Embed Size (px)

Citation preview

Introduction Model Results Conclusion

Does Human Capital Risk Explain The ValuePremium Puzzle?

Serginio Sylvain

Department of EconomicsUniversity of Chicago

Current Draft: March, 2014First Draft: January, 2013

1 / 25

Introduction Model Results Conclusion

OutlineIntroduction

MotivationLiterature

Model

PrimitivesPlanner’s ProblemEquilibriumAsset Pricing Implications

Results

Fama and French (1996, 1997)Empirical Evidence and Implications of the ModelCyclicity and Long Run RiskThe CAPM

Conclusion2 / 25

Introduction Model Results Conclusion

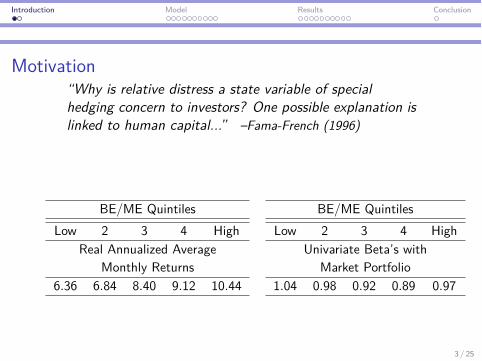

Motivation“Why is relative distress a state variable of specialhedging concern to investors? One possible explanation islinked to human capital...” –Fama-French (1996)

BE/ME QuintilesLow 2 3 4 High

Real Annualized AverageMonthly Returns

6.36 6.84 8.40 9.12 10.44

BE/ME QuintilesLow 2 3 4 High

Univariate Beta’s withMarket Portfolio

1.04 0.98 0.92 0.89 0.97

3 / 25

Introduction Model Results Conclusion

LiteratureI The Value Premium: Fama and French (1996; 1997; 1998),

Rouwenhorst (1999), Liew and Vassalou (2000), ...

I Empirical literature on Value Premium, human capital and laborincome: Jaganathan and Wang (1996), Jagannathan et al. (1998),Hansson (2004), Veronesi and Santos (2005), ...

I Some more theoretical approaches: Veronesi and Santos (2005),Zhang (2005), Bansal, Dittmar and Lundblad (2005), Hansen,Heaton and Li (2008), Garleanu, Kogan, and Panageas (2012), ...

I I complement the above research by producing a generalequilibrium model with endogenous growth where the ValuePremium arises endogenously from risk to human capital.

I I draw from the recent literature on asset pricing in aproduction economy: Kogan (2001, 2003), Eberly and Wang(2009, 2011), ... 4 / 25

Introduction Model Results Conclusion

PreviewI Model with 2 types of firms where Type A has more human capital risk

I ∆These firms are less valuable ∆ have greater BE/ME and equityreturns (hence the Value Premium) and lower investment-to-capitalratios

I Reallocation dynamics keep the “Value” (Type A) firms from disappearing∆Substantial variation in the Value premium and the relative BE/ME.

I Simple model mechanism yields:I Value premium, relative BE/ME, and price of risk are

counter-cyclical.I Value firms are more exposed to long-run riskI Failure of CAPM when we don’t take human capital returns into

account5 / 25

Introduction Model Results Conclusion

I Evidence: Value firms are more exposed to human capital risk

I Possible Explanations:I Aggr. human capital productivity covary more positively with

outcomes of Value firms: “negative shock to a distressed firm [...]implies a negative shock to the value of specialized human capital...Thus, workers avoid the stocks of [all] distressed firms.”–F&F(’96)

I Value firms have relatively more firm-specific human capital andhence are more burdened by their wage bill

6 / 25

Introduction Model Results Conclusion

PrimitivesThere is a continuum of identical agents with unit mass and recursivepreferences.

The agents maximize

Vt = Et

⁄ Œ

tf {Cs , Vs} ds

f {C , V } =—

fl

ACfl

((1 ≠ “)V )fl

1≠“ ≠1 ≠ (1 ≠ “)VB

“ and (1 ≠ fl)≠1 govern RA and IES respectively.— is the subjective discount rate.

7 / 25

Introduction Model Results Conclusion

At date zero, each agent is endowed with human capital H0.

There are 2 types of firms; each with a continuum (with unit mass) ofidentical firms endowed with physical capital K i

0 = K0 for i œ {A, B}.

Type A firms use physical capital (KA) and human capital (H) as inputsto production.

Firms of Type B use physical capital (KB).

8 / 25

Introduction Model Results Conclusion

The human capital at time tdHtHt

= � ln3

1 +IHt

◊Ht

4dt ≠ ”dt + ‡hdZA

t

IHt : investment in human capital on date t

”: depreciation rate

◊ and �: coe�cients for adjustment cost

If � © ”ln(1+ ”

◊ ), then as ◊ æ Œ we have Et(

dHtHt

) æ IHt

Htdt ≠ ”dt

and as ◊ æ 0 we have Et(dHtHt

) æ ≠”dt

Pictures Motivation for adj. cost

9 / 25

Introduction Model Results Conclusion

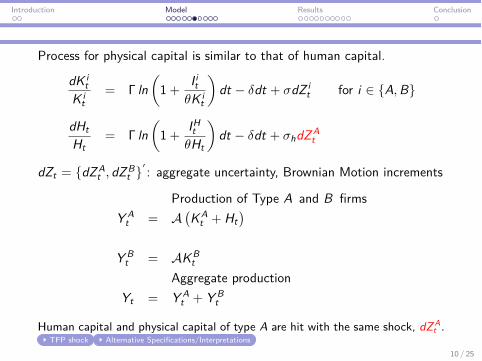

Process for physical capital is similar to that of human capital.

dK it

K it

= � ln3

1 +I it

◊K it

4dt ≠ ”dt + ‡dZ i

t for i œ {A, B}

dHtHt

= � ln3

1 +IHt

◊Ht

4dt ≠ ”dt + ‡hdZA

t

dZt = {dZAt , dZB

t }Õ : aggregate uncertainty, Brownian Motion increments

Production of Type A and B firmsY A

t = A!KA

t + Ht"

Y Bt = AKB

tAggregate production

Yt = Y At + Y B

t

Human capital and physical capital of type A are hit with the same shock, dZ At .

TFP shock Alternative Specifications/Interpretations10 / 25

Introduction Model Results Conclusion

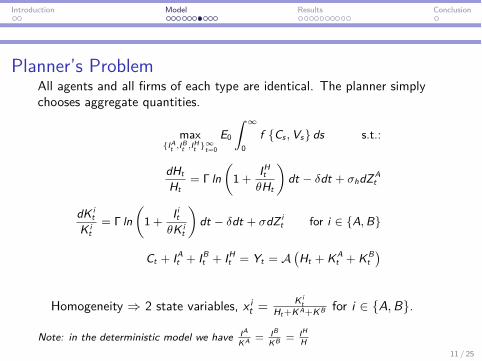

Planner’s ProblemAll agents and all firms of each type are identical. The planner simplychooses aggregate quantities.

max{IA

t ,IBt ,IH

t }Œt=0

E0

⁄ Œ

0f {Cs , Vs} ds s.t.:

dHtHt

= � ln3

1 +IHt

◊Ht

4dt ≠ ”dt + ‡hdZ A

t

dK it

K it

= � ln3

1 +I it

◊K it

4dt ≠ ”dt + ‡dZ i

t for i œ {A, B}

Ct + IAt + IB

t + IHt = Yt = A

!Ht + KA

t + KBt

"

Homogeneity ∆ 2 state variables, x it =

Kit

Ht+KA+KB for i œ {A, B}.

Note: in the deterministic model we have IA

KA = IB

KB = IHH

11 / 25

Introduction Model Results Conclusion

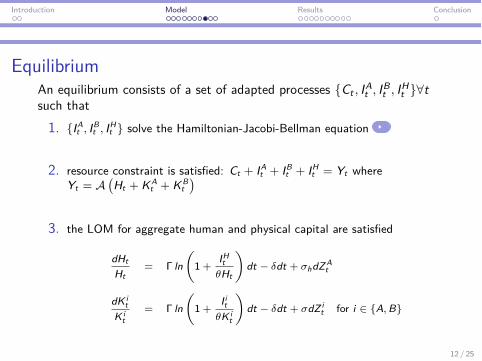

EquilibriumAn equilibrium consists of a set of adapted processes {Ct , IA

t , IBt , IH

t }’tsuch that

1. {IAt , IB

t , IHt } solve the Hamiltonian-Jacobi-Bellman equation

2. resource constraint is satisfied: Ct + IAt + IB

t + IHt = Yt where

Yt = A!Ht + KA

t + KBt

"

3. the LOM for aggregate human and physical capital are satisfied

dHtHt

= � ln3

1 +IHt

◊Ht

4dt ≠ ”dt + ‡hdZA

t

dKit

K it

= � ln3

1 +I it

◊Kit

4dt ≠ ”dt + ‡dZi

t for i œ {A, B}

12 / 25

Introduction Model Results Conclusion

Asset PricingThere are 2 risky securities: risky claims on sum of profits of 2 firm types.

Let ÿH = IH

H , and ÿi = I i

K i

qit : the value of physical of type i (Tobin Q)

qi =1�

!ÿi + ◊

"

pt : the value of human capital (Tobin Q)

p =1�

!ÿH + ◊

"

Stochastic Discount Factor, ⇤t , follows Decentralized Problem formulas

d⇤t⇤t

= ≠rtdt ≠ ‡⇤,t · dZt

13 / 25

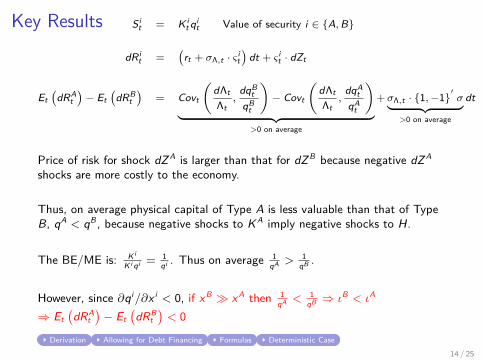

Key Results Sit = Ki

t qit Value of security i œ {A, B}

dRit =

!rt + ‡⇤,t · Î i

t"

dt + Î it · dZt

Et!

dRAt"

≠ Et!

dRBt

"= Covt

3d⇤t⇤t

,dqB

tqB

t

4≠ Covt

3d⇤t⇤t

,dqA

tqA

t

4

¸ ˚˙ ˝>0 on average

+‡⇤,t · {1, ≠1}Õ

‡¸ ˚˙ ˝>0 on average

dt

Price of risk for shock dZ A is larger than that for dZ B because negative dZ A

shocks are more costly to the economy.

Thus, on average physical capital of Type A is less valuable than that of TypeB, qA < qB , because negative shocks to KA imply negative shocks to H.

The BE/ME is: Ki

Ki qi = 1qi . Thus on average 1

qA > 1qB .

However, since ˆqi /ˆx i < 0, if xB ∫ xA then 1qA < 1

qB ∆ ÿB < ÿA

∆ Et!dRA

t"

≠ Et!dRB

t"

< 0

Derivation Allowing for Debt Financing Formulas Deterministic Case14 / 25

Introduction Model Results Conclusion

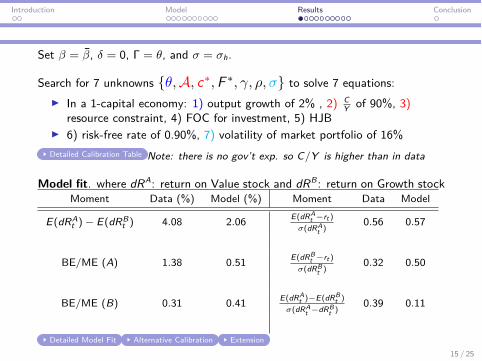

Set — = —, ” = 0, � = ◊, and ‡ = ‡h.

