Embed Size (px)

Citation preview

Appendix C – BACK OF TEXTBOOKHint: Not in back of Chapter 10!

Time Value of Money $$$$

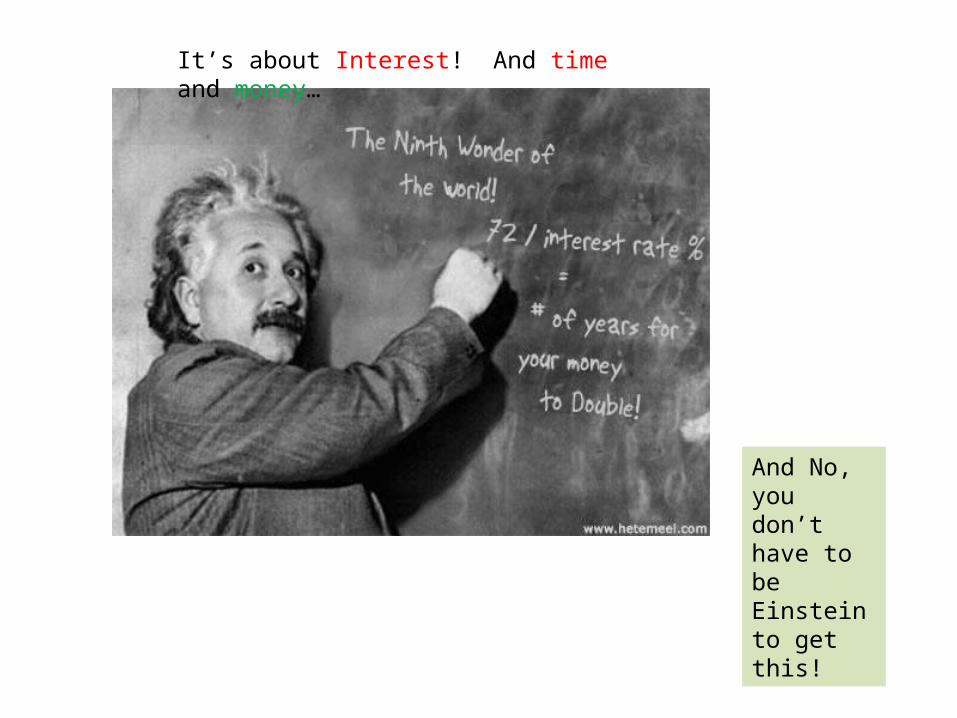

It’s about Interest! And time and money…

And No, you don’t have to be Einstein to get this!

Time Value of Money….

• The SAME amount of Money is worth more TODAY, then in the FUTURE.

• Why?• Because you could take that money and invest

it and earn interest on it.• How is interest calculated?

acct.220 4

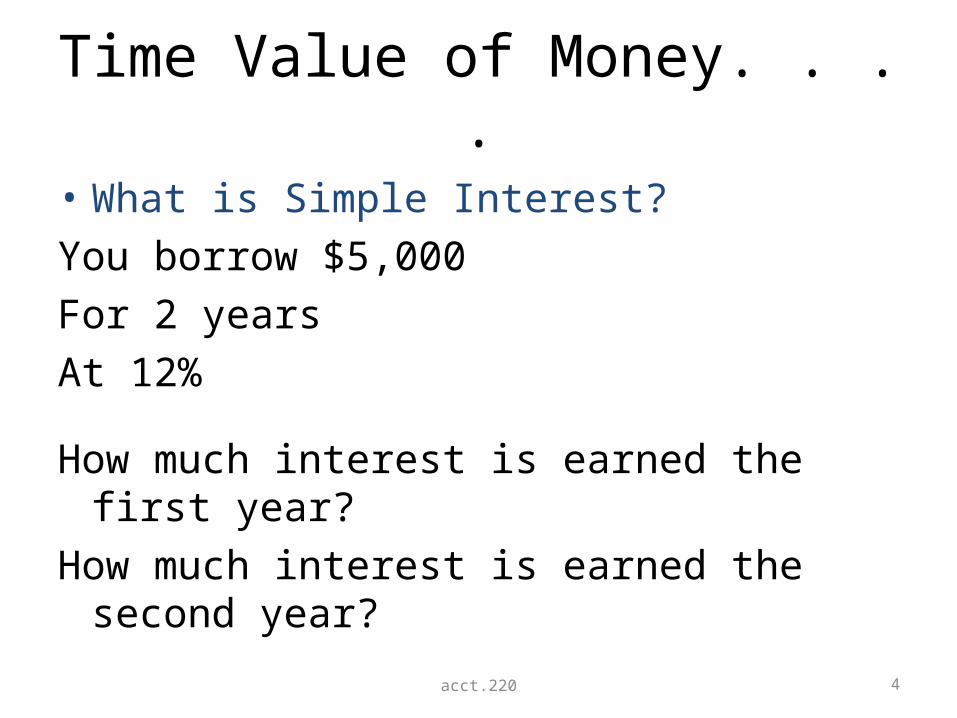

Time Value of Money. . . .

• What is Simple Interest?You borrow $5,000For 2 yearsAt 12%

How much interest is earned the first year?How much interest is earned the second year?

