1

M.St Penology

Pen 1222

Homerton College

Rachel M Spearing

Supervisor: Dr. K Mueller-Johnson

Moral Contexts and Rule-Breaking in Investment Banking:

The Application of Situational Action Theory

Submitted in part fulfillment of the requirements for the Masters Degree in

Applied Criminology, Penology & Management at the Institute of

Criminology, Cambridge University.

January 2014.

2

ACKNOWLEDGEMENTS

This study would have been impossible without the time and trust so generously

given to me by the investment bankers in London and New York. I would like to

offer my sincere thanks to those who participated in the research and assisted

with introductions to interviewees. I am also grateful for the patience and

guidance of Professor Per-Olof Wikström, Dr. Kyle Treiber and Dr. Katrin

Mueller-Johnson at the Institute of Criminology in relation to theoretical

considerations, research and the presentation of the study. Finally, I give my

heartfelt thanks for the love, support and encouragement received from my

family and friends, particularly from Gary and Aude.

3

SUMMARY

This study explores the moral context of bankers in investment banking and the

application of Situational Action Theory in this environment. It was an

explorative study which used a snowball sample method to produce successive

waves. A group of 20 was selected using key targeted informants, and no reward

was offered. The bankers were the sole informants and provided insights

focusing on their environment.

The study reviews the literature relating to Situational Action Theory, white-

collar crime and banking regulation. It presents a qualitative evaluation of the

findings which were gathered with one-to-one interviews using a structured

questionnaire which was designed using a collective efficacy model to capture

the moral context of the environment and of the rule-breaking activity. The core

areas discussed were illegitimate rate fixing, mismarking of profit and loss,

insider trading and misuse of company privileges.

The findings support the proposition that Situational Action Theory (SAT)

establishes itself as a theory applicable to white-collar crime in the core areas

tested.

SAT and the framework and mechanisms used to explain the interplay between

crime and crime causation can be used within the context of investment banking.

They offer valuable factors for assessing the moral norms of the social and

situational dynamics of this environment. SAT should be considered a valuable

concept when shaping new policy and compliance procedures in the wake of the

restructuring which is taking place in response to the guidance offered by the

regulators’ and parliamentary reports which followed the recent banking

scandals and crisis.

4

TABLE OF CONTENTS

I. Introduction page 6

II. Literature Review page 11

Background to the theory page 11

Situation Action Theory page 13

Perception-choice process page 14

The Moral Context page 15

Controls page 18

SAT: The causes of the causes page 19

Social and personal emergence page 21

Applying SAT page 22

III White-Collar Crime page 22

Scrutinizing the Powerful page 22

The definition of white-collar crime page 23

Lenience and legal lacunas page 26

IV Banking Regulation page 27

Historical Background page 27

The Regulatory Framework page 29

Parliamentary Banking Reviews page 30

V Research Method page 35

Specific research questions and design page 35

Participants and sample method page 36

Ethical considerations page 38

Participants and their general background page 39

Procedure page 40

VI Findings & Discussion page 45

The moral context of investment banking page 46

5

Does rule breaking occur and is there an application of SAT page 46

Illegitimate Rate Fixing page 48

Mismarking profit and loss page 56

Insider Trading page 62

Misuse of company privileges page 64

Causal process influencing factors page 65

Limitations of the study page 66

VII Conclusions & Implications page 67

Conclusions of the study page 67

Criminogenic Opportunity page 70

Perception choice process page 70

Controls page 70

The process linking the causes and the causes of causes page 71

Policy Implications page 71

Future Research page 72

References

Appendix

Appendix A Participation Information & Consent Form

Appendix B Questionnaire used for one to one interviews

Tables Appendix C

Table 1: Participants and their general backgrounds

Table 2a: Perceptions of Illegitimate Rate Fixing within Investment Banking

Table 2b: The process of reporting, consequences of action & factors promotion

and deterrence.

Table 3a: Anecdotal observations of mismarking actions in Investment Banking

Table 3b: Perception of mismarking activity within Investment Banks.

