Embed Size (px)

Citation preview

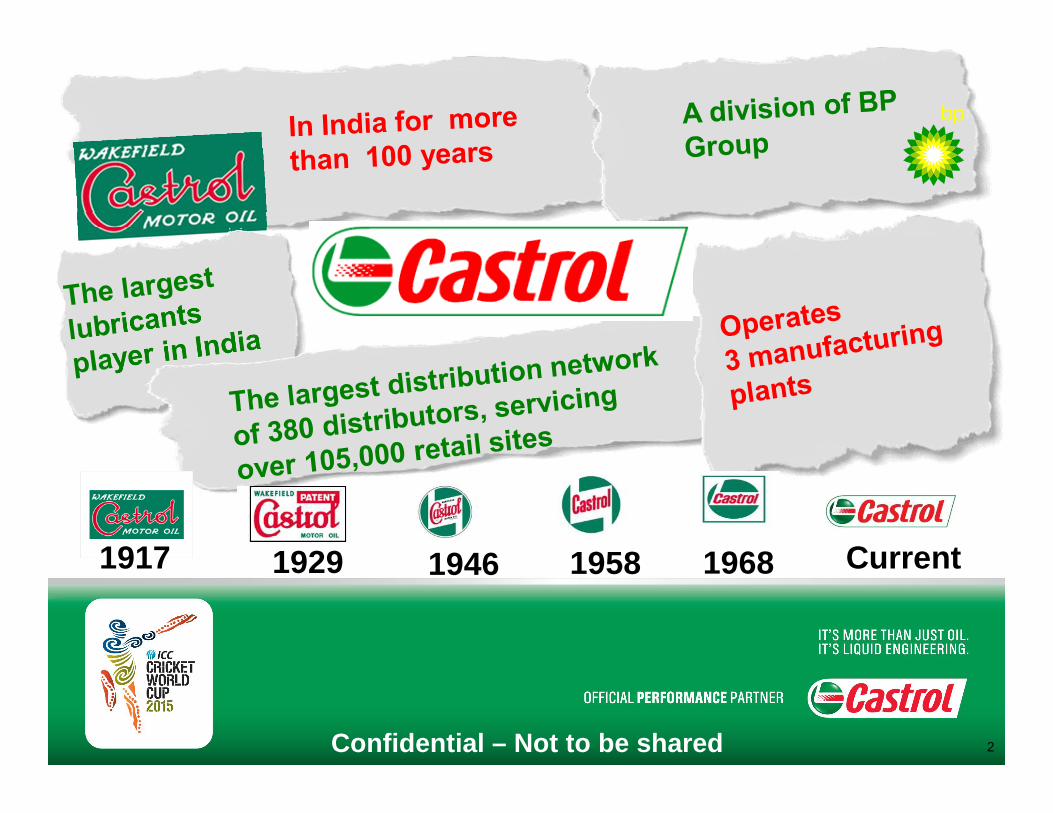

Castrol IndiaAnalyst Meeting - 2014

Confidential – Not to be shared

1917 1929 1946 1958 1968 Current

Confidential – Not to be shared 2

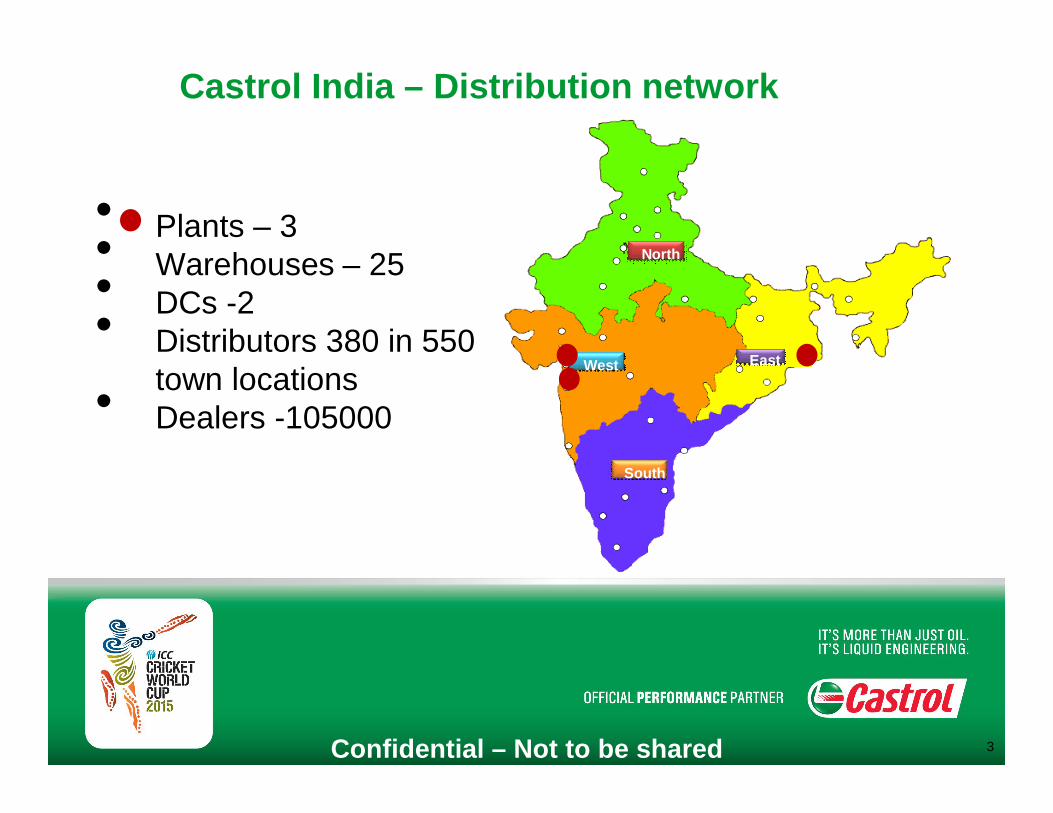

Castrol India – Distribution network

• Plants – 3 • Warehouses – 25• DCs -2 • Distributors 380 in 550 town locations• Dealers -105000

