Embed Size (px)

Citation preview

Colombia and SiemensHannover, April 2015

Colombia and SiemensEnrique Gonzalez Z., Corporate Strategy Siemens AG

© Siemens AG 2015. All rights reserved. siemens.com

Siemens’ solid portfolio and geographical mix is the base of today’s and tomorrow’s future success

Power and Gas18%16%

Healthcare Asia, Australia

20%

Germany15%

Revenue by RegionRevenue by Sector

Energy 15%

Wind PowerRenewables8%

18%Process Industries

and Drives 13%

13%

16% 20%

Europe, C.I.S.,Africa,26% 39%

15%

Based on customer locationBuilding Technologies

8%Management

Mobility

10%13%

Digital FactoryMiddle East(excl. Germany)

Americas39%

In millions of € FY 2013 FY 2014

Employees in thousandsRevenue in millions of €

Continuing operationsRevenue and employees

100,000 500 In millions of € FY 2013 FY 2014

New orders 79,755 78,350

Revenue 73,445 71,920

Income 4,409 5,507

,

80,000

60,000

40 000

500

400

300

200

As reported in annual reports

Free cash flow 5,328 5,201

Employees 348,000 343,000

40,000

20,000

0

200

100

FY 20001986 1990 1995 2005 2014

March 2015Page 2

© Siemens AG 2015. All rights reserved. siemens.com

As reported in annual reports

Siemens is a strong local partner for customers in more than 200 countries

Americas Europe, C.I.S., Africa, Middle East

70,00018.8 76

211 000Siemens in Colombia

38.7 139211,000

26% 26%

54% 48%

• Business partner for more than 60 years• More than 1600 employees• Main office for Austral-Andina region• More than 30% of the installed

20%

62% 54% 48%electrical transmission systems has Siemens equipment

• Siemens is the supplier for 49% of the installed fossil power generation C t t f l

62%

Asia, Australia

62,000 14.474

• Competence center for sales, engineering, project management for all Siemens business units

• Factory: 96.000 mt2, design, engineering and production of drives

Barranquilla

Medellin

Cali

Bogotá / Tenjo

20% 26%engineering and production of drives, LV, MV and control panels, high voltage and distribution transformers, shelters for O&G and mining industries

26%

Employees Major production facilitiesRevenue (billions of €)Main office

Production center

Region Austral-Andina main office

S l ffi

March 2015Page 3

© Siemens AG 2015. All rights reserved. siemens.com

All numbers FY 2014 and refering to continuing operations Due to rounding, percentages may not add up to precisely 100

Sales offices

Siemens has been in Colombia since the beginning of the last century

Leo Kopp (founder of Bavaria Brewery), imported a Siemens Water Plant

Siemens Colombia is established in Bogota

1907

1954

Built the first transformers in the manufacturing plant in Colombia

Supplies the control center for the national energy dispatch center

Siemens supplies the first gas turbine in Colombia used for

1960

1998

2004 Siemens supplies the first gas turbine in Colombia used for cogeneration in an industry in Colombia

Project for the interconnection at 550/230 KV for the electrical highway connecting the north and the south of Colombia

2004

2007

Project for the SCADA, protection, auxiliary and medium voltage systems for the power plant Porce III

Siemens opens a new factory in Tenjo, near Bogotá

2008

2009

Siemens supplies steam turbine generator (40 MW), the biggest generation unit in the sugar refinery industry

Seven Turbo generators (3x47 MW Gas Turbines plus 2x21+2x24MW 2012 g ( pSteam Turbines) for the oil refinery in Cartagena

Installation of a SVC system in the substation Bacata. One of the most power full systems installed at the highest level over the sea

2012

2013

March 2015Page 4

© Siemens AG 2015. All rights reserved. siemens.com

Global trends are driving our business along the value chain of electrification

Global trends Market development (illustrative)Global trends

Digital transformation Market growth: ~7-9%

Market development (illustrative)

1

Globalization

Digitalization

M k t th 4 6%

Market growth: 7 9%Networked world of complex and hetero-geneous systems

2 Globalization

AutomationMarket growth: ~4-6%

Global competitiondriving productivity & localization

2

3

Globalization

Urbanization

Electrification Market growth: ~2-3%Infrastructure invest-ment needs of urban agglomerations

3

Demographicchange

Today Mid term-2020Decentralized demand of a growing and aging population

4

Climate change

and aging population

Higher resource efficiency in an all-

5Power Generation Power Transmission,

Distribution & Smart GridEfficient Energy Application Imaging &

In-Vitro Diagnostics

March 2015Page 5

© Siemens AG 2015. All rights reserved. siemens.com

efficiency in an allelectric world

Based on the global trends we were looking for what is coming next after BRIC

SEWEC – Second wave emerging countries

March 2015Page 6

© Siemens AG 2015. All rights reserved. siemens.com

Note: Shown is only group A (Long-term); Not shown: Group B (Short-term), Group C (All ready addressed) and Group D (Watch list)

