Embed Size (px)

Citation preview

2014 ISRI Convention

Employee Benefits in the Obamacare World & How To Maximize Its Impact

Presented by:

Joseph AppelbaumPresidentPotomac Companies, Inc.

Purpose

Employers are offered the option to "Pay or Play" under Obamacare, but for most companies there is no choice - they must play in order to recruit and retain employees. Not only must they play in the

health insurance market, but also life, disability, and the whole spectrum of employee benefits from leave to pet insurance. In this session we will discuss the impact of Obamacare on the employee benefits mix

and employer decision-making, along with the importance of insurance benefits as a mandatory

piece of the total compensation puzzle.

THE BASICS

Patient Protection & Affordable Care Act (PPACA or Obamacare)

PPACA (Obamacare)

Key Components

Individual Mandate (2014)• Subsidies• Penalties

Insurance

Mandates

State Mandate

s (Exchang

es)

Employer

Mandate (postponed

to 2015 / 2016)

Individual Mandate

Beginning in 2014, ACA requires individuals to maintain health insurance for themselves and their dependents

Most individuals will be required to maintain "minimum essential coverage", which includes employer coverage individual coverage federal programs such as Medicare and Medicaid

Those who do not maintain minimum essential coverage, and who are not exempt from the mandate, will be required to pay a tax penalty for noncompliance

Individual Mandate

Individual annual Penalties: 2014: $95 per adult and $47.50 per child, up to a

family maximum of $285 or 1 percent of family income, whichever is greater

2015: $325 per adult and $162.50 per child, up to a family maximum of $975 or 2 percent of family income, whichever is greater

2016: $695 per adult and $347.50 per child, up to a family maximum of $2,085 or 2.5 percent of family income, whichever is greater

Employer Mandate

Employer Play or PayApplies to Applicable Large Employers

Employers with 50 or more Full-Time Equivalent Employees (FTEs)

ER penalty applies if coverage is not offered or coverage is offered but "Unaffordable" and a Full-Time Employee (30+ hrs/week) receives A Subsidy in an Exchange

PenaltyALE &

Insurance Not Offered

ORIs Unafford-

able

Full-Time Employee Obtains

Insurance in an Exchange

Employee receives Federal subsidy

$

$

$ $

Employer Mandate

Employers who do not provide coverage Employers who do not provide health coverage

to at least 95% of all full-time employees (and their children under age 26) are subject to a penalty• If at least one full-time employee (30+hrs/wk or 130+

hrs/mo) receives a subsidy to purchase Exchange coverage for himself or herself, the employer is subject to an annual penalty of $2,000 × all full-time employees (reduced by 30)

• Penalty is assessed monthly ($167.67 per full-time employee per month)

Employer Mandate

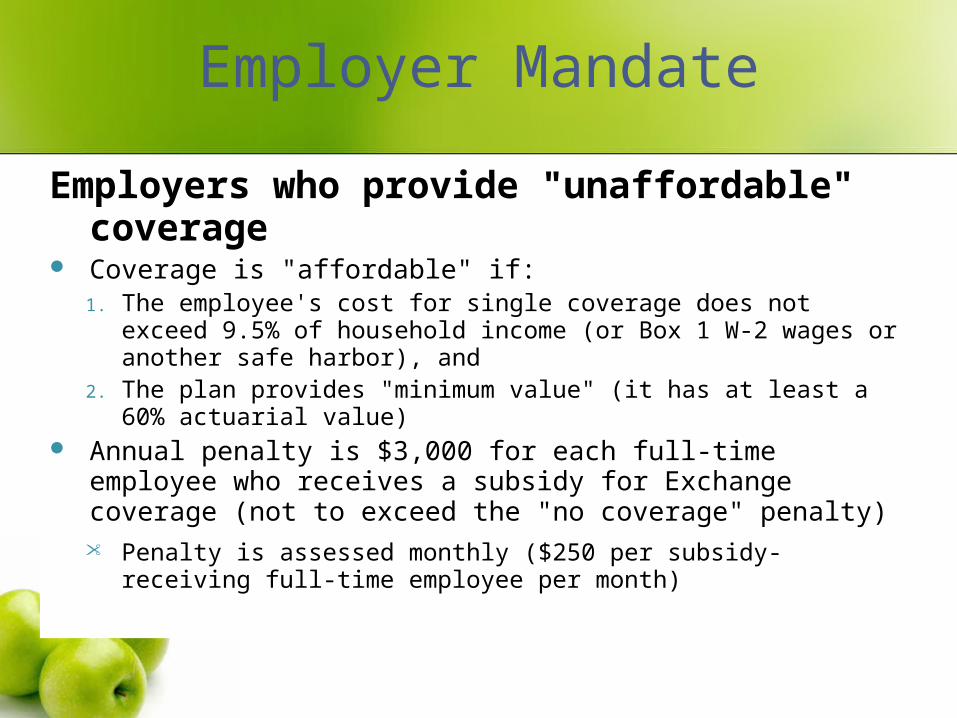

Employers who provide "unaffordable" coverage

Coverage is "affordable" if:1. The employee's cost for single coverage does not exceed 9.5%