Table 4a: Perceptions of insider trading activities in Investment Banking

6

CHAPTER I Introduction

In 2008 the global financial crisis, sparked by the collapse of US mortgage-

backed securities, saw the banking industry thrown under the spotlight and

subjected to scrutiny. It was a global review and of public importance because

the effects of the crisis were felt throughout society, from government treasury

and corporate business through to the general public whose savings,

investments and future pensions had been in some cases subject to catastrophic

losses. The picture which slowly began to emerge and to be critically reported

by the investigating authorities was one of endemic practices and systematic

failures which encouraged reckless actions, poor internal controls, poor risk

management, dishonesty, and an industry driven by short-term goals such as

profit and personal bonuses which lead to corrosive and corruptive practices

(FSA 2012; HM Treasury, Department for Business Innovation and Skills 2013).

Prior to 1986, it would have been reasonably accurate to describe investment

banking in the UK as unregulated (Gleeson 2013). Over the last 27 years a

tremendous number of rules and regulations have been introduced to make

banking one of the most regulated commercial activities in the country. But the

actions of those working within the industry have caused the greatest concern.

The image of intelligence, respectability and high standards of ethics within the

economy and of safe corporate structures and governance has given way to one

of greed, self interest and reckless behaviour, and of management cultures which

at best appear complicit in such behaviour, and at worst cultivated it with

environmental pressures, corporate goals, and bad role models in management.

7

(HL: Paper 133 2012). The result was a total loss of confidence among

institutions and a growth of distrust resulting in their being unable to play their

core role, financing economic growth, and in the loss of public faith and trust in

the management and governance of the banking industry, one of the pillars

which stabilises society.

Having worked in two investment banks between 1992 and 1995 in a capital

markets trading environment, I was particularly interested to read the media

and commissioned reports about the 2008 financial crisis. The conclusions

appeared to focus on what further organisation, regulation and statutory

legislation would be necessary to prevent the repetition of such problems, and

on a complex scrutiny of the individual causation of particular scandals. There

was little evaluation of the ‘causes of the causes’ in a wider context and how

these came to manifest themselves both personally and institutionally within the

banking industry. Whilst there was much comment regarding the greed and the

morality of bankers, the focus was on individual blame rather than reviewing the

environment in which the behaviour occurred. But criminological theory, for

example Situational Action Theory predicts and researches the moral context of

the environment as an indicator of whether individuals will choose to engage in

criminal behaviour. This study aims to explore this issue, applying the

framework of the Situational Action Theory of Professor Per-Olof Wikström.

Situational Action Theory (SAT) applies to all types of crimes (Wikström 2010)

but to date it has not been tested within a white-collar crime setting; this study

aims to fill this gap.

8

SAT is a contemporary theory which describes crime as actions. Central to the

theory is the concept that the individual contemplates a ‘perception-choice

process, which is initiated and guided by the interaction between a person’s

crime propensity and criminogenic exposure’ (i.e. their own personal

characteristics and those of their environment) (Wikström et al. 2012). Further,

crimes can simply and effectively be analysed as moral actions (Wikström

2010a). This is not using the word ‘morality’ literally, but is interpreting it as an

action which a person contemplates based on the guidance of rules about what it

is right or wrong to do. This is a helpful device in the context of my study

because considering moral contexts in this way and using SAT does not rely

upon an analysis of whether laws/rules are good or bad (‘virtuous or

reprehensible’) but simply talks in terms of conduct which offer guidance about

whether it is right or wrong to do something. ‘SAT focuses on how moral rules

guide human action’ (Wikström 2014).

