Embed Size (px)

Citation preview

CONDUCTING EFFECTIVE LISTER GRIEVANCES AND

PROPERTY TAX ASSESSMENT APPEALS

TUESDAY, APRIL 5, 2011

HOTEL COOLIDGE, WHITE RIVER JUNCTION, VT

OR

THURSDAY, APRIL 7, 2011

MIDDLEBURY INN, MIDDLEBURY, VT

Agenda(s)

12:30 Registration

1:00 Overview of the Appeal Process

This introductory session will provide an overview of the property tax assessment appeal

process from local lister grievances through Vermont Supreme Court decisions. We will

discuss the importance of managing the process to comply with statutory requirements, avoid

surprises, and minimize appeals.

1:30 Conducting Effective Lister Grievances

In this session, we will examine the lister grievance process in detail, from change of appraisal

notices through grievance decisions. We will review deadlines and discuss the role of

contracted professional appraisers in grievances. Particular attention will be paid to strategic

management of the grievance process through use of public informational meetings, press

releases, and other public education efforts.

2:45 Break

3:00 Conducting Effective BCA Hearings

This session will focus on the legal and practical considerations for conducting BCA hearings,

including compliance with statutory timelines and protection of due process rights, the

presumption of validity and the burden of persuasion, the responsibilities of the inspection

committee, effective management of evidence, and best practices throughout the hearing

process.

4:45 Conclusion and Safe Trip Home

CONDUCTING EFFECTIVE LISTER GRIEVANCES AND

PROPERTY TAX ASSESSMENT APPEALS

TUESDAY, APRIL 5, 2011

HOTEL COOLIDGE, WHITE RIVER JUNCTION, VT

OR

THURSDAY, APRIL 7, 2011

MIDDLEBURY INN, MIDDLEBURY, VT

About The Speaker

Jim Barlow joined the Vermont League of Cities and Towns (VLCT) staff as Staff Attorney in theMunicipal Assistance Center (MAC) in 2004. Jim is a 1998 graduate of the University of DenverCollege of Law. He regularly teaches, writes, and advises Vermont officials on various municipal topics.Previously, Jim was in private practice with the law firm of Jacobs McClintock and Scanlon, inBennington. There he counseled clients on a variety of laws, including those on contracts, employment,land use planning, and health. He also served as moderator for the Southwest Vermont RegionalTechnical School District. Now a Senior Staff Attorney, Jim lives in Marshfield with his wife Jenniferand sons Robert, William, and Wesley.

3/24/2011

1

2011Conducting

EffectiveProperty TaxAssessment

AppealsJim Barlow, Senior Staff Attorney

VLCT Municipal Assistance Center

Agenda

Overview of the Property Tax Assessment Appeal Process• Goals for the Listers and BCA• What to expect

Lister Grievances• Filing the preliminary grand list and sending change of appraisal notices• Public informational meeting• Conducting grievances• Attitude• Role of the contracted appraiser

BCA Appeals• Organizational meeting• Open meeting law requirements and exceptions• Due process – notice and a fair hearing• Site inspections• Decisions• Unusual appeals

3/24/2011

2

Overview of the PropertyTax Assessment Appeal

Process

Overview of the Property TaxAssessment Appeal Process

Each year Listers prepare and lodge a grandlist that contains all taxable property in thetown.

3/24/2011

3

Overview of the Property TaxAssessment Appeal Process

Listers are directed by law to appraiseproperty at 100 percent of fair market value.

Overview of the Property TaxAssessment Appeal Process

If the town’s common level of appraisal (CLA)drops below 80% or the coefficient of dispersal(COD) is greater than 20%, the town willreceive an appraisal order from the state.

If the town fails to carry out a plan forreappraisal, the state can withhold education,transportation, and other funds.

3/24/2011

4

Overview of the Property TaxAssessment Appeal Process

The appeal process begins whenthe Listers file a preliminarygrand list and notify taxpayersof changes in their propertyvalues.

Overview of the Property TaxAssessment Appeal Process

Dissatisfied taxpayers “grieve” theirassessment to the Listers.

3/24/2011

5

Overview of the Property TaxAssessment Appeal Process

Taxpayers can appeal Lister grievancedecisions to the Board of CivilAuthority.

Overview of the Property TaxAssessment Appeal Process

The Board of Civil Authority holds appealhearings, inspects each property and issuesa written decision.

3/24/2011

6

Overview of the Property TaxAssessment Appeal Process

Taxpayers can appeal the BCA’s decision tothe Director of Property Valuation andReview (the State Appraiser) or SuperiorCourt.

Overview of the Property TaxAssessment Appeal Process

The appeals heard by the State Appraiserand Superior Court are de novo!

3/24/2011

7

Overview of the Property TaxAssessment Appeal Process

State Appraiser and Superior Courtdecisions may be appealed to VermontSupreme Court.

Overview of the Property TaxAssessment Appeal Process

Appeals to the Vermont Supreme Courtare generally limited to questions of law.

3/24/2011

8

Overview of the Property TaxAssessment Appeal Process

As taxpayers move through the process thelevel of formality and complexity increases.

Overview of the Property TaxAssessment Appeal Process

Although there are statutory requirementsfor Lister grievances that must be followed,they tend to be conducted informally.

Grievances are a first-chance opportunity tocorrect obvious problems, errors and issues.

3/24/2011

9

Overview of the Property TaxAssessment Appeal Process

BCA hearings are a quasi-judicial process, akin to alocal tax appeal court.

• Taxpayers and Listers present evidence to theBCA.

• Each property is inspected by a committee.

• The BCA considers the evidence presented andmakes a written decision based on that evidence.

Goals for the Listers and theBoard of Civil Authority in the

Appeal Process

1. Make sure that each property subject to appeal hasbeen listed at the correct value.

2. Comply with statutory requirements for holdingLister grievances and BCA appeals.

3. Think strategically and manage the processeffectively.

4. Minimize subsequent appeals by treating peoplefairly professionally.

3/24/2011

10

You cannot make everyone happy buttaxpayers who feel that they have beentreated fairly and professionally are lesslikely to appeal even when the decisiondoes not turn out their way.

Remember:

What to Expect

Wilmington, Vermont 3,248 Parcels

2009 - Town Wide Reappraisal

• Grievances: 667 (20% of total parcels)

• BCA Appeal 135 (20% of grievances)

• Superior Court 1

• State Appraiser: 15 (12% of BCA Appeals)

2010

• Grievances: 55 (2% of total parcels)

• BCA Appeals 14 (25% of grievances)

• Superior Court 1 (7% of BCA appeals)

• State Appraiser 0

3/24/2011

11

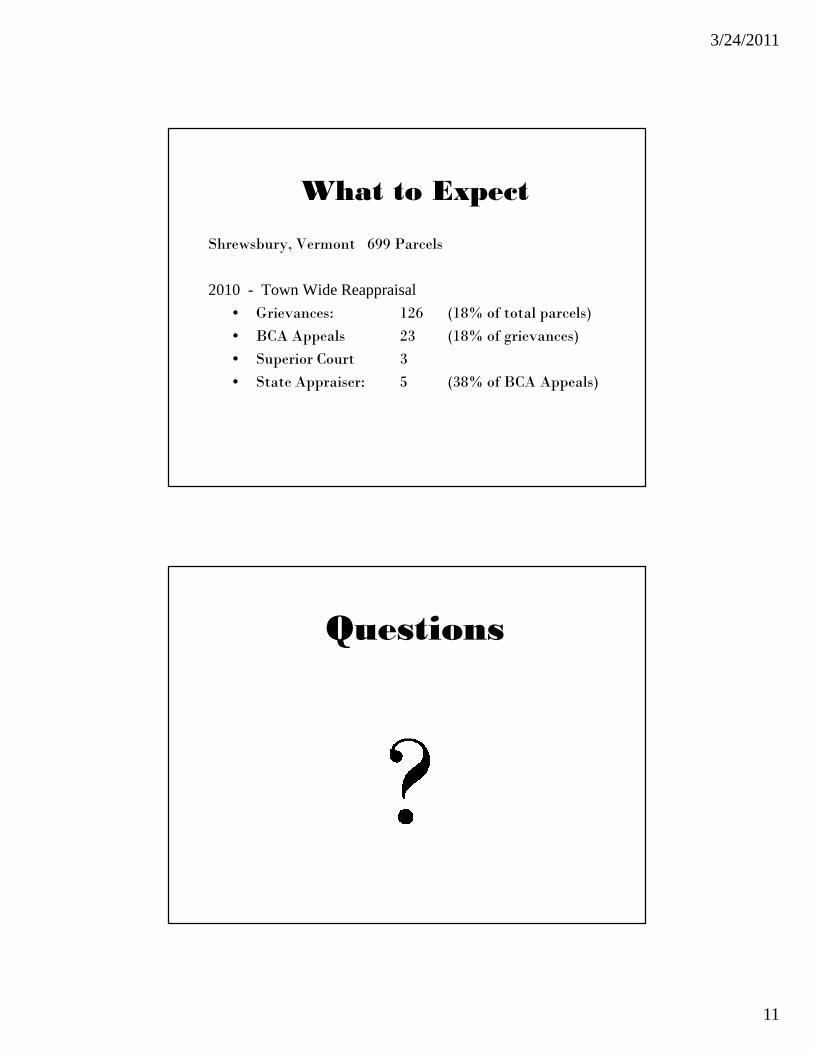

What to Expect

Shrewsbury, Vermont 699 Parcels

2010 - Town Wide Reappraisal

• Grievances: 126 (18% of total parcels)

• BCA Appeals 23 (18% of grievances)

• Superior Court 3

• State Appraiser: 5 (38% of BCA Appeals)

Questions

3/24/2011

12

Lister Grievances

Lister Grievances

By June 4, or June 24, the Listers “lodgethe abstract of individual lists” with theTown Clerk. 32 V.S.A. 4111(a).

This is also know as filing the preliminarygrand list.

3/24/2011

13

Lister Grievances

At the time the abstract is filed, the Listers mustpost notice in the Town Clerk’s office and four otherpublic places in town stating:

• That the Listers have completed and lodged thegrand list.

• The time, date and place of the Lister grievancemeeting.

32 V.S.A. 4111(e)

Lister Grievances

The Listers must also give written notice toproperty owners whose appraised value orhomestead value has changed. 32 V.S.A.4111(e)

These are know as change of appraisalnotices.

3/24/2011

14

Lister Grievances

The change of appraisal notices must include:

• Any change in appraised value or the changein the allocation of value to homestead orhousesite.

• The amount of the change.

• The time, date and place of the Listergrievance meeting.

32 V.S.A. 4111(e)

Lister GrievancesChange of appraisal notices must be sent at least14 days prior to the date fixed for listergrievances.

Change of appraisal notices must be sent byregistered or certified mail, or certificate ofmailing to the last known address of the owner.

