Embed Size (px)

Citation preview

Canada Research Published by Raymond James Ltd.

Please read domestic and foreign disclosure/risk information beginning on page 29 and Analyst Certification on page 28. Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

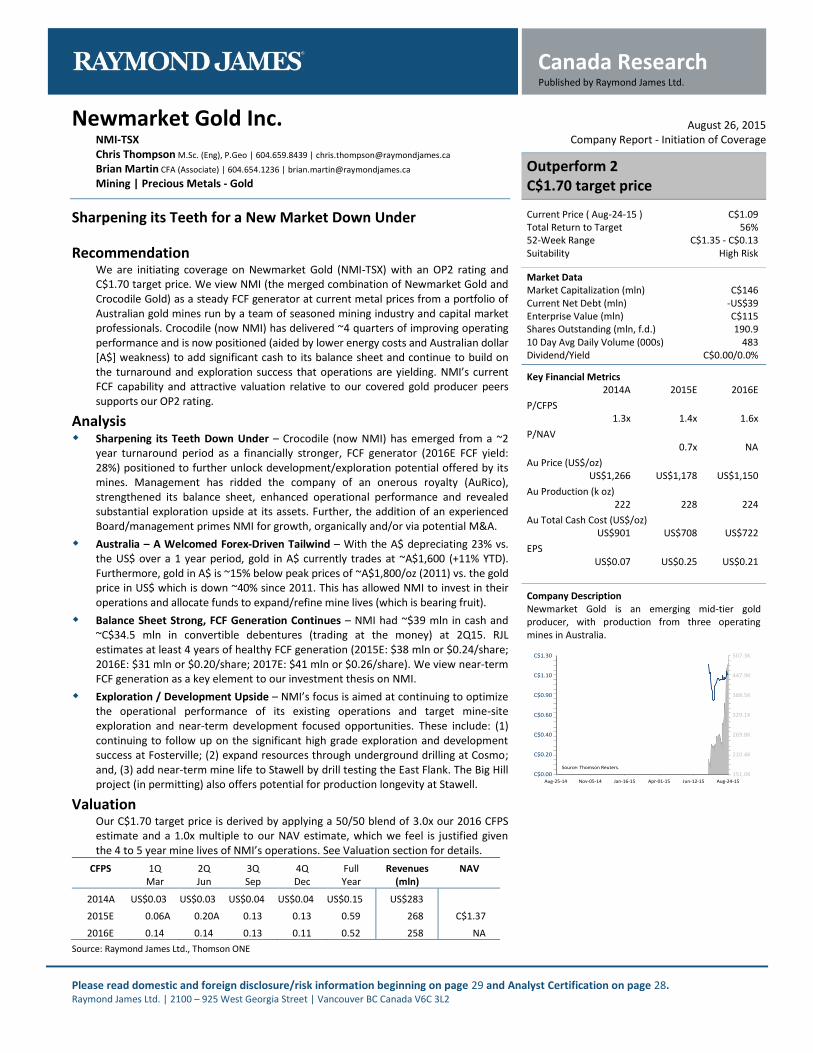

Newmarket Gold Inc. August 26, 2015 NMI-TSX Company Report - Initiation of Coverage Chris Thompson M.Sc. (Eng), P.Geo | 604.659.8439 | [email protected]

Brian Martin CFA (Associate) | 604.654.1236 | [email protected]

Mining | Precious Metals - Gold

Sharpening its Teeth for a New Market Down Under

Recommendation We are initiating coverage on Newmarket Gold (NMI-TSX) with an OP2 rating and C$1.70 target price. We view NMI (the merged combination of Newmarket Gold and Crocodile Gold) as a steady FCF generator at current metal prices from a portfolio of Australian gold mines run by a team of seasoned mining industry and capital market professionals. Crocodile (now NMI) has delivered ~4 quarters of improving operating performance and is now positioned (aided by lower energy costs and Australian dollar [A$] weakness) to add significant cash to its balance sheet and continue to build on the turnaround and exploration success that operations are yielding. NMI’s current FCF capability and attractive valuation relative to our covered gold producer peers supports our OP2 rating.

Analysis Sharpening its Teeth Down Under – Crocodile (now NMI) has emerged from a ~2

year turnaround period as a financially stronger, FCF generator (2016E FCF yield: 28%) positioned to further unlock development/exploration potential offered by its mines. Management has ridded the company of an onerous royalty (AuRico), strengthened its balance sheet, enhanced operational performance and revealed substantial exploration upside at its assets. Further, the addition of an experienced Board/management primes NMI for growth, organically and/or via potential M&A.

Australia – A Welcomed Forex-Driven Tailwind – With the A$ depreciating 23% vs. the US$ over a 1 year period, gold in A$ currently trades at ~A$1,600 (+11% YTD). Furthermore, gold in A$ is ~15% below peak prices of ~A$1,800/oz (2011) vs. the gold price in US$ which is down ~40% since 2011. This has allowed NMI to invest in their operations and allocate funds to expand/refine mine lives (which is bearing fruit).

Balance Sheet Strong, FCF Generation Continues – NMI had ~$39 mln in cash and ~C$34.5 mln in convertible debentures (trading at the money) at 2Q15. RJL estimates at least 4 years of healthy FCF generation (2015E: $38 mln or $0.24/share; 2016E: $31 mln or $0.20/share; 2017E: $41 mln or $0.26/share). We view near-term FCF generation as a key element to our investment thesis on NMI.

Exploration / Development Upside – NMI’s focus is aimed at continuing to optimize the operational performance of its existing operations and target mine-site exploration and near-term development focused opportunities. These include: (1) continuing to follow up on the significant high grade exploration and development success at Fosterville; (2) expand resources through underground drilling at Cosmo; and, (3) add near-term mine life to Stawell by drill testing the East Flank. The Big Hill project (in permitting) also offers potential for production longevity at Stawell.

Valuation Our C$1.70 target price is derived by applying a 50/50 blend of 3.0x our 2016 CFPS estimate and a 1.0x multiple to our NAV estimate, which we feel is justified given the 4 to 5 year mine lives of NMI’s operations. See Valuation section for details.

CFPS 1Q 2Q 3Q 4Q Full Revenues NAV Mar Jun Sep Dec Year (mln)

2014A US$0.03 US$0.03 US$0.04 US$0.04 US$0.15 US$283

2015E 0.06A 0.20A 0.13 0.13 0.59 268 C$1.37

2016E 0.14 0.14 0.13 0.11 0.52 258 NA

Source: Raymond James Ltd., Thomson ONE

Outperform 2 C$1.70 target price

Current Price ( Aug-24-15 ) C$1.09 Total Return to Target 56% 52-Week Range C$1.35 - C$0.13 Suitability High Risk

Market Data Market Capitalization (mln) C$146 Current Net Debt (mln) -US$39 Enterprise Value (mln) C$115 Shares Outstanding (mln, f.d.) 190.9 10 Day Avg Daily Volume (000s) 483 Dividend/Yield C$0.00/0.0%

Key Financial Metrics 2014A 2015E 2016E

P/CFPS 1.3x 1.4x 1.6x

P/NAV 0.7x NA

Au Price (US$/oz) US$1,266 US$1,178 US$1,150

Au Production (k oz) 222 228 224

Au Total Cash Cost (US$/oz) US$901 US$708 US$722

EPS US$0.07 US$0.25 US$0.21

Company Description Newmarket Gold is an emerging mid-tier gold producer, with production from three operating mines in Australia.

Canada Research | Page 2 of 32 Newmarket Gold Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Table of Contents

Investment Overview........................................................................................................................................... 3

Company Overview .............................................................................................................................................. 5

Valuation & Recommendation ............................................................................................................................ 15

Costs, Balance Sheet Strength & FCF Potential ................................................................................................... 17

Mine-Level AISC ................................................................................................................................................... 18

Profitability Index – Asset Level ........................................................................................................................... 19

Corporate Structure & Ownership ....................................................................................................................... 20

Appendix A: Management & Board of Directors ................................................................................................. 21

Appendix B: Financial Statements ....................................................................................................................... 23

Appendix C: Corporate Tearsheet........................................................................................................................ 25

Appendix D: RJL Gold Universe Comps ................................................................................................................ 26

Newmarket Gold Inc. Canada Research | Page 3 of 32

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Investment Overview

Newmarket Gold (NMI-TSX) offers a significant Australian domiciled gold production base (~200 k oz/year), a recent track record of improving operating economics, and a vehicle for a seasoned management team to exploit further potential M&A opportunities in the gold sector. The core asset strength of NMI is its three operating gold mines and a small portfolio of exploration assets located in Australia, acquired by merging with predecessor company Crocodile Gold (CRK).

NMI’s operating assets are the Fosterville and Stawell gold mines in the State of Victoria and the Cosmo gold mine in the Northern Territory, Australia. We view the Fosterville mine as providing the bulk of NMI’s near-term value (~50% of NAV) and near-term cash flow generating ability (~65% of mine-site EBITDA, ~50% of 2015E production), leveraging from recent exploration success and supported to a lesser (but still significant) degree by development/exploration upside offered at Cosmo and Stawell.

We view the recent business combination with Crocodile Gold favourably as we believe it combines a strong (and much improved) operating portfolio with a team of seasoned mining industry and capital market professionals in creating a platform for further consolidation in the gold sector. NMI’s management team is led by Douglas Forster (President and CEO) and a Board of Directors which includes Raymond Threlkeld (Chairman), Lukas Lundin, Chairman of Lundin Mining (LUN-TSX) and Randall Oliphant, Executive Chairman of New Gold (NGD-TSX). Management is actively seeking to fill the role vacated by Rodney Lamond (COO) who plans to resign for personal reasons effective September 15, 2015. Mr. Lamond was President and CEO of Crocodile Gold.

NMI has benefited significantly from a weakening Australian dollar (A$), which has depreciated 23% vs. the US$ over a 1 year period, resulting in gold in A$ currently trading at ~A$1,600 (+11% YTD). Furthermore, gold in A$ is only ~15% below peak prices of ~A$1,800/oz (in 2011), vs. the gold price in US$ which has weakened ~40% since its peak in 2011. As NMI reports in US$, the result is a significant reduction in US$ denominated costs.

