Embed Size (px)

Citation preview

Social

Social Science Research 36 (2007) 808–833

www.elsevier.com/locate/ssresearch

ScienceRESEARCH

Assets, earnings mobility and the black/white gap q

Juan Rafael Morillas

European University Institute, Italy

Available online 5 February 2007

Abstract

This paper derives two testable propositions from the theoretical literature on the relationbetween wealth ownership and stratification processes with the aim of explaining the inequality ofopportunities for earnings acquisition. The first proposition establishes a relation between wealthand earnings mobility. The second one provides an explanation of the black/white earnings mobilitygap in terms of the wealth inequality among blacks and whites. The analyses in the paper providesupport for both propositions. Assets are shown to be associated with the opportunities for earningsacquisition. Furthermore, on the basis of the estimated models, it can be concluded that the black/white earnings progression gap arises partly from the wealth inequality in assets ownership of blacksand whites.� 2006 Elsevier Inc. All rights reserved.

Keywords: Assets; Black–white earnings gap; Inequality; Opportunity; Stratification process; Wage mobility;Wealth

1. Introduction

In the recent decades, numerous contributions have established a new framework forthe analysis of stratification processes, living-standards and economic well-being

0049-089X/$ - see front matter � 2006 Elsevier Inc. All rights reserved.

doi:10.1016/j.ssresearch.2006.04.007

q This paper has benefited from comments by Pablo Beramendi, Richard Breen, Gosta Esping-Andersen, JohnGoldthorpe, Anthony Heath, Mike Hout, Uli Mayer, Javier G. Polavieja, Seymour Spilerman, and twoanonymous referees. I also thank participants in seminars at the Max Planck Institute for Human Development(Berlin) and the Center for Policy Research (Maxwell School of Citizenship, Syracuse University) as well asparticipants at several meetings of the Research Committee on Social Stratification and Mobility (ISA) and at theFirst Conference of the Harvard Inequality Program.

E-mail addresses: [email protected], [email protected]

J.R. Morillas / Social Science Research 36 (2007) 808–833 809

(Spilerman, 2000; Sorensen, 2000). The common theme of these contributions is the role ofassets or wealth, as a distinct variable from income, as a determinant of economic oppor-tunities or life-chances. This perspective has provided the rationale for a new way of look-ing both at stratification processes and public policy issues—especially those related topoverty persistence (e.g. Sherraden, 1991; Conley, 1999).

In addition to its contribution to the theory of social stratification, this literature hastriggered theoretical scholarship on the unequal patterns of wealth accumulation acrossdifferent segments of the population (Beverly and Sherraden, 1999; Edin, 2001; Carneyand Gale, 2001).1 Furthermore, an literature has followed those theoretical contribu-tions. Several investigations on the causes of wealth inequality have been produced(vid. Blau and Graham, 1990; Oliver and Shapiro, 1995; Conley, 1999, chapter 2; Keis-ter, 2000, chapter 7; Carney and Gale, 2001; Wilhelm, 2001). Those contributions haveshown that individuals’ social background is strongly associated with their capacity toaccumulate assets over their life-courses and, therefore, have shed light on the sociolog-ical determinants or causes of the inequality of assets accumulation. However importantthis contribution has been, the empirical literature is still unbalanced in the sense thatmost of the empirical investigations have been concerned with the causes of wealthinequality and accumulation, leaving the analysis of its consequences relativelyunattended.

As a result of the lack of empirical investigations on the consequences of wealth inequal-ity, the literature still retains a heavy programmatic spirit (Shapiro and Wolff, 2001). Partof the reason for that arises from the difficulties entailed in establishing a link betweenwealth and labor market processes (Shapiro and Wolff, 2001, chapter 2; Conley, 2001),namely plausible mechanisms connecting wealth ownership with the opportunities toobtain labor market rewards (e.g. earnings).

The most notable exception is Conley (1999), in which he investigates the implica-tions of parental wealth for a number of socioeconomic outcomes: educational attain-ment, welfare participation, wealth attainment, and wage attainment. This paper aimsat showing that there are empirical grounds, not only theoretical, for expecting the ‘‘as-sets matter’’ framework to be taken as sound. In this vein, this paper’s goal is to pro-vide evidence on the role of wealth in enhancing individuals’ economic life-chances. Themain difference between the contribution in this paper and Conley (1999, chapter 4) istwo-fold. Conley (1999, chapter 4) follows a static approach in his analysis of the pro-cess of wage attainment. He studies the wage attained at one particular point in timeand not across individuals’ life-courses. Furthermore, the process of wage attainment isexplained as a result of the effect of parental wealth. This paper differs from Conley(1999, chapter 4) in (i) providing a dynamic analysis of the wage attainment processby studying the opportunities for earnings acquisition across individuals’ life-course,and (ii) explaining it in terms of individuals’ past or accumulated wealth by testingthe existence of a dynamic relation between individuals’ accumulated wealth and theiropportunities for earnings acquisition.

The body of the paper is as follows. In Section 1, the literature that has established the‘‘assets matter’’ framework is reviewed and a theory of wealth as an opportunity-enhanc-

1 These investigations have been applied to the design of institutional mechanisms aiming at encouraging theaccumulation of assets by the poor, e.g. the Individual Development Accounts (IDAs) (vid. Seidman, 2001;Sherraden, 2001; Stern, 2001).

810 J.R. Morillas / Social Science Research 36 (2007) 808–833

ing device is sketched. From this literature and theory, two testable propositions on therole of wealth ownership as an opportunity-enhancing device are formulated. In Section2, I test the first of the empirical propositions formulated in Section 1, i.e. the one estab-lishing a relation between wealth and earnings mobility. I estimate panel data models ofearnings mobility. The estimated models show that individuals’ wealth is indeed an impor-tant determinant of their (future) opportunities. Net of the effect of a measure of cognitiveability, wealth is associated in the expected direction with the mobility of earnings. In Sec-tion 2.1, I test the second empirical proposition of the argument. From the analyses in thissection, it can be concluded that the unequal opportunities for earnings progression ofblacks and whites arise partly from the wealth inequality among them. In the last section,I summarize the findings of the paper and highlight the implications of the argument forthe explanation of the persistence of inequality, making special reference to the inequalitybetween blacks and whites in the US.

2. Wealth and opportunity: The argument and two testable propositions

The rationale for casting the analysis of economic opportunities on an assets-frame-work arises mainly from the conceptual distinction between wealth and income (e.g.Sherraden, 1991, chapter 8; Keister, 2000, 6–9; Wolff, 2002, chapter 2). Although relat-ed, they are not synonymous. The difference between wealth and income is that thefirst one is a stock variable, while the second is a flow variable. Wealth is the total val-ue of the economic resources that an individual or household has accumulated up tothe time at which it is measured. Income, on the other hand, is a flow of economicresources over time. It is the total amount of resources that an individual has obtainedduring a period of time. As a consequence of its stock nature, wealth provides a poolof resources that can be used in periods of hardship. It can be employed as a consump-tion-smoothing device to cope with events such as the loss of a job or the occurrenceof illness.

This distinction has important implications for a key sociological problem: theexplanation of the process of social stratification, i.e. why individuals’ opportunitiesbecome stratified in market economies. Indeed, as emphasized in a growing body ofsociological literature (vid. Oliver and Shapiro, 1995; Keister, 2000. 2002; Spilerman,2000; Shapiro, 2001; Edin, 2001), wealth is particularly relevant for understandingthe stratification processes and the origin of the heterogeneity in people’s life-chances.As Spilerman (2000, 518) has put it ‘‘a consideration of wealth becomes relevant oncethe agenda of the field is enlarged, from a focus narrowly on labor market success andits rewards to a concern with living standards and economic security’’. Most of strat-ification research has been concerned with labor market rewards, mainly occupationalattainment and status. As a result, living-standards have been relatively unattended(Spilerman, 2000). A recent example of the crucial role of wealth in stratification the-ory is Sorensen (2000). Sorensen (2000) proposes to base class concepts on personalwealth. His concept of class as life conditions is based on a person’s total wealth.The rationale for such a concept is that ‘‘the total wealth controlled by actors [. . .]by shaping welfare and well-being, as well as economic opportunities and the invest-ments that maximize these opportunities, [. . .] creates the behavioral dispositions thatare accountable for the inoculation and socialization mechanisms associated with classas life-conditions’’ (Sorensen, 2000, 1534).

