Embed Size (px)

Citation preview

Building a Strategic Position

in the Fluorspar Sector

Company Presentation

AGM February 19th 2014 1

Disclaimer

The content of information contained in these slides and the accompanying verbal presentation (together, the “Presentation”) has not been approved by an authorised person within the meaning of the

Financial Services and Markets Act 2000 (“FSMA”). Reliance upon this Presentation for the purpose of engaging in any investment activity may expose an individual to a significant risk of losing all of

the property or other assets invested. If any person is in any doubt as to the contents of this Presentation, they should seek independent advice from a person who is authorised for the purposes of

FSMA and who specialises in advising in investments of this kind.

This Presentation is being supplied to you solely for your information. This Presentation has been prepared by, and is the sole responsibility of, Tertiary Minerals plc (the “Company”). The directors of the Company

have taken all reasonable care to ensure that the facts stated herein are true to the best of their knowledge, information and belief.

This Presentation does not constitute, or form part of, an admission document, listing particulars or a prospectus relating to the Company, nor does it constitute, or form part of, any offer or invitation to sell or issue, or

any solicitation of any offer to purchase or subscribe for, any shares in the Company nor shall it or any part of it, or the fact of its distribution, form the basis of, or be relied upon in connection with, or act as any

inducement to enter into any contract therefor.

No reliance may be placed for any purpose whatsoever on the information contained in this Presentation or on its completeness, accuracy or fairness thereof, nor is any responsibility accepted for any errors,

misstatements in, or omission from, this Presentation or any direct or consequential loss however arising from any use of, or reliance on, this Presentation or otherwise in connection with it.

By accepting this Presentation you confirm, represent and warrant that you have consented to receive information in respect of securities of the Company and other price-affected securities (as defined in the Criminal

Justice Act 1993 (“CJA”)) which makes you an “insider” for the purposes of Part V of the CJA, and you agree not to deal in any securities of the Company until such time as the inside information (as defined in the CJA)

of which you have been made aware has been made public for the purposes of the CJA.

This Presentation may not be reproduced or redistributed, in whole or in part, to any other person, or published, in whole or in part, for any purpose without the prior consent of the Company. The contents of this

Presentation are confidential and are subject to updating, completion, revision, further verification and amendment without notice.

The Presentation is being distributed on request only to, and is directed at, authorised persons or exempt persons within the meaning of FSMA or any order made thereunder or to those persons falling within the

following articles of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended) (the “Financial Promotion Order”): Investment Professionals (as defined in Article 19(5)) and High Net

Worth Companies (as defined in Article 49(2)). Persons who do not fall within any of these definitions should not rely on this Presentation nor take any action upon it but should return it immediately to the Company.

This Presentation is exempt from the general restriction in section 21 of FSMA relating to the communication of invitations or inducements to engage in investment activity on the grounds that it is made only to certain

categories of persons.

Neither this Presentation nor any copy of it should be distributed, directly or indirectly, by any means (including electronic transmission) to any persons with addresses in the United States of America (or any of its

territories or possessions) (together, the “US”), Canada, Japan, Australia, the Republic of South Africa or the Republic of Ireland, or to any corporation, partnership or other entity created or organised under the laws

thereof, or in any other country outside the United Kingdom where such distribution may lead to a breach of any legal or regulatory requirement. The recipients should inform themselves about and observe any such

requirements or relationship.

The Company’s ordinary shares have not been, and are not expected to be, registered under the United States Securities Act 1933, as amended, (the “US Securities Act”) or under the securities laws of any other

jurisdiction, and are not being offered or sold, directly or indirectly, within or into the US, Canada, Japan, Australia, the Republic of South Africa or the Republic of Ireland or to, or for the account or benefit of, any US

persons or any national, citizen or resident of the US, Canada, Japan, Australia, the Republic of South Africa or the Republic of Ireland, unless such offer or sale would qualify for an exemption from registration under

the US Securities Act and/or any other applicable securities laws.

