Embed Size (px)

Citation preview

1Cattolica Group

Borsa ItalianaItalian Investor Conference 2006

New York, 3-4 April 2006

Cattolica Group:Strategy and Results

Giulio Fezzi - Chief Financial Officer and IR ManagerAndrea Battista - General Manager Duomo Assicurazioni and IR

2Cattolica Group

Agenda

Cattolica Group at a glance

Strategic framework and strategy implementation

Business growth and value creation

3Cattolica Group

Agenda

Cattolica Group at a glance

Strategic framework and strategy implementation

Business growth and value creation

4Cattolica Group

The Parent Company is a co-operative legal-entity structure, operating in the life and non-life insurance businesses in Italy

Today the Group consists of 22 companies, including 14 insurance companies

Insurance subsidiaries of the Parent Company, include:

• 8 life insurance companies (Duomo Previdenza, Risparmio & Previdenza, BPV Vita, Lombarda Vita, Eurosav, Axa-Cattolica Previdenza in Azienda, San Miniato Previdenza, Persona Life)

• 5 non-life insurance companies (Il Duomo Assicurazioni, ABC Assicura, Cattolica Aziende, Tua Assicurazioni, UniOne Assicurazioni)

Other Group companies consist of two real-estate companies, four service companies, one asset management company and one retail-brokerage (Fas) company

Cattolica Group

5Cattolica Group

Cattolica Group brands and companiesHISTORICAL PHASES

Cattolica Group Evolution

BIRTH CONS. GROUP DEVELOPMENT

Premiums (*) (Euro mln)

1896 1976 1994 20042000 2002 2003‘98‘95‘97

2001 2005

373 2,768 3,731 5,188

Listing

2006

(*) Including Investment Contracts

6Cattolica Group

Group Market Share trend

Group Market Share (2002 - 2005; Italian direct business)

Sources: Estimates on Cattolica Group reports and ANIA data

3.8%4.0% 3.9%

4.5% 4.5%

4.9%

4.2%4.3%

4.5%

2002 2003 2004

Non-life Life Total market share

2005

Non-life Life Total

7

6 65 th

traditional insurance

Italian Group

4.2%

5.2%

4.9%

2005

Ranking

7Cattolica Group

Development of Group’s multi-channel network

Tied Agencies n.

546

900 974 1,024 1,049 1,092

1999 2000 2001 2002 2003 2004 31/12/05

1,357

FAs n.

337511 613

895

1,212 1,138

1999 2000 2001 2002 2003 2004 31/12/05

975

Bank branches n.

2,066

2,653 2,717 2,748

3,053

2,702

1999 2000 2001 2002 2003 2004 31/12/05

2,913With the exclusion of

138 multi-mandatory agencies

8Cattolica Group

Rating on Cattolica: “excellent risk-adjusted capitalisation”

A Excellent

Stable outlook

NOTE

Aq Strong

Quantitative – Insurer Financial Strength

NOTE

A

NOTE

Strong

The rating reflects Cattolica’sprospective excellent risk-adjusted capitalisation, excellentoperating performance and distinctive business position in the Italian Market

The rating reflects very strongcapitalisation and strongearnings.

The rating reflects strongcompetitive position, strongoperating performance and strongcapitalization. The stable outlook represents S&P’s expectation Cattolica will maintain its strong competitive position.

Stable outlook

9Cattolica Group

Agenda

Cattolica Group at a glance

Strategic framework and strategy implementation

Business growth and value creation

10Cattolica Group

Mission and strategic objectives continued

Architettura industriale focalizzata, integrata e aperta

Crescita organica

Crescita per linee esterne

sul core business assicurativo, proseguendo nel consolidamento dei business attuali ed avviando nuovi percorsi di crescita

Focus integrated, openIndustrial architecture

Crescita organicaOrganicgrowth

Crescita per linee esterne

Externalgrowth

STRATEGIC PATHS

MISSION

Consolidate the insurance

business model

Integrated development of

financial services

Service centralisation and cost optimization

Strengthen controllership

Develop current business

Develop new markets, products,

channels

Accelerate development

Strategic objectives

… focus on insurance core business, consolidating current businesses and implementing new growth strategies through flexible development methods

11Cattolica Group

Details on strategy and key assumptions

nConsolidation of organization structure, insurance brands and corporate culture with a focused, integrated and open business architecture

