Embed Size (px)

Citation preview

BLUE FUELMay 2015/ Vol. 8/ Issue 2

www.gazpromexport.com | [email protected] | +7 (812) 646-14-14 | [email protected] 1© Gazprom Export

www.gazpromexport.com | [email protected] +7 (812) 646-14-14 | [email protected]

Page 8

Slovak Republic: An Introduction to Innovative LNG Buses

Page 17

Becker Marine Systems Presents the HUMMEL LNG Hybrid Barge

Page 9

North Asian Customers See Russian LNG as Useful Diversification

Page 5

Turkish Stream – An Essential Piece in the Energy Puzzle

BLUE FUELMay 2015/ Vol. 8/ Issue 2

Gazprom Export Global Newsletter

Page 11

Bergermeer: Increasing Energy Security with Gas Storage

2

Publishers Contact Info:www.gazpromexport.com | [email protected] +7 (812) 646-14-14 | [email protected]

In this issueMay 2015/ Vol. 8/ Issue 2

BLUE FUELGazprom Export Global Newsletter

To Our Readers ........................................................................................................ 4

Turkish Stream – An Essential Piece in the Energy Puzzle ......................................5

The “Blue Corridor-2015” NGV Rally: Eiffel Tour ....................................................7

Czech Republic: 50 percent Increase in CNG Stations in One Year .........................7

Slovak Republic: An Introduction to Innovative LNG Buses ....................................8

North Asian Customers See Russian LNG as Useful Diversification ...................... 9

Bergermeer: Increasing Energy Security with Gas Storage ........................................11

Natural Gas – The Energy of the Future .................................................................14

Becker Marine Systems Presents the HUMMEL LNG Hybrid Barge .....................17

Synergy in Music Brings Virtuosity to South Korea .............................................. 19

The Victory Day Photo-Wheel ............................................................................... 20

Gazprom Export in Russian PR Development Award’s Top 50 ..............................21

BLUE FUELMay 2015/ Vol. 8/ Issue 2

www.gazpromexport.com | [email protected] | +7 (812) 646-14-14 | [email protected] 54

To Our Readers

Turkish Stream – An Essential Piece in the Energy Puzzle Elena V. Burmistrova, Director General of Gazprom Export

Turkish Stream marks the opening of an exciting new chapter in Turkish-Russian energy relations. When Presidents Putin and Erdoğan in December 2014 agreed on this new natural gas

pipeline, they provided an essential piece in the energy puzzle and a historic opportunity to fortify Turkey’s standing in the international energy arena.

Building on the country’s emerging significance on the energy scene, Turkish Stream will turn Turkey into a global crossroads for gas supplies. By its geographical location – on the edges of both Europe and Asia – the country has the potential to evolve into a regional energy hub. Turkey will assume a critical role in catering for the European gas market and ensuring its supply security.

Turkey already plays host to a number of natural gas pipelines, satisfying the country’s ever-rising energy needs with gas from a multitude of suppliers, including Iran, Azerbaijan, and Russia. Ranging from the defunct Nabucco to the current construction of the TANAP pipeline system, Turkey has for

decades consolidated its position by being involved in a number of international energy projects.

Against this background, Turkish Stream will be an essential piece enhancing the security of gas supplies and turning the country into a junction of regional energy routes.

The pipeline will enter the Black Sea from the Russkaya compressor station in southern Russia and follow 910 km along the sea bed. It will finally land on Turkish shores near Kıyıköy with the delivery point for Turkish customers at Lüleburgaz and the delivery point for European customers at the gas hub near İpsala. The route will, to a large extent, follow the one planned for South Stream eliminating the need for new feasibility studies and surveys, while accelerating the pace of the project itself.

Combined with Blue Stream – another direct energy line from Russia – Turkish Stream will immensely improve Turkey’s energy security, eliminating transit risks while providing additional volumes. This is of course crucial when energy demand surges beyond normal levels, as is sometimes the case in Turkish winters.

Only last year Turkish experts estimated an increase of 15 mcm in the daily consumption of households alone. When daily peak demand exceeds 250 mcm and cold spells last more than a week, Turkey currently runs the risk of power outages. These facts and Turkey’s swiftly growing gas demand – BOTAŞ

Continues on page 6

Gazprom’s plan to build the Turkish Stream pipeline through the Black Sea up to the Turkish-Greek border has raised a number of questions. The main issue is how to transport a huge amount of gas to European customers? Especially since the European Commission does not seem to be keen to support the project.

The Gazprom Group does not want to build any more pipelines across the territory of EU Member States, having been subjected to a discouraging discriminatory treatment by Brussels. One only has to compare the regulatory regimes applied to TAP and the defunct South Stream projects, which were basically similar in their ownership structure with gas coming from an exclusive source.

In that dire situation, who will take care of EU energy security?

Meanwhile, responsible European leaders have started to look for the best option. The Slovaks, for instance, have put forward a proposal of a North-South connection called Eastring, with a view of it also being sourced from gas coming from Turkish Stream.

Moreover, some genuinely concerned countries decided to cooperate to put in place a new transportation network for the off-take of Russian gas from the Greek-Turkish border. Negotiations at the highest political level were held recently on one-to-one basis between Russia, Hungary and Greece.

No less symbolic was the meeting in Budapest by Foreign Ministers from Greece, Hungary, Macedonia, Serbia and Turkey. In reference to Turkish Stream, the final declaration of the Budapest Summit expressed the group’s support for the creation of a commercially viable option of delivering natural gas from the Republic of Turkey to the countries of Central and South-Eastern Europe, as well as to other EU countries.

These steps are a testimony towards a pragmatic approach by countries dependent on oil and gas imports to finding ways of ensuring energy security for them and Europe as a whole, irrespective of the highly politicized stance taken by the European Commission against Russian gas.

BLUE FUELMay 2015/ Vol. 8/ Issue 2

www.gazpromexport.com | [email protected] | +7 (812) 646-14-14 | [email protected] 76

expects an increase to 81 bcm in 2030 from 46.3 bcm in 2012 – make the new pipeline not only desirable, but imperative for the country’s energy security and the functioning of its energy-intensive economy.

