Embed Size (px)

Citation preview

Fluorspar is a commercial term for the miner-al fluorite (calcium fluoride, CaF2) which,

when pure contains 51.1% Ca and 48.9% F andis the most important and only UK source ofthe element fluorine (F).There are three maingrades — acid, metallurgical and ceramic. AllUK output is acid-grade fluorspar (>97%, CaF2),used principally in the production of hydrofluo-

ric acid (HF), the starting point for the manufac-ture of a wide range of fluorine-bearing chemi-cals.

Demand

Acid-grade fluorspar is a critical raw materialfor the UK fluorochemicals industry. Most(95%) is used in the manufacture of HF, whichin addition to being an important product in itsown right, is the key intermediate for the man-ufacture of all specialty fluorine-bearing chemi-

cals, notably fluorocarbons. Minor uses ofacid-grade fluorspar include, the manufactureof welding rods, aluminium and steel.

Demand for fluorspar in the UK is principallydriven by demand for HF and associated fluo-rochemical production. In the past this was forchlorofluorocarbon (CFC) production, but CFCproduction was banned in developed countriesfrom 1st January 1996 because of the ozonedepleting nature of the chlorine these sub-stances contain. This resulted in a decline indemand for HF and, consequently, fluorspar.

Hydrochlorofluorocarbons (HCFCs) are used asraw materials to make fluoropolymers, the pro-duction of which is generally increasing global-ly. In addition, HCFCs are used as transitoryreplacements for CFCs. This use is beingphased out and replaced by hydrofluorocar-bons (HFCs), which contain much higher fluo-rine contents. Future demand for HF, and thusacid-grade fluorspar, will depend on the suc-cess of these alternatives in retaining andexpanding market share and the growth ofHFCs used as feedstock for fluoropolymer pro-duction. Fluorine chemicals have many uses,including in refrigeration and air-conditioningsystems, as foam blowing agents, non-stickcoatings, aerosols, including medical propel-lants, anaesthetics, in pharmaceutical productsand for specialised cleaning applications. HF isalso supplied to home and export markets forthe manufacture of high-octane petrol, deter-gents, for metal pickling, as a specialisedetchant for crystal glass, the production of sili-con chips and other electronic applications, andin uranium processing.

Supply

Significant production of fluorspar in the UKbegan at the beginning of the 20th century withits use as a flux in steelmaking. Today steelmak-ing is a relatively minor use. Productionincreased with rising demand for fluorochemi-cals and peaked at 235 000 tonnes in 1975.Production has been on a downward trend since(Figure 1), because of a decline in demand bythe chemical and steel sectors and the closure ofsome producers. However, production has nowstabilised and increased somewhat.

Fluorspar

1

Mineral Planning Factsheet

Fluorspar

Fluorspar workingin Derbyshire.

This factsheet pro-vides an overviewof fluorspar supplyin the UK. It is oneof a series on eco-nomically-impor-tant minerals thatare extracted inBritain and It is pri-marily intended toinform the land-useplanning process.