acct.220 5

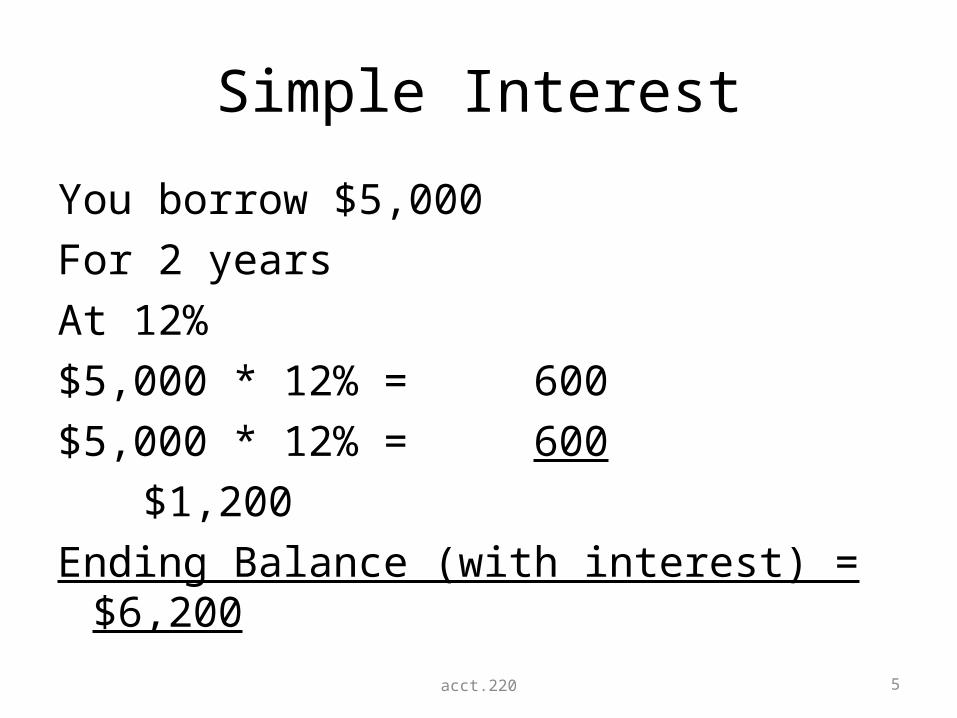

Simple Interest

You borrow $5,000For 2 yearsAt 12%$5,000 * 12% = 600$5,000 * 12% = 600

$1,200Ending Balance (with interest) = $6,200

acct.220 6

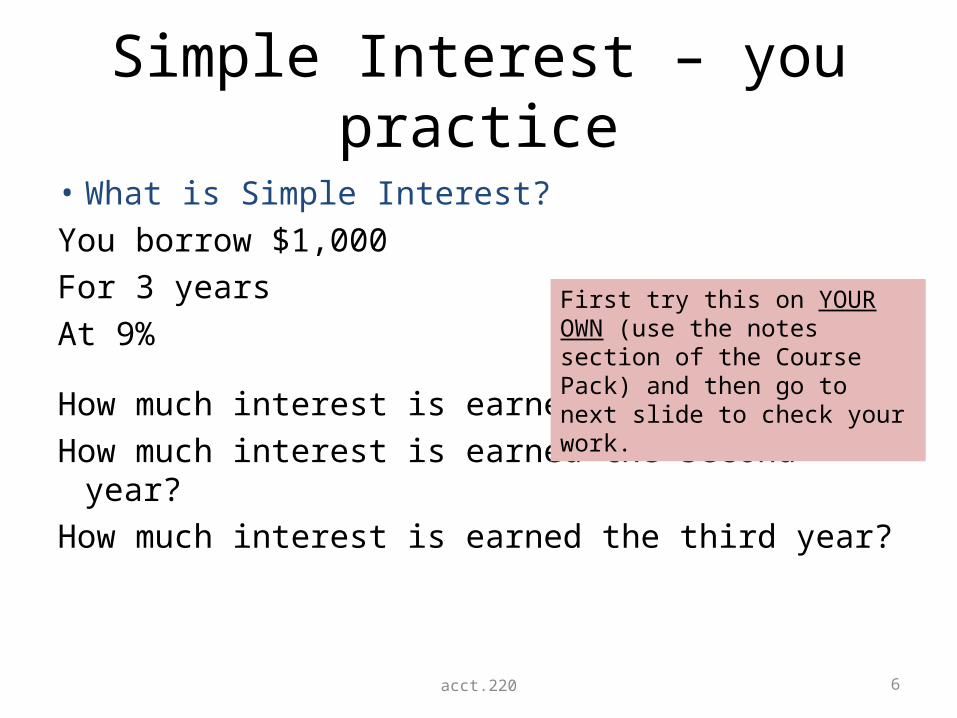

Simple Interest – you practice

• What is Simple Interest?You borrow $1,000For 3 yearsAt 9%

How much interest is earned the first year?How much interest is earned the second year?How much interest is earned the third year?

First try this on YOUR OWN (use the notes section of the Course Pack) and then go to next slide to check your work.

acct.220 7

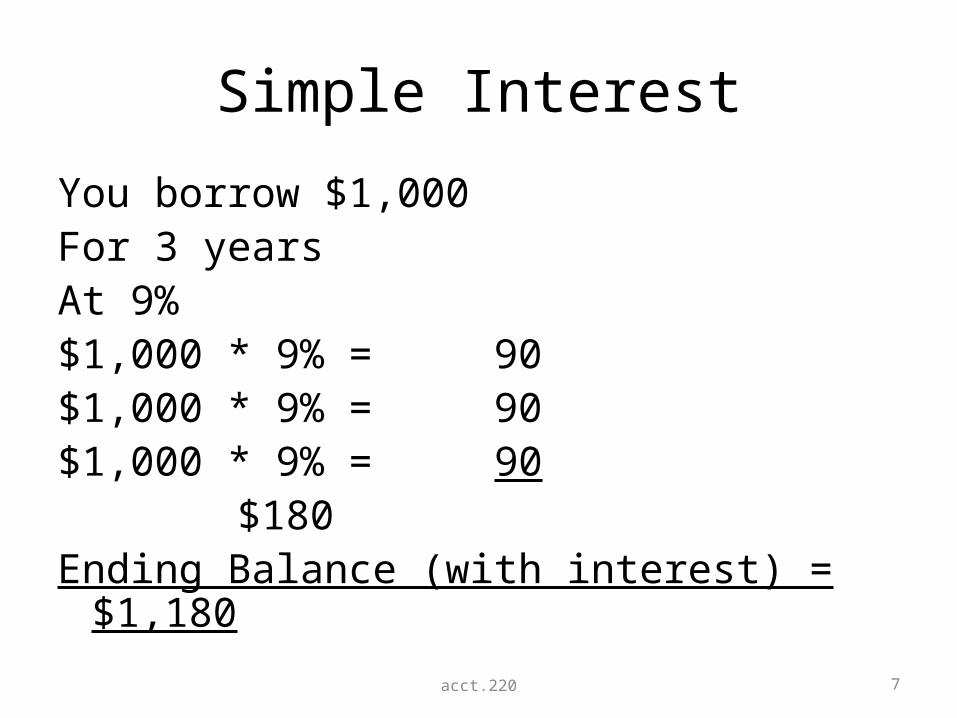

Simple Interest

You borrow $1,000For 3 yearsAt 9%$1,000 * 9% = 90$1,000 * 9% = 90$1,000 * 9% = 90

$180Ending Balance (with interest) = $1,180

acct.220 8

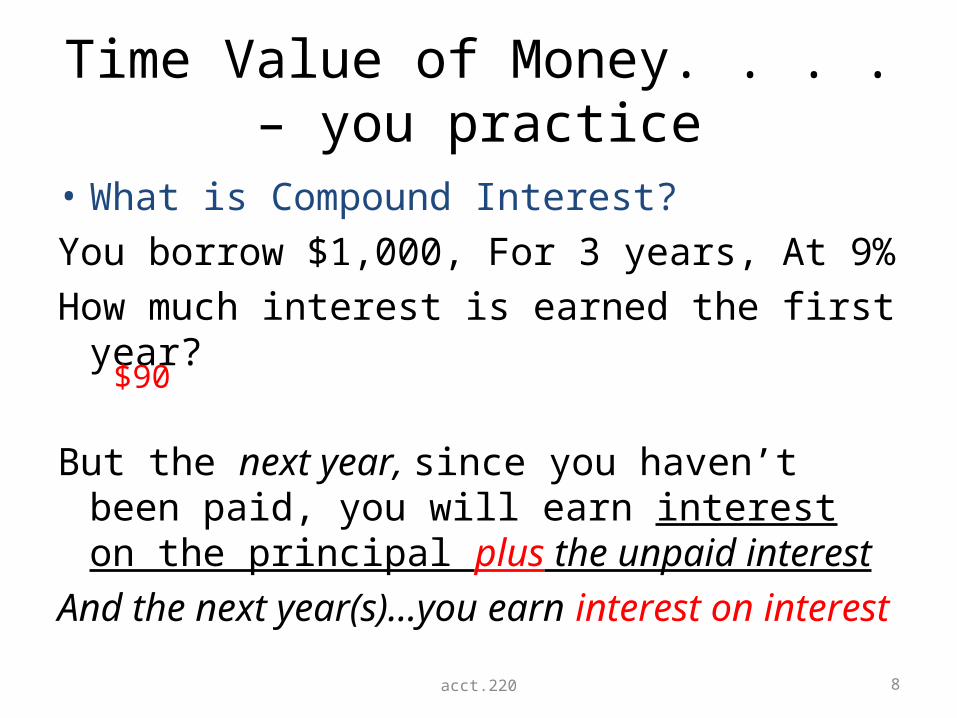

Time Value of Money. . . . – you practice

• What is Compound Interest?You borrow $1,000, For 3 years, At 9%How much interest is earned the first year?

But the next year, since you haven’t been paid, you will earn interest on the principal plus the unpaid interest

And the next year(s)…you earn interest on interest

$90

acct.220 9

Time Value of Money. . . . – you practice

• What is Compound Interest?You borrow $1,000For 3 yearsAt 9%How much interest is earned the first year?How much interest is earned the second year?How much interest is earned the third year?

