Embed Size (px)

Citation preview

JAMES PRIM NUN YOK NANH PAO ANAN

• Company’s Brief

• List of Accounting Policies Involved

• Presentation of Financial Statement

• Agriculture

• Plant, Property and Equipment

• Sales Recognition

• Business Combination

Charoen Pokphand Food

• leading agro-industrial and food conglomerate in the Asia Pacific Region

• Operates four business divisions

What is CPF?

Feed

Farm

Food

Retail Outlet

The Journey

1978Register under the name‘Charoen Pokphand FeedmillCompany Limited’Producing and distributing animal feed in Southern Thailand

1987Listed on the Stock Exchange ofThailand

1994Converted to a PublicCompany Limited

1998-1999Acquired ordinary shares in three agro-industrial public companies in Thailand from Charoen Pokphand Group, and another nine agro-industrial and food from CPGA fully integrated agro business in livestock and aquaculture

Renamed as ‘Charoen Pokphand FoodCompany Limited

Vision: Kitchen of the World

2002-2012

2006Began production of ready-to-eat products under CP brand and distributed product domestically and internationally

Start a retail business called ‘CP Fresh Mart’ selling fresh and cook meat, and ready-to-eat products

2012Started food court business

Acquired 99.99% Of issued shares In the restaurant

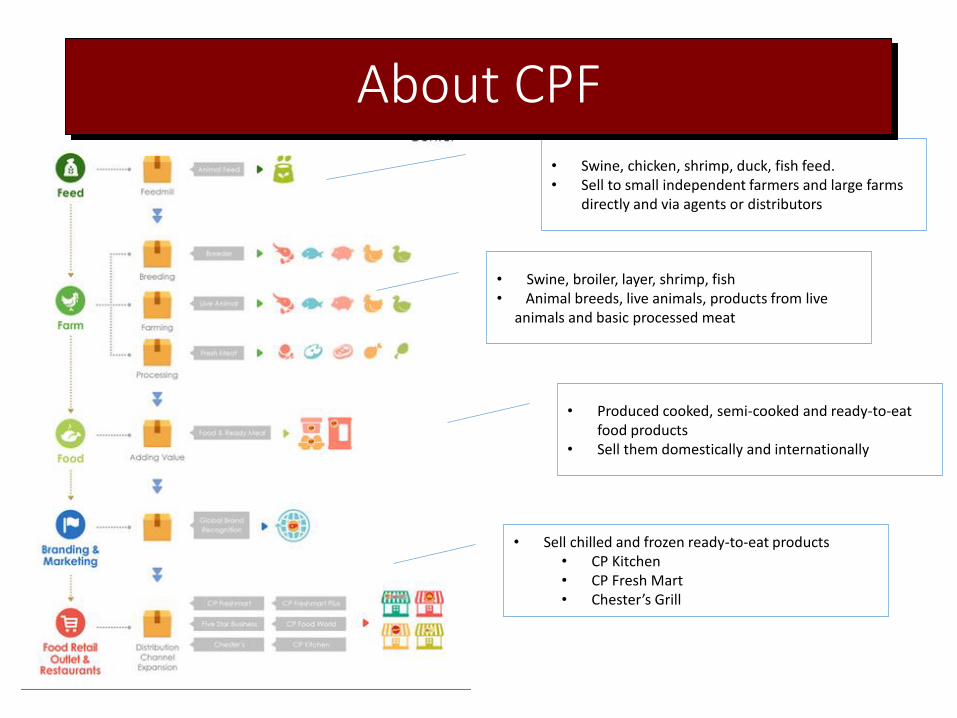

• Swine, chicken, shrimp, duck, fish feed.• Sell to small independent farmers and large farms

directly and via agents or distributors

• Swine, broiler, layer, shrimp, fish • Animal breeds, live animals, products from live

animals and basic processed meat

• Sell chilled and frozen ready-to-eat products • CP Kitchen• CP Fresh Mart• Chester’s Grill

• Produced cooked, semi-cooked and ready-to-eat food products

• Sell them domestically and internationally

About CPF

CPF

• Feed and Farm

Livestock

Aquaculture

CPF

• Food and Retail

Food

Retail

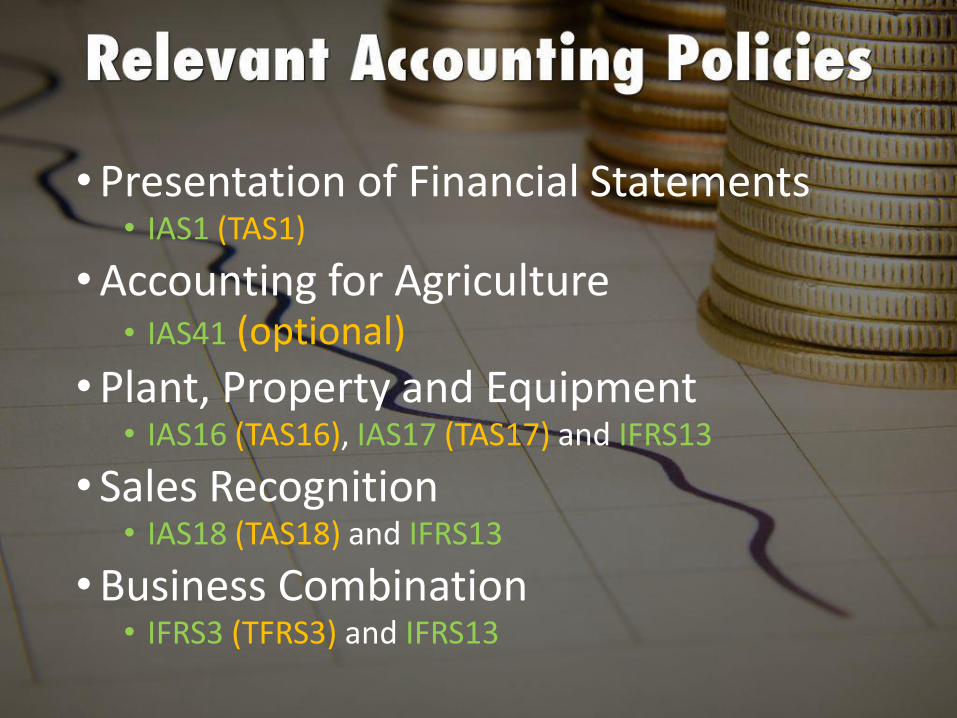

•Presentation of Financial Statements• IAS1 (TAS1)

•Accounting for Agriculture• IAS41 (optional)

•Plant, Property and Equipment• IAS16 (TAS16), IAS17 (TAS17) and IFRS13

• Sales Recognition• IAS18 (TAS18) and IFRS13

•Business Combination• IFRS3 (TFRS3) and IFRS13

1

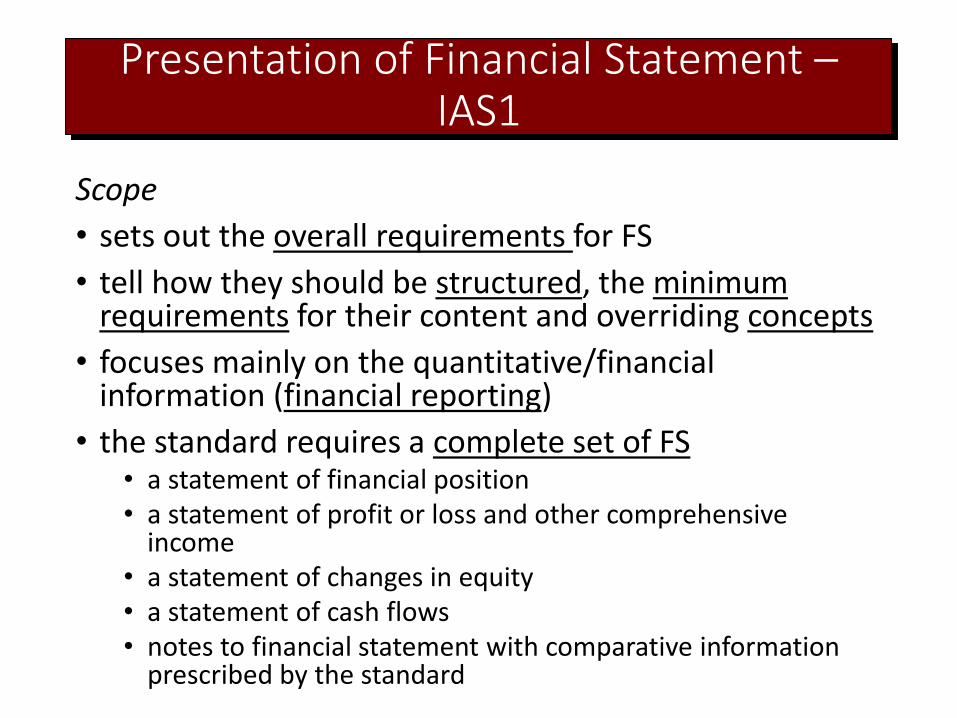

Presentation of Financial Statement –IAS1

Scope

• sets out the overall requirements for FS

• tell how they should be structured, the minimum requirements for their content and overriding concepts

• focuses mainly on the quantitative/financial information (financial reporting)

• the standard requires a complete set of FS • a statement of financial position• a statement of profit or loss and other comprehensive

income• a statement of changes in equity• a statement of cash flows• notes to financial statement with comparative information

prescribed by the standard

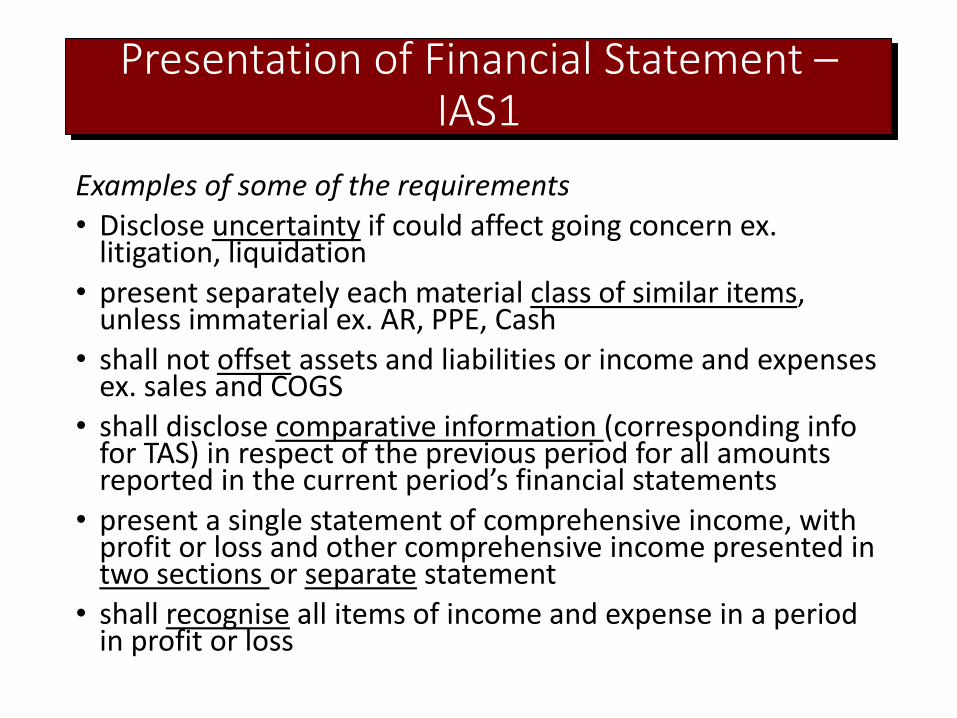

Presentation of Financial Statement –IAS1

Examples of some of the requirements

• Disclose uncertainty if could affect going concern ex. litigation, liquidation

• present separately each material class of similar items, unless immaterial ex. AR, PPE, Cash

