Embed Size (px)

DESCRIPTION

A presentation for students at Michigan State University studying journalism, digital media and entrepreneurialism.

Citation preview

1

A Digital Adver-sing Primer And Other Get Rich Slow (or Never) Schemes for Journalists

February 10, 2011

“Informa-on wants to be free. It also wants to be expensive.”

-‐ Stewart Brand

“Adver-sing sucks. The only thing that sucks more than adver-sing is paying for content.”

-‐ Some Kid (Somewhere)

Digital Content Between a Rock and a Hard Place

3

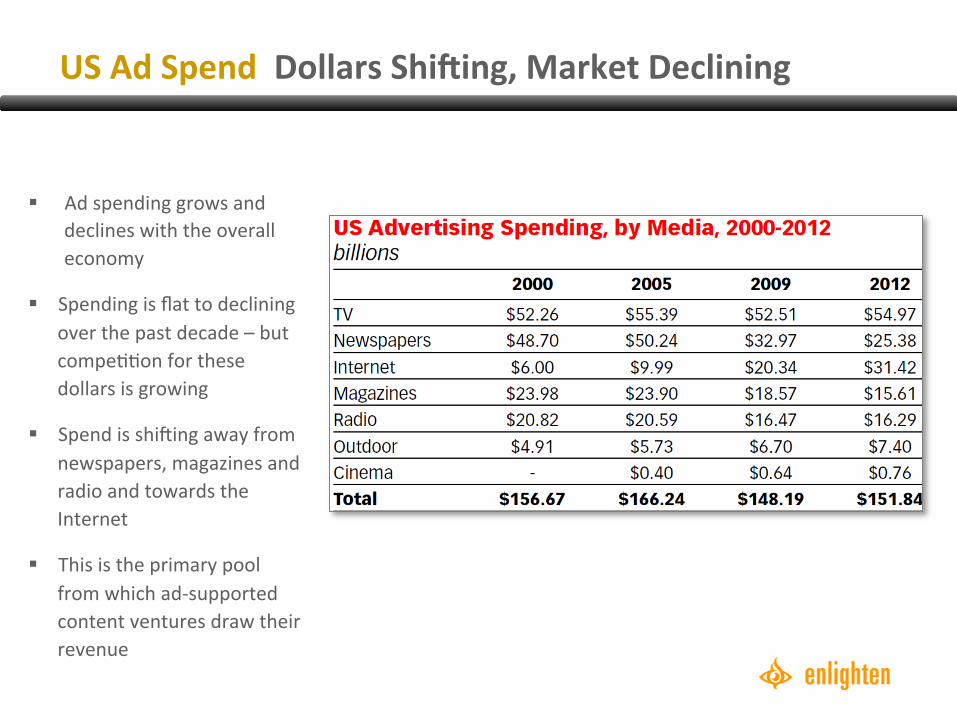

US Ad Spend Dollars ShiKing, Market Declining

§ Ad spending grows and declines with the overall economy

§ Spending is flat to declining over the past decade – but compe::on for these dollars is growing

§ Spend is shi<ing away from newspapers, magazines and radio and towards the Internet

§ This is the primary pool from which ad-‐supported content ventures draw their revenue

