Embed Size (px)

Citation preview

101

Chapter 6

Analysis and Discussion

6.1 Current Ratio

Current Ratio is a general and quick measure of liquidity of a firm. It represents the

margin of safety or cushion available to the creditors. It is an index of the firm’s financial

stability. It is also an index of technical solvency and an index of the strength of working

capital. A ratio equal to or near 2: 1 is considered as a standard or normal or satisfactory.

The idea of having doubled the current assets as compared to current liabilities is to

provide for the delays and losses in the realization of current assets.

Current Ratio = Current Assets / Current Liabilities

6.1.1 Current ratio of individual companies

(Rs in crores)

Table 1: Current Ratio of ITC

Year Current Assets Current Liabilities Ratio

2011-12 14444 9102 1.59

2010-11 13046 8477 1.54

2009-10 12497 8048 1.55

2008-09 10105 4704 2.15

2007-08 9108 4432 2.06

2006-07 8522 3858 2.21

2005-06 7894 3578 2.21

2004-05 6628 3034 2.18

2003-04 5382 3533 1.52

2002-03 4162 2720 1.53

Grand Average 1.85

102

As the table value of various years’ of ITC shows that the Current Ratio of almost all the

years is by and large near to the standard or the ideal value i.e. 2:1. The Current Ratio of

ITC in the first two years from 2002-2003 to 2003-2004 is below standard but still it is

quite comfortable as it is close to generally accepted norm of 1.33:1 so we can say that

ITC is performing well by maintaining proper current assets to meet its current liabilities.

As we move ahead, from 2004-2005 till 2008-2009, ITC sees an increase in current ratio

which is more than the ideal value of 2:1. It shows that the company was keeping a

conservative policy of working capital by keeping excess of current assets than the

required norms. In the later years, the company tried to maintain an ideal current ratio.

103

(Rs in crores)

Table 2: Current Ratio of HUL

Year Current Assets Current Liabilities Ratio

2011-12 7799 6449 1.21

2010-11 6074 6620 0.92

2009-10 5368 6733 0.80

2008-09 5601 5784 0.97

2007-08 3277 5111 0.64

2006-07 3170 4523 0.70

2005-06 2763 4118 0.67

2004-05 3305 3714 0.89

2003-04 3502 3871 0.90

2002-03 3431 3671 0.93

Grand Average 0.86

Table 2 shows value of current assets of various years’ of HUL. Current Ratio of almost

all the years is by and large lower than the standard or the ideal value i.e. 2:1. The

Current Ratio of HUL in the first three years from 2002-2003 to 2004-2005 is near to half

of the standard value 2:1 so we can say that HUL is keeping a very restrictive policy in

104

maintaining its current assets. As we move ahead, from 2005-2006 till 2007-2008, HUL

sees a further decline in current ratio which can be more harmful for the company if it

faces sudden payment of current liabilities or faces fall in sales. In the later years, the

company tried to increase its current ratio but still remain aggressive in maintaining low

current assets.

(Rs in crores)

Table 3: Current Ratio of Nestle

Year Current Assets Current Liabilities Ratio

2011-12 1407 2134 0.66

2010-11 1197 1670 0.72

2009-10 1060 1422 0.75

2008-09 833 1185 0.7

2007-08 732 958 0.76

2006-07 613 769 0.8

2005-06 567 685 0.83

2004-05 513 618 0.83

2003-04 438 492 0.89

2002-03 400 429 0.93

Grand Average 0.79

105

As the table value of various years’ of Nestle shows that the company believes in

managing the current assets at a lower level as compared to the current liabilities (Table

3). Current Ratio of almost all the years is much below the standard or the ideal value i.e.

2:1. The Current Ratio of Nestle in the first five years from 2002-2003 to 2006-2007 is

below standard and falls to0.80. As we move ahead, from 2007-2008 till 2011-2012,

Nestle sees a further decrease in current ratio which is much less than the ideal value of

2:1. It shows that the company went very aggressive and started keeping a more

restrictive policy of working capital by keeping current assets less than half of the current

liabilities.

(Rs in crores)

Table 4: Current Ratio of Dabur

Year Current Assets Current Liabilities Ratio

2011-12 1680 1078 1.56

2010-11 1396 925 1.51

2009-10 1158 872 1.33

2008-09 863 664 1.3

2007-08 756 583 1.3

2006-07 476 356 1.34

2005-06 325 307 1.06

2004-05 296 322 0.92

2003-04 334 236 1.42

2002-03 413 212 1.95

Grand Average 1.37

106

As the table value of various years’ of Dabur shows that the Current Ratio of almost all

the years is by and large more than 1 but not near to the standard value i.e. 2:1. The

Current Ratio of ITC in the first year 2002-2003 is touching the standard value but as we

move ahead in the later years, it starts falling till year 2005-2006 where it is the lowest of

all 10 years considered for analysis. From year 2006-2007, it remained almost stable at

around 1.3 till year 2009-2010. At 1.3 level of current ratio we can say that Dabur is

performing well by maintaining proper current assets to meet its current liabilities. In the

recent two years, Dabur sees an increase in current ratio which is more than the previous

year’s ratios but not touching the ideal value of 2:1. It can be interpret that Dabur has not

been very liberal or very strict in maintaining their current assets and in turn their current

ratio.

107

(Rs in crores)

Table 5: Current Ratio of Britannia

Year Current Assets Current Liabilities Ratio

2011-12 858 979 0.88

2010-11 704 456 1.54

2009-10 801 486 1.65

2008-09 836 413 2.02

2007-08 733 348 2.11

2006-07 571 323 1.77

2005-06 442 303 1.46

2004-05 392 303 1.29

2003-04 285 215 1.33

2002-03 276 191 1.45

Grand Average 1.55

In Table 5, it can be seen that the values of current ratio of Britannia do not follow any

consistent ratio and is changing every year from 2002-03 to 2011-12. It can also be seen

that out of 10 years of the period taken, Britannia has followed the standard value of 2:1

108

in only two years i.e. 2008-09 and 2007-08. And after that in the recent years, the current

ratio started falling from 1.65 in 2009-10 to 1.54 in 2010-11 and further fell to .88 in

2011-12. The Current Ratio of ITC in the most of the years is more than 1 which is again

not an ideal situation but still but it seems to be a comfortable one as all the current assets

are covering the current liabilities. The firm has neither followed a liberal working

management policy not a strict policy.

6.1.2 Comparison of Current Ratio among the Companies and with the Industry’s

Average

Table 6: Current Ratio of 5 companies and the industry Average

Year ITC HUL Nestle Dabur Britannia Industry

Average 2011-12 1.59 1.21 0.66 1.56 0.88 1.18

2010-11 1.54 0.92 0.72 1.51 1.54 1.25

2009-10 1.55 0.80 0.75 1.33 1.65 1.22

2008-09 2.15 0.97 0.70 1.30 2.02 1.43

2007-08 2.06 0.64 0.76 1.30 2.11 1.37

2006-07 2.21 0.70 0.80 1.34 1.77 1.36

2005-06 2.21 0.67 0.83 1.06 1.46 1.25

2004-05 2.18 0.89 0.83 0.92 1.29 1.22

2003-04 1.52 0.90 0.89 1.42 1.33 1.21

2002-03 1.53 0.93 0.93 1.95 1.45 1.36

Grand

Average 1.85 0.86 0.79 1.37 1.55 1.29

109

Year 2011-12

In year 2011-12, the average current ratio in the FMCG sectors comes out to be 1.18

which in itself is less than the ideal current ratio considered for manufacturing

companies. In the same year, the company having the least current ratio is Nestle with the

value of 0.66 which is less than half of the average ratio of the industry in that year. The

company with second lowest current ratio is Britannia with the value of .88 which is

again approximately half of the industry’s average. The company whose ratio is near and

above to the industry’s average are ITC with the value of 1.59, HUL with the value of

1.21 and Dabur with the value of 1.56. Refer Table 6.

110

2010-11

In year 2010-11, the average current ratio in the FMCG sectors comes out to be 1.25

which is slightly above the industry’s average in the previous year but it is again in itself

less than the ideal current ratio considered for manufacturing companies i.e.2:1. In this

year also, the company having the least current ratio is Nestle with the value of .72 which

is more than half of the average ratio of the industry in that year followed by HUL with

the value of .92. Rest of the three companies have a value of 1.5 and are above to the

industry’s average in this year. Refer Table 6.

2009-10

In year 2009-10, the average current ratio in the FMCG sectors comes out to be 1.22. In

the same year, the company which is following the trend of keeping the lowest current

ratio is Nestle with the value of .75 which is more than half of the average ratio of the

industry in that year. The company with second lowest current ratio is HUL with the

value of .80 which is again more than half of the industry’s average. The companies

whose ratio is above to the industry’s average are ITC with the value of 1.55, Britannia

with the value of 1.65 and Dabur with the value of 1.33. Refer Table 6.

2002-03 to 2008-09

In the past years from 2002-03 to 2008-09, the industry’s average has initially decreased

since 2002-03 from 1.36 till 2004-05 to 1.22 but then gradually started increasing till year

2008-09 with the value of 1.43. in all these 6 years , Nestle has maintained itself to be a

company with the most aggressive working capital policy with the minimum value of

current assets among all companies except for the period of 2005 to 2008 where HUL

111

took its place and kept the minimum current ratio. Moreover, the company that

maintained a reasonably higher and the best current ratio among all the companies is ITC.

