Embed Size (px)

Citation preview

HEALTH INFORMATION TECHNOLOGIES

Market Overview and Trends

Pawel Suwinski2nd Annual Asia EHR Conference2010, Singapore

2

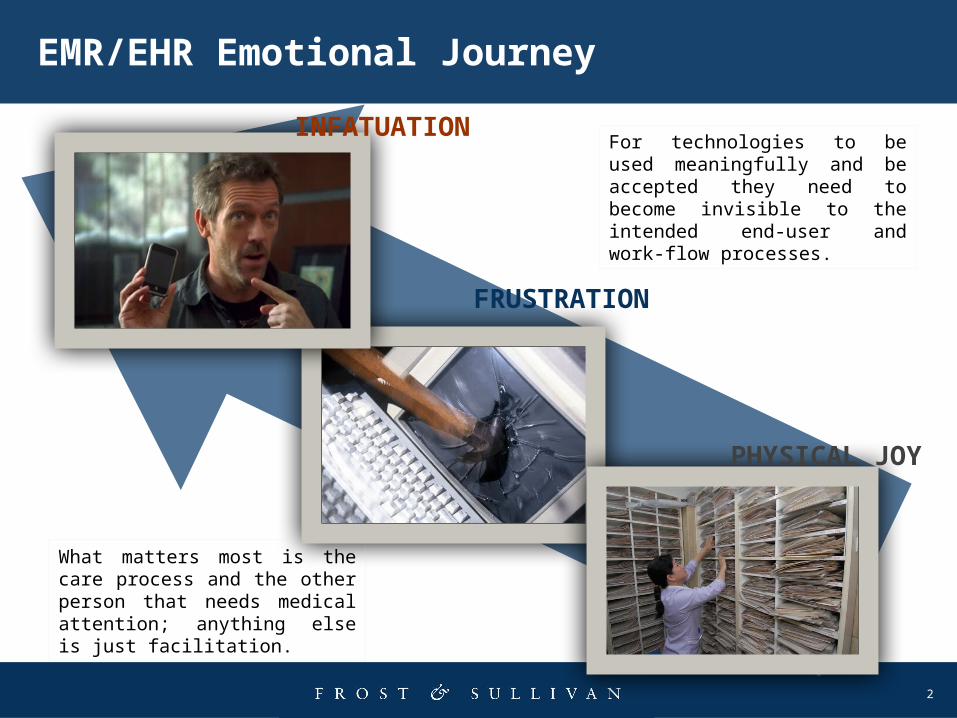

EMR/EHR Emotional Journey

PHYSICAL JOY

FRUSTRATION

INFATUATIONFor technologies to be used meaningfully and be accepted they need to become invisible to the intended end-user and work-flow processes.

What matters most is the care process and the other person that needs medical attention; anything else is just facilitation.

3

HIT ADOPTION AND GROWTH DRIVERS

4

HIT Adoption and Growth Drivers

• HIT will experience healthy growth in the next 3 years. This high growth path will be possible thanks to 3 main factors

– Innovations

– Government Spending

– Healthcare Demand

• Innovations play a crucial role in blending technologies into healthcare processes. They also are drivers of healthcare services transformation.

• Most regional governments recognised the importance of HIT and are rolling out national programs promoting the adoption of HIT, in most cases as EHR.

• Healthcare Demand will be constantly on the rise as a result of Epidemiological, Demographic, and Life-Style changes.

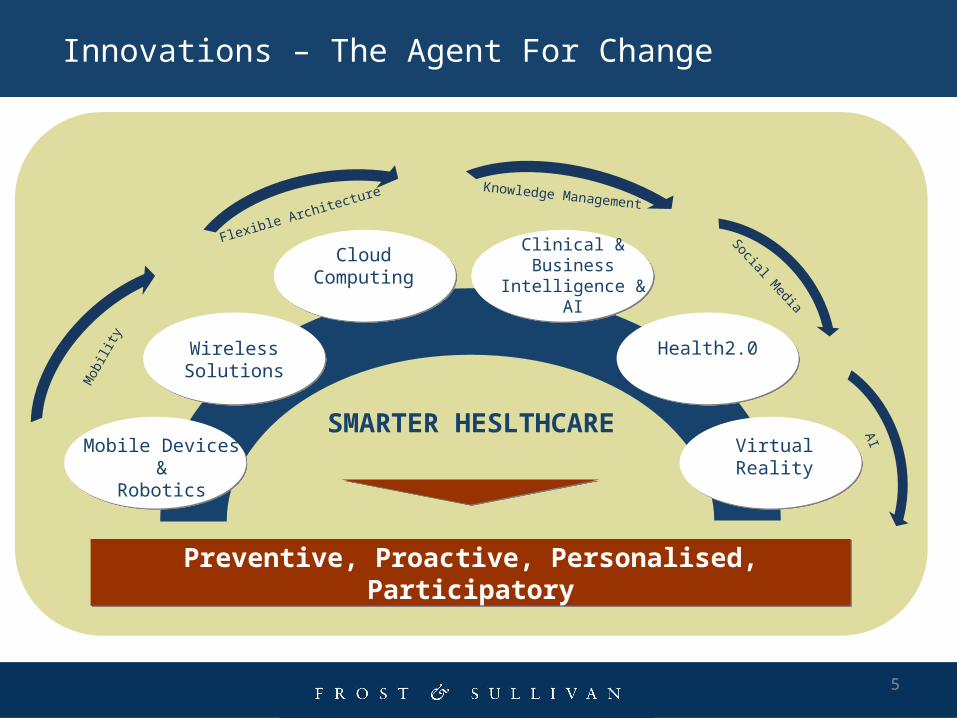

SMARTER HESLTHCARE

Innovations – The Agent For Change

Wireless Solutions

Virtual Reality

Cloud Computing

Health2.0

Preventive, Proactive, Personalised, ParticipatoryPreventive, Proactive, Personalised, Participatory

Mobile Devices &Robotics

Clinical & Business Intelligence & AI

Knowledge Management

Mob

ility

Social Media

5

Flexible Architecture

AI

Global Trends on Governments HIT/HER Initiatives

6

Singapore USD 140 million - National Electronic Health Record (NEHR) project / 10 yrs

Hong KongUSD 184 million – E-Health Programme. The first phase of the project is budgeted at USD 98m from 2010 to 2014. E-Health Record Office to be established with total recurrent spending of about USD 45m for the years 2010 to 2012.

AustraliaUSD 470 million – Under NEHTA guidance to develop Personally Controlled Electronic Health Record.

Malaysia USD 27 million – Telehealth Programme: started 1997 . Halted in 2003 and reactivated in 2007. National roll-out by 2020.

ChinaUSD 1.8 billion of total HIT investment pledged. Government published EHR policy in 2009.EHR projects are now expanded to each province Japan

In 2001, “GrandDesign for the Development of Information Systems in the Health care and Medical Fields”, targeting for EHR to at least 60 % of Japan's hospitals with 400 or more beds by2006. (Actual 10% in 2010)

South KoreaUSD 46 million– National Healthcare Information Infrastructure Plan to include development of EHR and interoperability standards (2007 to 2010)

USUSD 19 billion– Meaningful Use of EHR.

EuropeUnited Kingdom : USD 12 billion – The National Programme for IT (NPfIT) from 2002 for 8 to 10 yearsDenmark – National EHR since 2006France –EHR mandatory by 2008The Netherlands – 88 percent of GPs has an EHRSweden – Developing National EHRGermany – E-Health card since January 2007 Thailand

No legislation governing the use of EMR/EHR in the country. Less than 50% EHR utilization, mostly in public health institutions. USD 140 million – To revolutionize public hospital information system

CanadaUSD 1.2 billion – to set up National EHR

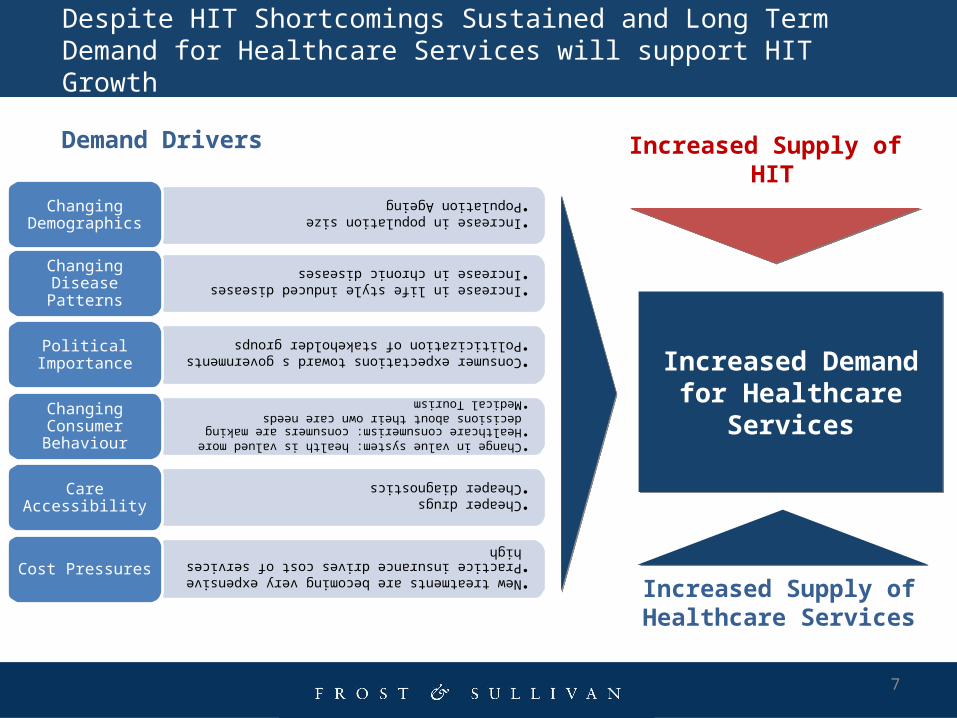

Despite HIT Shortcomings Sustained and Long Term Demand for Healthcare Services will support HIT Growth

