Embed Size (px)

Citation preview

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 1

Shared Services are new again –how can we get it right?Presented by Julie Sullivan

February 2016

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 2

Definitions

Shared Services

1. a collection of activities that cross various functional or process boundaries which can individually and collectively be pooled and provided to internal operating groups by a common service organization.

2. a service enterprise that creates and sells common, measurable, and scalable services to business entities within the same corporate structure for a fee or similar commercial model.

3. a passion to transform end-to-end business process through scale, automation, standardization, aggressive performance management, customer orientation and wage arbitrage via a global network of captive or outsourced service center

Global Business Services

The evolution of Shared Services

1. An integrated platform to deliver enterprise business services

2. Drives efficiency and business outcomes

3. Evolves with the market and company needs

Key Capabilities Multi-functional business processes Multi-channel service delivery – outsourced, shared

services and centers of excellence Process Ownership and Management Common information technology Enterprise-wide Governance

Business servicesa general term that describes work that supports a business but does not produce a tangible commodity. Information technology (IT) is an important business service that supports many other business services such as

procurement, shipping and finance, human resources, payroll etc.

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 3

Defining the Range of Operating Models

DecentralizedProcesses

CentralizedProcesses Business Services Global Business

Services (GBS)Multifunctional

GBS

Processes within functions performed by BUs on their own behalf

Process and outcomes consolidated and owned by centralized functions; BU’s are customers

Business Services model with global scope and delivery

GBS model extended across multiple functions with end-to-end global process ownership and accountability

Processes consolidated to a regional service entity and operated as a business with governance shared with BU’s

Business ServicesEntity

P1 P2 P3 P4

Business ServicesEntity

P1 P2 P3 P4

Process 1, 2, etc..P1Keys:

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 4

Why the renewed interest in Shared Services?

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 5

Issues driving business transformationUnderstand how to better engage with customers.

Brand

Loyalty

Customer Acquisition

Product/Svc Strategy

Customer Engagement

How to make global operations decisions? The most effective operating model?

Operating Strategy Global Business Svcs.

Shared Services

Global Operations

How to define growth strategies?

M&A

New markets

New products

New businesses

Growth

How to focus on the right data to convert to knowledge?

Big Data

Analytics

Knowledge to Insight

Data Overload

How to retain, empower and manage this critical corporate asset?

Learning & Development

Acquisition & Retention

Talent Development

Talent & Human Capital

Focus on opportunities in new technology while leveraging legacy investments.

Digital Mobile Social

Robotic Automation

Internet of Things Cloud

Technology Disruption

How to manage uncertainty around legislative change? Where to focus?

Government Regulation

Tax Issues

Legislative Where are the opportunities to reduce cost without impairment to the business?

Balance Growth goals with cost reduction

Cost Reduction

Where are opportunities aligned to your business?

How to manage risk/return

BRIC

MEA

Emerging Markets

All of these issues are driving choices in how business services are being delivered

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 6

The Foundation of Shared ServicesShared Services Evolved 20 Years Ago As Dramatically Different Model for Back-Office Services

Centralization

» Economies of Scale

» Economies of Scope

» Focus for Improvement

Shared Services» Economies of Scale, Scope & Place » Joint Governance» Customer Relationship Management» Service Levels Aligned with Price» Process Standardization and Best Practice

Deployment» “Run it Like a Business”

Decentralization» Responsiveness

» Service

» Ownership

Shared Services

DecentralizedServices

CentralizedServices

Support Services Pendulum

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 7

Demand Dashboard

Source: KPMG Global Pulse Survey 4Q15

Service Providers: Pipeline Growth Last Quarter

31%

2Q15

76%

2Q13

65%

3Q13

72%

4Q13

65%

1Q14

67%

2Q14

60%

1Q15

69%

3Q14

33%

4Q15

Advisors: Demand increase by Service Delivery ModelNext 1–2 Quarters

Service Providers: Demand Next 1–2 QuartersAdvisors: Top Functional Focus Areas for Service Delivery Improvement Efforts

Note: Numbers may not total 100% due to rounding.

