Embed Size (px)

Citation preview

Accepted Manuscript

Bankruptcy Law and Corporate Investment Decisions

Emanuele Tarantino

PII: S0378-4266(13)00082-4

DOI: http://dx.doi.org/10.1016/j.jbankfin.2013.02.007

Reference: JBF 4005

To appear in: Journal of Banking & Finance

Received Date: 15 January 2012

Accepted Date: 6 February 2013

Please cite this article as: Tarantino, E., Bankruptcy Law and Corporate Investment Decisions, Journal of Banking

& Finance (2013), doi: http://dx.doi.org/10.1016/j.jbankfin.2013.02.007

This is a PDF file of an unedited manuscript that has been accepted for publication. As a service to our customers

we are providing this early version of the manuscript. The manuscript will undergo copyediting, typesetting, and

review of the resulting proof before it is published in its final form. Please note that during the production process

errors may be discovered which could affect the content, and all legal disclaimers that apply to the journal pertain.

Bankruptcy Law and Corporate Investment Decisions∗

Emanuele Tarantino†

University of Bologna

21st February 2013

Abstract

Major European countries have recently adopted bankruptcy codes that strengthen entrepre-neurs’ power to renegotiate outstanding liabilities. Renegotiation in bankruptcy allows lendersto increase recovery rates, however it also weakens the contract’s ability to solve the moralhazard problem embedded in the production project. Hinging on this trade-off, I show in whichcircumstances a soft bankruptcy law that resembles Chapter 11 in the balance of lenders’ andentrepreneur’s rights encourages the choice of investments that privilege the achievement of long-term results. However, I also show that, in contrast to the common wisdom, soft bankruptcycan lead to the choice of investments that are biased towards the achievement of short-termoutcomes.

JEL classification: D82, G33, K22.

Keywords: bankruptcy law, financial contracts, limited commitment, soft budget constraint, short-termism.

∗This paper is a revised version of Chapter 1 of my Ph.D. Thesis (European University Institute, 2010). I am indebted

to Massimo Motta and Patrick Rey for precious guidance and encouragements, and to Piero Gottardi and Elu von Thadden

for suggestions and discussions. This paper also benefited from comments by Sara Biancini, Fabio Braggion, Elena Carletti,

Cathrine Casamatta, Fabio Castiglionesi, Gabriella Chiesa, Francesco Corneli, Pascal Courty, Wouter Dessein, Chiara Fu-

magalli, Igor Livshits, Salvatore Piccolo, Stephen Schaefer, the participants at the Toulouse School of Economics, European

University Institute, University of Mannheim, ECARES and Tilburg University seminars, and at the European Finance As-

sociation 2008 Doctoral Tutorial (Athens), European Association for Research in Industrial Economics 2008 Annual Meeting

(Toulouse), Association of Southern European Economic Theorists 2008 Annual Meeting (Florence), Bankruptcy and Distress

Resolution 2008 Conference (Ghent) and Mondragone-La Pietra-Moncalieri Doctoral Workshop (MOOD) 2009 (Turin). The

usual disclaimer applies.†University of Bologna, Department of Economics, piazza Scaravilli 1, I-40126, Bologna, Italy; Phone: +39-051-20-98885;

[email protected]. Also affiliated with TILEC (Tilburg University).

1

Bankruptcy Law and Corporate Investment Decisions

December 21, 2012

Abstract

Major European countries have recently adopted bankruptcy codes that strengthen en-trepreneurs’ power to renegotiate outstanding liabilities. Renegotiation in bankruptcy allowslenders to increase recovery rates, however it also weakens the contract’s ability to solve the moralhazard problem embedded in the production project. Hinging on this trade-off, I show in whichcircumstances a soft bankruptcy law that resembles Chapter 11 in the balance of lenders’ andentrepreneur’s rights encourages the choice of investments that privilege the achievement of long-term results. However, I also show that, in contrast to the common wisdom, soft bankruptcycan lead to the choice of investments that are biased towards the achievement of short-termoutcomes.

JEL classification: D82, G33, K22.

Keywords: bankruptcy law, financial contracts, limited commitment, soft budget constraint, short-termism.

1 Introduction

The literature in the fields of law and economics has traditionally distinguished the American softapproach to bankruptcy from the tough one of European legislators. Recently, this dichotomy hasbeen put at stake by a process of convergence due to the adoption, in major European countries,of bankruptcy codes inspired by American Chapter 11. The European Commission supportedthis process, based on the presumption that a harsh approach to failure would deter risk-taking,experimentation and innovation.

Consequently, major European countries (like France, Germany, Italy and Spain) have reformedtheir bankruptcy codes and the crucial novelty they introduced consisted in giving more powerto the entrepreneur to restructure the terms of outstanding financial contracts and prevent theopening of a liquidation phase.1 These days such reformed procedures are seriously challengedby the financial meltdown triggered in the fall of 2008 by the failure of major credit institutions,which has pushed a number of firms onto the verge of bankruptcy. Standard & Poor’s reports thatthe European companies default rate in its speculative-grade category is risen to 10% in 2009 and2010, from the average 3.2% over the last fifteen years. I contribute to the analysis of the recentbankruptcy reforms by showing when, in the presence of a problem of moral hazard, a bankruptcylaw that facilitates the renegotiation of financial liabilities encourages the undertaking of long-terminvestments and when, contrarily to the common wisdom, it causes a problem of short-termism ininvestments, that is the choice of investment projects that privilege the achievement of short-termresults.

I employ a principal-agent model with moral hazard, in which a cash constrained entrepreneurcan choose to undertake either a short-term project or a long-term project. The short-term projectreturns a lower net present value than the long-term project. However, the long-term project ex-poses the entrepreneur to the risk of bankruptcy.2 Bankruptcy can be of two types. Soft bankruptcyis designed as a financial renegotiation game that resembles Chapter 11 and the procedures recentlyadopted by European countries in the balance of lender and entrepreneur rights: on the one handthe entrepreneur has the right to ask for the opening of bankruptcy proceedings in front of a courtand devise a restructuring plan, on the other hand lenders have the right to approve or reject theplan. Tough bankruptcy is designed to capture the main characteristics of the pre-reform regimesin France, Germany and Italy, where the resolution of bankruptcy proceedings exhibited a clearbias towards the liquidation of the distressed company (Brouwer, 2006).3 My aim is to comparethe impact of the soft bankruptcy game on firm’s investment choices with respect to the toughbankruptcy benchmark, in which liquidation follows automatically in the case of project’s failure.

To show that renegotiation in bankruptcy affects the optimal contract (and thus the invest-ment choice), I prove that that lender’s behaviour is characterized by limited commitment undera soft code. In the presence of continuation rents, financial renegotiation reduces the room forentrepreneur’s punishment in the case of bad performance: even if the original contract prescribesproject’s termination, the lender allows production’s continuation provided recovery rates increase.This mechanism is borrowed from the literature on the “soft budget constraint” problem (Dewa-

1Section 1.2 discusses the main features of Chapter 11 and the new European codes.2In order to make things more concrete, in what follows the short-term project is designed as a risk-free investment,

like a government bond. Instead, the long-term project is an investment that may deliver high long-run payoffs atthe cost of early failures, like the investments in R&D.

3With particular regard to Italy, Bianco and Romano (2009) document that the number of “in-court” restructuringagreements was almost insignificant in the pre-reform regime (accounting for 1% of the total number of openedprocedures). At the same time, before the 2005-2006 reform, in Italy “out-of-court” renegotiation was inhibited bythe risk of having the court-appointed trustee annul the agreement via claw-back provisions. All this resulted in alegal environment that greatly discouraged financial restructuring (Costantini, 2009).

2

tripont and Maskin, 1995; von Thadden, 1995; Kornai et al., 2003). However, while Dewatripontand Maskin (1995) and von Thadden (1995) focus on the benefits to a principal from the lack ofcommitment to remain tough with an agent, I show that in the presence of moral hazard limitedcommitment can also be costly.

In the model, the softening of lender’s budget constraint generates the following trade-off.On the one hand, the renegotiation of the termination prescription increases ex-post efficiencybecause the lender improves recovery rates, on the other hand it decreases ex-ante efficiency be-cause the prospect of renegotiation raises the agency rent that the lender needs to bear to restoreentrepreneur’s incentives. This trade-off is taken from the literature on mutually advantageousrenegotiation (e.g., among the others, Fudenberg and Tirole, 1990), my contribution to this liter-ature consists in providing an analysis of the effects of renegotiation on ex-ante investment’s timehorizon: depending on whether recovery rates are able to offset the exacerbation of the incentiveproblem, soft bankruptcy can induce long-termism or short-termism in investment.

