Embed Size (px)

Citation preview

Elias GagasChief Digital Officer

360° ofFinTech (R)evolution

The “Great Divide / Gap” behind the FinTech (R)evolution

FinTech (R)evolutionKey Drivers

FinTech (R)evolution – Key DriversThe Winds of Change sweeping through Financial Services

Global Standards

Consumers

Internet Economy

Innovative Ideas

Global Standards

Consumers

Internet Economy

Innovative Ideas

FinTech (R)evolutionThe Stakeholders

FinTech (R)evolution – StakeholdersThe key actors / stars of this new world

Two worlds Collide

› Legacy Financial Services (e.g. Banks, Card / Payment Processors, Wealth Management etc.)

› FinTech driven Startups (e.g. NeoBanks, Alternative Payments, Aggregators etc.)

Two worlds must work together

› Legacy Financial Services follow regulations & have access to an established customer base

› FinTech driven Startups innovate without the “shackles” of regulation

Governments

Financial InstitutionsBanks

LegacyTechnology

FinancialMessaging

VCs

Internet & TechGiants

IncubatorsAccelerators

FinTechStartups

FinTech(R)evolution

The FinTech Yin Yang

Academia & Research

Regulators

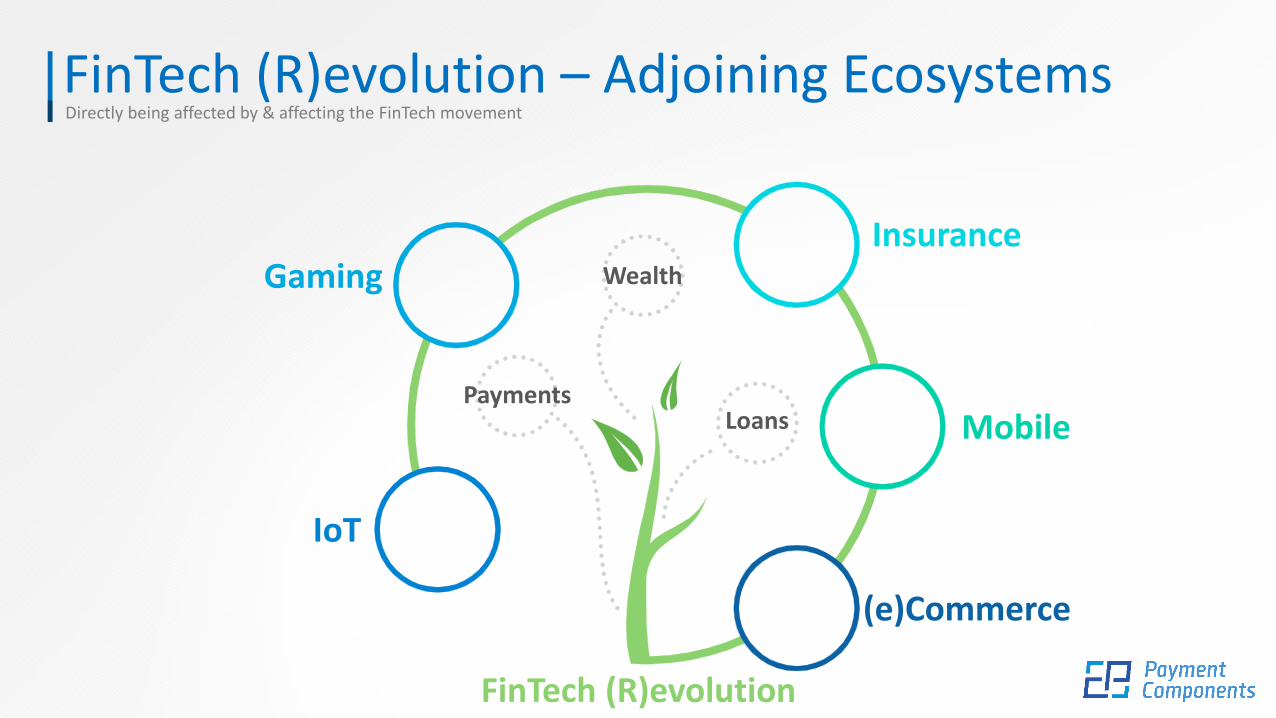

FinTech (R)evolutionAdjoining Ecosystes

FinTech (R)evolution – Adjoining EcosystemsDirectly being affected by & affecting the FinTech movement

FinTech (R)evolution

(e)Commerce

MobilePayments

IoT

Wealth

Loans

GamingInsurance

FinTech (R)evolutionSome Examples

FinTech (R)evolution –Unified Payments Interface - India

› Unified Payments Interface (UPI) is a payment system launched by National Payments Corporation of India and regulated by Reserve Bank of India which facilitates the fund transfer between two bank accounts on the mobile platform instantly.

› National Payments Corporation of India (NPCI) is an umbrella organization for all retail payments system in India. It was set up with the guidance and support of the Reserve Bank of India (RBI) and Indian Banks’ Association (IBA).

› Unified Payments Interface (UPI) is a system that powers multiple bank accounts into a single mobile application (of any participating bank), merging several banking features, seamless fund routing & merchant payments into one hood.

› It also caters to the “Peer to Peer” collect request which can be scheduled and paid as per requirement and convenience. Each Bank provides its own UPI App for Android, Windows and iOS mobile platform(s).

