The value premium puzzle

Alexis Eisenhofer

ATACAMA Capital

4th Value Investor ConferenceLos Angeles, 8th of May 2007

Alexis Eisenhofer The value premium puzzle 1/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

Table of contents

Empirical evidence: The value premium

The puzzle: The contradiction to the CAPM

Solutions: A review of the literature

Conclusion

Alexis Eisenhofer The value premium puzzle 2/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

Table of contents

Empirical evidence: The value premium

The puzzle: The contradiction to the CAPM

Solutions: A review of the literature

Conclusion

Alexis Eisenhofer The value premium puzzle 3/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

Investment professionals often classify stocks to a fewnumber of investment styles1

Small Caps Mid Caps Large Caps

MCAP < 1 bln. USD 10 bln. USD ≥ MCAP ≥ 1 bln. USD MCAP > 10 bln. USD

Low PE; high BtM Low PE; high BtM Low PE; high BtMValueHigh DivYld High DivYld High DivYld

MCAP < 1 bln. USD 10 bln. USD ≥ MCAP ≥ 1 bln. USD MCAP > 10 bln. USD

High PE; low BtM High PE; low BtM High PE; low BtMGrowthLow or no DivYld Low or no DivYld Low or no DivYld

MCAP := Market capitalization; PE := Price/earnings ratio; BtM := Book-to-market ratio;DivYld := Dividend yield

1Basu (1977), Banz (1981), Fama/French (1992)Alexis Eisenhofer The value premium puzzle 4/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

The value premium: In the long run value outperformsgrowth (and small stocks outperform large stocks)

Alexis Eisenhofer The value premium puzzle 5/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

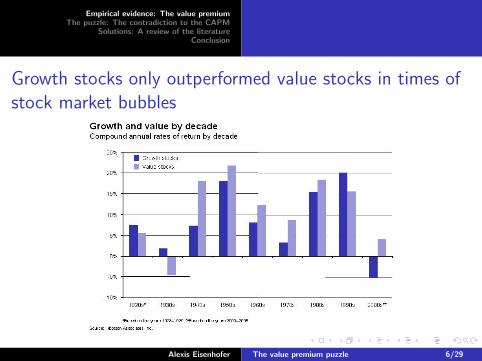

Growth stocks only outperformed value stocks in times ofstock market bubbles

Alexis Eisenhofer The value premium puzzle 6/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

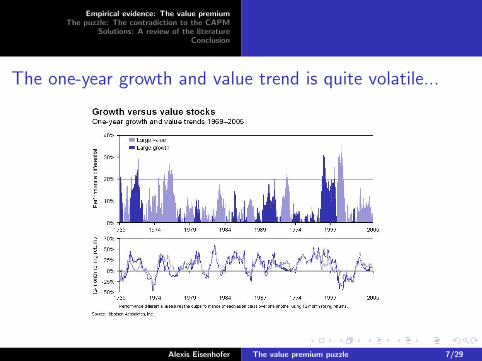

The one-year growth and value trend is quite volatile...

Alexis Eisenhofer The value premium puzzle 7/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

...but becomes more apparent with a longer (e.g.three-year) time horizon

Alexis Eisenhofer The value premium puzzle 8/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

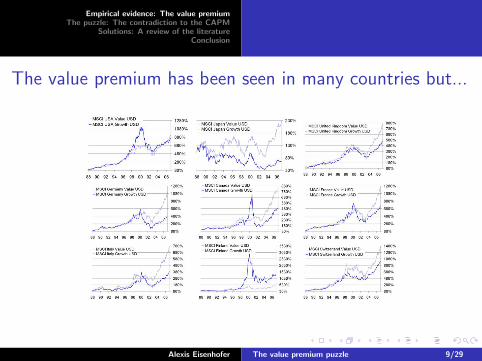

The value premium has been seen in many countries but...