NMI has a strong and flexible balance sheet with ~$39 mln in cash and ~C$34.5 mln in convertible debentures (trading at the money, conversion price C$1.02) at 2Q15. With a strengthening operational base, NMI (as CRK) generated ~$31 mln in FCF over the last nine months (4Q14 to 2Q15), including ~$7 mln in FCF in 2Q15. We believe that NMI is on the verge of significant FCF generation in 2015/16E, even at current depressed metal prices (we use $1,150/oz and a US$/A$ FX rate of $0.75 as our base case assumptions). RJL estimates ~$38 mln in FCF in 2015E ($21 mln delivered in 1H15E) and ~$31 mln in 2016E.

Key reasons to own NMI include: (1) Operational expertise; (2) a recent track record of delivering on guidance; (3) sustainable free cash flow generation; (4) exploration and development upside, specifically at Fosterville and Cosmo; (5) strong and flexible balance sheet; and (6) leverage to the gold price.

Operational Expertise

NMI’s operating expertise, recently reflected by success in unlocking and exploiting higher grade discoveries at the Fosterville mine (the Phoenix and Lower Phoenix Zones) has enabled the company to increase head grade to the mill (2Q14: 3.95 g/t -> 2Q15: 5.92 g/t) and improve the cash flow generating potential of the mine, despite current depressed metal prices. Fosterville generated ~$54 mln in mine level EBITDA during 2014 (at an average gold price of $1,260/oz). Despite recent metal price weakness we see Fosterville continuing to generate a healthy EBITDA (+$60 mln in 2015E and 2016E, at $1,150/oz in 2H15E). Management has succeeded in placing Cosmo and Stawell on secure economic platforms and is committed to maximizing both mine’s profitability in the current weak metal price environment (recently helped by lower fuel costs and A$ weakness).

Management’s Track Record – Delivering on Expectations

Management beat 2014 consolidated annual production guidance (222 k oz vs. guidance of 200-210 k oz) and delivered cash costs at the low end of guidance (~$900/oz). The company is on track to meet or potentially beat both 2015 production guidance (2015E: 228 k oz vs. guidance of 205-220 k oz) and cash cost guidance (2015E: ~$710/oz vs. guidance of $780-$860/oz).

Canada Research | Page 4 of 32 Newmarket Gold Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

FCF Generation

RJL estimates 4 years of sustainable FCF (2015E: ~$38 mln or ~$0.24/share; 2016E: ~$31 mln or ~$0.20/share; 2017E: ~$41 mln or ~$0.26/share, 2018E: ~$41 mln or ~$0.22/share), using RJL base case assumptions of $1,150/oz and an US$/A$ FX rate of $0.75.

Development/Exploration Upside

NMI’s focus is aimed at continuing to optimize the operational performance of its existing operations and target mine-site exploration and near-term development focused opportunities. These include: (1) continuing to follow up on the exploration and development of the newly discovered East Dipping, and Kestrall structures, and Eagle Fault at Fosterville; (2) expand resources through underground drilling at Cosmo and at Stawell; (3) continue to test the exploration potential offered by East Flank mineralization and engage with the local community and modify the operating plan for the Big Hill development stage project. NMI is also continuing to look for ways to improve Stawell’s operational efficiencies and economics.

Potential M&A – On the Lookout for Value

In time, we expect to see NMI engage in M&A activity with a view to grow production and leverage off the company’s cash flow, as well as the capital and operational expertise of management and the Board. NMI is positioned to partake in precious metal industry consolidation in Australia, Canada, United States and mining-friendly Central and South America. Management has indicated that preferred targets are assets that have 100-200 k oz of annual production potential, with large mineral resources and exploration upside.

Strong and Flexible Balance Sheet

NMI had a cash balance of ~$39 mln at June 30, 2015. With the transaction between Crocodile Gold and Newmarket closed on July 10, 2015, and the subsequent C$25 mln private placement and C$20 mln cash consideration paid to CRK shareholders, we estimate a 3Q15 cash balance of ~$47 mln. NMI also has C$34.5 mln in convertible debentures outstanding (April 2018 maturity, 8% coupon), convertible at the holder’s option into NMI shares at C$1.02/share. The debentures become callable if NMI’s shares trade above C$1.53 (for a period of 20 days). For the purpose of our valuation we include the convertible debentures as equity. We also note that NMI had working capital of ~$25 mln as of June 30, 2015.

Risks to Our 6 to 12 Month Outlook

Development Risk. 2015 and 2016 are critical years for NMI as the company builds out and converts resources to reserves at its operations, specifically at Cosmo and Stawell. Also, regulatory approvals (environmental and public approvals pending), the ability of Stawell to sustain itself economically until Big Hill is developed and Big Hill’s development potential will determine the longevity of Stawell.

Geopolitical Risk. Australia is recognized as a stable and low risk jurisdiction with access to infrastructure and skills.

Gold Price Risk. A drop in the gold price could cause deterioration in NMI’s ability to fund its operations. On an operating cash cost basis NMI is a relatively low cost producer, producing ounces at ~$710/oz (2015E). However, significant Capex is currently being deployed to its operations (specifically at Fosterville and Cosmo) to ensure their longevity which adds to their AISC profile (2015E Fosterville: ~$880/oz and Cosmo; $1,050/oz) and provides little protection (especially at Cosmo and Stawell) should the gold price fall.

Cost Inflation Risk. Our outlook assumes certain future capital and operating costs for development projects. Although we apply conservative estimates to these assumptions there is a risk that we have understated these costs or that these costs may increase in the future.

Operational and Labour Risk. There is a risk that NMI’s operations suffer accidents or disruptions to production or development which could impair the value of the assets. Risks of labour disruptions due to strike action may also impact production and profitability.

Newmarket Gold Inc. Canada Research | Page 5 of 32

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Company Overview

Newmarket Gold (NMI-TSX) is the product of a recent merger between Newmarket Gold, a former gold-focused explorer, and Crocodile Gold (CRK), a gold miner with three operating gold mines and a portfolio of exploration assets located in Australia. Newmarket is listed on the Toronto stock exchange under the ticker NMI. The company’s three primary operating assets are the Fosterville and Stawell gold mines in the State of Victoria and the Cosmo mine in the Northern Territory, Australia. We view NMI’s asset strength from predecessor company Crocodile Gold’s assets, specifically the Fosterville mine.

Of particular note, the combination of the two companies marries an experienced mining-focused management team and Board of Directors with a significant (~200 k oz/year) gold production base in a mining-friendly jurisdiction (Australia) supported by a large resource base (~4.8 mln oz measured and indicated resource) with relatively low operating costs (2015E: ~$710/oz). NMI’s management team is led by Douglas Forster (President and CEO) and a Board of Directors that includes Raymond Threlkeld (Chairman), Lukas Lundin, Chairman of Lundin Mining (LUN-TSX) and Randall Oliphant, Executive Chairman of New Gold (NGD-TSX).

Over the last year CRK has demonstrated its operational abilities by improving the operating performance of its mines and achieving mine-site exploration success at Fosterville, which has transformed the asset into a profitable operation that offers a healthy multi-year mine life supported by a robust resource base. We view Fosterville as NMI’s most attractive asset (NAV5%: ~$131 mln or ~50% of NAV) and the main driver of near-term free cash flow.

Key reasons to own NMI include: (1) Operational expertise; (2) a recent track record of delivering on guidance; (3) sustainable free cash flow generation; (4) exploration and development upside, specifically at Fosterville and Cosmo; (5) strong and flexible balance sheet; and (6) leverage to the gold price.

The Former Crocodile Gold – Turning from Swimming against the Tide

CRK purchased the Fosterville and Stawell gold mines from AuRico Gold in 2012, in a transaction which included consideration of C$55 mln in cash and C$10 mln in stock, plus a share in the future net free cash flows generated by these assets (under a net free cash flow sharing agreement). Whilst the transaction offered CRK an enlarged production base (~200 k oz/year) and the ability to generate free cash flow in the 2012 metal price environment (gold price average: $1,669/oz), in today’s price environment the net free cash flow sharing arrangement hampered CRK’s ability to generate adequate returns. In 1Q15, CRK successfully negotiated the termination of the net free cash flow sharing arrangement with AuRico for a cash payment of C$20 mln and a 2% NSR on the Fosterville mine and 1% on the Stawell mine (Stawell NSR begins January 1, 2016). With the net free cash flow agreement terminated, CRK enjoyed the full benefit of improved operating performance and delivered strong 1H15 financial performance, generating $21 mln in FCF.

CRK has enjoyed successive quarters (2Q14 to 1Q15) of consolidated production growth (55 k oz -> 60 k oz) with lowering cash operating costs (~$960 -> $680/oz). Whilst production in 2Q15 (56 k oz) was slightly lower than 1Q15, cash operating costs ($681/oz) were similar to those in 1Q15 (see Exhibit 1). We believe the key elements that enabled this operational improvement will continue to allow NMI to generate positive FCF despite a lower gold price environment. While a weakening A$ has provided cost relief tailwinds, much of the positive performance (2Q14 to 2Q15) was driven by improving head grades (3.95 -> 5.92 g/t) and plant efficiencies (recoveries: 86% -> 89%) at Fosterville (see Exhibit 2), both of which drove production growth (~22 -> ~30 k oz) at lower cash operating costs ($891 -> $532/oz).

Operational strength and financial prudence began to instill market confidence in CRK, reflected by an attractive YTD share price performance (+93% prior to the announcement of NMI merger on May 11, 2015) handily beating peers and the GDXJ’s performance (1.3%). We see this trend continuing – which justifies our OP2 rating.

Canada Research | Page 6 of 32 Newmarket Gold Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Exhibit 1: NMI Production and Cash Costs (2Q14 – 2Q15A) Exhibit 2: Fosterville Production and Cash Costs (2Q14 – 2Q15A)

0

200

400

600

800

1,000

1,200

40

45

50

55

60

65

2Q14 3Q14 4Q14 1Q15 2Q15

Ca

sh O

pe

rati

ng

Co

sts

(US

$ /

oz)

Pro

du

cti

on

(k o

z)

Production (k oz) Cash Operating Costs (US$/oz)

0

100

200

300

400

500

600

700

800

900

1,000

0

5

10

15

20

25

30

35

2Q14 3Q14 4Q14 1Q15 2Q15

Ca

sh O

pe

rati

ng

Co

sts

(U

S$ /

oz)

Pro

du

cti

on

(k o

z)

Production (k oz) Cash Operating Costs (US$/oz)

Source: Newmarket Gold Inc., Raymond James Ltd.