White-collar crime is a relatively new concept. It originated in academic

research from an American sociologist, Edwin Sutherland, who sought to

highlight illegal acts being conducted in business. It was defined initially as ‘all

offences committed by a person of respectability and in high social status in the

course of their occupation’ (Sutherland 1940). Ironically Sutherland’s studies

were criticised for being too unscientific as they covered areas which were illegal

but not outlawed by criminal statute, e.g. false accounting and anti-competitive

practices. There was much debate and division regarding the appropriate

definition of white-collar crime (Tappen 1947; Pearce 1976; Shappiro 1990;

Snider 1993). Arguably morality was at the heart of this debate, with some

9

believing that the concept should be defined by that which was morally wrong

(mala in se) and that which was simply illegal (mala prohibita) (Edelhertz

1970;). But is has until recently been a concept that has been absent from thd

heart of business operation or of concern to the public. Studies by Sutherland

and others were seeking to highlight the issue that harm that can be done to

society by the powerful, a proposition that was unpopular and poorly funded in

research in the early years (Snider 1999). I shall return to this discussion in

more detail later in this thesis (Tombs and Whyte 2003).

This work was an explorative study which used the theoretical framework of

SAT and tested the evidence to examine whether there is any support for the

theory. I will set out and discuss the theory and framework within the literature

review section of this dissertation, with reference to the development of ‘moral

norms’ in banking regulation.

The participants were the key informants. Research was conducted via

structured one-to-one interviews with investment bankers from three different

types of business: public banks (large high street institutions), private equity

business (privately owned companies) and boutique hedge funds (groups of

individuals who are accredited to trade/manage investments and private funds).

These settings were identified to factor in the possibility of considering different

settings within these groups, and whether variants then emerged from the data.

The sample group was selected via a targeted key informant who then facilitated

the process with a snowball introduction to produce successive waves. It was

10

very difficult to access the sample group and to obtain their trust and

cooperation. These trials and tribulations together with the ethical difficulties of

conducting this research will be explained in the method section of the study.

Whilst conducting the structured interviews I was always mindful to explain to

the banker being interviewed that the interview was constructed to encourage

them to comment as observers of their environment rather than to personalise

their answers. The interview was designed in such a way for ethical reasons and

to safeguard the interviewees’ disclosures. However I allowed the participants to

explain the reasoning behind their answers freely. In many cases this enabled

me to conduct a deeper analysis of their responses to their environment and

their own and others’ personal characteristics. Many shared their personal

experience of rule breaking and management culture which will be explained in

detail in the results and discussion section. Owing to the limitations in the size of

the sample group and the possible limitations of selection and response, the

results have been subjected to qualitative assessment.

Finally I consider the Parliamentary Banking Commission’s Report (HL: Paper

133. 2013) and the establishment of the commission in July 2012, in the wake of

the LIBOR scandal.

11

CHAPTER II

Literature Review

Background to the theory

Critical criminologists frequently revisit studies considering the theories and

causation of crime, and many agree that, whilst producing statistical covariates

of offending and correlates of crime, the studies are often fragmented and poorly

integrated with theories (Matza 1964, Farrington 1992, Vila 1994, Wikström

2012). From the 1990’s onwards criminological theory centered on the issue of

self-control as the strongest predictor of crime (Gottfredson and Hirshi,1990).

Critics argued that self-control was poorly defined (Akers 1989) but the theory

was further developed on the basis of ‘conceptualizing crime and deriving from

that a concept of the offender’s traits’ (Gottfredson and Hirshi 1990). A number

of empirical studies tested this theory. Pratt and Cullen undertook a meta-

analysis of existing empirical data and concluded that ‘low self control was an

important predictor of crime’; however the theory was weaker in longitudinal

studies where other variables were present (Pratt and Cullen 2005). The concept

of self-control being split into two elements emerged with Tittle, Ward and

Grasmick’s studies (2006) where self-control was considered and divided into

the capacity for self-control and the desire for it, the latter part being the first

emergence of an element of ‘choice’. Choice is at the heart of Situational Action

Theory and marks it out from self-control theory because it described choice as a

unique two stage process involving both the person and the environment.

