Embed Size (px)

Citation preview

2014 - 2015 CALIFORNIA ECONOMIC & MARKET

OUTLOOK October 29,2014

SILVAR

Leslie Appleton-Young, Chief Economist

OVERVIEW

• Economic Outlook

• California Housing Market Outlook

• Housing Affordability

• Regional Market

• 2015 Forecast

ECONOMIC OUTLOOK

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

200

5

200

6

200

7

200

8

200

9

2010

2011

2012

2013

2014

P

Q2

-10

Q3-

10

Q4

-10

Q1-

11

Q2

-11

Q3-

11

Q4

-11

Q1-

12

Q2

-12

Q3-

12

Q4

-12

Q1-

13

Q2

-13

Q3-

13

Q4

-13

Q1-

14

Q2

-14

ECONOMY: GAINING MOMENTUM

2013: 1.9%; 2014: 2.2%; 2015: 3.0%; 2014 Q2: 4.6% ANNUAL PERCENT CHANGE, CHAIN-TYPE (2005) $

ANNUALLY QUARTERLY

2009 Largest Annual Drop since 1938 (-3.4%)

SERIES: GDP SOURCE: US Dept. of Commerce, Bureau of Economic Analysis

US UNEMPLOYMENT RATE BELOW 6%

CA - 7.3% (Sep. 2014) vs. US - 5.9% (Sep. 2014)

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14% US-CA CA US

SERIES: Unemployment Rate SOURCE: US Bureau of Labor Statistics, CA Employment Development Division

EMPLOYMENT GROWTH, CA VS. U.S.

-8

-6

-4

-2

0

2

4 California US

ANNUAL PERCENT CHANGE

SERIES: Total Nonfarm Employment SOURCE: US Bureau of Labor Statistics, CA Employment Development Division

PERCENT JOB LOSSES PRIOR RECESSIONS – RECENT CYCLE WORST BY FAR

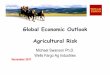

EMPLOYMENT GROWTH, BY INDUSTRY

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Construction Manufacturing Service

ANNUAL PERCENT CHANGE

SERIES: Total Nonfarm Employment By Industry SOURCE: CA Employment Development Division

September 2014: CA +2.3%, +390,600

CALIFORNIA JOB CHANGES BY INDUSTRY

-2.2%

-1.7%

-0.3%

0.9%

1.3%

1.4%

1.5%

1.5%

2.1%

2.3%

3.3%

4.7%

4.9%

5.3%

6.2%

-3% -2% -1% 0% 1% 2% 3% 4% 5% 6% 7%

Nondurable Goods

Finance & Insurance

Government

Durable Goods

Educational Services

Wholesale Trade

Retail Trade

Transportation, Warehousing & Utilities

Real Estate & Rental & Leasing

Leisure & Hospitality

Health Care & Social Assistance

Professional, Scientific & Technical Services

Information

Admistrative & Support & Waste Services

Construction

SERIES: Total Nonfarm Employment By Industry SOURCE: US Bureau of Labor Statistics, CA Employment Development Division

September 2014: CA +2.3%, +390,600 ANNUAL PERCENT CHANGE

JOB TRENDS BY CALIFORNIA METRO AREA

1.1%

1.3%

1.7%

1.8%

1.9%

2.0%

2.0%

2.1%

2.5%

2.5%

3.5%

3.7%

0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0%

Modesto

Stockton MSA

Bakersfield

Los Angeles

Orange …

Ventura

Oakland

Sacramento

Fresno MSA

San Diego

San Jose

San Francisco

SERIES: Total Nonfarm Employment SOURCE: CA Employment Development Division

AN

NU

AL

PE

RC

EN

T C

HA

NG

E

September 2014: CA +2.3%, +390,600

CONSUMER PRICE INDEX

September 2014: All Items +1.7% YTY; Core +1.7% YTY

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6% All Items Core

ANNUAL PERCENT CHANGE

SERIES: Consumer Price Index SOURCE: US Bureau of Labor Statistics

CONSUMER CONFIDENCE: UNCERTAINTY October 2014: 94.5

INDEX, 100=1985

SERIES: Consumer Confidence SOURCE: The Conference Board

0

20

40

60

80

100

120

0%

1%

2%

3%

4%

5%

6%

200

9/0

1

200

9/0

4

200

9/0

7

200

9/1

0

2010

/01

2010

/04

2010

/07

2010

/10

2011

/01

2011

/04

2011

/07

2011

/10

2012

/01

2012

/04

2012

/07

2012

/10

2013

/01

2013

/04

2013

/07

2013

/10

2014

/01

2014

/04

2014

/07

8.2

8.1

4

9.1

8.1

4

FRM

ARM

MORTGAGE RATES: WHAT HAPPENED?

January 2009 – October 2014

MONTHLY WEEKLY

SERIES: 30Yr FRM, 1Yr ARM SOURCE: Federal Home Loan Mortgage Corporation

FORECASTERS HAVE BEEN EXPECTING RATES TO RISE

Percent

0

1

2

3

4

5

6

0

1

2

3

4

5

6

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Actual 10-year Treasury yield (solid black line)

Predictions out to five quarters ahead of professional forecasters (hatched lines)

Percent

SERIES: Loan Officer Survey SOURCE: Philadelphia Federal Reserve Survey of Professional Forecasters, Bloomberg

MORTGAGE RATES + 1% SPRING 2013 ACTUAL TAPERING? NO IMPACT?

0%

1%

2%

3%

4%

5%

6%

7%

8% FRM ARM Federal Funds

SERIES: 30Yr FRM, 1Yr ARM, Federal Funds SOURCE: Federal Home Loan Mortgage Corporation

U.S. DEPOSITORY INSTITUTIONS: HIGH LEVEL OF EXCESS RESERVES SINCE 9/08

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

SERIES: Excess Reserves of Depository Institutions SOURCE: Federal Reserve Bank of Saint Louis

$ BILLIONS

U.S. ECONOMIC FORECAST

Gross Domestic Product

Nonfarm Job Growth

Unemployment Rate

Consumer Price Index

Real Disposable Income, % Change

2011

1.8%

1.2%

8.9%

3.1%

1.3%

2012

2.8%

1.7%

8.1%

2.1%

1.5%

2013

1.9%

1.7%

7.4%

1.5%

0.7%

2014 P

2.2%

1.8%

6.2%

2.0%

2.6%

2015 F

3.0%

2.2%

5.8%

2.2%

2.6%

SERIES: U.S. Economic Outlook SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

CALIFORNIA ECONOMIC FORECAST

SERIES: CA Economic Outlook SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