Throughout the 10 years of time period, ITC always has a current ratio which is more

than the industry’s average current ratio. So, it can be said that among all the FMCG

companies, ITC has the most liberal working capital policy. Dabur and Britannia have

also maintained a ratio near or above to the industry’s average. HUL kept the second

lowest value of current ratio among all the companies after Nestle. Refer Table 6.

112

6.2 Quick Ratio

Quick ratio is also known as liquid ratio or acid test ratio. This ratio measures the

liquidity of a business by matching its cash and near cash current assets with its total

liabilities. It helps us to determine whether a business would be able to pay off all its

debts by using its most liquid assets (i.e. cash, marketable securities and accounts

receivable). Rule of thumb for acid test ratio is 1: 1 i.e., if business liquid assets are 100

percent of its current liabilities it is considered to be having fairly good current financial

position.

Quick ratio = Liquid (quick) assets / Current Liabilities

6.2.1 Quick ratio of individual companies

(Rs in crores)

Table 7 : Liquid Ratio of ITC

Year Liquid Assets Current Liabilities Ratio

2011-12 8806 9102 0.97

2010-11 7777 8477 0.92

2009-10 7948 8048 0.99

2008-09 5505 4704 1.17

2007-08 5057 4432 1.14

2006-07 5168 3858 1.34

2005-06 5258 3578 1.47

2004-05 4625 3034 1.52

2003-04 3848 3533 1.09

2002-03 2910 2720 1.07

Grand Average 1.17

113

In Table 7, it can be seen that the quick ratio of ITC for almost all the 10 years is more or

less near to the ideal ratio of 1.1. In the years 2002-2003 and 2003-2004, the ratio is

slightly above the ideal. But the ratio increases sharply to 1.52 in year 2004-2005 and

further to 1.47 in year 2005-2006 which shows that ITC has kept surplus of liquid assets

in these two years. The ratio slightly declines to 1.34 in year 2006-2007. In year 2007-

2008 and 2008-2009, the ratio was near to one but slightly greater than it. From 2009-

2010 to 2011-2012, the ratio stayed near to ideal ratio of 1:1. So it can be said that

overall, ITC has maintained a satisfactory liquid ratio in all the 10 years.

114

(Rs in crores)

Table 8 :Liquid Ratio of HUL

Year Liquid Assets Current Liabilities Ratio

2011-12 5282 6449 0.82

2010-11 3263 6620 0.49

2009-10 3188 6733 0.47

2008-09 3072 5784 0.53

2007-08 1323 5111 0.26

2006-07 1622 4523 0.36

2005-06 1441 4118 0.35

2004-05 1835 3714 0.49

2003-04 2109 3871 0.54

2002-03 2152 3671 0.59

Grand Average 0.49

As was seen in the current ratio, the same trend is followed in the liquid ratio too by

HUL. The company has been very aggressive in maintaining liquid assets too. Table 8,

shows the position of HUL in case of liquid ratio. It can be seen that the quick ratio of

115

ITC for almost all the 10 years is much less than the standard value of 1:1. In the years

2002-2003, 2003-2004 and 2004-2005, the ratio is approximately half of the ideal ratio.

In the later years, 2005-2006 to 2007-2008, the ratio fell down and touched a low of .26.

At this time period, the company was very tight with its working capital policy. But the

ratio increased to .53 in year 2008-2009 and than declined to .47 and .49 in the next two

financial years. In the recent year 2001-2012, the company saw a drastic change in the

liquid ratio. It sharply increased the ratio to .82 which is near to the standard ratio. So it

can be said that overall, HUL has maintained an aggressive working capital by keeping

liquid assets at its low in all the 10 years.

(Rs in crores)

Table 9: Liquid Ratio of Nestle

Year Liquid Assets Current Liabilities Ratio

2011-12 673 2134 0.32

2010-11 621 1670 0.37

2009-10 561 1422 0.39

2008-09 398 1185 0.34

2007-08 331 958 0.35

2006-07 337 769 0.44

2005-06 314 685 0.46

2004-05 296 618 0.48

2003-04 219 492 0.45

2002-03 181 429 0.42

Grand Average 0.40

116

Table 9 shows that the liquid ratio maintained by Nestle is less than half of the ideal

value of 1:1. It significantly throws light on the strict working capital policy of the

company in which the company believes in maintain low level of liquid assets other than

inventory. The same trend was seen in the current ratio. The company has been very

aggressive in maintaining liquid assets too. It can be seen that the quick ratio of Nestle

for almost all the 10 years is much less than the standard value of 1:1. From 2002-2003 to

2006-2007, the ratio varies between .42 and .48 and is approximately half of the ideal

ratio. In the later years, 2007-2008 to 2011-2012, the ratio fell down further and ranged

between .32 and .39. At all these 10 years, the company was very tight with its working

capital policy. Less of all liquid assets have been maintained by Nestle. So it can be said

that overall, Nestle has maintained an aggressive working capital and has focused on Just

in time management.

117

(Rs in crores)

Table 10: Liquid Ratio of Dabur

Year Liquid Assets Current Liabilities Ratio

2011-12 1151 1078 1.07

2010-11 935 925 1.01

2009-10 860 872 0.99

2008-09 601 664 0.91

2007-08 555 583 0.95

2006-07 319 356 0.90

2005-06 209 307 0.68

2004-05 168 322 0.52

2003-04 223 236 0.94

2002-03 234 212 1.10

Grand Average 0.91

In Table 10, it can be seen that the quick ratio of Dabur for almost all the years is more or

less near to the ideal ratio of 1.1 except for year 2004-2005 in which the ratio fell to half

of the standard value 1:1. In the year 2002-2003, the ratio is slightly above the ideal. But

the ratio decreases to .94 in year 2003-2004 and further to .52 in year 2004-2005 which

118

shows that Dabur has been tight in keeping its liquid assets in this year. The ratio slightly

increased to .68 in year 2005-2006. From year 2006-2007 to 2009-2010, the ratio varied

between .91 and .99. In years 2010-2011 and 2011-2012, the ratio was near to one but

slightly greater than it. In these two years, the ratio stayed near to ideal ratio of 1:1. So it

can be said that overall, Dabur has maintained a acceptable liquid ratio in all the 10 years.

(Rs in crores)

Table 11:Liquid Ratio of Britannia

Year Liquid Assets Current Liabilities Ratio

2011-12 476 979 0.49

2010-11 393 456 0.86

2009-10 533 486 1.10

2008-09 582 413 1.41

2007-08 431 348 1.24

2006-07 356 323 1.10

2005-06 257 303 0.85

2004-05 258 303 0.85

2003-04 163 215 0.76

2002-03 194 191 1.02

Grand Average 0.97

119

Table 10 shows the quick ratio of Britannia for 10 years. In the year 2002-2003, the ratio

is slightly above the ideal .i.e. 1.02. But the ratio declines in the next few years from the

period of 2003-2004 to 2005-2006. The ratio slightly increased to 1.1 in year 2006-2007

and further increased to 1.24 in the next year. In year 2008-2009 the ratio further

increased to 1.41. In year 2009-2010, the company decreased the ratio to 1.10 which is

quite near to the ideal ratio. The ratio further declined to .86 in the year 2010-2011 and

.49 in the year 2011-2012. The liquid ratio of Britania shows that the company didn’t

follow any specific kind of working capital policy throughout the time considered in the

study.

120

6.2.2 Comparison of Liquid Ratio among the Companies and with the Industry’s

Average

Table 12: Liquid Ratio of 5 companies and the industry Average

Year ITC HUL Nestle Dabur Britannia Industry

Average

2011-12 0.97 0.82 0.32 1.07 0.49 0.73

2010-11 0.92 0.49 0.37 1.01 0.86 0.73

2009-10 0.99 0.47 0.39 0.99 1.10 0.79

2008-09 1.17 0.53 0.34 0.91 1.41 0.87

2007-08 1.14 0.26 0.35 0.95 1.24 0.79

2006-07 1.34 0.36 0.44 0.90 1.10 0.83

2005-06 1.47 0.35 0.46 0.68 0.85 0.76

2004-05 1.52 0.49 0.48 0.52 0.85 0.77

2003-04 1.09 0.54 0.45 0.94 0.76 0.76

2002-03 1.07 0.59 0.42 1.10 1.02 0.84

Grand

Average 1.17 0.49 0.40 0.91 0.97 0.79

121

Year 2011-12

In year 2011-12, the average quick ratio in the FMCG sectors comes out to be .734 which

is again less than the ideal quick ratio considered for manufacturing companies. In the

same year, the company having the least quick ratio is Nestle with the value of .32 which

is less than half of the average ratio of the industry in that year. The company with

second lowest quick ratio is Britannia with the value of .49 which is again approximately

half of the industry’s average. The company whose ratio is near and above to the

industry’s average are ITC with the value of .97 which is exactly the perfect quick ratio

showing neither excess nor deficit of liquid assets, HUL with the value of .82 and Dabur

with the value of 1.07 which is slightly more than the ideal value. Refer Table 12.

2010-11

In year 2010-11, the average quick ratio in the FMCG sectors comes out to be .730 which

is almost same with the industry’s average in the previous year but it is again in itself less

than the ideal quick ratio considered for manufacturing companies i.e.1:1. In this year

also, the company having the least quick ratio is Nestle with the value of .37 which is

almost equal to half of the average ratio of the industry in that year followed by HUL

with the value of .49. Rest of the three companies i.e. ITC, Dabur and Britannia have

values of .92, 1.01 and .86 respectively. Refer Table 12.