J.R. Morillas / Social Science Research 36 (2007) 808–833 811

This general insight on the role of wealth has been applied to the explanation of a par-ticular problem in social stratification: the persistence of poverty. Indeed, the role of assetsoccupies a central place in current debates and proposals in public policy in the US as away to improve people’s opportunities to escape poverty. This literature has been devel-oped to a large extent after Sherraden’s (1991) Assets and the Poor. Oliver (2001, xi)has summarized the bottom line of this perspective as follows:

Antipoverty policy [. . .] has tended to emphasize efforts to increase income to somepredetermined minimum level as the ‘‘magic bullet’’ that will solve poverty problems.But that approach builds on the common misconception that poverty is simply amatter of low income or low levels of consumption. Several critiques of thisapproach to poverty alleviation have pointed out that its emphasis on incomeignores key causes of inequity, overlooks the consequences of low asset accumula-tion, and fails to address long-term stability and security.

The conventional wisdom in poverty research and policy is that poverty is a ques-tion of low-income. In Shapiro and Wolff (2001, 2) words ‘‘the traditional assumptionthat governs our thinking [in poverty evaluation] is that income and labor marketsconstitute virtually the entire poverty story.’’ However, assets provide a sounder foun-dation than income for individuals’ living standards. Assets make available a pool ofresources that enhance individuals’ opportunities to protect their living standards,smooth their consumption streams, obtain income security, and invest in their eco-nomic future.

But, what are the more specific reasons why ‘‘wealth matters?’’ What are the mecha-nisms by which wealth ownership gives rise to unequal opportunities? In this section, Ishall make explicit the mechanisms linking wealth and opportunities. To provide a narra-tive of the associations between wealth ownership and opportunities, I shall elaborate themicro-level (Goldthorpe, 2000, chapter 5), i.e. provide an account of how wealth owner-ship is related to the behavioral dispositions for improving economic opportunities. Thisnarrative is based on an analysis of the interplay between the institutional underpinningsof market economies and the role of wealth ownership in imperfect economies. Thereafter,I shall apply such general argument to the explanation of individuals’ opportunities forearnings acquisition. I derive the empirical implications of the general argument for suchparticular case, and make explicit what empirical associations are to be found if the theoryis correct.

2.1. Wealth and life-chances: The argument

The theory linking economic opportunities and assets departs from a very basic andreasonable assumption. To improve their economic opportunities, individuals need tobe equipped with a safety net. Only when their living-standards are guaranteed indepen-dently of the working of market forces, may people start thinking about improving theirprospects. If agents are concerned with their mere day-to-day survival, they cannot under-take investments that will improve their prospects. If earnings are the only source of theirincome, they cannot move beyond the mere satisfaction of their more basic needs. Toachieve a minimum living standard, they need to participate in the labor market. It is inthis sense that their living standards are commodified. And only when a minimum levelof resources is guaranteed such as to provide enough welfare and security, may individuals

812 J.R. Morillas / Social Science Research 36 (2007) 808–833

be expected to undertake investments that will result in an improvement of theiropportunities.

If our economies were perfect, the market mechanism would provide individuals with asafety net. Indeed, the organization, working, and presence and/or absence of some mar-kets may affect mobility opportunities. In particular, the characteristics of credit and insur-ance markets are of enormous relevance in the production of mobility chances. If capitalmarkets were perfect, individuals could borrow the funds needed to invest in their personaldevelopment.

Similarly, if insurance markets provided enough protection against unexpected risks(e.g. income shocks, unemployment, illness) individuals would be encouraged to takeadvantage of mobility investments. We know from the classic work by Domar and Mus-grave (1944) that when insurance is available, risk-taking behavior is promoted. If individ-uals could obtain protection against unexpected contingencies, they would be encouragedto take advantage of mobility opportunities.

However, we know that the working of both capital and insurance markets is far fromperfect. Informational issues give rise to problems of adverse selection and moral hazardbetween borrowers and lenders, between the insured and insurers.2 In turn, the working ofcredit markets is imperfect (vid. Stiglitz and Weiss, 1981) and many insurance markets aremissing. As a consequence, the real world is far from the ideal economy of perfect insur-ance established in Debreu (1959) and Arrow (1964, 1974). And these imperfections incapital and insurance markets may affect mobility opportunities.

The welfare state provides some protection of individuals’ living standards. However, itreplaces individuals’ income at neither at one hundred percent rate nor during an indefiniteperiod of time. In addition, in the US residual welfare state, income replacement is limitedto those incapable of market participation. Therefore, it does not provide individuals witha safety net, which in turn gives them an incentive to undertake risky earning-enhancinginvestments.

This does not mean that individuals’ welfare cannot be made independent from marketforces, even in an ideal-type case of complete absence of state protection. As Esping-An-dersen (1990,; 37) writes ‘‘de-commodification is [. . .] a process with many roots.’’ Thesources of de-commodification may be multiple. However, there is a primary source thatneither Polanyi (1944) nor Esping-Andersen (1990) have considered: the self. Individualscan rely on their wealth to isolate their living standard from market participation. If theyfind neither market-protection nor state-decommodification, they can rely on their ownresources. If this is the case in general, it is even truer in the case of the US. Individuals,in the absence of economic protection through the market mechanism, can find self-decom-

modification by relying on their own wealth. They can use their wealth to undertake invest-ments that will secure them a good life. Certainly, assets enable people to invest in theirfuture. In addition, they provide individuals and families with protection against eventualeconomic contingencies: they can find protection, i.e. insurance, by running down theirassets. All in all, wealth creates a safety net and stimulates risk-taking behavior (vid. Sinn,1995).

In conclusion, given the imperfections of market and insurance markets, wealth owner-ship has two key properties that enhance individuals’ opportunities. First, it provides a

2 Vid. Stiglitz (1994: chapters 3 and 4) for an accessible presentation of these issues.

J.R. Morillas / Social Science Research 36 (2007) 808–833 813

source of funding for investments in personal development and, second, it supplies protec-tion against unexpected risks and contingencies and, as a result, promotes risk-takingbehavior.

Therefore, we should find an empirical association between wealth and life-chances.Those endowed with wealth may develop the behavioral predispositions required toimprove their economic opportunities. Do note that testing this theory with large-scalesurvey requires a considerable previous theoretical effort (Goldthorpe, 2000). Indeed, ina typical survey we cannot find variables measuring risk-taking behavior. Surveysincluding measures of wealth ownership together with other social and economic vari-ables, are infrequent—probably, by far, the most complete one is the National Longi-tudinal Survey of Youth. But there is no survey including psychological variablesmeasuring risk-taking behavior together with wealth variables. However, this doesnot imply that the plausibility of the ‘‘assets matter’’ theoretical framework cannotbe tested. To be sure, what the former comment implies is that the analysis of associ-ations between variables requires an elaboration of the theoretical reasons why wealthmatters. Certainly, as Goldthorpe (2000, 97) points out: ‘‘For [. . .] how far the quan-titative analysis of large scale data sets can serve as an effective means of testing the-ories of macrosocial processes will be heavily dependent of their degree of elaborationat the micro-level.’’ Providing a plausible account of the reasons behind the empiricalassociations to be tested is a necessary precondition for interpreting the associationsfound in statistical models.

This is not a specific difficulty facing this paper, but a more general sociological prob-lem that arises when we try to understand the substantive meaning of the associationsfound in statistical models. Indeed, as Abbott (1992, 57) has put it: ‘‘causality in socialprocesses cannot be established from quantitative analyses in themselves, but is logicallydependent upon action narrative.’’ Goldthorpe (2000, 97) argues along similar lines whenhe writes that ‘‘quantitative analyses of large scale data sets in itself is incomplete and [. . .]its contribution to sociology will be seriously limited unless it is allied in some way oranother to accounts of social action.’’ In such spirit, the theory provided above suppliesa plausible narrative that specifies the underlying mechanisms behind the associationsbetween wealth endowments and economic life-chances. Individuals undertake actionsthat are related to their future opportunities. And those actions are related to the wealththey posses and the institutional underpinnings of market economies.

2.2. Assets and earnings mobility: Two testable propositions

In this paper, the general argument formulated above on the role of wealth in thegeneration of social stratification is applied to a more specific sociological problem:the explanation of individuals’ opportunities for earnings mobility. If the ‘‘assets mat-ter’’ argument is correct in general, i.e. wealth ownership enhances individuals’ oppor-tunities, then it should provide an explanation, even if partial, of the origin of theinequality of opportunities for earnings mobility. Indeed, if wealth enhances opportu-nities in general, then it should improve individuals’ prospects for earningsacquisition.

