Embed Size (px)

Citation preview

Quan%ta%ve Finance in q/kdb+ Pricing Fixed Income Deriva%ves

Mark Lefevre Quan%ta%ve Analyst

Introduc%on

• q/kdb+ can be used for much more than lightning fast table manipula%on

• Excellent analy%cal capabili%es • Combining these strengths with 3rd-‐party soIware and/or linking with addi%onal libraries provides excep%onal opportuni%es to analyze, model and predict

Mo%va%on • q/kdb+ is oIen used in combina%on with MatLab and R for heavy

quan%ta%ve finance work • q/kdb+ integrates well with many foreign languages and

applica%ons – C, C#, Java, Python, Perl, Fortran, Scala – ODBC, GPUs (CUDA) – Matlab, R

• Moving algorithmic code into q/kdb+ is not always straighWorward – Out-‐of-‐the-‐box q/kdb+ lacks high-‐level sta%s%cs, op%miza%on, linear

algebra – Algorithmic code from other languages/environments usually was

developed with a different mindset • Let’s explore this topic by breaking in a dyadic manner

1. Mathema%cs Fundamentals/Numerical Analysis 2. Advanced, Prac%cal Applica%on: Pricing a Fixed Income Deriva%ve

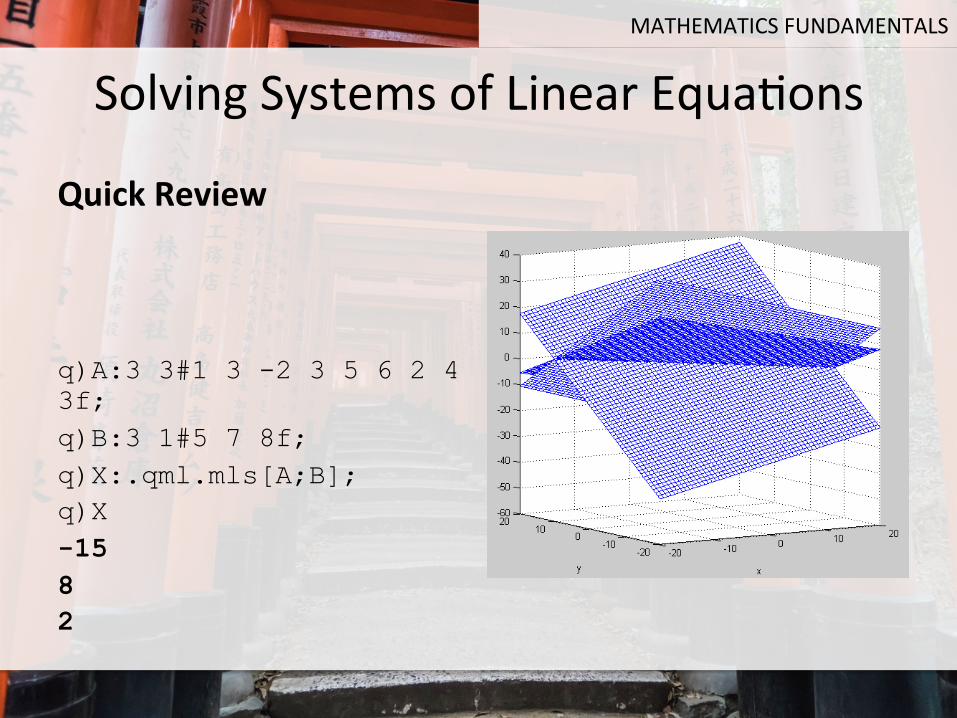

Solving Systems of Linear Equa%ons

Quick Review q)A:3 3#1 3 -2 3 5 6 2 4 3f; q)B:3 1#5 7 8f; q)X:.qml.mls[A;B]; q)X -15 8 2

