OF OUR TOURISM SECTOR

2015STATISTICS

63,3 %

22,1 %

4,3 %

0,3 %

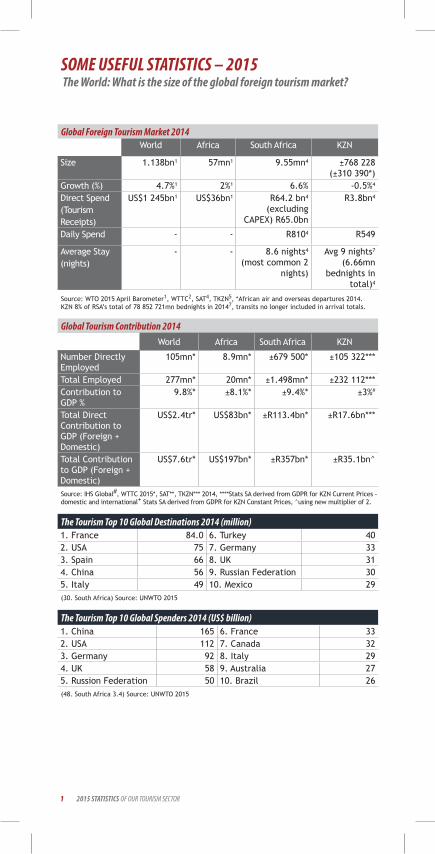

Source: WTO 2015 April Barometer1, WTTC2, SAT4, TKZN5, *African air and overseas departures 2014. KZN 8% of RSA’s total of 78 852 721mn bednights in 20147, transits no longer included in arrival totals.

Source: IHS Global#, WTTC 2015*, SAT**, TKZN*** 2014, ****Stats SA derived from GDPR for KZN Current Prices - domestic and international+ Stats SA derived from GDPR for KZN Constant Prices, ^using new multiplier of 2.

SOME USEFUL STATISTICS – 2015 The World: What is the size of the global foreign tourism market?

Global Foreign Tourism Market 2014

Global Tourism Contribution 2014

The Tourism Top 10 Global Destinations 2014 (million)

The Tourism Top 10 Global Spenders 2014 (US$ billion)

1 2015 STATISTICS OF OUR TOURISM SECTOR

(30. South Africa) Source: UNWTO 2015

(48. South Africa 3.4) Source: UNWTO 2015

World Africa South Africa KZN

Size 1.138bn1 57mn1 9.55mn4 ±768 228(±310 390*)

Growth (%) 4.7%1 2%1 6.6% -0.5%4

Direct Spend (Tourism Receipts)

US$1 245bn1 US$36bn1 R64.2 bn4 (excluding

CAPEX) R65.0bn

R3.8bn4

Daily Spend - - R8104 R549

Average Stay (nights)

- - 8.6 nights4 (most common 2

nights)

Avg 9 nights7 (6.66mn

bednights in total)4

World Africa South Africa KZN

Number Directly Employed

105mn* 8.9mn* ±679 500* ±105 322***

Total Employed 277mn* 20mn* ±1.498mn* ±232 112***Contribution to GDP %

9.8%* ±8.1%* ±9.4%* ±3%#

Total Direct Contribution to GDP (Foreign + Domestic)

US$2.4tr* US$83bn* ±R113.4bn* ±R17.6bn***

Total Contribution to GDP (Foreign + Domestic)

US$7.6tr* US$197bn* ±R357bn* ±R35.1bn^

1. France 84.0 6. Turkey 402. USA 75 7. Germany 33 3. Spain 66 8. UK 314. China 56 9. Russian Federation 305. Italy 49 10. Mexico 29

1. China 165 6. France 33 2. USA 112 7. Canada 32 3. Germany 92 8. Italy 294. UK 58 9. Australia 275. Russion Federation 50 10. Brazil 26

The South African Foreign Picture 2014:

South Africa’s Top 5 Overseas (Long Haul) Tourist Markets 2014:

South Africa’s Top 5 average spending markets per trip (excluding Capital Expenditure)

Source: SAT 2015, WTTC 2015

Source: SAT 2015

Source: SAT 2015

The Top 10 Global Generators of Tourists 2014:

(SA 5 168 000) Source: The World Bank 2015; UNWTO 2015

1. China 98 185 000 6. Russian Federation 54 069 0002. Hong Kong, China 84 414 000 7. Canada 32 977 0003. Germany 74 192 000 8. Italy 27 798 0004. USA 61 569 000 9. France 26 243 0005. UK 58 510 000 10. Ukraine 23 761 000

Numbers of Foreign Tourists 9.55mnSpend - pppd R810 (R7 000 per trip)Leisure Spend 66% of total, or R162.3bnBusiness Spend 34% of total, or R83.6bnAverage Length of Stay 8.6 nightsMain Overseas Source Markets UK, USA, Germany, France, NetherlandsSpend, Foreign vs Domestic 45.9% vs 54.1%