Alexis Eisenhofer The value premium puzzle 9/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

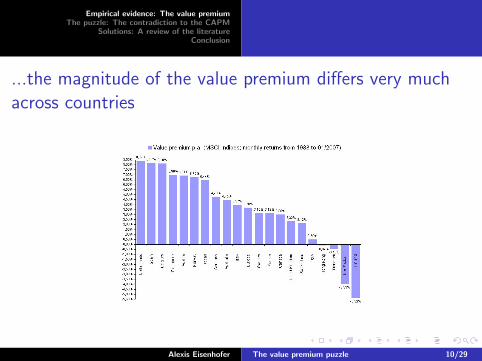

...the magnitude of the value premium differs very muchacross countries

Alexis Eisenhofer The value premium puzzle 10/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

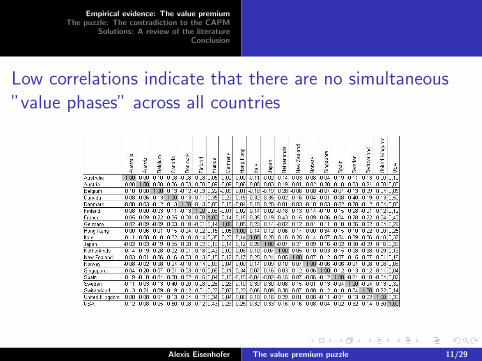

Low correlations indicate that there are no simultaneous”value phases” across all countries

Alexis Eisenhofer The value premium puzzle 11/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

Table of contents

Empirical evidence: The value premium

The puzzle: The contradiction to the CAPM

Solutions: A review of the literature

Conclusion

Alexis Eisenhofer The value premium puzzle 12/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

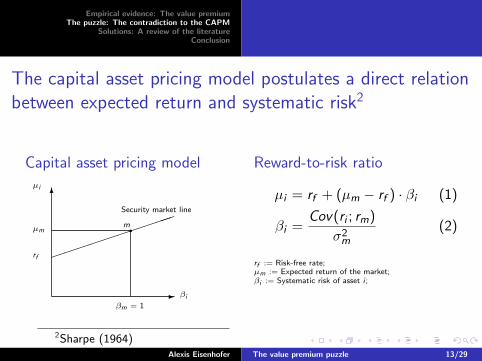

The capital asset pricing model postulates a direct relationbetween expected return and systematic risk2

Capital asset pricing model

6

-

����������

µi

µm

rf

βi

βm = 1

Security market line

m qReward-to-risk ratio

µi = rf + (µm − rf ) · βi (1)

βi =Cov(ri ; rm)

σ2m

(2)

rf := Risk-free rate;µm := Expected return of the market;βi := Systematic risk of asset i ;

2Sharpe (1964)Alexis Eisenhofer The value premium puzzle 13/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

Even though value stocks offered higher returns to theinvestor their risk was lower

Alexis Eisenhofer The value premium puzzle 14/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

The drawdown of value stocks was lower while their upsidepotential was almost equal to growth stocks

Alexis Eisenhofer The value premium puzzle 15/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

The assumptions of the CAPM are very simple and hardlyreflect real investor behavior

Major CAPM assumptions...

1 All investors share the sameinformation and act rationally

2 Returns are distributednormally

3 All investors hold the (same)market portfolio

4 Frictionless and efficient capitalmarkets

...conflict with reality

⇔ 1′ Investors are not perfectlyinformed and are irrational

⇔ 2′ Time varying nonsymmetricdistributions

⇔ 3′ Investors hold differentportfolios

⇔ 4′ Transaction costs andinefficiencies

Alexis Eisenhofer The value premium puzzle 16/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

Institutional imperative and overestimationInvestor disagreementA Duration-based explanationFixed-income hedgingEvolutionary financeTransaction costs and institutional ownership

Table of contents

Empirical evidence: The value premium

The puzzle: The contradiction to the CAPM

Solutions: A review of the literature

Conclusion

Alexis Eisenhofer The value premium puzzle 17/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

Institutional imperative and overestimationInvestor disagreementA Duration-based explanationFixed-income hedgingEvolutionary financeTransaction costs and institutional ownership