AS-IS

North

South

West East

Plants - 3Warehouses – 25DCs- 2

AS-IS

NorthNorth

SouthSouth

WestWest EastEast

Confidential – Not to be shared 3

Our Strategy & Strengths

Confidential – Not to be shared 4

Our Products & BrandsCastrol Activis the Largest selling brand in the two wheeler oil segment

Castrol GTX is the largest selling engine oil brand in the car segment

CRB Plus is the largest selling diesel engine oil in the country

Confidential – Not to be shared 5

How do we win1. Lead charge in personal mobility2. Drive premiumization3. Develop superior franchise

workshop offers 4. Win with key global OEMs5. Accelerate IWS agenda

Our Growth Strategy- Winning in India

Enablers1. New RTM2. Build People capability 3. Build Process capability4. Technology Leadership5. Agile and Efficient Supply Chain

Confidential – Not to be shared 6

Great Participation

Choices

Differentiated Marketing

Pioneering Technology

People

Winning with OEM’s

We want to be the profitable growth engine leading the drive to synthetisation and ensure protection to every third engine sold in India.

Confidential – Not to be shared 7

Affordability

Middle Kingdom

Availability

Distribution Expansion

Rural

Advantage

Focus Brands

Advocacy

Certified Engine

Expert Club (CEEC)

Bike Points

Focus on the 4 As

Confidential – Not to be shared 8

Enduring Relationships - Consumers

Confidential – Not to be shared 9

Enduring Relationships - Consumers

Confidential – Not to be shared 10

Enduring Relationships - Customers

Confidential – Not to be shared 11

Enduring Relationships - OEMs

Confidential – Not to be shared 12

Enduring Relationships – OEMs

Confidential – Not to be shared 13

Liquid Engineering Centre InaugurationAt Maruti Suzuki – Gurgaon PlantJuly’2014Co-sponsored by Castrol

2013 Key Highlights

OEM’s Aggressive Account Acquisition

GeostructureShipbuilding

Confidential – Not to be shared 14

Continuous Innovation - Products

Confidential – Not to be shared

1st

Diesel engine oil with

Synthetic technology

15

1st

MultigradeDiesel engine

oil

1st

API CF-4 Diesel engine

oil

1st

dedicated 2-stroke Motor

cycle oil

1st

Gel grease

Continuous Innovation – Products

Confidential – Not to be shared

Increased fuel efficiency of TATA trucks by 1.5%

First diesel engine oil to be recommended for fuel efficiency by an OEM

Increased fuel efficiency of TATA trucks by 1.5%

First diesel engine oil to be recommended for fuel efficiency by an OEM

16

Continuous Innovation - Packaging

Confidential – Not to be shared

Award winning standee pouch

Pouch pack

Blister packRolla pack

Unique anti-counterfeit features

17

Strong Brands

Confidential – Not to be shared 18

New Product Launch

19

Continuous Innovation – Route to Market

Confidential – Not to be shared

Castrol Point

Retail Transformation

Creation of “Bazaar” Trade

20

21

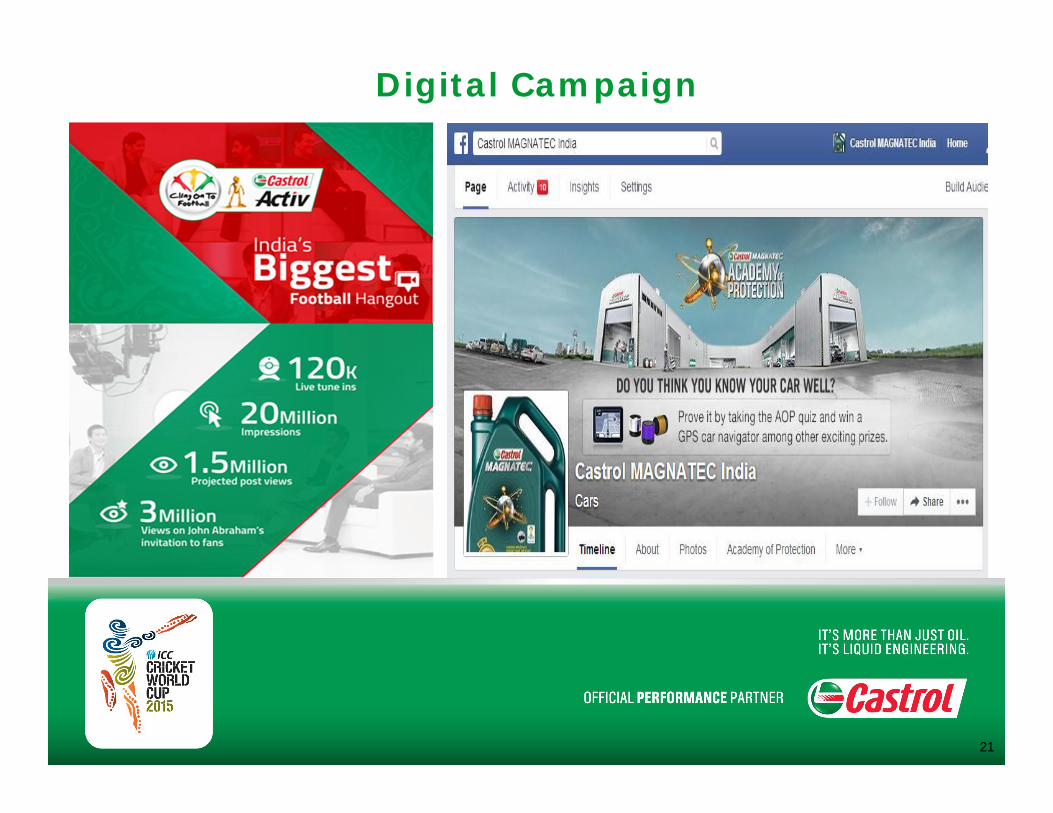

Digital Campaign

22

Awards & Recognition

• Castrol CEO ranked amongst Top 100 CEOs by Business Today-PWC -2013

• Won the top Indian company award under the sector Specialty Oils and Lubricants at the D & B Corporate Awards - 2014.