If the change in appraisal notice is not sent by oneof these methods and a dispute arises, the law willpresume that the notice was not sent. 32 V.S.A.4111(e)

3/24/2011

15

Lister Grievances

Tip: Use certificate of mailing. It costs $1.15 perarticle.

For more information on certificate of mailing, go to:

www.usps.com/send/waystosendmail/extraservices/certificateofmailingservice.htm

The point at which change ofappraisal notices are sent is a criticalpoint in management of the appealprocess.

Lister Grievances

3/24/2011

16

Surprise!You Are in the News

Tip No. 1Managing the Process

Hold a pre-grievance public informationalmeeting.

• Explain why a town-wide reappraisal wasconducted.

• Outline the reappraisal process and how areproperty values are determined.

• Acknowledge that some appraisals may beincorrect.

3/24/2011

17

Tip No. 1Managing the Process

Hold a pre-grievance public informational meeting.

• Explain the appeal process and what is requiredfrom taxpayers at each step. Explain wheretaxpayers can get information on propertyvalues (lister cards, etc.).

• Include notice of this informational meeting inthe change of appraisal notice. Publish it thenewspaper. Encourage everyone who hasreceived a change of appraisal notice to attend.

Tip No. 1Managing the Process

Hold a pre-grievance public informational meeting.

Make more information available for attendees:

A Handbook on Property Tax AssessmentAppeals, Vermont Secretary of State andVermont Department of Taxes, 2009.

Are You Appealing, Vermont Institute forGovernment, 1999.

3/24/2011

18

Lister Grievances

Taxpayers initiate the grievance process by filingtheir “objections” with the Listers in writing “onor before the day of the grievance meeting.” 32V.S.A. 4111, 4222

The bar to enter the process is very low. Writtennotes of the Chair of the Listers suffice to qualifyas “objections in writing.” Gionet v. Town ofGoshen, 152 Vt. 451, 456 (1989).

Lister Grievances

“Taxpayers who wish to grieve must get a written notice ofappeal to the board of listers on or before the grievancedate stated in the change of appraisal notice. Anygrievance notice received after that day – even if receivedwhile the listers are hearing grievances due to continuances– does not meet the requirement of being filed “at or priorto the time fixed for hearing appeals,” 32 V.S.A. §4222, isuntimely and should not be heard.

A Handbook on Property Tax Assessment Appeals, 2009Edition, page 13.

3/24/2011

19

Lister Grievances

In my opinion, any written objection filed with the listers beforethe conclusion of all the grievance hearings should be acceptedand the taxpayer afforded the opportunity to grieve.

Thirty two V.S.A. 4221 specifies that the listers “shall meet atthe place so designated by them and on that day and from day today thereafter shall hear persons aggrieved by their appraisals.”

See Murdoch v. Town of Shelburne, 2007 VT 93 (“[T]heLegislature apparently intended to require listers to correct errorsand omissions in the abstract as long as the abstract remainsopen.”)

Lister Grievances

Vermont’s Open Meeting Law applies to Listergrievances. Grievances must be open to the publicand minutes must be taken. 1V.S.A. 312

The Listers can use private deliberative session atthe end of the fact-finding portion of the grievanceto reach their decision. 1V.S.A. 312(f)

Deliberative session does not require public noticeor minutes. The public may be excluded.

1V.S.A. 312(e)

3/24/2011

20

Lister Grievances

The primary purpose of Lister grievances isto discover any errors or omissions in theabstract of individual lists.

Errors may include valuation, acreage,condition, ownership, etc.

Lister Grievances

All three Listers should participate whenholding grievances.

At least two Listers must be present and atleast two Listers must agree in order changean appraisal. 1 V.S.A. 172

3/24/2011

21

Lister Grievances

If a taxpayer files a written grievancerequest, the Listers must make adetermination even if the taxpayer does notappear at the grievance hearing.

A taxpayer may be represented by anattorney or other person. 32 V.S.A. 4222

Lister Grievances

Listers’ grievance decision must be in writing, sent byregistered or certified mail or certificate of mailing.

If the decision is not sent by one of these methods and adispute arises, the law will presume that it was not sent. 32V.S.A. 4224.

The decision must also inform the taxpayer of the right toappeal the decision to the Board of Civil Authority bylodging an appeal with the Town Clerk within 14 days ofthe mailing on the notice. 32 V.S.A. 4224.

3/24/2011

22

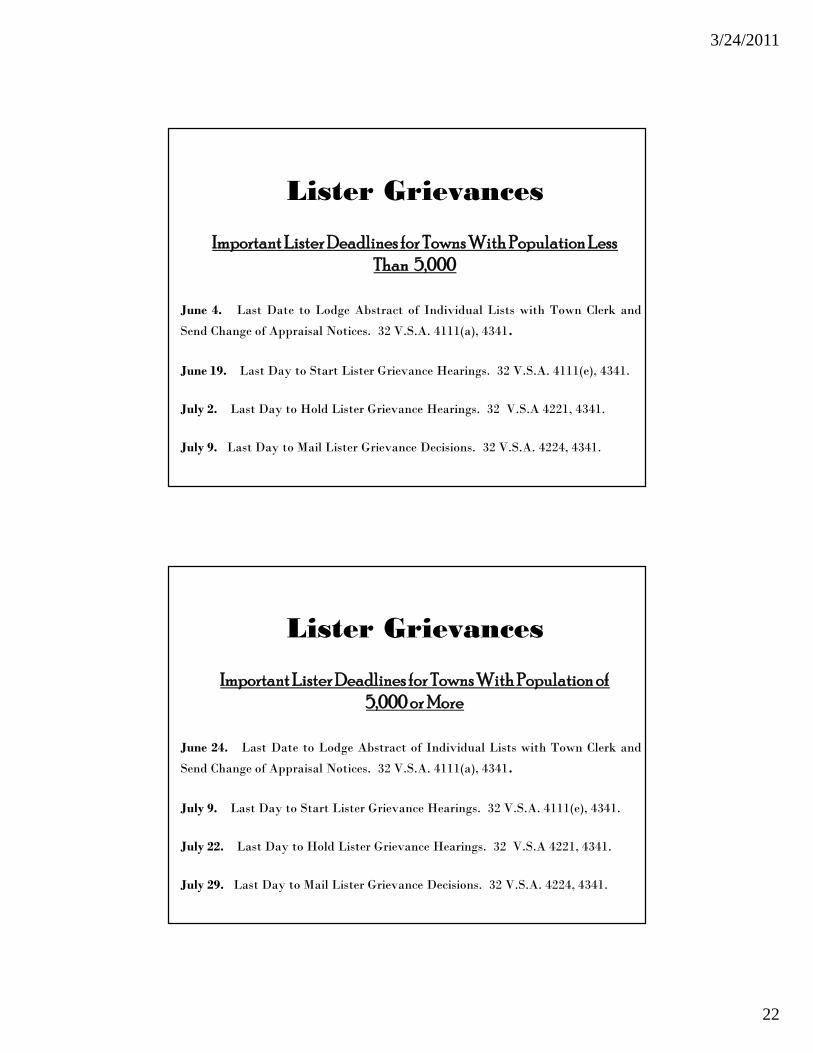

Lister Grievances

June 4. Last Date to Lodge Abstract of Individual Lists with Town Clerk and

Send Change of Appraisal Notices. 32 V.S.A. 4111(a), 4341.

June 19. Last Day to Start Lister Grievance Hearings. 32 V.S.A. 4111(e), 4341.

July 2. Last Day to Hold Lister Grievance Hearings. 32 V.S.A 4221, 4341.

July 9. Last Day to Mail Lister Grievance Decisions. 32 V.S.A. 4224, 4341.

Important Lister Deadlines for Towns With Population LessThan 5,000

Lister Grievances

June 24. Last Date to Lodge Abstract of Individual Lists with Town Clerk and

Send Change of Appraisal Notices. 32 V.S.A. 4111(a), 4341.

July 9. Last Day to Start Lister Grievance Hearings. 32 V.S.A. 4111(e), 4341.

July 22. Last Day to Hold Lister Grievance Hearings. 32 V.S.A 4221, 4341.

July 29. Last Day to Mail Lister Grievance Decisions. 32 V.S.A. 4224, 4341.

Important Lister Deadlines for Towns With Population of5,000 or More

3/24/2011

23

Lister Grievances

Under these statutes, there are only 14 days forListers to hear all grievances and 7 days to mail allgrievance decisions.

If the Listers cannot comply with these deadlines,the Listers and Selectboard can request extensionsfrom the Director of Property Valuation andReview. 32 V.S.A. 4342.

Tip No. 2Positive Attitude

Listers should maintain an open and receptive attitudeduring grievances.

Typically 15-20% of taxpayers receiving a change ofappraisal notice will grieve to the Listers andapproximately 15-20% of grievants will appeal to theBCA.

The likelihood that a taxpayer will appeal to the BCAcorresponds to the taxpayer’s perception of the grievanceprocess.

3/24/2011

24

Tip No. 2Positive Attitude

Listers should maintain an open and receptive attitudeduring grievances.

Many taxpayers will not appeal beyond grievance if theyperceive that appraisals were made fairly and that theywere treated respectfully by the Listers.

On the other hand, if taxpayers perceive that theirappraisals are arbitrary or that the Listers are undulydefensive, they are more likely to appeal.

Tip No. 2Positive Attitude

Listers should maintain an open and receptive attitudeduring grievances.

• Listen to the taxpayer.

• Explain what the law requires of you and explainhow you arrived at their appraisal.

• Be courteous!

• Accept that you will not be able to please everyone.