Search for 7 unknowns {◊, A, cú, F ú, “, fl, ‡} to solve 7 equations:I In a 1-capital economy: 1) output growth of 2% , 2) C

Y of 90%, 3)resource constraint, 4) FOC for investment, 5) HJB

I 6) risk-free rate of 0.90%, 7) volatility of market portfolio of 16%Detailed Calibration Table Note: there is no gov’t exp. so C/Y is higher than in data

Model fit. where dRA: return on Value stock and dRB : return on Growth stockMoment Data (%) Model (%) Moment Data Model

E(dRAt ) ≠ E(dRB

t ) 4.08 2.06 E(dRAt ≠rt )

‡(dRAt )

0.56 0.57

BE/ME (A) 1.38 0.51 E(dRBt ≠rt )

‡(dRBt )

0.32 0.50

BE/ME (B) 0.31 0.41 E(dRAt )≠E(dRB

t )

‡(dRAt ≠dRB

t )0.39 0.11

Detailed Model Fit Alternative Calibration Extension15 / 25

Introduction Model Results Conclusion

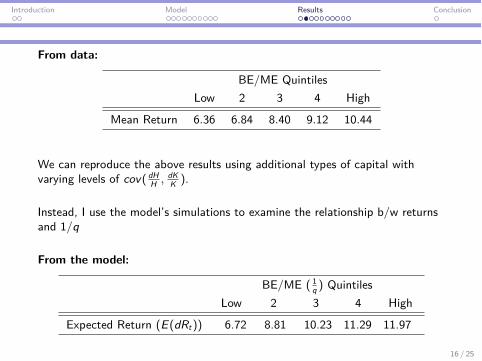

From data:

BE/ME QuintilesLow 2 3 4 High

Mean Return 6.36 6.84 8.40 9.12 10.44

We can reproduce the above results using additional types of capital withvarying levels of cov( dH

H , dKK ).

Instead, I use the model’s simulations to examine the relationship b/w returnsand 1/q

From the model:

BE/ME ( 1q ) Quintiles

Low 2 3 4 High

Expected Return (E(dRt)) 6.72 8.81 10.23 11.29 11.97

16 / 25

Introduction Model Results Conclusion

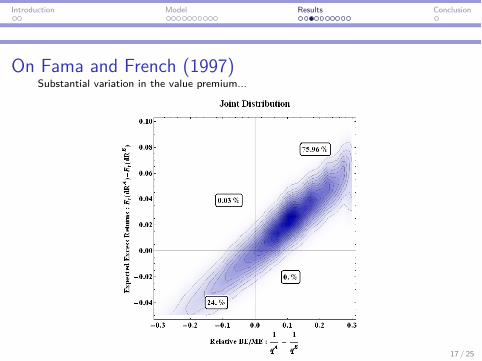

On Fama and French (1997)Substantial variation in the value premium...

17 / 25

Introduction Model Results Conclusion

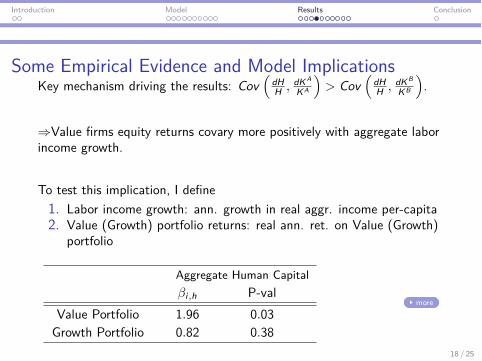

Some Empirical Evidence and Model ImplicationsKey mechanism driving the results: Cov

1dHH , dKA

KA

2> Cov

1dHH , dKB

KB

2.

∆Value firms equity returns covary more positively with aggregate laborincome growth.

To test this implication, I define1. Labor income growth: ann. growth in real aggr. income per-capita2. Value (Growth) portfolio returns: real ann. ret. on Value (Growth)

portfolio

Aggregate Human Capital—i,h P-val

Value Portfolio 1.96 0.03Growth Portfolio 0.82 0.38

more

18 / 25

Introduction Model Results Conclusion

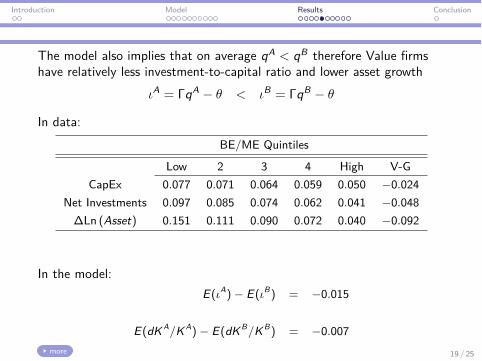

The model also implies that on average qA < qB therefore Value firmshave relatively less investment-to-capital ratio and lower asset growth

ÿA = �qA ≠ ◊ < ÿB = �qB ≠ ◊

In data:BE/ME Quintiles

Low 2 3 4 High V-GCapEx 0.077 0.071 0.064 0.059 0.050 ≠0.024

Net Investments 0.097 0.085 0.074 0.062 0.041 ≠0.048�Ln (Asset) 0.151 0.111 0.090 0.072 0.040 ≠0.092

In the model:E(ÿA) ≠ E(ÿB) = ≠0.015

E(dKA/KA) ≠ E(dKB/KB) = ≠0.007more 19 / 25

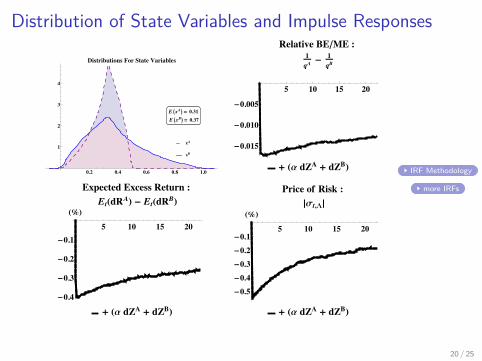

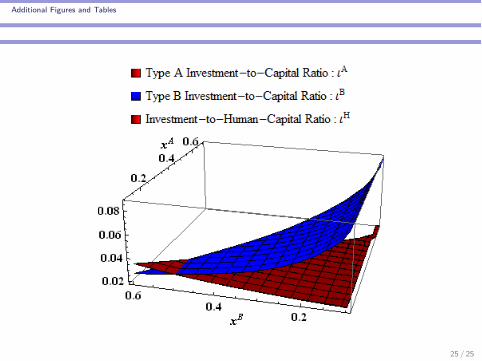

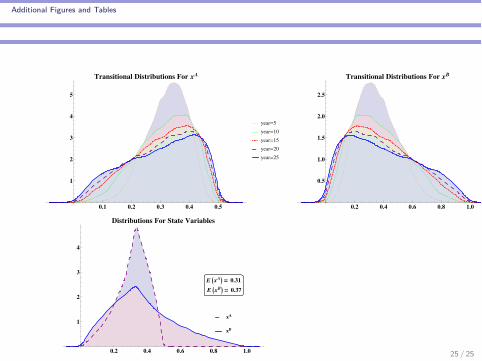

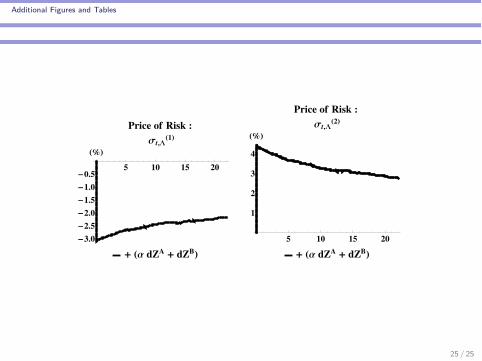

Distribution of State Variables and Impulse Responses

xA

xB

0.2 0.4 0.6 0.8 1.0

1

2

3

4

Distributions For State Variables

E !xA" ! 0.31

E !xB" ! 0.37

5 10 15 20

-0.015

-0.010

-0.005

Relative BEêME :1qA- 1qB

+ Ha dZA + dZBL

5 10 15 20

-0.4

-0.3

-0.2

-0.1

H%LExpected Excess Return :

EtHdRAL - EtHdRBL

+ Ha dZA + dZBL

5 10 15 20

!0.5

!0.4

!0.3

!0.2

!0.1

!""

Price of Risk :

#Σt,$#

% !Α dZA % dZB"

IRF Methodology

more IRFs

20 / 25

Introduction Model Results Conclusion

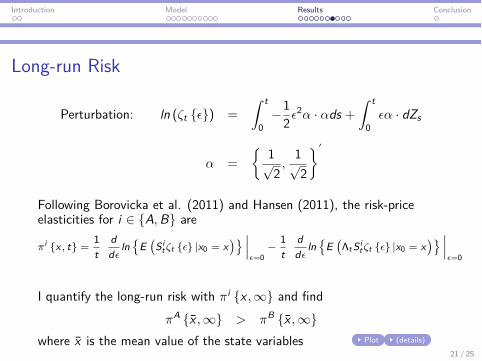

Long-run Risk

Perturbation: ln (’t {‘}) =

⁄ t

0≠1

2‘2– · –ds +⁄ t

0‘– · dZs

– =

;1Ô2

,1Ô2

<Õ

Following Borovicka et al. (2011) and Hansen (2011), the risk-priceelasticities for i œ {A, B} are

fii {x , t} =1t

dd‘

ln)

E!

Sit’t {‘} |x0 = x

"* ---‘=0

≠1t

dd‘

ln)

E!⇤tSi

t’t {‘} |x0 = x"* ---

‘=0

I quantify the long-run risk with fii {x , Œ} and findfiA {x , Œ} > fiB {x , Œ}

where x is the mean value of the state variables Plot (details)21 / 25

Introduction Model Results Conclusion

Conditional CAPMdRm

t and dRwt : returns on the market and total wealth portfolios.

dRm = dRAÊ + dRB(1 ≠ Ê) = µmt dt + Îm

t · dZt

dRw =

3dRH(1 ≠ ÊA ≠ ÊB) + dRAÊA

+dRBÊB

4= µw

t dt + Îwt · dZt

Consider the regression

Et!dRA

t"

≠ Et!dRB

t"

= –0¸˚˙˝Pricing Error

+ –1¸˚˙˝Slope

◊ Îwt .Îw

t!—A,w

t ≠ —B,wt

"dt

— i,wt =

covt(dR it , dRw

t )Îw

t .Îwt

for i œ {A, B}

With Log-Utitlity, the price of risk is ‡⇤,t = ‡c,t = Îwt ; thus the Conditional

CAPM holds: –0 = 0 and –1 = 1.

I will run the above regression with dRm and dRw and compare the pricing errors22 / 25

Introduction Model Results Conclusion

Conditional CAPM Regressions(1): Et

!dRA

t"

≠ Et!dRB

t"= –0¸˚˙˝

Pricing Error

+ –1¸˚˙˝Slope

◊ Îwt .Îw

t

1—A,w

t ≠ —B,wt

2dt

(2): Et!dRA

t"

≠ Et!dRB

t"= –0¸˚˙˝

Pricing Error

+ –1¸˚˙˝Slope

◊ Îmt .Îm

t

1—A,m

t ≠ —B,mt

2dt

“ = (1 ≠ fl) = 1 (log-utility) “ > (1 ≠ fl) ”= 1

–0 (%)t-stat

–1t-stat

R2

t-stat

(1) (2) Di�.0.00 1.1 ≠1.10.38 290. ≠290.

1. 0.97 0.041.3 ◊ 1016 290. 1.3 ◊ 1016

1. 1. 0.007000. 330. 1.5

(1) (2) Di�.≠0.06 1.9 ≠2.≠2.9 100. ≠110.

3.4 0.09 3.3370. 120. 260.