7

•Increase in population size

•Population Ageing

Changing Demographics

•Increase in life style induced diseases

•Increase in chronic diseases

Changing Disease Patterns

•Consumer expectations toward s governments

•Politicization of stakeholder groups

Political Importance

•Change in value system: health is valued more

•Healthcare consumerism: consumers are making decisions about their own care needs

•Medical Tourism

Changing Consumer Behaviour

•Cheaper drugs

•Cheaper diagnostics

Care Accessibility

•New treatments are becoming very expensive

•Practice insurance drives cost of services high

Cost Pressures

Increased Demand for Healthcare Services

Increased Demand for Healthcare Services

Demand Drivers

Increased Supply of Healthcare Services

Increased Supply of HIT

CHALLENGES TO HIT ADOPTION

8

9

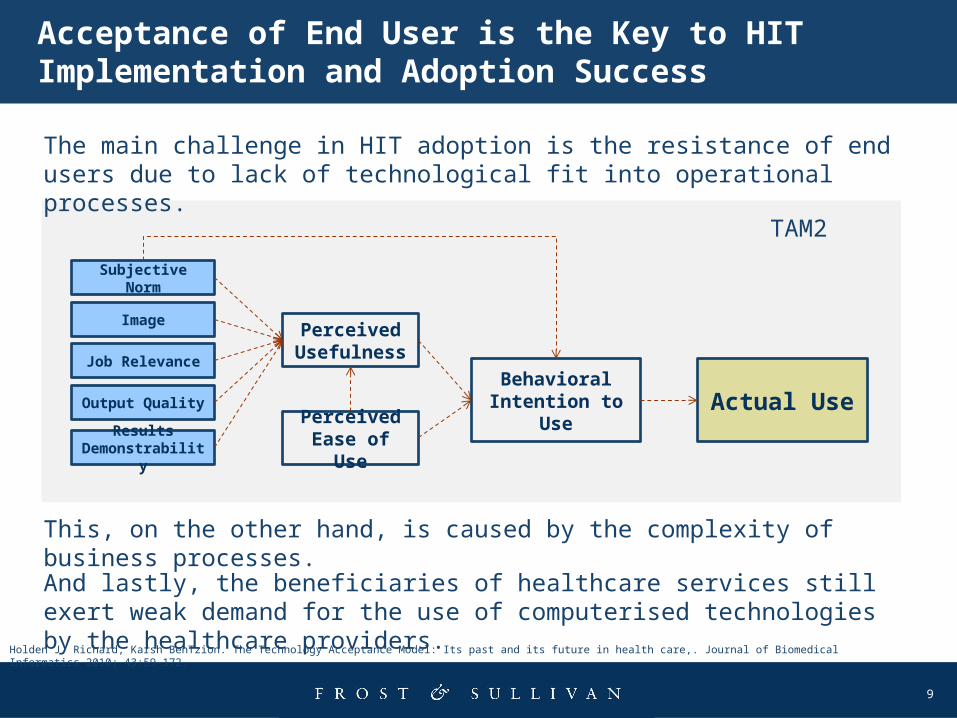

Acceptance of End User is the Key to HIT Implementation and Adoption Success

Actual UseBehavioral Intention to Use

Perceived Usefulness

Perceived Ease of Use

Subjective Norm

Image

Job Relevance

Output Quality

Results Demonstrability

The main challenge in HIT adoption is the resistance of end users due to lack of technological fit into operational processes.

This, on the other hand, is caused by the complexity of business processes.

And lastly, the beneficiaries of healthcare services still exert weak demand for the use of computerised technologies by the healthcare providers.

TAM2

Holden J. Richard, Karsh BenTzion. The Technology Acceptance Model: Its past and its future in health care,. Journal of Biomedical Informatics 2010; 43:59-172.

10

Technology Must Be Invisible to the End User

• Despite Healthcare Delivery Industry having much to gain from Information and Communication Technologies, it is the slowest from all industries in the adoption. There are many reasons for IT failures in healthcare environment, but the single most important cause is the HIT capability mismatch to address work processes within healthcare service organisation.

• Until today, for more than 20 years ICT and healthcare service organisations have been locked in a Love-&-Hate affair with neither being able the break the stalemate. It could be down to that we spent too much time on design and implementation and not on how end user react to already implemented HIT solutions.

• HIT investment will only be successful if the fit between IT and clinical processes will be close to matching, which will be reflected by the acceptance or rejection of end users.

• In the short history of HIT the emergence of new, disruptive technologies play a crucial role in closing the capability gap and gaining more acceptance from the main users.

• The latest innovations are changing not only how the medical care is organised, practiced and delivered but are also redefining host of other qualities including changing patient-physician model and facilitating the emergence of new industry players within the value chain.

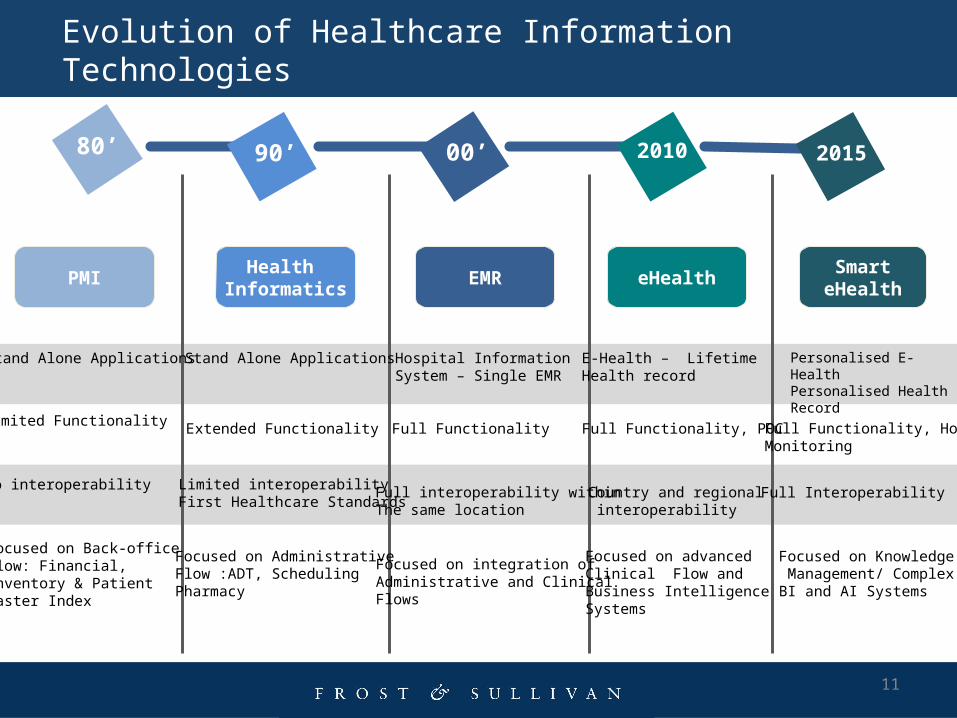

Evolution of Healthcare Information Technologies

PMI EMR eHealthSmart

eHealth

80’ 90’ 00’ 2010 2015

Health Informatics

Stand Alone Applications

Limited Functionality

Focused on Back-office Flow: Financial,Inventory & Patient Master Index

No interoperability

Stand Alone Applications

Extended Functionality

Focused on Administrative Flow :ADT, SchedulingPharmacy

Limited interoperabilityFirst Healthcare Standards

Hospital Information System – Single EMR

Full Functionality

Focused on integration of Administrative and ClinicalFlows

Full interoperability withinThe same location

E-Health – Lifetime Health record

Full Functionality, POC

Focused on advanced Clinical Flow and Business Intelligence Systems

Country and regional interoperability

Personalised E-HealthPersonalised Health Record

Full Functionality, HomeMonitoring

Focused on Knowledge Management/ Complex BI and AI Systems

Full Interoperability

11

12

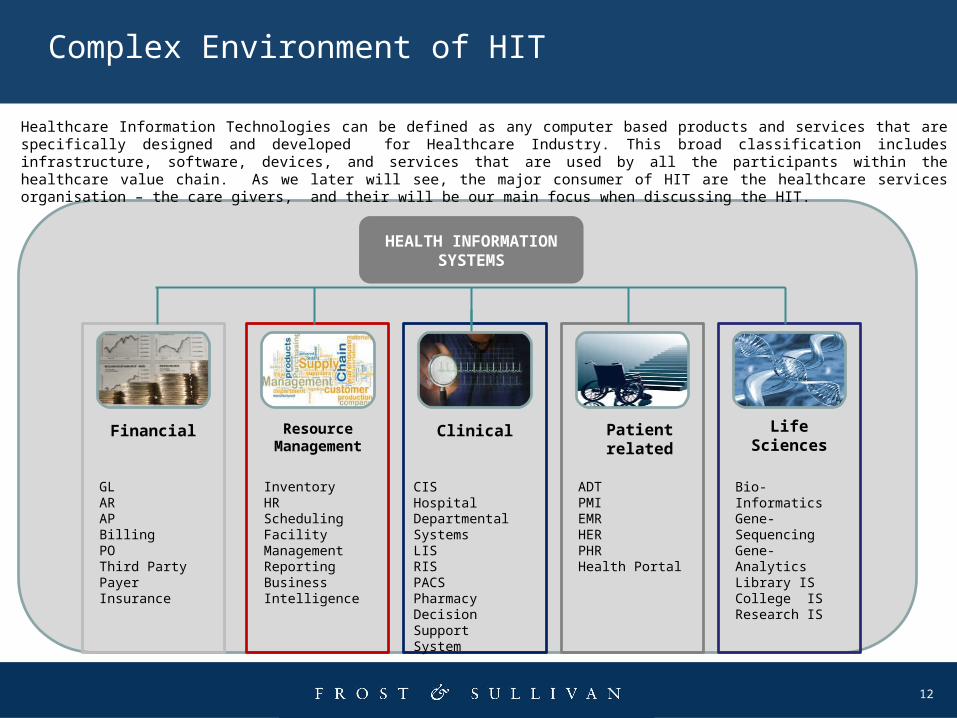

Complex Environment of HIT

Financial

GLARAPBillingPOThird Party PayerInsurance

Resource Management

Clinical Patient related

Life Sciences

Bio-InformaticsGene-SequencingGene-AnalyticsLibrary ISCollege ISResearch IS

ADTPMIEMRHERPHRHealth Portal

CISHospital Departmental Systems LISRISPACSPharmacyDecision Support System

InventoryHRSchedulingFacility ManagementReportingBusiness Intelligence

HEALTH INFORMATION SYSTEMS

Healthcare Information Technologies can be defined as any computer based products and services that are specifically designed and developed for Healthcare Industry. This broad classification includes infrastructure, software, devices, and services that are used by all the participants within the healthcare value chain. As we later will see, the major consumer of HIT are the healthcare services organisation – the care givers, and their will be our main focus when discussing the HIT.