Building on this general idea, two testable propositions are put forward. The first oneis of a generic nature and establishes a relation between wealth ownership and earningsmobility. The second proposition is a particular case of the former one and has to do

814 J.R. Morillas / Social Science Research 36 (2007) 808–833

with the unequal opportunities for wage mobility of Blacks and Whites. These proposi-tions are:

(1) Wealth ownership is related with individuals’ opportunities for earnings progression.There is a long-term dynamic relation between wealth ownership and earningsmobility. Certainly, if the argument is correct, we should find the existence of a rela-tion between individuals’ initial wealth and earnings mobility. The underlying logic isthat, those who have a right to income outside the market, like the wealthy do, find iteasier to take advantage of mobility opportunities.

(2) A consequence of the first proposition is that, at least partly, the origin of the black/white earnings gap is to be found in the extreme unequal distribution of wealthbetween these two groups. Certainly, if wealth ownership enhances individuals’opportunities, and more particularly, if wealth is a trigger of earnings mobility, thenthe argument put forward in the paper provides the basis for an explanation of theunequal opportunities for earnings acquisition of blacks and whites, i.e. the so-calledblack–white earnings gap. The argument underlying this proposition is developedfully in Section 4.

3. Wealth and earnings mobility

If the argument presented above is correct, we should find an association between indi-viduals’ initial wealth and their earnings mobility. To test the plausibility of this proposi-tion, we have to examine the relation over time between individuals’ accumulated assetsand their earnings mobility. For so doing, I shall rely on the estimation of an Error Cor-rection Model. Such model provides the tool to study the relations over time between thedependent and independent variables of interest. It supplies insights into the co-movementof the variables of interest (vid. Greene, 2000, 733 and ff.). The generic form of an errorcorrection model is the following one3:

Dyi t ¼ aþ dyi t�1 þ Rb1Dxi t þ Rb2xi t�1 þ ui þ ei t: ð1Þwhere D is the first difference operator: Dyt = yt � yt�1, yt is the dependent variable, yt�1 isthe first lag of the dependent variable. Dxt = xt � xt�1 is a vector that includes the first dif-ference of the independent variables, xt�1 is a vector that includes the first lag of the inde-pendent variables.

The model states that the difference in the dependent variable between two periods oftime is the result of both the lagged covariates as well as of the difference between two peri-ods of the covariates. It states that the there is both a long- and a short-term relationbetween the dependent and independent variables. The parameter of the lagged indepen-dent variables (b2) measures the long-term effect of those variables on the equilibrium pathof the dependent variable. The parameter of the first-difference (b1) measures the short-term effects of the independent variables on the long-run equilibrium (vid. Beck and Katz,1996; Greene, 2000, chapter 17).

3 Vid. Beck and Katz (1996) and Greene (2000, 733 and ff.) for the properties of the Error Correction Model.

J.R. Morillas / Social Science Research 36 (2007) 808–833 815

3.1. Data

The data set used in the statistical analyses in this paper is the National Longitudinal Sur-

vey of Youth. This data set is conducted at Ohio State University under the sponsorship ofthe US Department of Labor. It collects information regarding labor market experiences,investments in education and other variables for individuals aged 14–21 in 1979. This is anongoing panel that collects information for a sample of young men and women from Jan-uary 1978 on a yearly basis. The interviews have taken place yearly from 1979 until 1994,and every two years from then on (1996 and 1998), collecting information retrospectively.

The original data set includes three sub-samples: (i) a random sample of young people,(ii) a set of supplemental samples designed to over-sample civilian Hispanic, Black, andnon-Hispanic non-Black population, and (iii) a military sample of individuals designedto represent the population serving in the military. I have included in the analyses neitherthe military sample nor the over-sample of disadvantaged whites due to some drawbacksand statistical problems in those samples. To avoid the interaction between mobility andfertility choices, I have restricted the analyses to the labor market experiences of males. Asin any longitudinal survey, individuals do not respond to all interviews. I have included inthe analyses those individuals who have missed only three or fewer of the interviews in theperiod 1978–1997.4

It is possible to reorganize the original data in a form that is conductive to statisticalanalyses. Using the summary yearly information produced by the staff of the Center forHuman Resources of Ohio State University, I have generated a panel database in whichthe time unit is the year generating, therefore, a yearly time-series cross-sectional dataset.

3.2. Variables

The variables included in the analyses are described below:

Earnings rate. This variable is the result of dividing the total earnings obtained by theindividual in the year at which it is measured into the total number of hours worked inthat year.Age. It is a time-varying variable that measures the age in months since birth.Race. Time-invariant variable. The categories are: Hispanic, Black, non-Hispanic andnon-Black (I refer to this last category as White).Number of years of completed education. It is a continuous variable whose name is fullyself-explanatory.Armed Forces Qualifying Test (AFQT)5. Measured at one interview (1980). This is avariable created from the raw scores of a battery of questions included in a more gen-

4 As in any longitudinal survey, individuals do not respond to all interviews. I have included in the analysesthose individuals who have missed only three or fewer of the interviews in the period 1978 to 1997. This entails a15% reduction of the sample.

5 This is the proxy for intelligence used in Herrnstein and Murray (1994). I will be using the same variable inthis investigation, taken from the same survey (the NLSY). Even assuming that such a variable is actuallymeasuring intelligence, I show that it does not rule the effect of asset ownership out in explaining individuals’economic opportunities. However, it is worth noting that the very same use of this variable as a measure ofintelligence is problematic (Fisher et al., 1996, chapter 2).

6

varnumvar

816 J.R. Morillas / Social Science Research 36 (2007) 808–833

eral test, the Armed Services Vocational Aptitude Battery (ASVAB). More particularly,this is the AFQT80 generated by the staff of the Center for Human Resources at OhioState University. It consists of percentile scores obtained from the combination of thefollowing sections of the ASVAB: Section 2 (arithmetic reasoning), Section 2.1 (wordknowledge), Section 2.2 (paragraph comprehension), and one half of the score fromSection 3 (numerical operations).Assets. The variables measuring assets ownership have not been asked in every inter-view. By far, the two most complete series are the ones for the variables (i) ‘‘Amountof Money Assets’’ and (ii) home ownership. The first variable is a measure of the totalvalue of money assets owned by the household. Such variable has been measured fromthe 1985 interview onwards, with the exception of the year 1991. The second variable isa dummy variable measuring every year whether the individual owns a home or not.These are the only two wealth variables used in the analyses in the paper. Two arethe reasons for doing so. The first one has to do with data availability. The series arefar more complete for these two variables than for the rest of variables on assets hold-ing. The second reason is referred to the variable liquid assets. Since the argument ofthis paper is concerned with the protection that assets may provide against unexpectedrisks, liquid assets seem to be better at providing consumption smoothing than non-liquid assets because they can be immediately used and need not to be cashed out beforebeing used.Gini coefficient. This variable is not an individual- but an aggregate-level variable. It isthe Gini coefficient of the distribution of household income in the US. I use this variableto include a control for the effect of aggregate macroeconomic factors in inequality thatin turn may affect mobility opportunities. By so doing, I confront rival explanationsstressing the role of the labor market turbulences of the 1980s and 1990s as an imped-iment for earnings mobility.Experience. It is the cumulative number of weeks that the individual has spent in thelabor force and employed until the date of the interview at which this variable ismeasured.6

Type of industry. It is the type of industry in which the respondent worked. Theoriginal variable is coded according to the 3-digit classification of industries. Fol-lowing the 1970 Census of Population, the industries have been grouped into thefollowing categories:

- Agriculture, Forestry and Fisheries.- Mining.- Construction.- Manufacturing.- Transportation, Communication and Other Public Utilities.- Wholesale and Retail Trade.

In addition to this variable, in the models in Table 6, I have measured experience with two additionaliables: the cumulative number of weeks that the individual has spent in the unemployed and the cumulative

ber of weeks that the individual has spent out of the labor force up to the date of the interview at which theiables are measured.

J.R. Morillas / Social Science Research 36 (2007) 808–833 817

- Finance, Insurance and Real State.- Business and Repair Services.- Personal Services.- Entertainment and Recreation Services.- Professional and Related Services.- Public Administration.

3.3. Estimated models

If the argument is correct, we should find a long-term relation between assets and earn-ings mobility. To find out whether that is the case, I have estimated the parameters of thefollowing equation:

D logðearningsÞi t ¼ aþ d logðearningsÞi t�1 þ b1D logðassetsÞi t

þ b2 logðassetsÞi t�1 þ Rb3ci t þ ui þ ei t; ð2Þ

where c is a vector of control variables: age, age squared, and race.Do note that, by definition, the relation between earnings and wealth is not simulta-

neous, but one that takes place within a lag. Wealth is a stock variable—the value of whatthe individual owns up to the period at which it is measured, while earnings is a flow var-iable. A proportion of one’s earnings, if not consumed, will become part of wealth in thenext period. To put differently, if one does not consume her earnings today, she willbecome richer tomorrow, but not today. One’s wealth today depends on what onesaved—or did not consumed the day before. Equivalently, wealth at time (t) is related withearnings at time (t � 1). Therefore, there is no circularity in the previous equation in whichD log(earnings)i t is regressed on D log(assets)i t.