1. 0.97 0.03410. 33. 0.95

More23 / 25

Introduction Model Results Conclusion

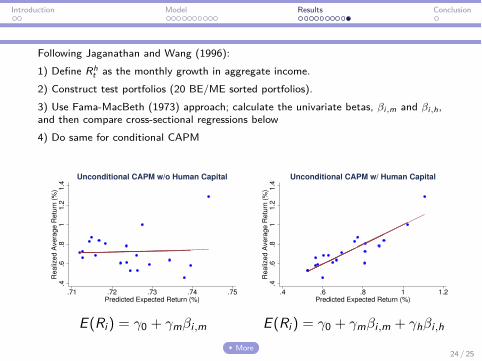

Following Jaganathan and Wang (1996):1) Define Rh

t as the monthly growth in aggregate income.2) Construct test portfolios (20 BE/ME sorted portfolios).3) Use Fama-MacBeth (1973) approach; calculate the univariate betas, —i,m and —i,h,and then compare cross-sectional regressions below4) Do same for conditional CAPM

.4.6

.81

1.2

1.4

Re

aliz

ed

Ave

rag

e R

etu

rn (

%)

.71 .72 .73 .74 .75Predicted Expected Return (%)

Unconditional CAPM w/o Human Capital

.4.6

.81

1.2

1.4

Re

aliz

ed

Ave

rag

e R

etu

rn (

%)

.4 .6 .8 1 1.2Predicted Expected Return (%)

Unconditional CAPM w/ Human Capital

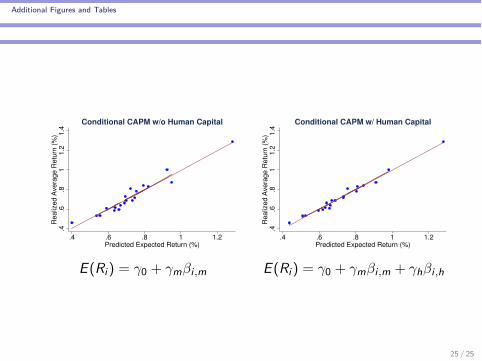

E (Ri) = “0 + “m—i ,m E (Ri) = “0 + “m—i ,m + “h—i ,h

More24 / 25

Introduction Model Results Conclusion

ConclusionI produce a general equilibrium model with endogenous growth andHuman capital risk which explains the Value Premium.

The model has the following features and implications

1) Firm-level and Aggregate Human capital growth covary morepositively with assets growth of Value firms. Hence, Value firms are lessvaluable (lower q), greater BE/ME (1/q), and greater equity returns.Lower q ∆ lower ÿ and lower asset growth for Value firms

2) There is endogenous reallocation due to diversification incentiveswhich leads to co-existence of both Value and Growth firms in equilibrium

3) Counter-cyclical Value premium, relative BE/ME and price of risk.Relatively more long-run risk exposure for Value firms. Failure of theCAPM

25 / 25

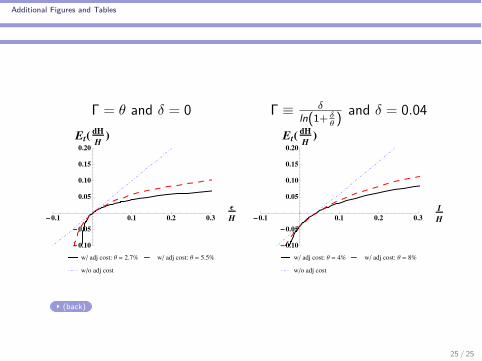

Additional Figures and Tables

� = ◊ and ” = 0 � © ”ln(1+ ”

◊ )and ” = 0.04

!0.1 0.1 0.2 0.3

Ε

H

!0.10

!0.05

0.05

0.10

0.15

0.20

Et!dH

H"

w! adj cost: Θ " 2.7# w! adj cost: Θ " 5.5#

w!o adj cost

!0.1 0.1 0.2 0.3

I

H

!0.10

!0.05

0.05

0.10

0.15

0.20

Et!dH

H"

w! adj cost: Θ " 4# w! adj cost: Θ " 8#

w!o adj cost

(back)

25 / 25

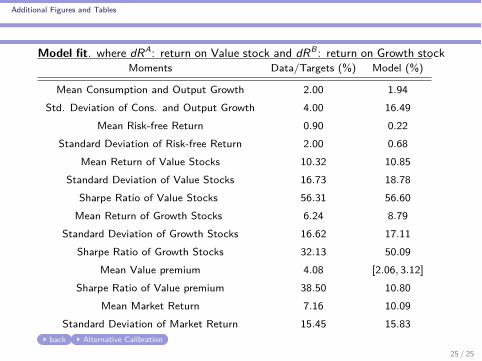

Additional Figures and Tables

Model fit. where dRA: return on Value stock and dRB : return on Growth stockMoments Data/Targets (%) Model (%)

Mean Consumption and Output Growth 2.00 1.94Std. Deviation of Cons. and Output Growth 4.00 16.49

Mean Risk-free Return 0.90 0.22Standard Deviation of Risk-free Return 2.00 0.68

Mean Return of Value Stocks 10.32 10.85Standard Deviation of Value Stocks 16.73 18.78

Sharpe Ratio of Value Stocks 56.31 56.60Mean Return of Growth Stocks 6.24 8.79

Standard Deviation of Growth Stocks 16.62 17.11Sharpe Ratio of Growth Stocks 32.13 50.09

Mean Value premium 4.08 [2.06, 3.12]Sharpe Ratio of Value premium 38.50 10.80

Mean Market Return 7.16 10.09Standard Deviation of Market Return 15.45 15.83

back Alternative Calibration

25 / 25

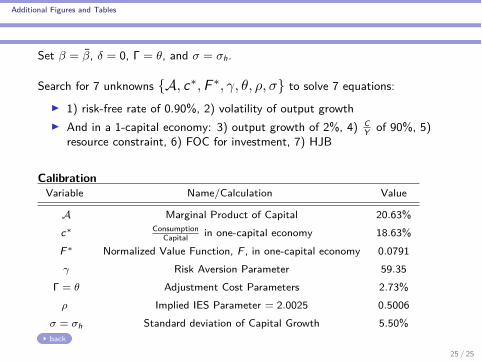

Additional Figures and Tables

Set — = —, ” = 0, � = ◊, and ‡ = ‡h.

Search for 7 unknowns {A, cú, F ú, “, ◊, fl, ‡} to solve 7 equations:I 1) risk-free rate of 0.90%, 2) volatility of output growthI And in a 1-capital economy: 3) output growth of 2%, 4) C

Y of 90%, 5)resource constraint, 6) FOC for investment, 7) HJB

CalibrationVariable Name/Calculation Value

A Marginal Product of Capital 20.63%cú Consumption

Capital in one-capital economy 18.63%F ú Normalized Value Function, F , in one-capital economy 0.0791“ Risk Aversion Parameter 59.35

� = ◊ Adjustment Cost Parameters 2.73%fl Implied IES Parameter = 2.0025 0.5006

‡ = ‡h Standard deviation of Capital Growth 5.50%back

25 / 25

Additional Figures and Tables

Model fit. where dRA: return on Value stock and dRB : return on Growth stockMoments Data/Targets (%) Model (%)

Mean Consumption and Output Growth 2.00 2.02Std. Deviation of Cons. and Output Growth 4.00 4.08

Mean Risk-free Return 0.90 0.90Standard Deviation of Risk-free Return 2.00 0.14

Mean Return of Value Stocks 10.32 10.97Standard Deviation of Value Stocks 16.73 4.66

Sharpe Ratio of Value Stocks 56.31 216Mean Return of Growth Stocks 6.24 9.34

Standard Deviation of Growth Stocks 16.62 4.15Sharpe Ratio of Growth Stocks 32.13 204

Mean Value premium 4.08 [1.64, 1.65]Sharpe Ratio of Value premium 38.50 41.42

Mean Market Return 7.16 10.05Standard Deviation of Market Return 15.45 3.92

back

25 / 25

Additional Figures and Tables

25 / 25

Additional Figures and Tables

25 / 25

Additional Figures and Tables

0.1 0.2 0.3 0.4 0.5

1

2

3

4

5

Transitional Distributions For xA

year!5

year!10

year!15

year!20

year!25

0.2 0.4 0.6 0.8 1.0

0.5

1.0

1.5

2.0

2.5

Transitional Distributions For xB

year!5

year!10

year!15

year!20

year!25

xA

xB

0.2 0.4 0.6 0.8 1.0

1

2

3

4

Distributions For State Variables

E !xA" ! 0.31

E !xB" ! 0.37

25 / 25

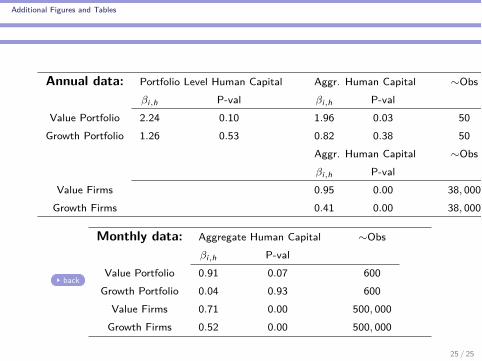

Additional Figures and Tables

Annual data: Portfolio Level Human Capital Aggr. Human Capital ≥Obs—i,h P-val —i,h P-val

Value Portfolio 2.24 0.10 1.96 0.03 50Growth Portfolio 1.26 0.53 0.82 0.38 50

Aggr. Human Capital ≥Obs—i,h P-val

Value Firms 0.95 0.00 38, 000Growth Firms 0.41 0.00 38, 000

back

Monthly data: Aggregate Human Capital ≥Obs—i,h P-val

Value Portfolio 0.91 0.07 600Growth Portfolio 0.04 0.93 600

Value Firms 0.71 0.00 500, 000Growth Firms 0.52 0.00 500, 000

25 / 25

Additional Figures and Tables

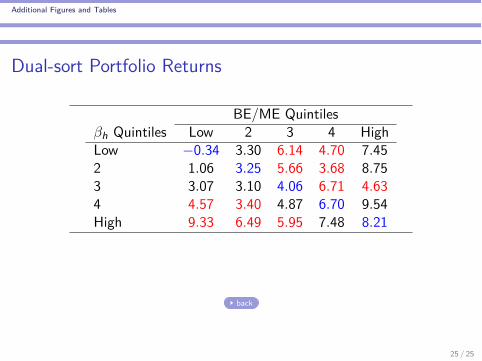

Dual-sort Portfolio Returns

BE/ME Quintiles—h Quintiles Low 2 3 4 HighLow ≠0.34 3.30 6.14 4.70 7.452 1.06 3.25 5.66 3.68 8.753 3.07 3.10 4.06 6.71 4.634 4.57 3.40 4.87 6.70 9.54High 9.33 6.49 5.95 7.48 8.21

back

25 / 25

Additional Figures and Tables

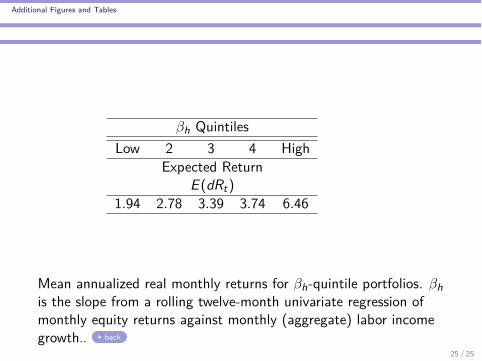

—h QuintilesLow 2 3 4 High

Expected ReturnE (dRt)

1.94 2.78 3.39 3.74 6.46

Mean annualized real monthly returns for —h-quintile portfolios. —his the slope from a rolling twelve-month univariate regression ofmonthly equity returns against monthly (aggregate) labor incomegrowth.. back

25 / 25

Additional Figures and Tables

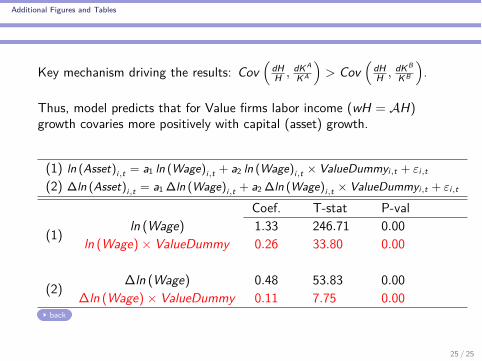

Key mechanism driving the results: Cov1

dHH , dKA

KA

2> Cov

1dHH , dKB

KB

2.

Thus, model predicts that for Value firms labor income (wH = AH)growth covaries more positively with capital (asset) growth.