SharedServices

51%

ITO

37%

BPO

40%

Internal ProcessImprovement

46%

7%7%

16%18%

23%30%

45%62%64%

Vertical industry…REFM

All areas, including ITCustomer care

Supply chainHR

Procurement/source to…F&A

IT

Flat

50%

Up

50%

Down

0%

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 8

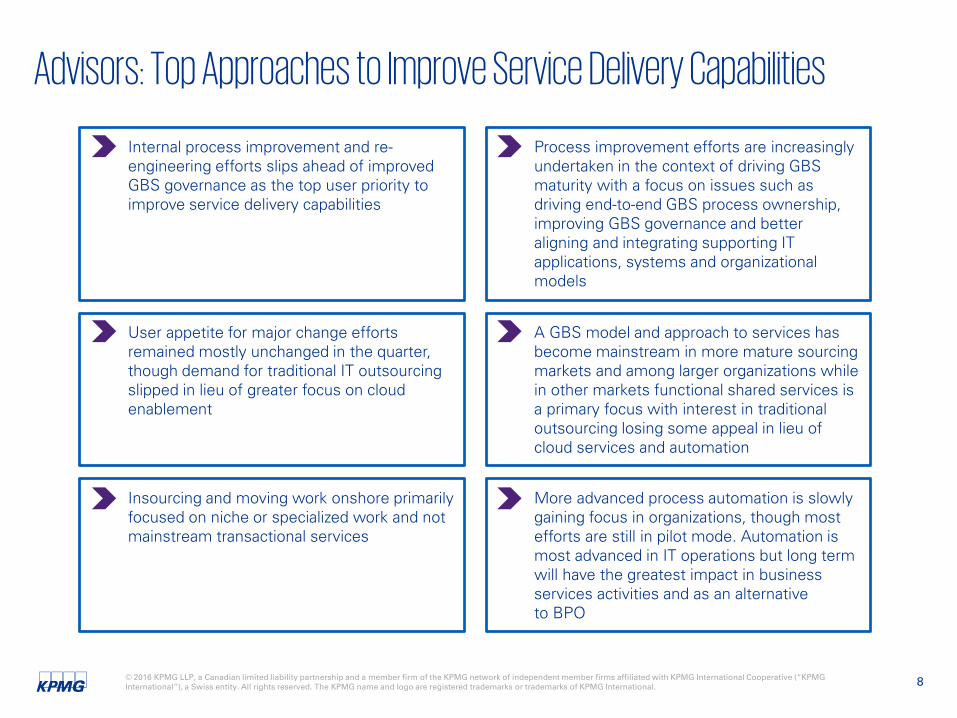

Advisors: Top Approaches to Improve Service Delivery Capabilities

Internal process improvement and re-engineering efforts slips ahead of improved GBS governance as the top user priority to improve service delivery capabilities

Process improvement efforts are increasingly undertaken in the context of driving GBS maturity with a focus on issues such as driving end-to-end GBS process ownership, improving GBS governance and better aligning and integrating supporting IT applications, systems and organizational models

User appetite for major change efforts remained mostly unchanged in the quarter, though demand for traditional IT outsourcing slipped in lieu of greater focus on cloud enablement

A GBS model and approach to services has become mainstream in more mature sourcing markets and among larger organizations while in other markets functional shared services is a primary focus with interest in traditional outsourcing losing some appeal in lieu of cloud services and automation

Insourcing and moving work onshore primarily focused on niche or specialized work and not mainstream transactional services

More advanced process automation is slowly gaining focus in organizations, though most efforts are still in pilot mode. Automation is most advanced in IT operations but long term will have the greatest impact in business services activities and as an alternative to BPO

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 9

Advisors: Top Approaches to Improve Service Delivery Capabilities

0%

1%

2%

11%

23%

29%

33%

37%

42%

48%

50%

51%

Nothing/major improvements not required

Nothing/lack of ambition/execute support/funding

Bringing work performed offshore back onshore

Insourcing work previously outsourced

Investments into/improvements to enterprisesoftware systems

Use/expansion of offshore captive SSCs

Investments into cloud computing services

Use/expansion of BPO

Use/expansion of ITO

Use/expansion of SSCs

Improve current SSC/outsourcing governance

Internal process improvement/re-engineering efforts

4Q15 3Q14 4Q13

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 10

The Evolution of Shared Services: Business Services Maturity Model

To best drive value from our business services, we must understand where we are today.

