Embed Size (px)

Citation preview

Welcome to the Gigabit era

Pierre-Michel ATTALI

Director of the

Digital Territories Business unit, IDATE

Future Networks Forum

18 November 2015

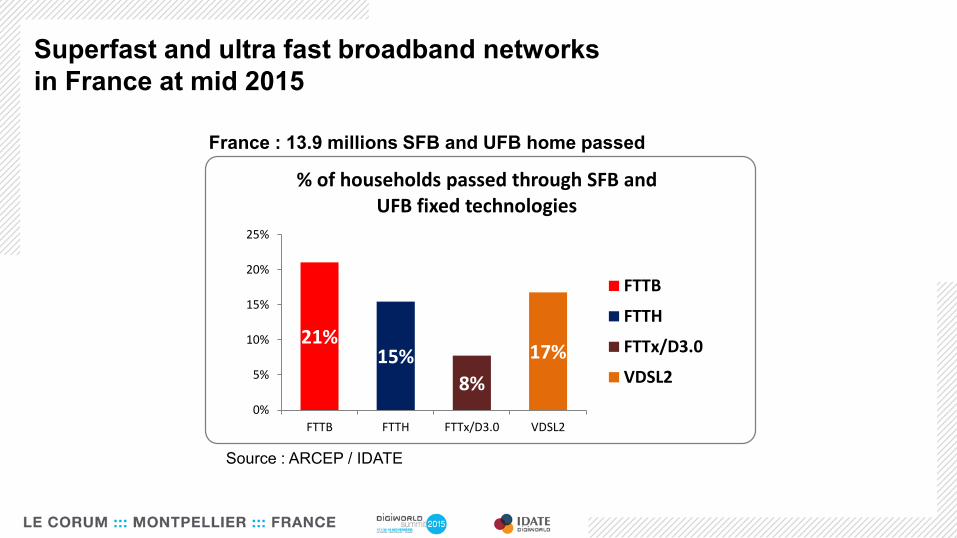

Superfast and ultra fast broadband networks

in France at mid 2015

France : 13.9 millions SFB and UFB home passed

Source : ARCEP / IDATE

21%15%

8%

17%

0%

5%

10%

15%

20%

25%

FTTB FTTH FTTx/D3.0 VDSL2

% of households passed through SFB and UFB fixed technologies

FTTB

FTTH

FTTx/D3.0

VDSL2

Superfast and ultra fast broadband networks

in France at mid 2015

France : 3.84 millions SFB and UFB subscribers

30%

26%15%

29%FTTH

FTTB

FTTx/D3.0

VDSL

Breakdown of SFB and UFB subscribers

Source : ARCEP / IDATE

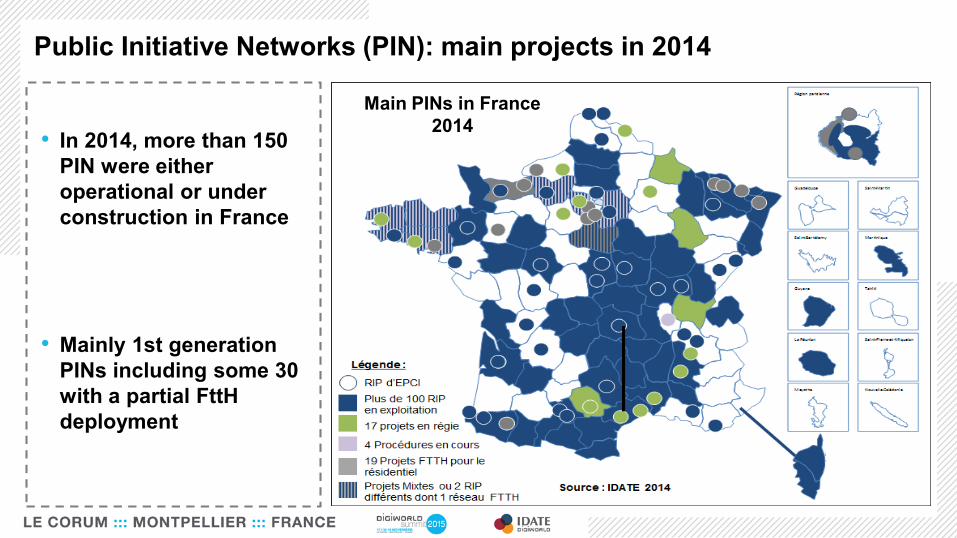

Public Initiative Networks (PIN): main projects in 2014