Past Performance

This Presentation contains statements regarding the past performance of the Company’s ordinary shares. Past performance cannot be relied upon as a guide to future performance.

Forward-looking Statements

This Presentation or documents referred to in it contain forward-looking statements. These statements relate to the future prospects developments and business strategies of the Company and its subsidiaries (the

“Group”). Forward-looking statements are identified by the use of such terms as “believe”, “could”, “envisage”, “estimate”, “potential”, “intend”, “may”, “plan”, “will” or the negative of those, variations or comparable

expressions, including references to assumptions. The forward-looking statements contained in this Presentation are based on current expectations and are subject to risks and uncertainties that could cause actual

results to differ materially from those expressed or implied by those statements. If one or more of these risks or uncertainties materialises, or if underlying assumptions prove incorrect, the Group’s actual results may

vary materially from those expected, estimated or projected. Given these risks and uncertainties, potential investors should not place any reliance on forward-looking statements. These forward-looking statements

speak only as at the date of this Presentation.

No undertaking, representation, warranty or other assurance, expressed or implied, is made or given by or on behalf of the Company or any of its directors, officers, partners, employees or advisers or any other person

as to the accuracy or the completeness of the information or opinions contained herein and to the extent permitted by law no responsibility or liability is accepted by any of them for any such information or opinions.

Notwithstanding the aforesaid, nothing in this paragraph shall exclude liability for any representation or warranty made fraudulently. 8 January 2013

2

Senior Management

• Geologist

• Company Founder, 26 years in public mineral company management

• Founder Dragon Mining Ltd, Archaean Gold NL & Sunrise Resources plc

1. Patrick Cheetham

Executive Chairman

• Chartered Engineer

• 20+ years experience in managing and developing mining projects worldwide for Derwent Mining, Lafarge, Hargreaves (GB) Ltd, Marshalls plc & CFE

2. Richard Clemmey

Managing Director

• Accountant

• Formerly Finance Director, Mwana Africa plc, Ridge Mining & Reunion Mining

3. Donald McAlister

Non-Executive Director

• Geologist

• Former CEO, Exploration & Development, Billiton Plc & Chairman ENK plc

• Director Consolidated Mines and Investments Ltd

4. David Whitehead

Non-Executive Director

• Barrister-at-Law & Chartered Secretary

• Formerly Corporate Finance Director Kleinwort Benson

5. Colin Fitch LLM, FCIS

Company Secretary

4 5 1 2 3

3

Company Aims, Strategy and

Business Plan

The Opportunity

• Fluorspar is an essential raw material in the chemical, steel and aluminium industries and in a

growing number of high-tech green technologies and pharmaceutical applications

• Fluorspar has a growing economic and strategic importance; ranked the fourth most important

strategic mineral in the US; identified by the European Commission as one of fourteen critical

raw materials facing a supply shortage

Company’s Aim

• To become a reliable long-term and competitive

supplier of fluorspar to the world markets

• To add value to the Group’s mineral projects

through the discovery of mineral resources

Company Strategy

• To acquire and develop large fluorspar deposits:

located to established infrastructure and markets

in stable, democratic and mining friendly jurisdictions

EXPLORATION

MB Fluorspar Project

Nevada USA

FEASIBILITY & PLANNING

Lassedalen Fluorspar Project, Norway

Storuman Fluorspar Project, Sweden

DEVELOPMENT MINING

CLOSURE & REHABILITATION

4

Fluorspar Market

Global Fluorspar Demand

6.5Mt/year

Acid Grade/Acid-spar

58% - 3.8 Mt/year

Hydrogen Fluoride HF

40% - 2.6 Mt/yr

Fluorocarbons - 2.16 Mt/year

e.g. refrigerants

Fluoropolymers

e.g. lithium batteries

Fluorochemicals

e.g. Electronics, Thermoplastics, Medicine, Metallurgy, Water, Detergents and Glass Aluminium Fluoride