Trend analysis was based on drivers, enablers andblocking points of GDP growth

SEWEC specific country trends GDP growth drivers

Population

Enablers and blocking points

Exploration of natural resourcesPopulation

Foreign direct investment

Existing infrastructure

Age distrib tion

Political system Laws Security

Exploration of natural resources Oil & Gas

Mining

Biological Age distribution

Education

Urbanization

Biological

Build-up of infrastructure Energy

W tGDP Growth Technology penetration

Lack of wealth

Natural resources

Water

Transportation

Buildings

GDP Growth

Regional associations

Geographic situation

Strength of corporations

Transformation of economic structure Healthcare

Production Public spending Environmental

protectiong p

Entrepreneurship Services protection

March 2015Page 7

© Siemens AG 2015. All rights reserved. siemens.com

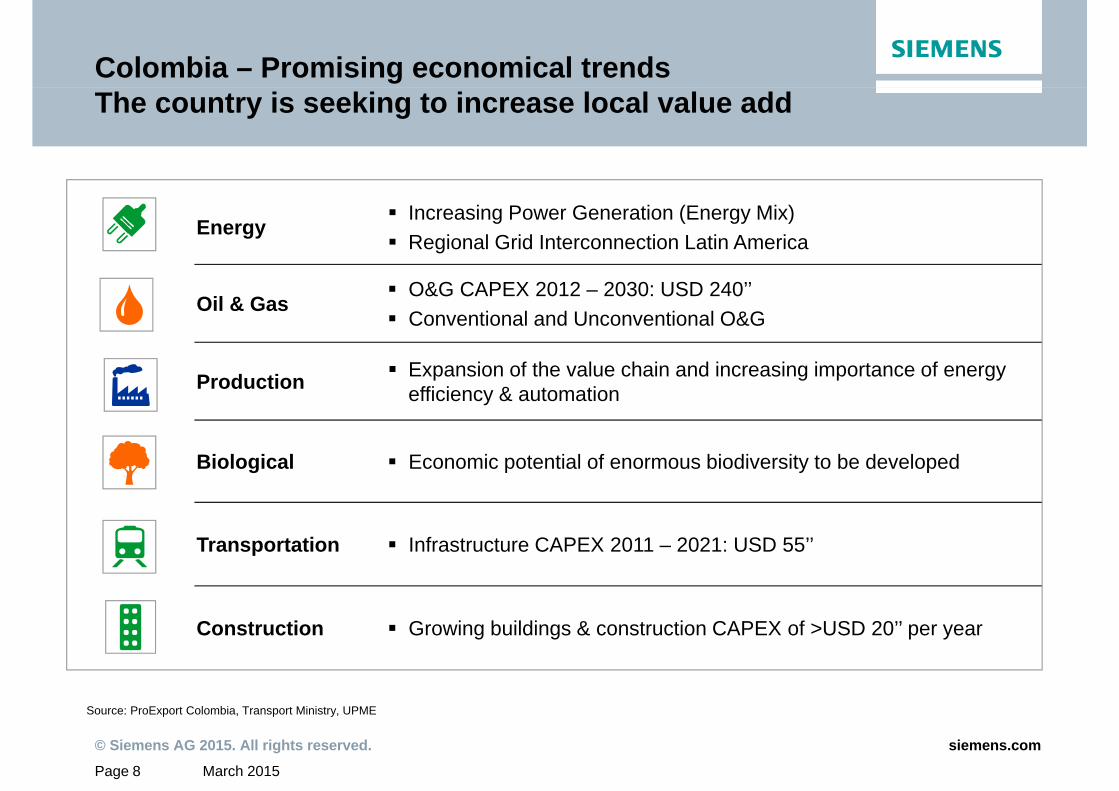

Colombia – Promising economical trendsThe country is seeking to increase local value add

Energy Increasing Power Generation (Energy Mix) Regional Grid Interconnection Latin America

Oil & Gas O&G CAPEX 2012 – 2030: USD 240’’ Conventional and Unconventional O&G

Production Expansion of the value chain and increasing importance of energy efficiency & automation

Biological Economic potential of enormous biodiversity to be developed

Transportation Infrastructure CAPEX 2011 – 2021: USD 55’’

Construction Growing buildings & construction CAPEX of >USD 20’’ per year

March 2015Page 8

© Siemens AG 2015. All rights reserved. siemens.com

Source: ProExport Colombia, Transport Ministry, UPME

Colombia has turned into a vibrant democracyFacts & Expectations along the economic growth path

2000 2014 Future

Economical Crisis beginning Economy in growth Competitive growth energy sector and

situation Crisis beginning y gafter financial crisis

gyexpansion of the value chain

Employment High levels of unemployment

Employment: Increase & formalization period

Low unemployment levelsp y unemployment & formalization period levels

Investment Low levels of investment

The highest levels of investment in history

Maintain investment degree

International relations

Isolated government of the rest of the world

Integrated with the international community

Integrated with the international community

Governability Low High HighGovernability Low High High

Public Institutions Weak Strong Strong

Security High levels of insecurity Democratic security Democratic prosperity

March 2015Page 9

© Siemens AG 2015. All rights reserved. siemens.com

Source: ANDI (Asociación Nacional de Empresarios de Colombia)

Contact

Thank youEnrique Gonzalez Zanetich

Siemens AGWittelsbacherplatz 2Thank you Wittelsbacherplatz 280333 MunichGermany

E-Mail: [email protected]

March 2015Page 10

© Siemens AG 2015. All rights reserved. siemens.com