Embed Size (px)

Citation preview

2016 Energy OutlookCommercial real estate markets adapt amid volatile energy market conditions North America | 2016

5 Key ThemesExploring:• Macroeconomic Factors Influencing Energy Markets• State of Oil and Gas Companies• The Impact to Upstream, Midstream and Downstream• Regulations and Legislation• Trends in Renewable Energy

2

3

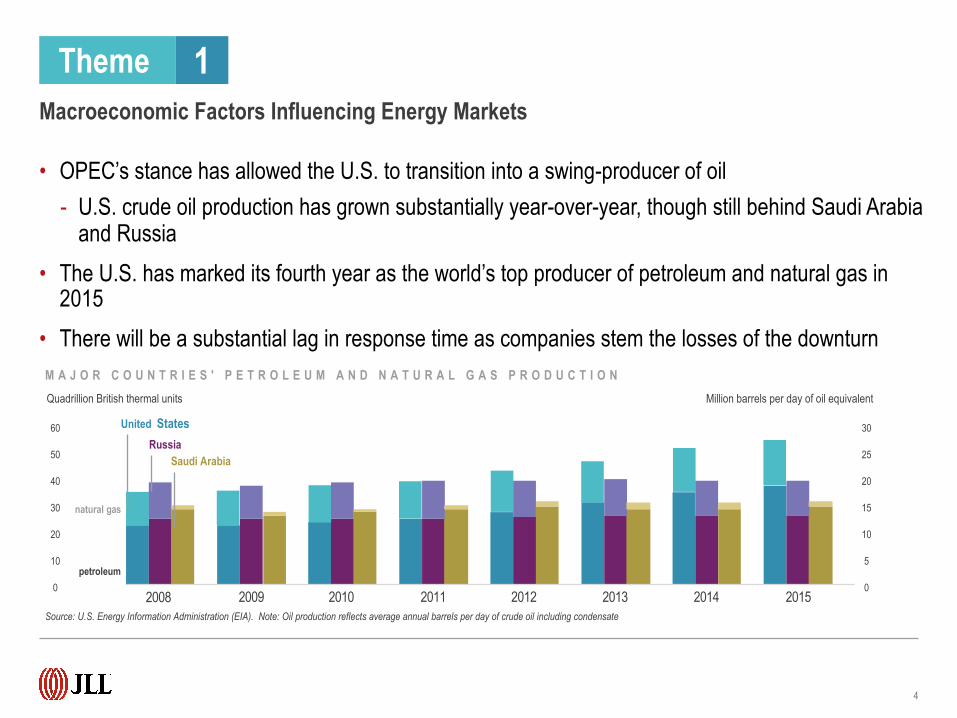

Macroeconomic Factors Influencing Energy Markets

Theme 1

60

50

40

30

20

10

0

30

25

20

15

10

5

0

• OPEC’s stance has allowed the U.S. to transition into a swing-producer of oil- U.S. crude oil production has grown substantially year-over-year, though still behind Saudi Arabia

and Russia• The U.S. has marked its fourth year as the world’s top producer of petroleum and natural gas in

2015• There will be a substantial lag in response time as companies stem the losses of the downturn

4

Macroeconomic Factors Influencing Energy Markets

05

101520253035404550

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32

M A J O R C O U N T R I E S ' P E T R O L E U M A N D N A T U R A L G A S P R O D U C T I O N

United StatesRussia

Saudi Arabia

natural gas

petroleum

Source: U.S. Energy Information Administration (EIA). Note: Oil production reflects average annual barrels per day of crude oil including condensate