• shall not offset assets and liabilities or income and expenses ex. sales and COGS

• shall disclose comparative information (corresponding info for TAS) in respect of the previous period for all amounts reported in the current period’s financial statements

• present a single statement of comprehensive income, with profit or loss and other comprehensive income presented in two sections or separate statement

• shall recognise all items of income and expense in a period in profit or loss

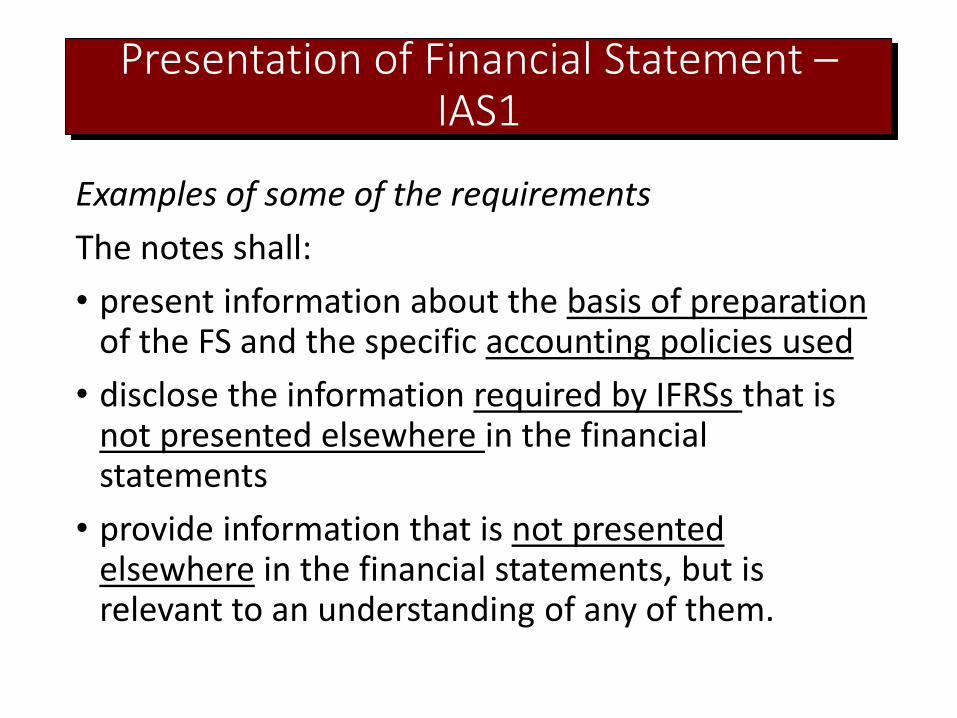

Presentation of Financial Statement –IAS1

Examples of some of the requirements

The notes shall:

• present information about the basis of preparation of the FS and the specific accounting policies used

• disclose the information required by IFRSs that is not presented elsewhere in the financial statements

• provide information that is not presented elsewhere in the financial statements, but is relevant to an understanding of any of them.

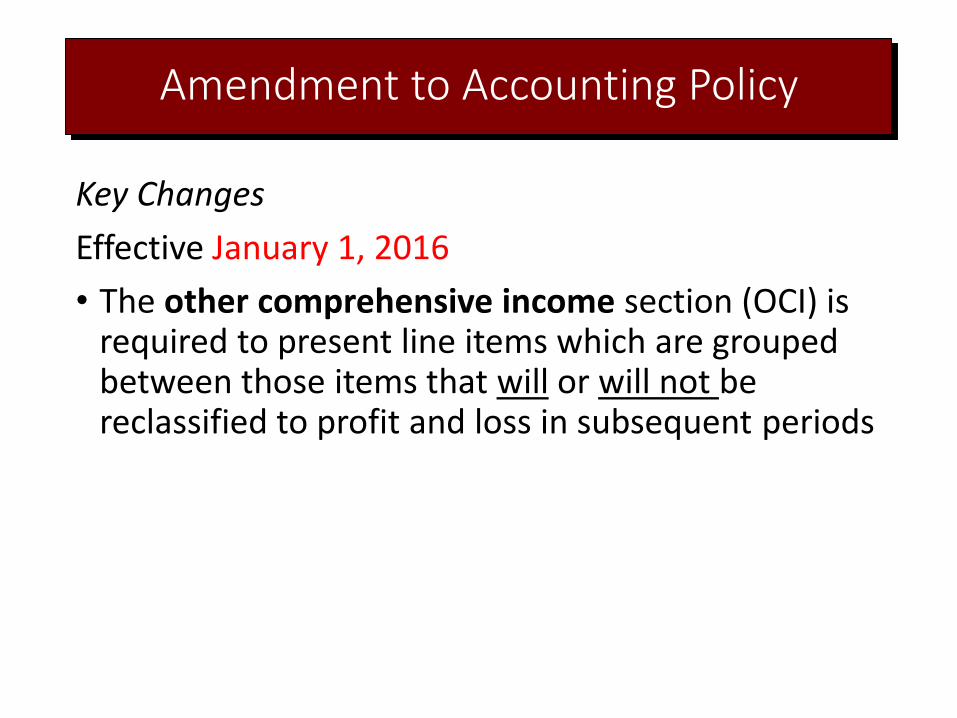

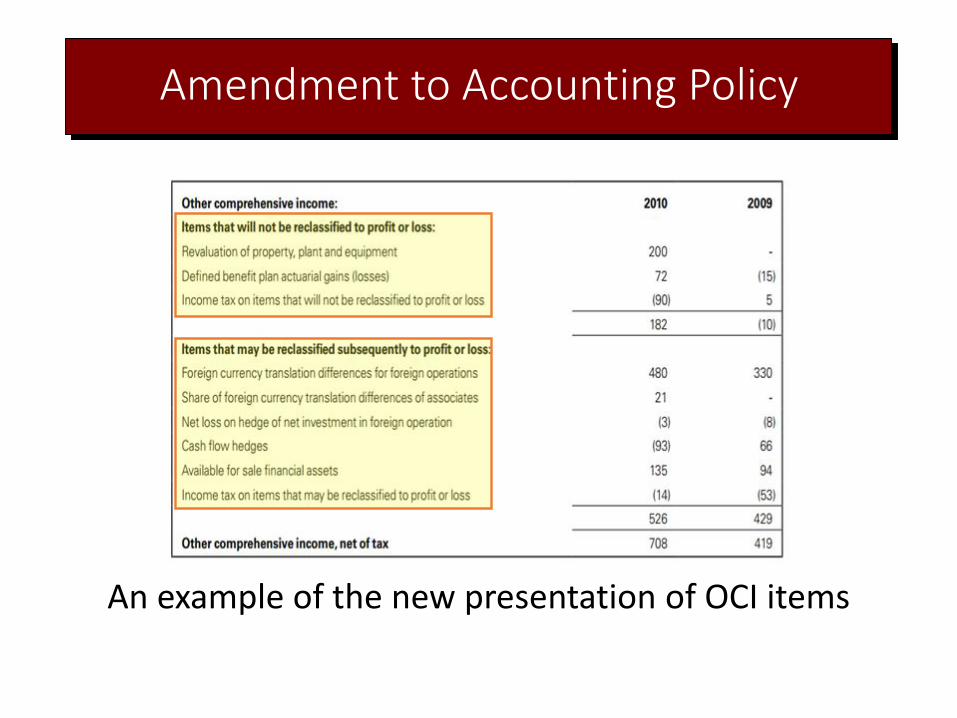

Amendment to Accounting Policy

Key Changes

Effective January 1, 2016

• The other comprehensive income section (OCI) is required to present line items which are grouped between those items that will or will not be reclassified to profit and loss in subsequent periods

Amendment to Accounting Policy

An example of the new presentation of OCI items

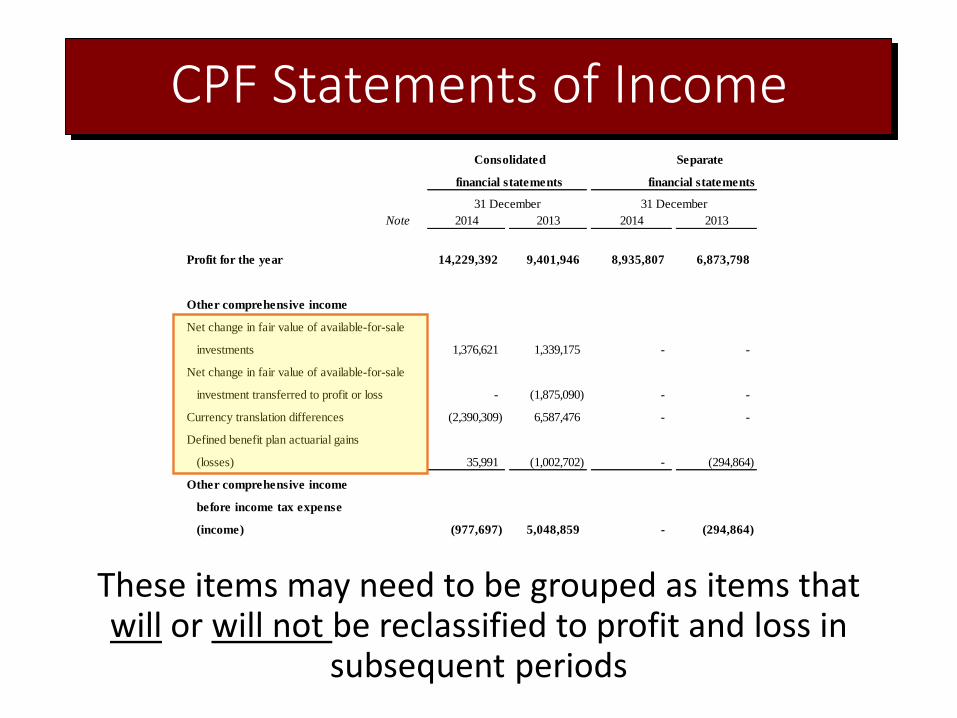

CPF Statements of Income

These items may need to be grouped as items that will or will not be reclassified to profit and loss in

subsequent periods

Note 2014 2013 2014 2013

Profit for the year 14,229,392 9,401,946 8,935,807 6,873,798

Other comprehensive income

Net change in fair value of available-for-sale

investments 1,376,621 1,339,175 - -

Net change in fair value of available-for-sale

investment transferred to profit or loss - (1,875,090) - -

Currency translation differences (2,390,309) 6,587,476 - -

Defined benefit plan actuarial gains

(losses) 35,991 (1,002,702) - (294,864)

Other comprehensive income

before income tax expense

(income) (977,697) 5,048,859 - (294,864)

