Embed Size (px)

Citation preview

Coal Sector Report Indonesia 2000American Embassy Jakarta

COAL REPORTCOAL REPORTIndonesia

2000

October 2000Embassy of the United States of America

Jakarta

Coal Sector Report Indonesia 2000American Embassy Jakarta

Table of Contents Page

Introduction and Summary 1

Coal Resources 2-Resources 2-Quality 2-Coal bed methane 2

Production and Exports-Production – another record year 4-Future production 4-Exports exceed target 4-Coal marketing 5

Domestic Demand and Utilization-Domestic demand continues to rise 6-Coal-fired power plants 6-Cement plants 7-Coal briquettes below target 7

Environment-Environmental damage 8-Strict environmental regulation 8-Clean coal technology 8

Transportation and Coal Terminals 9

Contract and Investment 10-The autonomy laws 10-The existing contracts 10-Application process 10-New draft fourth generation CCOW 11-A difficult to realize divestment obligation 11-New incentives planned 12-Contracts signed 12-Investment 12

Current Producers-PT Tambang Batubara Bukit Asam 14-PT Kaltim Prima Coal 14-PT Adaro Indonesia 15-PT Berau Coal 15-PT Arutmin Indonesia 15-PT Kideco Jaya Agung 16-PT Allied Indo Coal 16- i -

Coal Sector Report Indonesia 2000American Embassy Jakarta

-PT Multi Harapan Utama 16-PT Tanito Harum 17-PT BHP Kendilo Coal Indonesia 17-PT Indominco Mandiri 17-New producers 17-Other producers 17-Contractors at the construction stage 18-Illegal mines 18

Appendices-Appendix 1: Coal reserves and resources 19-Appendix 2: Coal quality by producers 19-Appendix 3: Coal production by company 20-Appendix 4: Coal production and exports 21-Appendix 5: Coal exports by company 22-Appendix 6: Coal exports by destination 23-Appendix 7: Domestic sales of coal 24-Appendix 8: Coal utilization by industrial sector 25-Appendix 9: Status of private coal-fired power plants 26-Appendix 10: Coal loading ports and export terminals 28-Appendix 11: Main differences between CCC and CCOW 29-Appendix 12: Key contacts in the coal sector 30-Appendix 13: Indonesian coal contractors 31

- ii -

Coal Sector Report Indonesia 2000American Embassy Jakarta

GG LOSSARYLOSSARY

CCC Coal Cooperation ContractCCOW Coal Contract of WorkCOW Contract of WorkDWT Dead Weight TonIBT Indonesia Bulk TerminalGOI Government of IndonesiaHV Heat ValueKP Kuasa Pertambangan (Mining Authorization)KPC Kaltim Prima CoalMOU Memorandum of UnderstandingMW MegawattsMT Metric TonMT/Y Metric Ton/yearPCI Pulverized Coal InjectionPD Presidential DecreePLN Perusahaan Listrik Negara (State Electricity

Company)PTBA Perusahaan Tambang Batubara Bukit Asam(State

Coal Company)TBI Terminal Batubara Indah (a Coal Loading

Terminal)TBCT Tanjung Bara Coal Terminal

Exchange rates used:1998 - Rp 10,447/US dollar1999 - Rp 7,976/US dollar

- iii -

Coal Sector Report Indonesia 2000American Embassy Jakarta

1Introduction and Summary

Despite a slump in coal prices, 1999was a good year for Indonesia's coalindustry as production and exportscontinued to grow and set new records.

Almost all major coal producersmaintained revenue by increasingoutput and exports. Production grewsignificantly to 73.6 million metric tons(MT) from 61 million MT in 1998.Export tonnages jumped to 55.2 millionMT in 1999 from 46.9 million MT in1998. Approximately 70 percent ofthis amount was shipped to Asianmarkets. Domestic coal utilization alsojumped 25 percent to 18.8 million MTin 1999 from 15.1 million MT in 1998.

Looking forward, the Ministry ofEnergy and Mineral Resources(formerly the Ministry of Mines andEnergy until renamed in August 2000)set coal production targets of 84.5million MT in 2000, 105.3 million MTin 2002 and 109.6 million MT in 2003.With coal production increasing rapidlyfrom only 340,000 MT in 1980,Indonesia is now one of the world’slargest coal producers. The electricitysector’s increased usage of coal,extensive exploration activities,infrastructure development, andinternational marketing effortscontributed to this significant growth.

The share of coal in the country’senergy mix rose from 8.0 percent in1993 to 17.5 percent in 1999, primarilydue to the development of large coal-fired power plants which now provide4,660 megawatts (MW) of electricgeneration capacity. This sectorconsumes about 85 percent of domesticcoal production. Public electric utilityPerusahaan Listrik Negara (PLN)prefers coal as an energy source due toits relatively low price compared withoil and natural gas.

Coal mining firm PT Arutmin signedthe first Coal Cooperation Contract(CCC) in 1981. Other CCC’sfollowed, including 14 in 1998 and 25in 1999, to make a total of 137contracts up to the present. TheGovernment revised the contractualagreement terms several times. Thelatest revision, introduced in 1998,changed contract arrangements to aroyalty-based Coal Contract of Work(CCOW). Existing contracts have alsobeen amended based on the newCCOW. Currently, the Government isformulating the 4th generation CCOWin anticipation of ceding greaterautonomy to regional administrations.

Fifteen coal contractors (including threecontractors which entered commercialproduction in 1998/99) produce 76percent of Indonesia’s total coalproduction. Kaltim Prima Coal andAdaro Indonesia are the largest coalproducers.

Although the long-term view is bright,there are some troubling aspectsentering the new millennium. Severalcoal mining companies, particularlythose solely dependent on the domesticmarket, have been affected by thepostponement or suspension of coalpower projects as a result of theeconomic downturn. New legislationregarding regional autonomy and fiscaldecentralization which will beimplemented in 2001 has createdadditional uncertainty. End of summary.

