Embed Size (px)

Citation preview

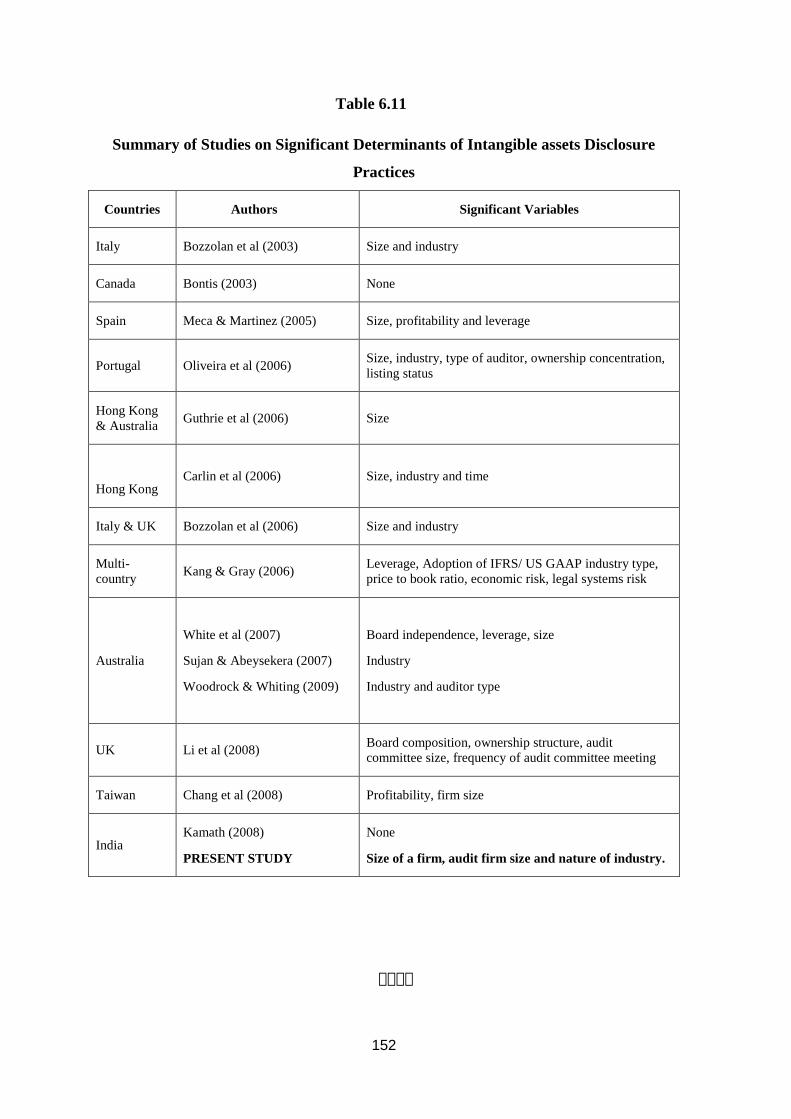

116

CHAPTER VI

COMPANY ATTRIBUTES AND EXTENT OF INTANGIBLE

ASSETS DISCLOSURE

The results of chapter 5 reveal that the extent of disclosure of intangible assets

varies from company to company. It could be due to the influence of different corporate

specific attributes.

This chapter analyses the association between the extent of intangible assets

disclosure and corporate attributes. The corporate attributes studied are size of a firm, its

profitability, leverage, listing category, nature of industry, foreign activity and audit firm

size. These explanatory variables have been divided into three groups, consistent with

Lang and Lundholm (1993), Wallace et al. (1994) and Oliveira et al (2006). These groups

are:

i) structural variables, including firm size, leverage, and audit firm size;

ii) performance variables, including profitability; and

iii) market variables, comprising industry, listing status and foreign activity

6.1. HYPOTHESES DEVELOPMENT

Based on the theoretical considerations and empirical research, several hypotheses

have been developed that relate company-specific characteristics to the disclosure of

intangible assets by companies in India. All hypotheses have been stated in both null and

alternate form.

6.1.1 Size of a firm

Firm size is perhaps the most consistent corporate specific characteristic which

has been found to be associated with the level of intangible assets disclosure. Bozzolan et

al (2003, 2006), Meca and Martinez (2005), Oliveira et al (2006), Guthrie et al (2006),

Carlin et al (2006) and White et al (2007) found positive relation between size of a firm

and extent of intangible assets disclosure. However, Kang and Gray (2006) and Kamath

117

(2008a) observed no correlation between intangible assets reporting in the annual reports

and size of the companies.

Larger companies may be hypothesised to disclose more intangible assets related

information in the annual report than smaller companies for a variety of reasons. Firstly,

the cost of disseminating and accumulating detailed information may be relatively low

for the larger corporations than the smaller corporations (Cerf, 1961; Singhvi & Desai,

1971; Buzby, 1975 and Firth, 1979). The big companies have the resources and expertise

to produce more information in their company‟s annual reports (Ahmed & Nicholls, 1994

and Hossain & Adams, 1994). Hence, little extra cost may be incurred to increase

disclosure, i.e. lower incremental cost of producing information for large firms (Lang and

Lundholm, 1993). In addition, larger corporations might need to collect more intangible

assets information for their internal management system.

Secondly, larger companies undertake more activities, and usually have different

business units which may have different critical success factors and different long term

value-creating potential (Hackstone and Milne, 1996). This means that more information

needs to be disclosed to provide stakeholders with a complete picture of the company.

Thirdly, larger firms tend to go to the stock market for financing more often than

smaller firms and as a result may disclose more information in their annual reports for

their own interest (i.e. capital need hypothesis; Cerf, 1961).

Fourthly, smaller firms may feel that their intangible assets disclosure activities

could endanger their competitive oppositions with respect to other larger firms in their

industry, i.e. reluctance of small firm to inform their competitors (Singhvi & Desai, 1971;

Buzby, 1975; Raffournier, 1995). As a result, smaller companies may tend to disclose

less information concerning its intangible assets than large companies.

Fifthly, Wallace and Naser (1995) state the impact of large size companies on the

economy. These can be considerable as these companies account for a significant

proportion of goods and services produced, consumption of raw materials and number of

people employed. The large companies are likely to come under the scrutiny of various

interested parties and therefore tend to disclose adequate and detailed intangible assets

related information in their annual reports.

118

Sixthly, large corporations are likely to have a higher level of internal reporting to

keep senior management informed and therefore likely to have relevant information

available (Cerf, 1961; Buzby, 1975 and Owusu-Ansah, 1998; Depoers, 2000).

Seventhly, it has been suggested that the annual reports of large corporations are

more likely to be scrutinised by financial analysts than those of smaller firms and

investors may interpret non-disclosure as bad news which could adversely affect firm

value. Thus, larger firms may have an incentive to disclose more information related to

its intangible assets than smaller firms.

Finally, as far as political costs are concerned, bigger companies are more vigil in

the public eye which will tend to make them exhibit greater disclosure than the smaller

firms (Firth, 1979; Holthausen and Leftwitch, 1983; Watts and Zimmerman, 1990).

Agency theory shows that a company has to satisfy the needs of creditors and investors.

Therefore, it should provide detailed information in annual reports to avoid information

asymmetries (Jensen & Meckling 1976). Thus, bigger firms make more disclosure to

minimise agency and political costs.

The priori expectation is that larger companies will have higher levels of

intellectual capital reporting than smaller companies. Several measures of size are

available in the literature. The total sales, total assets and market capitalisation are used

as surrogates of size of a firm in this study. The foregoing discussions lead to

development of the following null and alternate hypotheses:

H01: The size of a company as measured by its total assets or total sales or total market

capitalization has no significant impact on its intangible assets disclosure score.

H1: The size of a company as measured by its total assets or total sales or total market

capitalization has a significant impact on its intangible assets disclosure score.

6.1.2 Leverage of a firm

Several studies investigated the relationship between leverage (book value of debt

to shareholder‟s equity) and intangible assets disclosure. It is viewed that companies with

a higher level of leverage have high level of financial risk (Patton and Zelenka, 1997) and

thus disclose more information. Agency theory can also be used to explain the influence

of leverage on the level of voluntary disclosure by a firm. When firms incur outside debt,

119

agency costs arise from conflicts of interest between equity and debt investors (Berger &

Bonaccorsi di Patti, 2006). These agency costs are comprised of a reduction in value of

the firm and increased monitoring costs owing to the fact that the manager will try and

reallocate the wealth of the debt-holder to the firm. The greater the level of debt, the

wider apart the two parties‟ interests (Jensen & Meckling, 1976) and hence the need for

higher monitoring costs. Increased disclosure by a firm can reduce these monitoring

costs. Thus, firms with high leverage levels have an incentive to make voluntary

disclosures in order to reduce agency costs.

Media agenda-setting theory (Cohen, 1963) has also been used to explain why a

firm‟s leverage level could be associated with its intangible assets disclosure levels. If a

firm has „good news‟, low levels of debt for example, then it will attempt to highlight this

positive information to the market through making voluntary disclosures in its annual

report (Sujan & Abeysekera, 2007). Media agenda setting theory therefore suggests the

opposite of agency theory. If a company has low leverage levels it will increase its

voluntary disclosures to inform the market of its strong position.

Prior studies have provided mixed results on the association between leverage and

intangible assets disclosure levels. Oliveira et al (2006), Bozzolan el al (2006) and

Woodrock & Whiting‟s (2009) showed no association between the extent of voluntary

intangible assets disclosure and leverage, whereas Meca & Martinez (2005) and White et

al. (2007) observed a significant positive relationship between the two. The following

null and alternate hypotheses are tested in this study:

H02: The leverage of a company as measured by its debt-equity ratio has no significant

impact on its intangible assets disclosure score.

H2: The leverage of a company as measured by its debt-equity ratio has a significant

impact on its intangible assets disclosure score.

6.1.3 Audit Firm Size

Many authors have suggested that auditors play a role in defining the disclosure

policy of their clients (Raffournier, 1995). Large audit firms are widely scattered across

the world while small audit firms operate domestically. The classification of audit firms

into two groups has been drawn on the assumption that the large firms have more concern

120

for their reputation and therefore are more willing to associate with firms that disclose

more information in their published financial reports. On the other hand, small audit

firms do not possess the power to influence the disclosure practices of their clients.

Rather they attempt to meet the needs of their clients in order to retain them (Firth, 1979

and Wallace and Naser, 1995). Oliveira et al. (2006) argued that large auditing firms may

encourage their clients to disclose more information as they want to preserve their

reputation, develop their expertise, and ensure that they retain their clients.

Chalmers and Godfrey (2004) argue that high profile auditing companies are

more likely to demand high levels of disclosure to maintain their reputation and to avoid

reputation costs. Dumontier and Raffournier (1998) observe that the auditors want their

clients to comply with complex accounting standards for the sake of their reputation and

in their own interest. They may use the information disclosed by their clients as a signal

about their own quality (Inchausti, 1997). The other reason advocated by Patton and

Zelenka (1997) is that the audit by big-six-audit firm is believed to bring enhanced

credibility to the financial reports. This is also linked to the fact that major international

auditing companies have more knowledge about International Accounting Standards

(IAS) and so the costs of implementing and auditing them to their clients is lower than for

smaller auditing companies.

This hypothesis is based on the argument that companies audited by big-six audit

firms have substantial agency costs. They try to reduce them by contracting with these

auditing firms. Auditing is argued to be a way of reducing agency costs (Jensen &

Meckling, 1976 and Watts & Zimmerman, 1983) and the companies that have high

agency costs tend to contract high quality auditing companies. Thus, there is a positive

relationship between agency costs and the disclosure decision (Inchausti, 1997).

Oliveira et al. (2006) and Woodrock & Whiting‟s (2009) are the sole studies to

examine the relationship between the audit firm size and the extent of its intangible assets

disclosure. They concluded that companies with a Big Four auditor disclose more

121

intangible asset information as compared to companies with non-Big four auditors. The

following null and alternate hypotheses have been formulated and tested in this study:

H03: The audit firm size of a company has no significant impact on its intangible assets

disclosure score.

H3: The audit firm size of a company has a significant impact on its intangible assets

disclosure score.

This has been used as a dummy variable. The companies being audited by Big-six audit firms (Price

Waterhouse; A.F. Ferguson; S.B. Baltiboi; Delloitte; Haskins and Sells and B.S.R. & Co.) were assigned a

score of 1 and others 0.

6.1.4. Profitability of a Firm

A number of researchers have used profitability as an explanatory variable for

differences in the disclosure levels. A company‟s profit comes from its continued

investment in intangible assets. The companies which have more investment in intangible

assets will tend to disclose more information about them. Therefore the more an

enterprise can make profits, the more it will tend to disclose the information about

intangible assets. The higher the performance of companies is, the more it will discloses

intellectual capital to the public (Li et al, 2008). Singhvi and Desai (1971) pointed out

that a company with high profits will disclose more information about intellectual capital.

Meca and Martinez (2005) verified a positive relationship between intellectual capital

disclosure and the corporate profitability.