Nonfarm Job Growth

Unemployment Rate

Population Growth

Real Disposable Income, % Change

2011

1.1%

11.8%

0.7%

1.9%

2012

2.4%

10.4%

0.7%

1.1%

2013

3.0%

8.9%

0.9%

0.9%

2014 P

2.2%

7.5%

0.9%

3.0%

2015 F

2.4%

6.7%

0.9%

3.8%

CALIFORNIA HOUSING MARKET OUTLOOK

TODAY’S MARKET

• Clearly well on the road to recovering - Bay Area strongest regional market

• Volume – A bit down, still reliant on investment sales

• Prices up sharply, but increases slowing in most markets

• Inventory remains tight but up from last year

• Pent-up/unrealized demand not yet translating into sales

• Affordability challenges emerging once again…

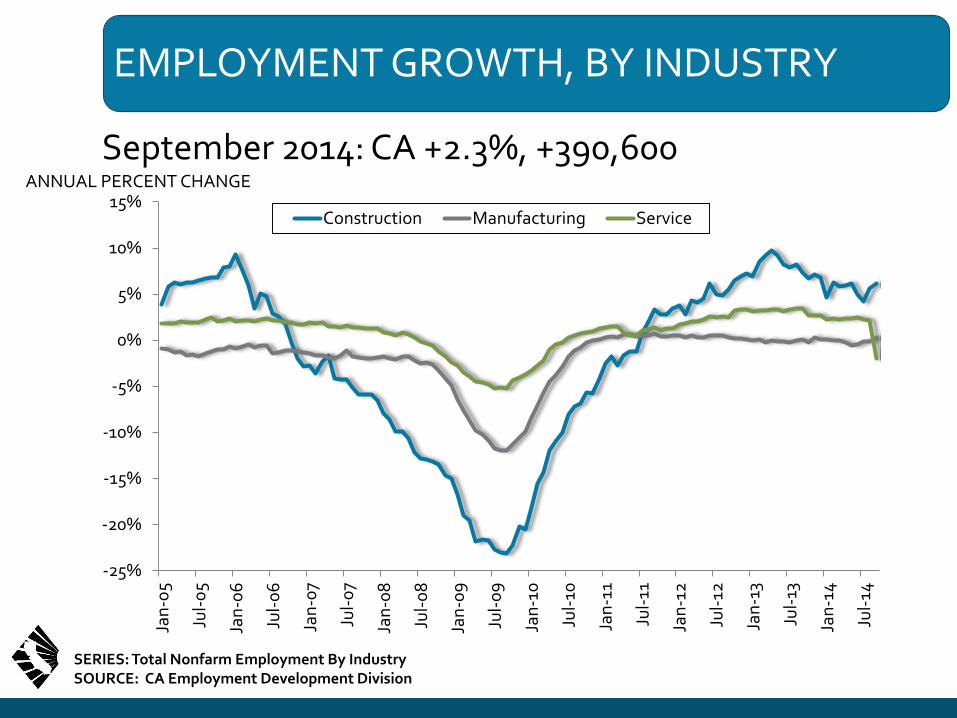

CA SALES FLAT SINCE SPRING 2014

California, Sep. 2014 Sales: 396,440 Units, -9.5% YTD, -4.2% YTY

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

*Sales are seasonally adjusted and annualized SERIES: Sales of Existing Single Family Homes SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

Sep-14: 396,440

Sep-13: 413,850

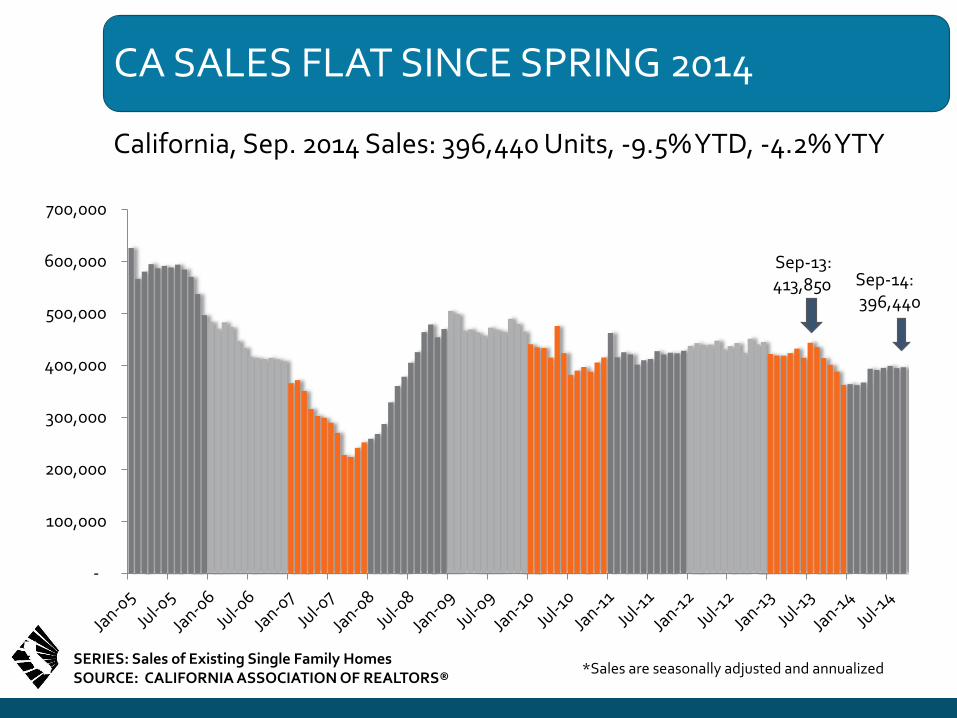

MULTIPLE OFFERS DECLINE WITH LESS INTENSE MARKET COMPETITION IN 2014 AFTER PEAKING IN 2013

72%

53% 5.7

4.3

0

1

2

3

4

5

6

7

0%

10%

20%

30%

40%

50%

60%

70%

80%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

% with Multiple Offers # of Multiple offers (Average)

SERIES: 2014 Housing Market Survey SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

49 % SOLD BELOW ASKING IN 2014

7%

11%

28%

54%

0% 20% 40% 60%

20% or more

10% to 19.99%

5% to 9.99%

Less than 5%

% of Price Reduction (Properties Sold Below Asking Price)

49%

18%

33%

Sale Price to Asking Price

Below Asking Price At Asking Price Above Asking Price

SERIES: 2014 Housing Market Survey SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

Median Reduction: 4.5% of List Price

50%

33%

0%

10%

20%

30%

40%

50%

60%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

% of Sales above Asking Price

Long Run Average = 19%

FEWER HOMES SOLD ABOVE THE ASKING PRICE AS MARKET COMPETITION COOLED IN 2014

0

2

4

6

8

10

12

14

16

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Med. Price Discount

Med. Weeks on MLS

0%, 2.1

weeks

Median Price Discount & Weeks on Market

QUESTION: What was the original list sales price of the property? What was the final sales price of the property? How many weeks did the property remain on the MLS? SERIES: 2014 Housing Market Survey SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

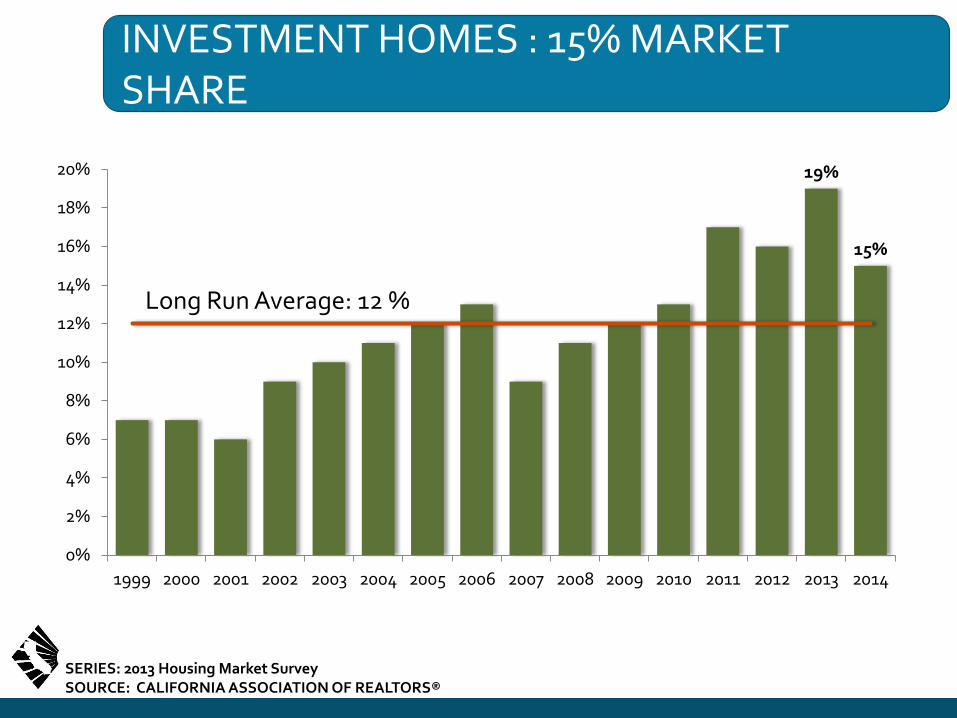

INVESTMENT HOMES : 15% MARKET SHARE

19%

15%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Long Run Average: 12 %

SERIES: 2013 Housing Market Survey SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

WE’VE COME A LONG WAY SINCE 2009: EQUITY SALES: 9 OUT OF 10 TRANSACTIONS

91.0%

4.6%

4.0% 0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-10

Jul-

10

Oct

-10

Jan

-11

Ap

r-11

Jul-

11

Oct

-11

Jan

-12

Ap

r-12

Jul-

12

Oct

-12

Jan

-13

Ap

r-13

Jul-

13

Oct

-13

Jan

-14

Ap

r-14

Jul-

14

Equity Sales Short Sale REO

SERIES: Distressed Sales, Not Seasonally Adjusted SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