I model the short-term project as a safe outside option that is not affected by moral hazard.Regarding the long-term project, its value is affected by a moral hazard problem and it exposesthe entrepreneur to the risk of bankruptcy.4 In a setting with tough bankruptcy, contingent ar-rangements can be used to limit the incidence of the moral hazard problem—by punishing theentrepreneur after a bad outcome. If soft bankruptcy is introduced, and in the presence of continu-ation rents, contingent contracts are not renegotiation-proof: on the one hand, this dampens theirability to limit the moral hazard issue, on the other hand this allows them to deliver a larger payoffthanks to recovery rates. I show that, provided the increase in recovery rates is able to offset theexacerbation of the agency problem, long-term projects can still be implemented, otherwise softbankruptcy causes a bias for short-termism.

The short-termism result goes against the conventional wisdom that soft bankruptcy stimulatesentrepreneurship and risk-taking (e.g., Acharya and Subramanian, 2009), however it is consistentwith the empirical evidence concerning the effects caused by the strengthening of entrepreneur’srenegotiation power in bankruptcy on the cost of funding. A widespread empirical proxy for short-termism is the value of the interest rate spreads set by lenders on firms (Blume et al. 1980; Poterbaand Summers, 1995): a higher cut-off value indicates higher pressure on a firm to achieve short-termresults. Interestingly, Scott and Smith (1986) and Rodano et al. (2012) find that the introductionof stronger entrepreneur’s protection to renegotiate outstanding liabilities in bankruptcy has leadto more costly funding contracts. Scott and Smith (1986) study the effects of the 1978 bankruptcyreform in the United States, Rodano et al. (2012) focus on the impact of the recent Italianbankruptcy reform. Both pieces of empirical evidence clearly support the short-termism result.

1.1 Related Literature

An important strand of the theoretical literature on bankruptcy has modeled soft codes as aninformation revelation process in which the economic viability of the distressed firm is examined(Mooradian, 1994; White, 1994). This approach highlights the trade-off between the excessive liq-uidation caused by tough procedures and the excessive continuation generated by soft procedures.5

For example, White (1994) investigates the role of bankruptcy as filtering device in a model withadverse selection and shows that bankruptcy can distort continuation decisions. My paper under-

4As will be clear later, the way I model the short-term and the long-term projects implies that, although the focusof the discussion is on long-termism versus short-termism, the conclusions of the paper are largely applicable to theanalysis of the impact of bankruptcy on the choice between risky versus safe projects.

5This trade-off has also influenced the debate over the design of the optimal bankruptcy reform. See Hart (1995),chapter 7, for a comprehensive discussion on this topic.

3

takes a different modeling approach by designing bankruptcy as a renegotiation game and focusingon the agency costs caused by lenient procedures in the presence of moral hazard.

Part of the received literature has focused on the benefits arising from Chapter 11 ability tosolve the frictions caused by creditors’ mis-coordination (Gertner and Scharfstein, 1991), insteadI look at the inefficiencies caused by the conflicting interests between lender and entrepreneur inbankruptcy. Like in Bolton and Scharfstein (1996), I study the effects of a renegotiation game thatis carried out between lender and entrepreneur. However, the aim of Bolton and Scharfstein (1996)is to determine the optimal number of creditors that is able to minimize the trade-off betweenentrepreneur’s ex-ante incentives to default strategically and the ex-post efficiency costs generatedby liquidation. Instead, in this paper I am rather concerned about the impact of renegotiation onfirm’s investment time horizon.

This article is also related to the literature that studies the “soft budget constraint” problem.Dewatripont and Maskin (1995) and von Thadden (1995) investigate the relationship between the“soft budget constraint” problem and investments’ time horizon, concluding that hardening thebudget constraint may induce short-termism in investment behaviour. In these articles, it is shownthat neglecting to re-finance the projects that yield a low outcome in the short-term hinders theimplementation of both bad projects, and slow, but good, projects that are able to generate veryhigh gains only in the long-run. Clearly, this is not efficient if the higher profitability of long-term projects offsets the losses caused by bad projects. As pointed out in the Introduction, mycontribution to Dewatripont and Maskin (1995) and von Thadden (1995) consists in borrowingthe tension between ex-post and ex-ante efficiency that is at the core of the literature on mutuallyadvantageous renegotiation to show that in the presence of a problem of repeated moral hazardand renegotiation hardening the budget constraint may induce long-termism.6

In analogy to the settings in the “soft budget constraint” literature, in the model the long-term project is more profitable than the short-term one, although more risky. In this respect, thisarticle also deals with financial contracting and corporate risk-taking (e.g., Bebchuk, 2002; Landier,2006). Bebchuk (2002) analyzes how the deviations from the absolute priority rule in Chapter11 proceedings influence equity-holders choice between two investment projects, one riskier thanthe other, and shows that Chapter 11 may trigger inefficient investment choices.7 Finally, Landier(2006) proves that soft bankruptcy stimulates entrepreneurial initiative,8 and the empirical evidencein Acharya and Subramanian (2009) documents the beneficial effects of soft codes on innovation.In what follows, I show that renegotiation in bankruptcy may generate both benefits and costsdepending on the value of recovery rates and the design of funding contracts.

6More specifically, my model differs from von Thadden (1995) insofar as I introduce a problem of moral hazardin both the first and the second period. Moreover, I depart from Baliga and Polak (2004), which also build onDewatripont and Maskin (1995) by introducing a problem of moral hazard, because there authors employ a one-shotgame to study the choice between monitored and non-monitored loans.

7Bebchuk (2002) shows that equity-holders may be tempted to choose the risky project because in failure statesthey are able to secure a positive rent from Chapter 11 negotiations. However, Bebchuk (2002) implicitly assumes thatcreditors are unaware of the type of investment projects available to equity-holders. Instead, I assume that a lendercan observe and verify the investment plan that the entrepreneur undertakes, and the contract can be designed so asto choose the most profitable one. Consequently, I derive the investment strategy choice as function of the equilibriumcontracts and study how the same choice changes with the type of bankruptcy.

8Landier (2006) develops a model where the attitude of capital markets towards failure is endogenous: en-trepreneurship depends on the cost of funding, which in turn depends on markets’ expectations over failed en-trepreneurs’ ability. Landier (2006) shows that soft bankruptcy rules stimulate entrepreneurship because they granta complete debt relief to the failed entrepreneur and reduce the cost of capital necessary to start new projects. Withrespect to the analysis in Landier (2006), I let the “cost of funding” depend on the severity of the moral hazardproblem, which in turn depends on bankruptcy law.

4

Finally, I contribute to the theoretical literature that investigates how an economy’s legal frame-work interacts with bankruptcy proceedings (Ayotte and Yun, 2009; Gennaioli and Rossi, 2010). Inparticular, Ayotte and Yun (2009) look at the role of bankruptcy courts on the efficient enforcementof contracts and Gennaioli and Rossi (2010) study how the degree of creditor’s protection interactswith judicial incentives in bankruptcy.

1.2 Chapter 11 and the New Codes in Europe

In the United States, the Chapter 7 and the Chapter 11 of the federal bankruptcy law providethe discipline that regulates corporate insolvency procedures. Chapter 7 governs the phase ofliquidation, whereas Chapter 11 governs the process of financial restructuring. They are bothcarried out under the oversight of specialized bankruptcy courts.

Chapter 11 ultimate target is to protect a bankrupt firm from outsiders’ pressure while it iscoping with a process of rehabilitation. Chapter 11 prescribes a system of countervailing rightsaimed at protecting both creditors’ and debtors’ interests. On the debtors’ side is the provisionthat allows the entrepreneur to file unilaterally for Chapter 11, at the prospect of potential default.Entry into Chapter 11 opens the debtor-in-possession phase, during which the entrepreneur hasthe right to stop payments to existing lenders (automatic stay) and devise a restructuring plan tobe submitted to creditors by a given period of time.9 During the debtor-in-possession phase, theentrepreneur can also search for new funds and in order to facilitate this, Chapter 11 prescribes thatthe lenders willing to finance bankrupt firms are privileged in the reimbursement of their claims atthe end of the restructuring process—i.e., they can be repaid before (even senior) existing investors.

Creditors have two important rights in Chapter 11: first, they can propose an alternative planto the entrepreneur’s and second, they vote on the restructuring project in a ballot disciplinedby a system of qualified majorities.10 In fact, by rejecting the plan, creditors can reverse therestructuring procedure into a Chapter 7 liquidation process.