AlF3

18% - 1.2 Mt/year

Metallurgical Grade/Met-spar & Ceramic Grade

42% - 2.7 Mt/year

Flux in Steel Production, Cement, Enamels,

Cooking Utensils, Glass, Glass Fibre

The Fluorine Supply Chain

• Fluorspar is the commercial name for concentrates of the mineral Fluorite, CaF2

• Fluorite is the main industrial source of Fluorine, F

• Major western acid-spar consumers: DuPont, Honeywell, Solvay, Lanxess, Boliden, Fluorsid,

DDF

5 Source: Industrial Minerals Magazine, Roskill, CRU, UN, USGS, CCM, Company Data

0 1,000,000 2,000,000

ChinaEuropeMexico

South AfricaCIS

MongoliaKenya

NamibiaMorocco

ArgentinaIran

BrazilIndiaUSA

CanadaJapan

Acidspar Production and Demand by Region 2011 (t)

Est Demand

Production

0

100

200

300

400

500

600P

rice U

S$/t

Average Acid-Spar Prices 2000-2013

FOB China

CIF Rotterdam

Fluorspar Market Dynamics

0

500000

1000000

1500000

2000000

2500000

China Acidspar Export vs Internal Consumption 2005 - 2012 (t)

China InternalConsumption

China Export CaF2>97%

40% 14%

• China produces >50% of the worlds fluorspar

• The price of acid-spar has increased >3 fold

since 2000

• Chinese exports have declined substantially

since 2000

• China may become a net importer in the future

• USA, Canada and Europe – largest acid-spar

consumers outside of China

Source: Industrial Minerals Magazine, Roskill, CRU, UN, USGS, CCM, Company Data

6

Storuman Fluorspar Project

Excellent Location & Infrastructure

• Adjacent to the main E12 highway

• Storuman town and new bulk rail terminal – 25 km

• Road and rail linked to Umeå Port – 240 km

Lars Lind

Umeå

7

Storuman Fluorspar Project

8m Glacial Till

Var. Shale

1m Transition unit

10m “Upper” quartzite horizon

2m Transition unit

10m “Lower” sandstone horizon

2m Cambrian Conglomerate

Proterozoic Granite Basement

Geology

• Horizontally bedded, replacement style mineralisation in “Upper” and “Lower” Zones

