Embed Size (px)

Citation preview

1

_Akzente für die Zukunft

Payment Services Directive

Zuzana Kalivodova National Expert

European CommissionInternal Market and Services DG

Retail Issues, Consumer Policy and Payment Systems [email protected] - +32-2-299.58.01

- +32-2-295.07.50http://ec.europa.eu/internal_market/payments/index_en.htm

Payment Services Directive Budapest, 17 November 2006

The views expressed are those of the author and do not necessarily reflect those of the Commission.

2

Points to cover

I. Present state of payments market integration

II. The vision

III. Role of industry – Self-regulationis the key

IV. How can regulators help? Payment Services Directive

V. ECOFIN conclusions

VI. Conclusions

3

I. Present state of payments market integration

• Studies estimates the Cost impact of the payment sytem to society to high 2-3% GDP (cash is the maim cost driver and accounts for as much as 60-70% of the total cost of the payment system)

• No Single Market in payments (25 different national payment systems) despite

creation of Single Market in 1992

introduction of single currency in 1999

• Does this matter we have no single market for payments?

4

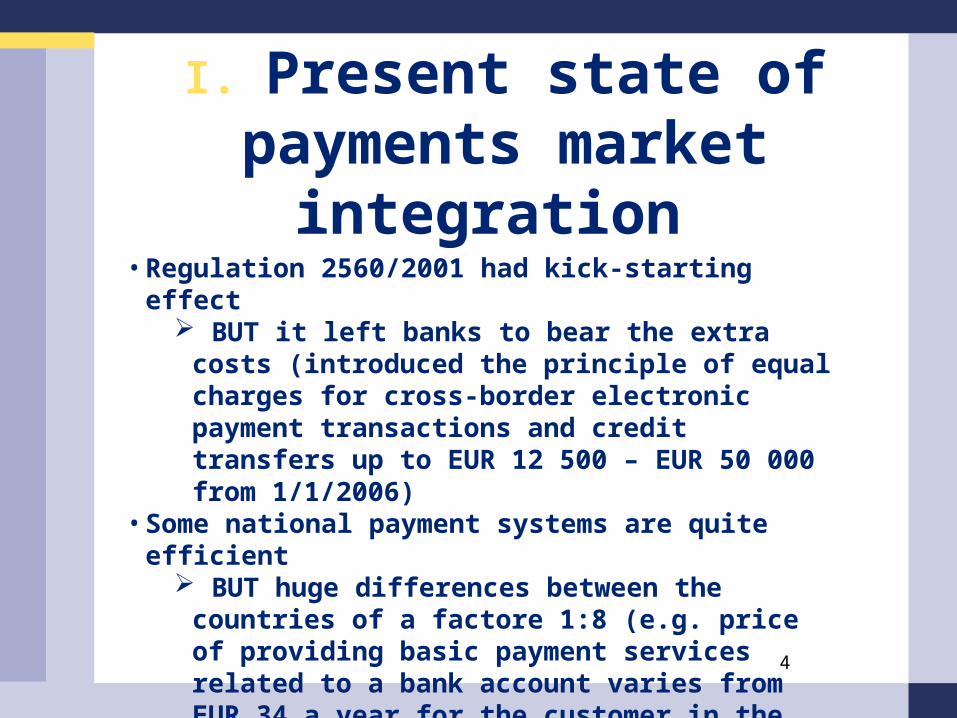

I. Present state of payments market integration

• Regulation 2560/2001 had kick-starting effect BUT it left banks to bear the extra costs

(introduced the principle of equal charges for cross-border electronic payment transactions and credit transfers up to EUR 12 500 – EUR 50 000 from 1/1/2006)

• Some national payment systems are quite efficient BUT huge differences between the countries of a

factore 1:8 (e.g. price of providing basic payment services related to a bank account varies from EUR 34 a year for the customer in the Netherlands to EUR 252 in Italy)

5

I. Present state of payments market integration

• Efficiency of cross-border payments is substantially lower– BUT should be at par with the best performing national