Several Euroepan countries have recently adopted bankruptcy procedures a-la-Chapter 11. InGermany, the reform of 1999 introduced a system of corporate reorganization analogous to Chapter11 in the balance of creditor and debtor rights. Like Chapter 11, Germany’s Insolvenzverfahrenprescribes the right of the entrepreneur to open the reorganization phase and the super-seniorityof lenders that fund the bankrupt firm. Moreover, creditors’ have the right to decide over theapproval of the reorganization plan. Unlike Chapter 11, it is a court-appointed administrator thatformulates the reorganization plan and not the bankrupt management.

In 2005, the French legislator reformed the insolvency law by introducing a procedure de sauve-garde: the new system gives to the incumbent management the right to open a reorganizationphase and retain control over the company while devising a financial restructuring plan under theprotection of the automatic stay of creditors’ claims.

Before the 2005/2006 reform, in Italy the insolvency procedure was rather tough with debtors,as bankrupt entrepreneurs were subject to a long phase of rehabilitation before they could starta new enterprise. The pre-reform regime constrained the effectiveness of “in-court” compositionprocedures. At the same time, the law inhibited parties to reach “out-of-court” restructuringagreements, because the bankruptcy trustee could declare invalid the transactions that occurredbetween six months and a year before the company declared bankruptcy via a claw-back provision.All this resulted in a limited use of “in-court” and “out-of-court” agreements as means to resolve the

9The deadline is set by law at 120 days, but the bankruptcy judge can concede extensions.10Creditors vote on the plan by classes of seniority. More specifically, an entire class of claims is deemed to accept

a plan if the plan is accepted by creditors that hold at least two-thirds in amount and more than one-half in number.A vote of acceptance by a class binds all creditors in the same class.

5

phase of distress before the opening of the liquidation phase (Costantini, 2009). The Italian reformstrengthened entrepreneur right to start a process of “in-court” financial reorganization (concordatopreventivo) and negotiate with creditors over the restructuring of outstanding liabilities. Thisresulted in a substantial increase of the number of opened reorganization procedures (Bianco andRomano, 2009).

The article proceeds as follows. Section 2 presents the main model. In Section 3, I firstdiscuss the benchmark case in which the lender can commit to the optimal initial contract with theentrepreneur and liquidate the firm in the case of project’s failure. Then, I relax the assumptionof full commitment, study the impact of the bankruptcy code’s features on equilibrium contractsand present the conditions under which a soft code causes short-termism. Section 4 studies theimplications of the paper main results’ for financial contracting and discusses the empirical evidencesupporting my findings. Section 5 concludes.

2 The Model

The model analyzes a financing game in an environment characterized by asymmetric informationand entrepreneur’s limited liability. There are two classes of risk-neutral agents in the economy:the cash constrained entrepreneur (or borrower, she) and competing lenders.11 I assume that theentrepreneur obtains funding from a single lender (or investor, he) and focus on a representativeentrepreneur-lender pair. Moreover, market interest rates are normalized to zero.

The entrepreneur can choose between two projects, a short-term project and a long-term project.This decision is observable and influences firm’s expected revenues in the following way. The short-term project is modeled as an outside option that returns a net payoff of π0, that, for simplicity isnormalized to zero.12 The long-term project extends over up to two periods, it requires an outlayof I > 0 to be started and a further infusion of I > 0 to be completed. In the first period thelong-term project delivers a payoff equal to Π > 0 in the case of success, zero in the case of failure.In the second period, the long-term project generates an expected return equal to ΠH if it deliversΠ in the first period, ΠL if it delivers a nil outcome in the first period, with ΠH > ΠL. I assumethat the entrepreneur can bring leftovers from the first to the second period.

The profitability of the long-term project is affected by a problem of repeated moral hazard.The entrepreneur must decide in each period whether to exert effort or shirk. In the first period, themoral hazard problem is designed as in Holmstrom-Tirole (1997). I assume that if the entrepreneurputs in effort she would succeed with probability σ ∈ (0, 1) and if she shirks, she would fail withcertainty but gain private benefits B > 0.13 In the second period, the moral hazard problem isdesigned in a reduced form: more specifically, the long-term project succeeds and returns a positivepayoff only if effort is exerted by the entrepreneur. In turn, the entrepreneur requires the paymentof a reward at least equal to B > 0 to put in effort.

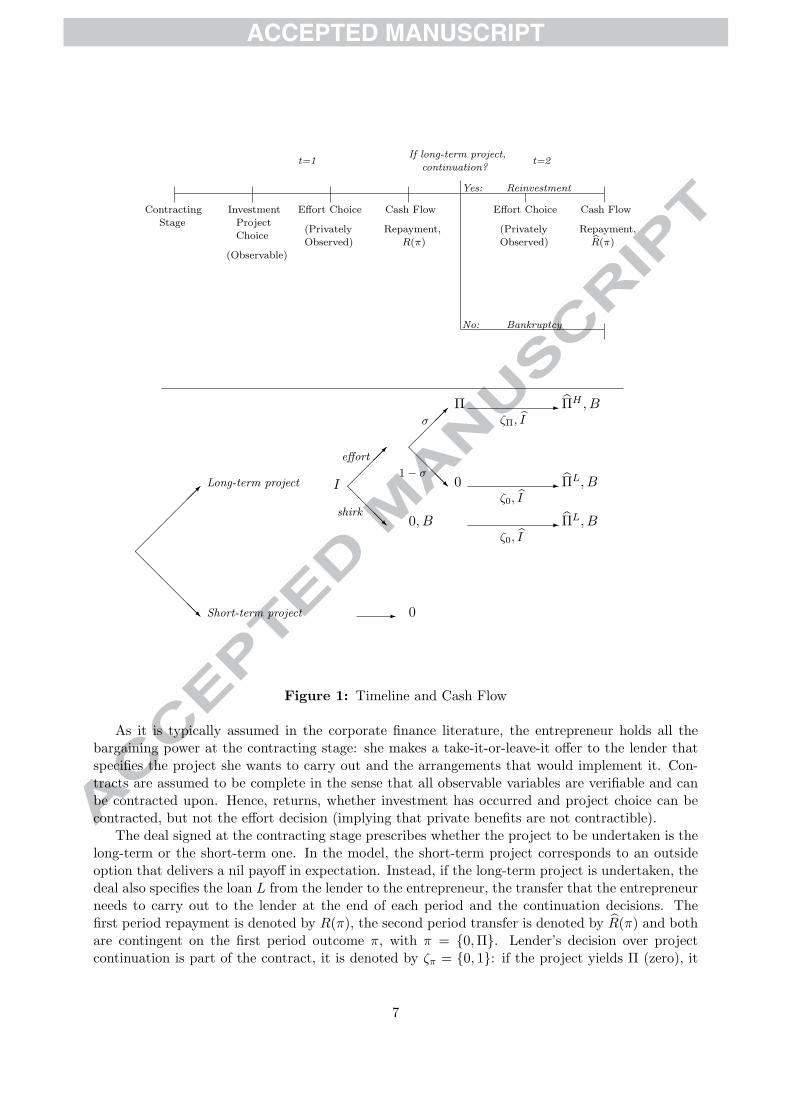

Time-line and cash flow of the game are given in Figure 1.

[FIGURE 1 ABOUT HERE]

11In fact, what follows also applies to managerial firms in which managers’ interests are perfectly aligned withequity-holders’.

12Notice that this is without loss of generality. The quality of the results would stay the same provided the short-term project’s probability of success is higher than the one of the long-term project and the short-term project presentvalue is lower in expectation.

13Assuming that the effort decision is binary simplifies the exposition. From the modeling point of view, theapproach employed implies that the private benefits B measure the opportunity cost of effort. Instead, in a modelwith a continuum of effort levels the agent would choose the optimal amount of effort by trading off the monetarycost of putting an additional unit of effort with the ensuing increase in the probability of project’s success.

6

Contracting

Stage

Investment

Project

Choice

(Observable)

Effort Choice

(Privately

Observed)

Cash Flow

Repayment,

R(π)

If long-term project,

continuation?t=1 t=2

Yes: Reinvestment

No: Bankruptcy

Effort Choice

(Privately

Observed)

Cash Flow

Repayment,R(π)

�������

�����

�����

�������

�

�

�

Long-term project

Short-term project

I

�����

�����

σ

1− σ

Π

0

0, B

ΠH , B

ΠL, B

ΠL, B

ζΠ, I

ζ0, I

ζ0, I

effort

shirk

� 0

Figure 1: Timeline and Cash Flow

As it is typically assumed in the corporate finance literature, the entrepreneur holds all thebargaining power at the contracting stage: she makes a take-it-or-leave-it offer to the lender thatspecifies the project she wants to carry out and the arrangements that would implement it. Con-tracts are assumed to be complete in the sense that all observable variables are verifiable and canbe contracted upon. Hence, returns, whether investment has occurred and project choice can becontracted, but not the effort decision (implying that private benefits are not contractible).

