Embed Size (px)

Citation preview

CHAPTER 5

CORPORATE ATTRIBUTES AND EXTENT OF

SUSTAINABILITY REPORTING IN INDIA

The results of chapter 4 depict that the scope of sustainability reporting differs

from company to company and country to country. Different corporate attributes tend to

influence sustainability reporting practices. This chapter scrutinizes the relationship

between the sustainability reporting by companies and selected corporate specific

attributes. The corporate attributes considered include size of a company, profitability,

growth, leverage, listing category, age, nationality, board size, board independence,

advertising intensity and nature of industry.

5.1 HYPOTHESES DEVELOPMENT

Based on the theoretical and empirical considerations, numerous hypotheses have

been framed that associate company-specific characteristics with the sustainability

reporting by Indian companies. These hypotheses are stated in both null and alternative

form.

5.1.1 Size of a company

Company size is in fact the most common corporate attribute which has been

found to be related with the extent of sustainability reporting. Several studies like Meek

et al. (1995), Hossain and Reaz (2007), Jennifer and Taylor (2007), Hoorik (2009),

Lattemann et al. (2009), Reverte (2009), Xiang (2009), Artiach et al. (2010), Yu (2010),

Li et al. (2011), Michelon (2011), Bhayani (2012), Birt (2012), Al-Shubiri et al. (2012),

Ghosh (2013) and Branco et al. (2014) exhibited positive relation between size and

extent of sustainability disclosure. However, Rahman & Widyasari (2008) and Lungu et

al. (2011) observed no correlation between social reporting and size of the companies.

It has been observed that the larger companies disclose more sustainability

information as compared to smaller companies for a number of reasons. First, large

companies have greater political popularity that motivates them to gather greater

consideration from the government, common people and other stakeholders (Artiach et

al. 2010). By providing sustainability information these companies demonstrate that they

Corporate Attributes and Extent of Sustainability Reporting in India

160

carry out their business operations in a liable manner. This enhances their image in the

eyes of public and their goodwill. This improved image reduces public criticism and

minimizes threat of government intervention (Al-Shammari, 2008).

Secondly, large companies are expected to grasp greater economies of scale in

perusing corporate sustainability activities (Artiach et al. 2010). They have lower

information generation costs, and costs of competitive disadvantage connected with their

reporting practices (Meek et al. 1995).

Thirdly, large companies are more likely to encounter greater social problems and

agendas because of their large scale operations & activities and generate greater

stakeholders’ expectations. For example, emissions in the environment that causes

pollution are to some extent in proportion to the size of operations (Artiach et al. 2010),

they have to take up more sustainability efforts to cover the adverse effects of their

activities.

Fourthly, large companies are more capable of putting more resources on

sustainability and its disclosure (Shum et al. 2009; Yu, 2010), as they have more

financial resources as compared to smaller companies.

Fifthly, large companies are supposed to have a superior level of internal

reporting in order to fulfill the information needs of the top management and thus incur

low cost in providing this information to the public (Buzby,1975).

Sixthly, smaller firms are more likely to assume that if they disclose their dealings

fully then this will place them at a competitive disadvantage with larger firms in their

industry (Buzby, 1975; Al-Shammari, 2008).

The previous estimation was that bigger companies will have higher levels of

sustainability disclosure than smaller companies. There are a number of measures of size

in the literature available on this subject. The net sales, total assets and market

capitalization are used as proxies of size of a company in this study. The preceding

discussions lead to development of the following null and alternate hypotheses:

H01: The size of a company as measured by its total assets or net sales or total market

capitalization has no significant impact on its sustainability disclosure score.

H1: The size of a company as measured by its total assets or net sales or total market

capitalization has a significant impact on its sustainability disclosure score.

Corporate Attributes and Extent of Sustainability Reporting in India

161

5.1.2 Profitability of a company

Numerous studies have examined the relationship between profitability and

sustainability disclosure. Companies which experience greater profitability may more

actively disclose sustainable information in comparison to the low-profit earning

companies. This is on account of number of reasons. First, the management of the

company with higher profits may disclose more sustainable information in order to

experience the advantages of communicating it, as it is a positive news (Mahajan and

Chander, 2007) and it helps them to avoid undervaluation of their shares (Oliveira et al.,

2006). Secondly, the higher profits motivate a company to disclose more information

because higher profits raise doubts in the minds of the public and the related disclosure

clears the doubts which lessens the risk of their being negatively selected by the market

(Prencipe, 2010) and to justify the level of profits. Moreover Oliveira et al. (2006)

pointed out that managers are motivated to report information voluntarily in order to

maintain their positions and compensation arrangements because disclosure works as a

tool to monitor their performance. So, they have to disclose better to prove that they are

performing better and thus mark their presence. On the other side, if profitability of a

company is low then management may report lesser information in order to hide the

reasons for declining profits (Singhvi and Desai, 1971).

The empirical studies, have, however found mixed results. Among these

researchers, Xiang (2009), Kartadjumena et al. (2011) and Branco et al. (2014) exhibited

a positive association between profitability and the extent of sustainability disclosure;

whereas Jennifer & Taylor (2007) and Lungu et al. (2011) supported a negative

association between variables. Others as Ho and Wong (2001), Rahman and Widyasari

(2008), Yu (2010) and Li et al. (2011) found no significant relationship regarding

variables.

Prior research reveals that a number of measures have been used by researchers to

determine the association between profitability and corporate disclosure. The return on

assets, return on net worth and return on capital employed have been used as

determinants of profitability and its association with the level of sustainability disclosure

in this study.

Corporate Attributes and Extent of Sustainability Reporting in India

162

Given the mixed results from previous empirical studies, one could expect a

positive, negative, or no relationship between profitability and the level of sustainability

reporting. This discussion, therefore, has directed to the formulation and testing of the

following null and alternate hypotheses:

H02: The profitability of a company as measured by its ROA or ROCE or RONW has

no significant impact on its sustainability disclosure score.

H2: The profitability of a company as measured by its ROA or ROCE or RONW has a

significant impact on its sustainability disclosure score.

5.1.3 Growth of a company

Some studies are using growth of a company as an independent variable for

variations in sustainability disclosure. It is expected that with superior growth

opportunities, companies tend to endeavor on the upgradation of sustainability disclosure

level (Yu, 2010). Faster growth is typically associated with environmental and social

challenges (Ghosh, 2013). However, Al-Shubiri et al. (2012) noticed a positive

significant relationship, whereas, Yu (2010), Prencipe (2010) and Ghosh (2013) noticed

no significant relationship between growth and sustainability disclosure. Eng and Mak

(2003) also observed no significant relationship between disclosure and growth

opportunities. The following null and alternate hypotheses have been formulated and

tested in the study:

H03: The growth of a company as measured in terms of its growth in total assets has no

significant impact on its sustainability disclosure score.

H3: The growth of a company as measured in terms of its growth in total assets has a

significant impact on its sustainability disclosure score.

5.1.4 Leverage of a company

Leverage represents the level of debt in the capital structure of a company which

in turn depicts the relative significance of the company’s financial stakeholders (Artiach

et al. 2010). Many researchers in their studies on disclosure have used leverage as an

explanatory variable. Some have advocated for its positive relationship for a variety of

reasons. First, companies with a greater level of leverage experience high level of

financial risk (Patton and Zelenka, 1997) and hence report more sustainability

Corporate Attributes and Extent of Sustainability Reporting in India

163

information. Companies with high leverage are required to explain their leverage position

in detail in order to get extra funds, whether from banks or stock markets because these

are labeled as risky ones and these companies find it difficult to raise funds without

disclosing detailed information (Al-Shubiri et al, 2012). Secondly, some assume that

companies with high leverage disclose more information as due to higher level of

leverage these are required to furnish detailed information by regulatory authorities, for

example, Ministry of Commerce and Industry, which assesses the obligations of company

and its future cash flows (Al-Shammari, 2008). On the other hand, some studies have

shown support for negative relation because it is also observed that as the companies’

leverage increases the disclosure of their sustainability information decreases. Companies

with high leverage are more interested in making financial disclosures for the sake of

debenture holders and lenders of money. The disclosure requirements of less powerful

claimants as the community and NGOs take a back seat. This leads to the negative

relationship between leverage and sustainability reporting (Artiach et al. 2010). Further,

some advocate that companies whose capital structure has more debt have policy of

disclosing only mandatory information because the companies disclose the maximum

information when they have more share capital (Bhayani, 2012) and sustainability

disclosure is voluntary in nature.

Previous studies have given mixed results on the association between leverage

and sustainability disclosure levels. Rahman and Widyasari (2008), Hoorik (2009) and

Artiach et al. (2010) showed no significant relationship between the extent of

sustainability disclosure and leverage, whereas Yu, (2010) and Al-Shubiri et al. (2012)

supported a significant positive relationship between the two. However, Eng and Mak

(2003), Jennifer & Taylor (2007), Bhayani (2012), Birt (2012) and Branco et al. (2014)

noticed a negative relationship. The foregoing discussion leads to the development of the

following null and alternate hypotheses:

H04: The leverage of a company as measured by its debt-equity ratio has no significant

impact on its sustainability disclosure score.

H4: The leverage of a company as measured by its debt-equity ratio has a significant

impact on its sustainability disclosure score.

Corporate Attributes and Extent of Sustainability Reporting in India

164

5.1.5 Listing Category of a Company

The listing category of a company also affects the corporate sustainability

disclosure level. A company which wants to get itself listed on a stock exchange has to

abide by its listing agreement. Stock market particularly investors are interested in those

companies whose shares are actively traded and hence keep watch on them vigilantly.