First try this on YOUR OWN (use the notes section of the Course Pack) and then go to next slide to check your work.

acct.220 10

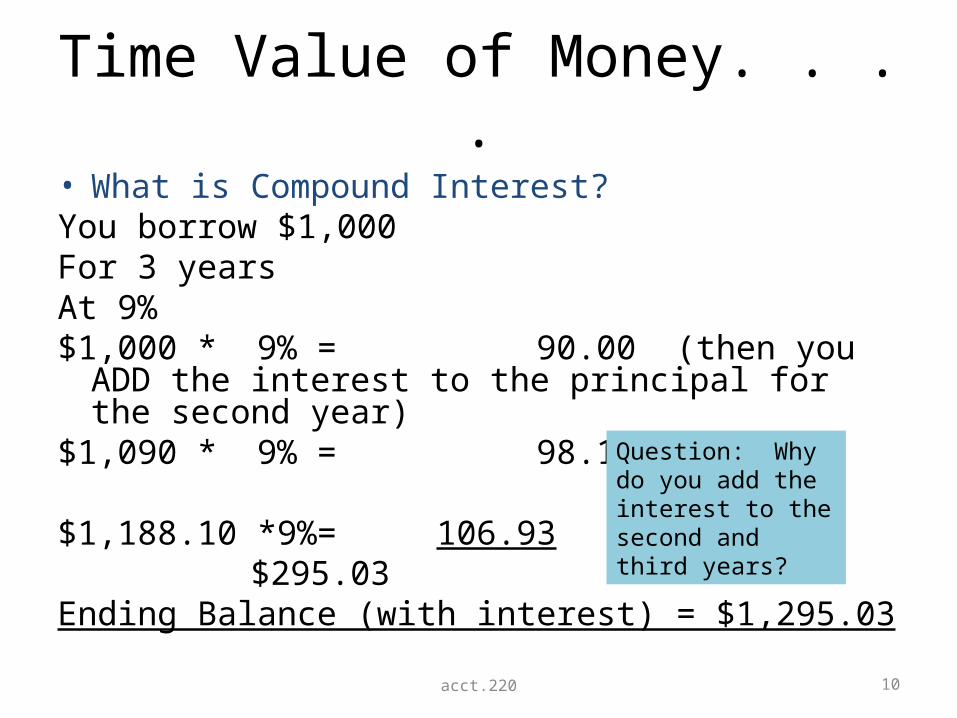

Time Value of Money. . . .• What is Compound Interest?You borrow $1,000For 3 yearsAt 9%$1,000 * 9% = 90.00 (then you ADD the interest to

the principal for the second year)$1,090 * 9% = 98.10

$1,188.10 *9%= 106.93 $295.03

Ending Balance (with interest) = $1,295.03

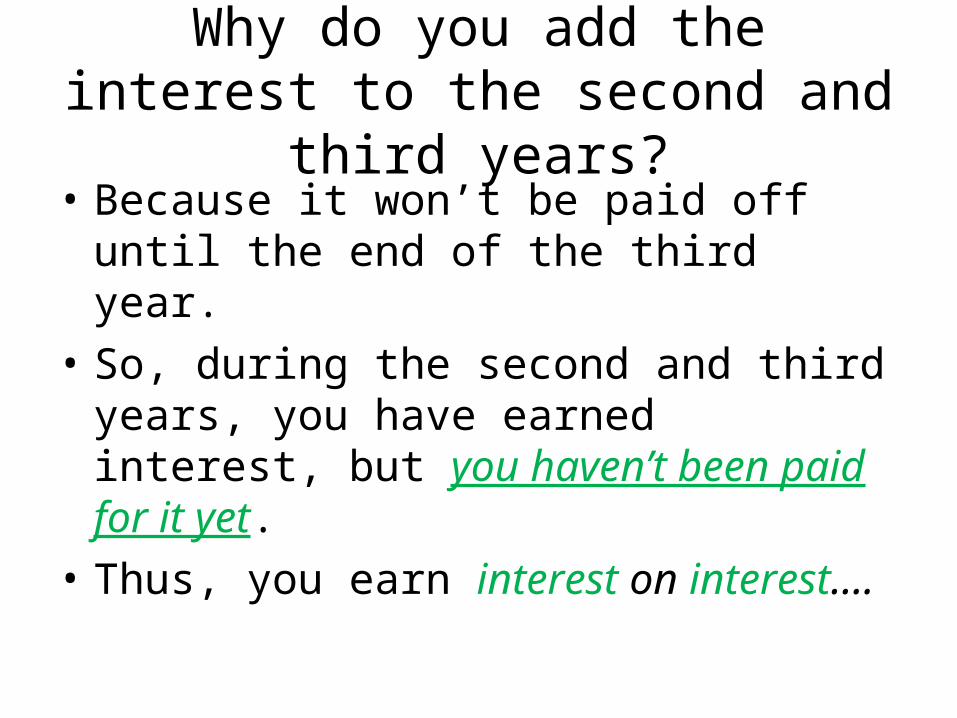

Question: Why do you add the interest to the second and third years?

Why do you add the interest to the second and third years?

• Because it won’t be paid off until the end of the third year.

• So, during the second and third years, you have earned interest, but you haven’t been paid for it yet.

• Thus, you earn interest on interest….

acct.220 12

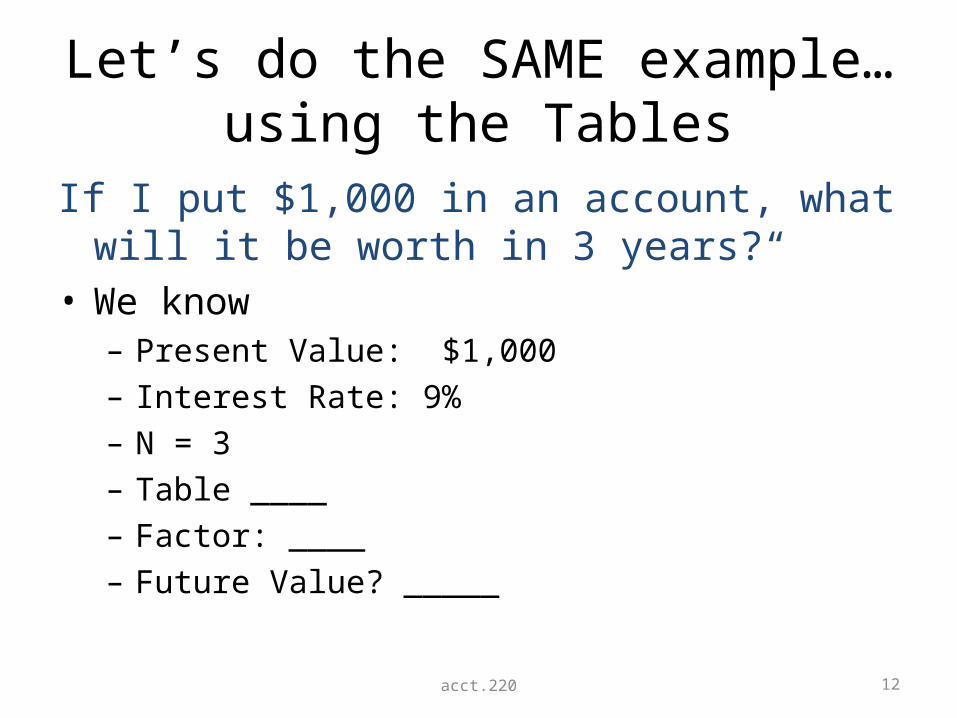

Let’s do the SAME example…using the Tables

If I put $1,000 in an account, what will it be worth in 3 years?“

• We know – Present Value: $1,000– Interest Rate: 9%– N = 3– Table ____– Factor: ____– Future Value? _____

acct.220 13

Table 1 Example – Future Value of a Single Amount

If I put $1,000 in an account, what will it be worth in 3 years?“

• We know – Present Value: $1,000– Interest Rate: 9%– N = 3– Table 1– Factor: 1.29503– Future Value? $1,000 * 1.29503 = $1,295.03