Companies having higher profitability may disclose more information relating its

intangible assets in their corporate annual reports than the companies with lower

profitability (or losses) for a number of reasons. Firstly, if the profitability of a company

is high, management may disclose more detailed information in their corporate annual

reports in order to experience the comfort of communicating it as good news. On the

other hand, if profitability is low, management may disclose less information in order to

cover up the reasons for losses or lower profits (Singhvi and Desai, 1971). It can be

linked to theoretical framework of reporting practices also. Agency theory suggests that

122

managers of very profitable firms will use external information in order to obtain

personal advantages. Therefore, they will disclose detailed information in order to

support the continuance of their positions and compensation arrangements (Inchausti,

1997).

Signalling theory suggests that profitable firms are more likely to disclose more

information to the market to differentiate themselves from poorer performers. Wallace

and Naser (1995) argue that a profitable company is more likely to signal its good

performance to the market by disclosing more information in its annual report. Political

process theory argues that firms with huge profits will be interested in disclosing more

information in order to justify the level of profits. However, the empirical studies found

mixed results.

Researchers have used a number of measures to determine the associations

between profitability and disclosure levels. The return on assets, returns on sales, return

on net worth and return on capital employed have been used as a determinant of

profitability and its association with the level of disclosure in the present study. The

following specific null and alternate hypotheses have been formulated and tested.

H04: The profitability of a company as measured by its ROA or ROS or ROCE or

RONW has no significant impact on its intangible assets disclosure score.

H4: The profitability of a company as measured by its ROA or ROS or ROCE or

RONW has a significant impact on its intangible assets disclosure score.

6.1.5 Listing Category of a Company

The listing category of a firm also influences the disclosure level of a firm. The

relationship between a company‟s listing category and disclosure practices is based on

agency cost and the signalling arguments (Lopes and Rodrigues, 2007). Every Indian

company listed on a stock exchange has to comply with its listing agreement. The

companies whose shares are actively traded have always been scrutinised sharply by the

123

market as a whole and investors in particular. Thus, to reduce agency, political and

monitoring costs more disclosure is being demanded from A category firms than others.

The other reasons being that the international investors have shown their interest

in the Indian capital market after 1993-94. The companies listed under A category are

assumed to be audited by big-six audit firms, have overseas operations and might have

listing on foreign stock exchange and are actively traded on stock exchanges. Such

companies are believed to be disclosing better and detailed information. This argument is

even stronger if the listed company wants to raise its capital in foreign markets (capital-

need hypothesis, Cooke, 1989).

Oliveira et al‟s (2006) study showed a significant influence of listing category on

the level of intangible assets disclosure. So, the above discussion has lead to the

formulation and testing of the following null and alternate hypotheses:

H05: The listing category of a firm has no significant impact on its intangible assets

disclosure score.

H5: The listing category of a firm has a significant impact on its intangible assets

disclosure score.

The impact of listing category of a firm has also been examined by introducing dummy variable. The score of

1 has been given for companies falling under „A‟ listing category and 0 otherwise.

6.1.6. Foreign Activity

Another possible motive for increased disclosures on intangible assets is the

degree of foreign activity of the firm. With the increase in the level of foreign trade, a

company needs to increase their disclosures relating to intangible assets to prove its credit

worthiness to its foreign clients. Managers of companies operating in several

geographical areas have to control a greater amount of information, due to the higher

complexity of the firm‟s operations (Cooke, 1989b). They are prone to increase their

disclosure to show their international presence to stakeholders as a perceived good signal

(Cooke, 1989b, Raffournier, 1995 and Depoers, 2000).. Accordingly, the following null

and alternate hypotheses have been framed:

124

H06: The extent of foreign activity of a company as measured by its total exports to

total sales ratio has no significant impact on its intangible assets disclosure score.

H6: The extent of foreign activity of a company as measured by its total exports to

total sales ratio has a significant impact on its intangible assets disclosure score.

6.1.7 Nature of Industry

The nature of industry and the degree of competition within an industry to which

a company belongs may also influence its intangible assets disclosure level. This can be

explained by stakeholder theory, signalling theory, legitimacy theory, proprietary theory

and media agenda-setting theory. Stakeholder theory purports that shareholders have a

right to be provided with information about how the organisation‟s activities affect them

(Vergauwen & Alem, 2005), particularly if they are less powerful shareholders who

cannot access information through private meetings (Holland, 2001). So in order to

satisfy the stakeholders‟ need for information, firms are forced to make voluntary

disclosures about their intangible assets.

Signalling theory suggests that, within an industry, any deviation from established

corporate reporting practice may be perceived by the market as bad news (Giner, 1997).

Additionally, mandatory financial reporting is claimed to be less informative in high

technology industries which make larger investments in intangibles (such as R&D,

human capital and brand development) (Collins et al., 1997; Francis and Schipper, 1999;

Lev and Zarowin, 1999).

Legitimacy theory asserts that organisations, as part of a social contract, will take

action to ensure that their activities are perceived as legitimate (Lindblom, 1994;

Wilmshurst & Frost, 2000). Firms with high levels of intangible assets are more likely to

engage in voluntary intangible assets disclosure because they cannot legitimise their

status through the traditional symbols of corporate success, the tangible hard assets

(Guthrie et al., 2004). They need to communicate how the firm uses its intangible assets

to generate value (Sciulli et al., 2002).

125

Proprietary costs also vary according to industry. Different industries have

different characteristics relative to market competition, the type of private information,

and the threat of entry of new firms into the market. These factors provide incentives for

companies belonging to the same industry to disclose more information than firms in

another industry.

The fifth theory that has been used to explain the level of voluntary intangible

assets disclosure is that of media agenda-setting theory. This theory suggests that firms

(as a form of media) set the agenda for public opinion by emphasizing or highlighting

certain issues. Therefore “intangible assets intensive firms” boast of their intangible

assets to signal their superiority over competitors (Sujan & Abeysekera, 2007).

Most studies have supported the hypothesis that firms that are high in intangible

assets (e.g. “high-tech.”, knowledge intensive industries) are more likely to engage in

voluntary intangible assets disclosures (e.g. Bozzolan et al., 2003; Petty & Cuganesan,

2005; Bozzolan et al., 2006; Oliveira et al., 2006; Sujan & Abeysekera, 2007; Woodrock

& Whiting, 2009) and some studies have chosen to base their research solely on samples

of firms from high intellectual capital industries (e.g. Sonnier et al., 2007; White et al.,

2007). Accordingly, the null and alternate hypotheses of the study are

H07: The nature of industry to which a company belongs has no significant impact on

its intangible assets disclosure score.

H7: The nature of industry to which a company belongs has a significant impact on its

intangible assets disclosure score.

6.2. RESULTS AND DISCUSSIONS

The effect of different corporate attributes on the extent of intangible assets

disclosure has been studied with the help of two-factor ANOVA test, Univariate and

backward step-wise regression analysis. The results of these have been discussed in the

following sub-parts:

6.2.1 Two-factor ANOVA

126

Intangible assets disclosure trends have been analysed for each of the corporate

attributes (size of the firm- total sales, total assets and market capitalization, leverage,

audit firm size, profitability- ROS, ROA, ROCE and RONW, listing status and foreign

activity) for both years of the study. Each attribute (except dummy variables) was divided

into three broad categories. First category, „High‟ consists of disclosure scores of all

those companies which fall above 66.67th

percentile values for each respective attribute.

„Medium‟ second category consists of disclosure scores of all those companies which fall

between 33.33 to 66.67th

percentile for each respective attribute. Third category „Low‟

comprises disclosure score of companies which fall below 33.33rd

percentile for each

respective attribute.

Table 6.1 shows mean and standard deviation values for categories of all the

above corporate attributes for both years of the study. Also, in order to examine any

significant difference in the mean disclosure score of each category (i.e. high, medium

and low) over two years of study, two factor ANOVA test was conducted. In table 6.1, F-

values „across years‟ highlights significant difference in disclosure score over both years

of the study; F-values „across categories‟ illustrates any significant difference in

intangible assets disclosure score across different categories; and F-values „Year and

category wise‟ shows differences in disclosure scores when both years and categories are

together taken into consideration. The ANOVA test pre-condition of equal variances was

satisfied by conducting Levene‟s test of homogeneity of variance. The Levene‟s test‟s

significance for all corporate attributes was greater than 0.05, which satisfied the above

ANOVA test prerequisite.