“A” category companies are expected to report more information to reduce agency,

political and monitoring costs. Empirical evidence also suggests a significant association

between level of reporting and the listing status of a company. Bhayani (2012) and

Branco et al. (2014) are of the opinion that there is a significant influence of listing

category on the sustainability reporting and assurance. However, Buzby (1975) found

that the disclosure is not affected by listing status. The following are the null and

alternate hypotheses which are framed and tested in this context:

H05: The listing category of a company has no significant impact on its sustainability

disclosure score.

H5: The listing category of a company has a significant impact on its sustainability

disclosure score.

The impact of listing category of a company has been scrutinized by means of

dummy variable. The companies falling under “A” category are given a score of 1 while

companies belonging to the other categories are given 0.

5.1.6 Age of a company

This corporate variable is selected on the basis that older companies might have

enhanced their sustainability reporting practices with the passage of time. The age of a

company also influences its sustainability disclosure level for variety of reasons. First, the

professional staff of older companies is expected to be established, regular and well

controlled to deal with the scientific aspects of sustainability disclosure. Their enhanced

accounting systems are in a better position to produce more exhaustive information at

lesser cost, compared to their younger counterparts (Al-Shammari, 2008). Secondly, a

young company may face a greater competitive disadvantage if it discloses information

regarding certain items namely, research & development expenditure, capital expenditure

and new products. Some companies might use this information in a wrong manner which

will raise the competitive disadvantage for younger company (Al-Shammari, 2008).

Corporate Attributes and Extent of Sustainability Reporting in India

165

However, Hossain & Reaz (2007) and Bhayani (2012) found no association of age with

disclosure level. Therefore, the above arguments have lead to the formulation of

following hypotheses:

H06: The age of a company has no significant impact on its sustainability disclosure

score.

H6: The age of a company has a significant impact on its sustainability disclosure

score.

The age of a company is computed from the year of its incorporation till March

31, 2011.

5.1.7 Nationality

Another possible reason for increased reporting on sustainability is the level of

expansion of operations of a company. Companies extending their operations

multinationally are envisaged to report more information (Chapple and Moon, 2013) and

follow higher standards of reporting for a number of reasons.

First, companies need to increase their disclosures relating to sustainability as it

proves their transparency and competitive positioning (KPMG, 2008b) which ultimately

enhances its credit worthiness among foreign investors.

Secondly, they have to fulfill the regulations of both host country and the parent

country (Karim and Ahmed, 2005). Even, it has been mandated by Securities and

Exchange Board of India (SEBI) for the top hundred NSE/BSE listed entities to submit

Business Responsibility Reports as a part of their annual reports from the year 2012-

2013.

Thirdly, multinational companies are usually equipped with superior accounting

software tools, skilled and efficient management & staff and so have the capacity to

report more information without incurring any increased costs of processing (Mahajan &

Chander, 2007).

Fourthly, they come across new requirements of information that are ahead of

domestic demands. Their internationalized operations result in a larger percentage of

foreign stakeholders in the company (Meek et al., 1995)

Lastly, they have to face closer inspection of political and pressure groups of the

host country that are of the view that these companies are a source of economic

Corporate Attributes and Extent of Sustainability Reporting in India

166

exploitation and agents of imperialist power (Mahajan & Chander, 2007). Hence, they

have a sufficiently good reason to disclose greater information in order to avoid any

excessive pressure or exploitation.

Meek et al. (1995) used multinationality (Extent of Multinational Operations) and

Mahajan & Chander (2007) used residential status as an explanatory variable in

developing their models and both found it to be an insignificant variable in explaining

disclosure levels. Therefore, the following hypotheses have been formulated and tested in

this context:

H07: The nationality of a company has no significant impact on its sustainability

disclosure score.

H7: The nationality of a company has a significant impact on its sustainability

disclosure score.

The influence of nationality is examined by introducing dummy variable, the

score of 1 is given for companies with multinational operations and 0 for domestic

operations.

5.1.8 Board size

Board size is not a common attribute in the studies on sustainability reporting.

However, this variable has been chosen on the basis that the level of sustainability

reporting may vary among companies in response to the number of directors on the

board. The Board of Directors represents the highest committee in the company and is

expected to control the reporting decisions by openly making decisions within the board

(Kent and Monem, 2008). Good corporate governance is anticipated to strengthen the

corporate responsibility attitude within companies (Wise and Ali, 2009). But researchers

came across only one study i.e. by Uyar et al. (2013), which found no significant

relationship between board size and reporting score. So, the following hypotheses have

been formulated and tested:

H08: The board size of a company has no significant impact on its sustainability

disclosure score.

H8: The board size of a company has a significant impact on its sustainability

disclosure score.

Corporate Attributes and Extent of Sustainability Reporting in India

167

5.1.9 Board independence

Board independence is defined as “the proportion of independent directors to the

total number of directors”. The independence of the board depends on the number of

independent, non-executive directors on the board. Their inclusion reduces the chances of

fraud, perhaps for the reason that outside directors are more inclined towards encouraging

companies to disclose better information to outside investors (Eng and Mak, 2003).

Hence it seems that the greater proportion of independent directors’ representation results

in more effective and efficient control on the activities of the board, and in more

voluntary reporting of corporate information. This stimulates more transparency resulting

in more disclosure (Kent and Monem, 2008). Further, Chau and Gray (2010) found that

the level to which independent directors are selected on the board is positively related

with the extent of voluntary disclosure. On the other hand, Xiang (2009) noticed that the

number of independent directors has no remarkable effect on information disclosure

level. Faisal et al. (2012) reported that board independence is not a significant predictor

for sustainability communication. While Eng and Mak (2003) conclude that increase in

number of directors reduces corporate disclosure. The following null and alternate

hypotheses are formulated and tested in the study:

H09: The board independence of a company has no significant impact on its

sustainability disclosure score.

H9: The board independence of a company has a significant impact on its

sustainability disclosure score.

5.1.10 Advertising intensity

Advertising provides companies a means of differentiation and a way of giving

information about sustainability, and hence amplifies the effects of corporate

sustainability performance (Fisman et al., 2008; Wagner 2010). The intensity of

advertisement expenses often influences the sustainability disclosure of a company. Very

few studies have considered this attribute. For example, Ghosh (2013) revealed that the

companies having higher advertisement expenses are likely to be superior in

sustainability. However one study by Gelb (2002) that studied advertising expenditures

indicated that companies with significant levels of this expenditure are expected to give

more importance to “voluntary and more flexible disclosures over traditional mandated

Corporate Attributes and Extent of Sustainability Reporting in India

168

accounting reports”. Therefore, the following null and alternate hypotheses have been

framed and are tested in this study:

H010: The advertising intensity of a company has no significant impact on its

sustainability disclosure score.

H10: The advertising intensity of a company has a significant impact on its

sustainability disclosure score.

5.1.11 Nature of Industry

Nature of industry influences the extent of corporate disclosure because

companies carry out different activities that require different recording and disclosure

(Naser and Hassan, 2013). Sustainability Disclosure tends to be industry specific

(Jennifer and Taylor, 2007; Yu, 2010; Elijido-Ten, 2011; Michelon, 2011; Birt, 2012).

Even Yu (2010) stated that the extent of disclosure varies as per types of industries.

Divergent industries have dissimilar characteristics relative to regulatory requirements,

stakeholder demands, market competition, type of private information, and the threat of

entry of new companies into the market. These characteristics offer incentives for

companies belonging to a particular industry to disclose more information than

companies falling under other industry. For example, the nature of product and research

& development activities of Chemical companies motivates them to be more responsive

about disclosure of information to competitors and the public than companies belonging

to certain other industries (Meek et al., 1995). Also, Consumer Good industry and

Information Technology industry have a low coverage of environmental and social

aspects (Yu, 2010). Proprietary costs also fluctuate according to the nature of industry.

Moreover, companies falling under the same industry have common interest in producing

the similar level of disclosure as this in turn helps them in avoiding negative appreciation

by the market competitive pressures (Lopes and Rodrigues, 2007). It seems that nature of

industry is expected to relate to the quality of sustainability disclosures (Hoorik, 2009). It

is obvious that some industries are comparatively more sensitive to sustainability issues

because they have more legitimate stakeholders to deal with. The urgency of responding

to these stakeholders through disclosure rises when these stakeholders take action against

the companies. Some studies like Newson and Deegan (2002) classified these industries

as high profile and low profile industries. Birt (2012) showed that nature of industry is

Corporate Attributes and Extent of Sustainability Reporting in India

169

positively and significantly related with sustainability disclosures. Moreover, Jennifer

and Taylor (2007), Hoorik (2009), Dilling (2010), Elijido-Ten (2011), Michelon (2011)

and Ghosh (2013) found industry to be a significant variable in sustainability disclosure.

The preceding discussions lead to development of the following null and alternate

hypotheses:

H011: The nature of industry to which a company belongs has no significant impact on

its sustainability disclosure score.

H11: The nature of industry to which a company belongs has a significant impact on its

sustainability disclosure score.

5.2 RESULTS AND DISCUSSIONS

The effect of various corporate attributes on the extent of sustainability reporting

has been investigated with the help of multiple regression analysis. The outcomes of

these have been conferred in the following sub-parts:

5.2.1 Regression Analysis

Since wide differences have been viewed in the sustainability disclosure score of

the selected Indian companies, it becomes crucial to know the reasons of such

differences. The reasons seem company specific. So here an attempt has been made to

find the effect of corporate specific attributes like size of a company, profitability,

growth, leverage, listing category, age of a company, nationality, board size, board

independence, advertising intensity and nature of industry on the sustainability disclosure

score of sample Indian non financial companies for the financial year 2010-11. For this

purpose, it is essential to assess the validity of the Model (regression equation).