MATHEMATICS FUNDAMENTALS

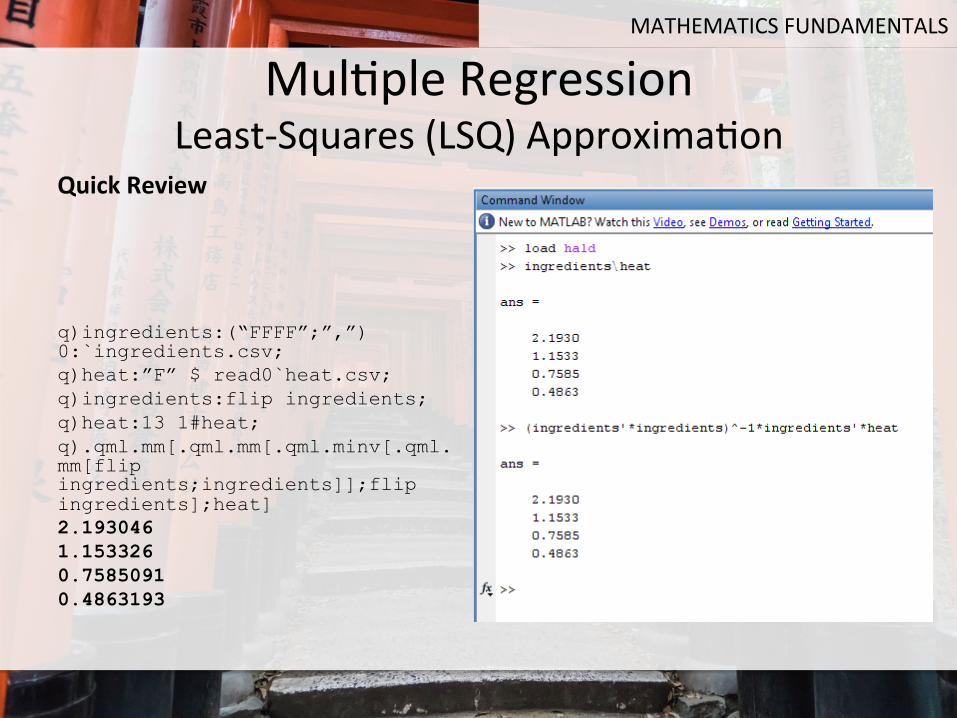

Mul%ple Regression Least-‐Squares (LSQ) Approxima%on

Quick Review q)ingredients:(“FFFF”;”,”) 0:`ingredients.csv; q)heat:”F” $ read0`heat.csv; q)ingredients:flip ingredients; q)heat:13 1#heat; q).qml.mm[.qml.mm[.qml.minv[.qml.mm[flip ingredients;ingredients]];flip ingredients];heat] 2.193046 1.153326 0.7585091 0.4863193

MATHEMATICS FUNDAMENTALS

Problema%c Linear Regression • One area of focus in Numerical Analysis is numerical stability

• We can demonstrate a numerical stability problem using a simple linear regression as an example