Quadrillion British thermal units Million barrels per day of oil equivalent

2009 2010 2011 2012 2013 2014 20152008

Theme 1

5

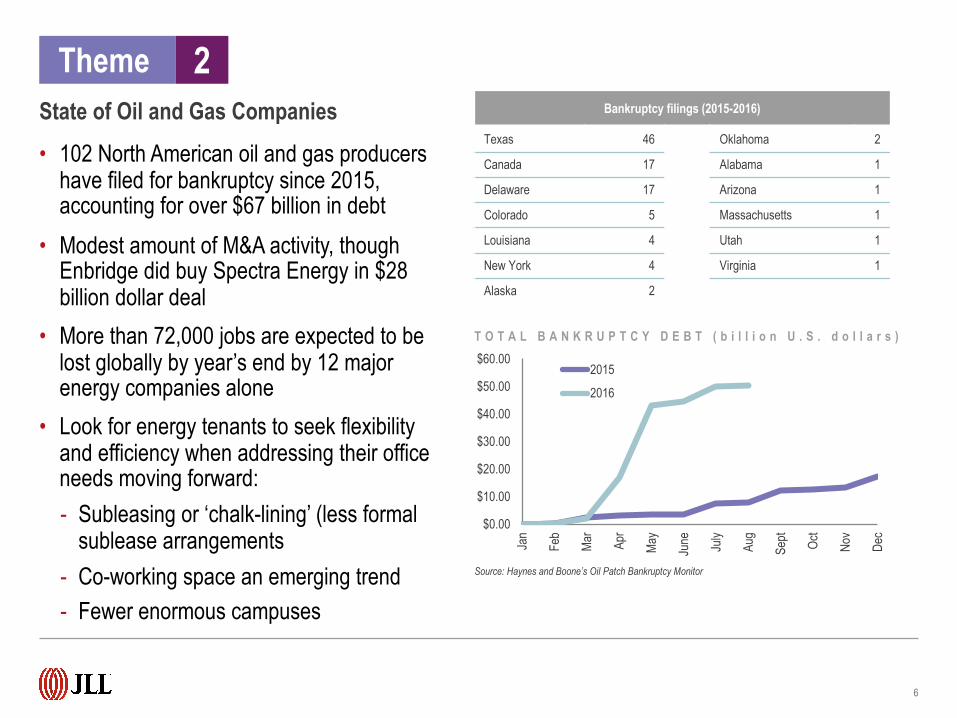

State of Oil and Gas Companies

Theme 2

• 102 North American oil and gas producers have filed for bankruptcy since 2015, accounting for over $67 billion in debt

• Modest amount of M&A activity, though Enbridge did buy Spectra Energy in $28 billion dollar deal

• More than 72,000 jobs are expected to be lost globally by year’s end by 12 major energy companies alone

• Look for energy tenants to seek flexibility and efficiency when addressing their office needs moving forward:- Subleasing or ‘chalk-lining’ (less formal

sublease arrangements- Co-working space an emerging trend- Fewer enormous campuses

6

State of Oil and Gas Companies

T O T A L B A N K R U P T C Y D E B T ( b i l l i o n U . S . d o l l a r s )

Source: Haynes and Boone’s Oil Patch Bankruptcy Monitor

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

Jan

Feb

Mar

Apr

May

June July

Aug

Sept Oct

Nov

Dec

2015

2016

Bankruptcy filings (2015-2016)

Texas 46 Oklahoma 2

Canada 17 Alabama 1

Delaware 17 Arizona 1

Colorado 5 Massachusetts 1

Louisiana 4 Utah 1

New York 4 Virginia 1

Alaska 2

Theme 2

7

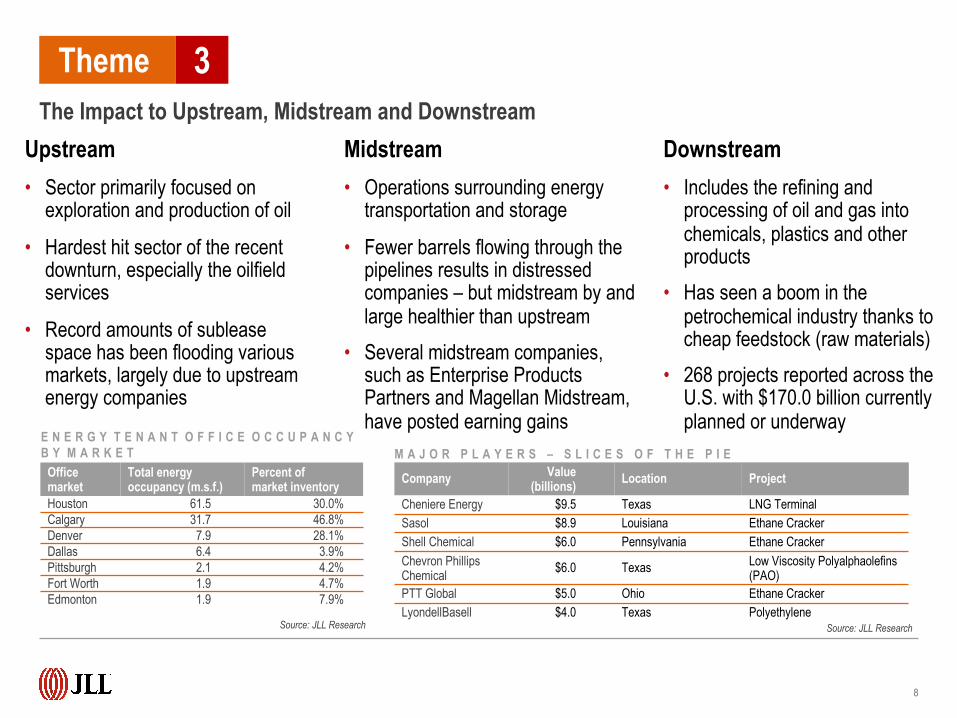

The Impact to Upstream, Midstream and Downstream

Theme 3

Upstream• Sector primarily focused on

exploration and production of oil

• Hardest hit sector of the recent downturn, especially the oilfield services

• Record amounts of sublease space has been flooding various markets, largely due to upstream energy companies