2009-10

In year 2009-10, the average quick ratio in the FMCG sectors comes out to be .788. In the

same year, the company which is following the trend of keeping the lowest quick ratio is

122

Nestle with the value of .39 which is equal to half of the average ratio of the industry in

that year. The company with second lowest quick ratio is again HUL with the value of

.47 which is more than half of the industry’s average. The companies whose ratio is

equivalent to the ideal ratio are ITC and Dabur with the same value of .99 which is near

to the ideal and Britannia with the value of 1.3023. Refer Table 12.

2002-03 to 2008-09

In the past years from 2002-03 to 2008-09, the industry’s average has initially decreased

since 2002-03 from .840 till 2005-06 to .762 but then gradually started increasing till year

2008-09 with the value of .872. In all these 6 years, Nestle has maintained itself to be a

company with the most aggressive working capital policy with the minimum value of

quick assets among all companies except for the period of 2005 to 2008 where HUL took

its place and kept the minimum quick ratio. The company that maintained ratio higher

than the ideal ratio in many years and the best quick ratio among all the companies is

ITC. Throughout the 10 years of time period, ITC always has a quick ratio which is more

than the industry’s average quick ratio. So, it can be said that among all the FMCG

companies, ITC has the most liberal working capital policy. Dabur and Britannia have

also maintained a ratio near or above to the industry’s average. HUL also followed an

aggressive working capital policy after Nestle and kept the second lowest value of quick

ratio. Refer Table 12.

123

6.3 Cash Ratio

Cash ratio is the ratio of cash and cash equivalents of a company to its current liabilities.

It is an extreme liquidity ratio since only cash and cash equivalents are compared with the

current liabilities. It measures the ability of a business to repay its current liabilities by

only using its cash and cash equivalents and nothing else. Since cashity ratio lays down

very strict and exacting standard of liquidity, therefore, acceptable norm of this ratio is 50

percent. It means cash assets worth one half of the value of current liabilities are

sufficient for satisfactory liquid position of a business.

Cash ratio = Absolute liquid assets / Current liabilities

6.3.1 Cash Ratio of Individual Companies

(Rs in crores)

Table 13:Cash Ratio of ITC

Year Absolute liquid assets Current Liabilities Ratio

2011-12 7182 9102 0.79

2010-11 6234 8477 0.74

2009-10 5496 8048 0.68

2008-09 2976 4704 0.63

2007-08 2659 4432 0.60

2006-07 3132 3858 0.81

2005-06 3588 3578 1.00

2004-05 3145 3034 1.04

2003-04 1931 3533 0.55

2002-03 1052 2720 0.39

Grand Average 0.72

124

Table 13 shows the value of cash ratio of ITC for a period of 10 years. The values of the

ratio of ITC are at a higher side of the standard value of .5:1. In the year 2002-2003, the

ratio is .39 which is less than the ideal value. In the next year the ratio increased and

reached to the ideal value of .5. Years 2004-2005 and 2005-2006 saw a drastic increase in

this ratio by keeping double the cash and cash equivalent assets and touched 1.04 and 1

respectively. In year 2006-2007 the value dropped to .81 but is still more than .5. The

values of the cash ratio in the next three years 2007-2008 to 2009-2010 varied between 6

and 68. The ratio increased in the next two years and reached to .79 in 2011-2012. On

seeing all the three ratios i.e. current ratio, liquid ratio and cash ratio of ITC for last 10

years , it can be said that the company ITC believe in keeping a very liberal working

capital policy by keeping excess of current assets.

125

(Rs in crores)

Table 14:Cash Ratio of HUL

Year Absolute liquid assets Current Liabilities Ratio

2011-12 4082 6449 0.63

2010-11 2768 6620 0.42

2009-10 1892 6733 0.28

2008-09 1777 5784 0.31

2007-08 201 5111 0.04

2006-07 417 4523 0.09

2005-06 355 4118 0.09

2004-05 698 3714 0.19

2003-04 806 3871 0.21

2002-03 943 3671 0.26

Grand Average 0.25

The values of cash ratio of HUL for last 10 years are very low than the standard value of

.5. Table 14 shows that in years 2002-2003 and 2003-2004 the ratio ranged in .2s which

126

is less than half of the ideal value. As we move further in the years 2004-2005 to 2007-

2008, the value further declined to the least of .04 which indicates that the company

maintained a very low value of cash and cash equivalent assets. In year 2008-2009, the

ratio increased drastically and reached .31 which is still lower than the standard value.

The value fell again to .28 in the next year. The company improved its ratio in the year

2010 -2011. It is only in year 2011-2012 that the ratio was found more than the standard

value. This shows that the company has been very strict in maintaining levels of all kinds

of current assets as was seen with current ratio and liquid ratio too.

(Rs in crores)

Table 15:Cash Ratio of Nestle

Year Absolute liquid assets Current Liabilities Ratio

2011-12 361 2134 0.17

2010-11 406 1670 0.24

2009-10 359 1422 0.25

2008-09 229 1185 0.19

2007-08 132 958 0.14

2006-07 154 769 0.20

2005-06 141 685 0.21

2004-05 164 618 0.27

2003-04 80 492 0.16

2002-03 39 429 0.09

Grand Average 0.19

127

The values of cash ratio in the above table show that Nestle has maintained very less cash

and cash equivalent assets in all last 10 years. The year 2002-2003 shows the lowest

value of this ratio at .09. In year 2003-2004 the ratio increased to .16 which further

increased to .27 in the next year. In years 2005-2006 and 2006-2007 the values were

almost the same at .20 which again is less than the ideal ratio. In 2007-2008, the ratio

further fell to .14. In the next years, the ratio rose slowly from .19 in 2008-2009 to .25 in

2009-2010 and further declined by .01 and reached .24 in year 2010-2011. The ratio fell

again in the last year to .17. Nestle also maintained a very tight working capital policy.

128

(Rs in crores)

Table 16: Cash Ratio of Dabur

Year Absolute liquid assets Current Liabilities Ratio

2011-12 684 1078 0.63

2010-11 610 925 0.66

2009-10 404 872 0.46

2008-09 262 664 0.39

2007-08 271 583 0.46

2006-07 130 356 0.37

2005-06 79 307 0.26

2004-05 55 322 0.17

2003-04 127 236 0.54

2002-03 45 212 0.21

Grand Average 0.42

129

Table 16 shows the values of cash ratio of Dabur. In 2002-2003 the value of this ratio

was less than half of the standard value of .5. But in 2003-2004 the company followed the

ideal value. In the next year the ratio again fell to .17. The value of the ratio increased to

.26 in 2005-2006 and further increased to .37 in year 2006-2007 which is still lower than

the ideal ratio of .5. In year 2007-2008, the value increased further to .46 which is

approximately near to the ideal. The value further decreased and then increased in the

next two years. It is years 2010-2011 and 2011-2012 that Dabur changed its strict

working capital policy to a liberal one by keeping more of cash and cash equivalent

assets as the ratio values are .66 and .63 respectively.

(Rs in crores)

Table 17: Cash Ratio of Britannia

Year Absolute liquid assets Current Liabilities Ratio

2011-12 242 979 0.25

2010-11 265 456 0.58

2009-10 303 486 0.62

2008-09 338 413 0.82

2007-08 225 348 0.65

2006-07 239 323 0.74

2005-06 141 303 0.47

2004-05 150 303 0.5

2003-04 66 215 0.31

2002-03 71 191 0.37

Grand Average 0.53

130

Table 17 shows the values of cash ratio of Britannia for 10 years period starting from

year 2002-2003 to 2011-2012. The ratio value was more than the ideal value of .5 for

most of the years except for .37, .31 and .25 in 2002-2003, 2003-2004 and 2011-2012

respectively. Britannia had the perfect value of the ratio in 2004-2005. It dropped slightly

to .47 in the next year. Although the ratio was at a higher side from 2006-2007 to 2010-

2011 with the highest value at .82 in the year 2008-2009. It can be said that the company

has been quite liberal in keeping cash and cash equivalent assets.

131

6.3.2 Comparison of Cash Ratio among the Companies and with the

Industry’s Average

Table 18: Cash Ratio of 5 companies and the industry Average

Year ITC HUL Nestle Dabur Britannia Industry

Average

2011-12 0.79 0.63 0.17 0.63 0.25 0.49

2010-11 0.74 0.42 0.24 0.66 0.58 0.53

2009-10 0.68 0.28 0.25 0.46 0.62 0.46

2008-09 0.63 0.31 0.19 0.39 0.82 0.47

2007-08 0.60 0.04 0.14 0.46 0.65 0.38

2006-07 0.81 0.09 0.20 0.37 0.74 0.44

2005-06 1.00 0.09 0.21 0.26 0.47 0.41

2004-05 1.04 0.19 0.27 0.17 0.50 0.43

2003-04 0.55 0.21 0.16 0.54 0.31 0.35

2002-03 0.39 0.26 0.09 0.21 0.37 0.26

Grand

Average 0.72 0.25 0.19 0.42 0.53 0.42

132

Year 2011-12

In year 2011-12, the average cash ratio in the FMCG sectors comes out to be .49 which is

almost equal to the ideal cash ratio considered for manufacturing companies. As was seen

with other two ratios , the company having the least cash ratio is again Nestle with the

value of .17 which is less than half of the average ratio of the industry in that year. The

company with second lowest cash ratio is Britannia with the value of .25 which is again

approximately half of the industry’s average. The company whose ratio is near and above

to the industry’s average are ITC with the value of .79, HUL and Dabur with the same

value of .63. Refer Table 18.