• Mineralisation up to 20m thick

NB: vertical scale x 4

Surface Topography

Pink Fluorspar Mineralisation in

the “Lower” Horizon Drill Core

8

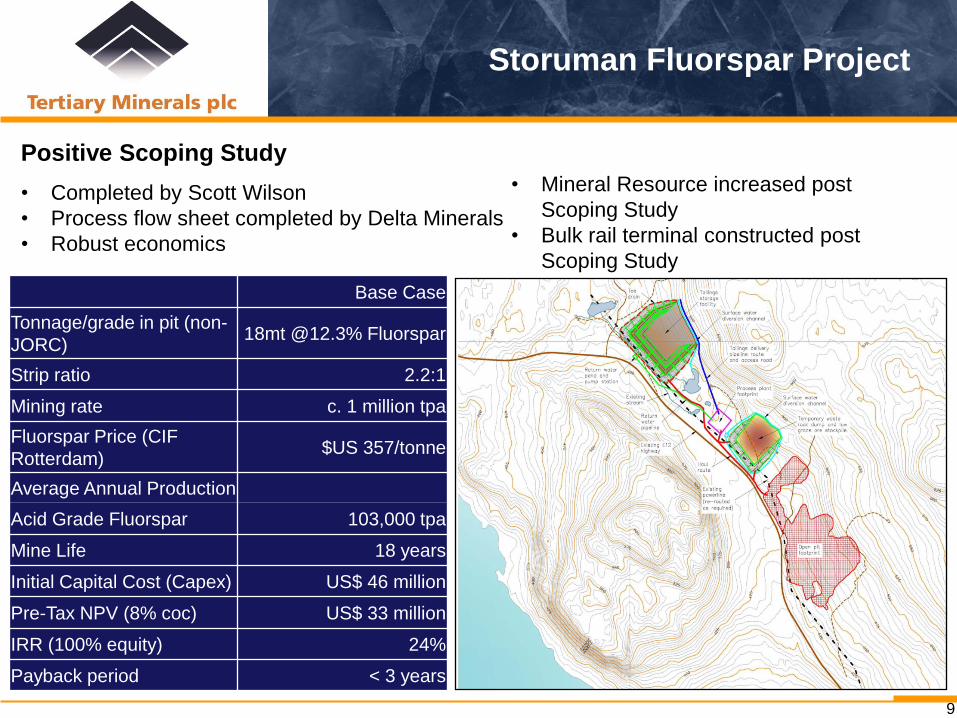

Storuman Fluorspar Project

Positive Scoping Study

• Completed by Scott Wilson

• Process flow sheet completed by Delta Minerals

• Robust economics

Base Case

Tonnage/grade in pit (non-

JORC) 18mt @12.3% Fluorspar

Strip ratio 2.2:1

Mining rate c. 1 million tpa

Fluorspar Price (CIF

Rotterdam) $US 357/tonne

Average Annual Production

Acid Grade Fluorspar 103,000 tpa

Mine Life 18 years

Initial Capital Cost (Capex) US$ 46 million

Pre-Tax NPV (8% coc) US$ 33 million

IRR (100% equity) 24%

Payback period < 3 years

• Mineral Resource increased post

Scoping Study

• Bulk rail terminal constructed post

Scoping Study

9

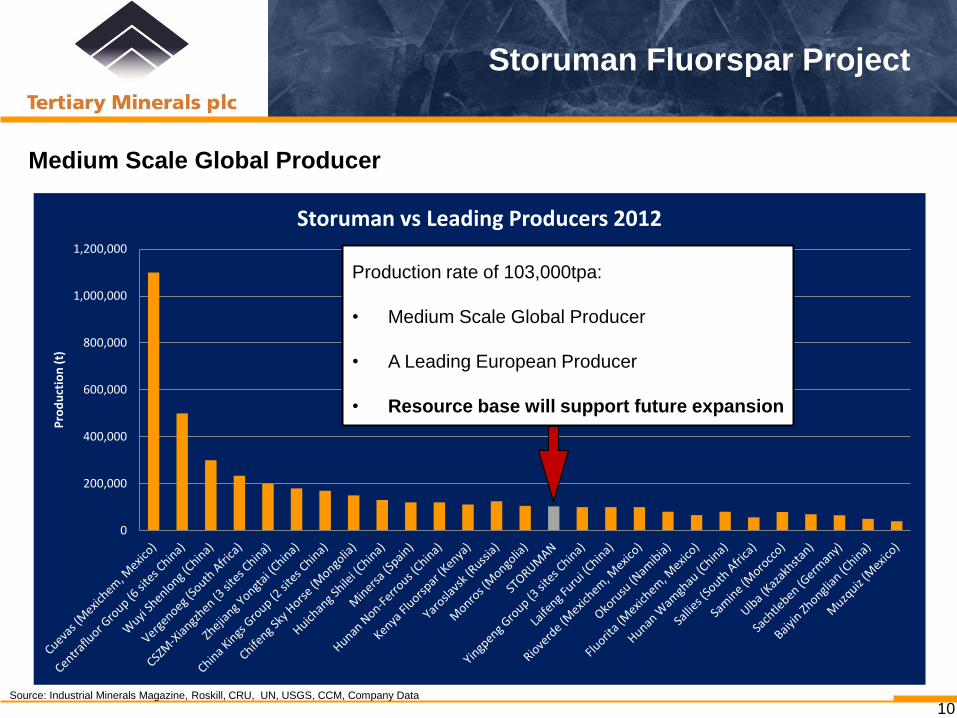

Storuman Fluorspar Project

Medium Scale Global Producer

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

Pro

du

ctio

n (

t)