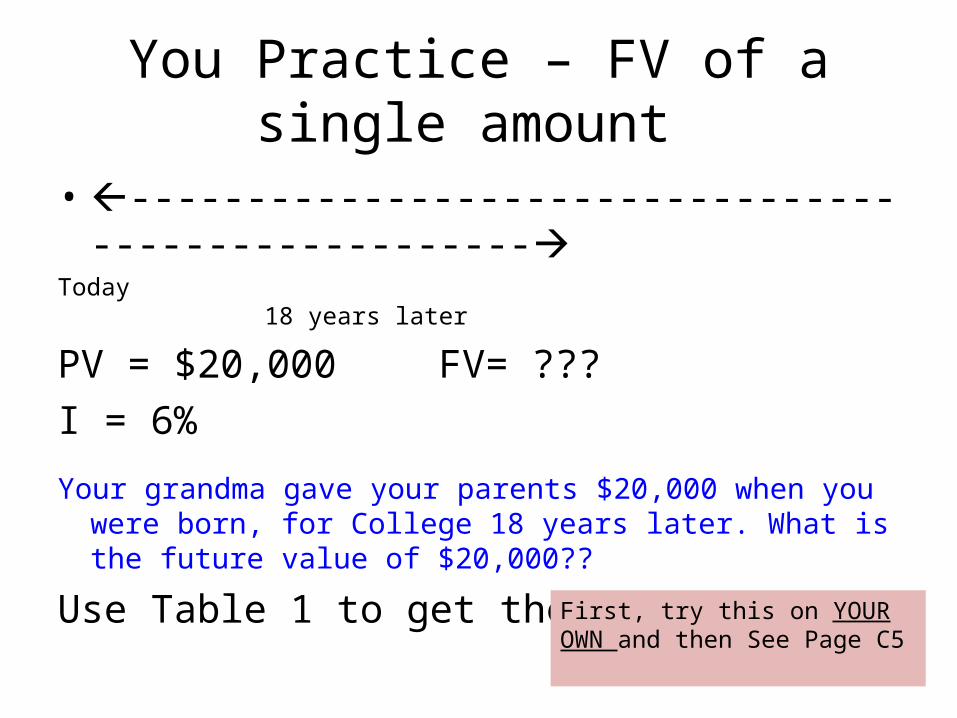

You Practice – FV of a single amount

• ----------------------------------------------------Today 18 years

later

PV = $20,000 FV= ???I = 6%

Your grandma gave your parents $20,000 when you were born, for College 18 years later. What is the future value of $20,000??

Use Table 1 to get the factor.First, try this on YOUR OWN and then See Page C5

You Practice – FV of a single amount

• ----------------------------------------------------Today 18 years

later

PV = $20,000 FV= ???I = 6%

Your grandma gave your parents $20,000 when you were born, for College 18 years later. What is the future value of $20,000??

Using Table 1 factor = 2.85434 * $20,000 = $57,086.80

What about Annuities?

• Question: What are annuities?

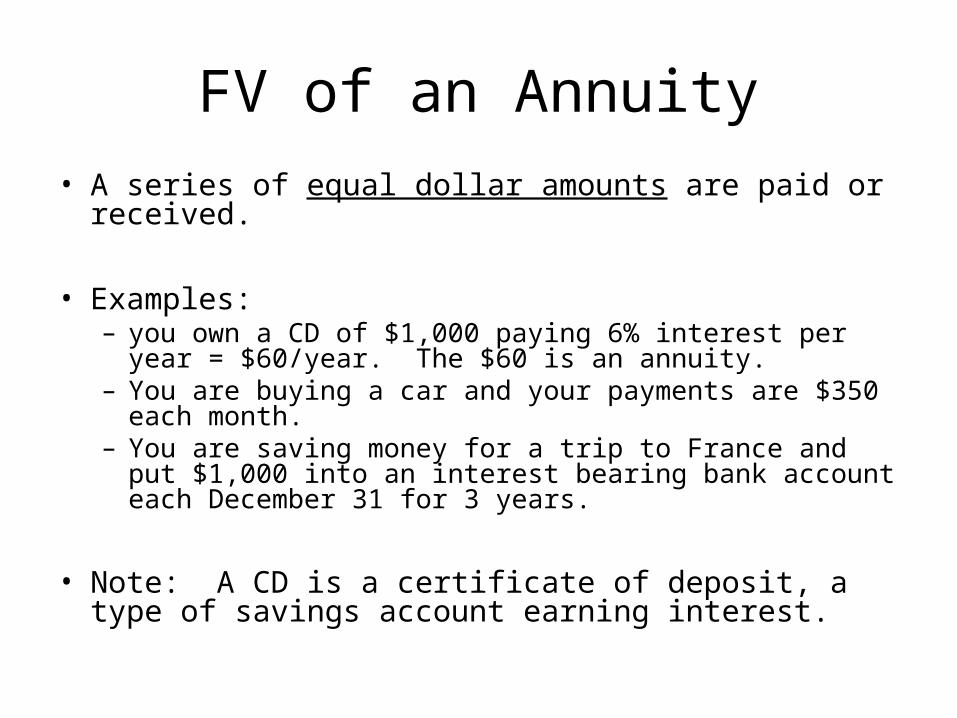

FV of an Annuity• A series of equal dollar amounts are paid or received.

• Examples: – you own a CD of $1,000 paying 6% interest per year = $60/year.

The $60 is an annuity.– You are buying a car and your payments are $350 each month.– You are saving money for a trip to France and put $1,000 into an

interest bearing bank account each December 31 for 3 years.

• Note: A CD is a certificate of deposit, a type of savings account earning interest.

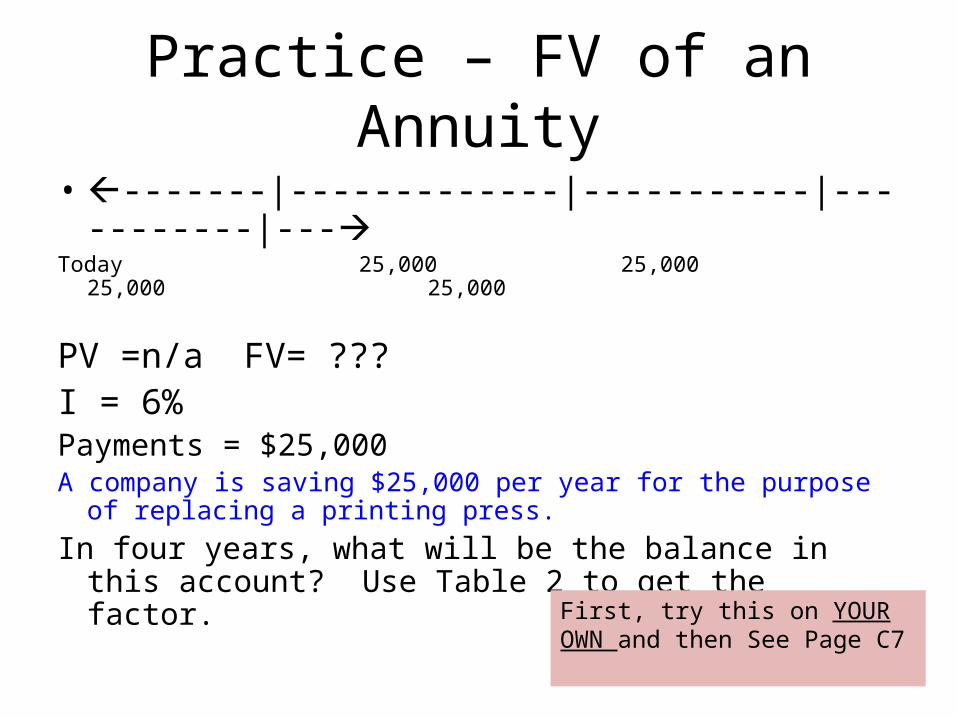

Practice – FV of an Annuity

• -------|-------------|-----------|-----------|---Today 25,000 25,000 25,000 25,000

PV =n/a FV= ???I = 6%Payments = $25,000A company is saving $25,000 per year for the purpose of

replacing a printing press. In four years, what will be the balance in this account?

Use Table 2 to get the factor. First, try this on YOUR OWN and then See Page C7

Practice – FV of an Annuity

• -------|-------------|-----------|-----------|---Today 25,000 25,000 25,000 25,000

PV =n/a FV= ???I = 6%Payments = $25,000

A company is saving $25,000 per year for the purpose of replacing a printing press.

In four years, what will be the balance in this accounts? Using Table 2 factor = 4.37462 * $25,000 = $109,365.50

acct.220 20

Present Value: what’s it worth now?

