Embed Size (px)

Citation preview

7TH ZAMBIA ECONOMIC BRIEF

22 June 2016

Dr. Gregory Smith

Macroeconomics & Fiscal Management Global Practice

BEATING THE SLOWDOWN:

MAKING EVERY KWACHA COUNT

DATA & INFORMATION FLOWS ARE BETTER

WBG ZAMBIA 2

“The availability of data has improved in 2016”

HUGE BODY OF KNOWLEDGE

WBG ZAMBIA 3

TOUGH CONDITIONS FOR GROWTH

WBG ZAMBIA 4

“Provisional estimates for 2015 from government suggest growth of 3.2%, a slowdown from the average of 7.4% between 2004 and 2014.”

WHAT DRIVES AND WHAT SLOWS GROWTH?

WBG ZAMBIA 5

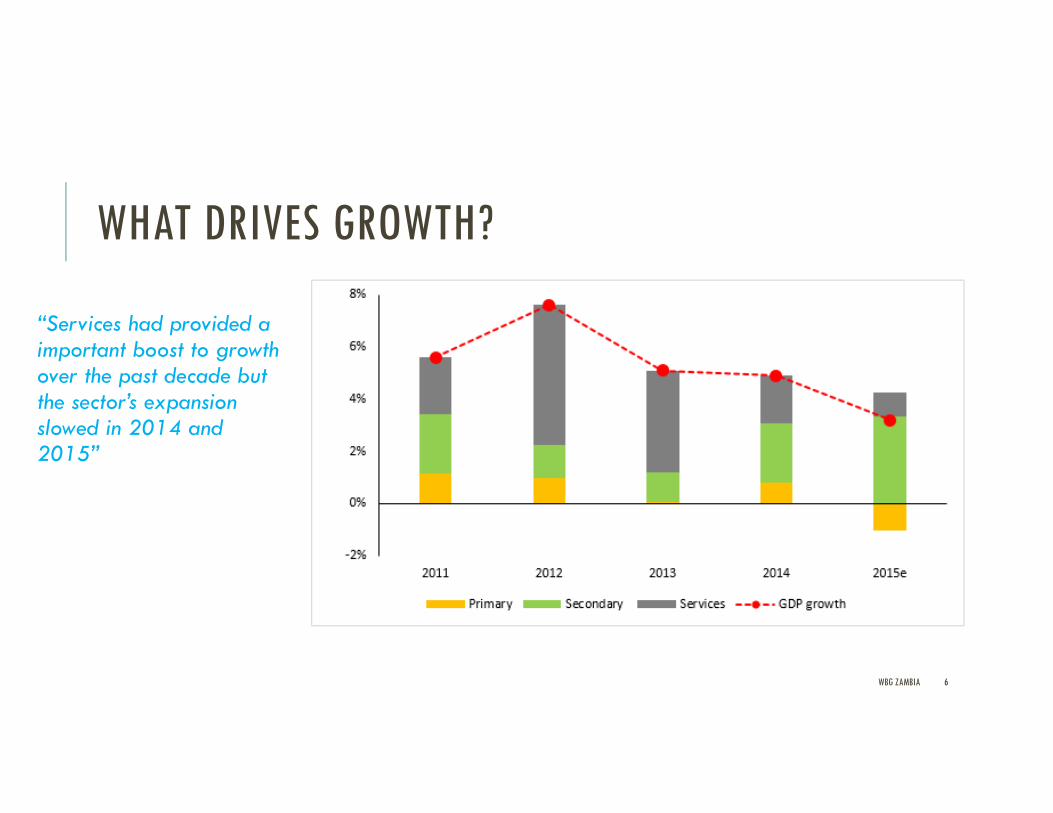

WHAT DRIVES GROWTH?