3/24/2011

25

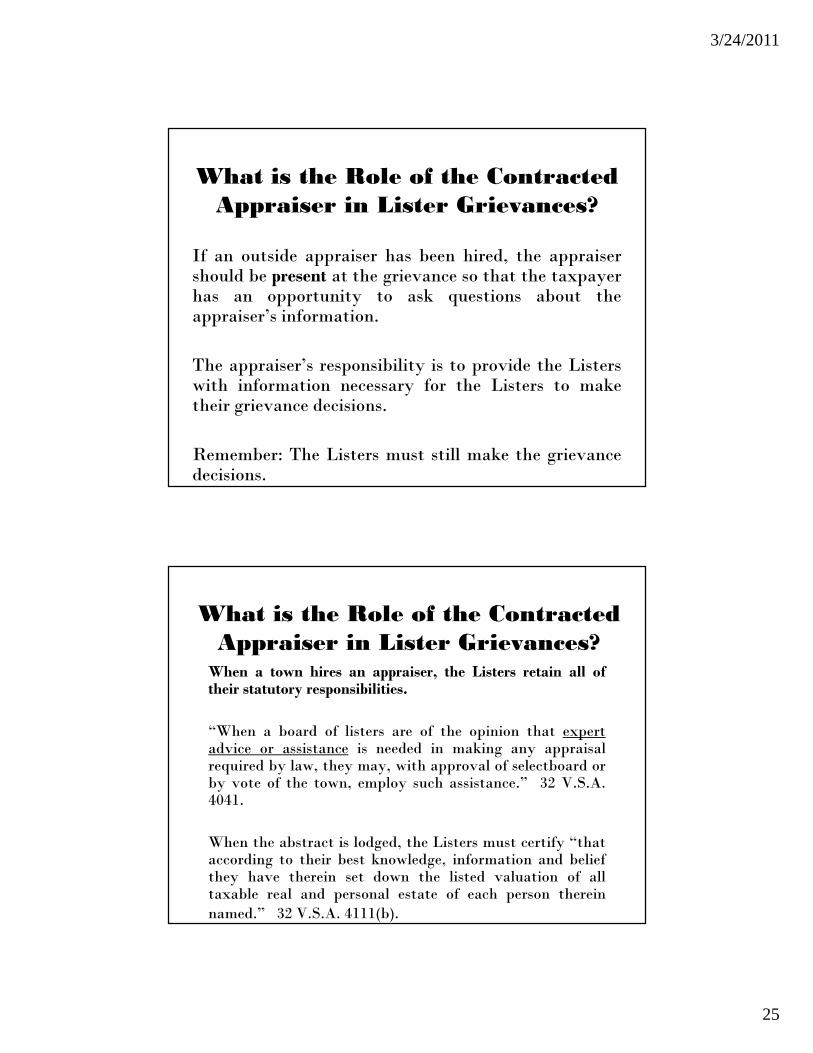

What is the Role of the ContractedAppraiser in Lister Grievances?

If an outside appraiser has been hired, the appraisershould be present at the grievance so that the taxpayerhas an opportunity to ask questions about theappraiser’s information.

The appraiser’s responsibility is to provide the Listerswith information necessary for the Listers to maketheir grievance decisions.

Remember: The Listers must still make the grievancedecisions.

What is the Role of the ContractedAppraiser in Lister Grievances?

When a town hires an appraiser, the Listers retain all oftheir statutory responsibilities.

“When a board of listers are of the opinion that expertadvice or assistance is needed in making any appraisalrequired by law, they may, with approval of selectboard orby vote of the town, employ such assistance.” 32 V.S.A.4041.

When the abstract is lodged, the Listers must certify “thataccording to their best knowledge, information and beliefthey have therein set down the listed valuation of alltaxable real and personal estate of each person thereinnamed.” 32 V.S.A. 4111(b).

3/24/2011

26

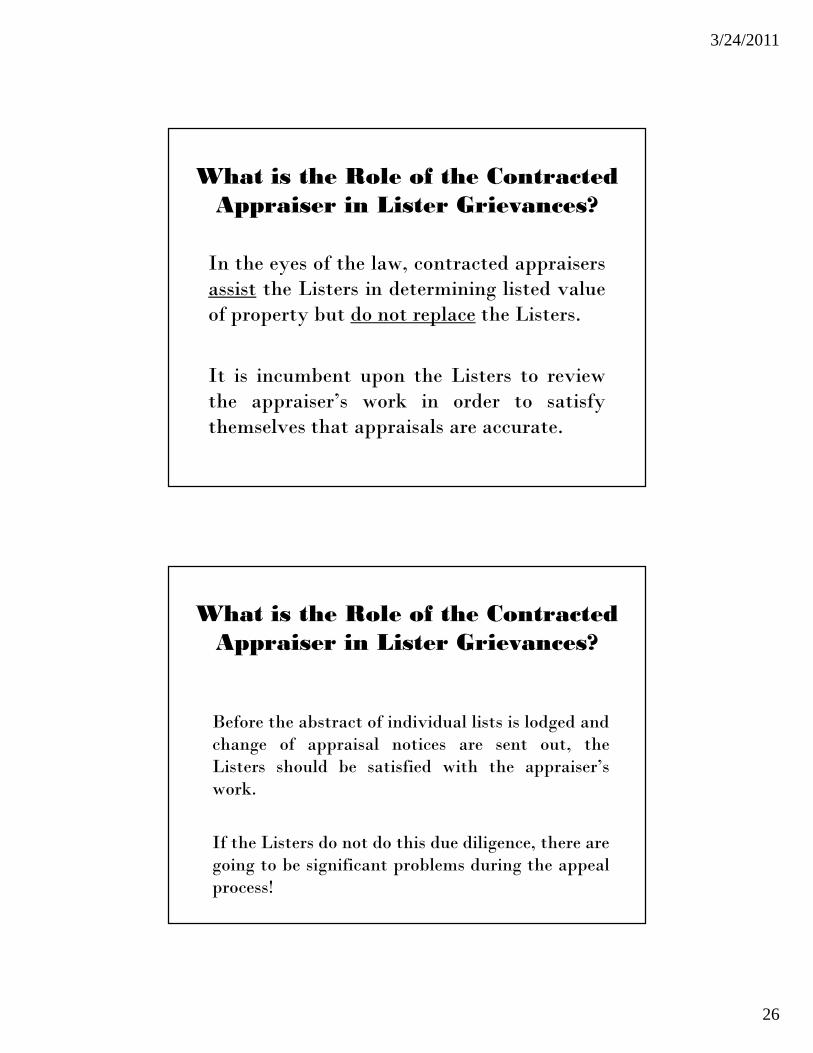

What is the Role of the ContractedAppraiser in Lister Grievances?

In the eyes of the law, contracted appraisersassist the Listers in determining listed valueof property but do not replace the Listers.

It is incumbent upon the Listers to reviewthe appraiser’s work in order to satisfythemselves that appraisals are accurate.

What is the Role of the ContractedAppraiser in Lister Grievances?

Before the abstract of individual lists is lodged andchange of appraisal notices are sent out, theListers should be satisfied with the appraiser’swork.

If the Listers do not do this due diligence, there aregoing to be significant problems during the appealprocess!

3/24/2011

27

Questions

Appeals to the Board of CivilAuthority

3/24/2011

28

Appeals to the Board of CivilAuthority

A taxpayer not satisfied with the Listers’grievance decision must file a written notice ofappeal with the Town Clerk within 14 days. Thenotice of appeal must briefly state the grounds forthe appeal. 32 V.S.A. 4404(a).

BCA hearings must begin no later than 14 daysafter the last date allowed for filing a notice ofappeal with BCA. 32 V.S.A. § 4404(b).

Tip No 3Hold an Organizational

Meeting ASAP

Before hearings begin, the BCA should holdan organizational meeting to elect a chair,adopt rules of procedure, set up a hearingschedule, etc.

3/24/2011

29

Who Is the Board ofCivil Authority?

BCA = The Selectboard + Justices of thePeace + Town Clerk. 24 V.S.A. 801

BCA must choose a chair. 24 V.S.A. 801

Town clerk is BCA clerk. 24 V.S.A. 801

What Does the BCA Do?

BCA holds quasi-judicial hearings onappeals of Lister grievance decisions. 32V.S.A. Chapter 131

3/24/2011

30

What Is a Quasi-JudicialHearing?

A matter in which the legal rights of one ormore persons are adjudicated, which isconducted in such a way that all parties havethe opportunity to present evidence and crossexamine witnesses, which results in a writtendecision, and the result of which is appealable bya party to a higher authority. 1 V.S.A.310(5)(B).

Open Meeting LawHow Does it Apply to the BCA?

BCA, Board of Abatement, Selectboard - allpublic bodies subject to the Open MeetingLaw.

Whenever these boards “meet” the OpenMeeting Law applies. 1V.S.A. § 312.

3/24/2011

31

Open Meeting LawRequirements for the BCA

• Meetings must be open to public, but thepublic does not have the right to comment orparticipate. 1 V.S.A. 312(a), (h).

• Minutes must be taken. 1 V.S.A. 312(b)(1).

• Meetings must be publicly warned. 1 V.S.A.312(c).

Three Open Meeting LawExceptions for the BCA

• One always applies.

• One almost never applies.

• One can apply if you want it to.

3/24/2011

32

Site Inspection ExceptionAlways Applies

Site inspections are specifically exemptedfrom the Open Meeting Law.

1 V.S.A. § 312(g)

Executive Session ExceptionAlmost Never Applies

In certain instances, public bodies can meet inprivate executive session.

These instances are defined by statute and include,among other things, contracts, real estate options,evaluation of employees. 1 V.S.A. § 313.

Almost never used by BCA.

3/24/2011

33

Deliberation Exception Can ApplyIf The BCA Chooses

The open meeting law does not apply todeliberations. 1 V.S.A. § 312(e).

Weighing and examining evidence, discussing thereasons for and against a decision. Expresslyexcludes the taking of evidence and the argumentsof the parties. 1 V.S.A. § 310(1).

A BCA can deliberate in private if it chooses.

Why Use DeliberativeSession?

• More frank and open discussion.

• Does not have to be warned.

• Does not require minutes.

• More convenient.

• Judges and juries do their deliberative work inprivate.

• Almost every BCA uses deliberative session.

3/24/2011

34

Questions

The Guiding Principle ForBCA Hearings

Afford the taxpayer due process.

3/24/2011

35

Due Process:A Constitutionally Protected

Right

Fourteenth Amendment to U.S.Constitution provides that no state maydeprive any person of life, liberty or

property, without due process of law.

The Essence of Due Process

Primary requirements of dueprocess are providing the taxpayer

notice and a fair hearing.

3/24/2011

36

Due Process: Notice

The town clerk calls a meeting of the BCA.

Notice of the meeting is posted in three ormore public places in town. A copy of thenotice is mailed to each member of the BCA,the town agent, the chair of the board oflisters, and to all persons so appealing. 32V.S.A 4404(b).

Due Process: FairHearing

Three components to a fair hearing:

• Maintaining order.

• Managing evidence.

• Managing conflicts of interest, ex parte

communication, and bias.

3/24/2011

37

Tip No. 5 KeepingOrder

The BCA must adopt rules of procedure.

Rules of procedure will help you mange yourhearings.

They can be used as a script to help you throughthe first few hearings.

See model rules in handout.

Fair Hearing: KeepingOrder

One of BCA’s goals should be to minimize appealsto Superior Court and/or State Appraiser.

The greater the taxpayer’s perception of order andfairness, the less likely the taxpayer is to appeal.

Make copies of your rules of procedure available totaxpayers.

3/24/2011

38

Fair Hearing: ManagingEvidence

Two basic types of evidence received by the BCA:documents and oral testimony.

Fair Hearing: ManagingEvidence

For Documentary Evidence:

• Mark each document.

• Include basic information such as:

1. Appellant’s Exhibit No.

2. Lister’s Exhibit No.

3. Name or Number of Appeal

• Keep it organized.

3/24/2011

39

Fair Hearing: ManagingEvidence

For Oral Testimony:

• Tape record proceedings.

• Keep proceedings orderly (follow your rules).