12

The study of crime as a ‘situated transaction’ has been considered by

criminologists other than Wikström. Wilkinson and Fagan (1996) stressed the

importance of correlating information about ‘individuals in their settings, the

characteristics of those settings, and the rules and contingencies that dictate

their interaction’. Indeed others mooted the necessity of theory and research

coming together to develop a more complete picture (McGloin et al. 2012). But

without a clear conception of ‘(1) what crime is (i.e. what the theory should

explain), (2) what moves people to commit acts of crime (a theory of action), and

(3) how individual characteristics and experiences and environmental features

interact in this process (integration of levels of explanation), we cannot fully

address the causes of crime’ (Wikström 2004). Situational Action Theory (SAT)

‘aimed to integrate, within an adequate action theory framework, main insights

from criminological theory and research as well as theory and research from

relevant social and behavioural sciences’ (Wikström 2012). It is presented to

create a greater understanding of crime causation and is the only theory that

connects both the individual and the environment with situational choice.

Connecting the two requires the integration of causally relevant personal and

environment factors and the analysis of their interaction within the context of an

adequate action theory (Wikström 2010). Rule-breaking in banking has thus far

focused on the individual’s personal characteristics and the flaws in supervision

and control. The interaction using SAT is pertinent in the context of my study

because of the ‘emergent’ phenomena of bankers who commit dubious acts and

the questions for policy makers and enforcement regulators as to how best to

prevent future rule breaking behaviour. SAT proposes that prediction of risk

factors can be identified by considering the environment and the question of

13

what moves people to commit crimes, and how individual characteristics,

experiences and environmental features interact in this process.

Situational Action Theory

The basic proposition of SAT is ‘that people are essentially rule-guided creatures’

(Wikström 2010a). Crimes are the commission of acts. To explain this ‘human

action (such as acts of crime) one needs to understand the process of rule-

guidance influences what action alternatives people perceive, and what choices

they make in relation to the motivations (temptations and provocations) they

experience’ (Wikström 2012).

‘SAT proposes that acts of crime ( C ) are ultimately an outcome of a perception-

choice process( ) that is initiated and guided by the interaction (x ) between

a person’s crime propensity ( P ) and criminogenic exposure (E).'

P x E C [Wikström 2012, figure 1.3.1]

SAT establishes itself as a theory applicable to all types of crime. It adopts a

normative and universally applicable definition of crime, suggesting that crimes

are actions that breach legal rules of conduct (Wikström 2010). These can be

described as moral rules because this does not differentiate as to whether they

are crimes or not. The advantage of considering crime as a moral action is that

the term is applicable to all kinds of action and equates them to rule-breaking or

abidance, therefore is not focusing on why people carry out an act, but rather on

why they break or comply with rules, which does not necessitate focusing on the

14

judgment of the act itself, but focuses on the individual and the impact of the

environment on that individual (Wikström 2012). This is important in the

context of my study because it focuses on the process of the perception choice of

the bankers and allows discussion without trespassing into judgment of the

commission of the act.

Perception-choice process

‘Perception-choice process’ is the process with which an individual makes a

decision, deciding either to take action or to choose inaction in relation to a

motivation (temptation or provocation). This can either be conducted in an

‘automated’ (expressing a habit) or ‘reasoned’ (making a judgment) way,

depending upon the circumstances and setting (Wikström 2012). To understand

the correlates between the two we need to understand the process that moves

people to act in one way or another. People act on their motivation, depending

upon the interaction between their criminal propensity and the criminogenic

features of the environment (settings) to which they are exposed. Since SAT

addresses the interaction between individuals and settings, I believe that its

concepts and mechanisms can be observed in the context of rule-breaking by

investment bankers.

The mechanisms of the situational process can be set out simply as follows:

(1) Motivation (goal-directed attention) initiating the action process;

(2) The moral filter (the interaction between personal moral rule and the

moral norms of the settings) guides what action alternatives a person

sees in relation to a motivation;

15

(3) Controls (self-control and deterrents) influence the process of choice

when a person deliberates and there is conflicting rule guidance

(Wikström 2014).

The moral context

‘If they are true to their calling, all criminologists have to be interested in

morality’ (Bottoms 2002). SAT proposes that crime is moral actions. ‘A moral

rule is a rule that states what it is right or wrong to do in a particular

circumstance’ (Wikström 2011). Crime can be evaluated by considering why

people break the rules and the effects can be explained using a theory of

causation. The law is a set of moral rules of conduct. SAT does not require the

existence of the law, only the existence of moral rules (Wikström 2012). This is

important in the context of my study which aims to focus on seeking to explore

what this proposition means in the context of investment bankers.