WBG ZAMBIA 6

“Services had provided a important boost to growth over the past decade but the sector’s expansion slowed in 2014 and 2015”

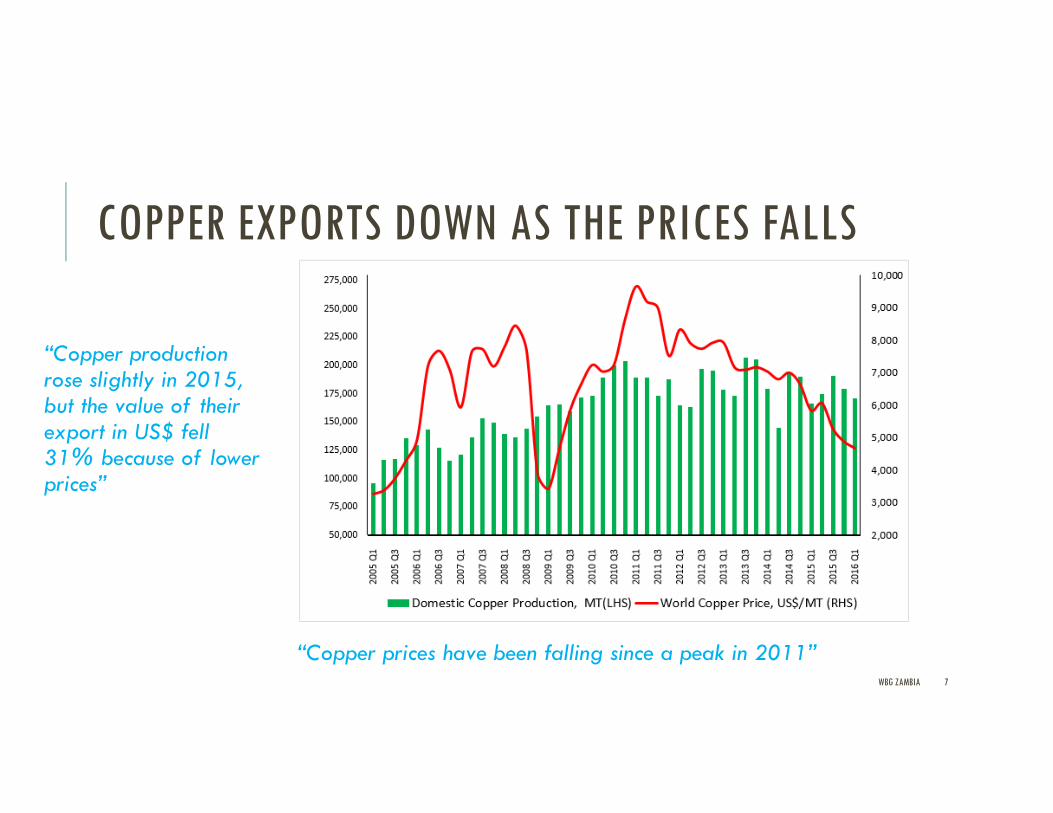

COPPER EXPORTS DOWN AS THE PRICES FALLS

WBG ZAMBIA 7

“Copper prices have been falling since a peak in 2011”

“Copper production rose slightly in 2015, but the value of their export in US$ fell 31% because of lower prices”