127

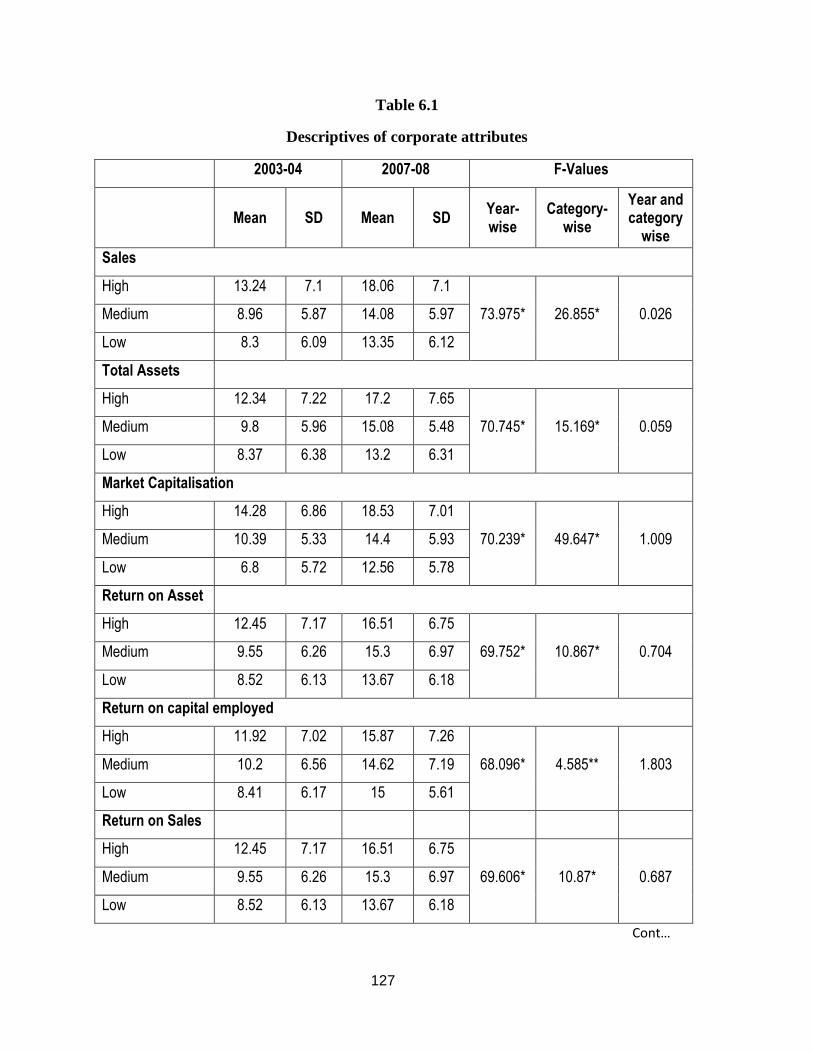

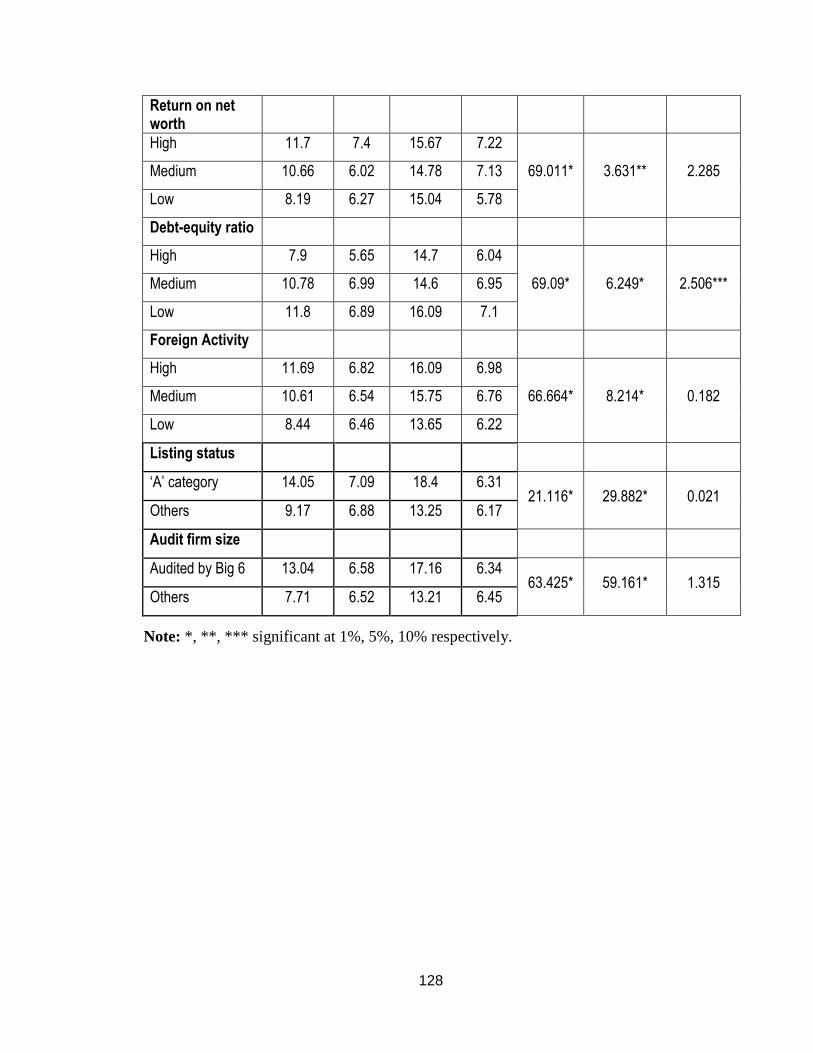

Table 6.1

Descriptives of corporate attributes

2003-04 2007-08 F-Values

Mean SD Mean SD

Year-wise

Category-wise

Year and category

wise

Sales

High 13.24 7.1 18.06 7.1

73.975* 26.855* 0.026 Medium 8.96 5.87 14.08 5.97

Low 8.3 6.09 13.35 6.12

Total Assets

High 12.34 7.22 17.2 7.65

70.745* 15.169* 0.059 Medium 9.8 5.96 15.08 5.48

Low 8.37 6.38 13.2 6.31

Market Capitalisation

High 14.28 6.86 18.53 7.01

70.239* 49.647* 1.009 Medium 10.39 5.33 14.4 5.93

Low 6.8 5.72 12.56 5.78

Return on Asset

High 12.45 7.17 16.51 6.75

69.752* 10.867* 0.704 Medium 9.55 6.26 15.3 6.97

Low 8.52 6.13 13.67 6.18

Return on capital employed

High 11.92 7.02 15.87 7.26

68.096* 4.585** 1.803 Medium 10.2 6.56 14.62 7.19

Low 8.41 6.17 15 5.61

Return on Sales

High 12.45 7.17 16.51 6.75

69.606* 10.87* 0.687 Medium 9.55 6.26 15.3 6.97

Low 8.52 6.13 13.67 6.18

Cont…

128

Return on net worth

High 11.7 7.4 15.67 7.22

69.011* 3.631** 2.285 Medium 10.66 6.02 14.78 7.13

Low 8.19 6.27 15.04 5.78

Debt-equity ratio

High 7.9 5.65 14.7 6.04

69.09* 6.249* 2.506*** Medium 10.78 6.99 14.6 6.95

Low 11.8 6.89 16.09 7.1

Foreign Activity

High 11.69 6.82 16.09 6.98

66.664* 8.214* 0.182 Medium 10.61 6.54 15.75 6.76

Low 8.44 6.46 13.65 6.22

Listing status

‘A’ category 14.05 7.09 18.4 6.31 21.116* 29.882* 0.021

Others 9.17 6.88 13.25 6.17

Audit firm size

Audited by Big 6 13.04 6.58 17.16 6.34 63.425* 59.161* 1.315

Others 7.71 6.52 13.21 6.45

Note: *, **, *** significant at 1%, 5%, 10% respectively.

129

ANOVA tests result reveals significant difference in disclosure score over both

years of the study. F- values are significant at 1% level of significance for all the

corporate attributes (sales, total assets, market capitalization, ROS, ROCE. RONW,

ROA, leverage, foreign activity, listing status and audit firm size). ANOVA test results in

table 6.1 also demonstrate significant differences among mean disclosure score of each

category of corporate attributes.

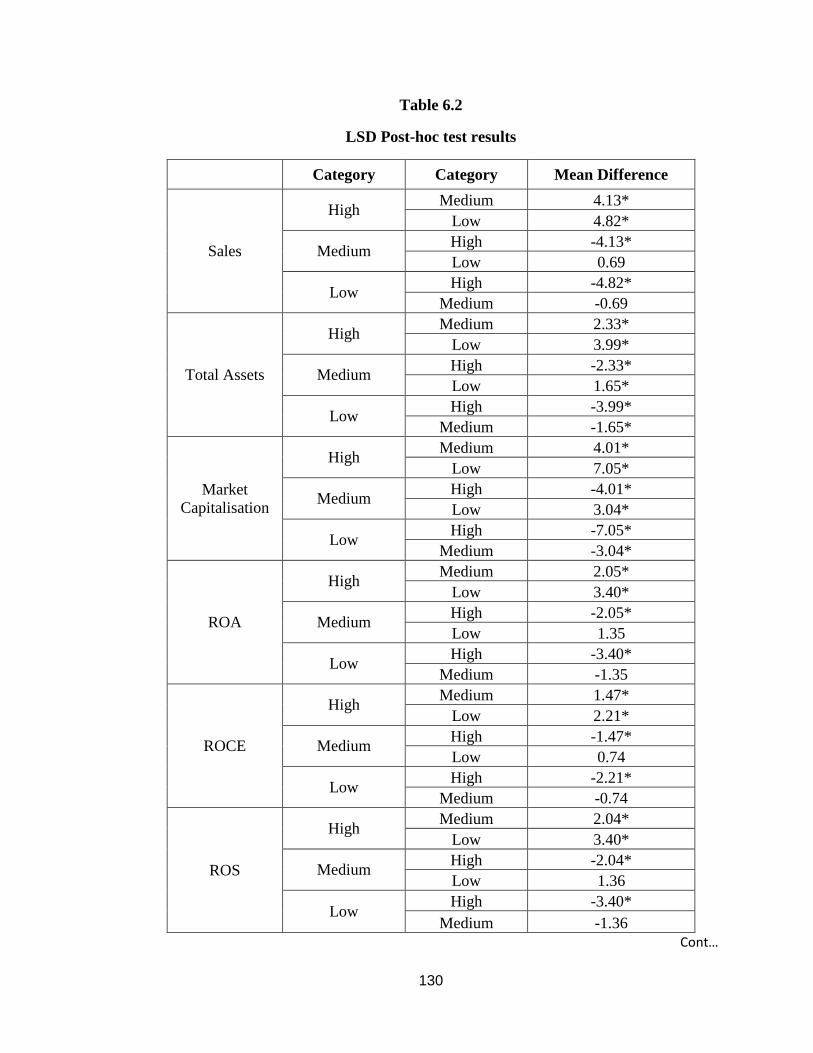

To find out which category differs significantly from others Fisher‟s LSD (Least

significant difference) post-hoc test was also conducted. Table 6.2 displays its results.

The Fisher LSD post-hoc test results on size of a firm measured by total sales

attribute reveal significant difference (at 1% level) between category high and category

medium & low. For size of the firm measured by total asset and market capitalization

attributes significant difference (at 1% level) was observed among all the three categories

(high, medium and low). This means firms with high sales, high total assets and high

market capitalization are reporting more on their intangible assets than firms with

medium and low sales, total assets and market capitalization.

In case of corporate attribute of profitability measured by ROS, ROA, ROCE and

RONW significant difference (1% level) was observed in mean disclosure score of

category high as compared to category medium and low. This reveals that companies

with high profitability disclose more about their intangible assets in their annual reports

than firms with medium and low profitability.

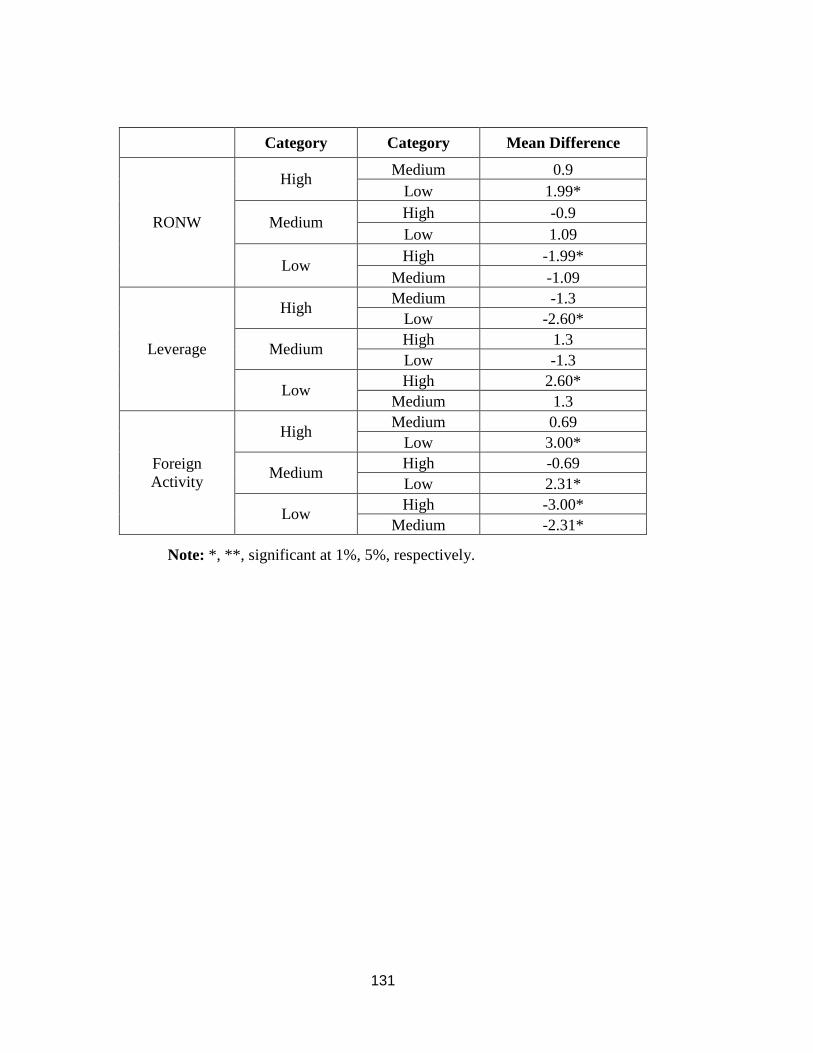

In case of corporate attribute of leverage, negative relationship can be seen

between high and medium & low categories. The negative association is significant (at

1% level) in case of high and low category. This means companies with high leverage

disclose less about their intangible assets. For corporate attribute of foreign activity,

significant positive relationship was observed among category high and medium with

category low. This reveals that companies with high level of foreign activity disclose

more about their intangible assets as compared to companies with low foreign activity.

130

Table 6.2

LSD Post-hoc test results

Category Category Mean Difference

Sales

High Medium 4.13*

Low 4.82*

Medium High -4.13*

Low 0.69

Low High -4.82*

Medium -0.69

Total Assets

High Medium 2.33*

Low 3.99*

Medium High -2.33*

Low 1.65*

Low High -3.99*

Medium -1.65*

Market

Capitalisation

High Medium 4.01*

Low 7.05*

Medium High -4.01*

Low 3.04*

Low High -7.05*

Medium -3.04*

ROA

High Medium 2.05*

Low 3.40*

Medium High -2.05*

Low 1.35

Low High -3.40*

Medium -1.35

ROCE

High Medium 1.47*

Low 2.21*

Medium High -1.47*

Low 0.74

Low High -2.21*

Medium -0.74

ROS

High Medium 2.04*

Low 3.40*

Medium High -2.04*

Low 1.36

Low High -3.40*

Medium -1.36

Cont…

131

Category Category Mean Difference

RONW

High Medium 0.9

Low 1.99*

Medium High -0.9

Low 1.09

Low High -1.99*

Medium -1.09

Leverage

High Medium -1.3

Low -2.60*

Medium High 1.3

Low -1.3

Low High 2.60*

Medium 1.3

Foreign

Activity

High Medium 0.69

Low 3.00*

Medium High -0.69

Low 2.31*

Low High -3.00*

Medium -2.31*

Note: *, **, significant at 1%, 5%, respectively.

132

6.2.2 Regression Analysis

Further, the detailed effect of different corporate attributes on the extent of

intangible assets disclosure has been studied with the help of regression analysis. For

regression analysis, it is essential to assess the validity of the Model (regression

equation).

Assessing the Validity of the Model (regression equation) is necessary to find out

the impact of various corporate-specific attributes on the disclosure practices of sample

Indian private sector companies for the financial years 2003-04 and 2007-08 respectively.

It is pre-emptive to check the existence of multicollinearity among the

explanatory independent variables before proceeding to the results of regression analysis.

Multicollinearity or collinearity is the situation where two or more independent variables

are highly correlated and can have damaging effects on the results of multiple regression.

The correlation matrix is a powerful tool for getting a rough idea of the relationship

between predictors. The suggested rule of thumb is that, if the pair-wise or zero-order

correlation coefficient between two regressors is high say, in excess of 0.8, then

multicollinearity is a serious problem (Gujarati, 2006, p.359). The solution to this

multicollinearity drawback is to drop that variable and thereafter run regression analysis

with rest of the variables. Another way to check the multicollinearity is to compute the

average VIF (Variance inflation factor). As a rule of thumb, if the average VIF of a

variable exceeds 1 which will happen if correlation coefficient exceeds 0.80, then that

variable is said to be highly collinear (Gujarati, 2006, p. 362).