- Strengthening parent company controls by controlling strategic processes using improved support tools (planning and control, Internal Audit, Organization & HR, new Program Management structure, Group Finance)

- Insurance business model consolidation with reorganization of technical areas, enabled by the new, enhanced non -life platform

- Integrated development of financial and asset management

- Completing integration of operating processes and procedures

nOrganic growth: research and development of internal growth initiatives, building on the existing business strengths

- Expansion of existing businesses, through distribution channel development and diversification

- Identification and entrance into new markets, products and channels: implementation and finalization of new initiatives like “Tua Assicurazioni” and “Axa – Cattolica Previdenza in Azienda”

- Assure the development of non-life bancassurance distribution

- Reentry/development of multi- mandatory agent distribution: from Eurosav to Persona Life

- Nurture the innovation culture as a growth driver for testing new products and market segments: Pension Center of Excellence, new health product development - from simple to LTC coverage

nExternal growth- Formalized process for screening and developing proposals for potential acquisitions (Corporate Development team)

- January 2005 – 50% Eurosav acquisition

- July 2005 – UniOne acquisition

12Cattolica Group

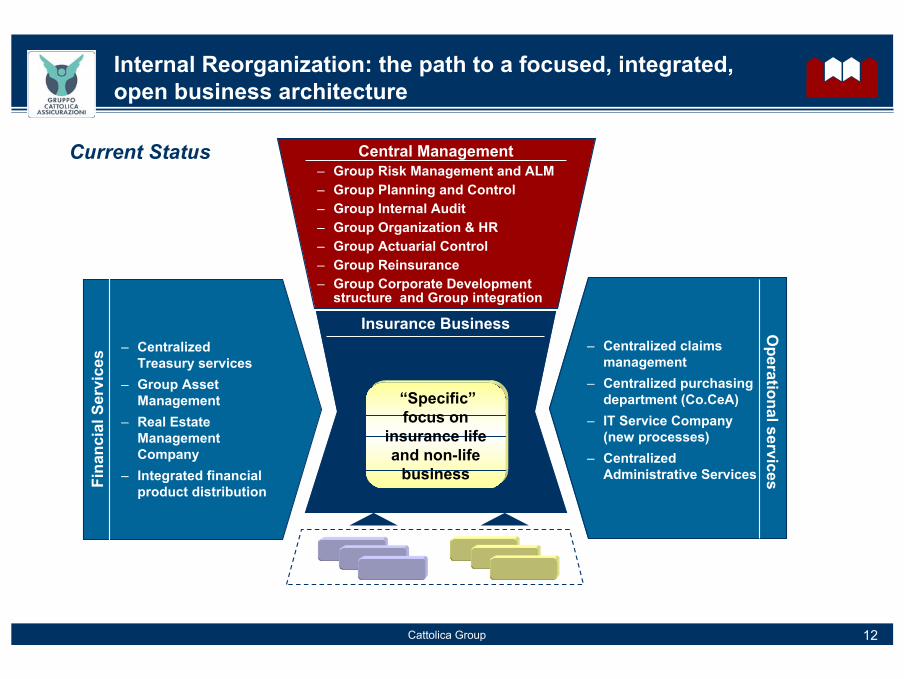

Internal Reorganization: the path to a focused, integrated, open business architecture

Central Management

Fina

ncia

l Ser

vice

s

Operational services

Insurance Business

– Group Risk Management and ALM– Group Planning and Control– Group Internal Audit– Group Organization & HR– Group Actuarial Control– Group Reinsurance– Group Corporate Development

structure and Group integration

– Centralized Treasury services

– Group Asset Management

– Real Estate Management Company

– Integrated financial product distribution

Current Status

– Centralized claims management

– Centralized purchasing department (Co.CeA)

– IT Service Company (new processes)

– Centralized Administrative Services

“Specific” focus on

insurance life and non-life

business

13Cattolica Group

Organic growth: multi-channel developmentB

USI

NES

S/SE

RVI

CE

LIN

ES

Tied agents Banks Brokers Other channels

CHANNELS

Non-Life

Life

Financial services and asset management

• Agency network develop-ment

• Product and channel innova-tion (TUA)

• Retail segment

• Selective corporate expansion

• Focus on profitability

• Penetration on preferred segments

• Social security

• Expansion of parent company units for direct assumption of corporate risks

• Private retail segment• Standard products• JV with BPVN and other

business/ partnerships agreements (OnLineDivision)

