Embed Size (px)

Citation preview

Network Connectivity,

Systematic Risk and

Diversification

SYstemic Risk TOmography:

Signals, Measurements, Transmission Channels, and Policy Interventions

Monica Billio, University Ca' Foscari Venezia (Italy) Massimiliano Caporin, University of Padova (Italy) Roberto Panzica Goethe University Frankfurt (Germany) Loriana Pelizzon University Ca' Foscari Venezia (Italy) and Goethe University Frankfurt (Germany) CSRA research meeting – December, 15 2014

Network Connectivity, Systematic Risk andDiversification

Monica Billio1 Massimiliano Caporin2

Roberto Panzica3 Loriana Pelizzon1,3

1University Ca’ Foscari Venezia (Italy)

2University of Padova (Italy)

3Goethe University Frankfurt (Germany)

CSRA, December, 2014

Billio, Caporin, Panzica and Pelizzon N&S December, 2014 1 / 18

Research questions

Introduction

There is a general agreement on the traditional decomposition of an asset(portfolio) total risk into systematic and idiosyncratic components followingthe CAPM model

Systematic risks comes from the dependence of returns on common factors

Idiosyncratic risks are asset-specific

But...

There is also a recent consensus on the existence of systemic risks

Billio, Caporin, Panzica and Pelizzon N&S December, 2014 2 / 18

Research questions

Introduction

Systemic risk definition: any set of circumstances that threatens the stabilityof, or public confidence in, the financial system

Systemic risk is a function of a system

Systemic risk arises endogenously from a system

Systemic risk is a function of connections between and the structure offinancial institutions or, more generally, between the companies and/oreconomic sectors

Billio, Caporin, Panzica and Pelizzon N&S December, 2014 3 / 18

Research questions

(Challenging) Research questions

What is the impact of network connectivity on the asset return loadingto common systematic factors?

Does network connectivity endanger the power of diversification?

Billio, Caporin, Panzica and Pelizzon N&S December, 2014 4 / 18

Literature review

Measuring systemic links

An increasing literature in economics investigates the role of interconnectionsbetween different firms and sectors, functioning as a potential propagationmechanism of idiosyncratic shocks throughout the economy.

Canonical idea: Lucas (1977), among others, that states that suchmicroeconomic shocks would average out and thus, would only havenegligible aggregate effects. Similarly, these shocks would have little impacton asset prices.

However:

Acemoglou et al. (2011) use network structure to show the possibility thataggregate fluctuations may originate from microeconomic shocks to firms.Such a possibility is discarded in standard macroeconomics models due to a“diversification argument”.

Shock propagation in static networks Horvath (1998, 2000), Dupor (1999),Shea (2002), and Acemoglu, Carvalho, Ozdaglar, and Tahbaz-Salehi (2011).

Billio, Caporin, Panzica and Pelizzon N&S December, 2014 5 / 18

Literature review

Pricing and diversification in multifactor models

General multi-factor model for a k−dimensional vector of risky assets (m riskfactors)

Rt = E [Rt ] + BFt + εt (1)

Under equilibrium expected returns depend on the factor risk premiums Λ

E [Rt ] = rf + BΛ (2)

Standard total risk decomposition

VAR [Rt ] = BVAR [Ft ]B′ + VAR [εt ] (3)

ΣR = BΣFB′ + Ω (4)

Billio, Caporin, Panzica and Pelizzon N&S December, 2014 6 / 18

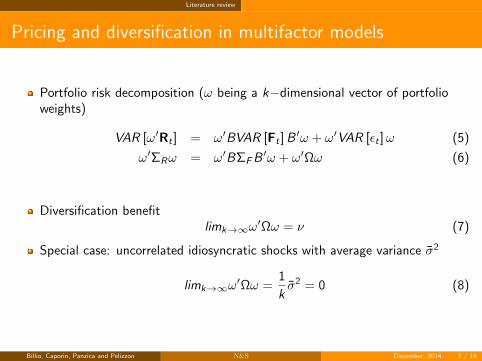

Literature review

Pricing and diversification in multifactor models

Portfolio risk decomposition (ω being a k−dimensional vector of portfolioweights)