Since the beginning of 1984, Turkey has imported around 350 bcm of Russian gas. Throughout the years, we have not hesitated to repeatedly assist our Turkish partners, ramping up supplies when delivery from alternative sources was disrupted. It was only last October that Turkey and Gazprom decided to enhance the capacity of Blue Stream to 19 bcm to meet its fast- growing energy requirements.

Today Gazprom remains Turkey’s largest and most reliable gas supplier while Turkey has grown to become Gazprom’s biggest export market after Germany. Turkey’s zest for gas has provided its industry and its households with an affordable, reliable and sustainable fuel. Natural gas is cleaner than any other fossil fuel. And as we develop new technologies, gas could be used more widely: it already shows great promise as a motor fuel. From our perspective, Turkey, as a dynamic economy and society, is a partner where such innovation may create a win-win situation for green and affordable transport.

The three decades of energy cooperation between Gazprom and Turkey have been marked by mutual benefit. Looking ahead, Gazprom sees Turkey as one of the most promising markets for broader and deeper cooperation. As part of this, Turkish Stream will transform Turkish-Russian energy ties from an interdependent to a symbiotic state. We will not just be counterparts in a regular trade relationship, we will become true partners.

In this spirit, we have made rapid progress over the past few weeks to fine-tune the details of Turkish Stream and are confident this commitment will pave the way towards a successful project. This commitment on both sides as well as the public endorsement of the project show that we are on the right path.

International cooperation is not a zero sum game. Embarking on this exciting journey with us does not prevent Turkey from exploring other opportunities that could enhance its position as an energy hub or improve its domestic supply security through diversification of suppliers. In any case, Turkish Stream is one part of the puzzle; but an essential one indeed, providing great benefits for both sides.

The ninth international ‘Blue Corridor’ rally of OEM-produced natural gas-fuelled vehicles (NGV) will start its engines on 24 May 2015. It will culminate in early June in Paris at the World Gas Congress. The rally will cover an overall distance of 6890 km to Paris and back in 19 days.

The participants of the “Blue Corridor-2015” will drive along the motorways of Russia, Belarus, Lithuania, Latvia, Poland, Germany, the Netherlands, Belgium, Luxemburg, and France. Throughout the rally, representatives of the gas and automotive industries, politicians, ecologists and motor fans will be able to share their views on various aspects of the developing NGV market in Europe.

Follow the “Blue Corridor-2015” rally on www.bluecorridor.org

The “Blue Corridor-2015” NGV Rally: Eiffel Tour

Czech Gas Association

There are currently more than 8,800 CNG-fuelled vehicles in the Czech Republic, including approximately 570 buses. This means there are some 2,100 more vehicles on the road than a year ago, also leading to a 50 percent increase in CNG stations in a year.

CNG-consumption in the Czech Republic in 2014 was almost 30 mcm which reflects more than 36% growth compared to 2013. Based on Eurogas data (wherein the Czech Republic is represented by the Czech Gas Association), CNG consumption in Europe may increase as much as seven times by 2035.

In the Czech Republic, there are currently 75 public CNG filling stations in operation. Dozens of new filling stations will become operational by the end of 2015. The objectives of the EU directive about the installation of infrastructure for alternative fuels focused on CNG have nearly already been fulfilled in the Czech Republic.

It is particularly Czech transportation companies that tend to buy CNG buses, saving them tens of millions of Czech Koruna per year. By the end of 2015 more than 800 CNG buses should be running in the Czech Republic. Based on the latest Navigant Research report, sales of CNG buses worldwide will increase from 170,200 per year in 2013 up to 400,000 per year by 2022. The European Union also supports alternative transport by all available means.

The Czech Ministry of the Environment is prepared to give substantial subsidies to replace the oldest buses (with the highest emissions) with new environment-friendly CNG buses. This initiative also supports the construction of new CNG filling stations. The Czech Gas Association welcomes this subsidy which will cover up to 85% of the actual price. The number of CNG buses in Europe reached almost 300,000 and almost 800,000 worldwide.

Czech Republic: 50 percent Increase in CNG Stations in One Year

You can find more information at: http://www.cng4you.cz/en.html

0

5

10

15

20

25

30

35

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

CNG sales in the Czech Republic in mcm

BLUE FUELMay 2015/ Vol. 8/ Issue 2

www.gazpromexport.com | [email protected] | +7 (812) 646-14-14 | [email protected] 98

Slovak Republic: An Introduction to Innovative LNG Buses The Slovak Republic is becoming the third country in Europe to get acquainted with LNG buses.

In February 2015, the innovative Solbus Solcity 12 LNG buses were presented to potential customers, users and municipal authorities in the Slovak town of Dunajská Streda. The approximately 60 participants could experience the LNG bus and Gazprom Germania’s mobile refueling station first hand. They were able to witness the LNG fueling process as the 367-litre-tank was filled with about 35 kg of LNG (maximum capacity 320 kg). The benefits of LNG were described to the audience by the representatives of Gazprom Germania, Vemex, Polish bus manufacturer Solbus, Chart Ferox, Czech producer of LNG equipment and Danube LNG, the Slovakian partner of Solbus and organizer of the trials.

These new, environmentally friendly and economically attractive busses became a powerful attraction for the Slovak audience. Mr. Michal Humeník from SAD Dunajská Streda, the local bus operator and first trial partner, said he was pleased to have such modern transport technology at display in the city.

Mr. Tobias Noack from Gazprom Germania explained the economical and environmental benefits of the LNG technology and noted how he was looking forward to introducing this new alternative to the Slovakian public transport sector through this trial project.

The Solbus Solcity12 LNG together with the mobile refueling station is being demonstrated to potential customers not only in Dunajská Streda, but also in the towns of Zvolen, Prievidza, and Trnava. The Solbus Solcity12 LNG busses will be integrated and tested in the daily operation of different Slovakian bus operators who will experience the benefits of LNG-fuelled busses.