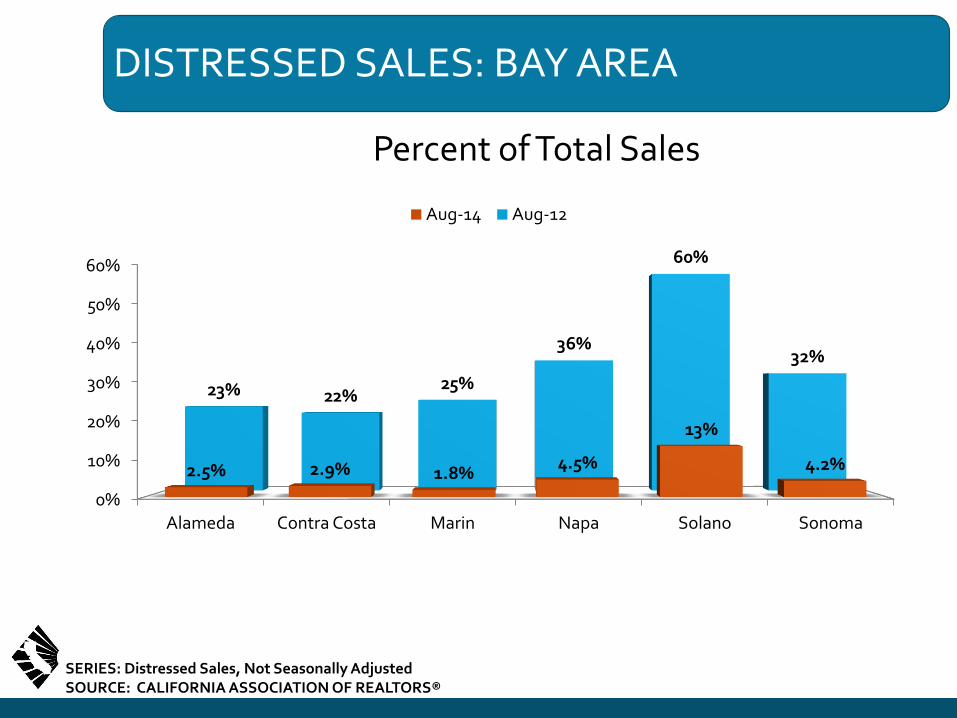

DISTRESSED SALES: BAY AREA

Percent of Total Sales

0%

10%

20%

30%

40%

50%

60%

Alameda Contra Costa Marin Napa Solano Sonoma

2.5% 2.9% 1.8% 4.5%

13%

4.2%

23% 22% 25%

36%

60%

32%

Aug-14 Aug-12

SERIES: Distressed Sales, Not Seasonally Adjusted SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

SANTA CLARA COUNTY

Preforeclosure: 486 • Auction: 465 • Bank Owned: 71

SOURCE: PropertyRadar.com as of 10/14/14

SANTA CLARA COUNTY

Preforeclosure: 486 • Auction: 465 • Bank Owned: 71

SOURCE: PropertyRadar.com as of 10/14/14

SANTA CLARA COUNTY

Preforeclosure: 486 • Auction: 465 • Bank Owned: 71

SOURCE: PropertyRadar.com as of 10/14/14

SAN JOSE

Preforeclosure: 326 • Auction: 321 • Bank Owned: 51

SOURCE: PropertyRadar.com as of 10/14/14

CITY OF SANTA CLARA

Preforeclosure: 19 • Auction: 24 • Bank Owned: 0

SOURCE: PropertyRadar.com as of 10/14/14

PALO ALTO

Preforeclosure: 1 • Auction: 2 • Bank Owned: 0

SOURCE: PropertyRadar.com as of 10/14/14

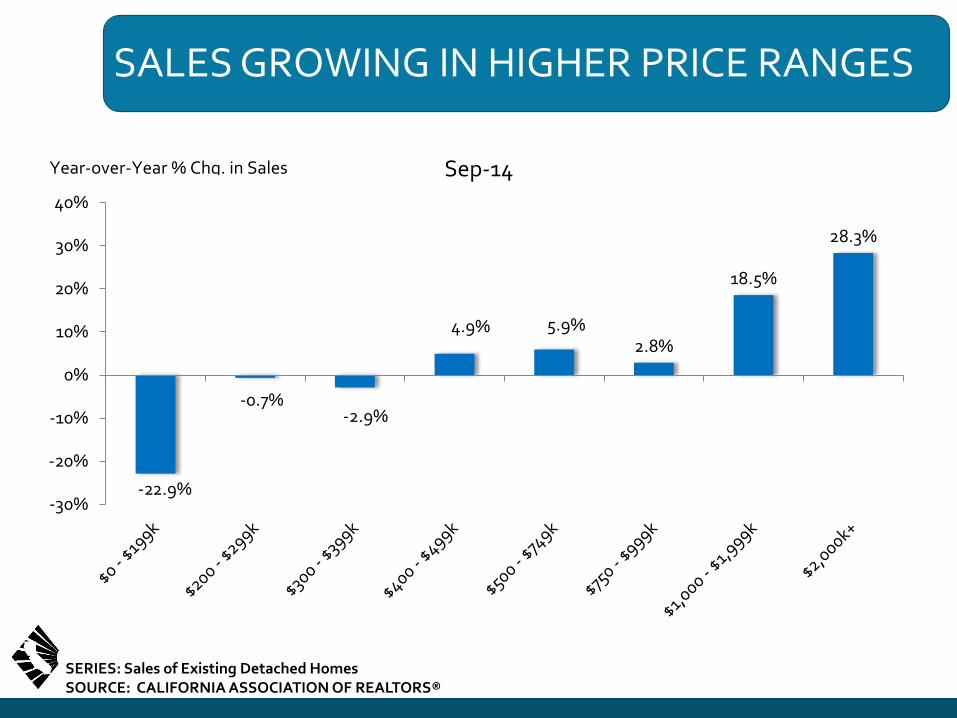

SALES GROWING IN HIGHER PRICE RANGES

SERIES: Sales of Existing Detached Homes SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

-22.9%

-0.7% -2.9%

4.9% 5.9% 2.8%

18.5%

28.3%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Sep-14 Year-over-Year % Chg. in Sales

CHANGE IN SALES BY PRICE RANGE

(Year-to-Year)

-22.9%

9.0%

-0.7%

-2.9%

4.9%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

$0 - $200k $500k+ $200 - $300k $300 - $400k $400 - $500k

SERIES: Sales of Existing Detached Homes SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

PRICE PLATEAU AHEAD; ANNUAL GAINS SLOWING

California, Sep. 2014: $460,940, Up 7.6% YTY

SERIES: Median Price of Existing Single Family Homes SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

Sep-14: $460,940

Sep-13: $428,290

$-

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

P: May-07 $594,530

T: Feb-09 $245,230 -59% from peak

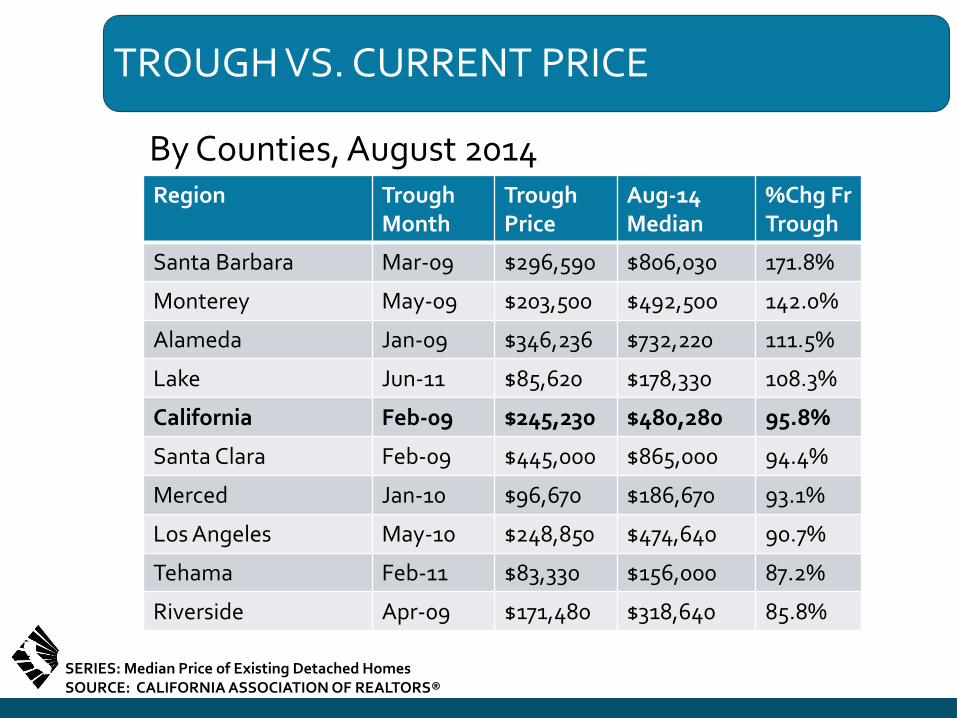

TROUGH VS. CURRENT PRICE

By Counties, August 2014

SERIES: Median Price of Existing Detached Homes SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