• Simple prac%cal example – Car loans regressed on year from U.S Fed Reserve

• References • R tutorial

hbp://www.cyclismo.org/tutorial/R/linearLeastSquares.html

MATHEMATICS FUNDAMENTALS

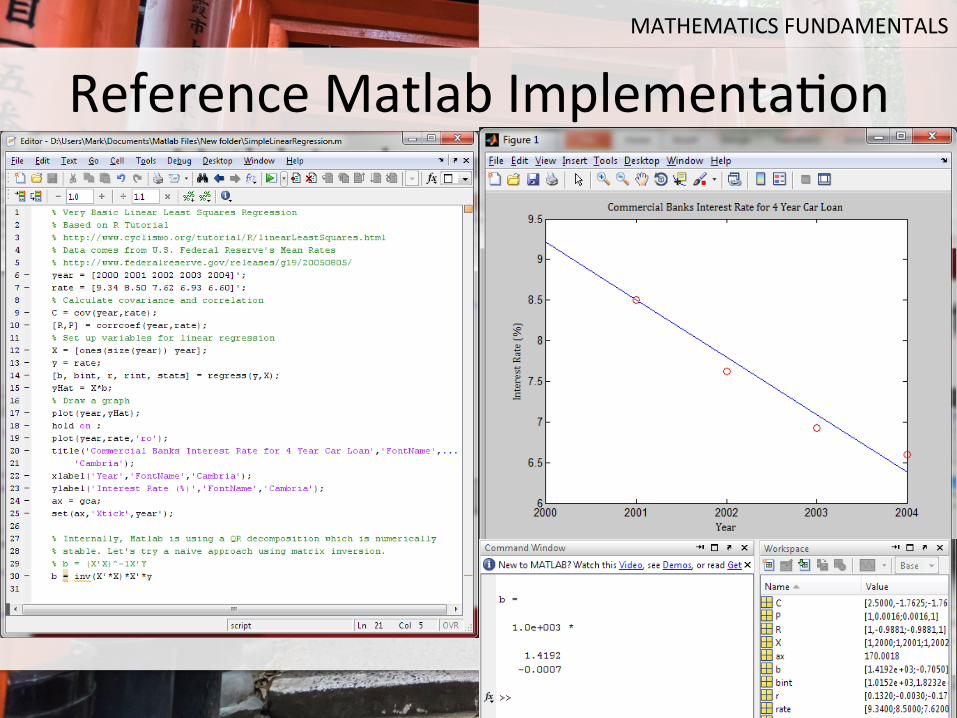

Reference Matlab Implementa%on MATHEMATICS FUNDAMENTALS

q/kdb+ Implementa%on

• Live Demonstra%on

MATHEMATICS FUNDAMENTALS

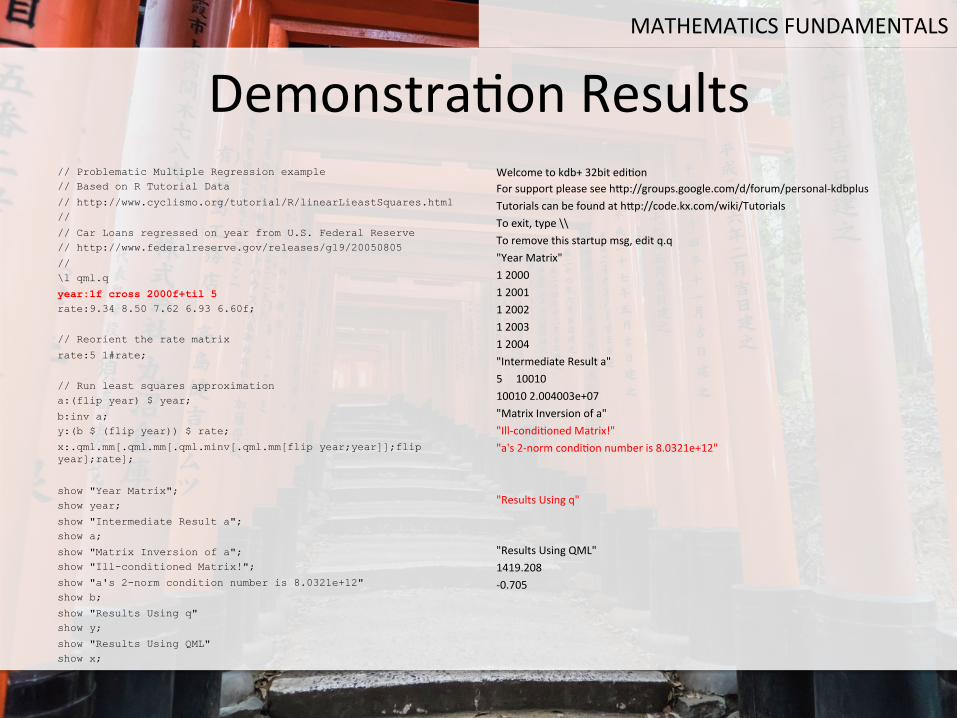

Demonstra%on Results // Problematic Multiple Regression example // Based on R Tutorial Data

// http://www.cyclismo.org/tutorial/R/linearLieastSquares.html //

// Car Loans regressed on year from U.S. Federal Reserve // http://www.federalreserve.gov/releases/g19/20050805

// \l qml.q

year:1f cross 2000f+til 5 rate:9.34 8.50 7.62 6.93 6.60f;

// Reorient the rate matrix

rate:5 1#rate;

// Run least squares approximation a:(flip year) $ year;

b:inv a; y:(b $ (flip year)) $ rate;

x:.qml.mm[.qml.mm[.qml.minv[.qml.mm[flip year;year]];flip year];rate];

show "Year Matrix"; show year;

show "Intermediate Result a"; show a;

show "Matrix Inversion of a"; show "Ill-conditioned Matrix!";

show "a's 2-norm condition number is 8.0321e+12" show b;

show "Results Using q" show y;

show "Results Using QML" show x;

Welcome to kdb+ 32bit edi%on For support please see hbp://groups.google.com/d/forum/personal-‐kdbplus Tutorials can be found at hbp://code.kx.com/wiki/Tutorials To exit, type \\ To remove this startup msg, edit q.q "Year Matrix" 1 2000 1 2001 1 2002 1 2003 1 2004 "Intermediate Result a" 5 10010 10010 2.004003e+07 "Matrix Inversion of a" "Ill-‐condi%oned Matrix!" "a's 2-‐norm condi%on number is 8.0321e+12" "Results Using q" "Results Using QML" 1419.208 -‐0.705

