Embed Size (px)

Citation preview

Carrier Billing for Dating ServicesSpecial report by Fortumo

This special report by Fortumo gives an overview of implementing carrier billing in the context of online dating services. Carrier billing is one of the most widely available online payment methods as the consumer only needs a mobile phone and a SIM card in order to make online payments. The purchases are either added to the user’s monthly phone bill or deducted from their prepaid balance. Carrier billing is becoming increasingly popular as traditional payment methods (bank cards) are not widely available in emerging markets. It is estimated that carrier billing transaction volumes will reach $47 billion by 2020, four times the amount being processed today.

In this report, we give an overview of how carrier billing �ts into the existing monetization strategy of online dating services. We also pro�le the markets with the biggest potential for carrier billing, also highlighting end-user spending trends for each market. Finally, the report highlights how mobile operators - often the biggest consumer-facing digital companies in their country - can help dating services increase user acquisition and revenue through marketing support, once a dating service merchant has decided to implement carrier billing.

Introduction

Mattias LiivakHead of Marketing & PRFortumo

If you have any questions about the data in this report, please reach out to us at [email protected].

Andrea BoettiVP of Global Business Development & SalesFortumo

Carrier billing for dating services

People look to online dating services for two reasons: fun (e.g. �nding a date for tonight) or serious commitment (�nding a long-term partnership). Dating services have accommodated their monetization strategy to match this.

For the �rst audience, services are usually sold through one-time payments and at low prices (such as incognito mode, or boosted visibility of the pro�le). For the long-term commitment seekers, service providers usually rely on recurring subscriptions with a higher ticket size.

There are also alternative monetization models (such as ad-based or a�liate network revenue) which rely on other sources of income beside the end-user.

Monetization of dating services: where does carrier billing fit in?

But when payments from end-users are already collected either through card-based payments or PayPal, why would there be motivation to add carrier billing as an additional payment method? Let’s look at three connected key trends in the digital ecosystem which explain the growing need for carrier billing.

Carrier billing for dating services

Digital trends impacting dating service owners

Smartphone ownership is growing fastest in emerging markets. Internet adoption is slowing down in Western markets, but accelerating in growing economies like India.

How it impacts dating service ability to generate revenue: Credit card reach is lacking in emerging markets.

Where does carrier billing �t in? Unlike bank cards or mobile wallets, carrier billing is by default available to any mobile phone owner.

Trend #1: New internet users are coming online primarily in emerging markets

2%India

60%US

Credit Card Ownership

More internet is now consumed on mobile devices compared than on desktop devices.

How it impacts dating service ability to generate revenue: Credit card checkout �ows are inconvenient on mobile devices, negatively impacting conversion rates.

Where does carrier billing �t in? With carrier billing, the user only needs to provide their phone number. Conversion rates are up to 10x higher on mobile devices with carrier billing compared to credit cards.

Trend #2: Mobile internet usage has overtaken desktop internet usage

Carrier billing for dating services

Let's add here comparison of carrier billing checkout �ow with Badoo vs credit card billing checkout �ow.

Carrier billing payment �ow

Credit Card payment �ow

10xHigher conversion

Phone number is pre-�lled from previous purchase

User receives PIN code via SMS and con�rms the purchase

User gets service

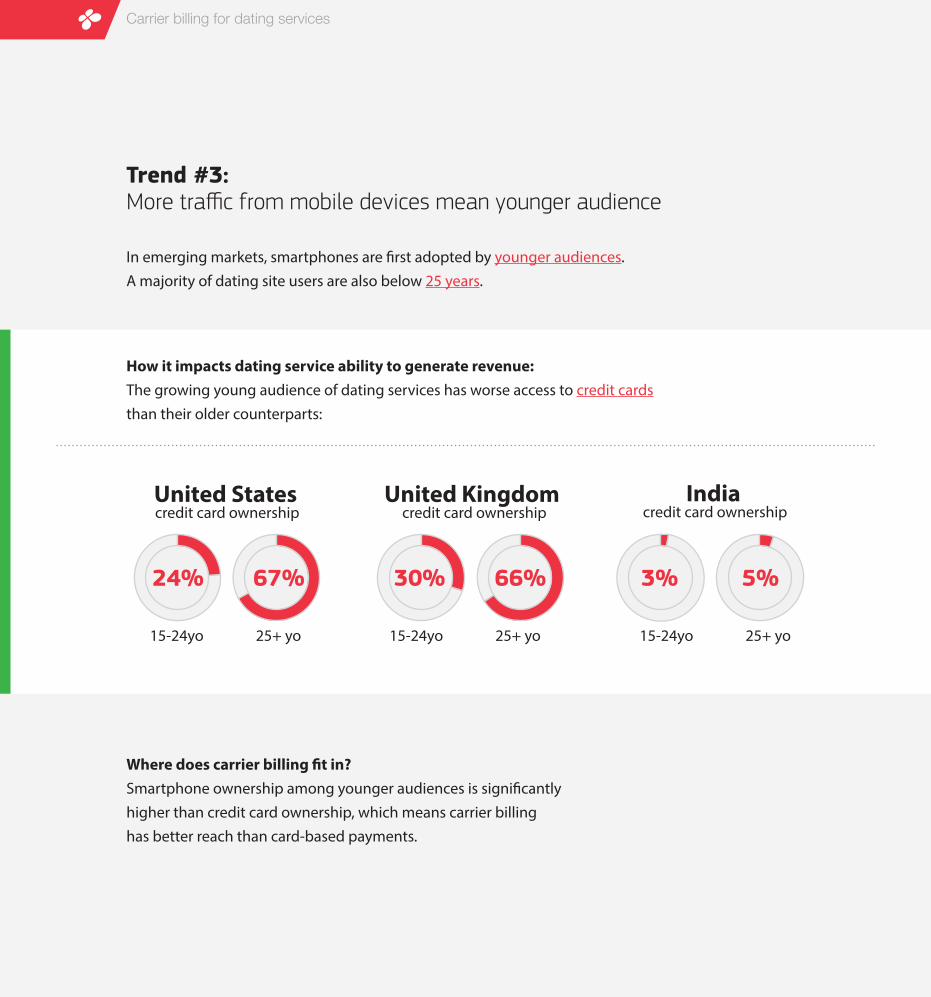

In emerging markets, smartphones are �rst adopted by younger audiences. A majority of dating site users are also below 25 years.