• Good Road safety project won Black Elephant Kyoorius Advertising & Digital Awards - 2014

• Paharpur Plant awarded 14th Annual Greentech Environment Award in Silver Category in Petrochemical Sector - 2013

• Patalganga Plant won Certificate of Merit from the National Safety Council Maharashtra Chapter for Zero Accident Frequency Rate - 2013

People Our Strength

Winning for investors Winning vs competition

Winning in the market

Winningfor our people

Win with Customers

Confidential – Not to be shared 23

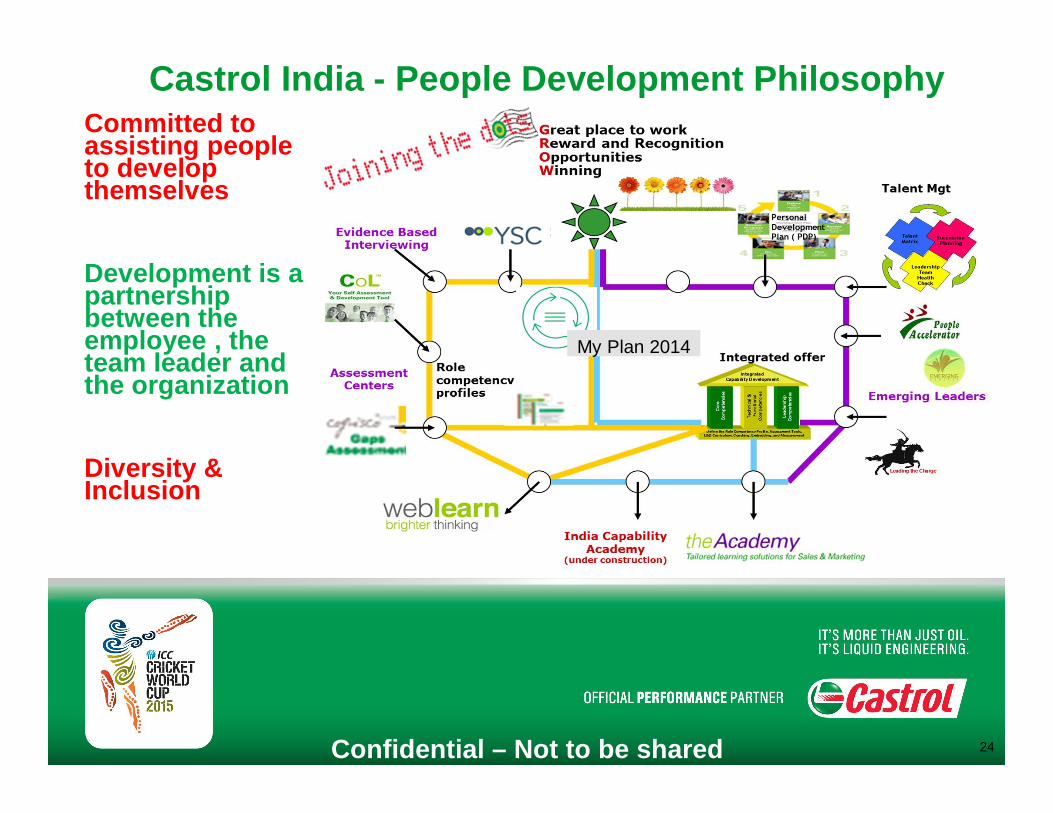

Castrol India - People Development PhilosophyCommitted to assisting people to develop themselves

Development is a partnership between the employee , the team leader and the organization

Diversity & Inclusion

My Plan 2014

Confidential – Not to be shared 24

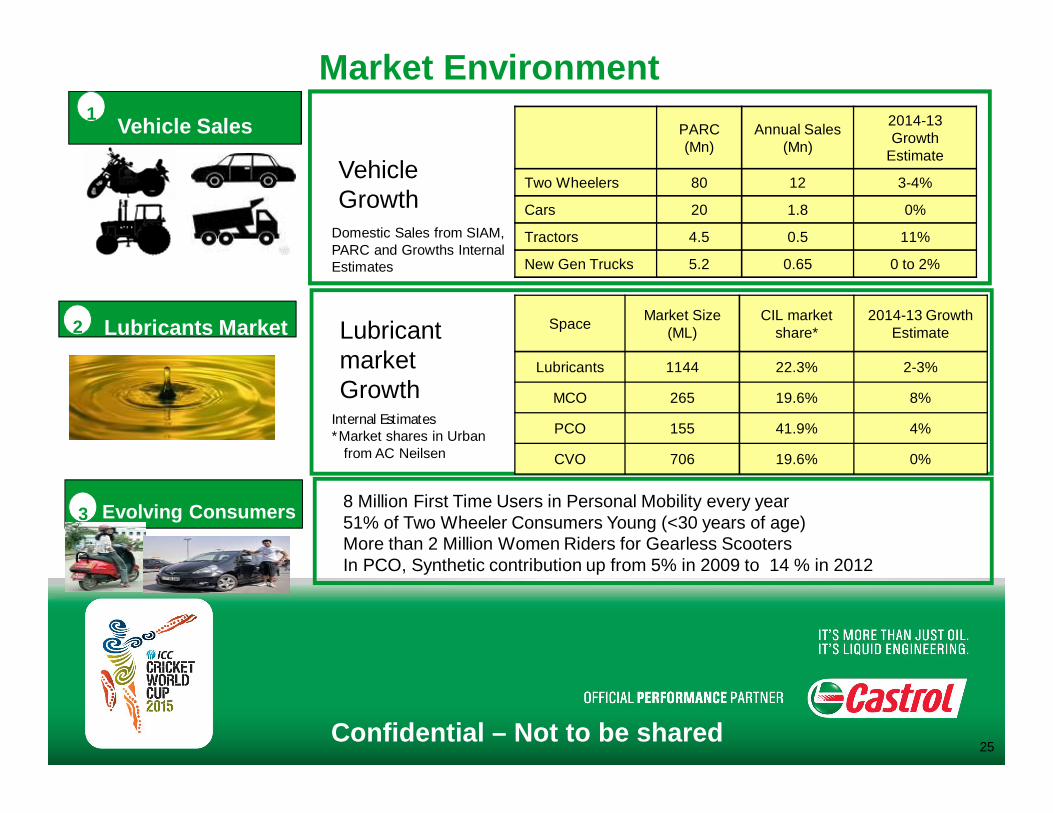

Market Environment

8 Million First Time Users in Personal Mobility every year51% of Two Wheeler Consumers Young (<30 years of age)More than 2 Million Women Riders for Gearless ScootersIn PCO, Synthetic contribution up from 5% in 2009 to 14 % in 2012