MATHEMATICS FUNDAMENTALS

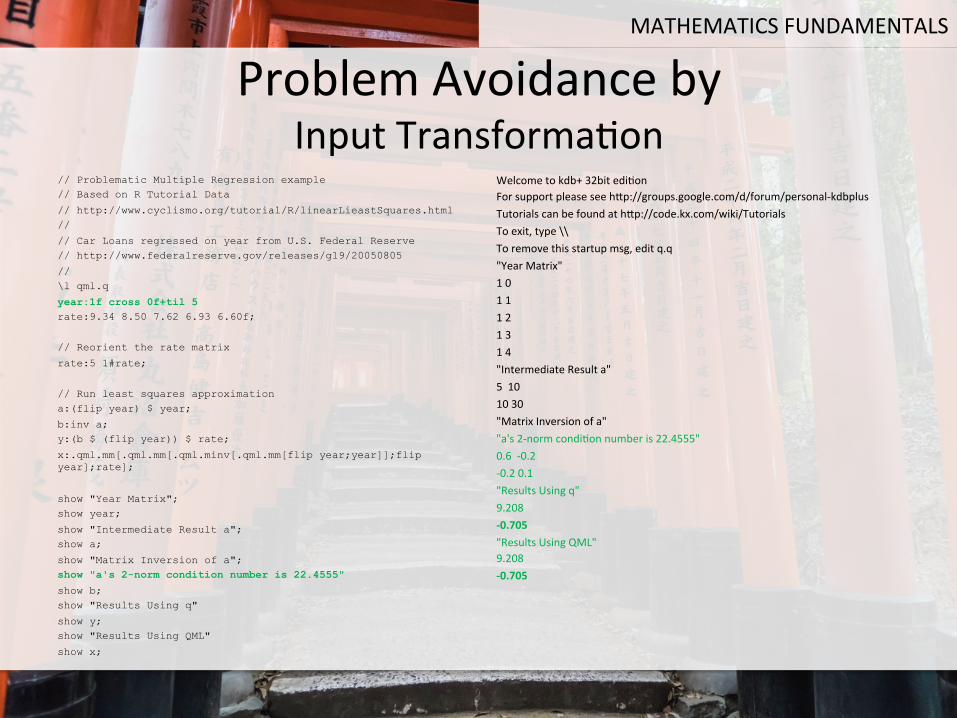

Problem Avoidance by Input Transforma%on

// Problematic Multiple Regression example // Based on R Tutorial Data

// http://www.cyclismo.org/tutorial/R/linearLieastSquares.html //

// Car Loans regressed on year from U.S. Federal Reserve // http://www.federalreserve.gov/releases/g19/20050805

// \l qml.q

year:1f cross 0f+til 5 rate:9.34 8.50 7.62 6.93 6.60f;

// Reorient the rate matrix

rate:5 1#rate;

// Run least squares approximation a:(flip year) $ year;

b:inv a; y:(b $ (flip year)) $ rate;

x:.qml.mm[.qml.mm[.qml.minv[.qml.mm[flip year;year]];flip year];rate];

show "Year Matrix"; show year;

show "Intermediate Result a"; show a;

show "Matrix Inversion of a"; show "a's 2-norm condition number is 22.4555"

show b; show "Results Using q"

show y; show "Results Using QML"

show x;

Welcome to kdb+ 32bit edi%on For support please see hbp://groups.google.com/d/forum/personal-‐kdbplus Tutorials can be found at hbp://code.kx.com/wiki/Tutorials To exit, type \\ To remove this startup msg, edit q.q "Year Matrix" 1 0 1 1 1 2 1 3 1 4 "Intermediate Result a" 5 10 10 30 "Matrix Inversion of a" "a's 2-‐norm condi%on number is 22.4555" 0.6 -‐0.2 -‐0.2 0.1 "Results Using q" 9.208 -‐0.705 "Results Using QML" 9.208 -‐0.705

MATHEMATICS FUNDAMENTALS

Q Math Library • qml is a free library for q/kdb+ that links into various

numerical libraries including LAPACK – Linear algebra – Sta%s%cs – Op%miza%on

• Compiling qml with 32-‐bit q/kdb+ on a 64-‐bit machine requires pa%ence and the correct compilers, but works – LAPACK is wriben in Fortran 90, so you will need a Fortran compiler, as