5.2.1.1 Checking the Multicollinearity of Data

Before going to the regression analysis, it was informative to verify the presence

of multicollinearity among the independent variables. Sometimes there is destructive

effect on the regression results because two or more of the independent variables are

highly correlated and this refers to the state of multicollinearity. The correlation matrix is

a prevailing measure for obtaining a rough view about the relationship between variables.

Multicollinearity is a serious problem when the pair-wise or zero-order correlation

Corporate Attributes and Extent of Sustainability Reporting in India

170

coefficient between two independent variables is high, that is it exceeds the

recommended rule of thumb, 0.8 (Gujarati, 2012, p. 356). This problem of very high

intercorrelations among independent variables can be solved by dropping that variable

and then running regression analysis with rest of the independent variables. An alternate

way to check this multicollinearity is to calculate the average VIF (Variance inflation

factor) and TOL (Tolerance Limit). As a suggested rule of thumb, the VIF of a variable

should not exceed 10 and the TOL should not exceed 0.10, this prescribed limit is crossed

when R2 go beyond 0.80, and this results in high colliniarity (Gujarati, 2012, p. 359).

5.2.1.2 Checking the Homoscedasticity of Data

Homoscedasticity means that all the disturbances i.e. ui appearing in the

regression function have the same variance (Gujarati, 2012, p. 386). This assumption

when violated is known by the name, heteroscedasticity and is generally expected in a

cross-sectional analysis, when small, medium and large size companies are taken together

in the sample (Gujarati, 2012, p. 397). However, in our sample we have resorted to only

large companies. But for the purpose of confirmation, White’s general hetroscedasticity

test through EViews has been used to check this assumption.

5.2.1.3 Checking the Normality of Data

Normality assumption means that the error term or the random variable of the

regression equation is assumed to follow normal distribution (Koutsoyiannis, 1977).

Skewness and kurtosis are computed to test the normality of data. As a rule of thumb, the

value of skewness for a distributed data is zero and the value of kurtosis can range from -

3 to +3. The skewness and kurtosis in our database is within the standard limit. However,

the size of a company taken in terms of different surrogates in different regression

equations is found to be not normal. If the rough values of these variables are considered

then this could give vast influence to the very large companies. This problem can be

solved by taking their logarithmic transformations as it will lessen the effect on the

regression results (Lungu et al., 2011). Thus, natural log transformation has been done to

make it normal (see Hoorik, 2009; Jennifer and Taylor, 2007; Ghosh, 2013; Lungu et al.,

2011).

Corporate Attributes and Extent of Sustainability Reporting in India

171

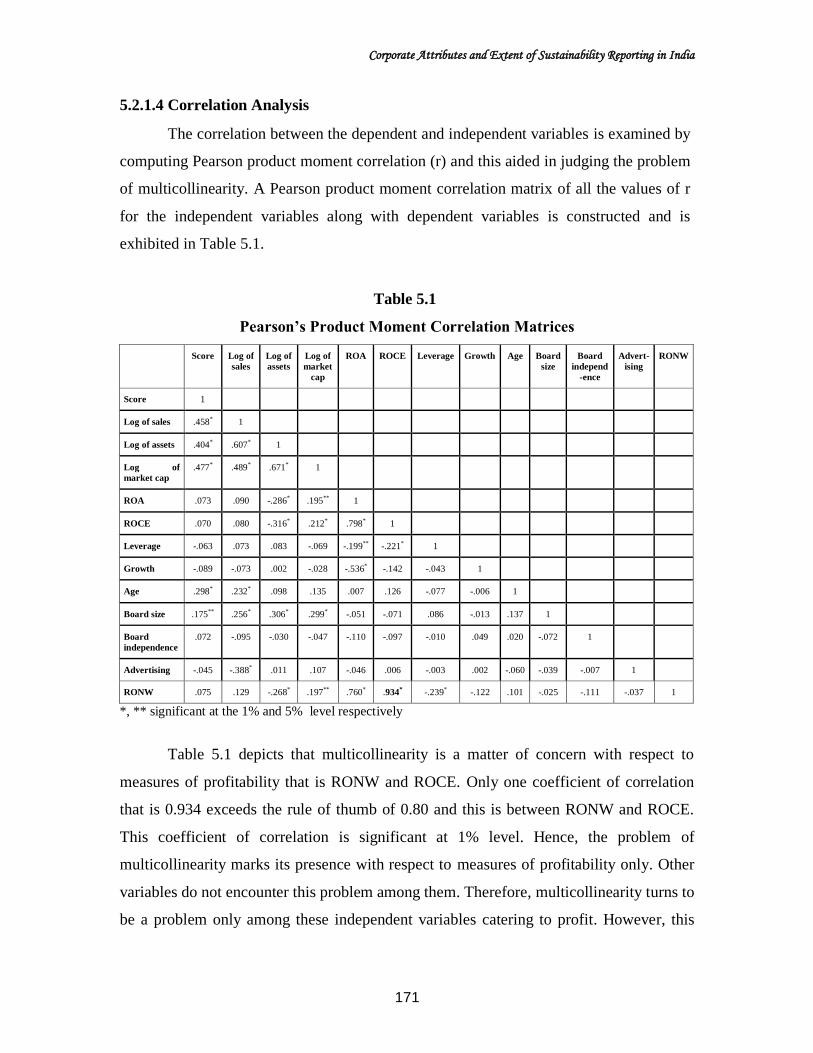

5.2.1.4 Correlation Analysis

The correlation between the dependent and independent variables is examined by

computing Pearson product moment correlation (r) and this aided in judging the problem

of multicollinearity. A Pearson product moment correlation matrix of all the values of r

for the independent variables along with dependent variables is constructed and is

exhibited in Table 5.1.

Table 5.1

Pearson’s Product Moment Correlation Matrices

Score Log of

sales

Log of

assets

Log of

market

cap

ROA ROCE Leverage Growth Age Board

size

Board

independ

-ence

Advert-

ising

RONW

Score 1

Log of sales .458* 1

Log of assets .404* .607* 1

Log of

market cap

.477* .489* .671* 1

ROA .073 .090 -.286* .195** 1

ROCE .070 .080 -.316* .212* .798* 1

Leverage -.063 .073 .083 -.069 -.199** -.221* 1

Growth -.089 -.073 .002 -.028 -.536* -.142 -.043 1

Age .298* .232* .098 .135 .007 .126 -.077 -.006 1

Board size .175** .256* .306* .299* -.051 -.071 .086 -.013 .137 1

Board

independence

.072 -.095 -.030 -.047 -.110 -.097 -.010 .049 .020 -.072 1

Advertising -.045 -.388* .011 .107 -.046 .006 -.003 .002 -.060 -.039 -.007 1

RONW .075 .129 -.268* .197** .760* .934* -.239* -.122 .101 -.025 -.111 -.037 1

*, ** significant at the 1% and 5% level respectively

Table 5.1 depicts that multicollinearity is a matter of concern with respect to

measures of profitability that is RONW and ROCE. Only one coefficient of correlation

that is 0.934 exceeds the rule of thumb of 0.80 and this is between RONW and ROCE.

This coefficient of correlation is significant at 1% level. Hence, the problem of

multicollinearity marks its presence with respect to measures of profitability only. Other

variables do not encounter this problem among them. Therefore, multicollinearity turns to

be a problem only among these independent variables catering to profit. However, this

Corporate Attributes and Extent of Sustainability Reporting in India

172

problem was monitored by considering only one measure of profitability in a regression

equation at one time.

Afterwards, Multiple Regression analysis is applied.

Multiple Regression Analysis

The regression equation analyzing the impact of various corporate specific

attributes on the sustainability disclosure score for 2010-2011 is framed as below:

Y = β0 +β1X1 +β2 X2 +β3 X3 +β4 X4 +β5 X5 +β6 X6 + β7 X7 +β8 X8 +β9 X9 +β10 X10+ β11-23

X11-23+ ε

Where:

Y = Sustainability disclosure score

X1 = Size of a company (log of market capitalization)

X2 = Profitability of a company (ROA)

X3 = Growth of a company

X4 = Leverage of a company

X5 = Listing category of a company

X6= Age of a company

X7= Nationality

X8 = Board size

X9= Board independence

X10= Advertising intensity

X11-23 = Industry type

β = Slopes of the independent variables while β0 is a constant or the value of Y

when all values of X are zero

ε = εi ~ (0, N)

