Embed Size (px)

Citation preview

1

Mergers and Acquisitions

Advanced Training Program in Finance

Jun QianBoston CollegeJuly 7, 2007

2

Outline

Introduction

Theoretical reasons for M&As

Empirical evidence

M&A mechanics

Hostile takeovers

Stock mergers

3

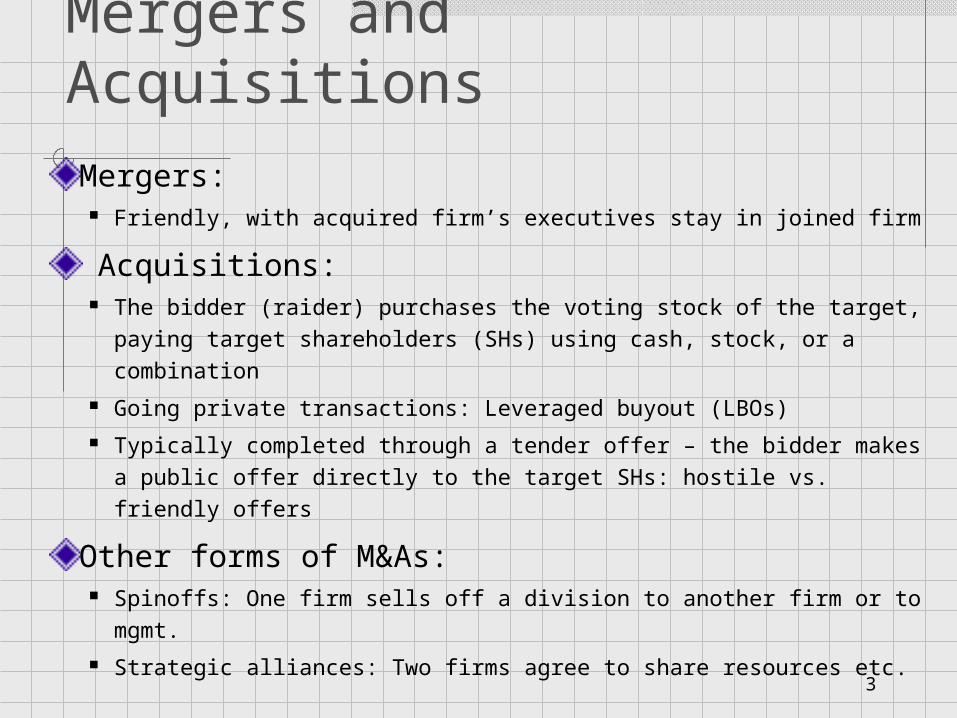

Mergers and Acquisitions

Mergers: Friendly, with acquired firm’s executives stay in joined firm

Acquisitions: The bidder (raider) purchases the voting stock of the target,

paying target shareholders (SHs) using cash, stock, or a combination

Going private transactions: Leveraged buyout (LBOs) Typically completed through a tender offer – the bidder makes a

public offer directly to the target SHs: hostile vs. friendly offers

Other forms of M&As: Spinoffs: One firm sells off a division to another firm or to mgmt. Strategic alliances: Two firms agree to share resources etc.

4

Types of Mergers and Acquisitions

Horizontal M&As: Two firms competing in the same industry Regulated by anti-trust (monopoly) laws

Vertical M&As: Firms at different stages in the

production/sale (supplier and customer)

Conglomerate M&As: Product extension Geographic market extension / cross-border Unrelated firms

5

Reasons for MergersEfficiency Operating synergy Financial synergy Market power Diversification

Solution to the holdup problemAgency costs Market for corporate control Mergers due to agency costs

Merger waves Stock market driven M&As.