4

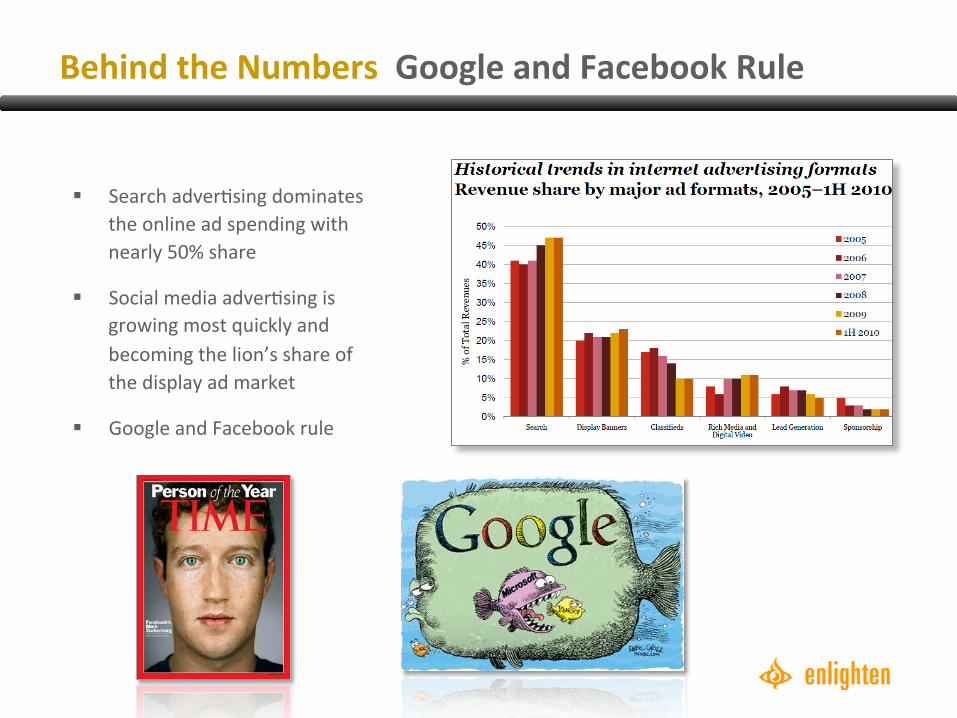

Behind the Numbers Google and Facebook Rule

§ Search adver:sing dominates the online ad spending with nearly 50% share

§ Social media adver:sing is growing most quickly and becoming the lion’s share of the display ad market

§ Google and Facebook rule

5

6

Who Wants What?