Lubricants Market2

Evolving Consumers3

Lubricant marketGrowth

Vehicle Growth

Vehicle Sales1

Domestic Sales from SIAM, PARC and Growths Internal Estimates

Space Market Size (ML)

CIL market share*

2014-13 Growth Estimate

Lubricants 1144 22.3% 2-3%

MCO 265 19.6% 8%

PCO 155 41.9% 4%

CVO 706 19.6% 0%

PARC (Mn)

Annual Sales (Mn)

2014-13 Growth

Estimate

Two Wheelers 80 12 3-4%

Cars 20 1.8 0%

Tractors 4.5 0.5 11%

New Gen Trucks 5.2 0.65 0 to 2%

Internal Estimates*Market shares in Urban

from AC Neilsen

Confidential – Not to be shared25

Value to Shareholders

Confidential – Not to be shared 26

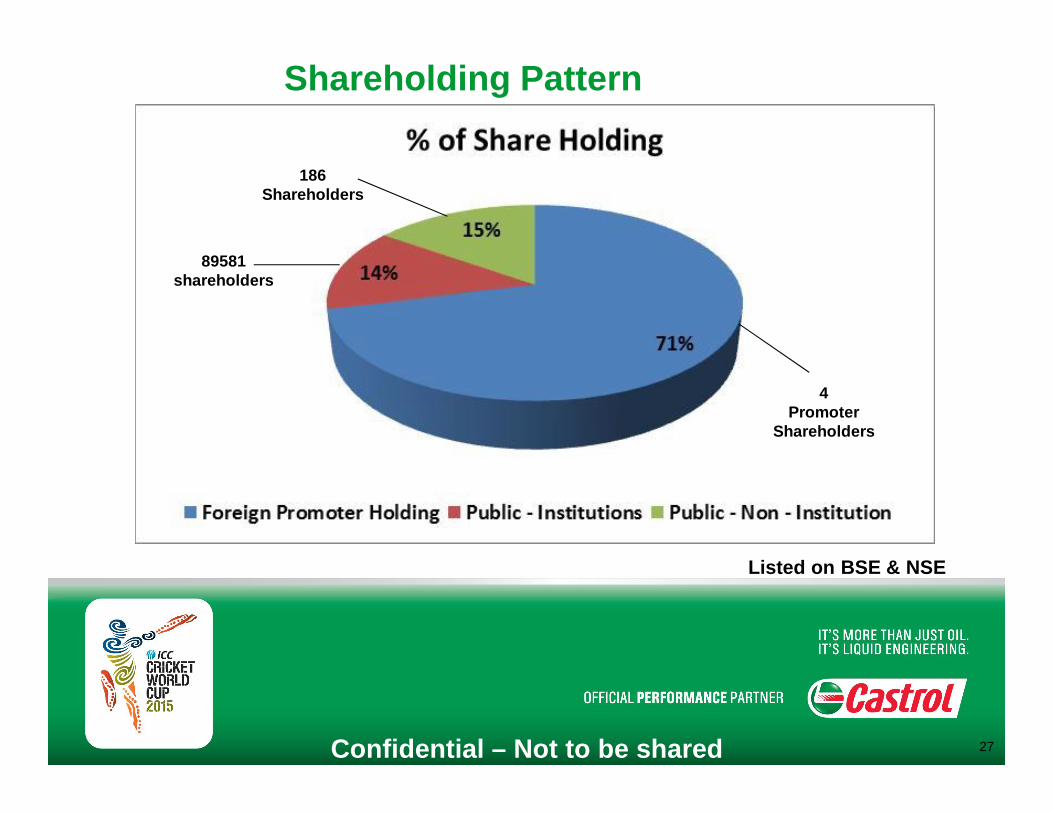

Shareholding Pattern

Listed on BSE & NSE

Confidential – Not to be shared 27

186 Shareholders

89581shareholders

4Promoter

Shareholders

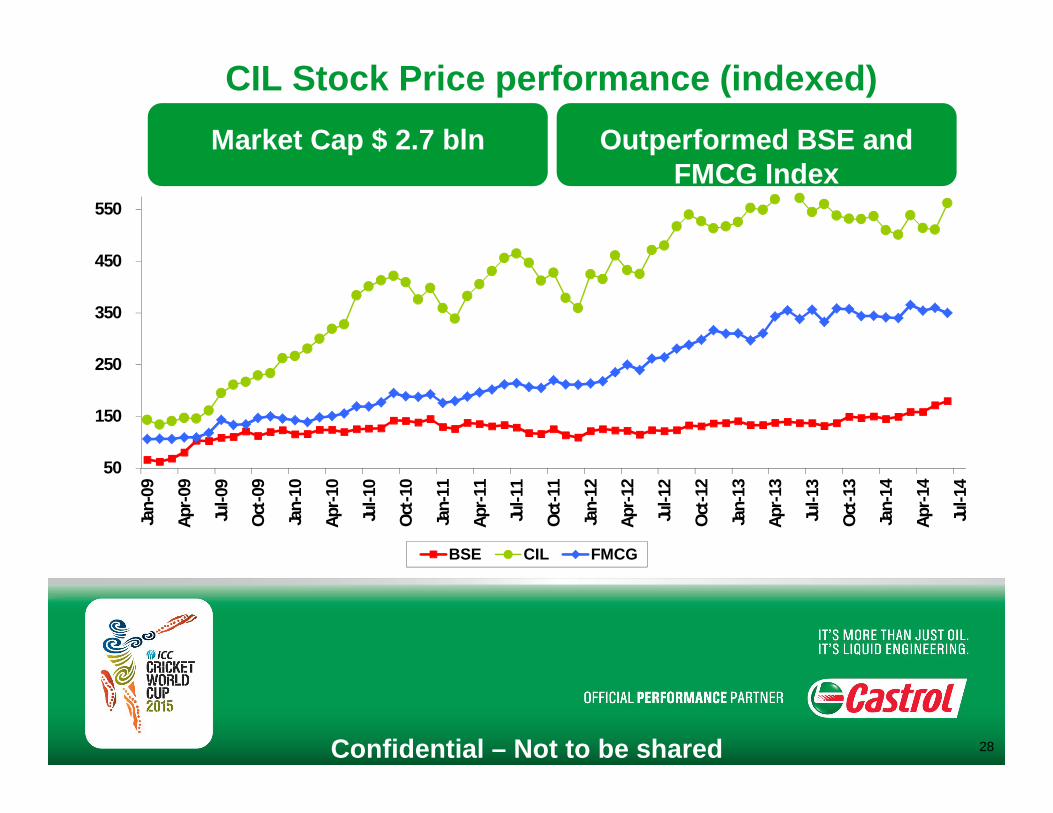