‘Understanding crime as action helps us comprehend the role of “systemic

factors” and the role that social change can have on crime causation’ (Wikström

2010).

Morality and Moral Norms

However, analysing crime as moral actions does not involve a ‘moralistic

approach’. SAT is not testing whether the actions are good or bad, but rather

offering guidance on how moral rules guide human action (Wikström 2011). It is

the balance of situational (moral norms) and social (moral settings) as a ‘moral

filter’ that determines whether a person will see an act of crime as an action

alternative in response to a particular motivation. This explains why individuals

16

will react differently in the same setting; the principle of moral correspondence

states that ‘if there is a correspondence between the person’s personal moral

rules and the moral norms of the setting, the person is likely to perceive his or

her action alternatives accordingly. If the person’s moral rules encourage

abidance by a particular rule of conduct and the moral norms of the setting in

which he or she takes part also encourage abidance by this rule of conduct, he or

she is unlikely to see a breach of this rule of conduct as an action alternative’. If

the contrary exists then the person is likely to see the breaking of the rule as an

action alternative (Wikström 2011).

‘Moral norms’ are developed within an environment according to the extent to

which they encourage or discourage the breaking of particular laws in relation to

the opportunities a setting provides and the frictions it creates (Wikström 2014).

This is an important concept within my study due to the development of certain

types of ‘cultures’ within the banking industry which have been described as

sub-cultures of deviant behaviour which corrupt practices and are divisive of

compliance policy (Gleeson 2013). SAT is a complex contemporary theory and

due to limitations of time, the sample and data available, this study will focus on

the moral context of investment bankers, situational and social factors, and the

dynamics which give rise to rule breaking.

Of interest to the theory of SAT, and relevant to my study of bankers, is how

people develop their particular moral rules. According to the theory of SAT this

occurs through a process of ‘moral education’, i.e. the way ‘people come to

acquire particular moral rules and their attached moral emotions through

17

processes of instruction, trial and error, and observations of reactions to and

sanctioning of others actions’ (Wikström 2011). This process could be

considered relevant in moving towards the ‘emergence’ of how a person comes

to acquire a criminal propensity or how an environment acquires a particular

criminogenity.

A person’s moral code is central to explaining whether a person will commit

crime as opposed to how they will commit it (Wikström and Svensson 2010).

Someone with a strong ‘moral compass’1 will make decisions based on certain

values (Wikström 2010) and is therefore unlikely to have to exercise self-control

or reflect upon the deterrents of their settings where there is a temptation or

pressure to break the rules. However an individual with a weaker constitution

will see crime as a legitimate alternative given their moral character is under-

developed, and they may fall foul to the pressures of their environment

(Wikström 2010). Weak morality and low levels of self-control are strong

predictors of crime propensity; however weak morality is the stronger indicator

of the two (Wikström and Svensson, 2010). Morality is therefore central to the

action theory, while self-control explains only a limited amount of information

about the cause.

Variations in crime propensity may occur due to the nature of the particular

crime. Some people may be prepared to engage in one type of crime (e.g. false

accounting) but not others (e.g. theft, fraud or sexual offences). SAT suggests

1 Adopting the language used by one of the sample group in describing moral values.

18

that even with moral rules and the interaction with the setting there can be some

filtering between the norms of moral rules and moral emotions and

environmental settings. For example a person’s moral reaction to crime may

promote or restrict the action. If the person sees their behaviour as wrong then

engaging in it may evoke guilt or shame. However, if one is able to justify or be

praised for an action, then one may experience an emotion of self righteousness

or being rewarded for the act and will adopt this as a moral act (Wikström and

Treiber 2009). Morality may even be psychologically divided by means of a

cognitive process, thus distancing the act from one’s normal moral belief, causing

it to become justified as an isolated act, e.g. retribution for a previous act against

the individual or in recompense for another justified cause. This allows the

person to leave one role and adopt another moral position, thus avoiding

cognitive dissonance (Rothe and Mullins 2006).