Consolidated Separate

financial statements financial statements

31 December 31 December

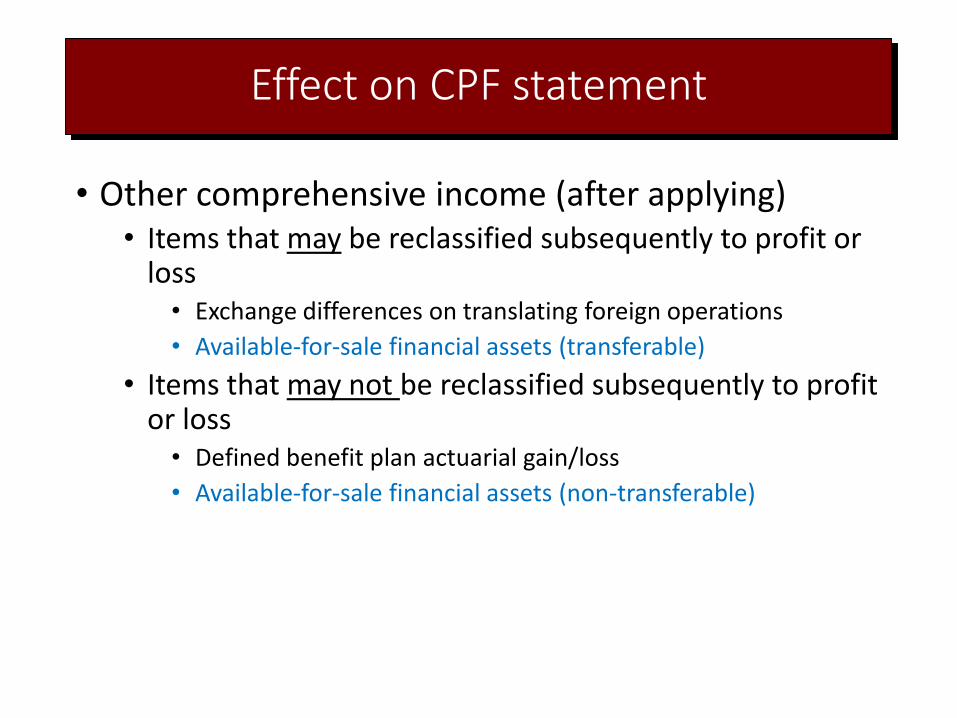

Effect on CPF statement

• Other comprehensive income (after applying)• Items that may be reclassified subsequently to profit or

loss• Exchange differences on translating foreign operations

• Available-for-sale financial assets (transferable)

• Items that may not be reclassified subsequently to profit or loss• Defined benefit plan actuarial gain/loss

• Available-for-sale financial assets (non-transferable)

2

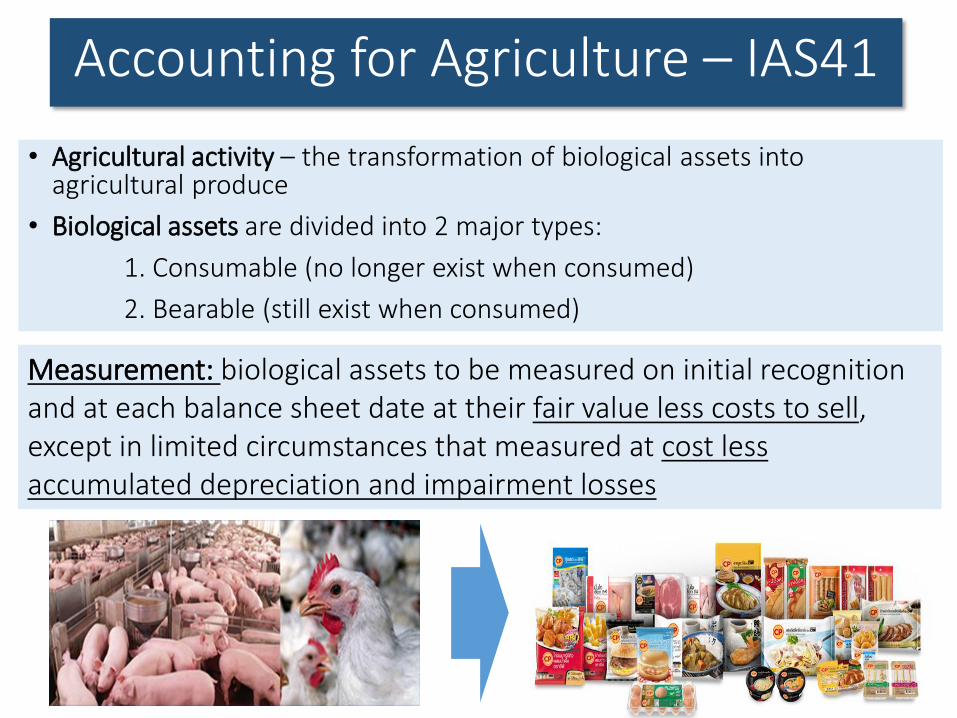

Accounting for Agriculture – IAS41

• Agricultural activity – the transformation of biological assets into agricultural produce

• Biological assets are divided into 2 major types:

1. Consumable (no longer exist when consumed)

2. Bearable (still exist when consumed)

Measurement: biological assets to be measured on initial recognition and at each balance sheet date at their fair value less costs to sell, except in limited circumstances that measured at cost less accumulated depreciation and impairment losses

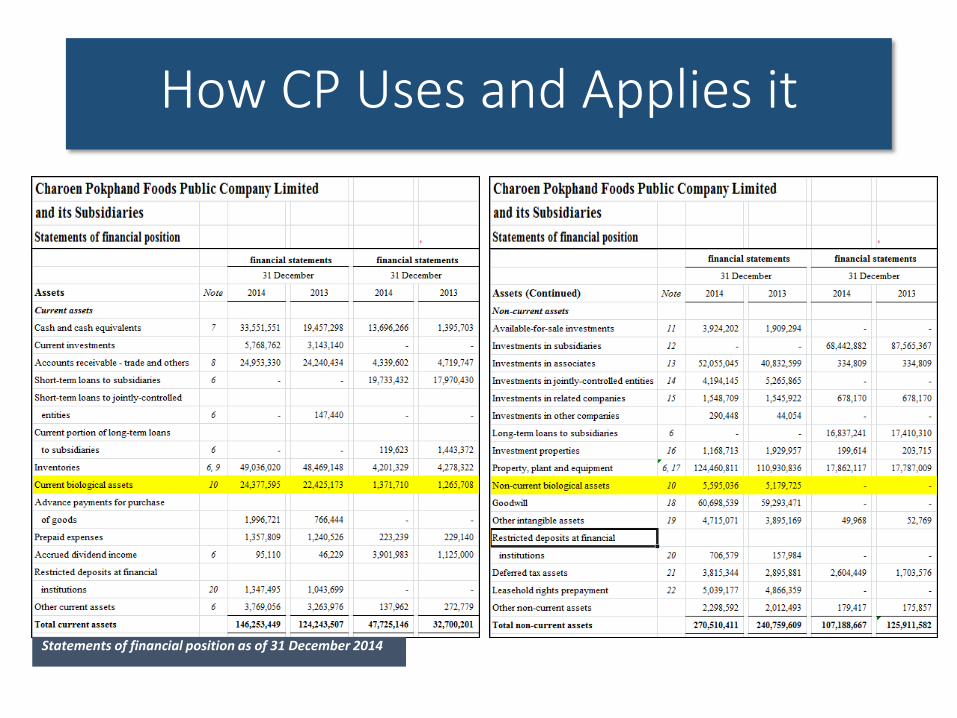

How CP Uses and Applies it

Statements of financial position as of 31 December 2014

Notes to Financial Statements 2014

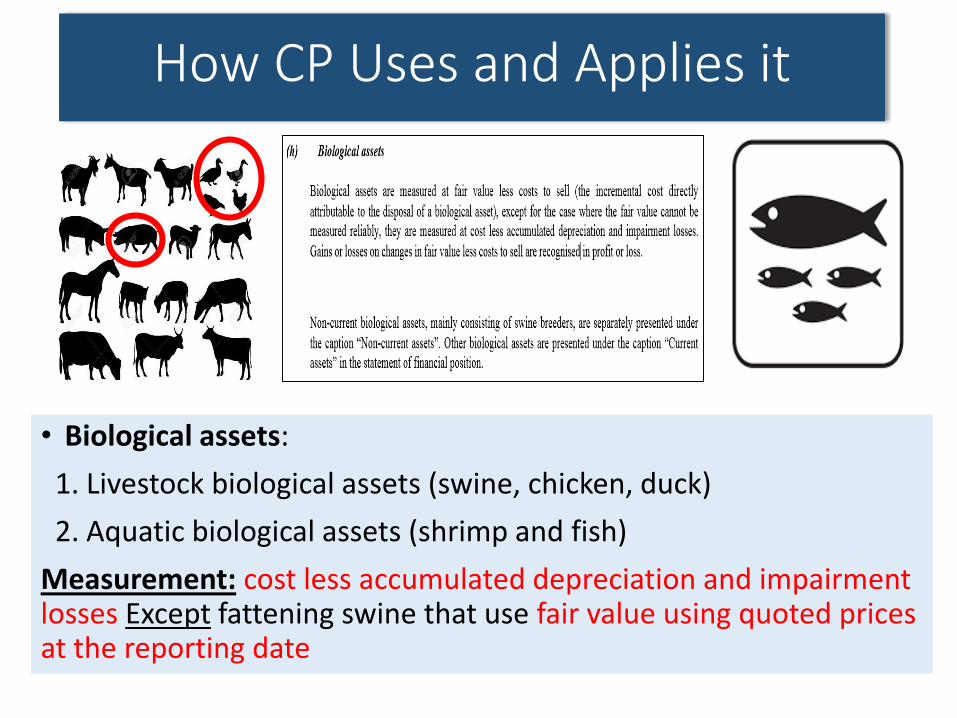

How CP Uses and Applies it

• Biological assets:

1. Livestock biological assets (swine, chicken, duck)

2. Aquatic biological assets (shrimp and fish)

Measurement: cost less accumulated depreciation and impairment losses Except fattening swine that use fair value using quoted prices at the reporting date

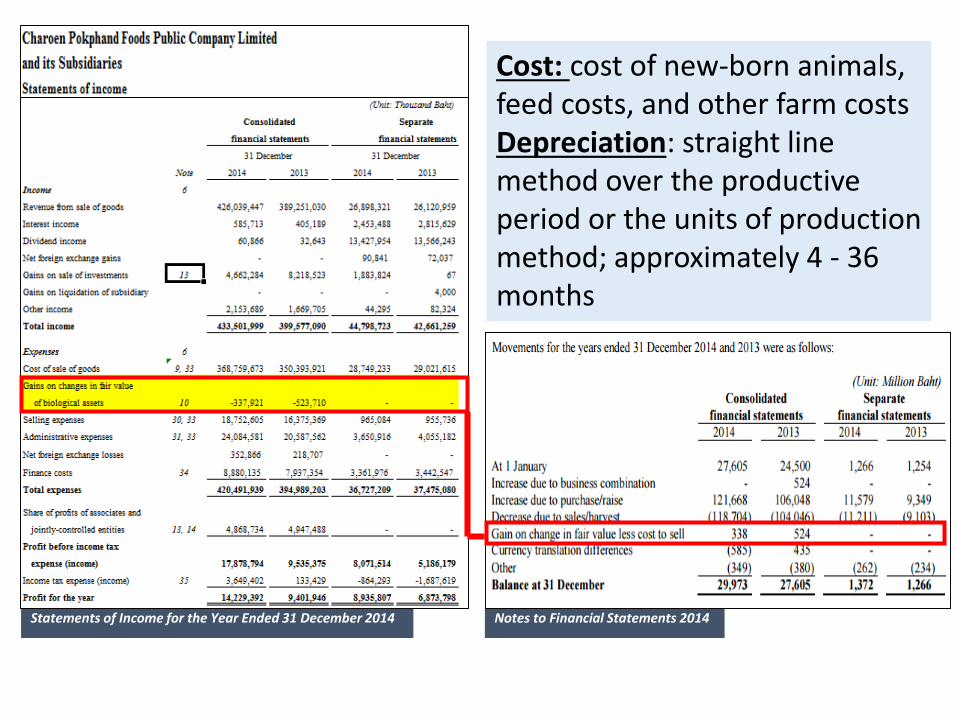

Statements of Income for the Year Ended 31 December 2014 Notes to Financial Statements 2014