Main PINs in France

2014• In 2014, more than 150

PIN were either

operational or under

construction in France

• Mainly 1st generation

PINs including some 30

with a partial FttH

deployment

Impact of PIN market players in 2014

Companies involved in PINs in 2014 (jobs and turnover)

• Extremely dynamic sector in terms of

job creation: over 82% of firms expect to

increase their (full time, open ended and

set term contract) employees over the

next three years

• A more than 91% increase in jobs

between 2010 and 2014 (representing

over 5,000 jobs in 2014)

Impact of PINs: Job creation

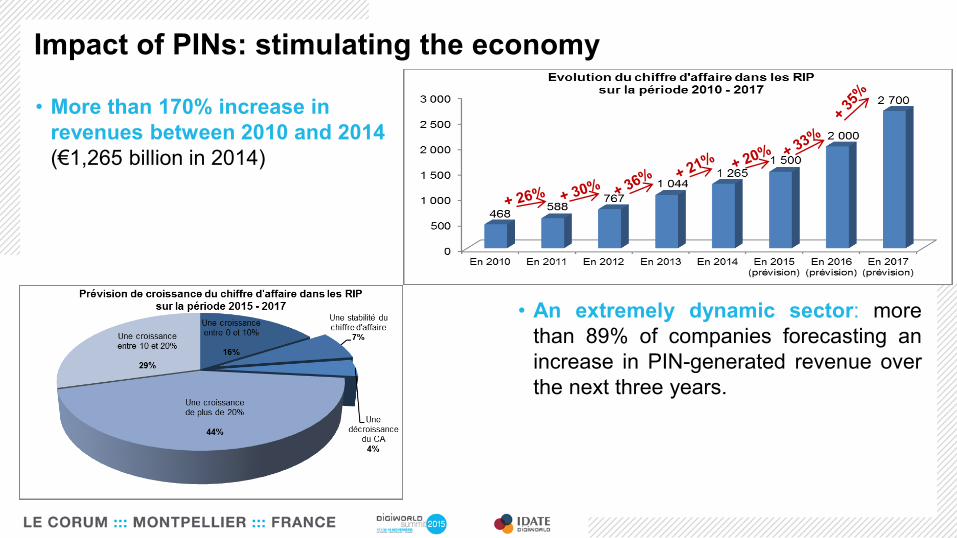

• More than 170% increase in

revenues between 2010 and 2014

(€1,265 billion in 2014)

• An extremely dynamic sector: more

than 89% of companies forecasting an

increase in PIN-generated revenue over

the next three years.