Storuman vs Leading Producers 2012

Production rate of 103,000tpa:

• Medium Scale Global Producer

• A Leading European Producer

• Resource base will support future expansion

10 Source: Industrial Minerals Magazine, Roskill, CRU, UN, USGS, CCM, Company Data

Storuman Fluorspar Project

Drilling (2010) & JORC Mineral Resource Estimate (SRK 2011)

• 46 diamond core drill holes

• 28% increase in resource compared with Scoping Study

Classification Million Tonnes (Mt) Fluorspar (CaF2%)

Indicated 25 10.28

Inferred 2.7 9.57

Total 27.8 10.21

Drilling (2011)

• Potential step-change for

scale of mineralisation

• Waste:ore strip ratio reduced

• 2.2t:1t to 0.8t:1t

11

Mining and Processing

• Low waste : ore ratio and horizontal ore horizons with no fluorspar mineralisation in the

granite basement lends itself to cut and fill mining technique (progressive restoration)

• Processing method is common in the mining industry – not bespoke

Open pit mining – cut

and fill Crushing Grinding

Flotation – fluorspar

concentration Silica tailings

Fluorspar concentrate for shipping

Storuman Fluorspar Project

12

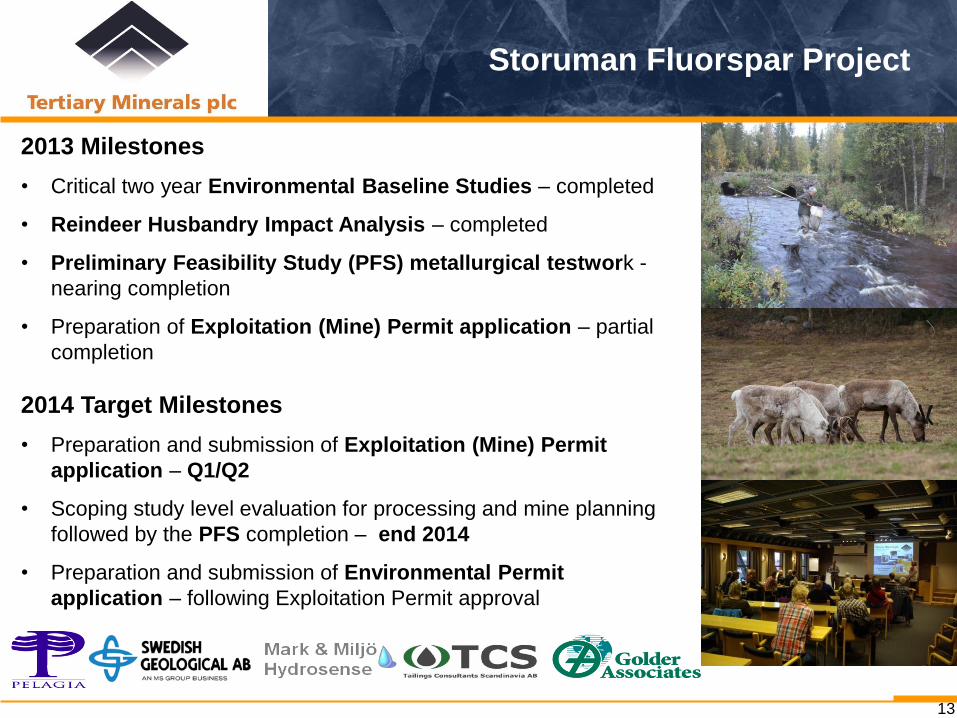

Storuman Fluorspar Project

2013 Milestones

• Critical two year Environmental Baseline Studies – completed

• Reindeer Husbandry Impact Analysis – completed

• Preliminary Feasibility Study (PFS) metallurgical testwork -

nearing completion

• Preparation of Exploitation (Mine) Permit application – partial

completion

2014 Target Milestones

• Preparation and submission of Exploitation (Mine) Permit

application – Q1/Q2

• Scoping study level evaluation for processing and mine planning

followed by the PFS completion – end 2014

• Preparation and submission of Environmental Permit

application – following Exploitation Permit approval

13

MB Fluorspar Project

Nevada - Most Favourable Mining

Jurisdiction in the USA

• Located 14km SW of Eureka, Eureka County,

Nevada

• Trans-national road and rail links, rail 161 km

from the project location

• 780 km to port of San Francisco

• Road access to and over property

• Government land – no special status

• 84% of Eureka County population employed in

mining industry

14

MB Fluorspar Project

2013 Milestones

• Independent Tonnage-Grade Estimate classified as an Exploration Target under JORC

Classification Million Tonnes (Mt) Fluorspar (CaF2%)