Cost: cost of new-born animals, feed costs, and other farm costsDepreciation: straight line method over the productive period or the units of production method; approximately 4 - 36 months

Amended by Agriculture: Bearer Plants (IAS 16 and IAS 41)

• Effective for annual periods beginning on or after 1 January 2016

• Bringing bearer plants from the IAS 41 into IAS 16 (treat as PPE)

• Mature bearer plant no longer undergo biological transformation but

still produce biological assets

• Measure at ‘cost’ subsequent to initial recognition

• A ‘bearer plant’ is defined as "a living plant that:

• is used in the production or supply of agricultural produce;

• is expected to bear produce for more than one period;

• and has a low likelihood of being sold as agricultural produce, except for incidental scrap sales."

• Produce growing on bearer plants treated as biological asset - IAS 41

Policy amendment

And how will it affect?

3

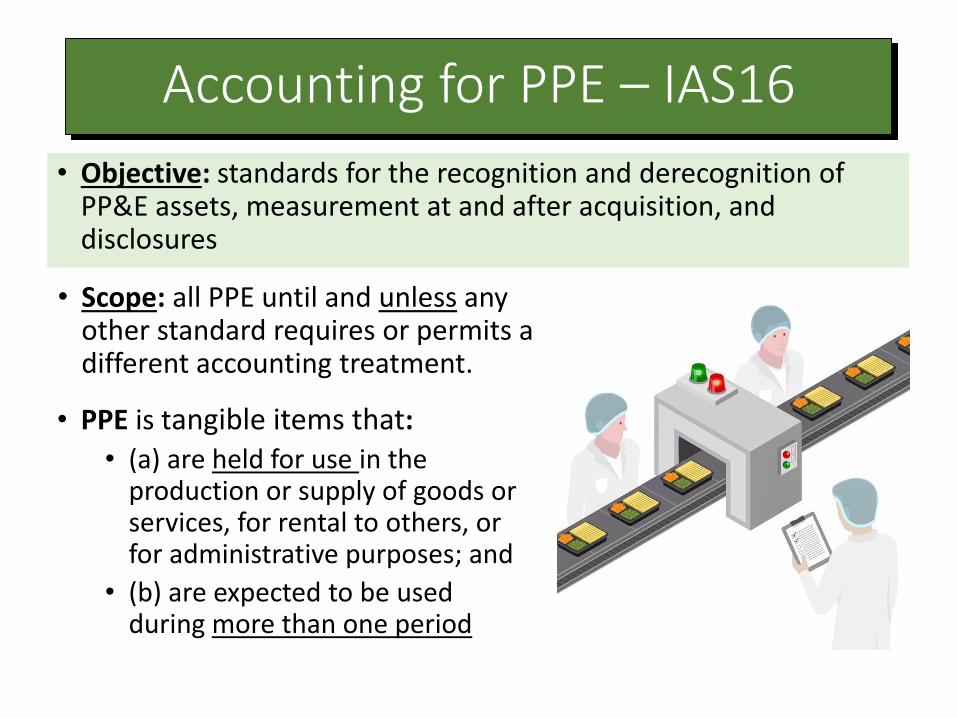

• Scope: all PPE until and unless any other standard requires or permits a different accounting treatment.

Accounting for PPE – IAS16

• Objective: standards for the recognition and derecognition of PP&E assets, measurement at and after acquisition, and disclosures

• PPE is tangible items that:

• (a) are held for use in the production or supply of goods or services, for rental to others, or for administrative purposes; and

• (b) are expected to be used during more than one period

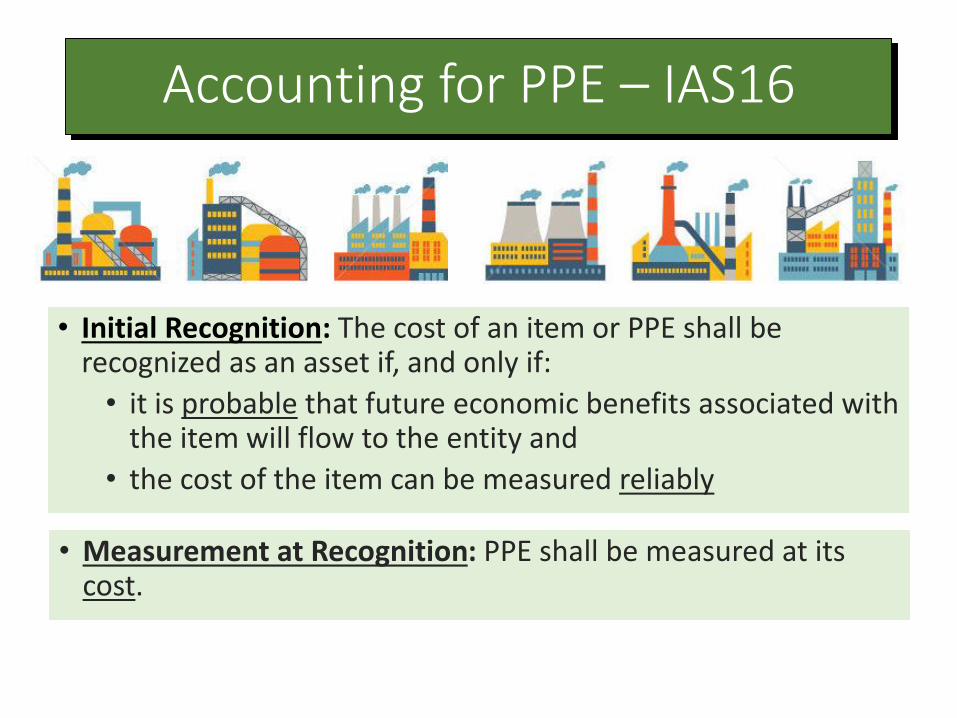

• Initial Recognition: The cost of an item or PPE shall be recognized as an asset if, and only if:

• it is probable that future economic benefits associated with the item will flow to the entity and

• the cost of the item can be measured reliably

Accounting for PPE – IAS16

• Measurement at Recognition: PPE shall be measured at its cost.

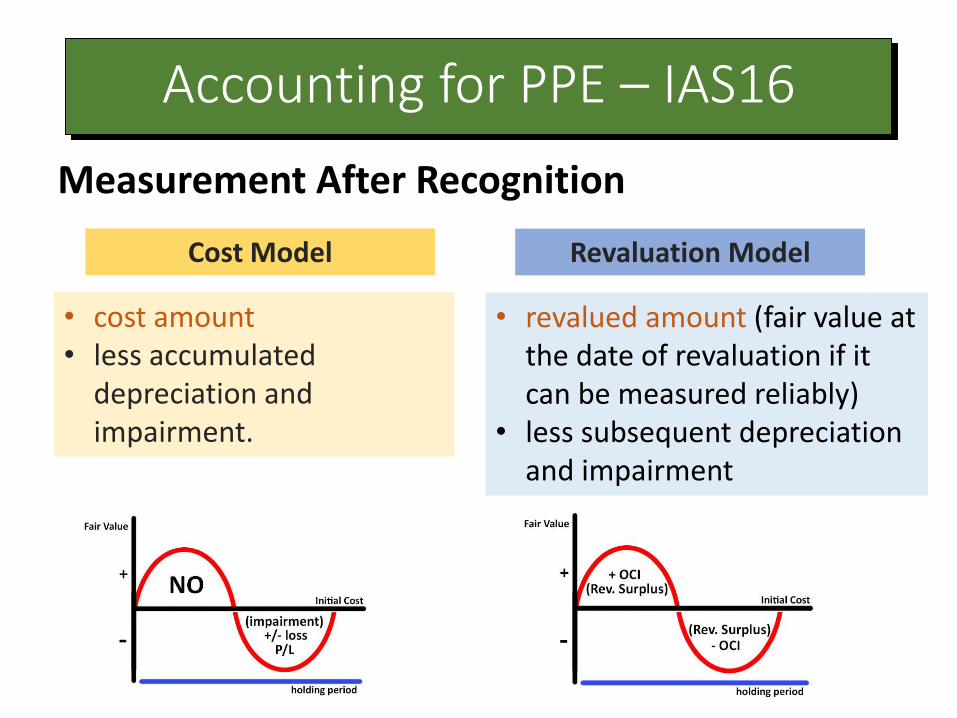

Measurement After Recognition

Accounting for PPE – IAS16

Cost Model Revaluation Model

• cost amount• less accumulated

depreciation and impairment.

• revalued amount (fair value at the date of revaluation if it can be measured reliably)

• less subsequent depreciation and impairment

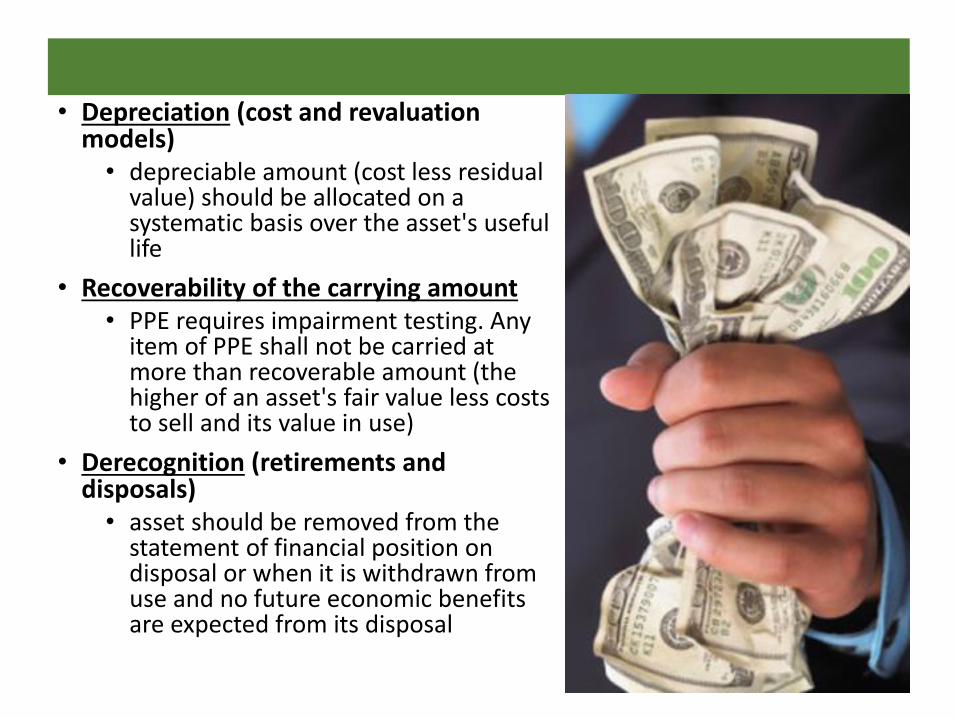

• Depreciation (cost and revaluation models)• depreciable amount (cost less residual

value) should be allocated on a systematic basis over the asset's useful life

• Recoverability of the carrying amount• PPE requires impairment testing. Any

item of PPE shall not be carried at more than recoverable amount (the higher of an asset's fair value less costs to sell and its value in use)