Impact of PINs: stimulating the economy

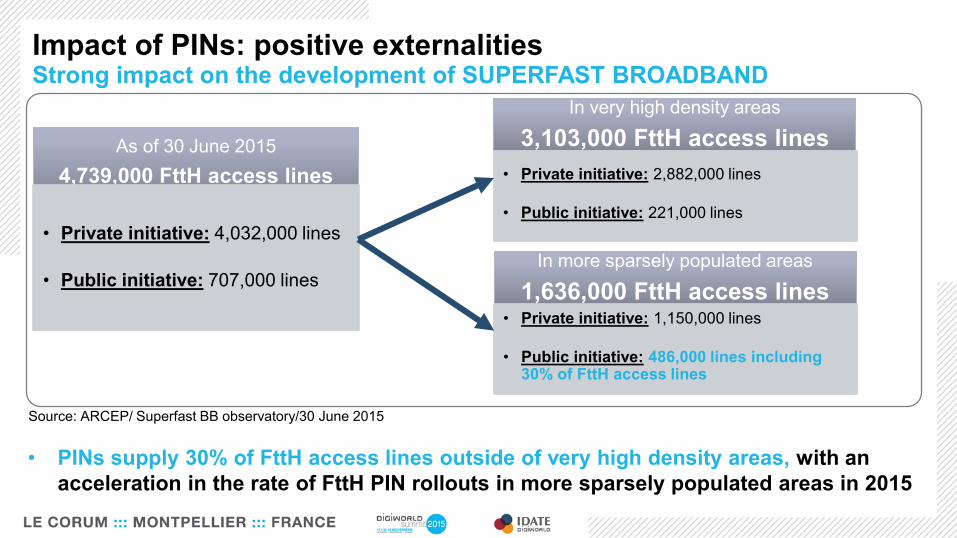

As of 30 June 2015

4,739,000 FttH access lines

• Private initiative: 4,032,000 lines

• Public initiative: 707,000 lines

In very high density areas

3,103,000 FttH access lines

• Private initiative: 2,882,000 lines

• Public initiative: 221,000 lines

In more sparsely populated areas

1,636,000 FttH access lines• Private initiative: 1,150,000 lines

• Public initiative: 486,000 lines including 30% of FttH access lines

• PINs supply 30% of FttH access lines outside of very high density areas, with an

acceleration in the rate of FttH PIN rollouts in more sparsely populated areas in 2015

Source: ARCEP/ Superfast BB observatory/30 June 2015

Impact of PINs: positive externalities Strong impact on the development of SUPERFAST BROADBAND

• PINs make it possible to attract operators and

so offer end users a larger selection of

products.

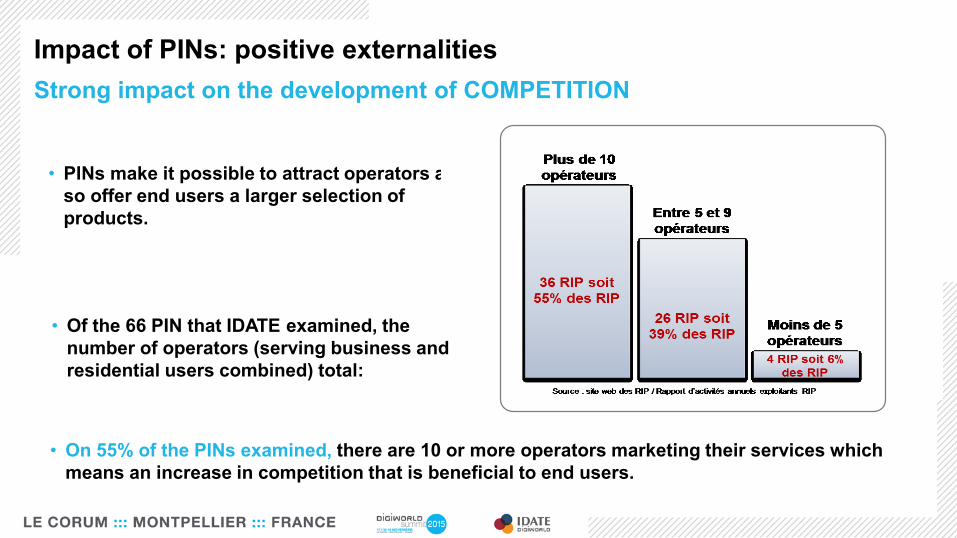

• On 55% of the PINs examined, there are 10 or more operators marketing their services which

means an increase in competition that is beneficial to end users.