Coal Sector Report Indonesia 2000American Embassy Jakarta

2

Resources

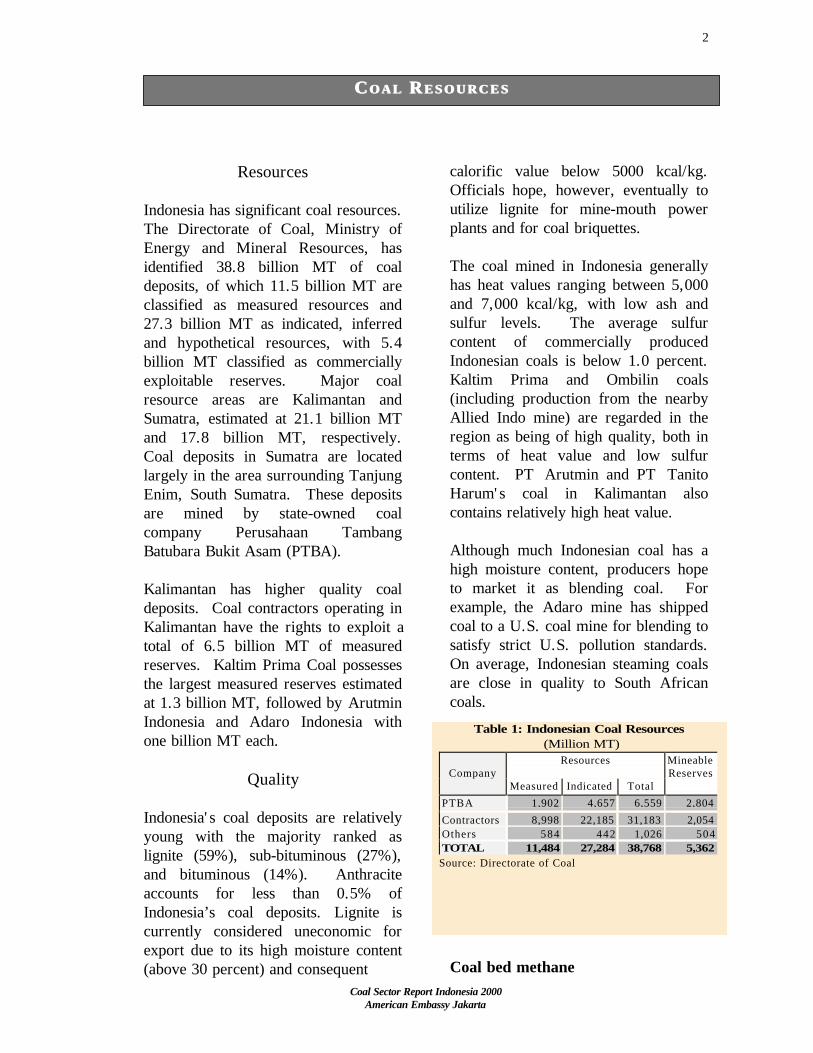

Indonesia has significant coal resources.The Directorate of Coal, Ministry ofEnergy and Mineral Resources, hasidentified 38.8 billion MT of coaldeposits, of which 11.5 billion MT areclassified as measured resources and27.3 billion MT as indicated, inferredand hypothetical resources, with 5.4billion MT classified as commerciallyexploitable reserves. Major coalresource areas are Kalimantan andSumatra, estimated at 21.1 billion MTand 17.8 billion MT, respectively.Coal deposits in Sumatra are locatedlargely in the area surrounding TanjungEnim, South Sumatra. These depositsare mined by state-owned coalcompany Perusahaan TambangBatubara Bukit Asam (PTBA).

Kalimantan has higher quality coaldeposits. Coal contractors operating inKalimantan have the rights to exploit atotal of 6.5 billion MT of measuredreserves. Kaltim Prima Coal possessesthe largest measured reserves estimatedat 1.3 billion MT, followed by ArutminIndonesia and Adaro Indonesia withone billion MT each.

Quality

Indonesia's coal deposits are relativelyyoung with the majority ranked aslignite (59%), sub-bituminous (27%),and bituminous (14%). Anthraciteaccounts for less than 0.5% ofIndonesia’s coal deposits. Lignite iscurrently considered uneconomic forexport due to its high moisture content(above 30 percent) and consequent

calorific value below 5000 kcal/kg.Officials hope, however, eventually toutilize lignite for mine-mouth powerplants and for coal briquettes.

The coal mined in Indonesia generallyhas heat values ranging between 5,000and 7,000 kcal/kg, with low ash andsulfur levels. The average sulfurcontent of commercially producedIndonesian coals is below 1.0 percent.Kaltim Prima and Ombilin coals(including production from the nearbyAllied Indo mine) are regarded in theregion as being of high quality, both interms of heat value and low sulfurcontent. PT Arutmin and PT TanitoHarum's coal in Kalimantan alsocontains relatively high heat value.

Although much Indonesian coal has ahigh moisture content, producers hopeto market it as blending coal. Forexample, the Adaro mine has shippedcoal to a U.S. coal mine for blending tosatisfy strict U.S. pollution standards.On average, Indonesian steaming coalsare close in quality to South Africancoals.

Coal bed methane

CC O A L O A L RR E S O U R C E SE S O U R C E S

Table 1: Indonesian Coal Resources (Million MT)

CompanyResources Mineable

ReservesMeasured Indicated Total

PTBA 1,902 4,657 6,559 2,804

Contractors 8,998 22,185 31,183 2,054Others 584 442 1,026 504TOTAL 11,484 27,284 38,768 5,362

Source: Directorate of Coal

2

Coal Sector Report Indonesia 2000American Embassy Jakarta

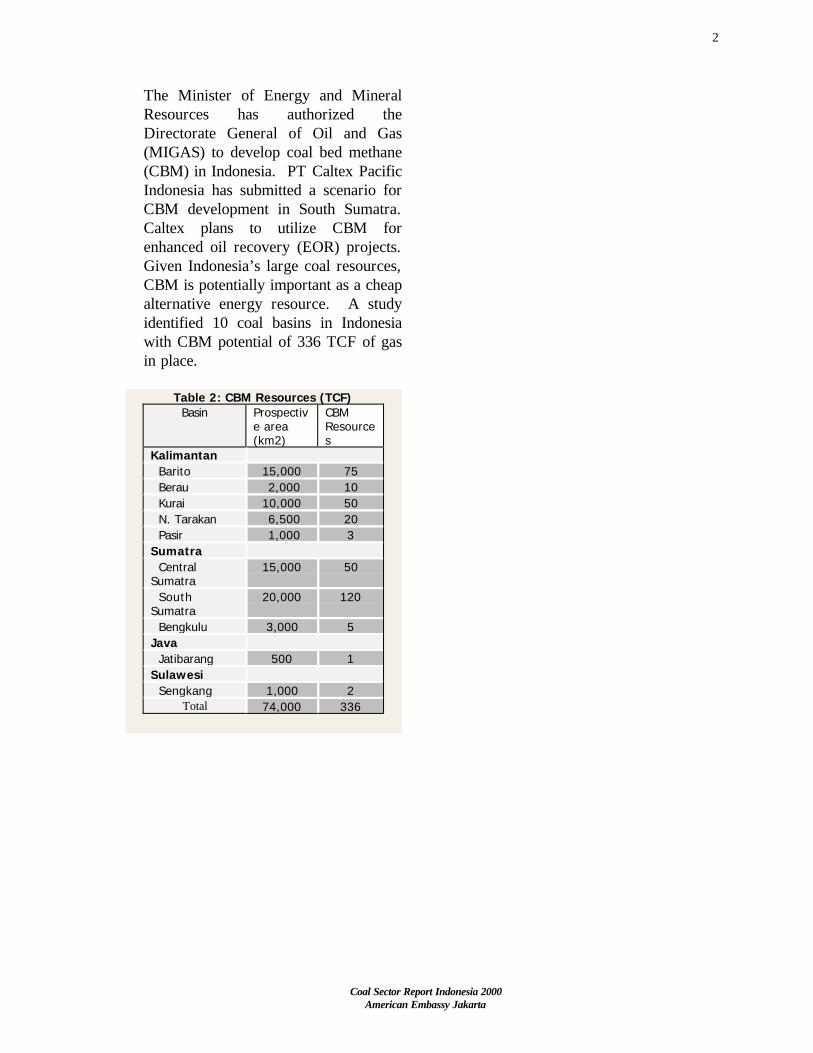

The Minister of Energy and MineralResources has authorized theDirectorate General of Oil and Gas(MIGAS) to develop coal bed methane(CBM) in Indonesia. PT Caltex PacificIndonesia has submitted a scenario forCBM development in South Sumatra.Caltex plans to utilize CBM forenhanced oil recovery (EOR) projects.Given Indonesia’s large coal resources,CBM is potentially important as a cheapalternative energy resource. A studyidentified 10 coal basins in Indonesiawith CBM potential of 336 TCF of gasin place.

