regulations for SMEs.

(iii) Enhance SMEs’ access to finance: (a) create simplified accounting sets that are better suited to SMEs' needs and capabilities, (b) develop a leasing framework as a potential alternative financing source for SMEs, and (c) establish a credit information system for the banking subsector.

1 ADB. 2004. Report and Recommendation of the President to the Board of Directors on a Proposed Loan and

Technical Assistance Grant to the Kingdom of Cambodia for the Small and Medium Enterprise Development Program. Manila (Loan 2129-CAM).

2

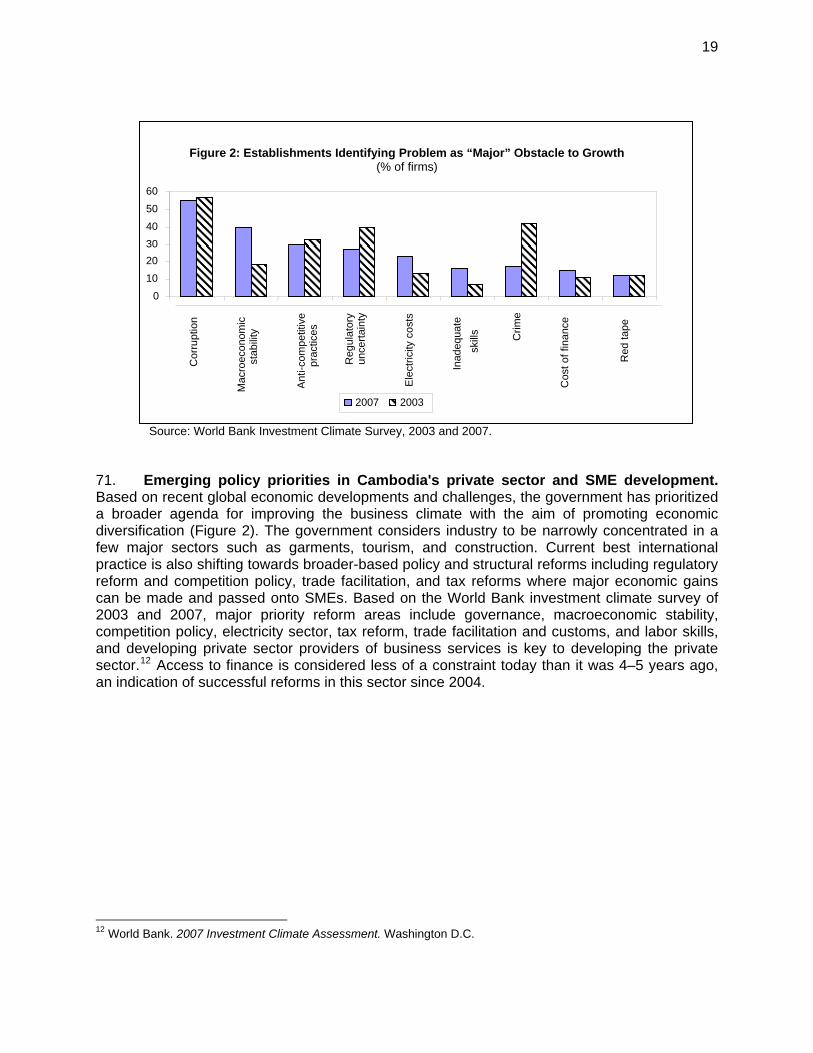

4. The CSDP comprised policy actions in the above three areas supported by the $20 million loan, which was disbursed in three tranches. The first tranche ($6.8 million) was released on 30 June 2005, when the loan took effect and after the seven conditions for its release were met (Appendix 2). The second tranche ($8.1 million) was released on 6 December 2006 after full compliance with all 12 conditions (Appendix 3), and the third tranche ($5.3 million) was released on 28 August 2008, with 11 out of 13 conditions fully complied with and two conditions partly complied with (Appendix 4). These two conditions were subsequently fully complied with. The program met its development objectives. With the help of the improvements it made in the regulatory framework and the political focus on SMEs it created, the operating environment for SMEs has improved significantly.

II. EVALUATION OF DESIGN AND IMPLEMENTATION A. Relevance of Design and Formulation 5. In the context of a falling (but still high) incidence of overall poverty, and a growing rural–urban divide, the government prepared its last two 5-year planning documents, the National Strategic Development Plan 2001–2005 and the National Strategic Development Plan 2006–2010. They aimed to achieve the interim (2010) targets of the Cambodia Millennium Development Goals and adopted the Rectangular Strategy in July 2004 focusing on the private sector (Appendix 5). At the core of the strategy is good governance, which is expected to facilitate growth and poverty reduction over the medium term, underpinned by the four pillars of (i) private sector development, particularly in SMEs; (ii) growth in the productivity and profitability of agriculture; (iii) improvements in physical infrastructure; and (iv) enhancement of human capacity. 6. As reflected in the Rectangular Strategy and the national strategic development plans, SME development represents an important pillar of Cambodia’s development. ADB’s country strategy and program for Cambodia 2005–2009, 2 which was approved in February 2005, emphasized (i) broad-based economic growth through investments in physical infrastructure, development of the finance sector, sustainable development of SMEs, and investments in agriculture and irrigation; (ii) inclusive social development through education, provision of rural water supply and sanitation facilities, and community-based sustainable management and conservation of natural resources in the Tonle Sap basin; (iii) good governance; and (iv) a geographic (Tonle Sap basin) and subregional (Greater Mekong Subregion) focus to support one of the poorest and most environmentally sensitive regions of Cambodia, and to benefit from the broader opportunities provided by ADB’s Greater Mekong Subregion program. 7. Specific to SME sector development, the country strategy and program 2005–2009 stated that ADB would help create an enabling environment by (i) establishing a development framework and appropriate institutional structures so that policy towards SMEs is effectively coordinated and implemented across various ministries; (ii) enhancing governance and business regulations by improving company registration processes and developing a transparent business licensing system; (iii) improving SME access to finance by developing a credit information system, assisting enterprises in accounting and taxation systems, and developing a legal framework for leasing; and (iv) assisting the development of business

2 ADB. 2005. Country Strategy and Program: Cambodia, 2005–2009. Manila.

3

services and public–private partnerships. This strategy was fully integrated with the government's Rectangular Strategy. B. Program Outputs 8. Outputs under the program can be grouped into three broad areas: (i) establishment of a coordinated approach to SME development, (ii) enhanced governance and business regulation, and (iii) enhanced SME access to finance.

1. Establishment of a Coordinated Approach to Small and Medium-Sized Enterprise Development

9. Building on the government’s Rectangular Strategy for growth, employment, equity, and efficiency, the CSDP included the establishment of an effective interministerial coordination body, the subcommittee for small and medium-sized enterprises (SCSME), and the formulation of an SME development framework (SMEDF). 10. To formulate and implement the SMEDF, the SCSME was established through Decision No. 46 SSR in August 2004 as part of the Private Sector Steering Committee. The SCSME consisted of members from nine line ministries and the Chamber of Commerce. The subcommittee’s role was to coordinate and implement government SME policies and donor programs for SMEs. The subcommittee had a permanent secretariat staffed with individuals charged with supporting the activities of the subcommittee. The secretariat facilitated meetings of the subcommittee and supported coordination with the government, aid agencies, and the private sector on SME policies. The secretariat has been carrying out activities outlined in its letter of assignment (No. 126 URTH-LB) of 17 December 2004. The SCSME and its secretariat continue to operate. 11. The SCSME, on behalf of the Government of Cambodia and with the assistance of its secretariat, has been playing a crucial role in implementing the government’s Rectangular Strategy. The implementation process for SMEs is outlined in the SMEDF, which was approved by the Council of Ministers in July 2005. Essentially, it is the road map for the Rectangular Strategy as it pertains to SMEs. Since it was formulated, the SMEDF has been used to align and coordinate government policy efforts with the objectives of development partner assistance. It continues to guide the government’s reform efforts. 12. In the first quarter of 2008, the SCSME produced a status update of the original SMEDF, as the time had come to take stock of what had been achieved against the SME sector road map and to update it to reflect (i) changes that have occurred in the business environment for SMEs, and (ii) developments during the last 4 years from the government’s perspective. 13. This update benefited strongly from efforts of the National Institute of Statistics (NIS) in the Ministry of Planning, which collected comprehensive information on SMEs and has generated gender-disaggregated data. The NIS started a survey on business establishment, with gender-disaggregated data, in October 2005 (with direct support from the Japan International Cooperation Agency and upon consultation with different ministries for content purposes). This survey was sampled based on the census initiated in October 2006, which was also disaggregated by gender. Results of the survey for the Phnom Penh municipality were made public in January 2008. Other results were published on an SME (web) portal site

4

(http://www.mime.gov.kh) which was created by the SCSME to improve dissemination of SME information to stakeholders.3 However, by the end of the program there were signs of SME "coordination fatigue" setting in among government counterparts and development partners and this is a risk to achieving longer-term results (para. 52).