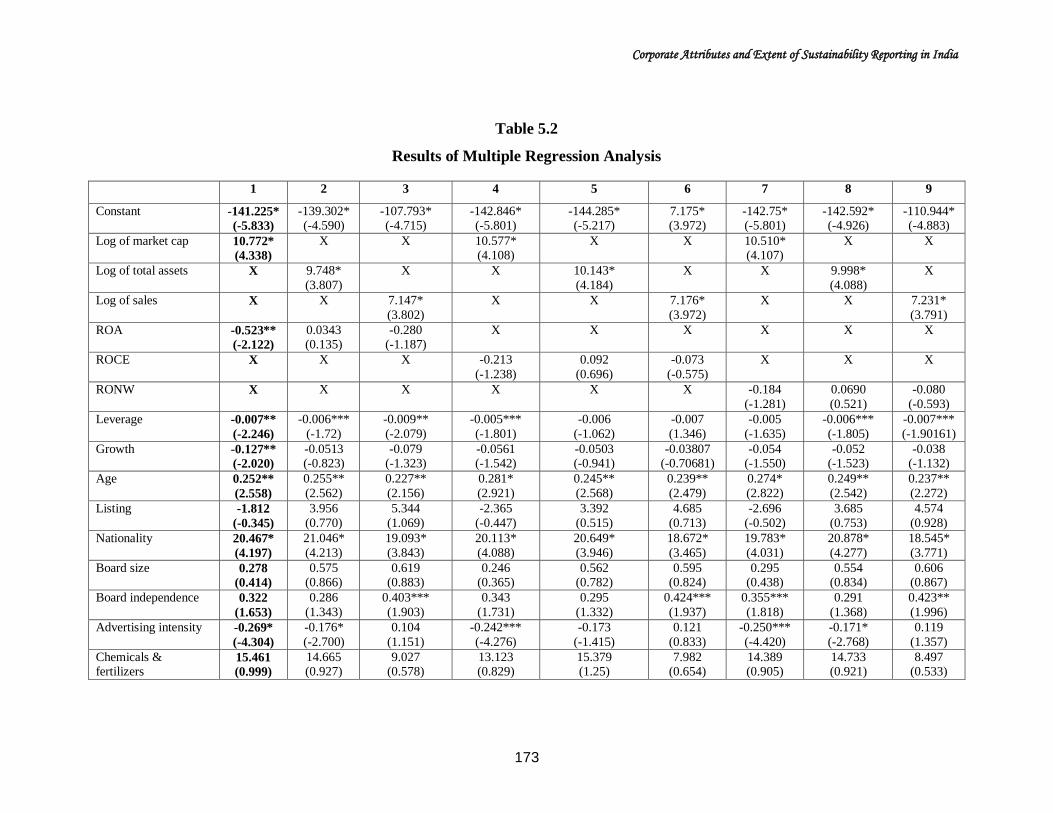

The results from the multiple regression analysis have been presented in Table

5.2. Three separate determinants of company size (sales, assets, and market

capitalization) as well as three different measures of profitability (ROA, ROCE, and

RONW) are used. Each substitute to represent size and profitability is used only once in a

model. This has led to the creation of nine regression equations, the results of which have

been presented in Table 5.2

Corporate Attributes and Extent of Sustainability Reporting in India

173

Table 5.2

Results of Multiple Regression Analysis

1 2 3 4 5 6 7 8 9

Constant -141.225*

(-5.833)

-139.302* (-4.590)

-107.793* (-4.715)

-142.846* (-5.801)

-144.285* (-5.217)

7.175* (3.972)

-142.75* (-5.801)

-142.592* (-4.926)

-110.944* (-4.883)

Log of market cap 10.772*

(4.338)

X X 10.577* (4.108)

X X 10.510* (4.107)

X X

Log of total assets X 9.748*

(3.807)

X X 10.143*

(4.184)

X X 9.998*

(4.088)

X

Log of sales X X 7.147*

(3.802)

X X 7.176*

(3.972)

X X 7.231*

(3.791)

ROA -0.523**

(-2.122)

0.0343 (0.135)

-0.280 (-1.187)

X X X X X X

ROCE X X X -0.213

(-1.238)

0.092

(0.696)

-0.073

(-0.575)

X X X

RONW X X X X X X -0.184

(-1.281)

0.0690

(0.521)

-0.080

(-0.593)

Leverage -0.007**

(-2.246)

-0.006***

(-1.72)

-0.009**

(-2.079)

-0.005***

(-1.801)

-0.006

(-1.062)

-0.007

(1.346)

-0.005

(-1.635)

-0.006***

(-1.805)

-0.007***

(-1.90161)

Growth -0.127**

(-2.020)

-0.0513 (-0.823)

-0.079 (-1.323)

-0.0561 (-1.542)

-0.0503 (-0.941)

-0.03807 (-0.70681)

-0.054 (-1.550)

-0.052 (-1.523)

-0.038 (-1.132)

Age 0.252**

(2.558)

0.255**

(2.562)

0.227**

(2.156)

0.281*

(2.921)

0.245**

(2.568)

0.239**

(2.479)

0.274*

(2.822)

0.249**

(2.542)

0.237**

(2.272)

Listing -1.812

(-0.345)

3.956

(0.770)

5.344

(1.069)

-2.365

(-0.447)

3.392

(0.515)

4.685

(0.713)

-2.696

(-0.502)

3.685

(0.753)

4.574

(0.928)

Nationality 20.467*

(4.197)

21.046*

(4.213)

19.093*

(3.843)

20.113*

(4.088)

20.649*

(3.946)

18.672*

(3.465)

19.783*

(4.031)

20.878*

(4.277)

18.545*

(3.771)

Board size 0.278

(0.414)

0.575 (0.866)

0.619 (0.883)

0.246 (0.365)

0.562 (0.782)

0.595 (0.824)

0.295 (0.438)

0.554 (0.834)

0.606 (0.867)

Board independence 0.322

(1.653)

0.286

(1.343)

0.403***

(1.903)

0.343

(1.731)

0.295

(1.332)

0.424***

(1.937)

0.355***

(1.818)

0.291

(1.368)

0.423**

(1.996)

Advertising intensity -0.269*

(-4.304)

-0.176*

(-2.700)

0.104

(1.151)

-0.242***

(-4.276)

-0.173

(-1.415)

0.121

(0.833)

-0.250***

(-4.420)

-0.171*

(-2.768)

0.119

(1.357)

Chemicals & fertilizers

15.461

(0.999)

14.665 (0.927)

9.027 (0.578)

13.123 (0.829)

15.379 (1.25)

7.982 (0.654)

14.389 (0.905)

14.733 (0.921)

8.497 (0.533)

Corporate Attributes and Extent of Sustainability Reporting in India

174

1 2 3 4 5 6 7 8 9

Consumer Goods

durables & FMCG 7.14

(0.758)

6.631

(0.63)

-0.619

(-0.061)

5.164

(0.554)

5.681

(0.564)

-2.421

(-0.241)

5.306

(0.559)

5.707

(0.543)

-1.994

(-0.196)

Cement and construction

21.621***

(1.799)

16.389 (1.261)

16.751 (1.419)

19.126 (1.587)

16.879 (1.509)

15.656 (1.388)

19.721 (1.638)

16.639 (1.262)

15.758 (1.317)

Diversified and others 3.087

(0.252)

4.182

(0.345)

3.472

(0.29)

0.736

(0.058)

5.217

(0.488)

2.647

(0.247)

1.483

(0.117)

4.778

(0.384)

2.786

(0.225)

Entertainment and

media 6.565

(0.615)

9.646

(0.913)

6.563

(0.582)

-0.499

(-0.05)

10.215

(0.588)

2.615

(0.151)

-4.379

(-0.377)

11.579

(0.994)

0.999

(0.086)

Metal, metal products

& mining 21.100

(1.600)

18.648

(1.435)

23.028***

(1.79)

17.667

(1.313)

18.838***

(1.809)

21.232**

(2.042)

18.842

(1.413)

18.493

(1.410)

21.609***

(1.673)

Oil & Gas 26.666**

(2.581)

19.415*** (1.704)

19.785*** (1.708)

24.336** (2.262)

19.13*** (1.695)

18.449 (1.611)

25.344** (2.361)

18.958 (1.645)

18.726 (1.585)

Drugs &

pharmaceuticals -7.439

(-0.780)

-4.930

(-0.469)

-6.352

(-0.636)

-9.303

(-0.954)

-4.231

(-0.406)

-7.131

(-0.687)

-8.581

(-0.877)

-4.648

(-0.436)

-6.866

(-0.674)

Power 4.813

(0.448)

1.111

(0.097)

10.405

(0.938)

3.623

(0.330)

1.407

(0.134)

10.033

(0.970)

4.101

(0.374)

1.292

(0.111)

10.070

(0.889)

Software, IT & ITES 32.243**

(2.607)

33.402** (2.509)

36.848* (2.882)

28.422** (2.271)

33.152* (2.803)

34.476* (2.901)

28.555** (2.267)

33.213** (2.464)

34.618* (2.679)

Textile -7.424

(-0.647)

-10.344 (-0.934)

-7.346 (-0.697)

-10.973 (-0.933)

-9.64 (-0.575)

-8.985 (-0.532)

-10.056 (-0.849)

-10.057 (-0.895)

-8.693 (-0.806)

Telecommunications -17.410

(-1.339)

-22.612***

(-1.673)

-18.641

(-1.529)

-16.078

(-1.225)

-22.383

(-1.458)

-17.520

(-1.149)

-15.691

(-1.199)

-22.422

(-1.641)

-17.691

(-1.426)

Automotives &

transport 5.799

(0.555)

2.43

(0.216)

1.607

(0.147)

3.741

(0.353)

2.526

(0.259)

0.502

(0.0509)

4.291

(0.403)

2.344

(0.206)

0.699

(0.063)