Table 2: CBM Resources (TCF)Basin Prospectiv

e area(km2)

CBMResources

Kalimantan Barito 15,000 75 Berau 2,000 10 Kurai 10,000 50 N. Tarakan 6,500 20 Pasir 1,000 3Sumatra CentralSumatra

15,000 50

SouthSumatra

20,000 120

Bengkulu 3,000 5Java Jatibarang 500 1Sulawesi Sengkang 1,000 2

Total 74,000 336

3

Coal Sector Report Indonesia 2000American Embassy Jakarta

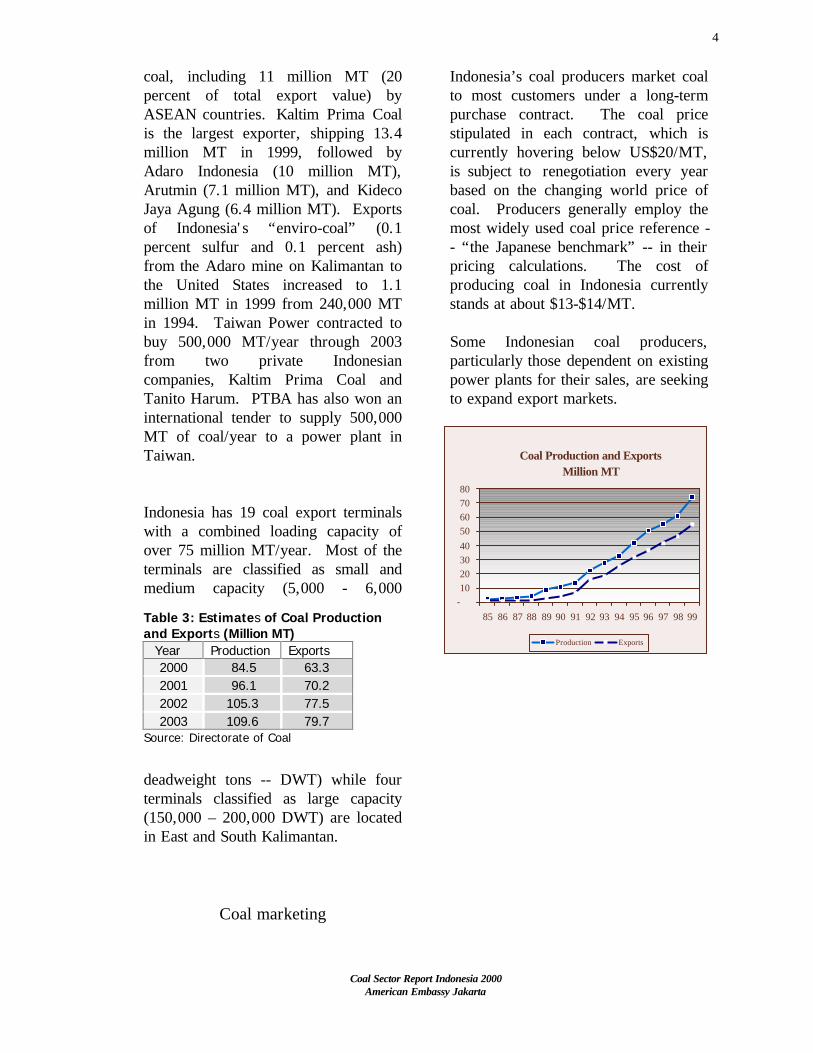

Production - Another record year

Coal production increased by over 20percent in 1999, reaching 73.6 millionMT compared to 61 million MT in1998. The fifteen private coalcompanies operating under CCOWproduced 57.6 million MT. The fourtop private producers, Kaltim PrimaCoal, Adaro Indonesia, Arutmin andKideco Jaya Agung, alone produced 14million MT, 13.6 million MT, 8.7million MT and 7.3 million MTrespectively (total of 43.6 million MT).State–owned coal company PerusahaanTambang Batubara Bukit Asam (PTBA)produced 11.2 million MT from twomining operations in Sumatra. Over 75percent of Indonesian coal productionoriginated from East Kalimantan andthe remainder from South and WestSumatra. Five producers operatingunder second generation CCOW inKalimantan, with a total output of 3.6million MT/year, entered commercialproduction in 1998 and 1999.

Open-cut mines provide about 99percent of Indonesian coal production.There are only three undergroundmines -- at PTBA’s Ombilin operationin West Sumatra and two smalldomestic private mines in Kalimantan.Most mines use conventional truck andshovel mining methods. Excavatorswith buckets of 2-3 cubic meters aregenerally used to remove coal, which ishauled in 20-30 ton trucks. OnlyKaltim Prima's large-scale operationuses trucks of up to 135 MT capacityand shovels of up to 20 cubic metercapacity.

Future production

Despite current low coal prices andslack domestic market conditions, theIndonesian coal industry is stillexpected to expand due to growingworldwide demand. Only a few yearsago, the Government had also projecteddomestic demand for electricity to riseand coal production to increase steeply.Officials note that, although producersstill have the potential to produce aboveits estimates, GOI projections wereadjusted downward after thegovernment rescheduled nine of 14private coal-fired power plant projects.The GOI now forecasts production togrow to 84.5 million MT in 2000,105.3 million MT in 2002 and 109.6million MT in 2003. Actual output willbe determined by future marketconditions.

Exports exceed target

Indonesia achieved an impressivegrowth rate in coal exports, from onlysix million MT in 1991 to 55.2 millionMT in 1999. The GOI set exporttargets of 63.3 million MT in 2000,77.5 million MT in 2002 and 79.7million MT in 2003. (Officials notedthat year 2000 exports might not reachthe target because of KPC’s period ofshutdown forced by labor problems.)This rapid growth resulted fromextensive marketing efforts, includingIndonesia coal producers’ willingness toset coal prices at competitive levels togain international market share. In1999, Indonesia earned US$1.3 billionby exporting 75 percent of total coalproduction. Asia purchased 39.0million MT (70 percent) of Indonesia’s

PP RODUCTION AND RODUCTION AND EE X P O R T SX P O R T S

4

Coal Sector Report Indonesia 2000American Embassy Jakarta

Coal Production and ExportsMillion MT

-10203040

50607080

85 86 87 88 89 90 91 92 93 94 95 96 97 98 99

Production Exports

Table 3: Estimates of Coal Productionand Exports (Million MT) Year Production Exports

2000 84.5 63.32001 96.1 70.22002 105.3 77.52003 109.6 79.7

Source: Directorate of Coal

coal, including 11 million MT (20percent of total export value) byASEAN countries. Kaltim Prima Coalis the largest exporter, shipping 13.4million MT in 1999, followed byAdaro Indonesia (10 million MT),Arutmin (7.1 million MT), and KidecoJaya Agung (6.4 million MT). Exportsof Indonesia's “enviro-coal” (0.1percent sulfur and 0.1 percent ash)from the Adaro mine on Kalimantan tothe United States increased to 1.1million MT in 1999 from 240,000 MTin 1994. Taiwan Power contracted tobuy 500,000 MT/year through 2003from two private Indonesiancompanies, Kaltim Prima Coal andTanito Harum. PTBA has also won aninternational tender to supply 500,000MT of coal/year to a power plant inTaiwan.

Indonesia has 19 coal export terminalswith a combined loading capacity ofover 75 million MT/year. Most of theterminals are classified as small andmedium capacity (5,000 - 6,000

deadweight tons -- DWT) while fourterminals classified as large capacity(150,000 – 200,000 DWT) are locatedin East and South Kalimantan.

Coal marketing

Indonesia’s coal producers market coalto most customers under a long-termpurchase contract. The coal pricestipulated in each contract, which iscurrently hovering below US$20/MT,is subject to renegotiation every yearbased on the changing world price ofcoal. Producers generally employ themost widely used coal price reference -- “the Japanese benchmark” -- in theirpricing calculations. The cost ofproducing coal in Indonesia currentlystands at about $13-$14/MT.

Some Indonesian coal producers,particularly those dependent on existingpower plants for their sales, are seekingto expand export markets.