well as the usual suspects

References LAPACK http://www.netlib.org/lapack/ qml http://althenia.net/qml

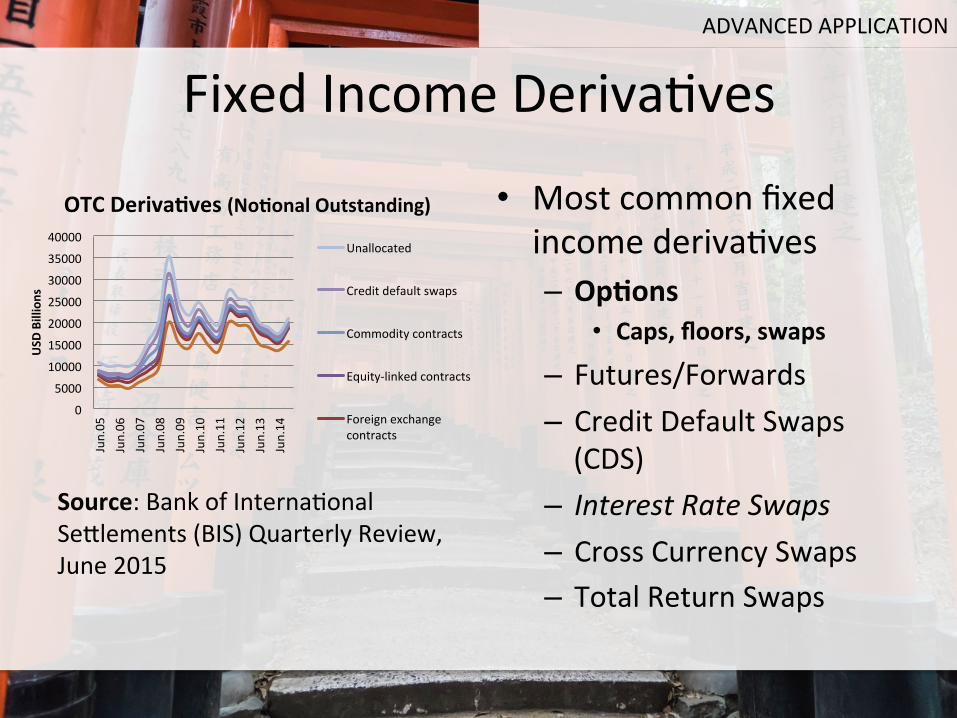

Fixed Income Deriva%ves

Source: Bank of Interna%onal Seblements (BIS) Quarterly Review, June 2015

• Most common fixed income deriva%ves – Op5ons

• Caps, floors, swaps – Futures/Forwards – Credit Default Swaps (CDS)

– Interest Rate Swaps – Cross Currency Swaps – Total Return Swaps

0

5000

10000

15000

20000

25000

30000

35000

40000

Jun.05

Jun.06

Jun.07

Jun.08

Jun.09

Jun.10

Jun.11

Jun.12

Jun.13

Jun.14

USD

Billions

OTC Deriva5ves (No5onal Outstanding)

Unallocated

Credit default swaps

Commodity contracts

Equity-‐linked contracts

Foreign exchange contracts

ADVANCED APPLICATION

Pricing Caps and Caplets

• A cap is an op%on on an underlying floa%ng interest rate, such as LIBOR, that provides investors with a hedge against the interest rate rising above the cap rate

• The cap is composed of individual caplets

• If the interest rate is above the strike, the caplet is in-‐the-‐money

• Rate set at %me t • Payoff at %me t+1 • Present Value

max( 𝑟↓𝑡 −𝑘,0)×𝜏×𝑁

𝐷𝐹↓𝑂𝐼𝑆 ↓𝑡+1 ×max( 𝑟↓𝑡 −𝑘,0)×𝜏×𝑁

ADVANCED APPLICATION

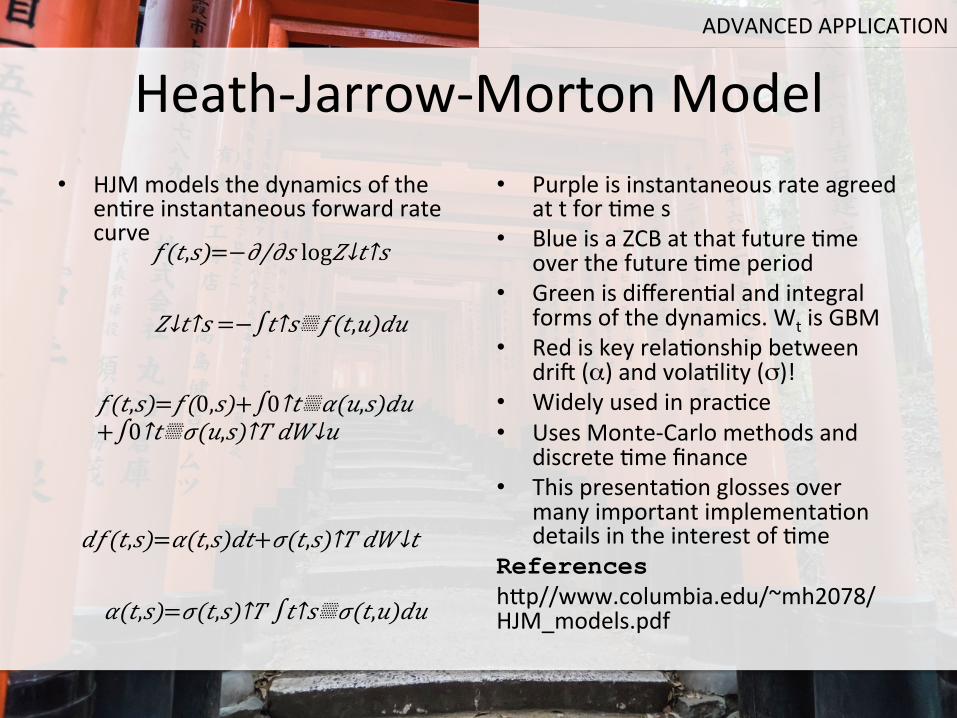

Heath-‐Jarrow-‐Morton Model • HJM models the dynamics of the

en%re instantaneous forward rate curve

• Purple is instantaneous rate agreed at t for %me s

• Blue is a ZCB at that future %me over the future %me period

• Green is differen%al and integral forms of the dynamics. Wt is GBM

• Red is key rela%onship between driI (α) and vola%lity (σ)!