The deal signed at the contracting stage prescribes whether the project to be undertaken is thelong-term or the short-term one. In the model, the short-term project corresponds to an outsideoption that delivers a nil payoff in expectation. Instead, if the long-term project is undertaken, thedeal also specifies the loan L from the lender to the entrepreneur, the transfer that the entrepreneurneeds to carry out to the lender at the end of each period and the continuation decisions. Thefirst period repayment is denoted by R(π), the second period transfer is denoted by R(π) and bothare contingent on the first period outcome π, with π = {0,Π}. Lender’s decision over projectcontinuation is part of the contract, it is denoted by ζπ = {0, 1}: if the project yields Π (zero), it

7

is allowed to continue when ζΠ = 1 (ζ0 = 1), terminated otherwise (ζπ = 0). Finally, the long-termproject has positive pledgeable income in the second period, that is ΠL − I −B > 0.14

If effort is put in the project, the expected payoff of the entrepreneur is denoted by E and isgiven by

L− I + σ[Π−R(Π) + ζΠ(ΠH − R(Π)− I)] + (1− σ)[−R(0) + ζ0(Π

L − R(0)− I)].

Instead, the expected payoff of the lender is denoted by P and is given by

−L+ σ[R(Π) + ζΠ R(Π)] + (1− σ)[R(0) + ζ0 R(0)].

The Nash equilibrium contract that implements the long-term project must satisfy the followingset of constraints. First, a constraint related to the amount of the loan:

L ≥ I.

Then, the entrepreneur incentive constraints related to effort provision in the first (IC1) and inthe second period (IC2,π) must be satisfied. They are all given in the following:

Π−R(Π) + ζΠ(ΠH − R(Π)− I) ≥ B/σ −R(0) + ζ0(Π

L − R(0)− I), (IC1)

ΠH − R(Π)− I ≥ B, (IC2,Π)

ΠL − R(0)− I ≥ B. (IC2,0).

The lender’s participation constraint is such that:

P ≥ 0. (PC)

The limited liability constraints that must be satisfied in the first period are:

R(π) ≤ L− I + π − ζπI. (LL1,π) (1)

This formulation of the first period limited liability constraints takes into account that the en-trepreneur needs to enter the second period with sufficient resources to fund the continuation ofthe long-term project. In the second period, limited liability is fulfilled if the constraints belowhold true:

R(Π) ≤ L− I +Π−R(Π) + ΠH − I, (LL2,Π) (2)

R(0) ≤ L− I −R(0) + ΠL − I. (LL2,0) (3)

The model will be solved under the following parametric assumptions.

ASSUMPTION 1.i. Π+ ΠH − I/σ −B/σ < I + I/σ + [B − (1− σ)(ΠL − I)]/σ.ii. σΠ > I + I.

Assumption 1.i allows me to restrict the scope of the analysis of the implementation of the long-term project to the case of short-term contingent contracts, ruling out long-term non-contingentcontracts. Assumption 1.ii implies that the expected payoff in the case of first period success is

14By pledgeable income I mean the surplus delivered by the project net of the cost related to the investmentallotment and private benefits (Tirole, 2006).

8

large enough, so that the first period limited liability condition relative to short-term contracts issatisfied.

At this stage it is instructive to illustrate the tension generated by the value of ζ0 on (IC1) andE in order to catch the main model’s trade-off. On the one hand, were ζ0 to be equal to 1, thenthe value of E would increase, due to the assumption of project’s positive net present value in thesecond period. On the other hand, setting ζ0 equal to 1 implies that the right-hand-side of (IC1)increases, as the entrepreneur will ask for a reward to carry out the project in the second period.

Before proceeding with the presentation of the bankruptcy game, a number of simplifications canbe operated to the constraints above. First, one can set ζΠ = 1, that is the entrepreneur is alwaysgiven the chance to continue if the project succeeds in the first period, for two reasons: first, becausea positive continuation decision improves entrepreneur’s incentives and, second, because the secondperiod pledgeable income is positive. Also, R(0) = 0, due to first period limited liability. Finally,perfectly competitive financial markets imply that lender participation constraint is binding, thatis P = 0.

2.1 The Bankruptcy Game

Under the tough procedure, entry into bankruptcy takes place when the project fails (π = 0) andis terminated (ζ0 = 0).15 The tough bankruptcy case provides a benchmark in which financialrestructuring is not permitted and with respect to which it is studied how the introduction ofrenegotiation in bankruptcy changes corporate investment time-horizon. To corroborate the validityof such a benchmark, note that this assumption is consistent with the evidence concerning thoselegal environments, like the United Kingdom and the pre-reform Italy, that are characterized bya tough code. Franks and Sussman (2005) show that in the United Kingdom banks keep a severestance towards debt renegotiations and argue that this is done to avoid strategic default. At thesame time, before the 2005/2006 reform, in Italy the number of financial restructuring procedureswas negligible, because of the inefficient design of the “in-court” procedure (Costantini, 2009).

Under the soft procedure the entrepreneur can open a financial restructuring stage. Thebankrupt entrepreneur is allowed to renegotiate the funding contract’s prescriptions under the pro-cedure provided by the law. In particular, the following “in-court” soft bankruptcy renegotiationgame takes place.16

1. The entrepreneur searches for new funds on competitive financial markets.

2. If the entrepreneur finds a new lender, this lender makes her an offer.

3. In the case of offer acceptance, the first period lender must decide either to agree on thecontinuation plan or reject it. Such a decision is the outcome of an ultimatum game in whichthe first period lender has all the bargaining power and makes a take-it-or-leave-it offer to theagent. This offer specifies the payoff that the lender requires to allow project continuationand is denoted by r.

4. If the entrepreneur accepts the first period lender’s offer, the firm continues its activity andthe second period time structure is the same as in the case of continuation out of bankruptcy.Otherwise, the firm is shut down and the entrepreneur is dismissed.

15Von Thadden (1995) interprets a termination policy of this sort (that is, featuring ζ0 = 0) as liquidation. Also,Povel (1999) adopts an analogous approach to characterize entry in bankruptcy by denoting project’s termination asa tough bankruptcy rule.

16The “in-court” label is employed to stress that the proposed renegotiation procedure is the one carried out underthe prescriptions of the law. In fact, the court plays no active role in the game.

9

The structure of the moral hazard problem in the event of continuation in bankruptcy is modeledin the same way as out of bankruptcy; the entrepreneur needs to be rewarded by B in order to putin effort.

The soft bankruptcy game above shares important analogies with a real Chapter 11. First, it isthe entrepreneur that has the right to file for the opening of the procedure in front of the competentbankruptcy court. Second, once the procedure is open the firm in Chapter 11 can search for newfunds while renegotiating with existing lenders. Finally, in a Chapter 11 the lenders vote on theplan proposed by the company. These three phases are clearly embedded in the soft bankruptcygame of the model.

Two other things must be stressed. First, the lender that provides new liquidity in the secondstage of the renegotiation game need not be different from the first period one. Indeed, in both casesthe model would deliver the same type of results.17 Then, since the renegotiation phase is structuredas an ultimatum game, the allocation of the bargaining power determines the equilibrium outcomes.I assume that the first period lender has all the bargaining power, thus giving to the lender thecrucial right to decide on firm continuation in bankruptcy. This approach might seem inconsistentwith the assumption of competitive financial markets (in such a case, the entrepreneur should holdall the bargaining power), nonetheless it allows the soft bankruptcy game to resemble as closelyas possible a real Chapter 11, in which creditors can reject the entrepreneur’s plan or propose analternative plan. This modeling choice also implies that the lender is the residual claimant of theproject therefore, depending on the offer he formulates, recovery rates’ can increase. In this way,I can study how lender’s incentives to allow continuation affect firm’s investment.18 Finally, it isimportant to remark that if I would assume that the bargaining power allocation in bankruptcyis consistent with the one in the first period contracting game my results would not change (ifanything, they would just be reinforced).

2.2 First Best

Analyze first the scenario in which the entrepreneur is not cash constrained and there is no problemof moral hazard. I assume that in these circumstances the long-term project generates a net presentvalue higher than the one attached to the short-term project and therefore determines the value ofthe firm in the first best scenario.