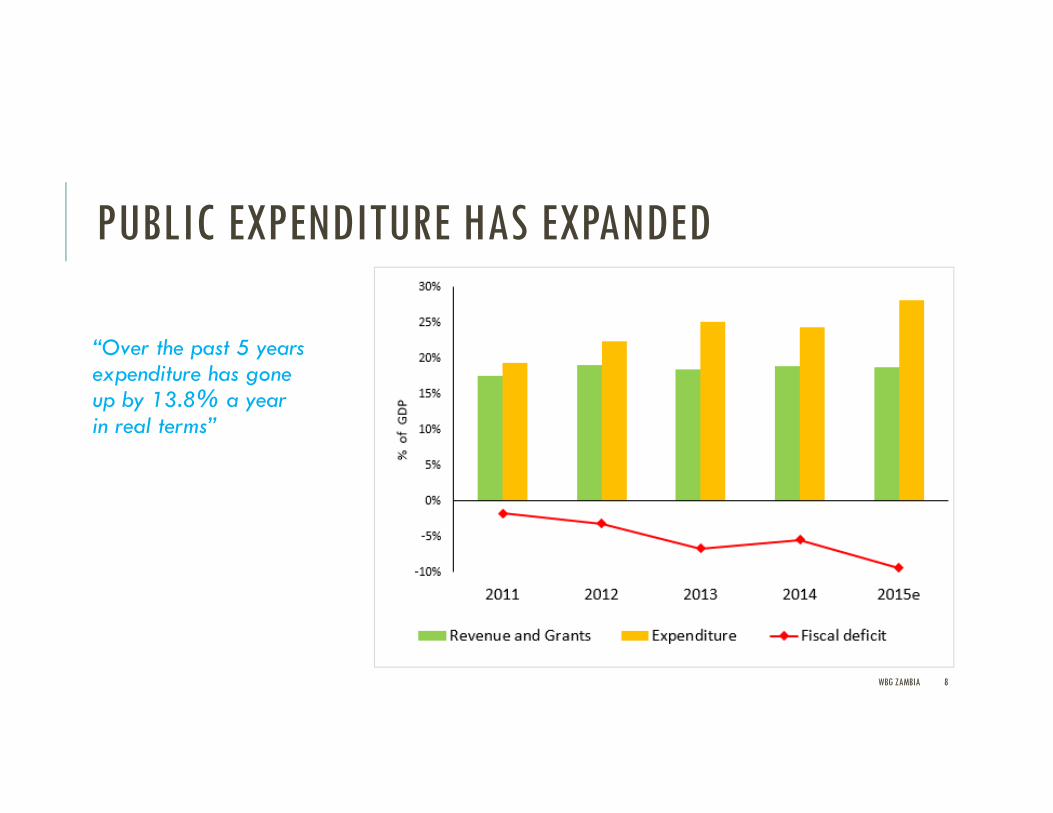

PUBLIC EXPENDITURE HAS EXPANDED

WBG ZAMBIA 8

“Over the past 5 years expenditure has gone up by 13.8% a year in real terms”