7

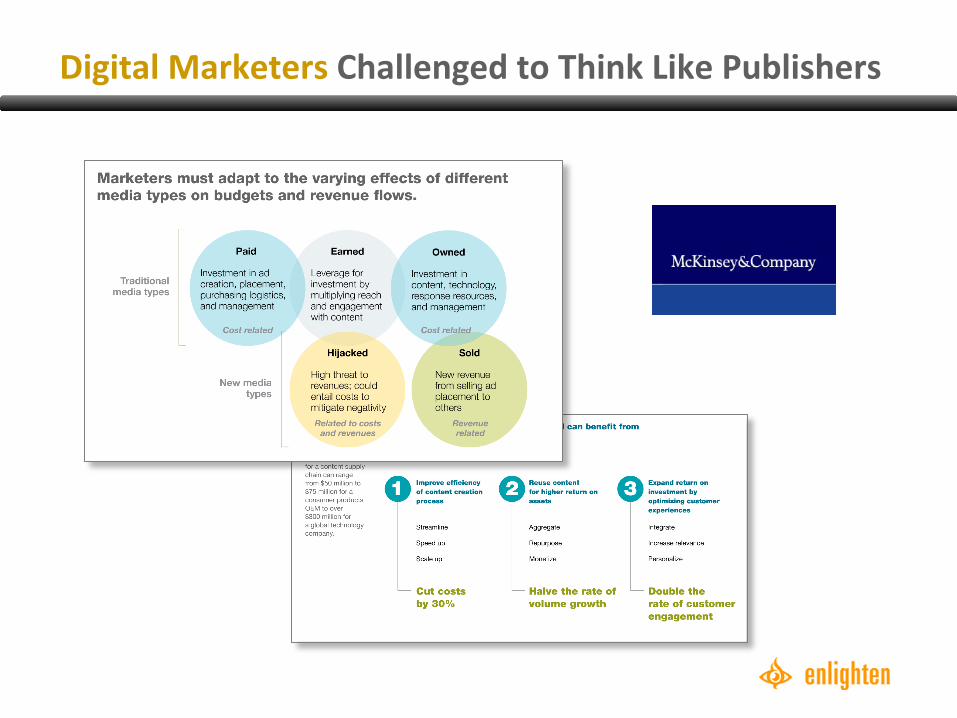

Digital Marketers Challenged to Think Like Publishers

8

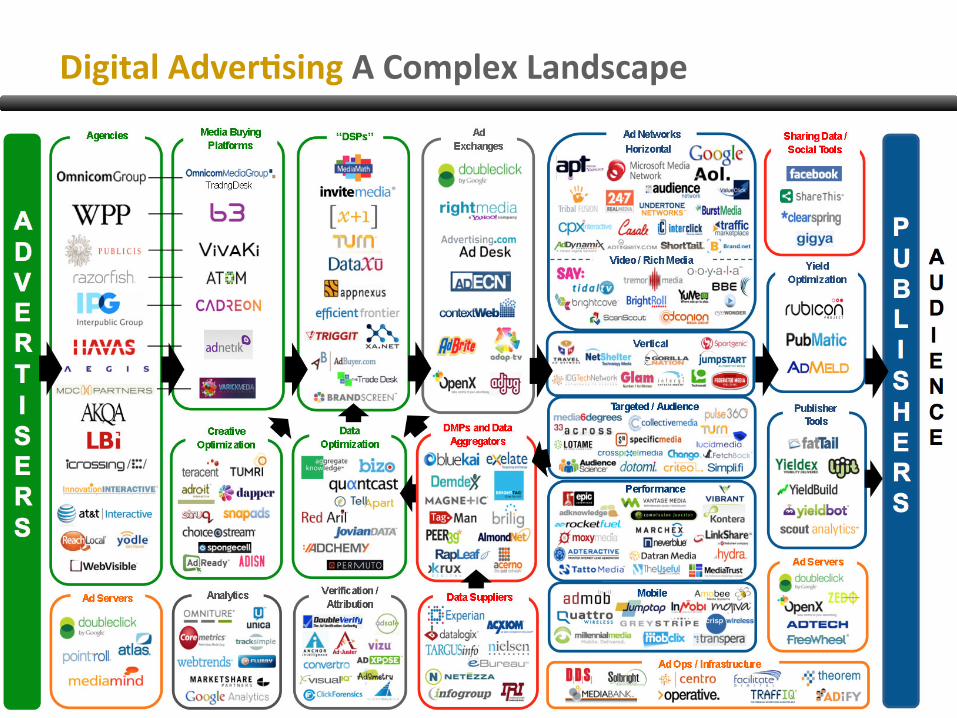

Digital Adver-sing A Simplified Landscape

9

Digital Adver-sing A Complex Landscape

10

The ABC’s

Cost per Impression (CPM)

ü Display and rich media

Cost per Click (CPC)

ü Search

Cost per Engagement (CPE)

ü In-‐text

Cost per Performance (CPP)