• “Flexible” confirmation of the JV model

• Protection/development of strategic commercial contracts

• Product and segment innovation

• Re-launch of Cattolica Aziende

• Focus and selection of middle size, high-contribu-tionbrokers

• Axa-Cattolica

• Middle company segment (B2B2E)

• Direct channel for corporate contracts

• Development of “preferred multi-mandatory” distribution

• FAs working inside agencies: Cattolica Investimenti SIM

• Cross-selling at sales outlets

• Banking partnerships to increase multi-bank financial products with specific proprietary brands

• Development of Cattolica Investimenti SIM model• Institutional Asset management: Verona Gestioni

SGR

14Cattolica Group

Agencies network development

Agency network development(1999 - 2003; no. agencies)

Proprietary agency network

546

900 974 1,024 1,049

1999 2000 2001 2002 2003

1,092

709

364

19

2004

+4,1%+4,1%

1,357

2005

382

732

187

56

+24.3%

Multi-mandatory agency network (number of agencies)

138 Eurosav multi-mandatory agencies as at 31 December 2005, which will sell non-life products starting in 2006.

2007E

1,523

15Cattolica Group

Agency network in 2005

Proprietary agency network

Number of proprietary agencies

14

7419

1574171

68

6623

291648

6511

65

33

38

69

1.3571.357

N: 704C: 371S: 28293

255 144

22

133

9223

49

14255

10

39

6017

73

42

51

3

38

16

27%

21%

52%

Multi-mandatory agency network

Number of multi-mandatory agencies

1474

191574

17168

6623

291648

6511

65

3338

69

138138

N: 66C: 26S: 4610

25 8

22

13

43

6

112

261

7

1

11

10

19%

33%

48%

Group integrated agency network

Number of total agencies

1474

191574

17168

6623

291648

6511

65

3338

69

1.4951.495

N: 770C: 397S: 328103

280 152

22

146

9626

55

15357

10

39

8618

80

43

62

3

48

16

27%

21%

52%

16Cattolica Group

Bancassurance consolidation

Cattolica Group bank branches distribution:

2,913 branches Market share of 9.3% in Italy

1474

191574

17168

6623

291648

6511

65

38

Market share 6.0%

Market share 6.6%

Market share 11.4%

December 2005Renewal until 2010 of Cattolica and Banca Lombarda agreementBusiness and commercial agreement

Cattolica Group insurance products will continue to be sold via the 796 bank branches and 578 Financial advisors of Banca Lombarda

Confirmation of Lombarda Vita activity: the joint-venture founded in 2000, 50.1% owned by Cattolica and 49.9 by Banca Lombarda

Non-life bancassurance - During 2006 a new joint-venture with Banca Lombarda Group will be set up for the sale of non-life products through the bank partner’s distribution network

17Cattolica Group

Non-Life Bancassurance development

A strategic opportunity in Italian Market

Mission: – Meet the increasing demand for Non-Life insurance from the

family segment– Use the commercial and operative synergies between the

insurance and banking partners– Guarantee customers consultancy services suitable to

different needs

Cattolica Group Non-Life Bancassurance development: maximise competitive advantage and optimise the

combination of Life Bancassurance experiences and Non-Life technical skills

Start-up of the new 50/50 JV with the Group Banco Popolare di Verona e Novara

Extend Non-Life Insurance activities to other Banking GroupsConsolidate the operations of the Cattolica Online Division (development of the agreement with ICCREA)Products: Motor TPL, fire, theft, simple general TPL, injury and healthTarget: Bank retail customersAssistance: dedicated call centerClaims settlement managed directly by Cattolica structure

In Italy Bancassurance business in the non-life sector is poorly developed, with a share of just 1%, whilst market share turns out higher in other European countries: in Germany it is 5%, in the Netherlands and France it is 8%

18Cattolica Group

UniOne acquisition

Relative young company, born in 1984, from 2000 in Generali Group

Agency network focused on P&C business, based most of them in middle and south Italy

Motor Transportation business is 86% of total premiums

Claims settlement network complementary to existing Cattolica network

High potential in life business which is a recent start-up

100%

UniOne history In 2006 – Plan of incorporation in DuomoAssicurazioni in order to increase the level of integration and profitability of non-life business generated via the single-card agency networkcreation of a strong non-life unit with 569 proprietary agencies