8

The Impact to Upstream, Midstream and DownstreamMidstream• Operations surrounding energy

transportation and storage

• Fewer barrels flowing through the pipelines results in distressed companies – but midstream by and large healthier than upstream

• Several midstream companies, such as Enterprise Products Partners and Magellan Midstream, have posted earning gains

Downstream• Includes the refining and

processing of oil and gas into chemicals, plastics and other products

• Has seen a boom in the petrochemical industry thanks to cheap feedstock (raw materials)

• 268 projects reported across the U.S. with $170.0 billion currently planned or underway

Theme 3

Office market

Total energy occupancy (m.s.f.)

Percent of market inventory

Houston 61.5 30.0%Calgary 31.7 46.8%Denver 7.9 28.1%Dallas 6.4 3.9%Pittsburgh 2.1 4.2%Fort Worth 1.9 4.7%Edmonton 1.9 7.9%

E N E R G Y T E N A N T O F F I C E O C C U P A N C YB Y M A R K E T

Source: JLL Research

Company Value (billions) Location Project

Cheniere Energy $9.5 Texas LNG TerminalSasol $8.9 Louisiana Ethane CrackerShell Chemical $6.0 Pennsylvania Ethane CrackerChevron Phillips Chemical $6.0 Texas Low Viscosity Polyalphaolefins

(PAO)PTT Global $5.0 Ohio Ethane CrackerLyondellBasell $4.0 Texas Polyethylene

M A J O R P L A Y E R S – S L I C E S O F T H E P I E

Source: JLL Research

9

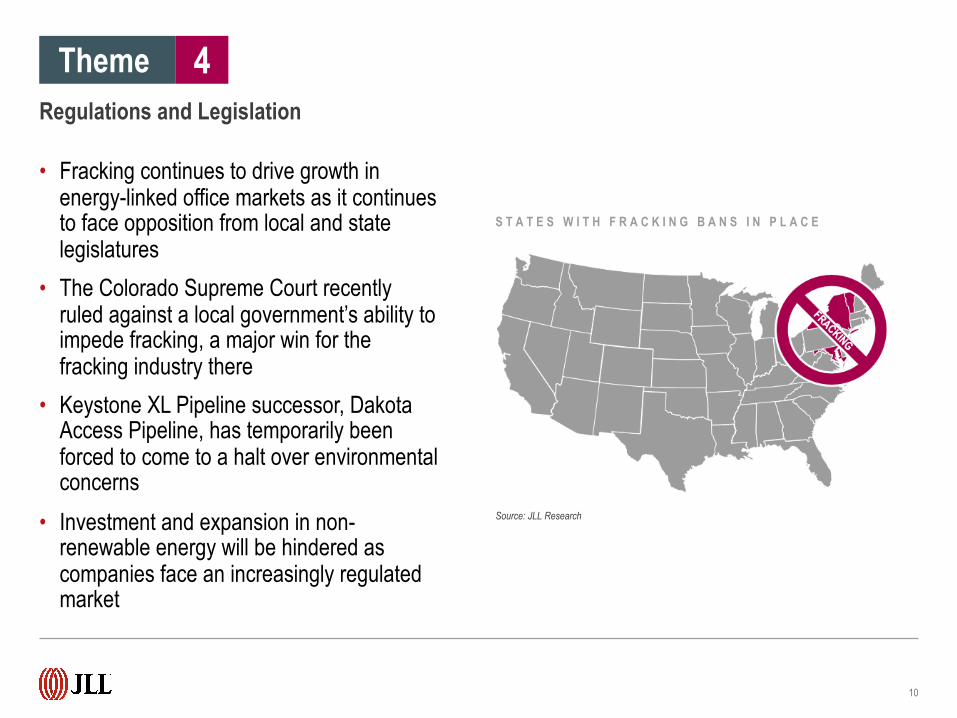

Regulations and Legislation

Theme 4

• Fracking continues to drive growth in energy-linked office markets as it continues to face opposition from local and state legislatures

• The Colorado Supreme Court recently ruled against a local government’s ability to impede fracking, a major win for the fracking industry there