From the estimated parameters of Eq. (2), we can see that the (accumulated) assets areassociated with the mobility of earnings. There is a relation between individuals’ (accumu-lated) assets and their (future) earnings. This result provides support for the argument inthe paper. There is a long-term dynamic relation between asset ownership and the mobilityof earnings.

The estimated parameters of Model 1 (Table 1) supply evidence in favor of a credit-con-straints interpretation of labor market careers. Nevertheless, it could be that such an asso-ciation between assets and earnings mobility is spurious. Certainly, Herrnstein andMurray (1994) would argue that wealth is significantly associated with earnings, but justbecause more intelligent individuals have better prospects to acquire earnings and at thesame time are better prepared to build up wealth. An account of life-chances in termsof intelligence would interpret the association found in Model 1 in this way: Wealth isimportant only because it is correlated with intelligence.

If the explanation of earnings mobility a la Herrnstein and Murray (1994) were correct,we should find that wealth is not associated with the increase of earnings after controllingfor intelligence. Holding intelligence constant, individuals’ assets should not be significant-ly associated with their earnings opportunities. Both the long- and the short-term relationshould become statistically non-significant. In Model 2 (Table 1), I have estimated a modelin which a new variable is added to the vector of independent variables: the AFQT-score.This variable is the measure of intelligence that Herrnstein and Murray (1994) used in The

Bell Curve.

Table 1Wealth and earnings mobility: random-effects estimatesa

Variables Model 1 Model 2 Model 3Coefficient(standard error)

Coefficient(standard error)

Coefficient(standard error)

Lagged dependent variable �0.592*** (0.006) �0.590*** (0.006) �0.584*** (0.006)First difference assets (log) 0.050*** (0.003) 0.047*** (0.003) 0.045*** (0.003)Lagged assets (log) 0.069*** (0.003) 0.063*** (0.003) 0.058*** (0.003)Home ownership 0.075*** (0.009) 0.074*** (0.009) 0.061*** (0.009)Age 0.009*** (0.0001) 0.009*** (0.001) 0.006*** (0.001)Age square �0.0000115*** (1.30e�06) �0.00001*** (1.32e�06) �8.19e�06*** (1.50e�06)Gini coefficient �52.429�� (31.056) �23.512 (31.719) �67.763� (32.702)Gini square 59.473�� (35.082) 27.882 (35.835) 76.571� (36.970)Cognitive ability — 0.002*** (0.0002) 0.001*** (0.0002)Number of years of

completededucation

— — 0.017*** (0.003)

Experience — — 0.0005009*** (0.000088)Experience—square — — �1.96e�07*** (6.07e�08)Industry (Reference:Manufacturing)Agriculture, Forestry

and Fisheries— — �0.289*** (0.028)

Mining — — �0.015 (0.043)Construction — — �0.027�� (0.016)Transportation,Communication andOther Public Utilities

— — �0.008 (0.016)

Wholesale and Retail Trade — — �0.119*** (0.013)Finance, Insurance andReal State

— — 0.030 (0.020)

Business and Repair Services — — �0.046** (0.016)Personal Services — — �0.142*** (0.031)Entertainment andRecreation Services

— — �0.186*** (0.034)

Professional andRelated Services

— — �0.061*** (0.015)

Public Administration — — �0.011 (0.018)Race (Reference: white)- Hispanic �0.015 (0.014) 0.031� (0.014) 0.034� (0.014)- Black �0.030� (0.013) 0.030� (0.014) 0.012 (0.014)Constant 10.070 (6.770) 3.601 (6.916) 13.867� (7.151)R2 27.1% 27.5% 28.1%N 3516 3352 3304

a The sample size in the models presented in this paper does not stay constant across different specifications. I havefollowed three different approaches to check the extent to which the results are sensitive to the missingness on thewealth variable: (1) an analysis of the pattern of missingness, (2) a regression-based imputation, and (3) a regressionbased-imputation plus a dummy variable adjustment. The first approach consists of a dynamic logit modelpredicting whether the covariates in the model predict if an observation of wealth is missing or not. The result revealsthat there is no systematic pattern of missingness: the covariates are not significantly associated with the observationof wealth. The other two approaches reveal that the results do not differ from those obtained in the analyses reportedin the paper. Therefore, the findings are robust and are not affected by the missingness in the wealth variable.

* Significant at p < 0.01.** Significant at p < 0.005.

*** Significant at p < 0.001.� Significant at p < 0.05.

�� Significant at p < 0.10 (two-tailed test).

818 J.R. Morillas / Social Science Research 36 (2007) 808–833

J.R. Morillas / Social Science Research 36 (2007) 808–833 819

D logðearningsÞi t ¼ aþ d logðearningsÞi t�1 þ b1D logðassetsÞi t

þ b2 logðassetsÞi t�1 þ b3ci t þ b4AFQT i þ ui þ ei t: ð3Þ

The estimation of the parameters of the equation in Model 2 reveals that wealthremains an important determinant of the mobility of earnings. Its effect is still significantand becomes only modestly weakened after controlling for the AFQT score. Therefore, itseems that there is a robust relation between assets and earnings mobility. Holding con-stant intelligence/cognitive ability, both a short- and a long-term relation between assetsand the increase of earnings remains. This result supports the argument. Intelligence orcognitive ability may help to improve one’s prospects. Indeed, more intelligent individualsmay have a higher probability of obtaining a ‘‘good position.’’ However, this does notimply that intelligence alone can let individuals to have access to opportunities. It is butone factor among others.

Therefore, the relation between assets and earnings mobility holds even after control-ling for the AFQT score. Nevertheless, a question could be raised as to whether theseresults confirm the link established between assets and opportunities for earnings mobil-ity. It could be that these results are the realization of a different causal process. Forinstance, they could be the result of the following process: more educated individualsget higher paying jobs; thus, over time, more educated individuals have higher earnings,save more, and as a result accumulate more assets. But there is no causal link fromassets to earnings.

To find out whether that is the case, I have estimated a new model (Model 3, inTable 1) in which the vector of independent variables includes some more variables:education (measured as number of years of completed education), type of industry(dummy variable with 12 categories constructed from the 3-digit standard classificationof industries), and experience. We know that education (vid. Card, 1999 for a review),the type of industry (Kalleberg et al., 1981; Baron, 1984; Smith, 1990), and the accu-mulation of experience (e.g. Spilerman, 1977; Rosenfeld, 1992, 45–50; Tienda and Stier,1996; Wilson et al., 1995; Hsueh and Tienda, 1995) have effects on wages. In Model 3 Icontrol for all those variables.

D logðearningsÞi t ¼ aþ d logðearningsÞi t�1 þ b1D logðassetsÞi t

þ b2 logðassetsÞi t�1 þ b3ci t þ b4AFQT i þ b5experiencei

þ b6industryi þ b7educationi þ ui þ ei t: ð4Þ

We can see from the estimated parameters that the coefficient of assets is still significant,and that the size of the coefficient has decreased slightly (Model 3 in Table 1). This is con-sistent with the argument put forward in the first section of the paper. Indeed, as explainedabove, wealth has two properties. It is a pool of resources that provides both as a source offunding for investing in one’s future prospects and for obtaining protection against unex-pected risks. People with assets can more readily invest in education. Consequently, afterwe control for education, as in Eq. (4), the size of the coefficient of assets becomesreduced.7

Therefore, it seems that the relation between assets and earnings mobility is robust.Nevertheless, it could be that there are some sources of heterogeneity, e.g. (unmeasured)

7 I thank an anonymous referee for having drawn my attention to this issue.

820 J.R. Morillas / Social Science Research 36 (2007) 808–833

intelligence, which are not controlled and are correlated with wealth. If such were thecase, wealth, if such an unmeasured heterogeneity could be controlled, would turn outnot being significantly associated with the opportunities for earnings acquisition. Tofind out whether that is the case, I shall estimate the former Eq. (4) using a differentestimation method: fixed-effects. This estimation method allows at capturing the influ-ence of unmeasured respondent’s (fixed) characteristics. The logic behind this methodconsists of decomposing the error-term into two terms: a random error plus an errorthat captures the impact of stable respondent’s characteristics.