6.2.2.1 Checking the Normality of Data

It was essential to check the distribution of independent and dependent variables.

Certain descriptives like skewness and kurtosis were calculated to test the normality of

data. The disclosure score is found to be within range of skewness (-1 to 1) and kurtosis

(-2 to 2) but the size of a firm measured in all explanatory variables is found to be not

normal. Thus, natural log transformation has been done to make it normal (see, for e.g.

Raffournier, 1995; Patton & Zelenka, 1997and Owusu-Ansah, 1998).

133

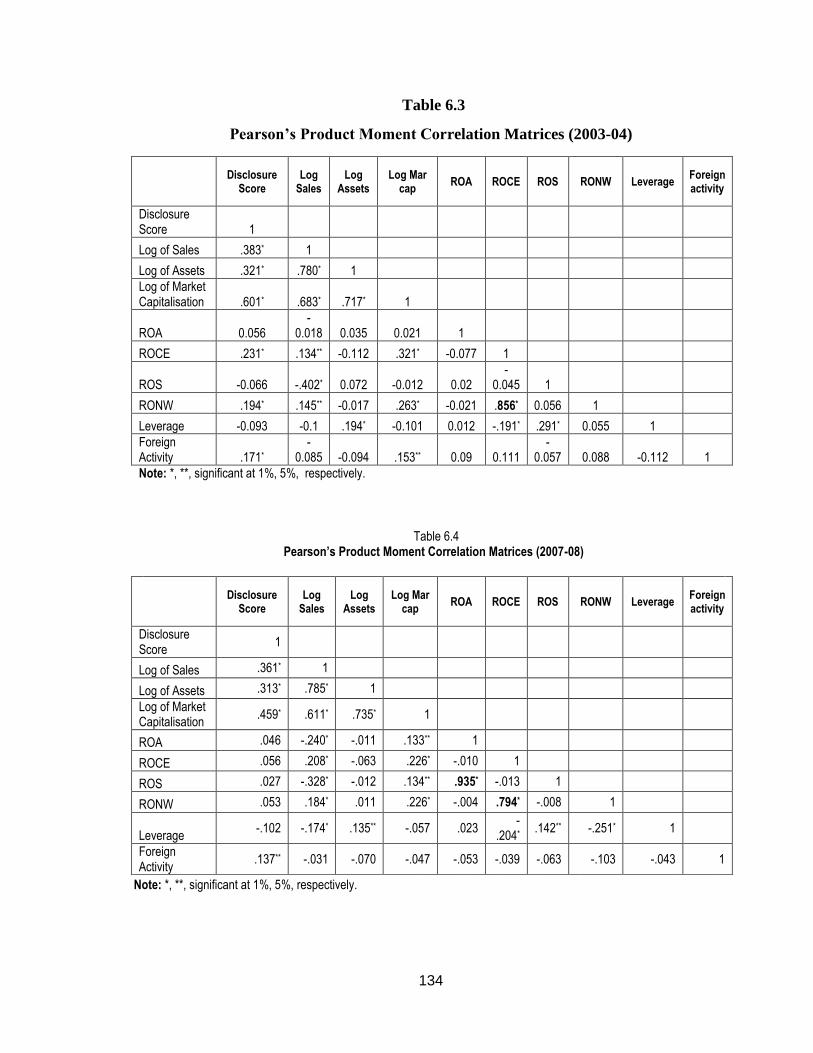

6.2.2.2 Correlation Analysis

The Pearson product moment correlation (r) was computed to examine the

correlation between the dependent and independent variables and with the dependent

variables. A correlation matrix of all the values of r for the explanatory variables along

with dependent variables was constructed and is shown in table 6.1 and table 6.2 for the

years 2003-04 and 2007-08 respectively.

Table 6.3 illustrates that multicollinearity is an issue of concern in the case of

measures of profitability of a firm i.e. between RONW and ROCE. RONW and ROCE

have coefficient of correlation (.856), above the rule of thumb (0.80), significant at 1%

level. Thus, the problem of multicollinearity exists only between these measures of

profitability for the financial year 2003-04. Rest of the variables do not have problem of

multicollinearity among them.

The results of table 6.4 bring to light that the problem of high value of correlation

coefficient appears in the case of measures of profitability for the year 2007-08. It was

found in the case of ROS and ROA (.935) and RONW and ROCE (.794) significant at

1% level. Thus the problem of multicollinearity exists among only these explanatory

variables. The problem was checked by taking only one measure of profitability in a

regression equation at a time. Rests of the variables do not have any problem of

multicollinearity among them for the year 2007-08.

134

Table 6.3

Pearson’s Product Moment Correlation Matrices (2003-04)

Disclosure

Score Log

Sales Log

Assets Log Mar

cap ROA ROCE ROS RONW Leverage

Foreign activity

Disclosure Score 1

Log of Sales .383* 1 Log of Assets .321* .780* 1

Log of Market Capitalisation .601* .683* .717* 1

ROA 0.056 -

0.018 0.035 0.021 1 ROCE .231* .134** -0.112 .321* -0.077 1

ROS -0.066 -.402* 0.072 -0.012 0.02 -

0.045 1 RONW .194* .145** -0.017 .263* -0.021 .856* 0.056 1

Leverage -0.093 -0.1 .194* -0.101 0.012 -.191* .291* 0.055 1 Foreign

Activity .171* -

0.085 -0.094 .153** 0.09 0.111 -

0.057 0.088 -0.112 1

Note: *, **, significant at 1%, 5%, respectively.

Table 6.4 Pearson’s Product Moment Correlation Matrices (2007-08)

Disclosure

Score Log

Sales Log

Assets Log Mar

cap ROA ROCE ROS RONW Leverage

Foreign activity

Disclosure Score

1

Log of Sales .361* 1

Log of Assets .313* .785* 1

Log of Market Capitalisation

.459* .611* .735* 1

ROA .046 -.240* -.011 .133** 1

ROCE .056 .208* -.063 .226* -.010 1

ROS .027 -.328* -.012 .134** .935* -.013 1

RONW .053 .184* .011 .226* -.004 .794* -.008 1

Leverage -.102 -.174* .135** -.057 .023

-.204*

.142** -.251* 1

Foreign Activity

.137** -.031 -.070 -.047 -.053 -.039 -.063 -.103 -.043 1

Note: *, **, significant at 1%, 5%, respectively.

135

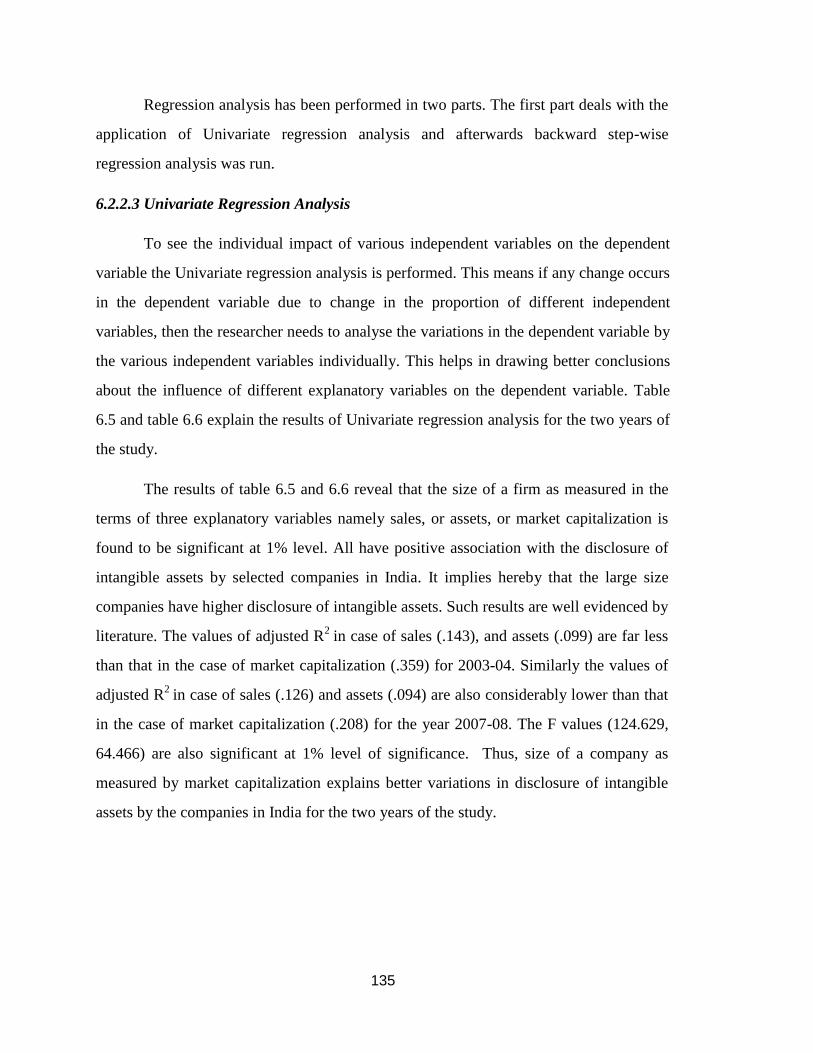

Regression analysis has been performed in two parts. The first part deals with the

application of Univariate regression analysis and afterwards backward step-wise

regression analysis was run.

6.2.2.3 Univariate Regression Analysis

To see the individual impact of various independent variables on the dependent

variable the Univariate regression analysis is performed. This means if any change occurs

in the dependent variable due to change in the proportion of different independent

variables, then the researcher needs to analyse the variations in the dependent variable by

the various independent variables individually. This helps in drawing better conclusions

about the influence of different explanatory variables on the dependent variable. Table

6.5 and table 6.6 explain the results of Univariate regression analysis for the two years of

the study.