The Solbus Solcity12 LNG is equipped with a Cummins ISL G; 8.9l engine with max. 280-320 horse power and a 320 kg LNG fuel tank which allows for a travelling distance of up to 600 kilometers.

First buses of that type are already being delivered to serve the city lines in the Polish cities of Olsztyn and Warsaw. LNG to fuel the fleet is supplied by Gazprom Germania.

Bernard Samuels, Deputy Commercial Director, Head of LNG Marketing, Sakhalin Energy

The Asia Pacific LNG market is by far a genuine pearl in the global LNG domain. There is Japan, the world’s largest LNG importer, which increased LNG imports after

the catastrophic Fukushima accident. There is China, one of the most rapidly growing gas markets in the world that accelerates the construction of LNG-terminals all along its eastern coastline. There are also South Korea and Taiwan: though lately they demonstrate near flat gas consumption growth rates, but still remain significant and mature players on the global LNG arena.

Finally, South-East Asian markets are still in their infancy, but with ambitious prospects to grow and thus impact global LNG trade, with even former leading exporters such as Malaysia and Indonesia starting to consume LNG in their own markets. The Asia Pacific region as a part of the global LNG market is not a rigid structure, but a constantly evolving one, which now meets both external and internal challenges like falling oil prices or domestic demand trends.

Bernard Samuels, Deputy Commercial Director, Head of LNG Marketing of Sakhalin Energy, the only operating exporter of Russian LNG, provides Blue Fuel with his personal views on the LNG market development in Asia Pacific, considers fears of a further oil price plunge and highlights the company’s business record in 2014.

Mr. Samuels, how was the business performance of Sakhalin Energy in 2014? 2014 was a very successful year for Sakhalin Energy’s LNG business. We delivered all our contracted volumes to our long-term customers. Total LNG production in 2014 was 10.8 million tonnes: 80% of this volume was sold to Japan, 18% to South Korea, with the remainder delivered to China, Taiwan and Thailand. These last three markets were served through our shareholder affiliates Gazprom Marketing & Trading and Shell Eastern Trading. Sakhalin Energy continues to sell its LNG into the closest — and premium — markets in Asia Pacific, mostly Japan and Korea. We have established a trustful and mutually beneficial co-operation with our customers, and we intend to build on this in the future.

How would you characterize the current state of the LNG market in Asia Pacific? Right now (first half of 2015) it seems to be more of a buyers’ market. LNG demand has been moderated by warmer winter weather, availability of cheap oil and customers taking LNG cargoes deferred from last summer. At the same time, LNG supply seems relatively plentiful, with new projects (e.g. QCLNG in Australia) coming on stream.

Although there may be an uptick in demand in the summer (to meet increased electricity consumption for air-conditioning), the market seems unlikely to tighten significantly until next winter.

What countries are projected to demonstrate the highest LNG consumption growth rates in the Asia Pacific region? In Asia the fastest growth rate of LNG consumption is still expected to be in China, because it is coming off a relatively low base. The much more mature market in Japan can only expect slow growth at best, while LNG demand in South Korea is actually falling as power generation switches to nuclear and coal.

South-East Asian markets also offer growth opportunities — but from a very low base, so the absolute volumes, for the time being, are not so large. Russian LNG is less competitive in these markets, because they are further away (incurring a greater freight cost) than other suppliers in Australia and the Middle East.

The Asian LNG market is still determined by long-term, oil-indexed contracts. Do you expect the share of spot trades to grow there? The proportion of short-term and single cargo (“spot”) sales has been increasing for a number of years. While this trend may be expected to continue in general, in the next one to two years this proportion may actually drop, as new projects start up with their own long-term contracts, displacing some spot volumes. Any declines in demand in the core markets of Japan and South Korea, due to economic slowdown and/or resumption of nuclear power, would also fall in the first instance on reduced spot purchases.

The question of oil-linkage is a different story. Some short-term and even spot deals are effectively linked to oil prices. By contrast, in the future there will be some long-term contracts that are not linked to oil prices. This is a sensible diversification on the part of customers. The recent steep fall in oil prices has probably reduced the pressure on oil-indexation.

North Asian Customers See Russian LNG as Useful Diversification

Continues on page 10

BLUE FUELMay 2015/ Vol. 8/ Issue 2

www.gazpromexport.com | [email protected] | +7 (812) 646-14-14 | [email protected] 1110

Emissions

What challenges does the falling oil price bring to LNG suppliers? The obvious challenge is that falling oil prices in general bring lower LNG prices and thus lower revenues. For existing suppliers this puts pressure on their costs, and affects their payments to governments (through taxes) and to shareholders. But, in the short term, there is no impact on LNG production. For potential new LNG suppliers, the low oil price environment may delay their investment decisions, which may sow the seeds of future tightening in the market.

An interesting side effect is that US Henry Hub-linked contracts no longer appear so “cheap” in Asia, after allowing for the cost of transportation. It will be interesting to see whether the enthusiasm for US LNG in Asia will be correspondingly reduced.

Last winter, LNG spot prices in Asia hit record lows. Why did that happen? There are two reasons. The first is the fall in oil prices, which has brought down the price of long-term oil-linked LNG. The traditional “14.85%xJCC” long-term LNG price formula has dropped from ~$17/MMBtu with oil at $115/bbl to below $9/MMBtu when oil dropped below $60/bbl. Spot prices are being dragged down by this.

The second reason is that the balance of supply and demand is different. In previous years some customers, notably KOGAS in South Korea, bought large volumes of spot LNG through the winter, taking winter spot prices above long-term prices. But last summer KOGAS

faced a surplus and deferred a number of cargoes for winter, so it needed to buy less winter spot volumes. Also, additional supply has come online (e.g. from PNG and Australia). With more supply chasing less demand, spot prices have declined to below the level of long term prices.