ü Leads/name acquisi:on

11

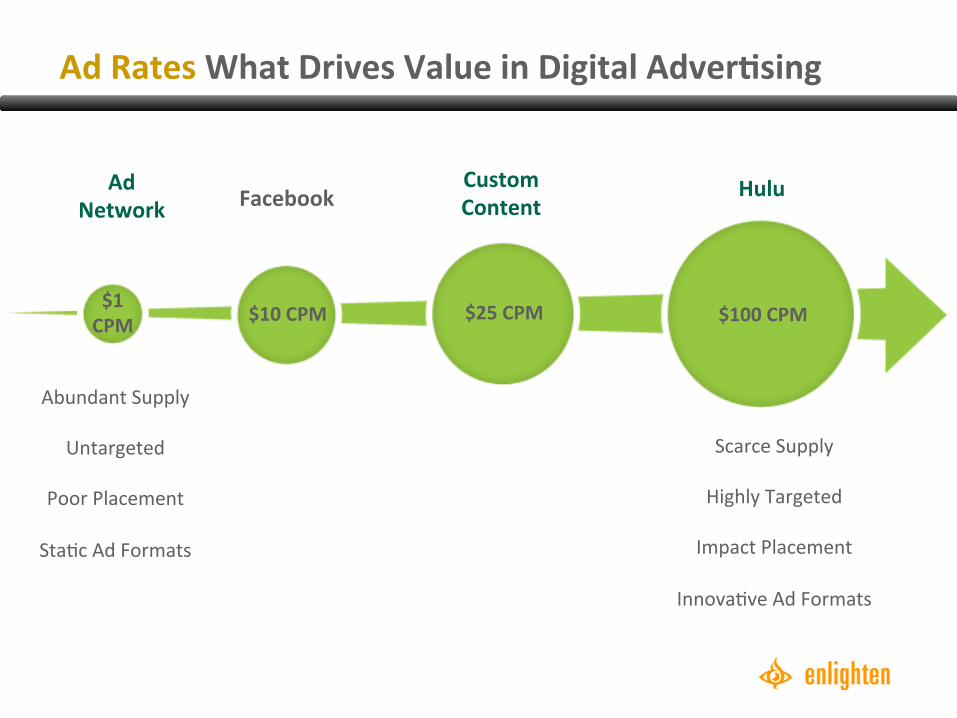

Ad Rates What Drives Value in Digital Adver-sing

Abundant Supply

Untargeted

Poor Placement

Sta:c Ad Formats

$10 CPM $25 CPM $100 CPM $1 CPM

Scarce Supply

Highly Targeted

Impact Placement

Innova:ve Ad Formats

Ad Network Facebook

Custom Content

Hulu

12

1. The Freemium Model

2. The Whatever you Want Model

3. The SyndicaBon Model

4. The Olive Garden Model

5. The Random Dudes Model

6. The Network Model

7. The I’ll Build My Own Damn Content Model

8. The UBlity Model

9. The Content = Commerce Model

10. The Altruism Model

Let’s Look At Some Models

13

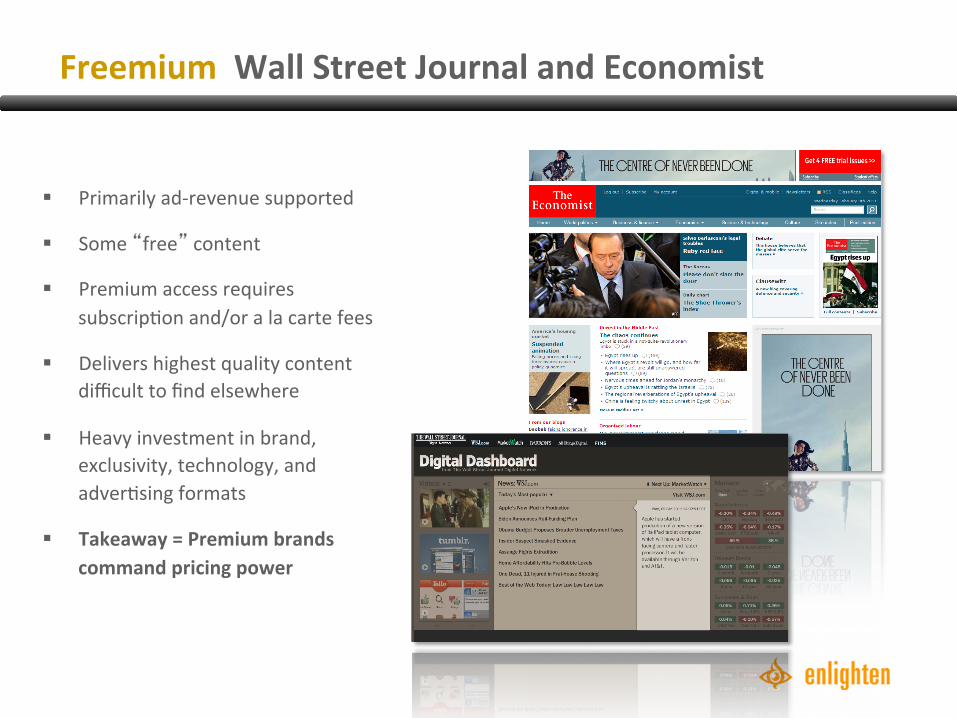

Freemium Wall Street Journal and Economist

§ Primarily ad-‐revenue supported

§ Some “free” content

§ Premium access requires subscrip:on and/or a la carte fees

§ Delivers highest quality content difficult to find elsewhere

§ Heavy investment in brand, exclusivity, technology, and adver:sing formats

§ Takeaway = Premium brands command pricing power

14

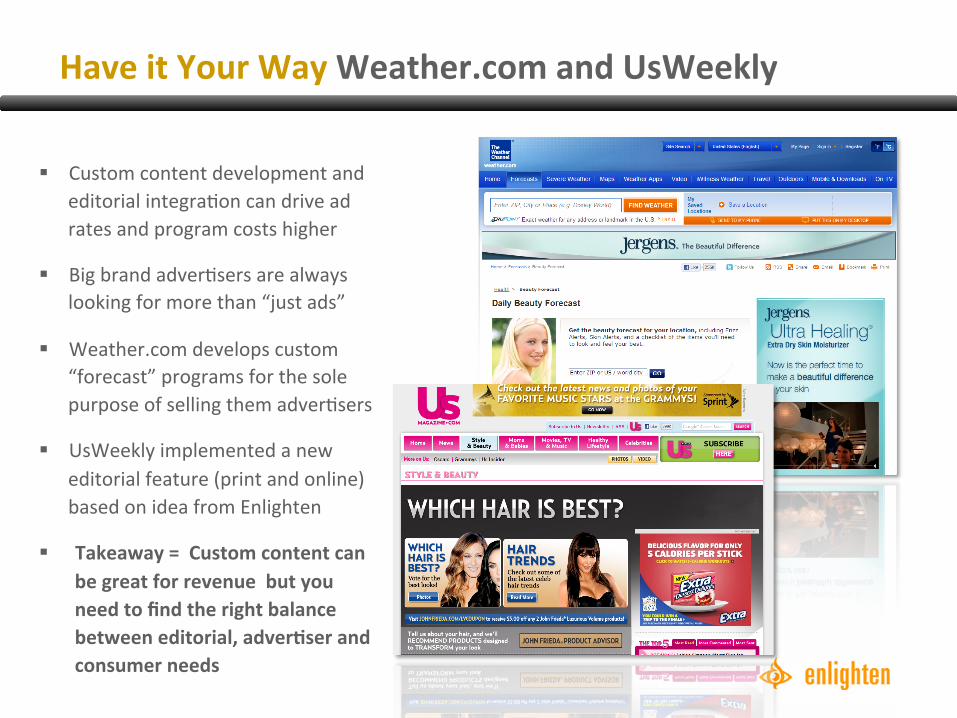

Have it Your Way Weather.com and UsWeekly

§ Custom content development and editorial integra:on can drive ad rates and program costs higher

§ Big brand adver:sers are always looking for more than “just ads”

§ Weather.com develops custom “forecast” programs for the sole purpose of selling them adver:sers

§ UsWeekly implemented a new editorial feature (print and online) based on idea from Enlighten

§ Takeaway = Custom content can be great for revenue but you need to find the right balance between editorial, adver-ser and consumer needs

15

Syndica-on All Music Guide and TechCrunch

§ Content start-‐ups can generate revenue by going narrow and deep in a par:cular area

§ All Music Guide expands revenue beyond adver:sing by licensing deep database of content to other publishers

§ TechCrunch grows revenue by syndica:ng brand to custom research and events

§ Takeaway = Look for opportuni-es to turn content depth in to addi-onal revenue streams