markets• Well-functioning national standards exist

– BUT protected national markets and competition stops at the border

6

I. Present state of payments market integration

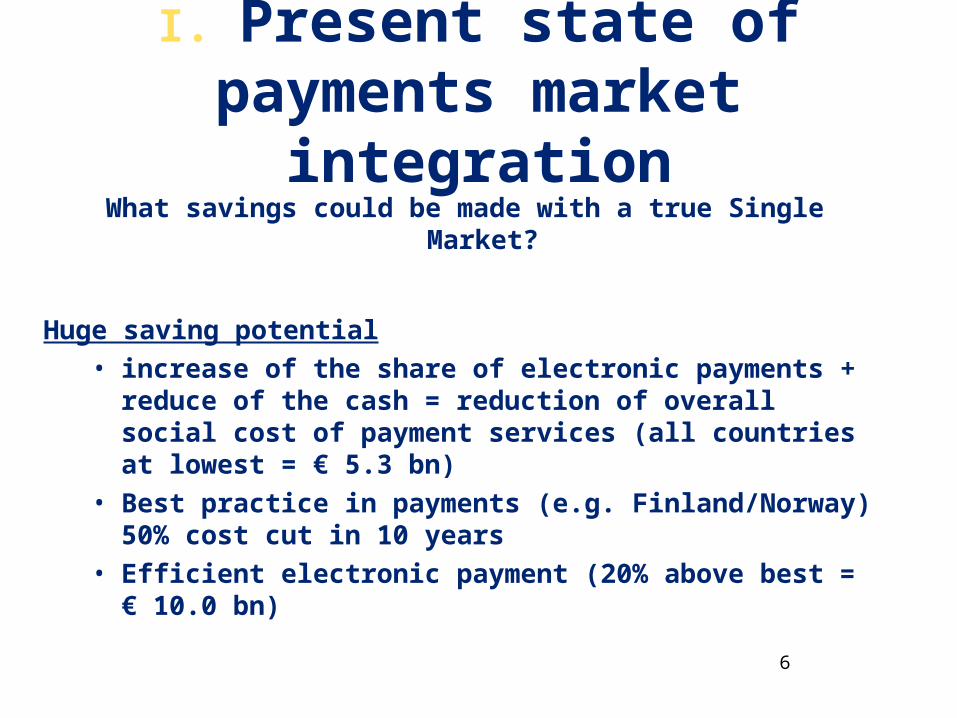

What savings could be made with a true Single Market?

Huge saving potential• increase of the share of electronic payments + reduce of the

cash = reduction of overall social cost of payment services (all countries at lowest = € 5.3 bn)

• Best practice in payments (e.g. Finland/Norway) 50% cost cut in 10 years

• Efficient electronic payment (20% above best = € 10.0 bn)