1. UK 401 9142. USA 309 2553. Germany 274 5714. France 131 5025. Netherlands 131 287

1. Malawi R19 7002. Zambia R17 6003. Australia R15 7004. Netherlands R15 600 5. Belgium R15 000

22015 STATISTICS OF OUR TOURISM SECTOR

Foreign Tourist Activities in South Africa 2014:Shopping 81.7%Nightlife 74.8%Social 53.6%Visiting Natural Attractions 16%Business 12.1%Cultural, Historical, Heritage 12.5%Beach 11.9%Wildlife 8.8%Theme Parks 10%Adventure 5.6%Source: SAT 2015

Purpose of Visit to South Africa

Source: SAT 2015

All Foreign Tourists (2014)Holiday 16.8%VFR 40.1%Shopping 21.6%Business Travel 0.6%Other 5.5%Medical 2.3%Business Tourism 12.4%

3

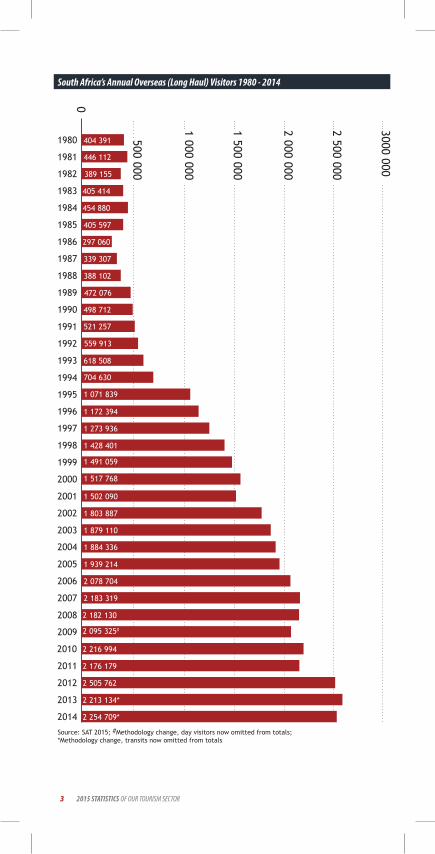

South Africa’s Annual Overseas (Long Haul) Visitors 1980 - 2014

1 500 000

2 000 000

1 000 000

500 000

0

2 500 000

3000 000

1997

1998

1999

2000

2004

2002

2006

2009

2001

2005

2008

2003

2007

2010

2012

2013

2014

2011

1 428 401

1 517 768

1 803 887

1 884 336

2 078 704

2 182 130

2 216 994

2 176 179

2 505 762

2 213 134*

2 254 709*

1 273 936

1 491 059

1 502 090

1 879 110

1 939 214

2 183 319

2 095 325#

1980

1985

1991

1981

1986

1992

1982

1987

1993

1983

1988

1984

1990

1989

1994

1995

404 391

389 155

454 880

297 060

388 102

498 712

559 913

704 630

446 112

405 414

405 597

339 307

472 076

521 257

618 508

1 071 839

1996 1 172 394

Source: SAT 2015; #Methodology change, day visitors now omitted from totals; *Methodology change, transits now omitted from totals

2015 STATISTICS OF OUR TOURISM SECTOR

4

Number of Tourists Annually 28mn trips, 12mn travellersSpend - Per Trip ±R950; R238 per daySpend - Total Market Value R26.8bn direct spend Average Length of Stay 4.0 nightsMain Source Markets Gauteng, KZN, Limpopo

VFR 73%Holiday 10%Business 6%Religious 7.4%Medical 0.5%

Source: SAT 2015

Source: SAT 2015

Source: SAT 2015

Source: SAT 2015

The South African Domestic Tourism Picture 2014:

Purpose of Visit

Source: SAT 2015

2010 2011 2012 20142013

50 000

150 000

100 000

250 000

300 000

200 000

Overseas Tourist (Inbound Long Haul) Seasonal Flow 2009-2014

J J JF M MA A S NO D0

Top 5 South African Domestic Tourism Source Markets 2014

KwaZulu-Natal – The Foreign Tourist Picture 2014Number of Visitors Annually ±768 228 Average Spend per Visitor ±R4 941 per trip, R549 per day Spend - Total Market Value R3.8 billionLength of Stay: Average 9 nights Main Overseas Source Markets Germany, UK, USA, France, India

Source: SAT 2014

KwaZulu-Natal’s Top Ten Foreign Tourism Source Markets 2014

3000 000

1. Swaziland 297 591 39% 6. Lesotho 31 534 4.1%2. Zimbabwe 49 305 6.5% 7. France 24 196 3.2%3. Germany 44 755 5.9% 8. India 20 639 2.7%4. UK 44 211 5.8% 9. Netherlands 20 349 2.7%5. USA 43 914 5.7% 10. Australia 18 017 2.4%