January 2006

Fluorspar

Fluorspar 2

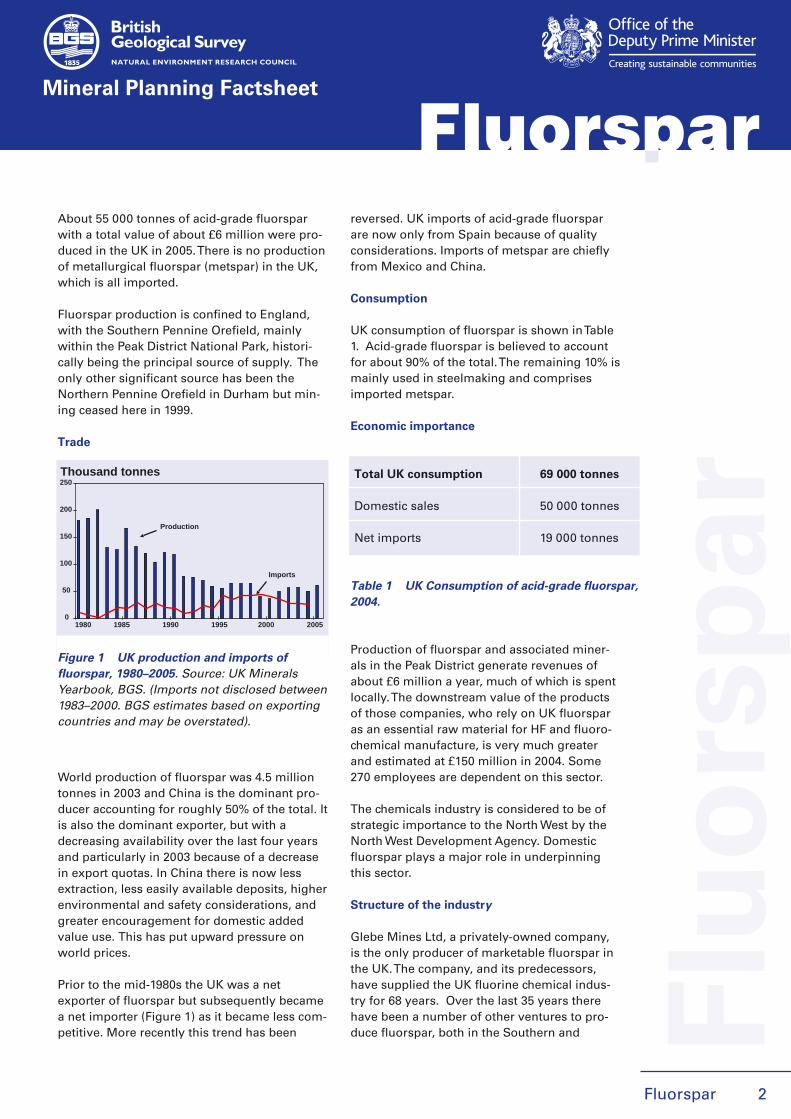

About 55 000 tonnes of acid-grade fluorsparwith a total value of about £6 million were pro-duced in the UK in 2005. There is no productionof metallurgical fluorspar (metspar) in the UK,which is all imported.

Fluorspar production is confined to England,with the Southern Pennine Orefield, mainlywithin the Peak District National Park, histori-cally being the principal source of supply. Theonly other significant source has been theNorthern Pennine Orefield in Durham but min-ing ceased here in 1999.

Trade

World production of fluorspar was 4.5 milliontonnes in 2003 and China is the dominant pro-ducer accounting for roughly 50% of the total. Itis also the dominant exporter, but with adecreasing availability over the last four yearsand particularly in 2003 because of a decreasein export quotas. In China there is now lessextraction, less easily available deposits, higherenvironmental and safety considerations, andgreater encouragement for domestic addedvalue use. This has put upward pressure onworld prices.

Prior to the mid-1980s the UK was a netexporter of fluorspar but subsequently becamea net importer (Figure 1) as it became less com-petitive. More recently this trend has been

reversed. UK imports of acid-grade fluorsparare now only from Spain because of qualityconsiderations. Imports of metspar are chieflyfrom Mexico and China.

Consumption

UK consumption of fluorspar is shown in Table1. Acid-grade fluorspar is believed to accountfor about 90% of the total. The remaining 10% ismainly used in steelmaking and comprisesimported metspar.

Economic importance

Production of fluorspar and associated miner-als in the Peak District generate revenues ofabout £6 million a year, much of which is spentlocally. The downstream value of the productsof those companies, who rely on UK fluorsparas an essential raw material for HF and fluoro-chemical manufacture, is very much greaterand estimated at £150 million in 2004. Some270 employees are dependent on this sector.

The chemicals industry is considered to be ofstrategic importance to the North West by theNorth West Development Agency. Domesticfluorspar plays a major role in underpinningthis sector.