(1) ln (Asset)i,t = a1 ln (Wage)i,t + a2 ln (Wage)i,t ◊ ValueDummyi,t + Ái,t

(2) �ln (Asset)i,t = a1 �ln (Wage)i,t + a2 �ln (Wage)i,t ◊ ValueDummyi,t + Ái,t

Coef. T-stat P-val

(1) ln (Wage) 1.33 246.71 0.00ln (Wage) ◊ ValueDummy 0.26 33.80 0.00

(2) �ln (Wage) 0.48 53.83 0.00�ln (Wage) ◊ ValueDummy 0.11 7.75 0.00

back

25 / 25

Additional Figures and Tables

Below I control for the number (or growth rate) of employees

(1) ln (Asset)i,t = a1 ln (Wage)i,t + a2 ln (Wage)i,t ◊ ValueDummyi,t

+a3 ln (Emp)i,t + Ái,t

(2) �ln (Asset)i,t = a1 �ln (Wage)i,t + a2 �ln (Wage)i,t ◊ ValueDummyi,t

+a3 �ln (Emp)i,t + Ái,t

Coef. T-stat P-value

(1)ln (Wage) 1.68 391.53 0.00

ln (Wage) ◊ ValueDummy 0.11 21.69 0.00ln (Emp) ≠0.92 ≠134.67 0.00

(2)�ln (Wage) 0.30 53.83 0.00

�ln (Wage) ◊ ValueDummy 0.07 7.75 0.00�ln (Emp) 0.47 50.34 0.00

back

25 / 25

Additional Figures and Tables

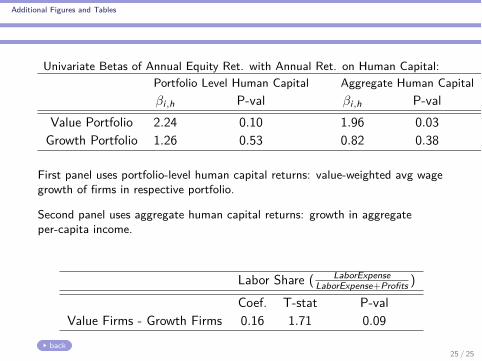

Univariate Betas of Annual Equity Ret. with Annual Ret. on Human Capital:Portfolio Level Human Capital Aggregate Human Capital—i,h P-val —i,h P-val

Value Portfolio 2.24 0.10 1.96 0.03Growth Portfolio 1.26 0.53 0.82 0.38

First panel uses portfolio-level human capital returns: value-weighted avg wagegrowth of firms in respective portfolio.

Second panel uses aggregate human capital returns: growth in aggregateper-capita income.

Labor Share ( LaborExpenseLaborExpense+Profits )

Coef. T-stat P-valValue Firms - Growth Firms 0.16 1.71 0.09

back25 / 25

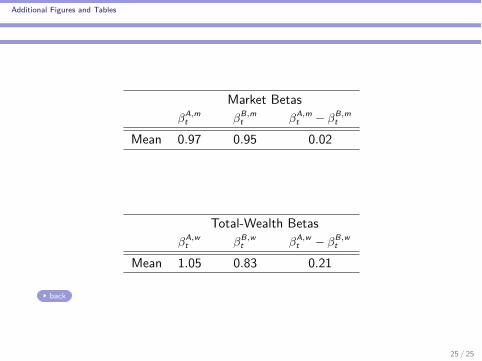

Additional Figures and Tables

Market Betas—A,m

t —B,mt —A,m

t ≠ —B,mt

Mean 0.97 0.95 0.02

Total-Wealth Betas—A,w

t —B,wt —A,w

t ≠ —B,wt

Mean 1.05 0.83 0.21

back

25 / 25

Additional Figures and Tables

Mean Returns and Univariate Regression Betas

Quantiles of BE/ME

Low 2 3 4 5 6 7 8 9 10—i,h 0.04 0.01 0.23 ≠0.07 0.09 0.03 0.32 0.70 0.24 0.57—i,m 1.08 1.00 1.05 1.09 1.02 0.99 0.98 0.97 1.00 0.91

—i,prem 0.39 0.51 0.61 0.58 0.60 0.49 0.58 0.54 0.63 0.66E(Ri ) 0.46 0.53 0.64 0.58 0.59 0.53 0.61 0.61 0.69 0.72

11 12 13 14 15 16 17 18 19 High—i,h 0.68 0.27 0.31 0.82 0.98 0.75 1.12 0.71 0.84 1.11—i,m 0.92 0.91 0.93 0.91 0.94 0.95 1.01 0.93 0.98 1.12

—i,prem 0.72 0.61 0.65 0.61 0.70 0.64 0.81 0.82 0.67 1.11E(Ri ) 0.83 0.66 0.69 0.73 0.84 0.81 1.00 0.87 0.78 1.29

back 25 / 25

Additional Figures and Tables

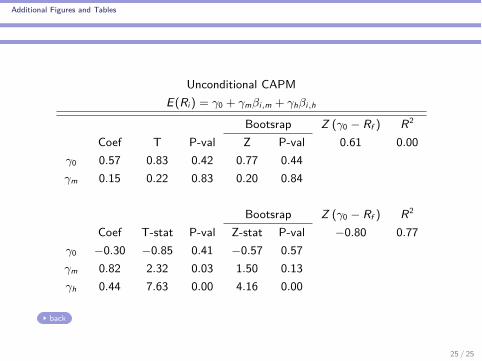

Unconditional CAPME(Ri) = “0 + “m—i,m + “h—i,h

Bootsrap Z (“0 ≠ Rf ) R2

Coef T P-val Z P-val 0.61 0.00“0 0.57 0.83 0.42 0.77 0.44“m 0.15 0.22 0.83 0.20 0.84

Bootsrap Z (“0 ≠ Rf ) R2

Coef T-stat P-val Z-stat P-val ≠0.80 0.77“0 ≠0.30 ≠0.85 0.41 ≠0.57 0.57“m 0.82 2.32 0.03 1.50 0.13“h 0.44 7.63 0.00 4.16 0.00

back

25 / 25

Additional Figures and Tables

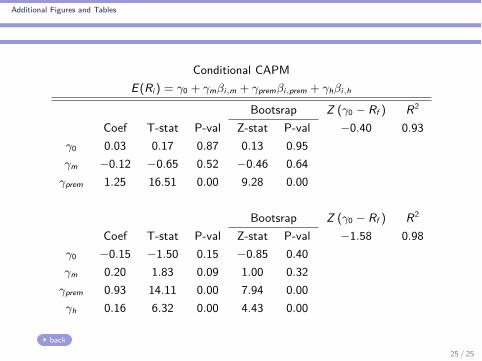

Conditional CAPME(Ri) = “0 + “m—i,m + “prem—i,prem + “h—i,h

Bootsrap Z (“0 ≠ Rf ) R2

Coef T-stat P-val Z-stat P-val ≠0.40 0.93“0 0.03 0.17 0.87 0.13 0.95“m ≠0.12 ≠0.65 0.52 ≠0.46 0.64

“prem 1.25 16.51 0.00 9.28 0.00

Bootsrap Z (“0 ≠ Rf ) R2

Coef T-stat P-val Z-stat P-val ≠1.58 0.98“0 ≠0.15 ≠1.50 0.15 ≠0.85 0.40“m 0.20 1.83 0.09 1.00 0.32

“prem 0.93 14.11 0.00 7.94 0.00“h 0.16 6.32 0.00 4.43 0.00

back25 / 25

Additional Figures and Tables

.4.6

.81

1.2

1.4

Re

aliz

ed

Ave

rag

e R

etu

rn (

%)

.4 .6 .8 1 1.2Predicted Expected Return (%)

Conditional CAPM w/o Human Capital

.4.6

.81

1.2

1.4

Re

aliz

ed

Ave

rag

e R

etu

rn (

%)

.4 .6 .8 1 1.2Predicted Expected Return (%)

Conditional CAPM w/ Human Capital

E (Ri) = “0 + “m—i ,m E (Ri) = “0 + “m—i ,m + “h—i ,h

25 / 25

Additional Figures and Tables

5 10 15 20 25

!0.03

!0.02

!0.01

0.01

0.02

0.03

Relative BE!ME :

1

qA !1

qB

" dZA" dZB

5 10 15 20 25

!0.5

0.5

1.0!""

Expected Excess Return :

Et!dRA" ! Et!dRB"

# dZA # dZB

5 10 15 20 25

!4

!2

2

4

6

!""

Investment!to!Human

Capital Ratio : ΙH

5 10 15 20 25

!0.10

!0.05

0.05

0.10

0.15

!""

Consumption!to!Total

Capital Ratio : c

back

25 / 25

Additional Figures and Tables

5 10 15 20 25

!6

!4

!2

2

4

6

!""

Investment!to!Physical

Capital Ratio : ΙA

5 10 15 20 25

!5

5

10!""

Investment!to!Physical

Capital Ratio : ΙB

5 10 15 20 25

!4

!2

2

4

6

!""

Investment!to!Human

Capital Ratio : ΙH

5 10 15 20 25

!0.10

!0.05

0.05

0.10

0.15

!""

Consumption!to!Total

Capital Ratio : c

+dZ A

+dZ B

25 / 25

Additional Figures and Tables

5 10 15 20

!3.0

!2.5

!2.0

!1.5

!1.0

!0.5

!""

Price of Risk :

Σt,$!1"

% !Α dZA % dZB"

5 10 15 20

1

2

3

4

!!"

Price of Risk :

Σt,#!2"

$ !Α dZA $ dZB"

25 / 25

Additional Figures and Tables

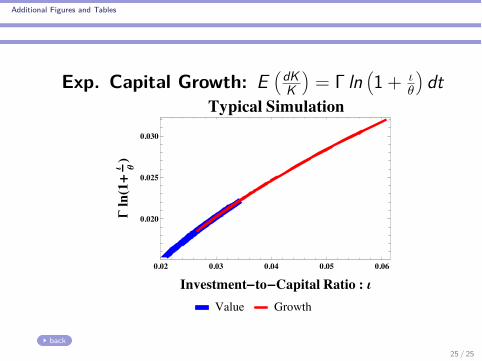

Exp. Capital Growth: E1dK

K2= � ln

11 + ÿ

◊

2dt

0.02 0.03 0.04 0.05 0.06

0.020

0.025

0.030

Investment-to-Capital Ratio : i

GlnH1+

i qLTypical Simulation

Value Growth

back25 / 25

Additional Figures and Tables

BE/ME: 1q = �

ÿ+◊

0.02 0.03 0.04 0.05 0.06

0.35

0.40

0.45

0.50

0.55

Investment-to-Capital Ratio : i

BEêME

Ratio:1 q

Typical Simulation

Value Growth

back25 / 25

Appendix

To calculate the returns on the Value and Growth stocks I merge monthlyreturns data from CRSP with fundamentals data from Compustat for the years1963-2012. Following the approach of Fama and French (1993 and 1996), Iform Value and Growth portfolios using the top thirtieth and the bottomthirtieth percentiles of BE/ME distributions with the BE/ME cut-o�s from theKenneth R. French Data Library.

BE is the sum of book equity, deferred taxes, and investment tax credit, minusthe book value of preferred stock for fiscal year t ≠ 1. ME is the value ofcommon equity at the end of year t ≠ 1. I then calculate returns from July ofyear t through June of year t + 1.

The mean return shown in the tables for the Value and Growth portfolios is theannualized average monthly returns. I multiply the average monthly return bytwelve and the standard deviation by the square-root of twelve.

I adjust the security returns for inflation using the GDP deflator. I use atwo-year rolling geometric average of the GDP deflator. I do so because Icalculate the security returns in data from July through June as done in Famaand French (1993; 1996). back

25 / 25

Appendix

The model is consistent with a setting where agents can invest inhuman capital by acquiring more schooling.