The Currency Effect – A$ Tailwinds

NMI has benefited significantly from a weakening Australian dollar (A$) which has depreciated 23% vs. the USD over a 1 year period, resulting in gold in A$ currently trading at ~A$1,600 (+11% YTD). Furthermore, gold in A$ is only ~15% below peak prices of ~A$1,800/oz (in late 2011), vs. the gold price in US$ which has weakened ~40% since late 2011.

On an average quarterly basis between 2Q14 to 2Q15 (inclusive), the A$ has depreciated 20% vs. the US$, while NMI’s consolidated cash operating cost has declined 41% over the same period (see Exhibits 3 and 4).

We see potential for further FX-related cost improvements as QTD 3Q15 the A$ has depreciated another 5.5% vs. the US$, currently trading at a US$/A$ rate of $0.72.

Exhibit 3: Gold in US$ vs. Gold in A$ (2014-Present) Exhibit 4: NMI Costs vs. US$/A$ Quarterly Averages

0.70

0.75

0.80

0.85

0.90

0.95

$400

$500

$600

$700

$800

$900

$1,000

2Q14 3Q14 4Q14 1Q15 2Q15

US

D /

AU

D

Ca

sh

Op

era

tin

g C

osts

(U

S$

/o

z)

Cash Op. Costs USD/AUD FX Rate

$1,000

$1,100

$1,200

$1,300

$1,400

$1,500

$1,600

$1,700

Go

ld P

rice

-U

S$

vs.

A$

Gold - AUD Gold - USD

Source: Newmarket Gold Inc., Capital IQ, Raymond James Ltd.

Newmarket Gold Inc. Canada Research | Page 7 of 32

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Fosterville – A Phoenix Rising from the Ashes

Fosterville is an underground mine sourcing sulphide ore from the Central, Phoenix and Harrier mine areas. Underground mining is conducted using a conventional fleet including jumbos, production drills, loaders, trucks and ancillary equipment. Fosterville operates a processing facility that incorporates flotation, bacterial oxidation and CIL circuits with a capacity of ~2,300 tpd. The bacterial oxidation process uses BIOX technology, operated under license from Goldfields Pty Ltd. Production at the Fosterville mine has been steadily increasing over the last 12 months with quarterly production increasing from ~22 k oz (2Q14) to ~30 k oz (2Q15), driven by the delivery of higher grade to the mill and improved blending practices of carbonaceous ore and ongoing optimization of the leaching circuit (recoveries: 84% (1Q14) to 89% (2Q15)). Mining is currently transitioning from the Harrier zone to the Central and Phoenix lodes which include the higher-grade Lower Phoenix area.

Fosterville has enjoyed a history of reserve replacement that has added over 1 mln oz of reserves over the past 10 years (current P&P reserves total ~1.5 mln tonnes grading 6.6 g/t for in-situ ~300 k oz). NMI is aggressively advancing underground development at Fosterville (~651 m per month for a total of 1,954 m in 2Q15), a strategy which we expect to continue.

Exploration Potential – Drill results released this year focused on Phoenix and Lower Phoenix mineralization and reveal encouraging high-grade gold intercepts along-strike (down-plunge) from current mineral reserves. Drilling has confirmed continuous mineralization along the newly identified structures (Phoenix, Lower Phoenix, Lower Phoenix Footwall or LPFW, East Dipping, Kestrel and Eagle Faults) (see Exhibit 5). Also, visible gold has been observed in addition to the more common disseminated sulphide gold mineralization.

Recent high-grade intercepts support potential to expand mineral resources and reserves southwards down-plunge and potentially provide multiple ore sources accessible from existing infrastructure (the Phoenix decline). Further, the presence of visible gold which appears to be introduced by a second gold event offers potential to significantly increase gold grades.

Exploration success at Fosterville in 2014 provided increased definition and confidence in the mine’s geological model which resulted in a ~3% increase in mineral reserve grade (to 6.6 g/t) as well as a ~8% increase in measured and indicated resource grade (to 4.2 g/t). Current reserves total ~1 mln tonnes grading 5.56 g/t (excluding the CIL tailings) for ~180 k in-situ oz which yield ~2 years of reserve supported mine-life. A global resource base (measured, indicated and inferred resources) of ~16.6 mln tonnes grading 4.02 g/t (2.1 mln in-situ oz) offers reserve growth potential.

Drilling is ongoing to better understand the extent, orientation, geometries and metallurgical characteristics of newly identified mineralized structures. Drilling is planned to occur in conjunction with the Phoenix and Lower Phoenix Footwall exploration programs.

Operating Assumptions – At Fosterville, RJL models ~5 years (mid-2015E to mid-2019E) of underground ore production (3.1 mln tonnes grading 5.44 g/t) at a mill rate of 2,000 tpd (see Exhibit 6). We note that reserves of 1.5 mln tonnes (~2 years) grading 6.57 g/t, M&I resources of 16.6 mln tonnes grading 4.02 g/t and inferred resources of 5.9 mln tonnes grading 3.71 g/t have been defined at Fosterville (as of December 31, 2014). M&I resources are inclusive of reserves.

RJL forecasts 113 k oz in 2015E at an AISC cost of $884/oz which compares with company production guidance of 100-105 k oz, and operating cash costs of ~$572/oz which compares with company guidance of $670-$750/oz (see Exhibit 6). For 2016, we forecast 110 k oz at an AISC cost of ~$834/oz. RJL assumes capital costs of ~A$45 mln in 2015E and ~A$35 mln for 2016E. Using the RJL base case metal price assumption ($1,150/oz 2H15E/2016E) we estimate the Fosterville mine generating mine level EBITDA of ~$60 mln in 2015E and 2016E. Recent exploration success supports reserve and resource expansion potential to expand Fosterville’s mine-life beyond 2019E, in our view.

Canada Research | Page 8 of 32 Newmarket Gold Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Exhibit 5: Fosterville Drill Results

Source: Newmarket Gold Inc.

Exhibit 6: Fosterville Operating Assumptions, Production and Cost Profile

Fosterville 2015E 2016E 2017E 2018E 2019E

Tonnes Milled (k tonnes) 717 732 730 730 196

Grade (g/t) 5.52 5.35 5.45 5.45 5.45

Recoveries (%) 89% 88% 88% 88% 88%

Gold Production (k oz) 113 110 112 112 30

Cash Operating Costs (US$/oz) $572 $596 $586 $586 $586

AISC (US$/oz) $884 $834 $821 $821 $756

0

100

200

300

400

500

600

700

800

900

1,000

0

20

40

60

80

100

120

2015E 2016E 2017E 2018E 2019E

Co

sts

(US

$ /

oz)

Pro

du

cti

on

(k o

z A

u)

Gold Production (k oz) AISC (US$/oz) Cash Operating Costs (US$/oz)

Source: Raymond James Ltd.

Newmarket Gold Inc. Canada Research | Page 9 of 32

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Cosmo – Unravelling a Geological Puzzle

Commercial production at the Cosmo mine in the Northern Territory was declared in early 2013. The mine is located on the prospective Cosmo/Howley corridor, which hosts the Howley Anticline and several deposits including Cosmo. The majority of drilling at Cosmo has been focused on the eastern limb of the anticline structure; however, most of the drilling at Howley has been on the western limb of the anticline.

Ore from Cosmo is trucked and processed at the Union Reefs plant (6,850 tpd CIL and gravity) located ~15 km from the mine. Whilst the Cosmo mine operates on a 24 hour basis, 7 days a week, milling operations at the Union Reefs mill currently run on a 9 days on, 5 days off roster with two 12 hour shifts. During the off days maintenance is conducted on the plant.

Over the past couple of years, a significant amount of work has been applied to understanding key structural and mineralogical controls at Cosmo. This has prompted a reinterpretation of mineral resources. Whilst much still needs to be done, RJL views Cosmo’s near-term production and economic potential as stable. The Cosmo mine has been operating consistently since commercial production was declared with quarterly production ranging between 17 k oz and 22 k oz (21 k oz in 1Q15). NMI has made great strides in increasing production tonnes (1Q14: ~2,000 -> 1Q15: 2,200 tpd) and lowering operating costs (1Q14: ~$1,170/oz -> 1Q15: ~$770/oz) driven in part by the change last year to a new mining contractor which resulted in record monthly and quarterly stoping rates. Whilst 2Q15 production was lower than 1Q15 (~17 k oz vs. ~21 k oz) and costs were higher (due to a drop in tonnes mined due to equipment availability), we believe that Cosmo is on a firm economic footing (2H15E cash costs: $850/oz, dropping in 2016E to ~$830/oz). We note that regular mining rates were restored by the end of May with a strong result for June, with over 68 kt tonnes mined and metallurgical recoveries during 2Q15 (92.7%), just short of record

recoveries, ranking 1H15 as the best half year result in Cosmo’s history.

Mining is focused on three main mineralized lodes. Two mining methods are being used at Cosmo, namely down-hole stope and fill (modified Avoca) for most stopes and up-hole bench stoping for isolated stopes. Cosmo uses a contract miner at the mine.

Gold mineralization at Cosmo is closely associated with sulphides (pyrite and arsenopyrite, with traces of sphalerite and chalcopyrite) and manifests itself as quartz veins, breccias and shears, with higher grades commonly hosted by banded iron formations. Key features of the Cosmo lodes are their consistency of grade, geological continuity and generally wide true thicknesses in the higher grade parts of the resource. The Cosmo resource model encompasses the Cosmo Eastern Lodes which includes the 100, 110 and 300 Lodes and the Western Lodes (down to a depth of 655 m and 350 m, respectively). The strike length of the Eastern Lodes and Western Lodes is ~440 m and ~260 m, respectively.