13

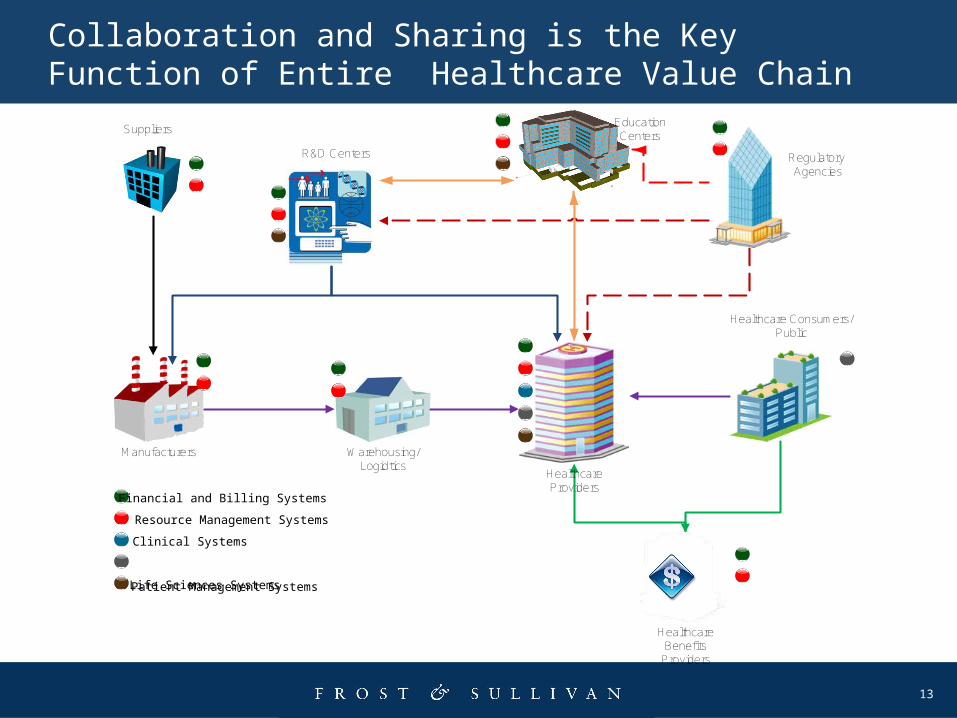

Warehousing/Logidtics

Manufacturers

Healthcare Providers

Healthcare Benefits

Providers

Healthcare Consumers/Public

Regulatory Agencies

R&D Centers

Education Centers

Suppliers

Financial and Billing Systems

Resource Management Systems

Clinical Systems

Life Sciences Systems

Collaboration and Sharing is the Key Function of Entire Healthcare Value Chain

Patient Management Systems

14

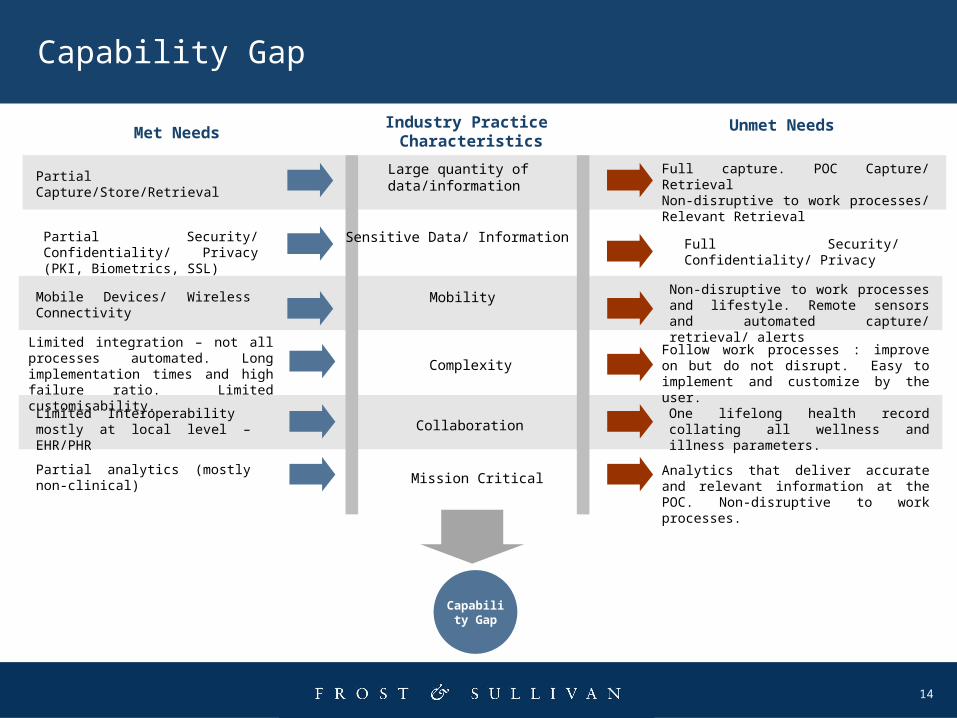

Capability Gap

Capability Gap

Industry Practice Characteristics

Unmet Needs

Large quantity of data/information

Met Needs

Partial Capture/Store/RetrievalFull capture. POC Capture/ RetrievalNon-disruptive to work processes/ Relevant Retrieval

Sensitive Data/ InformationPartial Security/ Confidentiality/ Privacy (PKI, Biometrics, SSL)

Full Security/ Confidentiality/ Privacy

MobilityMobile Devices/ Wireless Connectivity

Non-disruptive to work processes and lifestyle. Remote sensors and automated capture/ retrieval/ alerts

Complexity

Collaboration

Mission Critical

Follow work processes : improve on but do not disrupt. Easy to implement and customize by the user.

One lifelong health record collating all wellness and illness parameters.

Analytics that deliver accurate and relevant information at the POC. Non-disruptive to work processes.

Limited integration – not all processes automated. Long implementation times and high failure ratio. Limited customisability.

Limited Interoperability mostly at local level – EHR/PHR

Partial analytics (mostly non-clinical)

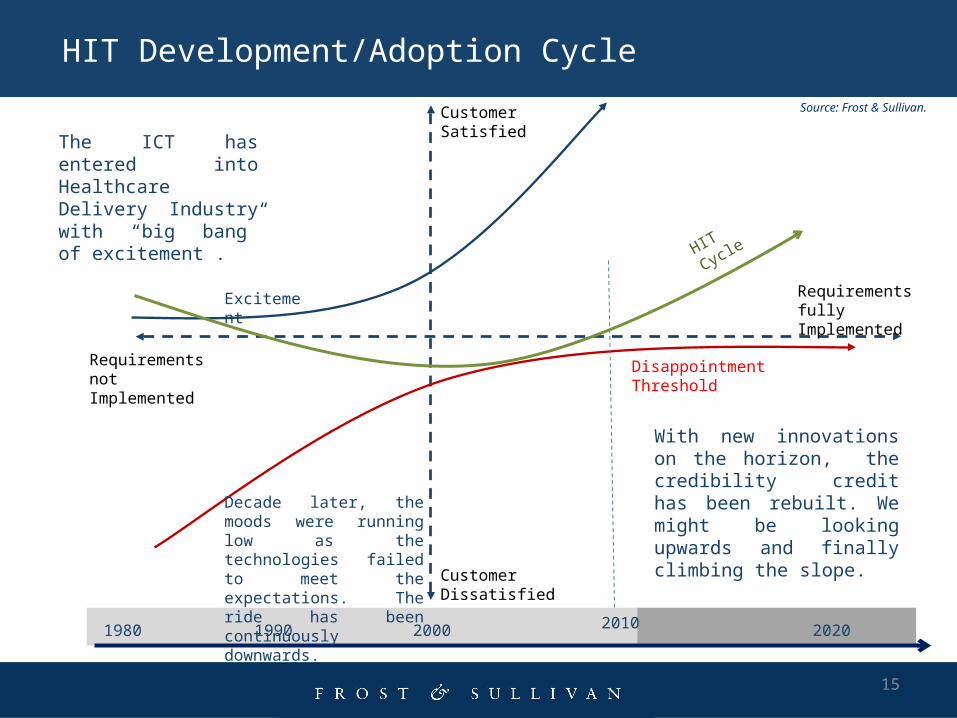

HIT Development/Adoption Cycle

Excitement

Disappointment Threshold

Requirements fully Implemented

Requirements not Implemented

Customer Satisfied

Customer Dissatisfied

Source: Frost & Sullivan.

1980 1990 2000 2010 2020

HIT Cycle

The ICT has entered into Healthcare Delivery Industry with “big bang” of excitement .

Decade later, the moods were running low as the technologies failed to meet the expectations. The ride has been continuously downwards.