16

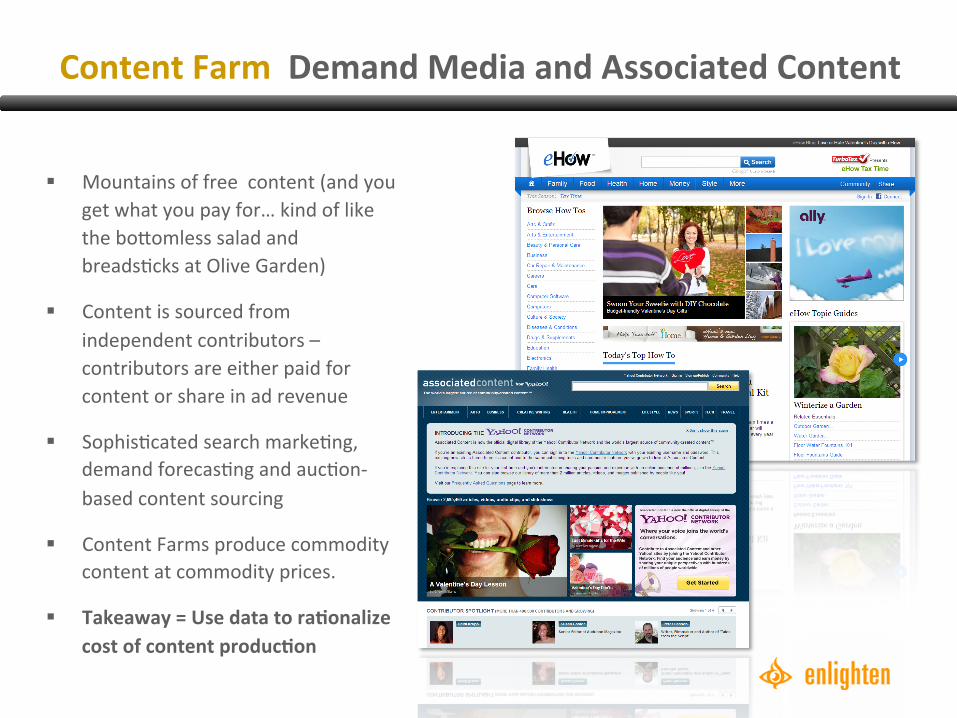

Content Farm Demand Media and Associated Content

§ Mountains of free content (and you get what you pay for… kind of like the bo_omless salad and breads:cks at Olive Garden)

§ Content is sourced from independent contributors – contributors are either paid for content or share in ad revenue

§ Sophis:cated search marke:ng, demand forecas:ng and auc:on-‐based content sourcing

§ Content Farms produce commodity content at commodity prices.

§ Takeaway = Use data to ra-onalize cost of content produc-on

17

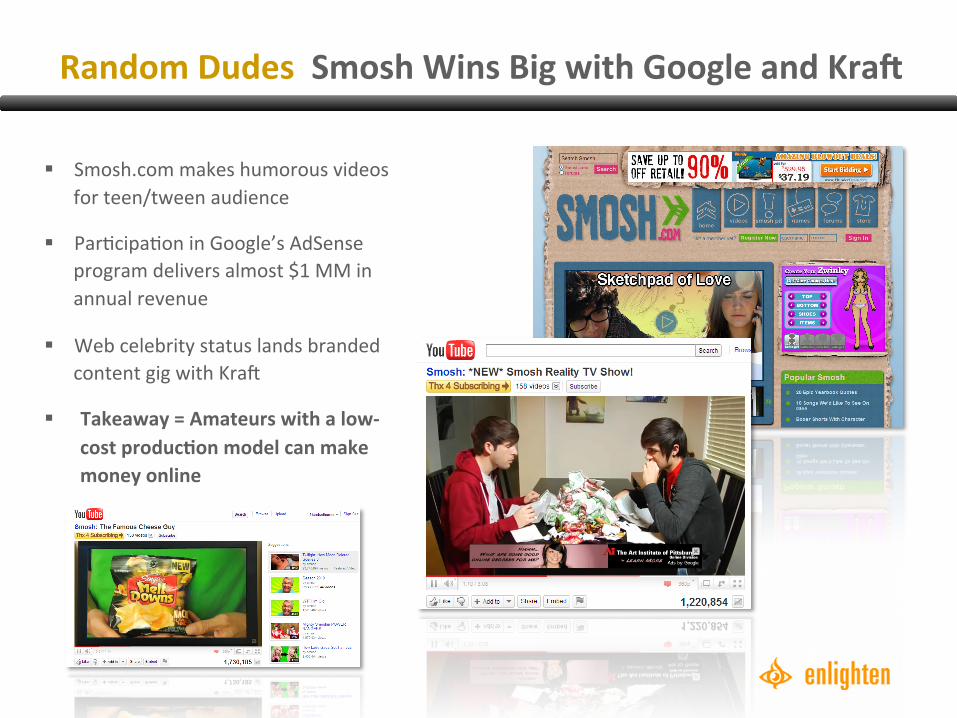

Random Dudes Smosh Wins Big with Google and KraK

§ Smosh.com makes humorous videos for teen/tween audience

§ Par:cipa:on in Google’s AdSense program delivers almost $1 MM in annual revenue