• Keep the discussion relevant.

Fair Hearing: ManagingEvidence

What is “relevant” evidence?

• Comparables, market studies,condition of property, etc.

• Evidence that will help establish thefair market value of the property.

3/24/2011

40

Fair Hearing: ManagingEvidence

What is irrelevant evidence?

• Appellant’s ability to pay.

• Why it is unfair that appellant’s taxes aregoing to increase.

Remember the board of abatement.

Managing Evidence: TheBalancing Act

BCA must balance expediency againstinclusion.

Taxpayers who feel they have been heardare less likely to appeal.

Err on the side of listening - just becauseyou listened to it doesn’t mean that youhave to consider it.

3/24/2011

41

Fair Hearing: ManagingConflicts of Interest

In smaller towns conflicts are morefrequent.

Due process requires recusal if a boardmember is conflicted.

Fair Hearing: ManagingConflicts of Interest

BCA member should recuse herself fromappeal that involves a relative within thefourth degree of consanguinity.

Relative by blood or marriage who is firstcousin, niece, nephew, aunt, uncle,grandparent, parent, sibling, child, spouse.12 V.S.A. § 61.

3/24/2011

42

Fair Hearing:Disqualification From the BCA For

ALL Tax Appeals

Listers and town agents cannot serve on BCA. 32V.S.A. § 4404 (d)

A selectboard member, JP or town clerk thatappeals to the BCA or his servant, agent orattorney, cannot serve on BCA for any tax appealhearing. 32 V.S.A. § 4404 (d)

If you grieve to the listers and decided not toappeal to BCA, you may serve on the BCA.

Fair Hearing:Managing Ex Parte Communication

Ex parte communication is any communicationbetween a BCA member and a party regarding anappeal.

Inappropriate – should only take place at openhearing

Disclose ex parte communication to the BCA andremind the persistent taxpayer of your duty todisclose.

3/24/2011

43

Fair Hearing:Quorum Requirements

Any number of board members (but neverless than the three needed for siteinspection) that attend a hearing can takeaction and make decision. 24 V.S.A. § 801.

Only those members that participated in thehearing should be involved in the decision.

Questions

3/24/2011

44

Site VisitInspection Committee

RequirementsEach property must be inspected. 32 V.S.A. § 4404(c) .

The inspection committee must be comprised of atleast three BCA members. 32 V.S.A. § 4404(c).

The inspection committee must report to the BCAwithin 30 days from the hearing. 32 V.S.A. 4404(c).

Site VisitInspection Committee

Requirements

All inspection committee members mustview the property, but are not required todo so at the same time.

Remember, site inspection is not subjectto the Open Meeting Law.

3/24/2011

45

Site VisitInspection Committee Best

Practices

Get started right away (remember the 30day deadline and the lesson of Town ofGeorgia).

Be firm about setting time for inspection(failure to allow inspection = deemedwithdrawal).

Site VisitInspection Committee Best

Practices

Give notice to the Listers so they cancome too.

Issue a written site visit report, but leaveout the written recommendation.

3/24/2011

46

Site VisitFrequently Asked QuestionsIs the site visit a fact-finding or a fact-checking mission?

Probably some of both. Remember, the BCA mayincrease, reduce, or sustain an appraisal made by thelisters. 32 V.S.A. § 4409.

Can the inspection committee request to see other parts ofthe property not addressed at the hearing?

Yes, and it should.

What if the request is refused?

Remember, inspection includes “interior andexterior of any structure on the property.” Youmay have to exercise some discretion.

Site VisitFrequently Asked Questions

Is it better to conclude the hearing and conduct the site visit(with no opportunity for further comment or testimony)

OR

Recess the hearing to a date and time certain, conduct the sitevisit, and then reconvene the hearing to receive additionalcomment or evidence on the inspection committee report.

• It has been done both ways.

•The second is the preferred method.

3/24/2011

47

Site VisitEx Parte Communication

Ex parte discussions at siteinspections are inevitable butinappropriate.

Be polite yet firm, patient yetpersistent.

QUESTIONS

3/24/2011

48

Making The Decision

The Listers’ assessment enjoys a presumption ofvalidity.

The taxpayer’s job is to convince the BCA that theListers were wrong.

Remember – BCA never has to prove anything –simply hear evidence presented and make a

decision.

Making The Decision:The Duty To Be Convinced

Become familiar with common real estateappraisal methods: cost approach, salescomparison approach, income approach.

Review Handbook on Property TaxAssessment Appeals

3/24/2011

49

Making The Decision:The Duty To Be Convinced

Taxpayer always has burden topersuade BCA that appraisal exceedsfair market value. Kruse v. Town ofWestford, 145 Vt. 368 (1985).

This burden never shifts from thetaxpayer.

Making the Decision:The Duty To Be Convinced

Bottom Line: Taxpayer’s evidencemust outweigh Lister’s evidence to winappeal.

Preponderance ofPreponderance ofEvidence StandardEvidence Standard

3/24/2011

50

Questions

Issuing The WrittenDecision

Decision MUST be in writing.

BCA may increase, reduce, or sustain anappraisal made by the Listers. 32 V.S.A. §4409.

3/24/2011

51

Issuing the WrittenDecision

Decision must be more than merely a "barestatement of result, without stated reasons," thatdo not "meet the underlying purpose of indicatingto the parties, and to an appellate court, what wasdecided and upon what considerations." Hojaboomv. Town of Swanton, 141 Vt. 43 (1982)

Use PVR Form 4404A available at:http://www.state.vt.us/tax/pdf.word.excel/forms/pvr/4404a.doc

Making the Decision:Issuing the Written

Decision

Boards need not be perfect.

Reasoning must simply be “withinthe range of rationality” tocomport with the law.

3/24/2011

52

Issuing The WrittenDecision

The BCA must issue its decision, with reasons,within 15 days of the report of the inspectioncommittee. 32 V.S.A. § 4404 (c).

Remedies For Failure to

Follow Timelines

If the BCA does not substantially comply withtimelines, appellants’ value for that year will bereset to prior year’s value. 32 V.S.A. Sec. 4404(c).

Complete reappraisal - Court can set appellant’svalue to a value that will produce a tax liabilityequal to the preceding year. 32 V.S.A. Sec.4404(c).

3/24/2011

53

Questions

What is the Role of TheContracted Appraiser in BCA

Appeals?

To provide assistance to the Listers insupporting their appraisal before the BCA.

3/24/2011

54

What is the Role of theTown Clerk?

The town clerk is a member of the BCA. 24V.S.A. § 801.

By statute, the town clerk must serve as theclerk of the BCA. 24 V.S.A. § 801.

What is the Role of theTown Clerk?

Upon receipt of written notice of an appeal, the Town Clerkcalls meeting of the BCA. 32 V.S.A. 4404(a).

The Town Clerk posts notice of the hearings in three or morepublic places within the town at least five days prior to themeeting and mails a copy of the notice to each member ofthe BCA, the Town Agent and the Chair of the Board ofListers. 32 V.S.A. § 4404(b); 24 V.S.A. § 801.

Before the members of the BCA begin to hear tax appeals,they must take, sign and file an oath with the Town Clerk.32 V.S.A. § 4405.

3/24/2011

55

What is the Role of theTown Clerk?

The Town Clerk typically takes the minutes of BCAmeetings, schedules hearings, and manages evidence.

When BCA issues decision, the Town Clerk records thedecision and notifies the taxpayer of the decision inwriting by certified mail. 24 V.S.A. § 4404(c).

Maintains institutional knowledge of how the townconducts tax appeals.

What is the Role of theTown Clerk?

The Town Clerk is a full voting member of the BCA,participates in hearings, site visits and decision making.

Town clerk accepts service of notice of appeal of the BCAdecision and forwards a copy of the notice to the stateappraiser or the superior court. 32 V.SA. § 4461.

When the appeal process is done, the board or court issuingthe final decision on appeal files a certified copy of thatdecision with the town clerk for recording in the grand listbook. 32 V.S.A. § 4468.

3/24/2011

56

After The BCA –Unusual Appeals

Selectboard can appeal BCA decision.32 V.S.A. 4461(a).

Taxpayers whose combined grand listexceeds 3% of town grand list maypetition the town agent to appeal toSuperior Court. 32 V.S.A. 4461(b).

Closing Thoughts

Gathering and providing evidence on fair marketvalue is the job of the listers and the appellant.

BCA need not be experts in real estate appraisal,but should be familiar with real estate appraisalmethods.

Focus on an impartial, effective, and efficientprocess.

You can do this.

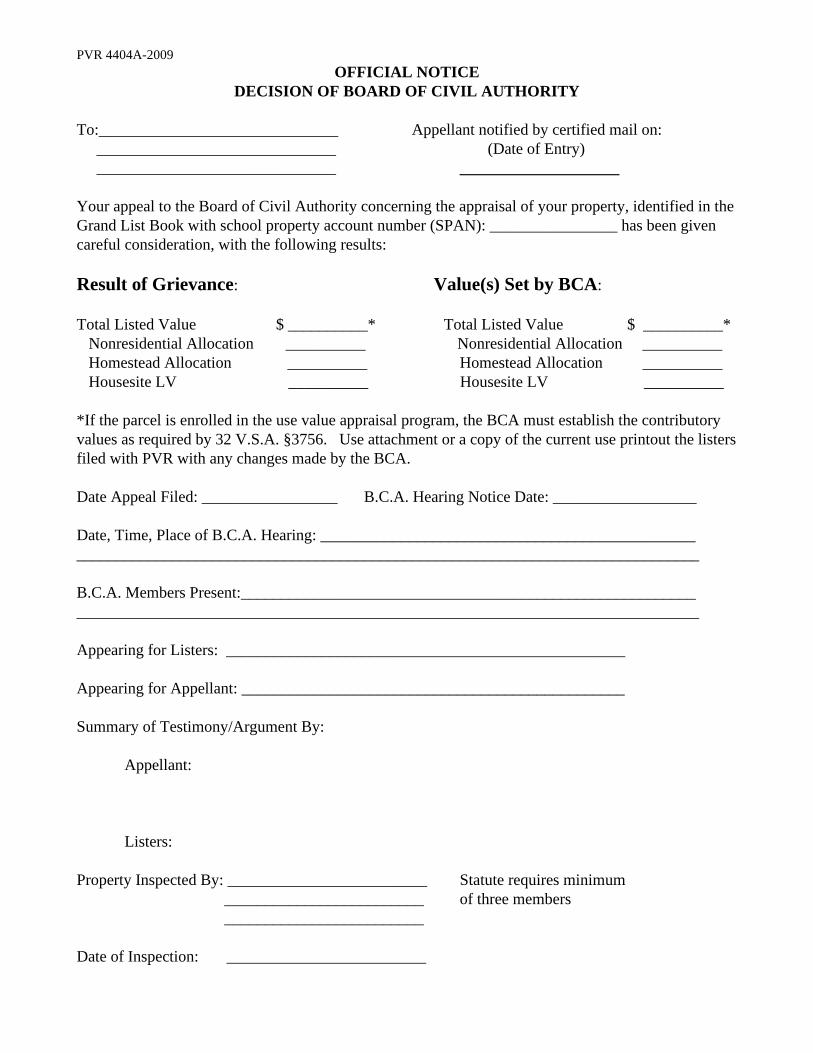

PVR 4404A-2009

OFFICIAL NOTICE

DECISION OF BOARD OF CIVIL AUTHORITY

To:______________________________ Appellant notified by certified mail on:

______________________________ (Date of Entry)

______________________________ ____________________

Your appeal to the Board of Civil Authority concerning the appraisal of your property, identified in the

Grand List Book with school property account number (SPAN): ________________ has been given

careful consideration, with the following results:

Result of Grievance: Value(s) Set by BCA:

Total Listed Value $ __________* Total Listed Value $ __________*

Nonresidential Allocation __________ Nonresidential Allocation __________

Homestead Allocation __________ Homestead Allocation __________

Housesite LV __________ Housesite LV __________

*If the parcel is enrolled in the use value appraisal program, the BCA must establish the contributory

values as required by 32 V.S.A. §3756. Use attachment or a copy of the current use printout the listers

filed with PVR with any changes made by the BCA.