Region Trough Month

Trough Price

Aug-14 Median

%Chg Fr Trough

Santa Barbara Mar-09 $296,590 $806,030 171.8%

Monterey May-09 $203,500 $492,500 142.0%

Alameda Jan-09 $346,236 $732,220 111.5%

Lake Jun-11 $85,620 $178,330 108.3%

California Feb-09 $245,230 $480,280 95.8%

Santa Clara Feb-09 $445,000 $865,000 94.4%

Merced Jan-10 $96,670 $186,670 93.1%

Los Angeles May-10 $248,850 $474,640 90.7%

Tehama Feb-11 $83,330 $156,000 87.2%

Riverside Apr-09 $171,480 $318,640 85.8%

$-

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000 California US

CALIFORNIA VS. U.S. MEDIAN PRICES

1970-2014

SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

SERIES: Median Price of Existing Single Family Homes SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

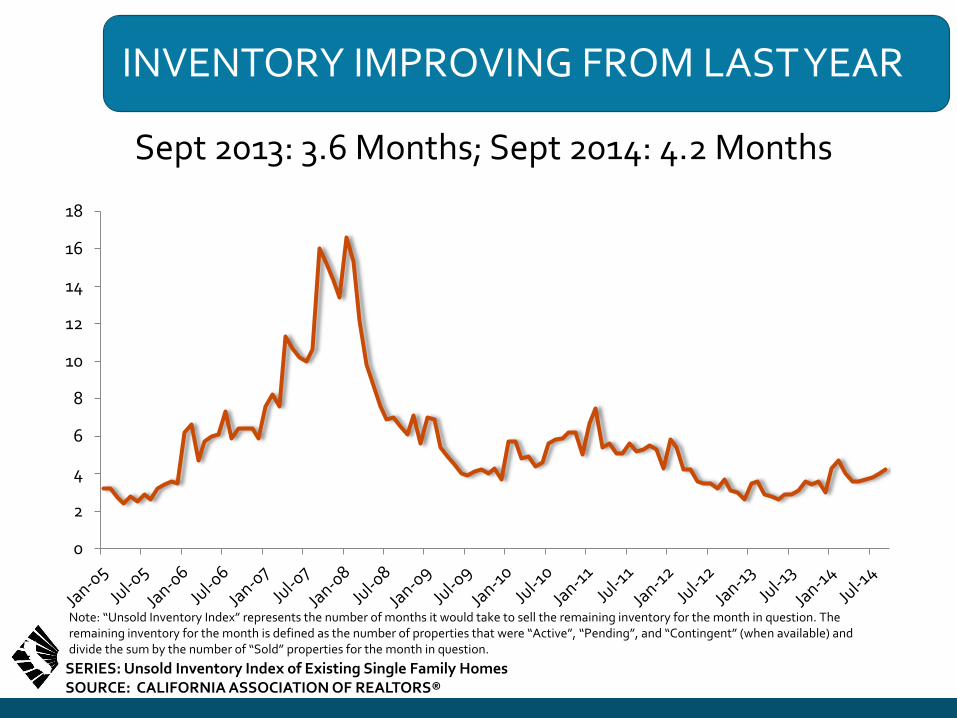

INVENTORY IMPROVING FROM LAST YEAR

Sept 2013: 3.6 Months; Sept 2014: 4.2 Months

Note: “Unsold Inventory Index” represents the number of months it would take to sell the remaining inventory for the month in question. The remaining inventory for the month is defined as the number of properties that were “Active”, “Pending”, and “Contingent” (when available) and divide the sum by the number of “Sold” properties for the month in question.

0

2

4

6

8

10

12

14

16

18

SERIES: Unsold Inventory Index of Existing Single Family Homes SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

INVENTORY HIGHER AT UPPER PRICE RANGES

Note: “Unsold Inventory Index” represents the number of months it would take to sell the remaining inventory for the month in question. The remaining inventory for the month is defined as the number of properties that were “Active”, “Pending”, and “Contingent” (when available) and divide the sum by the number of “Sold” properties for the month in question.

SERIES: Unsold Inventory Index of Existing Single Family Homes SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

Price Range (Thousand) Sep-14 Aug-14 Sep-13

$1,000K+ 5.5 5.0 5.9

$750-999K 4.3 3.9 3.7

$500-749K 3.9 3.8 3.5

$400-499K 3.9 3.8 3.3

$300-399K 4.1 4.0 3.3

$200-299K 4.0 4.0 3.2

$0-199K 3.9 3.8 3.2

WHY WAS/IS INVENTORY SO LOW?

• Demand Side – Housing affordability was at historic highs – Low rates hurt investment alternatives – International buyers

• Supply Side – Little new construction for last 5 years – Underwater homeowners are stuck – Mortgage Lock-In Effect – No inventory to move up – Foreclosure pipeline drying up – Investors are renting instead of flipping – Off-market (aka “pocket’) listings

BUYING TO RENT V. FLIP; CHANGE IN PREFERRED INVESTMENT STRATEGY

Investment to Flip

Rental Property

SERIES: 2014 Housing Market Survey SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

HOUSING AFFORDABILITY

REAL ENEMY OF THE FUTURE OF CALIFORNIA?

• Housing Affordability

• The Achilles Heel of the California Economy

• What happens when housing costs are too high?

• Impact on jobs and economic growth

• Impact on neighborhoods and family stability

HOUSING AFFORDABILITY DOWN SHARPLY SINCE Q1 2012

% OF HOUSEHOLDS THAT CAN BUY A MEDIAN-PRICED HOME

SERIES: Housing Affordability Index of Traditional Buyers SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

0%

10%

20%

30%

40%

50%

60%

70%

80% CA US

California vs. U.S. – 1984-2014

Annual Quarterly

SOME GOOD NEWS:MEDIAN CA HOUSE PAYMENT WELL BELOW PEAK PEAK

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

Jan-80 Jan-83 Jan-86 Jan-89 Jan-92 Jan-95 Jan-98 Jan-01 Jan-04 2009 Q1

SERIES: Housing Affordability Index SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

PITI/Month

Peak: $3,668/mo (2007 Q2)

Latest: $2,340/mo (2014 Q2)

… MINIMUM QUALIFYING INCOME ALSO WELL BELOW PEAK

$-

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

Jan-80 Jan-82 Jan-84 Jan-86 Jan-88 Jan-90 Jan-92 Jan-94 Jan-96

Jan-98 Jan-00 Jan-02 Jan-04 2006 Q1

2012 Q1

Min. Income Peak: $146,701/yr (2007 Q2)

Latest: $93,593/yr (2014 Q2)

SERIES: Housing Affordability Index SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

HOUSE PAYMENT (INFLATION ADJUSTED) IS AT LATE 1970’S LEVEL

SERIES: Housing Affordability Index SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

PITI/Month (ADJUSTED FOR INFLATION)

Peak: $928/mo (2006)

Latest: $458/mo (2013)

$-

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008 2011

MINIMUM QUALIFYING INCOME IS THE SAME AS 35 YEARS AGO

SERIES: Housing Affordability Index SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

Min. Income (Adjusted for Inflation) Peak: $37,122 (2006)

Latest: $18,337 (2013)