The adjustment cost for human capital may reflect someopportunity cost of time spent on schooling (as a means ofinvesting in human capital), psychic costs, or a reduction of thetime spent on leisure activities that are valuable to agents

The adjustment cost for physical capital may reflect some frictionsto capital reallocation, installation costs, or more general forms ofcapital illiquidity

In the model adj. costs are necessary for time-varying BE/ME andto ensure that both types of firms co-exist in equilibrium

back

25 / 25

Appendix

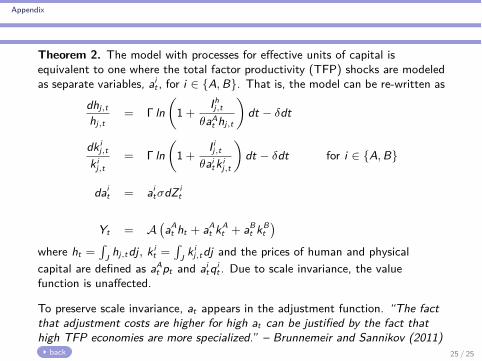

Theorem 2. The model with processes for e�ective units of capital isequivalent to one where the total factor productivity (TFP) shocks are modeledas separate variables, ai

t , for i œ {A, B}. That is, the model can be re-written asdhj,thj,t

= � ln3

1 +Ihj,t

◊aAt hj,t

4dt ≠ ”dt

dk ij,t

k ij,t

= � ln3

1 +I ij,t

◊aitk i

j,t

4dt ≠ ”dt for i œ {A, B}

dait = ai

t‡dZ it

Yt = A!aA

t ht + aAt kA

t + aBt kB

t"

where ht =s

J hj,tdj, k it =

sJ k i

j,tdj and the prices of human and physicalcapital are defined as aA

t pt and aitqi

t . Due to scale invariance, the valuefunction is una�ected.

To preserve scale invariance, at appears in the adjustment function. “The factthat adjustment costs are higher for high at can be justified by the fact thathigh TFP economies are more specialized.” – Brunnemeir and Sannikov (2011)

back 25 / 25

Appendix

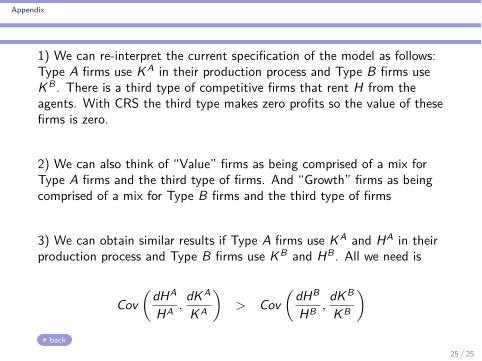

1) We can re-interpret the current specification of the model as follows:Type A firms use KA in their production process and Type B firms useKB . There is a third type of competitive firms that rent H from theagents. With CRS the third type makes zero profits so the value of thesefirms is zero.

2) We can also think of “Value” firms as being comprised of a mix forType A firms and the third type of firms. And “Growth” firms as beingcomprised of a mix for Type B firms and the third type of firms

3) We can obtain similar results if Type A firms use KA and HA in theirproduction process and Type B firms use KB and HB . All we need is

Cov3

dHA

HA ,dKA

KA

4> Cov

3dHB

HB ,dKB

KB

4

back25 / 25

Appendix

There are 2 state variables, x it =

Kit

Ht+KA+KB for i œ {A, B}.

We can write the value function as

V)

H + KA + KB , xA, xB*=

11 ≠ “

!!H + KA + KB"

F)

xA, xB*"1≠“

The Hamiltonian-Jacobi-Bellman (HJB) equation is

0 = maxIA,IB ,IH

f {C , V } dt + VHE (dH)

+VAE!dKA"

+ VBE!dKB"

+12

1VAA

!dKA"2

+ VBB!dKB"2

+ VHH (dH)2 + 2VAHdHdKA2

dH, dKA, dKB are given by the pre-specified LOM’sE (dH), E (dKA), and E (dKB) are the drifts and

Ct = Yt ≠!IAt + IB

t + IHt

"

Solution (back)

25 / 25

Appendix

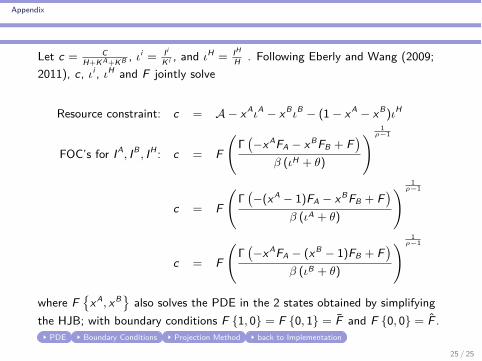

Let c = CH+KA+KB , ÿi = I i

K i , and ÿH = IH

H . Following Eberly and Wang (2009;2011), c, ÿi , ÿH and F jointly solve

Resource constraint: c = A ≠ xAÿA ≠ xBÿB ≠ (1 ≠ xA ≠ xB)ÿH

FOC’s for IA, IB , IH : c = F

A�

!≠xAFA ≠ xBFB + F

"

— (ÿH + ◊)

B 1fl≠1

c = F

A�

!≠(xA ≠ 1)FA ≠ xBFB + F

"

— (ÿA + ◊)

B 1fl≠1

c = F

A�

!≠xAFA ≠ (xB ≠ 1)FB + F

"

— (ÿB + ◊)

B 1fl≠1

where F)

xA, xB*also solves the PDE in the 2 states obtained by simplifying

the HJB; with boundary conditions F {1, 0} = F {0, 1} = F and F {0, 0} = F .PDE Boundary Conditions Projection Method back to Implementation

25 / 25

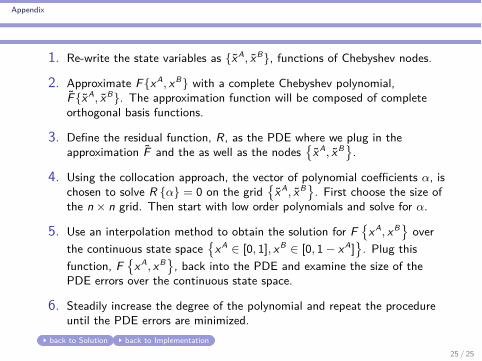

Appendix

1. Re-write the state variables as {xA, xB}, functions of Chebyshev nodes.

2. Approximate F{xA, xB} with a complete Chebyshev polynomial,F{xA, xB}. The approximation function will be composed of completeorthogonal basis functions.

3. Define the residual function, R, as the PDE where we plug in theapproximation F and the as well as the nodes

)xA, xB*

.

4. Using the collocation approach, the vector of polynomial coe�cients –, ischosen to solve R {–} = 0 on the grid

)xA, xB*

. First choose the size ofthe n ◊ n grid. Then start with low order polynomials and solve for –.

5. Use an interpolation method to obtain the solution for F)

xA, xB*over

the continuous state space)

xA œ [0, 1], xB œ [0, 1 ≠ xA]*

. Plug thisfunction, F

)xA, xB*

, back into the PDE and examine the size of thePDE errors over the continuous state space.

6. Steadily increase the degree of the polynomial and repeat the procedureuntil the PDE errors are minimized.

back to Solution back to Implementation25 / 25

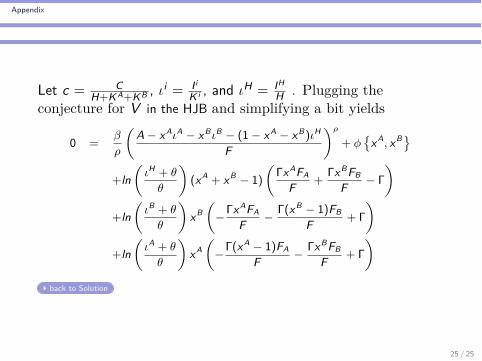

Appendix

Let c = CH+KA+KB , ÿi = I i

K i , and ÿH = IHH . Plugging the

conjecture for V in the HJB and simplifying a bit yields

0 =—fl

3A ≠ xAÿA ≠ xBÿB ≠ (1 ≠ xA ≠ xB)ÿH

F

4fl

+ „)

xA, xB*

+ln3

ÿH + ◊◊

4(xA + xB ≠ 1)

3�xAFA

F +�xBFB

F ≠ �

4

+ln3

ÿB + ◊◊

4xB

3≠�xAFA

F ≠ �(xB ≠ 1)FBF + �

4

+ln3

ÿA + ◊◊

4xA

3≠�(xA ≠ 1)FA

F ≠ �xBFBF + �

4

back to Solution

25 / 25

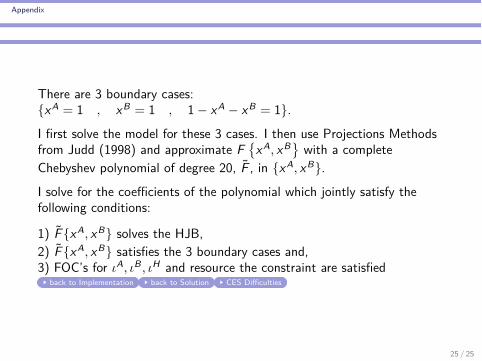

Appendix

There are 3 boundary cases:{xA = 1 , xB = 1 , 1 ≠ xA ≠ xB = 1}.

I first solve the model for these 3 cases. I then use Projections Methodsfrom Judd (1998) and approximate F

)xA, xB*

with a completeChebyshev polynomial of degree 20, F , in {xA, xB}.

I solve for the coe�cients of the polynomial which jointly satisfy thefollowing conditions:

1) F{xA, xB} solves the HJB,2) F{xA, xB} satisfies the 3 boundary cases and,3) FOC’s for ÿA, ÿB , ÿH and resource the constraint are satisfied

back to Implementation back to Solution CES Di�culties

25 / 25

Appendix

Proposition 1We can decentralize the planner’s problem as follows.1) Agent endowed with H0, takes wage rate Êt , price of human capital pt , andinitial financial wealth W0 as given. Agent has access to a risk-less bond withreturn rt and a risky claims. Risky security prices: St = {S(A)

t , S(B)t }

Õ follows

dSt =1

µÕ

t diag (St) ≠ Dt2

dt +A

S(A)t ÎAÕ

tS(B)

t ÎBÕ

t

BdZt

The agent solves

max{Cj,t ,IH

j,t ,Hj,t ,Èj,t }Œt=0

E0

⁄ Œ

0f (Cj,t , Vj,t) dt s.t.:

dWj,t =!Wj,trt + Èj,t · Wj,t(µt ≠ 1rt) ≠ Cj,t ≠ IH

j,t + ÊtHj,t"

dt + ÈÕj,tWj,tÎtdZt

dHj,t/Hj,t = � ln3

1 +IHj,t

◊Hj,t

4dt ≠ ”dt + ‡hdZ A

t

Èj,t = {ÈAj,t , ÈB

j,t}Õ : fraction of Wj,t invested in risky securitiesand Ît is a 2 ◊ 2 matrix Proposition 1 Summary

25 / 25

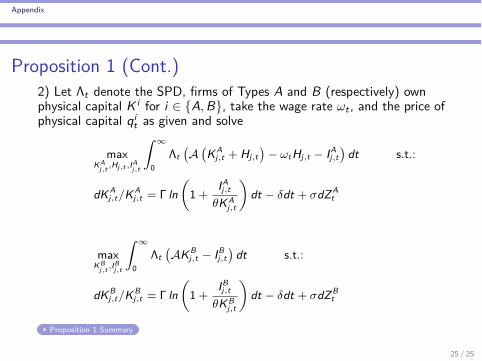

Appendix

Proposition 1 (Cont.)2) Let ⇤t denote the SPD, firms of Types A and B (respectively) ownphysical capital K i for i œ {A, B}, take the wage rate Êt , and the price ofphysical capital qi

t as given and solve

maxKA

j,t ,Hj,t ,IAj,t

⁄ Œ

0⇤t

!A

!KA

j,t + Hj,t"

≠ ÊtHj,t ≠ IAj,t

"dt s.t.:

dKAj,t/KA

j,t = � ln3

1 +IAj,t

◊KAj,t

4dt ≠ ”dt + ‡dZ A

t

maxKB

j,t ,IBj,t

⁄ Œ

0⇤t

!AKB

j,t ≠ IBj,t

"dt s.t.:

dKBj,t/KB

j,t = � ln3

1 +IBj,t

◊KBj,t

4dt ≠ ”dt + ‡dZ B

t

Proposition 1 Summary

25 / 25

Appendix

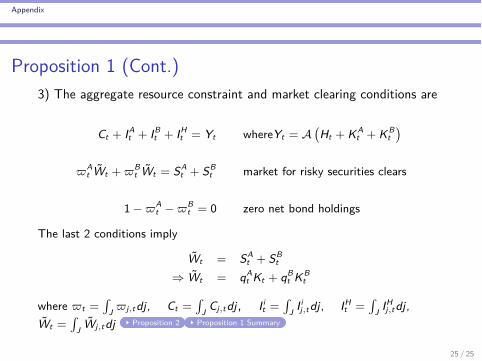

Proposition 1 (Cont.)3) The aggregate resource constraint and market clearing conditions are