Date Appeal Filed: _________________ B.C.A. Hearing Notice Date: __________________

Date, Time, Place of B.C.A. Hearing: _______________________________________________

______________________________________________________________________________

B.C.A. Members Present:_________________________________________________________

______________________________________________________________________________

Appearing for Listers: __________________________________________________

Appearing for Appellant: ________________________________________________

Summary of Testimony/Argument By:

Appellant:

Listers:

Property Inspected By: _________________________ Statute requires minimum

_________________________ of three members

_________________________

Date of Inspection: _________________________

PVR 4404A-2009

Report of Inspection Committee: (Use attachment if necessary)

Board’s Decision with Reasons: (Use attachment if necessary)

Certificate: I hereby certify that this is a true record of the action taken on this appeal by the

Board of Civil Authority of the town/city.

_____________________________,Chairman

Board of Civil Authority

Filed in the town/city clerk’s office on ______________, _____ at ____m.

to be recorded in the Grand List Book of April 1, _____(year).

Attest: ____________________________

Town/City Clerk

Pursuant to Title 32, V.S.A., section 4461, if you are aggrieved by this decision you may appeal either

to the Director of the Division of Property Valuation and Review or to the Superior Court of the county

in which the property is situated. The appeal to either the director or the superior court is governed

by Rule 74 of the Vermont Rules of Civil Procedure and is commenced by filing a notice of appeal

with the town clerk within 30 days of the day this decision was mailed to you by the town clerk

(date of entry noted on reverse). The town clerk transmits a copy of the notice to the director or to

the superior court as indicated in the notice and shall record or attach a copy of the notice in the

grand list book.

Be sure your appeal indicates which avenue of appeal you wish to pursue (court or director), clearly

identifies the property under appeal, and is accompanied by the correct filing fee. The appeal to the

Superior Court shall be accompanied by a $250 fee for each parcel being appealed; the fee is $70 per

parcel on appeal to the Director. If the property under appeal is enrolled in the use value appraisal

program, please indicate that in your appeal. If the property under appeal contains a homestead,

please include that information.

PVR 4404A-2009

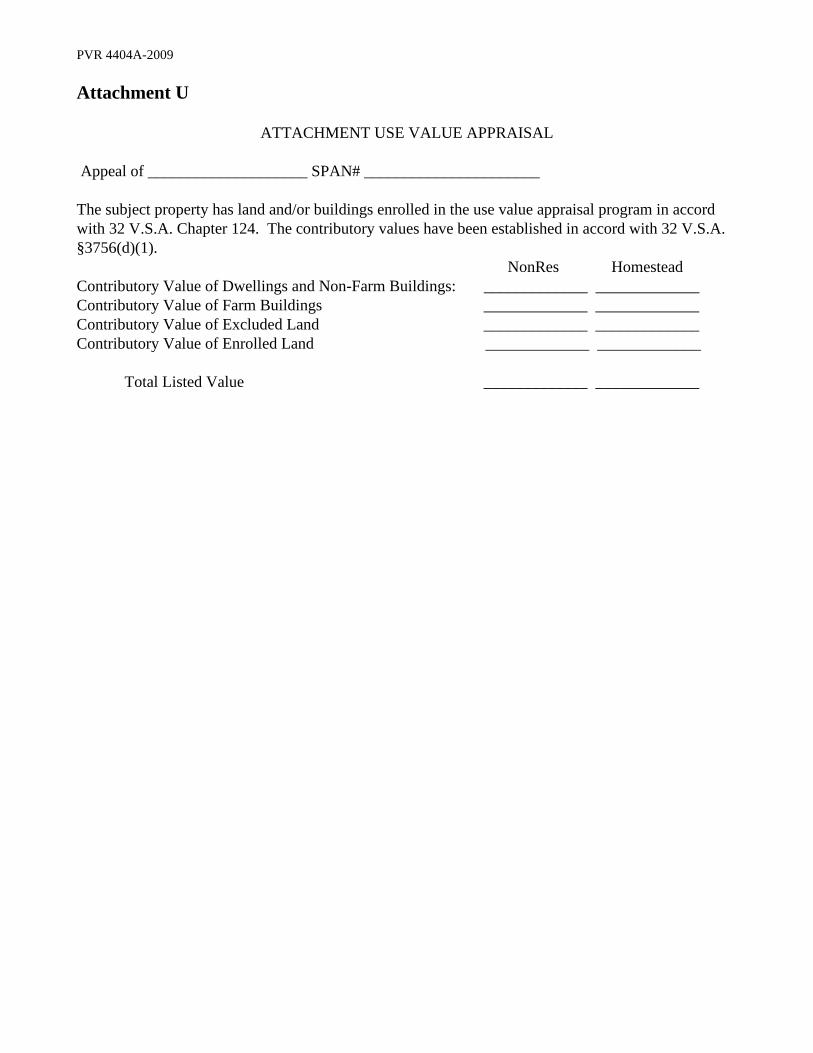

Attachment U

ATTACHMENT USE VALUE APPRAISAL

Appeal of ____________________ SPAN# ______________________

The subject property has land and/or buildings enrolled in the use value appraisal program in accord

with 32 V.S.A. Chapter 124. The contributory values have been established in accord with 32 V.S.A.

§3756(d)(1).

NonRes Homestead

Contributory Value of Dwellings and Non-Farm Buildings: _____________ _____________

Contributory Value of Farm Buildings _____________ _____________

Contributory Value of Excluded Land _____________ _____________

Contributory Value of Enrolled Land _____________ _____________

Total Listed Value _____________ _____________

Special Responsibilities of the Town Clerk in the BCAHearing Process

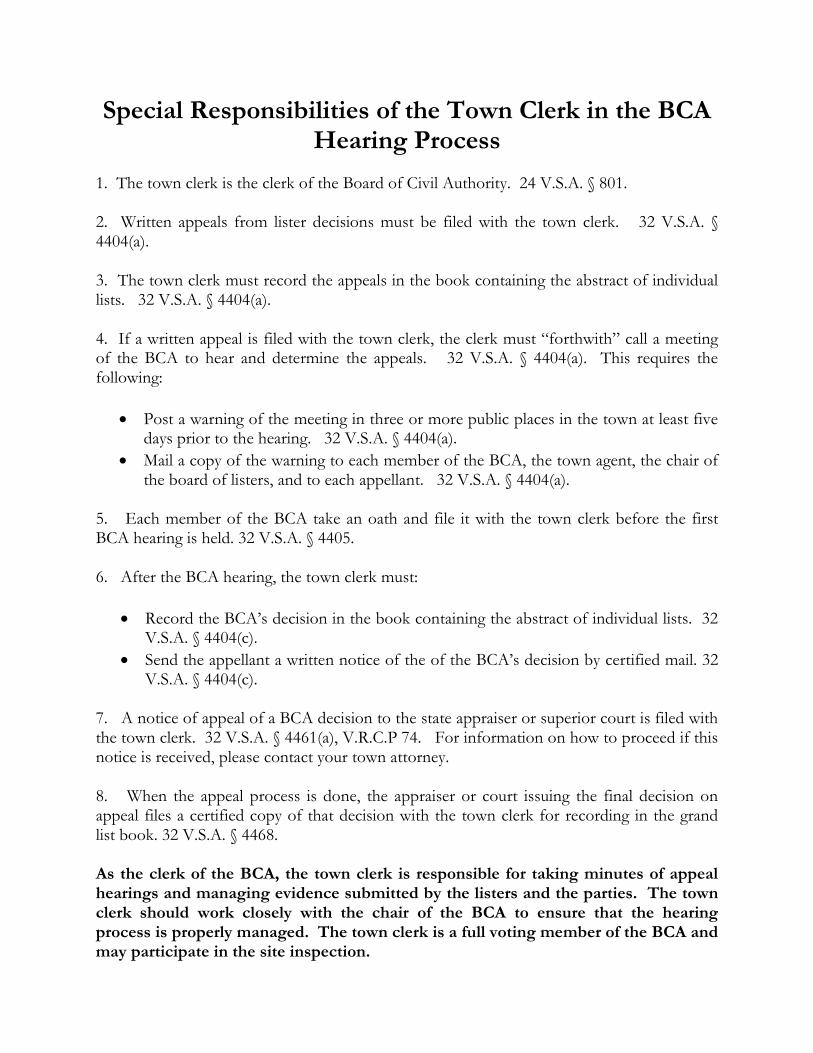

1. The town clerk is the clerk of the Board of Civil Authority. 24 V.S.A. § 801.

2. Written appeals from lister decisions must be filed with the town clerk. 32 V.S.A. §4404(a).

3. The town clerk must record the appeals in the book containing the abstract of individuallists. 32 V.S.A. § 4404(a).

4. If a written appeal is filed with the town clerk, the clerk must “forthwith” call a meetingof the BCA to hear and determine the appeals. 32 V.S.A. § 4404(a). This requires thefollowing:

Post a warning of the meeting in three or more public places in the town at least fivedays prior to the hearing. 32 V.S.A. § 4404(a).

Mail a copy of the warning to each member of the BCA, the town agent, the chair ofthe board of listers, and to each appellant. 32 V.S.A. § 4404(a).

5. Each member of the BCA take an oath and file it with the town clerk before the firstBCA hearing is held. 32 V.S.A. § 4405.

6. After the BCA hearing, the town clerk must:

Record the BCA’s decision in the book containing the abstract of individual lists. 32V.S.A. § 4404(c).

Send the appellant a written notice of the of the BCA’s decision by certified mail. 32V.S.A. § 4404(c).