Exploration Potential – Drilling over the last couple of years has focused on improving the structural understanding of mineralization and expanding Cosmo’s resource and reserve base. Exploration has focused on testing the repetition of the geological package on both limbs of the anticline structure; testing the footwall of the F1 Fault on the Eastern Limb for lode extensions along strike and at depth; testing the hanging‐wall of the F1 Fault and the fold hinge of the anticline structure; and testing the Western Limb of the fold hinge of the anticline structure (Western Lode Deeps exploration target). Two phases of drilling have been completed on the Western Lode target to date in 2015 and a third phase of drilling is currently underway. Select results include 7.42 g/t over 4.3 m (ETW 2.85 m) in hole CW69001 and 6.59 g/t over 6.4 m (ETW 1.65 m) in hole CW69006. Results support potential for grade and width amenable for underground mining and in close proximity to existing mine infrastructure. Drilling in the foot wall and hanging wall of the F1 Fault has centered on the “Inner Dolerite Target” (a second phase of drilling is underway) and “Central Internal Metasediments”. Targets are located only 160 m from current development and, as such, offer potential to expand the current mine plan to alternative mining areas outside of reserves. We see NMI’s continued focus at Cosmo as being aimed at exploring these opportunities and expanding reserves and resources through underground drilling.

Canada Research | Page 10 of 32 Newmarket Gold Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Exhibit 7: Cosmo Drill Results

Source: Newmarket Gold Inc.

Operating Assumptions – RJL models ~6 years (mid-2015E to mid-2021E) of underground ore production (~5.0 mln tonnes grading 3.34 g/t) at a mill rate of 2,100 tpd (30% of the Union Reef plant capacity) (see Exhibit 8). We note that reserves of 1.3 mln tonnes (~2 years) grading 3.57 g/t, M&I resources of 5 mln tonnes grading 3.35 g/t and inferred resources of 1 mln tonnes grading 2.72 g/t have been defined at Cosmo (December 31, 2014). M&I resources are inclusive of reserves.

RJL forecasts ~77 k oz in 2015E at an AISC cost of $1,055/oz which compares with production guidance of 75-85 k oz, and 2015E operating cash costs of $834/oz which compares with guidance of $850-$930/oz. For 2016E, we forecast ~80 k oz at an AISC cost of ~$1,014/oz. RJL assumes capital costs of ~A$20 mln in 2015E/2016E. Using RJL metal price assumption ($1,150/oz) RJL estimates the Cosmo mine generating mine level EBITDA of ~$25 mln in 2015E and 2016E.

Exhibit 8: Cosmo Operating Assumptions, Production and Cost Profile Cosmo 2015E 2016E 2017E 2018E 2019E 2020E

Tonnes Milled (k tonnes) 770 769 767 767 767 769

Grade (g/t) 3.40 3.58 3.27 3.27 3.27 3.27

Recoveries (%) 91% 91% 91% 91% 91% 91%

Gold Production (k oz) 77 80 73 73 73 73

Cash Operating Costs (US$/oz) $834 $827 $905 $905 $905 $905

AISC (US$/oz) $1,055 $1,014 $1,111 $1,111 $1,111 $1,110

0

200

400

600

800

1,000

1,200

50

55

60

65

70

75

80

85

2015E 2016E 2017E 2018E 2019E 2020E

Co

sts

(US

$ /

oz)

Pro

du

cti

on

(k o

z A

u)

Gold Production (k oz) AISC (US$/oz) Cash Operating Costs (US$/oz)

Source: Raymond James Ltd.

Newmarket Gold Inc. Canada Research | Page 11 of 32

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Stawell – Pared Back and Profitable

The Stawell mine has been in operation for over 25 years, while in recent years mining activity has been reduced. The lower portion of the mine was closed in 2013, since then mining has focused remnant resource and mining pillars in the upper levels as well as surface stockpiles. The closure of lower levels of the mine and an adjusted cost model has resulted in lower operating costs (cash operating costs: 1Q13: ~$1,200/oz -> 2Q15: ~$815/oz). This has allowed for the consideration of lower grade material. Over the last 12 months NMI has achieved operational sustainability at Stawell by streamlining operating activities, reducing manpower, and infrastructure.

The Stawell plant was commissioned in 1984 and has undergone a number of upgrades. Current mill capacity is ~2,600 tpd on underground hard rock and up to ~3,600 tpd on softer oxide ore types. The treatment facility employs gravity, flotation and fine grind and CIL processes.

During 2Q15, production at Stawell totaled 9,277 oz representing the 8th

consecutive quarter of production above 9,200 oz. Mill feed continued to be sourced from combining underground ore and surface oxide; as such, grade decreased to 1.57 g/t compared with 1.75 g/t in 1Q15, reflecting the lower-grade nature from the mining of the upper levels of the mine. Metallurgical recoveries continued to improve (2Q15: 83.1% vs. 1Q15: 80%) due to lower graphitic ore content in the mill feed and modifying the plant circuitry to remove high preg robbing materials and re-introducing concentrate down circuit. The operating strategy at Stawell remains focused on cost reduction activities and the downsizing of mine operations to ensure profitability of mined tonnes.

Potential for a significant boost in Stawell’s mine life is offered by the Big Hill development stage project, located on publically accessible Crown land which is partly leased by the Stawell mine. The project is currently the subject of an Environmental Effects Statement and ministerial assessment. In October 2014 the Victorian Government recommended that the project not proceed in its current form. Prior to the merger between NMI and Crocodile Gold, recommendations provided by the Victorian Government were being reviewed. A benching configuration, reduced blasting, dust suppressants, back filling of pits noise attenuation and restricted hours of operation are being considered.

Big Hill was the focus of an economic evaluation and a Feasibility Study in 2014 which called for the mining of 2.9 mln tonnes of ore (classified as Probable Reserve) grading ~1.5 g/t (~145 k in-situ oz) over a 2.5 to 4 year time frame.

Exploration potential – Near-term exploration work is being directed at in-fill drilling to confirm continuity and test for faulted extremities of the ore body as well as underground channel sampling to assist in identifying recoverable reserves. Recent drill results from the “Aurora B” drilling program on the East Flank are encouraging (see Exhibit 9). Little work exploration/ development has been done on the East Flank whereas over 2.3 mln ounces has been produced from the West Flank at Stawell. Select results include 7.06 g/t over 17.80 m (ETW 8.3 m) in MD6339 (located 500 m from existing underground infrastructure). Drilling is ongoing.

Canada Research | Page 12 of 32 Newmarket Gold Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Exhibit 9: Stawell Drill Results

Source: Newmarket Gold Inc.

Operating Assumptions – We model ~2 years of underground ore production (~1 mln tonnes of underground ore and low grade stock piles (combined grade = 1.7 g/t), at a mill rate of 2,000 tpd (below plant capacity). We note that reserves (including Big Hill) of 3.7 mln tonnes grading 1.5 g/t, M&I resources of 4.2 mln tonnes grading 1.83 g/t and inferred resources of 1 mln tonnes of 2.76 g/t have been defined at Stawell (December 31, 2014). M&I resources are inclusive of reserves. Reserves, outside of Big Hill, total 0.3 mln tonnes have been defined.

RJL forecasts ~38 k oz in 2015E at an AISC of ~$931/oz vs. production guidance of 30 k oz. RJL forecasts operating cash costs of $856/oz vs. guidance of $945- $1,025/oz. For 2016E, we forecast a similar production and cost profile as 2015. Capex of ~A$4mln in 2015E and ~A$13 mln in 2016E (Big Hill) are assumed. Using RJL base case metal price assumption ($1,150/oz in 2H15E/2016E) RJL estimates the Stawell mine generating mine level EBITDA of ~$10 mln in 2015E and 2016E.

Exhibit 10: Stawell / Big Hill Operating Assumptions Stawell 2015E 2016E 2017E 2018E 2019E 2020E

Tonnes Milled (k tonnes) 810 682 730 730 730 710

Grade (g/t) 1.87 1.93 1.70 1.68 1.40 1.40

Recoveries (%) 81% 80% 90% 90% 90% 90%

Gold Production (k oz) 38 34 36 35 29 29

Cash Operating Costs (US$/oz) $856 $887 $705 $715 $856 $856

AISC (US$/oz) $931 $921 $758 $769 $918 $920

0

100

200

300

400

500

600

700

800

900

1,000

0

5

10

15

20

25

30

35

40

2015E 2016E 2017E 2018E 2019E 2020E

Co

sts

(US

$ /

oz)

Pro

du

cti

on

(k o

z A

u)

Gold Production (k oz) AISC (US$/oz) Cash Operating Costs (US$/oz)

Source: Raymond James Ltd.

Newmarket Gold Inc. Canada Research | Page 13 of 32

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Consolidated = ~230 k oz / Year at ~$986/oz AISC (2015E)

Combining production from NMI’s three operations supports our estimates for ~220 k oz/year of sustainable production at an AISC of $950/oz, until 2019E (see Exhibit 11). We anticipate additional mine life through resource expansion, reflective of the exploration potential offered by NMI’s assets.

Exhibit 11: Consolidated Production and Cost Profile

0

200

400

600

800

1,000

1,200

1,400

1,600

0

50

100

150

200

250

2014 2015E 2016E 2017E 2018E 2019E 2020E 2021E

US

$ /

oz

Pro

du

cti

on

(k o

z)

Stawell Fosterville Cosmo AISC (US$/oz) TCC (US$/oz)

Source: Newmarket Gold Inc., Raymond James Ltd.

Other Exploration Stage Assets

Besides NMI’s operating mines, the company holds property interests in Australia and Canada. These include the Point Leamington Au-Zn-Cu-Ag-Pb deposit in Newfoundland, Canada, the Maud Creek Au deposit in the Northern Territory, Australia as well as properties in the Northern Territory (excluding Cosmo) that host reserves and resources. NMI’s near-term focus is its operations and the mine-site exploration potential offered by each. From NMI’s varied property portfolio, only the Point Leamington and Maud Creek projects are worthy of mention, in our view.

Point Leamington

The Point Leamington gold-zinc-copper-silver-lead massive sulphide deposit in Newfoundland, Canada was discovered by Noranda in 1971. An inferred resource estimate (2013) based on 24,152 m of drilling in 77 drill holes estimated 14.1 mln tonnes grading 1.07 g/t Au, 1.88% Zn, 0.42% Cu, 0.02% Pb, 17.12 g/t Ag (at a 4.0% ZnEq cut-off grade). The deposit contains a high grade core and the resource is open for expansion. No work is planned for Point Leamington and as such RJL ascribes no value to the project in our valuation for NMI.