5

Coal Sector Report Indonesia 2000American Embassy Jakarta

DD O M E S T I C O M E S T I C DD EMAND AND EMAND AND UU T I L I Z A T I O NT I L I Z A T I O N

Domestic demand continues to rise

Despite the weakness of the Indonesianeconomy, the Government estimatesdomestic coal demand will increase toover 32 million MT per year within thenext five years due to the operation ofcoal-fired power plants and utilizationof fuel briquette coal by households andindustry. In 1999, domestic demandrose 21.4 percent to 18.8 million MTfrom 15.4 million MT in 1998. Of thisamount, PTBA supplied 9.6 millionMT, coal contractors supplied 8.5million MT, and private mines andcooperatives supplied the balance.Power plants and the cement industryare the major coal consumers, togetheraccounting for 77 percent of totaldemand.

Coal-fired power plants

Coal-fired power plants are expected tosupply about 45% of total energyproduction in the year 2000 comparedto natural gas’ share of 21% and oil’sof 18%. Fuel consumption by steamcoal-fired power plants in Indonesia isexpected to increase from 14.7 millionMT in 1999 to 27.8 million MT by2005. State electricity utilityPerusahaan Listrik Negara (PLN) is thebiggest coal consumer, utilizing 12.4million MT of coal in 1999 and 11million MT in 1998 to fuel its coalpower plants, which produce 4,330MW of power. In 1999, PLNconsumed 8.2 million MT of coal forits Suralaya units I-VII (3,200 MW),2.2 million MT for Paiton units I-II

(800 MW), and 4 million MT for otherplants (Bukit Asam [130MW], Ombilin[100 MW] and Sijantang [100 MW]).

PLN prefers to use coal over othermore expensive fuels for its powergeneration. Production cost per KWhof coal steam power plants averagesUS 1.4 cents. This average is lowerthan the US 1.9 cents for oil steampower plants, US 2.2 cents for oilcombined cycle power plants, and US2.5 cents for natural gas combinedcycle power plants.

Additional domestic demand will comefrom independent power projects(IPP’s), such as Paiton Swasta I (2x615MW), Paiton Swasta II (2x610 MW)and Tanjung Jati B (2x660 MW). TheGovernments of Indonesia andMalaysia signed a memorandum ofunderstanding (MOU) in 1999 for thejoint development of a 1,200 MWpower station at Cerenti, RiauProvince, which will utilize ligniteresources to supply the Sumatra andMalaysian markets. Some mine-mouthpower stations are also planned inSumatra and Kalimantan, particularly inareas with large reserves of lignite.These plants will require a total of 2.8million MT/year of coal. If all plannedcoal-fired power plants become fullyoperational, total coal power plantinstalled capacity will reach 12,100MW by 2003/04, requiring about 42million MT of coal per year. Factoringin delayed power plant projects,however, the Government revised itscoal demand projection for powergeneration to 56 million MT by 2010.

6

Coal Sector Report Indonesia 2000American Embassy Jakarta

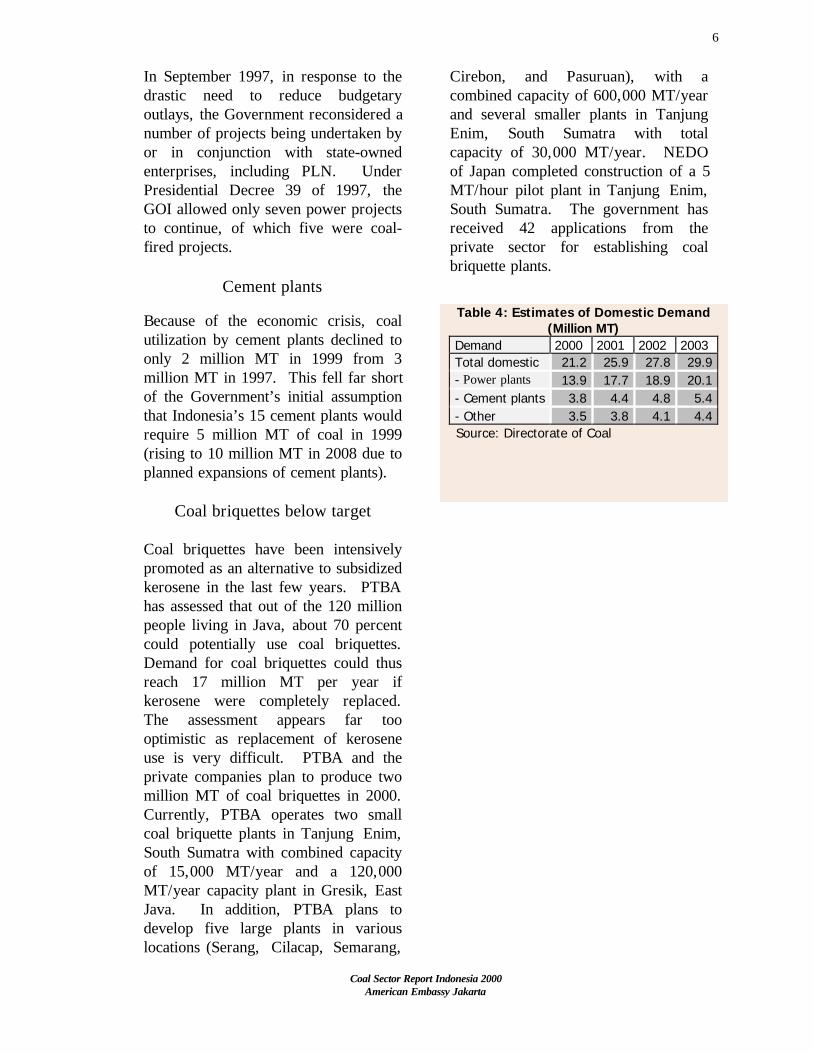

Table 4: Estimates of Domestic Demand(Million MT)

Demand 2000 2001 2002 2003Total domestic 21.2 25.9 27.8 29.9- Power plants 13.9 17.7 18.9 20.1- Cement plants 3.8 4.4 4.8 5.4- Other 3.5 3.8 4.1 4.4

Source: Directorate of Coal

In September 1997, in response to thedrastic need to reduce budgetaryoutlays, the Government reconsidered anumber of projects being undertaken byor in conjunction with state-ownedenterprises, including PLN. UnderPresidential Decree 39 of 1997, theGOI allowed only seven power projectsto continue, of which five were coal-fired projects.

Cement plants

Because of the economic crisis, coalutilization by cement plants declined toonly 2 million MT in 1999 from 3million MT in 1997. This fell far shortof the Government’s initial assumptionthat Indonesia’s 15 cement plants wouldrequire 5 million MT of coal in 1999(rising to 10 million MT in 2008 due toplanned expansions of cement plants).

Coal briquettes below target

Coal briquettes have been intensivelypromoted as an alternative to subsidizedkerosene in the last few years. PTBAhas assessed that out of the 120 millionpeople living in Java, about 70 percentcould potentially use coal briquettes.Demand for coal briquettes could thusreach 17 million MT per year ifkerosene were completely replaced.The assessment appears far toooptimistic as replacement of keroseneuse is very difficult. PTBA and theprivate companies plan to produce twomillion MT of coal briquettes in 2000.Currently, PTBA operates two smallcoal briquette plants in Tanjung Enim,South Sumatra with combined capacityof 15,000 MT/year and a 120,000MT/year capacity plant in Gresik, EastJava. In addition, PTBA plans todevelop five large plants in variouslocations (Serang, Cilacap, Semarang,

Cirebon, and Pasuruan), with acombined capacity of 600,000 MT/yearand several smaller plants in TanjungEnim, South Sumatra with totalcapacity of 30,000 MT/year. NEDOof Japan completed construction of a 5MT/hour pilot plant in Tanjung Enim,South Sumatra. The government hasreceived 42 applications from theprivate sector for establishing coalbriquette plants.