By so doing, it is possible to give an account of the influence of omitted variablesthat may be correlated with the observed covariates. Therefore, once the effect ofthose variables is being controlled for, it is possible to know the effect of wealth.Do note that, since the fixed effects absorb respondents’ fixed characteristics, it isnot possible to statistically identify neither the effect of race nor that of AFQT (cog-nitive ability).

The estimated parameters of Eq. (4) estimated by fixed-effects can be found in Table 2.We can see that wealth remains significantly associated with the mobility of earnings.There are both a short- and a long-term dynamic relationship between the (accumulated)wealth and the (future) mobility of earnings. This obviously reinforces the empirical sup-port of the argument put forward in the first part of the paper.

As a result of the statistical significance of the estimated parameters reported in Tables1 and 2, it seems that the relation between assets and earnings mobility is robust. Yet,however the robustness of such a relationship between assets and earnings mobility, theestimated coefficient may not be very precise. There are strong statistical, economic andsocial grounds from which to expect assets not being randomly assigned to individuals.And because of its endogeneity, the estimates of the coefficients of the asset variablesmay not be very accurate. There are three main factors that bring about such an endoge-neity of wealth.

First, there is a bi-directional relation between assets and earnings. If the theory inthis paper is correct, assets ownership may enhance the opportunities to acquire earn-ings. But, on the other hand, earnings are partly saved contributing to the accumula-tion of wealth. Second, the right-hand side variables of the earnings equation may becorrelated. The asset variables are definitely related with some of the other independentvariables. Third, it is obvious that assets or wealth are not randomly assigned to indi-viduals and families. Both the family of origin and individuals’ current family are inti-mately related with their capacity to build up wealth. Indeed, assets are notexogenously assigned to individuals and families. Both the family background andthe social context of the individual affect her ability to build up wealth. Intergenera-tional transfers are an important factor behind the process of wealth accumulation.Parents make transfers to their offspring, which constitute the basis from which theymay initiate their own accumulation of wealth (vid. Altonji, Hayashi and Kotlikoff,1997). Certainly, wealth is an excellent summary measure of how (dis-)advantagesbecome cumulated over time (vid. Oliver and Shapiro, 1995). In addition, individualsand families are heterogeneous on their earnings and income, as well as on their con-sumption profiles. The accumulation of assets depends on what people earn and onwhat they spend on consumption.

To give an account of the endogeneity of wealth, I shall estimate the model by relyingon an instrumental variables approach. I will instrument the variable measuring the

Table 2Wealth and earnings mobility: fixed-effects estimates

Variables Coefficieacnt (standard error)

Lagged dependent variable �0.768*** (0.007)First difference assets (log) 0.036*** (0.004)Lagged assets (log) 0.043*** (0.004)Home ownership 0.071*** (0.011)Age 0.007*** (0.001)Age square �9.86e�06*** (1.64e�06)Gini coefficient �83.252� (39.310)Gini square 91.870� (44.040)Cognitive Ability —Number of years of completed education 0.033*** (0.009)Experience 0.001*** (0.0001)Experience Square �4.89e�07*** (7.27e�08)Industry (Reference: Manufacturing)Agriculture, Forestry and Fisheries �0.107* (0.040)Mining 0.050 (0.057)Construction �0.041�� (0.024)Transportation, Communication and Other Public Utilities �0.026 (0.023)Wholesale and Retail Trade �0.071*** (0.018)Finance, Insurance and Real State �0.003 (0.030)Business and Repair Services �0.030 (0.020)Personal Services �0.090� (0.041)Entertainment and Recreation Services �0.171*** (0.043)Professional and Related Services �0.015 (0.022)Public Administration 0.012 (0.028)Race (Reference: white)- Hispanic —- Black —Constant 17.579� (8.619)R2 26.2%N 3304

*Significant at p < 0.01.**Significant at p < 0.005.

*** Significant at p < 0.001.� Significant at p < 0.05.

�� Significant at p < 0.10 (two-tailed test).

J.R. Morillas / Social Science Research 36 (2007) 808–833 821

long-term relation between wealth and earnings mobility (the lag of assets). I shall use asinstruments two sets of variables. First, variables that measure individuals’ propensity toattain economic resources and, second, variables that capture their capacity to save a frac-tion of those resources and build up wealth.

In the first group of instruments, I include the following variables:

(1) Intergenerational transfers, i.e. parents’ capacity to make intergenerational transfersto their offspring: father’s education8 and the number of siblings.

(2) Education

8 The best measure of parents’ capacity to transfer resources to their offspring is the family wealth. However,that information is not available in the NLSY.

822 J.R. Morillas / Social Science Research 36 (2007) 808–833

The second group of instruments includes the size of the current family. This is a goodmeasure of the propensity to save out of the family income. It is interrelated with thecapacity to save part of the income and, therefore, with the capacity to accumulate wealth.The bigger the size of the family, the higher its consumption requirements and thereforethe lower its saving potential. Other things being equal, bigger families need to spend ahigher share of the family income on consumption, and for that reason they are less pre-pared to accumulate wealth.

To sum up, I instrument the lag of assets using as instruments the following variables:father’s education, number of siblings, individual’s own education, and second lag of fam-ily size (individual’s own family).9

Those variables include at least one variable that seems to be a good instru-ment.10 All the listed variables, as discussed above, are related with the accumula-tion of assets. Intergenerational transfers, education, and the size of the familyare all related with the capacity to build up wealth. In addition, at least one ofthe variables above is not related to the dependent variable—the first difference ofthe earnings rate.

Certainly, the size of the family is related with the capacity to accumulate assets—the variable to be instrumented. However, there are no strong theoretical grounds fromwhich to expect that there is a causal link between the size of the family and the earn-ings potential—the dependent variable. I emphasize that the dependent variable is ameasure of the earnings potential to set aside possible misinterpretations. If the depen-dent variable would be a measure of the total earnings, the family size would not be agood instrument. Certainly, there are strong reasons from which to expect the size ofthe family to be related to the total earnings.11 Although such an argument is convinc-ing enough, it does not apply here. Do note that the dependent variable in the modelsestimated in the paper is not total earnings, but the increase in the earnings rate (totalearnings divided by the total number of hours worked). It is a measure of the earningscapacity, and not of the total earnings.

In Table 3, I report the estimated parameters of a new model in which the variablethat measures the long-term relation12 between wealth and earnings (the lag of assets)

9 I use the second lag of both the family income and of the family size as instruments of the first lag of wealth(or assets) because, by definition, the relation between income and family size and the accumulation of wealth isnot a simultaneous relationship, but one that takes place within a lag. Wealth is a stock variable—the value ofwhat the individual owns up to the period at which it is measured, while income is a flow variable (the sameapplies to the family size). A proportion of one’s income, if not consumed, will become part of wealth in the nextperiod. To put differently, if one does not consume her income today, she will be richer tomorrow, but not today.One’s wealth today depends on what she saved—or did not consumed—the day before. Equivalently, wealth attime (t � 1) is related with the income at time (t � 2).10 In the context of the instrumental variables (IV) estimation, a variable is said to be a good instrument if it is

associated with the variable to be instrumented, but not with the dependent variable. In our case, we need to findvariables that are related with individuals’ capacity to build up wealth, but not with the earnings potential i.e.,mobility of the earnings rate. (vid. Deaton, 1996, 111–116).11 The causal link results from the following underlying process. The bigger the family size, the higher its

consumption requirements. Those needs may be met via an increase in the supply of labor. To satisfy theconsumption needs of his family, an individual may work more hours to raise more income. For that reason, anassociation may be expected between the size of the family and the total earnings.12 Vid. the description of the Error Correction Model above.

Table 3Wealth and earnings mobility: instrumental variables estimation

Variables Coefficient (standard error)

Lagged dependent variable �0.525*** (0.020)First difference assets (log) 0.055*** (0.017)Lagged assets (log) 0.077� (0.033)Home ownership 0.045* (0.017)Age 0.005*** (0.001)Age square �6.96e�06*** (1.58e�06)Gini coefficient �70.046� (35.191)Gini square 80.077� (39.994)Cognitive ability 0.001*** (0.0002)Number of years of completed education 0.011� (0.005)Experience 0.0003*** (0.00009)Experience square �1.46e�07� (6.1e�08)Industry (Reference: Manufacturing)Agriculture, Forestry and Fisheries �0.316*** (0.027)Mining 0.020 (0.039)Construction �0.027�� (0.015)Transportation, Communication and Other Public Utilities �0.008 (0.015)Wholesale and Retail Trade �0.121*** (0.012)Finance, Insurance and Real State 0.026 (0.020)Business and Repair Services �0.045** (0.015)Personal Services �0.136*** (0.030)Entertainment and Recreation Services �0.180*** (0.033)Professional and Related Services �0.062*** (0.015)Public Administration �0.013 (0.016)Race (Reference: white)- Hispanic 0.034** (0.011)- Black 0.018 (0.013)Constant 14.338�� (7.650)R2 27.9%N 3297

* Significant at p < 0.01.** Significant at p < 0.005.