CIL Stock Price performance (indexed)Outperformed BSE and

FMCG Index

Confidential – Not to be shared

50

150

250

350

450

550

Jan-

09

Apr-

09

Jul-0

9

Oct

-09

Jan-

10

Apr-

10

Jul-1

0

Oct

-10

Jan-

11

Apr-

11

Jul-1

1

Oct

-11

Jan-

12

Apr-

12

Jul-1

2

Oct

-12

Jan-

13

Apr-

13

Jul-1

3

Oct

-13

Jan-

14

Apr-

14

Jul-1

4

BSE CIL FMCG

28

Market Cap $ 2.7 bln

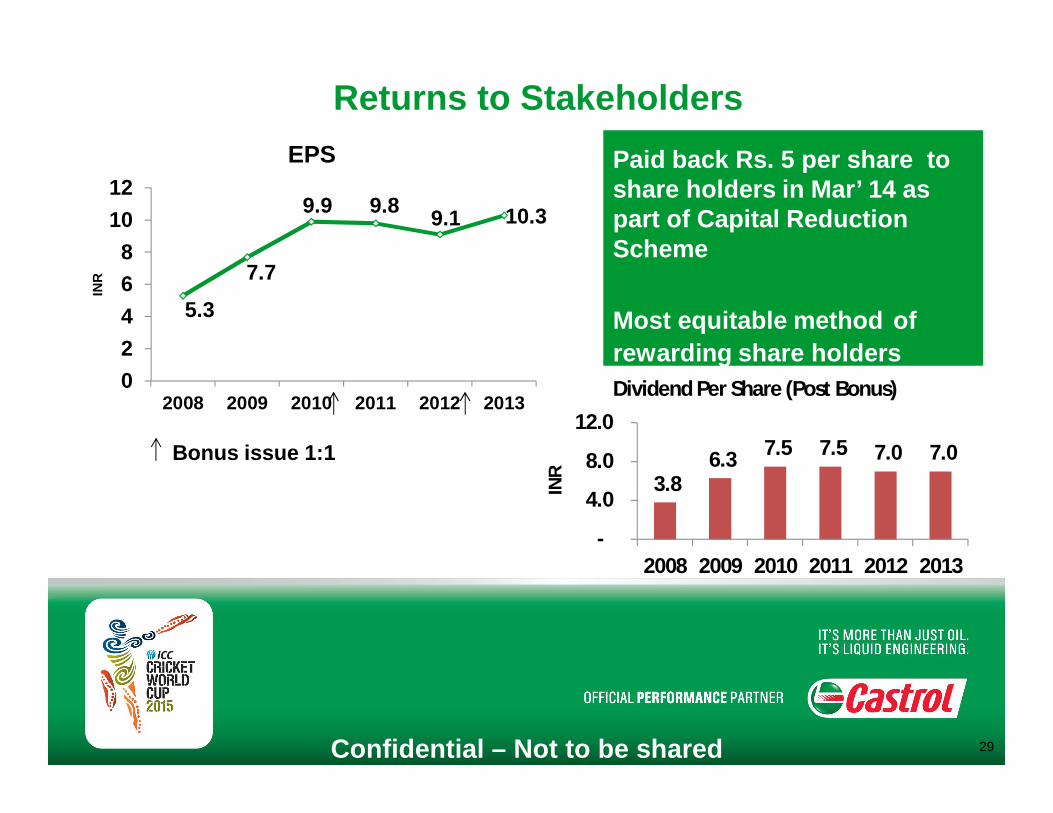

Returns to Stakeholders

Bonus issue 1:1

Paid back Rs. 5 per share to share holders in Mar’ 14 as part of Capital Reduction Scheme

Most equitable method of rewarding share holders

5.3

7.7

9.9 9.8 9.1 10.3

02468

1012

2008 2009 2010 2011 2012 2013

INR

EPS

3.8 6.3 7.5 7.5 7.0 7.0

-

4.0

8.0

12.0

2008 2009 2010 2011 2012 2013IN

R

Dividend Per Share (Post Bonus)