of household income (or Box 1 W-2 wages or another safe harbor), and

2. The plan provides "minimum value" (it has at least a 60% actuarial value)

Annual penalty is $3,000 for each full-time employee who receives a subsidy for Exchange coverage (not to exceed the "no coverage" penalty)• Penalty is assessed monthly ($250 per subsidy-receiving full-

time employee per month)

Transition Relief

For 2015, the rules will apply to employers with 100 or more full-time equivalent employees (employers in the 50-99 range will need to certify eligibility for this transition relief)

For 2016, the rules will apply to employers with 50 or more full-time equivalent employees

Transition Relief

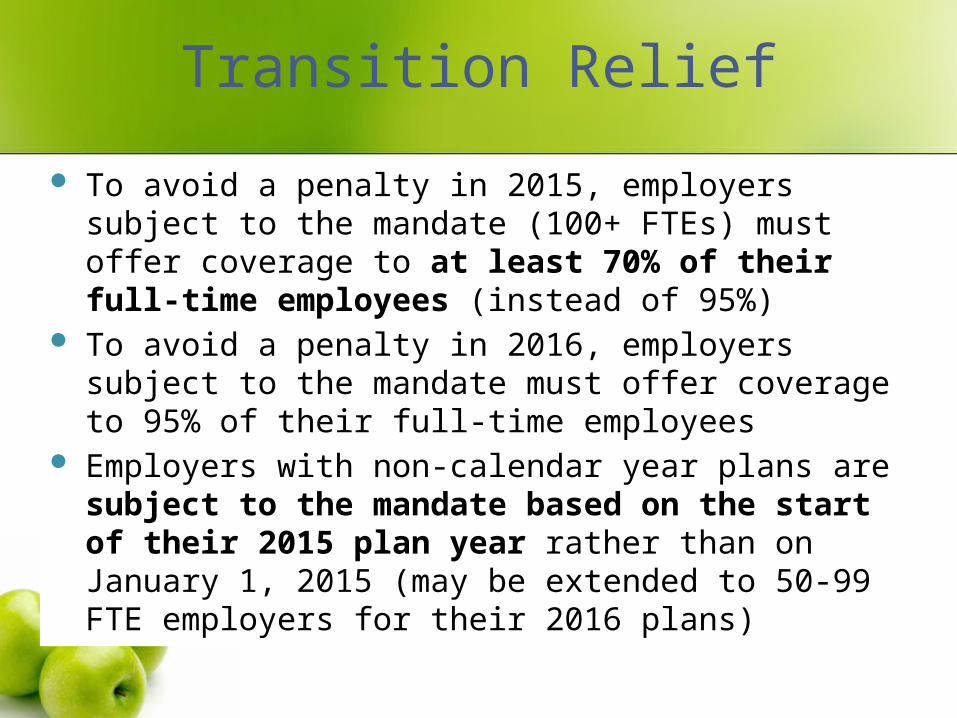

To avoid a penalty in 2015, employers subject to the mandate (100+ FTEs) must offer coverage to at least 70% of their full-time employees (instead of 95%)

To avoid a penalty in 2016, employers subject to the mandate must offer coverage to 95% of their full-time employees

Employers with non-calendar year plans are subject to the mandate based on the start of their 2015 plan year rather than on January 1, 2015 (may be extended to 50-99 FTE employers for their 2016 plans)

Transition Relief

Other transition relief contained in the proposed regulations were extended: The ability to use a short timeframe (at least 6

months) to determine whether an employer is large enough to be subject to the mandate

A delay in the requirement to provide coverage to dependent children to 2016 (as long as the employer is taking steps to arrange for such coverage to begin in 2016)

For 2015 ONLY, penalty calculated by reducing number of employees by 80 instead of 30