VAR [ω′Rt ] = ω′BVAR [Ft ]B′ω + ω′VAR [εt ]ω (5)

ω′ΣRω = ω′BΣFB′ω + ω′Ωω (6)

Diversification benefitlimk→∞ω

′Ωω = ν (7)

Special case: uncorrelated idiosyncratic shocks with average variance σ2

limk→∞ω′Ωω =

1

kσ2 = 0 (8)

Billio, Caporin, Panzica and Pelizzon N&S December, 2014 7 / 18

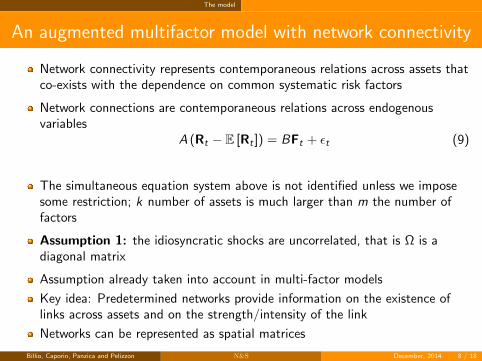

The model

An augmented multifactor model with network connectivity

Network connectivity represents contemporaneous relations across assets thatco-exists with the dependence on common systematic risk factors

Network connections are contemporaneous relations across endogenousvariables

A (Rt − E [Rt ]) = BFt + εt (9)

The simultaneous equation system above is not identified unless we imposesome restriction; k number of assets is much larger than m the number offactors

Assumption 1: the idiosyncratic shocks are uncorrelated, that is Ω is adiagonal matrix

Assumption already taken into account in multi-factor models

Key idea: Predetermined networks provide information on the existence oflinks across assets and on the strength/intensity of the link

Networks can be represented as spatial matrices

Billio, Caporin, Panzica and Pelizzon N&S December, 2014 8 / 18

The model

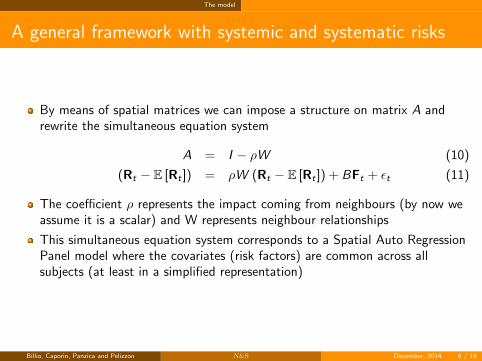

A general framework with systemic and systematic risks

By means of spatial matrices we can impose a structure on matrix A andrewrite the simultaneous equation system

A = I − ρW (10)

(Rt − E [Rt ]) = ρW (Rt − E [Rt ]) + BFt + εt (11)

The coefficient ρ represents the impact coming from neighbours (by now weassume it is a scalar) and W represents neighbour relationships

This simultaneous equation system corresponds to a Spatial Auto RegressionPanel model where the covariates (risk factors) are common across allsubjects (at least in a simplified representation)

Billio, Caporin, Panzica and Pelizzon N&S December, 2014 9 / 18

The model

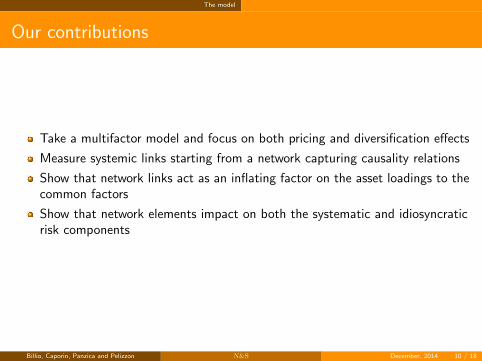

Our contributions

Take a multifactor model and focus on both pricing and diversification effects

Measure systemic links starting from a network capturing causality relations

Show that network links act as an inflating factor on the asset loadings to thecommon factors

Show that network elements impact on both the systematic and idiosyncraticrisk components