R-square 0.472 0.451 0.452 0.463 0.453 0.447 0.462 0.453 0.448

Adjusted R-square 0.382 0.357 0.358 0.371 0.359 0.352 0.37 0.359 0.353

F 5.216* 4.795* 4.802* 5.026* 4.832* 4.710* 5.003* 4.820* 4.722*

F (sig) 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000

DW 1.73 1.721 1.664 1.681 1.688 1.618 1.665 1.7 1.624

Note: * significant at 1% level

** significant at 5% level

*** significant at 10% level

Corporate Attributes and Extent of Sustainability Reporting in India

175

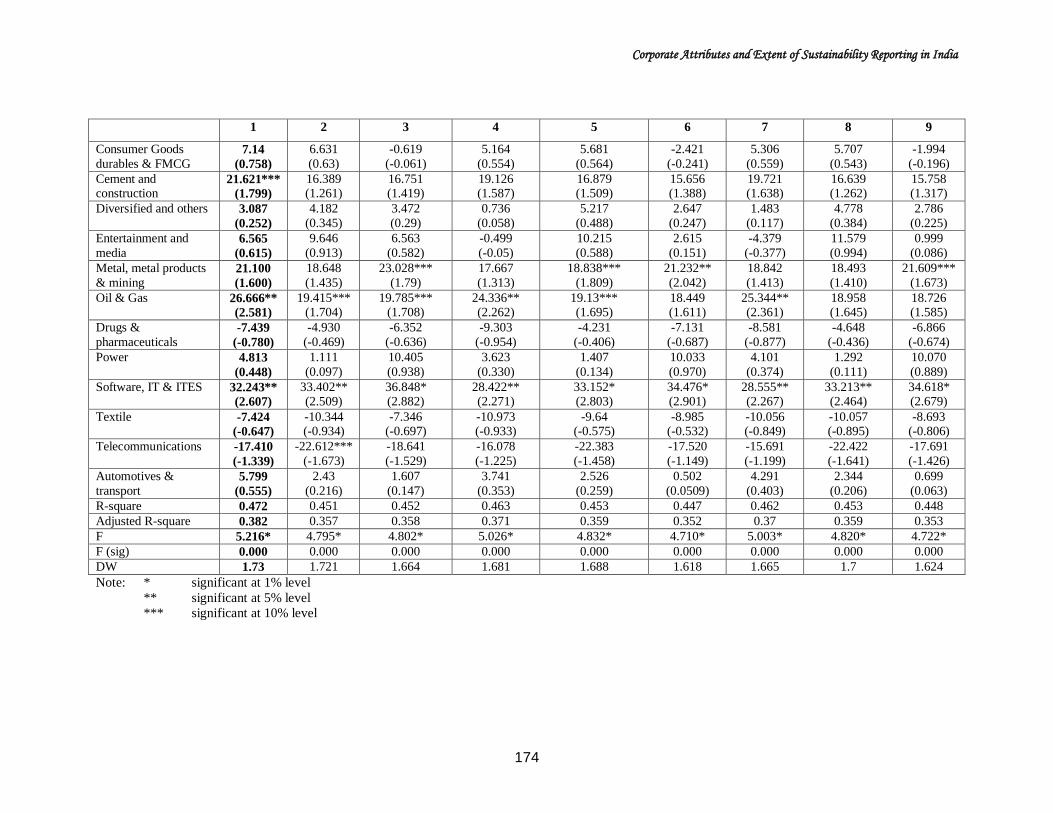

Table 5.2 reveals that for all models, different measures of size, age, nationality

and Software, IT & ITES industry are found to be significant. ROA and growth are

significant at 5% level when applied in combination with log of market capitalization.

Other profitability surrogates could not significantly explain variations in the disclosure

level. The board independence is found to be significant at 10% level in explaining

variations in sustainability disclosure, when applied in combination of log of sales with

ROA, ROCE and RONW, and log of market capitalization with RONW, the surrogate of

size and profitability. Leverage and advertising intensity are also found to be significant,

but only in certain surrogates of size and profitability. Other variables could not find any

place in explaining significant variations in the disclosure level. So, out of 9 models, the

model, which is satisfying validity requirements and having improved adjusted R2 has

been chosen and selected as a valid model. Hence, the model 1 i.e. with combination of

log of market capitalization, ROA, growth, leverage, listing category, age of a company,

nationality, board size, board independence, advertising intensity and nature of industry is

selected. It has an adjusted R

2 of 0.382, F value of 5.216. This is significant at 1% level of

significance. DW comes out to be 1.73 which is within the acceptable limits. In this

model, log of market capitalization ROA, growth, leverage, age of a company,

nationality, Oil & Gas, Cement & Construction and Software, IT & ITES industry are

found to be significant. Log of market capitalization and nationality are positively

significant at 1% level, while age and nature of industry (Software, IT & ITES and Oil &

Gas) are significant at 5% level. It shows that companies with large size, older,

multinational operations and belonging to Software, IT & ITES, Cement & construction

and Oil & Gas industry have significant sustainability disclosure. Since Capital &

Engineering goods industry has been taken as a dummy. The positive values of Oil &

Gas, Cement & Construction and Software, IT & ITES depicts that these industries are

reporting more information as compared to Capital & Engineering goods industry.

However, advertising intensity is negatively significant at 1% level and ROA, leverage,

growth at 5% level. This shows that the company’s profits, leverage, growth and

advertising intensity are negatively related with the extent of sustainability disclosure.

Other variables were found to be insignificant.

Corporate Attributes and Extent of Sustainability Reporting in India

176

5.2.2 Testing The Hypotheses

Multiple regression analysis has been performed in order to check the following

null and alternate hypotheses. These are discussed as below:

H01: The size of a company as measured by its total assets or net sales or total

market capitalization has no significant impact on its sustainability

disclosure score.

H1: The size of a company as measured by its total assets or net sales or total

market capitalization has a significant impact on its sustainability disclosure

score.

The results from multiple regression analysis support for the positive and

significant relationship between size of a company considered in terms of market

capitalization and sustainability reporting. So, the results of this study are in line with the

past research in India (Hossain and Reaz, 2007; Bhayani, 2012; Ghosh, 2103), India and

China (Lattemann et al., 2009), Netherlands (Hoorik, 2009), China (Xiang, 2009), US

and Japan (Jennifer and Taylor, 2007), US (Artiach et al., 2010), Continental Europe, UK

and USA (Meek et al. 1995; Michelon,2011), Jordan (Al-Shubiri et al., 2012), Hong

Kong (Yu, 2010), Spain (Reverte, 2009) and Portugal (Branco et al., 2014). These studies

support the positive relationship between size of a company and extent of sustainability

reporting. Perhaps it is because large corporations are more in limelight among general

public and government. These companies place greater weight on building their corporate

image and sustainability reporting is being used them as renowned measure to maintain

their public image and goodwill (Yu, 2010). Moreover, they have more financial

resources to implement the sustainability reporting framework. Also, Companies with

higher market capitalization can maintain their reputation in domestic as well as

international markets by disclosing more information. Thus, the null hypothesis H01 has

been rejected at 1% level of significance and the alternate hypothesis H1 has been

accepted.

H02: The profitability of a company as measured by its ROA or ROCE or RONW

has no significant impact on its sustainability disclosure score.

Corporate Attributes and Extent of Sustainability Reporting in India

177

H2: The profitability of a company as measured by its ROA or ROCE or RONW

has a significant impact on its sustainability disclosure score.

The multiple regression analysis depicts that the profitability of a company

measured in terms of ROA has significant negative relationship with sustainability

disclosure score. This result is in accordance with studies namely Jennifer and Taylor

(2007) and Lungu et al. (2011). The negative relationship of profitability with

sustainability disclosure score shows that the companies with high profits disclose less

sustainability information. This might be because companies have low disclosure because

they make profit at the cost of sustainability (Yu, 2010). Further, highly profitable

companies are able to build up internal resources for financing their future activities and

do not need to depend upon external resources for raising additional capital. Hence,

profitable companies develop a tendency of making less voluntary disclosures as

Sustainability (Chander, 1992). It also seems that the companies with higher profits are

focusing on their economic aspects and focus less on the betterment of society and

environment. Thus, the null hypothesis, H02 has been rejected at 5% level of significance

and the alternate hypothesis, H2 has been accepted.

H03: The growth of a company as measured in terms of its growth in total assets

has no significant impact on its sustainability disclosure score.

H3: The growth of a company as measured in terms of its growth in total assets

has a significant impact on its sustainability disclosure score.

The multiple regression analysis reveals that the growth measured in terms of

total assets has significant negative relationship with sustainability disclosure score.

Company’s growth depend upon the subsistence of rising markets and entry into fresh but

profitable markets. In both these circumstances higher level of information disclosure

may expose the reality of business opportunities to their counterparts and this will result

in potential disadvantage in terms of proprietary cost. Perhaps for this reason the extent

of voluntary disclosure is estimated to be negatively related to the growth rate of

company (Prencipe, 2010). Moreover, it might be because of the economic growth as the

priority of these companies that they put their financial resources in building up their

assets like a pure economic organization. Hence, these companies initiate less to promote

Corporate Attributes and Extent of Sustainability Reporting in India

178

sustainability. Thus, the null hypothesis H03 has been rejected at 5% level of significance

and the alternate hypothesis H3 has been accepted.

H04: The leverage of a company as measured by its debt-equity ratio has no

significant impact on its sustainability disclosure score.

H4: The leverage of a company as measured by its debt-equity ratio has a

significant impact on its sustainability disclosure score.

