Embed Size (px)

Citation preview

68

CHAPTER-V

EXTENT OF INTANGIBLE ASSETS DISCLOSURE

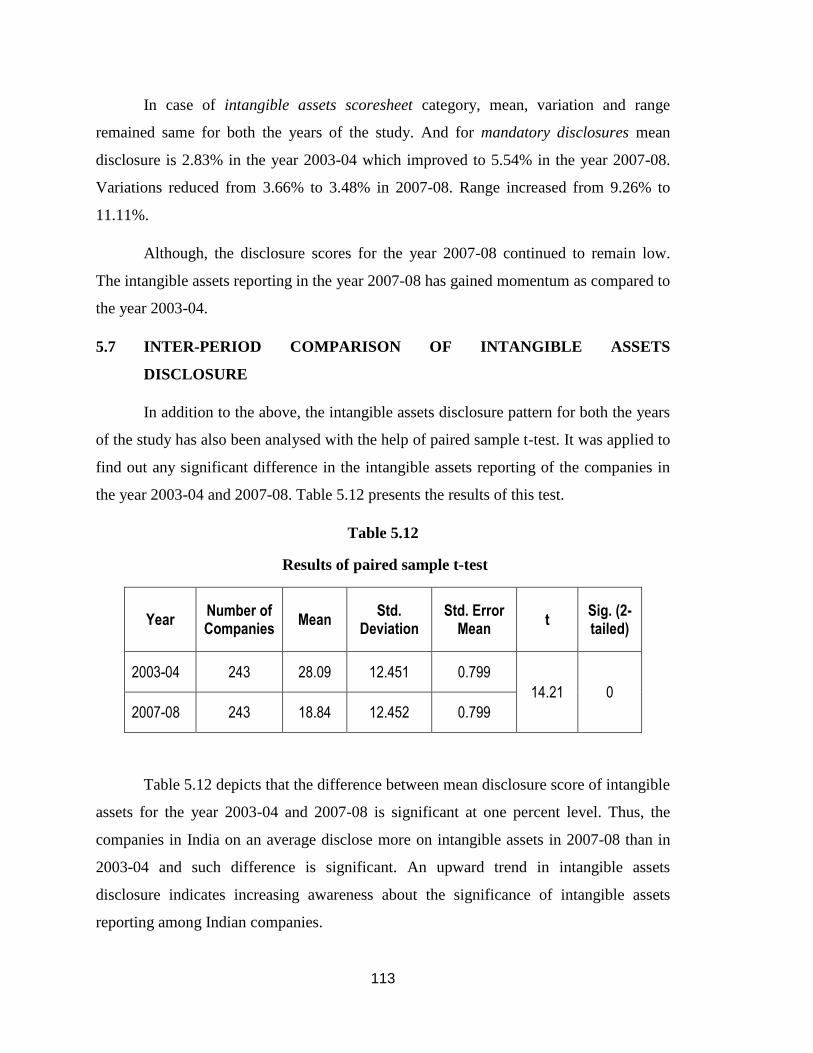

This chapter discusses the extent of intangible assets disclosure by the companies. The

extent of disclosure has been measured in terms of attribute-wise disclosure, category-wise

disclosure and company-wise disclosure by applying intangible assets disclosure index to the

annual reports of the sample companies in India for the years 2003-04 and 2007-08. The nature

of intangible asset disclosure has also been studied

This chapter has been divided into two sections. Section I discusses the attribute-wise

disclosure, category-wise disclosure and nature of disclosure. Section II deals with the

company-wise disclosure of intangible assets information presented in the annual reports of

selected sample companies in India for both the years of study.

SECTION – I

5.1. ATTRIBUTE-WISE DISCLOSURE IN ANNUAL REPORTS

This section explains the attribute-wise analysis for each and every category of

intangible assets disclosure index1. The intangible assets disclosure index consists of five main

categories, out of which four relate to voluntary intangible assets disclosure and one relate to

disclosure requirements as per Accounting Standard-26 on Intangible assets.

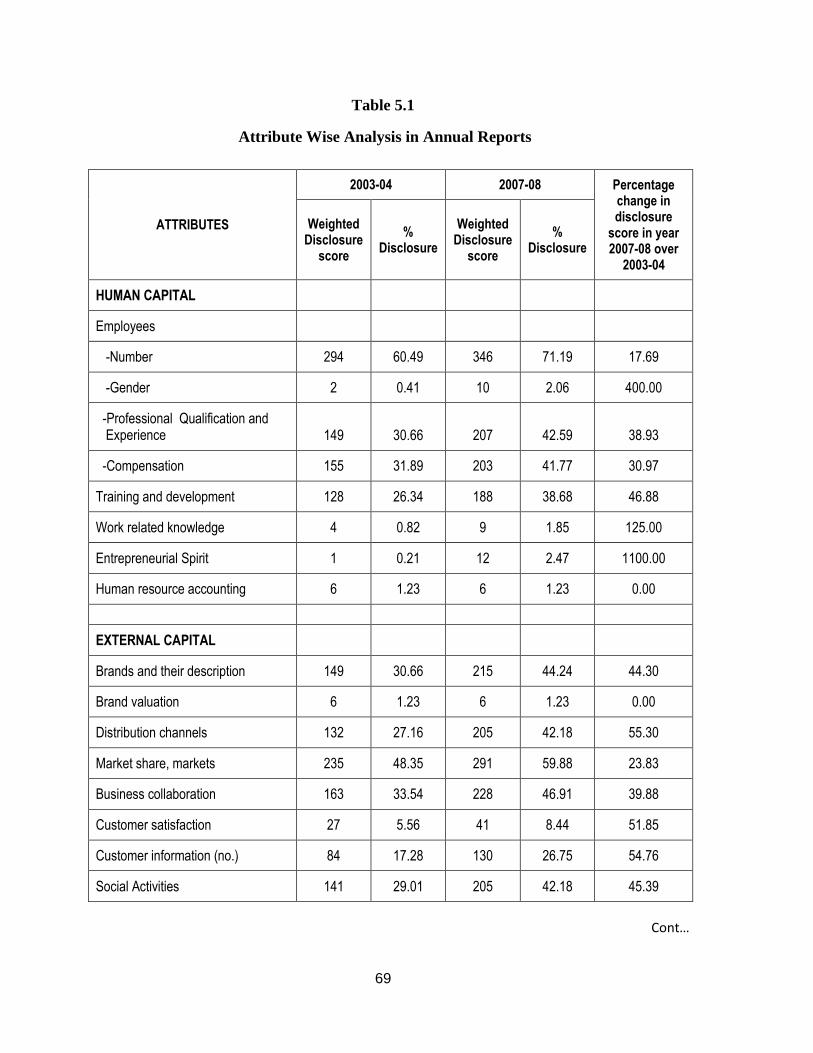

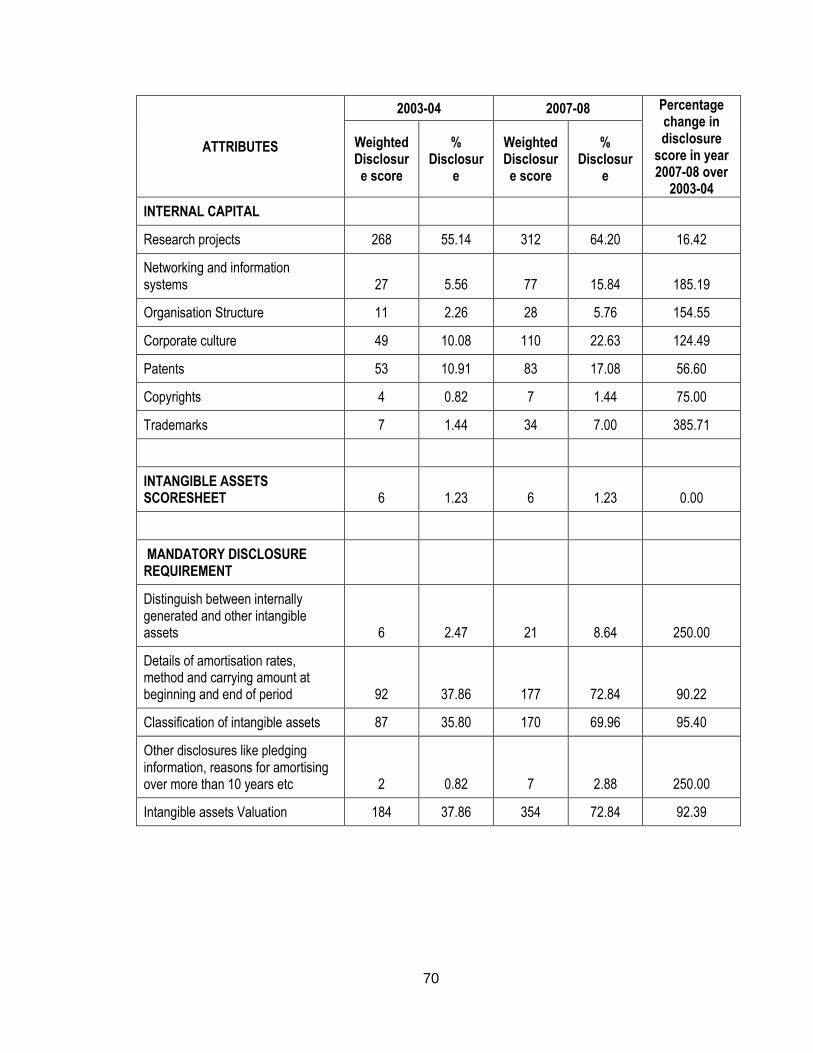

Table 5.1 presents the attribute-wise disclosure both in absolute figures as well as in

percentages for the years 2003-04 and 2007-08 respectively. The attribute-wise disclosure

score has been calculated for each attribute included in the intangible assets disclosure index,

by dividing the total weighted disclosure score attained for that attribute with the maximum

weighted disclosure score.

The maximum disclosure score for attributes in human capital, external capital,

internal capital, intangible assets scoresheet category and for attribute intangible assets

valuation2 in mandatory disclosure requirement category is 486 (243 companies multiply with

maximum score of 2). The maximum score for remaining attributes in mandatory disclosure

requirement category is 243 (243 companies multiply with maximum score of 1).

For example, the training and development attribute in human capital category for

the year 2003-04 has weighted disclosure score of 128 and the percentage disclosure of

26.34% (score attained 128 divided by 486 maximum disclosure score).

1 For details, see chapter III, Database and Research Methodology, pp. 40. 2 Intangible assets valuation falls in the Mandatory disclosure requirement category. A score of 0 or 2 has been given to this

attribute as valuation has to be in monetary terms and cannot be qualitatively stated.

69

Table 5.1

Attribute Wise Analysis in Annual Reports

ATTRIBUTES

2003-04 2007-08 Percentage change in disclosure

score in year 2007-08 over

2003-04

Weighted Disclosure

score

% Disclosure

Weighted Disclosure

score

% Disclosure

HUMAN CAPITAL

Employees

-Number 294 60.49 346 71.19 17.69

-Gender 2 0.41 10 2.06 400.00

-Professional Qualification and Experience 149 30.66 207 42.59 38.93

-Compensation 155 31.89 203 41.77 30.97

Training and development 128 26.34 188 38.68 46.88

Work related knowledge 4 0.82 9 1.85 125.00

Entrepreneurial Spirit 1 0.21 12 2.47 1100.00

Human resource accounting 6 1.23 6 1.23 0.00

EXTERNAL CAPITAL

Brands and their description 149 30.66 215 44.24 44.30

Brand valuation 6 1.23 6 1.23 0.00

Distribution channels 132 27.16 205 42.18 55.30

Market share, markets 235 48.35 291 59.88 23.83

Business collaboration 163 33.54 228 46.91 39.88

Customer satisfaction 27 5.56 41 8.44 51.85

Customer information (no.) 84 17.28 130 26.75 54.76

Social Activities 141 29.01 205 42.18 45.39

Cont…

70

ATTRIBUTES

2003-04 2007-08 Percentage change in disclosure

score in year 2007-08 over

2003-04

Weighted Disclosure score

% Disclosur

e

Weighted Disclosure score

% Disclosur

e

INTERNAL CAPITAL

Research projects 268 55.14 312 64.20 16.42

Networking and information systems 27 5.56 77 15.84 185.19

Organisation Structure 11 2.26 28 5.76 154.55

Corporate culture 49 10.08 110 22.63 124.49

Patents 53 10.91 83 17.08 56.60

Copyrights 4 0.82 7 1.44 75.00

Trademarks 7 1.44 34 7.00 385.71

INTANGIBLE ASSETS SCORESHEET 6 1.23 6 1.23 0.00

MANDATORY DISCLOSURE REQUIREMENT

Distinguish between internally generated and other intangible assets 6 2.47 21 8.64 250.00

Details of amortisation rates, method and carrying amount at beginning and end of period 92 37.86 177 72.84 90.22

Classification of intangible assets 87 35.80 170 69.96 95.40

Other disclosures like pledging information, reasons for amortising over more than 10 years etc 2 0.82 7 2.88 250.00

Intangible assets Valuation 184 37.86 354 72.84 92.39

71

A brief look of the table 5.1 shows that disclosure score in the year 2007-08 over

the year 2003-04 has improved for all attributes except three (for these three attributes it

remained constant). There is also significant change in percentage disclosure score in

year 2007-08 as compared to year 2003-04.

5.1.1 HUMAN CAPITAL

This category highlights the employee-based value drivers for a company. Human

capital depends on the competence, intellectual ability, and attitudes of the organization’s

members. It is usually described as the gathered knowledge, skills and experiences that a

company’s employees possess. Human capital is a binding factor between the various

components of intangible assets. “Our ASSETS walk out of the door each evening. We

have to make sure that they come back the next morning," says Narayana Murthy, Non-

Executive Chairman and Chief Mentor of Infosys (Infosys Technologies Ltd., Annual

report 2007-08). When a company invests in human capital, it increases its own value,

gaining a sustainable long-run competitive advantage. This category has total of eight

attributes.

The disclosure of Number of employees of a company is an indication of its

strength. As can be seen from the table 5.1, in both years, Number of employees is the

most reported attribute in the category of human resources. It has highest weighted

disclosure score of 60.49% in 2003-04 and 71.19% in 2007-08. The disclosure on number

of employees aids in analysing the change in operations of the company, and results in

depicting future growth prospects and stability to its investors.

The next attribute of human capital is the gender of employees working in a

company. It is an information regarding proportion of men and women who are

professional employees. This information is vital as businesses are consistently

recognising that a higher percentage of professional women in an organization translate

into a more innovative workforce. Companies acknowledge the valuable contributions

made by women at different managerial roles due to their innate skill sets. The present

study reveals least reporting regarding this attribute. Disclosure score is 0.41% and

72

2.06% for 2003-04 and 2007-08 respectively. Infosys Technologies is flagship company

to report this attribute : “we are the first Indian IT company to set up a Diversity Office

for promoting diversity and inclusivity Our gender inclusivity model is an individually-

tailored combination of support systems, company practices, and management policies

under the umbrella of IWIN – Infosys Women’s Inclusivity Network. IWIN is devoted to

creating a gender-sensitive work environment and making us the Employer of Choice for

women.” (Infosys Technologies Ltd., Annual report 2007-08, p.9)

Professional qualification and experience is one of the most significant intangible

assets attribute among the human capital category. These people-based skills are essential

for operation and success of any organisation. They also depict quality of employees

working in an organisation. Disclosing information relating to educational qualification

of employees may signal to investors about high calibre management staff in the

company and superior hiring policies. However, only moderate disclosures of 30.66% in

2003-04 and 42.59% in 2007-08 have been made by the selected companies for this

attribute. This attribute is second most reported attribute in human capital category for

the year 2007-08 (Table 5.4).

The attribute Compensation has a weighted disclosure score of 31.89% in 2003-

04 which improved to 41.77% in 2007-08. The significance of this attribute can be

judged from the fact that the compensation given to employees in financial and non-

financial forms has positive impact on their performance and motivation. It also cements

in the development of other intangibles within the same category like employee

capabilities and employee satisfaction. Tata Steel Ltd. reported on this attribute as

“Having always focussed on people as the key resources, fair compensation has been an

area of importance. A market based benchmarking of compensation is undertaken to

ensure that Tata Steel remains employer of choice in all the countries in which it

operates.” (Tata Steel Ltd., Annual report 2007-08, p.65). Table 5.4 shows that this

attribute is the second most reported for the year 2003-04.

73

Training and development activities are very essential for a company to update

the professional skills and knowledge of its employees. Galbreath (2005) found that

intangible resources like skills and capabilities of employees have a higher contribution

to a company’s success than other tangible or intangible assets. . Disclosure regarding

training and development information in the annual reports gives its stakeholders an

evidence of company’s commitment to invest in its employees which influences its

performance and thereby shareholders return. For example Sterlite Industries India Ltd

discloses in its 2007-08 annual report “During 2007-08, Sterlite conducted 437 training

programmes, which averaged 50.43 hours of training per employee. In the same period,

HZL invested a total of 14,252 man-days in employee training: an average of 6.24 man-

days per executive and an average of 2.24 man-days of training across all categories.”