With new innovations on the horizon, the credibility credit has been rebuilt. We might be looking upwards and finally climbing the slope.

15

MARKET OVERVIEW

16

17

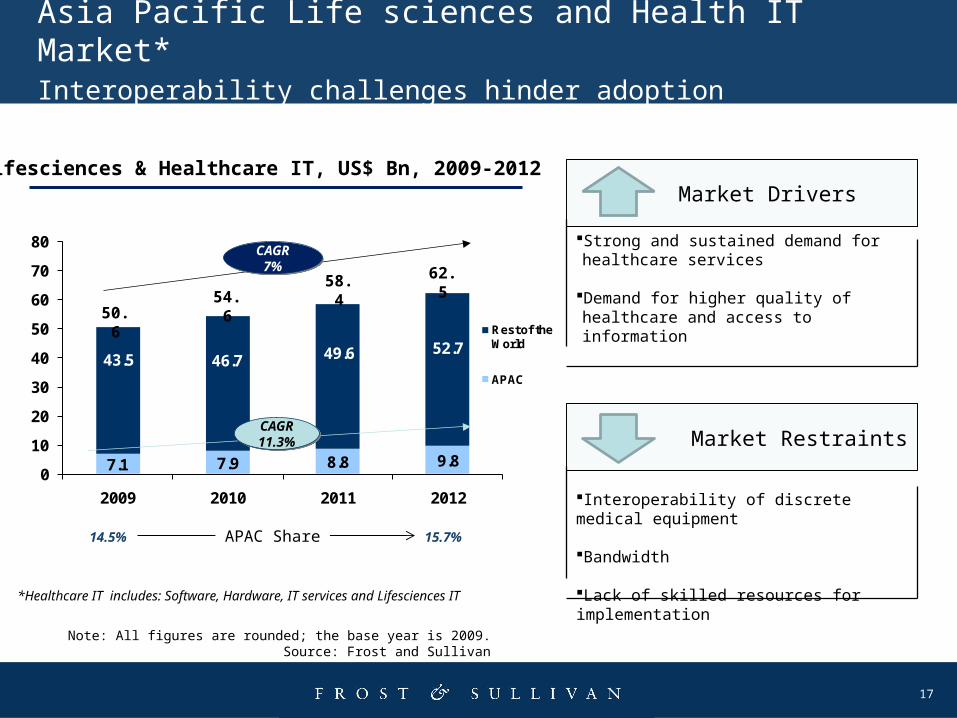

Note: All figures are rounded; the base year is 2009. Source: Frost and Sullivan

*Healthcare IT includes: Software, Hardware, IT services and Lifesciences IT

Asia Pacific Life sciences and Health IT Market*Interoperability challenges hinder adoption

7.1 7.9 8.8 9.8

43.5 46.7 49.6 52.7

0

10

20

30

40

50

60

70

80

2009 2010 2011 2012

Rest of the World

APAC

14.5% 15.7%

Market Drivers

Market Restraints

Strong and sustained demand for healthcare services

Demand for higher quality of healthcare and access to information

Interoperability of discrete medical equipment

Bandwidth

Lack of skilled resources for implementation

Lifesciences & Healthcare IT, US$ Bn, 2009-2012

CAGR7%

CAGR7%

CAGR11.3%CAGR11.3%

APAC Share

50.654.6

58.4 62.5

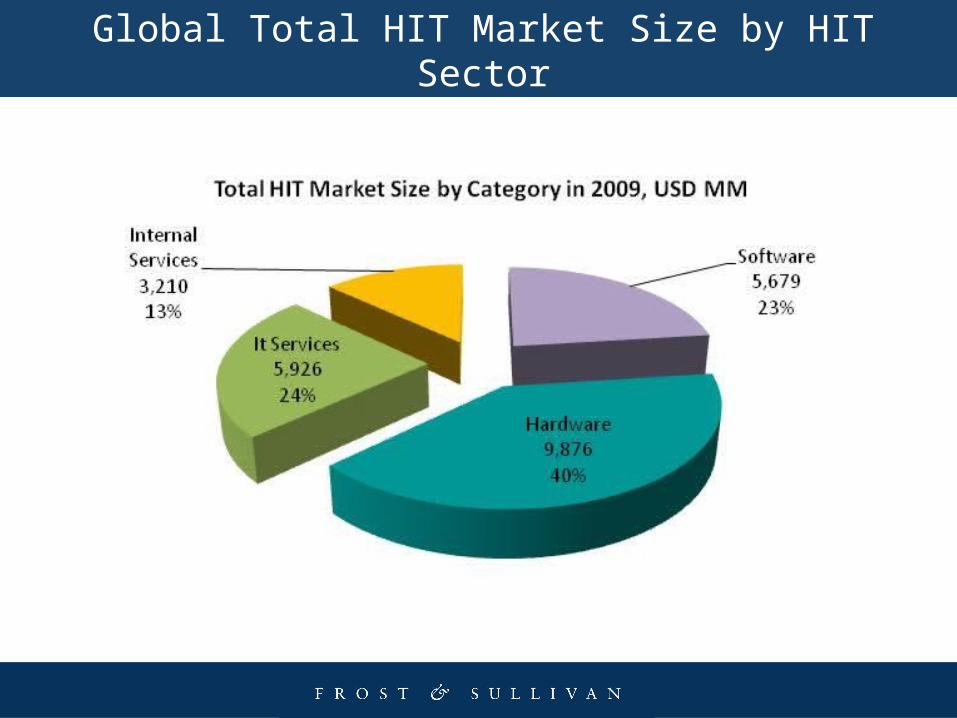

Global Total HIT Market Size by HIT Sector

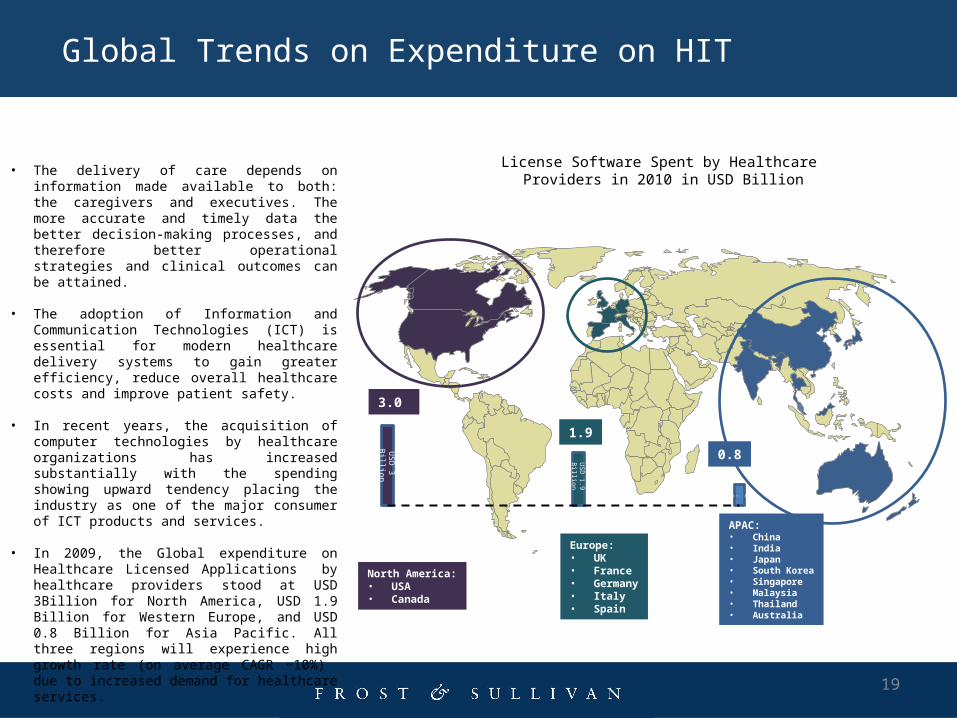

Global Trends on Expenditure on HIT

19

USD

3 Billion

US

D 1.9

Billion

0.8

North America:• USA• Canada

Europe:• UK• France• Germany• Italy• Spain

APAC:• China• India• Japan• South Korea• Singapore• Malaysia• Thailand• Australia

• The delivery of care depends on information made available to both: the caregivers and executives. The more accurate and timely data the better decision-making processes, and therefore better operational strategies and clinical outcomes can be attained.

• The adoption of Information and Communication Technologies (ICT) is essential for modern healthcare delivery systems to gain greater efficiency, reduce overall healthcare costs and improve patient safety.

• In recent years, the acquisition of computer technologies by healthcare organizations has increased substantially with the spending showing upward tendency placing the industry as one of the major consumer of ICT products and services.

• In 2009, the Global expenditure on Healthcare Licensed Applications by healthcare providers stood at USD 3Billion for North America, USD 1.9 Billion for Western Europe, and USD 0.8 Billion for Asia Pacific. All three regions will experience high growth rate (on average CAGR ~10%) due to increased demand for healthcare services.