How it impacts dating service ability to generate revenue: The growing young audience of dating services has worse access to credit cards than their older counterparts:

Where does carrier billing �t in? Smartphone ownership among younger audiences is signi�cantly higher than credit card ownership, which means carrier billing has better reach than card-based payments.

Trend #3: More traffic from mobile devices mean younger audience

Carrier billing for dating services

30% 66% 3% 5%

United Kingdom credit card ownership

Indiacredit card ownership

24%

15-24yo 25+ yo 15-24yo 25+ yo 15-24yo 25+ yo

United Statescredit card ownership

67%

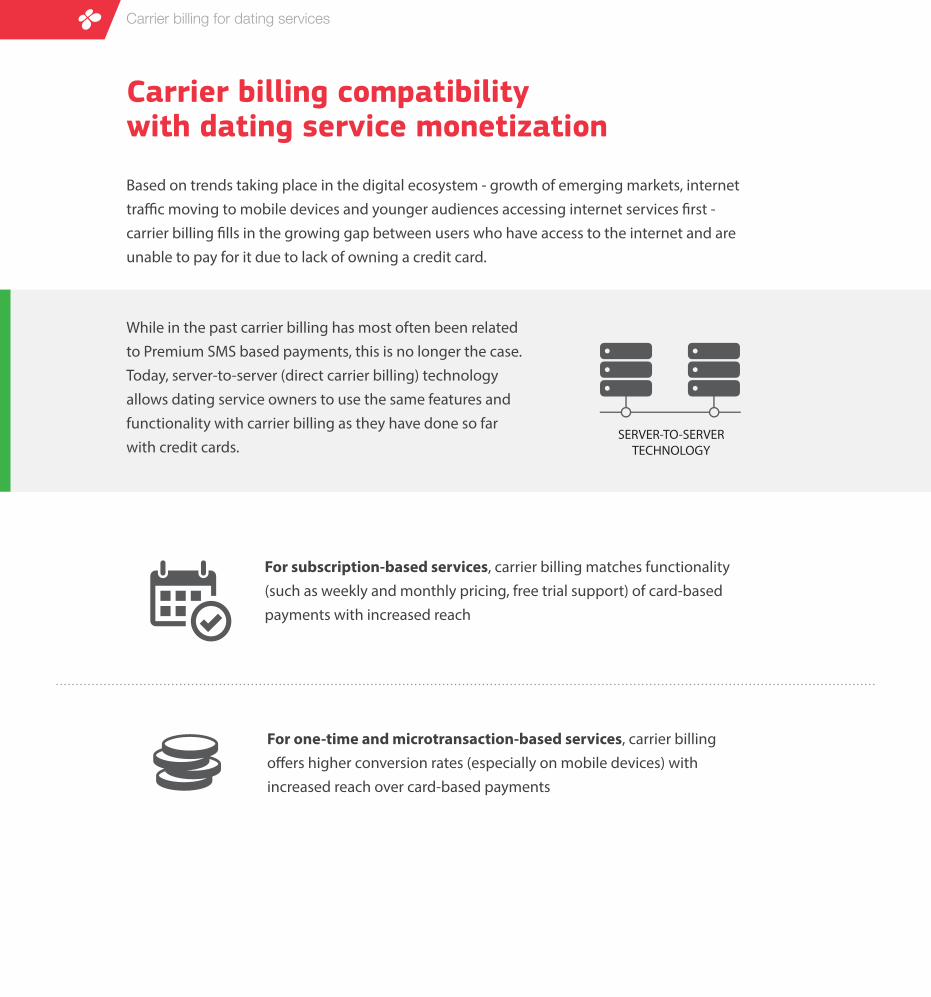

Based on trends taking place in the digital ecosystem - growth of emerging markets, internet tra�c moving to mobile devices and younger audiences accessing internet services �rst - carrier billing �lls in the growing gap between users who have access to the internet and are unable to pay for it due to lack of owning a credit card.

While in the past carrier billing has most often been related to Premium SMS based payments, this is no longer the case. Today, server-to-server (direct carrier billing) technology allows dating service owners to use the same features and functionality with carrier billing as they have done so far with credit cards.

For subscription-based services, carrier billing matches functionality (such as weekly and monthly pricing, free trial support) of card-based payments with increased reach

For one-time and microtransaction-based services, carrier billing o�ers higher conversion rates (especially on mobile devices) withincreased reach over card-based payments

Carrier billing compatibility with dating service monetization

SERVER-TO-SERVERTECHNOLOGY

Carrier billing for dating services

In addition, carrier billing can be used as an activation mechanism for people who have signed up for a dating service but have not become a paying user. For example, if the dating service provider knows that paying users generally convert within a week with credit card payments, carrier billing can be used to target those users who have not converted during the �rst week. These targeted users are either not paying with credit cards because they do not have one, do not wish to use them online, or do not feel the value proposition is strong enough. Carrier billing can in these cases be used as follows:

No ownership of credit card - carrier billing can be o�ered as an alternative to users who can’t pay otherwise

No desire to use credit card - carrier billing can be o�ered as an alternative to users who fear for their privacy

Weak sense of value proposition - carrier billing can be o�ered for a teaser service with a smaller ticket value (e.g. when regular VIP membership costs $20/month, such users can be targeted with an o�er of $5/week instead)

Carrier billing for dating services

During the past few years, there have been several data breaches with dating services where private information on millions of users has been exposed. This has made consumers more averse to making payments online with credit cards. In fact, in the United States people are more afraid of online identity theft than being robbed on the street.

In light of this, carrier billing can be presented as a payment option to users who are afraid that their identity may be exposed online. Carrier billing is signi�cantly more secure from the consumer perspective, because no personal data is transmitted or stored during the checkout process:

While with a card-based transaction, the payment is always linked to the consumer’s real identity, with carrier billing users can choose to remain anonymous (especially in cases where prepaid SIM cards are used, as then even the mobile operator does not know the identity of the user).

Carrier billing and user privacy

Credit Card Number

Expiration Month

Expiration Date

Card Security Code*

Name on Card

Billing Address

City

State/Province

Postal/Zip Code

Country

Mobile operator

Phone number (or encrypted identi�er)

User data transmitted during a credit card transaction

User data transmitted during a carrier billing transaction

Carrier billing for dating services

While Fortumo provides carrier billing in 90+ markets, dating service providers should focus on countries where impact from adding carrier billing is the biggest. In this report, we have highlighted markets where our existing dating service provider customers have seen the biggest uplift from implementing carrier billing.