(Sterlite Industries India Ltd., Annual Report 2007-08, p.32) Keeping in mind this fact a

high disclosure was expected. However, for the year 2003-04, the disclosure of this

attribute was only 26.34% which increased to 38.68% in the year 2007-08.

Work related knowledge and entrepreneurial spirit which are eminent intangible

assets attributes to contribute towards value-creation in business and thus the wealth of

investors. However these attributes have hardly been reported by companies for both the

years of study. Low disclosure regarding entrepreneurial spirit of employees is in contrast

to the Guthrie and Petty (2000) study on Australian companies, where it was the most

frequently reported attribute of intellectual capital. In the present study most of

disclosures relating to this attribute are in qualitative form. Information in the annual

reports, regarding problem-solving approach, risk-taking attitude, client handling

techniques, innovative abilities of employees helps investors in judging the strengths of

an organisation.

Bata India Ltd. reported its entrepreneurial spirit as: “To develop the culture of

entrepreneurship, the Company has encouraged existing employees to take the new stores

as a franchisee”. (Bata India Ltd., Annual report 2007-08, p.14)

74

Thermax Ltd. reported that: “We foster an entrepreneurial spirit throughout our

businesses and value the ability to foresee business opportunities early in the cycle and

act on them swiftly. Whether it is developing organic growth projects, making strategic

acquisitions or creating entrepreneurs from within, we ensure an entrepreneurial spirit at

the heart of our workplace. I would like to see more of this in the company as we grow,

where people take ownership of new ideas, new ways of doing the same thing and new

business models” (Thermax Ltd., Annual report 2007-08, p. 4)

Ambuja Cements Ltd. reported on work- related knowledge of its employees as

“Our trouble shooting and maintenance teams at Rabriyawas deserve acknowledgement

for the manner in which they applied innovation and ideas. They solved the problem of

SLC fan vibration and stopped losses in clinker production, estimated at around Rs 13

crores.” (Ambuja cement Ltd., Annual report 2007-08, p.14).

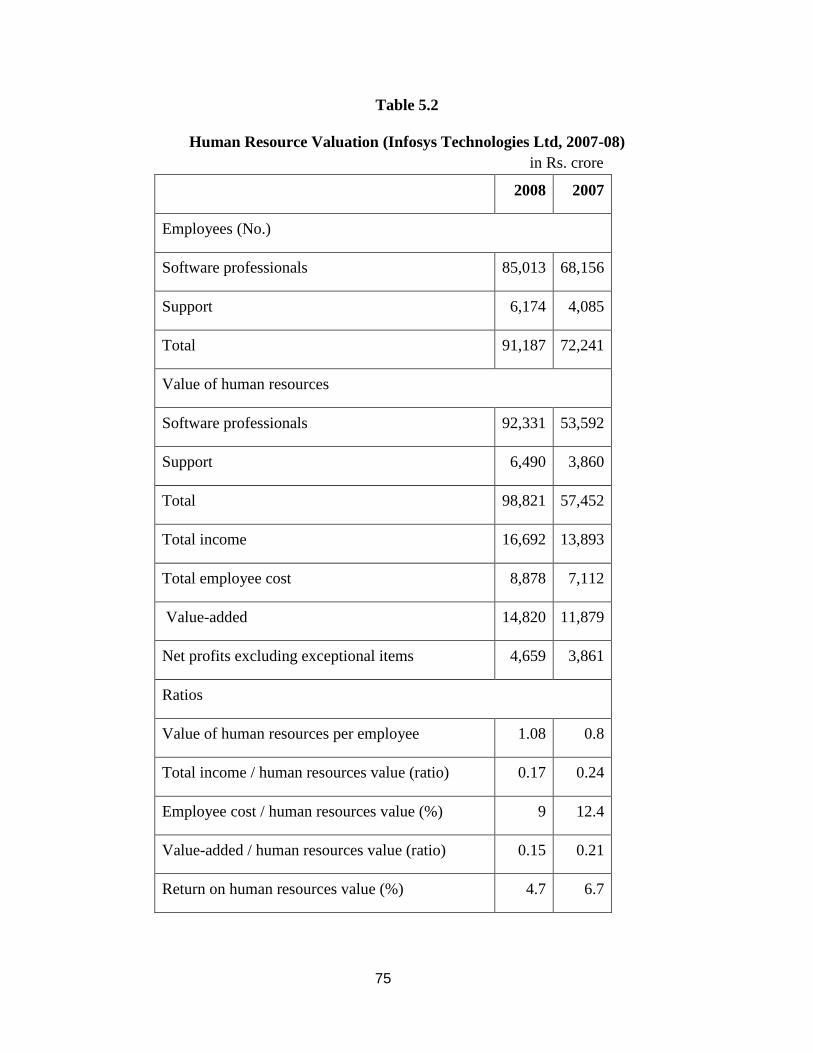

The disclosure regarding the final attribute human resource accounting in this

category is very low for both the years of the study. Only Infosys Technologies Ltd.,

Satyam Computer Services Ltd. and Infotech Enterprises Ltd. belonging to software

industry have disclosed this item as additional information to shareholders for the two

years of the study. The companies namely Infosys Technologies Ltd. and Satyam

Computer Services Ltd. have used Lev & Schwartz model for computing the human

resource value. Both the companies have given detailed disclosure of this information by

computing present value of future earnings of the employees (human resources) and

various ratios to evaluate it. Table 5.2 gives the summary of human resource valuation

from the annual report of Infosys Technologies Ltd.

75

Table 5.2

Human Resource Valuation (Infosys Technologies Ltd, 2007-08)

in Rs. crore

2008 2007

Employees (No.)

Software professionals 85,013 68,156

Support 6,174 4,085

Total 91,187 72,241

Value of human resources

Software professionals 92,331 53,592

Support 6,490 3,860

Total 98,821 57,452

Total income 16,692 13,893

Total employee cost 8,878 7,112

Value-added 14,820 11,879

Net profits excluding exceptional items 4,659 3,861

Ratios

Value of human resources per employee 1.08 0.8

Total income / human resources value (ratio) 0.17 0.24

Employee cost / human resources value (%) 9 12.4

Value-added / human resources value (ratio) 0.15 0.21

Return on human resources value (%) 4.7 6.7

76

5.1.2 EXTERNAL CAPITAL

This intangible assets category represents relationship of a company with its

customers. suppliers, business partners, industry associates, market channels, investors,

society etc. This category is classified into eight sub-categories which are brands and

their description, brand valuation, distribution channels, markets & market share,

business collaboration, customers, customer satisfaction and social activities.

In today’s market place, brands have primary importance to businesses. Many of

the world’s biggest companies derive more than half of their value because of their

brands. Building strong brands through effective marketing can have a very positive

impact on company’s share price as well. Also development of brands helps companies in

enhancing their market share by securing repeated customer orders and building brand

loyalty. Companies in India have increased the use of annual reports as a medium to

inform outside world about their brands. Information disclosure regarding this has

incremented from 30.66% in 2003-04 to 44.24% in 2007-08. Widespread distribution of

annual reports, have made them as an effective means, by which companies can exchange

detailed information regarding all its brand portfolio, number of brands, brand logos etc.

in an economical and effective way. An appropriate example of this is Reliance Industries

Ltd. annual report for the year 2007-08 (Page 2) where they have given list of all its

brands and products.

Brand valuation is a tool employed by companies to manage their brands in order

to deliver optimal and sustainable value to its stakeholders. A brand’s value constitutes

to be an important component in the value of a company. It is a powerful way of

identifying areas of strength and weakness for the brand. Brand valuation has become a

means for communicating about brand in shareholder value terms, both internally and

externally. Investors nowadays prefer greater understanding and disclosure of brand

valuation and marketing performance information to improve their investment decisions.

Despite the significance of its communication externally, only Infosys Technologies Ltd.

and Satyam Computer Services Ltd. from software industry and Alembic Ltd. from

pharmaceutical industry have disclosed their brand valuation information in their annual

reports for the years 2003-04 and 2007-08 respectively. Low disclosures regarding brand

77

valuation in annual reports could be inferred from the fact that companies yet do not

realise the significance of brand value in determining its true overall value. The other

reasons could be that companies do not want to share this information with its

stakeholders because of its brand value being low. Satyam Computers Services Ltd.

reported on brand valuation as

“As on March 31, 2008, the Brand value of the Company was Rs. 9,873 crores (US$2,467

mn.), as computed below:

i) PBIT reduced by non-branded income was taken as profit for brand valuation.

ii) Profits of previous two years were considered at present value and weightage

factor was applied to arrive at weighted profit.

iii) 5% of average capital employed was provided for non brand purposes.

iv) Income Tax at current rate was provided.

v) Brand multiple was estimated based on certain parameters and internal

evaluation.”

Distribution channels are the means used to transfer goods or services from its

manufacturer to its end user. A strong distribution network constitutes to be an important

intangible asset for an organisation, as it signifies regular sales and constant orders.

Distribution has emerged as one of the few remaining areas where companies can build

and sustain competitive advantage. The information disclosure regarding distribution

channels by companies was 27.16% in 2003-04. With a 55.30% increase, it was 42.18%

in the year 2007-08. For example, Aditya Birla Nuvo Ltd. quotes “To enhance its

competitive strength, BSLAMC more than doubled its distribution network to reach 78

branches and over 17,500 financial advisors in March 2008.” (Aditya Birla Nuvo Ltd.,

Annual report 2007-08, p.16)

Another vital attribute in external capital category, is the market where a company

operates and its market share. Market share can be defined as the percentage of all sales

within a market that is held by one brand / product or company. Information concerning

markets and market share of a company helps its stakeholders to assess its products,

customers, regional coverage, strengths, longevity, growth potential etc. Disclosure

regarding this attribute is 48.35% in 2003-04. It increased to 59.88% in 2007-08. Within

78

the external capital category, this attribute is the most frequently reported attribute for

both years of the study (Table 5.4). The high disclosure could be due to the fact that

information regarding this attribute is usually collected by company’s marketing

department. Thus, the marginal cost of preparing these data for external reporting

purposes is low.

Business collaborations is the second most reported intangible assets attribute in

this category, for both the years of study (Table 5.4). The importance placed to business

collaborations is not surprising as mutual alliances and other forms of collaborative

arrangements, of an organisation with its industry associates or strategic partners, are

becoming common way of conducting business and implementing growth strategies.

They also constitute to be an important source of competitive advantage. These joint

ventures help an organisation in improving its performance, increasing geographical

presence and diversifying into related businesses by developing alliances that

complement their core competencies. They also assist in gaining synergies in internal

operations and external opportunities. Effective reporting about business alliances

undertaken by a company helps its stakeholders in making sound investment decisions.

Disclosures regarding this attribute are 33.54% in 2003-04 which increased to 46.91% in

2007-08. Business collaboration is the top-scoring attribute in similar researches by

Guthrie et al (2006), Sujan & Abeysekera (2007) and Woodrock & Whiting (2009).

Also many companies equate their competitive advantage with their capacity to

deliver high levels of customer satisfaction. The products are changing, and so are

consumers. The companies have to make great efforts to improve and maintain good

relationships with their clients, who are increasingly demanding improved products and

services with accelerated delivery times and at lower prices. Satisfied customers are

challenging yet important intangible assets for an organisation For example Aruna

Sundarajan (Secretary IT Government of Kerela) appreciates Tulip Telecom Ltd “I am

extremely satisfied with the network rolled out by Tulip Telecom Limited Ltd and wish

them continuous success in this field -” (Tulip Telecom ltd., Annual report 2007-08, p.4).

But companies make meagre disclosure regarding this attribute in their annual reports.

Only 5.56% disclosure score in 2003-04 and 8.44% in 2007-08 has been reported

79

regarding this attribute. This non-disclosure pattern may be taken to indicate that only

companies with good customer feedbacks wants to mention this fact in their annual

report.

Further the information with regard to customers has a disclosure of 17.28% in

the year 2003-04 and 26.75% in the year 2007-08. This information helps the investors to

know about the major customers, reliance on major customers, customer base widespread

ness, new customers added, geographical distribution of customers etc of the respective

company. The investor analyses this information to draw conclusions on reputation,

credit worthiness and forward sales of the company. Though this information is

significant to investors its disclosure is not very high. The possible reason for these low

disclosures could be confidentiality of the information from its competitors. An

illustration of this attribute from the annual report of I-flex Solutions Ltd. is “Our

operations and business depend on our relationships with a number of large customers.

Our Revenues from our top ten customers for fiscal 2008 were at 32% and 26% for fiscal

year 2007, as a percentage of our total revenues. The top-ten customers in our Services

Business contributed 42% of the total services revenues and the top ten customers in the

Products Business contributed 36% of the total products revenues during fiscal 2008.” (I-

flex Solutions ltd., Annual report 2007-08, p. 44).

As a social citizen, it is the duty of every company to be sensitive towards societal

needs or meet its social responsibilities. Companies should also contribute towards

environment protection and community development. For discharging the above

responsibilities companies are focusing on creation of healthcare, food security,

education and income generation, through the development of rural infrastructure,

empowerment and community outreach programmes. Fulfilling societal needs helps

company in attracting investors, recruiting employees, creating positive press image,

developing new products and services etc. It also makes a company more competitive by

reducing risk of sudden damage to reputation and sales. There is 29.01% disclosure

related to this attribute in the annual reports for the year 2003-04, which increased to

42.18% in 2007-08. Few companies have disclosed it in details as separate report

80

annexed as additional information to the shareholders while others have disclosed it as

information annexed to the management discussion and analysis and director’s report

section of the annual report under the heading social concerns. A large number of

companies have also attached photographs of these corporate responsibility initiatives.

Tata Steel Ltd. reported its social responsibility as “The Tata Steel Group’s focus

in the area of corporate sustainability includes Social Sustainability; Environmental

Sustainability; Social Welfare; Sport; and Inclusive Growth. This last ensures that the

Group’s successes are shared by all its constituents and stakeholders.” (Tata Steel Ltd.,

Annual Report 2007-08, p- 67)

Annual report of Hindalco industries Ltd. mentions that. “As a Group we have

been and continue to be extremely sensitive to societal needs. In our own small way, we

try to bring in some relief and make a difference to the lives of the weaker sections of

society who live close to our plants. We try to provide health care and raise life

expectancy, and reduce infant mortality. Through our endeavours in education, we lift

literacy rates. Through empowerment and training processes, we promote sustainable

livelihood.” (Hindalco Industries Ltd., Annual report 2007-08, p.54)

5.1.3 INTERNAL CAPITAL

Internal capital is defined as the structure, processes, technologies,

methodologies, procedures, routines, systems and culture of an organisation. It comprises

the capabilities of a company, its infrastructure and organisational processes to

manufacture products and render services to the market. Intangible assets of this category

are idiosyncratic to a company and they constantly need to adapt to changing business

scenarios. These assets give the organization a unique advantage over its competitors as

these are not licensed to outsiders and are under company’s control. There are seven

attributes in this category namely research activities, networking and information system,

organisation structure, corporate culture, patents, trademarks and copyrights.

81

Research Activities is the most disclosed attribute in internal capital category for

both the years of study (Table 5.4). They represent lifeblood for any organisation. They

help the business to innovate its products and services. They can further help in boosting

sales, increasing profitability, opening new markets, attracting best employees, finding

new business partners, attracting external finance etc. Disclosure for this attribute is

around 55.14% in the year 2003-04 which increased to 64.20% in the year 2007-08. Easy

availability of research related information could be a possible reason for its high

disclosure. Sun pharmaceutical Industries Ltd. has disclosed on this attribute as “Our

teams at the R&D centres continue their task of building pipelines-developing cost

effective & efficient processes for dosage forms as well as APIs, scaling these up from the

labs to the plants, working on product development for demanding international markets,

developing ANDAs for a strong pipeline in the US.” (Sun pharmaceutical Industries Ltd,

Annual report 2007-08, p.12)

Networking and information systems which is another internal capital attribute,

refers to business’s modus operandi and methods in relation to its internal processes and

administrative systems. These internal methods, procedures, routines, technologies are

roots of an organisation. The information on these disclosures being company specific,

internal and confidential, low disclosures is found on this attribute. Disclosures regarding

networking and information systems is 5.56% in 2003-04 whereas it is15.84% in 2007-

08. Sterlite Industries Ltd. reports on its networking and information systems as “From

1999, Sterlite has been operating in a SAP environment. As on date, we operate nine

modules of SAP: Finance and Costing, Production Planning, Plant Maintenance, Quality

Management, Sales and Distribution, Material Management, Human Capital

Management and Supplier Relationship Management. In addition, we also have a non-

SAP based, web-enabled customer portal, where our customers can log in to extract

various information such as test certificates, account status, invoices, answers to

technical queries and so on.” (Sterlite Industries Ltd., Annual report 2007-08, p.34)

Another internal capital attribute unique to any company, is its organisation

structure. A company’s organisation structure determines the manner and extent to which

82

roles, power, and responsibilities are delegated, controlled, and coordinated, and how

information flows within the levels of management. A well managed and stable

organisation structure of any company is its important intangible assets and it depicts its

internal soundness and steadiness. The disclosure regarding this attribute is 2.26% in

2003-04 and 5.76% in 2007-08.