Exploration Target (8% CaF2 cut-off) 85 to 105 9 to 11

Exploration Target (2% CaF2 cut-off) 395 to 615 5 to 7

• Phase 1 drilling programme

4 holes, 550 metres

Twin diamond and percussion drilling

Evaluate the most cost-effective technique

Completed September 2013

• Phase 2 drilling programme

22 percussion holes, 2670 metres

Define a JORC resource and potential mine-starter pit

Target potential higher grade zones

Test alternative site for mine-starter pit

Completed November 2013

15

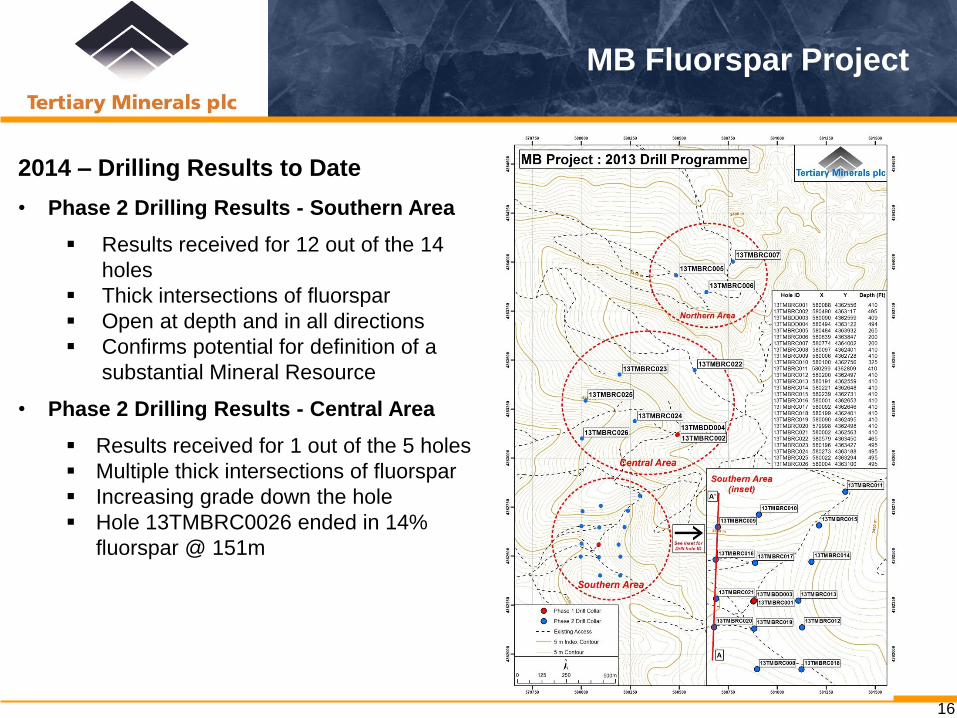

MB Fluorspar Project

2014 – Drilling Results to Date

• Phase 2 Drilling Results - Southern Area

Results received for 12 out of the 14

holes

Thick intersections of fluorspar

Open at depth and in all directions

Confirms potential for definition of a

substantial Mineral Resource

• Phase 2 Drilling Results - Central Area

Results received for 1 out of the 5 holes

Multiple thick intersections of fluorspar

Increasing grade down the hole

Hole 13TMBRC0026 ended in 14%

fluorspar @ 151m

16