σ(Π + ΠH) + (1− σ)ΠL − I − I > 0. (4)

In what follows, it is first presented how the contracting game changes when the moral hazardproblem is introduced into the analysis and then when the problem of limited commitment isaccounted for.

3 Model Solution

In this section, I derive the equilibrium contracts that the entrepreneur may want to propose tothe lender, first under the assumption of full commitment and then under limited commitment.

17The empirical evidence provided by Daihya et al. (2003) on Chapter 11 debtor-in-possession funding contractsconfirms that bankrupt firms receive money from both investors with whom they already have a lending relationshipand new investors.

18Indeed, by making an unfeasible offer the lender can implicitly enforce the optimal contract under full commit-ment.

10

3.1 Contracting with Full Commitment

To begin with, with respect to the first best scenario I assume that the entrepreneur is cashconstrained and a problem of moral hazard undermines the profitability of the long-term project.Therefore, the constraints related to entrepreneur’s private decisions on effort provision must betaken into account. Nevertheless, thanks to full commitment, renegotiation does not affect theinvestment strategy choice because at the interim stage the lender sticks to the contract signed atthe outset of the game.

Following von Thadden (1995), I define long-term non-contingent contracts those deals forwhich funds for both periods are given at the contracting stage and the long-term project continuesindependently from the first period outcome. Instead, short-term contingent contracts are suchthat the project is terminated in the event of a nil outcome and the loan provides funds only forthe first period. Lemma 1 shows that the long-term project cannot be implemented via long-termnon-contingent deals under the parametric assumptions of the model.

LEMMA 1. Under Assumptions 1.i, long-term non-contingent contracts violate the entrepreneurfirst period incentive constraint and cannot be employed to implement the long-term project.

Proof. See Appendix A.

By inducing the lender to commit to grant a loan that covers the outlays relative to periods 1and 2 and allowing the entrepreneur to continue independently from the first period outcome, long-term non-contingent contracts exacerbate the first period moral hazard problem. Consequently,under Assumption 1.i the incentive constraint related to effort provision is violated and this classof contracts cannot be employed to implement the long-term project.19 The result in Lemma 1allows me to restrict the analysis that follows to short-term contingent deals. In particular, Lemma2 presents the short-term contracts that implement the long-term project at an equilibrium withfull commitment.

LEMMA 2. The long-term project can be implemented by short-term contingent contracts thatfeature ζΠ = 1, ζ0 = 0 and L = I. Moreover, they feature R(Π) = I/σ and R(Π) = 0. At theseconditions, the lender’s breaks even in expectation and the relevant constraints are satisfied underAssumption 1.ii, and if the entrepreneur first period incentive constraint holds true:

Π+ ΠH − I/σ −B/σ ≥ I. (5)

The value of E generated by these contracts is equal to

σ(Π + ΠH − I)− I,

which is lower than in the first best.

Proof. See Appendix B.

The short-term contingent contracts in Lemma 2 reward the entrepreneur in the long-run, bytaxing her in the short-run. In particular, the first period repayment (R(Π)) allows the lender to

19This assumption is just for the sake of the exposition, all results would go through if non-contingent long-termcontracts would be feasible.

11

break-even in expectation. In turn, the entrepreneur funds the second period investment out offirst period profits and keeps for herself all long-run receipts.20

The equilibrium of the investment game is in Proposition 1.

PROPOSITION 1. Two cases must be distinguished:

1. If the first period incentive constraint related to the contract in Lemma 2 holds true, that is

Π+ ΠH − I/σ −B/σ ≥ I, (6)

the entrepreneur offers a short-term contingent contract as in Lemma 2 and the long-termproject is implemented if the following condition is satisfied:

σ(Π + ΠH − I)− I ≥ 0. (7)

2. Conversely, if the first period incentive constraint related to the contract in Lemma 2 doesnot hold true, that is

I > Π+ ΠH − I/σ −B/σ, (8)

then the offer formulated by the entrepreneur prescribes the choice of the short-term project.

If (6) holds, implying that (5) is fulfilled, short-term contingent contracts are viable and thelong-term project is chosen if condition (7) is satisfied. In turn, if (5) is violated, the short-termproject is chosen by the entrepreneur.

3.2 Contracting with Limited Commitment

In this section, I present how the contracting game is affected by limited commitment. The de-parture from full commitment implies that lender’s ability to enforce the contracts in Lemma 2depends on bankruptcy law.

Tough code If the procedure is tough, then liquidation follows project’s termination; therefore,the same contracts as in Lemma 2 can be employed to implement the long-term project and theinvestment choices at equilibrium are as in Proposition 1.21

Soft code If bankruptcy is soft and the initial contract prescribes project’s termination, theentrepreneur has the right to open a bankruptcy game as in Section 2.1, by which she can searchfor new lenders and the first period lender has the power to permit or prevent continuation.22 InLemma 3 I show that the lender allows continuation because this makes recovery rates improve;consequently, a tension arises between ex-post and ex-ante efficiency that influences the investmentchoice.

20Long-term contingent contracts can be constructed in analogy to the equilibrium short-term contingent dealsand would feature the provision of continuation finance only in the case of first period success. Although I do notconsider long-term contingent contracts in the analysis, it can be shown that the conditions for their implementationare the same as those related to short-term contingent arrangements. Moreover, they deliver the same payoff as theshort-term contingent contracts presented in Lemma 2.

21Note that this result can be rationalized by a model with “out-of-court” renegotiation in the shadow of a toughbankruptcy law. A formal proof can be provided by the author upon request.

22In this section I assume that renegotiation can only take place following the rules prescribed by the bankruptcycode. Also in this case, the same results can be obtained if contracts can be renegotiated under the shadow of thesoft bankruptcy game of Section 2.1. A formal proof is omitted, but is available upon request.

12

LEMMA 3. Under the soft bankruptcy game, the short-term contingent contracts in Lemma 2 arenot renegotiation proof. More specifically, the first period termination clause is renegotiated awayin exchange of a transfer of r = ΠL − I −B from the entrepreneur to the lender.

Proof. See Appendix C.

If the procedure is soft parties need to write renegotiation proof contracts at the outset of thegame. Indeed, Lemma 3 shows that contingent contracts’ termination clause is not renegotiationproof. The reason is that parties need to take into account that in the event of first periodproject failure the entrepreneur can open a restructuring phase and the lender accepts to let theentrepreneur continue behind the payment of r = ΠL − I − B > 0. The outcome of the newcontracting game is in Lemma 4.23

LEMMA 4. Under soft bankruptcy, the entrepreneur can offer renegotiation proof short-term con-tingent contracts that feature L = I, ζΠ = 1, ζ0 = 0, R(Π) = [I − (ΠL − I − B)(1 − σ)]/σ andR(0) = R(Π) = 0. At these conditions, the lender breaks even in expectation and the relevant con-ditions are satisfied under Assumption 1.ii and if the entrepreneur first period incentive constraintholds true:

Π+ ΠH − I/σ −B/σ ≥ I + [B − (1− σ)(ΠL − I)]/σ. (9)

Finally, E is as in the first best (4).

Proof. See Appendix D.

The contingent deals in Lemma 4 are renegotiation proof because the repayments’ scheduletakes into account that if π = 0 the consequent soft bankruptcy game allows the lender to squeezer = ΠL − I −B in the second period and improve recovery rates following a nil outcome.

Lemma 4 unveils the main trade-off triggered by renegotiation in bankruptcy. The upside fromsoft bankruptcy is that short-term contingent contracts generate the same payoff as in the firstbest. The downside from soft bankruptcy lies in its impact on incentives. More specifically, ifB > (1 − σ)(ΠL − I), that is, if the net present value of the project in the second period is smallenough, then the contingent contracts’ first period incentive constraint under the soft code (9) ismore binding than the one under the tough code (5). Conversely, if B ≤ (1− σ)(ΠL − I) then theopposite is true. The following proposition presents the impact of soft bankruptcy on investment.

PROPOSITION 2. Two cases must be distinguished:

1. If the first period incentive constraint related to the contract in Lemma 4 holds true, that is

Π+ ΠH − I/σ −B/σ ≥ I + [B − (1− σ)(ΠL − I)]/σ, (10)

the offer formulated by the entrepreneur prescribes the choice of the long-term project and thearrangements in the short-term contingent contracts of Lemma 4.