Corporate culture refers to the combined beliefs, values, ethics, procedures, and

atmosphere of an organization. It determines a company’s dress code, work environment,

working hours, rules for getting ahead and getting promoted, how the business world is

viewed, what is valued, who is valued, and much more. Intangible assets like

organisation culture are hard for competitors to replicate. This internal capital attribute

has mostly been reported in qualitative form in the annual reports. This attribute has

10.08% disclosure in 2003-04 and 22.63% disclosure in 2007-08. This is the second most

reported attribute in internal capital category for the year 2007-08 (Table 5.4).

Other significant intellectual capital attributes in internal capital category are

patents, copyrights and trademarks. Patents have voluntary disclosure score of 10.91% in

2003-04 and 17.08 % in 2007-08. Likewise copyrights have disclosure score of 0.82%

which increased to 1.44% in 2007-08 and trademarks have disclosure score of 1.44% in

2003-04 followed by 7..00% in 2007-08. These intellectual property assets are usually

owned by a corporation and are valued based on their commercial potential. A

corporation can derive its revenues from licensing these assets to outside users. Larsen

and Toubro Ltd. reported that “The Division has put serious and conscious efforts to

generate innovative ideas and create great value for the organisation by protecting them

through intellectual property rights. 2007-2008 has been another successful year on this

front, wherein 101 patent applications in addition to 31 Design Registrations and 11

Trademark filings have been made.” (Larsen and Toubro Ltd., Annual Report 2007-08,

p.58)

83

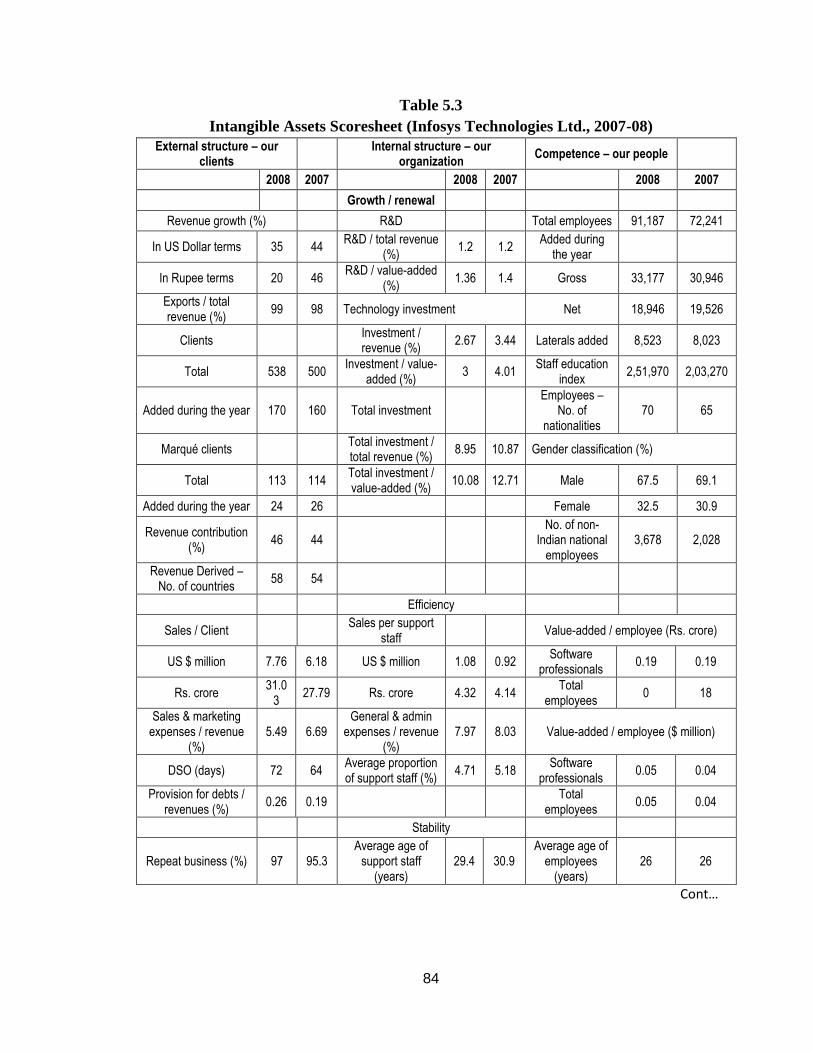

5.1.4 INTANGIBLE ASSETS SCORESHEET

Intangible assets Scoresheet has been disclosed only in annual reports of Infosys

Technologies Ltd., Satyam Computer Services Ltd. and Infotech Enterprises Ltd. for both

the years. The intangible assets statement provided by these companies clearly points out

the company’s intangible assets and their growth, by giving a comparative picture over

the years. It has been presented as additional information to the investors. These

companies strongly believe that the intangible assets scoresheet provides a tool to the

investors for evaluating their market worthiness. However lack of awareness among

corporates regarding the importance of intangible assets scoresheet in determining the

true value of their company could have resulted in its meagre disclosure. An illustration

of intangible assets scoresheet from the annual report of Infosys Technologies Ltd for the

year 2007-08 is given in Table 5.3:

5.1.5 MANDATORY DISCLSOURE REQUIREMENT

Accounting Standard 26 on Intangible assets issued by the Institute of Chartered

Accountants of India in 2002 specifies some disclosure requirements for companies

having intangible assets in their balance sheets. These requirements have been

categorised into four sub-heads which are:

(a) Distinguish between internally generated and other intangible assets;

(b) Details of amortisation rates, method and carrying amount at beginning and end

of period;

(c) Classification of intangible assets; and

(d) Other disclosures like pledging information, reasons for amortising over more

than 10 years etc.

The sub-head (a) above which is distinguishing between internally generated and

other intangible assets, has a disclosure score of 2.47% in the year 2003-04 and 8.64% in

the year 2007-08. Low disclosure score for both the years shows that not many

companies, which have intangible assets in their books, are differentiating between

internally generated and acquired intangible assets.

84

Table 5.3

Intangible Assets Scoresheet (Infosys Technologies Ltd., 2007-08)

External structure – our clients

Internal structure – our organization

Competence – our people

2008 2007

2008 2007

2008 2007

Growth / renewal

Revenue growth (%)

R&D

Total employees 91,187 72,241

In US Dollar terms 35 44 R&D / total revenue

(%) 1.2 1.2

Added during the year

In Rupee terms 20 46 R&D / value-added

(%) 1.36 1.4 Gross 33,177 30,946

Exports / total revenue (%)

99 98 Technology investment Net 18,946 19,526

Clients

Investment / revenue (%)

2.67 3.44 Laterals added 8,523 8,023

Total 538 500 Investment / value-

added (%) 3 4.01

Staff education index

2,51,970 2,03,270

Added during the year 170 160 Total investment

Employees – No. of

nationalities 70 65

Marqué clients

Total investment / total revenue (%)

8.95 10.87 Gender classification (%)

Total 113 114 Total investment / value-added (%)

10.08 12.71 Male 67.5 69.1

Added during the year 24 26

Female 32.5 30.9

Revenue contribution (%)

46 44

No. of non-Indian national

employees 3,678 2,028

Revenue Derived – No. of countries

58 54

Efficiency

Sales / Client

Sales per support staff

Value-added / employee (Rs. crore)

US $ million 7.76 6.18 US $ million 1.08 0.92 Software

professionals 0.19 0.19

Rs. crore 31.0

3 27.79 Rs. crore 4.32 4.14

Total employees

0 18

Sales & marketing expenses / revenue

(%) 5.49 6.69

General & admin expenses / revenue

(%) 7.97 8.03 Value-added / employee ($ million)

DSO (days) 72 64 Average proportion of support staff (%)

4.71 5.18 Software

professionals 0.05 0.04

Provision for debts / revenues (%)

0.26 0.19

Total employees

0.05 0.04

Stability

Repeat business (%) 97 95.3 Average age of

support staff (years)

29.4 30.9 Average age of

employees (years)

26 26

Cont…

85

External structure – our clients Internal structure – our organization Competence – our

people

2008 2007 2008 2007 2008 2007

No. of clients accounting > 5% of revenue

1 1

Attrition %

Client concentration

Excluding subsidiaries

13.4 13.7

Top client (%) 9.1 7

Excluding involuntary separation

12.1 12.2

Top 5 clients (%) 20.9 19.4

Top 10 clients (%) 31.4 31.4

Client distribution

1 million dollar+ 310 275

5 million dollar+ 141 107

10 million dollar+ 89 71

20 million dollar+ 47 36

30 million dollar+ 32 25

40 million dollar+ 22 16

50 million dollar+ 18 12

60 million dollar+ 13 11

70 million dollar+ 12 9

80 million dollar+ 10 4

90 million dollar+ 6 4

100 million dollar+ 6 3

200 million dollar+ 1 1

300 million dollar+ 1 –

The above figures are based on Indian GAAP consolidated financial statement

86

As-26 also requires that companies should give details of amortisation rates,

method and carrying amount at beginning and end of period. This requirement has been

fulfilled by all the companies which had intangible assets as a part of their balance sheet.

Disclosure score for this sub-head is 37.86% in 2003-04 and 72.84% in 2007-08.

Classification of intangible assets into separate classes is also one of the requisite

of AS 26. For the year 2003-04, out of 37.86% companies having intangible assets in

their balance sheet, 35.80% companies are categorising them into classes like software,

brand, licences etc. Similarly for the year 2007-08, 69.96% companies are categorising

their intangible assets, out of a total of 72.84% of sample companies which recognise

intangible assets in their books of accounts.

Other disclosures like pledging information, reasons for amortising over more

than 10 years etc. have achieved a score of 0.82% in 2003-04 and 2.88% in 2007-08.

Low disclosure for this sub-head could be due to limited applicability of this disclosure

requirement.

Intangible assets Valuation

In India there is an increasing awareness among corporate to disclose and value

their intangible assets. Intangible assets Valuation means assigning a fair monetary value

to intangible assets (whether internally generated or acquired from outside) in a company.

As mentioned in research methodology a score of “2” has been assigned to companies

valuing their intangible assets and “0” for not valuing them. Accordingly, this category

has received a disclosure score of 37.86% in 2003-04 and 72.84% in 2007-08.

87

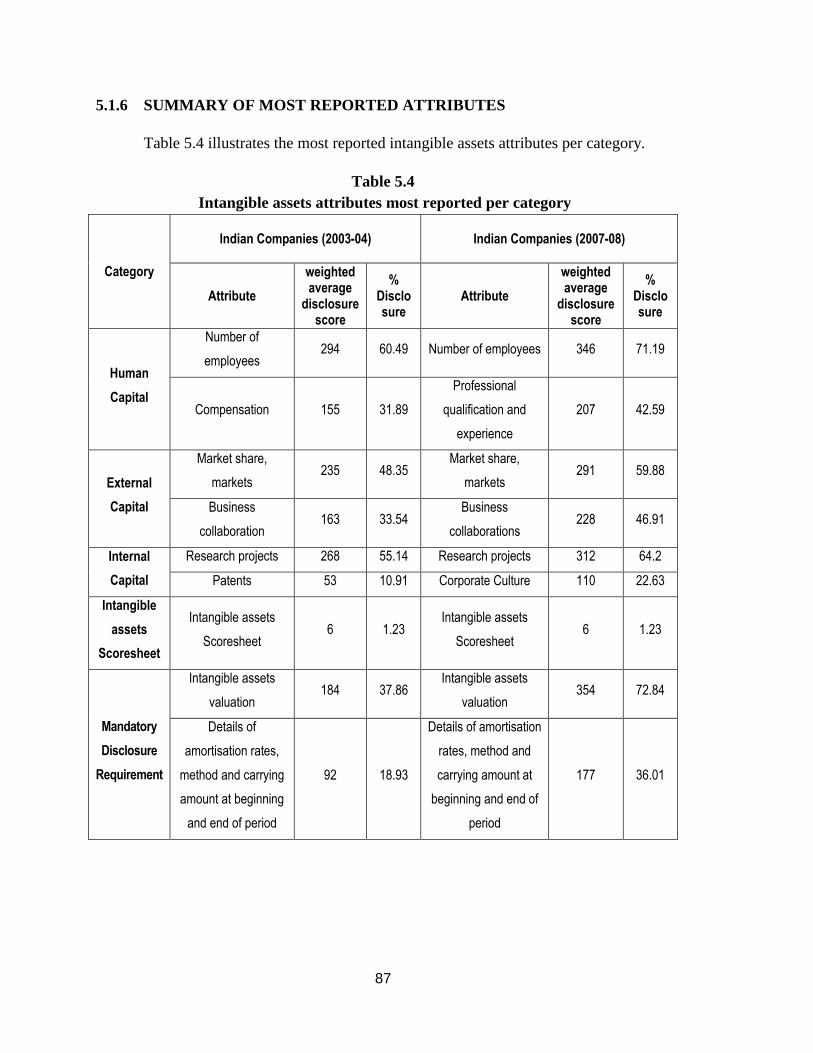

5.1.6 SUMMARY OF MOST REPORTED ATTRIBUTES

Table 5.4 illustrates the most reported intangible assets attributes per category.

Table 5.4

Intangible assets attributes most reported per category

Category

Indian Companies (2003-04)

Indian Companies (2007-08)

Attribute

weighted average

disclosure score

% Disclosure

Attribute

weighted average

disclosure score

% Disclosure

Human

Capital

Number of

employees 294 60.49 Number of employees 346 71.19

Compensation 155 31.89

Professional

qualification and

experience

207 42.59

External

Capital

Market share,

markets 235 48.35

Market share,

markets 291 59.88

Business

collaboration 163 33.54

Business

collaborations 228 46.91

Internal

Capital

Research projects 268 55.14 Research projects 312 64.2

Patents 53 10.91 Corporate Culture 110 22.63

Intangible

assets

Scoresheet

Intangible assets

Scoresheet 6 1.23

Intangible assets

Scoresheet 6 1.23

Mandatory

Disclosure

Requirement

Intangible assets

valuation 184 37.86

Intangible assets

valuation 354 72.84

Details of

amortisation rates,

method and carrying

amount at beginning

and end of period

92 18.93

Details of amortisation

rates, method and

carrying amount at

beginning and end of

period

177 36.01

88

The attribute “Number of employees” and “Compensation” for the year 2003-04

whereas attribute “Number of employees” and “Professional qualification and

experience” for the year 2007-08 are the most reported attributes from the human capital

category.

“Market share, markets” and “Business collaboration” are most highly disclosed

attributes in external capital category for both the years of study.

Further in internal capital category, “Research projects” and “Patents” for the

year 2003-04 plus “Research projects” and “Corporate culture” for the year 2007-08, are

most reported intangible assets.

Similarly for mandatory disclosure requirement category, “Intangible assets

valuation” and “Details of amortisation rates, method and carrying amount at beginning

and end of period” are most disclosed attributes in annual reports.