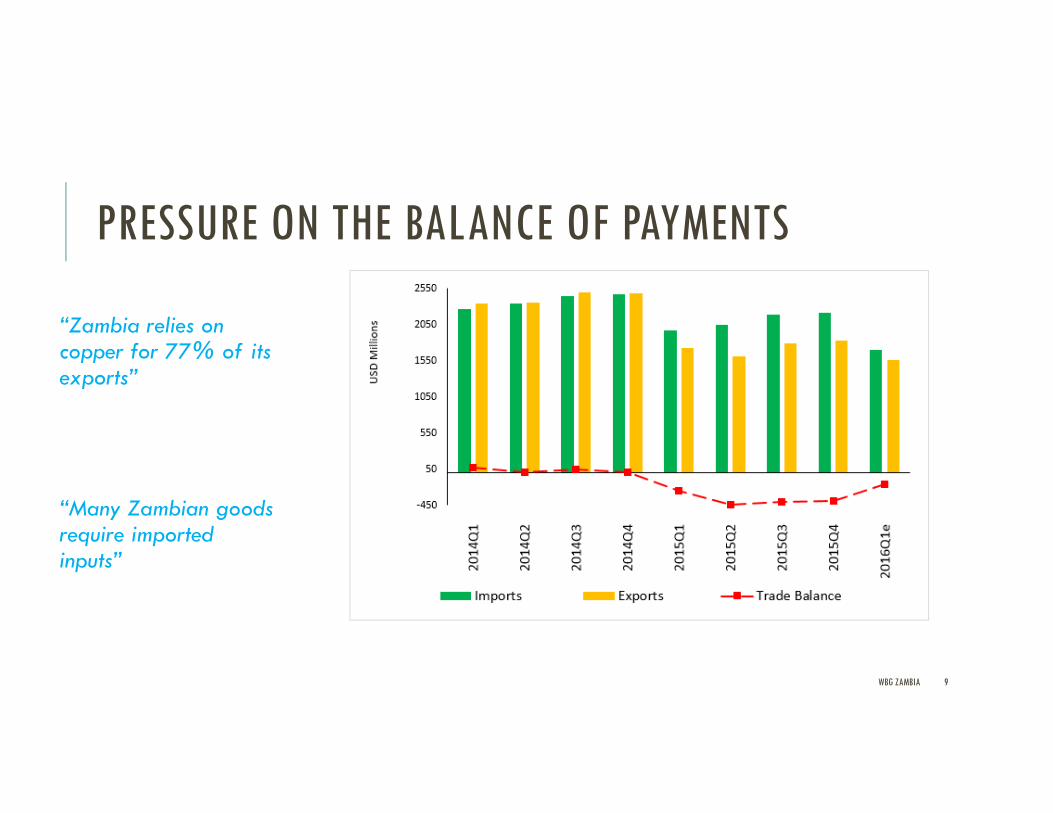

PRESSURE ON THE BALANCE OF PAYMENTS

WBG ZAMBIA 9

“Zambia relies on copper for 77% of its exports”

“Many Zambian goods require imported inputs”

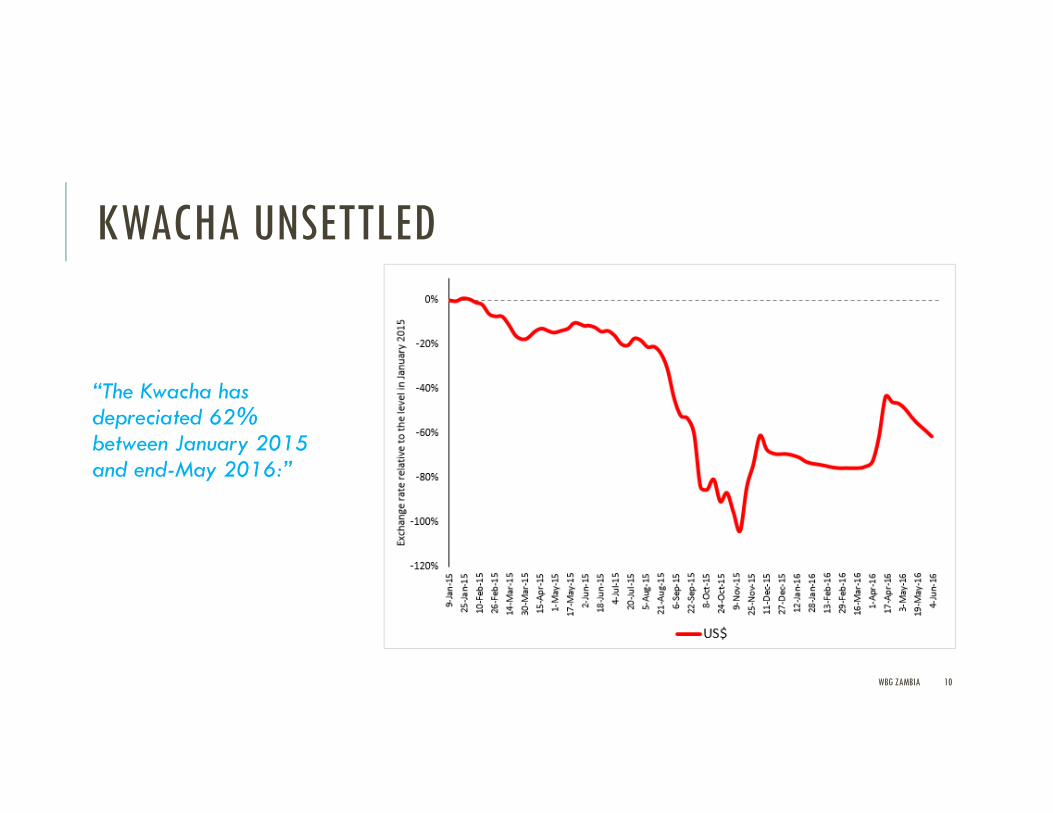

KWACHA UNSETTLED

WBG ZAMBIA 10

“The Kwacha has depreciated 62% between January 2015 and end-May 2016:”