7

Coal Sector Report Indonesia 2000American Embassy Jakarta

Environmental damage

Coal mining operations are accused ofinflicting considerable environmentaldamage. Coal mining is estimated tohave disturbed over 70,000 hectares(Ha) of ground. In some areas, fluidwaste was discharged into nearbyrivers, affecting local residents’ sourcesof fresh water. This environmentalimpact and local demands for greatercompany contributions to communitydevelopment have become importantcauses of demands to close miningoperations.

Strict environmental regulation

The Government responded with acommitment that coal-mining operationswould conform to environmentalsafeguards. In 1999, it issuedGovernment Regulation No. 18 onprocessing of poisonous and hazardouswaste. The regulation requires miningcompanies to process their waste to anextraordinary degree of cleanliness,with standards set for water purity fivetimes stricter than the United States andCanada. However, implementation ofthe regulation has been postponed whilethe Indonesian government reevaluatesits provisions to make themcommensurate with existingtechnological capability.

Clean coal technology

Since the sulfur content of Indonesiancoal meets current emission standardswithout any additional equipment, noneof PLN’s current power plants has had

to use Flue Gas Desulphurization(FGD) combustion technology thus farto control SO2 emission. FGDequipment has been installed in thenewly completed private coal powerplant (2x615 MW) at Paiton, East Java.

With the issuance of Minister ofEnvironment Decree No. 13 in 1995which regulates the maximumpermissible SO2 emission from coalpower plants, all coal power plants inIndonesia starting from 2000 onwardswill need to use FGD, particularly forcoal with sulfur content higher than0.3%. The decree reduced permissibleatmospheric SO2 levels from 1,500mg/m3 to 750 mg/m3 by 2000.

The Government has a keen interest inimproving coal technology to reducecoal’s environmental impact. Efforts toenhance clean coal technology (CCT)have included cooperation with foreigncountries to study possible effects ofcoal usage and to seek new ways forcoal-fired power plants to meetenvironmental standards. In November1999, the U.S. Federal EnergyTechnology Center (FETC) signed aletter of intent with the Agency forTechnology Assessment andApplication to implement CCT inIndonesia. PTBA is also cooperatingwith several American companies tocarry out technological studies ofmethods to raise coal quality, includingliquefied coal, Carbontec, Syncoal andK-Fuel. Carbontec and K-Fuel appearto be the most approppriatetechnologies for PTBA’s coal.

EE NVIRONMENTNVIRONMENT

8

Coal Sector Report Indonesia 2000American Embassy Jakarta

In the 1990’s, coal producers and otherfirms made heavy investments in thedevelopment of coal loading terminals.The expansion of Indonesian coalproduction and exports and the successof coal contractors in developing long-term exports depend heavily on thequality of facilities to transport coalfrom coalfields to customers. The GOIand contractors continue to developroad access and facilities to move coalfrom mine to stockpile and to load coalonto rails, barges or ocean-goingvessels. Transportation systems thatprovide access to the mining area andlink mine–mouth with domestic orexport markets are still limited,however, particularly in South and EastKalimantan.

Currently, Indonesia operates 19 coalloading terminals, including three cape-sized terminals, one panamax terminaland three handy-size terminals, with atotal export capacity of more than 75million MT/year. Four additional coalterminals are planned, includingBengalon by KPC, Sebuku byCakrawala Sebuku, Bontang byIndominco Mandiri and EastKalimantan by Indexim. Below is a listof the largest coal loading portscurrently in operation in Indonesia.

(1) The Indonesia Bulk Terminal (IBT),developed jointly by Consolidated BulkHandling of Australia and TerminalBatubara Indah, is the latest common-user deep-water port. IBT, whichcommenced operation in 1997, islocated on South Pulau Laut, a largeisland off South Kalimantan. It lies onmajor domestic and international

shipping routes. IBT has a stockyardcapacity of 800,000 MT and is capablereceiving 80,000 DWT vessels. IBT isexpanding its storage capacity to 1.6million MT, with a capacity to handle200,000 DWT vessels.

(2) Tanjung Bara Coal Terminal(TBCT), a 500,000 MT capacitystockpile, was developed by KPC toload its own coal production into shipsof up to 200,000 DWT. TBCT islocated in north Samarinda, EastKalimantan and has been operationalsince 1991.

(3) PT. Dermaga Prakasa Pratama(DPP), an independent company,developed a deep-water coal terminallocated at Balikpapan, East Kalimantan.The facility provides services to coalmining companies operating along theMahakam River, such as MultiHarapan Utama, Tanito Harum,Kitadin, Bukit Baiduri and Fajar BumiSakti. The terminal jetty is capable ofhandling 80,000 DWT bulk carriers.

(4) Terminal Batubara Indah (TBI) inCirebon, West Java, has a stockpilecapacity of 50,000 MT and a handlingcapacity of one million MT/year. TBIhandles mostly coal requirements of theCibinong cement plant and othernearby industries, and receives regulardeliveries from Adaro, Arutmin andother coal mines in Kalimantan.

TT RANSPORTATION AND RANSPORTATION AND CC O A L O A L TT ERMINALERMINAL SS

9

Coal Sector Report Indonesia 2000American Embassy Jakarta

The autonomy laws

Autonomy laws passed in 1999, lawNo. 22 on political autonomy and lawNo. 25 on fiscal decentralization,created uncertainty and brought newrequirements to bear on mineralresources investment policy. Thedecentralization policy clearly givesprovincial and local governments moreopportunity to manage mineralresources directly. To implement lawNo. 22, the Government recentlyissued Government Regulation No. 25of 2000, which, inter alia, states thatexisting contracts, including CoalContracts of Work, would be continueduntil the end of the agreement’seffective period. The format will berevamped and classification of mineralresources will be reformulated for newcontracts.

The existing contracts

Presidential Decree No. 75 ofSeptember 1996 changed contractarrangements from Coal CooperationContracts (CCC) where the statereceived 13.5 percent of productionvalue to royalty-based Coal Contractsof Work (CCOW). The CCOW modelhas been widely used for other mineralssuch gold, copper, nickel and granite.The new scheme applies to bothexisting and new contractors. Existingcontractors are obliged to amend theircontracts based on CCOW. CCOWallows contractors to proceed withexploitation programs during theexploration period.

Application process

A contractor must submit an applicationto the Minister of Energy and MineralResources through the DirectorGeneral of Mines along with thefollowing documents:

1) a topographic map to a 1:250,000scale;

2) an MOU for a joint venturebetween a foreign and nationalparty (not necessary if thecontractor is not a joint venture);

3) a company profile on management,production and marketingcapability, with a financial statementdemonstrating that the companyholds net assets of no less than twobillion rupiah;

4) a summary of the company'sexperience in mining activities;

5) a work plan and budgetingprogram, including a briefdescription of the area being appliedfor, a work plan for each stage ofactivities, and an investmentprogram; and

6) an employment agreement withmining experts or statement ofintent by mining experts to carryout the project.

Contractor's obligations are:

1) not to mine other minerals withoutthe Government’s approval;

2) to be fully responsible for all risksof all activities;

CC ONTRACTS AND ONTRACTS AND II NVESTMENTNVESTMENT

10

Coal Sector Report Indonesia 2000American Embassy Jakarta

3) to complete general survey,exploration, feasibility study,construction and exploitationprograms; and

4) to relinquish 25% of the initialcontract area within the first year ofgeneral survey, 50% of the initialcontract area within three years and75-80% of the initial contract areaon or before the end of theexploration period. When the initialcontract area is less than 100,000Ha, the contractor is entitled toretain 20,000 or 25,000 Ha.