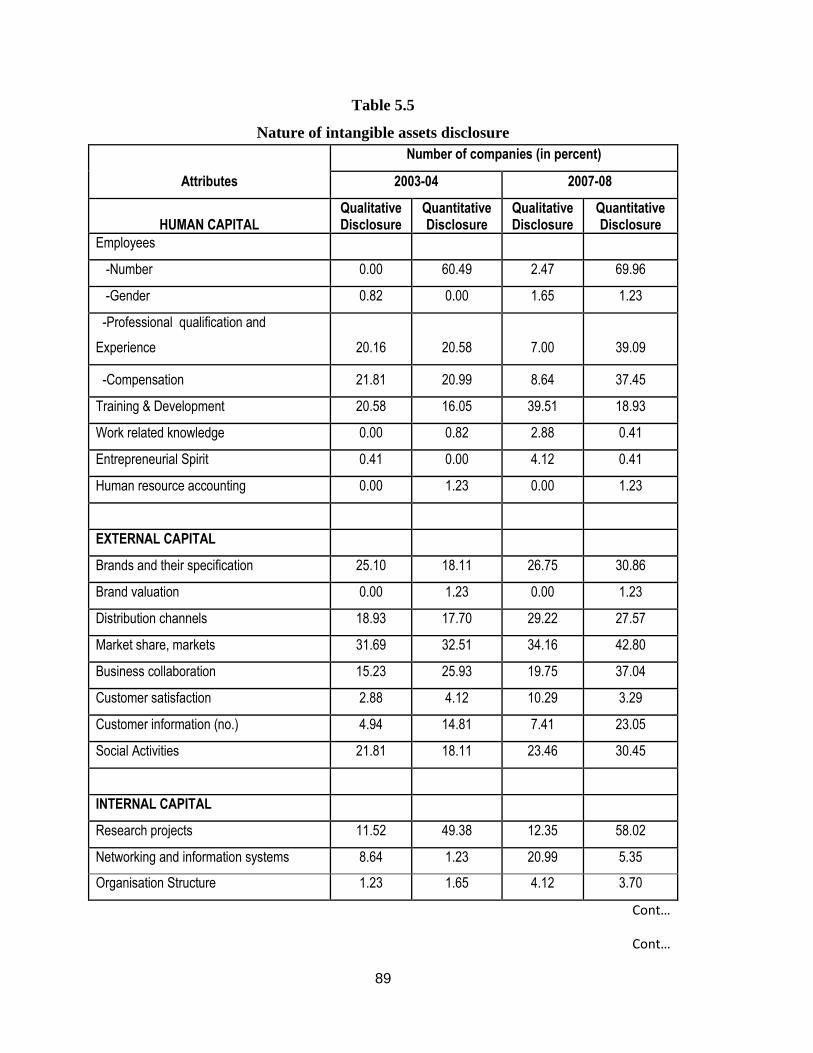

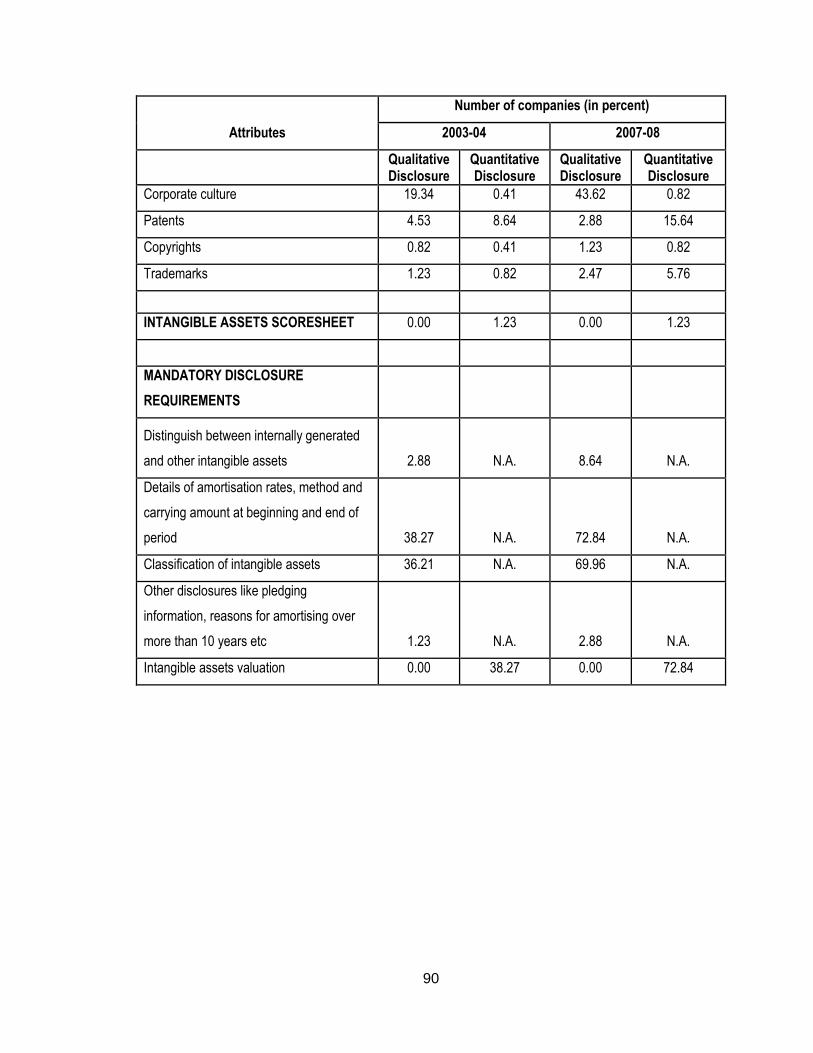

5.2 NATURE OF INTANGIBLE ASSETS DISCLOSURE

After explaining in detail the extent of disclosure it is very essential to discuss

about the nature of reporting of intangible assets as well. Nature of intangible assets

disclosure involves distinguishing between qualitative and quantitative nature of

reporting. The percentage number of companies as mentioned in the table 5.5 has been

calculated by dividing the total number of companies disclosing an attribute in qualitative

or quantitative form by total number of sample companies (which is 243). For example

training and development attribute for the year 2003-04 has been disclosed by 20.58%

companies in qualitative form and 16.05% in quantitative form. Table 5.5 depicts the

nature of intangible assets disclosure in annual reports for both years of the study.

89

Table 5.5

Nature of intangible assets disclosure

Attributes

Number of companies (in percent)

2003-04 2007-08

HUMAN CAPITAL Qualitative Disclosure

Quantitative Disclosure

Qualitative Disclosure

Quantitative Disclosure

Employees

-Number 0.00 60.49 2.47 69.96

-Gender 0.82 0.00 1.65 1.23

-Professional qualification and

Experience 20.16 20.58 7.00 39.09

-Compensation 21.81 20.99 8.64 37.45

Training & Development 20.58 16.05 39.51 18.93

Work related knowledge 0.00 0.82 2.88 0.41

Entrepreneurial Spirit 0.41 0.00 4.12 0.41

Human resource accounting 0.00 1.23 0.00 1.23

EXTERNAL CAPITAL

Brands and their specification 25.10 18.11 26.75 30.86

Brand valuation 0.00 1.23 0.00 1.23

Distribution channels 18.93 17.70 29.22 27.57

Market share, markets 31.69 32.51 34.16 42.80

Business collaboration 15.23 25.93 19.75 37.04

Customer satisfaction 2.88 4.12 10.29 3.29

Customer information (no.) 4.94 14.81 7.41 23.05

Social Activities 21.81 18.11 23.46 30.45

INTERNAL CAPITAL

Research projects 11.52 49.38 12.35 58.02

Networking and information systems 8.64 1.23 20.99 5.35

Organisation Structure 1.23 1.65 4.12 3.70

Cont…

Cont…

90

Attributes

Number of companies (in percent)

2003-04 2007-08

Qualitative Disclosure

Quantitative Disclosure

Qualitative Disclosure

Quantitative Disclosure

Corporate culture 19.34 0.41 43.62 0.82

Patents 4.53 8.64 2.88 15.64

Copyrights 0.82 0.41 1.23 0.82

Trademarks 1.23 0.82 2.47 5.76

INTANGIBLE ASSETS SCORESHEET 0.00 1.23 0.00 1.23

MANDATORY DISCLOSURE

REQUIREMENTS

Distinguish between internally generated

and other intangible assets 2.88 N.A. 8.64 N.A.

Details of amortisation rates, method and

carrying amount at beginning and end of

period 38.27 N.A. 72.84 N.A.

Classification of intangible assets 36.21 N.A. 69.96 N.A.

Other disclosures like pledging

information, reasons for amortising over

more than 10 years etc 1.23 N.A. 2.88 N.A.

Intangible assets valuation 0.00 38.27 0.00 72.84

91

Table 5.5 illustrates that nature of disclosures (both qualitative and quantitative)

has improved in the year 2007-08 as compared to the year 2003-04.

For Number of employees attribute in human capital category, 60.49% companies

were disclosing in quantitative form in the year 2003-04 which increased to 69.96% in

2007-08. Similarly in context of professional qualification and experience of employees,

20.16% were reporting in qualitative form and 20.58% in quantitative form in the year

2003-04. In the year 2007-08, companies reporting in qualitative form remained only 7%

and it seems they shifted to quantitative disclosures (39.09%). Likewise is the reporting

of attributes compensation, training and development and entrepreneurial spirit in

human capital category, where the quantitative disclosures have increased.

In external capital category, the attribute brands and its specification is reported

by 25.10% companies in qualitative form and 18.11% companies in quantitative form in

the year 2003-04. These numbers increased to 26.75% and 30.86% respectively in the

year 2007-08. Information concerning distribution channels which is reported by 17.70%

companies in quantitative form in year 2003-04, increased to 27.57% companies in 2007-

08. Disclosures regarding other attributes of external capital also improved in year 2007-

08 in comparison to year 2003-04.

Improved disclosures can be noticed for all the attributes of internal capital. For

the corporate culture attribute majority of the companies are reporting this attribute in

qualitative form. Difficulty in its quantification could have motivated for its reporting

mainly in narrative form. The percentages are 19.34% in the year 2003-04 and 43.62% in

2007-08.

As explained in chapter-3 on research methodology, the information regarding the

first four attributes of mandatory disclosure requirement category were given the score of

either “1” or “0” for its presence or absence in the annual report respectively.

Accordingly, quantitative disclosure column is not applicable for the four sub-heads in

this category. Qualitative disclosures of these attributes have improved in the year 2007-

08 in contrast to the year 2003-04.

92

Intangible assets valuation information has been provided by almost double the

number of companies in 2007-08 as compared to year 2003-04. While 38.27% companies

were valuing its intangibles in year 2003-04, it increased to 72.84% companies in the

year 2007-08.

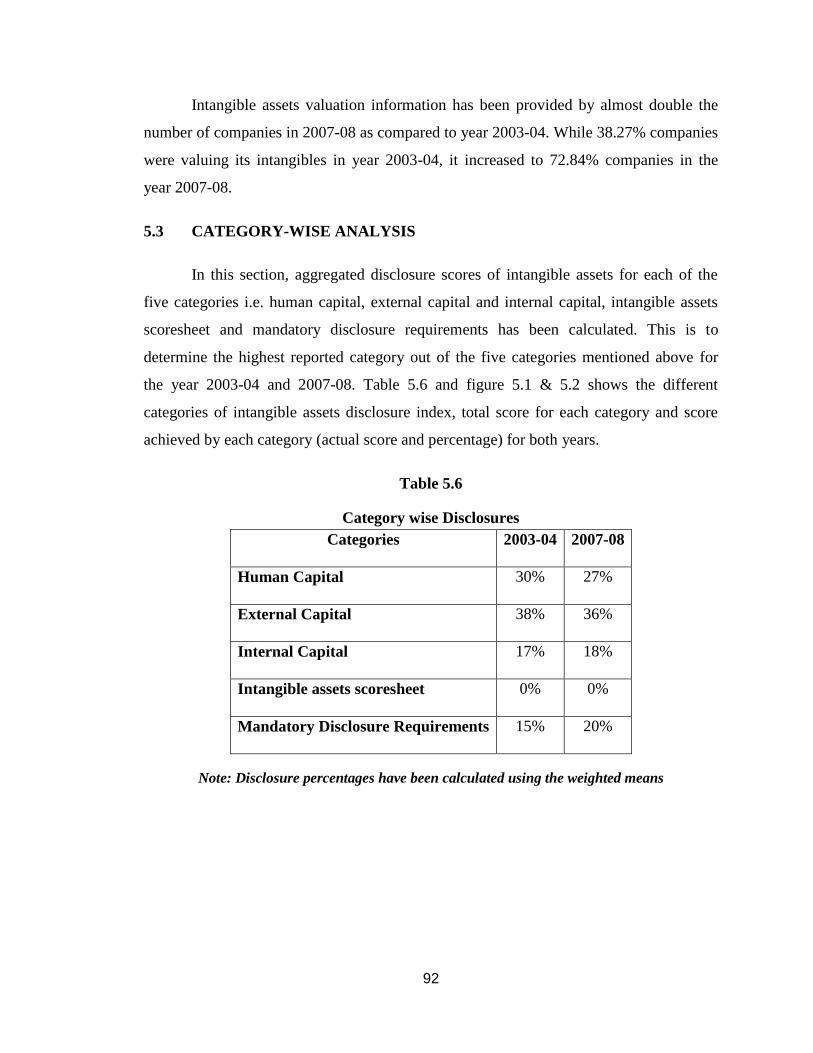

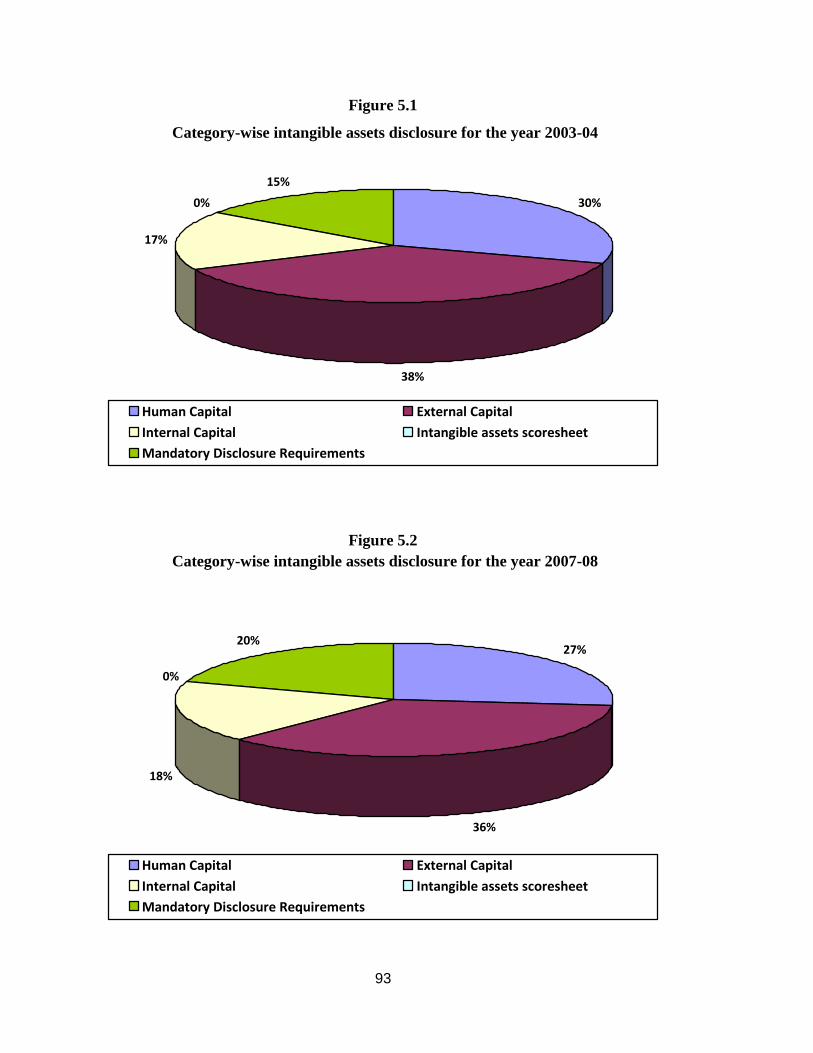

5.3 CATEGORY-WISE ANALYSIS

In this section, aggregated disclosure scores of intangible assets for each of the

five categories i.e. human capital, external capital and internal capital, intangible assets

scoresheet and mandatory disclosure requirements has been calculated. This is to

determine the highest reported category out of the five categories mentioned above for

the year 2003-04 and 2007-08. Table 5.6 and figure 5.1 & 5.2 shows the different

categories of intangible assets disclosure index, total score for each category and score

achieved by each category (actual score and percentage) for both years.

Table 5.6

Category wise Disclosures

Categories 2003-04 2007-08

Human Capital 30% 27%

External Capital 38% 36%

Internal Capital 17% 18%

Intangible assets scoresheet 0% 0%

Mandatory Disclosure Requirements 15% 20%

Note: Disclosure percentages have been calculated using the weighted means

93

Figure 5.1

Category-wise intangible assets disclosure for the year 2003-04

30%

38%

17%

0%

15%

Human Capital External Capital

Internal Capital Intangible assets scoresheet

Mandatory Disclosure Requirements

Figure 5.2

Category-wise intangible assets disclosure for the year 2007-08

27%

36%

18%

0%

20%

Human Capital External Capital

Internal Capital Intangible assets scoresheet

Mandatory Disclosure Requirements

94

The results reveal external capital to be the most disclosed intangible assets

category for both the years of the study. It has disclosure of 38% in the year 2003-04 and

36% in the year 2007-08. The studies from Australia (Guthrie & Petty, 2000); Ireland

(Brennan, 2001); Italy (Bozzolan et al, 2003); South Africa (April et al, 2003); Malaysia

(Goh & Lim, 2004); Sri Lanka (Abeysekera & Guthrie, 2005); Spain (Oliveras &

Kasperskaya, 2005); New Zealand (Wong & Gardner, 2004) also showed external capital

to be most frequently reported intangible assets category. This dominance of external

capital disclosures is due to the pivotal role of these disclosures in influencing

stakeholder decisions. Therefore in order to show their edge over their competitors the

companies might want to emphasise relations with their customers and other

organisations, and promote their brand, which are all attributes of external capital.

Guthrie and Petty (2000) explained skew ness towards external disclosure because of

increased emphasis in recent years on rationalising distribution channels, reconfiguring a

firm’s value chain and reassessing customer value.

External capital category is closely followed by human capital category, which

has disclosure of 30% in 2003-04 and 27% in 2007-08 The reason for high disclosures on

human capital could be that such disclosure is helpful for companies in attracting the

talented employees and companies take pride in their high calibre management. The

internal capital category has a disclosure of 17% in 2003-04 which increased to 18% in

2007-08. Low disclosures in internal capital category as compared to external and human

capital could be motivated by company’s need to maintain its confidentiality on business

processes, policies, systems etc over its competitors.

Further, the mandatory disclosure requirement category’s share in overall

disclosure has increased from 15% in 2003-04 to 20% in 2007-08. This implies increased

awareness among Indian corporate houses regarding worth of intangible assets and their

rising commitment to value these assets in their financial statements. The category

intangible assets scoresheet has negligible disclosure score for both the years.

To summarise the disclosure scores for each of the five categories have shown

increasing trends in the year 2007-08 over the year 2003-04.