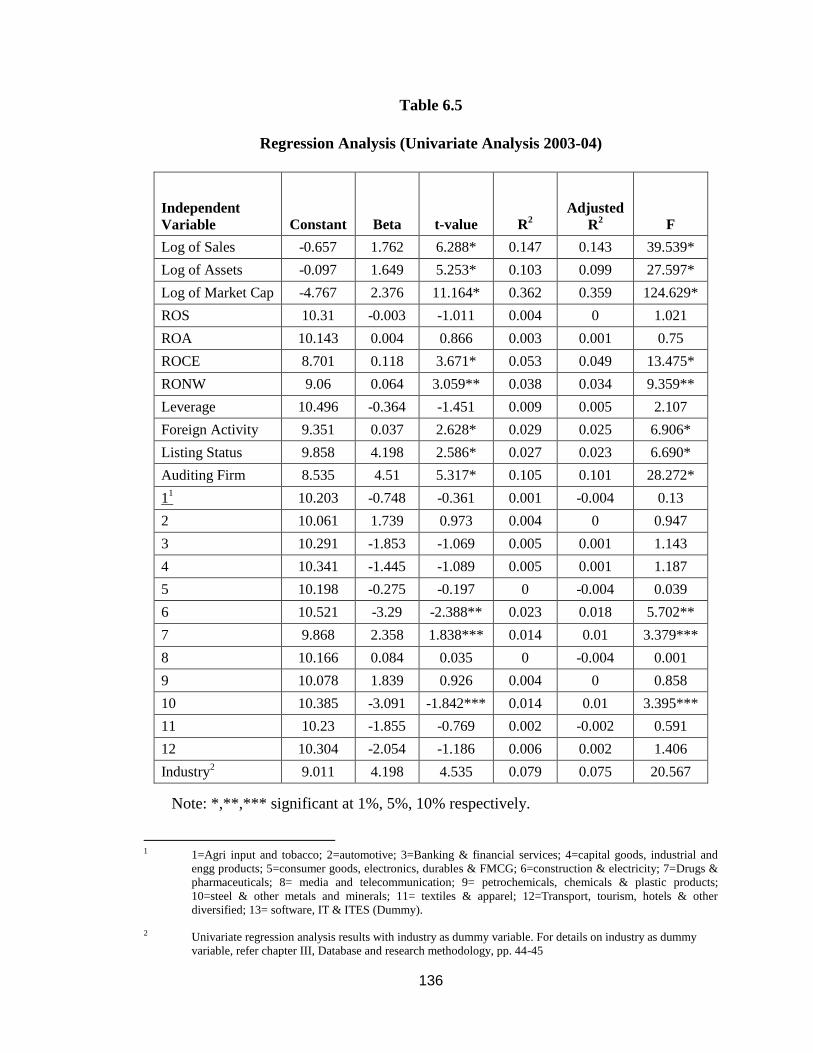

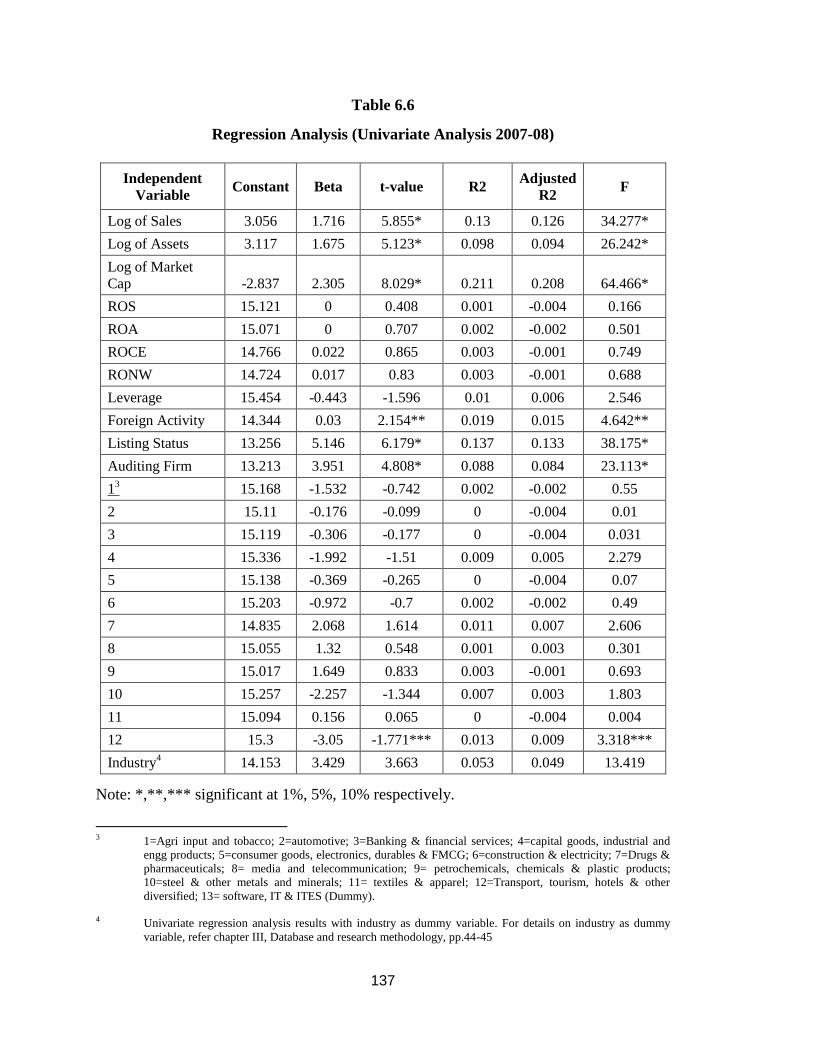

The results of table 6.5 and 6.6 reveal that the size of a firm as measured in the

terms of three explanatory variables namely sales, or assets, or market capitalization is

found to be significant at 1% level. All have positive association with the disclosure of

intangible assets by selected companies in India. It implies hereby that the large size

companies have higher disclosure of intangible assets. Such results are well evidenced by

literature. The values of adjusted R2

in case of sales (.143), and assets (.099) are far less

than that in the case of market capitalization (.359) for 2003-04. Similarly the values of

adjusted R2

in case of sales (.126) and assets (.094) are also considerably lower than that

in the case of market capitalization (.208) for the year 2007-08. The F values (124.629,

64.466) are also significant at 1% level of significance. Thus, size of a company as

measured by market capitalization explains better variations in disclosure of intangible

assets by the companies in India for the two years of the study.

136

Table 6.5

Regression Analysis (Univariate Analysis 2003-04)

Independent

Variable Constant Beta t-value R2

Adjusted

R2 F

Log of Sales -0.657 1.762 6.288* 0.147 0.143 39.539*

Log of Assets -0.097 1.649 5.253* 0.103 0.099 27.597*

Log of Market Cap -4.767 2.376 11.164* 0.362 0.359 124.629*

ROS 10.31 -0.003 -1.011 0.004 0 1.021

ROA 10.143 0.004 0.866 0.003 0.001 0.75

ROCE 8.701 0.118 3.671* 0.053 0.049 13.475*

RONW 9.06 0.064 3.059** 0.038 0.034 9.359**

Leverage 10.496 -0.364 -1.451 0.009 0.005 2.107

Foreign Activity 9.351 0.037 2.628* 0.029 0.025 6.906*

Listing Status 9.858 4.198 2.586* 0.027 0.023 6.690*

Auditing Firm 8.535 4.51 5.317* 0.105 0.101 28.272*

11 10.203 -0.748 -0.361 0.001 -0.004 0.13

2 10.061 1.739 0.973 0.004 0 0.947

3 10.291 -1.853 -1.069 0.005 0.001 1.143

4 10.341 -1.445 -1.089 0.005 0.001 1.187

5 10.198 -0.275 -0.197 0 -0.004 0.039

6 10.521 -3.29 -2.388** 0.023 0.018 5.702**

7 9.868 2.358 1.838*** 0.014 0.01 3.379***

8 10.166 0.084 0.035 0 -0.004 0.001

9 10.078 1.839 0.926 0.004 0 0.858

10 10.385 -3.091 -1.842*** 0.014 0.01 3.395***

11 10.23 -1.855 -0.769 0.002 -0.002 0.591

12 10.304 -2.054 -1.186 0.006 0.002 1.406

Industry2 9.011 4.198 4.535 0.079 0.075 20.567

Note: *,**,*** significant at 1%, 5%, 10% respectively.

1 1=Agri input and tobacco; 2=automotive; 3=Banking & financial services; 4=capital goods, industrial and

engg products; 5=consumer goods, electronics, durables & FMCG; 6=construction & electricity; 7=Drugs &

pharmaceuticals; 8= media and telecommunication; 9= petrochemicals, chemicals & plastic products;

10=steel & other metals and minerals; 11= textiles & apparel; 12=Transport, tourism, hotels & other

diversified; 13= software, IT & ITES (Dummy).

2 Univariate regression analysis results with industry as dummy variable. For details on industry as dummy

variable, refer chapter III, Database and research methodology, pp. 44-45

137

Table 6.6

Regression Analysis (Univariate Analysis 2007-08)

Independent

Variable Constant Beta t-value R2

Adjusted

R2 F

Log of Sales 3.056 1.716 5.855* 0.13 0.126 34.277*

Log of Assets 3.117 1.675 5.123* 0.098 0.094 26.242*

Log of Market

Cap -2.837 2.305 8.029* 0.211 0.208 64.466*

ROS 15.121 0 0.408 0.001 -0.004 0.166

ROA 15.071 0 0.707 0.002 -0.002 0.501

ROCE 14.766 0.022 0.865 0.003 -0.001 0.749

RONW 14.724 0.017 0.83 0.003 -0.001 0.688

Leverage 15.454 -0.443 -1.596 0.01 0.006 2.546

Foreign Activity 14.344 0.03 2.154** 0.019 0.015 4.642**

Listing Status 13.256 5.146 6.179* 0.137 0.133 38.175*

Auditing Firm 13.213 3.951 4.808* 0.088 0.084 23.113*

13 15.168 -1.532 -0.742 0.002 -0.002 0.55

2 15.11 -0.176 -0.099 0 -0.004 0.01

3 15.119 -0.306 -0.177 0 -0.004 0.031

4 15.336 -1.992 -1.51 0.009 0.005 2.279

5 15.138 -0.369 -0.265 0 -0.004 0.07

6 15.203 -0.972 -0.7 0.002 -0.002 0.49

7 14.835 2.068 1.614 0.011 0.007 2.606

8 15.055 1.32 0.548 0.001 0.003 0.301

9 15.017 1.649 0.833 0.003 -0.001 0.693

10 15.257 -2.257 -1.344 0.007 0.003 1.803

11 15.094 0.156 0.065 0 -0.004 0.004

12 15.3 -3.05 -1.771*** 0.013 0.009 3.318***

Industry4 14.153 3.429 3.663 0.053 0.049 13.419

Note: *,**,*** significant at 1%, 5%, 10% respectively.

3 1=Agri input and tobacco; 2=automotive; 3=Banking & financial services; 4=capital goods, industrial and

engg products; 5=consumer goods, electronics, durables & FMCG; 6=construction & electricity; 7=Drugs &

pharmaceuticals; 8= media and telecommunication; 9= petrochemicals, chemicals & plastic products;

10=steel & other metals and minerals; 11= textiles & apparel; 12=Transport, tourism, hotels & other

diversified; 13= software, IT & ITES (Dummy).

4 Univariate regression analysis results with industry as dummy variable. For details on industry as dummy

variable, refer chapter III, Database and research methodology, pp.44-45

138

The profitability of a firm is found to have positive and significant association

with disclosure score when measured in the terms of ROCE and RONW for the year

2003-04. It is positively associated in the terms of ROA for the year 2003-04 and ROS,

ROA, ROCE and RONW for the year 2007-08. But a negative association has been

found in the case of profitability of a firm measured in the terms of ROS for the year

2003-04. Hence, no conclusive result could be found out and is advocated by the

literature. However, profitability of a company as measured by ROCE has a positive

effect on disclosure score for the two years of the study. The value of adjusted R2 of

ROCE (.049) is more than RONW (.034) with F value (13.475) significant at 1% level

for the year 2003-04 implying hereby that ROCE is a better indicator of overall

profitability position of a firm. It means that the more profitable firms will disclose more

information.

The results of table 6.5 and 6.6 show, that the audit firm size and listing category

of a firm have positive association with the disclosure scores at 1% level of significance.

It implies hereby that the firms being audited by big-six audit firms and listed as A

category in the Indian stock exchanges have more extent of intangible assets disclosure.

The level of foreign activity of a firm is also found to have positive association with

disclosure score at 1% and 5% level of significance for the years 2003-04 and 2007-08

respectively. It shows that the firms having high exports disclose more information about

their intangible assets to their investors. Leverage of a firm was found to be negatively

associated with its intangible assets disclosure score for both years of the study. Thus the

firms with high debt in their capital structure disclose less on their intangible assets.

The nature of industry influences the intangible assets disclosure level of selected

companies in India. As per the first approach5, except construction, pharmaceutical and

steel industry for the year 2003-04 and transport industry for the year 2007-08, others

industrial sectors could not significantly influence the disclosure score individually. The

pharmaceutical industry has more extent of intangible assets disclosure while

construction, steel and transport industry has less extent of disclosure as compared to

software industry. But these sectors significantly influence the variations in the

intangible assets disclosure score for two years of the study. The second approach also

shows industry to be significant attribute (at 1% level of significance) that has an impact

on the level of intangible asset reporting by companies.

5 Industry attribute has been studied under two approaches. For more details refer Chapter III, Database and

Research Methodology, pp.44-45

139

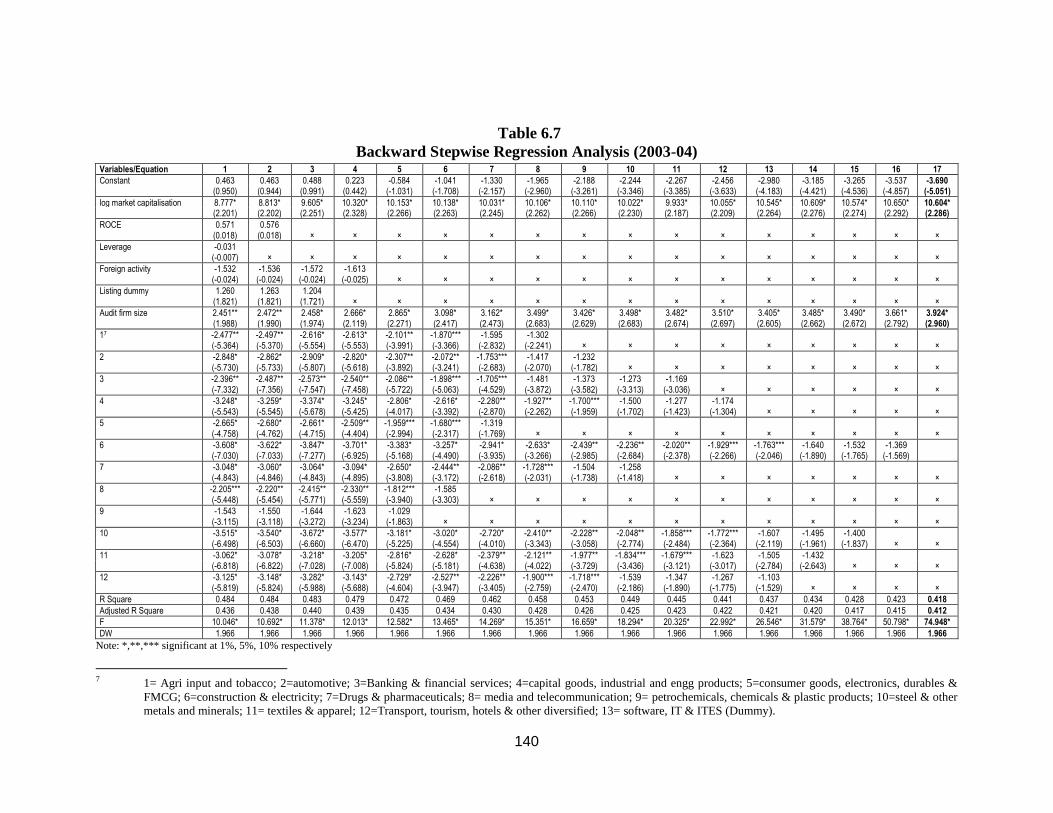

6.2.2.4. Backward Step-wise Regression Analysis

The regression equation analysing the impact of various corporate specific

attributes on the intangible assets disclosure score for two years of the study can be

framed as follows:

Y = β0 +β1X1 +β2 X2 +β3 X3 +β4 X4 +β5 X5 +β6 X6 +β7-18 X7-18+ ε

Where Y = Disclosure score;

X1 = Size of a firm (log of market capitalization);

X2 = Profitability of a firm (ROCE);

X3 = Leverage of a firm;

X4 = Foreign Activity;

X5 = Listing category of a firm;

X6 = Audit firm size of a firm;

X7-18 = Industry type6;

β = Slopes of the independent variables while β0 is a constant or

the value of Y when all values of X are zero;

ε = εt ~ (0, N).