Structure of the industry

Glebe Mines Ltd, a privately-owned company,is the only producer of marketable fluorspar inthe UK. The company, and its predecessors,have supplied the UK fluorine chemical indus-try for 68 years. Over the last 35 years therehave been a number of other ventures to pro-duce fluorspar, both in the Southern and F

luo

rsp

ar

Mineral Planning Factsheet

0

50

100

150

200

250

1980 1985 1990 1995 2000 2005

Thousand tonnes

Production

Imports

Figure 1 UK production and imports of

fluorspar, 1980–2005. Source: UK MineralsYearbook, BGS. (Imports not disclosed between1983–2000. BGS estimates based on exportingcountries and may be overstated).

Total UK consumption 69 000 tonnes

Domestic sales 50 000 tonnes

Net imports 19 000 tonnes

Table 1 UK Consumption of acid-grade fluorspar,

2004.

Northern Pennine orefields. None have provedsustainable.

Glebe Mines operates the Cavendish Mill, nearStoney Middleton in the Peak District NationalPark. Fluorspar ore to supply the Mill is mainlyderived from Glebe’s own operations, butsmaller, ‘tributer’ producers also supply someore. The Cavendish Mill is the only source ofmarketable fluorspar in the UK. If it were toclose it is extremely unlikely that sufficientreserves of fluorspar could be identified to jus-tify the capital investment of a new plant atsome future date.

The main consumer of fluorspar, accounting forsome 95% of total sales, is the HF and fluoro-chemicals producers INEOS Fluor. INEOS Fluor(acquired from ICI in 2001) is a worldwide manu-facturer of fluorochemicals with its headquartersand main manufacturing facility in Runcorn.

Rhodia formerly produced anhydrous HF at itsplant at Avonmouth but this closed in October2004. The company will continue to manufacturefluorochemicals at Avonmouth and HF will needto be sourced from other suppliers, includingINEOS Fluor.

Resources

Fluorspar resources are restricted to two areasin England: the Southern and Northern Pennineorefields (see Figure 2). Fluorspar occurs mainlyas vein infillings in faults that cut limestones ofCarboniferous age. Intense alteration of lime-stone, and occasionally other vein wall rocks,has led to the formation of important replace-ment deposits adjacent to several major veins.

Fluorspar always occurs in association withother minerals, the most important commer-cially being barytes (BaSO4) and galena (PbS).The proportion present can be highly variabledepending on location within the orefield.