• Widely used in prac%ce • Uses Monte-‐Carlo methods and

discrete %me finance • This presenta%on glosses over

many important implementa%on details in the interest of %me

References hbp//www.columbia.edu/~mh2078/HJM_models.pdf

𝑓(𝑡,𝑠)=− 𝜕/𝜕𝑠 log 𝑍↓𝑡↑𝑠

𝑍↓𝑡↑𝑠 =−∫𝑡↑𝑠▒𝑓(𝑡,𝑢)𝑑𝑢

𝑑𝑓(𝑡,𝑠)=𝛼(𝑡,𝑠)𝑑𝑡+𝜎(𝑡,𝑠)↑𝑇 𝑑𝑊↓𝑡

𝛼(𝑡,𝑠)=𝜎(𝑡,𝑠)↑𝑇 ∫𝑡↑𝑠▒𝜎(𝑡,𝑢)𝑑𝑢

𝑓(𝑡,𝑠)=𝑓(0,𝑠)+∫0↑𝑡▒𝛼(𝑢,𝑠)𝑑𝑢 +∫0↑𝑡▒𝜎(𝑢,𝑠)↑𝑇 𝑑𝑊↓𝑢

ADVANCED APPLICATION

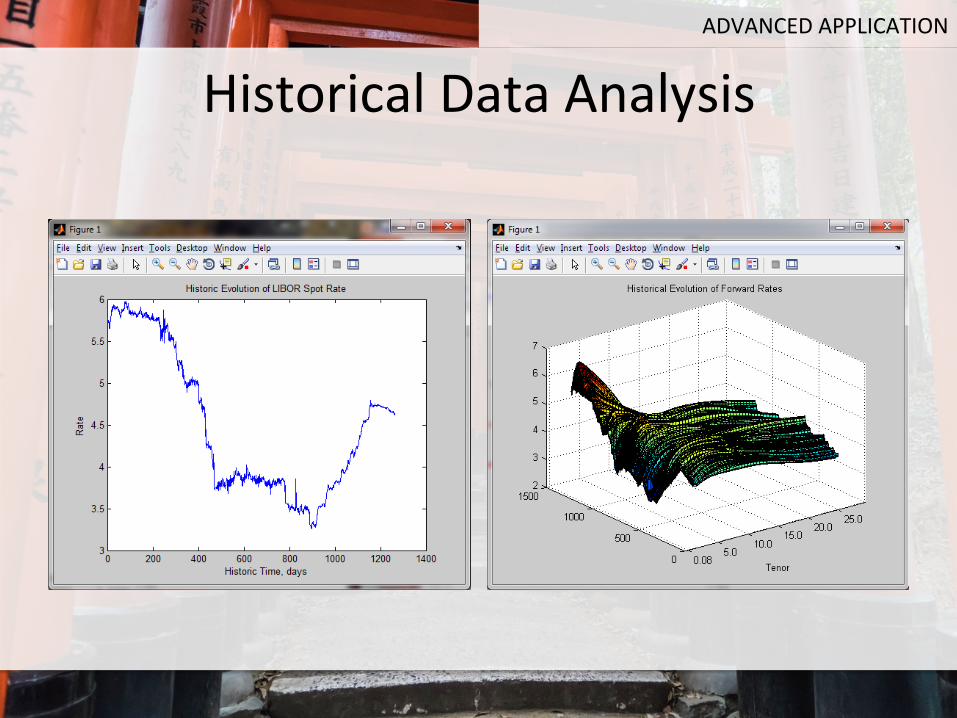

Historical Data Analysis ADVANCED APPLICATION

Principal Component Analysis (PCA)

• PCA is a sta%s%cal procedure that u%lizes orthogonal transforma%ons to convert a set of observa%ons of possibly correlated variables into a set of values of linearly uncorrelated variables called principal components.

• In a word, decorrela(on • The principal components are

the eigenvectors of a symmetric variance-‐covariance matrix

• Eigenvectors are ordered by their corresponding eigenvalues, which is also the amount of variance explained by the component

• If we take just a few of the first principal components, we can achieve – dimensionality reduc5on – work in linear parameter

space • This is very useful for

simula%ng high dimensionality problems, such as instantaneous forward curve evolu%ons