95

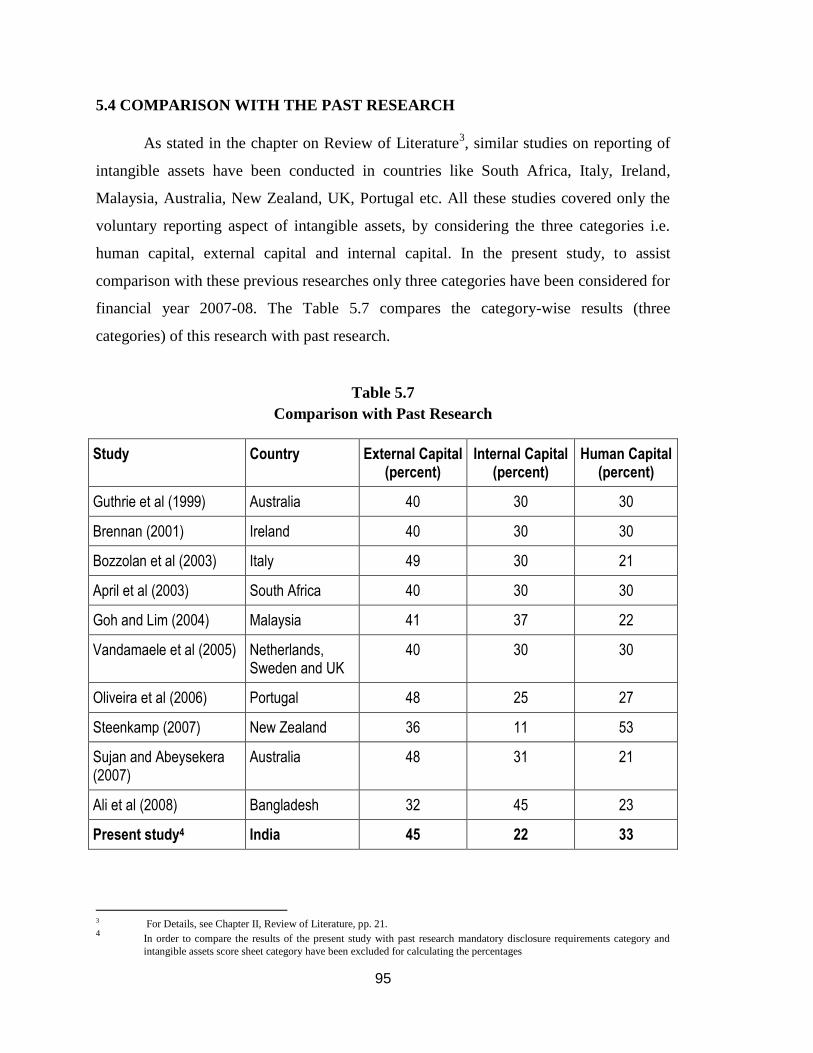

5.4 COMPARISON WITH THE PAST RESEARCH

As stated in the chapter on Review of Literature3, similar studies on reporting of

intangible assets have been conducted in countries like South Africa, Italy, Ireland,

Malaysia, Australia, New Zealand, UK, Portugal etc. All these studies covered only the

voluntary reporting aspect of intangible assets, by considering the three categories i.e.

human capital, external capital and internal capital. In the present study, to assist

comparison with these previous researches only three categories have been considered for

financial year 2007-08. The Table 5.7 compares the category-wise results (three

categories) of this research with past research.

Table 5.7

Comparison with Past Research

Study Country External Capital (percent)

Internal Capital (percent)

Human Capital (percent)

Guthrie et al (1999) Australia 40 30 30

Brennan (2001) Ireland 40 30 30

Bozzolan et al (2003) Italy 49 30 21

April et al (2003) South Africa 40 30 30

Goh and Lim (2004) Malaysia 41 37 22

Vandamaele et al (2005) Netherlands, Sweden and UK

40 30 30

Oliveira et al (2006) Portugal 48 25 27

Steenkamp (2007) New Zealand 36 11 53

Sujan and Abeysekera (2007)

Australia 48 31 21

Ali et al (2008) Bangladesh 32 45 23

Present study4 India 45 22 33

3 For Details, see Chapter II, Review of Literature, pp. 21. 4 In order to compare the results of the present study with past research mandatory disclosure requirements category and

intangible assets score sheet category have been excluded for calculating the percentages

96

As is clear from the table, external capital is the highest reported intangible assets

category for most of the studies. The results drawn from the current study covering

Indian companies also shows external capital as the highest disclosed intangible assets

category followed by human capital and internal capital category. Internal capital is least

reported and this is similar to the study on intellectual capital disclosure conducted in

Portugal (Oliveira et al, 2006) and New Zealand (Steenkamp, 2007).

SECTION-II

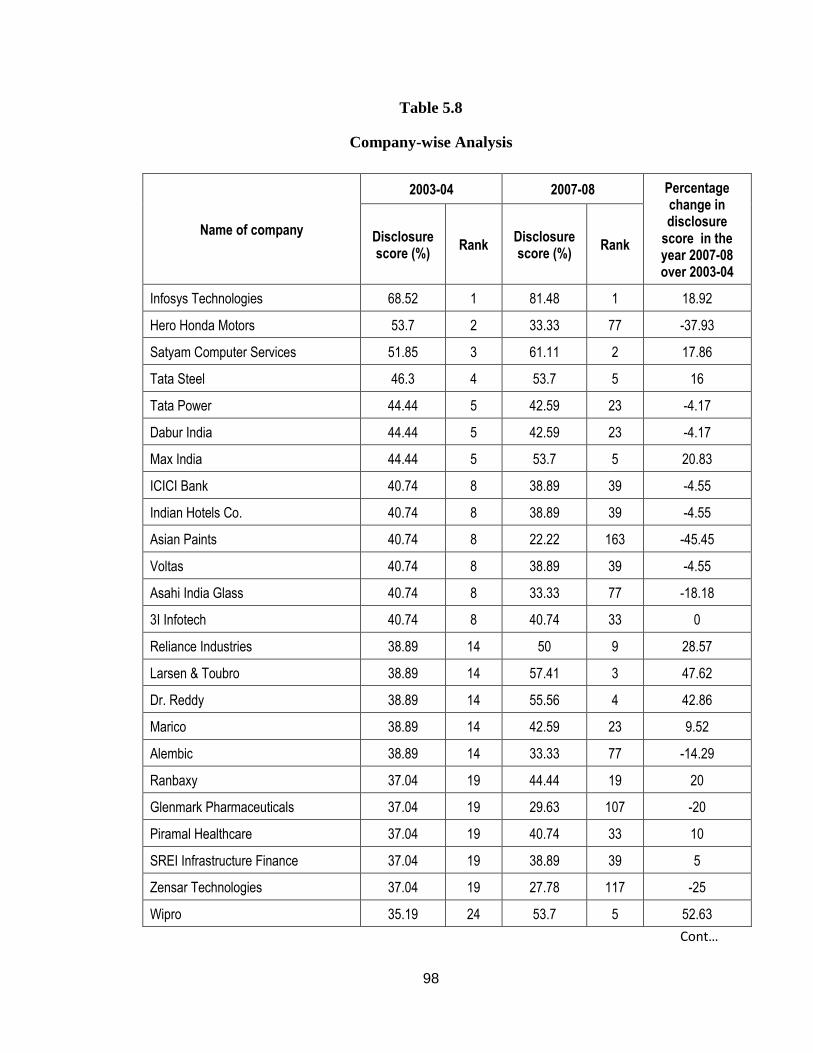

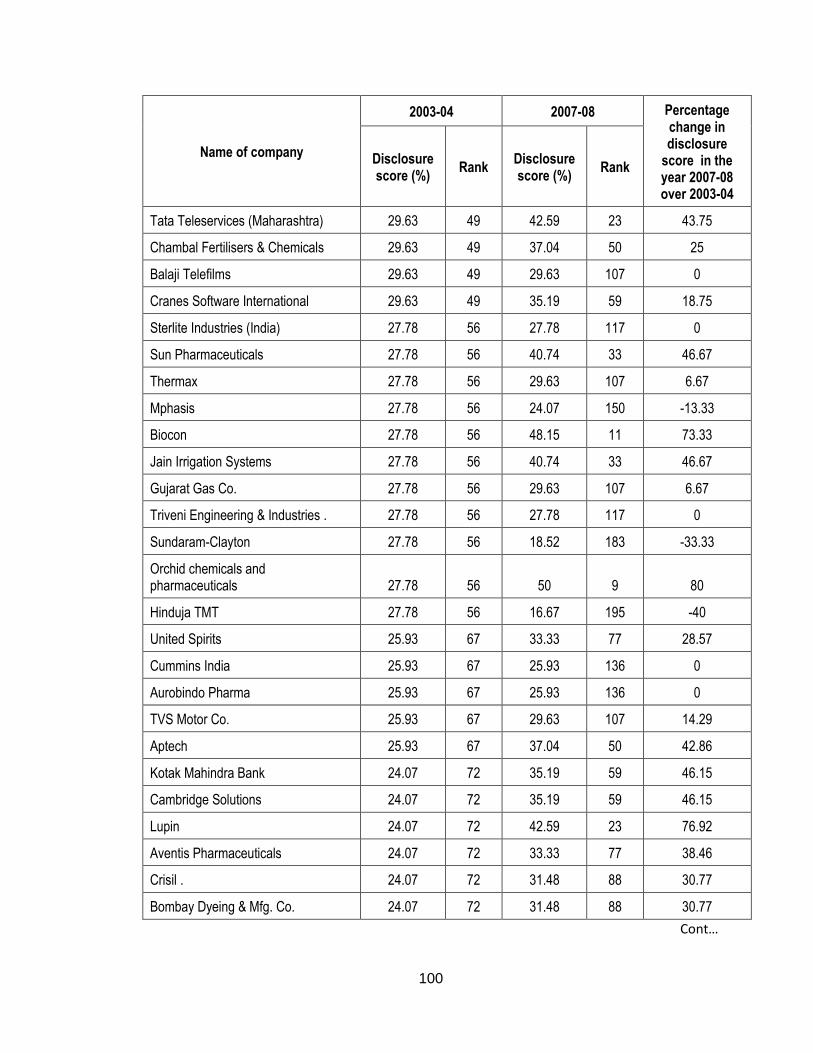

5.5 COMPANY- WISE ANALYSIS

The company-wise disclosure score has been calculated by dividing the total

weighted disclosure index score obtained by a company during a particular year by the

maximum score for the company (which is 54).The disclosure score has been calculated

in percentages so as to make the disclosure of the companies comparable.

Table 5.8 explains the company-wise disclosure of intangible assets for the years

2003-04 and 2007-08 respectively. The companies have been ranked in the descending

order of their 2003-04 disclosure score. The respective 2007-08 scores have been

mentioned corresponding to their 2003-04 scorecard.

An analysis of this table reveals that disclosure score has improved in case of 191

companies decreased in case of 35 companies and remained constant for 17 companies

in the year 2003-04 and 2007-08.

Infosys Technologies Ltd. occupies highest position in intangible assets disclosure

for both years of the study. The company’s disclosure score of 68.52% in the year 2003-

04 has increased to 81.48% in the year 2007-08. The highest disclosure maintained by

Infosys Technologies Ltd. (68.52) is followed by Hero Honda Motors Ltd (53.70),

Satyam Computer Services Ltd. (51.85%), Tata Steel Ltd. (46.30%) Tata Power Ltd.

(44.44%), Dabur India Ltd. (44.44%), Max India Ltd. (44.44%), ICICI Bank Ltd.

(40.74%). Indian Hotels Co Ltd , Asian Paints Ltd., Voltas Ltd. , Asahi India Glass Ltd ,

3i Infotech Ltd., Reliance Industries Ltd. (38.89%), Larsen and Toubro Ltd., Dr. Reddy

Ltd., Marico Ltd., Alembic Pharmaceuticals Ltd., Ranbaxy Ltd. ( 37.04%) for the year

2003-04.

97

A wide variation can be observed in the disclosure scores of companies for the

year 2007-08 over the year 2003-04. Table 5.6 exhibits that the highest disclosure score

has been achieved by Infosys Technologies Ltd. (81.48%) is followed by Satyam

Computer Services Ltd. ( 61.11%), Larsen and Toubro Ltd. ( 57.41%), Dr. Reddy Ltd.

(55.56%), Tata Steel Ltd (53.70), Max India Ltd., Wipro Ltd., JSW Steel Ltd. (51.85%),

Orchid Chemicals & Pharmaceuticals Ltd. ( 50%), Reliance Industries Ltd., SKF India

Ltd. (48.15%), ACC Ltd. (46.30%), Glaxosmithkline Ltd., KPIT Cummins Infosystems

Ltd. for the year 2007-08.

The table 5.8 also highlights that Infosys Technologies Ltd., Satyam Computer

services Ltd., Tata Steel Ltd., Max India Ltd., Reliance Industries Ltd., Larsen and

Toubro Ltd., Dr. Reddy Ltd., Wipro Ltd. are among top 10 companies, for disclosing

their intangible assets for the years 2003-04 as well as 2007-08.

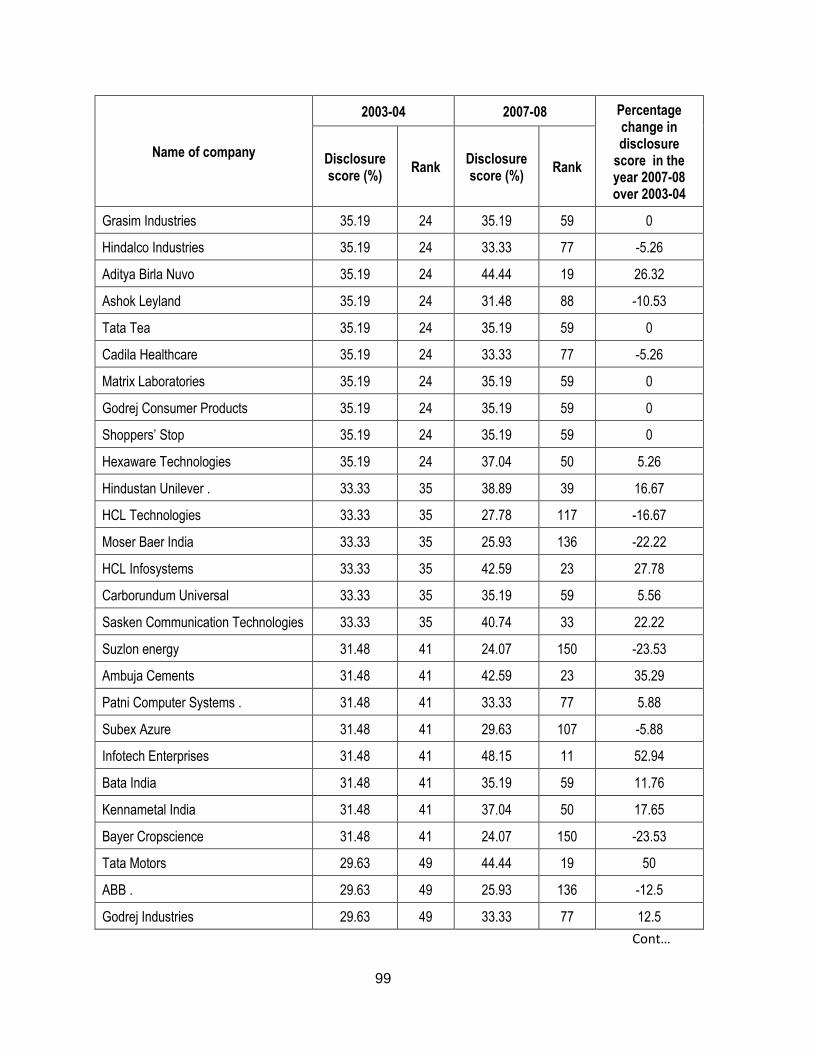

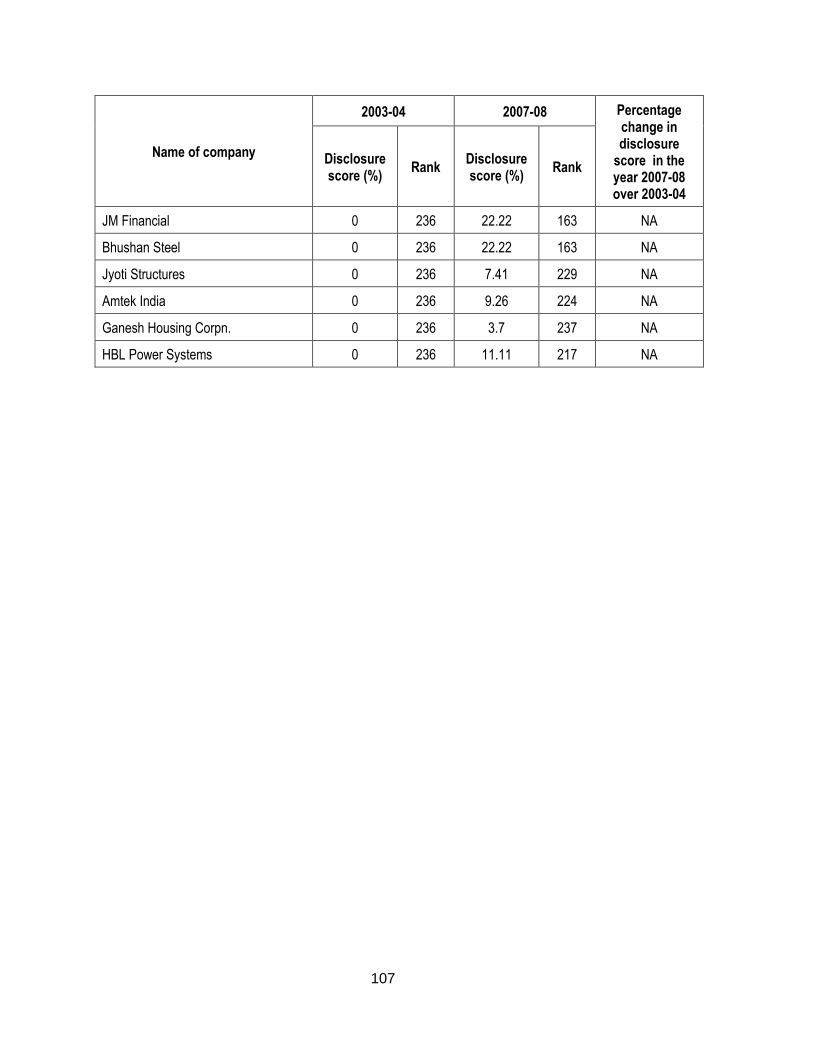

HBL Power Systems Ltd., Ganesh Housing Corporation Ltd., Amtek Auto Ltd.,

Jyoti Structures Ltd., Bhushan Steel Ltd., JM Financial Ltd., Gujurat Fluorochemicals

Ltd., Lanco Infratech Ltd. have zero disclosure score for the year 2003-04. The disclosure

score for these companies significantly improved upto 22.22% in the year 2007-08.