2010-11

In year 2010-11, the average cash ratio in the FMCG sectors comes out to be .53 which is

almost equal to ideal cash ratio considered for manufacturing companies i.e..5:1. In this

year also, the company having the least cash ratio is Nestle with the value of .24 which is

more than half of the average ratio of the industry in that year followed by HUL with the

value of .42 which is again not very bad. Rest of the three companies ITC, Dabur and

Britannia have values which are more than the ideal and are also above to the industry’s

average in this year which indicates that the company are keeping surplus of cash in hand

to meet the day to day requirement and smooth functioning of work. Refer Table 18

2009-10

In year 2009-10, the average cash ratio in the FMCG sectors comes out to be .47. In the

same year, the company which is following the trend of keeping the lowest cash ratio is

133

Nestle with the value of .24 followed by HUL with a value of .28. the third position in

keeping the lower value of cash ratio is Dabur although the value .46 is much near to the

ideal ratio. The companies whose ratio is not only above to the industry’s average but are

also above the ideal ratio of manufacturing FMCG sector are ITC with the value of .68

and Britannia with the value of .62. Refer Table 18.

2002-03 to 2008-09

If we analyse these seven years, we see that the value of industry average of cash ratio

has shown an increasing trend since 2002-03 to 2008-09, except an exception in year

2007-2008. In all these seven years , HUL has maintained itself to be a company with the

most aggressive working capital policy with the minimum value of cash among all

companies. Nestle took the second place in keeping the minimum cash ratio. Moreover,

the companies that have maintained a reasonably higher and the best cash ratio among all

the companies are ITC and Britannia. Throughout the 10 years of time period, ITC

always has a cash ratio which is more than the industry’s average cash ratio. So, it can be

said that among all the FMCG companies, ITC has the most liberal working capital

policy. Britannia has also maintained a ratio near or above to the industry’s average.

Refer Table 18.

134

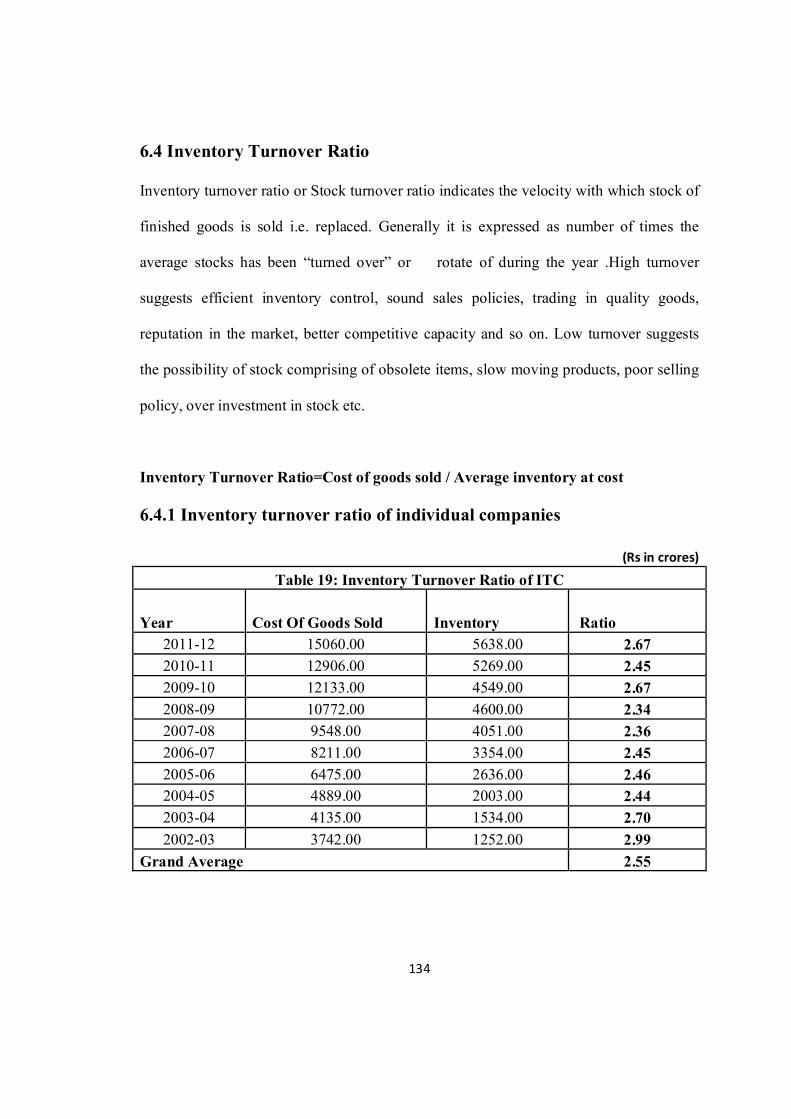

6.4 Inventory Turnover Ratio

Inventory turnover ratio or Stock turnover ratio indicates the velocity with which stock of

finished goods is sold i.e. replaced. Generally it is expressed as number of times the

average stocks has been “turned over” or rotate of during the year .High turnover

suggests efficient inventory control, sound sales policies, trading in quality goods,

reputation in the market, better competitive capacity and so on. Low turnover suggests

the possibility of stock comprising of obsolete items, slow moving products, poor selling

policy, over investment in stock etc.

Inventory Turnover Ratio=Cost of goods sold / Average inventory at cost

6.4.1 Inventory turnover ratio of individual companies

(Rs in crores)

Table 19: Inventory Turnover Ratio of ITC

Year Cost Of Goods Sold Inventory Ratio

2011-12 15060.00 5638.00 2.67

2010-11 12906.00 5269.00 2.45

2009-10 12133.00 4549.00 2.67

2008-09 10772.00 4600.00 2.34

2007-08 9548.00 4051.00 2.36

2006-07 8211.00 3354.00 2.45

2005-06 6475.00 2636.00 2.46

2004-05 4889.00 2003.00 2.44

2003-04 4135.00 1534.00 2.70

2002-03 3742.00 1252.00 2.99

Grand Average 2.55

135

Table 19 shows the value of inventory turnover ratio. On seeing the values of the 10

years, it can be said that the company has been very consistent in keeping the level of the

ratio. The value varies between 2.36 and 2.99. It also indicates that the company is

efficiently converting its inventory into sales and doesn’t believe in huge over stocking.

(Rs in crores)

Table 20: Inventory Turnover Ratio of HUL

Year Cost Of Goods Sold Inventory Ratio

2011-12 17718.00 2517.00 7.04

2010-11 16096.00 2811.00 5.73

2009-10 14975.00 2180.00 6.87

2008-09 17583.00 2529.00 6.95

2007-08 11832.00 1954.00 6.06

2006-07 10455.00 1548.00 6.75

2005-06 9617.00 1322.00 7.27

2004-05 8490.00 1470.00 5.78

2003-04 8162.00 1393.00 5.86

2002-03 7999.00 1279.00 6.25

Grand Average 6.46

136

Inventory turnover ratio of HUL has higher values than that of ITC. In Table 20, the

value of this ratio starts from 6.25 in the year 2002-2003 and then decreases in the next

two years. In year 2005-2006, the ratio again shows an increase to 7.27. In the next four

years, the ratio was more or less the same and then it declines in year 2010-2011. In the

year 2011-2012, the ratio again increased to 7.04.

(Rs in crores)

Table 21: Inventory Turnover Ratio of Nestle

Year Cost Of Goods Sold Inventory Ratio

2011-12 5939.00 734.00 8.09

2010-11 5006.00 576.00 8.69

2009-10 4095.00 499.00 8.21

2008-09 3460.00 435.00 7.95

2007-08 2808.00 401.00 7.00

2006-07 2274.00 276.00 8.24

2005-06 1955.00 253.00 7.73

2004-05 1777.00 217.00 8.19

2003-04 1710.00 219.00 7.81

2002-03 1538.00 219.00 7.02

Grand Average 7.89

137

Table 21 throws light on the inventory turnover ratio of Nestle. It can be seen that the

ratio is quite high as compared to the ratio of other companies taken in the study. It starts

with the value of 7.02 in the year 2002-2003 and then keeps on increasing in the next two

years till 2004-2005. In declines in the year 2005-2006 and then kept on increasing and

then decreasing in the next three years. In years 2010-2011 and 2011-2012, the ratio

increased to 8.69 and 8.09 respectively. The higher values of inventory turnover ratio

indicate that the company is having efficient inventory control and better competitive

capacity.

138

(Rs in crores)

Table 22: Inventory Turnover Ratio of Dabur

Year Cost Of Goods Sold Inventory Ratio

2011-12 2857.00 529.00 5.40

2010-11 2413.00 461.00 5.23

2009-10 1450.00 298.00 4.87

2008-09 1293.00 262.00 4.94

2007-08 1084.00 201.00 5.39

2006-07 822.00 157.00 5.24

2005-06 639.00 116.00 5.51

2004-05 616.00 128.00 4.81

2003-04 593.00 111.00 5.34

2002-03 624.00 179.00 3.49

Grand Average 5.02

Inventory turnover ratio of Dabur for 10 years has been more or less consistent except for

the year 2002-2003 in which the value is the least at 3.49. Table 22 shows that the value

139

of the ratio lays between 4.81 and 5.51. The value of the ratio indicates that the company

is not piling up too much stock in hand and also has a good selling policy.