Other terms and conditions of theCCOW include:

1) to commence the general survey nolater than six months after thesigning of the contract;

2) to spend at least US $2.50/Ha onthe coal field by the end of thegeneral survey period;

3) to commence exploration uponcompletion of the general survey;

4) to spend at least US$15.00/Ha onexploration;

5) to commence exploitation no laterthan eight years fromcommencement of the generalsurvey;

6) to deliver 13.5% of the productionshare in cash based on FOB priceto the Government; and

7) to pay taxes and other fees to theGovernment.

The new scheme also transferredadministrative management of coalcontractors to the Directorate General

of Mines from PTBA, with the mainobjective of avoiding potential conflictsof interest in marketing coal productionbetween PTBA and its contractors andto enable PTBA to better focus ondevelopment of its own operations.

New draft for fourth generationCCOW

The Government is drafting the fourthgeneration CCOW, which is aimed atfacilitating coal-mining investment andimplementing requirements of new lawsfor local government autonomy. Thedraft CCOW includes the adoption ofad valorem royalty rates denominatedin U.S. dollars and community andregional development requirements.New provisions will empower regionalgovernments, providing them withsubstantial input to mining companies’community development plans and alarger share of royalties and taxes. Thenew royalty scheme will require miningcontractors to provide the Governmentabout five percent of the sales ofmineral production, up from less thantwo percent at present. Miningcontractors have asked that theGovernment also address compensationdisputes with illegal miners.

A difficult to realize divestmentobligation

CCOW terms require that domesticentities must eventually have majorityownership of mining projects. Duringthe first ten years of production,foreign shareholders must transfershares according to a fixed timetable sothat 51% of a mining project iseventually held by Indonesiancompanies (state-owned companies,private companies and local investors).

11

Coal Sector Report Indonesia 2000American Embassy Jakarta

This requirement applies as well to coalproducers operating under the firstgeneration CCOW, such as KPC,Arutmin, BHP Kendilo and KidecoJaya Agung. The CCOW establishes aformula in which the price of sharesoffered to local partners is based on thetotal expenditures from the generalstudies to production stages lessdepreciation, amortization, andliabilities. However, local investorshave not been responsive to miningcompany sales offers since they do notconsider the resultant price to becommercially attractive.

In 1999, for example, KPC offered a30-percent share in the company at thegovernment’s agreed price of US $175million. State mining companies --PTBA for coal, PT Aneka Tambangfor miscellaneous mining and PT Timahfor tin -- objected to the high price ofKPC shares. KPC, for its part, hadrejected PT Timah’s initial offer toacquire a 25-percent share for US $121million. According to its contract,KPC would be required to divestanother 7 percent in 2000. In anothercase, PT Arutmin Indonesia wasobliged to divest 31 percent of itsshares. In 1999, Arutmin offered 24percent of its stock, valued at US$40million, to local investors withoutsuccess. Kideco Jaya Agung isrequired eventually to divest 30 percentof its shares. In 1999, Kideco was tohave sold 23 percent, but received noresponse from buyers.

New incentives planned

To encourage the development of low-quality coal in remote areas, the GOIplans to introduce new incentives, toinclude lower royalties which will vary

depending on the quality of coaldeposits and remoteness of the area.

Contracts signed

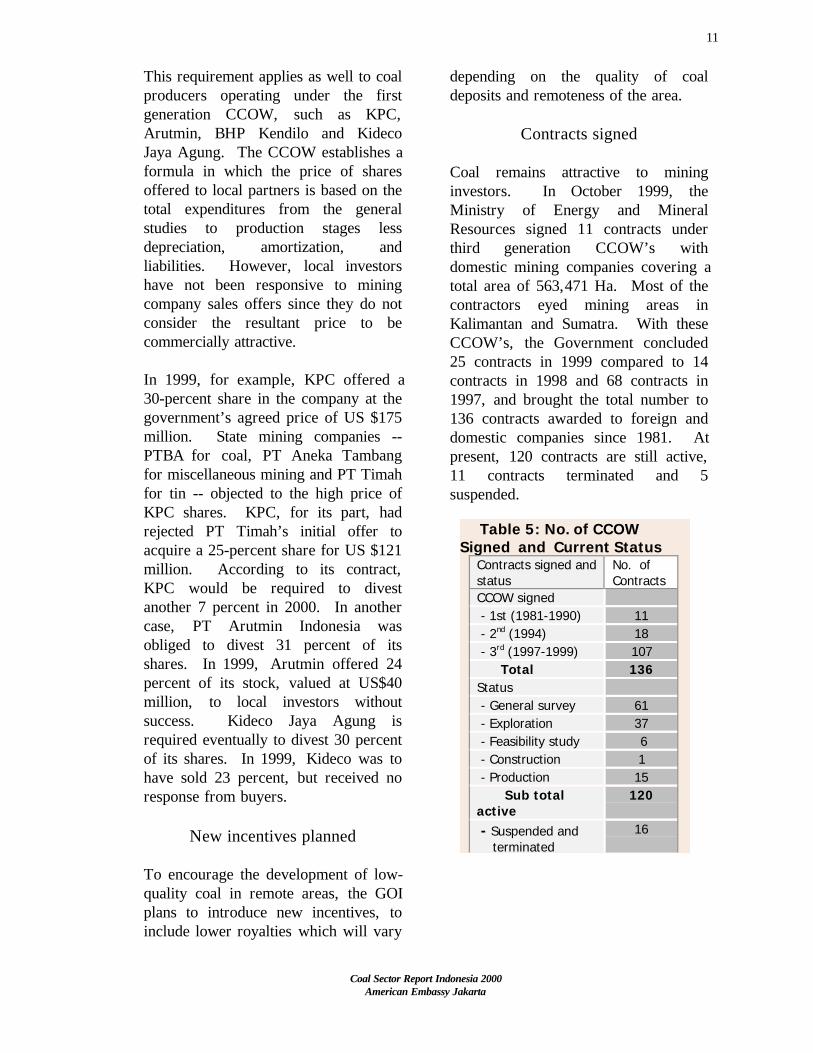

Coal remains attractive to mininginvestors. In October 1999, theMinistry of Energy and MineralResources signed 11 contracts underthird generation CCOW’s withdomestic mining companies covering atotal area of 563,471 Ha. Most of thecontractors eyed mining areas inKalimantan and Sumatra. With theseCCOW’s, the Government concluded25 contracts in 1999 compared to 14contracts in 1998 and 68 contracts in1997, and brought the total number to136 contracts awarded to foreign anddomestic companies since 1981. Atpresent, 120 contracts are still active,11 contracts terminated and 5suspended.

Table 5: No. of CCOWSigned and Current Status

Contracts signed andstatus

No. ofContracts

CCOW signed - 1st (1981-1990) 11 - 2nd (1994) 18 - 3rd (1997-1999) 107 Total 136Status - General survey 61 - Exploration 37 - Feasibility study 6 - Construction 1 - Production 15 Sub totalactive