7. A notice of appeal of a BCA decision to the state appraiser or superior court is filed withthe town clerk. 32 V.S.A. § 4461(a), V.R.C.P 74. For information on how to proceed if thisnotice is received, please contact your town attorney.

8. When the appeal process is done, the appraiser or court issuing the final decision onappeal files a certified copy of that decision with the town clerk for recording in the grandlist book. 32 V.S.A. § 4468.

As the clerk of the BCA, the town clerk is responsible for taking minutes of appealhearings and managing evidence submitted by the listers and the parties. The townclerk should work closely with the chair of the BCA to ensure that the hearingprocess is properly managed. The town clerk is a full voting member of the BCA andmay participate in the site inspection.

Suggested 2011 Property Tax Appeal Timeline andChecklist for Towns with Population of More Than 5,000

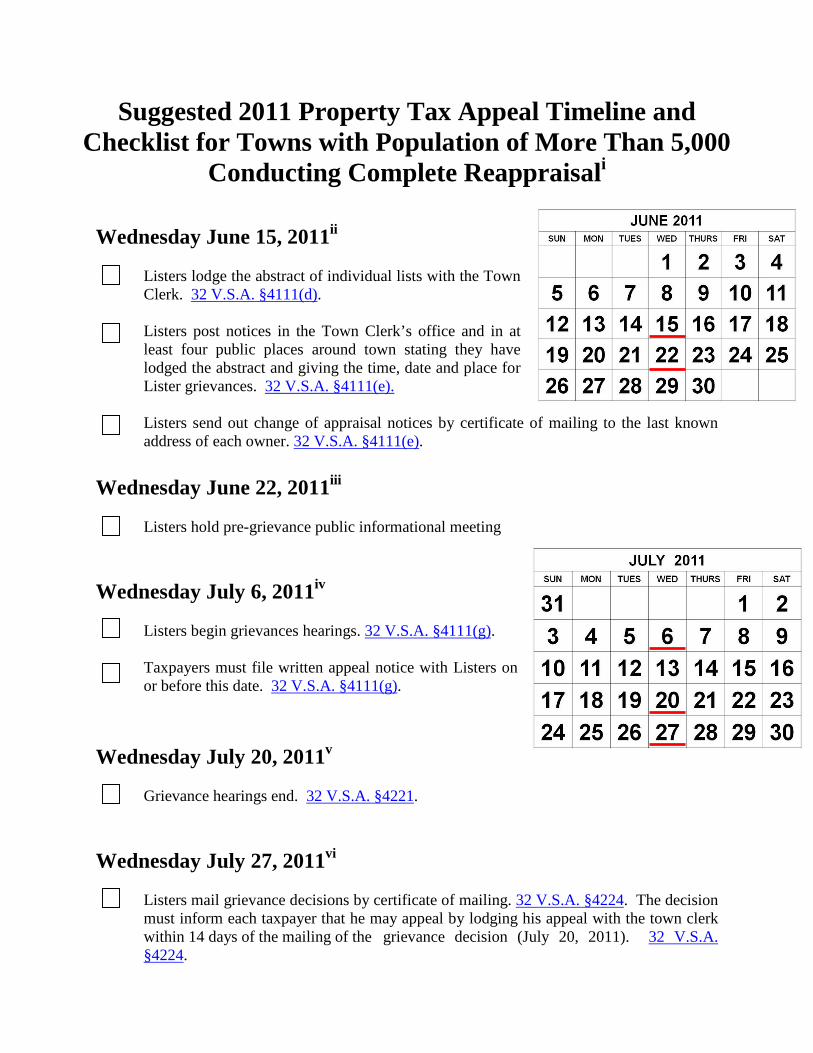

Conducting Complete Reappraisali

Wednesday June 15, 2011ii

Listers lodge the abstract of individual lists with the TownClerk. 32 V.S.A. §4111(d).

Listers post notices in the Town Clerk’s office and in atleast four public places around town stating they havelodged the abstract and giving the time, date and place forLister grievances. 32 V.S.A. §4111(e).

Listers send out change of appraisal notices by certificate of mailing to the last knownaddress of each owner. 32 V.S.A. §4111(e).

Wednesday June 22, 2011iii

Listers hold pre-grievance public informational meeting

Wednesday July 6, 2011iv

Listers begin grievances hearings. 32 V.S.A. §4111(g).

Taxpayers must file written appeal notice with Listers onor before this date. 32 V.S.A. §4111(g).

Wednesday July 20, 2011v

Grievance hearings end. 32 V.S.A. §4221.

Wednesday July 27, 2011vi

Listers mail grievance decisions by certificate of mailing. 32 V.S.A. §4224. The decisionmust inform each taxpayer that he may appeal by lodging his appeal with the town clerkwithin 14 days of the mailing of the grievance decision (July 20, 2011). 32 V.S.A.§4224.

Wednesday August 10, 2011vii

Last day for taxpayers to file written notice appeal of Listers' grievance decision withTown Clerk. The grounds upon which the appeal is based must be included in the appealnotice. 32 V.S.A. §4404(a). Town Clerk must record each taxpayer's written appealwith the abstract of individual lists. 32 V.S.A. §4404(a).

Friday, August 12, 2011viii

Listers lodge grand list in the office of the Town Clerk.32 V.S.A. §4151(a).

Listers complete oath described at 32 V.S.A.§4151(b).

Town clerk certifies the time the oath was taken and thedate the grand list was lodged. 32 V.S.A. §4151(b).

Board of Civil Authority holds pre-hearing organizational meeting to adopt rules ofprocedure, and develop hearing schedule with hearings to commence on August 3, 2011.

Monday, August 15, 2011

Town Clerk posts warning of the commencement of BCA hearings on August 3, 2011 inin three or more public places in town. 32 V.S.A. §4404(b).

Town Clerk mails a copy of the warning to each member of the BCA, the town agent, thechair of the board of listers and to each appellant. 32 V.S.A. §4404(b) Each mailingincludes copy of the BCA's hearing schedule and information on how the property taxassessment appeal hearings are conducted.

Wednesday, August 24, 2011ix

Board of Civil Authority commences appeal hearings.

iThe dates set forth in this document are suggested and based upon the statutory deadlines in chapter 129 of Title

32, Vermont Statutes Annotated. In the event that the listers or BCA are unable to comply with a statutory deadline,the listers with the approval of the selectboard may request an extension of the deadline from the Director ofProperty Valuation and Review. 32 V.S.A. §4342.

ii Statutory deadline for lodging the abstract of individual lists: June 24, 2011. 32 V.S.A. §4111(d).

iii A pre-grievance meeting is not required by statute, but is strongly recommended.

ivStatutory deadline to begin Lister grievances: July 9, 2011. 32 V.S.A. §§ 4111(c), 4221, 4341.

vStatutory deadline to conclude Lister grievances: July 22, 2011. 32 V.S.A. §4221

vi Statutory deadline for mailing Lister grievance decisions: July 29, 2011. 32 V.S.A. §4224

viiStatutory deadline for filing appeal notices is 14 days from date of mailing Listers' grievance decision: 32 V.S.A.

§4404(a).

viiiStatutory deadline to lodge grand list: August 14, 2011. 32 V.S.A. §4151(a)

ix Statutory deadline for commencing BCA hearings is 14 days from the after the last date allowed for notice ofappeal. 32 V.S.A. § 4404(b).

Suggested 2011 Property Tax Appeal Timeline andChecklist for Towns with Population of 5,000 or Less

Conducting Complete Reappraisali

Wednesday May 25, 2011ii

Listers lodge the abstract of individual lists with the TownClerk. 32 V.S.A. §4111(d).

Listers post notices in the Town Clerk’s office and in atleast four public places around town stating they havelodged the abstract and giving the time, date and place forLister grievances. 32 V.S.A. §4111(e).

Listers send out change of appraisal notices by certificateof mailing to the last known address of each owner. 32 V.S.A. §4111(e).

Wednesday June 1, 2011iii

Listers hold pre-grievance public informational meeting

Wednesday June 15, 2011iv

Listers begin grievances hearings. 32 V.S.A. §4111(g).

Taxpayers must file written appeal notice with Listers onor before this date. 32 V.S.A. §4111(g).

Wednesday June 29, 2011v

Grievance hearings end. 32 V.S.A. §4221.

Wednesday July 6, 2011vi

Listers mail grievance decisions by certificate of mailing. 32 V.S.A. §4224. The decisionmust inform each taxpayer that he may appeal by lodging his appeal with the town clerkwithin 14 days of the mailing of the grievance decision (July 20, 2011). 32 V.S.A.§4224.

Wednesday July 20, 2011vii

Last day for taxpayers to file written notice appeal of Listers' grievance decision withTown Clerk. The grounds upon which the appeal is based must be included in the appealnotice. 32 V.S.A. §4404(a). Town Clerk must record each taxpayer's written appealwith the abstract of individual lists. 32 V.S.A. §4404(a).

Monday, July 25, 2011viii

Listers lodge grand list in the office of the Town Clerk.32 V.S.A. §4151(a).

Listers complete oath described at 32 V.S.A.§4151(b).

Town clerk certifies the time the oath was taken and thedate the grand list was lodged. 32 V.S.A. §4151(b).

Board of Civil Authority holds pre-hearing organizational meeting to adopt rules ofprocedure, and develop hearing schedule with hearings to commence on August 3, 2011.

Tuesday, July 26, 2011

Town Clerk posts warning of the commencement of BCA hearings on August 3, 2011 inin three or more public places in town. 32 V.S.A. §4404(b).

Town Clerk mails a copy of the warning to each member of the BCA, the town agent, thechair of the board of listers and to each appellant. 32 V.S.A. §4404(b) Each mailingincludes copy of the BCA's hearing schedule and information on how the property taxassessment appeal hearings are conducted.

Wednesday, August 3, 2011ix

Board of Civil Authority commences appeal hearings.

iThe dates set forth in this document are suggested and based upon the statutory deadlines in chapter 129 of Title

32, Vermont Statutes Annotated. In the event that the listers or BCA are unable to comply with a statutory deadline,the listers with the approval of the selectboard may request an extension of the deadline from the Director ofProperty Valuation and Review. 32 V.S.A. §4342.

ii Statutory deadline for lodging the abstract of individual lists: June 4, 2011. 32 V.S.A. §4111(d).

iii A pre-grievance meeting is not required by statute, but is strongly recommended.

ivStatutory deadline to being Lister grievances: June 19, 2011. 32 V.S.A. §§ 4111(c), 4221, 4341.

vStatutory deadline to conclude Lister grievances: July 2, 2011. 32 V.S.A. §4221

vi Statutory deadline for mailing Lister grievance decisions: July 9, 2011. 32 V.S.A. §4224

viiStatutory deadline for filing appeal notices is 14 days from date of mailing Listers' grievance decision: 32 V.S.A.