Maud Creek

The Maud Creek project is located approximately 110 km from Union Reefs mill and approximately 285 km south-southeast of Darwin. Maud Creek hosts a significant underground probable reserve (~1 mln tonnes grading 5.4 g/t Au) and resource (~7.7 mln tonnes grading 3.5 g/t Au). It is open at depth and along strike. The mineralized material is refractory, containing arsenopyrite, and requires additional study before becoming part of NMI’s development plan. As such, RJL ascribes no value to the project in our valuation for NMI.

NMI has commenced a phased feasibility study (PEA, Pre-feasibility, feasibility) at Maud Creek (SRK Consulting). PEA results are anticipated in 1Q16 and based on the successful completion of a PEA, Pre-Feasibility and Feasibility Stages may be undertaken throughout 2016. Proximity to the Union Reefs mill offers potential to leverage existing infrastructure.

Canada Research | Page 14 of 32 Newmarket Gold Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Strong and Flexible Balance Sheet – Consistent Free Cash Flow Generation

NMI had a cash balance of ~$39 mln at June 30, 2015. With the transaction between Crocodile Gold and Newmarket closed on July 10, 2015, the subsequent C$25 mln private placement, and C$20 mln cash consideration paid to CRK shareholders, we estimate a 3Q15 cash balance of ~$47 mln. NMI also has C$34.5 mln in convertible debentures outstanding (April 2018 maturity, 8% coupon). The debentures are convertible at the holder’s option into NMI shares at C$1.02/share, and become callable if NMI’s shares trade above C$1.53 (for a period of 20 days). For the purpose of our valuation we include the convertible debentures as equity. We also note that NMI had working capital of ~$25 mln, as of June 30, 2015.

We forecast steady FCF generation in 2015E and 2016E, with cash balance increasing to ~$61 mln by year-end 2015E and ~$99 mln by year-end 2016E (assuming: $1,150/oz and a US$/A$ FX rate of $0.75).

Exhibit 12: Net Cash Flow (2014A-2018E) Exhibit 13: Cumulative FCF at Various Metal Prices (2014A-2018E)

-$100

-$50

$0

$50

$100

$150

$200

2014A 2015E 2016E 2017E 2018E

US

$ m

ln

Cash From Operations Cash From Investing

Cash From Financing Net Cash Flow

$0

$50

$100

$150

$200

$250

$300

2014A 2015E 2016E 2017E 2018E

US

$ m

ln

Cumulative FCF before debt at $1300

Cumulative FCF before debt at $1150

Cumulative FCF before debt at $1000

Source: Newmarket Gold Inc., Raymond James Ltd.

Gold Price and Operating Cost Sensitivity

Our valuation of NMI is sensitive to the price of gold and operating costs. RJL assumes a flat $1,150/oz gold price (from 3Q15 onwards). See Exhibit 14.

Exhibit 14: Raymond James Ltd.’s Gold Price Deck

Year 2014 2015E 2016E 2017E 2018E LT

Gold Price (US$/oz) $1,266 $1,178 $1,150 $1,150 $1,150 $1,150 Source: Raymond James Ltd.

A 10% increase in the gold from our base case (2016E: $1,150) delivers a NAVPS of C$2.10 estimate (53% increase from our C$1.37 base case estimate), all other assumptions being held constant. A 10% increase in operating costs from our base case delivers a NAVPS of C$0.92 estimate (33% decrease from our C$1.37 base case), all other assumptions being held constant (see Exhibit 15).

Newmarket Gold Inc. Canada Research | Page 15 of 32

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Exhibit 15: NAVPS Sensitivity Analysis to Gold Price/Operating Costs

$1 -30% -20% -10% 0% 10% 20% 30%

30% -$2.17 -$1.44 -$0.70 $0.03 $0.76 $1.50 $2.23

20% -$1.72 -$0.99 -$0.26 $0.48 $1.21 $1.94 $2.68

10% -$1.28 -$0.54 $0.19 $0.92 $1.66 $2.39 $3.12

0% -$0.83 -$0.10 $0.64 $1.37 $2.10 $2.84 $3.57

-10% -$0.38 $0.35 $1.08 $1.82 $2.55 $3.28 $3.97

-20% $0.06 $0.80 $1.53 $2.26 $3.00 $3.73 $4.33

-30% $0.51 $1.24 $1.98 $2.71 $3.44 $4.13 $4.71

Gold Price (US$/oz)O

pe

rati

ng

Co

sts

Source: Raymond James Ltd.

Based on our base case estimate for 2016E CFPS of $0.52/share, which is key component used to derive our target price, a 10% increase in the gold price from our base case assumptions delivers a $0.69/share estimate (a 31% increase over our base case). A 10% increase in operating costs delivers a $0.44/share estimate of 2016E CFPS (a 16% decrease in our base case) (see Exhibit 16).

Exhibit 16: Operating Cash Flow/Share Sensitivity Analysis (US$)

0.52 -30% -20% -10% 0% 10% 20% 30%

30% -$0.21 -$0.05 $0.11 $0.28 $0.44 $0.60 $0.76

20% -$0.13 $0.03 $0.20 $0.36 $0.52 $0.68 $0.85

10% -$0.05 $0.12 $0.28 $0.44 $0.60 $0.77 $0.93

0% $0.04 $0.20 $0.36 $0.52 $0.69 $0.85 $1.01

-10% $0.12 $0.28 $0.44 $0.61 $0.77 $0.93 $1.09

-20% $0.20 $0.36 $0.53 $0.69 $0.85 $1.01 $1.18

-30% $0.28 $0.45 $0.61 $0.77 $0.93 $1.10 $1.26

Gold Price (US$/oz)

Op

era

tin

g C

osts

Source: Raymond James Ltd.

Valuation & Recommendation

We are initiating coverage on Newmarket Gold (NMI-TSX) with an Outperform rating and a C$1.70 target price. To derive our target we apply a 50/50 weighting on a 1x NAV and a 3x 2016E CFPS.

In our view our valuation adequately captures the value of NMI’s operating assets and the free cash flow generating opportunity presented by exploiting these assets. We recognize management’s track record in delivering value by (1) growing production and mine lives organically through exploration, (2) maintaining a hold on operating costs, and (3) delivering on annual production and cost guidance.

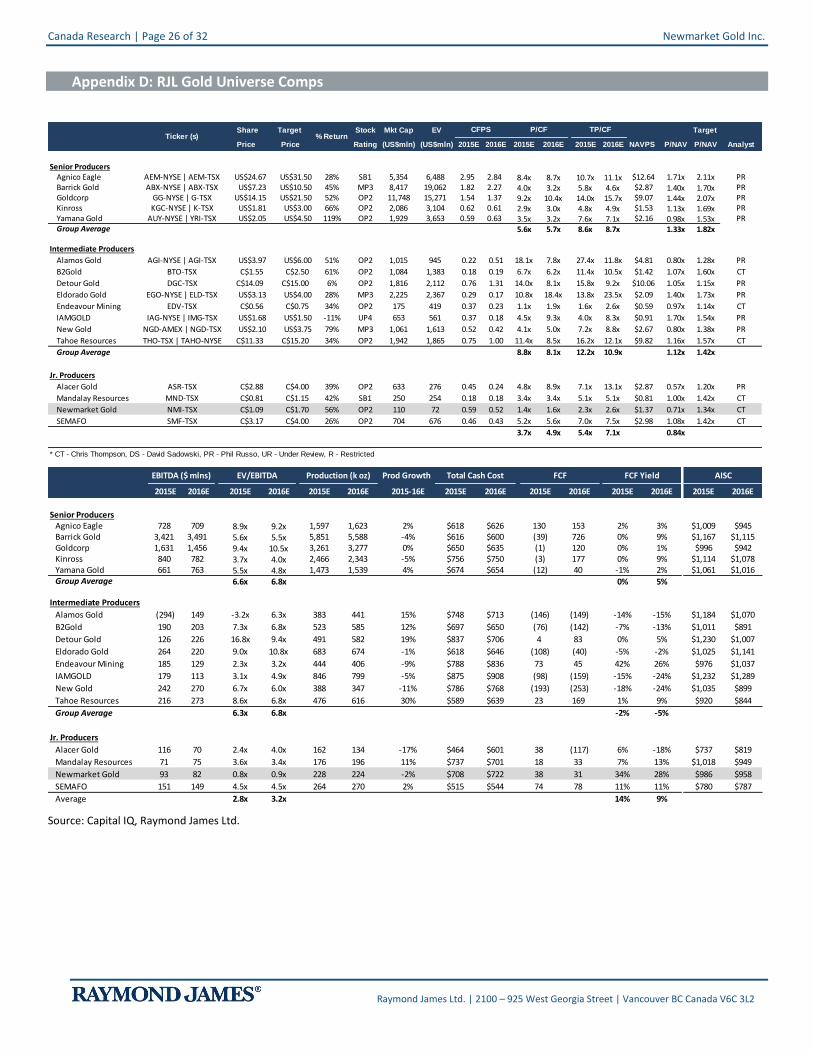

NMI is trading at ~1.6x 2016E CFPS, a significant discount to our junior gold producer peer group average of ~5.4x and our intermediate producer peer group at 8.1x. In our view, this discount is due to the relatively short reserve-supported mine lives (less than two years) of NMI’s operations. We see near-term potential for reserve expansion driven by mine-site exploration efforts at each of NMI’s mines. On a NAV basis, however, NMI trades at 0.71x Adj. NAV, at a discount to our junior gold producer peer group average at 0.84x and our intermediate producer group at 1.12x.

RJL estimates a NAV for NMI’s operating assets (Fosterville, Cosmo, Stawell) of ~C$184 mln or C$0.97/share. We also include a corporate adjustment of C$77 mln or C$0.40/share which justifies a total NAV of ~C$262 mln or $1.37/share. For the purpose of our valuation we include NMI’s C$34.5 mln in convertible debentures as equity.

See Exhibits 17-20 and Appendix D for valuations vs. RJL’s gold producer peer group.