2. If the first period incentive constraint related to the contract in Lemma 4 does not hold true,that is

I + [B − (1− σ)(ΠL − I)]/σ > Π+ ΠH − I/σ −B/σ, (11)

the offer formulated by the entrepreneur prescribes the choice of the short-term project.

23Note that the long-term non-contingent contracts ruled out as a result of Lemma 1 would be immune to renego-tiation, because they grant continuation independently of the first period outcome. Therefore, the result in Lemma1 is not affected by soft bankruptcy.

13

If (10) is satisfied, then the entrepreneur undertakes the long-term project and gets funded viaa short-term contingent deal. However, if (10) does not hold true then the long-term project cannotbe implemented by the short-term contracts in Lemma 4 and the entrepreneur is bound to choosethe short-term project. Proposition 3 puts forward the result on short-termism.

PROPOSITION 3. If I ≤ Π+ ΠH − I/σ − B/σ < I + [B − (1− σ)(ΠL − I)]/σ, then the long-term project cannot be implemented under soft bankruptcy. Instead, the long-term project can beimplemented under tough bankruptcy via a short-term contingent contract if the following conditionis satisfied:

σ(Π + ΠH − I)− I ≥ 0.

Proof. The proof follows by comparing the conditions for the investment decision in Proposition1 with the conditions in Proposition 2.

Proposition 3 shows that renegotiation in bankruptcy may cause short-termism in investment.24

The intuition for this result is straightforward. On the one hand, a lenient procedure reduces thescope for the implementation of the contractual instruments available to cope with entrepreneur’smoral hazard. On the other hand, it improves lender’s recovery rates in the event of first periodinsolvency. Once the assumption of full commitment is relaxed, Lemma 3 shows that it is notrational to the lender, at the interim stage, to refuse any finite rent from renegotiation, even if thiscomes at the cost of loosening the impact of the continuation decision.

Proposition 3 puts forward clear empirical predictions regarding the characteristics of real-lifeprojects that are associated with the condition under which soft bankruptcy leads to short-termismin investment. More specifically, the chances to implement the long-term project under a softprocedure decrease if the volatility of the project is large, that is, σ is low, or the value of theproject following a nil outcome is low, that is, ΠL is small. These features are consistent with thesalient characteristics of R&D projects, thus the condition in the proposition hints that innovativeentrepreneurial initiatives are more likely to be discouraged by the soft-budget constraint problem.At the same time, the condition is more likely to be met if the moral hazard problem is severe (highB), suggesting that in the presence of low monitoring or managerial entrenchment the long-termproject is less likely to be undertaken.

In the following section, I will analyze the implications of these results for financial contractingand the contractual instruments that may attenuate the short-termism bias. Indeed, by openingup the contracts’ box parties may try to circumvent the inefficiencies that arise because of therelaxation of the continuation decisions’ effect.

4 Implications for Financial Contracting and Empirical Evidence

In this section, I study two contractual arrangements that may be employed by parties to mitigatethe short-termism bias generated by soft bankruptcy under limited commitment. Namely, I considerthe adoption of a turnover clause and the use of collateral.

24Note that the mechanism by which short-termism arises in this paper is different from the one in Diamond (2004).Diamond (2004) shows that in weak legal environments and with multiple lenders, short-term debt is the contractthat allows a creditor to minimize the deadweight loss that he would suffer from a run on a borrower by the otherlenders. In other words, Diamond (2004) shows that holding the right to deny re-financing, and keep the budgetconstraint tight, a lender is less exposed to the negative externality imposed by other lenders when these require anearly stage repayment.

14

4.1 Management turnover

In what follows, I consider a game in which the parties can write on the financial contract signedat the outset of the game a clause that triggers the substitution of the incumbent entrepreneur(management) in the event of first period failure. The soft bankruptcy game played by parties atthe intermediate stage is structured as in what follows.

1. The first period lender searches for a new entrepreneur and decides whether to fire the oldentrepreneur.

2. The entrepreneur in charge searches for new funds on competitive financial markets.

3. If a new lender is found, this makes an offer to the entrepreneur.

4. In the case of offer acceptance, the first period lender must decide either to agree on thecontinuation plan or reject it. More specifically, such a decision is the outcome of an ultimatumgame in which the first period lender has all the bargaining power and makes a take-it-or-leave-it offer to the agent. This offer specifies the payoff that the lender requires to allowproject continuation and is denoted by r.

5. If the entrepreneur accepts the first period lender’s offer, the firm continues its activity andthe second period time structure is the same as in the case of continuation out of bankruptcy.Otherwise, the firm is shut down.

The lender exerts the substitution clause after first period project’s failure if the new en-trepreneur (management) is able to improve the value of the firm in the second period. Instead,if the net pledgeable income generated by the new entrepreneur (management) in the second pe-riod is lower than the one associated to the incumbent entrepreneur (management), at the interimstage the lender would not exert the turnover clause. This implies that the scope for entrepreneurturnover in the case of small and medium firms (entrepreneurial firms) might be limited, becausethe incumbent entrepreneur’s skills are often crucial for these firms to be profitable (Baird andRasmussen, 2002).25 Instead, as far as managerial firms are concerned, it is important that themarket for managers is lively enough for the lender to find a suitable substitute at the bankruptcystage.

COROLLARY 1. Under limited commitment and management turnover, if the lender can finda entrepreneur (manager) under which the pledgeable income generated by the firm increases afterfirst period failure, then the threat of incumbent entrepreneur (management) substitution is morelikely to lead to the choice of the long-term project.

Summarizing, the turnover clause has the potential of restoring an efficient investment choice,provided a new entrepreneur (manager) that is able to increase firm’s profitability in the secondperiod is hired. Regarding managerial enterprises, this prediction is consistent with the results of theempirical analysis in Bharath et al. (2007), who document that management turnover in Chapter11 has increased since 1990, leading to a smaller number of absolute priority rule’s violations. Asfar as entrepreneurial firms are concerned, the threat of substitution might be less binding becausethe know-how of the incumbent entrepreneur may turn out to be crucial for their business to beprofitable. Therefore, the short-term result in Proposition 3 is more likely to carry out for thecategory of entrepreneurial firms.

25In Bolton and Scharfstein (1996) a liquidated project can be taken over by a new manager (entrepreneur) thatcannot get out of it as much as the incumbent manager (entrepreneur). Under such an assumption, managementturnover would never solve the short-termism bias.

15

4.2 Collaterized Loan and Automatic Stay

In this section, I present the results of the contracting game with limited commitment and softbankruptcy when the entrepreneur can pledge collateral, C. I assume that C consists of en-trepreneur’s existing non-project-related wealth and that it can be seized by the lender in the caseof first period project’s failure.26

Moreover, as in Chapter 11, I assume that the procedure entitles the entrepreneur to invokethe automatic stay of creditor’s claim. If protected by automatic stay, the entrepreneur has theright to enter in bankruptcy and creditors cannot take any immediate action to recover theircollateral. Consequently, the collateral is added to project’s continuation value,27 so that the valueof r increases to ΠL − I − B + C. This leads to the conclusion that, if the entrepreneur is ableto raise C such that relevant constraints are satisfied,28 then the implementation of the long-termproject can be viable. The reason is that collateral provides a new stick to use as punishment inthe case of first period failure.

COROLLARY 2. Under limited commitment and soft bankruptcy, collateral facilitates the choiceof the long-term project.

The result in Corollary 2 is consistent with the findings in the empirical investigation by Bergeret al. (2011), where it is shown that the use of collateral is inherently related to lenders’ need tofix the problems caused by asymmetric information in the relationship with entrepreneurs.

Management turnover and collateral can help solve the short-termism bias, even though undersome limitations. The turnover clause is a natural candidate to solve the short-termism problemfor managerial firms. However, it is less clearcut whether it would be effective for entrepreneurialfirms whose business crucially relies on incumbent entrepreneurs’ skills. Finally, if the entrepreneuris able to raise collateral, then efficiency in investment is restored via the introduction of a newpunishment device.

4.3 Empirical Evidence: Bankruptcy Law and the Cost of Finance

The major prediction of the paper regards the effect that renegotiation in bankruptcy has on ex-ante investment choices: more specifically, in the model, agency costs increase to generate a biasfor short-termism. A widespread proxy for short-termism is the value of cut-off rates set by bankson firms (Blume et al. 1980; Poterba and Summers, 1995): a higher cut-off value indicates ahigher pressure on firm’s entrepreneur (management) to achieve short-term results. Accordingly,the model would suggest that the introduction of renegotiation in bankruptcy should trigger higherinterest spreads.