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008 2011

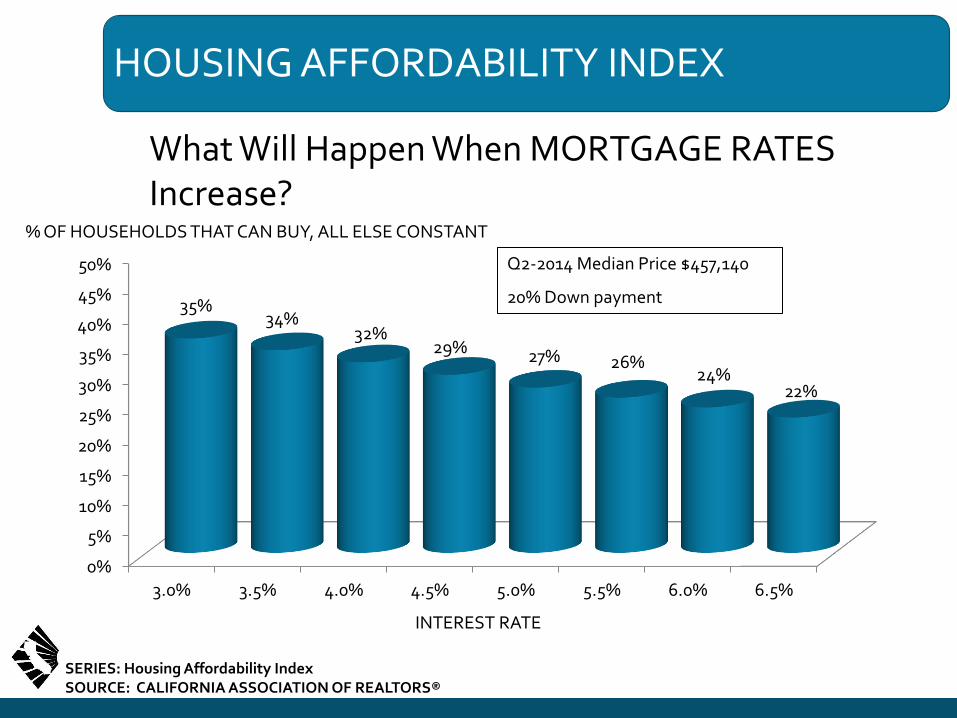

HOUSING AFFORDABILITY INDEX

What Will Happen When MORTGAGE RATES Increase?

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

3.0% 3.5% 4.0% 4.5% 5.0% 5.5% 6.0% 6.5%

35% 34%

32% 29% 27% 26%

24% 22%

Q2-2014 Median Price $457,140

20% Down payment

INTEREST RATE

% OF HOUSEHOLDS THAT CAN BUY, ALL ELSE CONSTANT

SERIES: Housing Affordability Index SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

MEDIAN MONTHLY MORTGAGE PAYMENT

What Will Happen When Mortgage Rates Increase?

$0

$400

$800

$1,200

$1,600

$2,000

$2,400

3.0% 3.5% 4.0% 4.5% 5.0% 5.5% 6.0% 6.5%

$1,542 $1,642

$1,746 $1,853 $1,963

$2,076 $2,193

$2,312

INTEREST RATE

MONTHLY MORTGAGE

SERIES: Housing Affordability Index SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

Q2-2014 Median Price $457,140

20% Down payment

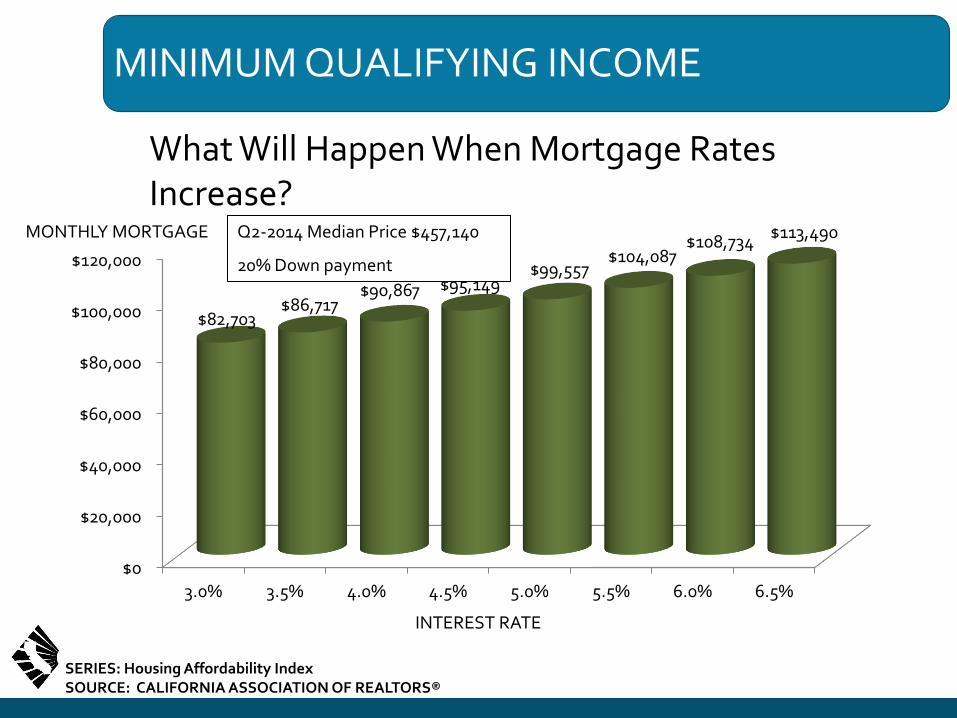

MINIMUM QUALIFYING INCOME

What Will Happen When Mortgage Rates Increase?

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

3.0% 3.5% 4.0% 4.5% 5.0% 5.5% 6.0% 6.5%

$82,703 $86,717

$90,867 $95,149 $99,557

$104,087 $108,734

$113,490

INTEREST RATE

MONTHLY MORTGAGE

SERIES: Housing Affordability Index SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

Q2-2014 Median Price $457,140

20% Down payment

INCOME REQUIRED TO BUY A MEDIAN-PRICED HOME IN CA: (PEAK VS. CURRENT)

$56,324

$93,593

$0

$20,000

$40,000

$60,000

$80,000

$100,000

2012 Q1 2014 Q2

• Change in minimum required income: $37,269

• Increase in income attributed to interest rate increase: $836 (2.2% of total change)

• Increase in income attributed to price increase : $36,433 (97.8% of total change)

SERIES: Housing Affordability Index SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

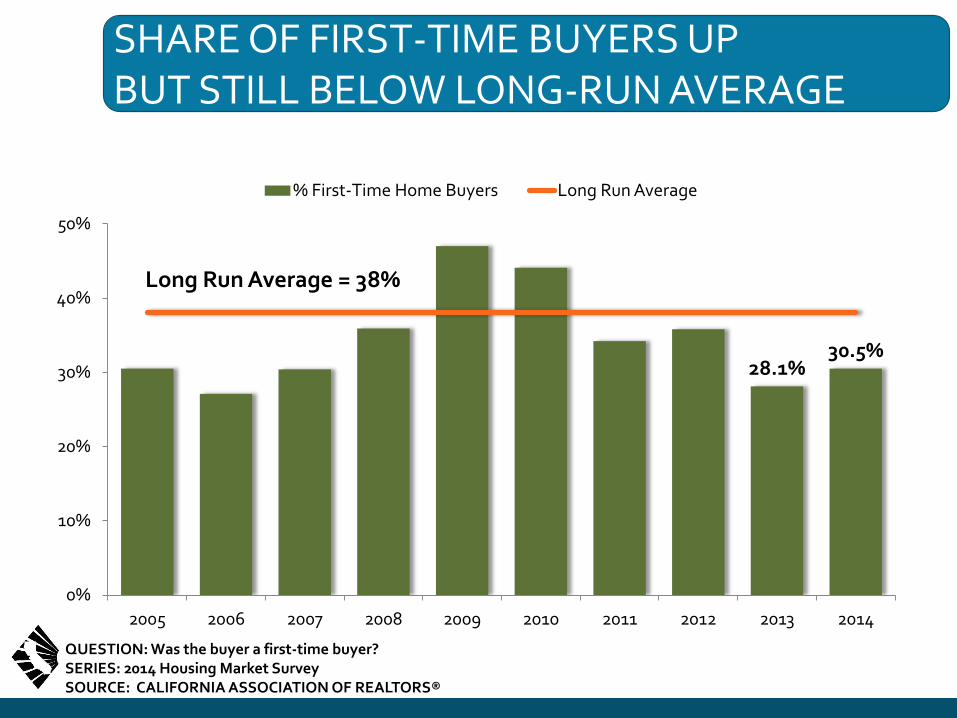

SHARE OF FIRST-TIME BUYERS UP BUT STILL BELOW LONG-RUN AVERAGE

28.1% 30.5%

0%

10%

20%

30%

40%

50%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

% First-Time Home Buyers Long Run Average

Long Run Average = 38%

QUESTION: Was the buyer a first-time buyer? SERIES: 2014 Housing Market Survey SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

WHY DO WE CARE ABOUT LOW LEVEL OF FIRST-TIME BUYER?