MB Fluorspar Project

2014 – Target Milestones

• Results for the balance 6 holes

• JORC Mineral Resource Estimate – Q1 2014

• Metallurgical testwork followed by Scoping Study – end 2014

17

Open Open

Lassedalen Fluorspar Project

Excellent Location & Infrastructure

• 500m from highway E134 & Railway

• 6km from famous silver mining town of Kongsberg

• 50km from Port of Drammen

• 80km SW of City of Oslo

18

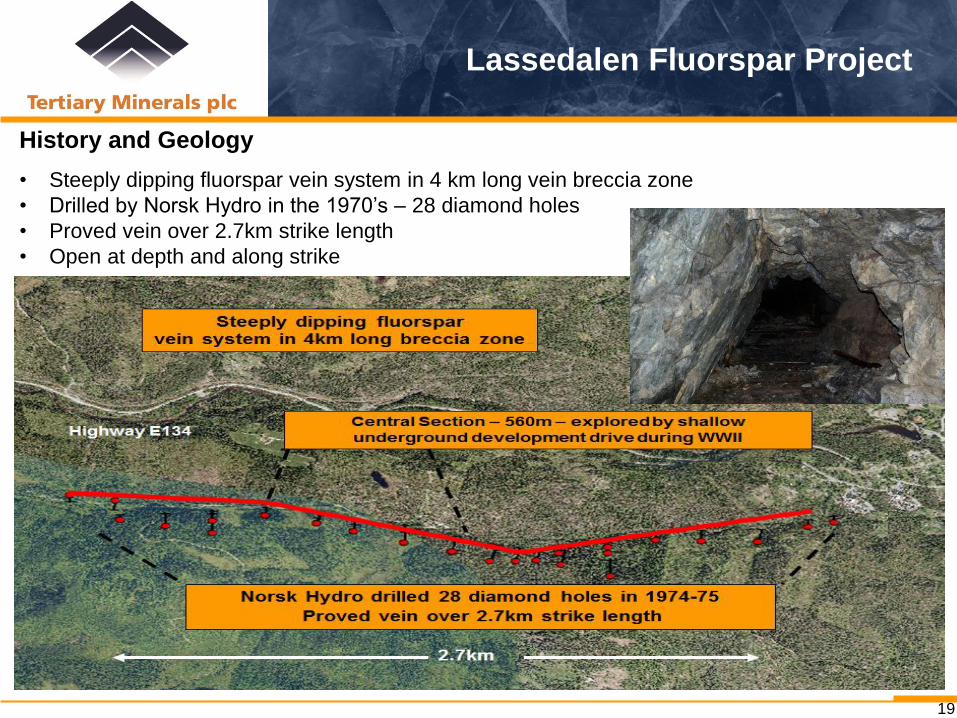

Lassedalen Fluorspar Project

History and Geology

• Steeply dipping fluorspar vein system in 4 km long vein breccia zone

• Drilled by Norsk Hydro in the 1970’s – 28 diamond holes

• Proved vein over 2.7km strike length

• Open at depth and along strike

19

Lassedalen Fluorspar Project

Milestones Achieved

• JORC Mineral Resource Estimate (SRK Consulting) – 2012

• Re-logged and sampled 3.5 km of drill core from 23 of the 28 diamond holes drilled in the

1970’s

• Scoping Study (Wardell Armstrong International) - 2012

Classification Million Tonnes (Mt) Fluorspar (CaF2%)