Confidential – Not to be shared 29

-

100

200

300

400

500

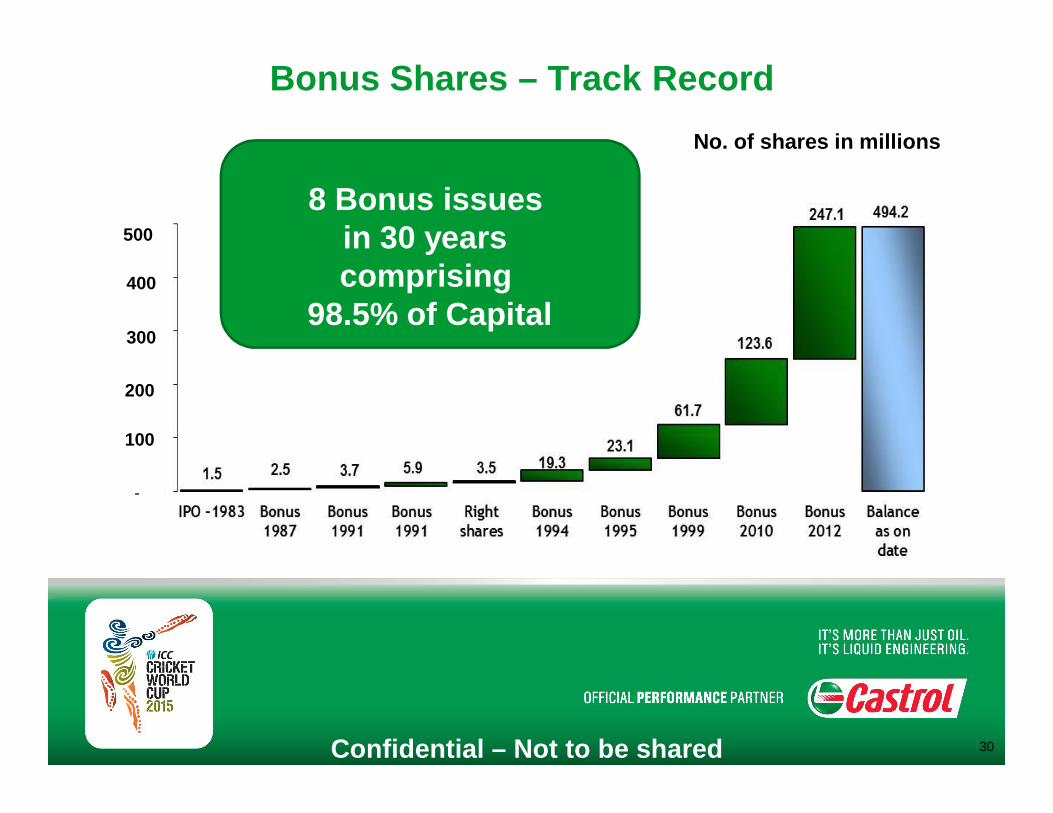

Bonus Shares – Track RecordNo. of shares in millions

8 Bonus issues in 30 years comprising

98.5% of Capital

Confidential – Not to be shared 30

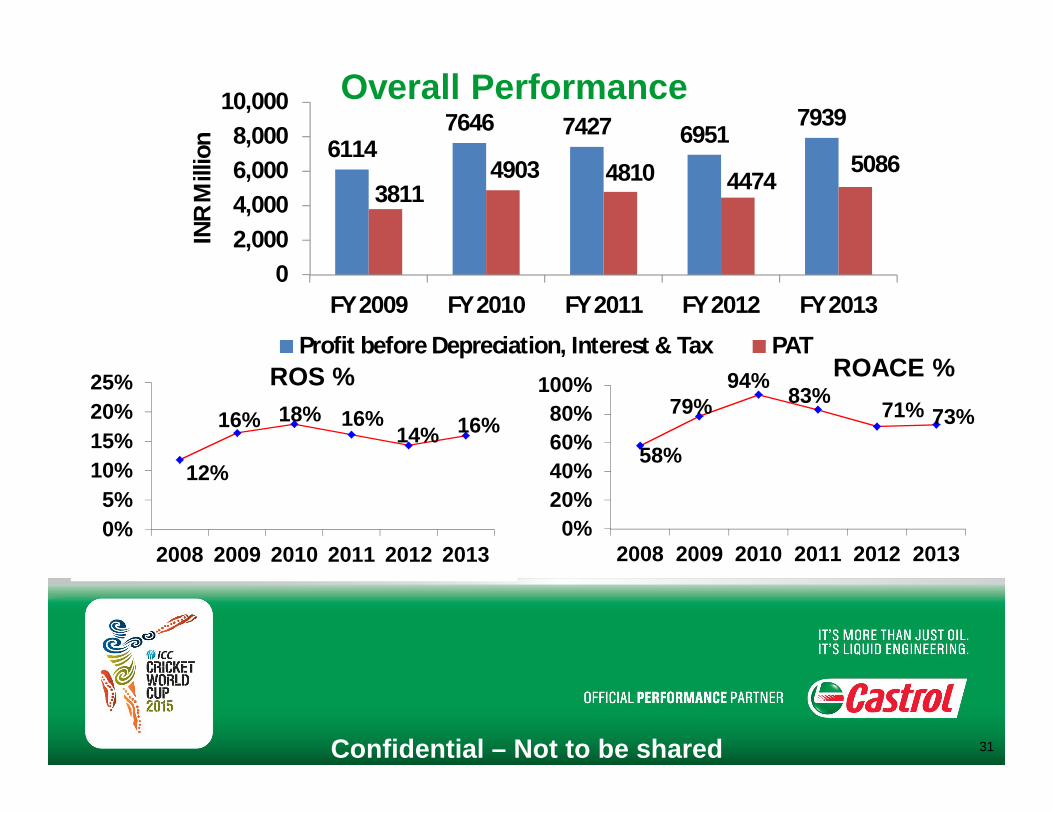

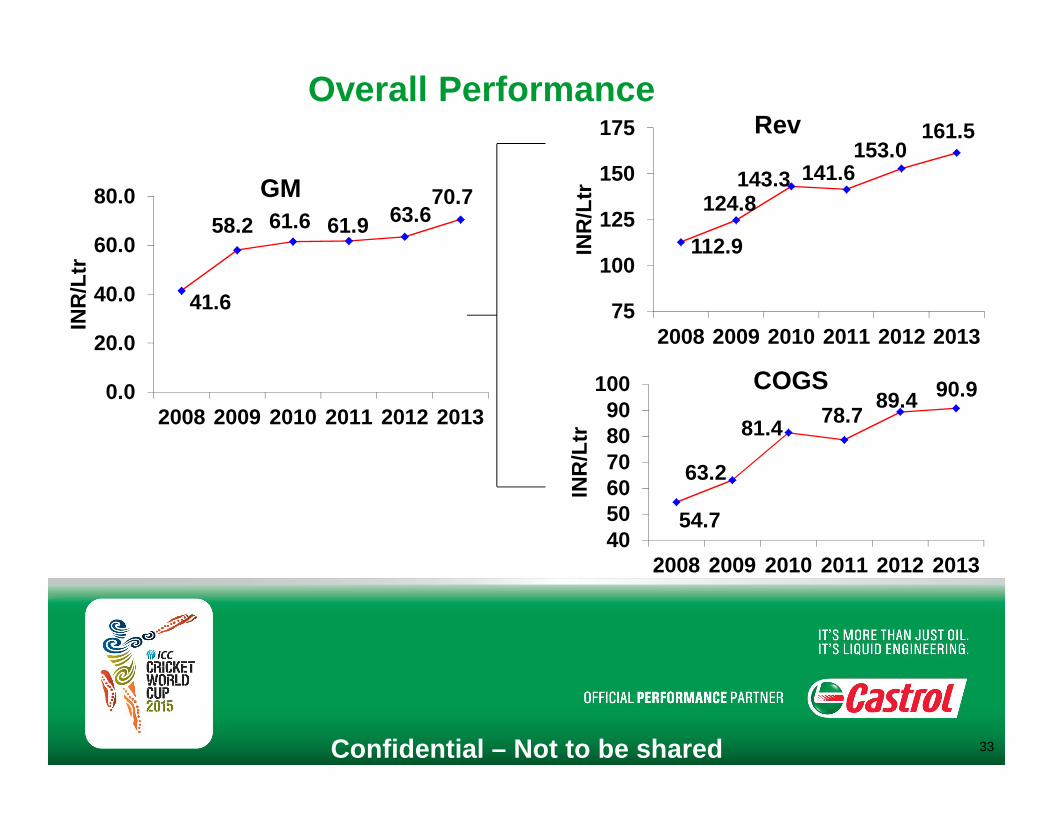

Overall Performance

Confidential – Not to be shared

12%

16% 18% 16%14% 16%

0%5%

10%15%20%25%

2008 2009 2010 2011 2012 2013

ROS %

58%

79%94%

83% 71% 73%

0%20%40%60%80%

100%

2008 2009 2010 2011 2012 2013

ROACE %

61147646 7427 6951

7939

38114903 4810 4474

5086

02,0004,0006,0008,000

10,000

FY 2009 FY 2010 FY 2011 FY 2012 FY 2013