The multiple regression analysis specifies negative and significant association

between leverage of a company and sustainability disclosure score. This negative

relationship of leverage with sustainability disclosure score shows that the corporations

whose capital structure includes high debt content report comparatively lesser

information about its social and environmental efforts than companies with low debt. The

disclosure is expected to reduce with the increase of leverage because leverage helps to

control the free cash flow problem. Also, the agency costs of debt are monitored through

restrictive debt covenants in debt agreements rather greater reporting of information in

the annual reports (Jensen, 1986). Previous empirical studies have also shown mixed

results on the relationship between leverage and sustainability disclosure. Our results are

similar to Bhayani (2012), Birt (2012), Ghosh (2013) and Branco et al. (2014), who

observed a significant negative relationship between the extent of sustainability reporting

and leverage, whereas Ho and Wong (2001), Rahman and Widyasari (2008), Hoorik

(2009), Jennifer and Taylor (2007) observed an insignificant relationship between these

variables. Hence the null hypothesis H04 has been rejected at 5% level of significance and

the alternate hypothesis H4 has been accepted for the purpose of current study.

H05: The listing category of a company has no significant impact on its

sustainability disclosure score.

H5: The listing category of a company has a significant impact on its

sustainability disclosure score.

The results of multiple regression analysis exhibits that the corporations listed as

A category on the BSE do not have significant impact on the extent of sustainability

disclosure in comparison to companies listed under other categories namely B, S, T, TS

and Z. It is in line with evidence advanced by literature as suggested by Buzby (1975)

Corporate Attributes and Extent of Sustainability Reporting in India

179

and Mahajan and Chander (2007). The reason being that all sample companies are

renowned and have strong market base both in Indian and foreign stock exchanges. Thus,

H05 has been accepted and alternatively H5 has been rejected.

H06: The age of a company has no significant impact on its sustainability

disclosure score.

H6: The age of a company has a significant impact on its sustainability disclosure

score.

The multiple regression analysis explains that the age of a company has positive

association with sustainability disclosure score and is significant at 5 percent level. It

seems that old firms might have improved their financial reporting practices over time

(Alsaeed, 2006). Further, Ghosh (2013) observed that older companies report more about

their sustainability performance. It seems they might have fulfilled their economic goals

and built sufficient resources and surpluses to report on sustainability. It also offers them

a competitive edge for their sustenance amongst their younger counterparts. The results

of this study are in consonance with those of the past research (Prencipe, 2003; Al-

Shubiri et al. 2012). Therefore, H06 has been rejected at 5 percent level of significance,

accepting alternate hypothesis H6.

H07: The nationality of a company has no significant impact on its sustainability

disclosure score.

H7: The nationality of a company has a significant impact on its sustainability

disclosure score.

The results of multiple regression analysis shows a positive association between

nationality and sustainability disclosure score and is significant at 1% level of

significance. It implies that the companies which are extending their operations

multinationally disclose more information about its sustainability performance in order to

fulfill the requirements of both domestic and international stakeholders. This could be

due to the fact that these companies are internationally recognized. Therefore,

governments and public also lay emphasis on their comprehensive disclosures practices.

These practices are essential for them to sustain their repute. The failure to accomplish

the informational needs of the users by the company raises doubts about the competence

Corporate Attributes and Extent of Sustainability Reporting in India

180

of the company. It is also predicted by Al-Shammari (2008) that companies equipped

with greater international activities report supplementary information as compared to

companies which cater only to local operations. Companies which have multinational

operations are required to increase their voluntary reporting in order to mark their

international presence in the eyes of stakeholders and this is considered as a good signal

(Oliveira et al. 2006). So, nationality has a positive and significant impact on the

sustainability disclosure score. Thus, H07 has been rejected at 1% level of significance

and H7 has been accepted.

H08: The board size of a company has no significant impact on its sustainability

disclosure score.

H8: The board size of a company has a significant impact on its sustainability

disclosure score.

The results of multiple regression analysis found that board size is not related to

the sustainability disclosure score. As the board size increases, the board's capacity for

monitoring also increases. But there are certain disadvantages related with larger board

size. Larger board size increases the innate cost of distorted communication and delayed

decision making (John and Senbet, 1998). Also board size and board quality are different.

The efficiency of board’s working is important rather than just its size (Uyar et al., 2013).

Therefore, H08 has been accepted. Thus, it is not a predictor of sustainability disclosure

score as found by final regression equation.

H09: The board independence of a company has no significant impact on its

sustainability disclosure score.

H9: The board independence of a company has a significant impact on its

sustainability disclosure score.

The results of multiple regression analysis found that board independence is not

related to the sustainability disclosure score. It means that the number of independent

directors has no remarkable effect on sustainability information disclosure level. As

pointed by Ho and Wang (2001), that independent directors are not actively forcing the

company to disclose more of the non mandatory information. And this is in line with

Corporate Attributes and Extent of Sustainability Reporting in India

181

evidence advanced by literature (Ho and Wang, 2001; Lopes and Rodrigues, 2007; Kent

and Monem, 2008; Xiang, 2009). Thus, H09 is accepted and H9 is rejected.

H010: The advertising intensity of a company has no significant impact on its

sustainability disclosure score.

H10: The advertising intensity of a company has a significant impact on its

sustainability disclosure score.

The results of multiple regression analysis found that advertising intensity has

negative association with the sustainability disclosure score and is significant at 1% level.

It shows that companies going for selling, advertisement and distribution activities are

resorting less towards sustainability reporting. Advertising oriented companies invest

their resources on generating product differentiation, building customer loyalty and

enhancing brand image. These companies do not like to spend exorbitantly on non

mandatory disclosures as sustainability. Thus, H010 has been rejected at 1% level of

significance and H10 has been accepted.

H011: The nature of industry to which a company belongs has no significant impact

on its sustainability disclosure score.

H11: The nature of industry to which a company belongs has a significant impact

on its sustainability disclosure score.

The results of multiple regression analysis indicate a significant association

between nature of industry and sustainability disclosure. Results reveal that Oil & Gas

and Software, IT & ITES are significant at 5% level while Cement and Construction is

significant at 10% level. Yu (2010) stated that Oil & Gas companies disclose more

information on the social contributions in order to sustain their public image and

goodwill. Oil and Gas industry operations also have potential impacts on the environment

(Tronkina, 2010). Therefore, companies in these industries i.e. with heavy environmental

impacts are expected to be subject to significantly more stakeholder pressure regarding

their environmental performance, and so would be expected to display a greater degree of

disclosure activism (Reverte, 2009). Even, Meek et al. (1995) emphasized that the

companies in certain industries namely Oil, Chemicals and Mining are more active to

report non-financial information for example, related to the environment in order to show

Corporate Attributes and Extent of Sustainability Reporting in India

182

their greater concern towards social accountability issues. Further the reason of high

sustainability disclosure in Software, IT & ITES industry is supported by the view that

the inappropriate and inefficient usage of energy in this industry causes release of

dangerous acids and toxic compounds which are harmful to human health (Adamson et

al., 2005). So, this industry undertakes more sustainable efforts to show its concern for

society. Cement and Construction industry has also realized the importance of

sustainability as it involves Carbon emissions and global cement manufacture accounts

for about five percent of all man-made CO2 emissions. In order to address the

sustainability issues the leading cement companies have created the Cement

Sustainability Initiative (CSI), under the support of the World Business Council for

Sustainable Development (WBCSD, 2012). Thus, in simple words it can be said that the

category of industry to which a particular company belongs definitely affects its

sustainability disclosure (Jennifer and Taylor, 2007; Al-Shammari, 2008); Hoorik, 2009;

Lattemann et al., 2009; Yu, 2010; Michelon, 2011; Ghosh, 2013)