1. Gauteng 9.96mn2. Limpopo 5.1mn3. KwaZulu-Natal 4.3mn4. Eastern Cape 3.1mn5. Northern Cape 1.8mn

2010 FIFA WORLD CUP

2015 STATISTICS OF OUR TOURISM SECTOR

Destinations Visited in KZN – Foreign Tourists 2014

Purpose of Visit to KZN – Overseas and African Air Departures 2014

Purpose of Visit to KZN – Land Departures 2014

KwaZulu-Natal’s Top Long Haul Source Markets

Durban 63.3%Pietermaritzburg 4.3%Zululand 22.1%Drakensberg 2.1%Elephant Coast 7.8%North Coast 0.3%South Coast 0%Battlefields 2.4%

Holiday Overseas: 27.7% African Air: 52.8%Business Overseas: 15% African Air: 18.7%VFR Overseas: 0.8% African Air: 18.7%Other Overseas: 5.2% African Air: 7.7%

Holiday 9.4%Business 12.3%VFR 74.9%Other 3.4%

2014 2013 2012 2011 20101. Germany 1. USA 1. UK 1. UK 1. UK2. UK 2. UK 2. USA 2. USA 2. USA3. USA 3. Germany 3. Germany 3. Germany 3. Germany4. France 4. India 4. India 4. France 4. France5. India 5. Australia 5. Netherlands 5. Netherlands 5. Australia6. Netherlands 6. France 6. Australia 6. Australia 6. Netherlands

Source: SAT 2015

Source: SAT 2015

Source: SAT 2015

Source: SAT 2015

OF OUR TOURISM SECTOR

2015STATISTICS

5 2015 STATISTICS OF OUR TOURISM SECTOR

62015 STATISTICS OF OUR TOURISM SECTOR

KZN – The Domestic Tourist Picture 2014

Some Activities Undertaken in KZN – African Land, African Air Departure and Overseas Visitors 2014

Monthly Foreign Tourist Arrivals in KZN – 2009-2014

Number of Visitors Annually ±5.3mn trips* Average Spend Per Trip ±R979Spend – Total Direct Value ±R5.2bnAverage Length of Stay 4.2 nights (8.02 – TKZN)Main Source Markets Gauteng, KwaZulu-Natal

Land Africa Air Rest of WorldNightlife 83.0% 59.3% 73.0%Shopping 95.1% 71.0% 84.9%Visiting Natural Attractions 7.3% 62.7% 30.6%Beach 49.7% 61.3% 54.6%Wildlife 2.3% 42.3% 19.2%Cultural, Historical and Heritage 13.9% 37.4% 23.8%Social 80.9% 23.6% 56.7%Business 5.6% 69.4% 10.6%Theme Parks 5.6% 39.2% 19.8%Adventure 26.8% 0.5% 11.6%Visited a Casino 5.8% 5.1% 5.5%Sporting - Spectator 1.8% 1.2% 1.6%Education 1.3% 4.0% 2.4%Sporting - Competed 0.4%- 0.7% 0.5%Hunting 0.1% 2.2% 1.0%Medical 0.6% 0.3% 0.5%Health 0.9% 3.5% 2.0%Trading 1.6% 1.1% 1.4%Source: SAT 2015

Source: SAT 2015

Source: SAT 2015 2009 2013 20142011 20122010

J J JF M MA A S NO D0

120 000

80 000

20 000

100 000

40 000

60 000

7 2015 STATISTICS OF OUR TOURISM SECTOR

KZN – Top 5 Domestic Source Markets 2014

KZN – Top Source Markets for Holiday Makers 2014

Purpose of Visit to KZN – Domestic Visitors 2014

Activities Undertaken in KZN - Domestic Visitors 2014Activity %

Go to the beach 62Go to a live show, theatre or concert 26Watch a live sports event 36Visit a museum, art gallery or historical building 30Visit a nature or wildlife or game reserve 23Take part in a sports event 35Take part in any water sport 25Visit an arts or craft outlet 22Visit an African township or cultural village on a tour 21Food and wine fair 30Go hiking or mountain-climbing 13Bird-watching 19Art and crafts festival 22Attend a conference, workshop or training session 17Visit a health spa 21See Bushman paintings 14Fly-fishing 14Horse riding 10Go backpack/hostel travelling 15Mountain biking or other cycling 11Tour of the battlefields 9

VFR 54%Holiday/Leisure 37%Business 9%Other 0.1%

Source: TKZN 2015

Source: TKZN 2015

Source: TKZN 2015

Source: TKZN 2014

1. Gauteng2. KwaZulu-Natal 3. Western Cape 4. Free State 5. Eastern Cape

1. Gauteng2. KwaZulu-Natal 3. Western Cape 4. Eastern Cape 5. Limpopo/Mpumalanga

82015 STATISTICS OF OUR TOURISM SECTOR

Domestic Trips to Destinations in KZN 2014

Average Trips in 2014

Destinations Visited in KZN – Domestic Tourists 2014

Durban 39%Pietermaritzburg 11%Zululand 19%Drakensberg 4%Elephant Coast 7%North Coast 7%South Coast 8%Battlefields 5%