Additional Items of Note

90-Day Enrollment Requirement (EFFECTIVE 2014) If EE clearly eligible,

must be enrolled on or before 90th day

This means coverage begins by 91st day

Acceptable waiting period: coverage effective 1st of month following 60 days

Affordability Safe Harbors W-2 safe harbor Rate of pay safe

harbor Federal poverty line

safe harbor

Exchanges

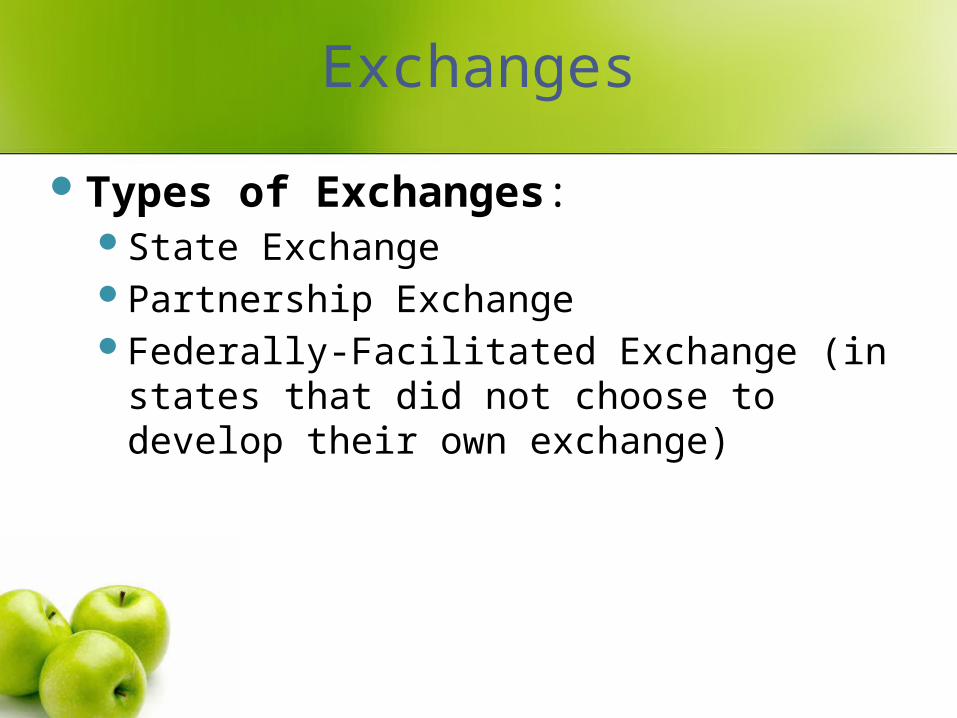

Types of Exchanges: State ExchangePartnership Exchange Federally-Facilitated Exchange (in states

that did not choose to develop their own exchange)

Exchanges

The Metals—Exchanges to Offer Four Levels of Coverage: Bronze (60%) Silver (70%) Gold (80%) Platinum (90%)

And a catastrophic plan for individuals under 30

Premium Tax Credits

Premium tax credits are federal subsidies—direct payments to insurance companies to subsidize coverage for lower-income individuals in the state-based Exchanges

The subsidy helps lower-income people between 100% and 400% of Federal Poverty Level (FPL) purchase a silver level plan (70% plan)

RECRUITMENT & RETENTIONWhy Choose to “Play”?

Getting & Keeping Employees

The cost of employee turnover can be extensive – 1/2 to 2 times annual pay per lost employeeCost of losing trained EECost of temp or OT while position emptyRecruitment costsTraining costsLost productivity costs

Getting & Keeping Employees

Average national turnover rate has been running at 25% for manufacturing, construction, scrap recycling & related industries

Example: 25% turnover; 200 employees; average pay rate $12.00 per hour; turnover cost at 1/2 X payTurnover costs to company equals $624K

on an annual basis based on this example

Getting & Keeping Employees

Employers are using benefits as leverage to recruit & retain employees: Total Rewards

Health care & retirement savings are the most leveraged benefits for recruitment & retention*

Employees must have health insurance now – easiest place to get it is through their employer

Premiums tax deductible to the employer & employee

Getting & Keeping Employees

If turnover can be reduced through the increase of the Total Reward package (i.e., added benefits), why not use the savings to fund the added benefits??

Improve

Total Rewards

Reduce Employee Turnover

Reduce Costs to Fund Total Rewards package

Retention & Profitability

Using the example of the 200 person company: If the 25% turnover cost your organization

$624k/year, what would you do with that money if it didn’t walk out the door?

How do you minimize that loss and add it back into your bottom line profitability?

Retention & Profitability

Will 50 cents an hour change that? 200 people times an average of 2,080 hours times 50

cents = $208k What would you do with $416k? What about

increasing benefits? Why are you losing employees?