• Single Amount Example: “What do I have to put into the bank NOW, to have $1,000 in 1 year?“ assume 10% interest rate

• We know: – Present Value: ???? (what we are solving for)– Interest Rate: 10%– N = 1– Table 3– Factor: 0.90909– Future Value? $1,000– PV = $1,000 * 0.90909 = $909.09

Present Value

• Also called “discounting”• Why? Because money now can earn interest

and will be worth more later.

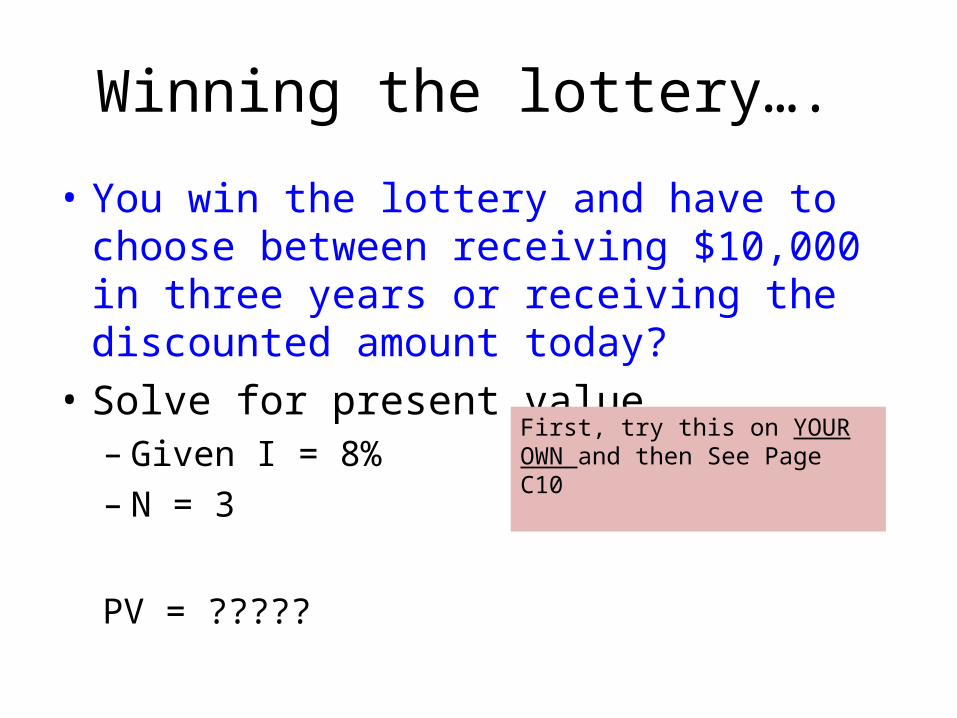

Winning the lottery….

• You win the lottery and have to choose between receiving $10,000 in three years or receiving the discounted amount today?

• Solve for present value– Given I = 8%– N = 3

PV = ?????

First, try this on YOUR OWN and then See Page C10

Winning the lottery….

• You win the lottery and have to choose between receiving $10,000 in three years or receiving the discounted amount today?

• Solve for present value– Given I = 8%– N = 3

Using Table 3 factor = 0.79383 * $10,000 = $7,938.30

First, try this on YOUR OWN and then See Page C10

What about Present Value of an annuity?

• For example, instead of making payments, I’ll just pay Cash NOW….

acct.220 25

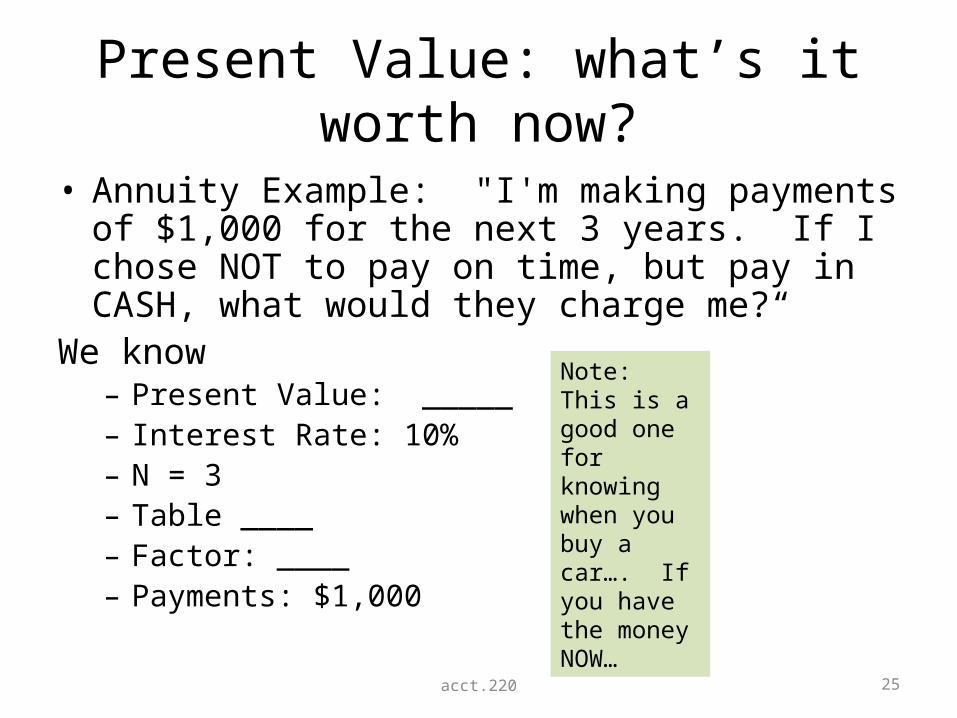

Present Value: what’s it worth now?

• Annuity Example: "I'm making payments of $1,000 for the next 3 years. If I chose NOT to pay on time, but pay in CASH, what would they charge me?“

We know – Present Value: _____– Interest Rate: 10%– N = 3– Table ____– Factor: ____– Payments: $1,000

Note: This is a good one for knowing when you buy a car…. If you have the money NOW…

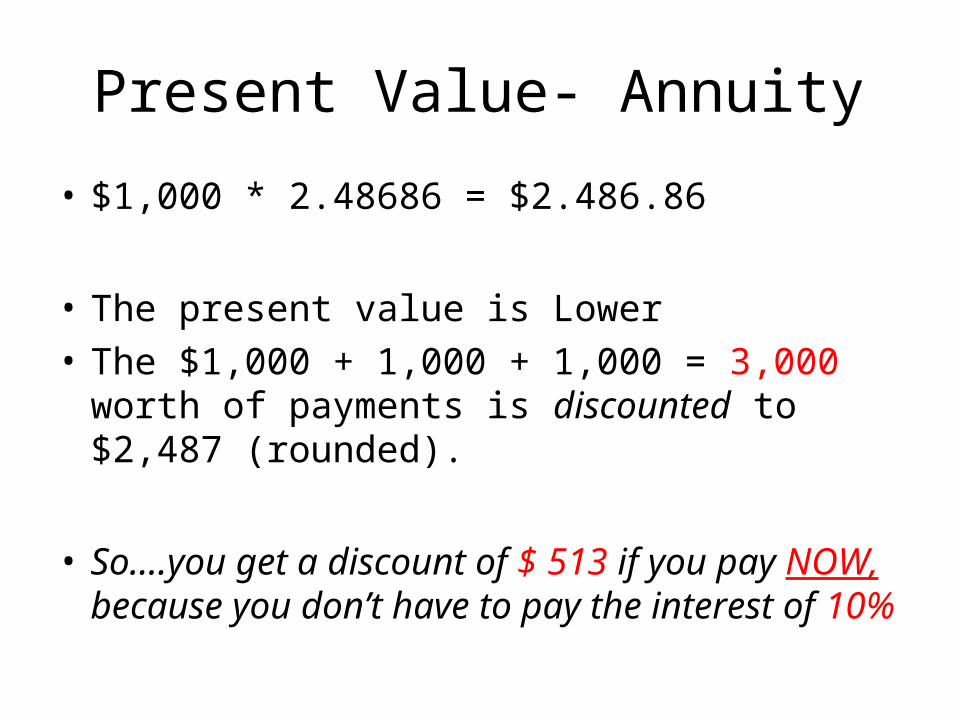

Present Value- Annuity

• $1,000 * 2.48686 = $2.486.86

• The present value is Lower• The $1,000 + 1,000 + 1,000 = 3,000 worth of

payments is discounted to $2,487 (rounded).