Initially, multivariate regression was performed by taking into consideration all

independent variables hypothesised to have association with the disclosure score. This

could not reveal any conclusive result. Afterwards backward stepwise regression analysis

was run. It appears to be the preferred method of exploratory analyses where the analysis

begins with a full or saturated model and variables are eliminated from the model in an

iterative process. The fit of the model is tested after the elimination of each variable to

ensure that the model still adequately fits the data. The analysis is complete when no

more variables could be eliminated from the model.

The results of backward step-wise regression analysis results for the year 2003-04

and 2007-08, including the adjusted R2, F-statistic values and significant corporate

attributes, of all regression equations has been shown in table 6.7 and 6.8 respectively.

6 1=Agri input and tobacco; 2=automotive; 3=Banking & financial services; 4=capital goods, industrial and

engg products; 5=consumer goods, electronics, durables & FMCG; 6=construction & electricity; 7=Drugs &

pharmaceuticals; 8= media and telecommunication; 9= petrochemicals, chemicals & plastic products;

10=steel & other metals and minerals; 11= textiles & apparel; 12=Transport, tourism, hotels & other

diversified; 13= software, IT & ITES (Dummy).

140

Table 6.7

Backward Stepwise Regression Analysis (2003-04) Variables/Equation 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

Constant 0.463 0.463 0.488 0.223 -0.584 -1.041 -1.330 -1.965 -2.188 -2.244 -2.267 -2.456 -2.980 -3.185 -3.265 -3.537 -3.690 (0.950) (0.944) (0.991) (0.442) (-1.031) (-1.708) (-2.157) (-2.960) (-3.261) (-3.346) (-3.385) (-3.633) (-4.183) (-4.421) (-4.536) (-4.857) (-5.051)

log market capitalisation 8.777* 8.813* 9.605* 10.320* 10.153* 10.138* 10.031* 10.106* 10.110* 10.022* 9.933* 10.055* 10.545* 10.609* 10.574* 10.650* 10.604* (2.201) (2.202) (2.251) (2.328) (2.266) (2.263) (2.245) (2.262) (2.266) (2.230) (2.187) (2.209) (2.264) (2.276) (2.274) (2.292) (2.286)

ROCE 0.571 0.576

(0.018) (0.018) × × × × × × × × × × × × × × ×

Leverage -0.031

(-0.007) × × × × × × × × × × × × × × × ×

Foreign activity -1.532 -1.536 -1.572 -1.613

(-0.024) (-0.024) (-0.024) (-0.025) × × × × × × × × × × × × ×

Listing dummy 1.260 1.263 1.204

(1.821) (1.821) (1.721) × × × × × × × × × × × × × ×

Audit firm size 2.451** 2.472** 2.458* 2.666* 2.865* 3.098* 3.162* 3.499* 3.426* 3.498* 3.482* 3.510* 3.405* 3.485* 3.490* 3.661* 3.924* (1.988) (1.990) (1.974) (2.119) (2.271) (2.417) (2.473) (2.683) (2.629) (2.683) (2.674) (2.697) (2.605) (2.662) (2.672) (2.792) (2.960)

17 -2.477** -2.497** -2.616* -2.613* -2.101** -1.870*** -1.595 -1.302

(-5.364) (-5.370) (-5.554) (-5.553) (-3.991) (-3.366) (-2.832) (-2.241) × × × × × × × × ×

2 -2.848* -2.862* -2.909* -2.820* -2.307** -2.072** -1.753*** -1.417 -1.232

(-5.730) (-5.733) (-5.807) (-5.618) (-3.892) (-3.241) (-2.683) (-2.070) (-1.782) × × × × × × × ×

3 -2.396** -2.487** -2.573** -2.540** -2.086** -1.898*** -1.705*** -1.481 -1.373 -1.273 -1.169

(-7.332) (-7.356) (-7.547) (-7.458) (-5.722) (-5.063) (-4.529) (-3.872) (-3.582) (-3.313) (-3.036) × × × × × ×

4 -3.248* -3.259* -3.374* -3.245* -2.806* -2.616* -2.280** -1.927** -1.700*** -1.500 -1.277 -1.174

(-5.543) (-5.545) (-5.678) (-5.425) (-4.017) (-3.392) (-2.870) (-2.262) (-1.959) (-1.702) (-1.423) (-1.304) × × × × ×

5 -2.665* -2.680* -2.661* -2.509** -1.959*** -1.680*** -1.319

(-4.758) (-4.762) (-4.715) (-4.404) (-2.994) (-2.317) (-1.769) × × × × × × × × × ×

6 -3.608* -3.622* -3.847* -3.701* -3.383* -3.257* -2.941* -2.633* -2.439** -2.236** -2.020** -1.929*** -1.763*** -1.640 -1.532 -1.369 (-7.030) (-7.033) (-7.277) (-6.925) (-5.168) (-4.490) (-3.935) (-3.266) (-2.985) (-2.684) (-2.378) (-2.266) (-2.046) (-1.890) (-1.765) (-1.569) 7 -3.048* -3.060* -3.064* -3.094* -2.650* -2.444** -2.086** -1.728*** -1.504 -1.258

(-4.843) (-4.846) (-4.843) (-4.895) (-3.808) (-3.172) (-2.618) (-2.031) (-1.738) (-1.418) × × × × × × ×

8 -2.205*** -2.220** -2.415** -2.330** -1.812*** -1.585

(-5.448) (-5.454) (-5.771) (-5.559) (-3.940) (-3.303) × × × × × × × × × × ×

9 -1.543 -1.550 -1.644 -1.623 -1.029

(-3.115) (-3.118) (-3.272) (-3.234) (-1.863) × × × × × × × × × × × ×

10 -3.515* -3.540* -3.672* -3.577* -3.181* -3.020* -2.720* -2.410** -2.228** -2.048** -1.858*** -1.772*** -1.607 -1.495 -1.400 (-6.498) (-6.503) (-6.660) (-6.470) (-5.225) (-4.554) (-4.010) (-3.343) (-3.058) (-2.774) (-2.484) (-2.364) (-2.119) (-1.961) (-1.837) × ×

11 -3.062* -3.078* -3.218* -3.205* -2.816* -2.628* -2.379** -2.121** -1.977** -1.834*** -1.679*** -1.623 -1.505 -1.432 (-6.818) (-6.822) (-7.028) (-7.008) (-5.824) (-5.181) (-4.638) (-4.022) (-3.729) (-3.436) (-3.121) (-3.017) (-2.784) (-2.643) × × ×

12 -3.125* -3.148* -3.282* -3.143* -2.729* -2.527** -2.226** -1.900*** -1.718*** -1.539 -1.347 -1.267 -1.103 (-5.819) (-5.824) (-5.988) (-5.688) (-4.604) (-3.947) (-3.405) (-2.759) (-2.470) (-2.186) (-1.890) (-1.775) (-1.529) × × × ×

R Square 0.484 0.484 0.483 0.479 0.472 0.469 0.462 0.458 0.453 0.449 0.445 0.441 0.437 0.434 0.428 0.423 0.418

Adjusted R Square 0.436 0.438 0.440 0.439 0.435 0.434 0.430 0.428 0.426 0.425 0.423 0.422 0.421 0.420 0.417 0.415 0.412

F 10.046* 10.692* 11.378* 12.013* 12.582* 13.465* 14.269* 15.351* 16.659* 18.294* 20.325* 22.992* 26.546* 31.579* 38.764* 50.798* 74.948*

DW 1.966 1.966 1.966 1.966 1.966 1.966 1.966 1.966 1.966 1.966 1.966 1.966 1.966 1.966 1.966 1.966 1.966

Note: *,**,*** significant at 1%, 5%, 10% respectively

7 1= Agri input and tobacco; 2=automotive; 3=Banking & financial services; 4=capital goods, industrial and engg products; 5=consumer goods, electronics, durables &

FMCG; 6=construction & electricity; 7=Drugs & pharmaceuticals; 8= media and telecommunication; 9= petrochemicals, chemicals & plastic products; 10=steel & other

metals and minerals; 11= textiles & apparel; 12=Transport, tourism, hotels & other diversified; 13= software, IT & ITES (Dummy).

141

Seventeen cross-sectional regression equations have been framed for the

financial year 2003-04 for the final analysis. The result of the multivariate regression

analysis (first regression equation) shows the R2 at 0.484. It signifies that 48.4%

variation in model is explained by all independent variables jointly. The adjusted R2

(.436) states that 43.6% variation in the disclosure score is explained by variations in

independent variables. The variables namely size of a company (positive at 1% level

of significance), audit firm size (positive at 5% level) and nature of industry

(automotive industry, capital goods industry, consumer goods industry, construction

industry, pharmaceuticals industry, steel industry, textiles industry and transport

industry at 1% level of significance; agri input industry, banking industry at 5% level

of significance; and media and telecommunication industry at 10% level of

significance) influence the disclosure of intangible assets. Rest of the variables could

not significantly influence the disclosure score. The value of F (10.046) is significant

at 1% level which shows the fitness of the model. The importance of good regression

equation lies in the fact that the model is correctly specified. The regressors have the

correct (i.e., theoretically expected) signs and that (hopefully) the regression

coefficients are statistically significant at lowest possible level (one or five percent) of

significance (Gujarati, 2006, p.260). Therefore, variables were removed one by one

and afterwards the model having highest adjusted R2, signs of independent variables

(moving in expected directions) and significant at the lowest possible level of

significant has been chosen for two years of the study.

The cross sectional regression equation namely 17 in table 6.7 has been

selected for the final analysis. The results of the backward step-wise regression

analysis explain that the regressors namely size of a firm (positive at 1% level of

significance) and audit firm size (positive at 1% level of significance), when

regressed jointly explain 41.2% variations in the disclosure score. The F value

(74.948) is significant at 1% level explains that model is best fit. All independent

variables move in the expected directions. It shows that the size of a firm and audit

firm size are found to be significantly affecting the disclosure of intangible assets in

the companies in India and is in predicted direction. The final model has been

selected on the basis of lowest possible level of significance of regressors with

predicted directions and highest adjusted R2

and F value.