7

I. Present state of payments market integration

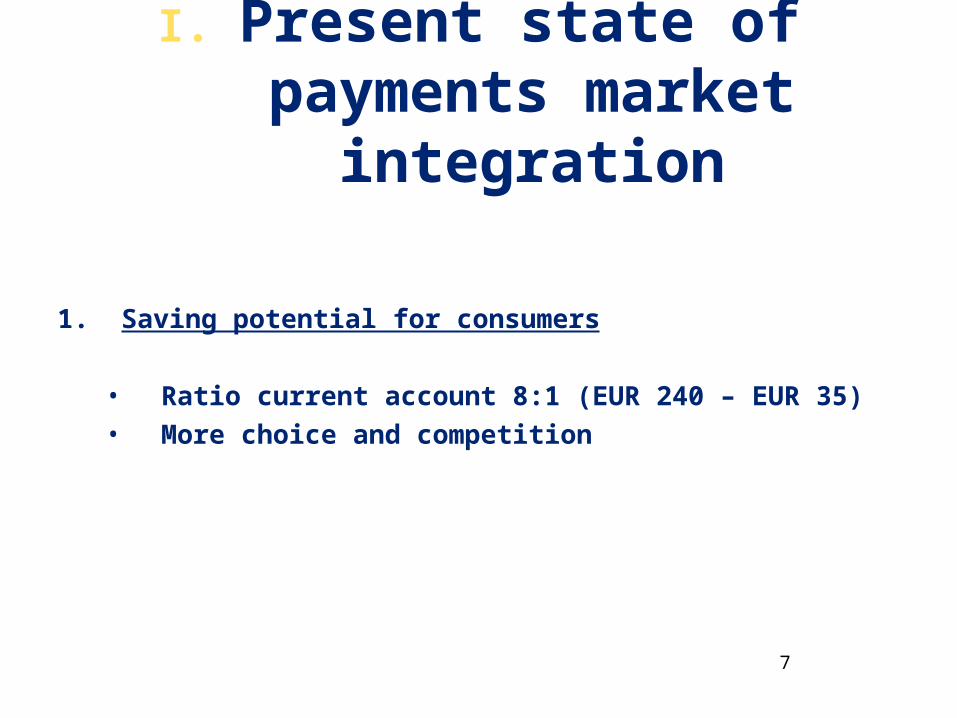

1. Saving potential for consumers

• Ratio current account 8:1 (EUR 240 – EUR 35)• More choice and competition

8

I. Present state of payments market integration

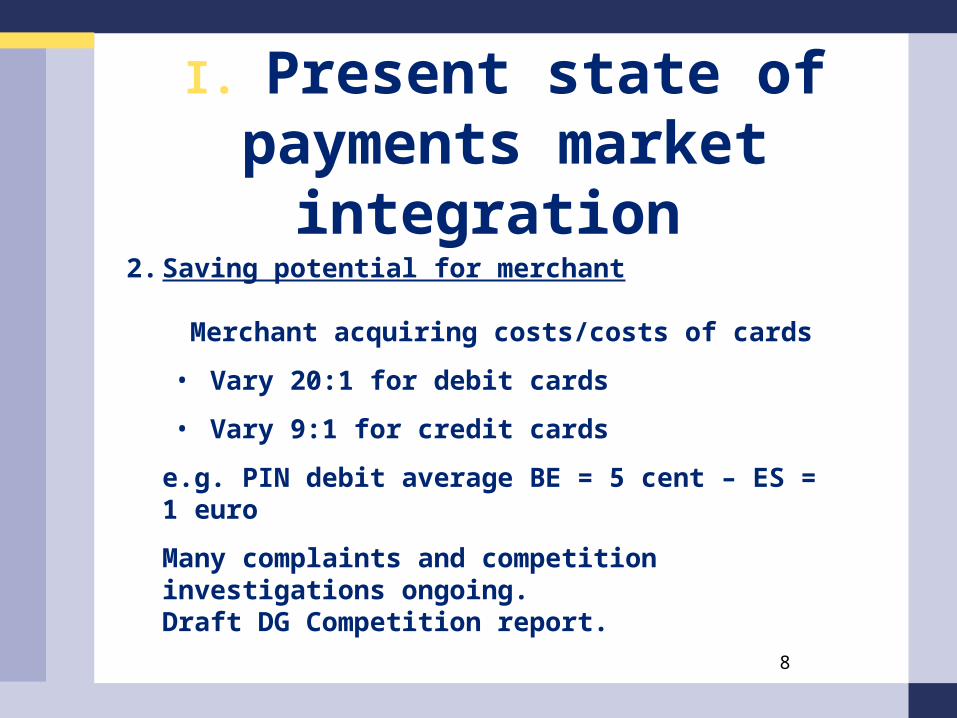

2. Saving potential for merchant

Merchant acquiring costs/costs of cards

• Vary 20:1 for debit cards

• Vary 9:1 for credit cards

e.g. PIN debit average BE = 5 cent – ES = 1 euro

Many complaints and competition investigations ongoing. Draft DG Competition report.

9

I. Present state of payments market integration

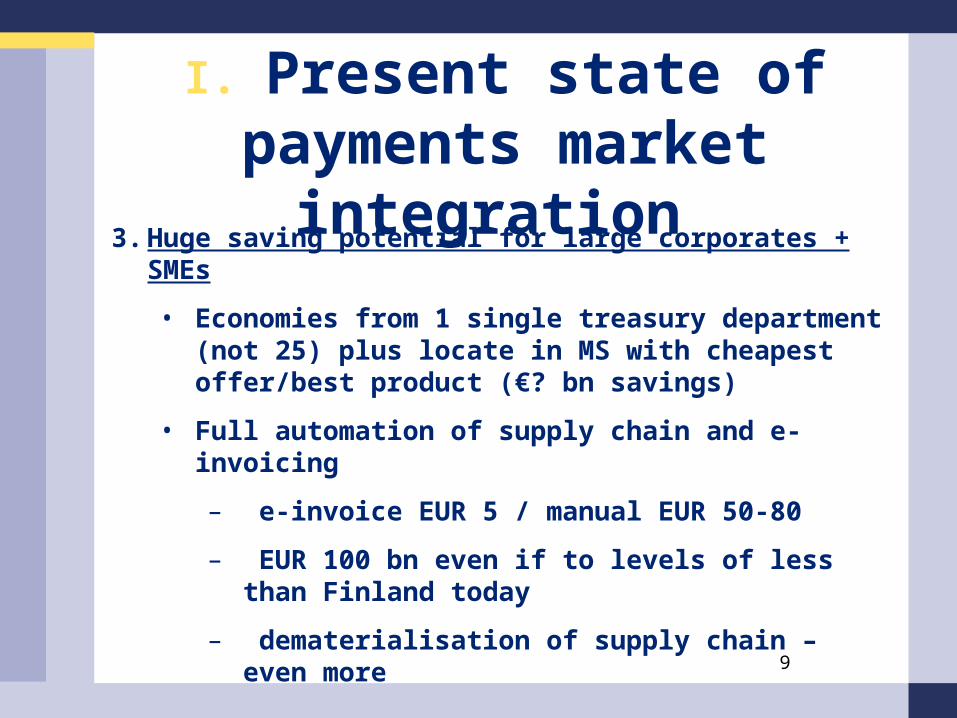

3. Huge saving potential for large corporates + SMEs

• Economies from 1 single treasury department (not 25) plus locate in MS with cheapest offer/best product (€? bn savings)