The companies having least disclosure score for the year 2007-08 are Rei agro

Ltd.( 1.85%), Essar Shipping Ltd. (1.85%), Rajesh Exports Ltd. (3.7%), Reliance

Industrial Infrastructure Ltd., Ahmednagar Forgings Ltd., Ruchi Infrastructure Ltd.,

Ganesh Housing corporation Ltd., Ratnamani Metals & Tubes Ltd (5.56%), Madras

Cements Ltd. (7.41%), Timken India Ltd., Oriental Hotels Ltd., Prism Cement Ltd.,

Shanthi Gears Ltd., Era Infra Engineering Ltd., Jyoti Structures Ltd., Deepak Fertilisers

& Petrochemicals Corporation Ltd. (9.26%). However, none of the companies have zero

disclosure score for the year 2007-08.

98

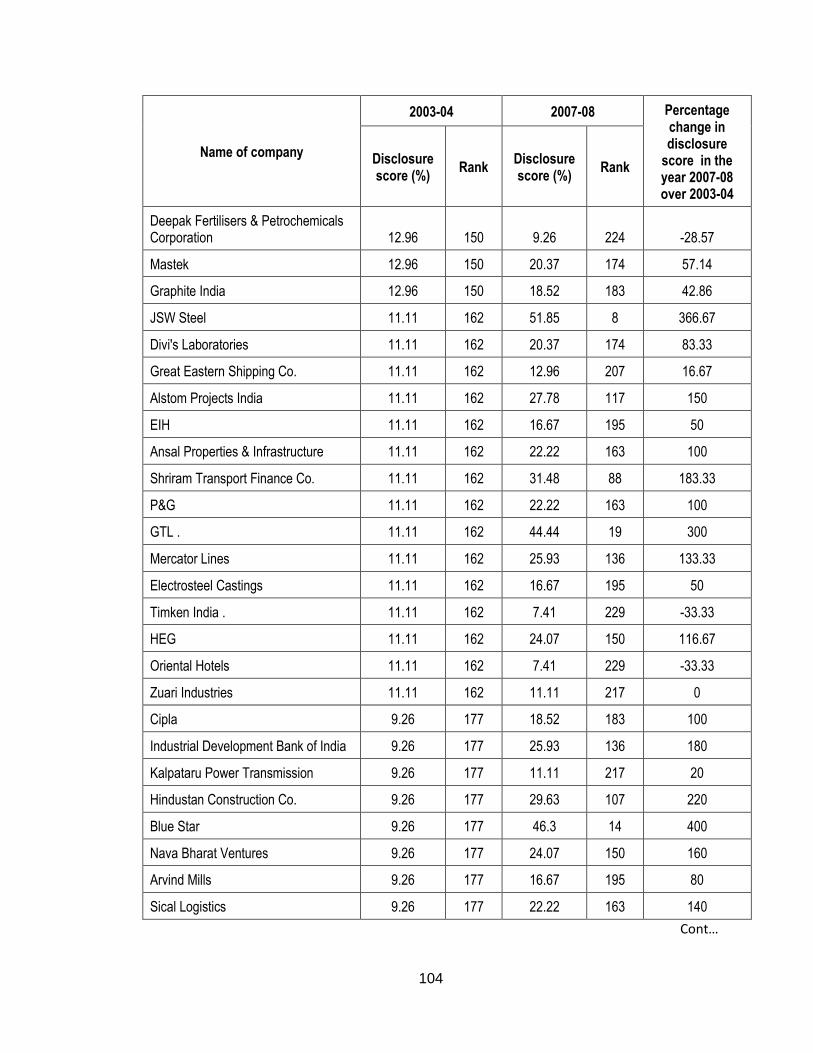

Table 5.8

Company-wise Analysis

Name of company

2003-04 2007-08 Percentage change in disclosure

score in the year 2007-08 over 2003-04

Disclosure score (%)

Rank Disclosure score (%)

Rank

Infosys Technologies 68.52 1 81.48 1 18.92

Hero Honda Motors 53.7 2 33.33 77 -37.93

Satyam Computer Services 51.85 3 61.11 2 17.86

Tata Steel 46.3 4 53.7 5 16

Tata Power 44.44 5 42.59 23 -4.17

Dabur India 44.44 5 42.59 23 -4.17

Max India 44.44 5 53.7 5 20.83

ICICI Bank 40.74 8 38.89 39 -4.55

Indian Hotels Co. 40.74 8 38.89 39 -4.55

Asian Paints 40.74 8 22.22 163 -45.45

Voltas 40.74 8 38.89 39 -4.55

Asahi India Glass 40.74 8 33.33 77 -18.18

3I Infotech 40.74 8 40.74 33 0

Reliance Industries 38.89 14 50 9 28.57

Larsen & Toubro 38.89 14 57.41 3 47.62

Dr. Reddy 38.89 14 55.56 4 42.86

Marico 38.89 14 42.59 23 9.52

Alembic 38.89 14 33.33 77 -14.29

Ranbaxy 37.04 19 44.44 19 20

Glenmark Pharmaceuticals 37.04 19 29.63 107 -20

Piramal Healthcare 37.04 19 40.74 33 10

SREI Infrastructure Finance 37.04 19 38.89 39 5

Zensar Technologies 37.04 19 27.78 117 -25

Wipro 35.19 24 53.7 5 52.63

Cont…

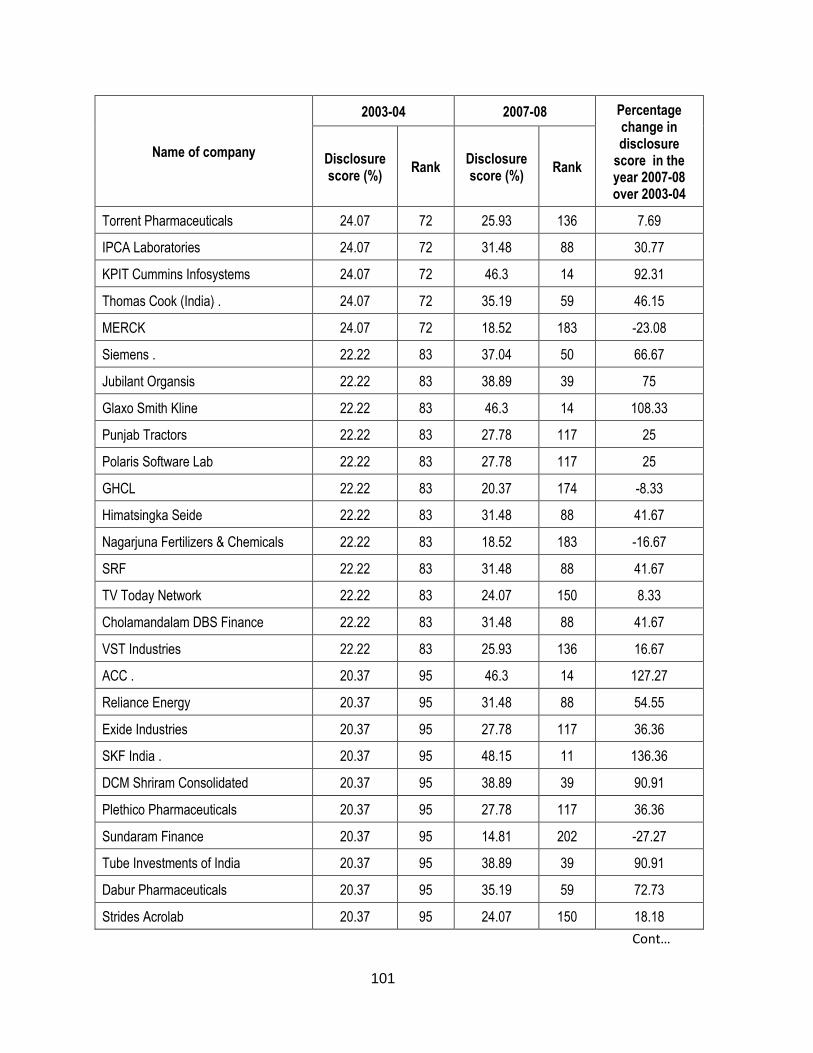

99

Name of company

2003-04 2007-08 Percentage change in disclosure

score in the year 2007-08 over 2003-04

Disclosure score (%)

Rank Disclosure score (%)

Rank

Grasim Industries 35.19 24 35.19 59 0

Hindalco Industries 35.19 24 33.33 77 -5.26

Aditya Birla Nuvo 35.19 24 44.44 19 26.32

Ashok Leyland 35.19 24 31.48 88 -10.53

Tata Tea 35.19 24 35.19 59 0

Cadila Healthcare 35.19 24 33.33 77 -5.26

Matrix Laboratories 35.19 24 35.19 59 0

Godrej Consumer Products 35.19 24 35.19 59 0

Shoppers’ Stop 35.19 24 35.19 59 0

Hexaware Technologies 35.19 24 37.04 50 5.26

Hindustan Unilever . 33.33 35 38.89 39 16.67

HCL Technologies 33.33 35 27.78 117 -16.67

Moser Baer India 33.33 35 25.93 136 -22.22

HCL Infosystems 33.33 35 42.59 23 27.78

Carborundum Universal 33.33 35 35.19 59 5.56

Sasken Communication Technologies 33.33 35 40.74 33 22.22

Suzlon energy 31.48 41 24.07 150 -23.53

Ambuja Cements 31.48 41 42.59 23 35.29

Patni Computer Systems . 31.48 41 33.33 77 5.88

Subex Azure 31.48 41 29.63 107 -5.88

Infotech Enterprises 31.48 41 48.15 11 52.94

Bata India 31.48 41 35.19 59 11.76

Kennametal India 31.48 41 37.04 50 17.65

Bayer Cropscience 31.48 41 24.07 150 -23.53

Tata Motors 29.63 49 44.44 19 50

ABB . 29.63 49 25.93 136 -12.5

Godrej Industries 29.63 49 33.33 77 12.5

Cont…

100

Name of company

2003-04 2007-08 Percentage change in disclosure

score in the year 2007-08 over 2003-04

Disclosure score (%)

Rank Disclosure score (%)

Rank

Tata Teleservices (Maharashtra) 29.63 49 42.59 23 43.75

Chambal Fertilisers & Chemicals 29.63 49 37.04 50 25

Balaji Telefilms 29.63 49 29.63 107 0

Cranes Software International 29.63 49 35.19 59 18.75

Sterlite Industries (India) 27.78 56 27.78 117 0

Sun Pharmaceuticals 27.78 56 40.74 33 46.67

Thermax 27.78 56 29.63 107 6.67

Mphasis 27.78 56 24.07 150 -13.33

Biocon 27.78 56 48.15 11 73.33

Jain Irrigation Systems 27.78 56 40.74 33 46.67

Gujarat Gas Co. 27.78 56 29.63 107 6.67

Triveni Engineering & Industries . 27.78 56 27.78 117 0

Sundaram-Clayton 27.78 56 18.52 183 -33.33

Orchid chemicals and pharmaceuticals 27.78 56 50 9 80

Hinduja TMT 27.78 56 16.67 195 -40

United Spirits 25.93 67 33.33 77 28.57

Cummins India 25.93 67 25.93 136 0

Aurobindo Pharma 25.93 67 25.93 136 0

TVS Motor Co. 25.93 67 29.63 107 14.29

Aptech 25.93 67 37.04 50 42.86

Kotak Mahindra Bank 24.07 72 35.19 59 46.15

Cambridge Solutions 24.07 72 35.19 59 46.15

Lupin 24.07 72 42.59 23 76.92

Aventis Pharmaceuticals 24.07 72 33.33 77 38.46

Crisil . 24.07 72 31.48 88 30.77

Bombay Dyeing & Mfg. Co. 24.07 72 31.48 88 30.77

Cont…

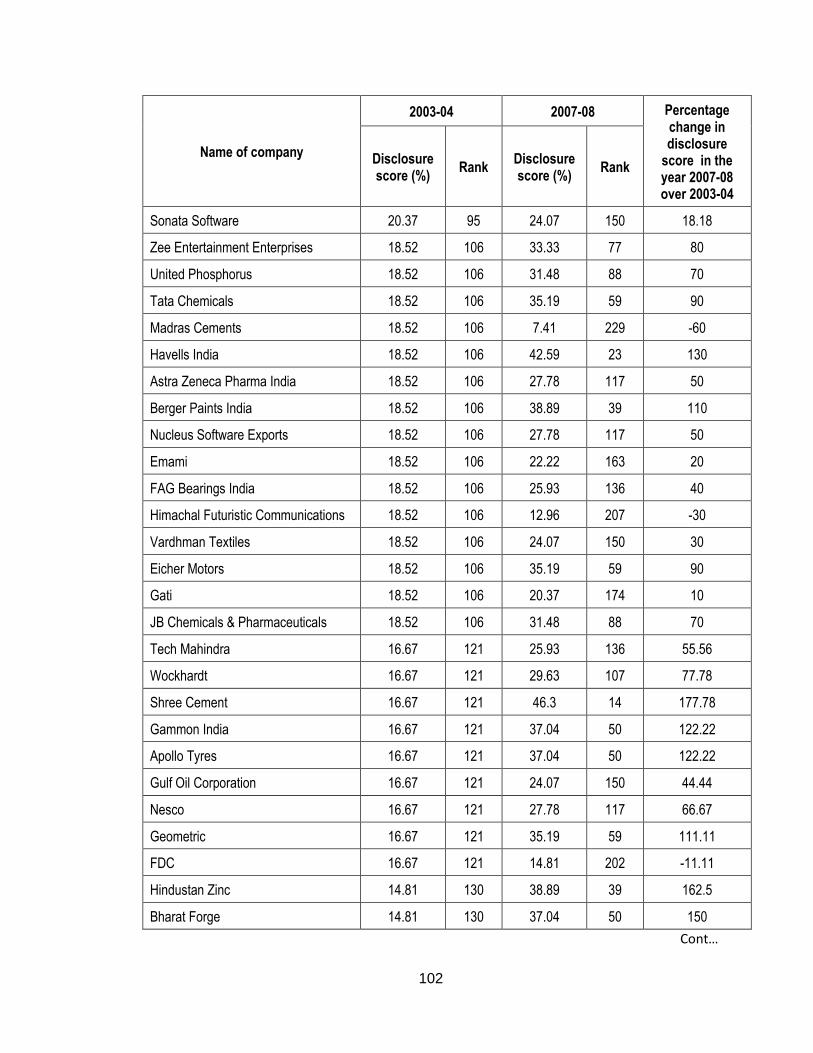

101

Name of company

2003-04 2007-08 Percentage change in disclosure

score in the year 2007-08 over 2003-04

Disclosure score (%)

Rank Disclosure score (%)