Durban 2.54Pietermaritzburg/Midlands 2.17South Coast 2.06North Coast 1.95Zululand 2.22Drakensberg 2.20Elephant Coast 1.45Battlefields 1.31

Source: TKZN 2015

Source: TKZN 2015

Source: TKZN 2015

2 500

3 000

3 500

569720

1 228

520 587

271

740

1 500

2 000

1 000

500

0

Tour

ists

(‘0

00)

2 200

Dur

ban

Sout

h Co

ast

PMB/

Mid

land

s

Zulu

land

Nor

th C

oast

Batt

lefie

lds

Dra

kens

berg

Elep

hant

Coa

st

Source: FEDHASA (KZN), STR Global, 2015

Hotel Room Occupancy % Graph KZN 2004 - 2015

%

10

30

50

70

90

0

20

40

60

80

Jan May SepFeb Jun OctMar Jul NovApr Aug Dec

2014 20152011 2012 20132010

9 2015 STATISTICS OF OUR TOURISM SECTOR

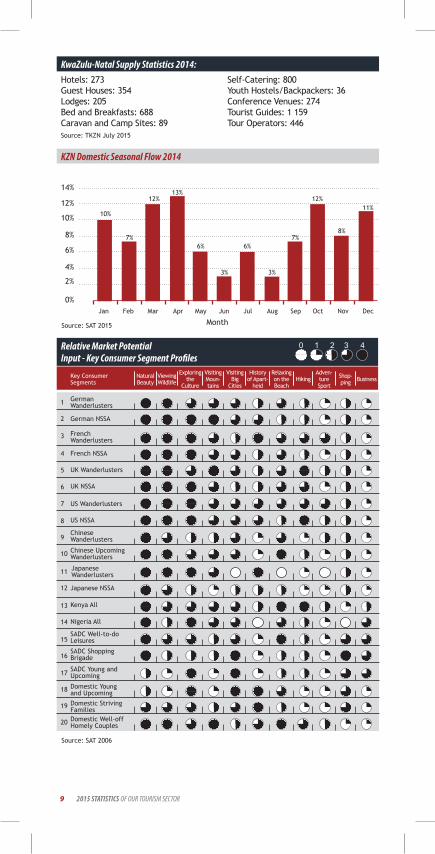

KZN Domestic Seasonal Flow 2014

Source: SAT 2015

Source: TKZN July 2015

2%

6%

10%

0%

4%

8%

12%

14%

Jan

MonthMar AugJun NovFeb May OctApr SepJul Dec

10%

12%

7%8%

12%13%

3%

6%6%

11%

3%

7%

Source: SAT 2006

Key ConsumerSegments

German Wanderlusters

20

18

16

14

12

6

10

4

8

2

19

17

15

13

11

5

9

3

7

1

Natural Beauty

Exploring the

Culture

VisitingMoun-tains

VisitingBig

Cities

History of Apart-

heid

Relaxing on the Beach

HikingAdven-ture Sport

Shop-ping BusinessViewing

Wildlife

German NSSA

French Wanderlusters

ChineseWanderlusters

Chinese UpcomingWanderlusters

Japanese Wanderlusters

Japanese NSSA

Kenya All

Nigeria All

SADC Well-to-doLeisures

SADC Shopping Brigade

SADC Young and Upcoming

Domestic Young and Upcoming

Domestic Striving FamiliesDomestic Well-off Homely Couples

French NSSA

UK Wanderlusters

UK NSSA

US Wanderlusters

US NSSA

KwaZulu-Natal Supply Statistics 2014:Hotels: 273Guest Houses: 354Lodges: 205Bed and Breakfasts: 688Caravan and Camp Sites: 89

Self-Catering: 800Youth Hostels/Backpackers: 36Conference Venues: 274Tourist Guides: 1 159Tour Operators: 446

Relative Market PotentialInput - Key Consumer Segment Profiles

102015 STATISTICS OF OUR TOURISM SECTOR

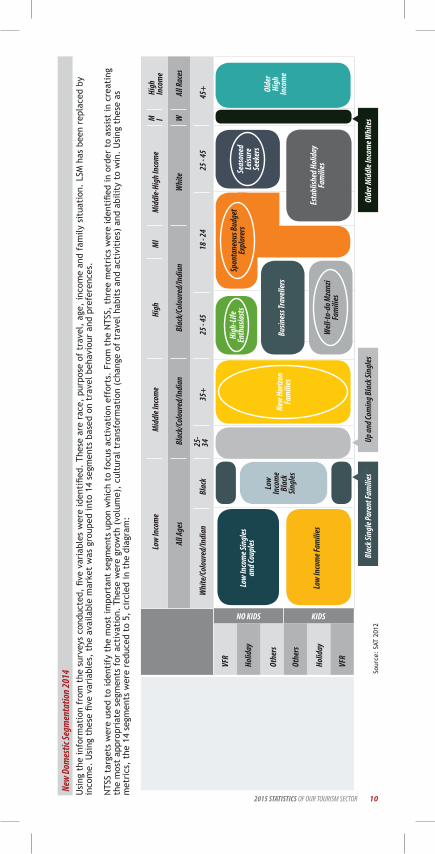

Usi

ng t

he in

form

atio

n fr

om t

he s

urve

ys c

ondu

cted

, fiv

e va

riab

les

wer

e id

enti

fied.