• Full automation of supply chain and e-invoicing

– e-invoice EUR 5 / manual EUR 50-80

– EUR 100 bn even if to levels of less than Finland today

– dematerialisation of supply chain – even more

10

I. Present state of payments market integration

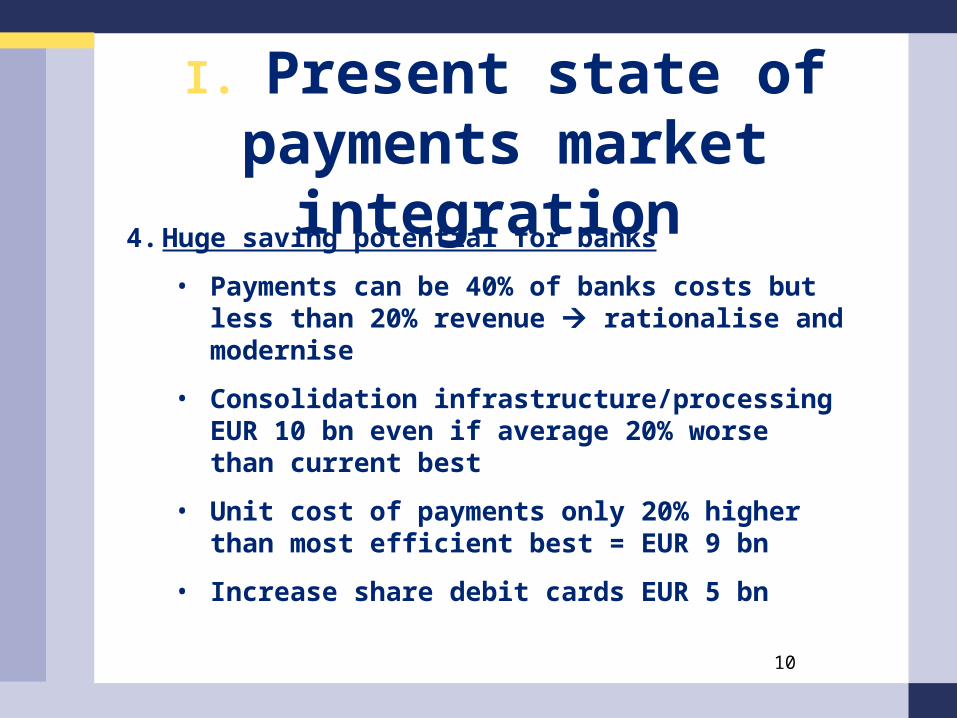

4. Huge saving potential for banks

• Payments can be 40% of banks costs but less than 20% revenue rationalise and modernise

• Consolidation infrastructure/processing EUR 10 bn even if average 20% worse than current best

• Unit cost of payments only 20% higher than most efficient best = EUR 9 bn

• Increase share debit cards EUR 5 bn

11

I. Present state of payments market integration

5. Huge saving potential for a society as a whole

• Cost of payments can be halved in 10 years

2% 1% GDP (e.g. Norway, Finland) (excludes e-invoicing savings)