These markets are:

Emerging markets of Latin America (Brazil, Chile): carrier billing usage is driven thanks to its accessibility, as most people don’t have a credit card

Mature economies in Europe (Germany, United Kingdom, Spain, Switzerland, Sweden): carrier billing usage is driven thanks to user-friendly checkout �ows and privacy

Top markets for dating (based on Fortumo dating merchants)

Carrier billing for dating services

Below you will �nd an overview of demographics in each market, carrier billing spending behavior speci�cally for dating services, as well as an overview of subscription-based payment performance for markets where this type of payment is available.

Carrier billing for dating services

Market profile August 2016 - October 2016

Brazil

GNI per capita:Median age:

31209Population:

$12,000209Mobile phones:

1 Brazilian Real (BRL) = $0.28

million years Gross National Income (IMF 2014 estimate)

million

Currency:

55%

Smartphonepenetration (of all

mobile phones):Debit card

penetration:

59%73%

Mobile broadband

access:

74%

Prepaid SIMmarket share:

Credit cardpenetration:

32%

Carrier billing for dating services

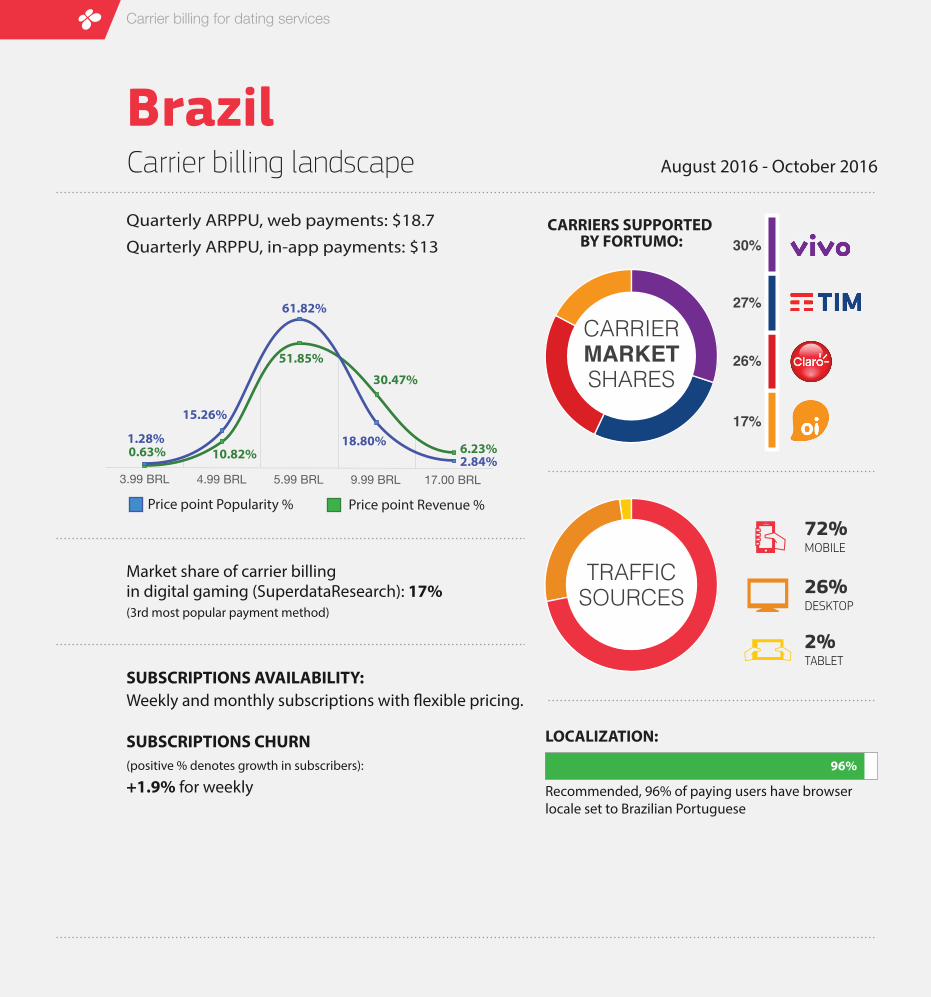

Carrier billing landscape August 2016 - October 2016

Brazil

Quarterly ARPPU, web payments: $18.7

Quarterly ARPPU, in-app payments: $13CARRIERS SUPPORTED

BY FORTUMO: 30%

27%

26%

17%

CARRIERMARKETSHARES

72%

TABLET

DESKTOP

MOBILE

26%

2%

TRAFFICSOURCES

LOCALIZATION:

Recommended, 96% of paying users have browser locale set to Brazilian Portuguese

Market share of carrier billing in digital gaming (SuperdataResearch): 17% (3rd most popular payment method)

SUBSCRIPTIONS AVAILABILITY: Weekly and monthly subscriptions with �exible pricing.

SUBSCRIPTIONS CHURN(positive % denotes growth in subscribers):

+1.9% for weekly96%

3.99 BRL 4.99 BRL 5.99 BRL 9.99 BRL 17.00 BRL

Price point Popularity % Price point Revenue %

1.28%0.63%

15.26%

10.82%

61.82%

51.85%

18.80%

30.47%

2.84%6.23%

Carrier billing for dating services

Market profile August 2016 - October 2016

Germany

GNI per capita:Median age:

46

60%

81

Smartphonepenetration (of all

mobile phones):

Population:

$48,000108

Debit cardpenetration:

92%

Mobile phones:

1 Euro (EUR) = $1.1

71%

Mobile broadband

access:

46%

Prepaid SIMmarket share:

Credit cardpenetration:

45%

million years Gross National Income (IMF 2014 estimate)

million

Currency:

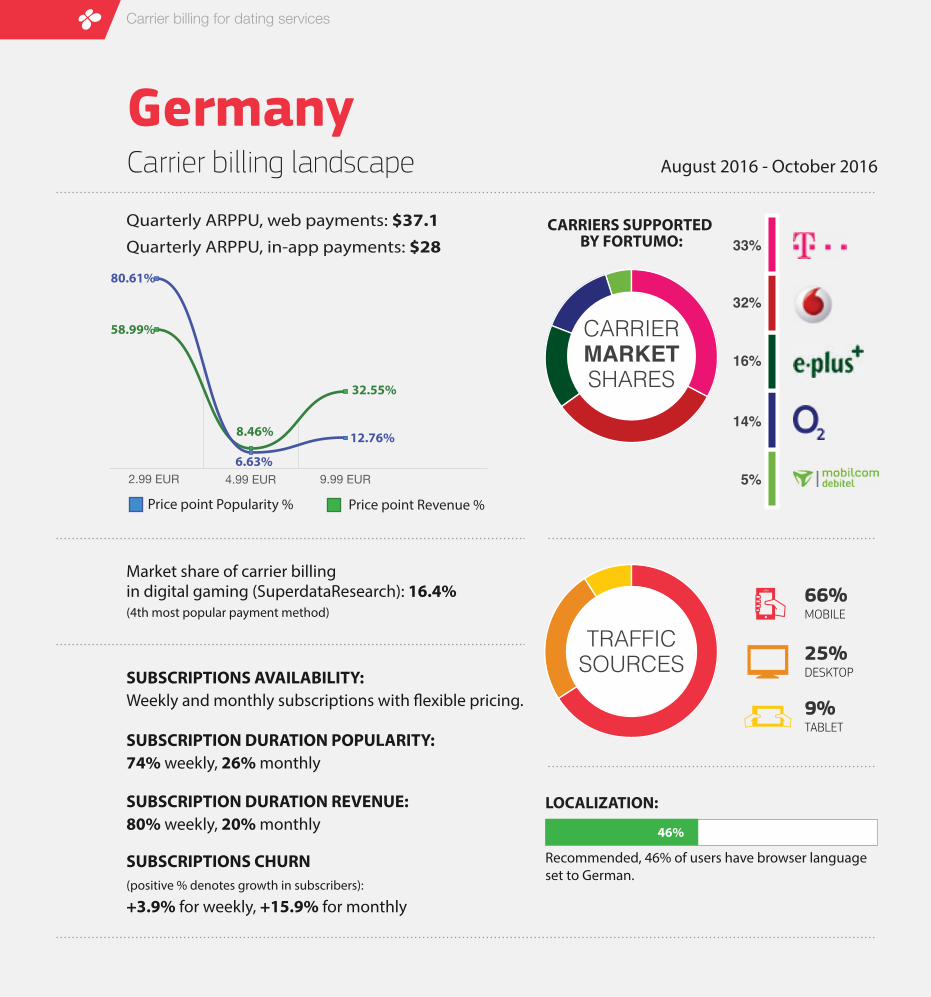

Carrier billing for dating services

Carrier billing landscape August 2016 - October 2016

Germany

Quarterly ARPPU, web payments: $37.1Quarterly ARPPU, in-app payments: $28

CARRIERS SUPPORTED BY FORTUMO: 33%

32%

16%

14%

5%

CARRIERMARKETSHARES

66%

TABLET

DESKTOP

MOBILE

25%

9%

TRAFFICSOURCES

LOCALIZATION:

Recommended, 46% of users have browser language set to German.

Market share of carrier billing in digital gaming (SuperdataResearch): 16.4% (4th most popular payment method)

SUBSCRIPTIONS AVAILABILITY: Weekly and monthly subscriptions with �exible pricing.

SUBSCRIPTION DURATION POPULARITY:74% weekly, 26% monthly

SUBSCRIPTION DURATION REVENUE:80% weekly, 20% monthly

SUBSCRIPTIONS CHURN(positive % denotes growth in subscribers):

+3.9% for weekly, +15.9% for monthly

46%

2.99 EUR 9.99 EUR4.99 EUR

Price point Popularity % Price point Revenue %

80.61%

58.99%

6.63%

8.46% 12.76%

32.55%

Important note: Due to United Kingdom’s decision to leave the European Union, volatility is to be expected for the exchange rate of the British Pound volatility and an extended period of time until the outcome of the referendum becomes clear.

Carrier billing for dating services

Market profile August 2016 - October 2016

United Kingdom

GNI per capita:Median age:

40

68%

65

Smartphonepenetration (of all

mobile phones):

Population:

$43,00074

Debit cardpenetration:

96%

Mobile phones:

1 British Pound (GBP) = $1.3

78%

Mobile broadband

access:

38%

Prepaid SIMmarket share:

Credit cardpenetration:

61%

million years Gross National Income (IMF 2014 estimate)

million

Currency:

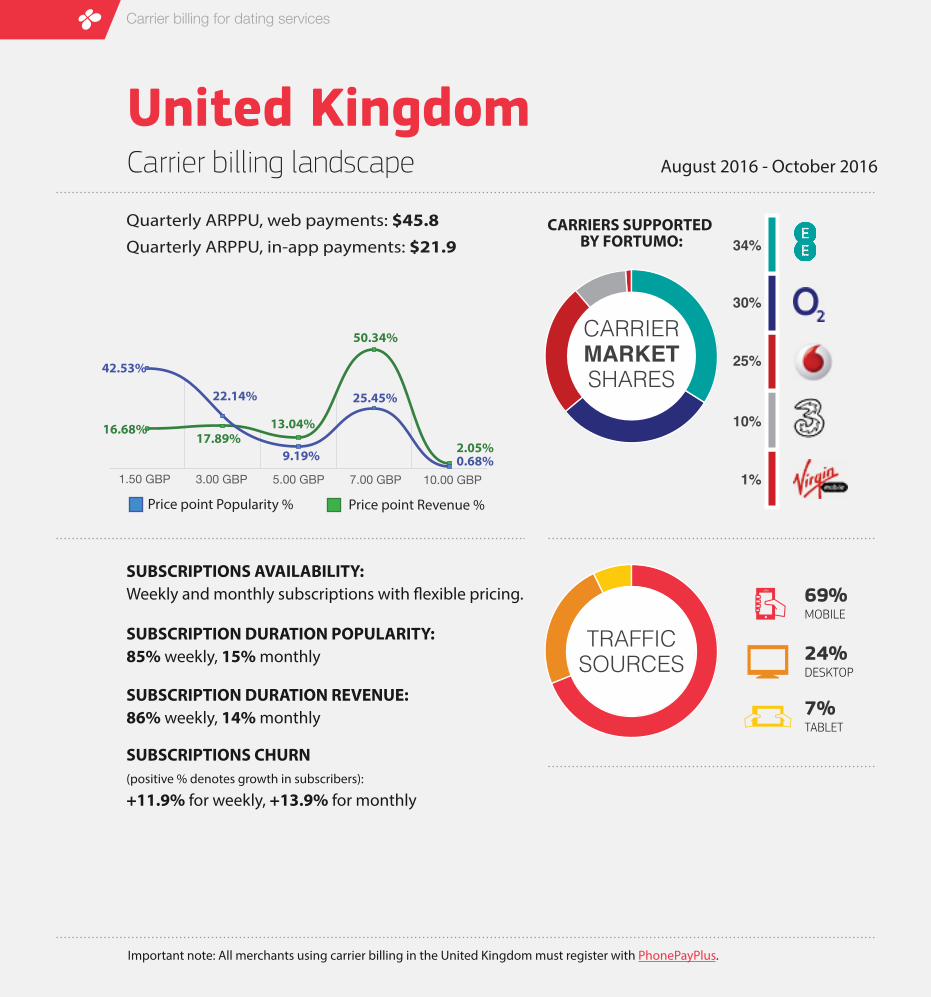

Carrier billing for dating services

Carrier billing landscape August 2016 - October 2016

United Kingdom

Quarterly ARPPU, web payments: $45.8Quarterly ARPPU, in-app payments: $21.9

1.50 GBP 3.00 GBP 5.00 GBP 7.00 GBP 10.00 GBP

Price point Popularity % Price point Revenue %

42.53%

16.68%

22.14%

17.89%9.19%

13.04%

25.45%

50.34%

0.68%2.05%

CARRIERS SUPPORTED BY FORTUMO: 34%

30%

25%

10%

1%

CARRIERMARKETSHARES

69%

TABLET

DESKTOP

MOBILE

24%

7%

TRAFFICSOURCES

SUBSCRIPTIONS AVAILABILITY: Weekly and monthly subscriptions with �exible pricing.

SUBSCRIPTION DURATION POPULARITY:85% weekly, 15% monthly

SUBSCRIPTION DURATION REVENUE:86% weekly, 14% monthly

SUBSCRIPTIONS CHURN(positive % denotes growth in subscribers):

+11.9% for weekly, +13.9% for monthly

Important note: All merchants using carrier billing in the United Kingdom must register with PhonePayPlus.

Carrier billing for dating services

Market profile August 2016 - October 2016

Spain

GNI per capita:Median age:

41

71%

46

Smartphonepenetration (of all

mobile phones):

Population:

$29,00049

Debit cardpenetration:

82%

Mobile phones:

1 Euro (EUR) = $1.1

74%

Mobile broadband

access:

24%

Prepaid SIMmarket share:

Credit cardpenetration:

54%

million years Gross National Income (IMF 2014 estimate)

million

Currency:

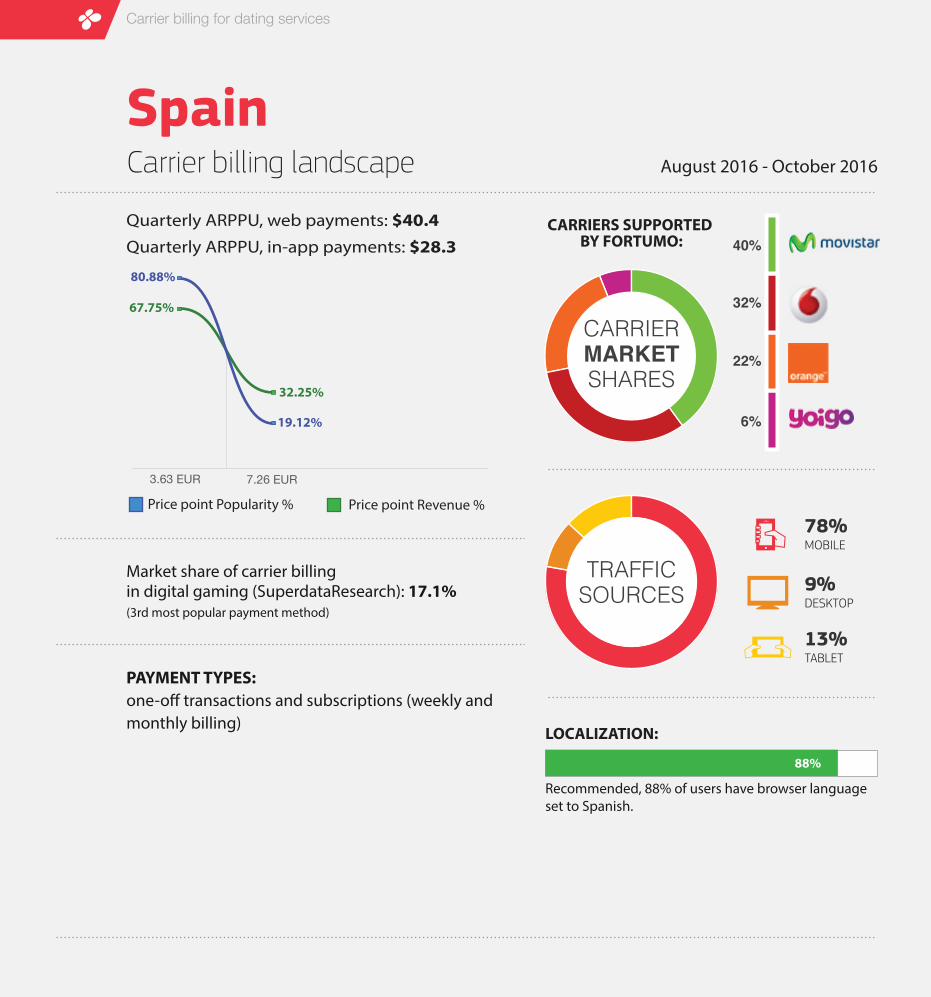

Carrier billing for dating services

Carrier billing landscape August 2016 - October 2016

Spain

Quarterly ARPPU, web payments: $40.4Quarterly ARPPU, in-app payments: $28.3

CARRIERS SUPPORTED BY FORTUMO: 40%

32%

22%

6%

CARRIERMARKETSHARES

78%

TABLET

DESKTOP

MOBILE

9%

13%

TRAFFICSOURCES

LOCALIZATION:

Recommended, 88% of users have browser language set to Spanish.