What will be the effect of a restart of Japan’s nuclear power plants on LNG demand in Asia Pacific? Roughly each 1 GW nuclear reactor generates as much electricity in a year as 1 million tons of LNG in a CCGT (“combined cycle gas turbine”) power station. Of the 54 reactors operating in Japan before the Great East Japan Earthquake in 2011, it has been decided that 11 will never restart (the six at Fukushima Daiichi itself and five other older/smaller reactors). None has actually restarted yet — although the first two are getting close. It remains unclear how many will eventually restart. When they do, we expect that they will first replace oil (being burned in older, less efficient power stations), so the impact is initially expected to be small, although it will grow when/if more than about a third of the reactors are restarted.

What do you think of new LNG suppliers to the Asia Pacific market? The new projects in Queensland and in the North and West of Australia are well advanced in construction and the first has already come on stream, with the others following over the next year or two.

This supply is essentially a given in the market. It is much less likely that any more new Australian projects will be committed under current market conditions.

North American LNG supply to Asia is more questionable. Only a limited number of export projects have received all required approvals and actually started with the construction phase. Others are likely to be delayed or even cancelled. Even for those that are built, it may be questioned whether they will deliver much LNG to Asia, as opposed to selling to closer European markets.

What are the perspectives of Russian LNG in Asia? Russian LNG has a relatively small share in the Asian LNG market – around 10% in Japan and Korea, and even smaller in China. Therefore, North Asian customers see Russian LNG as

a useful diversification from their much greater dependence on Middle Eastern and Australian LNG. Furthermore, they are fully aware that due to geography, they are the closest markets to Russian LNG from the Far East, which therefore is at a relative disadvantage in other markets. This makes it likely that Japanese customers would be interested to increase purchases of Russian LNG over time.

On the other hand, Japanese customers may be reluctant to be seen to enter into new commitments at this time of political tensions, which also creates perceptions that new Russian LNG projects face heightened completion risks. At the same time, China may prefer to focus on pipeline gas imports from Russia. The most important thing for prospective Russian suppliers is to be ready when the customers are ready.

Bergermeer: Increasing Energy Security with Gas Storage

Continues on page 11

Jan Willem van Hoogstraten, Managing Director, TAQA Netherlands

Underground Gas Storage Bergermeer (UGS Bergermeer) in the Netherlands was put into full commercial operation on 1 April 2015. The storage

has a capacity of 4.1 bcm, making it the largest gas storage in Europe with third-party access rights. TAQA, an international energy company listed in Abu Dhabi, holds a 60% stake in UGS Bergermeer and is the operator of the storage facility. EBN, an independent company with the Dutch State as its sole shareholder, holds a 40% stake. In exchange for storage capacity, Gazprom Export supplied the ‘cushion gas’ for the storage. Jan Willem van Hoogstraten, Managing Director of TAQA in the Netherlands, tells Blue Fuel about the importance of storage for the European gas market, UGS Bergermeer’s technological uniqueness and the role that Gazprom Export played in implementing this project.

Mr. van Hoogstraten, how does it feel to complete this large state-of-the-art project? One word – great! We have worked on this project for almost eight years. We started it in April 2007 and our first discussions with Gazprom date back to May-June 2007. During the first two years, one of the primary things we were working on was to reach an agreement with Gazprom Export for the supply of ‘cushion gas’ and for Gazprom Group to participate in the project. Our partnership with Gazprom Export has been excellent. We are really proud that we have completed this project within budget, time, scope, and with an outstanding safety performance. I think it was a great example of cooperation between companies from Abu-Dhabi, the Netherlands and Russia. And I want to thank everybody who made this project possible.

What does this facility mean for the Netherlands and for Europe in general? UGS Bergermeer is the largest open-access commercial gas storage in North-West Europe; therefore it will give a significant boost to the flexibility of the European gas market. Moreover, it will also increase the security of supply and guarantee that there always will be sufficient volumes of gas to cover energy demand in North-West Europe. The facility doubles the storage capacity of the Netherlands, but it will not only serve the needs of the Dutch market. We have customers from different states – France, Germany, and the UK. Gazprom is one of the most important customers, and so are Statoil (Norway) or EDF (France). Having such big gas storage is essential because the indigenous gas production in the UK and the Netherlands is declining and appetite for imports is growing. UGS Bergermeer is well located in close proximity to consumption markets thus ensuring that supply and demand are perfectly balanced.

Continues on page 12

“It was a great example of cooperation between companies from Abu-Dhabi, the Netherlands and Russia.”Jan Willem van Hoogstraten, Managing Director, TAQA Netherlands

BLUE FUELMay 2015/ Vol. 8/ Issue 2

www.gazpromexport.com | [email protected] | +7 (812) 646-14-14 | [email protected] 1312