6

Operating SynergiesPV (A+B) > PV(A) + PV(B)

Economies of scale Cost savings due to increased size/scale of output

Economies of scope Average cost of producing different products

together is lower than the cost when produced separately

Cost savings due to overlap in R&D, marketing channels, other sharing of resources

Strategic response to changing environment

7

Financial SynergiesPecking order financing

Matching of cash-rich firms with firms that have investment opportunities

Internal capital markets may have less frictions than markets No informational costs, issuance costs, or regulatory approval

But, inefficiencies of internal markets: Conflict of interests between divisional managers (over-

investment);

Allocation of investment capital is a bargaining process rather than “priced” by the markets

Increased debt capacity and tax shields

Implicit “too big to fail” guarantee Reduced costs of financial distress costs

8

Diversification-driven M&As?Diversification thru. merger may create value

Decrease cash flow variability; lower cost of capital Managers can take riskier projects and invest in human capital

Diversification may destroy value SHs can better diversify using capital markets; benefits of taking

controlling positions are not available to small SHs Inefficiencies of internal markets and decreasing returns to

organizational capitals; higher agency costs

Empirical evidence on diversification M&As: Diversification discount (Berger and Ofek, 1995): diversified firms

trade at 15% less than pre-merger levels The above test does not take into account what would have

happened to firms if they do not pursue diversifying mergers Redo previous test (by matching diversified and non-diversified

firms): discount is much smaller and could be 0

9

Holdup Problem and M&AsExample: Auto company A and tire company B

Assume B is only supplier of tires to A (perhaps only one knows how to produce special tires for A’s new vehicles)

Knowing this, B can “holdup” (like hostage) A, and demand that A pays high prices for new tires

Expecting this to occur, A loses incentives in producing the new vehicles, so that B also loses

Solution: A acquires B (Grossman and Hart, 1986) Internalizes the supply and holdup problem (if tire division

manager threatens to increase price, he will be fired) This is vertical integration: Optimal ownership and control of

assets – allowing A, which makes the most use out of the control of tire company’s assets, to own B

Similar logic behind horizontal integration

10

Agency Problems and M&As

Separation of ownership and control

Managers prefer Less effort; lower risk (ignores option grants);

and shorter horizon

Substitute low risk for high risk investments

Retain excessive cash reserves Keep leverage too low Keep dividends too low

Perk consumption

11

Corporate Governance Solutions for Agency Problems

Large shareholders as monitorsUse of debtExecutive compensationInput and product markets competitionCapital markets as monitors: markets for corporate control Managerial teams compete for firms M&As allow more efficient managers to replace