Level 01

Fragmented Decentralized service

delivery model Duplicative functions,

processes, and technology

Little central control and governance over business support services

Supply driven delivery model

Level 02

Sub-scaled Consolidated delivery

model Leverage economies of

scale for highly transactional services

Shared services or outsourcing typically on a single-function, regional basis

Supply driven delivery model

Level 03

Scaled Multi-functional service

delivery model that operates in siloes

Variation around the inclusion and level of processes, technology, and governance standardization

Transition to demand driven delivery model

Level 04

Integrated Enterprise wide multi-

functional transactional and specialist business service model

Coordinated processes, technology, governance, and multi-channel delivery for scale and adaptability

Demand driven delivery model

Level 05

Strategic Multi-functional, multi-

channel business service delivery synced end to end

Provides transactional, expert, and analytic services

Managed through integrated, outcome-oriented governance

Demand driven delivery model

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 11

Business Services have entered a new phase of disruption

Client organizations are advancing their operating models and increasing expectations for their Business Services organizations to deliver better business outcomes

Disruptive technologies such as robotic process automation (RPA), natural language processing and cognitive computing are creating new value streams

Business Services must embrace the As-a-Service model and innovate to redefine role in ecosystem or manage diminishing demand for low-cost staff augmentation

1

2

3

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 12

How is excellence achieved?

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 13

GBS excellence Is achieved in multiple ways

Enterprise-wide

Multi-functional

Integratedgovernance

End-to-endprocess ownership

Enterprise wide processefficiencies

Standardized processesRationalized service delivery

Cohesive, insightfulanalytics

Value and cost focusedStrategic location(s) rationalized

Adaptable to business needs and strategy

Leverages a global talentstrategy

IT architectural strategy

Enable service through unified technology/cloud

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 14

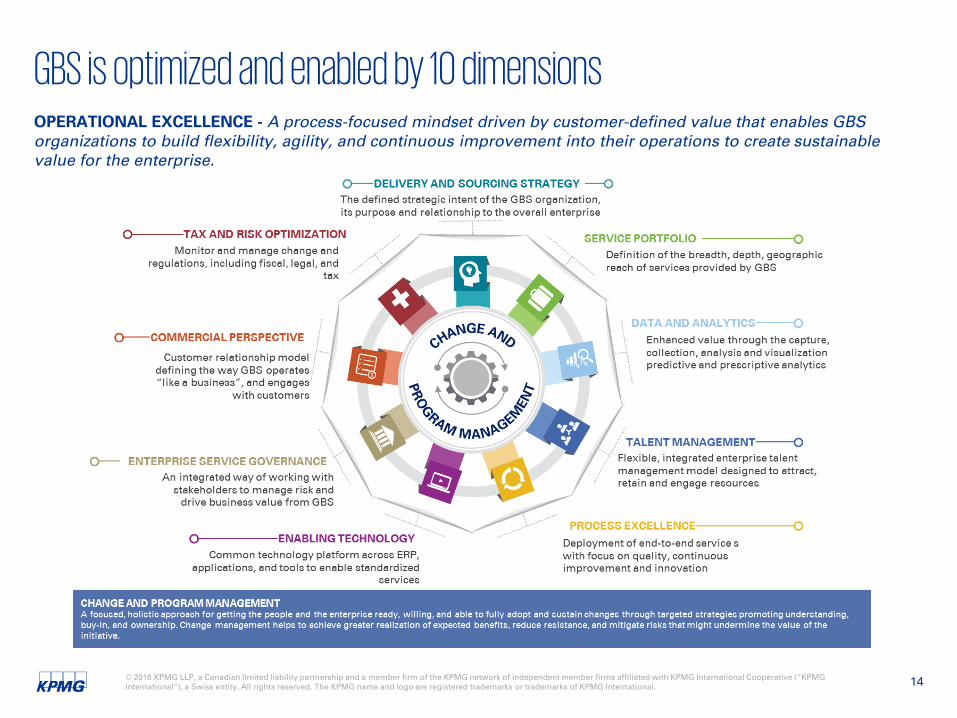

GBS is optimized and enabled by 10 dimensionsOPERATIONAL EXCELLENCE - A process-focused mindset driven by customer-defined value that enables GBS organizations to build flexibility, agility, and continuous improvement into their operations to create sustainable value for the enterprise.