Direct support to this result is provided by Scott and Smith (1986) and Rodano et al. (2012).Scott and Smith (1986) analyze the impact of the United States 1978 reform of corporate bankruptcyon the cost of financing for small and medium enterprises. The reform aimed at facilitating dis-tressed firms’ financial restructuring in Chapter 11 (for example, it is the 1978 reform that intro-duced the automatic stay of creditors’ claims in Chapter 11). The results in Scott and Smith (1986)corroborate the results in this paper, because they show that interest spreads on loans increased

26I follow Tirole (2006) chapter 4 in the way collateral is modeled. More specifically, C may consist of wealth thatis too illiquid to be invested directly into the project, but can be used as collateral, like an entrepreneur’s house orfirm’s stock holdings in other companies.

27If the automatic stay is not contemplated by the bankruptcy law, then the lender can decide either to seize thecollateral or to allow for project’s continuation in bankruptcy and analogous results would be obtained.

28Note that the limited liability conditions in this framework will be more binding than in the benchmark model.

16

after the reform. Rodano et al. (2012) test the impact of the 2005/2006 Italian bankruptcy lawreform on firms’ access to credit and show that interest rates’ spreads on loans and credit linesincreased after the introduction of the new concordato preventivo, which strengthened entrepreneurright to renegotiate outstanding liabilities (see Section 1.2 above for more details).

Indirect support to the results in this article is in Qian and Strahan (2007) and John et al.(2008). The former show that stronger creditor protection is associated with lower interest ratesand longer term lending, the latter find that stronger creditor protection triggers more value-enhancing investments. The interpretation to the results in John et al. (2008) is that strongercreditor protection hampers managers’ rent extraction behavior and triggers efficient investmentchoices, and is consistent with the theoretical arguments in this paper.

5 Conclusions

The model challenges the common wisdom that soft bankruptcy encourages long-termism and risk-taking by developing a theory that hinges on two well-known principles: the “soft budget constraint”problem and the impact of renegotiation on ex-ante incentives in the presence of moral hazard. Ina nutshell, the basic mechanism goes as follows. Under a soft procedure, the implementationof contingent funding contracts is subject to a problem of “soft budget constraint”, for which thelender is tempted to renegotiate the termination clause and let the entrepreneur continue if recoveryrates increase. In other words, the lender cannot commit to liquidate the firm if there is a positivebenefit to be captured from second period production. This weakens the ability of the contract tosolve the moral hazard problem embedded in the first period production and implies that if thereare not sufficient rents in the second period it may be optimal for the entrepreneur to select theshort-term project.

The short-termism result is supported by several pieces of empirical evidence on the effects ofthe introduction of stronger entrepreneur’s renegotiation power in bankruptcy on the cost of finance(e.g., Scott and Smith, 1986; Rodano et al., 2012). Moreover, the model is simple and can be easilyextended to analyze the robustness of the short-termism result in alternative contracting environ-ments. For example, in my future research I plan to extend the analysis developed in this articlein a setting with multiple lenders, so to disentangle to what extent and in which circumstancesthe ability of a bankruptcy law a-la-Chapter 11 to solve creditors’ mis-coordination (Gertner andScharfstein, 1991) can offset the inefficiencies arising from agency problem’s exacerbation.

17

A Proof of Lemma 1

To show that long-term non-contingent contracts are not implementable under Assumption 1.i and fullcommitment, I analyze two classes of arrangements of this sort that feature L = I + I and ζ0 = ζΠ = 1.First, I consider long-term contracts that subsidize the entrepreneur following first period failure by leavingall the net pledgeable income of the project to the entrepreneur. Then, I consider long-term contracts thattax the entrepreneur after first period failure by squeezing the full net pledgeable income of the project. Ishow that the latter class of contracts would be preferred to the former, but neither is implementable underAssumption 1.i.

1. Consider the family of arrangements such that R(Π) + R(Π) = I/σ + I/σ and R(0) = 0. By settingR(0) = 0, the entrepreneur fully squeezes the surplus generated by the project in the second period

following a nil outcome. Moreover, since, by Assumption 1.ii, σΠ ≥ I + I then one can set R(Π) =

I/σ + I/σ and R(Π) = 0.

The value of E associated to this kind of contracts is as in the first best (4), and all relevant constraintsare satisfied under Assumption 1 and (IC1), that is if

Π + ΠH − I/σ −B/σ ≥ ΠL + I/σ. (12)

2. Consider the long-term contracts that feature R(Π) + R(Π) = [I + I − (ΠL − I − B)(1 − σ)]/σ ≡ ˜R

and R(0) = ΠL − I − B. R(0) = ΠL − I − B implies that the lender squeezes the payoff generated

by the project in the second period following a nil outcome. Moreover, σΠ ≥ I + I (Assumption 1.ii)

implies that one can set R(Π) = ˜R and R(Π) = 0.

The value of E under this contract is as in the first best (4), and all relevant constraints are satisfiedunder Assumption 1 and (IC1), that is if

Π + ΠH − I/σ −B/σ ≥ I + I/σ + [B − (1− σ)(ΠL − I)]/σ, (13)

which is less binding than (12) if ΠL − I −B > 0 (true by assumption).

Given that (12) is more binding than (13) and both types of contracts generate the first best, theentrepreneur would prefer to offer a long-term non-contingent contract in the second category. However,(13), and thus (12), is never satisfied under Assumption 1.i, implying that neither class of long-term non-contingent contracts can be employed to implement the long-term project.�

B Proof of Lemma 2

In what follows I present the short-term contingent contracts that implement the long-term project underthe assumption of full commitment. These contracts feature L = I and ζ0 = 0. Moreover, R(Π) = I/σ andR(Π) = 0. Consequently, the value of E is equal to

σ(Π + ΠH − I)− I,

which is lower than in the first best, the lender’s participation constraint holds with equality and the firstperiod incentive constraint is given by:

Π + ΠH − I/σ −B/σ ≥ I. (14)

If (14) is satisfied and under Assumption 1.ii all relevant conditions are satisfied (see Table 1).

[TABLE 1 ABOUT HERE]

18

Table 1: Short-term Contingent Contracts Constraints

Constraints

ΠH − I −B ≥ 0 (IC2,Π)

σΠ ≥ I + σI (LL1,Π)

0 ≥ 0 (LL1,0)

Π + ΠH − I/σ ≥ I (LL2,Π)

C Proof of Lemma 3

Under the short-term deal in Lemma 2, the initial contract prescribes project termination (ζ0 = 0) in thecase of first period failure. If the procedure is soft, the bankruptcy game in Section 2.1 takes place. I solveit in what follows.

If the entrepreneur finds a new lender on competitive financial markets, this makes her an offer atwhich the entrepreneur is residual claimant and the new lender breaks even in expectation. Consequently,conditional on offer acceptance, second period net present value is equal to ΠL− I−B > 0. However, beforethe project is implemented, the first period lender must agree on continuation.

The first period lender has monopoly power in the ultimatum game with the entrepreneur: he makesher an offer consisting in the value of r required to allow continuation. The initial lender’s offers eitherr > ΠL − I − B or r = ΠL − I − B.29 In the former case, the lender would implicitly enforce the ex-anteoptimal contract, because the entrepreneur would not be able to repay and parties’ payoffs would be zero atthe end of bargaining. In the latter case, the offer is feasible for the entrepreneur.

At the Nash equilibrium of the bargaining game, the first period lender asks for r = ΠL − I −B and theentrepreneur accepts. This implies that the termination clause is not renegotiation proof.30

D Proof of Lemma 4

In Appendix C, I show that contingent contracts are not renegotiation-proof. In particular, the Nashequilibrium of the bankruptcy game of Section 2.1 is such that the entrepreneur gets B and the lender getsr = ΠL − I −B, so the new contracting problem can be reformulated as in what follows.

The expected payoff of the entrepreneur is given by

L− I + σ[Π−R(Π) + ΠH − R(Π)− I] + (1− σ)[ζ0(ΠL − R(0)− I) + (1− ζ0)B].

Instead, the expected payoff of the lender (P) is given by

−L+ σ[R(Π) + R(Π)] + (1− σ)[ζ0 R(0) + (1− ζ0)(ΠL − I −B)].

The optimal contract must satisfy the following set of constraints. First of all, a constraint related tothe amount of the loan:

L ≥ I.

29Offering less than the value of the pledgeable income is not rational, given the assumption on the bargainingpower, because the lender could always increase the offer and induce the entrepreneur to accept.