End 2005 – UniOne Vita integration into Duomo Previdenza and following “multi-mandatory agencies” branch of business transfer from Eurosav to UniOne Vita

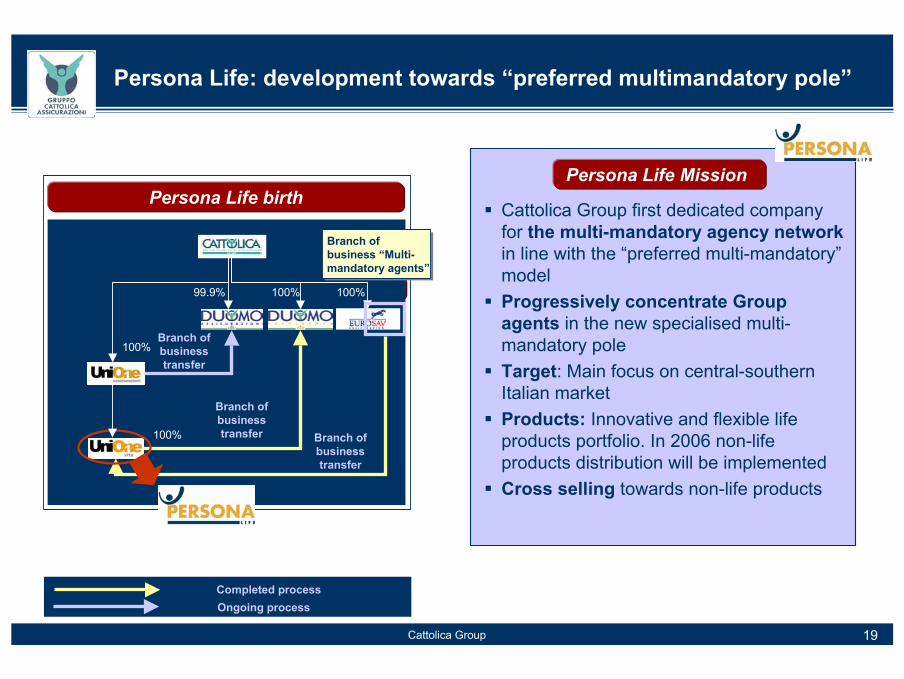

Persona Life birth: UniOne Vita new denomination; the first Group company dedicated to multi-mandatory agency network

Restructuring and Integration process

19Cattolica Group

Persona Life: development towards “preferred multimandatory pole”

Cattolica Group first dedicated company for the multi-mandatory agency network in line with the “preferred multi-mandatory” modelProgressively concentrate Group agents in the new specialised multi-mandatory poleTarget: Main focus on central-southern Italian marketProducts: Innovative and flexible life products portfolio. In 2006 non-life products distribution will be implementedCross selling towards non-life products

Persona Life birth

Set up a Cattolica Group Pole for “preferred multi-mandatory” distribution (see the French experience)

TARGET

100%

99.9% 100%

Branch of business transfer

100%

100%

Branch of business “Multi-mandatory agents”

Branch of business transfer Branch of

business transfer

Persona Life Mission

Completed processOngoing process

20Cattolica Group

Completing Life Operations restructuring

MAIN OBJECTIVES

merger

merger

Life operations restructuringSpecialize companies by business area

and distribution channel

• R&P: center of excellence in bankinsurance agreements

– Scope economies (products, commercial initiatives)

– Scale economies (IT, back-office and other operations)

• Cattolica: set-up of a Group Pole for Life Business through all tied agency networks

– Scope economies (products, commercial initiatives)

– Scale economies (IT, back-office and other operations)