License Software Spent by Healthcare Providers in 2010 in USD Billion

3.0

1.9

0.8

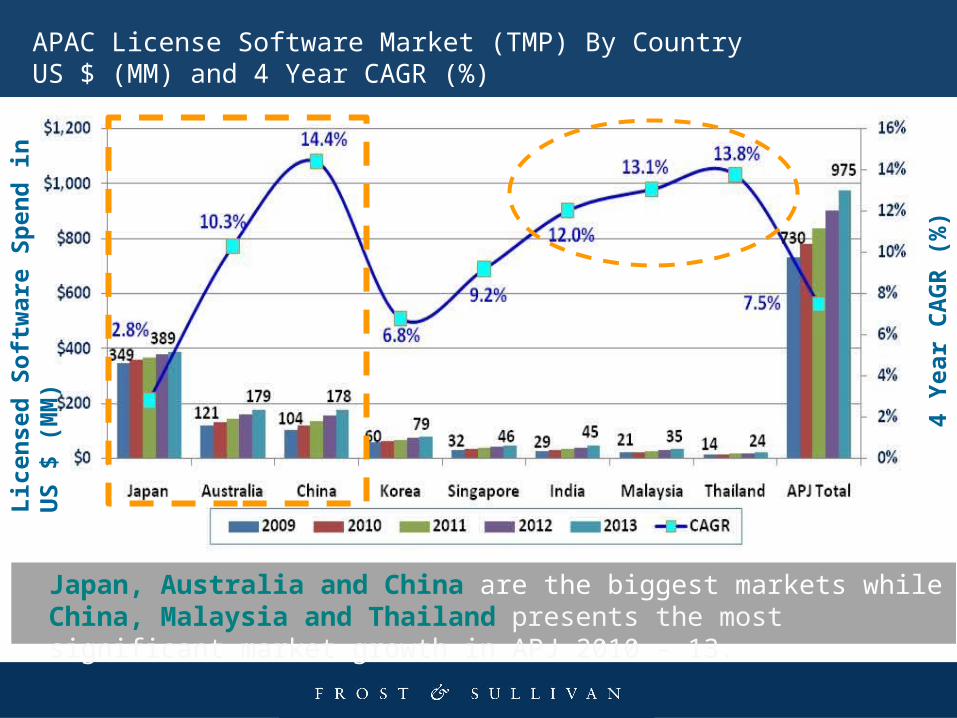

APAC License Software Market (TMP) By CountryUS $ (MM) and 4 Year CAGR (%)

Lice

nsed

Soft

war

e Sp

end

in U

S $

(MM

)

4 Ye

ar C

AGR

(%)

Japan, Australia and China are the biggest markets while China, Malaysia and Thailand presents the most significant market growth in APJ 2010 – 13.

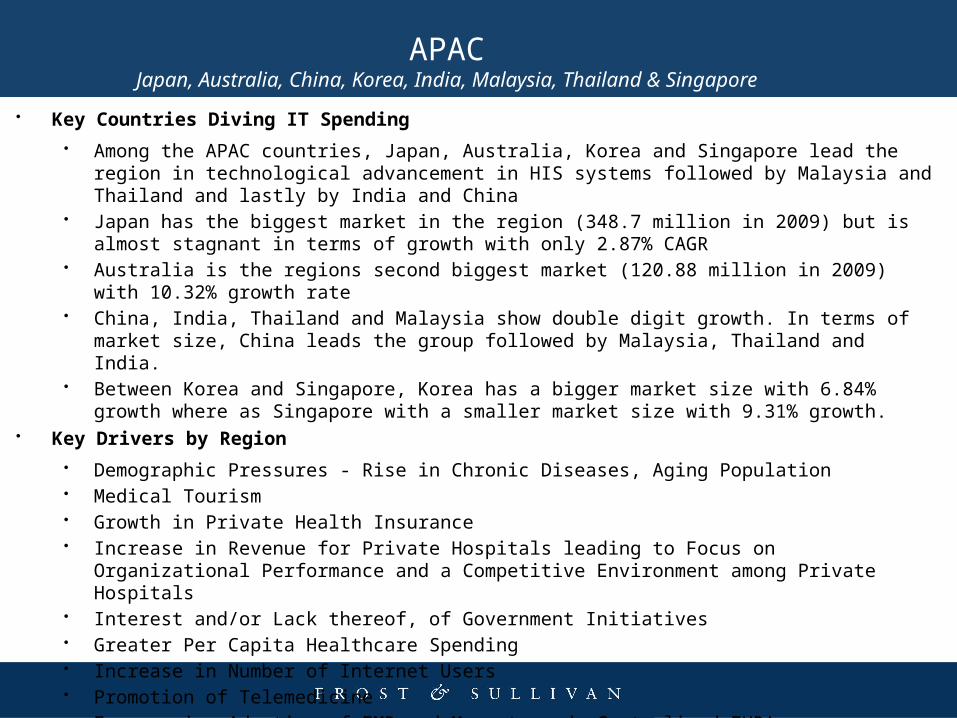

APACJapan, Australia, China, Korea, India, Malaysia, Thailand & Singapore

• Key Countries Diving IT Spending• Among the APAC countries, Japan, Australia, Korea and Singapore lead the region in technological

advancement in HIS systems followed by Malaysia and Thailand and lastly by India and China• Japan has the biggest market in the region (348.7 million in 2009) but is almost stagnant in terms of growth

with only 2.87% CAGR• Australia is the regions second biggest market (120.88 million in 2009) with 10.32% growth rate• China, India, Thailand and Malaysia show double digit growth. In terms of market size, China leads the group

followed by Malaysia, Thailand and India. • Between Korea and Singapore, Korea has a bigger market size with 6.84% growth where as Singapore with a

smaller market size with 9.31% growth.• Key Drivers by Region

• Demographic Pressures - Rise in Chronic Diseases, Aging Population • Medical Tourism• Growth in Private Health Insurance • Increase in Revenue for Private Hospitals leading to Focus on Organizational Performance and a Competitive

Environment among Private Hospitals• Interest and/or Lack thereof, of Government Initiatives • Greater Per Capita Healthcare Spending• Increase in Number of Internet Users• Promotion of Telemedicine• Encouraging Adoption of EMR and Move towards Centralized EHR’s

22

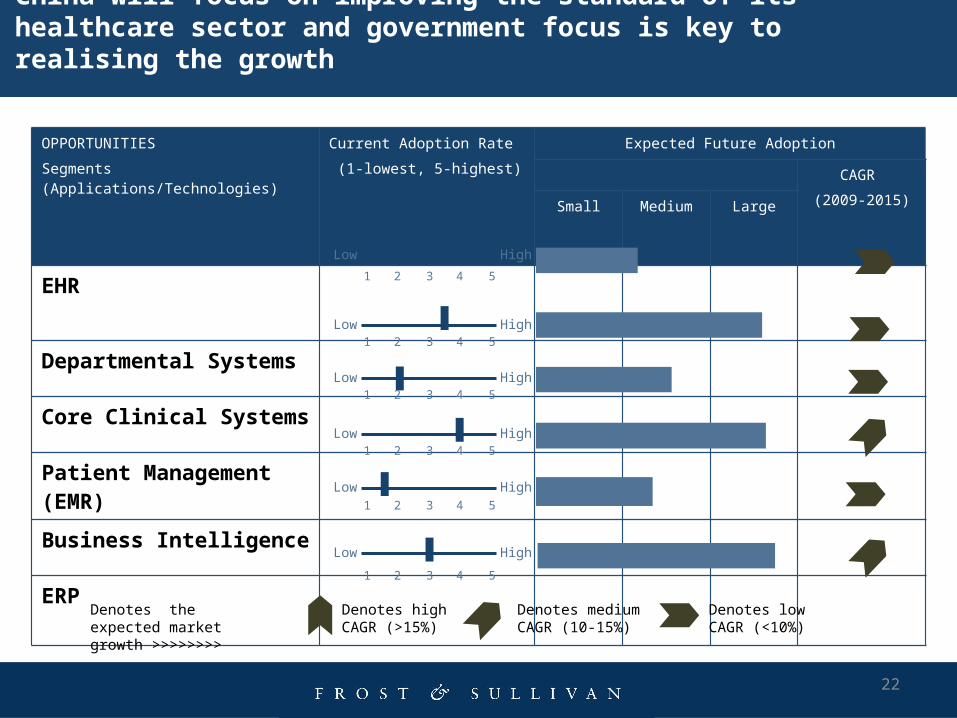

OPPORTUNITIESSegments (Applications/Technologies)

Current Adoption Rate (1-lowest, 5-highest)

Expected Future Adoption

CAGR (2009-2015)

Small Medium Large

EHR

Departmental Systems

Core Clinical Systems

Patient Management (EMR)

Business Intelligence

ERP

Low High

1 52 3 4

Low High1 52 3 4

Low High1 52 3 4

Low High1 52 3 4

Low High1 52 3 4

Low High

1 52 3 4

China will focus on improving the standard of its healthcare sector and government focus is key to realising the growth

Denotes the expected market growth >>>>>>>>

Denotes high CAGR (>15%)

Denotes medium CAGR (10-15%)

Denotes low CAGR (<10%)

23

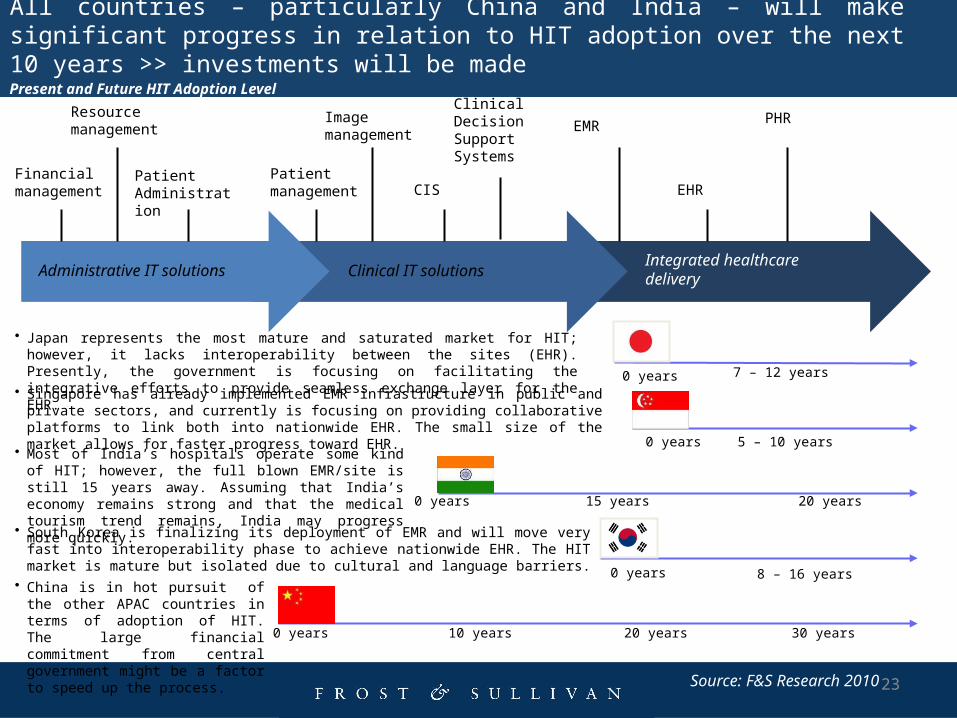

All countries – particularly China and India – will make significant progress in relation to HIT adoption over the next 10 years >> investments will be made

Administrative IT solutions Clinical IT solutionsIntegrated healthcare delivery

Financial management

Resourcemanagement

Patient Administration

Patient management

Image management

CIS

EMR

EHR

PHRClinical Decision Support Systems

0 years

0 years

7 – 12 years

0 years 15 years 20 years

0 years 10 years 20 years 30 years

Present and Future HIT Adoption Level

• Singapore has already implemented EMR infrastructure in public and private sectors, and currently is focusing on providing collaborative platforms to link both into nationwide EHR. The small size of the market allows for faster progress toward EHR.