2. Enhanced Governance and Business Regulations a. Improve the Business Registration Process

14. The CSDP included several reforms to enhance public governance and business regulations. First, reform of the business registration system entailed reducing costs as well as procedures and requirements; enhancing transparency; and decentralization. Second, specific measures to improve the current operating and regulatory licensing systems included identifying and removing unnecessary licenses (and licensing requirements), developing criteria for the issuance of any new licenses, and implementing mechanisms for enterprises to state their grievances pertaining to administrative decisions concerning licensing and inspection. 15. The company registration process was improved and made more transparent so as to ease the incorporation of businesses without the need for hiring expensive facilitators. The Ministry of Commerce (MOC) has made significant progress in reforming the registration system by introducing measures to reduce costs, simplify procedures, and make the process more transparent. Official fees were reduced to $177 in August 2004 when the MOC issued prakas4 No. 163 MOC/M 2004, which established clear guidelines on the costs of registering, and further reduced the official fee to $105 in August 2007 upon issuance of the interministerial prakas between the Ministry of Economy and Finance (MEF) and the MOC (ref: 679, 7 August 2007). The estimated total costs of incorporation have dropped from almost $1,000 before the reforms to approximately $500. 16. All of these reforms are reflected in the Handbook on Commercial Registration5 and the Law on Commercial Enterprises, which includes (i) procedures, cost, and benefits of business registration; and (ii) a series of optional templates on articles of incorporation. Furthermore, the MOC has implemented a computerized database of the enterprise registry and linked the database to the MOC website, thereby making corporate information accessible to the public. 17. Overall, since these reforms were implemented, the development impact has been positive. The average number of enterprises registered has risen to an average of 238 per month during 2007, compared with 61 per month in the period between January 2003 and August 2004. Enterprise registrations over the first few months of 2008 averaged 245 per month. However, numbers dropped during the second half of 2008 as a consequence of the impact of the global recession. Figure 1 reflects this development. 3 ADB has (i) provided recommendations to the SCSME for the design and development of the SME portal site; (ii)

included information on laws and regulations, and SME statistics; and (iii) developed a searchable database of all SMEs licensed by the Ministry of Industry, Mines and Energy (MIME). The database provides an opportunity for improved market links for SMEs. ADB has also supported the development of a one-stop information window on the website, which provides detailed information on all licenses affecting SMEs. So far, the regulatory documentation of several licenses has been uploaded to this website and the SCSME is continuing to add to the database. The website also contains information on selected SME business associations.

4 A prakas is a banking or finance regulation issued by a government minister or by the governor of the National Bank of Cambodia (NBC).

5 Ministry of Commerce. 2008. Handbook on Commercial Registration. Phnom Penh.

5

Figure 1: Number of Companies Registering at the Ministry of Commerce

0100200300400500600700800900

1000

Q2, 200

4

Q4, 200

4

Q2, 200

5

Q4, 200

5

Q2, 200

6

Q4, 200

6

Q2, 2

007

Q4, 2

007

Q2, 2

008

Q4, 2

008

Date of

Start of Recession

Source: Ministry of Commerce, Department of Business Registration.

18. In the longer term, the government's registration reform plan aims to decentralize business registration. In line with this plan, ADB supported a pilot project in the province of Battambang which took only 4 months to implement and was successfully completed at the end of November 2007. Battambang now has an operational commercial registration branch. 19. The statistics for business registrations at the Battambang branch are shown in Table 1.

Table 1: Battambang Business Registration, since 17 September 2007 Type of Enterprise Number Registered

at 31 March 2008 Number Registered

at 31 March 2009 Company 20 56 Sole proprietorship 5 15 Branch of a Cambodian company 5 24 Amendments to business details 6 15 Source: Ministry of Commerce

b. Develop a Transparent Business Licensing System

20. The main objective in business licensing reform under the CSDP was to reduce the costs of doing business in Cambodia, specifically the regulatory compliance costs. The CSDP attempted to streamline current licensing by eliminating duplicative licenses and/or their requirements. Furthermore, enterprises were to be given the right to ask for clarification on the process of licensing and inspections. 21. Accordingly, with ADB support, on 27 October 2006 the Council of Ministers approved a comprehensive licensing reform plan.6 The plan was divided into two phases. In the first phase, existing licenses affecting SMEs were reviewed by the SME secretariat and recommendations for reform were presented to the SME subcommittee. The focus of the second phase was to build administrative capacity in the government and provide immediate results of the measures under phase one, to demonstrate the benefits of establishing the licensing review mechanism.

6 Ministry of Commerce. 2006. Plan for Establishing Licensing Review Mechanism. Phnom Penh.

6

In addition, the SCSME has established a means of recourse for enterprises to file grievances regarding disputes resulting from licensing and inspection and to have decisions reviewed. This mechanism involves a hotline for reporting grievances to the government, and has been documented. The pilot business licensing hotline is in operation and is managed by the SCSME secretariat. While the licensing reform measures were complied with, outcomes are mixed and this reflects insufficient attention to the institutional set up necessary to institutionalize a licensing reform program in government (para 66[v]).

c. Commercial Legal Framework 22. The SCSME worked with the Ministry of Justice and appropriate government authorities to (i) remove inconsistencies between laws that comprise the commercial legal framework, (ii) improve the laws where necessary, and (iii) enact the laws with implementing regulations. 23. Enactment of the draft laws required to establish the commercial legal framework, which was also necessary to meet the requirements under World Trade Organization (WTO) accession, was pursued with great success during both phases of the CSDP. The SCSME worked with the MOC to ensure that the major commercial laws were enacted and prepared necessary implementing regulations that are consistent with the provisions of the laws. The SCSME assisted the government in developing a mechanism to determine inconsistencies and conflicts within the various draft laws, especially with the civil code and code of civil procedures. Once these were determined, harmonization was achieved through necessary changes to the relevant draft laws. The government only adopted the civil code and code of civil procedures after all efforts were made to avoid conflicts with other commercial laws. With the Law on Commercial Enterprises (promulgated in June 2005), the government provided a clear legal framework for the operations of sole proprietorships, branches, companies, and partnerships.

3. Enhance Small and Medium-Sized Enterprise Access to Finance

24. Before the start of this program, several factors had been identified as obstacles to SME access to finance. These included (i) insufficient legal security for the use of collateral in secured transactions and an underdeveloped land titling7 system (focus of phase I for second tranche release), (ii) limited availability of credit information on prospective borrowers, and (iii) the weak financial reporting capacity of SMEs. An additional concern was the lack of an adequate legal and regulatory framework to enable leasing as a new financial product to address the medium- and long-term financing needs of enterprises.

a. Secured Transactions and Land Titling 25. The law on secured transactions was enacted during phase I (May 2007) and the Secured Transactions Filing Office online filing registry was officially launched in September 2007, at the start of phase II. These were major advances in Cambodia that reduce the involvement of civil servants in the registration and collection of fees, enhance the priority claims on securities, and provide public access to information on secured chattels and their owners. 7 Another issue relevant to collateral is insurance. Normally banks will require the borrower or lessee to insure assets

which are subject to collateral interests or are being leased. The issue of insurance is not covered under this program as the Financial Sector Blueprint has a number of actions dealing with the insurance sector for 2006–2015.

7

26. The enactment of this law was a requirement of the Financial Sector Blueprint and was implemented under the first Financial Sector Program Cluster for Cambodia,8 and is a condition for WTO accession. This law considerably improves the position of creditors wishing to secure obligations with real rights in secured local collateral. Further, the creation of the secured transactions legal framework allows a creditor to take security interest over a debtor’s movable property, which is hugely beneficial to SMEs that do not own land and buildings but require access to readily available, cheap, long-term credit and, equally importantly, leasing finance. The MOC has included the Secured Transactions Law in its ongoing public dissemination program. 27. With the assistance of the World Bank and the governments of Finland and Germany, the government has introduced systematic land registration which is an important contribution towards (i) strengthening land title security, (ii) improving the land market, (iii) increasing national revenue, and (iv) reducing land conflicts. The geographical coverage of systematic land registration has expanded from 11 to 15 provinces and municipalities. The legal framework for land registration was established through the subdecree on systematic land registration and subdecree on sporadic land registration in 2003. The Land Administration Subsector Program has worked out additional legal papers to these subdecrees. Land transactions are also legally secured through land registration. A modern, computerized land registration system has been put in place, and this has shown excellent performance. More than 1 million land titles have been surveyed and adjudicated upon, with more than 800,000 titles distributed to the owners during the program. This was essential for improving the use of land as collateral.

b. Credit Information System

28. A credit information system (CIS) was identified as an important area of reform in the CSDP. With the support of ADB, the National Bank of Cambodia (NBC), the Association of Banks in Cambodia (ABC), and participating banks, a pilot web-based CIS database has been developed. This CIS helps reduce risks (asymmetric information) and transaction costs of lending by providing credit information on borrowers. A report was produced by the NBC in partnership with the ABC which (i) reviewed the pilot CIS, (ii) examined options to expand the system, (iii) assessed the feasibility of establishing a private credit bureau, and (iv) made recommendations for the necessary legal framework. To enable the pilot CIS, an accompanying legal framework was implemented to allow banks to share information and to protect the rights of both lenders and borrowers. The NBC took the lead in developing the necessary legal framework to enable and implement the CIS.