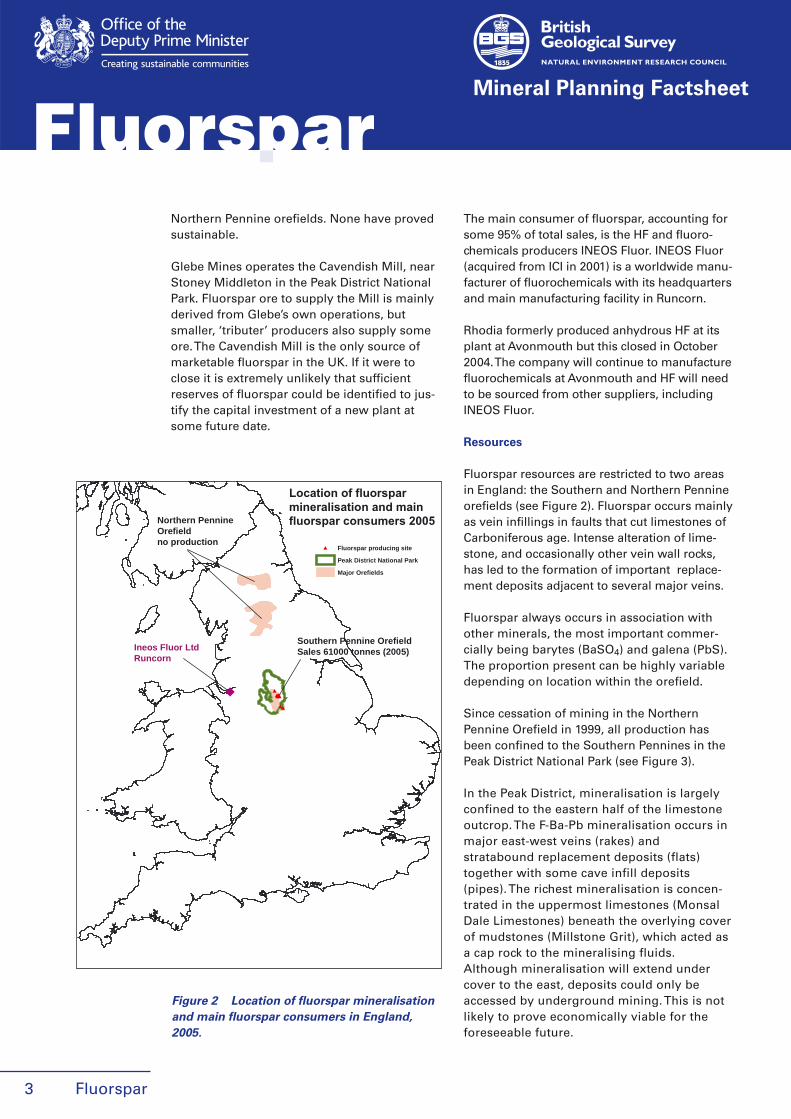

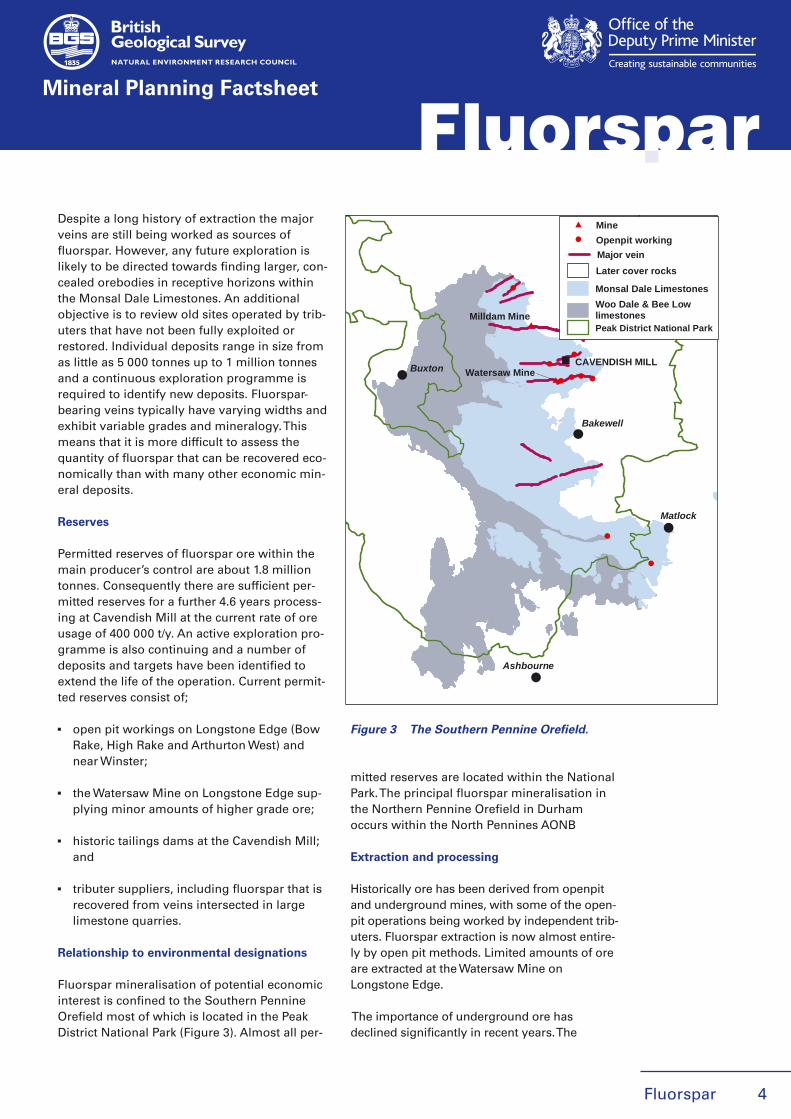

Since cessation of mining in the NorthernPennine Orefield in 1999, all production hasbeen confined to the Southern Pennines in thePeak District National Park (see Figure 3).