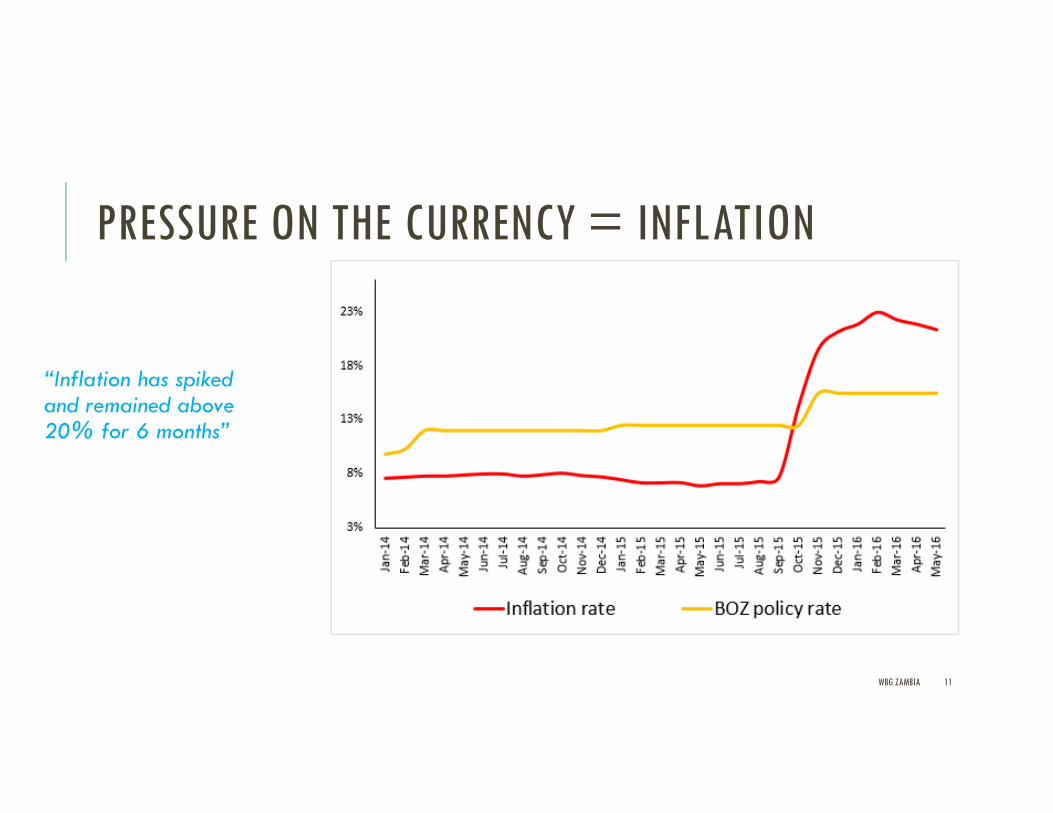

PRESSURE ON THE CURRENCY = INFLATION

WBG ZAMBIA 11

“Inflation has spiked and remained above 20% for 6 months”

FOOD PRICES HIT THE POOREST HARDEST

The CSO data April 2015 to April 2016:

•Roller mealie meal (+30%)

•Maize grain (+35%)

•Tomatoes (+114%)

•Onions (+38%)

•Dried beans (+30%)

•Sugar (+35%)

•Table salt (+37%)

•Hammer mill charges (+45%)