8 ADB. 2005. Report and Recommendation of the President to the Board of Directors on a Proposed Loan and

Technical Assistance Grant to the Kingdom of Cambodia for Subprogram III of the Financial Sector Program. Manila (Loan 2185-CAM).

8

29. A code of conduct regarding the operational rules and obligations of the member banks of the CIS was also signed by the 18 banks in July 2006. The objective of the code of conduct is to set out the rules for the pilot project in which the NBC and the CIS member banks collect, disseminate, manage, and utilize credit information, thereby preventing the misuse and abuse of credit information. The code of conduct is meant to ensure that the CIS operations are transparent and maintain accuracy, security, and confidentiality of the credit information maintained in the system.

c. Assist Small and Medium-Sized Enterprises in the Accounting and Taxation Systems

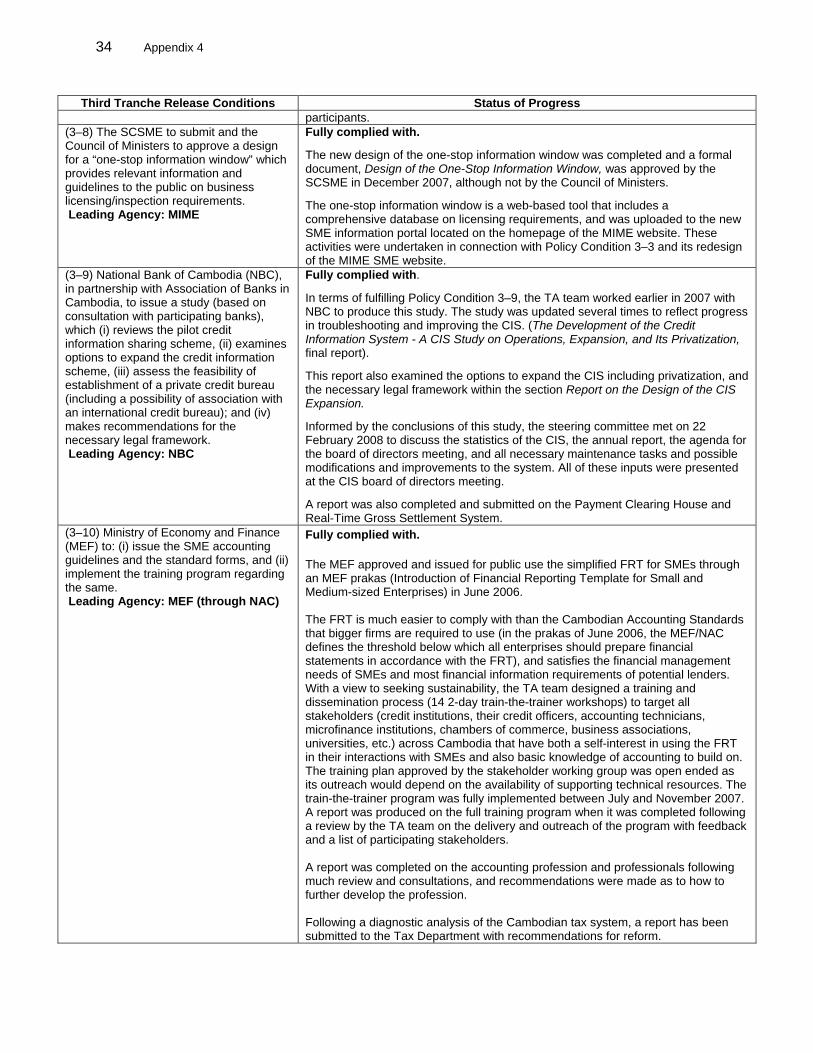

30. During fact finding, the mission found that the quality and availability of financial information on SME borrowers in Cambodia ranged from minimally acceptable to wholly nonexistent. One reason for this lack of financial information is that SMEs generally are unable to prepare financial statements and provide information relevant to the needs of the lenders. The SMEs were largely unaware of the need for, and benefit of, preparing financial statements. The SMEs’ willingness to invest in maintaining basic accounting systems is hampered by technical difficulties and the high cost of outsourcing such tasks (as the accounting profession is still in the developing stage). Therefore, specific financial reporting and tax-filing reforms are needed to increase the benefits that accurate financial reporting can bring to the enterprise in terms of financial management and the ability to borrow. Increasing general awareness and disseminating simple financial reporting guidelines were seen as crucial steps. 31. The MEF approved and issued for public use the financial reporting template (FRT) for SMEs through an MEF prakas on 16 June 2006. The FRT is a simplified financial statement that is easier to prepare than financial statements that comply with the complicated Cambodian Accounting Standards (CASs), which do not offer a practical approach for smaller enterprises. The FRT also satisfies the financial management needs of SMEs and provides the financial information required by lenders and investors. In addition, a training program was also submitted to the MEF by the National Accounting Council and SME Accounting Task Force in July 2006, and it was carried out over the second half of 2007. The training program disseminated the FRT and provided training to microfinance institutions, banks, and business associations in order to give these professionals the ability to build capacity among their SME clients on the use of the FRT. Some 251 trainers were trained in 14 2-day training workshops. 32. Going beyond the demands of the CSDP, the Cambodian Taxation Department went through a process of reform and restructuring, with the objective of improving taxpayer services, which should result in increased compliance and therefore improved revenue collection. The Taxation Department developed a new annual tax on profit return, which was implemented for the year ended 31 December 2005, together with guidelines on the completion of the tax return form, which were issued for the first time, with a view to assisting taxpayers complete the annual tax return. The MEF issued Notification Letter No. 004-MEF-NT on 18 January 2006 advising of the implementation of the new annual tax return. The Taxation Department also recently revised the monthly tax returns which reduces duplication of information and should simplify the completion of monthly tax compliance procedures. 33. To date, two Cambodian financial reporting standards and 18 CASs have been issued after endorsement by the senior minister. The MEF, through the National Accounting Council, issued CAS 17 that sets out best accounting practices for finance and operating leasing, and required compliance with its provisions by lessors and lessees. CAS 17 mirrors the International Accounting Standard 17.

9

34. Because of CAS 17, the Taxation Department was able to implement a tax treatment for finance leases that puts it on an equal footing with corporate lending. This was achieved through consultation with the private sector and consideration of the benefits of finance leasing to the development of the economy of Cambodia. The Taxation Department has reached agreement that (i) for tax depreciation, the lessor and lessee can agree upon who has the benefit of tax depreciation; (ii) the time of supply for value-added tax (VAT) reflects the timing of the actual payments made; (iii) the time of supply for profit on tax purposes also reflects the timing of the actual payments made; (iv) for withholding tax, an automatic credit system is the most equitable with no loss of revenue to the Treasury; and (v) financial leasing is exempted from VAT, as is the case for bank business in general.

d. Develop a Legal Framework for Leasing

35. At the time of third tranche release, the Leasing Law had not yet passed Parliament and the implementing regulation had not been issued, due to the looming election. In lieu of the law, the Governor of the NBC issued an implementing regulation (prakas) to the Law on Banking and Financial Institutions that substitutes for the the Leasing Law and its implementing regulation. This prakas established the same legal certainty for the leasing industry as if the Leasing Law had been promulgated. On this base, the following conditions were waived: (i) the approval of the draft Leasing Law and its submission to the National Assembly and (ii) the issuance of the required implementing prakas upon promulgation of the Leasing Law. The law was finally adopted by the National Assembly on 29 May 2009 and ratified by the senate on 10 June 2009. The law supersedes the prakas, which will be reissued to fit the Leasing Law. C. Program Costs and Disbursements 36. The program was funded by a $20 million (SDR13.34 million) loan from ADB's Special Fund. Two technical assistance (TA) grants supported the program. The first TA grant of $1 million was financed by ADB's Technical Assistance Special Fund (TASF) ($500,000), Danish International Development Assistance (Danida) (350,000), and the government ($150,000). The second TA grant of $950,000 was funded by the TASF ($800,000) and the government ($150,000). Disbursements of the loan followed the simplified procedures and related requirements for a program loan. The loan proceeds were released in three tranches. The first tranche of $6,834,826.11 (equivalent to SDR4.67 million) was released on 30 June 2005; the second tranche of $8,064,917.30 (equivalent to SDR5.39 million) was released on 6 December 2006); the third tranche of $5,255,533.45 (equivalent to SDR3.37 million) was released on 28 August 2008. The release of the first tranche did not require Board approval; Board approval for the release of the second tranche was given on 4 December 2006, and Board approval for the third tranche was given on 8 August 2008. D. Program Schedule 37. The implementation period of the program was planned for 36 months from effectiveness of the loan. The original closing date was 31 December 2007. The planned tranche releases were as follows: first tranche release upon loan effectiveness, second tranche release 18 months after loan effectiveness, and third tranche release 36 months after loan effectiveness. The implementation required three extensions of loan closing, i.e., 30 June 2008, 31 July 2008, and 31 September 2008. There was a 6-month delay of loan effectiveness due to problems in the Cambodian administration. Therefore, the original closing date of 31 December 2008 had to be extended to 30 June 2009. A further extension of 2 months to 31 August 2008

10

became necessary, mainly due to delays in passing the Leasing Law in the National Assembly, and also because of the national elections held in July 2008 which resulted in the delay of the submission of the requirements for release of the third tranche. The program was financially closed on 31 August 2008. E. Implementation Arrangements 38. The Ministry of Industry, Mines and Energy (MIME) was the executing agency of the program with the MOC, Ministry of Planning, MEF, NBC, and MIME itself as the implementing agencies. The SCSME secretariat managed the production of reports, and website creation and updating. To coordinate program implementation activities among the different implementing agencies, a program steering committee (PSC) was formed, chaired by the minister of the MIME. It was composed of senior officers from all ministries and government agencies concerned, i.e., MOC, MEF, Ministry of Planning, and the NBC. The PSC met twice yearly to review pending issues on the program and propose concrete actions for the resolution of these issues.