• It signals a constrained flow of new households in the housing market

• Trade-up market cannot be replenished in the long run

• First-time buyers represent the main impulse that drives the state’s homeownership rate

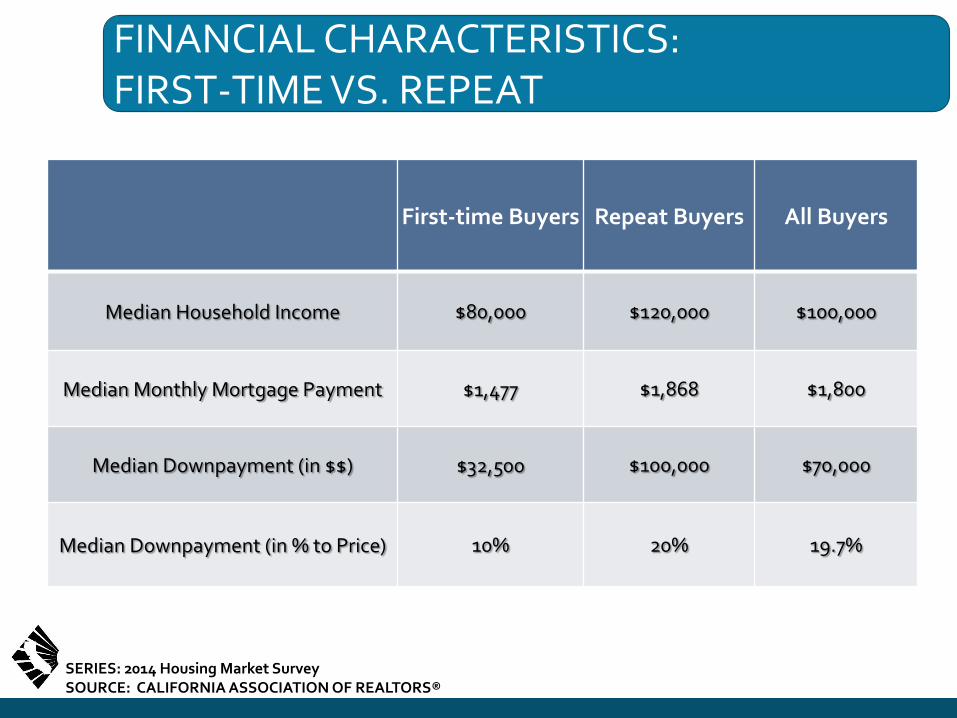

FINANCIAL CHARACTERISTICS: FIRST-TIME VS. REPEAT

SERIES: 2014 Housing Market Survey SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

First-time Buyers Repeat Buyers All Buyers

Median Household Income $80,000 $120,000 $100,000

Median Monthly Mortgage Payment $1,477 $1,868 $1,800

Median Downpayment (in $$) $32,500 $100,000 $70,000

Median Downpayment (in % to Price) 10% 20% 19.7%

REASONS FOR RENTING INSTEAD OF BUYING

SERIES: 2013 Renter Survey SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

44%

9%

6%

6%

6%

5%

5%

3%

2%

Can't afford to buy

Poor credit / Can't qualify

Renting is easier

Young/Starting out/Not ready

Flexibility/Freedom if renting

Cost/Upkeep/Responsibility

Plan to / Saving for down

Never considered it/No interest

Disabled/On disability

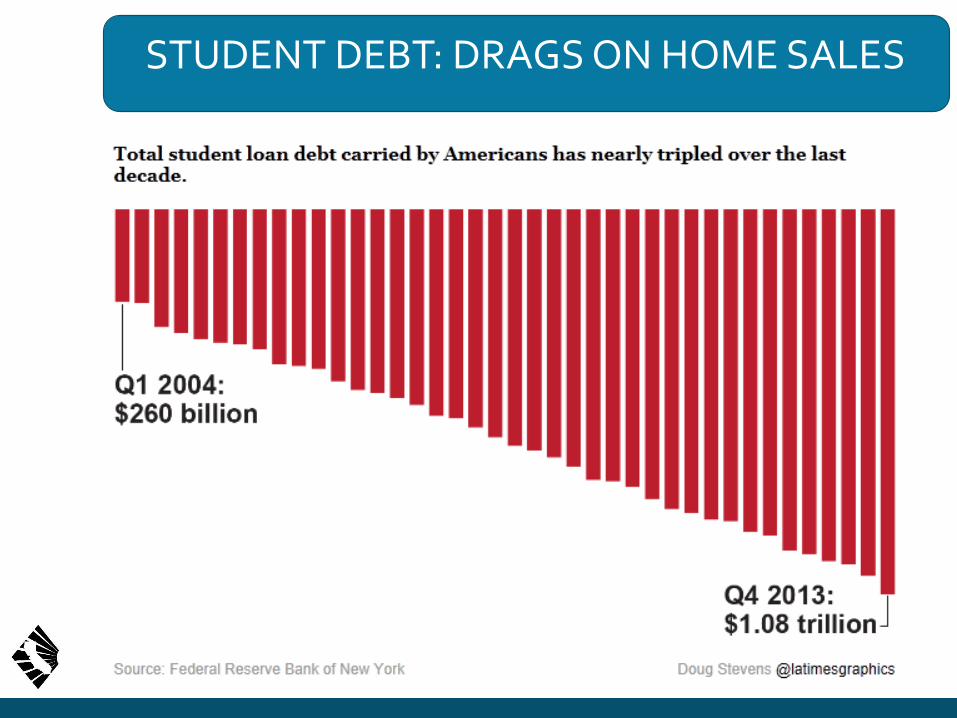

STUDENT LOAN DEBT AN ISSUE FOR 25% OF RENTERS

SERIES: 2013 Renter Survey SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

Yes, 23%

No, 75%

Refused, 2%

Student Loan Debt

78%

8%

6%

3%

2%

2%

<$10,000

$10-$20K

$20-$50K

$50-$100K

> $100K

Refused

Amount of Debt

STUDENT DEBT: DRAGS ON HOME SALES

HOMEOWNERSHIP RATE LOWER IN CA

California Vs. U.S.

40%

45%

50%

55%

60%

65%

70%

75% CA US

SERIES: Homeownership Rates SOURCE: U.S. Census Bureau

HOMEOWNERSHIP RATE BY AGE OF HOUSEHOLDER

SOURCE: Census Bureau

MILLENNIAL HOMEOWNERSHIP FALLING

SOURCE: Census Bureau

CALIFORNIA’S HOUSING DELEMMA

• Even with everything (or at least most things) going right, our homeownership market is in trouble…

• The rental market, even with the conversion of 500,000 SFH’s, is still exhibiting inadequate supply

HOW TO MAKE IT MORE AFFORDABLE? ONE WORD: SUPPLY

• CA Housing Needs = Minimally 165,000 Units Annually

– Regulatory Problem

– Impact Fees

– Public Attitudes

CA PERMITS UP BUT MORE UNITS NEEDED

2013: 57,496 Units, Up 43.0% from 2012

SERIES: New Housing Permits SOURCE: Construction Industry Research Board

0

50000

100000

150000

200000

250000

300000

350000 Single Family Multi-Family

Household Growth: 220,000-250,000/yr

REGIONAL HOUSING MARKETS

SANTA CLARA COUNTY

SALES OF RESIDENTIAL HOMES

Santa Clara County, September 2014: 844 Units

Down 9.8% MTM, Down 11.9% YTY

SOURCE: Clarus Market Metrics

MEDIAN PRICE OF RESIDENTIAL HOMES

Santa Clara County, September 2014: $852,500

Down 0.9% MTM, Up 10.0% YT

SOURCE: Clarus Market Metrics

FOR SALE PROPERTIES

Santa Clara County, September 2014: 2,598 Units

Down 4.0% MTM, Down 10.8% YTY

Note: “For Sale Properties” represents the overall supply that exist throughout the entire month, including any listings that appear as “Active” any point in time during the month.