*** Significant at p < 0.001.� Significant at p < 0.05.

�� Significant at p < 0.10 (two-tailed test).

J.R. Morillas / Social Science Research 36 (2007) 808–833 823

is instrumented as explained above. We can see that the relation between wealth andearnings mobility remains significant and its coefficient becomes increased. This resultoffers support for the hypothesis about the role of wealth in the production ofopportunities.

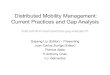

We can see from the estimated parameters that the elasticity of the increase of the wagerate and the lag of assets is 0.077. In other words, a 1% increase in the lag of liquid assets isassociated to an (practically) 8% increase in the first difference of the wage rate. To illus-trate the importance of wealth, I have calculated, at each age, the predicted wage rate ofindividuals endowed with different levels of wealth. More specifically, based on the param-eters of the model estimated by instrumental variables (Table 3), at all ages, and setting allother independent variables at their means, I have calculated the predicted wage rate inthese two cases:

Age and Earnings Potential

0

0,5

1

1,5

2

2,5

3

3,5

4

192

202

212

222

232

242

252

262

272

282

292

302

312

322

332

342

352

Age (in months)

Wag

e ra

te (

in c

on

stan

t 19

78 U

S $

)

Fig. 1. Wealth and earnings potential.

Table 4Wealth and earnings rate at selected ages

Age Wage rate (1) Wage rate (2) Difference

16 1.78 3.19 1.4118 1.86 3.32 1.4620 1.92 3.43 1.5122 1.96 3.51 1.5524 1.99 3.57 1.5826 2.01 3.59 1.58

824 J.R. Morillas / Social Science Research 36 (2007) 808–833

(1) When the individual owns no home and his level of money assets is equal to zero.(2) When the individual owns a home and his money assets are equal to the mean in the

sample.

In Table 4, the predicted values of the wage rate for two individuals characterized asdescribed above are presented at ages 18, 20. 22, 24 and 26 are reported. We can see thatthe hourly wage rate enjoyed by those individuals who have liquid assets equal to the meanvalue and own a house are around 1.5$ higher (in 1978 constant dollars) that the wage rateof those who have neither a home nor liquid assets, but are equal otherwise.

Fig. 1 plots the predicted wage rate at all ages in the range 192–360 months (16–30 yearsall). The inferior curve is the one described by the evolution of the hourly wage rate ofthose who own no assets and the superior curve is the one followed by the wage rate ofthose owing a home and liquid assets equal to the mean value.

4. Wealth inequality and the black/white wage mobility gap

In the previous section, I have showed that assets do indeed matter. Individuals’ accu-mulated wealth is related with their opportunities for earnings acquisition: the mobility ofearnings is related with the initial assets individuals are endowed with. In this section,

J.R. Morillas / Social Science Research 36 (2007) 808–833 825

I formulate and test the second proposition formulated in Section 1, namely the proposi-tion according to which the black/white wage progression gap arises from the initialwealth inequality between these two groups.

The difference between blacks and whites in terms of their opportunities for earningsacquisition has constituted the battleground of different theories. In particular, Herrnsteinand Murray (1994) have argued that the black/white earnings gap is mainly or substantial-ly the result of their heterogeneity with respect to intelligence: blacks are less intelligentthan whites and this is why their earnings are lower. If the explanation of opportunitiesin terms of intelligence would be correct, we should find the gap between these two groupsto become closed when holding intelligence constant. However, I shall show below that isnot the case. After controlling for intelligence, a substantial and significant gap remainsbetween the two groups.

Recently, Oliver and Shapiro (1995) have shown in a very influential book that blacksand whites display an extremely unequal pattern of wealth holding. A considerable part ofthis inequality is the result of what Oliver and Shapiro (1995, chapter 2) call ‘‘the sedimen-tation of racial inequality.’’ The history of blacks’ discrimination, economic segregationand low-wages is the factor underlying such a wealth inequality. Blacks, in the past, facedlegal, social and economic circumstances that worked against their ability to build upwealth. Former generations faced segregation and discrimination that brought aboutreduced opportunities to build up wealth. New generations have not inherited muchwealth and, because of the strong intergenerational component underneath the buildupof wealth, are not able to accumulate much. This is why a focus on wealth provides thebasis from which to ‘‘discover how black’s socioeconomic status results from a sociallylayered accumulation of disadvantages passed on from generation to generation’’ (Oliverand Shapiro, 1995, 6).

Therefore, if the ‘‘assets matter’’ argument is correct, it should provide an explanationof the origin of the black/white earnings gap. If the initial inequality in the possession ofassets gives rise to unequal opportunities for earnings acquisition, and if blacks and whitesdisplay an extremely unequal pattern of wealth holding, the black/white earnings gap is atleast partly the result of the assets inequality between them.

In the parts in this section, I first describe the explanandum, i.e., the black–white earn-ings gap. Thereafter, I formulate in detail the second testable proposition and proceed totest it: I investigate whether the unequal wage progression of blacks and whites is relatedwith their differences in wealth ownership.

4.1. Race and opportunities: The persistent color of life-chances

De jure, blacks and whites are equal. Needless to say, de facto they are unequal.Although it has been a long time since slavery came to an end, even if extreme forms ofsegregation have been put apart, and in spite of the achievements of the Civil Rights move-ment, blacks still have less favorable economic opportunities than whites. More particu-larly, blacks and whites earn unequal wages. The mean hourly wage for white males in1995 was $19. The equivalent figure for black males was $12.13 Although some progresswas made in reducing the black/white earnings gap during the 1960s and early 1970s, such

13 Data from the Current Population Survey, March, 1996 taken from Altonji and Blank (1999, 3147).

826 J.R. Morillas / Social Science Research 36 (2007) 808–833

a gap has stagnated for the last two decades (vid. Altonji and Blank, 1999, 3146–64 for areview).

This regularity has attracted the attention of social scientists and many explana-tions have been put forward to explain it. The explanations can be broadly dividedinto two groups: demand- and supply-side explanations. The explanations in the firstgroup emphasize the role of employers’ decisions and hiring practices as the mainunderlying reason of the lower earnings of blacks. More particularly, the gap emergesfrom the application of discriminatory hiring practices by employers who decide nothiring, or hiring only in bad-jobs, black workers because of the color of their skinand not because of their job-related personal characteristics.14 Such discriminationresults in blacks becoming concentrated in, or being relegated to, economic sectorswhere wages are lower. That is, at least partly, the reason why they have lower wagesthan whites.

The explanations in the second group emphasize the role of the supply-side of the labormarket. They offer an account of the earnings gap based on individual characteristics ofblack workers that operate against their labor market advantage. These personal charac-teristics are of two types: pre-market differences, and market-factors. The bottom line ofthe explanation in terms of pre-market factors is the following one: blacks and whites donot attain the same level of education and acquire different skills before entering the labormarket. As a result, they are less prepared to obtain higher-paying jobs (vid. O’Neill, 1990;Maxwell, 1994; Neal and Johnson, 1996). The market-factors explanations, on the otherhand, emphasize the role of market-related factors as the underlying cause of the racialgap: blacks accumulate less labor market experience and this results in obtaining lowerwages (vid. Rosenfeld, 1992 for a review).15

Needless to say, the many explanations produced in the literature have shed light on thefactors affecting the earnings disparity of blacks and whites. However, a gap still remainsunexplained. In the statistical models estimated and presented below, control variableshave been included that capture the factors behind the emergence of the black–white earn-ings gap highlighted in the specialized literature. We can see that after controlling for bothpre-market and market factors, blacks experience less earnings mobility than whites (Mod-el 1 in Table 5).

In this section, I am going to put forward a new explanation. Building on the argumentin Section 1, and given the empirical findings of Oliver and Shapiro (1995) according towhich Blacks have lower wealth than Whites-I articulate a new explanation, which is madeexplicit below.

14 The literature on discrimination is quite broad. Although the common element is that blacks are relegated tolow-paying jobs, the motivation behind employers has not to respond to a single factor. In this branch of theliterature two types of discrimination are distinguished: prejudice (e.g. Becker, 1971) and statistical discriminationas a device to overcome imperfect information about the job-related personal characteristics of the discriminatedgroup (e.g. Borjas and Bronars, 1989; Black, 1995).15 Two papers worthy of note are Tienda and Stier (1996) and Western (2002). Tienda and Stier (1996) show how

racial disparities in the access to entry-level jobs and longer periods of unemployment give rise to earningsdifferentials for blacks and whites. Western (2002) shows that the impact of incarceration on wage mobility andinequality is channeled through the interruption of careers that imprisonment brings about.