39. The SCSME secretariat served as program implementation unit and was headed by a senior officer of the MIME to help the PSC and ADB implement the program. The unit was staffed by MIME officials with sufficient knowledge and capacity to assist the PSC and ADB, and was responsible for the day-to-day activities related to the program.

40. Capacity building of all agencies involved was supported by two TA grants with the services of international and domestic consultants (paras 43-46). F. Conditions and Covenants 41. Seven specific first tranche release conditions were included in the program and have been successfully complied with.

(i) Establishment of an interministerial national subcommittee. The Government

of Cambodia issued Decision No. 46 SSR for the establishment of the National Subcommittee on 11 August 2004.

(ii) The MIME’s establishment of a secretariat to support the activities of the subcommittee. The MIME issued Assignment Letter no. 126 URTH-LB on 14 December 2004 for the establishment of the secretariat.

(iii) The MOC’s issuance of legal instruments, which would announce the official business registration costs and explain and clarify the procedure of registration. The MOC issued Prakas No. 163 MOC/M 2004 on 23 August 2004 on the determination of the cost of company registration.

(iv) Amendment and promulgation of the Law of Commercial Enterprises reducing the minimum capital requirements from KR20 million to KR5 million. The government amended Article 127 of the draft law to reflect the change in the minimum capital requirement.

(v) National SME subcommittee’s identification of central regulatory licenses. The national subcommittee documented 70 licenses from 10 ministries.

(vi) The MEF’s formation of a task force to develop a set of accounting guidelines appropriate to SMEs' needs. The MEF issued Prakas No. 236 SHV/BR on the establishment of an accounting and auditor task force on 10 August 2004.

(vii) The NBC, in partnership with the ABC, to enter into a memorandum of understanding with other commercial banks on the voluntary credit information

11

sharing scheme. The NBC has entered into memorandums of understanding with 11 banks for the automated credit information sharing.

42. Conditions for the releases of each tranche and the status of compliance are given in Appendixes 2–4. The first tranche had seven conditions and the second tranche had 12 conditions; all 19 conditions were fully complied with. Of the 13 conditions for the third tranche, 11 were fully complied with and two were partially complied with and were waived for tranche release. However, the project completion review mission was able to confirm that all third-tranche conditions are now fully complied with. G. Related Technical Assistance 43. Two associated TA grants on capacity building of SMEs complemented implementation of the CSDP: an attached TA grant9 that provided support for the compliance of covenants related to first and second tranche releases, and a stand-alone TA grant,10 approved in 2006, that supported compliance of covenants for the final tranche release. The TA grants supported the implementation of various policy and institutional reform measures related to the CSDP. Accordingly, the main activities of the TA involved (i) providing technical inputs to support the government's policy reform efforts, (ii) building the capacity of government officials through training and discussions, and (iii) building consensus and disseminating information activities through a series of workshops and other related events. 44. Processed as attached TA to the Small and Medium Enterprise Development Program, the Technical Assistance to Cambodia for Small and Medium Enterprise Development, which focused on capacity building for SME development, was meant to assist capacity building for policy formulation and implementation. The TA was cofinanced by ADB ($500,000) and the Government of Denmark ($350,000), and was completed on 31 May 2006 and financially closed on 30 June 2007. The TA completion report, which was circulated on 10 December 2007, rated the TA highly successful. 45. The Technical Assistance to Cambodia for SME Development Phase II, approved as stand-alone TA on 10 May 2006, assisted the program in the completion of the policy actions related to the release of third and final tranche. The major objective of the TA was to assist the government in creating a regulatory environment conducive to SME development. The TA was financed from the TASF for $800,000, and was completed and financially closed in February 2009. Circulation of the TA completion report has been programmed the first half of 2010.

H. Consultant Recruitment and Procurement 46. The two associated TA projects engaged a combined total of 29 individual consultants—13 under the attached TA project and 16 under the stand-alone project. It was planned that individual consultants would be engaged due to the diverse skill requirements of the TA. No problems were encountered in consultant recruitment and procurement, except under the stand-alone project where there was difficulty looking for a replacement for the international accounting and taxation expert who resigned from the TA before completion of all tasks. It was

9 ADB. 2004. Technical Assistance to Cambodia for Small and Medium Enterprise Development. Manila (TA4476-

CAM for $850,000 from the TASF [$$500,000] and Danida [$350,000], attached to Loan 2129-CAM). 10 ADB. 2006. Technical Assistance to Cambodia for SME Development Phase II. Manila (TA4786-CAM for $800,000

from the TASF).

12

difficult to identify an expert who could perform both the accounting and taxation-related tasks of the original terms of reference. Hence, the terms of reference were divided into two separate assignments through a minor change in implementation arrangements. The two replacement consultants commenced services 3 months after the resignation of the previous expert. I. Performance of Consultants 47. The TA completion report for the Technical Assistance to Cambodia for Small and Medium Enterprise Development rated the consultants either excellent or satisfactory, indicating the overall efficiency and effectiveness of the TA. The 16 consultants under the Technical Assistance to Cambodia for SME Development Phase II were rated as follows: six were rated excellent, five were rated satisfactory, and five were classified not rated. Based on Project Administration Instructions section 2.05B, a consultant's performance evaluation report (PER) must be completed within 2 months from contract end date, otherwise it will be classified not rated. The PAI was issued later than the consultants' contract termination dates (between May and August 2007). There were no problems encountered in accomplishing the individual PERs, but by the time the final reminders were received by the most recent project officer, the time allocation for accomplishing all PERs had lapsed. J. Performance of the Borrower and the Executing Agency 48. Overall, the performance of the government and its agencies involved in the program is rated highly satisfactory. The government, led by the MOC, has made significant progress in reforming the registration system with significant reduction in the registration costs. The procedures have been simplified and streamlined, eliminating the need for a statement of conformity and local government approvals, including the publication of announcement of registration in the newspapers. The government's commitment to SME development was shown in the issuance of the different regulations and laws to effect reforms of the SME sector, e.g., the passage of a law that reduces the minimum capital requirements. Establishing the website, developing an SME development framework, and issuing the different implementing regulations to perform the supervisory functions of the different agencies are among the major successes in its implementation. 49. The MIME, as the executing agency of the project, has closely coordinated with ADB, the different implementation agencies, and other agencies for the satisfactory compliance of the covenants and the conditions for the release of the tranches. The PSC, chaired by the minister of the MIME, was the first step in the program implementation. The PSC was responsible for developing the framework which serves as the road map on the activities relative to the program implementation. K. Performance of the Asian Development Bank 50. ADB has highly satisfactorily performed its function in the overall implementation of the program. This is evidenced by the successful releases of the three tranches, although with a few months delay in the release of the third tranche for reasons beyond its control.

51. The program loan was closely monitored by the ADB as evidenced by the missions fielded during its implementation. An inception mission mounted 1 month after the loan became effective and seven review missions were fielded from October 2005 to May 2008. The program outputs were realized because of the combined efforts of ADB and the MIME. Very significant in the implementation was the development of the legal framework and reforms in the business

13

regulation providing simplified registration processes at reduced cost and with improved transparency.

III. EVALUATION OF PERFORMANCE A. Relevance 52. The program is assessed relevant given the significance of SMEs for the country's economic growth. Its objective of improving the business environment to improve opportunities for the development of SMEs supported an important pillar of the government’s strategy for economic growth and poverty reduction. The program loan provided the development framework which still gives the government a road map for its SME development. The establishment of an interministerial committee provided the coordination among different government agencies in its regulatory work for all SMEs in the country. The reforms of the legal framework focused on the integration of all SMEs into the formal economy, thereby boosting the government’s revenues through sustainable economic growth. 53. While the program was relevant at the time of approval (based on international good practice) and remained relevant throughout its implementation, there were indications at the end of the program period of some SME "coordination and reform fatigue" setting into the program. This was reflected in less stakeholder attendance at the regular SME coordination meetings and less government input into the update of the SME strategy compared with when it was first formulated. At the same time, the government's priorities were shifting to broader private sector development issues and the particular strategies to promote economic diversification through trade facilitation and backward linkages to agriculture, among others. This shift was motivated by emerging challenges to the Cambodian economy, as reflected in the surge in food prices in early 2008 and slowing growth in the garment sector, which accounts for about 75% of the country's exports. Furthermore, recent investment climate surveys also highlight changing priorities among investors (para 71).