• So….you get a discount of $ 513 if you pay NOW, because you don’t have to pay the interest of 10%

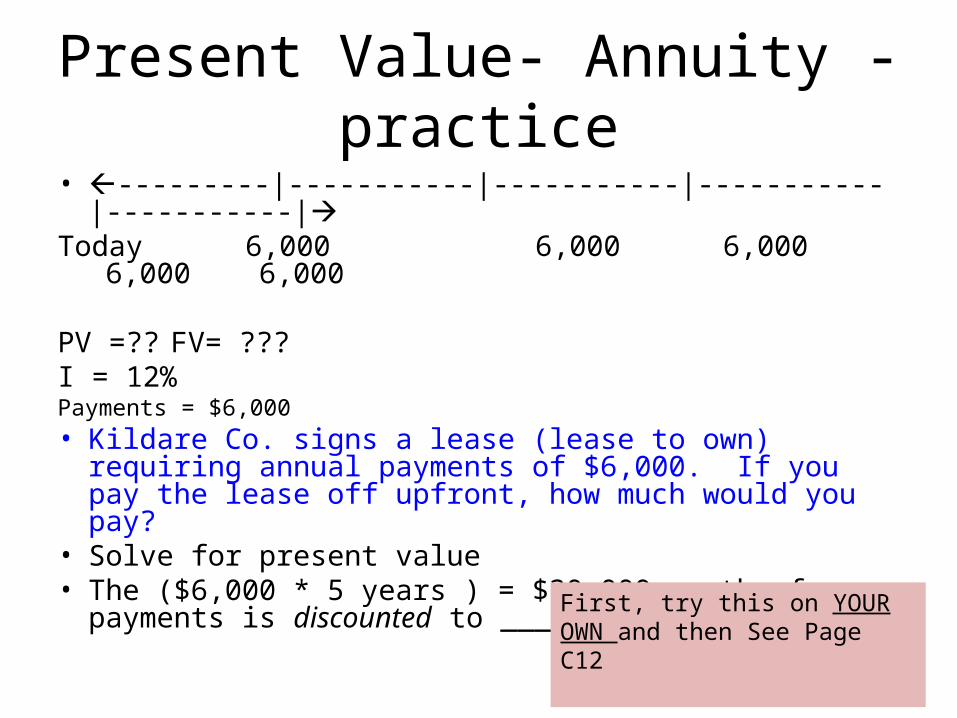

Present Value- Annuity -practice• ---------|-----------|-----------|-----------|-----------|Today 6,000 6,000 6,000 6,000 6,000

PV =?? FV= ???I = 12%Payments = $6,000• Kildare Co. signs a lease (lease to own) requiring annual

payments of $6,000. If you pay the lease off upfront, how much would you pay?

• Solve for present value• The ($6,000 * 5 years ) = $30,000 worth of payments is

discounted to ____________ First, try this on YOUR OWN and then See Page C12

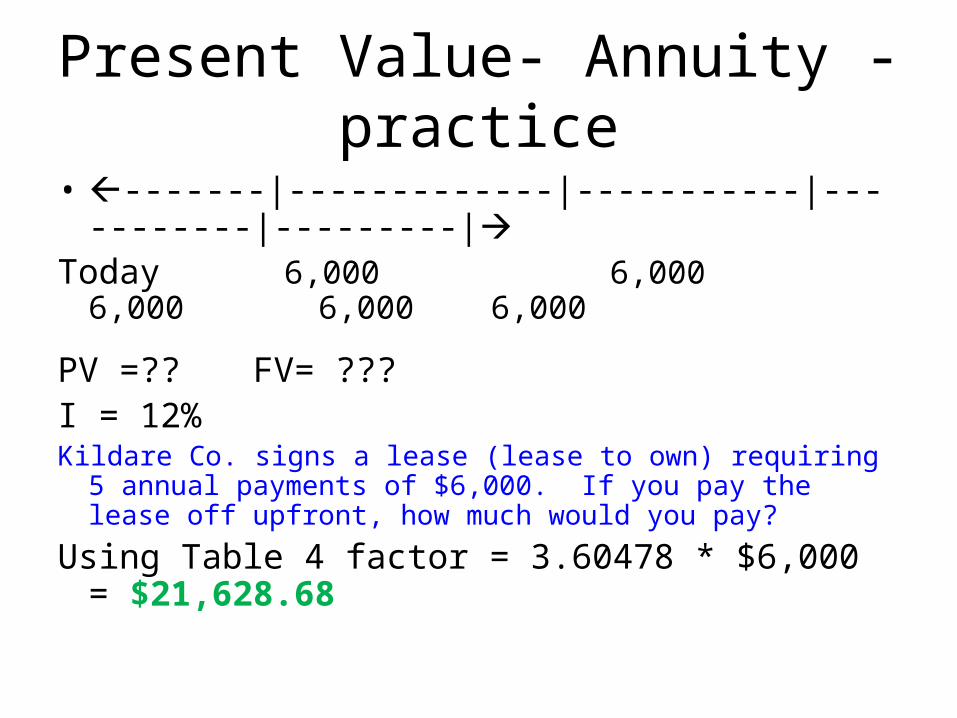

Present Value- Annuity -practice

• -------|-------------|-----------|-----------|---------|Today 6,000 6,000 6,000 6,000 6,000

PV =?? FV= ???I = 12%Kildare Co. signs a lease (lease to own) requiring 5 annual

payments of $6,000. If you pay the lease off upfront, how much would you pay?

Using Table 4 factor = 3.60478 * $6,000 = $21,628.68

acct.220 29

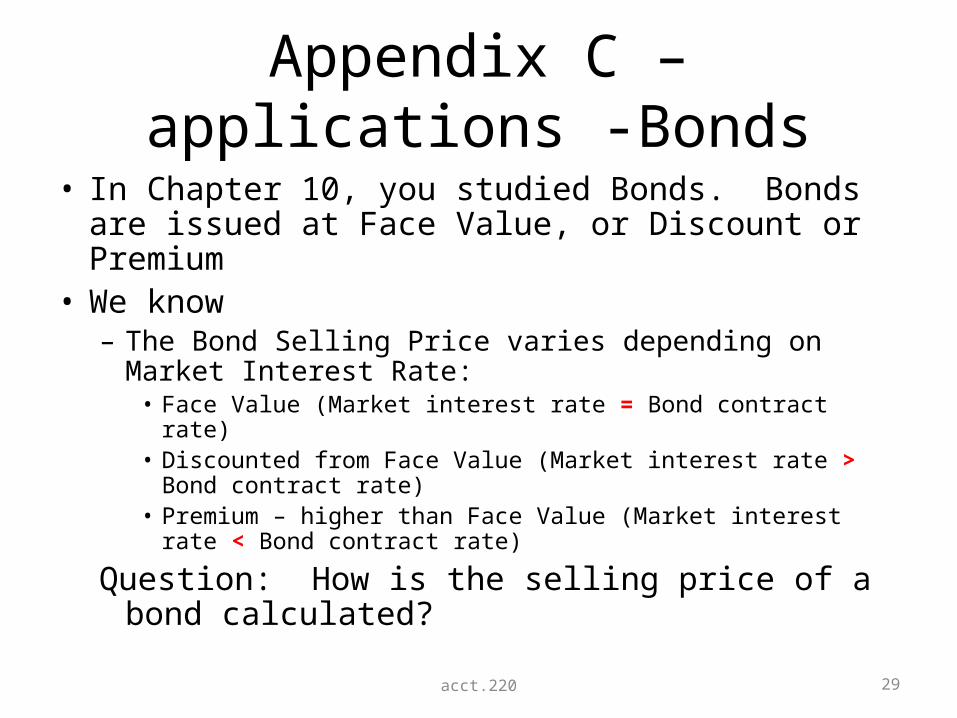

Appendix C – applications -Bonds

• In Chapter 10, you studied Bonds. Bonds are issued at Face Value, or Discount or Premium

• We know – The Bond Selling Price varies depending on Market

Interest Rate:• Face Value (Market interest rate = Bond contract rate)• Discounted from Face Value (Market interest rate > Bond contract

rate)• Premium – higher than Face Value (Market interest rate < Bond

contract rate)

Question: How is the selling price of a bond calculated?

acct.220 30

Appendix C – applications -Bonds

NEED TO KNOW:– Bond Interest Rate (the contract rate)– Face Value of Bond Issuance ($1,000 x number of bonds

sold)– Bond Interest Payments (Face Value of Bond Issuance x

semi annual bond interest (contract) rate– Market Interest Rate

31

The Cash Flow of Bonds

Let’s say you have 1,000 bonds. Review: What is the face value of a single bond?