i.e. 1% GDP saving every year

• Example of Lisbon economy

12

I. Present state of payments market integration

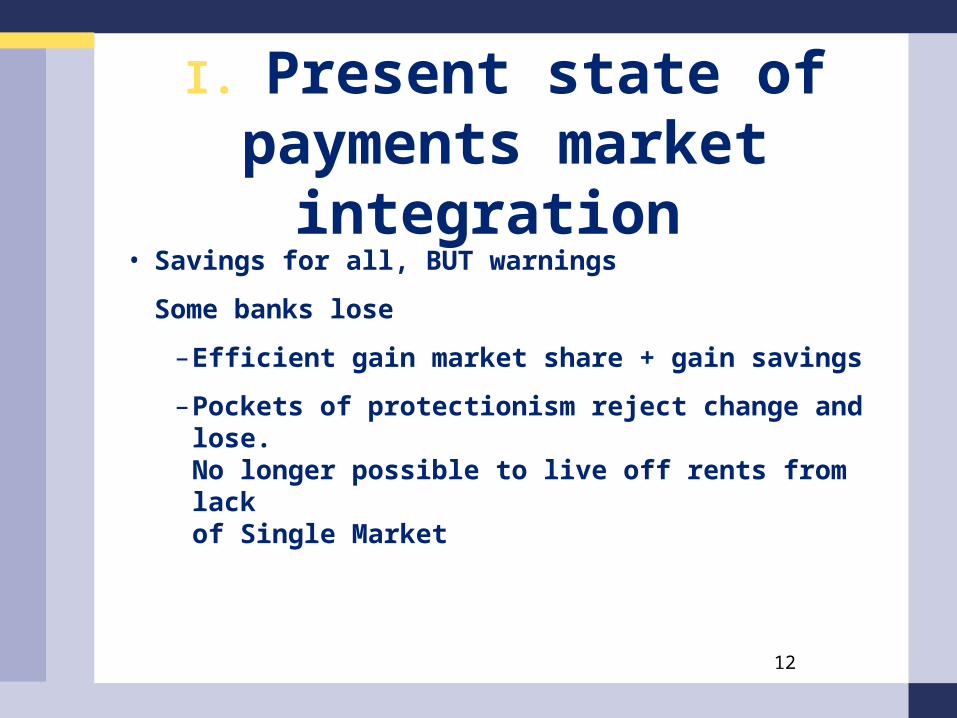

• Savings for all, BUT warnings

Some banks lose

–Efficient gain market share + gain savings

–Pockets of protectionism reject change and lose. No longer possible to live off rents from lack of Single Market

13

II. The visionCommission & ECB Joint Statement, May 2006

• integrated market: no distinction cross-border/national

• one single a/c in euro area enough

• improved efficiencies (competition & economies)

• forward-looking – best practices/level up and e-invoicing basis

• milestones

• support of users as early adoption (especially public sector)

• support EPC process/self-regulation

14

III. Role of industry – self-regulation is the key

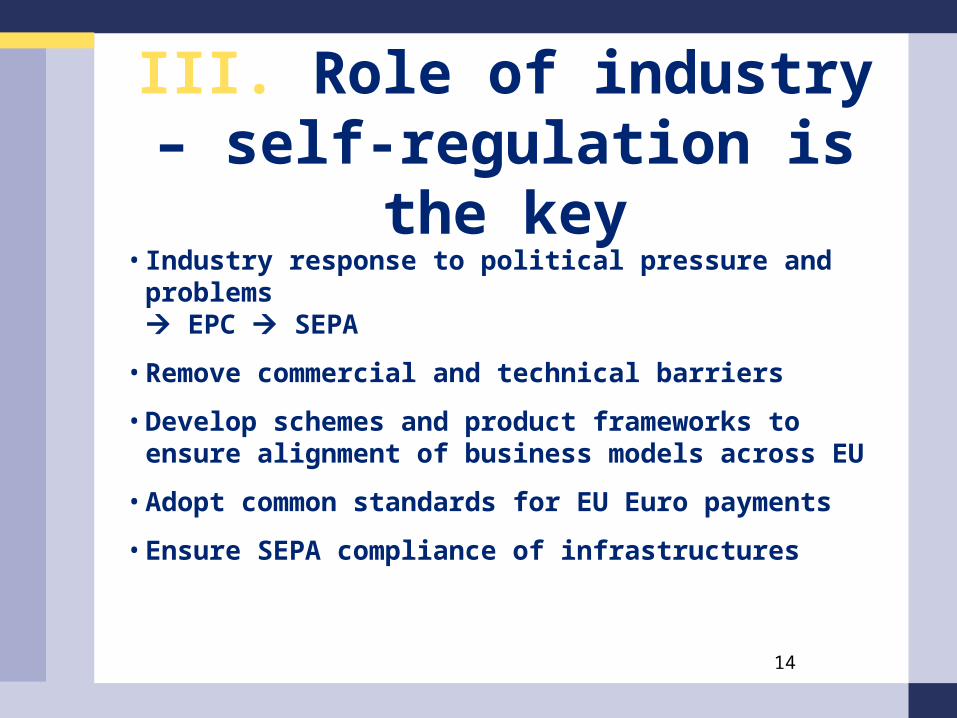

• Industry response to political pressure and problems EPC SEPA

• Remove commercial and technical barriers

• Develop schemes and product frameworks to ensure alignment of business models across EU