142

Table 6.8

Backward Stepwise Regression Analysis (2007-08) Variables/Equation 1 2 3 4 5 6 7 8 9 10 11 12

Constant -0.384 -0.386 -0.406 -0.668 -0.910 -1.044 -0.954 -1.039 -1.195 -1.344 -1.481 -1.611 (-1.381) (-1.367) (-1.040) (-1.562) (-2.045) (-2.323) (-2.108) (-2.291) (-2.604) (-2.918) (-3.203) (-3.476) log market capitalisation 5.617* 5.660* 8.684* 8.698* 8.717* 8.672* 8.752* 8.671* 8.641* 8.614* 8.544* 8.572* (2.631) (2.630) (2.582) (2.565) (2.568) (2.545) (2.481) (2.433) (2.421) (2.418) (2.398) (2.410) ROCE -1.105 -1.128 -1.127 -1.080 -0.969 -0.851 (-0.027) (-0.027) (-0.027) (-0.025) (0.022) (-0.020) × × × × × × Leverage 0.024 (0.007) × × × × × × × × × × × Foreign activity -0.495 -0.496 -0.500 (-0.008) (-0.008) (-0.008) × × ×× × × × × × × Listing dummy -0.136 -0.134 (-0.169) (-0.166) × × × × × × × × × × Audit firm size 2.576** 2.616* 2.619* 2.697* 2.784* 2.883* 2.927* 3.163* 3.150* 3.206* 3.507* 3.495* (2.058) (2.054) (2.048) (2.092) (2.148) (2.214) (2.244) (2.392) (2.381) (2.426) (2.611) (2.606) 18 -2.302** -2.312** -2.341** -2.369** -2.252** -2.103** -2.083** -1.879*** -1.707*** -1.541 -1.367 (-5.187) (-5.183) (-5.212) (-4.717) (-4.316) (-3.933) (-3.891) (-3.433) (-3.026) (-2.713) (-2.386) × 2 -2.047** -2.056** -2.071** -2.109** -1.977** -1.808*** -1.801*** -1.566 -1.365 (-4.293) (-4.289) (-4.306) (-3.782) (-3.387) (-3.005) (-2.991) (-2.522) (-2.114) × × × 3 -3.079* -3.274* -3.278* -3.575* -3.511* -3.388* -3.337* -3.141* -3.002* -2.823* -2.626* -2.513** (-7.087) (-7.068) (-7.053) (-6.474) (-6.077) (-5.665) (-5.561) (-5.039) (-4.619) (-4.300) (-3.941) (-3.764) 4 -3.094* -3.101* -3.115* -3.380* -3.318* -3.188* -3.394* -3.193* -3.064* -2.849* -2.624* -2.472** (-5.483) (-5.483) (-5.492) (-5.018) (-4.657) (-4.309) (-4.511) (-4.048) (-3.640) (-3.327) (-2.998) (-2.809) 5 -2.132** -2.138** -2.163** -2.244** -2.116** -1.937*** -2.038*** -1.766*** -1.548 -1.312 (-3.969) (-3.967) (-3.990) (-3.499) (-3.115) (-2.739) (-2.865) (-2.359) (-1.952) (-1.627) × × 6 -3.164* -3.177* -3.192* -3.632* -3.587* -3.470* -3.476* -3.278* -3.150* -2.942* -2.705* -2.569** (-6.380) (-6.377) (-6.388) (-5.784) (-5.390) (-4.986) (-4.992) (-4.455) (-4.041) (-3.714) (-3.325) (-3.146) 7 -1.645 -1.650*** -1.669*** -1.598 -1.427 -1.209 -1.233 -0.925 (-2.594) (-2.592) (-2.608) (-2.328) (-1.948) (-1.577) (-1.607) (-1.148) × × × × 8 -1.128 -1.158 -1.189 -1.080 -0.922 (-2.925) (-2.938) (-2.982) (-2.450) (-2.024) × × × × × × × 9 -1.578 -1.582 -1.589 -1.520 -1.368 -1.185 -1.149 (-3.448) (-3.445) (-3.451) (-3.001) (-2.595) (-2.185) (-2.116) × × × × × 10 -3.385* -3.393* -3.405* -3.545* -3.484* -3.360* -3.347* -3.148* -3.010* -2.823* -2.607* -2.488** (-6.753) (-6.752) (-6.759) (-6.327) (-5.922) (-5.512) (-5.485) (-4.949) (-4.538) (-4.209) (-3.811) (-3.630) 11 -0.856 -0.864 -0.864 -0.753 (-2.065) (-2.056) (-2.052) (-1.708) × × × × × × × × 12 -3.414* -3.426* -3.445* -3.565* -3.506* -3.384* -3.338* -3.141* -3.003* -2.820* -2.610* -2.491** (-6.865) (-6.862) (-6.876) (-6.461) (-6.043) (-5.629) (-5.536) (-5.016) (-4.609) (-4.281) (-3.892) (-3.707) R Square 0.356 0.356 0.356 0.355 0.353 0.351 0.349 0.345 0.343 0.338 0.333 0.327 Adjusted R Square 0.304 0.307 0.310 0.312 0.314 0.314 0.315 0.314 0.314 0.312 0.310 0.307 F 6.873* 7.310* 7.799* 8.330* 8.901* 9.527* 10.273* 11.071* 12.100* 13.189* 14.578* 16.333* DW 2.154 2.154 2.154 2.154 2.154 2.154 2.154 2.154 2.154 2.154 2.154 2.154

Note: *,**,*** significant at 1%, 5%, 10% respectively

8 1= Agri input and tobacco; 2=automotive; 3=Banking & financial services; 4=capital goods, industrial and engg products; 5=consumer goods, electronics, durables &

FMCG; 6=construction & electricity; 7=Drugs & pharmaceuticals; 8= media and telecommunication; 9= petrochemicals, chemicals & plastic products; 10=steel & other

metals and minerals; 11= textiles & apparel; 12=Transport, tourism, hotels & other diversified; 13= software, IT & ITES (Dummy).

143

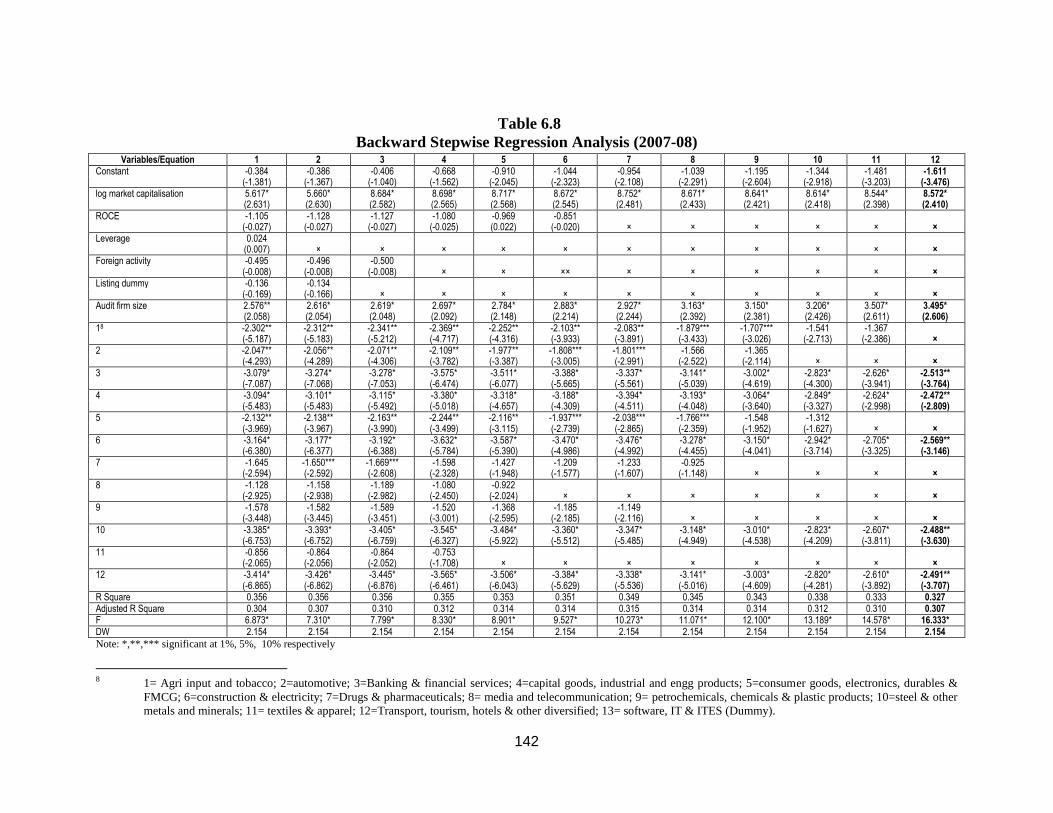

Table 6.8 shows that twelve cross-sectional regression equations have been

framed for the financial year 2007-08 for the final analysis. The result of the multivariate

regression analysis (first regression equation) shows the R2

at 0.356. It reveals that 35.6%

variation in model is explained by all independent variables jointly. The adjusted R2

(.304) shows that 30.4% variation in disclosure score is explained by all independent

variables. The size of a company (positive at 1 % level of significance), audit firm size

(positive at 5 % level of significance) and nature of industry (banking industry, capital

goods industry, construction industry, steel industry and transport industry at 1% level of

significance; agri input and tobacco industry, automotive industry and consumer goods

industry at 5% level of significance) influence the disclosure score. Rest of the variables

could not significantly influence the disclosure score. The value of F (6.873) is

significant at 1% level which shows the fitness of the model. Afterwards, variables were

removed one by one to see the impact of independent variables on disclosure score to get

the best-fit model.

Following the statement by Gujarati (2006; p.260) the regression equation 12 has

been chosen for the final analysis. The selected regression equation in table 6.6

approximates the value for adjusted R2 (0.307) explains hereby that 30.7 % variations in

intangible assets disclosure score is explained by attributes namely size, industry type and

audit firm size of a company.

The size and audit firm size of a firm is significant (positive at 1% level of

significance) and nature of industry (Banking industry, capital goods industry,

construction industry, steel industry and transport industry) is negative at 5% level of

significance. Since software, IT and ITES industry has been used as a dummy so the

negative values of banking, capital goods, construction, steel and transport industry

reveals that these industries are disclosing less in comparison to software, IT and ITES

industry. The value of F (16.333) is significant at 1% level indicates that the model is

best-fit model.

Additionally, to test the assumption of independent errors (autocorrelation), the

Durbin-Watson statistic was used. The value of this statistic between 1.5 and 2.5 is

considered as better and for this data the value is 1.966 for the year 2003-04 and 2.154 for

the year 2007-08. Hence, the assumption has almost been accomplished. In sum, the

diagnostics indicate the model to be valid and reliable.

144

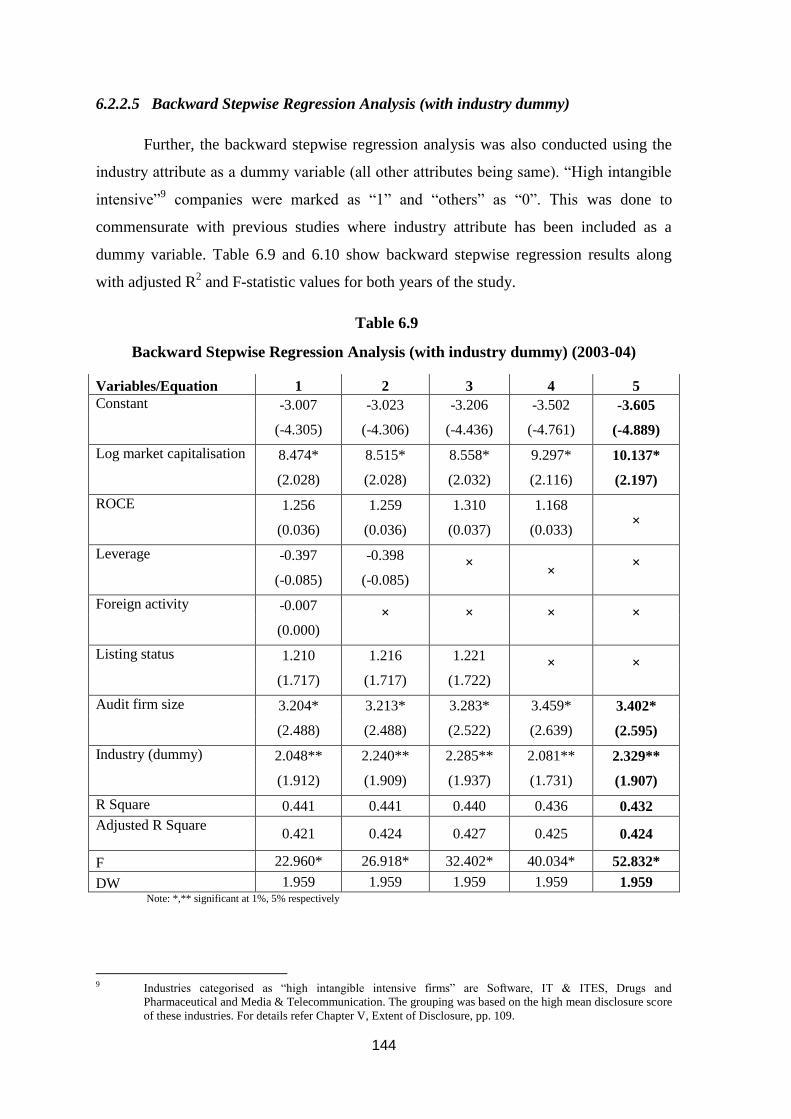

6.2.2.5 Backward Stepwise Regression Analysis (with industry dummy)

Further, the backward stepwise regression analysis was also conducted using the

industry attribute as a dummy variable (all other attributes being same). “High intangible

intensive”9 companies were marked as “1” and “others” as “0”. This was done to

commensurate with previous studies where industry attribute has been included as a

dummy variable. Table 6.9 and 6.10 show backward stepwise regression results along

with adjusted R2 and F-statistic values for both years of the study.