§ Web celebrity status lands branded content gig with Kra<

§ Takeaway = Amateurs with a low-‐cost produc-on model can make money online

18

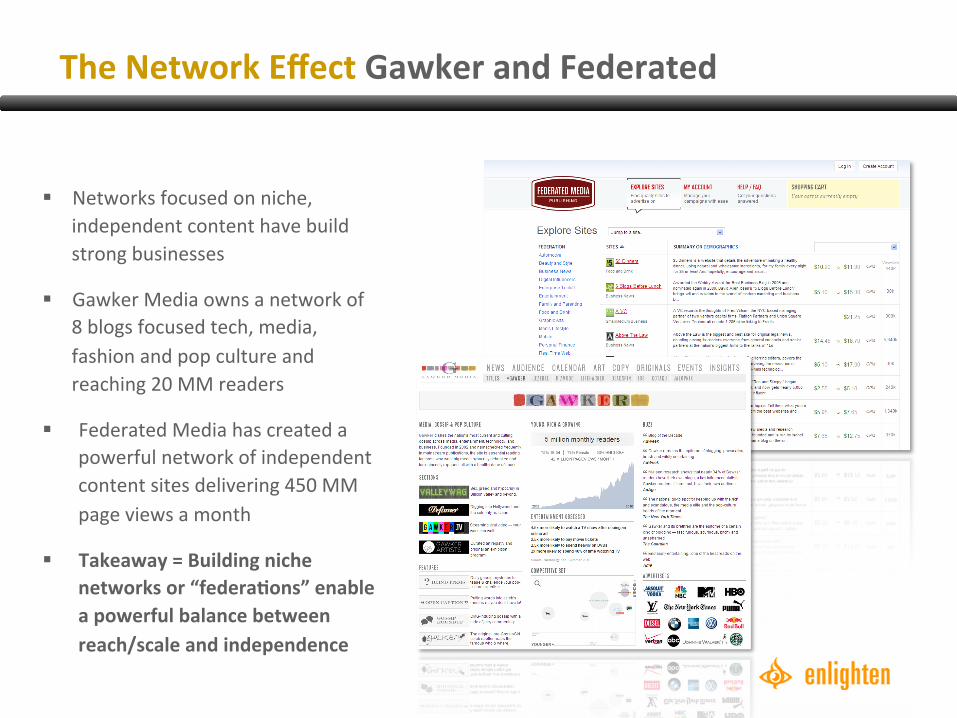

The Network Effect Gawker and Federated

§ Networks focused on niche, independent content have build strong businesses

§ Gawker Media owns a network of 8 blogs focused tech, media, fashion and pop culture and reaching 20 MM readers

§ Federated Media has created a powerful network of independent content sites delivering 450 MM page views a month

§ Takeaway = Building niche networks or “federa-ons” enable a powerful balance between reach/scale and independence