• Adopt common standards for EU Euro payments

• Ensure SEPA compliance of infrastructures

15

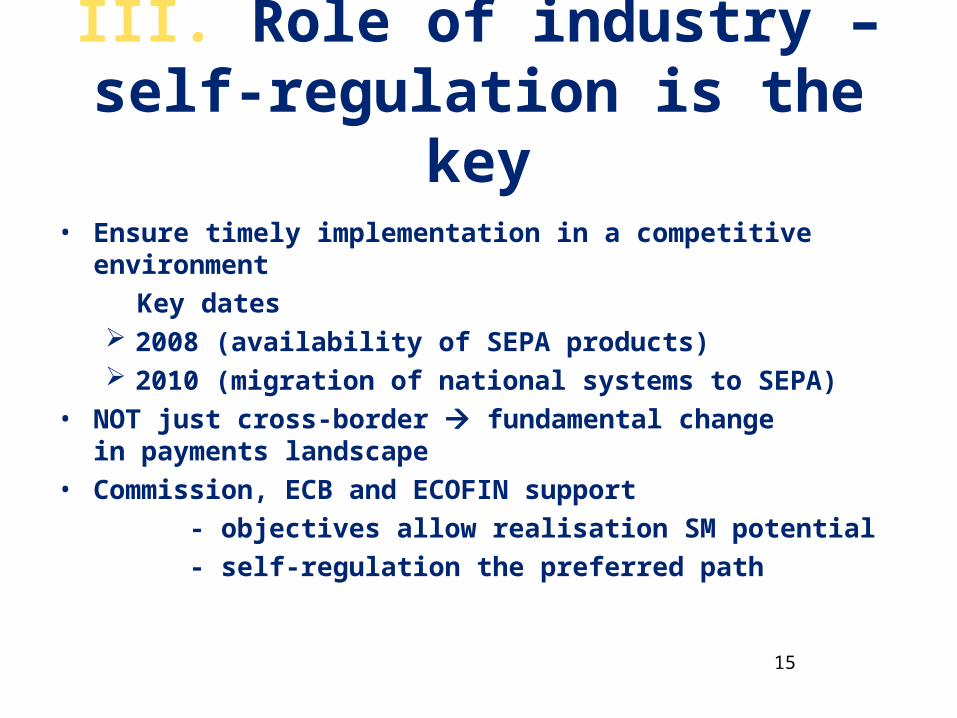

III. Role of industry – self-regulation is the key

• Ensure timely implementation in a competitive environment

Key dates 2008 (availability of SEPA products) 2010 (migration of national systems to SEPA)

• NOT just cross-border fundamental change in payments landscape

• Commission, ECB and ECOFIN support

- objectives allow realisation SM potential

- self-regulation the preferred path

16

IV. How can regulators help?

Commission proposal for the Payment Services Directive

Objectives and principles• Facilitate SEPA by removing legal barriers for

development of pan-European payment services

• Improve competition (remove market entry barriers and guarantee fair market access)

• Facilitate STP/efficiency

• Promote consumer confidence in modern payment instruments and protection

• Full harmonisation – no gold plating

• Min. regulation and max. self-regulation (=responsibility to industry)

17

IV. How can regulators help?

3 Pillars:

1. Market acces / new providers / prudential rules

(Increase competition)

2. Transparency / imformation requirements

(Allow customers to exercise choice)

3. Rights and obligations of users + providers

(Harmonise legal requirements)