ADVANCED APPLICATION

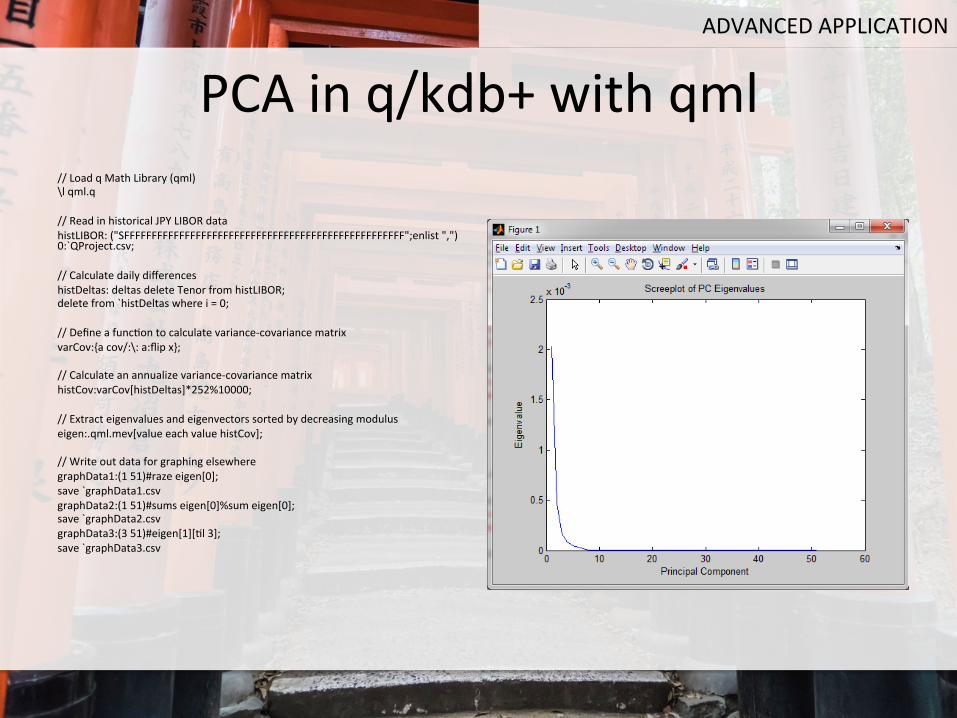

PCA in q/kdb+ with qml // Load q Math Library (qml) \l qml.q // Read in historical JPY LIBOR data histLIBOR: ("SFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFFF";enlist ",") 0:`QProject.csv; // Calculate daily differences histDeltas: deltas delete Tenor from histLIBOR; delete from `histDeltas where i = 0; // Define a func%on to calculate variance-‐covariance matrix varCov:{a cov/:\: a:flip x}; // Calculate an annualize variance-‐covariance matrix histCov:varCov[histDeltas]*252%10000; // Extract eigenvalues and eigenvectors sorted by decreasing modulus eigen:.qml.mev[value each value histCov]; // Write out data for graphing elsewhere graphData1:(1 51)#raze eigen[0]; save `graphData1.csv graphData2:(1 51)#sums eigen[0]%sum eigen[0]; save `graphData2.csv graphData3:(3 51)#eigen[1][%l 3]; save `graphData3.csv

ADVANCED APPLICATION

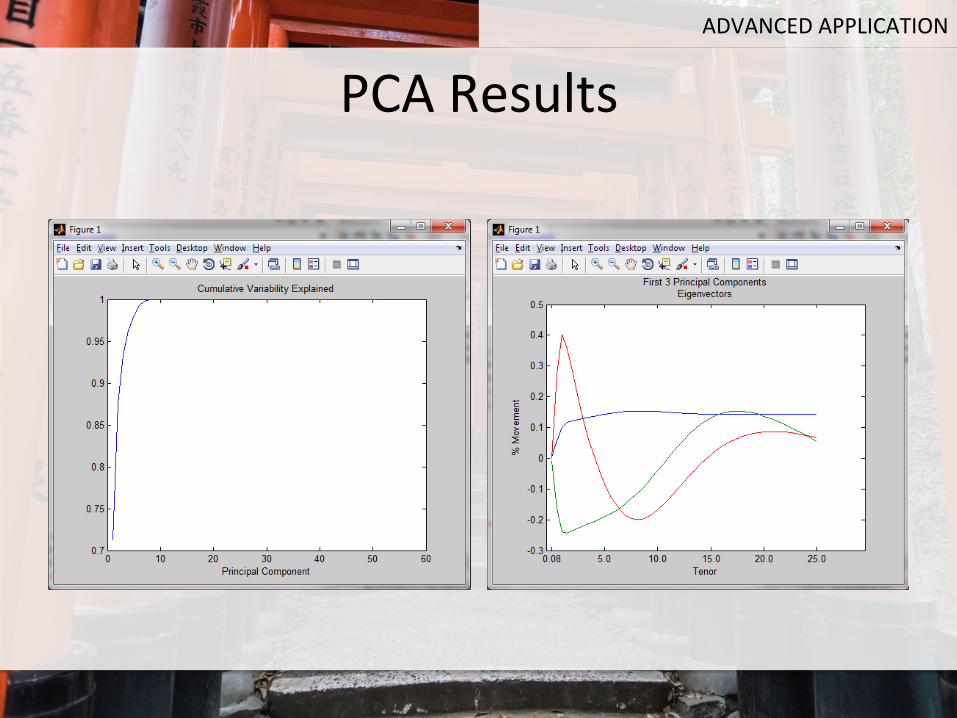

PCA Results ADVANCED APPLICATION

Vola%lity Fi�ng • In a mul%-‐factor HJM

framework, we need to integrate over vola%lity func%ons of a form like

• What this means in

English, is we have several eigenvalue /eigenvector func%ons driving the dynamics at par%cular tenors