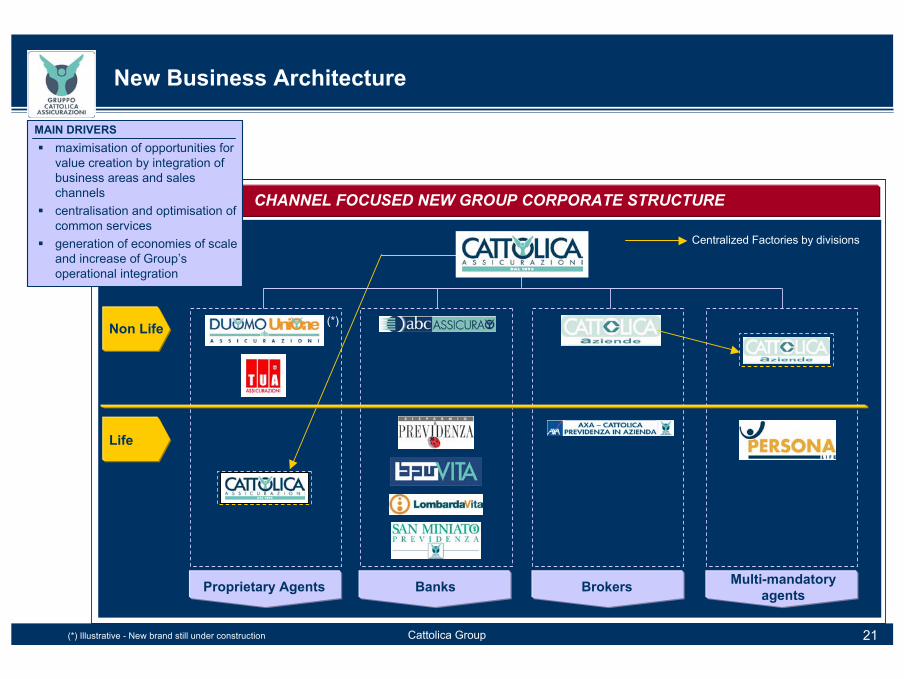

21Cattolica Group

New Business Architecture

Proprietary Agents Banks Brokers Multi-mandatoryagents

Centralized Factories by divisions

Non Life

Life

(*) Illustrative - New brand still under construction

(*)

CHANNEL FOCUSED NEW GROUP CORPORATE STRUCTURE

maximisation of opportunities for value creation by integration of business areas and sales channels centralisation and optimisation of common servicesgeneration of economies of scale and increase of Group’s operational integration

MAIN DRIVERS

22Cattolica Group

Agenda

Cattolica Group at a glance

Strategic framework and strategy implementation

Business growth and value creation

23Cattolica Group

Development of consolidated premiums

2005

1.542

3.646

5.188

2005 Result***

70%

30%

(*) With the inclusion of indirect business (**) Only direct business ( ***) IAS/IFRS results with the inclusion of investments contracts

Change % 2005/2004

525 7561,053 1,267 1,392

917

2,012

2,2982,464

2,820

1999 2000 2001 2002 2003

1,442

2,768

3,3513,731

4,212

Gross Consolidated Premiums Direct and indirect business (IT GAAP)

(1999 - 2004; Euro mn)

73%64% 69% 66% 67%Non-lifeLife

Breakdown

27%36% 31% 34% 33%

Life

Non-life(*)

1,420

3,197

2004

4,617

69%31%

23.8%23.8%

With the inclusion of Investments contract s

for € 327 mn

+9.1%**+9.1%**

+14.1%+14.1%

+12.4%+12.4%

2007E

2,010

3,499

5,510

64%

36%

2007 TargetCAGR04/07

6%6%

3%3%

12%12%

Note: 2007 Premiums IT GAAP

CAGR99/05

24Cattolica Group

Non-life business

2003

1,3981,523

2004 2005

9.1%9.1%(Direct business - Euro mn)

Premiums(Direct business - Euro mn)

2005 Non-Life business mix

Motor65%

Non-motor35%

(Direct business - Euro mn)

Non-Life business mix

1,3981,523

996938

527460

9.1%9.1%

2004 2005

Motor

Non-motor+14.8%+14.8%

+6.3%+6.3%

2005 significant growth of more profitable business lines:

Health at 58 mn (+ 14.5%)

Accident at 105 mn (+ 15.4%)

Fire at 88 mn (+ 8.6%)

25Cattolica Group

Life business

3,1973,646

2004 2005

(Direct business - Euro mn)

Life business collection

14.1%14.1%

With the inclusion of Investments

contract s for € 327 mn

(Direct business - Euro mn)

2005 Life business mix

Traditional48.8%

Index32%

Unit16.4%

Class VI2.8%

2.981

3.428

2004 2005

+15%+15%(Direct business - Euro mn)

Life new business collection

2004 2005

50.4%

9.7%

39.8%

Index

Unit

Traditional

34.4%

16.5%

12.8%49.1%

(Direct business)

Mix by type of product

26Cattolica Group

Development of consolidated net profit

2005 Result **Consolidated net profit 1999-2004 *( Euro mn)

26

4753

63

125

1999 2000 2001 2002 2003

Group net profit 25 44 46 57 116

150

2004

136

2005

139

115

2007 Target*CAGR04/07

2007E

176

162

5,5%5,5%

6%6%

(*) Italian GAAP results (**) IAS/IFRS result

27Cattolica Group

Development of dividend per share

Pay-out (Euro mln)

Other indicators

30 43 48

Dividend per share(1999-2004; Euro)

Dividend yield(1) 2.28% 3.60% 4.59% 3.50%

43(**)17

n.a.