The

se a

re r

ace,

pur

pose

of

trav

el,

age,

inco

me

and

fam

ily s

itua

tion

. LS

M h

as b

een

repl

aced

by

inco

me.

Usi

ng t

hese

five

var

iabl

es,

the

avai

labl

e m

arke

t w

as g

roup

ed in

to 1

4 se

gmen

ts b

ased

on

trav

el b

ehav

iour

and

pre

fere

nces

.

NTS

S ta

rget

s w

ere

used

to

iden

tify

the

mos

t im

port

ant

segm

ents

upo

n w

hich

to

focu

s ac

tiva

tion

eff

orts

. Fr

om t

he N

TSS,

thr

ee m

etri

cs w

ere

iden

tifie

d in

ord

er t

o as

sist

in c

reat

ing

the

mos

t ap

prop

riat

e se

gmen

ts f

or a

ctiv

atio

n. T

hese

wer

e gr

owth

(vo

lum

e),

cult

ural

tra

nsfo

rmat

ion

(cha

nge

of t

rave

l hab

its

and

acti

viti

es)

and

abili

ty t

o w

in.

Usi

ng t

hese

as

met

rics

, th

e 14

seg

men

ts w

ere

redu

ced

to 5

, ci

rcle

d in

the

dia

gram

:

Low

Inco

me

VFR

NO KIDS KIDS

VFR

Holid

ay

Holid

ay

Othe

rs

Othe

rs

Mid

dle I

ncom

eM

iddl

e-Hi

gh In

com

eHi

gh

Inco

me

M I WAl

l Rac

esW

hite

Blac

k/Co

lour

ed/In

dian

Blac

k/Co

lour

ed/In

dian

Whi

te/C

olou

red/

Indi

an

Low

Inco

me S

ingl

esan

d Cou

ples

New

Horiz

onFa

mili

es

Olde

r Hi

ghIn

com

e

High

-Life

Enth

usia

sts

Low

Inco

me

Blac

k Sin

gles

Low

Inco

me F

amili

es

Busin

ess T

rave

llers

Well

-to-d

o Mza

nzi

Fam

ilies

Spon

tane

ous B

udge

tEx

plor

ers

Esta

blish

ed H

olid

ayFa

mili

esSeas

oned

Leisu

reSe

eker

s

Blac

k35

+45

+25

- 45

25 - 4

518

- 24

25-

34

All A

ges

High

MI

Blac

k Sin

gle P

aren

t Fam

ilies

Up an

d Com

ing B

lack

Sing

lesOl

der M

iddl

e Inc

ome W

hite

sSo

urce

: SA

T 20

12

New

Dom

estic

Segm

enta

tion 2

014

11 2015 STATISTICS OF OUR TOURISM SECTOR

Wan

derl

uste

rs

• W

ande

rlus

ters

(U

SA)

• U

psca

le W

ande

rlus

ters

(U

SA)

• W

ande

rlus

ters

(U

K)•

Ups

cale

Wan

derl

uste

rs (

UK)

•

Wan

derl

uste

rs (

De)

• W

ande

rlus

ters

(Fr

)•

Wan

derl

uste

rs (

In)

• W

ande

rlus

ters

(N

e)•

Emer

ging

Wan

derl

uste

rs (

Aust

)•

Wan

derl

uste

rs (

Aust

)•

Ex-P

at W

ande

rlus

ters

(N

i, K

)•

Org

anis

ed W

ande

rlus

ters

(Ch

)•

Expe

rien

ced

Wan

derl

uste

rs (

Ch)

• O

rgan

ised

Wan

derl

uste

rs (

Jp)

• Ex

peri

ence

d W

ande

rlus

ters

(Jp

)•

Wan

derl

uste

rs (

Jp) Po

siti

ve C

onve

rtib

les

• Co

nver

tibl

e Sh

ort

Hau

l (N

e)•

Posi

tive

Con

vert

ible

s (U

SA)

• Po

siti

ve C

onve

rtib

le c

oupl

es (

UK)

• Po

siti

ve C

onve

rtib

les

(Jap

an)

Seni

or E

xplo

rers

• Se

nior

Exp

lore

rs (

De)

• Se

nior

Exp

lore

rs (

Fr)