In the Peak District, mineralisation is largelyconfined to the eastern half of the limestoneoutcrop. The F-Ba-Pb mineralisation occurs inmajor east-west veins (rakes) andstratabound replacement deposits (flats)together with some cave infill deposits(pipes). The richest mineralisation is concen-trated in the uppermost limestones (MonsalDale Limestones) beneath the overlying coverof mudstones (Millstone Grit), which acted asa cap rock to the mineralising fluids.Although mineralisation will extend undercover to the east, deposits could only beaccessed by underground mining. This is notlikely to prove economically viable for theforeseeable future.

Fluorspar

Fluorspar

3

Mineral Planning Factsheet

Northern PennineOrefieldno production

Ineos Fluor LtdRuncorn

Southern Pennine OrefieldSales 61000 tonnes (2005)

Peak District National Park

Major Orefields

Fluorspar producing site

Figure 2 Location of fluorspar mineralisation

and main fluorspar consumers in England,

2005.

Fluorspar

Fluorspar 4

Despite a long history of extraction the majorveins are still being worked as sources offluorspar. However, any future exploration islikely to be directed towards finding larger, con-cealed orebodies in receptive horizons withinthe Monsal Dale Limestones. An additionalobjective is to review old sites operated by trib-uters that have not been fully exploited orrestored. Individual deposits range in size fromas little as 5 000 tonnes up to 1 million tonnesand a continuous exploration programme isrequired to identify new deposits. Fluorspar-bearing veins typically have varying widths andexhibit variable grades and mineralogy. Thismeans that it is more difficult to assess thequantity of fluorspar that can be recovered eco-nomically than with many other economic min-eral deposits.

Reserves

Permitted reserves of fluorspar ore within themain producer’s control are about 1.8 milliontonnes. Consequently there are sufficient per-mitted reserves for a further 4.6 years process-ing at Cavendish Mill at the current rate of oreusage of 400 000 t/y. An active exploration pro-gramme is also continuing and a number ofdeposits and targets have been identified toextend the life of the operation. Current permit-ted reserves consist of;

▪ open pit workings on Longstone Edge (BowRake, High Rake and Arthurton West) andnear Winster;

▪ the Watersaw Mine on Longstone Edge sup-plying minor amounts of higher grade ore;

▪ historic tailings dams at the Cavendish Mill;and

▪ tributer suppliers, including fluorspar that isrecovered from veins intersected in largelimestone quarries.

Relationship to environmental designations

Fluorspar mineralisation of potential economicinterest is confined to the Southern PennineOrefield most of which is located in the PeakDistrict National Park (Figure 3). Almost all per-

mitted reserves are located within the NationalPark. The principal fluorspar mineralisation inthe Northern Pennine Orefield in Durhamoccurs within the North Pennines AONB

Extraction and processing

Historically ore has been derived from openpitand underground mines, with some of the open-pit operations being worked by independent trib-uters. Fluorspar extraction is now almost entire-ly by open pit methods. Limited amounts of oreare extracted at the Watersaw Mine onLongstone Edge.

The importance of underground ore hasdeclined significantly in recent years. The

Mineral Planning Factsheet

CAVENDISH MILL

Milldam Mine

Bakewell

Buxton

Matlock

Ashbourne

Watersaw Mine

Monsal Dale Limestones

Major vein

Mine

Openpit working

Peak District National Park

Later cover rocks

Woo Dale & Bee Lowlimestones

Figure 3 The Southern Pennine Orefield.