INR

Mill

ion

Profit before Depreciation, Interest & Tax PAT

31

Overall Performance

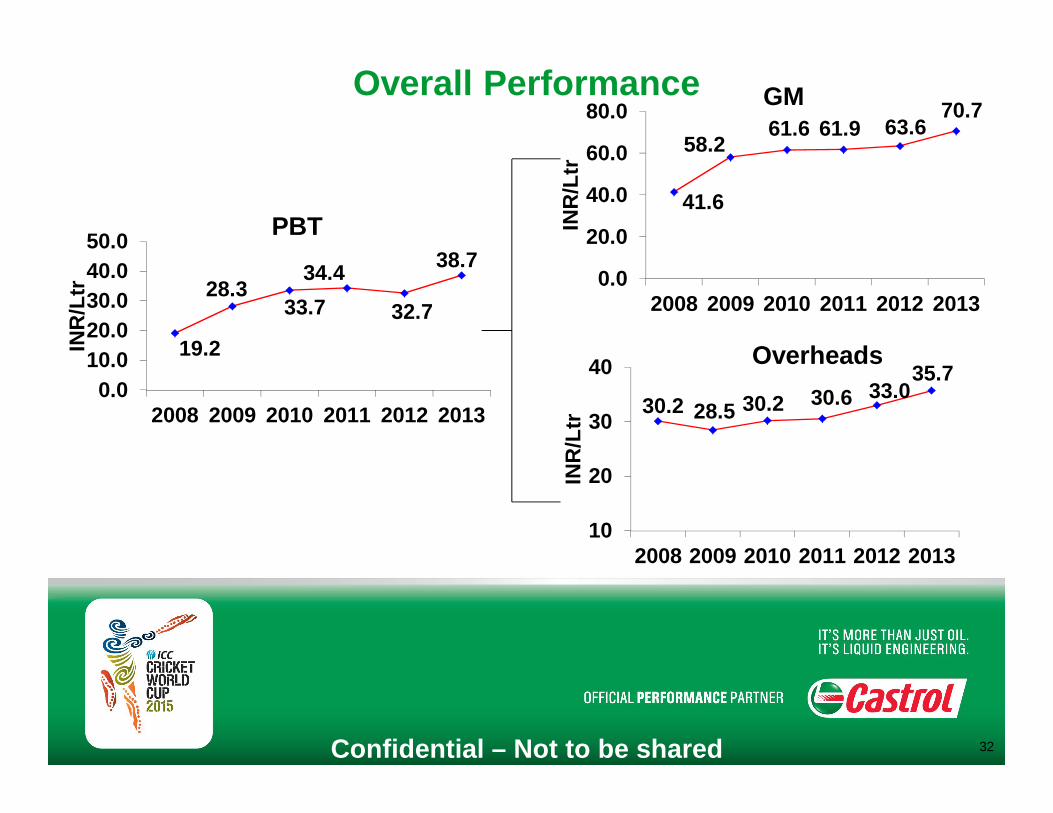

Confidential – Not to be shared

19.2

28.3 33.7

34.4

32.7

38.7

0.010.020.030.040.050.0

2008 2009 2010 2011 2012 2013

INR

/Ltr

PBT 41.6

58.2 61.6 61.9 63.6

70.7

0.0

20.0

40.0

60.0

80.0

2008 2009 2010 2011 2012 2013

INR

/Ltr

GM

30.2 28.5 30.2 30.6 33.0 35.7

10

20

30

40

2008 2009 2010 2011 2012 2013IN

R/L

tr

Overheads

32

Overall Performance

Confidential – Not to be shared

41.6

58.2 61.6 61.9 63.6 70.7

0.0

20.0

40.0

60.0

80.0

2008 2009 2010 2011 2012 2013

INR

/Ltr

GM

112.9

124.8 143.3 141.6