Canada Research | Page 16 of 32 Newmarket Gold Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Exhibit 17: NAV Estimate Summary Exhibit 18: Target Price Calculation

Valuation Summary C$ 000 C$/fd % NAV Value Multiple%

Weighted

Target

Value

Project (Comp Based) Blended Target Price

Cosmo (DCF 5%) $23,449 $0.12 9% 2016 CFPS (C$) $0.65 3.0x 50% $0.98

Fosterville (DCF 5%) $131,141 $0.69 50% NAVPS (C$) $1.37 1.0x 50% $0.69

Stawell (DCF 5%) $29,768 $0.16 11% Value $1.67

Project Total $184,358 $0.97 70% Target Price $1.70

Return to Target 56%

Corporate NAV

Working Capital $61,831 $0.32 24% P/NAV 0.71x

Additional Capital $15,380 $0.08 6% Target P/NAV 1.34x

LT Debt $0 $0.00 0% P/CFPS (2016E) 1.57x

$77,212 $0.40 30% Target P/CFPS (2016E) 2.60x

Net Asset Value $261,570 $1.37 100% US$/A$ FX Rate $0.75

US$/C$ FX Rate $0.80

Market P/NAV 0.71x

Target P/NAV 1.34x I/O F/D - ITM

Share Count (000's) 134,221 190,869 Source: Raymond James Ltd.

Exhibit 19: P/CF and TP/CF (2016E) Exhibit 20: P/NAV and TP/NAV

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

AS

R

NM

I

NG

D

AG

I

ED

V

YR

I

MN

D

DG

C

BT

O

SM

F K

TH

O

ELD

AB

X G

IMG

AE

M

P/N

AV

(x

)

P/NAV

Target P/NAV

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

NM

I

ED

V K

AB

X

YR

I

MN

D

NG

D

SM

F

BT

O

DG

C

TH

O

AG

I

AE

M

AS

R

IMG G

ELD

P/C

FP

S (

x)

P/2016E CFPS

TP/2016E CFPS

Source: Raymond James Ltd.

Newmarket Gold Inc. Canada Research | Page 17 of 32

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Costs, Balance Sheet Strength & FCF Potential

We note that NMI’s (previously Crocodile Gold) costs have steadily decreased driven by high grade discoveries at Fosterville, ranking the company as a sub-$1,000/oz producer (on an AISC basis).

A noteable differentiator that NMI enjoys is their potential to deliver FCF, something that we feel the market doesn’t fully appreciate, based on sector leading 2016E FCF yields (see Exhibit 23).

NMI has a clean balance sheet (as of 2Q15) compared with peers (see Exhibit 24).

Exhibit 21: Total Cash Costs US$/oz (2015/16E) Exhibit 22 AISC - US$/oz (2015/16E)

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

SM

F

ASR

TH

O

BTO

NG

D G

AEM

MN

D

NM

I

DG

C

YRI

ED

V

AG

I K

ABX

ELD

IMG

AIS

C (

US

$/

oz A

uEq

)

AISC - (2015E) AISC (2016E)

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

SM

F

ABX

ASR

AEM G

TH

O

ELD

BTO

YRI

MN

D

DG

C

AG

I

NM

I K

NG

D

ED

V

IMG

To

tal

Ca

sh

Co

sts

(U

S$

/o

z A

uEq

)

TCC (2015E) TCC (2016E)

Source: Raymond James Ltd.

Exhibit 23: FCF Yield (2015/16E) - % Exhibit 24: Net Debt (US$ mln)

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

NM

I

ED

V

MN

D

SM

F

TH

O

ABX K

DG

C

AEM

YRI G

ELD

BTO

AG

I

ASR

NG

D

IMG

FCF

Yie

ld (%

)

FCF Yield - 2015E

FCF Yield - 2016E

-$1,000

-$500

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

ASR

IMG

TH

O

AG

I

NM

I

SM

F

MN

D

ELD

ED

V

DG

C

BTO

NG

D K

AEM

YRI G

ABX

Ne

t D

eb

t (U

S$

mln

s)

Net Debt (US$ mlns)

Sources: Raymond James Ltd.

Canada Research | Page 18 of 32 Newmarket Gold Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Mine-Level AISC

Of the ~90 mines and projects of our gold producers under coverage, NMI’s mines rank below average on a mine-level all-in cost basis (average LOM). Fosterville ranks in the lower third on an AISC basis, while NMI’s Stawell and Cosmo mines rank as higher costs assets.

Exhibit 25: Mine-Level AISC

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

East

ern

Dra

gon

Otj

iko

to

La I

ndia

Agb

aou

Co

rte

z

Espe

ranz

a

Tanj

ians

han

Oly

mp

ias

Feko

la

Cop

ler

Kup

ol D

voin

oye

Man

a

Kir

azl

i

Me

liad

ine

Gol

dex

New

Aft

on

Ho

un

de

Esco

bal

Agi

Da

gi

Pasc

ua

Lam

a

Lagu

nas

No

rte

Cerr

o N

egro

Ma

lart

ic

Mea

dow

bank

Cert

ej

La L

iber

tad

Upp

er B

eave

r

Cost

erfie

ld

Lapa

Fost

ervi

lle

Aur

ora

Gol

dstr

ike

Pino

s A

ltos

Shah

uind

o

Kis

lad

ag

Eleo

nore

Efe

mcu

ku

ru

Roun

d M

ount

ain

Mul

ato

s

Ra

iny

Riv

er

Sko

urie

s

Los

Filo

s

Re

d L

ake

Pueb

lo V

iejo

Pueb

lo V

iejo

LaR

onde

Det

our

Lake

Bjo

rkd

al

Turq

uoise

Rid

ge

Pen

asqu

ito

Mas

bate

La A

ren

a

Ve

lad

ero

Porg

era

Wh

ite

Mo

un

tain

Sa

dio

la

Me

squ

ite

Asa

nko

Go

ld M

ine

Po

rcu

pin

e

Cerr

o Sa

n P

edro

Chir

ano

He

mlo

Kitt

ila

Ess

ak

ane

Tasi

ast

Kett

le R

iver

Sta

we

ll

Taba

koto

Kalg

oorl

ie

El L

imon

Jinfe

ng

Pea

k M

ines

Youg

a

Ruby

Hill

We

stw

oo

d

Pa

raca

tu

Fo

rt K

no

x

Youn

g D

avid

son

Gol

den

Sun

light

No

rth

Ma

ra

El C

hana

te

Buly

anhu

lu

Ba

ld M

ou

nta

in

Mu

sse

lwh

ite

Ma

rlin

Nze

ma

Buzw

agi

Co

sm

o

Mar

icun

ga

Ro

seb

el

Co

st P

er

Ou

nce

NMI Royalty Per Ounce Taxes Per Ounce Sustaining CAPEX Per Ounce Operating Cost Per Ounce Average Mine-Level All-In Costs

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

East

ern

Dra

gon

Otj

iko

to

La I

ndia

Agb

aou

Co

rte

z

Espe

ranz

a

Tanj

ians

han

Oly

mp

ias

Feko

la

Cop

ler

Kup

ol D

voin

oye

Man

a

Kir

azl

i

Me

liad

ine

Gol

dex

New

Aft

on

Ho

un

de

Esco

bal

Agi

Da

gi

Pasc

ua

Lam

a

Lagu

nas

No

rte

Cerr

o N

egro

Ma

lart

ic

Mea

dow

bank

Cert

ej

La L

iber

tad

Upp

er B

eave

r

Cost

erfie

ld

Lapa

Fost

ervi

lle

Aur

ora

Gol

dstr

ike

Pino

s A

ltos

Shah

uind

o

Kis

lad

ag

Eleo

nore

Efe

mcu

ku

ru

Roun

d M

ount

ain

Mul

ato

s

Ra

iny

Riv

er

Sko

urie

s

Los

Filo

s

Re

d L

ake

Pueb

lo V

iejo

Pueb

lo V

iejo

LaR

onde

Det

our

Lake

Bjo

rkd

al

Turq

uoise

Rid

ge

Pen

asqu

ito

Mas

bate

La A

ren

a

Ve

lad

ero

Porg

era

Wh

ite

Mo

un

tain

Sa

dio

la

Me

squ

ite

Asa

nko

Go

ld M

ine

Po

rcu

pin

e

Cerr

o Sa

n P

edro

Chir

ano

He

mlo

Kitt

ila

Ess

ak

ane

Tasi

ast

Kett

le R

iver

Sta

we

ll

Taba

koto

Kalg

oorl

ie

El L

imon

Jinfe

ng

Pea

k M

ines

Youg

a

Ruby

Hill

We

stw

oo

d

Pa

raca

tu

Fo

rt K

no

x

Youn

g D

avid

son

Gol

den

Sun

light

No

rth

Ma

ra

El C

hana

te

Buly

anhu

lu

Ba

ld M

ou

nta

in

Mu

sse

lwh

ite

Ma

rlin

Nze

ma

Buzw

agi

Co

sm

o

Mar

icun

ga

Ro

seb

el

Co

st P

er

Ou

nce

NMI Royalty Per Ounce Taxes Per Ounce Sustaining CAPEX Per Ounce Operating Cost Per Ounce Average Mine-Level All-In Costs

Source: Raymond James Ltd.

Newmarket Gold Inc. Canada Research | Page 19 of 32

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Profitability Index – Asset Level

We utilize Profitability Index (PI) as a measure to analyze the individual mines and projects of our 85 gold producing assets currently under coverage. We rank the assets on a total PI score for each company that represents the present value of cash flow divided by the present value of total capital invested (development + sustaining). NMI’s Fosterville and Stawell mines rank near the middle of the peer group, while NMI’s Cosmo ranks near the low end of the group (due to its high costs).