Continues on page 15

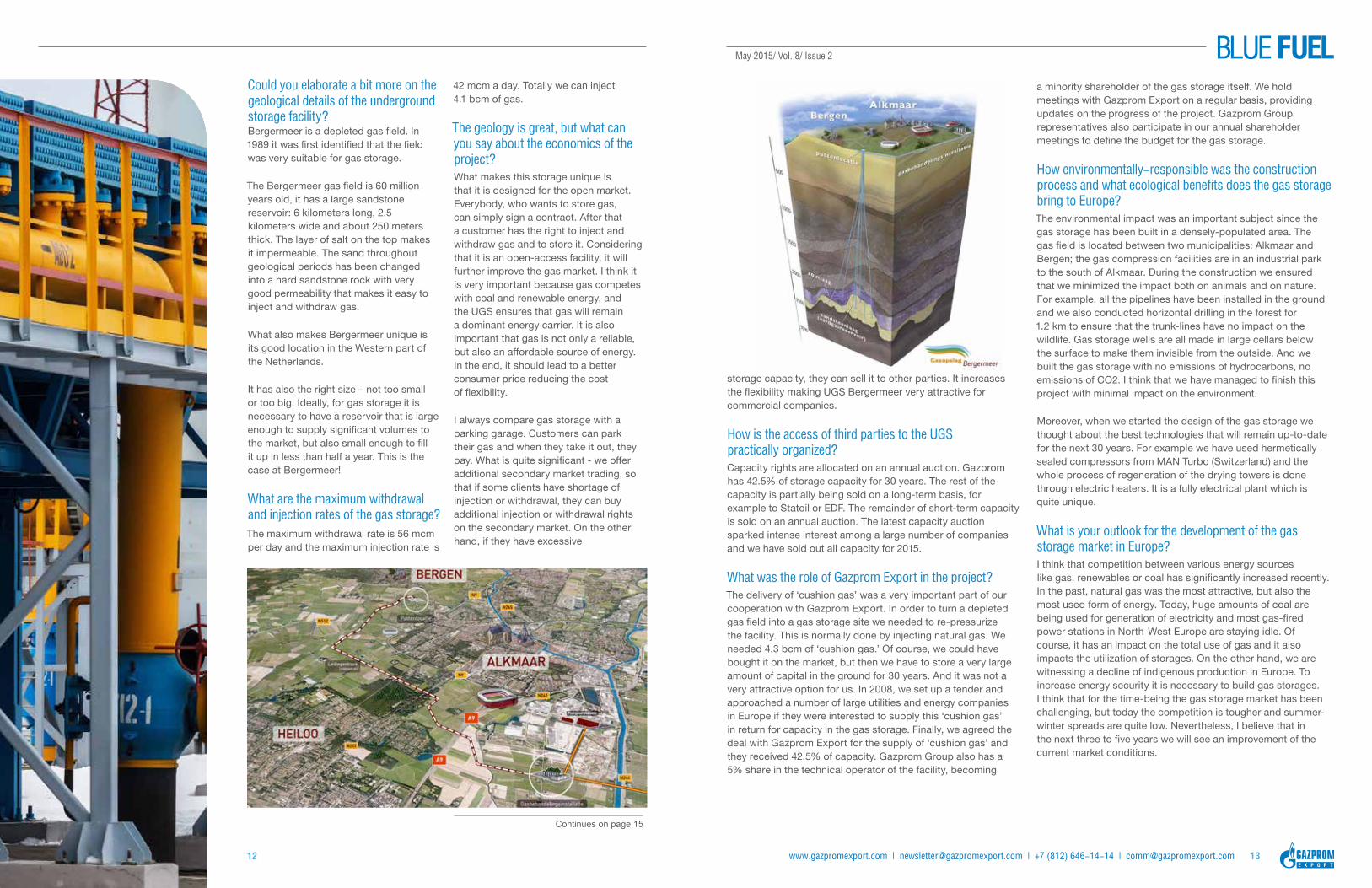

Could you elaborate a bit more on the geological details of the underground storage facility? Bergermeer is a depleted gas field. In 1989 it was first identified that the field was very suitable for gas storage.

The Bergermeer gas field is 60 million years old, it has a large sandstone reservoir: 6 kilometers long, 2.5 kilometers wide and about 250 meters thick. The layer of salt on the top makes it impermeable. The sand throughout geological periods has been changed into a hard sandstone rock with very good permeability that makes it easy to inject and withdraw gas.

What also makes Bergermeer unique is its good location in the Western part of the Netherlands.

It has also the right size – not too small or too big. Ideally, for gas storage it is necessary to have a reservoir that is large enough to supply significant volumes to the market, but also small enough to fill it up in less than half a year. This is the case at Bergermeer!

What are the maximum withdrawal and injection rates of the gas storage? The maximum withdrawal rate is 56 mcm per day and the maximum injection rate is

42 mcm a day. Totally we can inject 4.1 bcm of gas.

The geology is great, but what can you say about the economics of the project? What makes this storage unique is that it is designed for the open market. Everybody, who wants to store gas, can simply sign a contract. After that a customer has the right to inject and withdraw gas and to store it. Considering that it is an open-access facility, it will further improve the gas market. I think it is very important because gas competes with coal and renewable energy, and the UGS ensures that gas will remain a dominant energy carrier. It is also important that gas is not only a reliable, but also an affordable source of energy. In the end, it should lead to a better consumer price reducing the cost of flexibility.

I always compare gas storage with a parking garage. Customers can park their gas and when they take it out, they pay. What is quite significant - we offer additional secondary market trading, so that if some clients have shortage of injection or withdrawal, they can buy additional injection or withdrawal rights on the secondary market. On the other hand, if they have excessive

storage capacity, they can sell it to other parties. It increases the flexibility making UGS Bergermeer very attractive for commercial companies.

How is the access of third parties to the UGS practically organized?Capacity rights are allocated on an annual auction. Gazprom has 42.5% of storage capacity for 30 years. The rest of the capacity is partially being sold on a long-term basis, for example to Statoil or EDF. The remainder of short-term capacity is sold on an annual auction. The latest capacity auction sparked intense interest among a large number of companies and we have sold out all capacity for 2015.

What was the role of Gazprom Export in the project?The delivery of ‘cushion gas’ was a very important part of our cooperation with Gazprom Export. In order to turn a depleted gas field into a gas storage site we needed to re-pressurize the facility. This is normally done by injecting natural gas. We needed 4.3 bcm of ‘cushion gas.’ Of course, we could have bought it on the market, but then we have to store a very large amount of capital in the ground for 30 years. And it was not a very attractive option for us. In 2008, we set up a tender and approached a number of large utilities and energy companies in Europe if they were interested to supply this ‘cushion gas’ in return for capacity in the gas storage. Finally, we agreed the deal with Gazprom Export for the supply of ‘cushion gas’ and they received 42.5% of capacity. Gazprom Group also has a 5% share in the technical operator of the facility, becoming

a minority shareholder of the gas storage itself. We hold meetings with Gazprom Export on a regular basis, providing updates on the progress of the project. Gazprom Group representatives also participate in our annual shareholder meetings to define the budget for the gas storage.

How environmentally-responsible was the construction process and what ecological benefits does the gas storage bring to Europe?The environmental impact was an important subject since the gas storage has been built in a densely-populated area. The gas field is located between two municipalities: Alkmaar and Bergen; the gas compression facilities are in an industrial park to the south of Alkmaar. During the construction we ensured that we minimized the impact both on animals and on nature. For example, all the pipelines have been installed in the ground and we also conducted horizontal drilling in the forest for 1.2 km to ensure that the trunk-lines have no impact on the wildlife. Gas storage wells are all made in large cellars below the surface to make them invisible from the outside. And we built the gas storage with no emissions of hydrocarbons, no emissions of CO2. I think that we have managed to finish this project with minimal impact on the environment.