SOURCE: Clarus Market Metrics

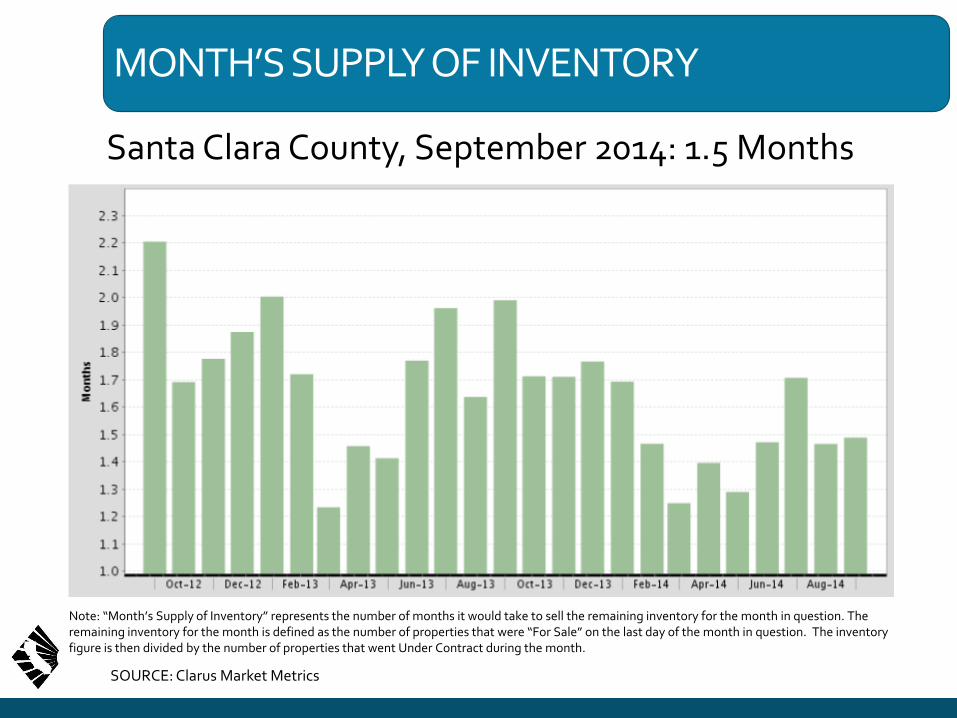

MONTH’S SUPPLY OF INVENTORY

Santa Clara County, September 2014: 1.5 Months

Note: “Month’s Supply of Inventory” represents the number of months it would take to sell the remaining inventory for the month in question. The remaining inventory for the month is defined as the number of properties that were “For Sale” on the last day of the month in question. The inventory figure is then divided by the number of properties that went Under Contract during the month.

SOURCE: Clarus Market Metrics

CITY OF SANTA CLARA

SALES OF RESIDENTIAL HOMES

City of Santa Clara, September 2014: 57 Units

Up 21.3% MTM, Up 16.3% YTY

SOURCE: Clarus Market Metrics

MEDIAN PRICE OF RESIDENTIAL HOMES

City of Santa Clara, September 2014: $840,000

Down 4.1% MTM, Up 14.9% YTY

SOURCE: Clarus Market Metrics

FOR SALE PROPERTIES

City of Santa Clara, September 2014: 77 Units

Down 30.6% MTM, Down 35.8% YTY

Note: “For Sale Properties” represents the overall supply that exist throughout the entire month, including any listings that appear as “Active” any point in time during the month.

SOURCE: Clarus Market Metrics

MONTH’S SUPPLY OF INVENTORY

City of Santa Clara, September 2014: 0.9 Months

Note: “Month’s Supply of Inventory” represents the number of months it would take to sell the remaining inventory for the month in question. The remaining inventory for the month is defined as the number of properties that were “For Sale” on the last day of the month in question. The inventory figure is then divided by the number of properties that went Under Contract during the month.

SOURCE: Clarus Market Metrics

SAN JOSE

SALES OF RESIDENTIAL HOMES

San Jose, September 2014: 444 Units

Down 15.7% MTM, Down 18.4% YTY

SOURCE: Clarus Market Metrics

MEDIAN PRICE OF RESIDENTIAL HOMES

San Jose, September 2014: $746,994

Down 3.6% MTM, Up 7.5% YTY

SOURCE: Clarus Market Metrics

FOR SALE PROPERTIES

San Jose, September 2014: 1,396 Units

Down 5.7% MTM, Down 12.2% YTY

Note: “For Sale Properties” represents the overall supply that exist throughout the entire month, including any listings that appear as “Active” any point in time during the month.

SOURCE: Clarus Market Metrics

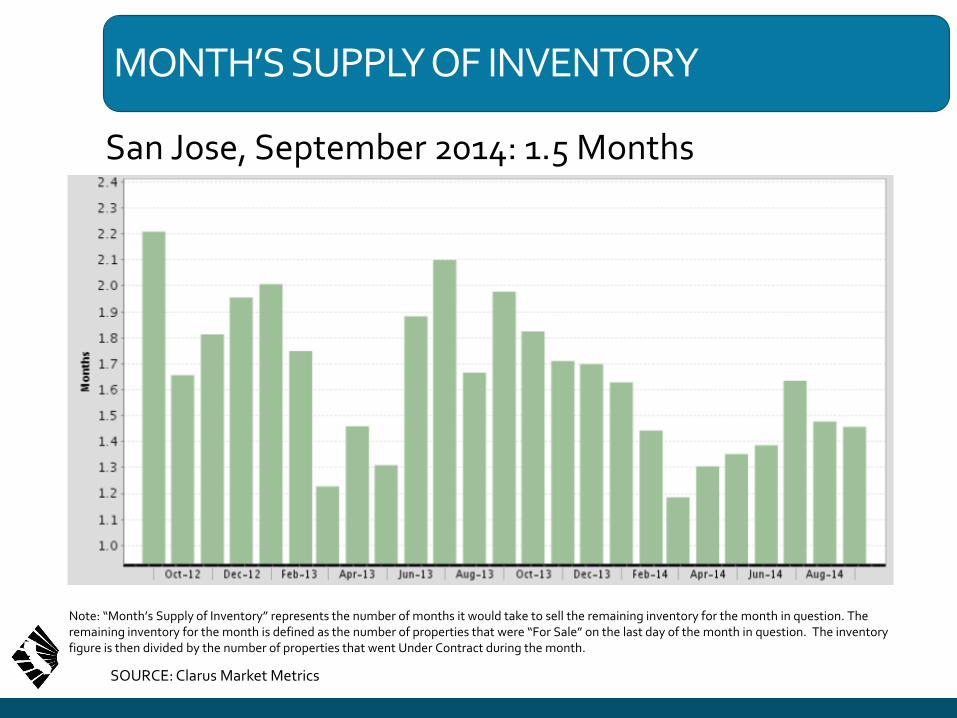

MONTH’S SUPPLY OF INVENTORY

San Jose, September 2014: 1.5 Months

Note: “Month’s Supply of Inventory” represents the number of months it would take to sell the remaining inventory for the month in question. The remaining inventory for the month is defined as the number of properties that were “For Sale” on the last day of the month in question. The inventory figure is then divided by the number of properties that went Under Contract during the month.