Ct + IAt + IB

t + IHt = Yt whereYt = A

!Ht + KA

t + KBt

"

ÈAt Wt + ÈB

t Wt = SAt + SB

t market for risky securities clears

1 ≠ ÈAt ≠ ÈB

t = 0 zero net bond holdings

The last 2 conditions imply

Wt = SAt + SB

t

∆ Wt = qAt Kt + qB

t KBt

where Èt =s

J Èj,tdj, Ct =s

J Cj,tdj, I it =

sJ I i

j,tdj, IHt =

sJ IH

j,tdj,Wt =

sJ Wj,tdj Proposition 2 Proposition 1 Summary

25 / 25

Appendix

Ct + IAt + IB

t + IHt = Yt whereYt = A

!Ht + KA

t + KBt

"

ÈAt Wt + ÈB

t Wt = SAt + SB

t market for risky securities clears1 ≠ ÈA

t ≠ ÈBt = 0 zero net bond holdings

The last 2 conditions implyWt = SA

t + SBt

∆ Wt = qAt Kt + qB

t KBt

Using the static constraint

Wt = Et

⁄ Œ

t

⇤s⇤t

!Cs + IH

s ≠ ÊsHs"

ds

Using SHt = ptHt = Et

s Œt

⇤s⇤t

!AHs ≠ IH

s"

ds (given by FOCs and Prop. 2)back Proposition 2

Et

⁄ Œ

t

⇤s⇤t

!Cs + IH

s ≠ ÊsHs"

ds = qAt Kt + qB

t KBt

∆ Et

⁄ Œ

t

⇤s⇤t

Cs ds = ptHt + qAt Kt + qB

t KBt as expected

25 / 25

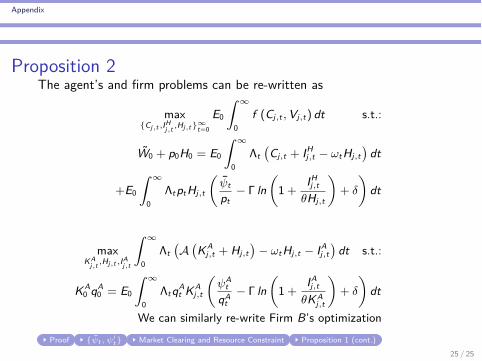

Appendix

Proposition 2The agent’s and firm problems can be re-written as

max{Cj,t ,IH

j,t ,Hj,t }Œt=0

E0

⁄ Œ

0f (Cj,t , Vj,t) dt s.t.:

W0 + p0H0 = E0

⁄ Œ

0⇤t

!Cj,t + IH

j,t ≠ ÊtHj,t"

dt

+E0

⁄ Œ

0⇤tptHj,t

3Âtpt

≠ � ln3

1 +IHj,t

◊Hj,t

4+ ”

4dt

maxKA

j,t ,Hj,t ,IAj,t

⁄ Œ

0⇤t

!A

!KA

j,t + Hj,t"

≠ ÊtHj,t ≠ IAj,t

"dt s.t.:

KA0 qA

0 = E0

⁄ Œ

0⇤tqA

t KAj,t

3ÂA

tqA

t≠ � ln

31 +

IAj,t

◊KAj,t

4+ ”

4dt

We can similarly re-write Firm B’s optimizationProof {Ât , Âi

t } Market Clearing and Resource Constraint Proposition 1 (cont.)25 / 25

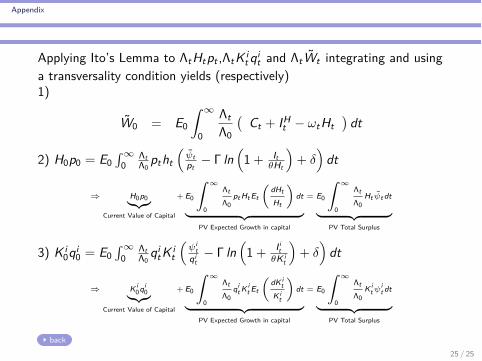

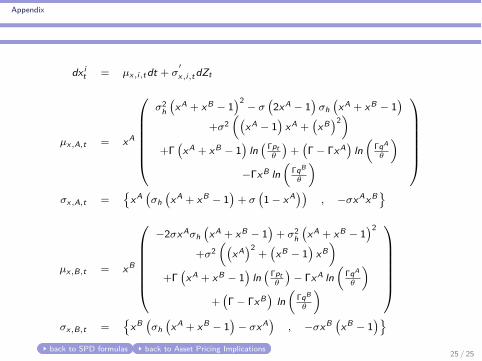

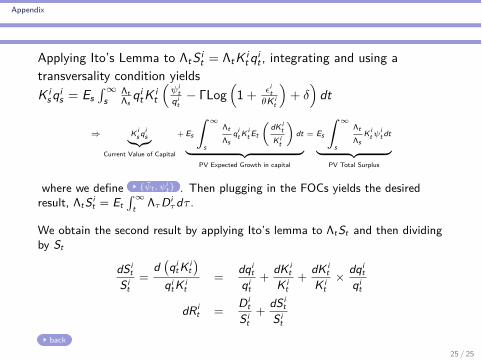

Appendix

Applying Ito’s Lemma to ⇤tHtpt ,⇤tK it qi

t and ⇤tWt integrating and usinga transversality condition yields (respectively)1)

W0 = E0

⁄ Œ

0

⇤t⇤0

!Ct + IH

t ≠ ÊtHt"

dt

2) H0p0 = E0s Œ

0⇤t⇤0

ptht1

Âtpt

≠ � ln1

1 + It◊Ht

2+ ”

2dt

∆ H0p0¸˚˙˝Current Value of Capital

+ E0

⁄ Œ

0

⇤t⇤0

pt Ht Et

1dHtHt

2dt

¸ ˚˙ ˝PV Expected Growth in capital

= E0

⁄ Œ

0

⇤t⇤0

Ht Ât dt

¸ ˚˙ ˝PV Total Surplus

3) K i0qi

0 = E0s Œ

0⇤t⇤0

qitK i

t

1Âi

tqi

t≠ � ln

11 + I i

t◊Ki

t

2+ ”

2dt

∆ Ki0qi

0¸˚˙˝Current Value of Capital

+ E0

⁄ Œ

0

⇤t⇤0

qit K i

t Et

1dKi

tK i

t

2dt

¸ ˚˙ ˝PV Expected Growth in capital

= E0

⁄ Œ

0

⇤t⇤0

Kit Âi

t dt

¸ ˚˙ ˝PV Total Surplus

back25 / 25

Appendix

Ât © pt

1≠Et

Ëd(⇤tpt)

⇤tpt

È+ ‡h‡

(A)⇤,t

2

Âit © qi

t

3≠Et

5d(⇤tqi

t)

⇤tqit

6+ ‡‡

(i)⇤,i,t

4

‡⇤,t = {‡(A)⇤,t , ‡

(B)⇤,t }

Õ= Di�usion

Ëd(⇤tpt)

⇤tpt

È

‡⇤,i,t = {‡(A)⇤,i,t , ‡

(B)⇤,i,t}

Õ= Di�usion

5d(⇤tqi

t)

⇤tqit

6

In equilibrium we have

FOC for Cand H: Ât = Êt¸˚˙˝marginal benefit from human capital

≠1

≠pt

1� ln

1pt

�

◊

2≠ ”

2+ pt� ≠ ◊

2

¸ ˚˙ ˝marginal cost to human capital

FOC for Ki : Âit = A¸˚˙˝

marginal product of physical capital

≠1

≠qit

1� ln

1qi

t�

◊

2≠ ”

2+ qi

t� ≠ ◊

2

¸ ˚˙ ˝marginal cost to physical capital

back to Prop2 back to AP25 / 25

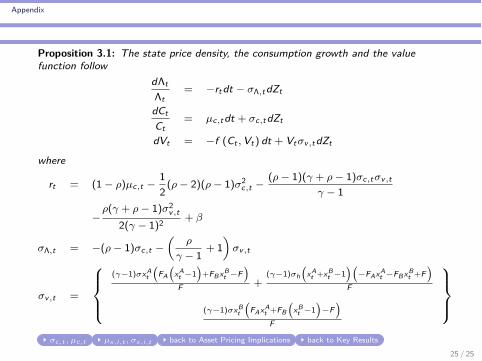

Appendix

Proposition 3.1: The state price density, the consumption growth and the valuefunction follow

d⇤t⇤t

= ≠rtdt ≠ ‡⇤,tdZt

dCtCt

= µc,tdt + ‡c,tdZt

dVt = ≠f (Ct , Vt) dt + Vt‡v,tdZt

where

rt = (1 ≠ fl)µc,t ≠12(fl ≠ 2)(fl ≠ 1)‡2

c,t ≠(fl ≠ 1)(“ + fl ≠ 1)‡c,t‡v,t

“ ≠ 1

≠fl(“ + fl ≠ 1)‡2

v,t2(“ ≠ 1)2 + —

‡⇤,t = ≠(fl ≠ 1)‡c,t ≠1

fl

“ ≠ 1+ 1

2‡v,t

‡v,t =

Y_]

_[

(“≠1)‡xAt!

FA!

xAt ≠1

"+FBxB

t ≠F"

F +(“≠1)‡h

!xA

t +xBt ≠1

"!≠FAxA

t ≠FBxBt +F

"

F

(“≠1)‡xBt!

FAxAt +FB

!xB

t ≠1"

≠F"

F

Z_

_\

‡c,t , µc,t µx,i,t , ‡x,i,t back to Asset Pricing Implications back to Key Results25 / 25

Appendix

Ct = A!

Ht + KAt + KB

t"

≠ Ht!�pt

)xA

t , xBt

*≠ ◊

"≠ KA

t!�qA

t)

xAt , xB

t*

≠ ◊"

≠KBt

!�qB

t)

xAt , xB

t*

≠ ◊"

Using Ito’s Lemma

µc,t =1Ct

Q

ccca

ˆCtˆHt

◊ Ht

1� ln

11 +

IHt

◊Ht

2≠ ”

2+ 1

2ˆ2CtˆH2

t◊ Ht‡2

h + ˆ2CtˆHt ˆKA

t◊ HtKA

t ‡‡h

+ ˆCtˆKA

t◊ KA

t

1� ln

11 +

IAt

◊KAt

2≠ ”

2+ 1

2ˆ2Ct

ˆ(KAt )

2 ◊ KAt ‡2

+ ˆCtˆKB

t◊ KB

t

1� ln

11 +

IBt

◊KBt

2≠ ”

2+ 1

2ˆ2Ct

ˆ(KBt )

2 ◊ KBt ‡2

R

dddb

‡c,t =1Ct

;ˆCtˆHt

◊ Ht‡h +ˆCtˆKA

t◊ KA

t ‡ ,ˆCtˆKB

t◊ KB

t ‡

<

SPD Formulas back to Asset Pricing Implications

25 / 25

Appendix

dxit = µx,i,tdt + ‡

Õx,i,tdZt

µx,A,t = xA

Q

ccccca

‡2h!

xA + xB ≠ 1"2 ≠ ‡

!2xA ≠ 1

"‡h

!xA + xB ≠ 1

"

+‡21!

xA ≠ 1"

xA +!

xB"2

2

+�!

xA + xB ≠ 1"

ln!�pt◊

"+

!� ≠ �xA

"ln

1�qA

◊

2

≠�xB ln1

�qB

◊

2

R

dddddb

‡x,A,t =)

xA !‡h

!xA + xB ≠ 1

"+ ‡

!1 ≠ xA""

, ≠‡xAxB*

µx,B,t = xB

Q

ccccca

≠2‡xA‡h!

xA + xB ≠ 1"+ ‡2

h!

xA + xB ≠ 1"2

+‡21!

xA"2

+!

xB ≠ 1"

xB2

+�!

xA + xB ≠ 1"

ln!�pt◊

"≠ �xA ln

1�qA

◊

2

+!� ≠ �xB

"ln

1�qB

◊

2

R

dddddb

‡x,B,t =)

xB !‡h

!xA + xB ≠ 1

"≠ ‡xA"

, ≠‡xB !xB ≠ 1

"*

back to SPD formulas back to Asset Pricing Implications 25 / 25

Appendix

dRm = dRA qAKA

qAKA + qBKB + dRB qBKB

qAKA + qBKB

dRw =

Q

cadRH pH

pH+qAKA+qBKB + dRA qAKA

pH+qAKA+qBKB

+dRB qBKB

pH+qAKA+qBKB

R

db

back

25 / 25

Appendix

Applying Ito’s Lemma to ⇤tS it = ⇤tK i

t qit , integrating and using a

transversality condition yieldsK i

s qis = Es

s Œs

⇤t⇤s

qitK i

t

1Âi

tqi

t≠ �Log

11 + ‘i

t◊Ki

t

2+ ”

2dt

∆ Kis qi

s¸˚˙˝Current Value of Capital

+ Es

⁄ Œ

s

⇤t⇤s

qit K i

t Et

1dKi

tK i

t

2dt

¸ ˚˙ ˝PV Expected Growth in capital

= Es

⁄ Œ

s

⇤t⇤s

K it Âi

t dt

¸ ˚˙ ˝PV Total Surplus

where we define {Ât , Âit } . Then plugging in the FOCs yields the desired

result, ⇤tS it = Et

s Œt ⇤· Di

· d· .