WBG ZAMBIA 12

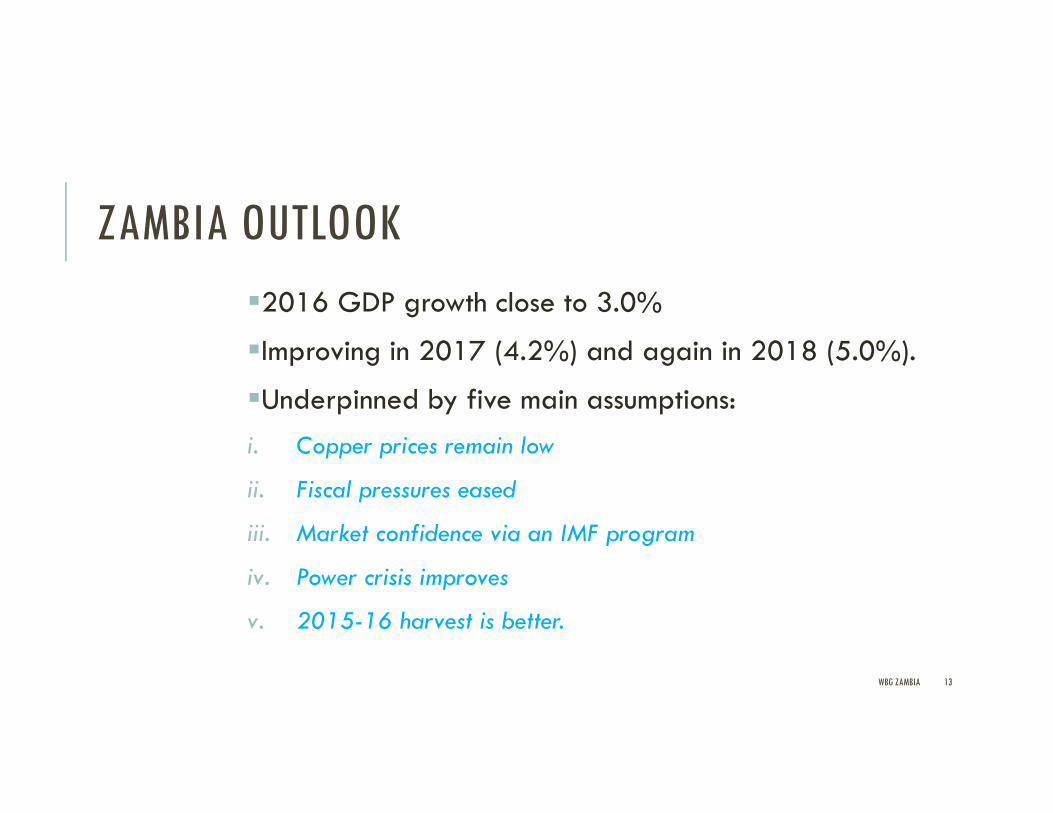

ZAMBIA OUTLOOK

�2016 GDP growth close to 3.0%

�Improving in 2017 (4.2%) and again in 2018 (5.0%).

�Underpinned by five main assumptions:

i. Copper prices remain low

ii. Fiscal pressures eased

iii. Market confidence via an IMF program

iv. Power crisis improves

v. 2015-16 harvest is better.

WBG ZAMBIA 13

LIVING CONDITIONS SURVEY 2015

WBG ZAMBIA 14

IDEAS FOR BEATING THE SLOWDOWN

WBG ZAMBIA 15

FUEL SUBSIDIES �Since December 2014, four price adjustments but no changes since July 2015despite kwacha depreciation.

�Savings from fuel subsidies are estimated at around US$36 million per month.

�A review of the current price setting mechanism is also a priority, as are efforts to fix underlying problems associated with the supply of fuel.

WBG ZAMBIA 16

POWER SECTOR FINANCIAL SUSTAINABILITY

�Power crisis has impacted on all sectors of the economy.

�Savings of US 26 million per month could be realized if the power crisis could be resolved.

�Wider reforms and investment will ensure sustainable supply in future.

WBG ZAMBIA 17

“A clear power strategy is needed, on tariffs and far beyond”.

CASH TRANSFER PROGRAMME

�Scaling-up the government’s Social Cash Transfer programme would be a crucial complement to any subsidy removal.

� There remains a need to provide better support to the poorest households.

WBG ZAMBIA 18

“There remains a need to protect the poor during a transition”

PUBLIC EXPENDITURE REVIEW

�A full review of what is being spent in key sectors can help ensure that every kwacha is put to productive use.

�By comparing objectives and past spending patterns, the allocation of expenditure can be improved

WBG ZAMBIA 19

“Lessons to boost the efficiency of spending can be found.”

THANK YOU

FOR LISTENING

WBG ZAMBIA 20

PLEASE DOWNLOAD

AND READ OUR

7TH ECONOMIC BRIEF