Moreover, when we started the design of the gas storage we thought about the best technologies that will remain up-to-date for the next 30 years. For example we have used hermetically sealed compressors from MAN Turbo (Switzerland) and the whole process of regeneration of the drying towers is done through electric heaters. It is a fully electrical plant which is quite unique.

What is your outlook for the development of the gas storage market in Europe?I think that competition between various energy sources like gas, renewables or coal has significantly increased recently. In the past, natural gas was the most attractive, but also the most used form of energy. Today, huge amounts of coal are being used for generation of electricity and most gas-fired power stations in North-West Europe are staying idle. Of course, it has an impact on the total use of gas and it also impacts the utilization of storages. On the other hand, we are witnessing a decline of indigenous production in Europe. To increase energy security it is necessary to build gas storages. I think that for the time-being the gas storage market has been challenging, but today the competition is tougher and summer-winter spreads are quite low. Nevertheless, I believe that in the next three to five years we will see an improvement of the current market conditions.

BLUE FUELMay 2015/ Vol. 8/ Issue 2

www.gazpromexport.com | [email protected] | +7 (812) 646-14-14 | [email protected] 1514

Dr. Christian Wipperfürth, Associate Fellow, German Council on Foreign Relations (DGAP)

Does the headline seem a little optimistic, even if it appears in Gazprom Export’s Blue Fuel? Let us take a look at the forecasts of Gazprom’s competitors, the major oil corporations. I will firstly look at the “bigger picture”, before focusing on gas as an energy source. As the developments of the last 150 years illustrate, the commercialization of energy has undergone a complete overhaul.

British Petroleum (BP), Exxon Mobil and Shell all expect an increase in demand for energy in the future. In 2011, Shell predicted that global demand will increase from 536 Exajoules in 2010 to 734 Exajoules in 2030.1 By 2013, Shell adjusted its

estimates to 749 Exajoules by 2013, thus raising its prediction by another 2%.2

In early 2015, Exxon Mobil expected that global energy demand would grow by 1% annually on average between 2010 and 2040.3 BP even calculated an increase of 1.5% per year between 2012 and 2035.4 Although Exxon Mobil and BP analysed two different time periods, their results hardly differ from each other. Moreover, the OECD’s International Energy Agency made similar predictions.

How reliable are these forecasts? They serve as a basis for energy corporations’ investment decisions which require long-term planning security, so they must be quite dependable. Exploration and exploitation of oil and gas reserves, construction of gas liquefaction facilities, pipelines or refineries are all major investments that only pay off after years, if not decades.

As regards consumption of gas specifically, BP’s experts expect to see global growth of 1.9% annually between 2012 and 2035.5 Exxon Mobil recently drew the following conclusions:

Natural Gas – The Energy of the Future

The Outlook for Energy. A View to 2040, Exxon Mobil, 2015, Page 22

BP Energy Outlook 2035, bp.com/energyoutlook, Page. 16

1 Shell Energy Scenarios to 2050, 2011 Shell International BV, p. 762 New Lens Scenarios. A Shift in Perspective for a World in Transition, Shell 2013, p. 433 The Outlook for Energy. A View to 2040, Exxon Mobil, 2015, p. 224 BP Energy Outlook 2035, bp.com/energyoutlook, p. 9