153.0 161.5

75

100

125

150

175

2008 2009 2010 2011 2012 2013

INR

/Ltr

Rev

54.7

63.2

81.4 78.7 89.4 90.9

405060708090

100

2008 2009 2010 2011 2012 2013IN

R/L

tr

COGS

33

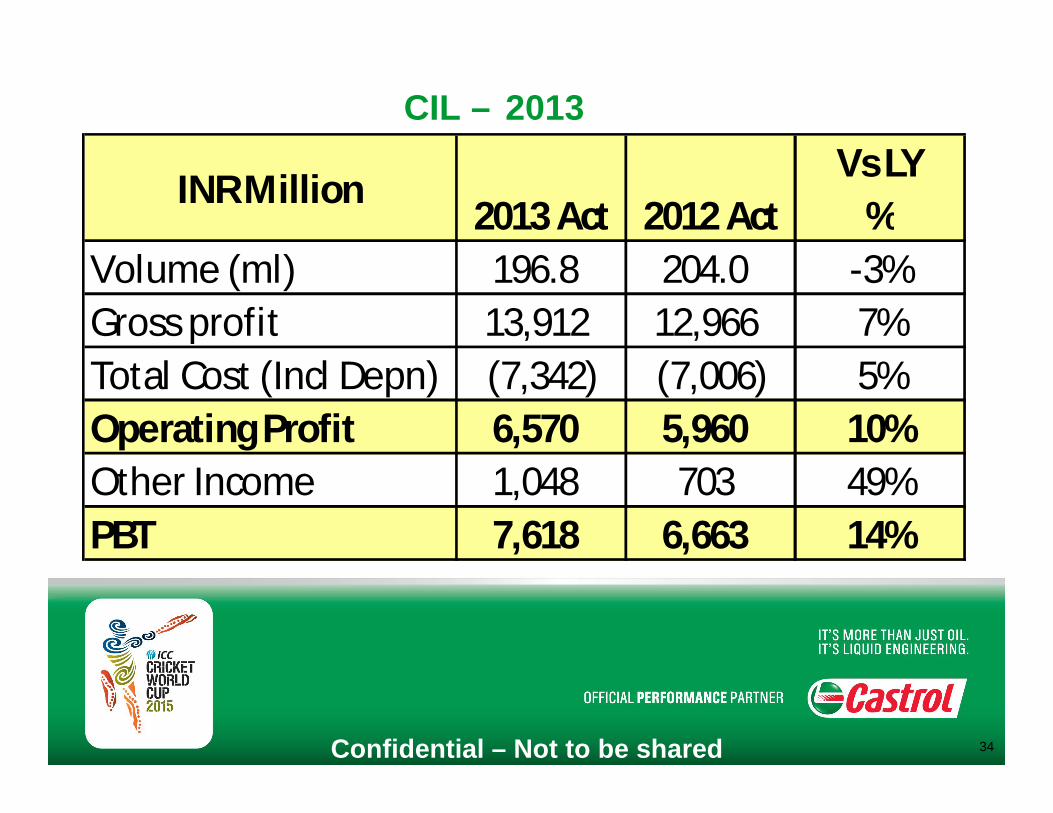

CIL – 2013

INR Million2013 Act 2012 Act

Vs LY %

Volume (ml) 196.8 204.0 -3%Gross profit 13,912 12,966 7%Total Cost (Incl Depn) (7,342) (7,006) 5%Operating Profit 6,570 5,960 10%Other Income 1,048 703 49%PBT 7,618 6,663 14%

Confidential – Not to be shared 34

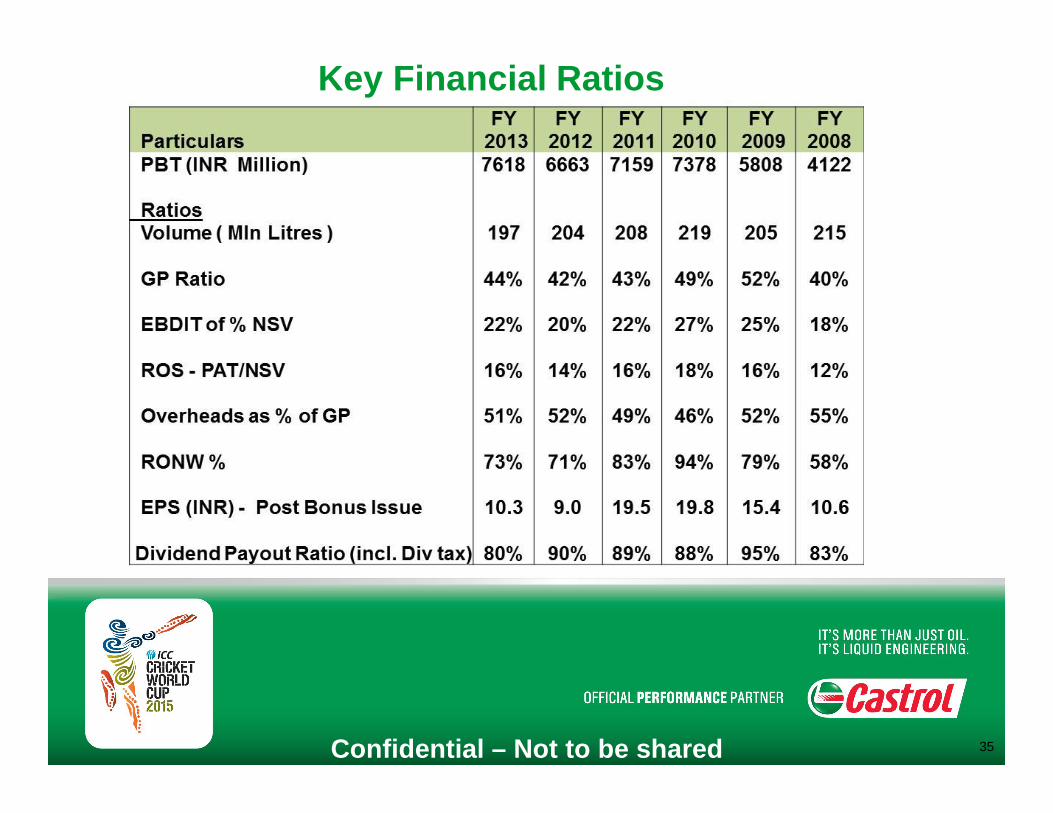

Key Financial Ratios

Confidential – Not to be shared 35

36

CSR Initiatives

Confidential – Not to be shared 36

Confidential – Not to be shared 37