19

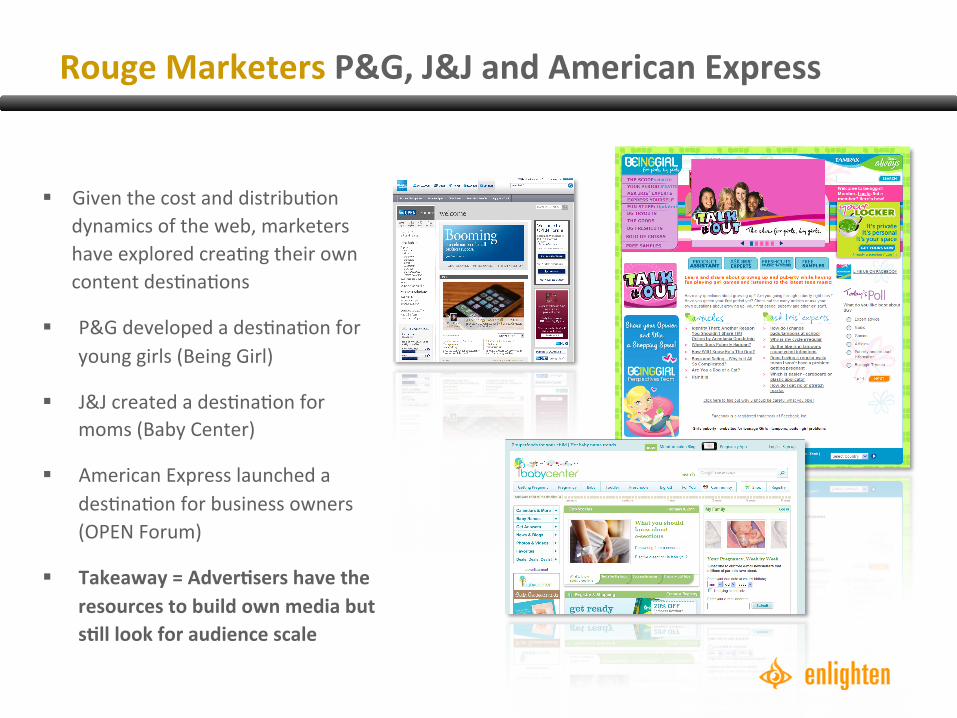

Rouge Marketers P&G, J&J and American Express

§ Given the cost and distribu:on dynamics of the web, marketers have explored crea:ng their own content des:na:ons

§ P&G developed a des:na:on for young girls (Being Girl)

§ J&J created a des:na:on for moms (Baby Center)

§ American Express launched a des:na:on for business owners (OPEN Forum)

§ Takeaway = Adver-sers have the resources to build own media but s-ll look for audience scale

20

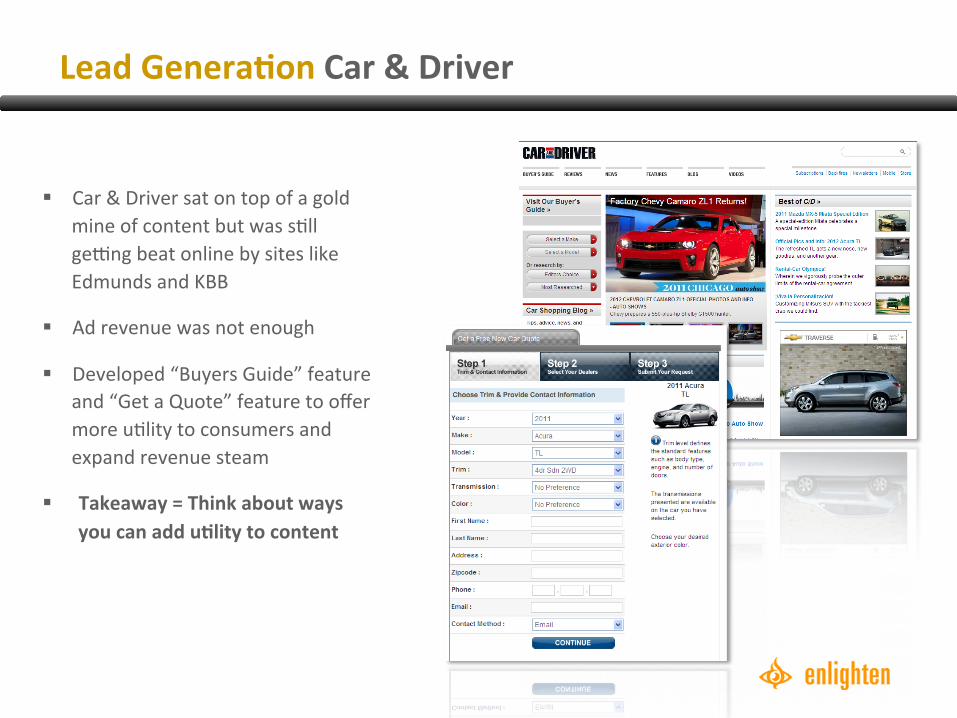

Lead Genera-on Car & Driver

§ Car & Driver sat on top of a gold mine of content but was s:ll gejng beat online by sites like Edmunds and KBB

§ Ad revenue was not enough

§ Developed “Buyers Guide” feature and “Get a Quote” feature to offer more u:lity to consumers and expand revenue steam