§4404(a).

viiiStatutory to lodge grand list: July 25, 2011. 32 V.S.A. §4151(a)

ix Statutory deadline for commencing BCA hearings is 14 days from the after the last date allowed for notice ofappeal. 32 V.S.A. § 4404(b).

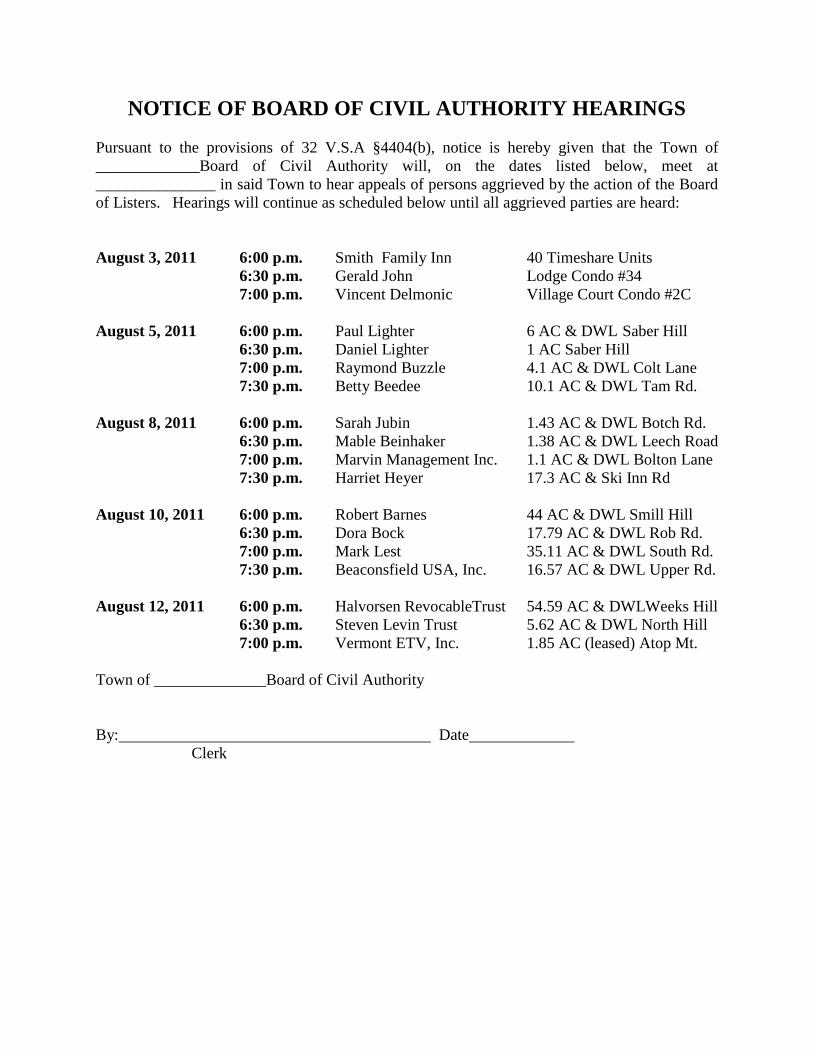

NOTICE OF BOARD OF CIVIL AUTHORITY HEARINGS

Pursuant to the provisions of 32 V.S.A §4404(b), notice is hereby given that the Town of_____________Board of Civil Authority will, on the dates listed below, meet at_______________ in said Town to hear appeals of persons aggrieved by the action of the Boardof Listers. Hearings will continue as scheduled below until all aggrieved parties are heard:

August 3, 2011 6:00 p.m. Smith Family Inn 40 Timeshare Units6:30 p.m. Gerald John Lodge Condo #347:00 p.m. Vincent Delmonic Village Court Condo #2C

August 5, 2011 6:00 p.m. Paul Lighter 6 AC & DWL Saber Hill6:30 p.m. Daniel Lighter 1 AC Saber Hill7:00 p.m. Raymond Buzzle 4.1 AC & DWL Colt Lane7:30 p.m. Betty Beedee 10.1 AC & DWL Tam Rd.

August 8, 2011 6:00 p.m. Sarah Jubin 1.43 AC & DWL Botch Rd.6:30 p.m. Mable Beinhaker 1.38 AC & DWL Leech Road7:00 p.m. Marvin Management Inc. 1.1 AC & DWL Bolton Lane7:30 p.m. Harriet Heyer 17.3 AC & Ski Inn Rd

August 10, 2011 6:00 p.m. Robert Barnes 44 AC & DWL Smill Hill6:30 p.m. Dora Bock 17.79 AC & DWL Rob Rd.7:00 p.m. Mark Lest 35.11 AC & DWL South Rd.7:30 p.m. Beaconsfield USA, Inc. 16.57 AC & DWL Upper Rd.

August 12, 2011 6:00 p.m. Halvorsen RevocableTrust 54.59 AC & DWLWeeks Hill6:30 p.m. Steven Levin Trust 5.62 AC & DWL North Hill7:00 p.m. Vermont ETV, Inc. 1.85 AC (leased) Atop Mt.

Town of ______________Board of Civil Authority

By: DateClerk

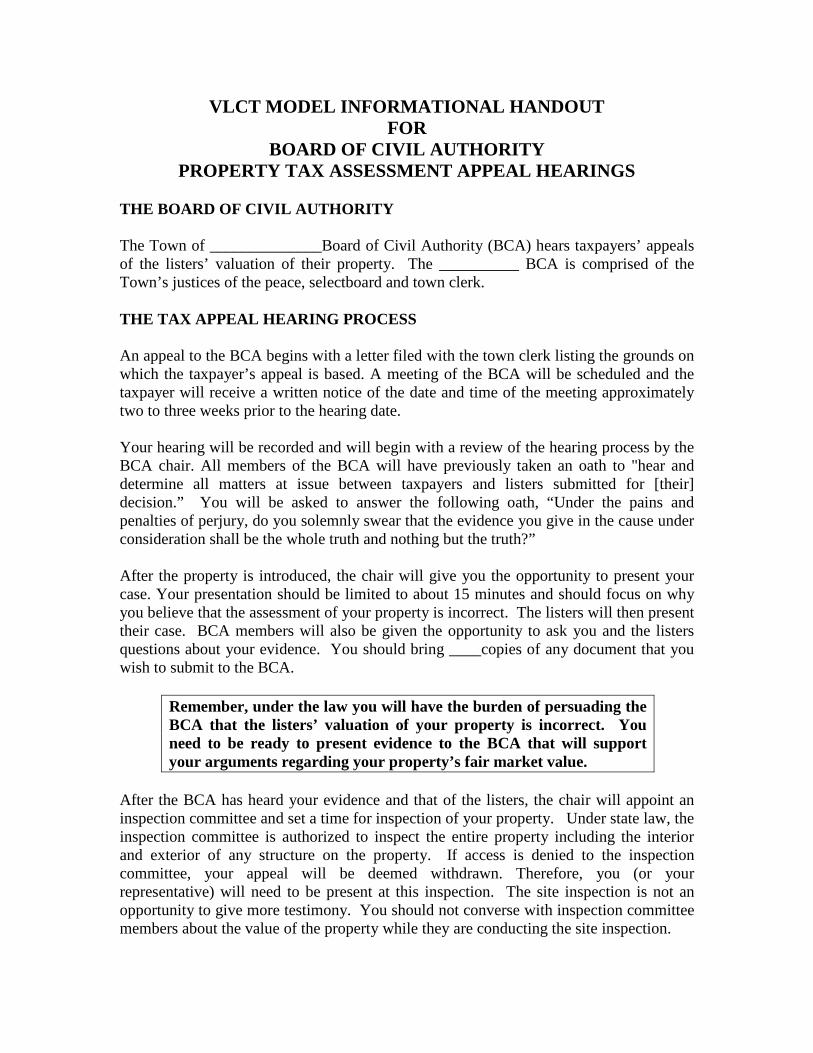

VLCT MODEL INFORMATIONAL HANDOUTFOR

BOARD OF CIVIL AUTHORITYPROPERTY TAX ASSESSMENT APPEAL HEARINGS

THE BOARD OF CIVIL AUTHORITY

The Town of ______________Board of Civil Authority (BCA) hears taxpayers’ appealsof the listers’ valuation of their property. The __________ BCA is comprised of theTown’s justices of the peace, selectboard and town clerk.

THE TAX APPEAL HEARING PROCESS

An appeal to the BCA begins with a letter filed with the town clerk listing the grounds onwhich the taxpayer’s appeal is based. A meeting of the BCA will be scheduled and thetaxpayer will receive a written notice of the date and time of the meeting approximatelytwo to three weeks prior to the hearing date.

Your hearing will be recorded and will begin with a review of the hearing process by theBCA chair. All members of the BCA will have previously taken an oath to "hear anddetermine all matters at issue between taxpayers and listers submitted for [their]decision.” You will be asked to answer the following oath, “Under the pains andpenalties of perjury, do you solemnly swear that the evidence you give in the cause underconsideration shall be the whole truth and nothing but the truth?”

After the property is introduced, the chair will give you the opportunity to present yourcase. Your presentation should be limited to about 15 minutes and should focus on whyyou believe that the assessment of your property is incorrect. The listers will then presenttheir case. BCA members will also be given the opportunity to ask you and the listersquestions about your evidence. You should bring ____copies of any document that youwish to submit to the BCA.

Remember, under the law you will have the burden of persuading theBCA that the listers’ valuation of your property is incorrect. Youneed to be ready to present evidence to the BCA that will supportyour arguments regarding your property’s fair market value.

After the BCA has heard your evidence and that of the listers, the chair will appoint aninspection committee and set a time for inspection of your property. Under state law, theinspection committee is authorized to inspect the entire property including the interiorand exterior of any structure on the property. If access is denied to the inspectioncommittee, your appeal will be deemed withdrawn. Therefore, you (or yourrepresentative) will need to be present at this inspection. The site inspection is not anopportunity to give more testimony. You should not converse with inspection committeemembers about the value of the property while they are conducting the site inspection.