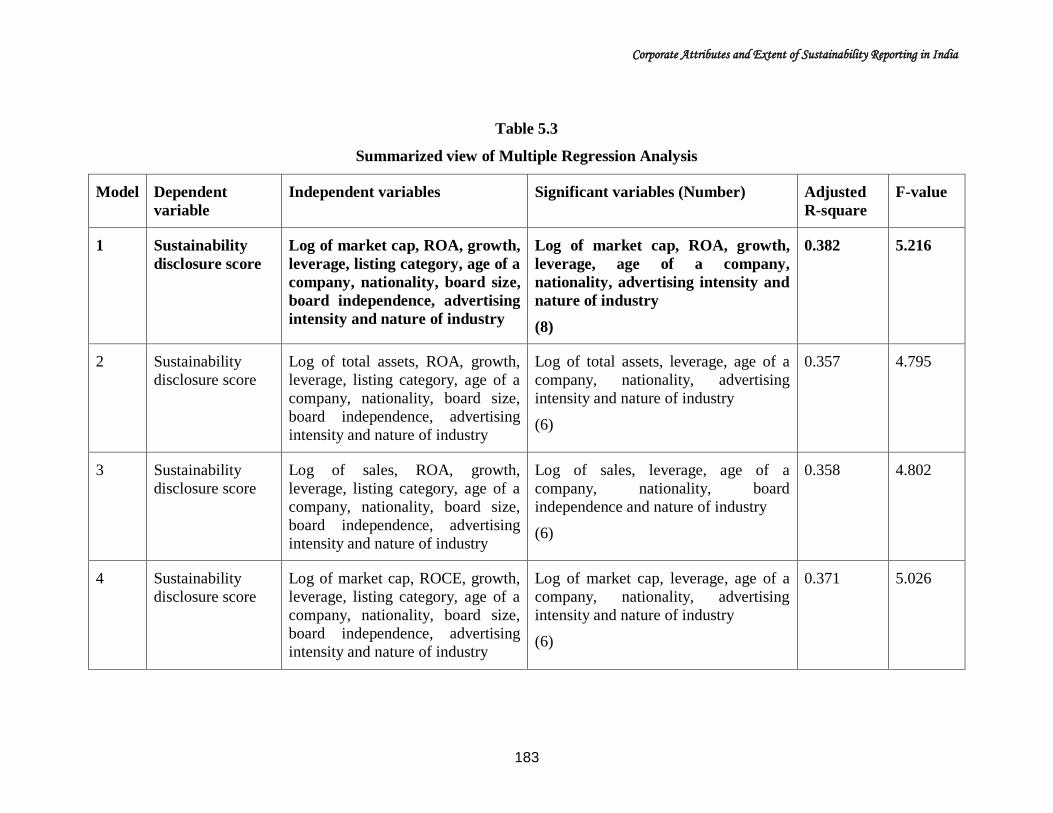

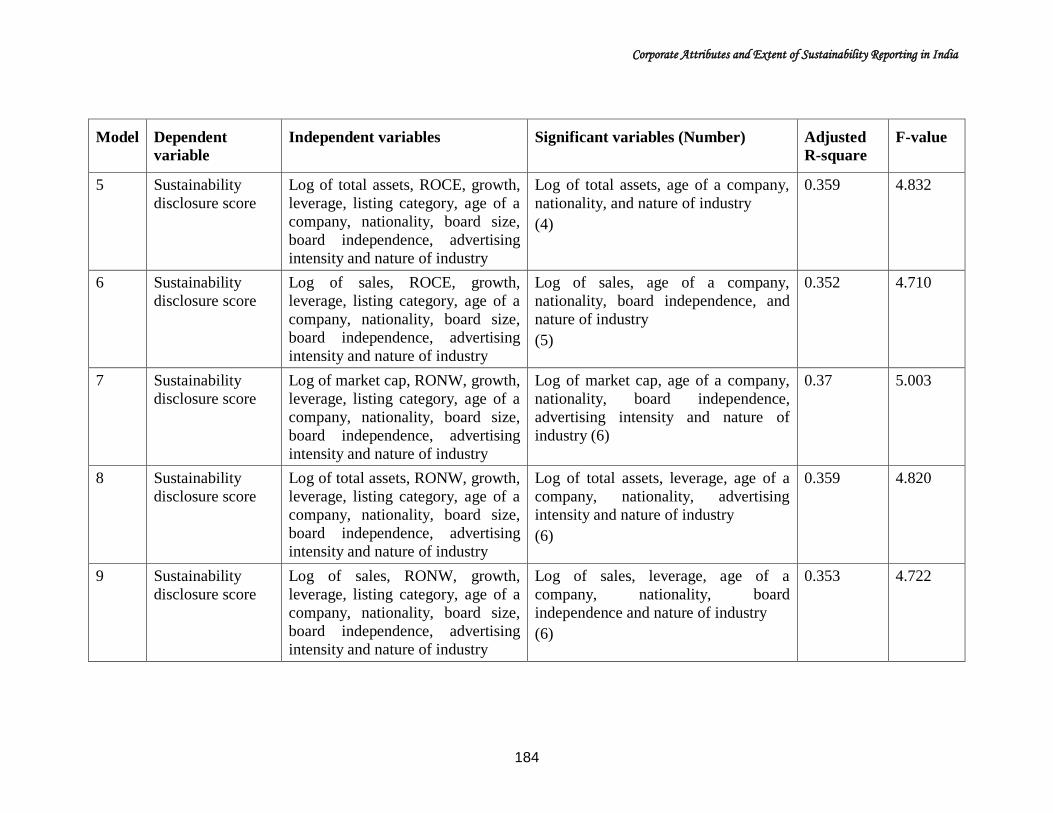

5.3 CONCLUSION

The preceding analysis explains the impact of various corporate attributes on the

sustainability reporting practices of selected Indian companies and their association. The

findings can be summarized as shown in table 5.3.

Corporate Attributes and Extent of Sustainability Reporting in India

183

Table 5.3

Summarized view of Multiple Regression Analysis

Model Dependent

variable

Independent variables Significant variables (Number) Adjusted

R-square

F-value

1 Sustainability

disclosure score

Log of market cap, ROA, growth,

leverage, listing category, age of a

company, nationality, board size,

board independence, advertising

intensity and nature of industry

Log of market cap, ROA, growth,

leverage, age of a company,

nationality, advertising intensity and

nature of industry

(8)

0.382 5.216

2 Sustainability

disclosure score

Log of total assets, ROA, growth,

leverage, listing category, age of a

company, nationality, board size,

board independence, advertising

intensity and nature of industry

Log of total assets, leverage, age of a

company, nationality, advertising

intensity and nature of industry

(6)

0.357 4.795

3 Sustainability

disclosure score

Log of sales, ROA, growth,

leverage, listing category, age of a

company, nationality, board size,

board independence, advertising

intensity and nature of industry

Log of sales, leverage, age of a

company, nationality, board

independence and nature of industry

(6)

0.358 4.802

4 Sustainability

disclosure score

Log of market cap, ROCE, growth,

leverage, listing category, age of a

company, nationality, board size,

board independence, advertising

intensity and nature of industry

Log of market cap, leverage, age of a

company, nationality, advertising

intensity and nature of industry

(6)

0.371 5.026

Corporate Attributes and Extent of Sustainability Reporting in India

184

Model Dependent

variable

Independent variables Significant variables (Number) Adjusted

R-square

F-value

5 Sustainability

disclosure score

Log of total assets, ROCE, growth,

leverage, listing category, age of a

company, nationality, board size,

board independence, advertising

intensity and nature of industry

Log of total assets, age of a company,

nationality, and nature of industry

(4)

0.359 4.832

6 Sustainability

disclosure score

Log of sales, ROCE, growth,

leverage, listing category, age of a

company, nationality, board size,

board independence, advertising

intensity and nature of industry

Log of sales, age of a company,

nationality, board independence, and

nature of industry

(5)

0.352 4.710

7 Sustainability

disclosure score

Log of market cap, RONW, growth,

leverage, listing category, age of a

company, nationality, board size,

board independence, advertising

intensity and nature of industry

Log of market cap, age of a company,

nationality, board independence,

advertising intensity and nature of

industry (6)

0.37 5.003

8 Sustainability

disclosure score

Log of total assets, RONW, growth,

leverage, listing category, age of a

company, nationality, board size,

board independence, advertising

intensity and nature of industry

Log of total assets, leverage, age of a

company, nationality, advertising

intensity and nature of industry

(6)

0.359 4.820

9 Sustainability

disclosure score

Log of sales, RONW, growth,

leverage, listing category, age of a

company, nationality, board size,

board independence, advertising

intensity and nature of industry

Log of sales, leverage, age of a

company, nationality, board

independence and nature of industry

(6)

0.353 4.722

Corporate Attributes and Extent of Sustainability Reporting in India

185

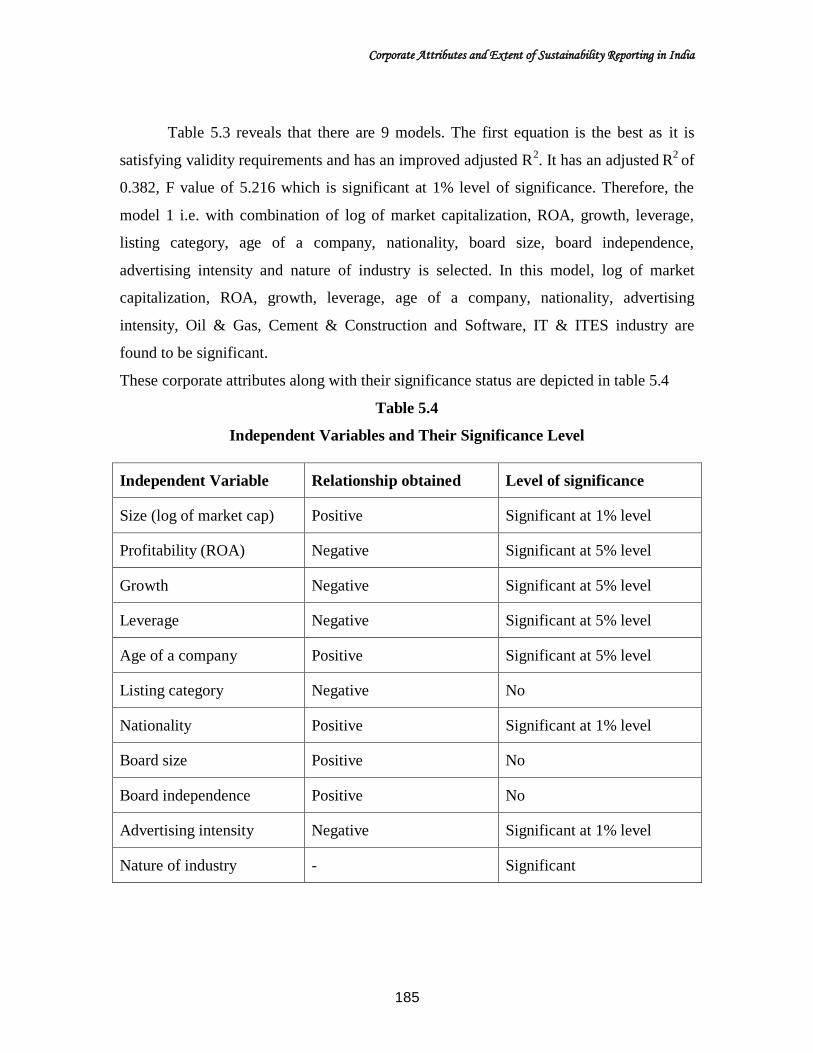

Table 5.3 reveals that there are 9 models. The first equation is the best as it is

satisfying validity requirements and has an improved adjusted R2. It has an adjusted

R

2 of

0.382, F value of 5.216 which is significant at 1% level of significance. Therefore, the

model 1 i.e. with combination of log of market capitalization, ROA, growth, leverage,

listing category, age of a company, nationality, board size, board independence,

advertising intensity and nature of industry is selected. In this model, log of market

capitalization, ROA, growth, leverage, age of a company, nationality, advertising

intensity, Oil & Gas, Cement & Construction and Software, IT & ITES industry are

found to be significant.