Impact of PINs: positive externalities

• Of the 66 PIN that IDATE examined, the

number of operators (serving business and

residential users combined) total:

Strong impact on the development of COMPETITION

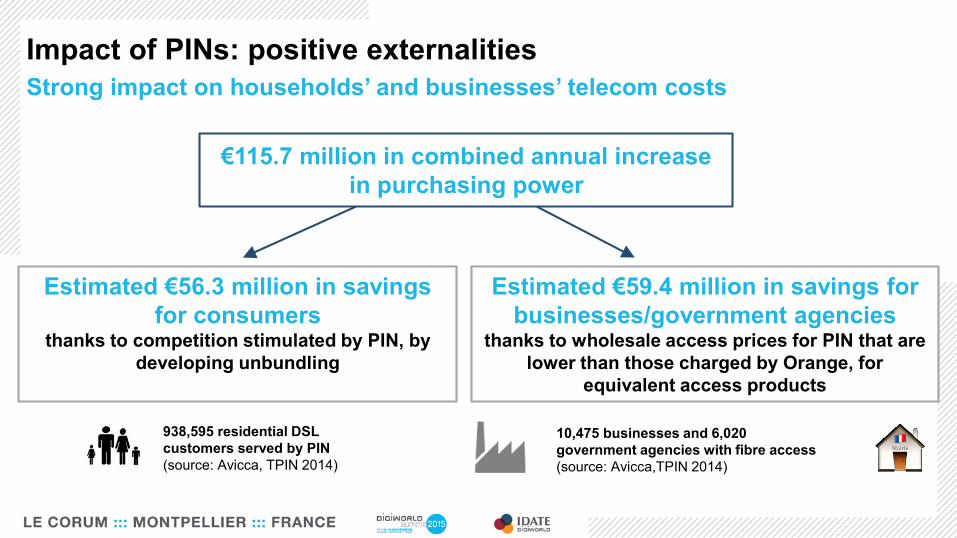

€115.7 million in combined annual increase

in purchasing power

Impact of PINs: positive externalities

938,595 residential DSL

customers served by PIN

(source: Avicca, TPIN 2014)

Estimated €56.3 million in savings

for consumersthanks to competition stimulated by PIN, by

developing unbundling

Estimated €59.4 million in savings for

businesses/government agenciesthanks to wholesale access prices for PIN that are

lower than those charged by Orange, for

equivalent access products

10,475 businesses and 6,020

government agencies with fibre access

(source: Avicca,TPIN 2014)

Strong impact on households’ and businesses’ telecom costs

In municipalities with a population of over 500: an overall correlation between the presence of a PIN

and a lower rate of unemployment and a higher rate of new businesses creation than in equivalent size

towns not covered by a PIN.

Impact of PINs: positive externalities

Average number of new businesses (Source: INSEE

2013)

Average unemployment rate

(Source: INSEE 2011)

In municipalities with

optical fibre supplied by a

PIN

In municipalities without

optical fibre supplied by a

PIN

In municipalities with

optical fibre supplied by

a PIN

In municipalities without

optical fibre supplied by a

PIN

Municipalities with a population of between 500

and 2,000 (11,608 municipalities)6.83 5.90 7.14% 7.30%

Municipalities with a population of between

2,000 and 4,999 (3,060 municipalities)22.09 21.26 7.80% 8.56%

Municipalities with a population of between

5,000 and 9,999 (1,073 municipalities)52.77 50.77 9.18% 9.89%

Municipalities with a population of between

10,000 and 49,999 (783 municipalities)175.05 15.80 10.85% 11.81%

Municipalities with a population of between

50,000 and 200,000 (103 municipalities)826.78 689.59 12.06% 13.61%

Stimulating jobs and new BUSINESSES

![[FR] PR Hangout of the DigiWorld Summit 2015 - #DWS15](https://img.pdfslide.us/doc/110x75/58e669e91a28ab8d758b62db/fr-pr-hangout-of-the-digiworld-summit-2015-dws15.jpg)