• Consistent with Musiela parameteriza%on

• This permits a rich evolu%on of forward rates exhibi%ng – Level shiIs – Twists – Buberfly-‐like inflec%on about specific tenors

• Subject to regimes

ADVANCED APPLICATION

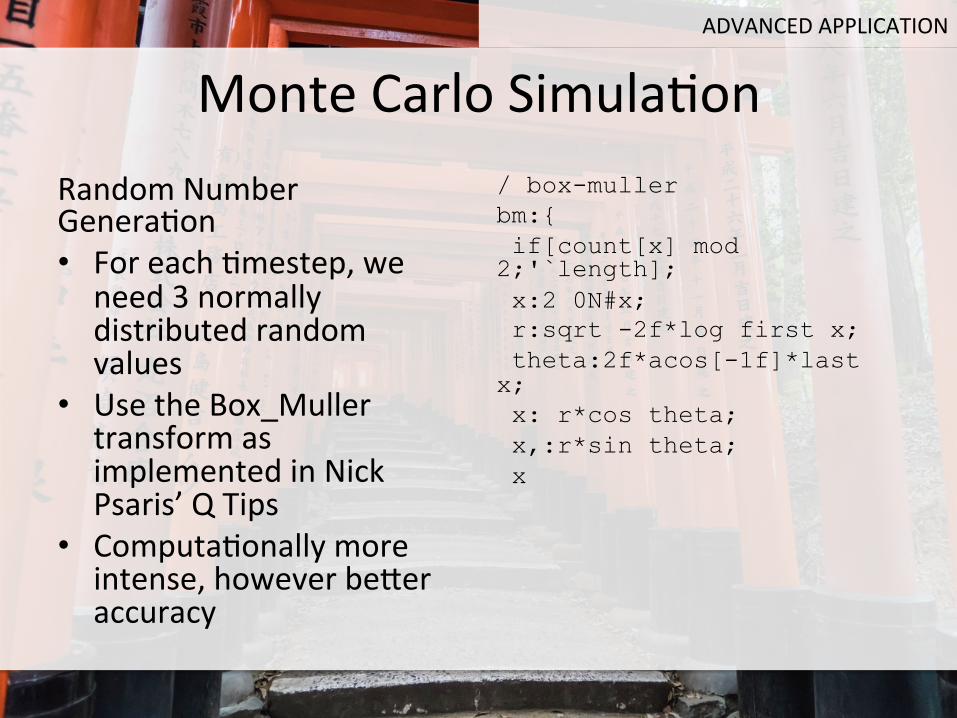

Monte Carlo Simula%on Random Number Genera%on • For each %mestep, we

need 3 normally distributed random values

• Use the Box_Muller transform as implemented in Nick Psaris’ Q Tips

• Computa%onally more intense, however beber accuracy

/ box-muller bm:{ if[count[x] mod 2;'`length]; x:2 0N#x; r:sqrt -2f*log first x; theta:2f*acos[-1f]*last x; x: r*cos theta; x,:r*sin theta; x

ADVANCED APPLICATION

Pricing

• Live Demonstra%on

ADVANCED APPLICATION

Conclusion

• q/kdb+ can be used for much more than table manipula%on

• Demonstrated some basic mathema%cs and an advanced, prac%cal applica%on to pricing caplets

• Used 3rd-‐party soIware for visualiza%on, however the new HTML5 capabili%es hold lots of promise

• Linked to and leveraged industrial-‐strength mathema%cs libraries

• Hopefully, this has provide a glimpse at the excep%onal opportuni%es to analyze, model and predict that q/kdb+ can provide

About Me • Mark is currently consul%ng at one of the largest banks in Tokyo as a quan%ta%ve

analyst developing high-‐performance algorithmic trading systems on the e-‐FX desk. Prior to moving to Japan, he worked in London for Unicredit on the Equity-‐Linked Origina%on desk crea%ng conver%ble bonds for European corporates, consulted in the US on e-‐commerce analy%cs and worked for several high-‐tech soIware companies.

• Earlier in his career, he worked for Mitsubishi Semiconductor America designing semiconductors and a startup developing a DSP. He then moved into applica%ons engineering for an Electronic Design Automa%on (EDA) company and, subsequently, internet soIware companies in CA and Europe.

• Mark has a bachelors degree in Electrical Engineering and Computer Science from Duke University, a masters degree in Computer Engineering from North Carolina State University and an MBA in Quan%ta%ve Finance from the Wharton School of Business. He recently completed a Cer%ficate in Quan%ta%ve Finance (CQF).

• He dreams of the day when he can create soIware without encountering a single type error