Rank

Torrent Pharmaceuticals 24.07 72 25.93 136 7.69

IPCA Laboratories 24.07 72 31.48 88 30.77

KPIT Cummins Infosystems 24.07 72 46.3 14 92.31

Thomas Cook (India) . 24.07 72 35.19 59 46.15

MERCK 24.07 72 18.52 183 -23.08

Siemens . 22.22 83 37.04 50 66.67

Jubilant Organsis 22.22 83 38.89 39 75

Glaxo Smith Kline 22.22 83 46.3 14 108.33

Punjab Tractors 22.22 83 27.78 117 25

Polaris Software Lab 22.22 83 27.78 117 25

GHCL 22.22 83 20.37 174 -8.33

Himatsingka Seide 22.22 83 31.48 88 41.67

Nagarjuna Fertilizers & Chemicals 22.22 83 18.52 183 -16.67

SRF 22.22 83 31.48 88 41.67

TV Today Network 22.22 83 24.07 150 8.33

Cholamandalam DBS Finance 22.22 83 31.48 88 41.67

VST Industries 22.22 83 25.93 136 16.67

ACC . 20.37 95 46.3 14 127.27

Reliance Energy 20.37 95 31.48 88 54.55

Exide Industries 20.37 95 27.78 117 36.36

SKF India . 20.37 95 48.15 11 136.36

DCM Shriram Consolidated 20.37 95 38.89 39 90.91

Plethico Pharmaceuticals 20.37 95 27.78 117 36.36

Sundaram Finance 20.37 95 14.81 202 -27.27

Tube Investments of India 20.37 95 38.89 39 90.91

Dabur Pharmaceuticals 20.37 95 35.19 59 72.73

Strides Acrolab 20.37 95 24.07 150 18.18

Cont…

102

Name of company

2003-04 2007-08 Percentage change in disclosure

score in the year 2007-08 over 2003-04

Disclosure score (%)

Rank Disclosure score (%)

Rank

Sonata Software 20.37 95 24.07 150 18.18

Zee Entertainment Enterprises 18.52 106 33.33 77 80

United Phosphorus 18.52 106 31.48 88 70

Tata Chemicals 18.52 106 35.19 59 90

Madras Cements 18.52 106 7.41 229 -60

Havells India 18.52 106 42.59 23 130

Astra Zeneca Pharma India 18.52 106 27.78 117 50

Berger Paints India 18.52 106 38.89 39 110

Nucleus Software Exports 18.52 106 27.78 117 50

Emami 18.52 106 22.22 163 20

FAG Bearings India 18.52 106 25.93 136 40

Himachal Futuristic Communications 18.52 106 12.96 207 -30

Vardhman Textiles 18.52 106 24.07 150 30

Eicher Motors 18.52 106 35.19 59 90

Gati 18.52 106 20.37 174 10

JB Chemicals & Pharmaceuticals 18.52 106 31.48 88 70

Tech Mahindra 16.67 121 25.93 136 55.56

Wockhardt 16.67 121 29.63 107 77.78

Shree Cement 16.67 121 46.3 14 177.78

Gammon India 16.67 121 37.04 50 122.22

Apollo Tyres 16.67 121 37.04 50 122.22

Gulf Oil Corporation 16.67 121 24.07 150 44.44

Nesco 16.67 121 27.78 117 66.67

Geometric 16.67 121 35.19 59 111.11

FDC 16.67 121 14.81 202 -11.11

Hindustan Zinc 14.81 130 38.89 39 162.5

Bharat Forge 14.81 130 37.04 50 150

Cont…

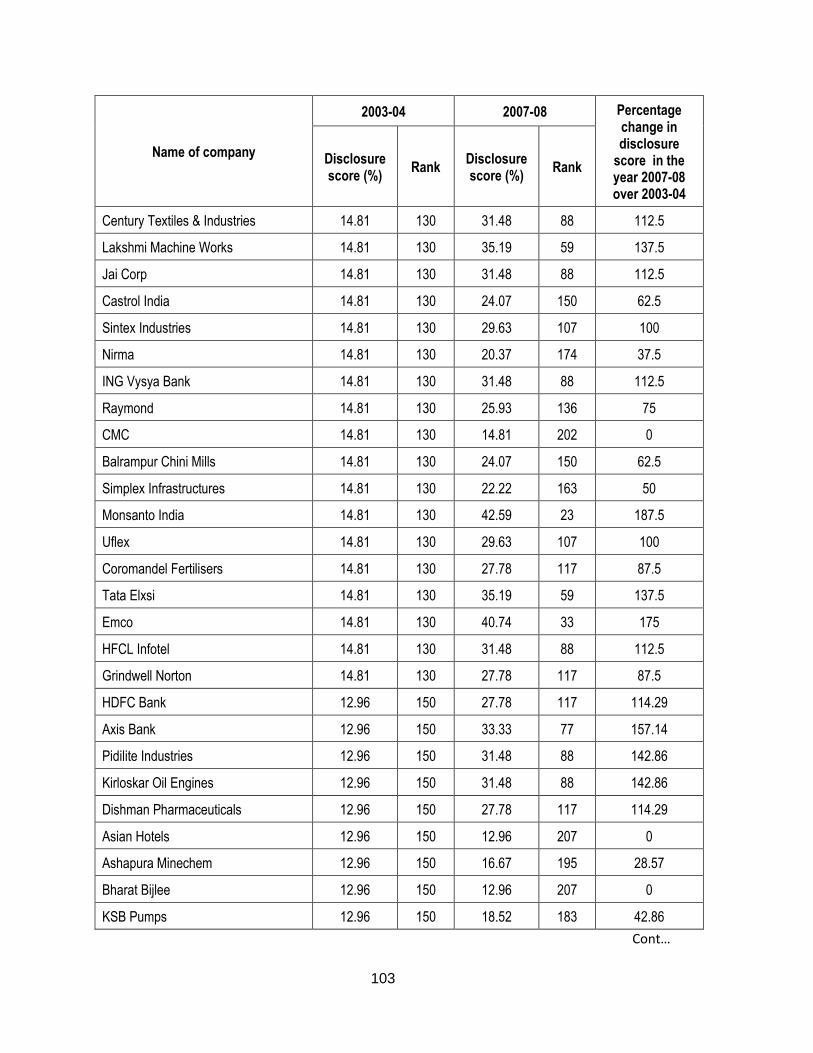

103

Name of company

2003-04 2007-08 Percentage change in disclosure

score in the year 2007-08 over 2003-04

Disclosure score (%)

Rank Disclosure score (%)

Rank

Century Textiles & Industries 14.81 130 31.48 88 112.5

Lakshmi Machine Works 14.81 130 35.19 59 137.5

Jai Corp 14.81 130 31.48 88 112.5

Castrol India 14.81 130 24.07 150 62.5

Sintex Industries 14.81 130 29.63 107 100

Nirma 14.81 130 20.37 174 37.5

ING Vysya Bank 14.81 130 31.48 88 112.5

Raymond 14.81 130 25.93 136 75

CMC 14.81 130 14.81 202 0

Balrampur Chini Mills 14.81 130 24.07 150 62.5

Simplex Infrastructures 14.81 130 22.22 163 50

Monsanto India 14.81 130 42.59 23 187.5

Uflex 14.81 130 29.63 107 100

Coromandel Fertilisers 14.81 130 27.78 117 87.5

Tata Elxsi 14.81 130 35.19 59 137.5

Emco 14.81 130 40.74 33 175

HFCL Infotel 14.81 130 31.48 88 112.5

Grindwell Norton 14.81 130 27.78 117 87.5

HDFC Bank 12.96 150 27.78 117 114.29

Axis Bank 12.96 150 33.33 77 157.14

Pidilite Industries 12.96 150 31.48 88 142.86

Kirloskar Oil Engines 12.96 150 31.48 88 142.86

Dishman Pharmaceuticals 12.96 150 27.78 117 114.29

Asian Hotels 12.96 150 12.96 207 0

Ashapura Minechem 12.96 150 16.67 195 28.57

Bharat Bijlee 12.96 150 12.96 207 0

KSB Pumps 12.96 150 18.52 183 42.86

Cont…

104

Name of company

2003-04 2007-08 Percentage change in disclosure

score in the year 2007-08 over 2003-04

Disclosure score (%)

Rank Disclosure score (%)

Rank

Deepak Fertilisers & Petrochemicals Corporation 12.96 150 9.26 224 -28.57

Mastek 12.96 150 20.37 174 57.14

Graphite India 12.96 150 18.52 183 42.86

JSW Steel 11.11 162 51.85 8 366.67

Divi's Laboratories 11.11 162 20.37 174 83.33

Great Eastern Shipping Co. 11.11 162 12.96 207 16.67

Alstom Projects India 11.11 162 27.78 117 150

EIH 11.11 162 16.67 195 50

Ansal Properties & Infrastructure 11.11 162 22.22 163 100

Shriram Transport Finance Co. 11.11 162 31.48 88 183.33

P&G 11.11 162 22.22 163 100

GTL . 11.11 162 44.44 19 300

Mercator Lines 11.11 162 25.93 136 133.33

Electrosteel Castings 11.11 162 16.67 195 50

Timken India . 11.11 162 7.41 229 -33.33

HEG 11.11 162 24.07 150 116.67

Oriental Hotels 11.11 162 7.41 229 -33.33

Zuari Industries 11.11 162 11.11 217 0

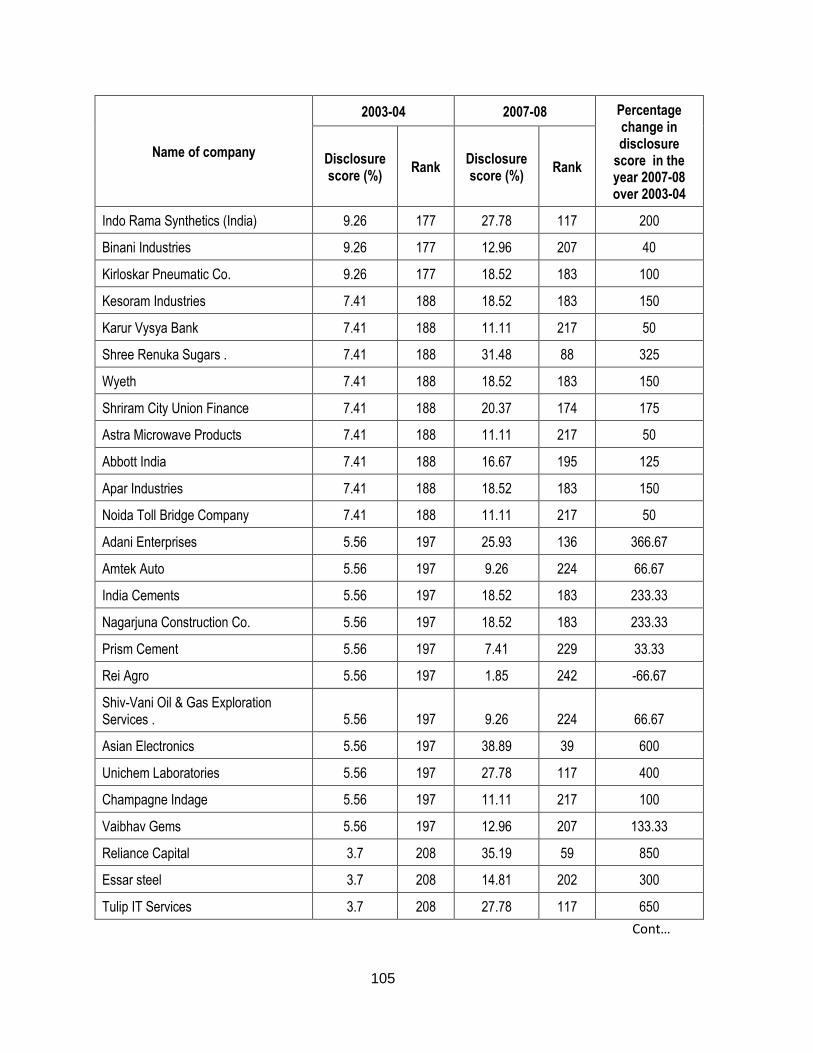

Cipla 9.26 177 18.52 183 100

Industrial Development Bank of India 9.26 177 25.93 136 180

Kalpataru Power Transmission 9.26 177 11.11 217 20

Hindustan Construction Co. 9.26 177 29.63 107 220

Blue Star 9.26 177 46.3 14 400

Nava Bharat Ventures 9.26 177 24.07 150 160

Arvind Mills 9.26 177 16.67 195 80

Sical Logistics 9.26 177 22.22 163 140

Cont…

105

Name of company

2003-04 2007-08 Percentage change in disclosure

score in the year 2007-08 over 2003-04

Disclosure score (%)

Rank Disclosure score (%)

Rank

Indo Rama Synthetics (India) 9.26 177 27.78 117 200

Binani Industries 9.26 177 12.96 207 40

Kirloskar Pneumatic Co. 9.26 177 18.52 183 100

Kesoram Industries 7.41 188 18.52 183 150

Karur Vysya Bank 7.41 188 11.11 217 50

Shree Renuka Sugars . 7.41 188 31.48 88 325

Wyeth 7.41 188 18.52 183 150

Shriram City Union Finance 7.41 188 20.37 174 175

Astra Microwave Products 7.41 188 11.11 217 50

Abbott India 7.41 188 16.67 195 125

Apar Industries 7.41 188 18.52 183 150

Noida Toll Bridge Company 7.41 188 11.11 217 50

Adani Enterprises 5.56 197 25.93 136 366.67

Amtek Auto 5.56 197 9.26 224 66.67

India Cements 5.56 197 18.52 183 233.33

Nagarjuna Construction Co. 5.56 197 18.52 183 233.33

Prism Cement 5.56 197 7.41 229 33.33

Rei Agro 5.56 197 1.85 242 -66.67

Shiv-Vani Oil & Gas Exploration Services . 5.56 197 9.26 224 66.67

Asian Electronics 5.56 197 38.89 39 600

Unichem Laboratories 5.56 197 27.78 117 400

Champagne Indage 5.56 197 11.11 217 100

Vaibhav Gems 5.56 197 12.96 207 133.33

Reliance Capital 3.7 208 35.19 59 850

Essar steel 3.7 208 14.81 202 300

Tulip IT Services 3.7 208 27.78 117 650

Cont…

106

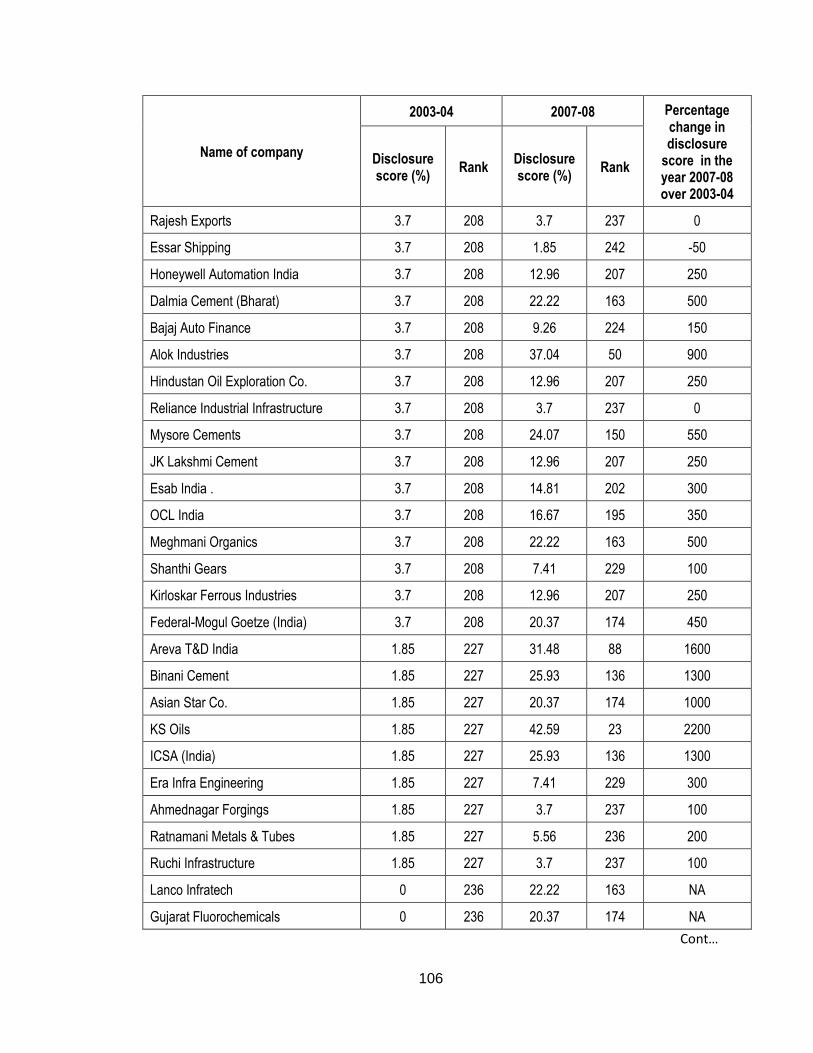

Name of company

2003-04 2007-08 Percentage change in disclosure

score in the year 2007-08 over 2003-04

Disclosure score (%)

Rank Disclosure score (%)