Billio, Caporin, Panzica and Pelizzon N&S December, 2014 10 / 18

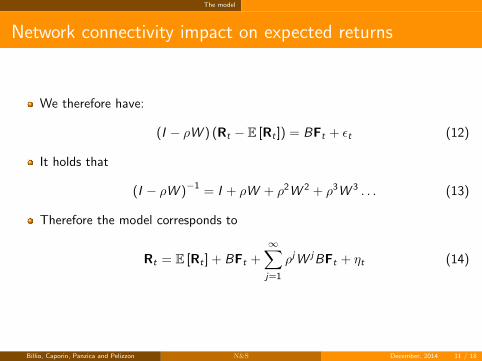

The model

Network connectivity impact on expected returns

We therefore have:

(I − ρW ) (Rt − E [Rt ]) = BFt + εt (12)

It holds that

(I − ρW )−1 = I + ρW + ρ2W 2 + ρ3W 3 . . . (13)

Therefore the model corresponds to

Rt = E [Rt ] + BFt +∞∑j=1

ρjW jBFt + ηt (14)

Billio, Caporin, Panzica and Pelizzon N&S December, 2014 11 / 18

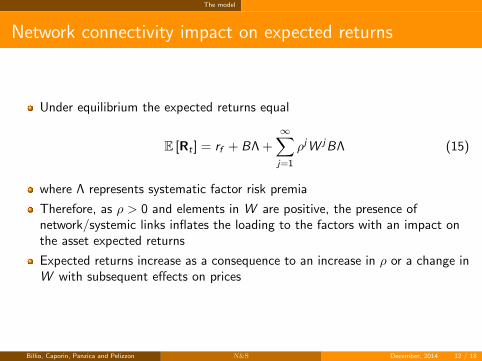

The model

Network connectivity impact on expected returns

Under equilibrium the expected returns equal

E [Rt ] = rf + BΛ +∞∑j=1

ρjW jBΛ (15)

where Λ represents systematic factor risk premia

Therefore, as ρ > 0 and elements in W are positive, the presence ofnetwork/systemic links inflates the loading to the factors with an impact onthe asset expected returns

Expected returns increase as a consequence to an increase in ρ or a change inW with subsequent effects on prices

Billio, Caporin, Panzica and Pelizzon N&S December, 2014 12 / 18

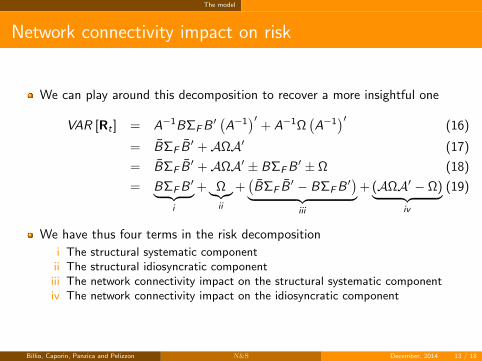

The model

Network connectivity impact on risk

We can play around this decomposition to recover a more insightful one

VAR [Rt ] = A−1BΣFB′ (A−1)′ + A−1Ω

(A−1

)′(16)

= BΣF B′ +AΩA′ (17)

= BΣF B′ +AΩA′ ± BΣFB

′ ± Ω (18)

= BΣFB′︸ ︷︷ ︸

i

+ Ω︸︷︷︸ii

+(BΣF B

′ − BΣFB′)︸ ︷︷ ︸

iii

+ (AΩA′ − Ω)︸ ︷︷ ︸iv

(19)

We have thus four terms in the risk decomposition

i The structural systematic componentii The structural idiosyncratic componentiii The network connectivity impact on the structural systematic componentiv The network connectivity impact on the idiosyncratic component

Billio, Caporin, Panzica and Pelizzon N&S December, 2014 13 / 18

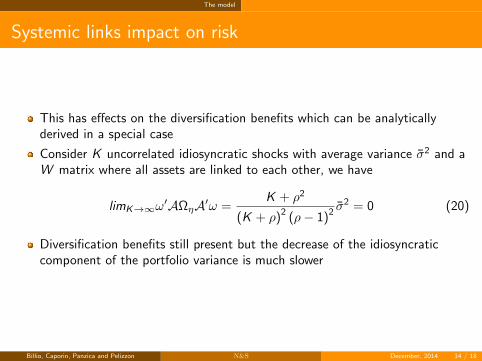

The model

Systemic links impact on risk

This has effects on the diversification benefits which can be analyticallyderived in a special case