Controls

Control can be complex and vary in definition within criminology. Within the

context of SAT the term means ‘any personal or social factors that (directly or

indirectly) influence whether or not a person follows or breaches the moral

norms and law of society’ (Wikström 2011). Controls may have ‘internal’ (via

self-control) or ‘external’ (deterrent) application and thus are part of the

situational process (Wikström 2012). As explained earlier the principle of moral

correspondence and conditional relevance of control play a key role in the action

choice of crime. The purpose of controls within SAT is the compliance with

moral rules when the person deliberates about whether to act on a certain

motivation (Wikström 2010a). Thus an individual potentially goes through a

19

two-stage process when considering an action, control being exercised as self-

control in reasoning about a moral judgment, and control as an external

deliberation in considering the deterrents. These are distinctly different

processes, as moral rules impact upon the action alternatives, whilst controls

(may) impact action choice (Wikström and Treiber 2007). SAT is unique in the

situational application of controls in this way as other models tend to focus on

control as a personal characteristic. People naturally vary in their ability to

exercise self-control. The effectiveness relies upon ‘executive functions’

(cognitive abilities) which measure effective deterrents or properly evaluate

moral norms, i.e. if someone is under extreme pressure and experiencing acute

anxiety they will be less able to process an effective evaluation of the moral

norms and may be less fearful of the consequences. The effectiveness of

deterrents often relies upon the likelihood of intervention and the application of

sanction (Wikström and Treiber 2007). This is particularly pertinent in the

study of my bankers who break rules because contexts can become criminogenic

if they encourage crime as an action alternative.

SAT: The causes of the causes

The hypothesis of SAT is that all crimes are situational and thus the causes of the

causes are a convergence of personal causes of crime with the social causes of

crime. The social causes develop historically via criminogenic settings, emerging

and creating crime-prone environments, because people are within them who

are responding to their motivations and committing crime. Person emergence

occurs via criminal propensities manifesting within self and social settings

(Wikström 2014).

20

There is some interplay between the two features of ‘life histories’ (personal

factors) and ‘social systemic factors’ (environmental factors) but these are

described as ‘the causes of the causes’, rather than the causes of crime

(Wikström 2012). Wikström asserts that by understanding how these individual

characteristics and experiences and environmental features interact, we can

then consider how to properly address the causes of crime (2004). But the

challenge is to identify what are correlates and what are causes. ‘When factors

become too numerous … we are in the hopeless position of arguing that

everything matters’ (Matza 1964). The danger of considering the identity of the

causes of the causes is that whilst a correlation or prediction may be implied, this

is not proof of causation, and thereby may be unclear (Farrington 2000). Thus

Wikström suggests that the focus should be on the causal process rather than the

individual risk factors (Wikström 2011a). The process linking the causes and the

causes of the causes is explained by SAT in the following points:

(1) Crime is ultimately the outcome of a perception-choice process.

(2) This perception-choice process is initiated and guided by relevant

aspects of the person-environment interaction.

(3) Processes of social and self-selection place certain kinds of people in

certain kinds of settings (creating particular kinds of interactions).

(4) The kinds of people and the kinds of environments (settings) that are

present in a jurisdiction are the result of historical processes of personal

and social emergence.

(Wikström 2012, Figure 1.6)

21

This process is relevant in my study because, whilst one may not be fully able to

assess the personal characteristics underpinning a person’s moral context due to

data limitations, one can consider the processes within social and self-selection

contexts which affect the environments. This may have a bearing on the social

and personal ‘emergence’ of the recent types of activity within the banking

industry.

Social and personal emergence

The concept of emergence simply refers to how something comes into being

(Bunge 2003). Sullivan et al. suggest that using a framework which adopts ‘a

novel, conceptual and empirical framework’ will give a more accurate picture of

why crime occurs (McGloin, Sullivan, and Kennedy 2012). When developing an

emergence framework, one has to use blocks of ‘individual’ and ‘situational risk’.