• Japan represents the most mature and saturated market for HIT; however, it lacks interoperability between the sites (EHR). Presently, the government is focusing on facilitating the integrative efforts to provide seamless exchange layer for the EHR.

5 – 10 years0 years

8 – 16 years

• Most of India’s hospitals operate some kind of HIT; however, the full blown EMR/site is still 15 years away. Assuming that India’s economy remains strong and that the medical tourism trend remains, India may progress more quickly.

• South Korea is finalizing its deployment of EMR and will move very fast into interoperability phase to achieve nationwide EHR. The HIT market is mature but isolated due to cultural and language barriers.

• China is in hot pursuit of the other APAC countries in terms of adoption of HIT. The large financial commitment from central government might be a factor to speed up the process.

Source: F&S Research 2010

24

INNOVATIONS

TRANSFORMING HEALTHCARE DELIVERY

THROUGH DISRUPTIVE TECHNOLOGIES

24

25

Extending Care Beyond Hospitals - Connected Healthcare

• Connected Healthcare is a care delivery model that uses technology enabled solutions to expand the care capabilities beyond healthcare institutions to natural human habitats.

• The main aim of Connected Healthcare is to maximize healthcare resources, increase preventive and predictive component of care with the expectation of keeping individuals as healthy as possible and less dependent on curative care.

• It works through deploying sensor – monitoring devices, data storage and analytics, and communication channels to healthcare providers for decision making process, care planning and delivery. It empowers the individuals to self manage medical needs, and provide cannels for more interactive communications with healthcare professionals.

• At present, It is directed at chronic diseases, aged population, and dependency. The scope, however, is rapidly expanding to include entire population to mange health rather than to monitor illness. Smart homes, the mush up of real estate and healthcare is a natural expansion of Connected Healthcare.

26

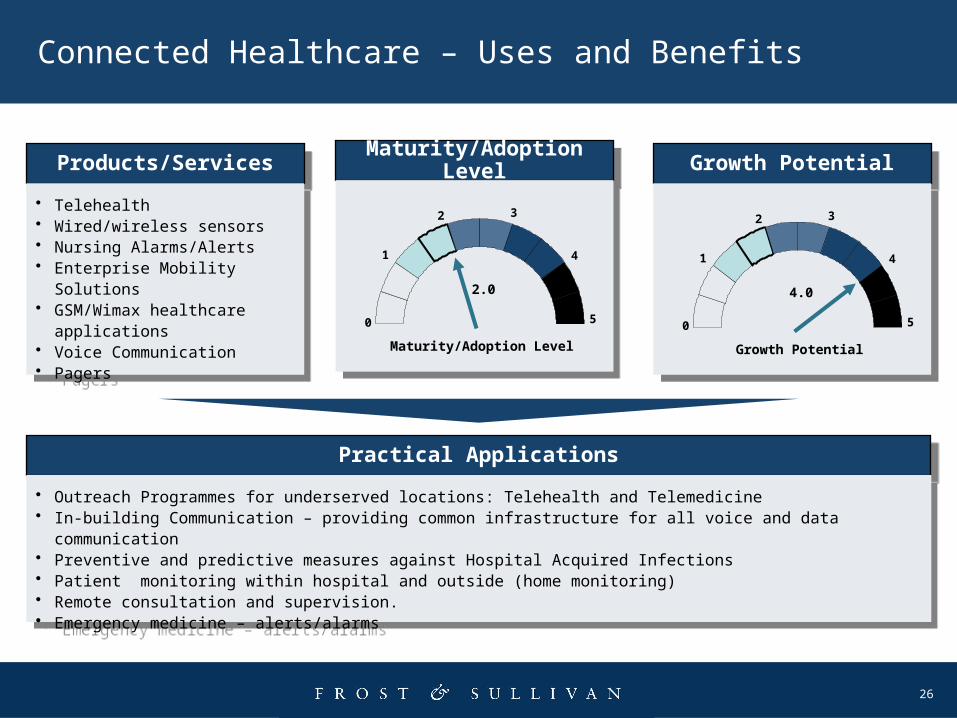

Connected Healthcare – Uses and Benefits

Products/ServicesProducts/Services

Practical ApplicationsPractical Applications

• Telehealth• Wired/wireless sensors• Nursing Alarms/Alerts• Enterprise Mobility Solutions• GSM/Wimax healthcare

applications• Voice Communication• Pagers

• Telehealth• Wired/wireless sensors• Nursing Alarms/Alerts• Enterprise Mobility Solutions• GSM/Wimax healthcare

applications• Voice Communication• Pagers

• Outreach Programmes for underserved locations: Telehealth and Telemedicine• In-building Communication – providing common infrastructure for all voice and data communication• Preventive and predictive measures against Hospital Acquired Infections• Patient monitoring within hospital and outside (home monitoring)• Remote consultation and supervision. • Emergency medicine – alerts/alarms

• Outreach Programmes for underserved locations: Telehealth and Telemedicine• In-building Communication – providing common infrastructure for all voice and data communication• Preventive and predictive measures against Hospital Acquired Infections• Patient monitoring within hospital and outside (home monitoring)• Remote consultation and supervision. • Emergency medicine – alerts/alarms

Growth PotentialGrowth Potential

Growth Potential

0

1

2 3

4

5

4.0

Maturity/Adoption LevelMaturity/Adoption Level

Maturity/Adoption Level

0

1

2 3

4

5

2.0

27

Empowering Patients/Individuals - Interactive Healthcare

• With the adoption of Web 2.0, collaborative technologies were introduced allowing unprecedented level of social interactivity. The use of Web 2.0 applications and resources for health related purposes is called Health 2.0

• Health 2.0 has become very popular and important platform for patients and consumers to find health information, interact with each other in virtual communities, and communicate with care givers. It empowers individual to manage own health according to personal preferences.

• Health 2.0 provides communication platform to healthcare organisations to reach out to their existing and potential clients. Hospital Portals and presence in the Social Networking Medias (e. g. Facebook, Twitter) has redefined marketing and sales strategies.

• According to the Pew Internet & American Life Project, 83 percent of Internet users have looked online for health information. New data released by Pew this week show many people are now using cell phones to search for health information - 29 percent of cell phone owners age 18 to 29, and 17 percent of cell owners overall. It's the first time Pew has surveyed health searches on cell phones.

28

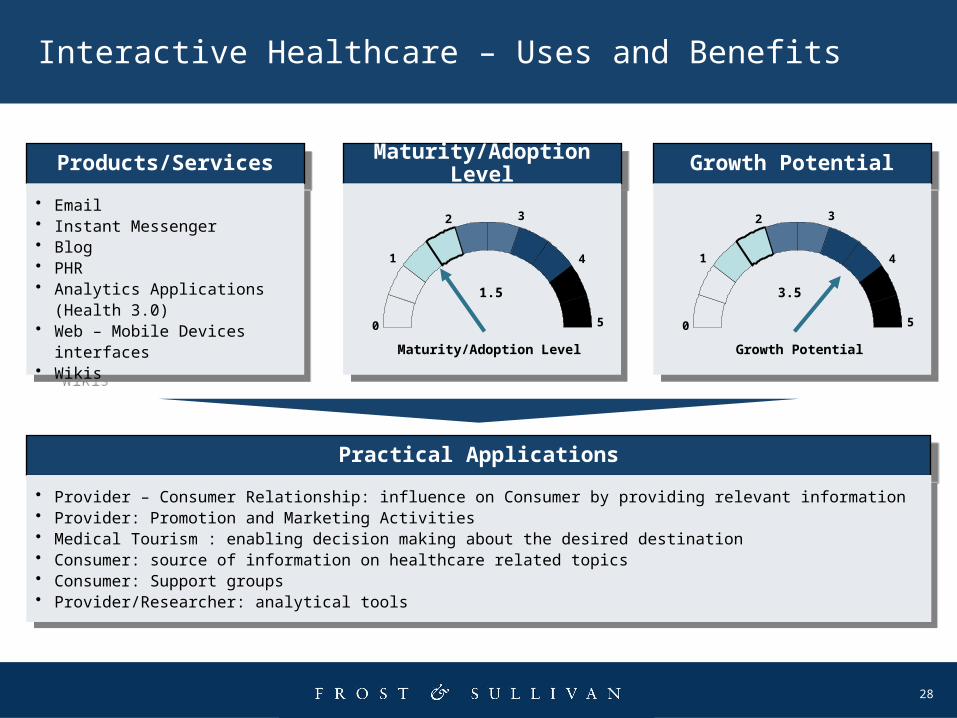

Interactive Healthcare – Uses and Benefits

Products/ServicesProducts/Services Maturity/Adoption LevelMaturity/Adoption Level

Practical ApplicationsPractical Applications

• Email• Instant Messenger• Blog• PHR• Analytics Applications (Health

3.0)• Web – Mobile Devices interfaces• Wikis

• Email• Instant Messenger• Blog• PHR• Analytics Applications (Health

3.0)• Web – Mobile Devices interfaces• Wikis

• Provider – Consumer Relationship: influence on Consumer by providing relevant information• Provider: Promotion and Marketing Activities • Medical Tourism : enabling decision making about the desired destination• Consumer: source of information on healthcare related topics• Consumer: Support groups• Provider/Researcher: analytical tools

• Provider – Consumer Relationship: influence on Consumer by providing relevant information• Provider: Promotion and Marketing Activities • Medical Tourism : enabling decision making about the desired destination• Consumer: source of information on healthcare related topics• Consumer: Support groups• Provider/Researcher: analytical tools

Maturity/Adoption Level

0

1

2 3

4

5

1.5

Growth PotentialGrowth Potential

Growth Potential

0

1

2 3

4

5

3.5

29

Making Care More Efficient - Cloud Healthcare

• Cloud Computing is an IT architecture model that virtualises computing resources to deliver them on demand and in required quantities. These resources are highly scalable (almost infinite) and highly available (24/7).