(Rs in crores)

Table 23: Inventory Turnover Ratio of Britannia

Year Cost Of Goods Sold Inventory Ratio

2011-12 4548.00 382.00 11.91

2010-11 3872.00 311.00 12.45

2009-10 3239.00 268.00 12.09

2008-09 2849.00 254.00 11.22

2007-08 2353.00 302.00 7.79

2006-07 2070.00 215.00 9.63

2005-06 1512.00 185.00 8.17

2004-05 1323.00 134.00 9.87

2003-04 1276.00 122.00 10.46

2002-03 1159.00 82.00 14.13

Grand Average 10.77

140

Britannia shows the highest value of inventory turnover ratio among all the companies

taken in the study. Table 23 shows that the company has touched the highest value of

14.13 in the first year of 2002-2003 and the lowest value of 7.79 in the year 2007-2008.

But still the company has maintained very efficient values which show proficient

inventory control, sound sales policies, trading in quality goods, reputation in the market

and better competitive capacity.

6.4.2 Comparison of Inventory Turnover Ratio among the Companies

and with the Industry’s Average

Table 24: Inventory Turnover Ratio of 5 companies and the industry Average

Year ITC HUL Nestle Dabur Britannia Industry

Average

2011-12 2.67 7.04 8.09 5.40 11.91 7.02

2010-11 2.45 5.73 8.69 5.23 12.45 6.91

2009-10 2.67 6.87 8.21 4.87 12.09 6.94

2008-09 2.34 6.95 7.95 4.94 11.22 6.68

2007-08 2.36 6.06 7.00 5.39 7.79 5.72

2006-07 2.45 6.75 8.24 5.24 9.63 6.46

2005-06 2.46 7.27 7.73 5.51 8.17 6.23

2004-05 2.44 5.78 8.19 4.81 9.87 6.22

2003-04 2.70 5.86 7.81 5.34 10.46 6.43

2002-03 2.99 6.25 7.02 3.49 14.13 6.78

Grand

Average 2.55 6.46 7.89 5.02 10.77 6.54

141

Year 2011-12

Year 2011-12, saw the highest average inventory turnover ratio in last 10 years in the

FMCG sector. It was 7.02 with Britannia having the highest value followed by Nestle at

8.09 and HUL at 7.04. Higher the inventory turnover ratio, better it is considered for

FMCG companies because the goods are cheap and are consumed very fast and on the top they

are perishable also. The company having the least inventory turnover ratio is ITC with the

value of 2.67 which is less than half of the average ratio of the industry in that year. It

shows that the company is converting its inventory into sales at a very low pace. Refer

Table 24.

142

2010-11

In year 2010-11, the average inventory turnover ratio in the FMCG sectors comes out to

be 6.91 which is lesser than the ratio in year 2011-2012. In this year also, the company

having the highest inventory turnover ratio is Britannia with the value of 12.45 which is

even more than the average ratio of the industry. It is followed by Nestle with the value

of 8.69 which is again not very bad. Rest of the three companies ITC, Dabur and HUL

have values which are less than the industry’s average in this year which indicates that

the company are keeping surplus of inventory turnover in hand to meet the day to day

requirement and smooth functioning of work. Refer Table 24.

2009-10

In year 2009-10, the average inventory turnover ratio in the FMCG sector comes out to

be 6.94 which is reasonably good for FMCG companies. In the same year, the company

having the highest inventory turnover ratio is Britannia. The ratio is 12. And that shows

that the company is converting its goods produced into sales many a times during one

year. Nestle is the company with the second highest ratio of 8.21, followed by HUL with

the value of the ratio as 6.87. Dabur was able to maintain the ratio at a value of 4.87 and

the company with a very low ratio in the year 2009-2010 is ITC. It can be said that ITC

was least effective and efficient in converting its inventory into sales. Refer Table 24.

2002-03 to 2008-09

If we analyse these seven years, we see that the value of industry average of inventory

turnover ratio has been revolving around 6 with the only exception in year 2007-2008

143

when the value dropped to 5.72. In all these seven years, Britannia has maintained itself

to be a company with the most effective and efficient ways of converting its inventory

into sales by maintain the highest average inventory turnover ratio among all the

companies. Nestle took the second place in keeping the maximum inventory turnover

ratio. The companies that have maintained reasonably low and below average inventory

turnover ratio are Dabur, HUL and ITC. Throughout the 10 years of time period, ITC

always has a inventory turnover ratio which is least compared to all the companies. So, it

can be said that among all the FMCG companies, ITC has the most poor inventory

turnover ratio. Refer Table 24.

144

6.5 Accounts Receivable Turnover Ratio

Accounts receivable turnover measures the efficiency of a business in collecting its credit

sales. It is an activity or efficiency ratio and it measures average number of times a

business collects its accounts receivables in a period usually a year .Generally a high

value of accounts receivable turnover is favorable and lower figure may indicate

inefficiency in collecting outstanding sales but a normal level of receivables turnover is

different for different industries. Increase in accounts receivable turnover overtime

indicates improvement in credit sales collection process.

Receivables turnover ratio = Annual net credit sales / Average accounts receivables

6.5.1 Accounts Receivable Turnover ratio of individual companies

(Rs in crores)

Table 25: Accounts Receivable Turnover Ratio of ITC

Year Net Sales Sundry Debtors Ratio

2011-12 25999.00 986.00 26.37

2010-11 22039.00 885.00 24.90

2009-10 18757.00 859.00 21.84

2008-09 16147.00 669.00 24.14

2007-08 14558.00 737.00 19.75

2006-07 12501.00 637.00 19.62

2005-06 10077.00 548.00 18.39

2004-05 7875.00 528.00 14.91

2003-04 6695.00 230.00 29.11

2002-03 6035.00 207.00 29.15

Grand Average 22.82

145

Table 25 shows the value of account receivable turnover ratio of ITC for 10 years. The

value is almost same in the first two years of 2002-2003 and 2003-2004 i.e. 29.11 and

29.15. It showed that the company is quite efficient in collecting its credit sales. In year

2004-2005, the ratio declines to less than half of the previous year value at 14.91. In the

next 4 years, the value keeps on increasing and reached at 24.14 in year 2008-2009. In

year 2009-2010, the value decreased and after that kept on increasing for the next two

years with the value of 26.37 in 2011-2012. It can be concluded that overall the ITC has

been maintaining a satisfactory accounts receivable turnover ratio.

146

(Rs in crores)

Table 26: Accounts Receivable Turnover Ratio of HUL

Year Net Sales Sundry Debtors Ratio

2011-12 22395.00 679.00 32.98

2010-11 20008.00 943.00 21.22

2009-10 17873.00 678.00 26.36

2008-09 20829.00 537.00 38.79

2007-08 14180.00 443.00 32.01

2006-07 12458.00 440.00 28.31

2005-06 11365.00 523.00 21.73

2004-05 10246.00 489.00 20.95

2003-04 10598.00 471.00 22.50

2002-03 10339.00 368.00 28.10

Grand Average 27.30

The values of Account receivable turnover ratio of HUL are given in table 26. It shows

that the company is quite efficient in converting its outstanding sales favorable. The

company has the highest turnover ratio in the year 2008-2009 with a value of 38.79 and

147

lowest turnover ratio in the year 2004-2005 with the value of 20.95. The company

doesn’t follow any particular trend but the ratio keeps on fluctuating every year.

(Rs in crores)

Table 27:Accounts Receivable Turnover Ratio of Nestle

Year Net Sales Sundry Debtors Ratio

2011-12 7542.00 115.00 65.58

2010-11 6297.00 63.00 99.95

2009-10 5167.00 64.00 80.73

2008-09 4358.00 46.00 94.74

2007-08 3530.00 53.00 66.60

2006-07 2837.00 56.00 50.66

2005-06 2501.00 31.00 80.68

2004-05 2242.00 26.00 86.23

2003-04 2308.00 32.00 72.13

2002-03 2076.00 23.00 90.26

Grand Average 78.76

Table 27 shows the value of account receivable turnover ratio of Nestle for last 10 years.

The values in the table indicates that the company has been extremely efficient in

148

maintain the ratio by converting credit sales favorable. In year 2002-2003, the value is

90.26 and decreased to 72.13 in the next year. It increased for the next 2 years. In 2006-

2007, the value declined and reached 50.66. it increased in the next two years. It

decreased to 80.73 in year 2009-2010 and then reached the highest value of 99.95 in year

2010-2011. The ratio then declined in the year 2011-2012.

(Rs in crores)

Table 28: Accounts Receivable Turnover Ratio of Dabur

Year Net Sales Sundry Debtors Ratio

2011-12 3813.00 224.00 17.02

2010-11 3307.00 202.00 16.37

2009-10 2890.00 130.00 22.23

2008-09 2439.00 112.00 21.78

2007-08 2111.00 100.00 21.11

2006-07 1617.00 61.00 26.51

2005-06 1375.00 27.00 50.93

2004-05 1280.00 49.00 26.12

2003-04 1160.00 43.00 26.98

2002-03 1241.00 117.00 10.61

Grand Average 23.97

149

The values of accounts receivable turnover ratio are indicated in table 28. The values

indicate that the company doesn’t follow any trend in the 10 years considered in this

study. The lowest value maintained by the company is 10.61 in the year 2002-2003 and

the highest value is 50.93 in the year 2005-2006. The values give a satisfactory image of

the company in converting its outstanding sales favourable.