Table 6.9

Backward Stepwise Regression Analysis (with industry dummy) (2003-04)

Variables/Equation 1 2 3 4 5

Constant

-3.007 -3.023 -3.206 -3.502 -3.605

(-4.305) (-4.306) (-4.436) (-4.761) (-4.889)

Log market capitalisation

8.474* 8.515* 8.558* 9.297* 10.137*

(2.028) (2.028) (2.032) (2.116) (2.197)

ROCE

1.256 1.259 1.310 1.168

× (0.036) (0.036) (0.037) (0.033)

Leverage

-0.397 -0.398

× ×

×

(-0.085) (-0.085)

Foreign activity

-0.007

× × × ×

(0.000)

Listing status

1.210 1.216 1.221

× ×

(1.717) (1.717) (1.722)

Audit firm size

3.204* 3.213* 3.283* 3.459* 3.402*

(2.488) (2.488) (2.522) (2.639) (2.595)

Industry (dummy)

2.048** 2.240** 2.285** 2.081** 2.329**

(1.912) (1.909) (1.937) (1.731) (1.907)

R Square 0.441 0.441 0.440 0.436 0.432

Adjusted R Square 0.421 0.424 0.427 0.425 0.424

F 22.960* 26.918* 32.402* 40.034* 52.832*

DW 1.959 1.959 1.959 1.959 1.959 Note: *,** significant at 1%, 5% respectively

9 Industries categorised as “high intangible intensive firms” are Software, IT & ITES, Drugs and

Pharmaceutical and Media & Telecommunication. The grouping was based on the high mean disclosure score

of these industries. For details refer Chapter V, Extent of Disclosure, pp. 109.

145

Table 6.9 shows, five cross-sectional regression equations which have been framed

for the financial year 2003-04. Results of the fifth (final) regression equation show that the

regressors namely size of a firm (positive at 1% level of significance), audit firm size

(positive at 1% level of significance) and nature of industry (positive at 5% level of

significance) when regressed jointly explain 42.4% variations in the disclosure score. The

value of adjusted R2 has slightly improved as compared to the previous model (model with

13 categories of industry explained above). Thus the inclusion of industry as dummy variable

barely contributed to the explanatory power of the model.

The F value of 52.832 is significant at 1% level explains that model is best fit.

The value of Durbin-Watson statistic (1.959) is also within the acceptable limits.

Table 6.10

Backward Stepwise Regression Analysis (with industry dummy) (2007-08)

Variables/Equation 1 2 3 4 5

Constant -1.698 -2.278 -2.348 -2.314 -2.255

(-5.369) (-5.043) (-5.117) (-5.013) (-4.867)

Log market

capitalisation

5.391* 8.360* 8.380* 8.403* 8.428*

(2.402) (2.352) (2.352) (2.355) (2.298)

ROCE -0.886 -0.883 -0.862 -0.887 × (-0.020) (-0.020) (-0.019) (-0.020)

Leverage -0.204 -0.204

×

×

× (-0.050) (-0.050)

Foreign activity 0.518 0.524 0.514

×

× (0.007) (0.007) (0.007)

Listing status -0.145 ×

×

×

× (-0.176)

Audit firm size 3.188* 3.191* 3.247* 3.232* 3.267*

(2.423) (2.419) (2.438) (2.420) (2.444)

Industry dummy 3.103* 3.106* 3.201* 4.033* 4.014*

(3.081) (3.073) (3.110) (3.364) (3.346)

R Square 0.319 0.319 0.319 0.318 0.316

Adjusted R Square 0.299 0.302 0.305 0.307 0.307

F 15.736 18.432 22.200 27.770 36.797

DW 2.157 2.157 2.157 2.157 2.157

Note: *,** significant at 1%, 5% respectively

For the year 2007-08, the final regression equation showed size of the firm

(positive at 1% level of significance), audit firm size (positive at 1% level of significance)

and industry (positive at 1% level of significance) affects the level of disclosure (Table

6.10). The value for adjusted R2 (0.307) explains hereby that 30.7 % variations in

146

disclosure score is explained by attributes namely size of a company, industry type and

audit firm size. The value of adjusted R2,

for the year 2007-08, remained same as in case

of previous model.

F-value (36.797) is also significant at 1% level of significance. The value of

Durbin-Watson statistic (2.157) is also within the acceptable limits.

6.2.6 Testing the Hypotheses

The two-factor ANOVA, Univariate and backward step-wise regression analysis

have been run to test the underlined null and alternate hypotheses.

H01: The size of a company as measured by its total assets or total sales or total

market capitalization has no significant impact on its intangible assets

disclosure score.

H1: The size of a company as measured by its total assets or total sales or total

market capitalization has a significant impact on its intangible assets

disclosure score.

The results from two-factor ANOVA, univariate and backward stepwise

regression analysis reveal that there exists positive and significant relationship between

size of a company measured in terms of market capitalisation and intangible assets

disclosure level. So, this study corroborates the past research in Italy (Bozzolan et al,

2003, 2006), Spain (Meca and Martinez, 2005), Portugal (Oliveira et al, 2006), Australia

(Guthrie et al, 2006; White et al 2007) and Hong Kong (Carlin et al, 2006) where a

positive relationship between size of a firm and extent of intangible assets disclosure was

found. The reasons might be that the large companies are more in the public and

government limelight. Companies with higher market capitalisation tend to disclose more

information to maintain their reputation in domestic as well as international markets, to

reduce agency conflicts and political costs. Also, large companies are likely to be more

progressive and innovative because they have the financial resources that enable this type

of behaviour and therefore have more intangible assets on which to report (Guthrie et al,

2006). According to Carlin et al (2006) firstly large companies are better resourced and

therefore have the financial wherewithal to support pioneering moves such as voluntary

disclosure of intangible assets deemed significant. Secondly, large companies are likely to

have more intangible assets within their structures as they will often have more staff and a

greater number of stakeholders generally. They therefore have more to report. Thus, H1

has been accepted at 1% level of significance and H01 has been rejected.

147

H02: The leverage of a company as measured by its debt-equity ratio has no

significant impact on its intangible assets disclosure score.

H2: The leverage of a company as measured by its debt-equity ratio has a

significant impact on its intangible assets disclosure score.

The Univariate regression analysis indicates negative but insignificant association

between leverage of a firm and its intangible assets disclosure level for both years of the

study. While two-factor ANOVA test revealed negative (significant at 1% level)

association between category „high‟ and category „low‟. The negative relationship of

leverage with intangible assets disclosure score reveals that the firms with high debt content

in their capital structure disclose less information about its intangible assets in comparison

to firms with low debt. This corporate specific attribute is also insignificant when combined

with other independent factors in backward stepwise regression for both years of the study.

Prior studies have shown mixed results on the relationship between leverage and intangible

assets disclosure levels. Oliveira et al (2006), Bozzolan el al (2006) and Woodrock &

Whiting‟s (2009) studies showed no association between the extent of intangible assets

disclosure and leverage, whereas Meca & Martinez (2005), Kang & Gray (2006) and White

et al. (2007) observed a significant negative relationship. Hence null hypothesis (H02) has

been accepted and alternate hypothesis (H2) is rejected for the purpose of current study.

H03: The audit firm size of a company has no significant impact on its intangible

assets disclosure score.

H3: The audit firm size of a company has a significant impact on its intangible

assets disclosure score.

The results of two-factor ANOVA, Univariate and backward step-wise regression

analysis found audit firm size to have positive and significant association with the

disclosure score at 1% level for the years 2003-04 and 2007-08. It implies that the firms

being audited by big-six audit firms disclose more information about its intangible assets in

their annual reports. This could be due to the fact that the big-six audit firms are

internationally recognised auditors who lay emphasis on comprehensive disclosures

practices to maintain their reputation. If the information disclosed in the annual report does

not fulfil the informational needs of the users, it also raises doubts on the efficiency of the

audit firms. Also, big audit firms always compel their clients to meet the investment

decision-making information criterion for the various users of the annual reports. Other

reason that supports the result is that the internationally recognised big audit firms are

meant to signal companies‟ foreign investors of their high quality financial statements

(Owusu-Ansah and Leventis, 2006, p.283). So, audit firm size has significant positive

impact on the intangible assets disclosure score of selected Indian companies (for e.g., see,

148

Oliveira et al, 2006 and Woodrock & Whiting, 2009). H3 has been accepted at 1% level of

significance and H03 has been rejected.

H04: The profitability of a company as measured by its ROA or ROS or ROCE or

RONW has no significant impact on its intangible assets disclosure score.

H4: The profitability of a company as measured by its ROA or ROS or ROCE or

RONW has a significant impact on its intangible assets disclosure score.

The Univariate regression analysis explains that the profitability measured in

terms of ROCE is directly associated with disclosure score in years 2003-04 (1% level of

significance) and 2007-08 This result is supported by studies in Spain (Meca and

Martinez, 2005) and Taiwan (Chang et al, 2008). Two-factor ANOVA test also showed

category „high‟ of ROCE to be positively (at 1% level) related to intangible assets

disclosure score as compared to category „medium‟ and „low‟. But this corporate attribute

is not included in the final regression equation for the years 2003-04 and 2007-08

respectively. Singhvi and Desai (1971) found as expected a positive relation when

profitability alone is considered. This positive influence disappears when the rate of

return is included in conjunction with other variables. Similarly, the multivariate

regression results by Oliveira et al (2006) and Bozzolan et al (2006) also concluded

profitability to be insignificant in affecting the level of intangible assets disclosure. Thus,

H4 has been accepted at 1% level of significance on the basis of two-factor ANOVA and

univariate regression analysis and H04 has been rejected.

H05: The listing category of a firm has no significant impact on its intangible assets

disclosure score.

H5: The listing category of a firm has a significant impact on its intangible assets

disclosure score.

The results of two-factor ANOVA and Univariate regression analysis reveal that the

companies listed in A category on the BSE/NSE have more extent of intangible assets

disclosure as compared to companies listed under other categories, for both years of the study

and this association is significant at 1% level. It is in line with Oliveira et al‟s (2006) study.

The reasons being that A category companies have well-renowned market base in Indian as

well as foreign stock exchanges. These companies are thought to be profitable, efficient and

actively traded by the investors (both domestic as well as foreign). Listing status does not

enter the final regression equation for both the years of the study (similar to Meca &

Martinez, 2005 and Kang & Gray, 2006). Thus, H5 has been accepted at 1% level of

149

significance on the basis of two-factor ANOVA and univariate regression analysis and H05

has been accepted on the basis of backward step-wise regression analysis.

H06: The extent of foreign activity of a company as measured by its total exports to

total sales ratio has no significant impact on its intangible assets disclosure score.

H6: The extent of foreign activity of a company as measured by its total exports to

total sales ratio has a significant impact on its intangible assets disclosure score.

The results of two-factor ANOVA and univariate regression analysis show foreign

activity to be positive and significantly associated with the level of intangible assets

disclosure score for the year 2003-04 at 1% level of significance and at 5% level of

significance for the year 2007-08. It implies that companies with higher levels of foreign

activity disclose more information about its intangible assets to satisfy the needs of

domestic and international stakeholders. But it is not the case when effect of all

independent variables has been taken together. Foreign activity attribute does not enter

the final regression equation. Thus, H6 has been accepted at 1% level of significance for

the year 2003-04 and at 5% level of significance for the year 2007-08 on the basis of

univariate regression analysis. H6 is also accepted at 1% level of significance on the basis

of two-factor ANOVA test. The null hypothesis (H06) can be accepted on the basis of

backward step-wise regression analysis

H07: The nature of industry to which a company belongs has no significant impact

on its intangible assets disclosure score.

H7: The nature of industry to which a company belongs has a significant impact

on its intangible assets disclosure score.

The results of the Univariate and backward step-wise regression analysis indicate

an association between the nature of industry and intangible assets disclosures made by

Indian corporate. Outcome of backward regression analysis for the year 2007-08 shows

the extent of intangible assets disclosure in Indian companies from banking, capital

goods, construction, steel and transport industry is significantly (at 5% level) negatively

associated with the extent of intangible assets disclosure in software and IT industry

(which was taken as a dummy while measuring the industry effect). Also the findings of

backward regression analysis based on classification into two industry groups “high

intangible intensive firms” and “other firms” showed industry attribute affecting the

extent of intangible assets disclosure positively at 5% level of significance for 2003-04

and 1% level of significance for 2007-08. Kang and Gray (2006) explained the reason

being the companies operating in industries heavily influenced by intangible resources

would naturally have more intangible assets, and hence, would disclose more information

150

on intangible assets as a result. Also high intangible intensive firms have incentive to

report and boast of their intangibles in the annual reports to signal their superiority over

competitors in possessing immutable intangibles in their industry (Sujan & Abeysekera,

2007). Further the influence of industry confirms the claims of the stakeholder and

legitimacy theories which propose that if a firm is an intangible assets intensive, it has no

option but to disclose information about its intangible assets so that its stakeholders‟ need

for information is satisfied. Moreover, intangible intensive firms could have limited

physical assets on which they could report, and therefore disclose information on

intangible assets to gain a legitimate status in their communities (Woodrock & Whiting,

2009). Hence, the nature of industry has significant positive impact on the disclosure of

intangible assets (Bozzolan et al., 2003; Meca et al, 2003; Olsson, 2004; Petty &

Cuganesan, 2005; Bozzolan et al., 2006; Oliveira et al., 2006; Sujan & Abeysekera, 2007;

Woodrock & Whiting, 2009).Thus H7 has been accepted for “high intangible intensive

industries” at 5% level of significance for the year 2003-04 and 1% level of significance

for the year 2007-08. The null hypothesis (H07) has been rejected.

6.3 CONCLUSION

The foregoing analysis shows the impact and association of various corporate

attributes on the corporate disclosure practices of selected Indian companies for the two