less efficient ones The possibility of a takeover may discipline

existing managers

12

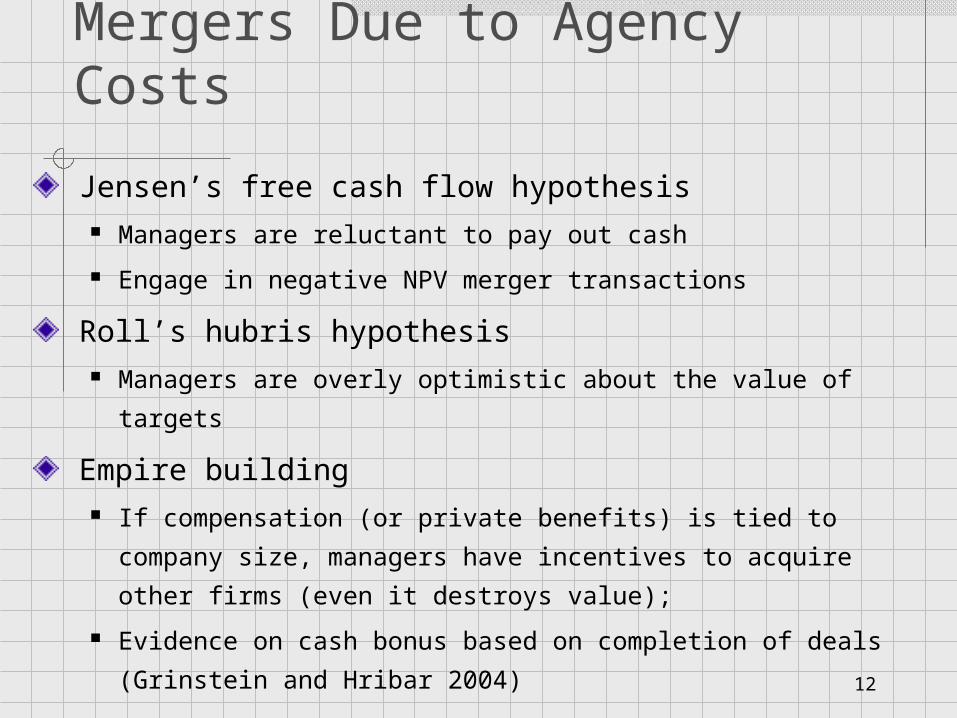

Mergers Due to Agency Costs

Jensen’s free cash flow hypothesis Managers are reluctant to pay out cash

Engage in negative NPV merger transactions

Roll’s hubris hypothesis Managers are overly optimistic about the value of targets

Empire building If compensation (or private benefits) is tied to company

size, managers have incentives to acquire other firms (even

it destroys value);

Evidence on cash bonus based on completion of deals

(Grinstein and Hribar 2004)

13

History of Merger WavesFirst wave (1897-1904) – horizontal mergers

Second wave (1916-1929) – vertical mergers

Third wave (1960s) – conglomerate mergers

Fourth wave (1980s) – hostile takeovers, LBOs and MBOs

Fifth wave (1992 - 2000) – stock-based friendly mergers: Industry-wide consolidations after de-regulation Peak was reached during 2000 – $3.8 trillion,

35,000 announced deals

14

Merger WavesM&As occur in waves and are clustered in industriesTechnology shocks and macro-factors

Regulations In the US: M&As must be cleared by Dept. of Justice (e.g., anti-trust laws)

and the FTC; many states have anti-takeover laws (solution: Delaware) Europe: workers have 50% board repres. in Germany and difficult to

remove; in France govt. can impose costs on takeovers Japan: role of Keiretsu – firms combine with each other thru. reciprocal

shareholdings and trading agreements

Deregulation-driven M&A waves? Some of the deregulated industries:

Airlines (78), broadcasting (84 & 96), entertainment (84), banks and thrifts (94), utilities (92), and telecommunications (96)

15

Evidence: Announcement effects of M&As

Significant wealth gain for target SHs: Price runup prior to announcement (-10 days); Announcement day:

Tender offers: 20% to 30% abnormal return 1st day, Stock mergers: Smaller positive effect

Firms “similar” to target also get a boost

Bidder SHs break even or suffer losses: Depends on method of payment: cash vs. stock Stock mergers:

Significant negative abnormal returns Show signs of over-valuation (earnings manipulations

and insider selling prior to deal announcement)

Net effect (bidder plus target)

16

Evidence: Long-run performance

Performance of merged firms:

Stock mergers: negative abnormal returns

Cash acquisitions: positive abnormal returns

Findings robust after correction of Fama-

French factor of beta, size, book-to-market

Market efficiency: Initial guess correct, but

wrong magnitude

17

Merger Mechanics

Preliminary actions

Proxy fight

Tender offer and defensive tactics

Friendly (stock) mergers

18

Preliminary Actions

Identifying potential targets

Bidder may establish a toehold by open market

(anonymous) purchase of target shares Once a certain threshold has been passed, the intentions of

the bidder have to be revealed

Bear hug (quasi-friendly) Bidder contacts the target board of directors and threatens

with a tender offer if friendly deal is not agreed

Accompanied by public announcement of tender offer

intent

19

Proxy Fight

An attempt by a group of SHs to take control through the use of voting by proxy mechanisms

The term “proxy” denotes the ability of a SH to delegate her voting rights to another SH, who can vote by proxy

Goals of proxy fights: Replace portions of the board (and management) Refuse proposed merger agreement To change charter or to approve a merger

Frequency of proxy fights Less frequent in economies with active takeover market

(higher frequency of proxy contests in Germany than in the US and UK)