54. The program made a contribution to the development of the banking industry. The sharing of credit information among banks facilitates better credit information, and faster processing of loans benefits SMEs. The passage of the Leasing Law will give SMEs alternative capital resources.

55. Capacity building through training and workshops has strengthened government agencies as institutions and enabled them to effectively perform their regulatory functions. Beneficiaries of this improvement are the SMEs served by the agencies. 56. The reform of the business registration system has been one of the key achievements of the program. It has given both new and existing SMEs the opportunity to be registered efficiently and at low cost. Creation of a website will keep SMEs up to date with information related to business opportunities, operations, and regulation.

B. Effectiveness in Achieving Outcome 57. The program is assessed effective in achieving its outcome since it improved the business environment which has provided opportunities for the development of SMEs inside the formal sector. Output of small industrial establishments increased from KR745.1 billion in 2003 to KR2.6 trillion in 2006. The PCR mission found ample evidence that the program outputs (paras. 8-35) were well selected and well suited for achieving the overall outcome.

14

58. While some SME reform fatigue set in towards the end of the program, the SCSME (which was established under the program) has been playing a crucial role in implementing the government's Rectangular Strategy, while the SMEDF continues to guide government reform efforts pertaining to SMEs. 59. Improvements in the business registration process eased the incorporation of businesses through (i) reduced procedures and requirements, (ii) enhanced transparency, and (iii) reduced official fees (from $1,000 in 2003 to $105 in August 2007). These improvements resulted in the rise in the average number of enterprises registered, from 61 per month before August 2004 to 245 per month during the first quarter of 2008, indicating a significant increase in the number of established SMEs.

60. To enhance SMEs' access to finance, the program supported (i) developing a web-based credit information system (CIS) that helped reduce risks and cost of lending by providing credit information on borrowers; and (ii) providing legal security for the use of collateral in secured transactions and developing a land titling system, which was essential for the use of land as collateral. These may have greatly contributed to the increase in domestic credit to the private sector, from KR1.82 trillion as of December 2004 to KR2.94 trillion as of May 2006. The CIS can be considered one of the more successful components of the program. About 200–300 registrations are made per month, or about 3,000 per year, since it was reformed. 61. However, the effort to implement a licensing review mechanism produced mixed results. While the measures under the program were implemented, actual outcomes were less satisfactory. Several license reviews were undertaken and results posted on the SCSME website, but no significant reform of licenses occurred during implementation, except for those related to business registration. Recent best international practice on regulatory reforms in developing countries provides some lessons why the reform effort in Cambodia was less effective. Evidence shows that the institutional set up for supporting a regulatory reform program should be in place, and this usually includes some oversight agency such as an office of best or better regulatory practice that provides advocacy information for a regulatory review mechanism and monitors progress by implementing agencies. These were not in place in Cambodia under the program. C. Efficiency in Achieving Outcome and Outputs 62. The program is assessed efficient in achieving its outcome and outputs as it was efficiently managed by the MIME, the implementing agencies, and ADB. Despite its complex design—a large number of individual interventions in the SME sector were bundled into one package and financial issues were included—30 of the 32 conditions and all covenants were fully met by the end of the program. The two conditions which were partially complied with were subsequently met 1 year later. Unfortunately, in designing the program, a lesson from earlier programs was neglected: not to include conditions that require the passing of new legislation by parliament. The requirement to pass a leasing law and its implementing regulation, which was waived for third tranche release, caused considerable friction during implementation, and necessitated intensive involvement of ADB staff. Another inefficiency involved the time spent creating specialized software, supported with ADB TA, for business registration and credit information systems, when off-the-shelf software was available—even a spreadsheet application would have done for the simple requirements. While both problems were ultimately resolved, they demanded a high level of attention from ADB staff and consultants, and in both cases the clients remain unsatisfied with the performance of the software.

15

D. Preliminary Assessment of Sustainability 63. The program's sustainability is assessed likely to be sustainable. All outcomes achieved under the program have proven to be sustainable in the year since it ended. All legislative and regulatory reforms are still in place. The reforms undertaken under the program laid the foundation for the development of a business environment that is conducive to business, especially for SMEs. Appendix 6 provides a detailed overview of the other measures of the program and their current status. However, two measures are already becoming marginalized. First, the recourse mechanism, essentially a hotline to complain about the bureaucracy, is hardly used—there were only three registrations in the second and third quarters of 2009. According to MIME officials, Cambodians in general prefer to complain personally through informal channels they trust and know to work, rather than formally and in a confrontational way with uncertain result. Second, the simplified financial reporting template, while still in use, is in itself not incentive enough to convince unregistered SMEs to switch into the formal sector, which was the original intention. However, if it could be combined with temporary tax breaks after the switch, it could result in a sustainable increase of the formal sector. It is noted that regulatory reform did not progress beyond business registration reforms at the time of program implementation and therefore additional institutional reforms may be needed to sustain these reforms. Discussions with the government regarding follow-through of the strategy developed under the program may prove helpful to promote sustainability of reforms. E. Impact 64. The program was assessed category C with respect to environment, involuntary resettlement, and impact on indigenous people. The long-term objective of the CSDP was to create an environment that is conducive to business development and results in sustainable economic growth. The program, in cooperation with the efforts of other donors, has built a sound foundation for SME development.

IV. OVERALL ASSESSMENT AND RECOMMENDATIONS A. Overall Assessment 65. The program was implemented as conceived and was assessed relevant to the government’s development strategy, ADB’s partnerships strategy with Cambodia, and ADB’s strategic objectives at the time of approval. Due to strong government commitment, a well-sequenced reform framework, effective high-level coordination among the executing and implementing agencies, and ADB-led coordination amongst the donor community, the program was rated effective and efficient in achieving the expected outcomes. Based on the government’s strong ownership of program reforms and ongoing commitment to further reforms as envisaged in the Rectangular Strategy, and supported by a follow-on program financed by ADB, the program is rated likely to be sustainable. Overall, the program is rated successful. B. Lessons 66. Several lessons have been learned from this performance evaluation.

(i) Broad-based reforms like those pursued by the program require long-term institutional development, which is insufficiently accommodated in even a three-tranche program loan. A program cluster approach would have been more useful,

16

as it combines a long-term approach that permits a wide range of policy and institutional reforms with flexibility to adjust to changing circumstances. Critical components such as corporate governance and the optimal treatment of public service obligations can be gradually introduced. A program cluster is also useful in setting benchmarks and unifying policy makers who advocate reforms. A move from a multitranche program cluster approach to a medium-term framework based on single-tranche programs within a program loan cluster could be recommended to provide more flexibility while emphasizing achievable outcomes up-front. With such an approach, ADB could also support genuine commitment from stakeholders over a longer period.

(ii) Linking tranche release conditions involving approval of draft laws (Leasing Law, in this case) is subject to a great degree of uncertainty, given that ADB and the government have no control over actions of the National Assembly. Hence, the time required to meet conditions can be easily underestimated.

(iii) At the start of the program, there appeared to be strong enthusiasm for the SME committee and secretariat but by the time of the program's completion, this enthusiasm seemed to have waned. This is an inherent problem with establishing an interagency committee with a wide and seemingly permanent mandate with no exit strategy—it may lose effectiveness, especially if initial targets are not seen to be accomplished. Perhaps a missing element to the process was an independent monitoring unit that could develop performance targets, monitor progress, and identify steps to address delays in the SME strategy.

(iv) While focus was correctly placed on developing tax and accounting guidelines for SMEs and provisioning of training, this effort should have been accompanied by reform of tax policy and administration to lower the compliance costs of SMEs within the tax system. More effort should have been made to identify and address policy or structural barriers to development of the private sector in providing accounting services and other business development services.

(v) The program did not have the necessary institutional requirements for a licensing review mechanism to be successfully institutionalized and therefore sustainable, such as the establishment of an office of best or better regulatory practice and building its capacity to oversee the licensing review process. Lessons could be drawn from Viet Nam's successful institutionalization of regulatory impact assessments, which has occurred over a 5-year period.

C. Recommendations 67. Future monitoring. Monitoring of SME-related reforms should be aligned with emerging and relevant priorities of the government and where there is consensus with development partners. According to recent investment climate surveys, regulatory uncertainty and red tape are identified by investors as remaining key constraints on growth. ADB should continue monitoring the progress of government efforts in licensing and regulatory review mechanisms and look at ways to institutionalize them. ADB should also continue to monitor changes in the economic environment, and the initiatives on improving the business climate environment.

68. Covenants. Policy conditions relating to the approval and promulgation of legislation should be avoided because this leaves the timing of compliance open to a great degree of uncertainty (para. 66[ii]).