Rank

Rajesh Exports 3.7 208 3.7 237 0

Essar Shipping 3.7 208 1.85 242 -50

Honeywell Automation India 3.7 208 12.96 207 250

Dalmia Cement (Bharat) 3.7 208 22.22 163 500

Bajaj Auto Finance 3.7 208 9.26 224 150

Alok Industries 3.7 208 37.04 50 900

Hindustan Oil Exploration Co. 3.7 208 12.96 207 250

Reliance Industrial Infrastructure 3.7 208 3.7 237 0

Mysore Cements 3.7 208 24.07 150 550

JK Lakshmi Cement 3.7 208 12.96 207 250

Esab India . 3.7 208 14.81 202 300

OCL India 3.7 208 16.67 195 350

Meghmani Organics 3.7 208 22.22 163 500

Shanthi Gears 3.7 208 7.41 229 100

Kirloskar Ferrous Industries 3.7 208 12.96 207 250

Federal-Mogul Goetze (India) 3.7 208 20.37 174 450

Areva T&D India 1.85 227 31.48 88 1600

Binani Cement 1.85 227 25.93 136 1300

Asian Star Co. 1.85 227 20.37 174 1000

KS Oils 1.85 227 42.59 23 2200

ICSA (India) 1.85 227 25.93 136 1300

Era Infra Engineering 1.85 227 7.41 229 300

Ahmednagar Forgings 1.85 227 3.7 237 100

Ratnamani Metals & Tubes 1.85 227 5.56 236 200

Ruchi Infrastructure 1.85 227 3.7 237 100

Lanco Infratech 0 236 22.22 163 NA

Gujarat Fluorochemicals 0 236 20.37 174 NA

Cont…

107

Name of company

2003-04 2007-08 Percentage change in disclosure

score in the year 2007-08 over 2003-04

Disclosure score (%)

Rank Disclosure score (%)

Rank

JM Financial 0 236 22.22 163 NA

Bhushan Steel 0 236 22.22 163 NA

Jyoti Structures 0 236 7.41 229 NA

Amtek India 0 236 9.26 224 NA

Ganesh Housing Corpn. 0 236 3.7 237 NA

HBL Power Systems 0 236 11.11 217 NA

108

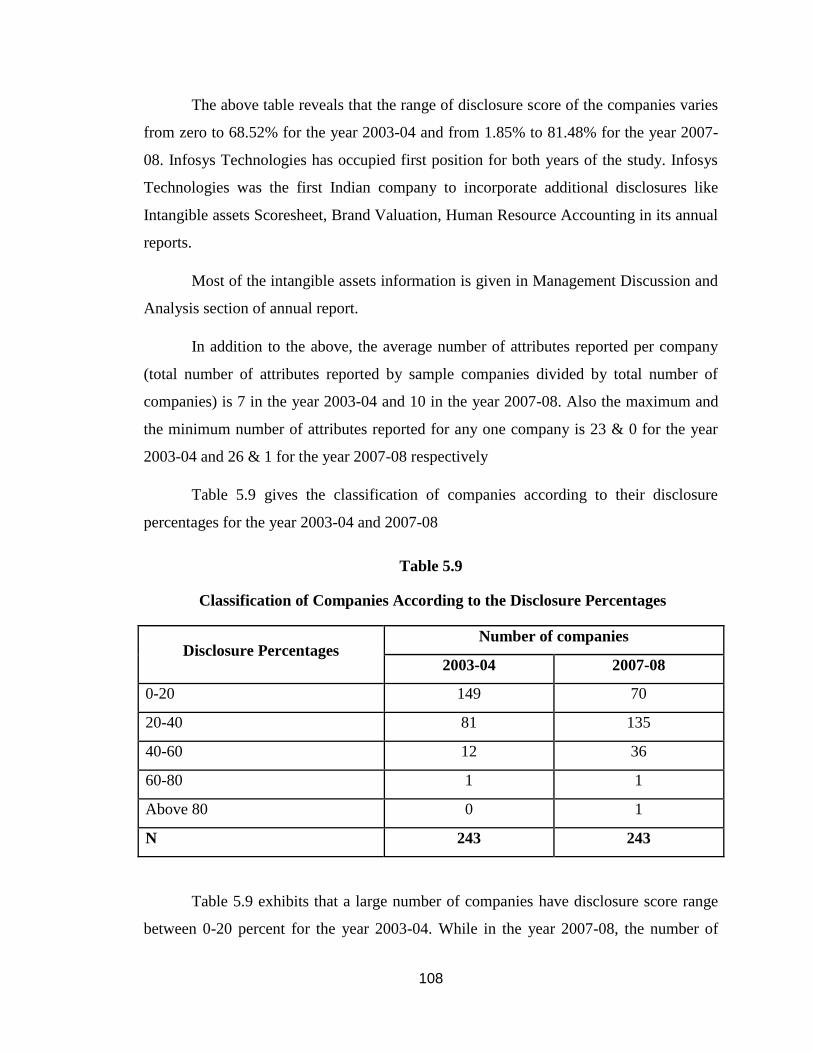

The above table reveals that the range of disclosure score of the companies varies

from zero to 68.52% for the year 2003-04 and from 1.85% to 81.48% for the year 2007-

08. Infosys Technologies has occupied first position for both years of the study. Infosys

Technologies was the first Indian company to incorporate additional disclosures like

Intangible assets Scoresheet, Brand Valuation, Human Resource Accounting in its annual

reports.

Most of the intangible assets information is given in Management Discussion and

Analysis section of annual report.

In addition to the above, the average number of attributes reported per company

(total number of attributes reported by sample companies divided by total number of

companies) is 7 in the year 2003-04 and 10 in the year 2007-08. Also the maximum and

the minimum number of attributes reported for any one company is 23 & 0 for the year

2003-04 and 26 & 1 for the year 2007-08 respectively

Table 5.9 gives the classification of companies according to their disclosure

percentages for the year 2003-04 and 2007-08

Table 5.9

Classification of Companies According to the Disclosure Percentages

Disclosure Percentages Number of companies

2003-04 2007-08

0-20 149 70

20-40 81 135

40-60 12 36

60-80 1 1

Above 80 0 1

N 243 243

Table 5.9 exhibits that a large number of companies have disclosure score range

between 0-20 percent for the year 2003-04. While in the year 2007-08, the number of

109

companies having disclosure score range between 0-20 percent has declined and shifted

to higher disclosure score range of 20-40 percent. The companies whose disclosure score

remarkably improved in the year 2007-08 over the year 2003-04 are KS Oils ltd (1.85%

to 42.59%), ICSA ltd ( 1.85% to 25.93%), Binani Cement (1.85% to 25.93%), Asian Star

Co. (1.85% to 20.37%) etc. This shift marks the companies’ consistent efforts to improve

their intangible assets disclosures.

Table 5.9 also exhibits that number of companies disclosing within the range of

40-60 percent have also increased from 12 to 36. While none of the companies is

disclosing in “above 80” range in the year 2003-04, Infosys Technologies is the first

company to break into this range for the year 2007-08.

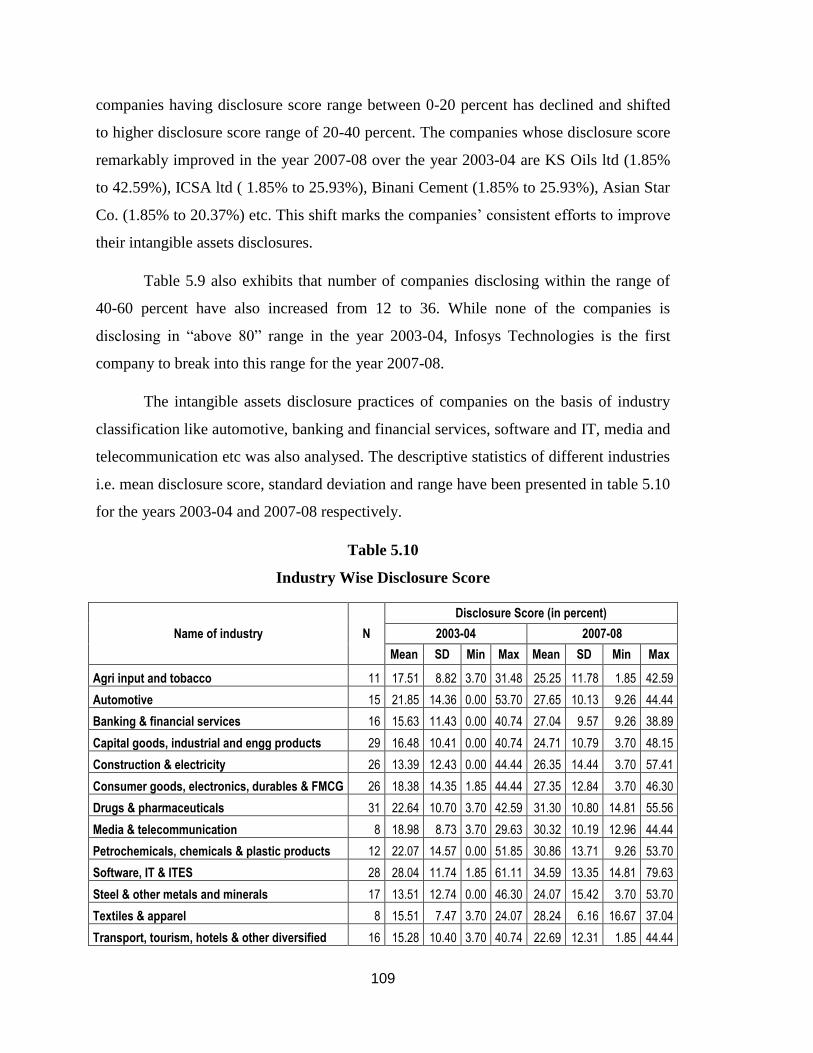

The intangible assets disclosure practices of companies on the basis of industry

classification like automotive, banking and financial services, software and IT, media and

telecommunication etc was also analysed. The descriptive statistics of different industries

i.e. mean disclosure score, standard deviation and range have been presented in table 5.10

for the years 2003-04 and 2007-08 respectively.

Table 5.10

Industry Wise Disclosure Score

Name of industry N

Disclosure Score (in percent)

2003-04 2007-08

Mean SD Min Max Mean SD Min Max

Agri input and tobacco 11 17.51 8.82 3.70 31.48 25.25 11.78 1.85 42.59

Automotive 15 21.85 14.36 0.00 53.70 27.65 10.13 9.26 44.44

Banking & financial services 16 15.63 11.43 0.00 40.74 27.04 9.57 9.26 38.89

Capital goods, industrial and engg products 29 16.48 10.41 0.00 40.74 24.71 10.79 3.70 48.15

Construction & electricity 26 13.39 12.43 0.00 44.44 26.35 14.44 3.70 57.41

Consumer goods, electronics, durables & FMCG 26 18.38 14.35 1.85 44.44 27.35 12.84 3.70 46.30

Drugs & pharmaceuticals 31 22.64 10.70 3.70 42.59 31.30 10.80 14.81 55.56

Media & telecommunication 8 18.98 8.73 3.70 29.63 30.32 10.19 12.96 44.44

Petrochemicals, chemicals & plastic products 12 22.07 14.57 0.00 51.85 30.86 13.71 9.26 53.70

Software, IT & ITES 28 28.04 11.74 1.85 61.11 34.59 13.35 14.81 79.63

Steel & other metals and minerals 17 13.51 12.74 0.00 46.30 24.07 15.42 3.70 53.70

Textiles & apparel 8 15.51 7.47 3.70 24.07 28.24 6.16 16.67 37.04

Transport, tourism, hotels & other diversified 16 15.28 10.40 3.70 40.74 22.69 12.31 1.85 44.44

110

Table 5.10 shows that the companies belonging to different industries have

variations in their mean disclosure score for both years of the study. It clearly shows that

the mean disclosure score of software industry is highest for both years of the study. The

score is 28.04% in 2003-04 and this increased to 34.59% in the year 2007-08.Variations

and range has also increased in the year 2007-08 over 2003-04.The mean disclosure score

of drugs and pharmaceutical industry has increased from 22.62% in the year 2003-04 to

31.30% in year 2007-08. This industry occupies second highest mean disclosure score for

both years of the study. A slight increase in variations and range is also noticed for this

industry in the year 2007-08 as compared to 2003-04.

The mean disclosure score of petrochemicals, chemicals & plastic products

industry has also increased from 22.07% to 30.86% in the year 2007-08. Variations for

this industry have reduced from 14.57% to 13.71%. The textiles and apparel industry has

also improved its mean disclosure score from15.51% to 28.64% in the year 2007-08.The

variations in the disclosure score for this industry are the least of all industries. It is

7.47% for the year 2003-04 and it further decreased to 6.16% for the year 2007-08.

Though the range of disclosure score has remained constant over the period of study.

The mean disclosure score of automotive industry increased from 21.85% in year

2003-04 to 27.65% in year 2007-08. Variations and range declined over the two periods

of study. In case of banking and financial services industry mean disclosure score has

also increased from 15.63% to 27.04% in the year 2007-08. Variations declined from

11.43% to 9.57%.

The mean disclosure score for remaining industries has improved in year 2007-08

over the year 2003-04. The score is 13.39% or above 13.39% for the two years of study.

Variations and range has also increased for all the industries.

Thus, the disclosure regarding intangible assets has improved for almost all the

industries for the year 2007-08 over the year 2003-04.This might be inspired by higher

investor expectation from all the companies belonging to different industries.

111

The finding that the mean disclosure score of software, IT and ITES industry is

highest as compared to other industries is not surprising. Firms in this knowledge based

industry need to be more proactive as they face greater competition and they often have

to rely on immutable intangibles that are difficult for competitors to imitate (Teece,

2000).

The high mean disclosure score for Drugs and pharmaceutical industry could be

motivated by the need to recognise the research activities and patents in this industry.

Further brands, customers and markets are key competitive factors which influence the

business of companies in media and telecommunication industry. This could be the

reason for high mean disclosure score for this industry.

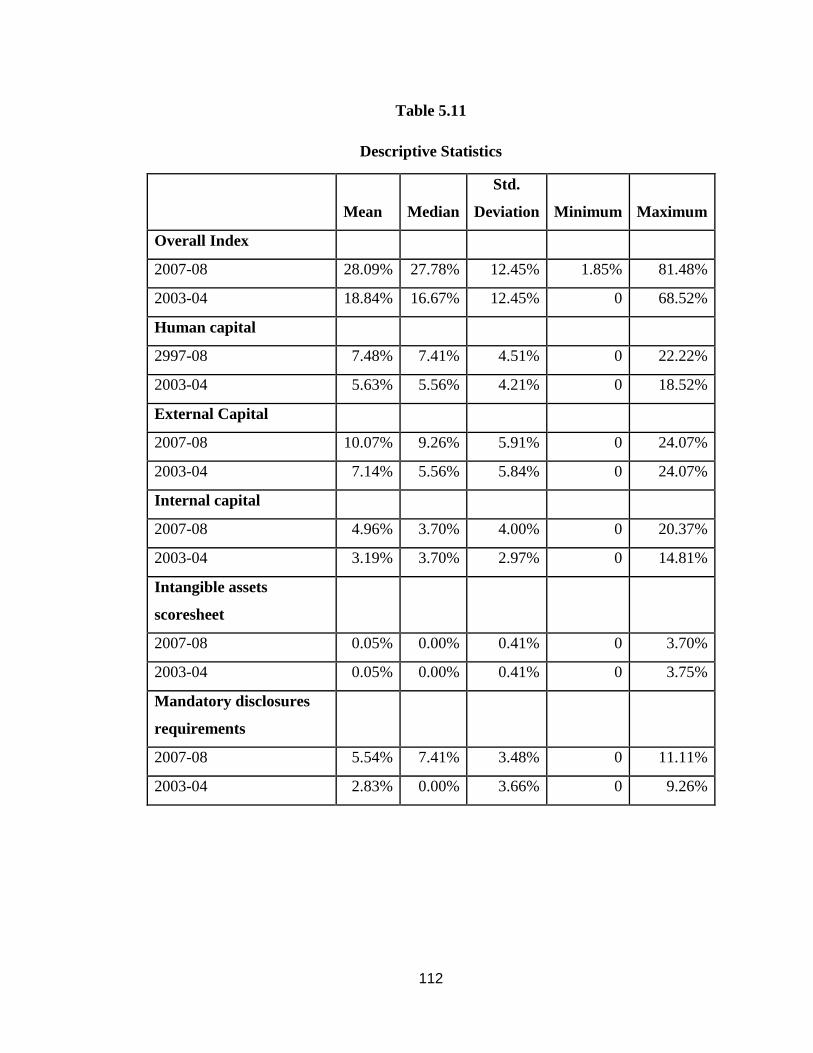

5.6 DESCRIPTIVE STATISTICS

Table 5.11 explains the descriptive statistics for each of the five categories of

intangible assets disclosure index. The table shows that the disclosures (though low) have

improved for both the years of the study. The overall mean disclosure is 18.84% for the

year 2003-04. It increased to 28.09% in the year 2007-08. Overall variation remained

same for both the years but the range of disclosures has increased in the year 2007-08.

The range of intangible asset disclosure is zero to 68.52% in 2003-04 and 1.85%

to 81.48% in 2007-08. After removing the disclosure score of outperforming companies

(namely Infosys Technologies Ltd. and Satyam Computer Services Ltd.) the range comes

down to zero to 53.70% for the year 2003-04 and 1.85% to 57.41% for the year 2007-08.

The mean disclosure score of human capital is 5.63% in the year 2003-04 and it

increased to 7.48% in the year 2007-08. Variation and range of scores also improved in