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 15

Enterprise service governance is critical to sustain value

Governance takes on an Enterprise role across delivery channels

Integration is the new challenge, to drive business value

Risk mitigation and monitoring remain a core tenant of governance

Expansion of the traditional governance framework is needed

Adaptability to govern new delivery technologies critical

Outcomes and value delivery will be a focus for the business

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 16

Unleashing the Power of GBS

■ Increase sophistication and centralize DA (remove duplicate systems, add tracking where needed, one ERP system, process requests faster, ability to track process breakdown utilizing analytics, identify missing process controls)

■ Common platforms and common processes and capabilities

■ End to end process standardization for non standardized products/services and business units

■ Process owners identification and accountability

■ Process controls and continuous process improvement

■ Process automation

■ Proactive vs reactive response to regulatory demands

■ Global repository of regulatory requirements (tracking, reporting, and process driven common response to regulatory mandates)

■ Provide a consistent experience to the customer (uniform and consistent methods and platforms to respond to customer requests)

■ Utilize VOC and validate using internal DA information

■ Implement user satisfaction Indexes

Unlock the Power of Data and Analytics

Drive Process Excellence

Mitigate Overall Business Risk and Foster Compliance

Achieve Excellenceand Consistency in

Customer Experience

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 17

Unleashing the Power of GBS (continued)

■ Build professionals within GBS that can be sourced out to the other business functions and train/provide services –source of internal high quality talent

■ Establish a clearer career path for GBS professionals

■ Leverage skills and build training (not just technical but soft skills and relationship management skills needed to work with different parts of the organization, different cultures, etc.)

Build Internal Repository of High

Quality Talent

■ Need to be able to provide effective services, effective outcomes

■ Example: Integrate project management –greatest project management skills live in GBS, so ability to deploy lean six sigma and continuous improvement and effectiveness of delivery goes up due to centralized leadership of the different functions. Run it like a business (internal SLAs, KPIs)

Increase Effectiveness and Ability to Scale

■ Improve competitive position

■ Support consistency of global brand experience

Establish a Consistent Brand Experience

■ Mind shift in terms of professionalism; GBS organizations have much higher level of expectation in terms of it being a provider of choice, and a lever for cost competitiveness

■ Share skills and knowledge across the organization

Enhance Sophistication and

Collaboration

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 18

Characteristics at each level of maturityThere are five stages to reaching full GBS maturity. Reaching Level 5 is not right for all organizations, but those that get there see significant value from their operations.

Characteristics

■ Delivery of business services providing true end-to-end customer-centric services

■ Customer-focused organization that provides value■ Value creation versus cost reduction

■ Shared services cover transactional and some high-end processes■ Optimized balance of internal/external capabilities■ Integrated internal capabilities supporting service delivery■ Global process owners

■ Multi-function shared services covering all transactional processes, with all business units and locations supported

■ Non-integrated internal (shared services center) capabilities■ Outsourcing strategically used

■ Single function shared services covers most transactional processes with tactical on/offshore outsourcing

■ Most BUs and locations supported by shared services.■ Outsourcing tactically used

■ Decentralized functions with little central control over business support services

■ Outsourcing not used

Bu

sin

ess

serv

ices

mat

uri

ty

The journey…development stages…time

Level 1 – Fragmented

Level 5 – Strategic

Level 4 – Integrated

Level 3 – Scaled

Level 2 – Sub-Scaled

1

2

3

4

5

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 19

What drives confidence for service organizations?

.Confidence

High

Good

Low

Poor

Trust

Co

ntr

ol

Confidence = Trust + Control

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 20

Transformation PitfallsMISTAKES TO

AVOIDREPRESENTATIVE PITFALLS PRE-EMPTIVE ACTIONS

Inadequate focus on the challenges of change

Passive / aggressive behavior Raising of barriers to success

Assess readiness and issues early Actively and honestly communicate, addressing specific stakeholder group

concerns and needs Involve HR early and Ensure key employees have a secure transition process and

needs are addressed

Absent or unsophisticated governance

Degraded service and infighting Inability to effectively meet demand with the

provided services Failure to meet cost and quality expectations

Define an appropriate governance model, framework and structure early in the process; recognize that this will likely be different for the planning and implementation versus steady-state operation

Involve executive leadership in the governance Build the key stakeholders into the governance model and keep them involved

(“Governance” is not an organizational entity – it is about how decisions will be made and enforced)

Inadequate focus on transition

Delays and loss in financial benefits Stakeholder dissatisfaction Business disruption Loss of stakeholder confidence and support