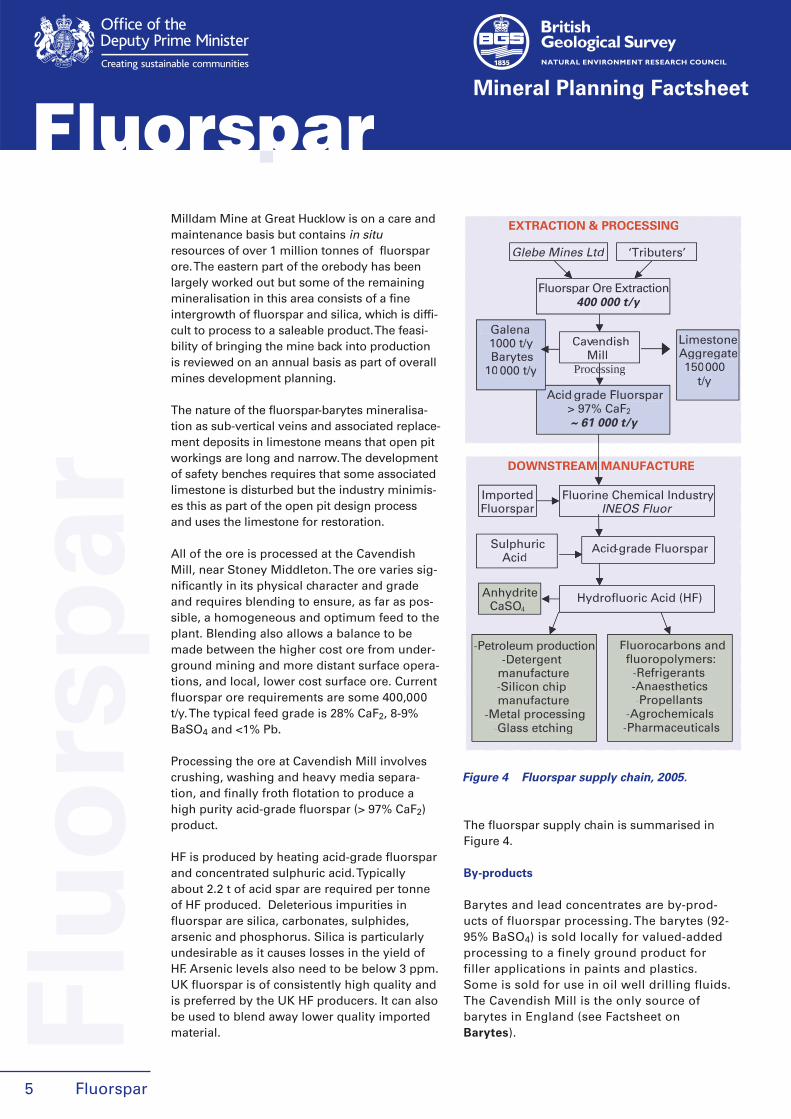

Milldam Mine at Great Hucklow is on a care andmaintenance basis but contains in situresources of over 1 million tonnes of fluorsparore. The eastern part of the orebody has beenlargely worked out but some of the remainingmineralisation in this area consists of a fineintergrowth of fluorspar and silica, which is diffi-cult to process to a saleable product. The feasi-bility of bringing the mine back into productionis reviewed on an annual basis as part of overallmines development planning.

The nature of the fluorspar-barytes mineralisa-tion as sub-vertical veins and associated replace-ment deposits in limestone means that open pitworkings are long and narrow. The developmentof safety benches requires that some associatedlimestone is disturbed but the industry minimis-es this as part of the open pit design processand uses the limestone for restoration.

All of the ore is processed at the CavendishMill, near Stoney Middleton. The ore varies sig-nificantly in its physical character and gradeand requires blending to ensure, as far as pos-sible, a homogeneous and optimum feed to theplant. Blending also allows a balance to bemade between the higher cost ore from under-ground mining and more distant surface opera-tions, and local, lower cost surface ore. Currentfluorspar ore requirements are some 400,000t/y. The typical feed grade is 28% CaF2, 8-9%BaSO4 and <1% Pb.

Processing the ore at Cavendish Mill involvescrushing, washing and heavy media separa-tion, and finally froth flotation to produce ahigh purity acid-grade fluorspar (> 97% CaF2)product.

HF is produced by heating acid-grade fluorsparand concentrated sulphuric acid. Typicallyabout 2.2 t of acid spar are required per tonneof HF produced. Deleterious impurities influorspar are silica, carbonates, sulphides,arsenic and phosphorus. Silica is particularlyundesirable as it causes losses in the yield ofHF. Arsenic levels also need to be below 3 ppm.UK fluorspar is of consistently high quality andis preferred by the UK HF producers. It can alsobe used to blend away lower quality importedmaterial.