• Derecognition (retirements and disposals)• asset should be removed from the

statement of financial position on disposal or when it is withdrawn from use and no future economic benefits are expected from its disposal

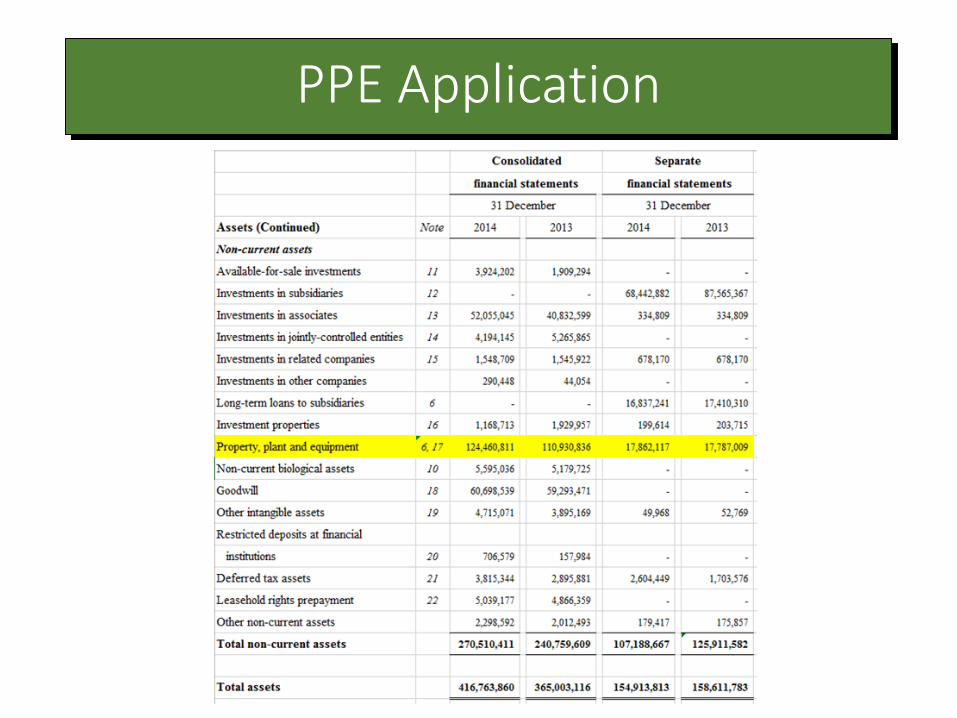

PPE Application

PPE Application

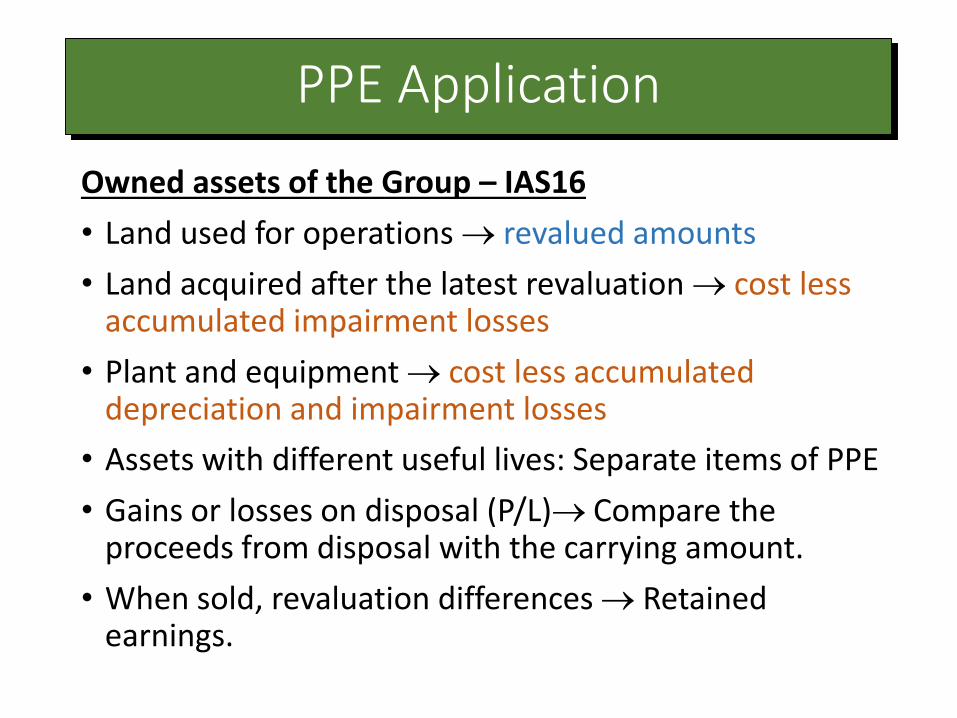

Owned assets of the Group – IAS16

• Land used for operations revalued amounts

• Land acquired after the latest revaluation cost less accumulated impairment losses

• Plant and equipment cost less accumulated depreciation and impairment losses

• Assets with different useful lives: Separate items of PPE

• Gains or losses on disposal (P/L) Compare the proceeds from disposal with the carrying amount.

• When sold, revaluation differences Retained earnings.

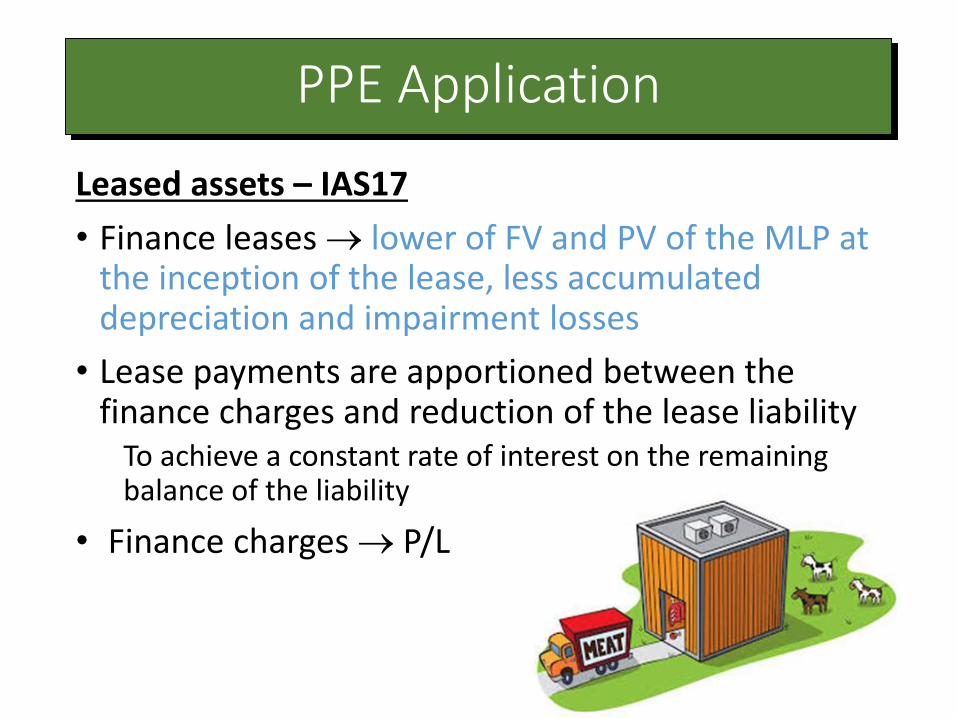

PPE Application

Leased assets – IAS17

• Finance leases lower of FV and PV of the MLP at the inception of the lease, less accumulated depreciation and impairment losses

• Lease payments are apportioned between the finance charges and reduction of the lease liability

To achieve a constant rate of interest on the remaining balance of the liability

• Finance charges P/L

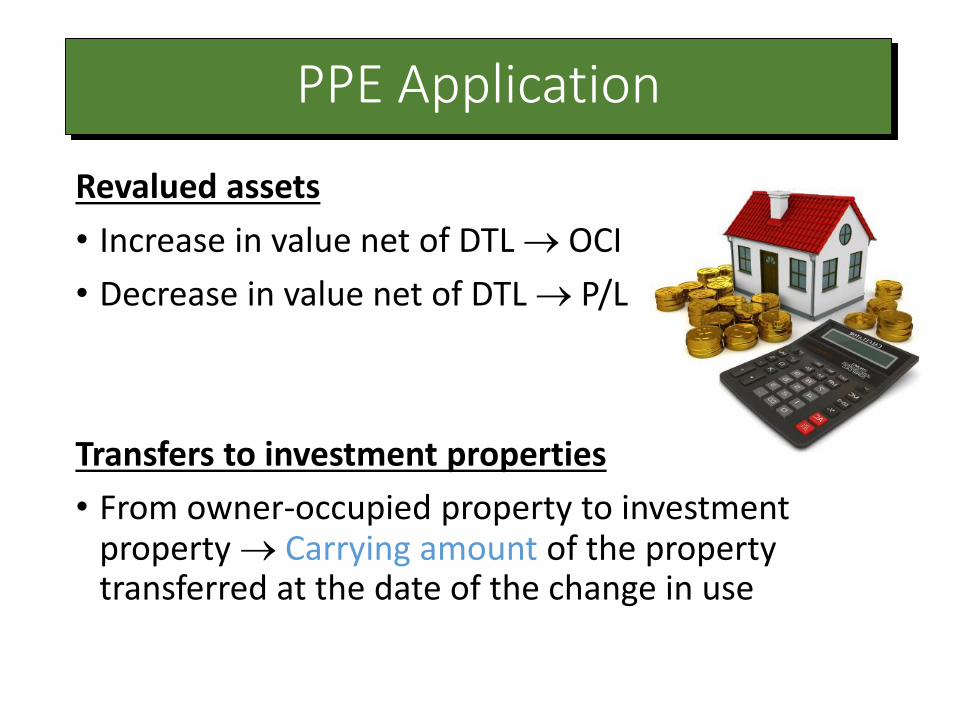

PPE Application

Revalued assets

• Increase in value net of DTL OCI

• Decrease in value net of DTL P/L

Transfers to investment properties

• From owner-occupied property to investment property Carrying amount of the property transferred at the date of the change in use

PPE Application

Subsequent costs

• Cost of replacing part Carrying amount of the item IF:

(1) Probable that the future economic benefits

(2) Cost can be measured reliably

• Carrying amount of the replaced part is derecognized

• Costs of the day-to-day servicing P/L

PPE Application

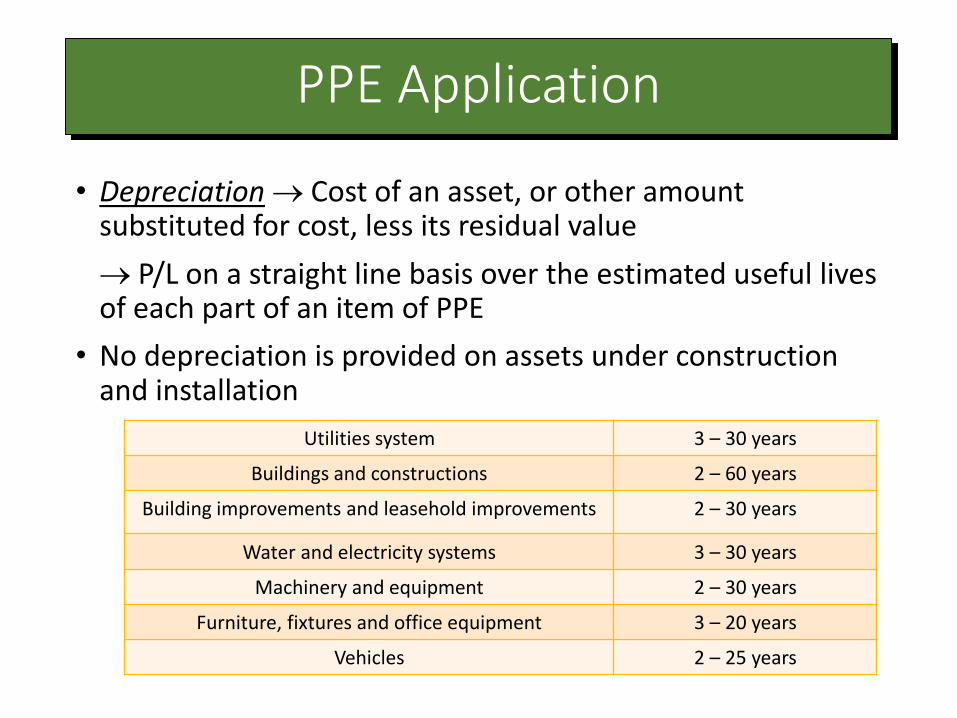

• Depreciation Cost of an asset, or other amount substituted for cost, less its residual value

P/L on a straight line basis over the estimated useful lives of each part of an item of PPE

• No depreciation is provided on assets under construction and installation

Utilities system 3 – 30 years

Buildings and constructions 2 – 60 years

Building improvements and leasehold improvements 2 – 30 years

Water and electricity systems 3 – 30 years

Machinery and equipment 2 – 30 years

Furniture, fixtures and office equipment 3 – 20 years

Vehicles 2 – 25 years

Amended by Clarification of Acceptable Methods of Depreciation and

Amortization (IAS 16)

• Effective for annual periods beginning on or after 1 January 2016

• The depreciation method used should reflect the pattern in which the

asset's economic benefits are consumed by the entity. Depreciation

method that is based on revenue that is generated by an activity that

includes the use of an asset is not appropriate.

• Pattern of generation of economic benefits that arise from the operation of

the business of which an asset is part, NOT pattern of consumption of an

asset’s expected future economic benefits

• When depreciation method is reviewed annually, expected future

reductions in selling prices could be indicative of a higher rate of

consumption of the future economic benefits embodied in an asset.

PPE – Policy amendment

4

Revenue Recognition - IAS18

• Revenue Recognition – IAS18• probable that future economic benefits will flow to the

entity

• benefits can be measured reliably

• Revenue is inflow of economic benefits during the period arising in the course of the ordinaryactivities

• Revenue Types• Sales of goods

• Render of services

• Interest, royalties and dividend

Sales Recognition – IAS18

• Sales are measured at Fair Value

• Fair Value (IFRS 13) = amount for which the goods could be exchanged between knowledgeable, willing parties in an arm’s length transaction

• Recognize sales when:• Risk and reward transferred to buyer• No control over the goods sold• Revenue can be measured reliability• Probable that economic benefit will flow into the

entity• Cost incurred can be measured reliability

• No amendment to IAS18

How is it applied?

• Sold as stand-alone products

How is it applied?

• Revenue and expenses recognized as “principal”

• Sales of biological goods are made to external customers, such as supermarkets and restaurants, as well as CP stores

How is it applied?

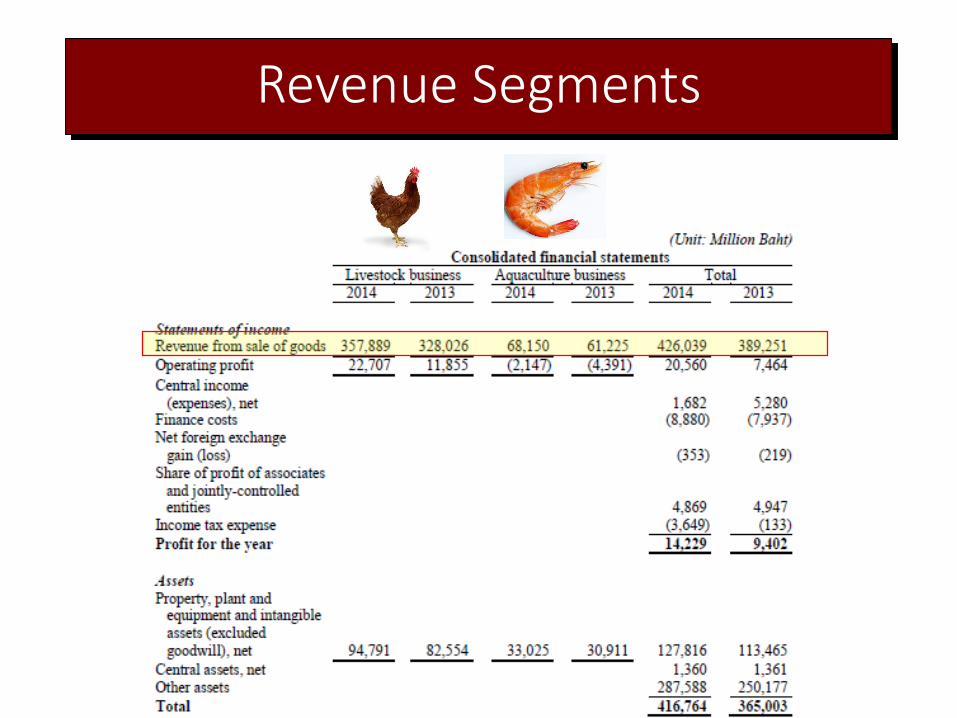

Revenue Segments

• CPF has two revenue segments

Livestock

Aquaculture

Revenue Segments

5

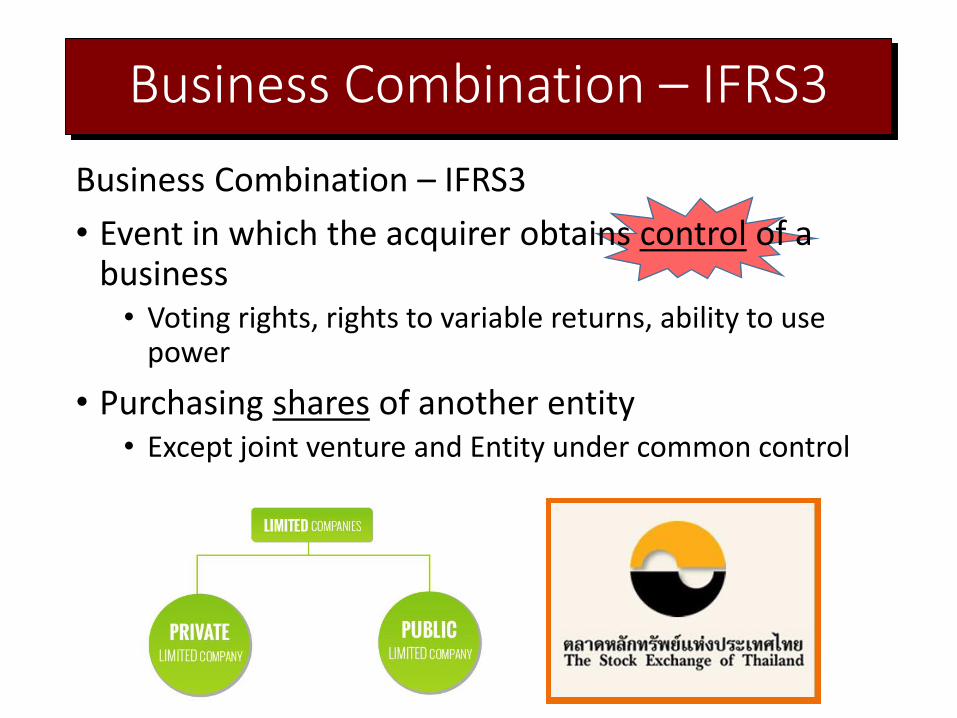

Business Combination – IFRS3

Business Combination – IFRS3

• Event in which the acquirer obtains control of a business• Voting rights, rights to variable returns, ability to use

power

• Purchasing shares of another entity• Except joint venture and Entity under common control

Business Combination – IFRS3

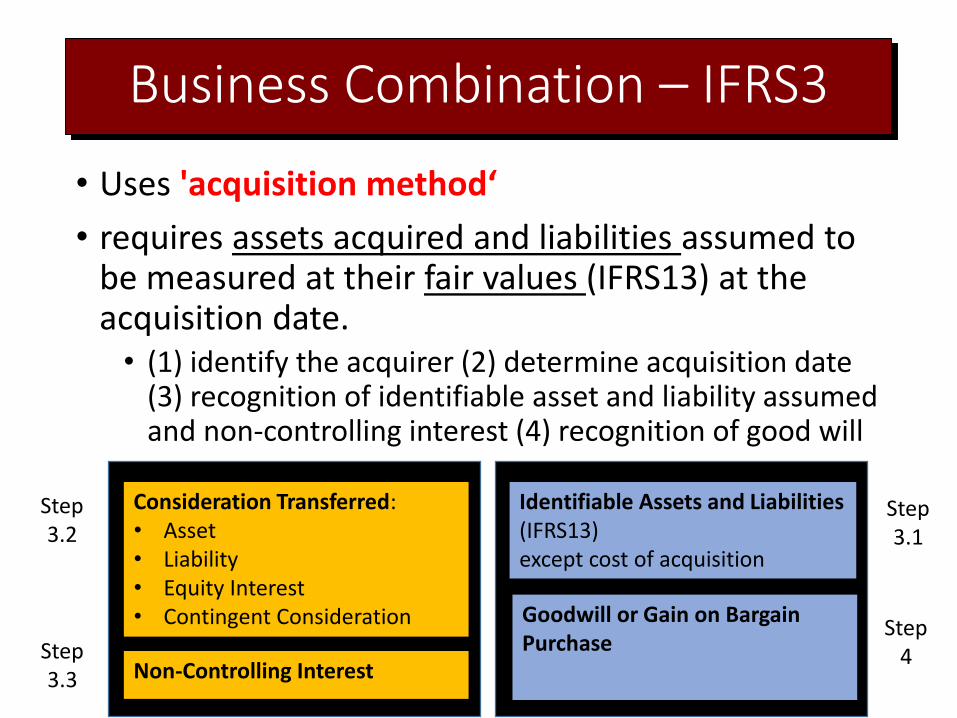

• Uses 'acquisition method‘

• requires assets acquired and liabilities assumed to be measured at their fair values (IFRS13) at the acquisition date.• (1) identify the acquirer (2) determine acquisition date