› Learn more at http://www.npci.org.in/UPI_Background.aspx

FinTech (R)evolution –Alipay.com - China

› Alipay.com is a third-party online payment platform. It was launched in China in 2004 by Alibaba Group and its founder Jack Ma.

› Alipay is one of China's biggest payment services and competes with Tencent's WeChat Payment. Alipay is deeply ingrained in the lives of Chinese consumers and is used to pay for items in-store and online for goods and services ranging from taxis to restaurants and clothing.

› Alibaba is hoping that its active Alipay users, which now total 450 million, according to the company, will continue to use the app abroad allowing the company to take advantage of the increasing number of Chinese tourists who are spending more.

› "The vision is targeting two billion people within next five to ten years, not only in China but other countries too," Sabrina Peng, president of Alipay International, told CNBC at the Money 2020 fintech conference in Copenhagen on 2016.

FinTech (R)evolution – CellulantCellulant - Africa

› Cellulant has been named the ‘Best African Payments & Transfers company’ of 2016. At the African FinTechAwards (#afta16)

› Cellulant is connected to more than 50 banks, 40 mobile operators, over 100 merchants and 200 businesses; touching the lives of more than 40 million consumers Africa-wide.

FinTech (R)evolution – P2P FinancingRaboBank– Netherlands

› Rabobank offers financing to businesses through high net worth customers

› Rabobank has run a trial in which SMEs can borrow money from high net worth customers of the bank.

› This offers broader access to financing for businesses and a new investment opportunity for high net worth customers.

› This form of ‘peer-to-peer lending’ supplements existing forms of financing such as regular bank credit and crowdfunding.

› Rabobank is building an online platform (Rabo & Co) that brings together businesses and Private Banking customers.

› Businesses place their financing request on the platform and Private Banking customers state which loan they wish to co-finance. In the trial phase, Rabobank itself will provide at least 50% of every loan.

FinTech (R)evolution – PSD2Payment Services Directive 2 – European Union

› On November 16, 2015, the Council of the European Union passed PSD2. Member states will have two years to incorporate the directive into their national laws and regulations. 2018 is the milestone year for PSD2 going live.

› In short, PSD2 enables bank customers, both consumers and businesses, to use third-party providers to manage their finances.

› The new rules aim to better protect consumers when they pay online, promote the development and use of innovative online and mobile payments, and make cross-border European payment services safer.

› Banks, are obligated to provide these third-party providers access to their customers’ accounts through open APIs. This will enable third-parties to build financial services on top of banks’ data and infrastructure.

› AISP (Account Information Service Provider) are the service providers with access to the account information of bank customers. Such services could analyze a user’s spending behavior or aggregate a user’s account information from several banks into one overview.

› PISP (Payment Initiation Service Provider) are the service providers initiating a payment on behalf of the user. P2P transfer and bill payment are PISP services we are likely to see when PSD2 is implemented.

› In September 2016, Smart Money People estimated that PSD2 had placed a 4% premium on FinTech valuations.

The Bank of the Future is a PlatformIt’s the Everyday Bank – facilitating several customer journeys

Inter-Connected

OpenAPIs

Everyday Bank

PlatformBaaS BaaP

A few words aboutPayment Components

Payment ComponentsWho we are? What we do?

› Payment Components Ltd is a catalyst, empowering FinTech Innovation in Financial Institutions, Corporates and FinTechs.

› Our mantra is “If it’s not Simple, It’s Wrong”

Financial MessagingSoftware Libraries

(SWIFT, SEPA, ISO20022)

Payment Components360° of FinTech Solutions & Services

Corporate Treasury Management System (TMS)

API Management Platform

Financial Messaging & Payments Gateway

AVACAS

Personal Finance Manager (PFM)

Validate Parse

Build

Innovation – R&DPartner

FinTech (R)evolutionBest Practices

Best Practices – What to DOThings to Do

Be informed – Read about it – Accept it – Embrace it – participate!

Assign clear Ownership for change initiative / Digital Transformation

Collaborate – Collaborate – Collaborate. Reach out to the other side!!!

Build a multidisciplinary think tank (with internal & external resources)

Start with properly scoped initiatives & gradually evolve – it’s a journey…

Best Practices – What to AVOIDThings to Avoid

!

Design change by committee BIG BANG Approach

Keep it solely as an in-house endeavor

Treat it as yet another technology project

View FinTech as a threat

Final ThoughtsEmbrace the (R)evolution & Play the Game!!!

What we’re experiencing in Financial Services has happened before (airlines, hotels, taxis, commerce, advertising etc.)

The technologies involved are complex & diverse – but the rules of the game are the same

Educate yourself & your team, acquire new skillsets & start selecting strategic partners

Assemble the necessary pool of skillsets (internal & external) & create the appropriate

organizational structure

It’s NOT OLD vs NEW, LEGACY vs FINTECH but rather a collaborative next step – it’s

truly a Yin-Yang situation

Play & Enjoy the new game!

64 Princes Court , 88 Brompton Road , Knightsbridge, London SW3 1ET, United Kingdom | Tel. : +44 2071172538 | www.paymentcomponents.com

Empowering FinTech Innovation!

@paymentcomp

Elias GagasChief Digital [email protected]