18

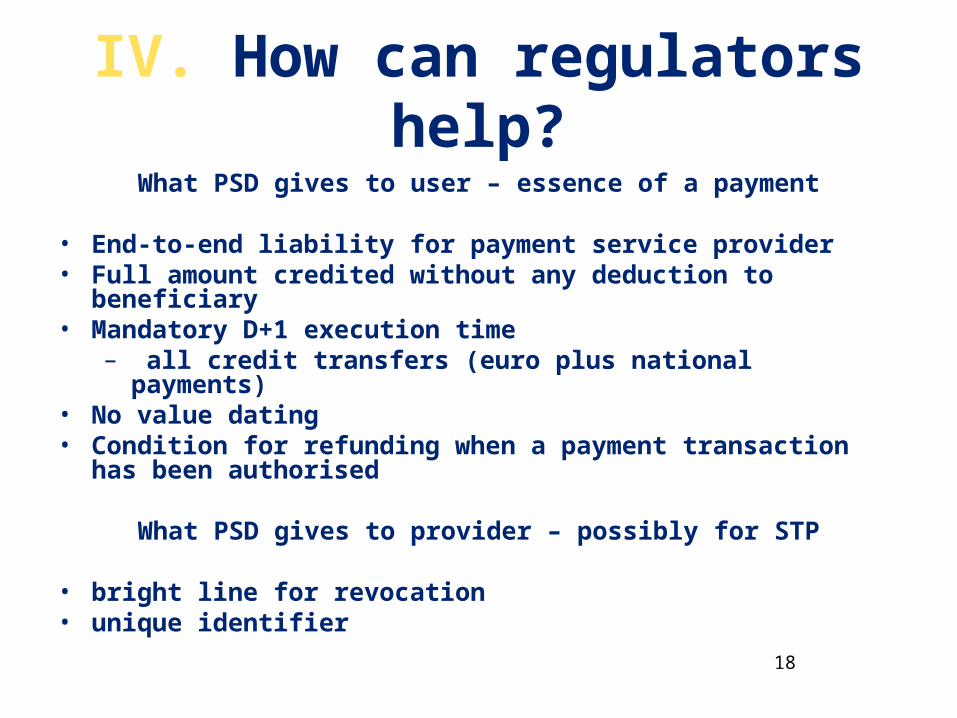

IV. How can regulators help?What PSD gives to user – essence of a payment

• End-to-end liability for payment service provider• Full amount credited without any deduction to beneficiary• Mandatory D+1 execution time

– all credit transfers (euro plus national payments)• No value dating• Condition for refunding when a payment transaction has been

authorised

What PSD gives to provider – possibly for STP

• bright line for revocation• unique identifier

19

V. ECOFIN Conclusions

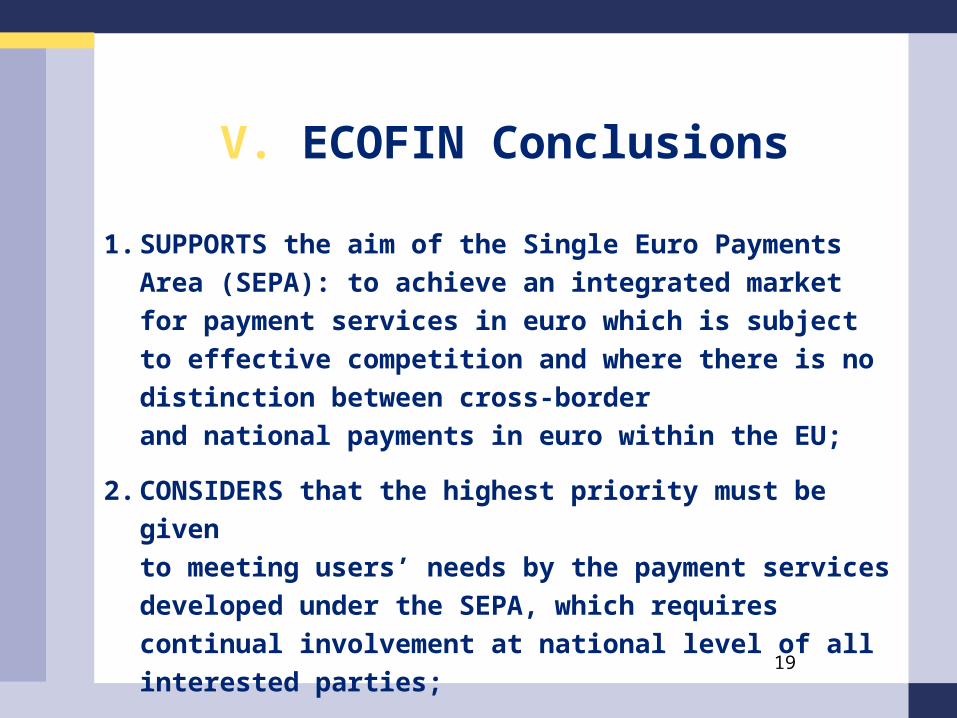

1. SUPPORTS the aim of the Single Euro Payments Area

(SEPA): to achieve an integrated market for payment

services in euro which is subject to effective competition

and where there is no distinction between cross-border

and national payments in euro within the EU;

2. CONSIDERS that the highest priority must be given

to meeting users’ needs by the payment services

developed under the SEPA, which requires continual

involvement at national level of all interested parties;