(3) recognition of identifiable asset and liability assumed and non-controlling interest (4) recognition of good will

Consideration Transferred:• Asset• Liability• Equity Interest• Contingent Consideration

Identifiable Assets and Liabilities(IFRS13) except cost of acquisition

Goodwill or Gain on Bargain Purchase

Non-Controlling Interest

Step3.1

Step3.2

Step3.3

Step4

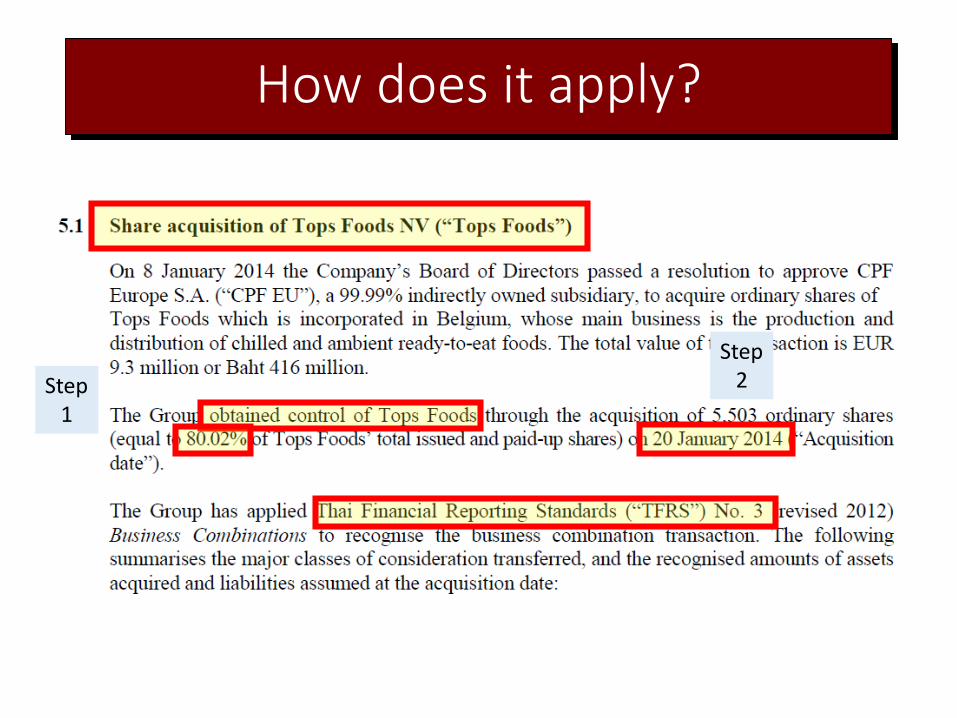

How does it apply?

Step1

Step2

How does it apply?

• Consideration Transferred: 416

• NCI: 68

Total: 484

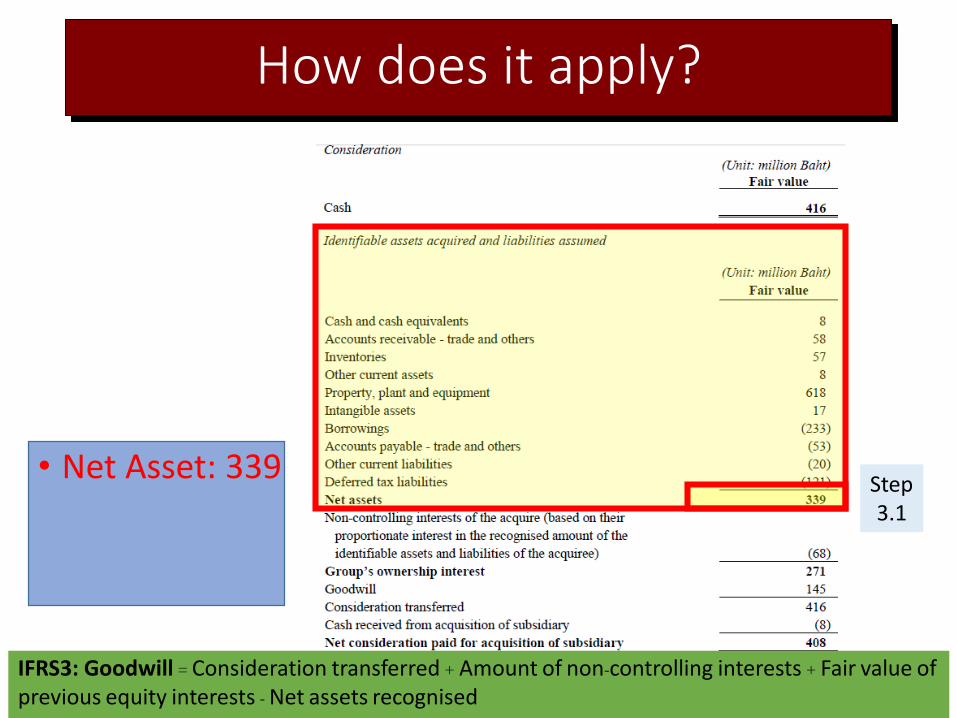

• Net Asset: 339

IFRS3: Goodwill = Consideration transferred + Amount of non-controlling interests + Fair value ofprevious equity interests - Net assets recognised

Step3.1

How does it apply?

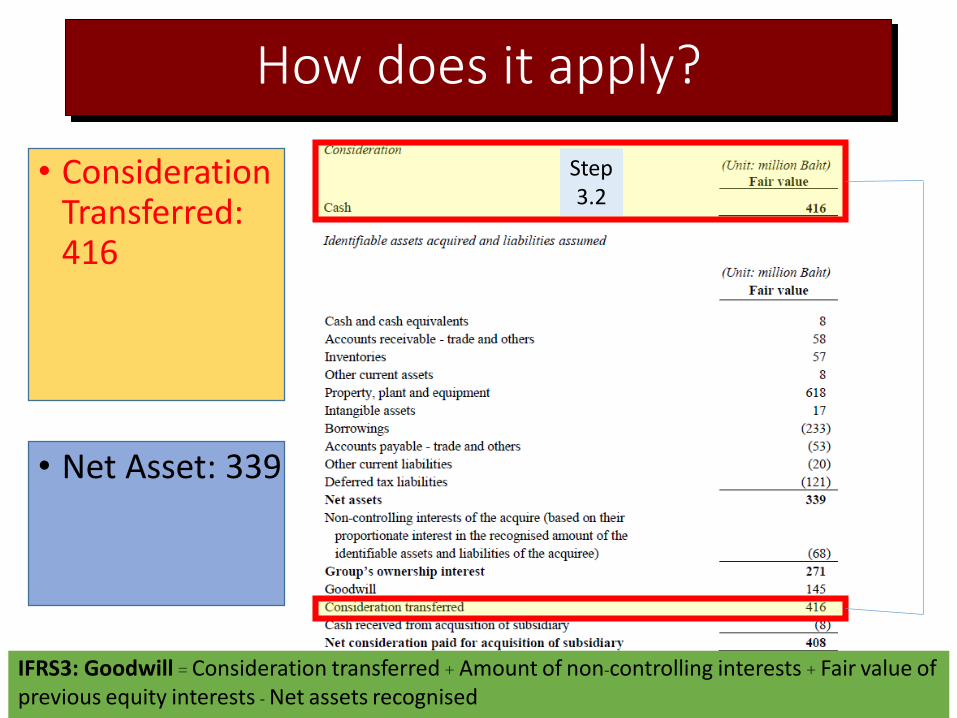

• Consideration Transferred: 416

• Net Asset: 339

IFRS3: Goodwill = Consideration transferred + Amount of non-controlling interests + Fair value ofprevious equity interests - Net assets recognised

Step3.2

How does it apply?

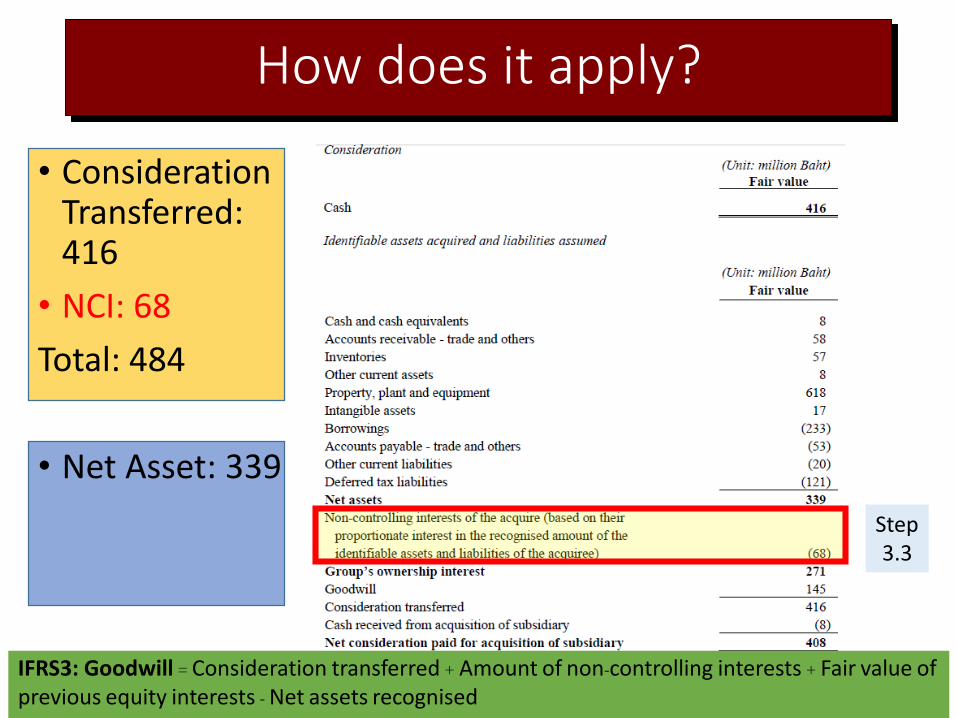

• Consideration Transferred: 416

• NCI: 68

Total: 484

• Net Asset: 339

IFRS3: Goodwill = Consideration transferred + Amount of non-controlling interests + Fair value ofprevious equity interests - Net assets recognised

Step3.3

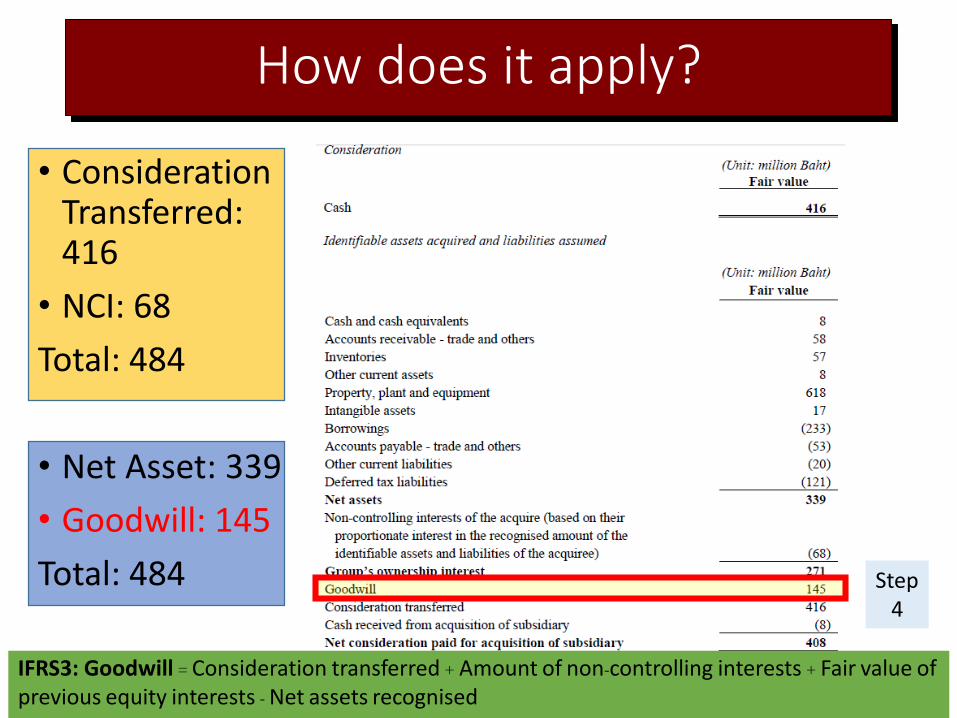

How does it apply?