• Se

nior

Exp

lore

rs (

Japa

n)•

Empt

y N

este

rs (

In)

• Se

nior

Exp

lore

rs (

Aust

)

Purp

ose

Trav

elle

rs

• In

depe

nden

t Bu

sine

ss P

eopl

e (N

i)•

Trad

ers/

Impo

rter

s (N

i)•

Purp

ose

Trav

elle

rs (

Chin

a)•

Busi

ness

Pro

fess

iona

ls (

SADC

)•

Priv

ate

Trad

ers

(SAD

C)•

Taxi

Tra

ders

(SA

DC)

• Tr

adin

g Tr

ucke

rs (

SADC

)

• U

S Ad

vent

ure/

Cult

ure

NSS

As•

UK

NSS

As (

UK)

• G

erm

an N

SSAs

(De

)•

Fre

nch

NSS

As (

Fr)

• D

utch

NSS

As (

Ne)

• E

x-Pa

t N

SSAs

(N

i, K

e)

• N

SSAs

(Ke

) •

NSS

As (

Japa

n)

• N

SSAs

(Au

st)

• U

S R e

laxe

r N

SSAs

• H

igh

End

P ack

age

(Ne)

• Lu

xury

Eld

erly

Bre

ak (

Ne)

• H

igh

Spen

d P a

ckag

e (A

) •

Hyp

er W

ealt

hy (

Wit

hout

Kid

s) (

Ni)

• E

x-Pa

t Pa

mpe

red

NSS

As (

Ni,

Ke)

Caco

oned

/Low

Adv

entu

re•

Fam

ily E

xplo

rers

(U

SA)

• H

yper

Wea

lthy

(W

ith

kids

) (N

i)•

Ex-P

at L

ow A

dven

ture

Fa

mily

Tra

velle

rs (

Ni,

Ke)

• Y o

ung

Fam

ilies

(In

)

Expl

orer

s/Ad

vent

urou

s•

Fam

ily A

fric

an D

isco

vere

rs (

De)

• Fr

ench

Fam

ily E

xplo

rers

• Ex

-Pat

Fam

ily E

xplo

rers

(N

i, K

e)•

New

Fam

ily E

xplo

rers

(In

)•

Expe

rien

ced

Fam

ily E

xplo

rers

(In

)

NSS

As

Fam

ily T

rave

llers

Adve

ntur

ous,

exp

lora

tive

(G

row

n-up

Wan

derl

uste

rs)

NSS

A Ex

plor

ers

Rela

xati

on a

nd lu

xury

wit

h so

me

disc

over

y

Pam

pere

d N

SSAs

Source: SAT 2012

Inte

rnat

ional

Segm

enta

tion

SA to

urism

has id

entifi

ed ke

y seg

men

ts in

its fo

cus m

arke

ts ac

ross

the w

orld.

..KE

Y FOC

US SE

GMEN

TS

Thro

ugh

the

segm

enta

tion

of

mar

kets

, a

num

ber

of g

loba

l seg

men

ts h

ave

emer

ged

acro

ss c

ount

ries

, of

peo

ple

who

are

pos

itiv

e an

d ke

en t

o vi

sit

Sout

h Af

rica

. The

dia

gram

bel

ow d

epic

ts t

he la

test

seg

men

tati

on:

122015 STATISTICS OF OUR TOURISM SECTOR

YOUNG SOUTH AFRICA

SEEKERS

CENTRE OF GRAvITY

MATURE SOUTH AFRICA

SEEKERS

SOUTH AFRICA

SEEKERS

• 26 - 40 years old.• Predominantly

male (61%).• Make decisions by

themselves.• Almost all work

full-time.• Have ±2 weeks for

holiday.• Holiday Spend:

<$2 000.• Use Internet for info and

travel agents for fulfillment.

• Don’t like tours. They want largely

independent adventure.

• They are active explorers.

• Concerns: getting around, safety and perceived expense.

• Well-travelled. Worldly.

• Independent.• Travellers, not

tourists.• Travel is a state of mind for them. They are global citizens

for whom travel is an essential part of their

everyday lives.• They travel to expand their knowledge and to evolve (It keeps them

interesting).• They want to engage the destination, not see

it at arm’s length.• They seek out

interesting and high quality experiences.• They like to make

their own decisions and maintain a sense of control over their

own destiny.

• 41 - 60 years old.• Most married, make

decisions together.• 40% retired. 20%

semi-retired.• Travel for between

2 and 5 weeks.• High holiday spend: between $2 000 and

$5 000.• Use travel agents for information and fulfillment (have a

relationship).• May use tours if they are flexible.• Interested in a large variety of

activities that allow them to explore.

• Demanding travellers who are constantly looking

for the next amazing thing.