SOURCE: Clarus Market Metrics

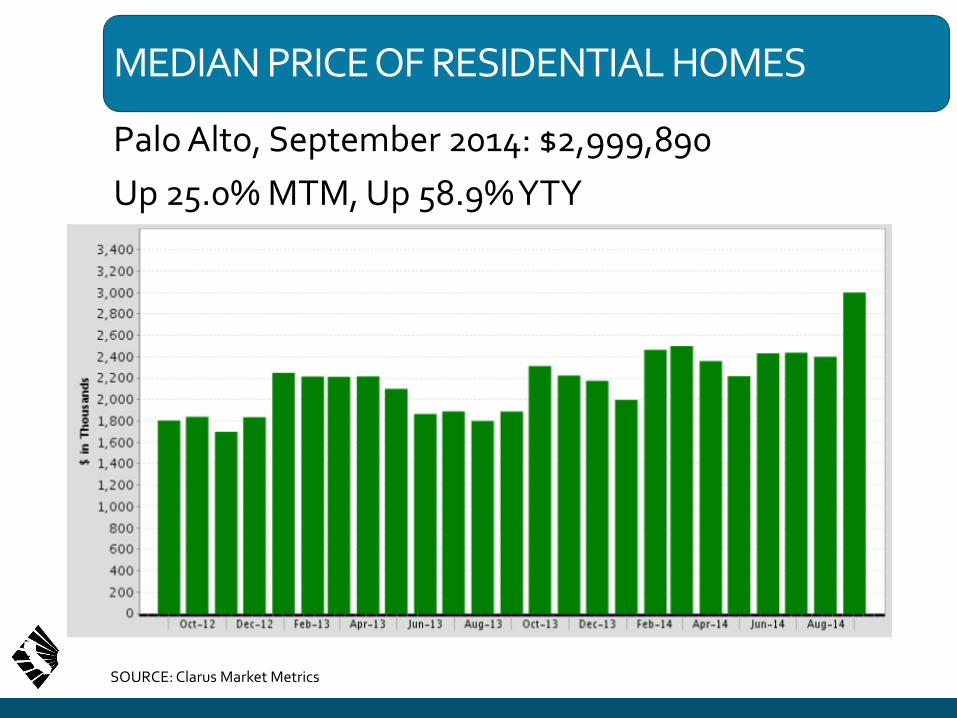

PALO ALTO

SALES OF RESIDENTIAL HOMES

Palo Alto, September 2014: 27 Units

Down 18.2% MTM, Down 6.9% YTY

SOURCE: Clarus Market Metrics

MEDIAN PRICE OF RESIDENTIAL HOMES

Palo Alto, September 2014: $2,999,890

Up 25.0% MTM, Up 58.9% YTY

SOURCE: Clarus Market Metrics

FOR SALE PROPERTIES

Palo Alto, September 2014: 83 Units

Up 15.3% MTM, Up 3.8% YTY

Note: “For Sale Properties” represents the overall supply that exist throughout the entire month, including any listings that appear as “Active” any point in time during the month.

SOURCE: Clarus Market Metrics

MONTH’S SUPPLY OF INVENTORY

Palo Alto, September 2014: 1.1 Months

Note: “Month’s Supply of Inventory” represents the number of months it would take to sell the remaining inventory for the month in question. The remaining inventory for the month is defined as the number of properties that were “For Sale” on the last day of the month in question. The inventory figure is then divided by the number of properties that went Under Contract during the month.

SOURCE: Clarus Market Metrics

2015 FORECAST

CALIFORNIA HOUSING MARKET FORECAST

SERIES: CA Housing Market Outlook SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

SFH Resales (000s)

% Change

Median Price ($000s)

% Change

Housing Affordability Index

30-Yr FRM

2011

422.6

1.4%

$286.0

-6.2%

53%

4.5%

2012

439.8

4.1%

$319.3

11.6%

51%

3.7%

2013

413.3

-5.8%

$407.2

27.5%

36%

4.0%

2014 P

380.5

-8.2%

$455.0

11.8%

30%

4.3%

2015 F

402.5

5.8%

$478.7

5.2%

27%

4.5%

CALIFORNIA HOUSING MARKET OUTLOOK

Sales Down for 2014 but will Improve in 2015; Price Gains Slowing

Units (Thousand)

380 403

0

100

200

300

400

500

600

700

2005 2007 2009 2011 2013 2015f

Sales of Existing Detached Homes

$455

$479

$0

$100

$200

$300

$400

$500

$600

2005 2007 2009 2011 2013 2015f

Median Price Price

(Thousand)

SERIES: CA Housing Market Outlook SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

CA: DOLLAR VOLUME UP FOR 4TH YEAR

$301

$244

$164

$133 $131 $127 $121 $140

$169 $173 $193

-40%

-30%

-20%

-10%

0%

10%

20%

30%

$0

$50

$100

$150

$200

$250

$300

$350

$400

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014p 2015f

$ Volume of Sales Percent Change

% Change $ in Billion

-60%

SERIES: CA Housing Market Outlook SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

Up 2.7% in 2014, Up 11.3% in 2015

REAL ESTATE IS CONSIDERED THE BEST LONG TERM INVESTMENT

SOURCE: Gallup

“Make no mistake about it, the way that working-class people build wealth is through

homeownership, not the stock market, not their 401(k) and not a pension.”

John Taylor, President of the National Community Reinvestment Coalition,

ATTITUDE TOWARD THE HOME BUYING PROCESS – MIXED RESULTS

SOURCE: How would you describe your attitude towards the home buying process?

C.A.R. 2014 Millennial Survey

0%

10%

20%

30%

40%

50%

60%

Positive Negative Neutral N/A Other

50%

34%

8% 4%

4%

MOST MILLENNIALS UNCERTAIN/DOUBTFUL THAT THEY COULD OBTAIN A MORTGAGE NOW?AMILLENNIAL ETHNICITY

SOURCE: C.A.R. 2014 Millennial Survey Q: Could you obtain a mortgage if you applied now ?

Yes 22%

No 33%

Don't know 45%

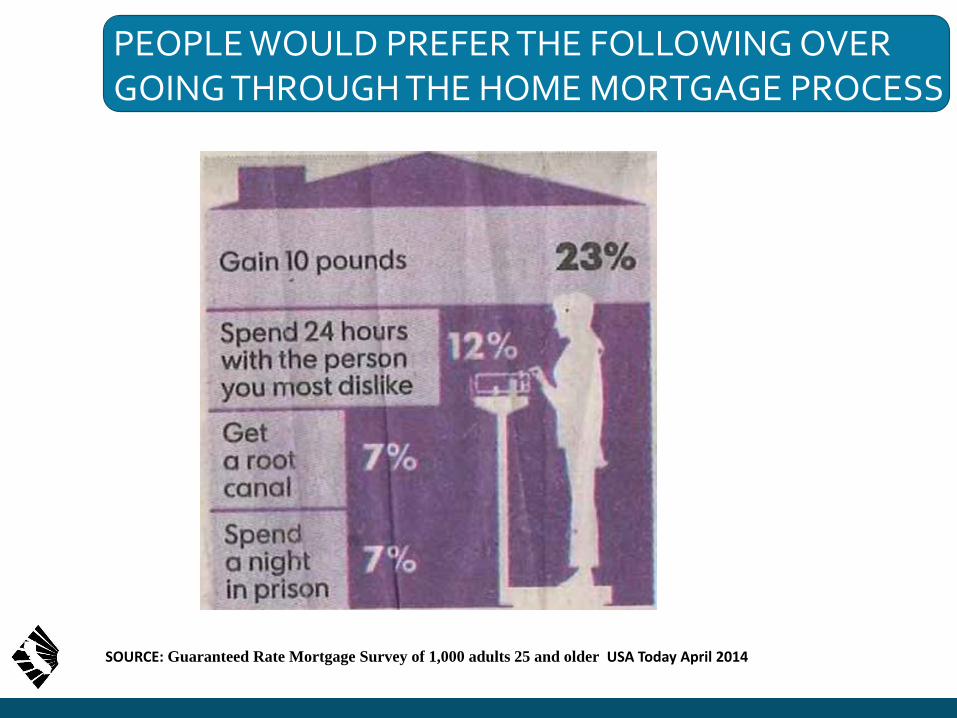

PEOPLE WOULD PREFER THE FOLLOWING OVER GOING THROUGH THE HOME MORTGAGE PROCESS AGAIN:

SOURCE: Guaranteed Rate Mortgage Survey of 1,000 adults 25 and older USA Today April 2014

C.A.R. Strategic Planning Books