(Rs in crores)

Table 29: Accounts Receivable Turnover Ratio of Britannia

Year Net Sales Sundry Debtors Ratio

2011-12 5033.00 52.00 96.79

2010-11 4272.00 57.00 74.95

2009-10 3458.00 39.00 88.67

2008-09 3152.00 50.00 63.04

2007-08 2635.00 46.00 57.28

2006-07 2231.00 29.00 76.93

2005-06 1735.00 21.00 82.62

2004-05 1589.00 44.00 36.11

2003-04 1494.00 19.00 78.63

2002-03 1329.00 29.00 45.83

Grand Average 70.09

150

Table 29 shows the values of accounts receivable turnover ratio of Britannia. The values

show that the company has been successful in maintaining and managing its accounts

receivable turnover ratio. It is efficiently turning its outstanding sales favorable. The

company has achieved the highest value of 96.79 in the year 2011-2012. It has 36.11 as

the lowest value in the year 2004-2005. The value of account receivable turnover is quite

high in most of the years.

151

6.5.2 Comparison of Accounts Receivable Turnover Ratio among the Companies

and with the Industry’s Average

Table 30: Accounts Receivable Turnover Ratio of 5 companies and the industry

Average

Year ITC HUL Nestle Dabur Britannia Industry

Average

2011-12 26.37 32.98 65.58 17.02 96.79 47.75

2010-11 24.90 21.22 99.95 16.37 74.95 47.48

2009-10 21.84 26.36 80.73 22.23 88.67 47.97

2008-09 24.14 38.79 94.74 21.78 63.04 48.50

2007-08 19.75 32.01 66.60 21.11 57.28 39.35

2006-07 19.62 28.31 50.66 26.51 76.93 40.41

2005-06 18.39 21.73 80.68 50.93 82.62 50.87

2004-05 14.91 20.95 86.23 26.12 36.11 36.86

2003-04 29.11 22.50 72.13 26.98 78.63 45.87

2002-03 29.15 28.10 90.26 10.61 45.83 40.79

Grand

Average 22.82 27.30 78.76 23.97 70.09 44.59

152

Year 2011-12

In year 2011-12, the average receivable turnover ratio in the FMCG sector is 47.75 which

is quite high with the major reason that customers don’t take long credits on Fast moving

consumer goods. It was 96.79 with Britannia having the highest value followed by Nestle

at 65.58 and HUL at 32.98. Higher the receivable turnover ratio, better it is considered

for FMCG companies because it generally indicates improvement in the process of cash

collection on credit sales. The company having the least receivable turnover ratio is

Dabur with the value of 17.02 which is less than half of the average ratio of the industry

in that year. It shows that the company is converting its receivable into sales at a very low

pace. Refer Table 30.

2010-11

In year 2010-11, the average receivable turnover ratio in the FMCG sector comes out to

be 47.48 which is slightly lesser than the ratio in year 2011-2012. In this year, the

company having the highest receivable turnover ratio is Nestle with the value of 99.95

which is double the average ratio of the industry. It is followed by Britannia with the

value of 74.95 which is again very high and more than the industry’s average. Rest of the

three companies ITC, Dabur and HUL have values which are much less than the

industry’s average in this year which indicates that the company are not keeping strict

credit terms since such policies may repel potential buyers.. Refer Table 30.

2009-10

In year 2009-10, the average receivable turnover ratio in the FMCG sector comes out to

be 47.97 which is reasonably good for FMCG companies. In the same year, the company

153

having the highest receivable turnover ratio is Britannia. The ratio is 88.67. And that

shows that the company is keeping an efficient credit policy and is converting its credit

into cash effectively during one year. Nestle is the company with the second highest ratio

of 80.73. All other three companies namely Dabur, ITC and HUL had their ratios around

20. It can be said that ITC was least effective and efficient in converting its receivable

into cash. Refer Table 30.

2002-03 to 2008-09

If we analyse these seven years, we see that the value of industry average of receivable

turnover ratio has been revolving around 40 with the only exception in year 2005-2006

when the value reached to 50.87. In all these seven years, Britannia and Nestle have

maintained itself to be the two companies with the most effective and efficient ways of

converting its receivable into cash by maintain the highest average receivable turnover

ratio among all the companies. The companies that have maintained reasonably low and

below average receivable turnover ratio are Dabur, HUL and ITC. Throughout the 10

years of time period, ITC always has a receivable turnover ratio which is least compared

to all the companies. So, it can be said that among all the FMCG companies, ITC has

maintained a very liberal credit policy to capture more and more of customers in the

FMCG market. Refer Table 30.

154

6.6 Accounts Payable Turnover Ratio

Accounts payable turnover is the ratio of net credit purchases of a business to its average

accounts payable during the period. It measures short term liquidity of business since it

shows how many times during a period, an amount equal to average accounts payable is

paid to suppliers by a business. Accounts payable turnover is a measure of short-term

liquidity. A higher value indicates that the business was able to repay its suppliers

quickly. Thus higher value of accounts payable turnover is favorable.

Payable turnover ratio = Annual net credit purchases / Average accounts payable

6.6.1 Accounts Payable Turnover Ratio of individual companies

(Rs in crores)

Table 31: Accounts Payable Turnover Ratio of ITC

Year Net Purchases Sundry Creditors Ratio

2011-12 9698 1425 6.81

2010-11 8431 1395 6.04

2009-10 7337 3444 2.13

2008-09 6092 2924 2.08

2007-08 6767 2740 2.47

2006-07 6032 2343 2.57

2005-06 4607 2148 2.14

2004-05 3236 1892 1.71

2003-04 2601 2804 0.93

2002-03 2331 2051 1.14

Grand Average 2.80

155

Table shows the value of account payable turnover ratio of ITC. The values started with

1.14 in the year 2002-2003. It decreased in the next year. In year 2004-2005, it increased

to 1.71. From year 2005-2006 to 2009-2010, the value stayed in twos. Then the value

increased sharply and touched 6.04 in year 2010-2011 and further increased to 6.81 in

year 2011-2012. The values shows `that the company is comfortable in paying to its

suppliers and managing the creditors properly.

156

(Rs in crores)

Table 32: Accounts Payable Turnover Ratio of HUL

Year Net Purchases Sundry Creditors Ratio

2011-12 11609 4623 2.51

2010-11 10369 5009 2.07

2009-10 8901 4374 2.03

2008-09 11232 3305 3.40

2007-08 7455 2878 2.59

2006-07 6619 2464 2.69

2005-06 6114 2345 2.61

2004-05 5357 2029 2.64

2003-04 5389 1841 2.93

2002-03 5199 2072 2.51

Grand Average 2.60

Values of accounts payable turnover ratio are shown in table. The values of almost all the

years except for year 2008-2009 are ranging between 2.03 to 2.69. The year 2008-2009

has the increased value of 3.40. This shows that the company is satisfying its creditors by

157

making payments to them on time. The company has managed to keep short term

liquidity.

(Rs in crores)

Table 33: Accounts Payable Turnover Ratio of Nestle

Year Net Purchases Sundry Creditors Ratio

2011-12 3638 997 3.65

2010-11 3139 745 4.21

2009-10 2457 582 4.22

2008-09 2139 502 4.26

2007-08 1752 456 3.84

2006-07 1337 366 3.65

2005-06 1128 317 3.56

2004-05 1041 266 3.91

2003-04 950 236 4.03

2002-03 851 212 4.01

Grand Average 3.93

Table shows the values of account payable turnover ratio of nestle. Year 2002-2003 has

4.01 as the ratio which got increased to 4.03 in the next year. Year 2004-2005 sees a

slight decline in the ratio value to 3.91 which further declined to 3.56 in the next year.

158

The ratio is 3.65 in the year 2006-2007 which got increased to 3.84 in the next year. The

value stayed more or less near four in the next three years and then it declined to 3.65 in

year 2011-2012. The value of account payable ratio indicates that the company is

maintaining its trade creditors.

(Rs in crores)

Table 34: Accounts Payable Turnover Ratio of Dabur

Year Net Purchases Sundry Creditors Ratio

2011-12 2080 585 3.56

2010-11 1729 495 3.49

2009-10 1400 349 4.01

2008-09 1283 282 4.55

2007-08 1029 250 4.12

2006-07 796 190 4.19

2005-06 564 132 4.27

2004-05 560 133 4.21

2003-04 483 115 4.20

2002-03 540 81 6.67

Grand Average 4.33

159

Table shows that Dabur has maintained quite a comfortable account payable turnover

ratio by paying the suppliers on time and satisfying them. Year 2002-2003 has a value of

6.67 which is quite high. Then the ratio kept on declining and reached 4.12 in year 2007-

2008. It increased to 4.55 in year 2008-2009 and then again kept on declining and

reached 3.56 in the year 2011-2012.