Dividend 2005

2005

1.50

71

3.2%(***)

Cattolica dividend policy is consistent with the 3-year plan value creation program

+11%+11%

CAGR99/05

16%16%

18.8%18.8%Pay-out ratio (*) 76.5% 72.4%(3) 78.3%77.1 %(2)71.7% 69.6%

Fonti: Cattolica – Bilancio d’esercizio 2003 – Analisi interne(1) Dividend yield: Dividend per share/Official price of last day of the year (2) With the inclusion of extraordinary dividend (3) Pay out, net of property transfer (*) Pay-out at Parent Company level

(***) Calculated on a price per share of € 47.13 (as at 24.3.2006)

2000 2001 2002 2003

0.70

1.00 1.00 1.02

0.78

0.22

Extraordinary dividend

1 free share for every 10

1999

0.62

2004

1.35

64

3.98%60.2%

0.20

1.30

28Cattolica Group

Cattolica stock performance in 2005-2006

Source: Bloomberg

PERFORMANCE 2005-2006as at 24 March 2006

Cattolica +39.2%

MIB INS.

Mibtel

S&P/MIB

+24.9%

+23.1%

+27.6%

Change % 01/01/2005-24/03/2006

01/01/2005

Cattolica S&P/MIBMIB INS. MIBTEL

24/03/2006

Stock performance in comparisonwith the main indexes

29Cattolica Group

This document has been prepared by Cattolica Assicurazioni – based on data from internal sources (year-end financial statements, consolidated group financial statements, internal reporting and other company documentation, etc.) – for the sole purpose of providing information on the group’s results and future operating strategies. Given this, it can in no way be used as a basis for possible investment decisions. It is not a solicitation to buy or sell shares. No part of the document can be taken to be the cause of or reason for agreements or commitments of any type or kind whatsoever, nor can it be relied upon for agreements and commitments.Information contained in the document concerning forecasts has been prepared according to various assumptions and/or elements that might ultimately materialise differently to present expectations. Results might therefore change. Cattolica therefore in no way provides any guarantee, either explicit or tacit, as regards the integrity or accuracy of the information or opinions contained in the document, nor can any degree of reliability be attributed to the same, inasmuch as it has not been subjected to independent verification. Responsibility for use of the information and opinions contained in the document lies solely with the user. In any case Cattolica, within legally admissible limits, will not consider itself liable for any damages, direct or indirect, that third parties might claim due to utilisation of incomplete or inaccurate information. For any further information concerning Cattolica Assicurazioni and its related group, reference must be made exclusively to the information given in the annual, quarterly, and interim reports and financial statements. The full versions of these documents, which constitute the factual basis and proof for all legal purposes, are lodged at the company’s registered offices and are available to anyone requesting them. Reproduction or full or partial publication and distribution of the information contained herein to third parties is prohibited. Acceptance of the present document automatically signifies recognition of the aforesaid constraints.

DISCLAIMER

30Cattolica Group

Borsa ItalianaItalian Investor Conference 2006

New York, 3-4 April 2006

Cattolica Group:Strategy and Results

Giulio Fezzi - Chief Financial Officer and IR ManagerAndrea Battista - General Manager Duomo Assicurazioni and IR

![VITTORIA ASSICURAZIONI FINAL 2.ppt [modalità compatibilità] · Microsoft PowerPoint - VITTORIA ASSICURAZIONI FINAL_2.ppt [modalità compatibilità] Author: v_rispo Created Date:](https://img.pdfslide.us/doc/110x75/5ee0d282ad6a402d666beb12/vittoria-assicurazioni-final-2ppt-modalit-compatibilit-microsoft-powerpoint.jpg)

![Diploma Supplement Giurisprudenza Universita Cattolica[2305843009213743626]](https://img.pdfslide.us/doc/110x75/589a21561a28ab2a678b6b51/diploma-supplement-giurisprudenza-universita-cattolica2305843009213743626.jpg)