Market share of carrier billing in digital gaming (SuperdataResearch): 17.1% (3rd most popular payment method)

PAYMENT TYPES:one-o� transactions and subscriptions (weekly and monthly billing)

88%

3.63 EUR 7.26 EUR

Price point Popularity % Price point Revenue %

80.88%

67.75%

19.12%

32.25%

Carrier billing for dating services

Market profile August 2016 - October 2016

Chile

GNI per capita:Median age:

33

40%

18

Smartphonepenetration (of all

mobile phones):

Population:

$15,00018

Debit cardpenetration:

54%

Mobile phones:

1 Chilean Peso (CLP) = $0.0015

57%

Mobile broadband

access:

71%

Prepaid SIMmarket share:

Credit cardpenetration:

28%

million years Gross National Income (IMF 2014 estimate)

million

Currency:

Carrier billing for dating services

Carrier billing landscape August 2016 - October 2016

Chile

Quarterly ARPPU, web payments: $12.6Quarterly ARPPU, in-app payments: $12.9

CARRIERS SUPPORTED BY FORTUMO:

41%

39%

20%

CARRIERMARKETSHARES

45%

TABLET

DESKTOP

MOBILE

53%

2%

TRAFFICSOURCES

LOCALIZATION:

Recommended, 95% of paying users have browser locale set to Spanish

Market share of carrier billing in digital gaming (SuperdataResearch): 24.3%(most popular payment method)

PAYMENT TYPES:one-o� transactions and subscriptions (weekly and monthly billing)