(Rs in crores)

Table 35: Accounts Payable Turnover Ratio of Britannia

Year Net Purchases Sundry Creditors Ratio

2011-12 3184 336 9.48

2010-11 2782 240 11.59

2009-10 2183 133 16.41

2008-09 1862 88 21.16

2007-08 1643 94 17.48

2006-07 1428 86 16.60

2005-06 1054 86 12.26

2004-05 869 74 11.74

2003-04 642 155 4.14

2002-03 560 157 3.57

Grand Average 12.44

160

The values of Account payable turnover ratio of Britannia are very high and are highest

among all the companies taken in the study. The year 2002-2003 has the lowest value of

3.57 among all 10 years. The value started increasing and reached 21.16 in the year 2008-

2009 which shows a very efficient turnover ratio and indicate that the company is paying

to the creditors very fast. The ratio value started declining after that year and reached

9.48 in the year 2011-2012. Still the value of account payable turnover ratio is

comparatively very high.

161

6.6.2 Comparison of Accounts Payable Turnover Ratio among the Companies and

with the Industry’s Average

Table 36: Accounts Payable Turnover Ratio of 5 companies and the industry

Average

Year ITC HUL Nestle Dabur Britannia Industry

Average

2011-12 6.81 2.51 3.65 3.56 9.48 5.20

2010-11 6.04 2.07 4.21 3.49 11.59 5.48

2009-10 2.13 2.03 4.22 4.01 16.41 5.76

2008-09 2.08 3.40 4.26 4.55 21.16 7.09

2007-08 2.47 2.59 3.84 4.12 17.48 6.10

2006-07 2.57 2.69 3.65 4.19 16.60 5.94

2005-06 2.14 2.61 3.56 4.27 12.26 4.97

2004-05 1.71 2.64 3.91 4.21 11.74 4.84

2003-04 0.93 2.93 4.03 4.20 4.14 3.25

2002-03 1.14 2.51 4.01 6.67 3.57 3.58

Grand

Average 2.80 2.60 3.93 4.33 12.44 5.22

162

Year 2011-12

In year 2011-12, the average payable turnover ratio in the FMCG sector is 5.20 which is

not very high. It was 9.48 with Britannia having the highest value followed by ITC at

6.81 and Nestle at 3.65. Higher the payable turnover ratio, better it is considered for

FMCG companies because it generally indicates that the business was able to repay its

suppliers quickly. Thus higher value of accounts payable turnover is favorable. The

company having the least payable turnover ratio is HUL with the value of 2.51 which is

less than the average ratio of the industry in that year. It shows that the company is

converting its payable into sales at a very low pace because of the short term liquidity

problem. Refer Table 36.

2010-11

In year 2010-11, the average payable turnover ratio in the FMCG sector comes out to be

5.48 which is slightly more than the ratio in year 2011-2012. In this year, the company

having the highest payable turnover ratio is Britannia with the value of 11.59 which is

double the average ratio of the industry. It is followed by ITC with the value of

6.04which is again high and more than the industry’s average. Rest of the three

companies Nestle, Dabur and HUL have values which are much less than the industry’s

average in this year which indicates that the companies are not having short term liquidity

to pay regularly to their suppliers. Refer Table 36.

163

2009-10

In year 2009-10, the average payable turnover ratio in the FMCG sector comes out to be

5.76 which is reasonably good for FMCG companies. In the same year, the company

having the highest payable turnover ratio is Britannia. The ratio is 16.41. And that shows

that the company is keeping an efficient payment system by paying its creditors on time

and maintaining its short term liquidity effectively during one year. Nestle and Dabur are

the companies with the second and third highest ratio of 4.22 and 4.02 respectively. Other

two companies namely ITC and HUL had their ratios around 2. Refer Table 36.

2002-03 to 2008-09

If we analyse these seven years, we see that the value of industry average of payable

turnover ratio has been moving in the northward direction from the value of 3.58 in 2002-

2003 to 7.09 in 2008-2009. In all these seven years, Britannia is the only company that

have maintained itself to be the most effective and efficient in converting its account

payables into cash on time followed by Dabur. All other companies have maintained

reasonably low and below average payable turnover ratio. Throughout the 10 years of

time period, ITC always has a payable turnover ratio which is least compared to all the

companies. So, it can be said that among all the FMCG companies, ITC has maintained a

very poor picture in the eyes of the suppliers. Refer Table 36.

164

6.7 Working Capital Turnover Ratio:

This ratio represents the number of times the working capital is turned over in the course

of year. The working capital turnover ratio measures the efficiency with which the

working capital is being used by a firm. A high ratio indicates efficient utilization of

working capital and a low ratio indicates otherwise. But a very high working capital

turnover ratio may also mean lack of sufficient working capital which is not a good

situation.

Working Capital Turnover Ratio = Net Sales / Net Working Capital

6.7.1 Working Capital Turnover Ratio of individual companies

(Rs in crores)

Table 37 :Working Capital Turnover Ratio of ITC

Year Net Sales Net Working Capital Ratio

2011-12 25999 5342 4.87

2010-11 22039 4569 4.82

2009-10 18757 4449 4.22

2008-09 16147 5401 2.99

2007-08 14558 4676 3.11

2006-07 12501 4664 2.68

2005-06 10077 4316 2.33

2004-05 7875 3594 2.19

2003-04 6695 1849 3.62

2002-03 6035 1442 4.19

Grand Average 3.50

165

Table 37 indicates that the working capital turnover ratio of ITC is satisfactory. It

indicates that the company is quite efficient in turning the working capital into sales. It

can be seen that ITC started with a working capital turnover ratio of 4.19 in the 2002-

2003 that indicated that the company is operationally very efficient in maintain its current

assets and current liabilities. As it moved ahead in year 2003-2004 and further to 2005-

2006, the ratio started decreasing but still had a reasonably high value throughout these

years. The ratio gradually started increasing and reached a high of 4.87 in year 2011-

2012. Throughout these 10 years, the company has maintained a good working capital

turnover ratio which indicates that the company has been efficient operationally.

166

(Rs in crores)

Table 38: Working Capital Turnover Ratio of HUL

Year Net Sales Net Working Capital Ratio

2011-12 22395 1350 16.59

2010-11 20008 -546 -36.64

2009-10 17873 -1365 -13.09

2008-09 20829 -183 -113.82

2007-08 14180 -1834 -7.73

2006-07 12458 -1353 -9.21

2005-06 11365 -1355 -8.39

2004-05 10246 -409 -25.05

2003-04 10598 -369 -28.72

2002-03 10339 -240 -43.08

Grand Average -26.91

Working capital turnover ratio of HUL shows negative values from year 2002-2003. The

ratio cannot be analysed alone but values of inventory and account receivables are also

167

considered. A negative working capital in the denominator is not bad all the times. It

shows that HUL can generate cash so quickly they actually have a negative working

capital. This happens because customers pay upfront and so rapidly, the business has no

problems raising cash. In HUL, products are delivered and sold to the customer before

the company ever pays for them. Moreover if the inventory and account receivables are

seen for all these years, the value of both the current assets are very low that shows that

the HUL is capable of maintaining low inventory and receivables as the company is

capable of doing business on cash basis. In such a scenario, the negative values of

working capital turnover ratio of all the years from 2002-2011 is a good thing for HUL.

(Rs in crores)

Table 39: Working Capital Turnover Ratio of Nestle

Year Net Sales Net Working Capital Ratio

2011-12 7542 -727 -10.37

2010-11 6297 -473 -13.31

2009-10 5167 -362 -14.27

2008-09 4358 -352 -12.38

2007-08 3530 -226 -15.62

2006-07 2837 -156 -18.19

2005-06 2501 -118 -21.19

2004-05 2242 -105 -21.35

2003-04 2308 -54 -42.74

2002-03 2076 -29 -71.59

Grand Average -24.10

168

As it can be seen in Table 39 that the working capital turnover ratio of Nestle is negative

for all the ten years considered for the study, the reason is similar to that of HUL

discussed in the previous paragraph. It can be seen that the negative value of the ratio is

because of the negative working capital in all these years. The company has also

maintained low inventories and account receivables throughout these years. It can be

analysed that Nestle works on cash basis and believes that as long as the transactions are

timed right, they can pay each bill as it comes due, maximizing their efficiency.

169

(Rs in crores)

Table 40: Working Capital Turnover Ratio of Dabur

Year Net Sales Net Working Capital Ratio

2011-12 3813 602 6.33

2010-11 3307 471 7.02

2009-10 2890 286 10.1

2008-09 2439 199 12.26

2007-08 2111 173 12.2

2006-07 1617 120 13.48

2005-06 1375 18 76.39

2004-05 1280 -26 -49.23

2003-04 1160 98 11.84

2002-03 1241 201 6.17

Grand Average 10.66

Dabur has very mixed values of the ratio. It reflects a poor working capital policy framed

by the company. The ratio started with 6.17 in the year 2002-2003 and increased during

the next year too. In year 2004-2005, it went negative and touched -49.23. In the next

170

year again it turned positive and reached a high of 76.39. A very high ratio of 76.39

indicates that the denominator i.e. working capital is very low that shows that the

company has very few current assets in this year. In the next few years, it went on falling

and reached a low of 6.33 in the year 2011-2012. The reason behind it was the increasing

working capital year after year.