30The remaining prescriptions of the short-term contingent deals are renegotiation proof. In particular, partieshave no incentive to renegotiate the prescription of continuation in the event of first period success because it is inboth interest to continue. Moreover, repayments required in the first and in the second period (R(Π) and R(Π)) arenot affected by renegotiation because the sum of the two is such that the lender breaks even in expectation.

19

Then, the entrepreneur incentive constraints related to effort provision in the first and in the secondperiod are:

Π−R(Π) + ΠH − R(Π)− I ≥ B/σ + ζ0(ΠL − R(0)− I) + (1− ζ0)B, (IC1)

ΠH − R(Π)− I ≥ B, (IC2,Π)

ΠL − R(0)− I ≥ B, (IC2,0)

and the lender’s participation constraint is given by:

P ≥ 0. (PC)

Finally, the limited liability constraints that must be satisfied in the first period are in the following:

R(π) ≤ L− I + π − ζπ I. (LL1,π)

Instead, in the second period, limited liability is fulfilled if the constraints below hold true:

R(Π) ≤ L− I +Π−R(Π) + ΠH − I, (LL2,Π) (15)

R(0) ≤ L− I −R(0) + ΠL − I. (LL2,0) (16)

The problem above incorporates the implications of setting ζ0 = 0 in a framework with the soft codein Section 2.1, so it can be concluded that the short-term contingent renegotiation proof contracts that theentrepreneur offers to the lender have the following features:

• ζΠ = 1, ζ0 = 0, L = I, R(Π) = [I − (ΠL − I −B)(1− σ)]/σ, R(Π) = 0.

The lender’s participation constraint holds with equality and the relevant conditions are satisfied underAssumption 1.ii, and if the entrepreneur first period incentive constraint holds true (see Table 2):

Π + ΠH − I/σ −B/σ ≥ I + [B − (1− σ)(ΠL − I)]/σ. (17)

Finally, E is as in the first best (4).�

[TABLE 2 ABOUT HERE]

Table 2: Renegotiation-proof Short-term Contingent Contracts Constraints

Constraints

ΠH − I −B ≥ 0 (IC2,Π)

σΠ ≥ I + σI − (1− σ)(ΠH − I −B) (LL1,Π)

0 ≥ 0 (LL1,0)

Π + ΠH − I/σ −B/σ ≥ I −B − (ΠL − I)(1− σ)/σ (LL2,Π)

20

References

[1] Acharya, Viral V., and Krishnamurthy Subramanian, 2009, Bankruptcy Codes and Innovation,Review of Financial Studies, 22(12), 4949-4988 .

[2] Ayotte, Kenneth M., and Hayong Yun, 2009, Matching Bankruptcy Laws to Legal Environ-ments, Journal of Law, Economics, and Organization, 25, 2-30.

[3] Baird, Douglas G., and Robert K. Rasmussen, 2002, The End of Bankruptcy, Stanford LawReview, Vol. 55.

[4] Baliga, Sandeep, and Ben Polak, 2004, The Emergence and Persistence of the Anglo-Saxonand German Financial Systems, Review of Financial Studies, 17(1), 129-163.

[5] Bebchuk, Lucian A., 2002, Ex-ante Costs of Violating Absolute Priority in Bankruptcy, Journalof Finance, 57(1), 445-460.

[6] Berger, Allen N., Marco A. Espinosa-Vega, W. Scott Frame, and Nathan H. Miller, 2011,Why Do Borrowers Pledge Collateral? New Empirical Evidence on the Role of AsymmetricInformation, Journal of Financial Intermediation, 20(1), 55-70.

[7] Bharath, Sreedhar T., Venky Panchapegesan, and Ingrid Werner, 2007, The Changing Natureof Chapter 11, Fisher College Business Working Paper, No. 2008-03-003.

[8] Bianco, Magda, and Guido Romano, 2009, I Fallimenti in Italia e in Europa, I Rapporti Cervedsulle Imprese, 5/2009.

[9] Blume, Marshall E., Irwin Friend, and Randolph Westerfield, 1980, Impediments to CapitalFormation, Rodney L. White Center for Financial Research Working Paper, University ofPennsylvania.

[10] Bolton, Patrick, and David S. Scharfstein, 1996, Optimal Debt Structure and the Number ofCreditors, Journal of Political Economy, 104(1), 1-25.

[11] Brouwer, Maria, 2006, Reorganization in US and European Bankruptcy Law, European Journalof Law and Economics, 22, 5-20.

[12] Costantini, James A., 2009, Effects of Bankruptcy Procedures on Firm Restructuring: Evi-dence from Italy, unpublished manuscript.

[13] Daihya, Sandeep, Kose John, Manju Puri, and Gabriel G. Ramirez, 2003, Debtor-in-possessionFinancing and Bankruptcy Resolution: Empirical Evidence, Journal of Financial Economics,69(1), 259-280.

[14] Dewatripont, Mathias, and Eric Maskin, 1995, Credit and Efficiency in Centralized andDecentralized Economies, Review of Economic Studies, 62(4), 541-555.

[15] Diamond, Douglas W., 2004, Committing to Commit: Short-term Debt when Enforcement isCostly, Journal of Finance, 59(4), 1447-1480.

[16] Franks, Julian R., and Oren Sussman, 2005, Financial Distress and Bank Restructuring ofSmall to Medium Size UK Companies, Review of Finance, 9, 65-96.

21

[17] Fudenberg, Drew, and Jean Tirole, 1990, Moral Hazard and Renegotiation in Agency Con-tracts, Econometrica, 58, 1279-1320.

[18] Gennaioli, Nicola, and Stefano Rossi, 2010, Judicial discretion in corporate bankruptcy, Reviewof Financial Studies, 23(1), 4078-4114.

[19] Gertner, Robert, and David S. Scharfstein, 1991, A Theory of Workouts and the Effects ofReorganizational Law, Journal of Finance, 46(4), 1189-1222.

[20] Hart, Oliver, 1995, Firms, Contracts, and Financial Structure (Oxford University Press, Ox-ford, UK).

[21] Holmstrom, Bengt, and Jean Tirole, 1997, Financial Intermediation, Loanable Funds, and theReal Sector, Quarterly Journal of Economics, 112(3), 663-691.

[22] John, Kose, Lubomir Litov, and Bernard Yeung, 2008, Corporate Governance and Risk-Taking, Journal of Finance, 63(4), 1679-1728.

[23] Kornai, Janos, Eric Maskin, and Gerard Roland, 2003, Understanding the Soft Budget Con-straint, Journal of Economic Literature, 41(4), 1095-1136.

[24] Landier, Augustin, 2006, Entrepreneurship and the Stigma of Failure, Stern School of BusinessWorking Paper, New York University.

[25] Mooradian, Robert M., 1994, The Effect of Bankruptcy Protection on Investment: Chapter11 as a Screening Device, Journal of Finance, 49(4), 1403-1430.

[26] Poterba, James M., and Lawrence H. Summers, 1995, A CEO Survey of U.S. Companies, TimeHorizons, and Hurdle Rates, Sloan Management Review, 37, 43-53.

[27] Povel, Paul, 1999, Optimal “Soft” or “Tough” Bankruptcy Procedures, Journal of Law, Eco-nomics and Organization, 15(3), 659-684.

[28] Qian, Jun, and Philip E. Strahan, 2007, How Law and Institutions Shape Financial Contracts:The Case of Bank Loans, Journal of Finance, 62(6), 2803-2834.

[29] Rodano, Giacomo, Nicolas Serrano-Velarde, and Emanuele Tarantino, 2012, Bankruptcy Lawand the Cost of Banking Finance, unpublished manuscript.

[30] Scott, Jonathan A., and Terence C. Smith, 1986, The Effect of the Bankruptcy Reform Act of1978 on Small Business Loan Pricing, Journal of Financial Economics, 16(1), 119-140.

[31] von Thadden, Ernst Ludwig, 1995, Long-term Contracts, Short-term Investment and Moni-toring, Review of Economic Studies, 62(4), 557-575.

[32] Tirole, Jean, 2006, The Theory of Corporate Finance (Princeton University Press, Princetonand Oxford).

[33] White, Michelle J., 1994, Corporate Bankruptcy as a Filtering Device: Chapter 11 Reorgani-zations and Out-of-Court Debt Restructuring, Journal of Law, Economics, and Organization,10(2), 268-295.

22

Highlights

• Analysis of bankruptcy law impact on firms’ investment choice

• A game-theory principal-agent model with moral hazard and project choice is proposed

• Soft bankruptcy law might trigger the choice of inefficient short-term projects

• Help assess consequences of new bankruptcy codes designed as US Chapter 11 in the EU

1