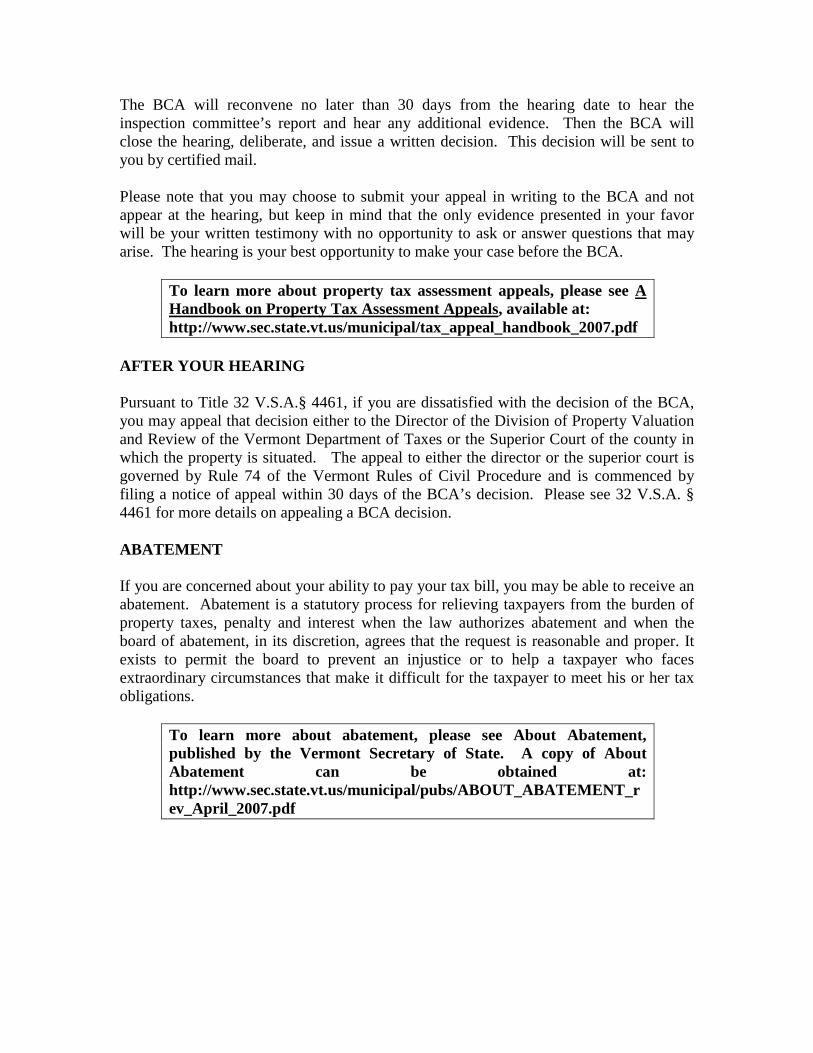

The BCA will reconvene no later than 30 days from the hearing date to hear theinspection committee’s report and hear any additional evidence. Then the BCA willclose the hearing, deliberate, and issue a written decision. This decision will be sent toyou by certified mail.

Please note that you may choose to submit your appeal in writing to the BCA and notappear at the hearing, but keep in mind that the only evidence presented in your favorwill be your written testimony with no opportunity to ask or answer questions that mayarise. The hearing is your best opportunity to make your case before the BCA.

To learn more about property tax assessment appeals, please see AHandbook on Property Tax Assessment Appeals, available at:http://www.sec.state.vt.us/municipal/tax_appeal_handbook_2007.pdf

AFTER YOUR HEARING

Pursuant to Title 32 V.S.A.§ 4461, if you are dissatisfied with the decision of the BCA,you may appeal that decision either to the Director of the Division of Property Valuationand Review of the Vermont Department of Taxes or the Superior Court of the county inwhich the property is situated. The appeal to either the director or the superior court isgoverned by Rule 74 of the Vermont Rules of Civil Procedure and is commenced byfiling a notice of appeal within 30 days of the BCA’s decision. Please see 32 V.S.A. §4461 for more details on appealing a BCA decision.

ABATEMENT

If you are concerned about your ability to pay your tax bill, you may be able to receive anabatement. Abatement is a statutory process for relieving taxpayers from the burden ofproperty taxes, penalty and interest when the law authorizes abatement and when theboard of abatement, in its discretion, agrees that the request is reasonable and proper. Itexists to permit the board to prevent an injustice or to help a taxpayer who facesextraordinary circumstances that make it difficult for the taxpayer to meet his or her taxobligations.

To learn more about abatement, please see About Abatement,published by the Vermont Secretary of State. A copy of AboutAbatement can be obtained at:http://www.sec.state.vt.us/municipal/pubs/ABOUT_ABATEMENT_rev_April_2007.pdf

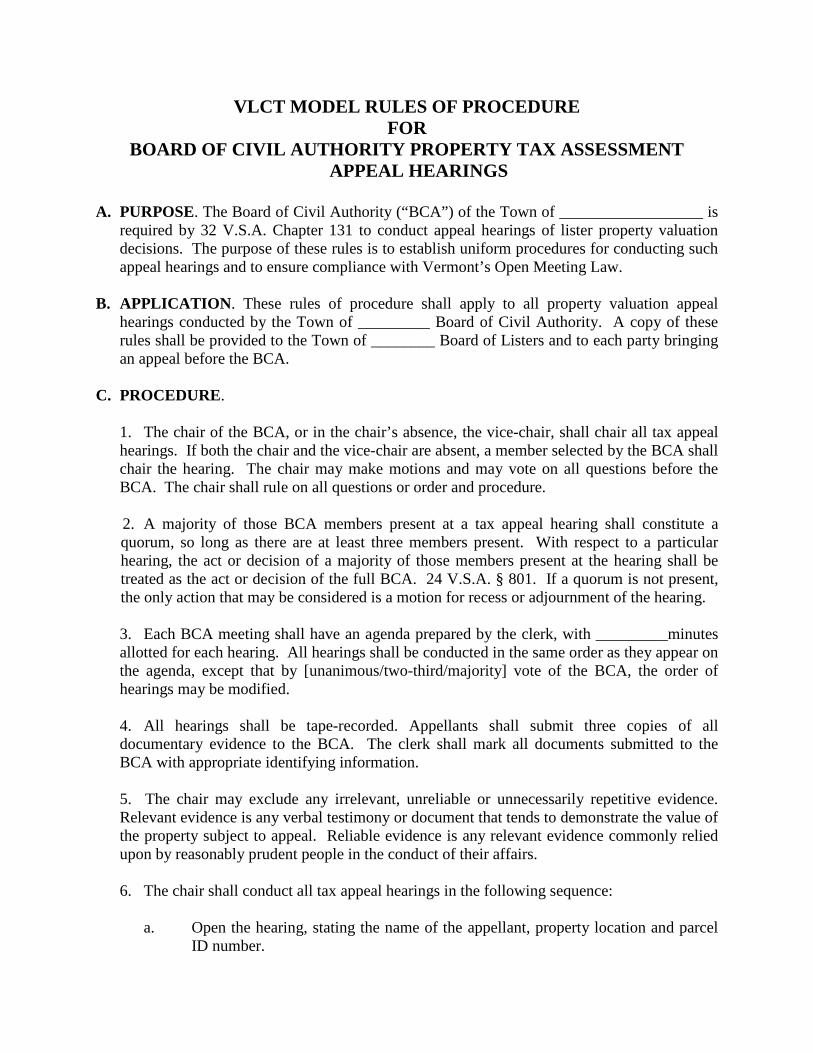

VLCT MODEL RULES OF PROCEDUREFOR

BOARD OF CIVIL AUTHORITY PROPERTY TAX ASSESSMENTAPPEAL HEARINGS

A. PURPOSE. The Board of Civil Authority (“BCA”) of the Town of __________________ isrequired by 32 V.S.A. Chapter 131 to conduct appeal hearings of lister property valuationdecisions. The purpose of these rules is to establish uniform procedures for conducting suchappeal hearings and to ensure compliance with Vermont’s Open Meeting Law.

B. APPLICATION. These rules of procedure shall apply to all property valuation appealhearings conducted by the Town of _________ Board of Civil Authority. A copy of theserules shall be provided to the Town of ________ Board of Listers and to each party bringingan appeal before the BCA.

C. PROCEDURE.

1. The chair of the BCA, or in the chair’s absence, the vice-chair, shall chair all tax appealhearings. If both the chair and the vice-chair are absent, a member selected by the BCA shallchair the hearing. The chair may make motions and may vote on all questions before theBCA. The chair shall rule on all questions or order and procedure.

2. A majority of those BCA members present at a tax appeal hearing shall constitute aquorum, so long as there are at least three members present. With respect to a particularhearing, the act or decision of a majority of those members present at the hearing shall betreated as the act or decision of the full BCA. 24 V.S.A. § 801. If a quorum is not present,the only action that may be considered is a motion for recess or adjournment of the hearing.

3. Each BCA meeting shall have an agenda prepared by the clerk, with _________minutesallotted for each hearing. All hearings shall be conducted in the same order as they appear onthe agenda, except that by [unanimous/two-third/majority] vote of the BCA, the order ofhearings may be modified.

4. All hearings shall be tape-recorded. Appellants shall submit three copies of alldocumentary evidence to the BCA. The clerk shall mark all documents submitted to theBCA with appropriate identifying information.

5. The chair may exclude any irrelevant, unreliable or unnecessarily repetitive evidence.Relevant evidence is any verbal testimony or document that tends to demonstrate the value ofthe property subject to appeal. Reliable evidence is any relevant evidence commonly reliedupon by reasonably prudent people in the conduct of their affairs.

6. The chair shall conduct all tax appeal hearings in the following sequence:

a. Open the hearing, stating the name of the appellant, property location and parcelID number.

b. Ask the appellant and listers to take the following oath:

Under the pains and penalties of perjury, do you solemnly swear that theevidence you give in the cause under consideration shall be the whole truthand nothing but the truth?

c. Ask the appellant if he/she has received a copy of these rules of procedure andwhether he/she has any questions about how the hearing will proceed.

d. Request BCA members to disclose any conflict of interest and/or ex partecommunication.

e. Ask the Listers to introduce the property on appeal by describing the property andits present valuation.

f. Ask the appellant to present his/her valuation and supporting evidence.

g. Ask the listers to respond to the information presented by the appellant.

h. Invite questions from BCA members.

i. Ask the listers to present their valuation and supporting evidence.

j. Ask the appellant to respond to the information presented by the listers.

k. Invite questions from BCA members.

l. Appoint an inspection committee of at least three BCA members to inspect theproperty at a date and time set by the chair and report its findings back to theBCA.

m. Recess to a date and time not more than 30 days from the hearing to accept theinspection committee report.

n. Reopen the hearing at the date and time specified.

o. Invite the inspections committee to present its report.

p. Invite final questions from the BCA.

q. Invite final comments from the appellant.

r. Invite final comments from the Listers.

s. Close the hearing and explain that the BCA will enter deliberative session andwill issue a written decision in writing within 15 days.

7. Each property shall be subject to an inspection by a site inspection committee of not less thanthree BCA members appointed by the chair. The site inspection committee shall report to theboard within 30 days of the hearing. If, after notice, an appellant refuses to allow an inspectionof the property as required under 32 V.S.A. 4404(c), including the interior and exterior of anystructure on the property, the appeal shall be deemed withdrawn.

8. These rules may be amended by [unanimous/two thirds/majority] vote of the Board of CivilAuthority.

Adopted by the ________________ Board of Civil Authority at its organizational meeting held__________, 2011.

_________________________ChairBoard of Civil Authority

Attest:Town Clerk