• The main characteristics of cloud computing are:– User does not own hardware, network, and application resources

– Computing resources are provided through remote data centres on a subscription basis (on demand).

– The infrastructure and services are delivered, accessed by user, via web browser (cloud).

• In cloud computing architecture, user is running services not on the local terminal but remotely. It means that instead of transferring data from remote host to be processed on the local terminal all transactions take place outside the local terminal.

• Healthcare industry is just exploring the capabilities and benefits of cloud computing. The main concern is over security of medical information as all is residing off-site in remote datacenter. However, the economic advantages to healthcare providers are making some to venture into the virtual realm of cloud computing.

30

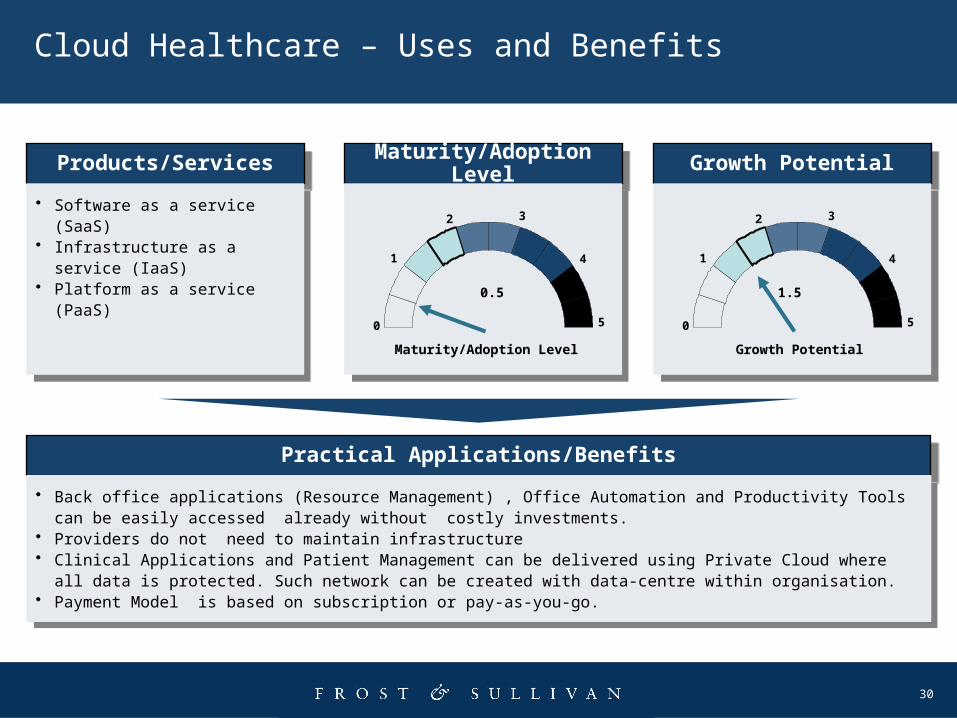

Cloud Healthcare – Uses and Benefits

Products/ServicesProducts/Services

Practical Applications/BenefitsPractical Applications/Benefits

• Software as a service (SaaS)• Infrastructure as a service (IaaS)• Platform as a service (PaaS)

• Software as a service (SaaS)• Infrastructure as a service (IaaS)• Platform as a service (PaaS)

• Back office applications (Resource Management) , Office Automation and Productivity Tools can be easily accessed already without costly investments.

• Providers do not need to maintain infrastructure• Clinical Applications and Patient Management can be delivered using Private Cloud where all data is protected. Such

network can be created with data-centre within organisation.• Payment Model is based on subscription or pay-as-you-go.

• Back office applications (Resource Management) , Office Automation and Productivity Tools can be easily accessed already without costly investments.

• Providers do not need to maintain infrastructure• Clinical Applications and Patient Management can be delivered using Private Cloud where all data is protected. Such

network can be created with data-centre within organisation.• Payment Model is based on subscription or pay-as-you-go.

Maturity/Adoption LevelMaturity/Adoption Level

Maturity/Adoption Level

0

1

2 3

4

5

0.5

Growth PotentialGrowth Potential

Growth Potential

0

1

2 3

4

5

1.5

31

Knowledge care - Business Intelligence in Healthcare

• Business Intelligence (BI) is a broad concept describing the process of transforming data into actionable knowledge. In recent years the term has became a label for information technologies: software and infrastructure that facilitate the BI process. Such applications capture, collate, store, transfer, retrieve, and analyse data to generate best choices for strategic decisions in the form of “what-if” analysis, predictive analytics, and multi dimensional data mining that in a blink of an eye deliver, insightful advises for managerial and clinical use.

• BI applications act as integration platform across the entire organisation. They connect together disparate systems to collect and exchange needed data. They glue the “silo” environment together to provide a seamless framework for information exchange and processing.

• Can be used as Health 2.0 and 3.0 applications linking data sources with analytical capabilities.

• By linking applications that otherwise were not communicating freely the BI is able to reduce the manual process effort used to facilitate exchange of information. The automation significantly can reduce access to data as well the occurrence of unintentional human errors while handling the data.

• BI solutions provide dedicated informational path linking the source of request/query with timely and relevant information.

32

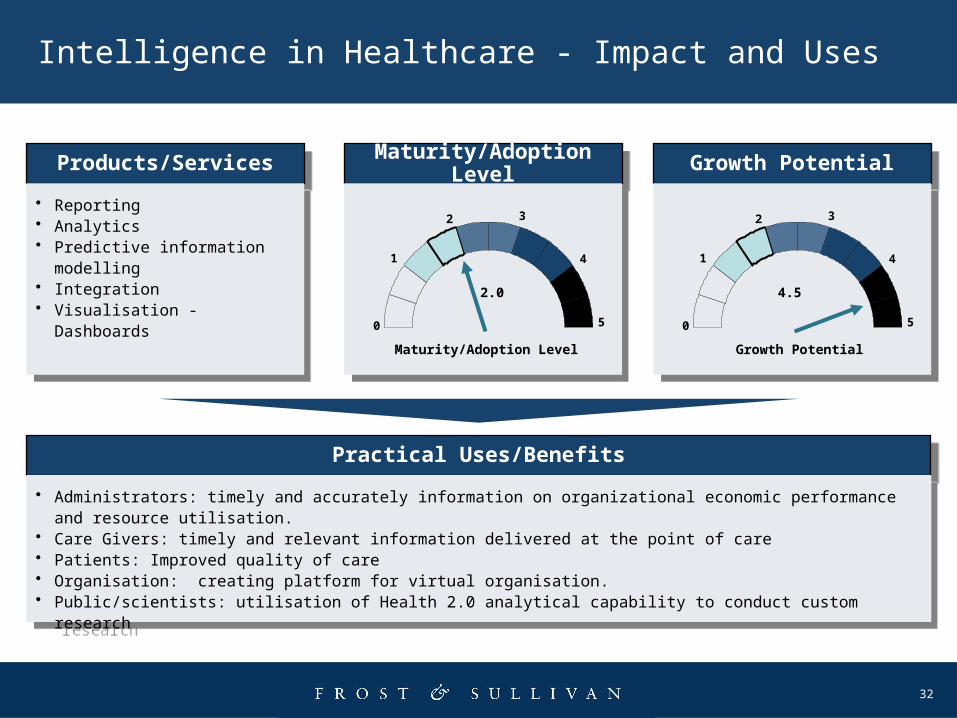

Intelligence in Healthcare - Impact and Uses

Products/ServicesProducts/Services

Practical Uses/BenefitsPractical Uses/Benefits

• Reporting• Analytics• Predictive information modelling• Integration• Visualisation - Dashboards

• Reporting• Analytics• Predictive information modelling• Integration• Visualisation - Dashboards

• Administrators: timely and accurately information on organizational economic performance and resource utilisation. • Care Givers: timely and relevant information delivered at the point of care• Patients: Improved quality of care• Organisation: creating platform for virtual organisation.• Public/scientists: utilisation of Health 2.0 analytical capability to conduct custom research

• Administrators: timely and accurately information on organizational economic performance and resource utilisation. • Care Givers: timely and relevant information delivered at the point of care• Patients: Improved quality of care• Organisation: creating platform for virtual organisation.• Public/scientists: utilisation of Health 2.0 analytical capability to conduct custom research

Maturity/Adoption LevelMaturity/Adoption Level

Maturity/Adoption Level

0

1

2 3

4

5

2.0

Growth PotentialGrowth Potential

Growth Potential

0

1

2 3

4

5

4.5

33

Moving Beyond Reality - Virtual Healthcare

• Virtual Reality is the ability to create artificial environment with the ability to act as it was real. It used advanced technologies to generate space and physical fabric and applies artificial intelligence to add interactive component. It is experienced by two senses (presently): sight and sound.