These can vary according to theory. SAT proposes that people’s morality and

ability to exercise self-control are the key to propensity, combined with the

criminogenic setting of the environment within which they are situated and the

perception choice process which they use when deliberating. ‘Cognitive skills

development is the role key to social institutions’ with family, schools and peer

networks providing impact (Wikstöm 2014).

Social emergence creates criminogenic features according to the extent to which

moral norms and their enforcement encourage rule-breaking conduct. Of

interest in relation to my study therefore are the processes by which the

environments (settings) develop (1) particular moral norms and (2) specific

22

levels of moral norm enforcement through monitoring or intervention, and (3)

the frictions that are created (Wikström 2012).

Applications of SAT

SAT is a relatively new theory and unique in its framework. However, its

application has been considered in other recent studies in connection with

torture (Jerath 2011), violence (Haar and Wikström 2010), young offenders

(Wikström and Svensson, 2010), compliance (Wikström, Tseloni and Karlis

2011), anti-social behaviour (Wikström 2011b), adolescence (Wikström 2009),

self-control (Wikström and Svensson 2008), terrorism (Bouhana and Wikström

2008), and radicalism (Bouhana and Wikström 2011). There have to date been

no studies applying SAT to white-collar crime.

CHAPTER III

White-Collar Crime

‘Scrutinising the powerful’

Tombs and Whyte suggest that corporations are becoming similar to states: they

battle for control of power in the global markets, and their ‘activities’ have

become hidden from regulators and the public in pursuit of dominance and

wealth (2003). These hegemonic practices developed post-war into settings

which create an oligopoly (where only a few control the market) leading to

corporate deviance, typified by power, privilege and secrecy (Simon and Hagan

1999).

23

Research in the 70’s developed a ‘typology’ of white-collar crime which consisted

of:

1. Crimes by individuals on an individual or ad hoc basis [general white-

collar crime].

2. Crimes committed in the course of carrying out their occupations by those

operating inside business, government or other establishments, in

violation of their duty of loyalty and fidelity to their employer or client

[occupational].

3. Crimes incidental to and in furtherance of business operations, but not

the central purpose of business [organisational/corporate

crime/deviance].

4. White-collar crime as a business, or as the central activity [professional

white-collar crime/deviance] (Edelhertz 1970).

The definition of white-collar crime

The definition of white-collar crime was problematic for a number of years after

the concept was introduced by Sutherland in 1949. One of the key issues of

disagreement was the issue of the ‘development of social norms which became

harmful to society’ (Tombs and Whyte 2003). This paradigm is akin to part of

the framework of SAT. However progress in criminological research into white-

collar crime has been slow (Snider 1993). Snider’s studies reveal that

historically the funding available to review the acts and morality of corporations

was poor and it was not until the mid 90’s that major funding became available

24

in the US and UK (National Institute of Justice, Research Data, 1999, and Oxford

Research Project, 1995).

In 1996 ethical issues were ‘officially’ introduced into the definition of white-

collar crime. Simon had argued for a number of years that ‘measurable

standards of harm (damage) - physical, financial, and moral - constitute an

objective empirical standard by which the ethical dimensions of a deviant act

may be assessed’ (Simon and Hagan 1999). At the National White Collar Crime

Centre academic workshop held in Liverpool a broad agreement was reached on

including in the definition ‘planned illegal and unethical acts of deception

committed by an individual or organisation, usually during the course of

legitimate occupational activity by persons of high or respectable social status

for personal or organisational gain that violate fiduciary responsibility or public

trust’ (Helmkemp, Ball and Townsend 1996). This is the first time that a

definition has included concepts outside strict violations of the law. In my

opinion, leaning towards a concept of considering the moral context and

implications of rule-breaking, which may be both statutory and moralistic.

In this context ‘moral harm’ has been assessed as occurring where deviant

behaviour by elites creates deviance distrust and cynicism or alienation among

the rest of the population. Simon and Hagan use analogies in relation to

government scandals such as Watergate which resulted in a dramatic loss of

confidence in government and politics among the public. Similar financial

scandals in connection with insurance and mortgage mis-selling and public

losses which resulted in losses to the public are another example in the UK.