120

- Suspended and terminated

16

12

Coal Sector Report Indonesia 2000American Embassy Jakarta

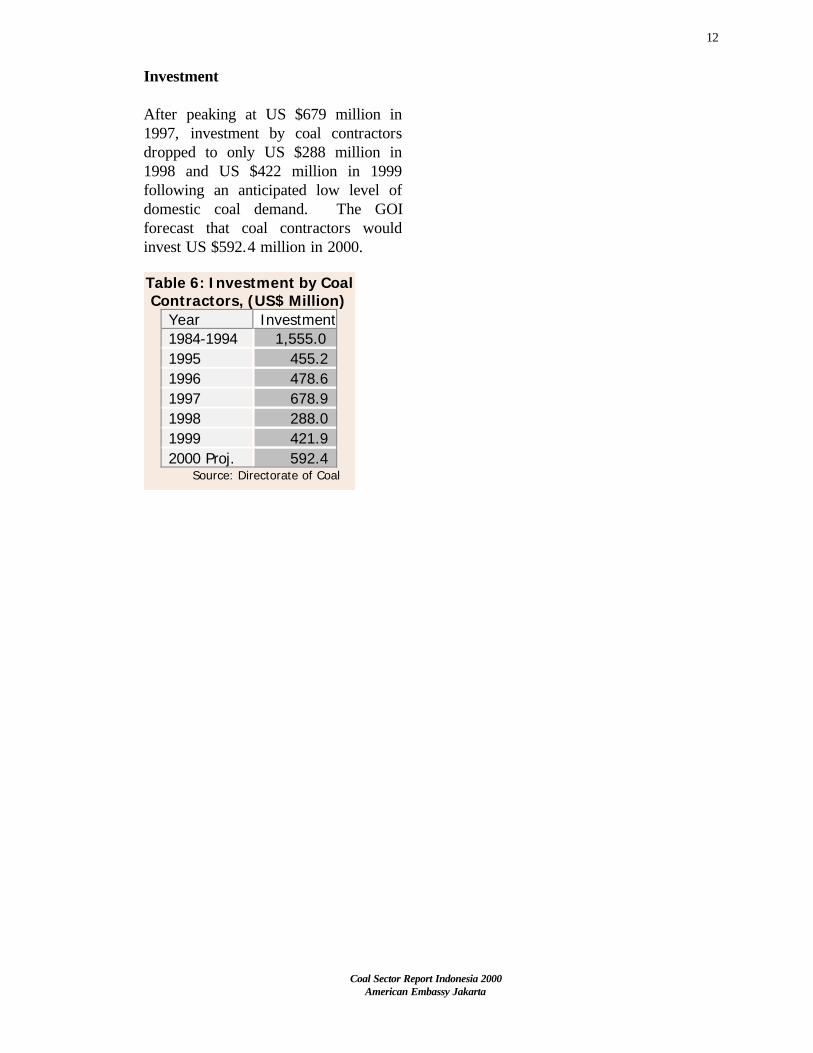

Investment

After peaking at US $679 million in1997, investment by coal contractorsdropped to only US $288 million in1998 and US $422 million in 1999following an anticipated low level ofdomestic coal demand. The GOIforecast that coal contractors wouldinvest US $592.4 million in 2000.

Table 6: Investment by CoalContractors, (US$ Million)

Year Investment1984-1994 1,555.01995 455.21996 478.61997 678.91998 288.01999 421.92000 Proj. 592.4

Source: Directorate of Coal

13

Coal Sector Report Indonesia 2000American Embassy Jakarta

PT Tambang Batubara Bukit Asam

State-owned coal company, PTTambang Batubara Bukit Asam(PTBA), is the third largest coalproducer in Indonesia, producing 11.2million MT of coal in 1999 from twomines, Tanjung Enim in South Sumatraand Ombilin in West Sumatra.Production is expected to reach 13.5million MT/year in 2000, 12.5 millionMT from Tanjung Enim and 1.0million MT from Ombilin. Under itsexpansion programs, PTBA started thedevelopment of two new mines, BankoBarat with a production capacity of 5.4million MT per year and Muara Tigawith a production capacity of 5.9million MT per year.

PTBA sells coal mostly in the domesticmarket to PT Pembangkit Listrik JawaBali (PJB-I), a PLN subsidiary. PJB-Isigned a contract to purchase 20.42million MT of coal from PTBAbetween the years 1997-2002 worth US$85 million. In 1999, PTBA shipped7.1 million MT of coal to PJB-I tosupply Suralaya steamdriven powerplants and 2.4 million MT to exportmarkets.

PTBA operates four coal terminals(Teluk Bayur in West Sumatra,Kertapati, Tarahan and Pulau Baai inSouth Sumatra). The completion of theTarahan Coal port expansion in 1999increased its delivery capacity to 12million MT per year.

PTBA has coal reserves of 6.6 billionMT of which 83 percent (5.5 billion

MT) is located in the Tanjung Enimarea and 3.0 percent (0.28 billion MT)in the Ombilin area. The TanjungEnim area has a large reserve ofsurface mineable sub-bituminous andlignite suitable for use in powerstations.

PTBA contributed Rp 439.9 billion(approximately US $55.3 million) in1999 and Rp 241.4 billion(approximately US $23.1 million) in1998 from income taxes, royalties anddividends to central governmentrevenue. To enhance the efficiency ofstate-owned enterprises, theGovernment is still carrying outpreparations to offer limited sales ofequity in PTBA. The sale, originallyplanned for June 2000, was postponed.

PT Kaltim Prima Coal – Thelargest coal producer

PT Kaltim Prima Coal (KPC), jointlyowned by the Rio Tinto group ofAustralia (50%) and British Petroleumof UK (50%), is the largest coaloperator in Indonesia. Commencingcommercial production in 1991, KPCsteadily increased coal production tonearly 15 million MT in 1999 aferinvesting about one billion US dollars.At the current production rate, thecompany’s marketable coal reserves of650 million MT can sustain mining formore than 20 years. Its high qualitycoal, extensive exploration, and heavyinvestment in infrastructure were thekey factors in its success.

CC URRENTURRENT PP RODUCERSRODUCERS

14

Coal Sector Report Indonesia 2000American Embassy Jakarta

Production is currently exportedthrough the Tanjung Bara CoalTerminal (TBCT), a deep-waterload-out facility which is capable ofhandling cape-size vessels of 200,000dead weight ton (DWT) capacity. In1999, KPC exported 13.9 million MTof coal to destinations in Europe, theU.S., Japan and other Asian countries.KPC produces two brands of coal –“Prima Coal” and “Pinang Coal.”Prima Coal is a high quality,internationally traded coal,predominantly sold on the basis oflong- term contracts. While targeted toreach a production level of 15 millionMT in 2000, KPC operations andproduction were affected for the firsttime in its history by labor actions.The company was shut downintermittently in the third quarter of theyear, losing some 1.8 million MT ofproduction, and had to declare forcemajeure to all its customers beforestarting back up on August 18.

PT Adaro Indonesia – the “BestCoal Company in 1999”

PT Adaro, a joint venture betweenNew Hope Corporation of Australia(50%), PT Asminco Bara Utama ofIndonesia (40%) and Mission Energy ofthe U.S. (10%), is the second largestcoal producer in Indonesia. Productionincreased rapidly to 13.6 million MT in1999 from its production start-up in1991. However, Adaro’s ambitiousplan to increase coal production to 20million MT by 2000 may not beattained due to a delay in full operationof Paiton Swasta I. The companyentered into a US $5.5 billion 30-year

coal supply agreement with PaitonEnergy to supply 4.3 million MT/year.

Adaro has a coal reserve of two billionMT in its contract area covering theTabalong and Hulusungai Utararegencies. Due to its 0.1 percent sulfurcontent and excellent combustioncharacteristics, as well as being wellsuited for use in power plants, thecompany has trademarked its coal“envirocoal.” Due to Adaro’soperational efficiency, innovation inmarketing and its commitment to theenvironment and the surroundingpopulation, the company wasrecognized as Best Coal Company 1999by the Financial Times Energy Awardsin New York.

Adaro hopes to increase exports tomarkets in Asia, Europe and the U.S.by using Indonesia Bulk Terminalfacilities at South Pulau Laut. Adaroexported 10 million MT in 1999 ornearly 75 percent of its output.