Table 5Race, wealth and earnings mobility: random-effects estimatesa

Variables Model 1 Model 2Coefficient (standard error) Coefficient (standard error)

Lagged dependent variable �0.694*** (0.004) �0.584*** (0.006)First difference assets (log) — 0.045*** (0.003)Lagged assets (log) — 0.058*** (0.003)Home ownership — 0.061*** (0.009)Age 0.009*** (0.0007) 0.006*** (0.001)Age square �0.00001*** (9.40e�07) �8.19e�06*** (1.50e�06)Gini coefficient �137.623*** (12.304) �67.763� (32.702)Gini square 152.758*** (14.042) 76.571� (36.969)Cognitive ability 0.002*** (0.000183) 0.001*** (0.0002)Number of years of completed education 0.035*** (0.002) 0.017*** (0.003)Experience 0.001*** (0.0000605) 0.0005*** (0.00009)Experience Square �4.07e�07*** (4.52e�08) �1.96e�07*** (6.06e�08)Industry (Reference: Manufacturing)Agriculture, Forestry and Fisheries �0.301*** (0.017) �0.289*** (0.028)Mining 0.082** (0.028) �0.015 (0.043)Construction �0.044*** (0.011) �0.027�� (0.016)Transportation, Communication andOther Public Utilities

�0.019 (0.012) �0.008 (0.016)

Wholesale and Retail Trade �0.153*** (0.009) �0.119*** (0.013)Finance, Insurance and Real State 0.014 (0.017) 0.030 (0.020)Business and Repair Services �0.116*** (0.011) �0.046** (0.016)Personal Services �0.216*** (0.020) �0.142*** (0.031)Entertainment and Recreation Services �0.164*** (0.022) �0.186*** (0.034)Professional and Related Services �0.135*** (0.012) �0.061*** (0.015)Public Administration �0.039* (0.015) �0.011 (0.018)Race (Reference: white)- Hispanic 0.045*** (0.011) 0.034� (0.014)- Black �0.049*** (0.010) 0.012 (0.014)Constant 29.478*** (2.641) 13.867� (7.151)R2 30.9% 27.9%N 4382 3305

a See footnote [a] of Table 1.* Significant at p < 0.01.

** Significant at p < 0.005.*** Significant at p < 0.001.

� Significant at p < 0.05.�� Significant at p < 0.10 (two-tailed test).

J.R. Morillas / Social Science Research 36 (2007) 808–833 827

4.2. Race, wealth and opportunities: A new explanation of the black/white opportunities gap

The argument that I have developed in this paper provides the basis from which to for-mulate an explanation of the black/white earnings gap. If assets inequality matters forimproving individual’s economic opportunities, and if wealth is unequally distributedbetween blacks and whites, we should predict different opportunities for them. Let usmake explicit the underlying syllogism to clarify this proposition.

(1) Assets inequality matters. In the former section in this paper, evidence has been pro-vided in support of the first proposition—wealth is related with individuals opportu-nities for earnings acquisition.

828 J.R. Morillas / Social Science Research 36 (2007) 808–833

(2) Blacks and whites are unequal wealth-wise. As a consequence of what Oliver andShapiro (1995) have called ‘‘the sedimentation of inequality,’’ blacks have less wealththan whites. Net of the effect of education, income, propensity to save, and otherdeterminants of wealth accumulation, blacks and whites are characterized by a veryunequal pattern of asset holding.

(3) The logical conclusion that we can obtain from the former premises is that theBlack/White Earnings Gap arises from their unequal initial wealth. If they wouldhave the same wealth, their opportunities for earnings acquisition would besimilar.

If the proposition is correct, given that blacks and whites are unequal wealth-wise, theearnings gap between these two groups should be reduced once the effect of wealth is con-trolled. If we could make the distribution of assets between blacks and whites more equal,the earnings gap would be reduced. Put it differently, in a regression context, controllingfor the accumulated wealth, the black/white gap should be reduced.

To test this proposition, I shall estimate two models (vid. Table 5 below). In the firstmodel, I do not control for wealth. In Model 2, I consider the effect of wealth. The vari-ables included in the three models in Table 5 provide a control for the main dimensions ofthe black–white heterogeneity underlying the earnings gap. I include in the vector of inde-pendent variables the number of years of completed education and a measure of cognitiveability to control for the role of pre-market factors in the generation of the earnings gap.The economic sector in which the individual is employed is intended to capture the role ofsegregation. And the variable experience is intended to capture the role of market factorsand the accumulation of labor market experience.

We can see that, once we control for wealth, there are no significant differences betweenblacks and whites in terms of earnings mobility. The gap between the two becomes close tozero and turns out to be statistically non-significant. These results show that if blacks andwhites would own the same level of assets, they would enjoy the same opportunities forearnings acquisition across their life-courses.

To confirm the robustness of the former analysis, I have estimated new models. Thenew estimated models differ from those in Table 5 in the way experience is measured. Ihave included two additional variables: (i) the individual’s experience unemployed and(ii) the experience out of the labor force, both measured in weeks. The rationale behindthis robustness analysis is the following one. Due to a more frequent pattern of intermit-tent labor force participation of blacks (Rosenfeld, 1992; Tienda and Stier, 1996), a singlemeasure of experience–experience employed- may overstate the labor market experience ofone or another race. Insofar as such differences in experience could be correlated with theaccumulation of assets, the previous conclusion about the role of wealth in explaining theblack/white gap could be challenged. Therefore, we need to analyze its robustness to dif-ferent measures of experience. These models can be found in Table 6.16

If we compare the estimated parameters of the dummy variable ‘‘black’’ from Model 1in Tables 5 and 6, we can see that the black/white gap is smaller when we include, in addi-tion to the measure of experience working, the experience unemployed and out of theforce. In other words, part of the black/white gap arises from the fact that blacks spend

16 I thank an anonymous referee for her/his suggestion for carrying out this robustness analysis.

Table 6Race, wealth and earnings mobility: random-effects estimatesa

Variables Model 1 Model 2Coefficient (standard error) Coefficient (standard error)

Lagged dependent variable �0.697*** (0.004) �0.585*** (0.006)First Difference assets (log) — 0.044*** (0.003)Lagged assets (log) — 0.057*** (0.003)Home ownership — 0.060*** (0.009)Age 0.009*** (0.001) 0.006*** (0.001)Age square �0.00001*** (9.40e�07) �8.16e�06*** (1.50e�06)Gini coefficient �115.135*** (12.851) �69.826� (32.157)Gini square 128.296*** (14.600) 79.082� (37.431)Cognitive ability 0.002*** (0.0002) 0.001*** (0.0002)Number of years of completed education 0.031*** (0.002) 0.016*** (0.003)Experience employed 0.001*** (0.00007) 0.0005*** (0.0001)Experience employed square �3.99e�07*** (4.59e�08) �2.05e�07*** (6.26e�08)Experience unemployed �0.001*** (0.0001) �0.0003 (0.0002)Experience unemployed square 1.81e�06*** (4.43e�07) �1.78e�07 (8.61e�07)Experience out of the labor force �0.0001 (0.00008) 0.00008 (0.0001)Experience out of the labor force square 3.34e�07� (1.52e�07) 1.48e�07 (1.70e�07)Industry (Reference: Manufacturing)Agriculture, Forestry and Fisheries �0.301*** (0.017) �0.293*** (0.028)Mining 0.085** (0.028) �0.013 (0.042)Construction �0.039*** (0.011) �0.026 (0.016)Transportation, Communication andOther Public Utilities

�0.021�� (0.012) �0.010 (0.016)

Wholesale and Retail Trade �0.155*** (0.009) �0.121*** (0.013)Finance, Insurance and Real State 0.012 (0.017) 0.029 (0.020)Business and Repair Services �0.115*** (0.011) �0.047** (0.016)Personal Services �0.213*** (0.020) �0.142*** (0.031)Entertainment and Recreation Services �0.163*** (0.022) �0.187*** (0.034)Professional and Related Services �0.137*** (0.012) �0.062*** (0.015)Public Administration �0.044** (0.015) �0.013 (0.018)Race (Reference: white)- Hispanic 0.045*** (0.011) 0.033� (0.014)- Black �0.039*** (0.010) 0.014 (0.014)Constant 24.383*** (2.776) 14.291� (7.263)R2 31.2% 28.1%N 4382 3304

a See footnote [a] of Table 1.* Significant at p < 0.01.