Exhibit 26: NMI Assets – Profitability Index Total Capital

0

1

2

3

4

5

6

7

8

9

10

Mar

icu

nga

Kalg

oorli

e

Nze

ma

Lum

wan

a

Jaco

bin

a

He

mlo

Ta

sia

st

Wes

two

od

Bald

Mou

ntai

n

Cosm

o

Turq

uois

e Ri

dge

Mus

selw

hite

Kit

tila

El L

imo

n

C1 S

anta

Luz

Mar

lin

Los

Filo

s

Porc

upin

e

Taba

koto

Fort

Kno

x

Ruby

Hill

Go

lden

Sun

light

Para

catu

Copl

er

Pila

r

La L

ibe

rta

d

Chap

ada

Buly

anhu

lu

Yo

un

g D

avi

dso

n

No

rth

Mar

a

Mas

bat

e

Mer

ced

es

Vel

ader

o

Red

Lak

e

El C

hana

te

Gu

alca

may

o

Pea

k M

ines

Jin

fen

g

Ch

iran

o

Essa

kane

El P

enon

Min

era

Flo

rida

Staw

ell

Kisl

adag

Whi

te M

ount

ain

Fost

ervi

lle

Man

a

Ele

on

ore

Faz

en

da

Bra

silie

ro

Bjo

rkd

al

Cerr

o N

egro

Pin

os A

ltos

Sad

iola

Efem

cuku

ru

Mes

qui

te

Roun

d M

oun

tain

Go

ldex

Kett

le R

iver

LaR

on

de

Go

ldst

rike

Det

our

Lak

e

Cerr

o B

ayo

Cana

dian

Mal

arti

c

Mul

ato

s

Otji

koto

La A

ren

a

Ce

rro

Sa

n P

ed

ro

Youg

a

Lagu

nas

Nor

te

Pueb

lo V

iejo

Pena

squ

ito

Zald

ivar

Cres

ton

Mas

cota

New

Aft

on

Cost

erfi

eld

Buzw

agi

Cort

ez

Lapa

Mea

dow

bank

Agb

aou

Tanj

ian

shan

Kup

ol D

voin

oye

Esco

bal

Alu

mb

rera

La In

dia

Profitability Index - Total Capital NMI Assets

Source: Raymond James Ltd.

Canada Research | Page 20 of 32 Newmarket Gold Inc. Newmarket Gold Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

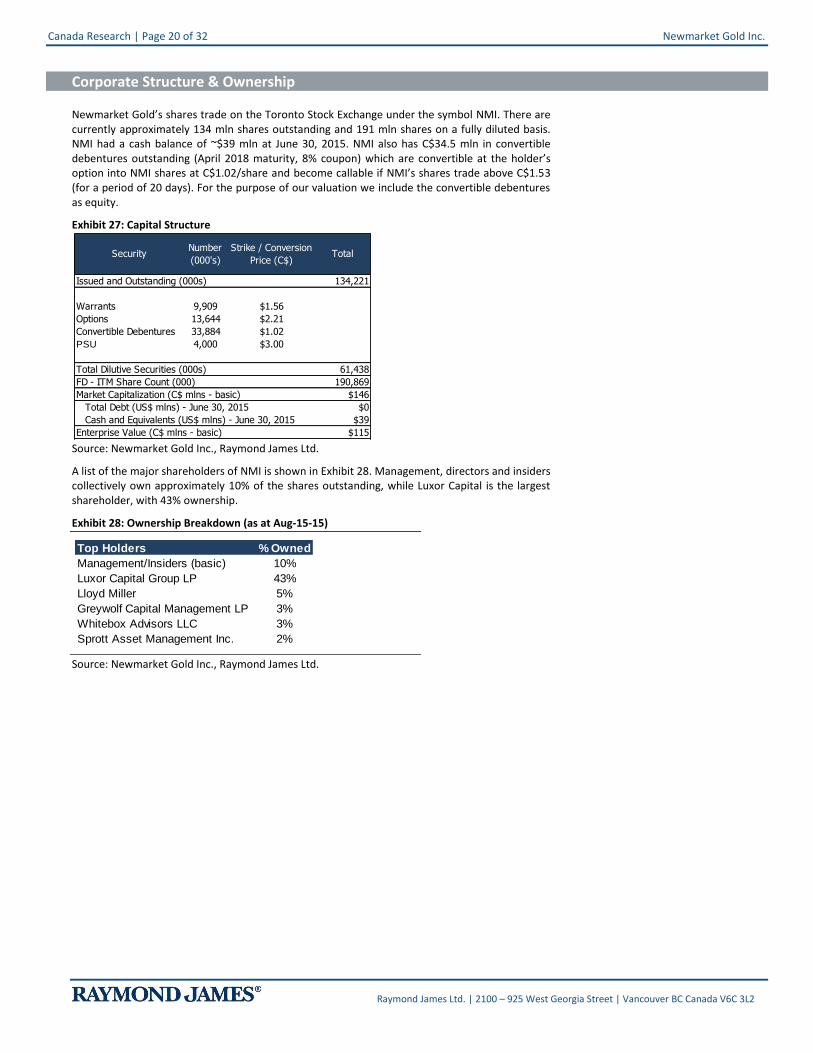

Corporate Structure & Ownership

Newmarket Gold’s shares trade on the Toronto Stock Exchange under the symbol NMI. There are currently approximately 134 mln shares outstanding and 191 mln shares on a fully diluted basis. NMI had a cash balance of ~$39 mln at June 30, 2015. NMI also has C$34.5 mln in convertible debentures outstanding (April 2018 maturity, 8% coupon) which are convertible at the holder’s option into NMI shares at C$1.02/share and become callable if NMI’s shares trade above C$1.53 (for a period of 20 days). For the purpose of our valuation we include the convertible debentures as equity.

Exhibit 27: Capital Structure

Issued and Outstanding (000s) 134,221

Warrants 9,909 $1.56

Options 13,644 $2.21

Convertible Debentures 33,884 $1.02

PSU 4,000 $3.00

Total Dilutive Securities (000s) 61,438

FD - ITM Share Count (000) 190,869

Market Capitalization (C$ mlns - basic) $146

Total Debt (US$ mlns) - June 30, 2015 $0

Cash and Equivalents (US$ mlns) - June 30, 2015 $39

Enterprise Value (C$ mlns - basic) $115

SecurityNumber

(000's)

Strike / Conversion

Price (C$)Total

Source: Newmarket Gold Inc., Raymond James Ltd.

A list of the major shareholders of NMI is shown in Exhibit 28. Management, directors and insiders collectively own approximately 10% of the shares outstanding, while Luxor Capital is the largest shareholder, with 43% ownership.

Exhibit 28: Ownership Breakdown (as at Aug-15-15)

Top Holders % Owned

Management/Insiders (basic) 10%

Luxor Capital Group LP 43%

Lloyd Miller 5%

Greywolf Capital Management LP 3%

Whitebox Advisors LLC 3%

Sprott Asset Management Inc. 2%

Source: Newmarket Gold Inc., Raymond James Ltd.

Newmarket Gold Inc. Canada Research | Page 21 of 32

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Appendix A: Management & Board of Directors

Management Team

President and CEO: Douglas Forster, M.Sc., P.Geo. – Mr. Forster has been associated with the mining industry for over 30 years as a geologist, senior executive, Director, and company founder. He holds a B.Sc. (1981) and M.Sc. (1984) in Economic Geology from the University of British Columbia, Canada. Mr. Forster has worked with numerous companies, including Terrane Metals which was acquired by Thompson Creek in 2010 for $750 mln and Potash One that was acquired by K+S in 2011 for $434 mln. Over the past 25 years Mr. Forster has been involved in a number of large-scale Canadian mine development projects including the Mt. Milligan gold-copper mine, the Kemess South gold-copper mine, the Golden Bear gold mine and the Legacy potash project. Mr. Forster has a proven track record in resource project development, mergers and acquisition, equity finance and public company management. He is a registered member of the Association of Professional Engineers and Geoscientists of British Columbia.

CFO: Robert Dufour, CA, CPA – Robert Dufour was appointed Chief Financial Officer of Newmarket Gold in July 2015. Prior to this appointment and the Newmarket Gold merger, Mr. Dufour was CFO of Crocodile Gold. Mr. Dufour joined Crocodile Gold in June 2012 as Director of Finance and was appointed Chief Financial Officer in April 2013. Mr. Dufour is a Chartered Accountant with over 10 years of finance and accounting experience. He started his career with the Toronto office of PriceWaterhouseCoopers. He later joined Northgate Minerals Corporation as Corporate Controller and subsequently was promoted to Group Financial Controller for Northgate’s Australian subsidiaries, and was based out of Victoria, Australia until its acquisition by AuRico Gold.

Executive Vice President: Blayne Johnson – Mr. Johnson has been involved in the investment community for the over 27 years. As a Vice President of First Marathon Securities he played a key role in providing institutional financing to junior resource companies. During his tenure at the firm, First Marathon participated in over $5 bln of equity financings for natural resource companies. His work at First Marathon involved equity and debt financings as well as mergers and acquisitions. Mr. Johnson also advised institutional clients on investments. Mr. Johnson was a founder of Terrane Metals which was acquired by Thompson Creek in 2010 for $750 mln. He is currently Chairman of Featherstone Capital Inc.

Board of Directors

Non-Executive Chairman: Raymond Threlkeld – Mr. Threlkeld is a seasoned mining professional with more than 32 years of experience in mineral exploration, mine operations and construction and executive management. Most recently he was President and CEO of Rainy River Resources that was developing the 4.0 mln ounce Rainy River gold deposit in Ontario. New Gold purchased Rainy River for $310 mln in 2013. From 2006 to 2009, Mr. Threlkeld led the team along with Randall Oliphant that acquired, developed and put into operation the Mesquite gold mine in California with Western Goldfields subsequently being purchased by New Gold for $314 mln in 2009. From 1996 to 2004, he held a variety of senior executive positions with Barrick Gold Corporation rising to the position of Vice President, Project Development. During his tenure at Barrick, Mr. Threlkeld was responsible for placing more than 30 mln ounces of gold resources into production in Africa, South America and Australia. Among his accomplishments were the Pierina Mine in Peru, Bulyanhulu Mine in Tanzania, Veladero Mine in Argentina, Lagunas Norte Mine in Peru and the Cowel Mine in Australia. Mr. Threlkeld holds a B.Sc. degree in Geology from the University of Nevada.

Director: Lukas Lundin – Mr. Lundin is Chairman of Lundin Mining Corporation. He graduated from the New Mexico Institute of Mining and Technology (Engineering). He has been responsible for various resource discoveries including the multi-million ounce Veladero gold deposit in Argentina that was sold to Homestake for $300 mln in 1999. He has led numerous companies through very profitable business acquisition and mergers including the $7.1 bln sale of Red Back Mining in 2010.