• Consideration Transferred: 416

• NCI: 68

Total: 484

• Net Asset: 339

• Goodwill: 145

Total: 484

IFRS3: Goodwill = Consideration transferred + Amount of non-controlling interests + Fair value ofprevious equity interests - Net assets recognised

Step4

How does it apply?

• Consideration Transferred: 416

• NCI: 68

Total: 484

• Net Asset: 339

• Goodwill: 145

Total: 484

IFRS3: Goodwill = Consideration transferred + Amount of non-controlling interests + Fair value ofprevious equity interests - Net assets recognised

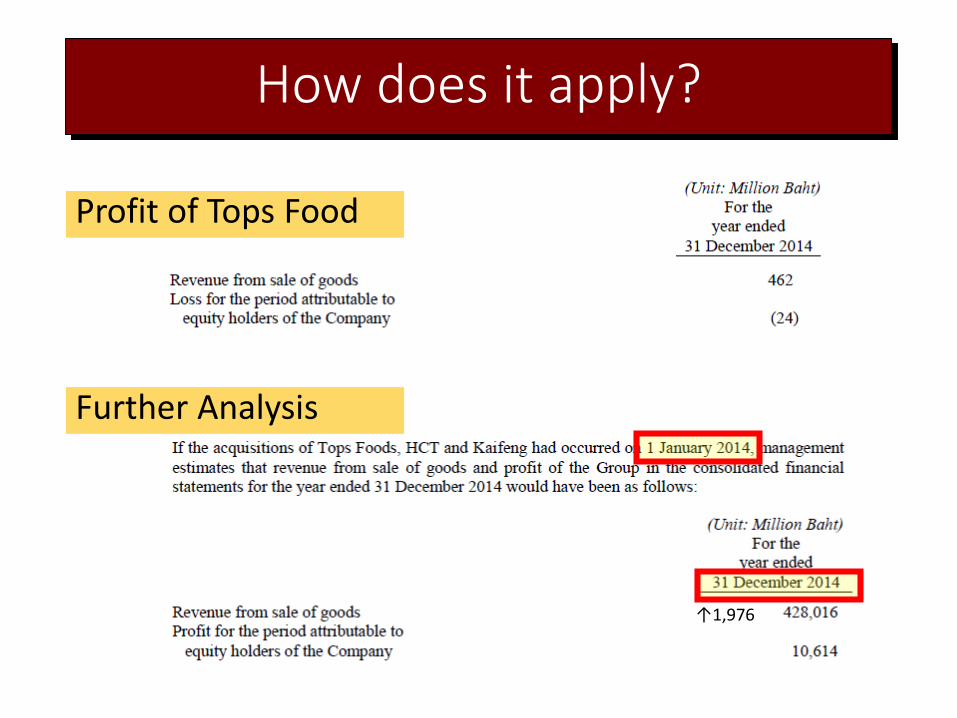

How does it apply?

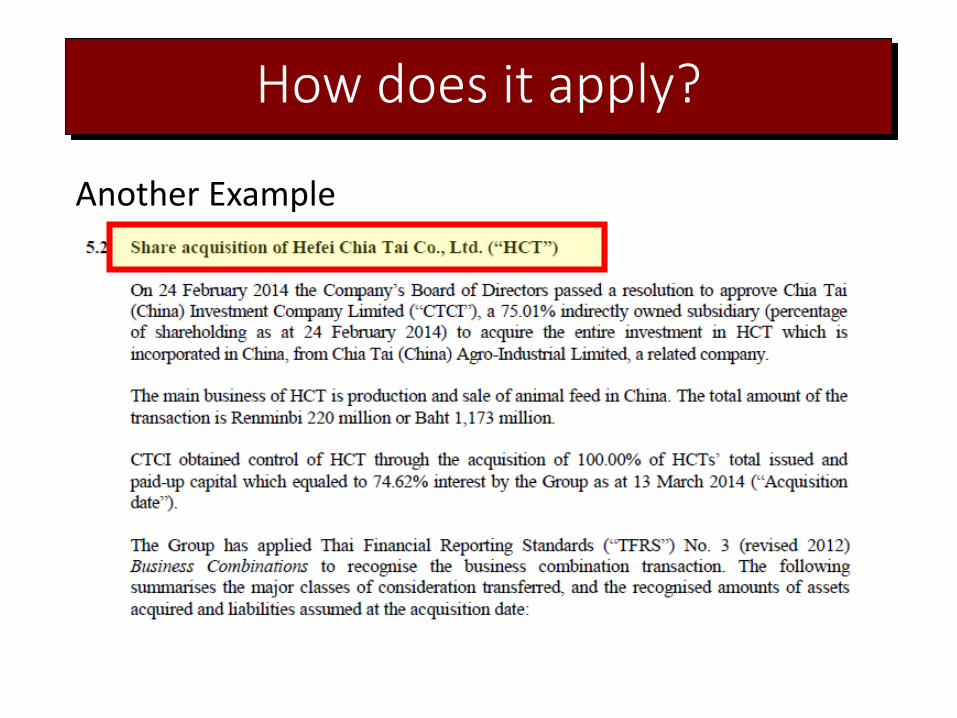

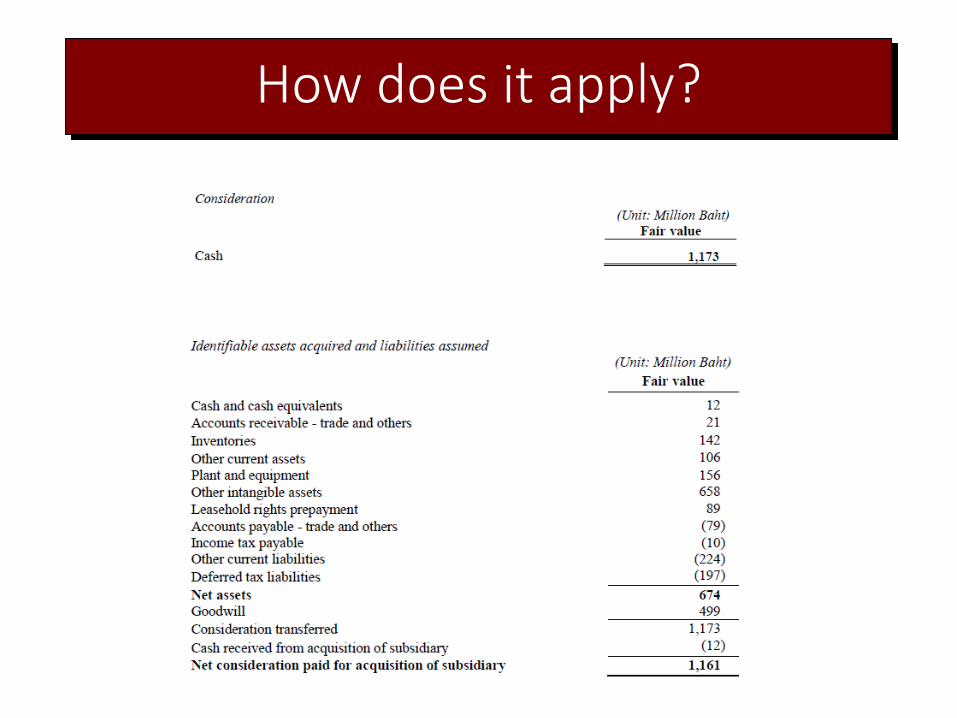

Another Example

How does it apply?

How does it apply?

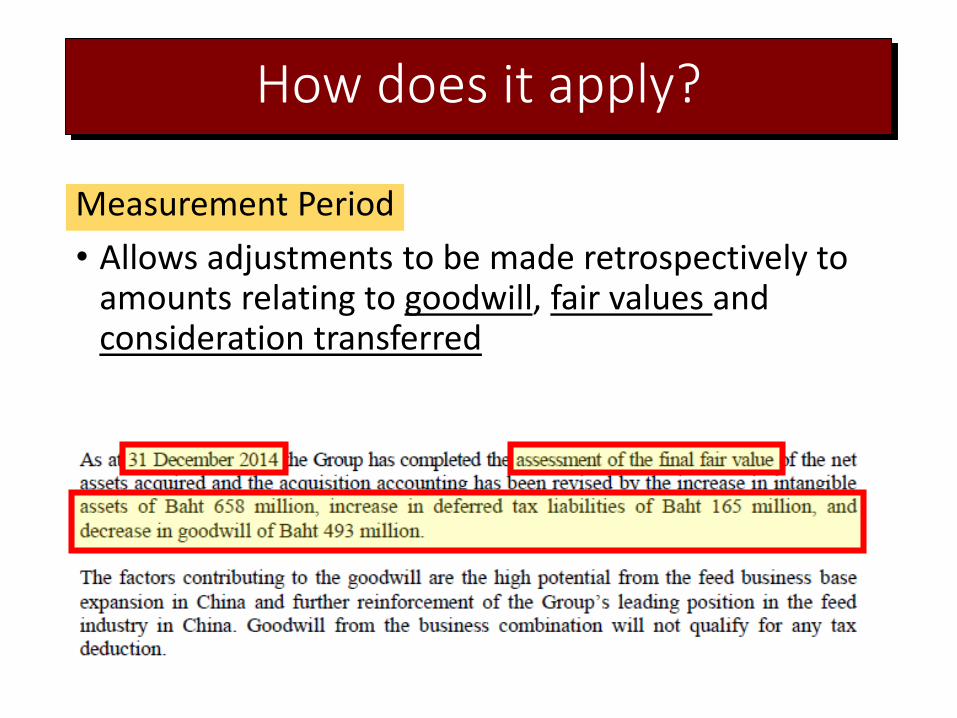

Measurement Period

• Allows adjustments to be made retrospectively to amounts relating to goodwill, fair values and consideration transferred

How does it apply?

Profit of Tops Food

Further Analysis

↑1,976

Thank You