** Significant at p < 0.005.*** Significant at p < 0.001.

� Significant at p < 0.05.�� Significant at p < 0.10 (two-tailed test).

J.R. Morillas / Social Science Research 36 (2007) 808–833 829

more time unemployed and out of the labor force than whites. And if we do not considerit, we obtain a 1% upward estimate of the black/white. In Table 5, the gap is a 5%, while inTable 6 the gap is a 4%.

In any case, the argument is still confirmed with the available data in both cases. Wecan see in Model 2 both in Tables 5 and 6, that the gap disappears and turns out to bestatistically non-significant. This conclusion is robust to the way experience is measured.In both cases, using a single- or multiple-measures of labor market experience, we obtain

830 J.R. Morillas / Social Science Research 36 (2007) 808–833

the same result. The black/white gap arises partly from the unequal wealth of blacks andwhites.

5. Discussion: Assets, persistent inequalities, and the black/white divide

In this paper, evidence has been provided showing that assets are indeed associated withthe opportunities for earnings acquisition in the labor market. The mobility of earnings isassociated with the endowment of wealth. In the context of the error correction modelspresented in Section 3, a long-term relation between (past or accumulated) wealth and(future) earnings mobility has been found. These results show that there are empiricalgrounds, not only theoretical, for expecting the ‘‘assets matter’’ framework to be takenas sound. This is consistent with the first of the two testable propositions formulated inthe paper.

Moreover, the second proposition has obtained empirical support from the analyses inthis study. As argued in Section 4, if blacks and whites are unequal in terms of their pat-tern of wealth ownership, as it has been shown in Oliver and Shapiro (1995), and if assetsdo indeed matter, we would expect blacks and whites to display different opportunities forearnings acquisition in the labor market. To put it differently, in a regression context, forthe argument to be accurate, the black–white gap in earnings mobility should be reducedonce wealth differences are held constant. In the context of the two models presented inTables 5 and 6, it can be concluded that the black/white wage mobility gap arises partlyfrom the unequal patter of wealth holding of those two groups.

Incidentally, this explanation of the black/white earnings gap is quite novel. Fol-lowing the path-breaking study of Oliver and Shapiro (1995), many empirical analyseshave shed light on the racial differences of wealth ownership, particularly the unequalpattern of assets holding of blacks and whites. However, the consequences of thisunequal pattern of wealth remain relatively unattended. Wealth inequality amongblacks and whites has been the explanandum of several empirical investigations, butat least to my knowledge only one study has elaborated it as an explanans of theblack/white inequality. The only exception is Conley (1999, chapter 4), in which hestudies the relation between parents’ wealth and individuals wage attainment. Theanalyses in this paper go beyond those of Conley (1999) by introducing a dynamicelement into the analysis. Indeed, in Conley (1999, chapter 4) the process of wageattainment is analyzed in a different way to the one in this paper due to the fact thathis analysis is static, in the sense that the dependent variable is the wage attained bythe individual at a point in time. In any case, there is a good deal of empirical evi-dence on the causes of the black–white wealth inequality, but the actual as well as thepotential consequences of such an inequality are yet to be explored, and this paper isan step in this direction.

In this spirit, the analysis of earnings mobility allows concluding that the gap betweenblacks and whites in the opportunities for earnings acquisition in the labor market is relat-ed to their initial assets. Indeed, after controlling for wealth, the differential between thetwo groups decreases substantially. These results reinforce the expectations about the rela-tion between assets and individuals’ opportunities for earnings acquisition. This providessupport to the second proposition put forward in the paper, and supplies empirical foun-dations for the ‘‘assets framework’’ and its role as a tool for the analysis of opportunitiesand stratification processes.

J.R. Morillas / Social Science Research 36 (2007) 808–833 831

Appendix A

Mean SD

Descriptive statistics

Lagged earnings rate (log) 1.358 0.846 First difference assets (log) 0.071 1.324 Lagged assets (log) 6.913 1.845 Age 320.599 74.030 Gini 0.427 0.018 Cognitive ability 38.885 29.647 Number years comp. educ. 12.330 2.421 Experience 357.920 294.698Descriptive statistics by race

White

Lagged earnings rate (log)

1.464 0.811 First difference assets (log) 0.079 1.328 Lagged assets (log) 7.139 1.848Age

321.007 74.158 Gini 0.427 0.018 Cognitive ability 53.067 28.530 Number years comp. educ. 12.785 2.456 Experience 388.706 303.770Black

Lagged earnings rate (log)

1.170 0.897 First difference assets (log) .064 1.350 Lagged assets (log) 6.434 1.760 Age 320.005 73.818 Gini 0.427 0.018 Cognitive ability 20.922 20.767 Number years comp. educ. 12.023 2.087 Experience 308.961 275.782Hispanic

Lagged earnings rate (log)

1.343 0.822 First difference assets (log) 0.045 1.276 Lagged assets (log) 6.699 1.797 Age 320.459 74.022 Gini 0.427 0.018 Cognitive ability 29.959 25.248 Number years comp. educ. 11.609 2.560 Experience 353.645 288.573

832 J.R. Morillas / Social Science Research 36 (2007) 808–833

References

Abbott, A., 1992. What do cases do? In: Ragin, C., Becker, H. (Eds.), What is a Case? Cambridge UniversityPress, Cambridge.

Altonji, J., Hayashi, F., Kotlikoff, L., 1997. Parental altruism and inter vivos transfers: theory and evidence.Journal of Political Economy 105, 1121–1166.

Altonji, J., Blank, R., 1999. Race and gender in the labor market. In: Ashenfelter, O., Card, D. (Eds.), Handbookof Labor Economics, vol. 3. North Holland, Oxford.

Arrow, K., 1964. The role of securities in the optimal allocation of risk-bearing. Review of Economic Studies 31,91–96.

Arrow, K., 1974. Essays in the Theory of Risk-Bearing. Amsterdam, North Holland.Baron, J., 1984. Organizational perspectives on stratification. Annual Review of Sociology 10, 37–69.Beck, N., Katz, J., 1996. Nuisance vs. substance: specifying and estimating time series cross-section models.

Political Analysis 6, 1–34.Becker, G., 1971. The Economics of Discrimination. University of Chicago Press, Chicago.Beverly, S., Sherraden, M., 1999. Institutional determinants of savings: implications for low-income households

and public policy. Journal of Socio-Economics 28, 457–473.Black, D., 1995. Discrimination in an equilibrium search model. Journal of Labor Economics 13, 309–

334.Blau, F., Graham, J., 1990. Black–white differences in wealth and asset composition. Quarterly Journal of

Economics 105, 321–339.Borjas, G., Bronars, S., 1989. Consumer discrimination and self-employment. Journal of Political Economy 97,

581–606.Card, D., 1999. The causal effect of education on earnings. In: Ashenfelter, O., Card, D. (Eds.), Handbook of

Labor Economics, vol. 3. North Holland, Oxford.Carney, S., Gale, W., 2001. Assets accumulation among low-income households. In: Shapiro, T., Wolff, E. (Eds.),

Assets for the Poor. Russell Sage, New York.Conley, D., 1999. Being Black, Living in the Read. University of California Press, Berkeley and Los Angeles.Conley, D., 2001. Wrap-up with Rapporteurs. In: Shapiro, T., Wolff, E. (Eds.), Assets for the Poor. Russell Sage,

New York.Deaton, A., 1996. The Analysis of Household Surveys: A Microeconometric Approach to Development Policy.

Johns Hopkins University Press, Baltimore.Debreu, G., 1959. Theory of value: an axiomatic analysis of economic equilibrium. Yale University Press, New

Haven.Domar, E., Musgrave, R., 1944. Proportional income taxation and risk-taking. Quarterly Journal of Economics

58, 388–422.Edin, K., 2001. More than money: the role of assets in the survival strategies and material well-being of the poor.

In: Shapiro, T., Wolff, E. (Eds.), Assets for the Poor. Russell Sage, New York.Esping-Andersen, G., 1990. The Three Worlds of Welfare Capitalism. Princeton University Press, Princeton.Fisher, C., Hout, M., Sanchez-Janowski, M., Lucas, S., Swidler, A., Voss, K., 1996. Inequality by Design:

Cracking the Bell Curve Myth. Princeton University Press, Princeton.Goldthorpe, J., 2000. On Sociology. Oxford University Press, Oxford.Greene, W., 2000. Econometric Analysis. Prentice & Hall International, London.Herrnstein, R., Murray, C., 1994. The Bell Curve: Intelligence and Class Structure in American Life. Free Press,

New York.Hsueh, S., Tienda, M., 1995. Earnings consequences of employment instability among minority men. Research in