The fluorspar supply chain is summarised inFigure 4.

By-products

Barytes and lead concentrates are by-prod-ucts of fluorspar processing. The barytes (92-95% BaSO4) is sold locally for valued-addedprocessing to a finely ground product forfiller applications in paints and plastics.Some is sold for use in oil well drilling fluids.The Cavendish Mill is the only source ofbarytes in England (see Factsheet onBarytes).

Fluorspar

Fluorspar

5

Flu

ors

par

Mineral Planning Factsheet

Glebe Mines Ltd

Fluorspar Ore Extraction400 000 t/y

Cavendish Mill

Processing

Acid-grade Fluorspar > 97% CaF2

~ 61 000 t/y

Fluorine Chemical IndustryINEOS Fluor

Acid-grade Fluorspar

Hydrofluoric Acid (HF)Anhydrite CaSO4

Imported Fluorspar

Sulphuric Acid

Limestone Aggregate150 000

t/y

Galena1000 t/yBarytes

10 000 t/y

Fluorocarbons and fluoropolymers:

-Refrigerants-Anaesthetics-Propellants

-Agrochemicals-Pharmaceuticals

-Petroleum production-Detergent

manufacture-Silicon chip manufacture

-Metal processing-Glass etching

‘Tributers’

EXTRACTION & PROCESSING

DOWNSTREAM MANUFACTURE

Fluorine Chemical IndustryINEOS Fluor

Acid-dd grade Fluorspar

Hydrofluoric Acid (HF)AnhydriteCaSO4

Imported Fluorspar

Sulphuric Acid

Fluorocarbons andfluoropolymers:

-Refrigerants-Anaesthetics-Propellants

-Agrochemicals-Pharmaceuticals

-Petroleum production-Detergent

manufacture-Silicon chip manufacture

-Metal processing-Glass etching

DOWNSTREAM MANUFACTURE

Glebe Mines Ltd

Fluorspar Ore Extraction400 000 t/y

CavendishvvMill

Processing

Acid-dd grade Fluorspar > 97% CaF2

~ 61 000 t/y

Limestone Aggregate150000

t/y

Galena1000 t/yBarytes

10 000 t/y

‘Tributers’

EXTRACTION & PROCESSING

Figure 4 Fluorspar supply chain, 2005.

Fluorspar

Fluorspar 6

The lead concentrate is also the only source oflead in the UK and is sold locally.

Limestone is also recovered as a by-product offluorspar processing and is sold as secondaryaggregate.

Alternatives/recycling

Fluorspar is essentially consumed in use andrecycling or reuse is not usually feasible.

Small amounts of calcium fluoride are recov-ered from the waste streams in HF manufactureand recycled. Some limited recycling of HF isfeasible in downstream applications.

Fluosilicic acid, a by-product of the manufac-ture of phosphoric acid for fertiliser production,is used as a limited source of fluorine in somecountries for uses other than HF production.Phosphoric acid will continue to be producedfor the foreseeable, although there is no pro-duction in the UK. However, fluosilicic acid isnot currently seen as a cost effective alternativeto fluorspar for HF manufacture.

Effects of economic Instruments

The nature of the fluorspar mineralisation assub-vertical veins and replacement deposits inlimestone means that the associated extractionof limestone is often unavoidable. This lime-stone is obtained in two quite distinct ways.During openpit extraction, limestone is pro-duced as waste rock and material that is notused in restoration is crushed, screened andsold as aggregate. This material is subject tothe Aggregates Levy of £1.60/t. Although asmuch as possible of the coarse limestone isremoved from the ore prior to transfer to theCavendish Mill, significant quantities stillremain. This limestone is separated from therest of the ore in the heavy media process andis sold as a low quality secondary aggregate,providing an additional income stream. Thislimestone is exempt from the Aggregates Levy.