Inferred 4 24.6

Base Case Extended Mine Case

Tonnage Mined (underground) 3.6mt @ 22.4% Fluorspar 4.5mt @22.4% Fluorspar

Mining rate 543,000 tpa 543,000 tpa

Fluorspar Price (CIF Rotterdam) $US 491/tonne $US 491/tonne

Average Annual Production

Acid Grade Fluorspar 100,000 tpa 100,000 tpa

Mine Life 6.6 years 8.25 years

Initial Capital Cost (Capex) US$ 78 million US$ 78 million

Pre-Tax NPV (10% coc) US$ 31.6 million US$ 52.2 million

IRR (100% equity) 20.20% 24.10%

20

Fluorspar Project Timetable

Fluorspar Projects - Indicative Schedule

Storuman 2014

Q1 Q2 Q3 Q4

Pre-Feasibility Study (PFS) Metallurgical Testwork Complete

Scoping Study evaluation followed by full Pre-Feasibility Study (PFS) Complete

Exploitation (Mining) Permit Submit

Environmental Permit Submit ?

Target production date - 2017

MB Project 2014

Q1 Q2 Q3 Q4

Phase 2 Drilling Results Complete

Maiden JORC Mineral Resource Estimate Complete

Metallurgical Testwork and Scoping Study Complete

Lassedalen 2014

Q1 Q2 Q3 Q4

PFS Drilling and JORC (indicated)

Project currently on hold - prioritise Storuman and MB Project

Note: All schedules are subject to change, funding and successful completion of each phase of work

21

Non-Core Projects

• Kaaresselkä - Kiekerömaa - Gold, Finland

Kaaresselkä licence renewal granted in March 2013

Re-evaluating historic exploration results

• Rosendal Tantalum Project, Finland

Evaluating production opportunities and how best to valorise the project

• Ghurayyah Tantalum–Niobium-Rare-Earth Project, Saudi Arabia

Re-issue of licence pending with Deputy Ministry for Mineral Resources in Saudi

Arabia.

Other Projects

22

Investment Case

BROKER RESEARCH - Price Targets

Cantor Fitzgerald Europe

16p per share 20 Aug 2013

VSA Capital 21p per share 13 Feb. 2013

Valuations based on Fluorspar peer group comparison

and deal metrics

• Broker research suggest shares are undervalued

• Tertiary Minerals plc is the only UK public traded

company offering an exciting exposure to looming

fluorspar market shortage

• Fluorspar market is going through a “paradigm

shift” – with China evolving from a large net

exporter to a potential net importer

• Scoping Study on the Storuman fluorspar project (Sweden) shows robust economics, highly

levered to rising fluorspar price

• Positive October 2011 drill results deliver step-change in expectations for ultimate size of

Storuman deposit. Working towards PFS and mine permits

• January 2012 JORC Resource Estimate at Lassedalen in Norway adds 1Mt fluorspar to 3Mt

Storuman resource - second European fluorspar project in pipeline

• 2012 Scoping Study on the Lassedalen fluorspar project (Norway) shows positive economics,

levered to mine life – further drilling required

• New MB Fluorspar Project, Nevada, USA – World Class Potential. Exploration Target minimum

8Mt contained fluorspar – first drilling programme completed, Maiden JORC Mineral Resource

Estimate expected Q1 2014

23

Building a Strategic Position

in the Fluorspar Sector

For further information please contact:

Tertiary Minerals plc Patrick Cheetham/ Richard Clemmey

Tel: +44 (0)845 868 4580 [email protected] [email protected]

Nominated Adviser & Joint Broker Cantor Fitzgerald Europe Stewart Dickson/ Jeremy Stephenson

Tel: +44 (0)207 894 7000 [email protected] [email protected]

Joint Broker Beaufort Securities Ltd Christopher Rourke/ Guy Wheatley

Tel: +44 (0)207 382 8300 [email protected] [email protected]

Public Relations Yellow Jersey PR Dominic Barretto/ Kelsey Traynor Tel: +44 (0)20 3664 4087 [email protected] [email protected]

THANK YOU FOR YOUR TIME AND SUPPORT

This presentation is available on our website: www.tertiaryminerals.com

24