These corporate attributes along with their significance status are depicted in table 5.4

Table 5.4

Independent Variables and Their Significance Level

Independent Variable Relationship obtained Level of significance

Size (log of market cap) Positive Significant at 1% level

Profitability (ROA) Negative Significant at 5% level

Growth Negative Significant at 5% level

Leverage Negative Significant at 5% level

Age of a company Positive Significant at 5% level

Listing category Negative No

Nationality Positive Significant at 1% level

Board size Positive No

Board independence Positive No

Advertising intensity Negative Significant at 1% level

Nature of industry - Significant

Corporate Attributes and Extent of Sustainability Reporting in India

186

Table 5.4 highlights that size measured in terms of log of market capitalization

and nationality are positively significant at 1% level, while age and nature of industry

(Software, IT & ITES and Oil & Gas) significant at 5% level. Companies with large size,

older, multinational operations and belonging to Software, IT & ITES and Oil & Gas

industry have significant sustainability disclosure. However, advertising intensity is

negatively significant at 1% level while ROA, leverage, growth are negatively significant

at 5% level. This shows that the company’s profits, leverage, growth and advertising

intensity are negatively related with the extent of sustainability disclosure. Other

variables were found to be insignificant.

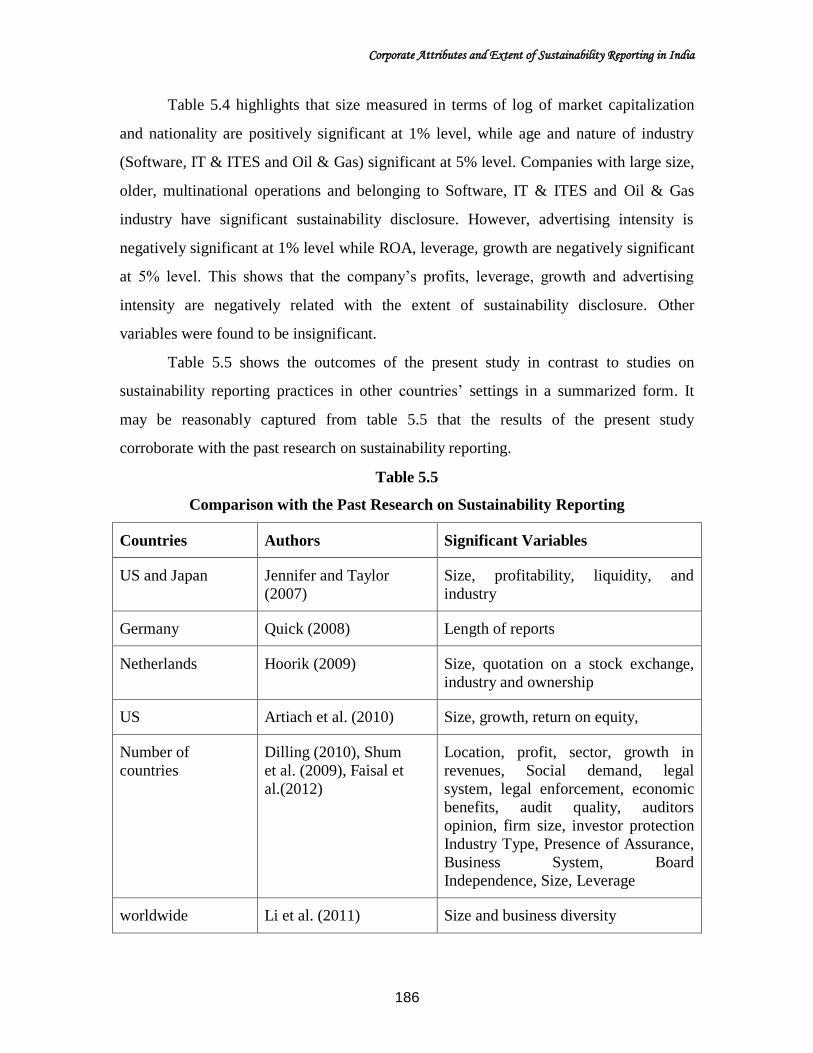

Table 5.5 shows the outcomes of the present study in contrast to studies on

sustainability reporting practices in other countries’ settings in a summarized form. It

may be reasonably captured from table 5.5 that the results of the present study

corroborate with the past research on sustainability reporting.

Table 5.5

Comparison with the Past Research on Sustainability Reporting

Countries Authors Significant Variables

US and Japan Jennifer and Taylor

(2007)

Size, profitability, liquidity, and

industry

Germany Quick (2008) Length of reports

Netherlands Hoorik (2009) Size, quotation on a stock exchange,

industry and ownership

US Artiach et al. (2010) Size, growth, return on equity,

Number of

countries

Dilling (2010), Shum

et al. (2009), Faisal et

al.(2012)

Location, profit, sector, growth in

revenues, Social demand, legal

system, legal enforcement, economic

benefits, audit quality, auditors

opinion, firm size, investor protection

Industry Type, Presence of Assurance,

Business System, Board

Independence, Size, Leverage

worldwide Li et al. (2011) Size and business diversity

Corporate Attributes and Extent of Sustainability Reporting in India

187

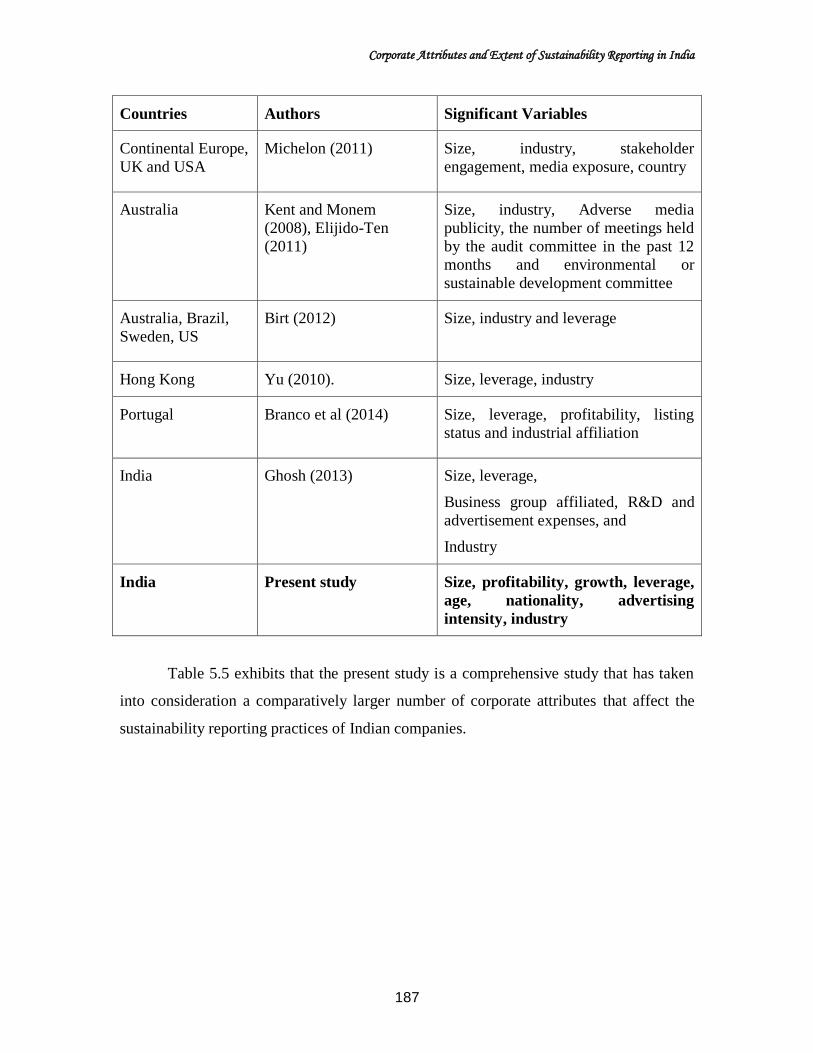

Countries Authors Significant Variables

Continental Europe,

UK and USA

Michelon (2011)

Size, industry, stakeholder

engagement, media exposure, country

Australia Kent and Monem

(2008), Elijido-Ten

(2011)

Size, industry, Adverse media

publicity, the number of meetings held

by the audit committee in the past 12

months and environmental or

sustainable development committee

Australia, Brazil,

Sweden, US

Birt (2012)

Size, industry and leverage

Hong Kong Yu (2010). Size, leverage, industry

Portugal Branco et al (2014)

Size, leverage, profitability, listing

status and industrial affiliation

India Ghosh (2013) Size, leverage,

Business group affiliated, R&D and

advertisement expenses, and

Industry

India Present study Size, profitability, growth, leverage,

age, nationality, advertising

intensity, industry

Table 5.5 exhibits that the present study is a comprehensive study that has taken

into consideration a comparatively larger number of corporate attributes that affect the

sustainability reporting practices of Indian companies.