We obtain the second result by applying Ito’s lemma to ⇤tSt and then dividingby St

dS it

S it

=d

!qi

tK it"

qitK i

t=

dqit

qit+

dK it

K it

+dK i

tK i

t◊ dqi

tqi

t

dR it =

Dit

S it+

dS it

S it

back25 / 25

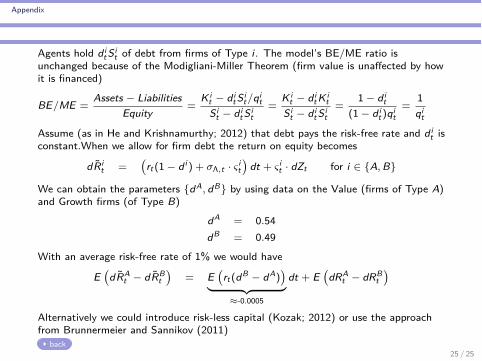

Appendix

Agents hold dit Si

t of debt from firms of Type i . The model’s BE/ME ratio isunchanged because of the Modigliani-Miller Theorem (firm value is una�ected by howit is financed)

BE/ME =Assets ≠ Liabilities

Equity=

Kit ≠ di

t Sit/qi

tSi

t ≠ dit Si

t=

Kit ≠ di

t K it

Sit ≠ di

t Sit

=1 ≠ di

t(1 ≠ di

t)qit=

1qi

t

Assume (as in He and Krishnamurthy; 2012) that debt pays the risk-free rate and dit is

constant.When we allow for firm debt the return on equity becomes

dRit =

!rt(1 ≠ di ) + ‡⇤,t · Î i

t"

dt + Î it · dZt for i œ {A, B}

We can obtain the parameters {dA, dB} by using data on the Value (firms of Type A)and Growth firms (of Type B)

dA = 0.54dB = 0.49

With an average risk-free rate of 1% we would have

E!

dRAt ≠ dRB

t"

= E!

rt(dB ≠ dA)"

¸ ˚˙ ˝¥-0.0005

dt + E!

dRAt ≠ dRB

t"

Alternatively we could introduce risk-less capital (Kozak; 2012) or use the approachfrom Brunnermeier and Sannikov (2011)

back25 / 25

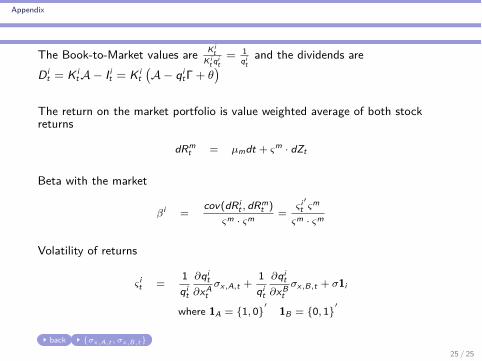

Appendix

The Book-to-Market values are Kit

Kit qi

t= 1

qit

and the dividends areDi

t = K it A ≠ I i

t = K it!A ≠ qi

t�+ ◊"

The return on the market portfolio is value weighted average of both stockreturns

dRmt = µmdt + Îm · dZt

Beta with the market

—i =cov(dRi

t , dRmt )

Îm · Îm =Î iÕt Îm

Îm · Îm

Volatility of returns

Î it =

1qi

t

ˆqit

ˆxAt

‡x,A,t +1qi

t

ˆqit

ˆxBt

‡x,B,t + ‡1i

where 1A = {1, 0}Õ

1B = {0, 1}Õ

back {‡x,A,t , ‡x,B,t }

25 / 25

Appendix

Set — = —, ” = 0, � = ◊, and ‡ = ‡h.

Search for 7 unknowns {◊, A, cú, F ú, “, fl, ‡} to solve 7 equations:I In a 1-capital economy: 1) output growth of 2% , 2) C

Y of 90%, 3)resource constraint, 4) FOC for investment, 5) HJB

I 6) risk-free rate of 0.90%, 7) volatility of market portfolio of 16%Note: there is no gov’t exp. so C/Y is higher than in data

CalibrationVariable Name/Calculation Value

A Marginal Product of Capital 20.63%cú Consumption

Capital in one-capital economy 18.63%F ú Normalized Value Function, F , in one-capital economy 0.0791“ Risk Aversion Parameter 3.97

� = ◊ Adjustment Cost Parameters 2.73%fl Implied IES Parameter = 2.0025 0.5006

‡ = ‡h Standard deviation of Capital Growth 21.27%back Alternative Calibration

25 / 25

Appendix

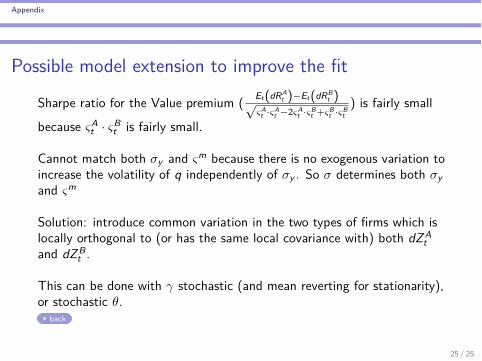

Possible model extension to improve the fit

Sharpe ratio for the Value premium ( Et(dRAt )≠Et(dRB

t )ÔÎA

t ·ÎAt ≠2ÎA

t ·ÎBt +ÎB

t ·ÎBt

) is fairly small

because ÎAt · ÎB

t is fairly small.

Cannot match both ‡y and Îm because there is no exogenous variation toincrease the volatility of q independently of ‡y . So ‡ determines both ‡yand Îm

Solution: introduce common variation in the two types of firms which islocally orthogonal to (or has the same local covariance with) both dZA

tand dZB

t .

This can be done with “ stochastic (and mean reverting for stationarity),or stochastic ◊.

back

25 / 25

Appendix

Impulse Responses

Let ‰t denote a given endogenous variable of the model. Following Koop,Pesaran and Potter (1996) and Kozak (2012), I construct two non-linearimpulse responses for ‰t using

IRF‰

)xA

t , xBt

*= E

1‰t

---xA0 = xA, xB

0 = xB , dZ0 = 1i

2

1i œÓ

{1, 0}Õ, {0, 1}

Õ, {0.5, 1}

ÕÔ

Thus, starting at the mean values for the state variables {xA, xB}, I introduce aone-standard-deviation positive shock through dZ A or dZ B or both at date zeroand simulate twenty-five years of observations one-hundred-thousand times. Ithen compute the average across simulations. I define the impulse responserelative to a baseline with no shock at date zero. back

25 / 25

Appendix

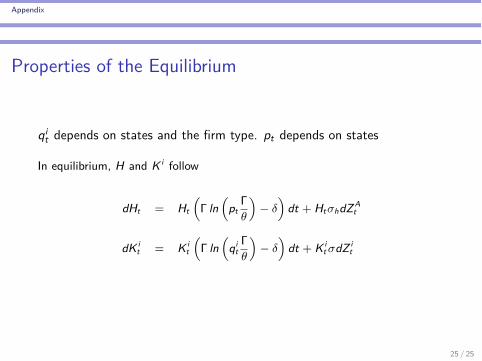

Properties of the Equilibrium

qit depends on states and the firm type. pt depends on states

In equilibrium, H and K i follow

dHt = Ht

1� ln

1pt

�◊

2≠ ”

2dt + Ht‡hdZ A

t

dK it = K i

t

1� ln

1qi

t�◊

2≠ ”

2dt + K i

t ‡dZ it

25 / 25

Appendix

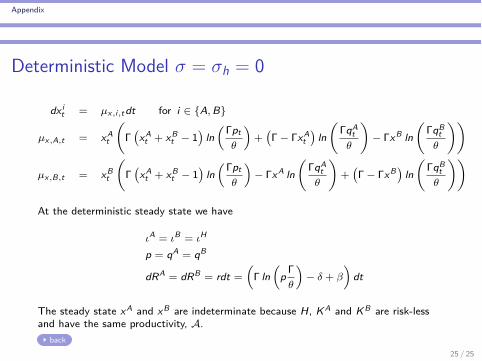

Deterministic Model ‡ = ‡h = 0

dxit = µx,i,tdt for i œ {A, B}

µx,A,t = xAt

3�

!xA

t + xBt ≠ 1

"ln

1�pt◊

2+

!� ≠ �xA

t"

ln3

�qAt

◊

4≠ �xB ln

3�qB

t◊

44

µx,B,t = xBt

3�

!xA

t + xBt ≠ 1

"ln

1�pt◊

2≠ �xA ln

3�qA

t◊

4+

!� ≠ �xB"

ln3

�qBt

◊

44

At the deterministic steady state we have

ÿA = ÿB = ÿH

p = qA = qB

dRA = dRB = rdt =1� ln

1p �

◊

2≠ ” + —

2dt

The steady state xA and xB are indeterminate because H, KA and KB are risk-lessand have the same productivity, A.

back25 / 25

Appendix

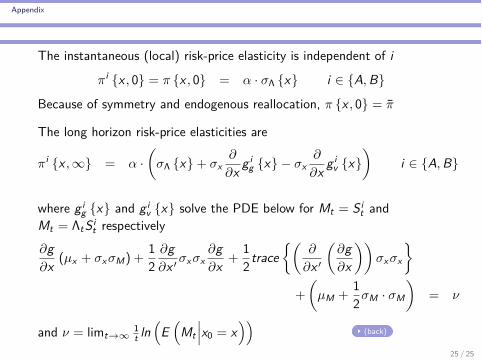

The instantaneous (local) risk-price elasticity is independent of i

fii {x , 0} = fi {x , 0} = – · ‡⇤ {x} i œ {A, B}

Because of symmetry and endogenous reallocation, fi {x , 0} = fi

The long horizon risk-price elasticities are

fii {x , Œ} = – ·3

‡⇤ {x} + ‡xˆ

ˆx g ig {x} ≠ ‡x

ˆ

ˆx g iv {x}

4i œ {A, B}

where g ig {x} and g i

v {x} solve the PDE below for Mt = S it and

Mt = ⇤tS it respectively

ˆgˆx (µx + ‡x ‡M) +

12

ˆgˆx Õ ‡x ‡x

ˆgˆx +

12 trace

;3ˆ

ˆx Õ

3ˆgˆx

44‡x ‡x

<

+

3µM +

12‡M · ‡M

4= ‹

and ‹ = limtæŒ1t ln

1E

1Mt

---x0 = x22

(back)

25 / 25

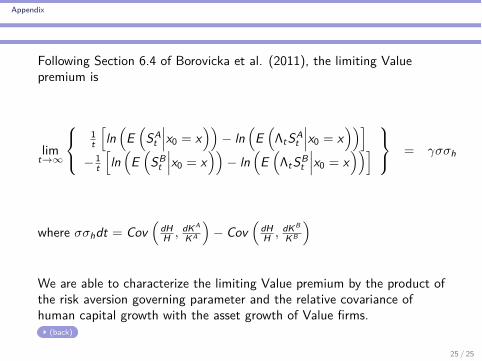

Appendix

Following Section 6.4 of Borovicka et al. (2011), the limiting Valuepremium is

limtæŒ

Y]

[

1t

Ëln

1E

1SA

t

---x0 = x22

≠ ln1

E1⇤tSA

t

---x0 = x22È

≠ 1t

Ëln

1E

1SB

t

---x0 = x22

≠ ln1

E1⇤tSB

t

---x0 = x22È

Z^

\ = “‡‡h

where ‡‡hdt = Cov1

dHH , dKA

KA

2≠ Cov

1dHH , dKB

KB

2

We are able to characterize the limiting Value premium by the product ofthe risk aversion governing parameter and the relative covariance ofhuman capital growth with the asset growth of Value firms.