The value premium can be explained by emotions andcognitive errors of investors

I The institutional imperative (managers tend to act like theirpeers) leads to investments in ”glamor stocks”, even if theirvaluation is inferior to ”unknown” stocks3

I Investors are too optimistic because they naivelyextrapolate earnings trends and stick too long to highgrowth rates4

I Hope and fear drives overvaluation (undervaluation) ofgrowth (value)

3Buffett (1989)4DeBondt/Thaler (1987)

Alexis Eisenhofer The value premium puzzle 18/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

Institutional imperative and overestimationInvestor disagreementA Duration-based explanationFixed-income hedgingEvolutionary financeTransaction costs and institutional ownership

Value stocks and small-cap stocks earn higher returnsbecause there is greater disagreement about the stocksfuture payoffs5

I The divergence in analysts earnings forecasts is a proxy forinvestor disagreement

I Value stocks have a greater divergence of opinion thangrowth stocks

I Small-capitalization stocks exhibited greater forecastdispersion than stocks of large companies

5Daniel/Titman (1997)Alexis Eisenhofer The value premium puzzle 19/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

Institutional imperative and overestimationInvestor disagreementA Duration-based explanationFixed-income hedgingEvolutionary financeTransaction costs and institutional ownership

Growth companies have higher betas because of their highduration of cash flows while their low covariance to cashflow risk accounts for lower returns6

I Risk is explained through cash flow risk and discount raterisk (Duration)

I Value stocks, as short-horizon equity, vary more withfluctuations in cash flows (⇒ lower Duration); Growthstocks, as long-horizon equity, vary more with fluctuationsin discount rates (⇒ higher Duration)

I Investors fear cash flow risk far more than discount rate riskwhich is why value investors claim a premium on theirinvestment

6Lettau/Wachter (2005)Alexis Eisenhofer The value premium puzzle 20/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

Institutional imperative and overestimationInvestor disagreementA Duration-based explanationFixed-income hedgingEvolutionary financeTransaction costs and institutional ownership

The value premium can be explained as an insurance forinstitutional investors because growth stocks offer a goodhedge against fixed-income risk7

I Value stocks with constant dividends are similar tofixed-income instruments such as bills, bonds and loans

I Institutional investors such as life-insurance companies,banks and pension funds typically invest heavily infixed-income instruments

I Despite the sizeable premium for value stocks, growthstocks are attractive to these investors because they offer agood hedge against fixed-income risk

7Post/Van Vliet (2006)Alexis Eisenhofer The value premium puzzle 21/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

Institutional imperative and overestimationInvestor disagreementA Duration-based explanationFixed-income hedgingEvolutionary financeTransaction costs and institutional ownership

The value strategy dominates a growth, momentum orglamor portfolio in the long run due to the convergence ofmarkets towards fundamental values8

I A Darwinian approach: The market as a heterogeneouspopulation of portfolio strategies in competition for marketcapital

I The value strategy wins because markets tend to convergetowards fundamental values

I This convergence property gives rise to a predictability ofasset returns based on fundamental criteria

8Hens/Schenk-Hoppe/Woehrmann (2006)Alexis Eisenhofer The value premium puzzle 22/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

Institutional imperative and overestimationInvestor disagreementA Duration-based explanationFixed-income hedgingEvolutionary financeTransaction costs and institutional ownership

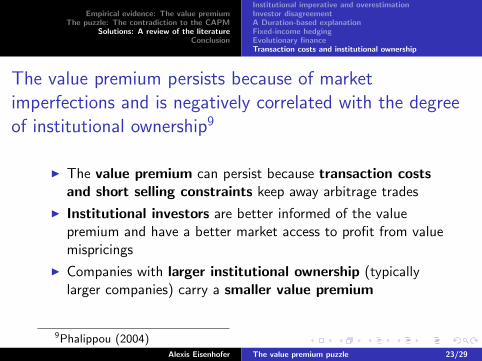

The value premium persists because of marketimperfections and is negatively correlated with the degreeof institutional ownership9