The Outlook for Energy. A View to 2040, Exxon Mobil, 2015, Page 22

Continues on page 16

BP Energy Outlook 2030, London, January 2011, Page 10

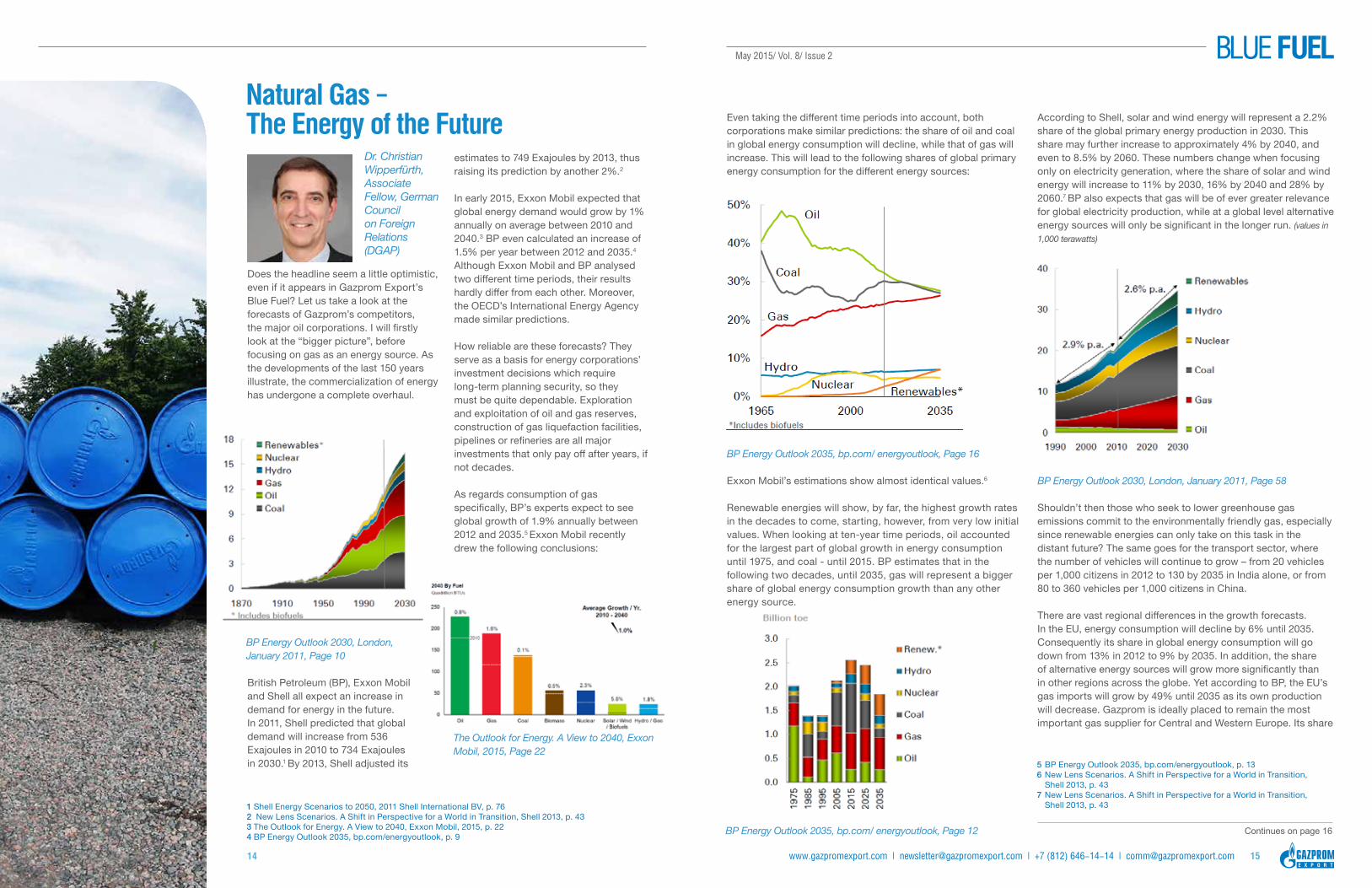

Even taking the different time periods into account, both corporations make similar predictions: the share of oil and coal in global energy consumption will decline, while that of gas will increase. This will lead to the following shares of global primary energy consumption for the different energy sources:

Exxon Mobil’s estimations show almost identical values.6

Renewable energies will show, by far, the highest growth rates in the decades to come, starting, however, from very low initial values. When looking at ten-year time periods, oil accounted for the largest part of global growth in energy consumption until 1975, and coal - until 2015. BP estimates that in the following two decades, until 2035, gas will represent a bigger share of global energy consumption growth than any other energy source.

According to Shell, solar and wind energy will represent a 2.2% share of the global primary energy production in 2030. This share may further increase to approximately 4% by 2040, and even to 8.5% by 2060. These numbers change when focusing only on electricity generation, where the share of solar and wind energy will increase to 11% by 2030, 16% by 2040 and 28% by 2060.7 BP also expects that gas will be of ever greater relevance for global electricity production, while at a global level alternative energy sources will only be significant in the longer run. (values in

1,000 terawatts)

Shouldn’t then those who seek to lower greenhouse gas emissions commit to the environmentally friendly gas, especially since renewable energies can only take on this task in the distant future? The same goes for the transport sector, where the number of vehicles will continue to grow – from 20 vehicles per 1,000 citizens in 2012 to 130 by 2035 in India alone, or from 80 to 360 vehicles per 1,000 citizens in China.

There are vast regional differences in the growth forecasts. In the EU, energy consumption will decline by 6% until 2035. Consequently its share in global energy consumption will go down from 13% in 2012 to 9% by 2035. In addition, the share of alternative energy sources will grow more significantly than in other regions across the globe. Yet according to BP, the EU’s gas imports will grow by 49% until 2035 as its own production will decrease. Gazprom is ideally placed to remain the most important gas supplier for Central and Western Europe. Its share

BP Energy Outlook 2035, bp.com/ energyoutlook, Page 16

BP Energy Outlook 2035, bp.com/energyoutlook, Page 12

BP Energy Outlook 2030, London, January 2011, Page58

BP Energy Outlook 2030, London, January 2011, Page 58

BP Energy Outlook 2035, bp.com/ energyoutlook, Page 12

5 BP Energy Outlook 2035, bp.com/energyoutlook, p. 13 6 New Lens Scenarios. A Shift in Perspective for a World in Transition, Shell 2013, p. 43 7 New Lens Scenarios. A Shift in Perspective for a World in Transition, Shell 2013, p. 43

BLUE FUELMay 2015/ Vol. 8/ Issue 2

www.gazpromexport.com | [email protected] | +7 (812) 646-14-14 | [email protected] 1716

The Outlook for Energy. A View to 2040, Exxon Mobil, 2015, Page 29 The Outlook for Energy. A View to 2040, Exxon Mobil, 2015, Page 29

8 BP Energy Outlook 2035, bp.com/energyoutlook, p. 619 BP Energy Outlook 2035, Regional Insights European Union 203510 Forbes.com, March 25, 2015, How Much Energy Does Russia Have Anyways? By Jude Clemente

of EU gas imports already increased from 48 % in 2010 to 64% in 2014.

There has been a lot of commotion in the global energy market since the turn of the century. Gazprom is facing considerable challenges. Gas extraction in the U.S. has increased considerably. LNG, where Gazprom is not among the pioneers due to its efficient pipeline network, has experienced a boom. Finally, the political differences between Russia and the EU have prompted discussions about the outlook for Gazprom’s most important export market.

Gazprom has managed to react to these challenges, most recently by means of an export deal with China. In 2010, gas consumption in the Asia-Pacific region was still slightly below that of the EU. By 2030, however, it will be almost twice as high.

All indicators therefore suggest that Russia will maintain its position as the world’s most important gas exporter, and Gazprom will remain its flagship.

Becker Marine Systems Presents the HUMMEL LNG Hybrid BargeUsing an environmentally-friendly LNG hybrid barge to supply power to cruise ships lying at port is currently one of the most innovative projects in the shipping industry. Together with Aida Cruises, Hamburg-based Becker Marine Systems initiated the world’s first LNG hybrid barge.

Up until today, no shore-side power supply for cruise ships has been implemented in Europe. Now, however, the LNG hybrid barge, named the HUMMEL, can be deployed as a mobile system at different terminals in European ports. Due to its clean combustion, the use of LNG as a fuel reduces the

emission of soot particles and sulphur oxides by 100%, CO2 by approximately 20% and nitrogen oxides by about 88%.