(back)

25 / 25

Appendix

(back)

25 / 25

Appendix

!0.05 0.05 0.10 0.15 0.20 0.25

5

10

15

20

Distribution For Relative Risk!Price Elasticity

ΠA!x,#" ! ΠB!x,#"

E #ΠA !x, #" ! ΠB !x, #"$ $ 0.06

(back)

25 / 25

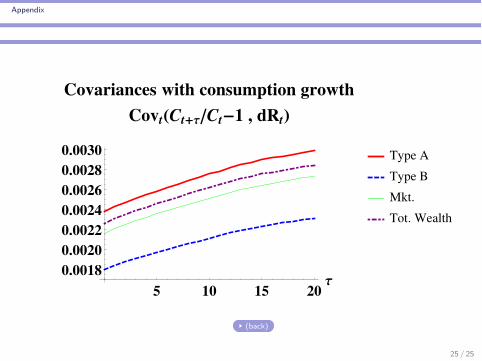

Appendix

5 10 15 20Τ

0.0018

0.0020

0.0022

0.0024

0.0026

0.0028

0.0030

Covariances with consumption growth

Covt!Ct"Τ"Ct#1 , dRt#

Type A

Type B

Mkt.

Tot. Wealth

(back)

25 / 25

Appendix

5 10 15 20Τ

"0.2

0.2

0.4

0.6

0.8

1.0

Autocorrelations with lag of Τ years

Μc

Et!dRA"

Et!dRB"

Et!dRm"

Et!dRw"

(back)

25 / 25

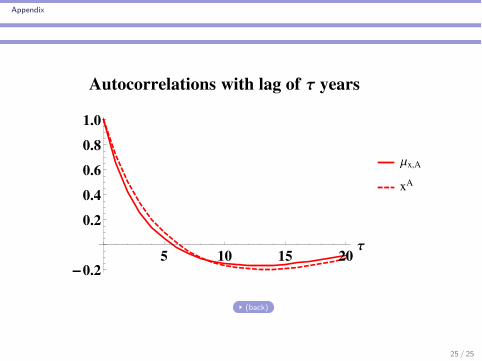

Appendix

5 10 15 20Τ

"0.2

0.2

0.4

0.6

0.8

1.0

Autocorrelations with lag of Τ years

Μx,A

xA

(back)

25 / 25

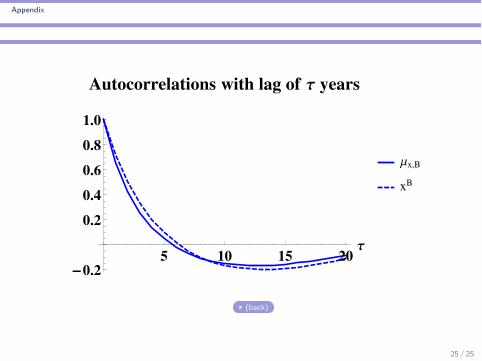

Appendix

5 10 15 20Τ

"0.2

0.2

0.4

0.6

0.8

1.0

Autocorrelations with lag of Τ years

Μx,B

xB

(back)

25 / 25

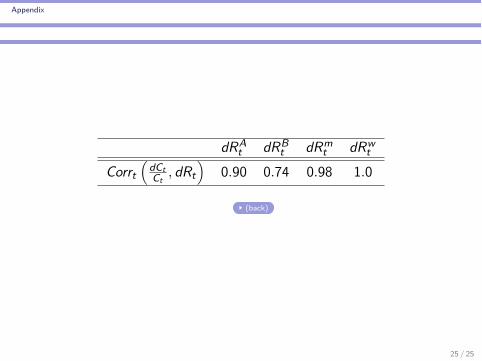

Appendix

dRAt dRB

t dRmt dRw

t

Corrt1

dCtCt

, dRt2

0.90 0.74 0.98 1.0

(back)

25 / 25

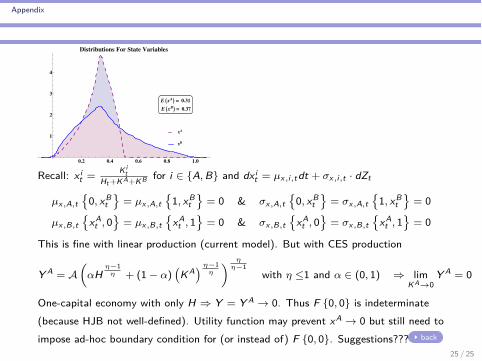

Appendix

xA

xB

0.2 0.4 0.6 0.8 1.0

1

2

3

4

Distributions For State Variables

E !xA" ! 0.31

E !xB" ! 0.37

Recall: x it =

Kit

Ht+KA+KB for i œ {A, B} and dxit = µx,i,tdt + ‡x,i,t · dZt

µx,A,t)

0, xBt

*= µx,A,t

)1, xB

t*

= 0 & ‡x,A,t)

0, xBt

*= ‡x,A,t

)1, xB

t*

= 0

µx,B,t)

xAt , 0

*= µx,B,t

)xA

t , 1*

= 0 & ‡x,B,t)

xAt , 0

*= ‡x,B,t

)xA

t , 1*

= 0

This is fine with linear production (current model). But with CES production

Y A = A1

–H÷≠1

÷ + (1 ≠ –)!

KA" ÷≠1÷

2 ÷÷≠1

with ÷ Æ1 and – œ (0, 1) ∆ limKAæ0

Y A = 0

One-capital economy with only H ∆ Y = Y A æ 0. Thus F {0, 0} is indeterminate(because HJB not well-defined). Utility function may prevent xA æ 0 but still need toimpose ad-hoc boundary condition for (or instead of) F {0, 0}. Suggestions??? back

25 / 25

Appendix

Constructing Modified HmL Portfolios

BE/ME Quintiles—h Quintiles Low 2 3 4 HighLow Short Short2 Short Short34 Long LongHigh Long Long

The modified HmL portfolios are long the Value portfolio and short the Growthportfolio. The Value portfolio is a value-weighted sum of securities in the cellslabelled “Long”. The Growth portfolio is a value-weighted sum of securities inthe cells labelled “Short”. Modified Portfolio 1 contains securities from all cellslabelled “Long” or “Short”. Modified Portfolio 2 contains only securitieslabelled in bold letters.

25 / 25

Appendix

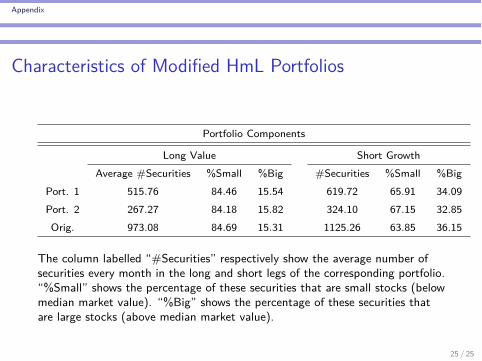

Characteristics of Modified HmL Portfolios

Portfolio Components

Long Value Short GrowthAverage #Securities %Small %Big #Securities %Small %Big

Port. 1 515.76 84.46 15.54 619.72 65.91 34.09Port. 2 267.27 84.18 15.82 324.10 67.15 32.85Orig. 973.08 84.69 15.31 1125.26 63.85 36.15

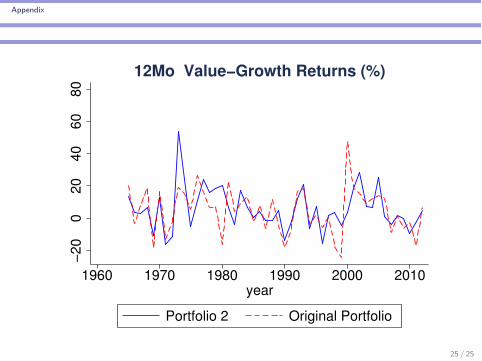

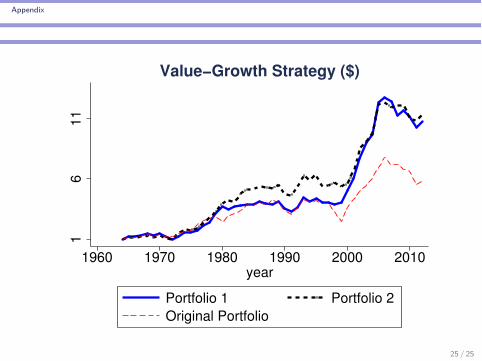

The column labelled “#Securities” respectively show the average number ofsecurities every month in the long and short legs of the corresponding portfolio.“%Small” shows the percentage of these securities that are small stocks (belowmedian market value). “%Big” shows the percentage of these securities thatare large stocks (above median market value).

25 / 25

Appendix

Performance of Modified HmL Portfolios

Portfolio Characteristics From Monthly Returns

Annualized (%) CAPM Results Correlations

E (R) ‡ (R) S.R. – — Port. 1 Port. 2 Orig. Mkt.

Port. 1 5.59 13.30 42.03 0.48 ≠0.03 1.00 0.89 0.54 ≠0.04

[3.00] [≠0.84]

Port. 2 5.70 13.37 42.63 0.51 ≠0.08 1.00 0.45 ≠0.10

[3.20] [≠2.29]

Orig. 4.08 10.60 38.49 0.38 ≠0.09 1.00 ≠0.13

[3.02] [≠3.23]

Mkt. 7.16 15.45 40.52 ≠ ≠ 1.00

Calculations are done with monthly portfolio returns. Returns are annualized bymultiplying the mean by 12 and the standard deviations by

Ô12.

25 / 25

Appendix

Portfolio Characteristics From Cumulative Annual Returns

(%) CAPM Results Correlations

E (Re ) ‡ (Re ) S.R. – — Port. 1 Port. 2 Orig. Mkt.

Port. 1 5.83 12.85 45.37 6.56 ≠0.14 1.00 0.83 0.62 ≠0.13

[10.82] [≠4.00]

Port. 2 5.94 13.13 45.24 7.39 ≠0.27 1.00 0.54 ≠0.31

[12.86] [≠8.28]

Orig. 4.70 14.15 33.22 5.83 ≠0.25 1.00 ≠0.29

[10.27] [≠7.87]

Mkt. 7.56 16.74 39.79 ≠ ≠ 1.00

Calculations are done with (twelve-month cumulative) annual portfolio returns.

25 / 25

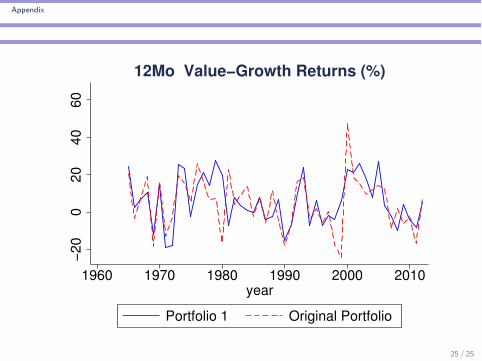

Appendix

−2

00

20

40

60

1960 1970 1980 1990 2000 2010year

Portfolio 1 Original Portfolio

12Mo Value−Growth Returns (%)

25 / 25

Appendix

−2

00

20

40

60

80

1960 1970 1980 1990 2000 2010year

Portfolio 2 Original Portfolio

12Mo Value−Growth Returns (%)

25 / 25

Appendix

16

11

1960 1970 1980 1990 2000 2010year

Portfolio 1 Portfolio 2

Original Portfolio

Value−Growth Strategy ($)

25 / 25