Increasing institutional activism over the past decade => proxy fights much more common in the US

20

Proxy Fight (cont’d)The proxy fight process:

The dissenting party or bidder campaign and solicit vote-proxies from dissatisfied target SHs

Collect proxy votes File the proxy documents with the SEC Call a special shareholder meeting: votes/proxies exercised

Evaluation of effectiveness of proxy fight: Advantage: no need to acquire/purchase equity; Disadvantage: costly to contact SHs; incumbents tend to

have credibility among small SHs; Attitude and involvement of institutional SHs may be critical Proxy fights are often unsuccessful, but it may change But, they are a cheap alternative to a tender offer Used as a initial step before a tender offer (hostile takeover)

21

Tender OfferOffer to purchase a pre-specified number of shares

directly from target SHs Method of payment: cash, stock, debentures, warrants, and

combination

Procedure and important factors: Active and widespread solicitation of SHs

Solicitation for substantial fraction of shares

Offer at a premium to current stock price

Contingent on tender of a fixed minimum number of shares

Tender offer open for a limited period of time

Finishing touch: regulatory procedure, cleanup price

22

Types of Tender OffersTwo-tiered (front-end loaded)

Front-end: tender offer price (shares tendered in the 1st step may receive a higher premium);

Back-end, clean-up price: effectively a merger offer price (“fair” price/legal problem)

Creates incentives for shareholders to tender first instead of wait; coercive but can solve the free-rider problem

All partial offers are implicitly two-tiered offers

All-or-nothing (conditional offer) Bid is conditional on a minimum number of shares: usually

50% of all outstanding shares tendered or on success; or nothing

Any-or-all (unconditional offer) Bidder will buy all tendered shares

Saturday night special

23

Free-rider Problem Among Target SHs

How to explain the following facts: Initial bid premium on average 30% Announcement effect for raiders 0 or negative

Free-rider problem (Grossman and Hart 1980) Disperse equity ownership for target; each small SH thinks

she is non-pivotal in determining outcome of tender offer To start, assume current target price is $50 per share;

assume everyone knows a tender offer by the current raider will increase value to $100 per share

What happens if raider bids $50? $75? $99? Smaller shareholders will reject/tend to wait as long as bid < $100

The raider must significantly bid over the current target price in order convince the SHs to tender

But this is very costly to the raider

24

Solutions to Free-rider Problem?

Punishing non-tendering shareholders: Two-tiered offers

Toehold acquisition by raiders: Shares purchased before bidding for the target Profitable strategy in takeovers? (Shleifer and Vishny 1986)

Disclosure requirements on toeholds and takeovers:

5% threshold in the US and filing of 13d with SEC; More disclosure at the time of the tender offer (e.g, 14d, 14e filings)

Evidence on toeholds: Mean much smaller than 5%; many bidders do not acquire any

toehold; Empirical “puzzle”: Goldman and Qian (2005) provide a solution

25

Defense MeasuresPreventive defense measures: Poison pills Corporate charter amendments (shark

repellents) Golden parachutes

Reactive defense measures: Greenmail, standstill, and reverse greenmail White knights Scorched earth defense Litigation Pac-man defense: Acquiring the acquirer Just say no

26

Defense Measures: Poison Pills

Definition and characteristics: Represents the creation of special rights to receive extra

payments, similar to call options/warrants, issued to (some or all) existing common SHs; to the exclusion and detriment of potential raiders

Triggered after takeover-related events: e.g., a bidder acquires 10% of shares;

Warrants are exercisable at the triggering of another event (e.g. bidder acquires 100% of the shares)

Examples and terminologies: Share rights plans: current SHs receive right to buy stocks at fixed

price, with a “flip over” provision In the event of M&A, the holders can exercise and receive stock of the

merged firm worth twice of the exercise price Other terms: Flip-in – rights to purchase target securities; Back-

end plans – exchange stock for cash or senior securities; Poison puts – right to sell bonds