The core segments which SAT will be focusing on are the NSSAs (Next Stop South Africa) and the Wanderlusters. The major differentiator between these two segments is age. The Wanderluster is a more ‘youthful’ segment, whereas the NSSAs are more ‘mature’. However, they both know and are positive about South Africa and have a desire to travel here. They travel abroad regularly, however, they have several destination choices. The challenge is to switch them from other destinations to South Africa. Centre of gravity descriptions: “The person and situation for which the brand is always the best choice is defined in terms of their attitudes and values, NOT just demographics”.

Source: TKZN, IHS, STATSSA, KZN Provincial Treasury, *Quantec

MARKET GEOGRAPHIC SCOPE TARGET SEGMENTS CORE EXPERIENCES

Domestic • KwaZulu-Natal• Gauteng• Western Cape• Eastern Cape• Free State

• New horizon families• High-life enthusiasts• Well-to-do Mzansi families• Spontaneous budget explorers• Seasoned leisure seekers

• Beaches• Natural beauty• Nightlife• Shopping• Heritage• Culture

SADCRest of Africa

• Swaziland• Lesotho• Botswana• Mozambique• Zambia• Zimbabwe• Kenya• Nigeria• Angola

• Business professionals• Traders

• Shopping• Big cities• Beaches (not coastal markets)• Wildlife• Heritage

EUROPEAMERICASASIA

CORE OPPORTUNITY INVESTMENTS STRATEGIC HUB

• United Kingdom

• USA• Germany

• France• Netherlands• Australia

• India• China• Brazil• Sweden• Eastern

Europe (Russia)

• Middle East (GCC countries)

• NSSA, Wanderlusters • Family explorers• New beach-lovers

• Natural beauty• Wildlife• Culture• Visiting mountains• Beach• Adventure (USA Wanderluster)

13 2015 STATISTICS OF OUR TOURISM SECTOR

KZN’s International and Domestic Segmentation 2014 - 2019

MARKET GEOGRAPHIC SCOPE TARGET SEGMENTS CORE EXPERIENCES

Domestic • KwaZulu-Natal• Gauteng• Western Cape• Eastern Cape• Free State

• New horizon families• High-life enthusiasts• Well-to-do Mzansi families• Spontaneous budget explorers• Seasoned leisure seekers

• Beaches• Natural beauty• Nightlife• Shopping• Heritage• Culture

SADCRest of Africa

• Swaziland• Lesotho• Botswana• Mozambique• Zambia• Zimbabwe• Kenya• Nigeria• Angola

• Business professionals• Traders

• Shopping• Big cities• Beaches (not coastal markets)• Wildlife• Heritage

EUROPEAMERICASASIA

CORE OPPORTUNITY INVESTMENTS STRATEGIC HUB

• United Kingdom

• USA• Germany

• France• Netherlands• Australia

• India• China• Brazil• Sweden• Eastern

Europe (Russia)

• Middle East (GCC countries)

• NSSA, Wanderlusters • Family explorers• New beach-lovers

• Natural beauty• Wildlife• Culture• Visiting mountains• Beach• Adventure (USA Wanderluster)

142015 STATISTICS OF OUR TOURISM SECTOR

OF OUR TOURISM SECTOR

2015STATISTICS

15 2015 STATISTICS OF OUR TOURISM SECTOR

KZN Provincial InformationArea 94 361 km2 (7.7% of South Africa)Coastline 560kmsClimate Sub-tropical. Summer 17-28 ºC, Winter 11–25 ºC,

Durban average rainfall 1 009mmHighest Elevation 3 451 m (Mafadi, in the Drakensberg)Population 10.5mn (19.8% of South Africa) mid-2014 (growth

rate 1.3%)Population Density 113 people per square kilometre 2014Capital PietermaritzburgLanguages Mainly Zulu and EnglishHolidays 1 January, 21 March, 24 March, 27 April, 28 April,

1 May, 2 May, 16 June, 9 August, 24 September, 16 December, 25 December, 26 December.

Time Zone GMT +2Currency The Rand is made up of 100 centsGDP 2014 R585.6 billion or 16.7% of South Africa’s GDP*Electricity 220 VoltsHarbours Durban, Richards BayAirports King Shaka International Airport, Oribi, Richards

Bay, Margate, Ulundi.Literacy Rate 75.6% (2012)Employment Rate Between 57.2% - 61.5% (2014, using strict and

expanded definitions)Source: TKZN, IHS, STATSSA, KZN Provincial Treasury, *Quantec