17

69. Further action or follow-up. The following recommendations relate to initiatives under the program that have not been completed.

(i) Company registration. The decentralization process should be expanded to more

provincial urban centers as permitted and guided by prakas 249 from the MOC allowing decentralized registration across Cambodia. The MOC should begin developing an online business registration system by establishing the necessary legal and regulatory framework and the detailed operating procedures. Online registration should speed up the process of registration, reduce the administrative costs for both the government and businesses, and ensure transparency in the process by significantly reducing human intervention. After adopting the necessary procedures, the MOC should develop information and communication technologies to facilitate online registration. The MOC should then implement and operationalize an online registration system. Issues for the government’s future consideration may include expanding registration to a wider segment of the economy. Following the example of Singapore, Thailand, and other countries in the region, clear registration requirements should be established to include a broad segment of the economy by setting clear thresholds for firms to register either as sole proprietors or companies. To streamline interministerial registration and licensing, the MOC should link the registration process to other ministries by automatically registering the company for income tax and value-added tax (VAT) using the same process and by harmonizing the tax identification number with the registration number. Eventually registration as a new legal entity and tax registration could be merged into one procedure. A single identification number would help to facilitate registration and licensing and facilitate government-wide data management. It is further recommended that the government should fund its own roll out of the registration system and look at ways to ensure that the registration offices are financially viable. Other development partners such as the International Finance Corporation are providing assistance in the rollout of the business registry system.

(ii) Commercial legal framework. The government still has to enact the draft Law on

Commercial Contracts to establish the necessary framework for contracts and contract enforcement. This will provide increased clarity for contracts between businesses. As a means of avoiding lengthy court cases related to commercial disputes, it is necessary to create an operational commercial arbitration process by implementing the Law on Commercial Arbitration. The law determines the forms of arbitration agreements, the composition and jurisdiction of arbitration panels, the conduct of the arbitration proceedings, and how awards are made and enforced. Commercial arbitration will help to reduce the cost and time needed to resolve disputes. Strengthening legal education is crucial to increasing the supply of well-trained lawyers. Given the current levels of education among judges and prosecutors, long-term legal training is needed to improve the performance of the judiciary. Judges will need to be targeted with intensive training in commercial and business-related law, particularly as more complex commercial laws are enacted and more complex commercial contracts are to be enforced. However, the commercial legal framework goes beyond SME development and is constrained by government capacity. The government has a large legislative agenda under WTO commitments and many of these are not yet completed. Many enactments are not effectively implemented due to weak administrative capacity and a weak judicial system. Lessons learned suggest that a more comprehensive, separate legislative reform and judicial capacity

18

development program may be more effective than an ad hoc approach to judicial reforms.

(iii) Leasing. To enable banks and nonbanks to provide finance leasing now that an

appropriate leasing law has been enacted, the MEF, through the Taxation Department, should introduce new and amended regulations (no need for changes to the Tax Law) to clarify the tax treatment (VAT, timing of supply, tax on profit, depreciation, withholding tax) of financial and operating leases and harmonize the tax treatment of leasing and lending. This would allow all lending products—including collateralized loans, leases, and secured transactions—to compete on how they satisfy market needs rather than on regulatory or tax advantages. To expand the institutional framework for leasing, the NBC should promote joint-venture finance leasing companies, while the MOC or NBC should promote joint-venture or stand-alone leasing companies that provide operating and/or finance leases.

(iv) Credit information sharing.11 The NBC should issue a review of the operations of

the pilot credit information system, examine options to expand it (to include “positive” information, include other financial institutions, and make it compulsory) and assess the feasibility of establishing a fully fledged private credit bureau that operates on a sustainable basis. Depending on the development of the CIS system, information provided by merchants and utilities could be included, and a credit scoring system could be developed, as a starting point for risk management systems. Finally, during this phase, consideration should be given to establishing a joint venture with one of the international firms that operate credit registries and is known to support the strengthening of credit registries in developing countries. This is better accomplished under the ongoing finance sector and development program.

70. Timing of the program performance evaluation report. To further assess the impact of program reforms, the conduct of a program performance audit report is recommended by the end of 2010. 11 A World Bank survey of 56 countries with credit registries highlighted the different functions of private and public

credit registries (public registries are almost always operated by a central bank). The survey of October 2003 found that most developed countries have private credit registries. Latin America has the most widespread credit registries, with most countries having both private and public credit registries. Africa and Eastern Europe have the least-developed credit reporting. Developed countries that have both public and private credit registries include Germany, Italy, Portugal, and Spain. France has only a public credit registry. Other developed countries with public credit registries include Austria and Belgium. Countries with only private credit registries include Australia, Canada, Sweden, the United Kingdom, and the United States. In the region, Malaysia, Philippines, Singapore and Thailand operate private credit registries, although Indonesia, the Lao People's Democratic Republic, Malaysia and Viet Nam have public credit registries. Including overlaps, i.e., countries that operate both kinds, 27 countries operate public credit registries, and 28 operate private credit registries.

19

Figure 2: Establishments Identifying Problem as “Major” Obstacle to Growth (% of firms)

Source: World Bank Investment Climate Survey, 2003 and 2007.

0

10 20 30 40 50 60

Cor

rupt

ion

Mac

roec

onom

ic

stab

ility

Ant

i-com

petit

ive

prac

tices

Reg

ulat

ory

unce

rtain

ty

Ele

ctric

ity c

osts

Inad

equa

te

skill

s Crim

e

Cos

t of f

inan

ce

Red

tape

2007 2003

71. Emerging policy priorities in Cambodia's private sector and SME development. Based on recent global economic developments and challenges, the government has prioritized a broader agenda for improving the business climate with the aim of promoting economic diversification (Figure 2). The government considers industry to be narrowly concentrated in a few major sectors such as garments, tourism, and construction. Current best international practice is also shifting towards broader-based policy and structural reforms including regulatory reform and competition policy, trade facilitation, and tax reforms where major economic gains can be made and passed onto SMEs. Based on the World Bank investment climate survey of 2003 and 2007, major priority reform areas include governance, macroeconomic stability, competition policy, electricity sector, tax reform, trade facilitation and customs, and labor skills, and developing private sector providers of business services is key to developing the private sector.12 Access to finance is considered less of a constraint today than it was 4–5 years ago, an indication of successful reforms in this sector since 2004.

12 World Bank. 2007 Investment Climate Assessment. Washington D.C.

Appendix 1 20

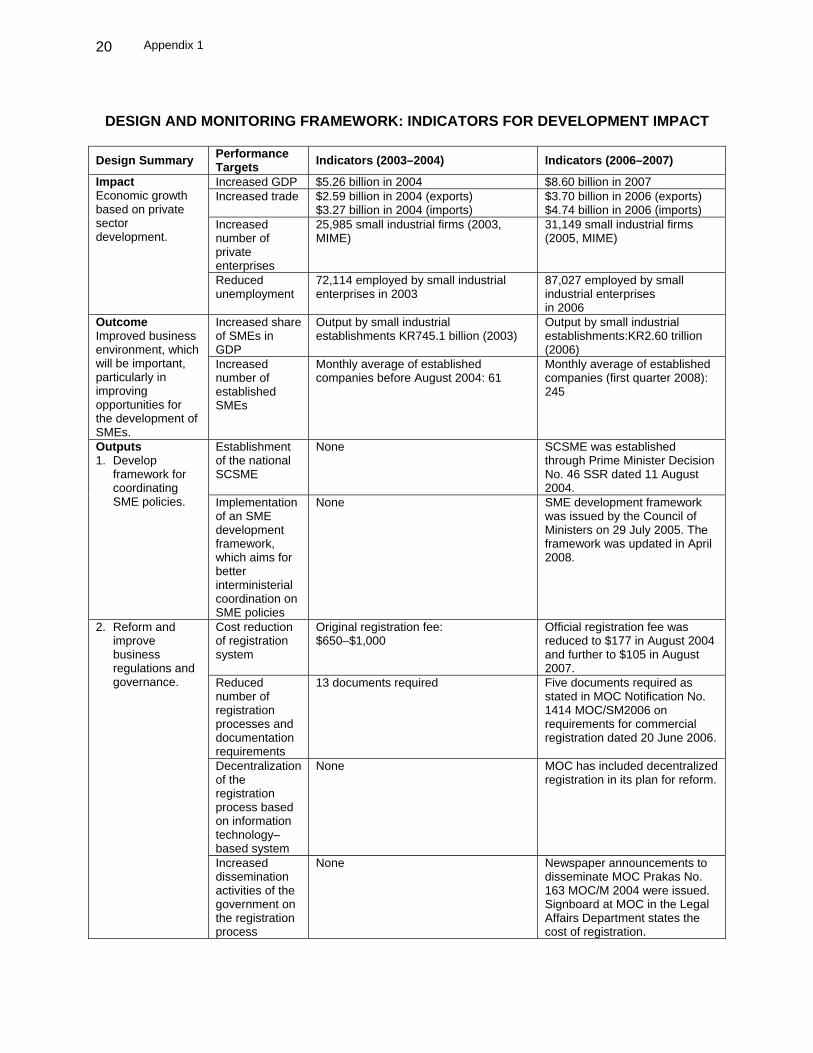

DESIGN AND MONITORING FRAMEWORK: INDICATORS FOR DEVELOPMENT IMPACT

Design Summary Performance

Targets Indicators (2003–2004) Indicators (2006–2007) Increased GDP $5.26 billion in 2004 $8.60 billion in 2007 Increased trade $2.59 billion in 2004 (exports)

$3.27 billion in 2004 (imports) $3.70 billion in 2006 (exports) $4.74 billion in 2006 (imports)

Increased number of private enterprises

25,985 small industrial firms (2003, MIME)

31,149 small industrial firms (2005, MIME)

Impact Economic growth based on private sector development.