• Lighter version of Virtual Reality – Simulation has been well adopted by most industries including healthcare.

• The major users of these technology are gaming and military industries. It has also been successfully adopted by healthcare for simulations, 3D Image modelling for laparoscopic procedures, treatments, rehabilitation, and assessment.

• Virtual reality can be divided into:– The simulation of a real environment for workflow processes analysis and design,

training, education, therapies.– The development of an imagined environment for health assessment, capability

assessment, and therapies.

34

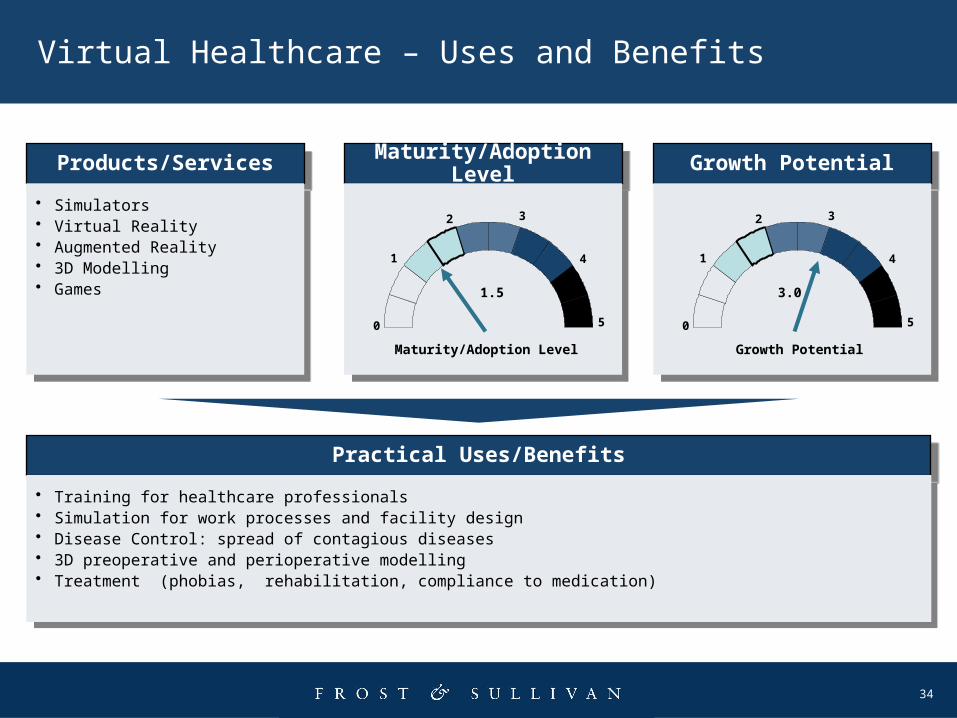

Virtual Healthcare – Uses and Benefits

Products/ServicesProducts/Services

Practical Uses/BenefitsPractical Uses/Benefits

• Simulators• Virtual Reality• Augmented Reality• 3D Modelling• Games

• Simulators• Virtual Reality• Augmented Reality• 3D Modelling• Games

• Training for healthcare professionals• Simulation for work processes and facility design• Disease Control: spread of contagious diseases• 3D preoperative and perioperative modelling• Treatment (phobias, rehabilitation, compliance to medication)

• Training for healthcare professionals• Simulation for work processes and facility design• Disease Control: spread of contagious diseases• 3D preoperative and perioperative modelling• Treatment (phobias, rehabilitation, compliance to medication)

Maturity/Adoption LevelMaturity/Adoption Level

Maturity/Adoption Level

0

1

2 3

4

5

1.5

Growth PotentialGrowth Potential

Growth Potential

0

1

2 3

4

5

3.0

OutcomesProvider Consumer

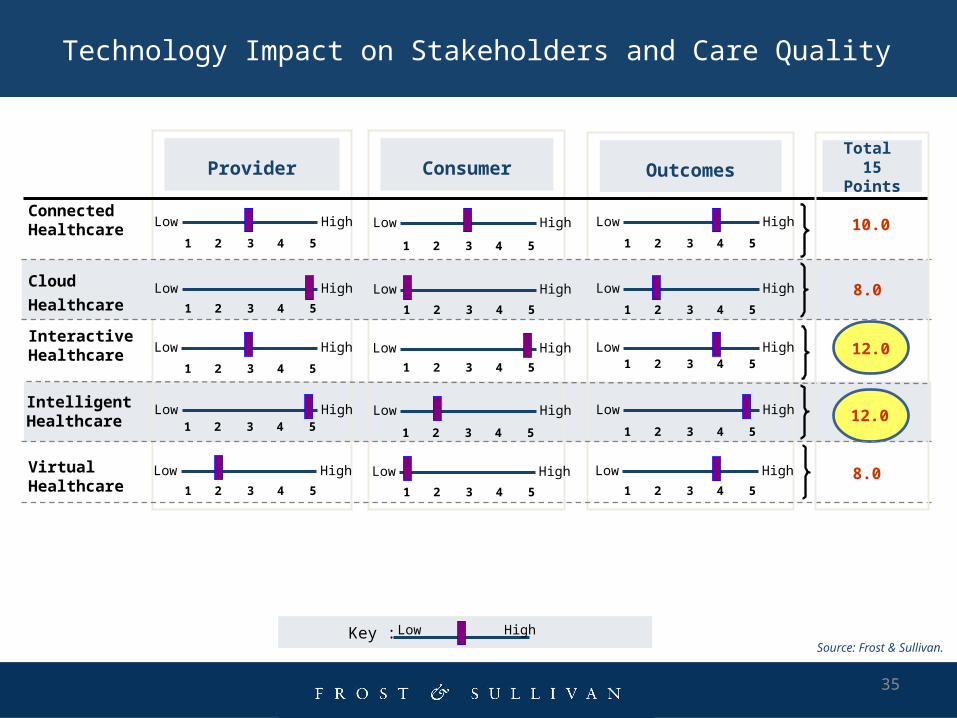

Technology Impact on Stakeholders and Care Quality

Source: Frost & Sullivan.Low HighKey :

Intelligent Healthcare

Low High1 52 3 4

Low High

1 52 3 4

Low High 12.0

Cloud Healthcare Low High1 52 3 4

Low High

1 52 3 4

Low High 8.0

Connected Healthcare Low High

1 52 3 4

Low High

1 52 3 4

Low High 10.0

Virtual Healthcare Low High1 52 3 4

Low High

1 52 3 4

Low High 8.0

Interactive Healthcare Low High

1 52 3 4

Low High1 52 3 4

Low High 12.0

Total 15 Points

1 52 3 4

1 52 3 4

1 52 3 4

1 52 3 4

1 52 3 4

35

36

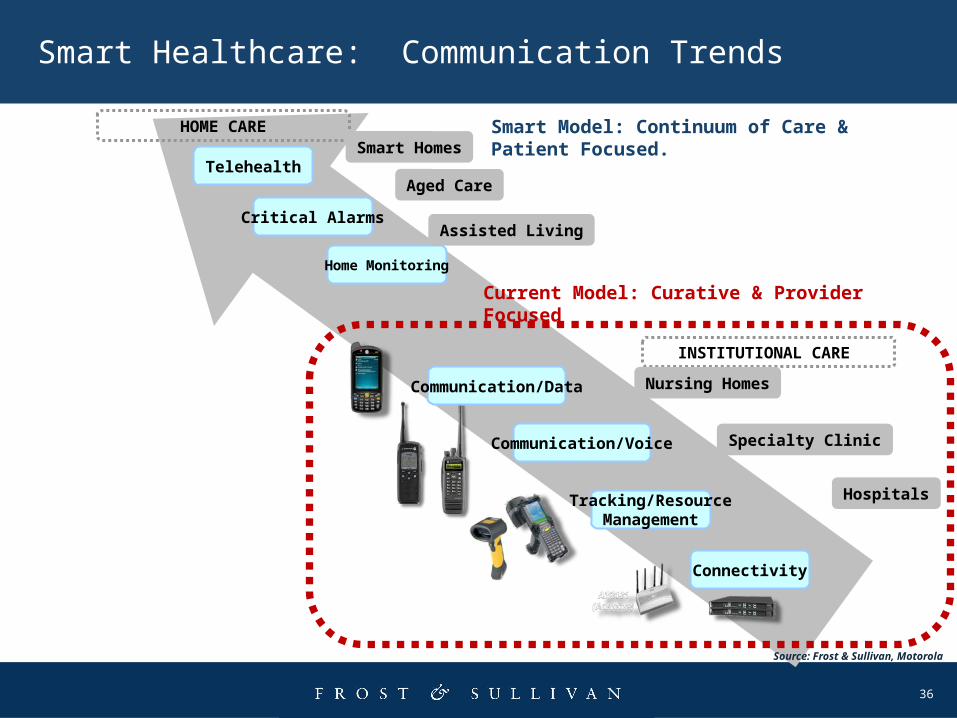

Smart Healthcare: Communication Trends

HOME CARE

INSTITUTIONAL CARE

Specialty Clinic

Hospitals

Current Model: Curative & Provider Focused

Telehealth

Connectivity

Communication/Voice

Source: Frost & Sullivan, Motorola

Tracking/ResourceManagement

Nursing HomesCommunication/Data

Home Monitoring

Aged Care

Smart Homes

Assisted Living

Critical Alarms

Smart Model: Continuum of Care & Patient Focused.

![Zensar Technologies Cited as a Vendor to Watch in Gartner 2016 Market Trends [Company Update]](https://img.pdfslide.us/doc/110x75/577c7b141a28abe054972fdf/zensar-technologies-cited-as-a-vendor-to-watch-in-gartner-2016-market-trends.jpg)