27

Poison Pills (cont’d)History of poison pills:

Invented in 1982 by Martin Lipton, an M&A attorney First generation: dividend of preferred shares convertible

into acquirer’s shares Second generation: flip-over pill (fails to provide protection) Third generation: flip-in pill

Example: Conrail’s poison pill Flip-in pill: Right to buy an additional share at half price

when a hostile bidders acquires 10% of Conrail’s shares Background: Conrail – 90.5 million shares at $71; total MV

$6,426 million; hostile Bidder buys 10% of shares for a total of $643 million

28

Poison Pills: example (cont’d)Before poison pill kicks in:

After poison pill becomes effective:

Group # Shares % of total Value

Friendly shareholders 81.45 90.0 $5,783

Hostile bidder 9.05 10.0 $643

Total 90.50 100.0 $6,426

Per Share $71.00

Group # Shares % of total Value

Friendly shareholders 162.90 94.7 $8,827

Hostile bidder 9.05 5.3 $490

Total 171.95 100.0 $9,317

Per Share $54.18

29

Poison Pills (cont’d)Conrail’s poison pill:

Purchase triggers poison pill: Conrail issues 81.45 million

shares at $35.50 a share, receives $2,891 million

Total MV is $9,317, total number of shares is now 171.95

million; share price drops to $54.18

Bidder’s block drops to 5.3% of shares

Bidder’s equity value drops from $643 million to $490 million

A transfer or $153 million to existing shareholders plus

additional voting rights

Overall empirical evidence: Early 1980s – value reducing;

Mid- and late-1980s – less negative to value increasing

30

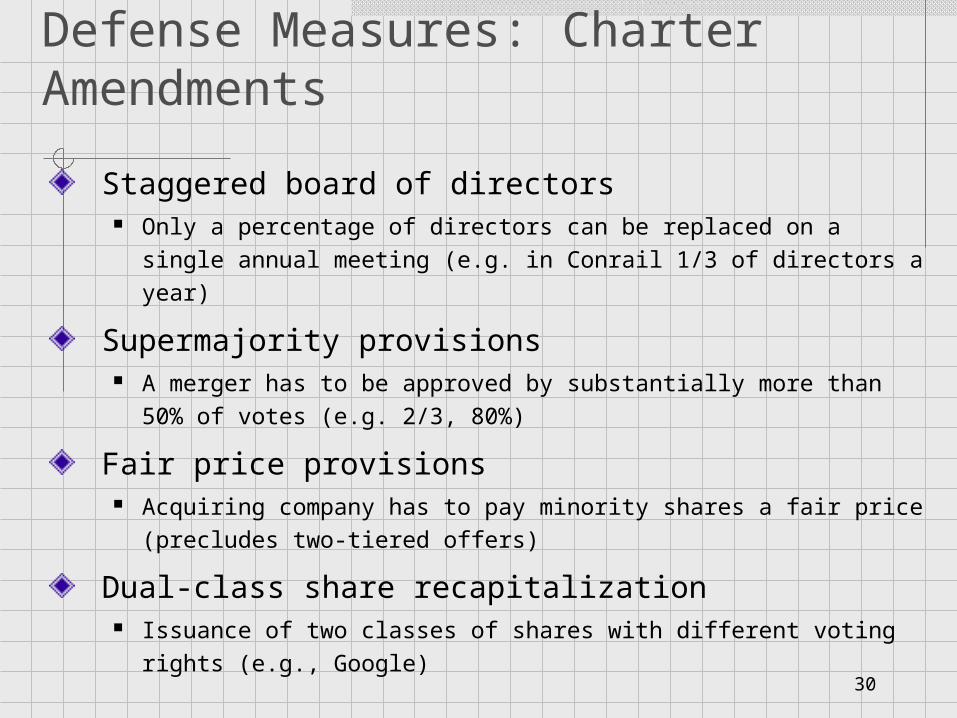

Defense Measures: Charter Amendments

Staggered board of directors Only a percentage of directors can be replaced on a single

annual meeting (e.g. in Conrail 1/3 of directors a year)