Start out with a clear / agreed understanding of the baseline Explicitly plan for knowledge transfer Develop contingency plans Ensure the as-is (e.g., current processes, exception handling, systems, contacts) are

well documented Be creative and don’t get bogged down with constraints too easily

Improper funding or chargeback mechanisms

Underfunding of the planning, design and implementation of shared services may lead to unwise cutting of important corners

Unfair cost allocations, disadvantaging certain divisions

Squabbling and resistance to participation Inaccurate picture of the cost of services that

may lead to wrong decisions

Honestly assess the work and associated costs to execute the program; establish appropriate funding; consider needs for corporate–level funding

Seek to understand each division’s unique cost commitments & challenges Start out with a pricing strategy to drive behavior consistent with expectations and

strategies Agree the pricing approaches along with levels of transparency and granularity,

and implications for service design and service management Develop a clear and agreed approach for cost allocation and chargeback

Inadequate risk management or monitoring

Unexpected surprises and irreversible costly errors

Loss of confidence by key stakeholders Business disruption

Build risk management into the process and actively risk monitor Agree appropriate mitigations and accountabilities

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 21

Julie SullivanPartner– Shared Services and Outsourcing

Background

Julie Sullivan is a Partner in KPMG’s Management Consulting practice in Toronto and National Lead for the Shared Services and Outsourcing Practice. Julie’s team covers all alternative delivery structures including Shared Services ITO, BPO arrangements spanning strategy, business casing, transition and governance throughout all phases of the sourcing journey. Julie’s focus has been on Services Portfolio Management and Governance and Transition. Julie has substantial experience in helping companies optimize the value of alternative delivery models and has advised on large technology (ADM), Human Resources, Facilities Management, ITO and BPO outsourcing deals from strategy assessment through to implementation.

She has been engaged in projects helping companies develop and launch centers of excellence: shared services; vendor management; outsourcing and business process management. Additionally Julie has assisted major corporations in restructuring/designing governance organizations, policies, methodology and practices as well as coaching and training governance personnel.

Professional and Industry Experience

Prior to joining KPMG Julie was a Senior Advisor with EquaTerra. Julie consulted on Shared Services, ITO, BPO, F & A, Facilities and HR transactions including new deals, renewals and on-going relationships.

Julie created an Outsourcing Center of Competence for a Canadian bank. Julie was responsible for the vision, practice and methodology of the Centers both in the U.S. and Canada.

Julie was responsible for a team of sourcing consultants advising and reviewing and negotiating all material third party contracts for a Canadian bank (onshore and offshore)

Julie’s experience includes advising senior executives on all aspects of alternative service delivery including change management and organizational readiness

Julie has also extensive experience in the Banking Industry, Consumer Goods, Oil and Gas and Healthcare

Alternative Service Delivery

Advised several Health Care Shared Service Entities on Strategy, Governance, HIS strategies and business casing

Advised at the Federal, Provincial and Municipal levels of government on alternative service delivery

Training internal staff for a Global Insurance Company on Shared Services (design, run and govern)

Assessed and realigned major outsourcing relationships for Global Firms

Advised on the largest IT outsourcing in Canada in 2014

Julie SullivanPartner

KPMG LLPBay Adelaide Centre333 Bay Street Suite 4600Toronto ON M5H 2S5

Tel 416-777-8512Cell 416 721 0507Fax [email protected]

Function and SpecializationJulie is a Partner in KPMG Advisory Services practice, based in Toronto. Julie’s focus is on services portfolio management as well as governance and transition for ITO and BPO relationships.

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. 22© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International

Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Thank you

© 2016 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

kpmg.ca

Detail

Heading

Detail

Heading

Detail

Heading

Detail

Heading

![Untitled-1 []€¦ · Potenzfunktionen mit negativen Exponenten Untitled-1.nb . 4 Untitled-1.nb. Untitled-1.nb 5](https://img.pdfslide.us/doc/110x75/605b197ad57d6d08187081fc/untitled-1-potenzfunktionen-mit-negativen-exponenten-untitled-1nb-4-untitled-1nb.jpg)

![SYNOPSYS™ Input General Formats · 2019. 10. 1. · format: sn option where option is one of the following: null sph rd nb rad nb cv nb ncop pcv nb [ m [ b ] ] umc nb upc nb ymc](https://img.pdfslide.us/doc/110x75/60b65647ea53da7a652209e1/synopsysa-input-general-formats-2019-10-1-format-sn-option-where-option.jpg)