Stop and Answer before checking the next slide

32

The Cash Flow of Bonds

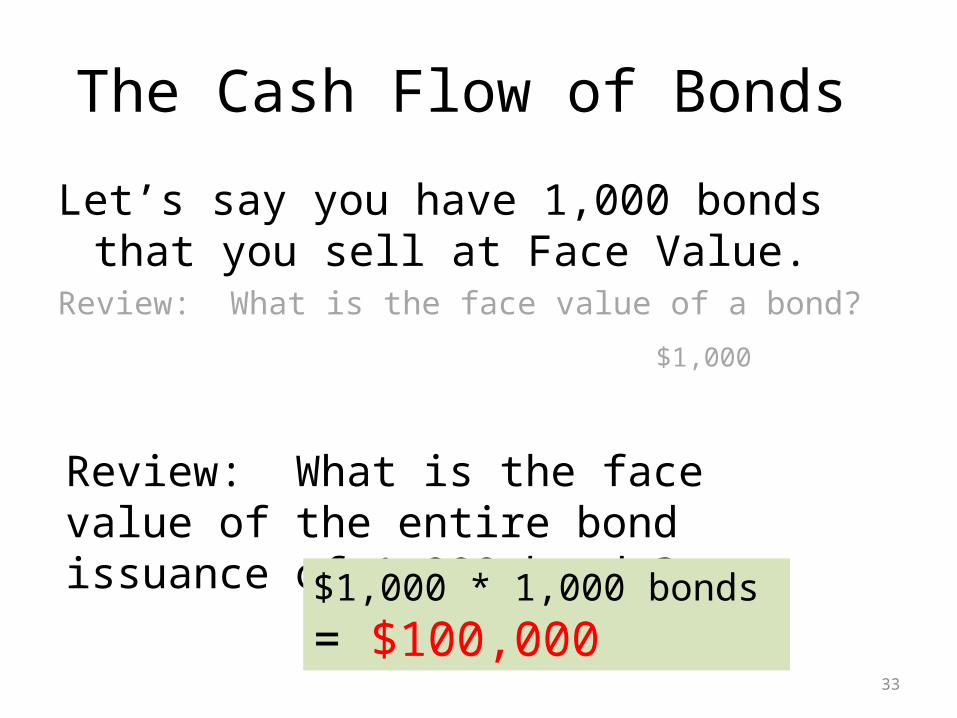

Let’s say you have 1,000 bonds. that you sell at Face Value.

Review: What is the face value of a single bond?

$1,000

Review: What is the face value of the entire bond issuance of 1,000 bonds?

33

The Cash Flow of Bonds

Let’s say you have 1,000 bonds that you sell at Face Value.

Review: What is the face value of a bond?

$1,000

Review: What is the face value of the entire bond issuance of 1,000 bonds?

$1,000 * 1,000 bonds = $100,000

34

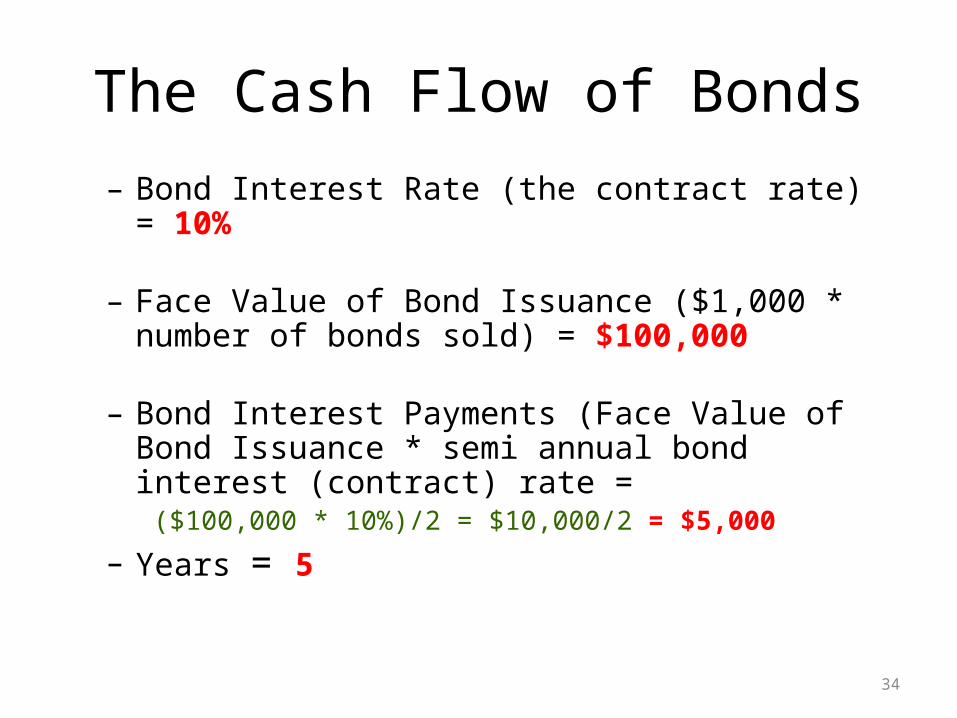

The Cash Flow of Bonds– Bond Interest Rate (the contract rate) = 10%

– Face Value of Bond Issuance ($1,000 * number of bonds sold) = $100,000

– Bond Interest Payments (Face Value of Bond Issuance * semi annual bond interest (contract) rate =

($100,000 * 10%)/2 = $10,000/2 = $5,000

– Years = 5

35

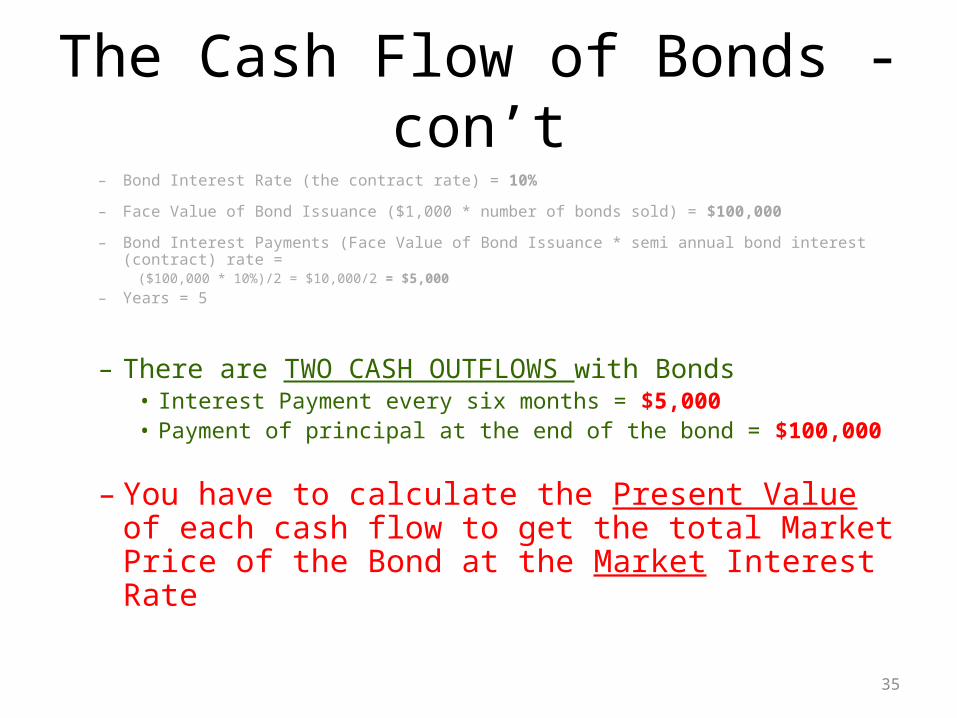

The Cash Flow of Bonds - con’t– Bond Interest Rate (the contract rate) = 10%

– Face Value of Bond Issuance ($1,000 * number of bonds sold) = $100,000

– Bond Interest Payments (Face Value of Bond Issuance * semi annual bond interest (contract) rate =($100,000 * 10%)/2 = $10,000/2 = $5,000