• Keystone XL Pipeline successor, Dakota Access Pipeline, has temporarily been forced to come to a halt over environmental concerns

• Investment and expansion in non-renewable energy will be hindered as companies face an increasingly regulated market

10

Regulations and Legislation

S T A T E S W I T H F R A C K I N G B A N S I N P L A C E

Source: JLL Research

Theme 4

11

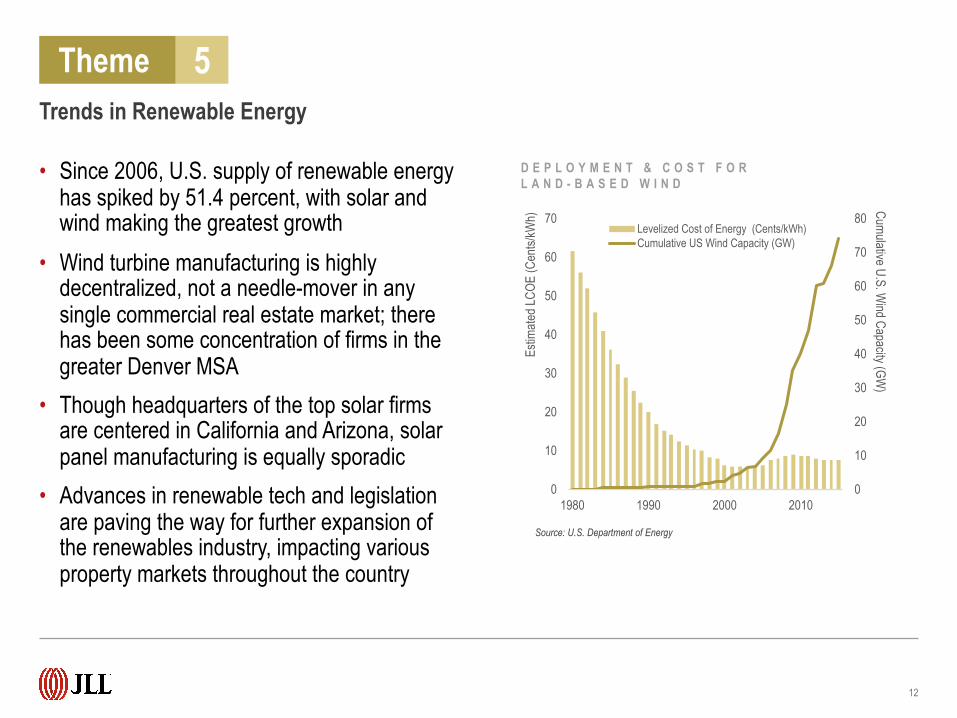

Trends in Renewable Energy

Theme 5

• Since 2006, U.S. supply of renewable energy has spiked by 51.4 percent, with solar and wind making the greatest growth

• Wind turbine manufacturing is highly decentralized, not a needle-mover in any single commercial real estate market; there has been some concentration of firms in the greater Denver MSA

• Though headquarters of the top solar firms are centered in California and Arizona, solar panel manufacturing is equally sporadic

• Advances in renewable tech and legislation are paving the way for further expansion of the renewables industry, impacting various property markets throughout the country

12

Trends in Renewable Energy

D E P L O Y M E N T & C O S T F O R L A N D - B A S E D W I N D

0

10

20

30

40

50

60

70

80

1980 1990 2000 20100

10

20

30

40

50

60

70

Cumulative U.S. Wind Capacity (GW

)

Estim

ated L

COE

(Cen

ts/kW

h)

Levelized Cost of Energy (Cents/kWh)Cumulative US Wind Capacity (GW)

Source: U.S. Department of Energy

Theme 5

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016

For more information, please contact:

Bruce RutherfordInternational DirectorEnergy Practice Group+1 (713) [email protected]

Eli GilbertDirector of Energy ResearchAmericas Research+1 (713) [email protected]

Lindsay BrownSenior Vice PresidentEnergy Practice Group+1 (303) [email protected]

Rachel AlexanderResearch ManagerAmericas Research +1 (713) [email protected]

Like what you saw here? >>> Get more from our 2016 Energy Outlook.

![[Unchanged] Opportunity amid adversity - I3investorcdn1.i3investor.com/my/files/dfgs88n/2016/01/07/1483882668... · Opportunity amid adversity Adapt ... for corporate exercises](https://img.pdfslide.us/doc/110x75/5b0a24417f8b9abe5d8dc293/unchanged-opportunity-amid-adversity-i3investorcdn1-amid-adversity-adapt-.jpg)