Supermajority provisions A merger has to be approved by substantially more than 50% of

votes (e.g. 2/3, 80%)

Fair price provisions Acquiring company has to pay minority shares a fair price

(precludes two-tiered offers)

Dual-class share recapitalization Issuance of two classes of shares with different voting rights

(e.g., Google)

31

Defense measures (cont’d)

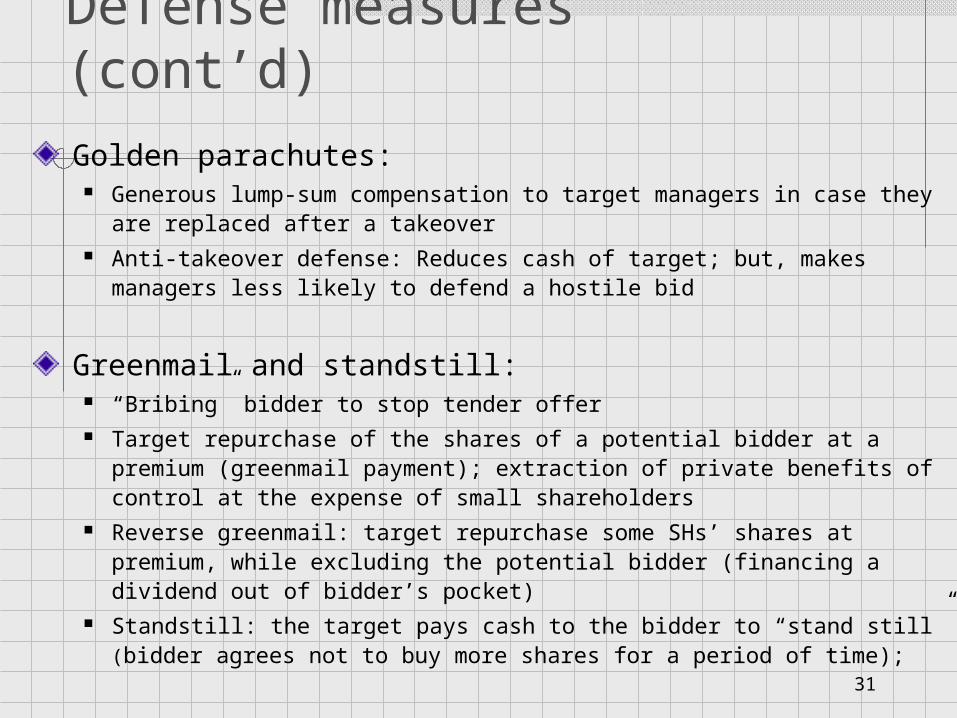

Golden parachutes: Generous lump-sum compensation to target managers in case they

are replaced after a takeover Anti-takeover defense: Reduces cash of target; but, makes

managers less likely to defend a hostile bid

Greenmail and standstill: “Bribing” bidder to stop tender offer Target repurchase of the shares of a potential bidder at a premium

(greenmail payment); extraction of private benefits of control at the expense of small shareholders

Reverse greenmail: target repurchase some SHs’ shares at premium, while excluding the potential bidder (financing a dividend out of bidder’s pocket)

Standstill: the target pays cash to the bidder to “stand still” (bidder agrees not to buy more shares for a period of time);

32

Defense measures (cont’d)

White knight: Target solicit another bidder after receiving a hostile bid;

The white knight is friendly to target managers, and usually

overpays (bad for white knight SHs)

White esquire – a large shareholder that is friendly to managers

Scorched earth defense: Make target less attractive: increase leverage, use money to pay

dividends; scorched earth – sell off the best assets (crown jewels)