95%

900.00 CLP 1500.00 CLP

Price point Popularity % Price point Revenue %

82.83%74.15%

17.17%

25.85%

Carrier billing for dating services

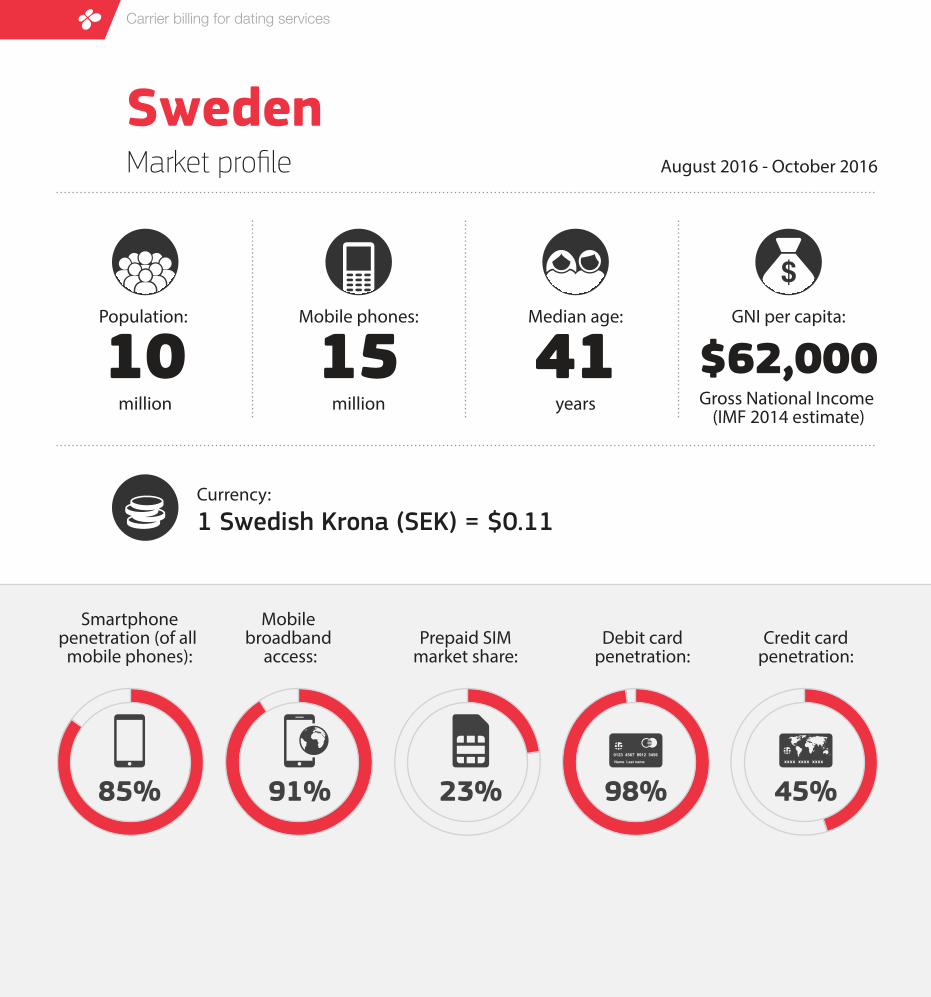

Market profile August 2016 - October 2016

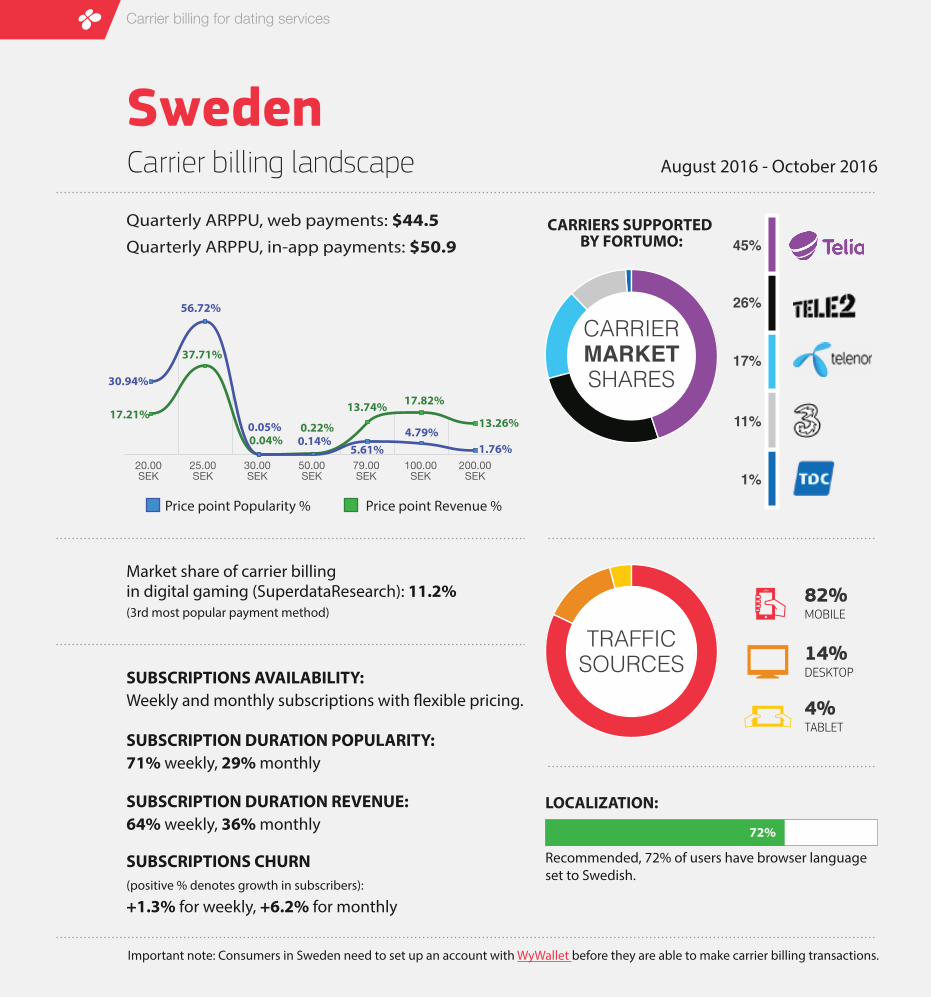

Sweden

GNI per capita:Median age:

41

85%

10

Smartphonepenetration (of all

mobile phones):

Population:

$62,00015

Debit cardpenetration:

98%

Mobile phones:

1 Swedish Krona (SEK) = $0.11

91%

Mobile broadband

access:

23%

Prepaid SIMmarket share:

Credit cardpenetration:

45%

million years Gross National Income (IMF 2014 estimate)

million

Currency:

Carrier billing for dating services

Carrier billing landscape August 2016 - October 2016

Sweden

20.00SEK

25.00SEK

30.00SEK

50.00SEK

79.00SEK

100.00SEK

200.00SEK

Quarterly ARPPU, web payments: $44.5Quarterly ARPPU, in-app payments: $50.9

Price point Popularity % Price point Revenue %

30.94%

17.21%

56.72%

37.71%

0.05%0.04% 0.14%

0.22%

1.76%

13.26%

5.61%

13.74%

4.79%

17.82%

CARRIERS SUPPORTED BY FORTUMO: 45%

26%

17%

11%

1%

CARRIERMARKETSHARES

82%

TABLET

DESKTOP

MOBILE

14%

4%

TRAFFICSOURCES

LOCALIZATION:

Recommended, 72% of users have browser language set to Swedish.

Market share of carrier billing in digital gaming (SuperdataResearch): 11.2% (3rd most popular payment method)

SUBSCRIPTIONS AVAILABILITY: Weekly and monthly subscriptions with �exible pricing.

SUBSCRIPTION DURATION POPULARITY:71% weekly, 29% monthly

SUBSCRIPTION DURATION REVENUE:64% weekly, 36% monthly

SUBSCRIPTIONS CHURN(positive % denotes growth in subscribers):

+1.3% for weekly, +6.2% for monthly

Important note: Consumers in Sweden need to set up an account with WyWallet before they are able to make carrier billing transactions.

72%

Carrier billing for dating services

Market profile August 2016 - October 2016

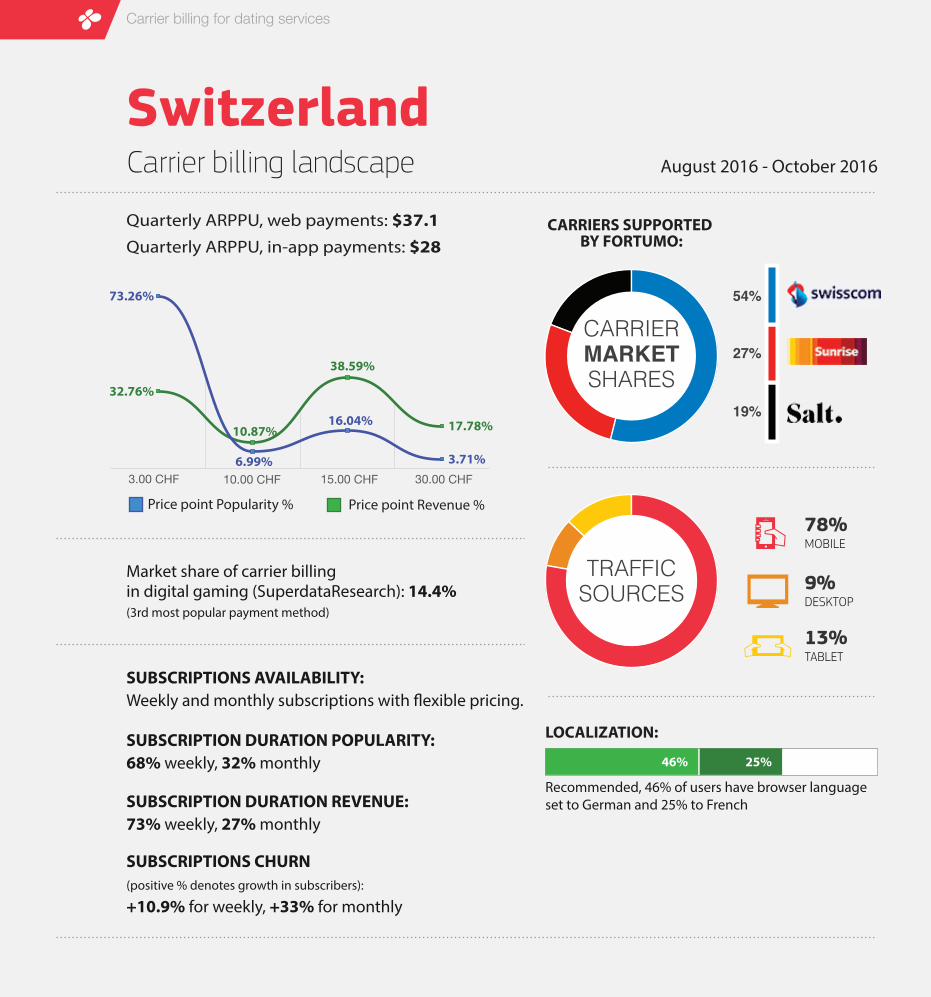

Switzerland

GNI per capita:Median age:

42

77%

8

Smartphonepenetration (of all

mobile phones):

Population:

$88,00011

Debit cardpenetration:

84%

Mobile phones:

1 Swiss Franc (CHF) = $1.02

85%

Mobile broadband

access:

36%

Prepaid SIMmarket share:

Credit cardpenetration:

54%

million years Gross National Income (IMF 2014 estimate)

million

Currency:

Carrier billing for dating services

Carrier billing landscape August 2016 - October 2016

Switzerland

Quarterly ARPPU, web payments: $37.1Quarterly ARPPU, in-app payments: $28

CARRIERS SUPPORTED BY FORTUMO:

54%

27%

19%

CARRIERMARKETSHARES

78%

TABLET

DESKTOP

MOBILE

9%

13%

TRAFFICSOURCES

LOCALIZATION:

Recommended, 46% of users have browser language set to German and 25% to French

Market share of carrier billing in digital gaming (SuperdataResearch): 14.4% (3rd most popular payment method)

SUBSCRIPTIONS AVAILABILITY: Weekly and monthly subscriptions with �exible pricing.

SUBSCRIPTION DURATION POPULARITY:68% weekly, 32% monthly

SUBSCRIPTION DURATION REVENUE:73% weekly, 27% monthly

46% 25%

3.00 CHF 15.00 CHF 30.00 CHF10.00 CHF

Price point Popularity % Price point Revenue %

73.26%

32.76%

6.99%

10.87%

3.71%

17.78%

38.59%

16.04%

SUBSCRIPTIONS CHURN(positive % denotes growth in subscribers):

+10.9% for weekly, +33% for monthly

Dating service merchants who have implemented carrier billing through Fortumo generally use our cross-platform mobile payments solution. We recommend using this product (or similar ones from competitors) due to the following reasons:

One integration works for all platforms (web, mobile web, in-app)

Platform interoperability

One integration allows launching carrier billing across 90+ markets

Rapid time to market

All checkout �ows are compliant with local regulations, supporting 40+ currencies and 50+ languages.

Compliance and localization

How to implement carrier billing?

Carrier billing for dating servicesCarrier billing for dating services

Product can be branded by the merchant to increase user familiarity, trust and payment conversion rate.

Branding opportunities

Product has built-in capability for voucher distribution (e.g. o�ering free trials for user acquisition), real-time changing of prices etc.

Flexible user acquisition and marketing features

With a dataset of more than 300M transactions each year, checkout �ows have been tested and optimized to ensure users can complete payments as seamlessly as possible.

Optimized for conversion improvement

Carrier billing for dating services

Fortumo has a dedicated carrier account management team who helps organize partnerships and promotions for our partners with carriers. Dating service providers and Fortumo identify markets and carriers with biggest potential for promotion where carrier billing can generate biggest impact on revenue. Fortumo helps planning and conducting of campaigns, managing the entire process with carriers on behalf of the dating service provider.

In many cases, carriers are willing to give out an increase in payouts to service providers for marketing campaigns. Such campaigns bring on average 40% additional revenue to the merchant during campaign period. In exchange for the increased payouts during campaigns, dating service providers utilize following activities to increase end-user spending:

Display carrier billing as default payment option

Give bonus credits to users paying via carrier billing

Give user voucher for unlocking additional premium feature (easily be managed by Fortumo’s voucher distribution solution)

Cross-sell items (e.g. buying increased visibility on the dating site also gives 1 week access of VIP membership)

Negotiating custom promotion opportunities for Rovio with carriers in India

Enabling leading streaming companies like HOOQ and Spotify with user acquisition by having carriers develop complex features such as free trials and dynamic pricing

Supporting leading digital games marketplace Kinguin in Europe by helping negotiate custom promotion deals with carriers

Marketing by carriers: additional opportunities for revenue and user acquisition

Carrier billing for dating services

Besides helping our existing dating service providers launch campaigns across Europe, Fortumo has global experience in organizing and conducting marketing campaigns with carriers:

The dating service audience is increasingly becoming mobile and shifting to emerging markets. This means the gap between online users and users able to make payments with credit cards is increasing.

Carrier billing can be used to supplement card-based payments and collect revenue from users who do not have a credit card, do not want to pay online with it (privacy) or feel the process is too tedious.

Modern direct carrier billing providers dating services with the same features and functionality as card-based payments. Additionally, carrier billing can be used as a mechanism to re-engage people who have not become paying users through credit cards.

When implementing carrier billing, dating service providers should �rst consider large markets in Western Europe and Latin America as experience shows these are the regions with biggest potential for additional revenue from adopting the new payment method. Here, carriers are also willing to work together with service providers on custom marketing campaigns to drive increased revenue for all parties involved.

Conclusion

Carrier billing for dating services

https://fortumo.comhttps://facebook.com/fortumohttps://twitter.com/fortumohttps://www.linkedin.com/company/fortumo-ltd

Fortumo is a mobile payments company that enables direct carrier billing with more than 350 mobile operators in 90+ countries. Fortumo's payment products work across a wide range of platforms including desktop devices, smartphones, feature phones, tablets and smart TV-s. These products give consumers a simple, 1-click payment method to charge online purchases to their phone bill. For app stores, digital media companies and game developers, Fortumo provides one integration with 350 mobile operators as well as a single point of contact for settlements, reporting, support and infrastructure upgrades. Founded in 2007, Fortumo has offices in Estonia, San Francisco, Beijing, Delhi, Singapore & Hanoi and is backed by Intel Capital and Greycroft Partners.

This document is for informational purposes only. Fortumo and the authors make no expressed or implied warranties in this document. Fortumo and the author(s) make no representation or warranty in relation to the accuracy, completeness or reliability of the information contained in this document. Any opinions expressed in this document are subject to change without notice. This document may be based on a number of assumptions and different assumptions could result in materially different results. This document should not be regarded by recipients as a substitute for obtaining independent advice and/or the exercise of their own judgement, and is not to be relied upon by recipients. Fortumo and the authors, and any of their members, directors, employees or agents do not accept any liability for any loss or damage arising out of the use of all or any part of this document. Copyright © 2016 Fortumo | All rights reserved.