Becker Marine Systems’ LNG Hybrid department is currently working on a small and more mobile solution – LNG Hybrid PowerPac. The objective is for freighters and container ships requiring less energy than cruise ships to also be supplied with electricity from environmentally-friendly LNG during layovers at port. In addition, LNG ferry projects and ship propulsion systems are in the planning stage.

Engine room There is a large engine room on board the LNG hybrid barge, which at its current stage of development holds five generators that run on LNG. The generators are the first gas engines with

marine approval from Caterpillar. Built in the U.S. and then prepared for use and tested by Zeppelin in Bremen/Achim, Germany, each individual generator produces approx. 1.5 MW.

Continues on page 18

BLUE FUELMay 2015/ Vol. 8/ Issue 2

www.gazpromexport.com | [email protected] | +7 (812) 646-14-14 | [email protected] 1918

Synergy in Music Brings Virtuosity to South KoreaIn March 2015, Gazprom’s Synergy in Music initiative brought renowned Russian musicians, violinist Tatiana Samouil and cellist Alexander Buzlov to South Korea’s capital Seoul. Together with their Korean colleagues Tatiana Samouil and Alexander Buzlov performed at the Munhwa Cultural Center Hall of Seoul National University.

Violinist and recording artist Tatiana Samouil plays a 1714 Stradivarius once owned by the legendary Fritz Kreisler and whose debut album received 5 stars from France’s Diapason magazine. Performing with Tatiana was award-winning cellist Alexander Buzlov, who was lauded by the New York Times as “a cellist of true Russian tradition, possessing a great gift to make an instrument sing, bewitching the audience with his sound.” Both artists also hosted tutorial master classes at the Seoul National University as well as a workshop at Yonsei University.

“Synergy in Music celebrates the power of passion, talent and cultural exchange on a single stage, sharing Russia’s rich classical music heritage to help forge deeper intercultural bonds between Russia and South Korea. It is part of a long-term initiative by the Gazprom Group to promote cultural understanding between Russia and the nations of the Asia-Pacific region,” said Elena Burmistrova, Director General of Gazprom Export.

The Synergy in Music project was launched in 2012 in Singapore. The project embraces not only the performances by Russian musicians captivating the public with their virtuosity, but also their educational master classes for students of various musical schools. Such tutoring provides the opportunity to glean fresh insights on how to better the artistic technique and style, be inspired by peers who achieved success professionally, and broaden their horizons with new knowledge about Russian culture.

LNG container & gas processing unit All LNG equipment is housed in the rear section of the barge. It primarily consists of two 40 foot containers and a gas treatment plant. The containers are currently filled with approximately 15 tonnes of LNG at the Fluxys Terminal in Zeebrugge and delivered to Hamburg just in time for each cruise ship to be supplied.

In the adjacent gas treatment plant, the cryogenic (-163 °C) and liquefied gas is heated, turning it into the actual gaseous phase, passed on to the gas generators, and there in the gas train it is specifically adjusted for the engine.

Source: Becker Marine Systems

Pump room The pump room can be reached from the engine room. Fresh water pumps, seawater pumps and pumps for gas

heating are installed here. This is where waste heat from the engines is used to heat the LNG.

Main switchboard room The main switchboard room is situated behind the pump room, which in addition to the control container houses the LNG hybrid barge’s central control unit

and contains all control units for air conditioning, fire extinguishing, gas, engines and the earthing resistances.

BLUE FUELMay 2015/ Vol. 8/ Issue 2

www.gazpromexport.com | [email protected] | +7 (812) 646-14-14 | [email protected] 2120

On April 28 Gazprom Export’s office hosted the final part of the Victory Day Photo-Weel educational experience program, run by our Company in conjunction with Russ Press Photo cultural project. Over 50 children from children’s homes and social institutions from Saint Petersburg, Leningrad, Smolensk and Kostroma regions took part in the project.

The event started with the opening of the exhibition and ceremony of awarding of all the participants of the contest, who received diplomas and souvenirs. The main prizes went to Alina Levchenkova from Smolensk, Zhenya Velikasova from Saint Petersburg and Margarita Surkova from Kostroma. Indisputable winner was named Vlad Timofeev from Shatalovo children’s home from Smolensk region with his work “I remember”. In addition to diploma and souvenirs Vlad will enjoy a unique opportunity to take part in Energy for life summer arts academy in Austria. There he together with his peers from

different countries will have a chance to acquire skills of the work of modern photo correspondent under the guidance of the experienced tutors and press photographers.

After these ceremonies the news photographer Vasily Prudnikov, Chief Manager of the project, addressed the children with the final lecture. It became the summarizing master class and an advanced training. Renowned master told the audience how the winning photos were selected and which advantages they have, what participants have to pay attention in their future photo works.

The theme for Photo-Wheel 2015 is the anniversary of Victory in World War II. Participants will be encouraged to test their skills by creating photographs that reflect the image of the Defender and Liberator, artistic or documentary photographs of World War II memorial sites, and photographs of individuals who lived through the war.

This March saw the Silver Archer National Public Relations Development Award announce the seventh annual collection of best communications projects. The Silver Archer Award was launched in 1997 by the Russian Chamber of Commerce and Industry, the Russian Union of Journalists, and the Russian Public Relations Association.

The collection entitled 50 Best Projects from the National Public Relations Development Award, covering the most successful projects in the areas of international, social, marketing, and business communications, includes Gazprom Export’s activities nominated for Best Project in Business Communications and Best Project in Social Communications and Charity.

The Victory Day Photo-Wheel

Gazprom Export in Russian PR Development Award’s Top 50

The Photo-Wheel program has been a successful annual event since 2012 for children from children’s homes and social institutions sponsored by the company in the Smolensk and Kostroma regions. This year, the project was expanded to include children from social institutions in St. Petersburg and

the Leningrad region. The program’s main goal is to introduce children to leading photojournalists and their best works, familiarize them with the culture of photography, and enable them to acquire basic photography skills.

Continues on page 21