Change distribution of voting rights: issue more shares to friendly

shareholders (dilutes bidders voting rights), repurchase shares

33

Effects for Defense Measures

Actions taken by managers: retain control

(entrenchment); increase offer price

“Mild” resistance causes restructuring of bid; “severe”

resistance deters bid

Reduce probability of takeover bids; but increase

premium given a takeover bid/success

Allow managers and large shareholders to expropriate

small shareholders (private benefits of control)

Empirical evidence is mixed

34

Top 10 M&As up to 1995Year Acquirer Target Value

$billion

1989

Kohlberg, Kravis & Roberts

RJR Nabisco 25.1

1995

Walt Disney Co. Capital Cities/ABC 19.0

1995

Glaxo PLC Wellcome PLC 15.0

1990

Time Inc. Warner Comm. 14.1

1988

Philip Morris Inc Kraft Inc 13.4

1984

Standard Oil Inc Gulf Inc 13.4

1989

Squibb Co. Bristol-Myers Co. 12.1

1984

Texaco Inc Getty Oil Co 10.1

1995

Lockheed Corp Martin Marietta Corp 10.0

1995

Chemical Bank Chase Manhattan Bank

10.0

35

More Recent Mergers

Year Buying Company Selling CompanyPayment

($bil)

1999 MCI WorldCom Sprint 1151999 Viacom CBS 351999 AT&T MediaOne Group 541999 Travelers Citicorp 831999 Exxon Mobil 801999 TotalFina (France) Elf Aquitaine (France) 551999 Olivetti (Italy) Telecom Italia (Italy) 581999 Vodafone (UK) Air Touc Comm. 611998 British Petroleum (UK) Amoco Corp. 481998 Daimler-Benz (Germany)Chrysler 381998 Zeneca (UK) Astra (Sweden) 351998 Nationsbank Corp. BankAmerica Corp. 621998 WorldCom Inc. MCI Communications 421998 Norwest Corp. Wells Fargo & Co. 34

36

Stock Market Driven M&As

Shleifer & Vishny (2003): Markets inefficient, managers take advantage through M&As

When do we expect to see cash offers? Undervalued acquirers tend to use cash to acquire targets; they will earn

positive long-run returns after acquisitions;

Wave can occur if market- or industry-wide valuations are low;

Targets earn low returns prior to acquisitions; high, short-run returns after

M&A but long run return can be flat

What about stock mergers? Acquirers are likely to be (relatively more) over-valued;

Wave occurs when market- or industry-wide valuations are high;

Long-run returns to acquirers after M&As tend to be negative, but M&As still

serve the interests of long-term acquirer shareholders

37

Agency Problems of Overvalued EquityJensen (2004):

Shock (tech sector) in the market increases equity value in 1990s;

Firms’ managers realize that their equity is over-valued: Correction? Yes, otherwise investors and market will have (overly

optimistic) expectations that cannot be fulfilled by firms; But, no one wants to be the “party pooper” More importantly, managers’ compensation tied to stock pricesHow

to correct (lower) expectations on your own equity value?

Series of (stock-based) acquisitions: If market does not “get the message,” large scale acquisition, or, (After all other means fail) accounting frauds

Overall lessons: Important for mgmt./board to correct over-valuation of equity early; Otherwise they may engage in activities that will destroy value.

38

Insider Trading around M&As: All Acquirers (86-00)(from Song 2005)

0

50,000

100,000

150,000

200,000

250,000

300,000

Num

ber of Shares T

raded

Month

All Acquirers Purchase Sale

39

Insider Trading by “Pure Seller” Acquirers around M&As

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

Num

ber of Shares T

raded

Month

Pure Seller Group Purchase Sale

40

Insider Trading by “Pure Buyer” Acquirers around M&As

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Num

ber of Shares T

raded

Month

Pure Buyer Group Purchase Sale

41

Summary and Concluding RemarksGood M&As, and bad M&As

Empirical evidence: announcement effect

and long-run performance

Tender offers: techniques, free-rider problem

and solutions, defense measures

Stock mergers: (over-) valuations; risk and

uncertainty; method of payment; due

diligence