20

V. ECOFIN Conclusions

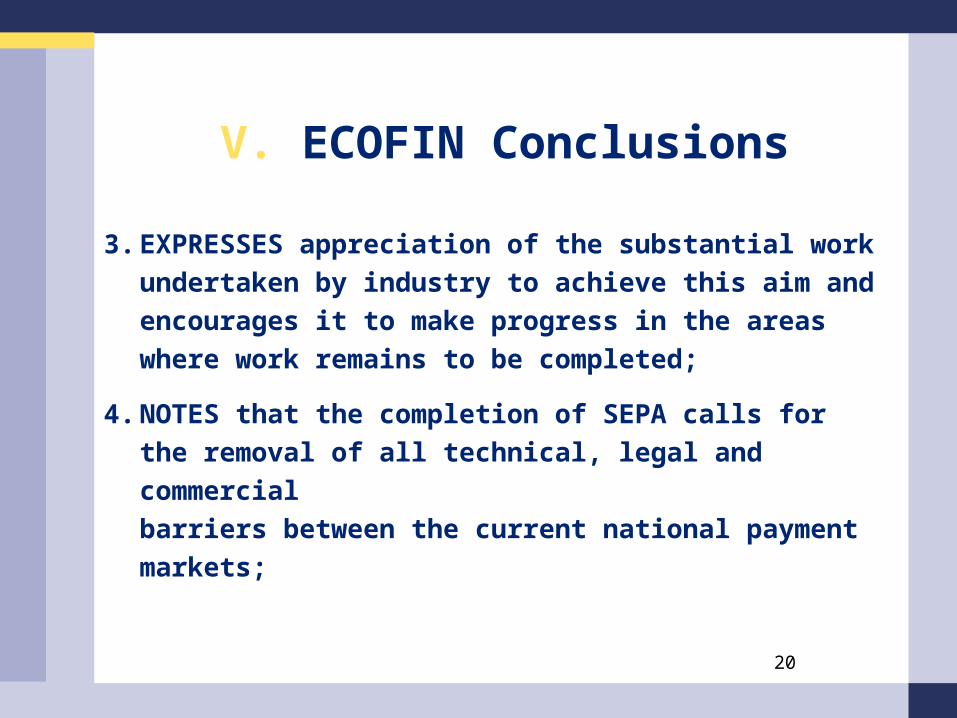

3. EXPRESSES appreciation of the substantial work

undertaken by industry to achieve this aim and

encourages it to make progress in the areas

where work remains to be completed;

4. NOTES that the completion of SEPA calls for

the removal of all technical, legal and commercial

barriers between the current national payment markets;

21

V. ECOFIN Conclusions

5. NOTES that continued attention is needed to ensure

that SEPA-payment services, including their supporting

technology and procedures, do not represent

a deterioration compared to the national cost and

service level in the most efficient Member States and

that SEPA products and services are offered in

a competitive environment;

6. STRESSES the importance of ensuring a level-playing field

as regards the application of competition principles to all

market participants, including new entrants to the payment

services market, and INVITES the Commission to continue

without delay, its work on this subject;

22

V. ECOFIN Conclusions

7. UNDERTAKES to work, together with the European

Parliament, towards a swift adoption of the Proposal

for a Directive on Payments Services;

8. WELCOMES that the Commission intends to come forward

with the final report regarding the sector enquiry into

competition in the retail banking market (which includes

payment cards) before the end of the year;

23

V. ECOFIN Conclusions

9. In order to facilitate commitment to an early use of SEPA,

INVITES Member States to carry out cost and benefit

analysis, where necessary, to check that SEPA products

are better or at least equivalent to existing products

in terms of price and quality, including as regards

the security of payments and INVITES the industry

to provide information to this end;

24

V. ECOFIN Conclusions

10. INVITES Finance Ministries of Member States to monitor

progress on SEPA at national level, with all interested

parties; as well as the Commission and the ECB

to continue monitoring the overall development,

together with the Financial Services Committee and

the Economic and Financial Committee, and report back

to the Council if progress is not satisfactory and

at the latest in 2008;

25

V. ECOFIN Conclusions

11. INVITES the Commission to assess the economic

and competition impacts of the SEPA taking into account

its planned time schedule; and;

12. INVITES the Commission to continue its work on

the next steps regarding the issues raised in its

consultative paper on SEPA, including the responses

to the public consultation, without delay.

26

VI. Where are we in the negotiation

COUNCIL

• High priority for Finnish Presidency

• Latest documents published by the Council

Proposal/Presidency compromise text (12285/06 of 28 August 2006)

Addendum to note from Presidency (13061/06 of 25 September 2006)

Note from the Presidency (13061/06 of 25 September 2006)

http://register.consilium.europa.eu

27

VI. Where are we in the negotiation

EUROPEAN PARLIAMENT

• Leading Committee: ECON (rapporteur Mr Jean Pièrre Gauzes Report voted on 12 September (285 amendments) http://www.europarl.europa.eu/omk/sipade3?PUBREF=-//EP//N

ONSGML+REPORT+A6-2006-0298+0+DOC+PDF+V0//EN&L=EN&LEVEL=1&NAV=S&LSTDOC=Y&LSTDOC=N

All parties working hard for rapid adoption through a first reading adoption

28

VI. Conclusions

• SEPA potential for economies huge

• Rapid adoption of Payment Services Directive: top priority

• Self-regulatory action by Industry for other barriers preferred approach – but

• SEPA too important to fail

29

Thank you very much for your attention!

Your questions are welcomed!

If you should need further information please contact:

Zuzana Kalivodova

Internal Market and Services DG

+32-2-299.58.01