– Years = 5

– There are TWO CASH OUTFLOWS with Bonds• Interest Payment every six months = $5,000• Payment of principal at the end of the bond = $100,000

– You have to calculate the Present Value of each cash flow to get the total Market Price of the Bond at the Market Interest Rate

36

Cash Flow of the Principal

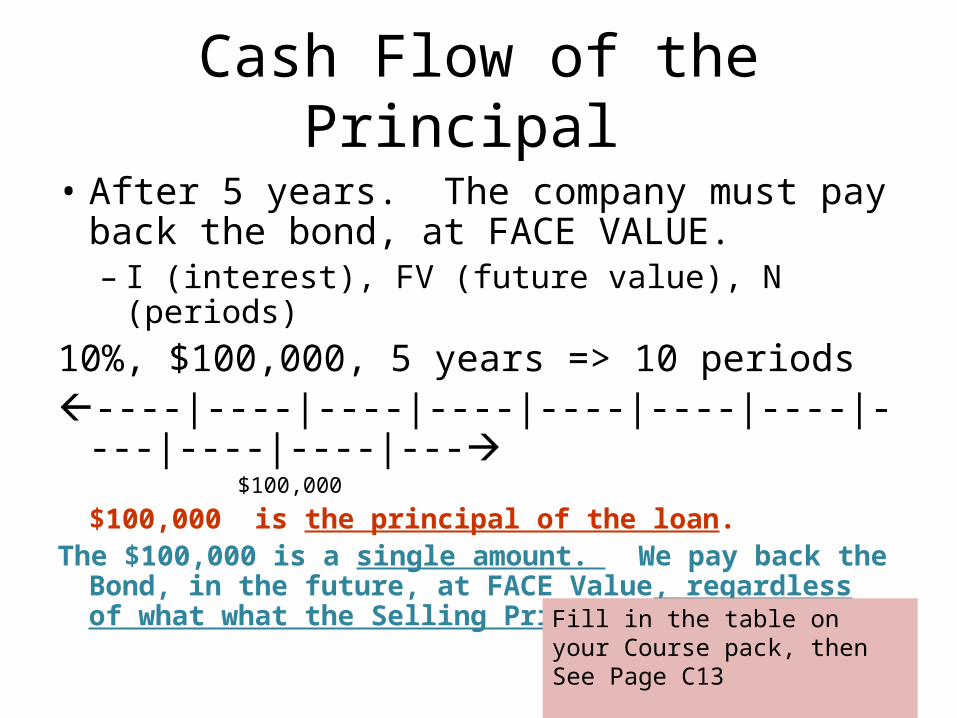

• After 5 years. The company must pay back the bond, at FACE VALUE.– I (interest), FV (future value), N (periods)

10%, $100,000, 5 years => 10 periods----|----|----|----|----|----|----|----|----|----|--- $100,000

$100,000 is the principal of the loan.The $100,000 is a single amount. We pay back the Bond, in the

future, at FACE Value, regardless of what what the Selling Price of the Bond was.

Fill in the table on your Course pack, then See Page C13

37

Cash Flow of Interest Paid

• I’m LOCKED IN WITH:– I (interest), FV (future value), N (periods)

10%, $100,000, 5 years => 10 periods----|----|----|----|----|----|----|----|----|----|--- $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000

$5,000 will be paid out in interest, every six months for 10 periods, over the life of the bond, for a total of $50,000.

The $5,000 is an annuity. We use the Bond contract rate to calculate the $5,000. It doesn’t change, regardless of the Selling Price of the Bond.

38

Present Value of Bonds -Face Value

• If contract rate is 10% and market is 10%. . . . You can sell the Bond at face value . Proof:

---------------------------------------------

--------------------------------------------- $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000

Total = $100,000

Imarket = 5%, table 4, factor = 7.72173 x $5,000 = $38,609

Imarket = 5%, table 3, factor =.61391 x $100,000 = $61,391

$61,391 + 38,609 = $100,000 would be Issue Price or 100

39

Present Value of Bonds -Discount

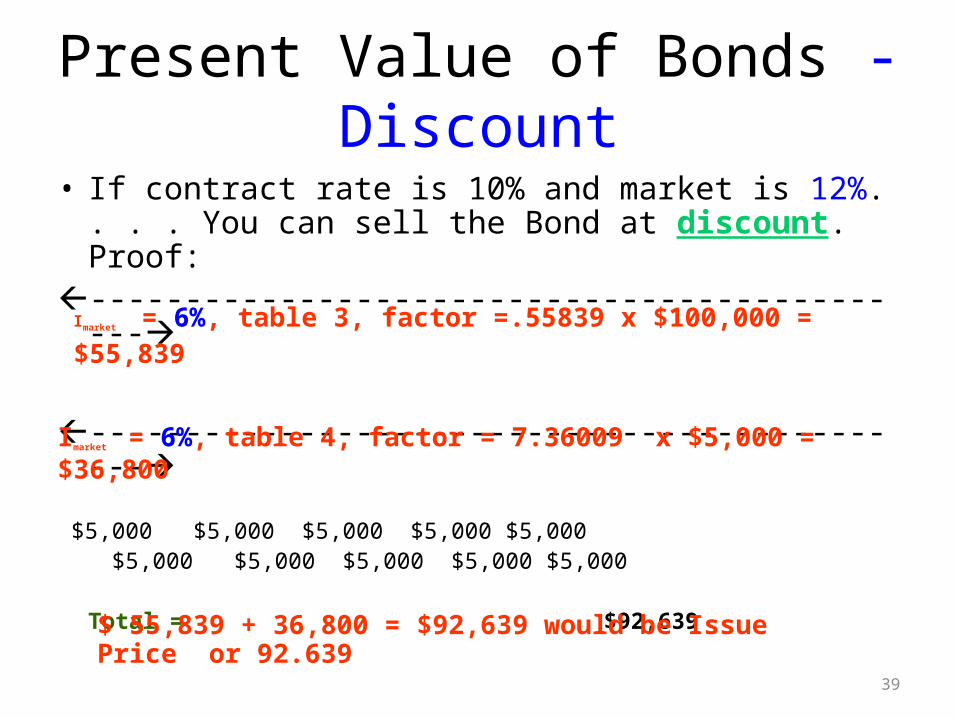

• If contract rate is 10% and market is 12%. . . . You can sell the Bond at discount. Proof:

---------------------------------------------

--------------------------------------------- $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000

Total = $92,639

Imarket = 6%, table 4, factor = 7.36009 x $5,000 = $36,800

Imarket = 6%, table 3, factor =.55839 x $100,000 = $55,839

$ 55,839 + 36,800 = $92,639 would be Issue Price or 92.639

40

Present Value of Bonds -Premium

• If contract rate is 10% and market is 8%. . . . You can sell the Bond at premium. Proof:

---------------------------------------------

--------------------------------------------- $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000

Total = $108,111

Imarket = 4%, table 4, factor = 8.11090 x $5,000 = $40,555

Imarket = 4%, table 3, factor =.67556 x $100,000 = $67,556

$ 67,556 + 40,555 = $108.111 would be Issue Price or 108.111

acct.220 41

Appendix C

• You are responsible for pages C1-C14

End of Appendix C• Good Bye and Good Luck!