OF OUR TOURISM SECTOR

2015STATISTICS

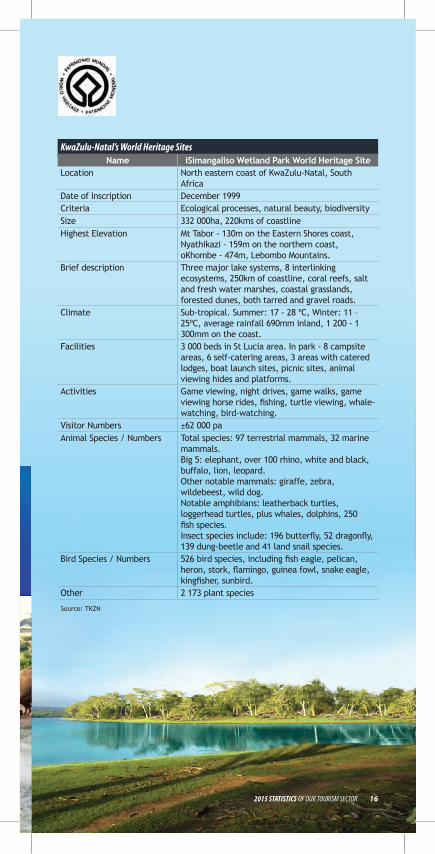

Name iSimangaliso Wetland Park World Heritage SiteLocation North eastern coast of KwaZulu-Natal, South

AfricaDate of Inscription December 1999Criteria Ecological processes, natural beauty, biodiversitySize 332 000ha, 220kms of coastlineHighest Elevation Mt Tabor - 130m on the Eastern Shores coast,

Nyathikazi - 159m on the northern coast, oKhombe - 474m, Lebombo Mountains.

Brief description Three major lake systems, 8 interlinking ecosystems, 250km of coastline, coral reefs, salt and fresh water marshes, coastal grasslands, forested dunes, both tarred and gravel roads.

Climate Sub-tropical. Summer: 17 - 28 ºC, Winter: 11 – 25ºC, average rainfall 690mm inland, 1 200 - 1 300mm on the coast.

Facilities 3 000 beds in St Lucia area. In park - 8 campsite areas, 6 self-catering areas, 3 areas with catered lodges, boat launch sites, picnic sites, animal viewing hides and platforms.

Activities Game viewing, night drives, game walks, game viewing horse rides, fishing, turtle viewing, whale- watching, bird-watching.

Visitor Numbers ±62 000 paAnimal Species / Numbers Total species: 97 terrestrial mammals, 32 marine

mammals.Big 5: elephant, over 100 rhino, white and black, buffalo, lion, leopard.Other notable mammals: giraffe, zebra, wildebeest, wild dog.Notable amphibians: leatherback turtles, loggerhead turtles, plus whales, dolphins, 250 fish species.Insect species include: 196 butterfly, 52 dragonfly, 139 dung-beetle and 41 land snail species.

Bird Species / Numbers 526 bird species, including fish eagle, pelican, heron, stork, flamingo, guinea fowl, snake eagle, kingfisher, sunbird.

Other 2 173 plant species

KwaZulu-Natal’s World Heritage Sites

Source: TKZN

162015 STATISTICS OF OUR TOURISM SECTOR

Name uKhahlamba Drakensberg Park World Heritage SiteLocation Forms western KwaZulu-Natal border between

South Africa and Lesotho, major watershedDate of Inscription November 2000Criteria Cultural (3) and natural (4) criteriaSize 242 813haHighest Elevation 3 451mBrief description High basalt mountain range overlying sandstone

bands over shale, foothills, incised valleys, grassland and protea, yellowwood and bottlebrush forests.

Climate Summer: 22ºC, Winter 5ºC, average rainfall: 900mm, frequent snow in winter.

Facilities 700 beds inside the park, 2 000 closely adjacent, 9 campsites, ±150 caves, picnic sites, view sites, ‘vultures restaurant’.

Activities Walking, hiking, climbing, ice-climbing, bird- watching, fly-fishing, paragliding, mountain biking, hang-gliding, horse riding, horse trekking, river swimming, rock art viewing, picnicking.

Visitor Numbers Annual total 2009 – ±110 000Animal Species / Numbers Mammals: 48 species including eland, water buck,

oribi, mountain reed buck, ±1 800 rhebok, jackals, leopard.Insects include 46 species of millipedes and centipedes, 44 dragonfly species (about a third of South Africa’s total) and 74 butterfly species, 124 frog species, 23 lizard and 25 snake species.

Bird Species / Numbers Total: 296 species, including Lammergeyer, Cape vulture, black eagles.

Other 2 153 plant species

KwaZulu-Natal’s World Heritage Sites

Source: TKZN 2012

17 2015 STATISTICS OF OUR TOURISM SECTOR

OF OUR TOURISM SECTOR

2015STATISTICS

7,8 %

www.zulu.org.za

2nd Floor Ithala Trade Centre

29 Canal Quay Road

Point, Durban, 4001

PO Box 2516

Durban, 4000

Switchboard: +27 (0) 31 366 7500

Fax: +27 (0) 31 305 6693

Airport Office: +27 (0) 32 436 0013

V&A Cape Town Office: +27 (0) 21 418 1684

Airport Office Gauteng: +27 (0) 11 390 1000

Customer Care: 0860 101 099

uShaka Marine World: +27 (0) 31 337 8099

Email: [email protected]

TOURISM REGIONS OF KWAZULU-NATAL

2,1 %

2,4 %

Recommended