PT Berau Coal

PT Berau Coal, a joint venture betweenUnited Tractors (60%), PT PanduaDian Pertiwi (20%) and Nissho Iwai(20%), operates coal mines locatedaround Latek River (about 600 kmnorth of Samarinda), East Kalimantan.Berau Coal reported measured reservesof 745 million MT from its fivepotential fields. Production rosesharply from 300,000 MT in 1994 to2.3 million MT in 1998 and 3.3 millionMT in 1999. Berau Coal plans toexpand its mining capacity to 8.0million MT/year in 2000. Thecompany has been contracted to supply

15

Coal Sector Report Indonesia 2000American Embassy Jakarta

4.5 million MT/year of coal by powercompanies. The contracts include a30–year deal with Daya Listrik Pratamavalued at US $1 billion for 1.1 millionMT/year; a deal with the developer ofa rescheduled 400 MW coal powerplant project at Cilegon; a 30–year dealwith Paiton II worth US $1.5 billion tosupply two million MT/year; and a 5–year deal with Paiton I valued at US$300 million.

PT Arutmin Indonesia

PT Arutmin Indonesia, a joint venturebetween BHP Minerals of Australia(80%) and Bakrie Brothers (20%),operates two open-cut coal mines and acoal loading facility located in SouthKalimantan. The two mines areSenakin mine with a capacity of fourmillion MT/year and Sentui mine witha capacity of two million MT/year.Commencing trial production in 1988,Arutmin increased production to 6.3million MT in 1998 and 8.7 million MTin 1999 and targeted production of 12million MT/year of bituminous coal inthe near future from its seven separateprojects. Arutmin exported 7.1 millionMT in 1999 through its deep-water coaltransshipment point at North PulauLaut. The port is designed toaccommodate Panamax size vesselswith a stockyard capacity of 500,000MT.

Japanese buyers postponed transactionsto purchase 700,000 MT of coal fromArutmin due to fears of supplyinterruptions following deteriorating tiesbetween Australia and Indonesia.Officials said the postponement wouldnot only affect PT Arutmin, but also

coulld diminish Indonesia’s foreignexchange earnings, as the Japanesebuyers may switch to coal contractswith other countries.

PT Kideco Jaya Agung

PT Kideco Jaya Agung, owned bySamtan Co. Ltd of South Korea,produced 7.3 million MT of coal in1999 up from 5.5 million MT in 1998.Commencing commercial production in1993 at a production rate of 1.2 millionmetric tons, the company continued anexpansion project to increaseproduction capacity to over 10 millionMT by 2000 from its total measuredand indicated reserves of one billionMT located in Pasir, East Kalimantan.In 1999, Kideco exported 6.4 millionMT, mostly shipped to South Korea.Kideco operates a US $140 millionTanah Merah transshipment terminal,with an 8.5 million MT per year bargeloading capacity for transhipment up tocape size 149,000 DWT ships.

PT Allied Indo Coal (AIC)

PT Allied Indo Coal (AIC), a jointventure between the Thohir family ofIndonesia (50%) and the Salway family(50%), commenced commercialproduction in 1987 from theParambahan deposit in West Sumatra,adjacent to PTBA’s Ombilin. In 1999,AIC produced 426,000 MT, downfrom 1.7 million MT in 1998. All ofthe company’s production was forexport. Its relatively high quality coalcan be processed into three differentproducts: steam coal with heat value(HV) of 6,900 Kcal/kg; Pulverized

16

Coal Sector Report Indonesia 2000American Embassy Jakarta

Coal Injection (PCI) with HV of 7,200kcal/kg; and lump coal for householduse with a 50-mm sized product.

PT Multi Harapan Utama

PT Multi Harapan Utama (MHU), ajoint venture between New HopeGroup Pty. Ltd. of Australia (40%) andIndonesian companies PT AsmincoBara Utama (10%) and the Risjadgroup (40%), started production in1988 from the Busang deposit in EastKalimantan. MHU estimated potentialreserves at 126 million MT. In 1999,MHU produced 1.6 million MT orslightly more than the year beforeprimarily to satisfy increased demand.The company’s current equipment iscapable of handling annual productionof up to three million MT/year.

PT Tanito Harum

PT Tanito Harum, a domesticcompany, changed its status fromprivate mining to coal contractor in1987. It obtained a portion of thecontract area relinquished by AGIP -Carbone on the Mahakam River nearSamarinda. In 1999, the companyproduced one million MT and hasaggressively marketed all of itsproduction to South America.

PT BHP Kendilo Coal Indonesia

PT BHP Kendilo Coal Indonesia, ajoint venture between BHP (80%) andMitsui (20%), operates two open-cutcoal mines at Petangis and Rindudeposits in East Kalimantan, an areareleased by PT Utah Indonesia. BHPKendilo commenced production in 1995

and produced one million MT/year in1999.

PT Indominco Mandiri

PT Indominco Mandiri, a domesticmining company owned by the Salimgroup, signed a first generation CCOWin 1990 to develop coal resources inBlock III at Bontang, East Kalimantan.Indominco commenced commercialproduction in 1997 at 1.2 million MTand increased its output to 2.0 millionMT in 1998 and 3.0 million in 1999.The company is constructing allfacilities to support full productioncapacity of 3.5 million MT/year by2000.

New producers

Five contractors in Kalimantan (PTBahari Cakrawala Sebuku, PT AntangGunung Meratus, PT Bentala CoalMining, PT Jorong Barutama Grestonand PT Gunung Bayan Pratama)operating under second generationCCOW signed in 1994 enteredcommercial production in 1998 and1999, with initial production rangingfrom 150,000 MT to 1.2 millionMT/year. PT Bahari CakrawalaSebuku (BCS), a joint venture betweenStrait Sebuku Pte Ltd. (80%) and PT.Rekya Wahana Digdjaya (20%), is thefirst of the 18 coal contracts under thesecond generation signed in 1994 tostart commercial operation (in May1998).

PT Bentala Coal Mining, a nationalmining company, has an initial target ofproducing three million MT of coal peryear to supply coal power plants.

17

Coal Sector Report Indonesia 2000American Embassy Jakarta

PT Gunung Bayan Pratama (GBP)started commercial production in July1999, reached production for the yearat one million MT, and exported 836thousand MT to Japan, Europe andMalaysia.

Other producers

The Government permits privatenational companies and cooperatives tomine coal under a Kuasa Pertambangan(KP) or Mining Authorization. Nineprivate companies and 12 cooperativescurrently produce coal, with acombined output rising from 1.3 millionMT in 1993 to 4.8 million MT in 1999.Their domestic sales reached 700,000MT and exports totaled 4.4 million MTin 1999. Coal production by KPholders is expected to increase to over5 million MT in 2000.

Three firms produced significantamounts of coal; PT. Bukit Baiduri -1.7 million MT; PT. Kitadin - 0.9million MT; and PT. Bukit Sanur - 0.7million MT. PT Bukit Baiduri, whichmines coal resources in Kutai District,East Kalimantan, doubled coal output inthe last three years from 0.8 millionMT in 1995 to 1.7 million MT in 1999and exported all of its production,mostly to Taiwan. The companyexpected to produce over three millionMT in 2000 and signed a contractvalued at US $61 million with PT.Petrosea, a subsidiary of CloughEngineering and Construction ofAustralia, to transport five million MTof steaming coal. Baiduri has identifiedcoal reserves of 40 million MT.

CC ONTRACTORSONTRACTORSOther second generation coalcontractors targeting production in2000 include PT Kartika SelabumiMining, PT Mandiri Inti Perkasa andPT Nusa Mineral Utama.

Illegal mines

Illegal mining increased over the pastthree years, causing numerousproblems for the industry. Illegalminers mined over three million MT ofcoal in 1999, according to informedestimates. Illegal miners ignoreenvironmental and safety guidelines andmarket their coal at lower prices. Thecoal industry requested the Governmentto take legal action and regulate thisactivity. Proposed measures includerequiring end users to stop buying coalfrom anyone without coal miningtransportation and marketing licenses.