(Rs in crores)

Table 41: Working Capital Turnover Ratio of Britannia

Year Net Sales Net Working Capital Ratio

2011-12 5033 -121 -41.6

2010-11 4272 248 17.23

2009-10 3458 315 10.98

2008-09 3152 423 7.45

2007-08 2635 385 6.84

2006-07 2231 248 9

2005-06 1735 139 12.48

2004-05 1589 89 17.85

2003-04 1494 70 21.34

2002-03 1329 85 15.64

Grand Average 7.72

171

Table 41 shows the working capital turnover ratio of Britannia. The value in almost all

the years is good indicating efficient operations by the company. In year 2002-2003, the

ratio was at 15.64 and than increased in the next year. In year 2004-2005, it dropped to

17.85 which further kept on declining and reached to 6.84 in the year 2007-2008. From

this year, the ratio kept on increasing and reached 17.23 in the year 2010-2011. It was

year 2011-2012, when the situation changed all together and the company reached a

negative ratio due the falling working capital.

172

6.7.2 Comparison of Working Capital Turnover Ratio among the Companies and

with the Industry’s Average

Table 42: Working Capital Turnover Ratio of 5 companies and the industry

Average

Year ITC HUL Nestle Dabur Britannia

Industry

Average

2011-12 4.87 16.59 -10.37 6.33 -41.60 -7.18

2010-11 4.82 36.64 -13.31 7.02 17.23 4.12

2009-10 4.22 13.09 -14.27 10.10 10.98 3.05

2008-09 2.99 113.82 -12.38 12.26 7.45 2.66

2007-08 3.11 7.73 -15.62 12.20 6.84 1.93

2006-07 2.68 9.21 -18.19 13.48 9.00 1.93

2005-06 2.33 8.39 -21.19 76.39 12.48 14.47

2004-05 2.19 25.05 -21.35 -49.23 17.85 -9.67

2003-04 3.62 28.72 -42.74 11.84 21.34 -0.46

2002-03 4.19 43.08 -71.59 6.17 15.64 -8.28

Grand

Average 3.50 30.23 -24.10 10.66 7.72 0.26

173

Year 2011-12

Year 2011-12, the average working capital turnover ratios in the FMCG sector is -7.18.

The reason for a negative ratio is because of the dominant effect of Nestle and Britannia

as both were having a high negative working capital ratio. It was -41.60 with Britannia

having the highest negative value followed by Nestle at -10.37. Higher the working

capital turnover ratio, better it is considered for FMCG companies because it shows that

how efficiently the company is able to convert its working capital into sales. Although a

negative value of this ratio is confusing because it can be good or bad depending on the

cash policy and other current assets maintained by the company. Negativity in the ratio

shows that their current liabilities or payables are higher than current assets or

receivables. This essentially means the companies do not have to deploy their own capital

or borrow from banks to carry out their routine business activities. It is actually very good

to have negative working capital because this entitles companies to earn relatively better

returns on capital and equity. This also shows the operational efficiency of a company.

The value is negative in these two companies because being the FMCG companies, they

work on cash basis and moreover both the companies are maintaining a very low

inventory and account receivables. The company having positive working capital

turnover ratios are Dabur, ITC and HUL which again reflect the efficacy of the

operations of these companies. Refer Table 42.

2010-11

In year 2010-11, the average working capital turnover ratio in the FMCG sectors comes

out to be 4.12 which is higher than the ratio in year 2011-2012. In this year also, the

174

company having the highest working capital turnover ratio is Britannia with the value of

17.23 which is even more than the average ratio of the industry. It also reflects that this

company is not having any defined working capital policy. It is followed by Dabur with

the value of 7.02 which is again very high. ITC has value which is slightly less than the

industry’s average in this year. Nestle is still maintaining a negative value of this ratio

indicating a cash basis policy used by them. HUL has a negative working capital ratio of

36.64. Refer Table 42.

2009-10

In year 2009-10, the average working capital turnover ratio in the FMCG sector comes

out to be 6.94 which is reasonably good for FMCG companies. In the same year, the

company having the highest working capital turnover ratio is Britannia. The ratio is

10.98. And that shows that the company is converting its goods produced into sales

many a times during one year. Dabur is the company with the second highest ratio of

10.10, followed by ITC with the value of the ratio as 4.22. Nestle maintained a negative

ratio at a value of -14.27. negative ratio maintained by Nestle in all the years shows that

Nestle collects its money from customers in just four days (average collection period),

whereas it pays in 52 days to its raw material suppliers. It shows the strength of this

company in efficiently maintaining its current assets less than the current liabilities. Hul

also maintained the same policy that of Nestle with a negative working capital ratio of

13.09. Refer Table 42.

175

2002-03 to 2008-09

If we analyse these seven years, we see that the value of industry average of working

capital turnover ratio is not following any trend. In all these seven years, Nestle has

maintained itself to be a company with the most effective and efficient ways of

converting its working capital into sales by maintaining a negative working capital

working capital turnover ratio among all the companies followed by HUL. It shows that

Nestle and HUL being the fastest growing FMCG companies works on cash basis.

Britannia is the company with the highest positive working capital in almost all the years

except for the year 2004-2005. Dabur has maintained the ratio lower than that of

Britannia but still quite high. The company that has maintained reasonably low and below

average working capital turnover ratio is ITC. Throughout the 10 years of time period,

ITC always has a working capital turnover ratio which is least compared to all the

companies. So, it can be said that among all the FMCG companies, ITC has the most

poor working capital turnover ratio. Refer Table 42.

176

6.8 Current Assets Turnover Ratio

Current assets turnover is an efficiency measurement accountants apply to a company’s

financial statements. The result from this formula is a metric that indicates how well a

company generates sales revenue from the current assets it owns. A higher number is

generally preferable as the company uses its assets in the most efficient manner possible.

Current assets turnover = Net sales / current assets

6.8.1 Current Assets Turnover Ratio of individual companies

(Rs in crores)

Table 43: Current Assets Turnover Ratio of ITC

Year Net Sales Current Assets Ratio

2011-12 25999 14444 1.8

2010-11 22039 13046 1.69

2009-10 18757 12497 1.5

2008-09 16147 10105 1.6

2007-08 14558 9108 1.6

2006-07 12501 8522 1.47

2005-06 10077 7894 1.28

2004-05 7875 6628 1.19

2003-04 6695 5382 1.24

2002-03 6035 4162 1.45

Grand Average 1.48

177

Table above shows the current asset turnover ratio of ITC. If we look at all the years, the

ratio varied from 1.19 to 1.80 and it has also shown an increasing trend in the recent

years. It started with 1.45 in the year 2002-2003 and then fell in the next year to 1.24 and

then further fell to 1.119 in the year 2004-2005. After that , the ratio kept on increasing

till 2011-2012. Higher the ratio, better is for the company as it shows how many times the

current assets are converting into sales. ITC has the lowest ratio among all the other

companies taken in the study.

178

(Rs in crores)

Table 44: Current Assets Turnover Ratio of HUL

Year Net Sales Current Assets Ratio

2011-12 22395 7799 2.87

2010-11 20008 6074 3.29

2009-10 17873 5368 3.33

2008-09 20829 5601 3.72

2007-08 14180 3277 4.33

2006-07 12458 3170 3.93

2005-06 11365 2763 4.11

2004-05 10246 3305 3.1

2003-04 10598 3502 3.03

2002-03 10339 3431 3.01

Grand Average 3.47

Table 44 shows the current assets turnover ratio of HUL for last 10 years. The ratio

seems to be high and ranges between 2.87 and 4.33. it indicates that the current assets of

HUL are efficient in maintain the current assets in such a way that lesser current assets

179

are resulting in higher sales of the company specially as compared to ITC. Moreover we

have also seen that HUL has maintained a low level of current assets in all the other

ratios like inventory turnover ratio, account receivable ratio and working capital turnover

ratio. This shows the efficacy of HUL in maintain its working capital.

(Rs in crores)

Table 45: Current Assets Turnover Ratio of Nestle

Year Net Sales Current Assets Ratio

2011-12 7542 1407 5.36

2010-11 6297 1197 5.26

2009-10 5167 1060 4.87

2008-09 4358 833 5.23

2007-08 3530 732 4.82

2006-07 2837 613 4.63

2005-06 2501 567 4.41

2004-05 2242 513 4.37

2003-04 2308 438 5.27

2002-03 2076 400 5.19

Grand Average 4.94

180

Current assets turnover ratios of Nestle for last 10 years are indicated in the above table.

The table shows that the ratios maintained by Nestle are quite high which indicate that

Nestle has been maintaining a low level of current assets and with this level, it is

resulting in high sales. This kind of situation is very beneficial for the company as it

results in increasing return on total capital and equity. This reflects a light on the stringent

working capital policy followed by Nestle in all the years as the value of current assets

turnover ratio revolves around 5 in all the 10 years considered for the study.

(Rs in crores)

Table 46: Current Assets Turnover Ratio of Dabur

Year Net Sales Current Assets Ratio

2011-12 3813 1680 2.27

2010-11 3307 1396 2.37

2009-10 2890 1158 2.50

2008-09 2439 863 2.83

2007-08 2111 756 2.79

2006-07 1617 476 3.40

2005-06 1375 325 4.23

2004-05 1280 296 4.32

2003-04 1160 334 3.47

2002-03 1241 413 3.00

Grand Average 3.12

181

Table 46 shows the current assets turnover ratio of Dabur. The values indicate that Dabur

is able to cover its sales almost three times of its current assets. This reflects the efficacy

of the company in maintaining its current assets. The ratio was 3 in year 2002-2—3 and

kept on increasing till year 2004-2005 when it reached 4.32. From this year, the value of