I The value premium can persist because transaction costsand short selling constraints keep away arbitrage trades

I Institutional investors are better informed of the valuepremium and have a better market access to profit from valuemispricings

I Companies with larger institutional ownership (typicallylarger companies) carry a smaller value premium

9Phalippou (2004)Alexis Eisenhofer The value premium puzzle 23/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

BibliographyContact

Table of contents

Empirical evidence: The value premium

The puzzle: The contradiction to the CAPM

Solutions: A review of the literature

Conclusion

Alexis Eisenhofer The value premium puzzle 24/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

BibliographyContact

Value investing is a superior investment style in the longrun

I The value premium has been seen for many years and willprobably persist in the future

I Small cap stocks show a higher premium than large caps

I The correlation of the value premium in different countriesis low

I Behavioral rather than rational aspects can ”solve” thepuzzle

Alexis Eisenhofer The value premium puzzle 25/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

BibliographyContact

References

* Banz, Rolf W. (1981): The relationship between return and marketvalue of common stocks, Journal of Financial Economics 9, 3-18.

* Basu, Sanjoy (1977): Investment performance of common stocksin relationship to their price-earnings ratios: A test of the efficientmarket hypthesis, Journal of Finance 32, 663-682.

* Buffett, Warren (1989): Chairmans letter,http://berkshirehathaway.com/letters/1989.html.

* Daniel, Kent, and Sheridan Titman (1997): Evidence on thecharacteristics of cross sectional variation in stock returns, Journalof Finance 52, 1-33.

Alexis Eisenhofer The value premium puzzle 26/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

BibliographyContact

References

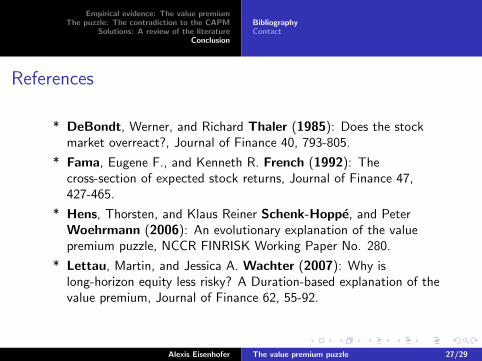

* DeBondt, Werner, and Richard Thaler (1985): Does the stockmarket overreact?, Journal of Finance 40, 793-805.

* Fama, Eugene F., and Kenneth R. French (1992): Thecross-section of expected stock returns, Journal of Finance 47,427-465.

* Hens, Thorsten, and Klaus Reiner Schenk-Hoppe, and PeterWoehrmann (2006): An evolutionary explanation of the valuepremium puzzle, NCCR FINRISK Working Paper No. 280.

* Lettau, Martin, and Jessica A. Wachter (2007): Why islong-horizon equity less risky? A Duration-based explanation of thevalue premium, Journal of Finance 62, 55-92.

Alexis Eisenhofer The value premium puzzle 27/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

BibliographyContact

References

* Phalippou, Ludovic (2004): What drives the value premium,INSEAD Working Paper May 2004.

* Post, Thierry, and Pim van Vliet (2006): Loss aversion and thevalue premium puzzle, SSRN Working Paper No. 764164.

* Sharpe, William F. (1964): Capital asset prices: A theory of market

equilibrium under conditions of risk, Journal of Finance 19, 425-442.

Alexis Eisenhofer The value premium puzzle 28/29

Empirical evidence: The value premiumThe puzzle: The contradiction to the CAPM

Solutions: A review of the literatureConclusion

BibliographyContact

Thank you for your attention!

Dr. Alexis EisenhoferATACAMA Capital GmbHMaria-Probst-Str. 19D-80939 MunichGermany

Phone: +49-(0)89-2000320Fax: +49-(0)89-20003232eMail: [email protected]: http://www.atacap.com

This presentation will be available on the web sitehttp://www.atacap.com/

Alexis Eisenhofer The value premium puzzle 29/29

Recommended