More than a decade of anti-dumping measuresimposed on Chinese fluorspar imports into theEuropean Union ended in September 2005. Theduty was imposed to ensure that the EU’s

fluorspar industry remained viable. However,reduced availability of Chinese fluorspar andrising prices has put the price of fluorspar wellabove the minimum import price.

Planning issues

Fluorspar resources in England are foundexclusively in mineralised veins inCarboniferous limestones. These limestonestend to form attractive scenery with consider-able ecological significance and amenity value.The veins are linear in form and can extendover considerable distances, often in elevatedand/ or highly visible locations.

Almost all permitted reserves in the SouthernPennine Orefield lie within the Peak DistrictNational Park. The fluorspar industry thusfluorspar operates in a very sensitive area. Thenow defunct operations in the NorthernPennine Orefield lie exclusively within theNorth Pennines AONB.

Surface working of fluorspar and other veinminerals, especially to significant depths, raisesissues of surface limestone storage and possi-ble sale as aggregate. Some sites may belocated in places where limestone workingwould not normally be permitted. Both thePeak District National Park Authority and theindustry are seeking to minimise any associat-ed production of limestone.

Fluorspar is different from most of the otherindustrial minerals produced in the UK in thatdeposits are more difficult to identify and eval-uate. In addition, individual deposits tend to berelatively small and isolated. A continuous pro-gramme to identify and evaluate new depositsand progress them through the planningprocess is required to maintain an adequatereserve base. However, operations tend to havea short life when compared with other industri-al mineral workings and, due to their limitedextent, are often easier to integrate back intothe landscape.

There are permitted resources of fluorsparwhich are accessible by underground mining,and there is scope for further deposits beingidentified at depth. However, the high cost of F

luo

rsp

ar

Mineral Planning Factsheet

proving underground reserves, together withthe high cost of this method of extraction(which also requires relatively high grade ore)means that future commercial interest is likelyto be confined to sites suitable for surfaceextraction. However, the feasibility of increas-ing underground extraction is being consid-ered.

There is a chance that operators of small-scale,short-term fluorspar workings in environmen-tally acceptable locations may discover moreextensive resources that are capable of furtherexcavation, either laterally or in depth.Extensions to operations may then have theeffect of increasing the scale of the activity andprolong development longer than was original-ly intended. This may, sometimes, be less envi-ronmentally acceptable than when permissionwas first granted. There are also a number ofplanning permissions for vein minerals in thePeak District National Park which were grantedmany years ago with operating and restorationconditions that are inadequate by modern stan-dards. The reactivation of some of these wouldhave significant environmental effects.However, the industry has sought to consoli-date old permissions to remove any ambiguityon how they are worked. This has resulted inmodern conditions of working and, important-ly, restoration to be agreed where formerlythere were none.

Fluorspar has economic importance wellbeyond the extraction locations. It has a down-stream value far in excess of the value of crudeproduction as an essential raw material for the

UK fluorine chemical industry. With constraintson world supplies of fluorspar, access to anindigenous source of supply is very importantto the future of fluorochemical manufacturingin the UK.

Authorship and acknowledgements

This factsheet was produced by the BritishGeological Survey for the Office of the DeputyPrime Minster to support the research project‘Review of Planning Issues Relevant to SomeNon-Energy Minerals other than Aggregates, inEngland’ (2004). It was updated under the theresearch project ‘ODPM-BGS Joint MineralsProgramme’.

It was compiled by David Highley, Kevin Bonel(British Geological Survey) and Richard Bate(Green Balance Planning and EnvironmentalServices), with the assistance of Don Cameron,Paul Lusty and Deborah Rayner.

The invaluable advice and assistance of theminerals industry in the preparation of this fact-sheet is gratefully acknowledged.

Mineral Planning Factsheets for a range ofother minerals produced in England are avail-able for download from www.mineralsUK.com

© Crown Copyright 2006.

Unless otherwise stated all illustrations andphotos used in this factsheet are BGS©NERC.All rights reserved.

Fluorspar

Fluorspar

7

Flu

ors

par

Mineral Planning Factsheet