Reduced unemployment

72,114 employed by small industrial enterprises in 2003

87,027 employed by small industrial enterprises in 2006

Increased share of SMEs in GDP

Output by small industrial establishments KR745.1 billion (2003)

Output by small industrial establishments:KR2.60 trillion (2006)

Outcome Improved business environment, which will be important, particularly in improving opportunities for the development of SMEs.

Increased number of established SMEs

Monthly average of established companies before August 2004: 61

Monthly average of established companies (first quarter 2008): 245

Establishment of the national SCSME

None SCSME was established through Prime Minister Decision No. 46 SSR dated 11 August 2004.

Outputs 1. Develop

framework for coordinating SME policies. Implementation

of an SME development framework, which aims for better interministerial coordination on SME policies

None SME development framework was issued by the Council of Ministers on 29 July 2005. The framework was updated in April 2008.

Cost reduction of registration system

Original registration fee: $650–$1,000

Official registration fee was reduced to $177 in August 2004 and further to $105 in August 2007.

Reduced number of registration processes and documentation requirements

13 documents required Five documents required as stated in MOC Notification No. 1414 MOC/SM2006 on requirements for commercial registration dated 20 June 2006.

Decentralization of the registration process based on information technology–based system

None MOC has included decentralized registration in its plan for reform.

2. Reform and improve business regulations and governance.

Increased dissemination activities of the government on the registration process

None Newspaper announcements to disseminate MOC Prakas No. 163 MOC/M 2004 were issued. Signboard at MOC in the Legal Affairs Department states the cost of registration.

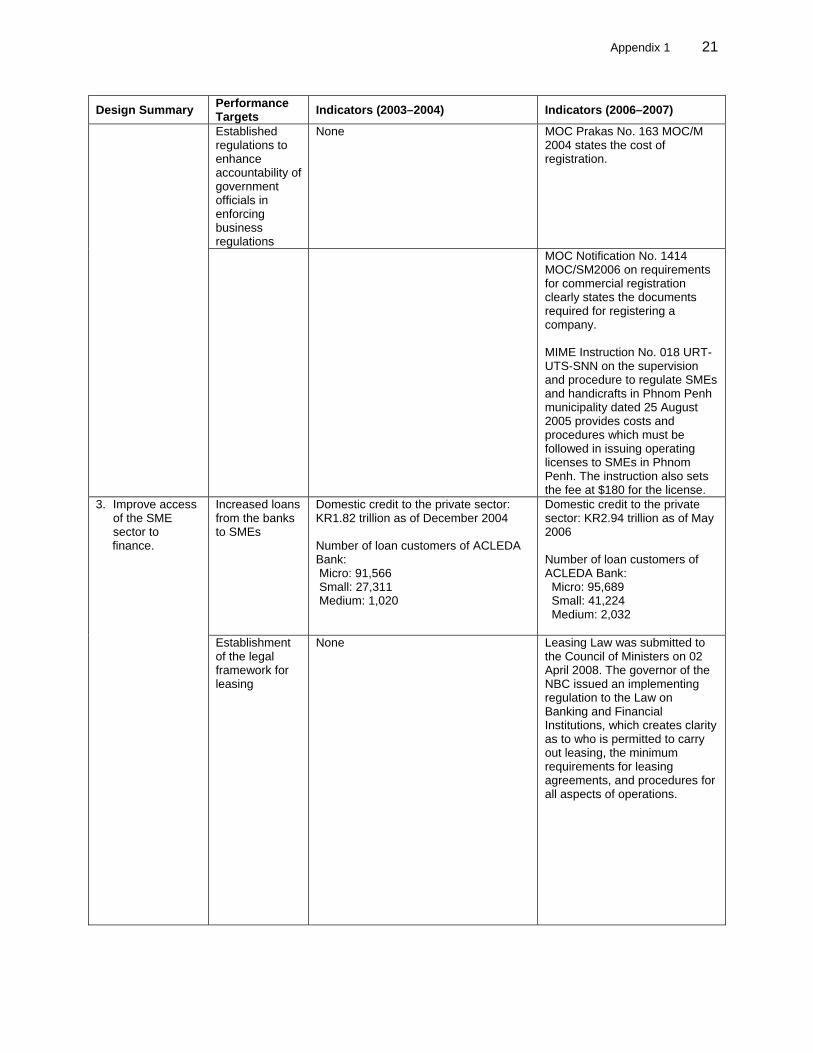

Appendix 1 21

Design Summary Performance Targets Indicators (2003–2004) Indicators (2006–2007) Established regulations to enhance accountability of government officials in enforcing business regulations

None MOC Prakas No. 163 MOC/M 2004 states the cost of registration.

MOC Notification No. 1414 MOC/SM2006 on requirements for commercial registration clearly states the documents required for registering a company. MIME Instruction No. 018 URT-UTS-SNN on the supervision and procedure to regulate SMEs and handicrafts in Phnom Penh municipality dated 25 August 2005 provides costs and procedures which must be followed in issuing operating licenses to SMEs in Phnom Penh. The instruction also sets the fee at $180 for the license.

Increased loans from the banks to SMEs

Domestic credit to the private sector: KR1.82 trillion as of December 2004 Number of loan customers of ACLEDA Bank: Micro: 91,566 Small: 27,311 Medium: 1,020

Domestic credit to the private sector: KR2.94 trillion as of May 2006 Number of loan customers of ACLEDA Bank: Micro: 95,689 Small: 41,224 Medium: 2,032

3. Improve access of the SME sector to

finance.

Establishment of the legal framework for leasing

None Leasing Law was submitted to the Council of Ministers on 02 April 2008. The governor of the NBC issued an implementing regulation to the Law on Banking and Financial Institutions, which creates clarity as to who is permitted to carry out leasing, the minimum requirements for leasing agreements, and procedures for all aspects of operations.

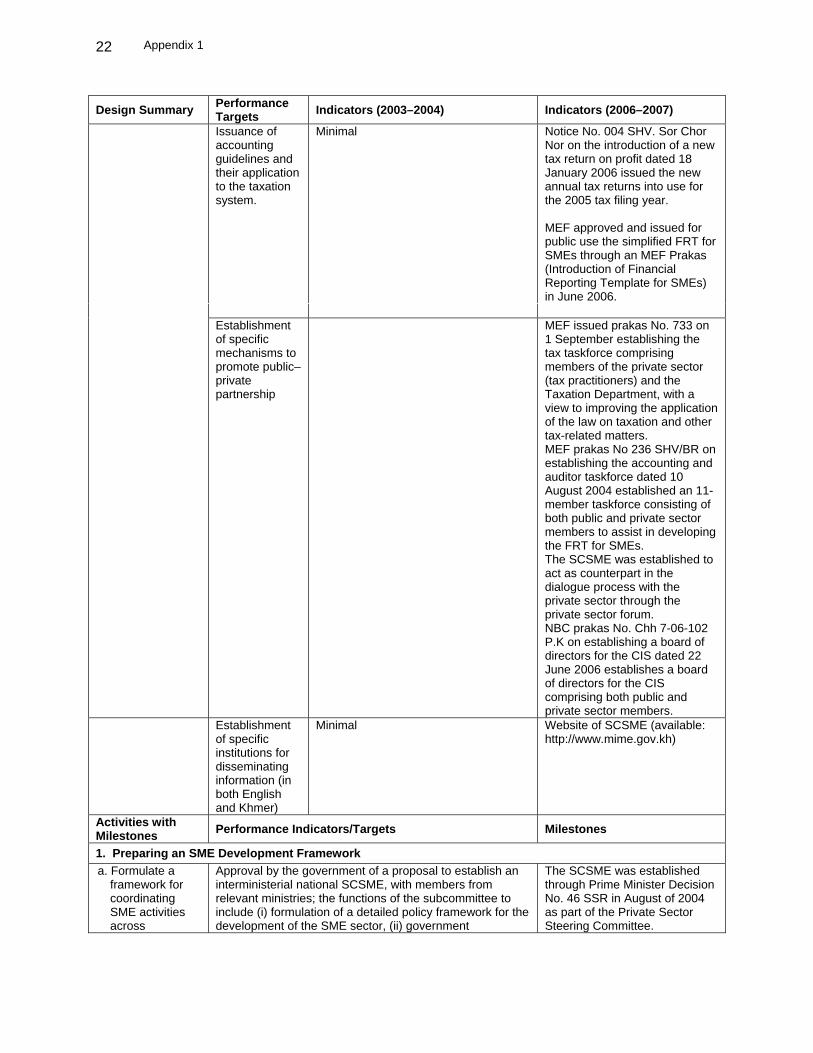

Appendix 1 22

Design Summary Performance Targets Indicators (2003–2004) Indicators (2006–2007) Issuance of accounting guidelines and their application to the taxation system.