Consider K uncorrelated idiosyncratic shocks with average variance σ2 and aW matrix where all assets are linked to each other, we have

limK→∞ω′AΩηA′ω =

K + ρ2

(K + ρ)2 (ρ− 1)2σ2 = 0 (20)

Diversification benefits still present but the decrease of the idiosyncraticcomponent of the portfolio variance is much slower

Billio, Caporin, Panzica and Pelizzon N&S December, 2014 14 / 18

The model

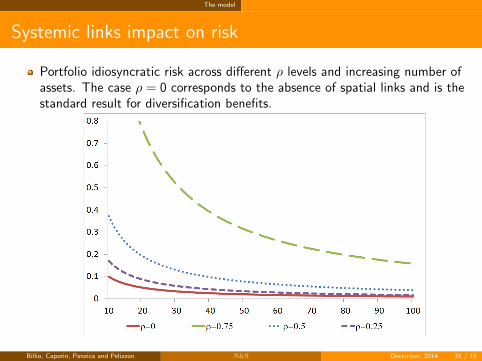

Systemic links impact on risk

Portfolio idiosyncratic risk across different ρ levels and increasing number ofassets. The case ρ = 0 corresponds to the absence of spatial links and is thestandard result for diversification benefits.

Billio, Caporin, Panzica and Pelizzon N&S December, 2014 15 / 18

The model

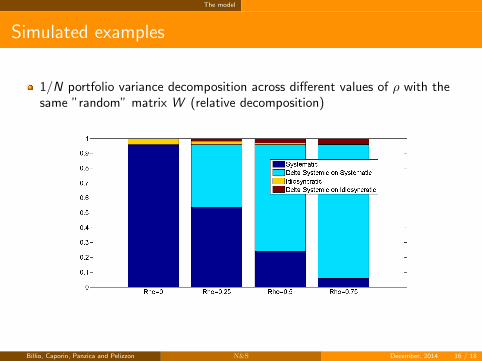

Simulated examples

1/N portfolio variance decomposition across different values of ρ with thesame ”random” matrix W (relative decomposition)

Billio, Caporin, Panzica and Pelizzon N&S December, 2014 16 / 18

The model

Future developments

Generalize the model in four directions

First by adding heterogeneity to the asset reaction to the systemic links

A = I −RW (21)

R = diag (ρ1, ρ2, . . . , ρN) (22)

Second, by allowing for a time-variation in the W matrix

A⇒ At = I −RWg(t) (23)

In this way the matrices Wg(t) capture the dynamic in the links across assets(the evolution of the newtork), while the spatial coefficients included in Rrepresent the impact on each asset of the neighbours, and are assumed to betime-independent

The Wg(t) matrices are also assumed to be known at time t and thus wecondition the model estimation and the analysis to their availability

Billio, Caporin, Panzica and Pelizzon N&S December, 2014 17 / 18

The model

Future developments

We assume the evolution of Wg(t) is smooth or acts at a time scale muchlower than that affecting the evolution of asset returns (i.e. for monthlyreturns the W change with, say, a yearly frequency); to highlight this aspectwe index the spatial links matrices to a function of time

Deeper evaluation of risk factor exposure and pricing implications; analysis ofdiversification impact of network exposure

Third: time-variation in the ρ coefficients

Fourth: different design of the W matrices taking into account the strengthof the relation across subjects

Billio, Caporin, Panzica and Pelizzon N&S December, 2014 18 / 18

This project has received funding from the European Union’s

Seventh Framework Programme for research, technological

development and demonstration under grant agreement n° 320270

www.syrtoproject.eu

This document reflects only the author’s views.

The European Union is not liable for any use that may be made of the information contained therein.