§ Takeaway = Think about ways you can add u-lity to content

21

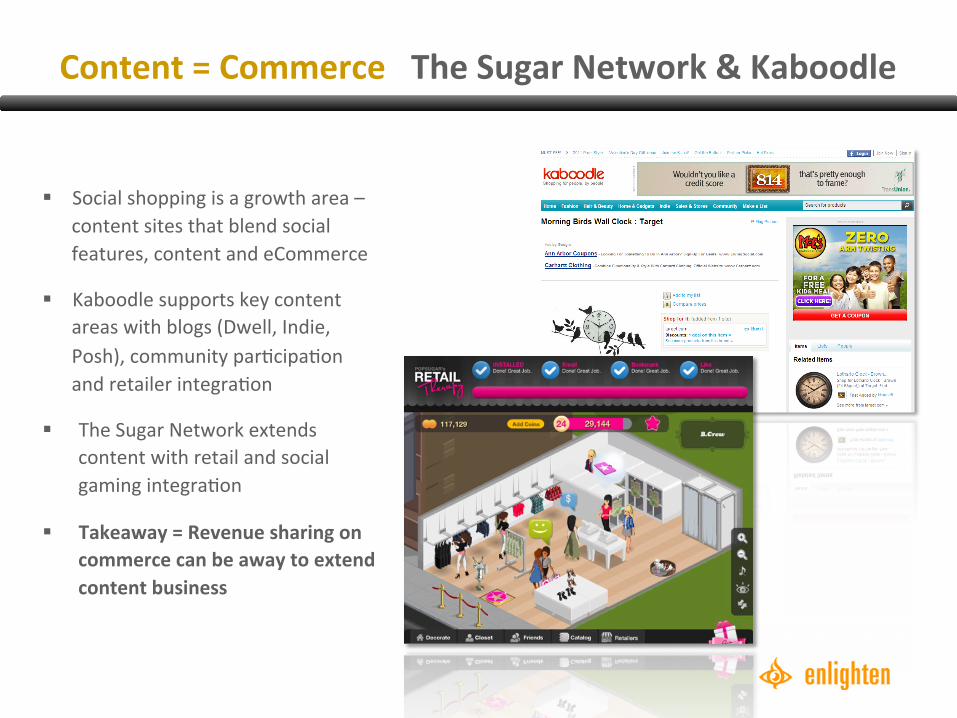

Content = Commerce The Sugar Network & Kaboodle

§ Social shopping is a growth area – content sites that blend social features, content and eCommerce

§ Kaboodle supports key content areas with blogs (Dwell, Indie, Posh), community par:cipa:on and retailer integra:on

§ The Sugar Network extends content with retail and social gaming integra:on

§ Takeaway = Revenue sharing on commerce can be away to extend content business

22

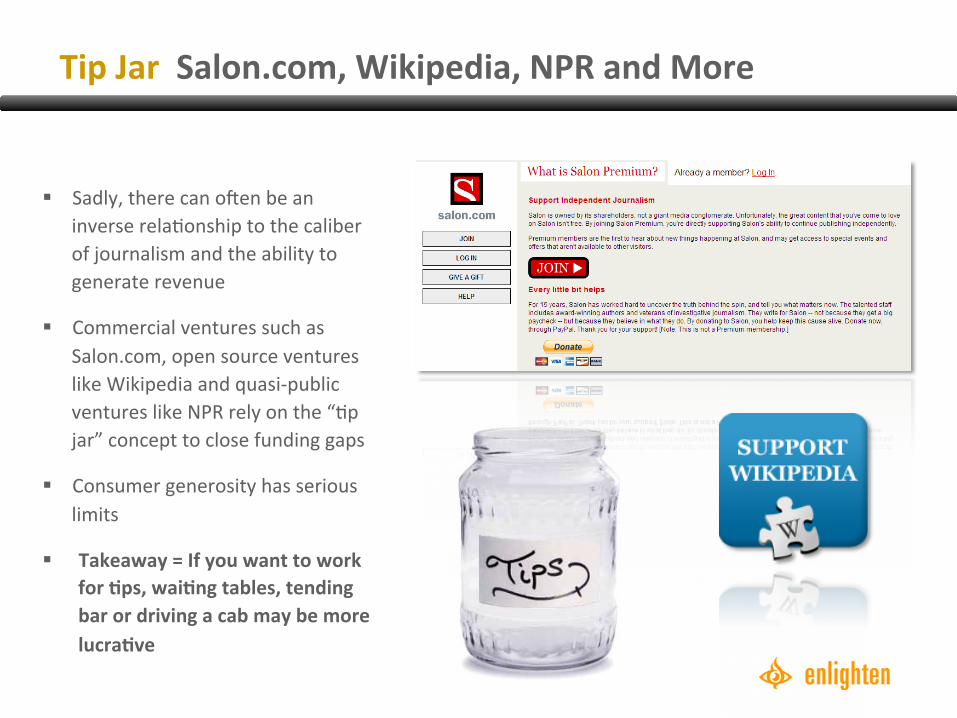

Tip Jar Salon.com, Wikipedia, NPR and More

§ Sadly, there can o<en be an inverse rela:onship to the caliber of journalism and the ability to generate revenue

§ Commercial ventures such as Salon.com, open source ventures like Wikipedia and quasi-‐public ventures like NPR rely on the “:p jar” concept to close funding gaps

§ Consumer generosity has serious limits

§ Takeaway = If you want to work for -ps, wai-ng tables, tending bar or driving a cab may be more lucra-ve

23

A Par-ng Thought

Who Will Start The Next Small Thing?

![[How digital changes Advertising industry] Impacts of digital in advertising, and how it changes advertising people](https://img.pdfslide.us/doc/110x75/58f286991a28ab01178b4573/how-digital-changes-advertising-industry-impacts-of-digital-in-advertising.jpg)

![[How digital changes Advertising industry] Rethink "digital" in advertising](https://img.pdfslide.us/doc/110x75/5873150b1a28ab673e8b4e6f/how-digital-changes-advertising-industry-rethink-digital-in-advertising.jpg)