Minimal Notice No. 004 SHV. Sor Chor Nor on the introduction of a new tax return on profit dated 18 January 2006 issued the new annual tax returns into use for the 2005 tax filing year. MEF approved and issued for public use the simplified FRT for SMEs through an MEF Prakas (Introduction of Financial Reporting Template for SMEs) in June 2006.

Establishment of specific mechanisms to promote public–private partnership

MEF issued prakas No. 733 on 1 September establishing the tax taskforce comprising members of the private sector (tax practitioners) and the Taxation Department, with a view to improving the application of the law on taxation and other tax-related matters. MEF prakas No 236 SHV/BR on establishing the accounting and auditor taskforce dated 10 August 2004 established an 11-member taskforce consisting of both public and private sector members to assist in developing the FRT for SMEs. The SCSME was established to act as counterpart in the dialogue process with the private sector through the private sector forum. NBC prakas No. Chh 7-06-102 P.K on establishing a board of directors for the CIS dated 22 June 2006 establishes a board of directors for the CIS comprising both public and private sector members.

Establishment of specific institutions for disseminating information (in both English and Khmer)

Minimal Website of SCSME (available: http://www.mime.gov.kh)

Activities with Milestones Performance Indicators/Targets Milestones

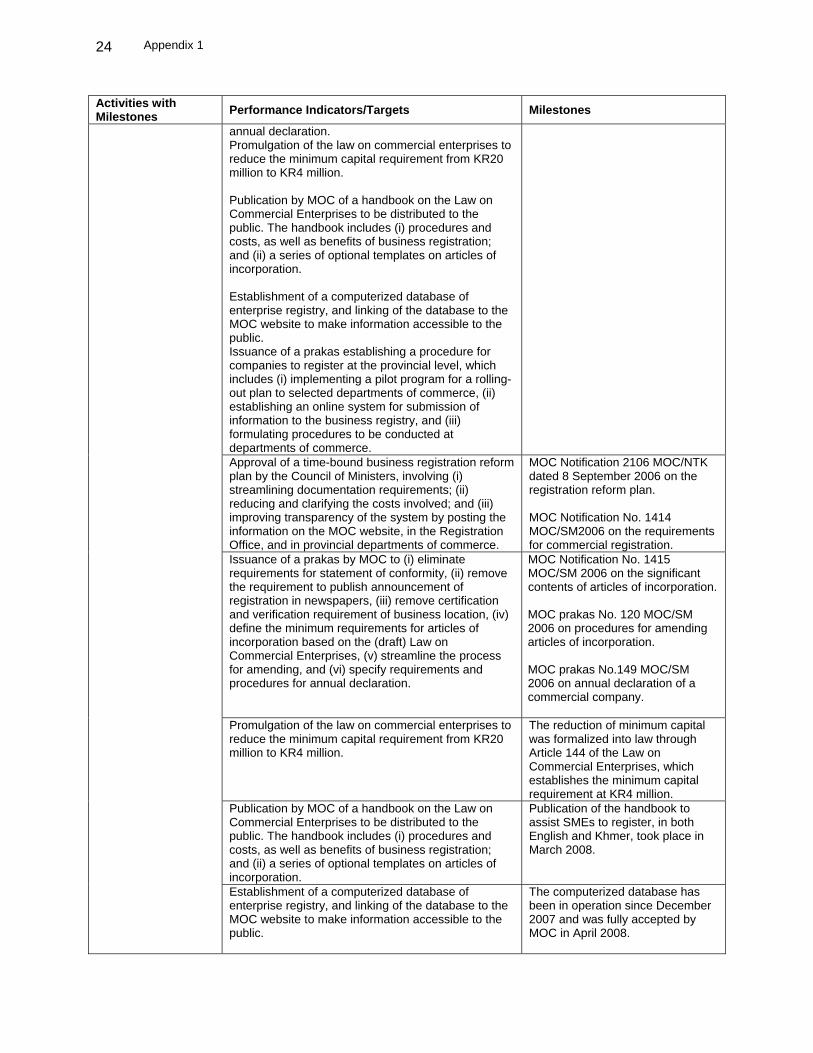

1. Preparing an SME Development Framework a. Formulate a

framework for coordinating SME activities across

Approval by the government of a proposal to establish an interministerial national SCSME, with members from relevant ministries; the functions of the subcommittee to include (i) formulation of a detailed policy framework for the development of the SME sector, (ii) government

The SCSME was established through Prime Minister Decision No. 46 SSR in August of 2004 as part of the Private Sector Steering Committee.

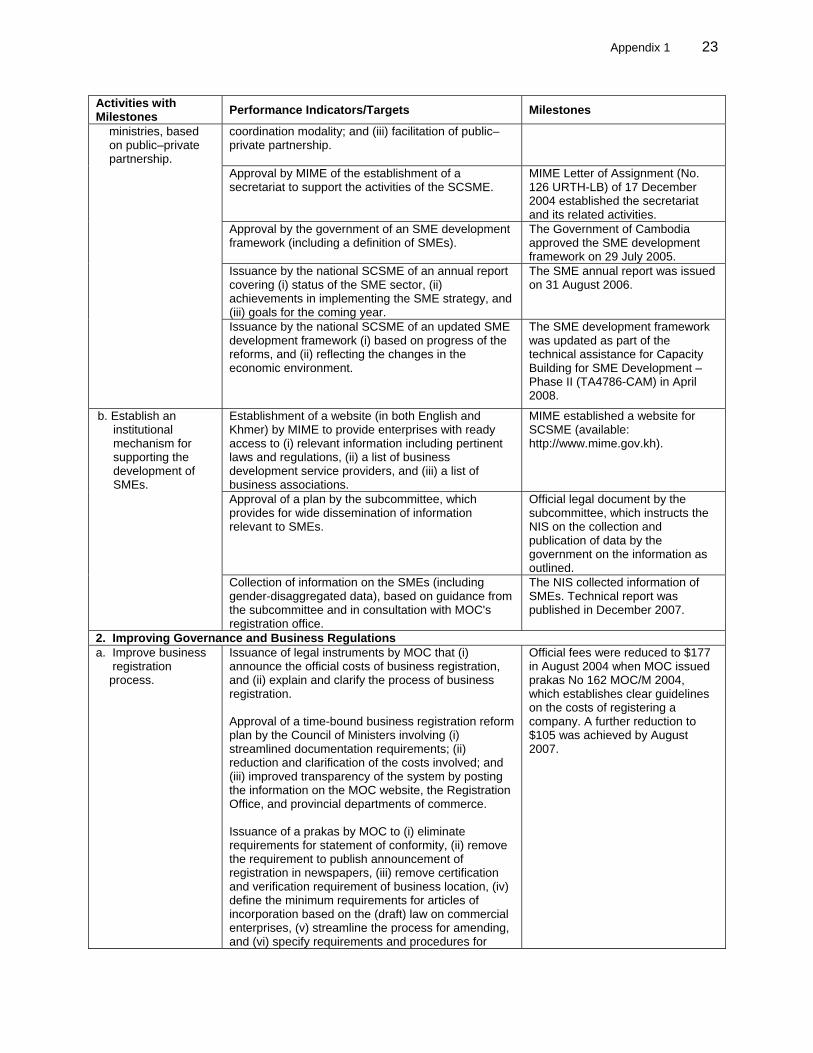

Appendix 1 23

Activities with Milestones Performance Indicators/Targets Milestones

coordination modality; and (iii) facilitation of public–private partnership.

Approval by MIME of the establishment of a secretariat to support the activities of the SCSME.

MIME Letter of Assignment (No. 126 URTH-LB) of 17 December 2004 established the secretariat and its related activities.

Approval by the government of an SME development framework (including a definition of SMEs).

The Government of Cambodia approved the SME development framework on 29 July 2005.

Issuance by the national SCSME of an annual report covering (i) status of the SME sector, (ii) achievements in implementing the SME strategy, and (iii) goals for the coming year.

The SME annual report was issued on 31 August 2006.

ministries, based on public–private partnership.

Issuance by the national SCSME of an updated SME development framework (i) based on progress of the reforms, and (ii) reflecting the changes in the economic environment.

The SME development framework was updated as part of the technical assistance for Capacity Building for SME Development – Phase II (TA4786-CAM) in April 2008.

Establishment of a website (in both English and Khmer) by MIME to provide enterprises with ready access to (i) relevant information including pertinent laws and regulations, (ii) a list of business development service providers, and (iii) a list of business associations.

MIME established a website for SCSME (available: http://www.mime.gov.kh).