Are they transient? Will they move for an extra 50 cents an hour? Are you not offering benefits (ACA requirement)? Not contributing enough? Improper hiring practices? Or improper training? Settling for a belly button?

WHAT TO DOConsidering the Investment

Benefits in the Mix

Health Insurance – 97% of ALL employers offer health coverage for at least the employeeDental – 96%Vision 79%

Life Insurance – 84% of employers offer life insurance

Disability – 68% offer STD and 80% offer LTD (primarily paid 100% by ER)

*Results from 2012 SHRM National Benefits Survey

Benefits in the Mix

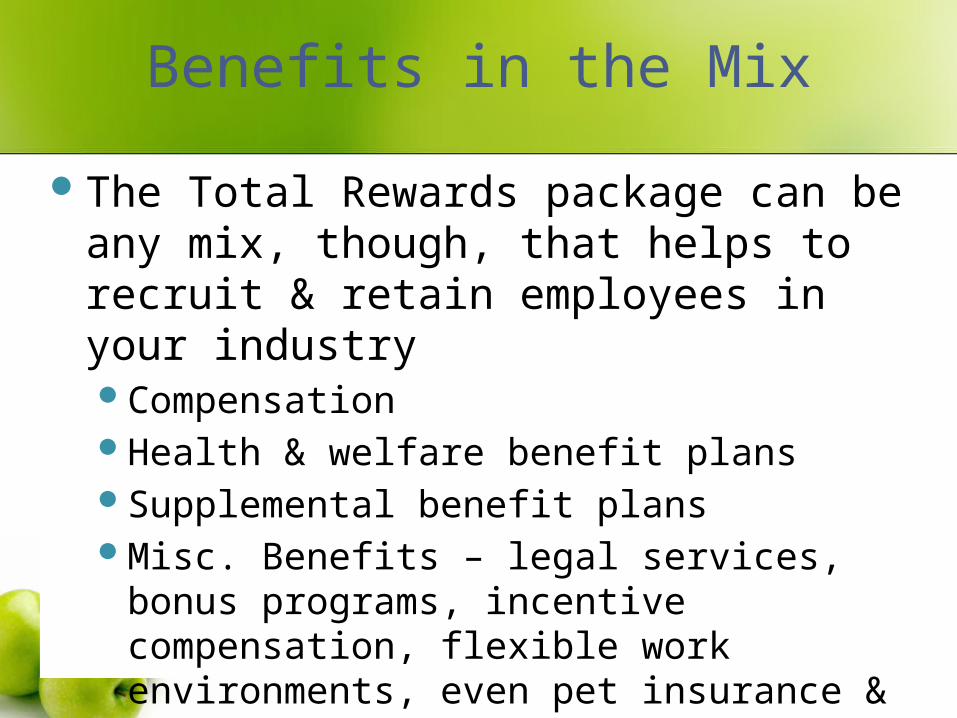

The Total Rewards package can be any mix, though, that helps to recruit & retain employees in your industryCompensationHealth & welfare benefit plansSupplemental benefit plansMisc. Benefits – legal services, bonus

programs, incentive compensation, flexible work environments, even pet insurance & the list goes on

Employee Healthcare

Despite the cost pressures of health care benefits, majority of employers will continue to offer coverage*, but…They are resetting benefit valueThey are actively engaging employees in

improving their own healthThey are focusing on choiceThey are exploring new options like

Private Exchanges & Self-Funding

Private Exchanges

A private exchange is an on-line portal used to sell insurance products directly to employees

Employees are allowed to become consumers and shop from among a wide variety of major medical health plans and supplemental insurance products

A private exchange reduces the role the employer plays in the selection of insurance coverage for its employees

Private Exchanges

Why are employer’s looking at Private HC ExchangesOne-stop shopping across core

medical, life, disability, & voluntary benefits

Technology & choice eases employee decision-making

Collective buying power & influence help control total benefit costs

Partially Self-Funding

Partially self-funding insurance benefits for groups with 50 or more employees is an option for controlling costs

Not for everyone – works well for groups with relatively low claims costs (low plan utilizers)

Wrap-Up

Your employees are a corporate asset – retain them

Your employees are what drives your business

Taking care of them is a required business practice in today’s economy - it translates into healthier, more productive & longer term employees

Wrap-Up

Obamacare may seem complicated, but it does not alter the fundamental need for companies to offer a Total Rewards package that effectively attracts and retains employees

Find the right guidance in a broker or consultant to help you navigate the Total Rewards options

Thank you!

Joseph AppelbaumPresident

Potomac Companies, Inc.www.potomacco.com