Director: Randall Oliphant, CA – Mr. Oliphant is Executive Chairman of New Gold and was recently appointed Chairman of the World Gold Council. Mr. Oliphant is on the Advisory

Canada Research | Page 22 of 32 Newmarket Gold Inc. Newmarket Gold Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Board of Metalmark Capital LLC (formally Morgan Stanley Capital Partners) and serves on the Boards of WesternZagros Resources Ltd. and Franco-Nevada Corporation. Since 2003, Mr. Oliphant has served on the Boards of a number of public and private companies and not-for-profit organizations. From 1999 to 2003 he was President and Chief Executive Officer of Barrick Gold Corporation, the largest gold producer in the world. From 2006 to 2009 he served as Chairman of Western Goldfields Inc. where he oversaw the successful sale of the company to New Gold for $314 mln. Mr. Oliphant is a Chartered Accountant.

Newmarket Gold Inc. Canada Research | Page 23 of 32

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Appendix B: Financial Statements

Income Statement (US$ 000's) 2013 2014 2015E 2016E

Revenues 300,825 282,739 267,737 257,764

Operating Expenses

Production Costs 218,900 202,034 161,562 162,315

Depreciation and Depletion 76,857 39,424 42,163 48,742

Total Operating Expenses 295,757 241,458 203,725 211,057

Mine Operating Profit 81,925 41,281 64,012 46,707

Total Other Expenses 166,360 11,310 14,214 11,000

Operating Income (161,291) 29,971 49,799 35,707

Non-Operating Income (Expenses) 74,373 (6,939) (2,677) (2,208)

Adj. Net Income (Loss) 54,435 32,977 43,302 30,979

Adj. Basic EPS (Loss) per share 0.13 0.07 0.25 0.21

WA Shares Outstanding

Basic Shares Outstanding (000's) 406,379 464,798 138,888 144,130

F/D Shares Outstanding (000's) 406,379 471,874 156,985 156,985

Adj. EBITDA 126,319 84,549 92,580 82,241

Adj. EBITDA Margin % 42% 30% 35% 32%

BALANCE SHEET (US$ 000's) 2013 2014 2015E 2016E

Assets

Cash & Equivalents 27,591 33,775 60,676 99,308

Total Current Assets 66,952 62,750 82,424 115,244

Mining Assets 128,243 157,794 147,734 149,992

Total Assets 234,842 256,129 260,001 295,079

Liabilities

Current Liabilities

Trade & Other Payables 36,276 30,579 22,649 17,500

Interest Bearing Loans and Borrowings 9,676 3,887 3,160 3,160

Total Current Liabilities 51,642 50,150 32,959 27,809

Non Current Liabilities

Interest Bearing Loans and Borrowing 24,568 25,205 23,432 23,432

ARO 36,588 35,555 31,623 31,623

Total Liabilities 135,122 132,348 88,014 82,864

Shareholders' Equity

Share Capital 306,773 322,303 330,075 336,804

Equity Reserves 21,493 21,844 21,990 21,990

Accumulated Other Comp. Income (21,269) (33,041) (38,657) (38,657)

Retained Earnings (deficit) (207,276) (187,324) (141,421) (107,922)

Total Equity 99,721 123,781 171,987 212,215

Total Liabilities & Shareholders' Equity 234,842 256,129 260,001 295,079

Source: Newmarket Gold Inc., Raymond James Ltd.

Canada Research | Page 24 of 32 Newmarket Gold Inc. Newmarket Gold Inc.

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Cash Flow Statement (US$ 000's) 2013 2014 2015E 2016E

Operating Activities

Net Income (92,766) 19,952 44,642 30,979

Add:Non-Cash items:

Depreciation & Depletion 76,857 39,424 42,163 48,742

Stock Based Comp 921 368 242 0

Impairments etc. 92,687 (7,357) 1,108 0

Operating CF before changes in WC 73,849 73,020 93,197 82,241

Net change in non-cash WC (6,386) 1,137 (713) 662

Cash flow from Operations 67,463 74,157 92,483 82,903

CFO/ diluted share (Excluding WC) 0.18 0.15 0.59 0.52

Investing Activities

Capital Expenditures (67,578) (59,437) (47,401) (51,000)

Cash flow from Investing (68,156) (70,996) (85,138) (51,000)

Financing Activities

Cash flow from Financing 10,177 5,405 21,480 6,729

Net Change in Cash 2,850 6,184 26,900 38,632

Cash, BOP 24,741 27,591 33,775 60,676

Cash, EOP 27,591 33,775 60,676 99,307

Free Cash Flow

Free Cash Flow (5,298) 7,414 37,858 31,241

FCF/Diluted Share (0.01) 0.02 0.24 0.20

Source: Newmarket Gold Inc., Raymond James Ltd.

Newmarket Gold Inc. Canada Research | Page 25 of 32

Raymond James Ltd. | 2100 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2

Appendix C: Corporate Tearsheet

RAYMOND JAMES LTD. RESEARCH

Rating: OUTPERFORM 2 Share Price: $1.09 Analyst: Chris Thompson 604 659 8439

6-12 Mth Target C$ 1.70 NAVPS $1.37 Associate: Brian Martin 604 654 1236

Projected Return: 56% YR-END: 31-Dec

Reporting Currency: US

Investment Thesis Management % Ownership Significant Shareholders % Ownership

Management/Insiders 10% Luxor Capital Group LP 43%

Lloyd Miller 5%

Greywolf Capital Management LP 3%

Key Attributes:

Market Statistics

- Benefited from a weakening A$ vs. US$ = Significant cost reductions Share Price C$ 1.09 Shares Basic (mln) 134.2

- Stable ~200 k oz producer with competitive AISC profile 52 Week High/Low (C$) 1.35 - 0.13 Shares Fully Diluted (mln) 190.9

- Management has successfully mine lives through exploration Market Cap. (C$mln) $146 Adj. Shares used in NAV calc (mln) 190.9

- Exploration Upside Enterprise Value (C$mln) $115 Avg Daily Volume: 333

Financial Metrics 2013A 2014A 2015E 2016E 2017E

Cash & Equiv. (mlns) 28 34 61 99 140

Key Concerns Working capital (mlns) 15 13 49 87 128

-Development Risk -Cost Inflation -Gold Price Risk Current ratio (x) 1.3x 1.3x 2.5x 4.1x 5.6x

-Political Risk -Operational / Labour Risk Debt (mlns) 34 - - - -

Common Equity (mlns) 100 124 172 212 247

(As of Dec-31-14) Project Category Tonnes (000) Au (g/t) Au (k oz) Price/book (x) 1.1x 1.0x 0.9x 0.7x 0.6x

Fostervil le P&P 1,458 6.57 308 ROE 0% 16% 26% 15% 13%

Reserves Cosmo P&P 1,295 3.57 149

Stawell P&P 3,727 1.50 180 CFO (US$mln) 67 74 92 83 83

Other P&P 2,770 3.35 299 CFI (US$mln) (68) (71) (85) (51) (43)

Total 9,250 3.14 935 CFF (US$ mln) 10 5 21 7 0

Resources FCF (US$mln) (5) 7 38 31 41

Fostervil le M&I + Inf 22,500 3.94 2,850

Cosmo M&I + Inf 5,967 3.25 623

Stawell M&I + Inf 5,137 2.00 330

Other M&I + Inf 44,500 2.08 2,981 Earnings/Cash Flow 2013A 2014A 2015E 2016E 2017E

Total M&I + Inf 78,104 2.70 6,784 RJL Gold Forecast US$/oz 1,413 1,266 1,178 1,150 1,150

Revenue ($mln) 300.8 282.7 267.7 257.8 253.9

Adj. EBITDA ($mln) 126.3 84.5 92.6 82.2 83.3

Operating Summary 2013 2014 2015E 2016E 2017E EBITDA margin (%) 42% 30% 35% 32% 33%

Production - Au (k oz) - 100% basis EV/EBITDA (x) 0.6 0.8 0.8 0.9 0.9

Fostervil le 98 105 113 110 112 Net Earnings ($mln) -92.8 20.0 44.6 31.0 32.0

Cosmo 74 78 77 80 73 Adj. Earnings ($ mlns) 54.4 33.0 43.3 31.0 32.0

Stawell 38 39 38 34 36

Total - Au (k oz) 211 222 228 224 221 Adj. EPS (US$) 0.13 0.07 0.25 0.21 0.22

P/E (x) 1.5x 2.9x 3.3x 3.8x 3.7x

Cash Costs (US$/oz Au) CFPS (US$) 0.18 0.15 0.59 0.52 0.53

Fostervil le 829 738 572 596 586 P/CF (x) 1.1x 1.3x 1.4x 1.6x 1.6x

Cosmo 1162 997 834 827 905

Stawell 1288 1151 856 887 705 Capex ($mln) (73) (67) (54) (51) (43)

Consolidated (US$/oz) 1029 901 708 722 711

AISC (US$/oz) 1365 1211 986 958 954

Valuation (C$)

Blended Target Price Value Multiple % Weighted Target Value

2016 CFPS (C$) $0.65 3.0x $0.50 $0.98

NAVPS (C$) $1.37 1.0x $0.50 $0.69

$1.67

Target Price $1.70

Return to Target 56%

P/NAV 0.71x

Target P/NAV 1.34x

P/CFPS (2016E) 1.57x

Target P/CFPS (2016E) 2.60x

US$/C$ FX Rate $0.80

US$/A$ FX Rate $0.75

Share Count Used in Valuation (000's) - FD ITM 190,869

RJL Covered Gold's P/CFPS Multiples (2016E) RJL Covered Gold's P/NAV Multiples

Newmarket Gold Inc.

Newmarket Gold produces ~200 k oz year from three gold mines in Australia.

- Sustainable FCF Generation in current metal price environment

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

AS

R

NM

I

NG

D

AG

I

ED

V

YR

I

MN

D

DG

C

BT

O

SM

F K

TH

O

ELD

AB

X G

IMG

AE

M

P/N

AV

(x

)

P/NAV Target P/NAV

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

NM

I