25

Large corporations who evade tax and are evasive and lie to the regulatory

authorities could also fall into this category and the events since 2008

demonstrate the ultimate knock-on effect on the government where public

confidence is damaged, especially when governments delay in intervening to

stop the wrong doing and wait until a crisis has developed.

But the trouble with white-collar crime has been that for so long both the

government and the public have neither categorised it as being serious nor have

they considered the damaging effects, both short and long term, of the behaviour.

White-collar criminals do not view themselves as criminals, and crime is not

their main activity (Simon and Hagan 1999). This distinguishes them from other

types of organised criminals; however I believe that there are behavioural

similarities between the two groups. Serious and organised wrongdoing is pre-

planned and conspiratorial, with potential individuals being identified and then

recruited into the action. White-collar crime may be considered to be possibly

more harmful than juvenile crime because of the resources that the powerful

elite possess.

Perhaps one of the reasons that the public has not viewed white-collar crime as

harmful to society is because of a lack of insight into the extent of the rule-

breaking. High profile trials such as the Guinness and Saunders frauds and the

UBS and Barings rogue trader prosecutions were complex and appeared distant

from the ordinary man on the street as opposed to knife crime or robbery which

have a much greater victim impact. Also unlike British crime statistics and data

which are publically available and freely reported in the press, financial and

26

banking crime is only revealed through the regulation process, through

transparency, reporting, investigation and sanctions, and ultimately criminal

prosecution. There has been much criticism by criminologists, politicians,

consumer groups and the police regarding the way in which regulatory

authorities act and the low number of prosecutions brought against individuals.

Lenience and legal lacuna’s

Criminologists have argued that white-collar criminals are treated differently

from other offenders (Pontell, Rosoff, and Peterson 2008). This raises a serious

question as to what impact this has on any deterrent effect or the way people

faced with an action alternative may perceive choices. This could arguably be

contributing to the criminogenic evolution of individuals and their environment

if one considers this in the light of the hypothesis and application of SAT. Often

the nature of individuals’ offenses, the social demographics of their backgrounds,

and the power of the organisations within which they work act as a ‘status

shield’ so that society could be not be blamed for feeling that ‘the rich get richer

and the poor get prison’ (Reiman 1995).

The absence of a lack of any criminal prosecution and transparent investigation

may lead the public to believe that the actions are due to incompetence, poor

controls, poor training and inadequate systems rather than dishonesty. But this

could arguably also be due to the sharp practices and skills of the lawyers who

are helping the organisations to evade culpability, thus being complicit in the

development of the moral conduct, are offering protection in connection with the

immoral behaviour, and are thereby complicit in the sense of ‘professional

27

white-collar crime’, an observation made by one of my sample group. This has

led to the regulators being criticised for their policies, practices, and

management and the ineffectiveness of their regulation and oversight of

corporations (HL: Paper 133 2013).

CHAPTER IV

Banking Regulation

History of Banking

The core business of investment banking is raising capital, sales and trading for

institutions and asset management companies, usually with non-retail clients.

This differs from the business of consumer banks, those that deal with the

everyday banking business of the general public. Arguably, until the financial

crisis in 2008 the general public had little idea of the day-to-day business of

investment banks, and saw them as remote and unconnected to their lives. Since

2008 and the collapse which resulted in several banks having to be rescued at a

cost to the tax payer with wider implications to savings and consumer

investments, greater awareness and interest is now levied towards investment

banks and bankers in general.

The City of London has became a centre for financial activity, housing global

operations within the square mile, and financial markets have experienced

staggering growth which continues to accelerate to service the global needs of

the world. The UK together with other common law countries (USA/Australia)

developed a combined regulatory and enforcement structure to manage the

sector. This historically evolved with the Securities Act 1933 and the Bank of

28

England’s supervision (Nelken 1994). The City of London operates uniquely as a

village with specific terms; however ‘many of the same factors that have

protected the City’s relative autonomy for so long persist and have contributed

significantly to the litany of scandals that have been a perennial feature of the UK

financial sector’ (Gillligan 1999). The incestuous nature of the banking industry

and the rule-breaking going on within it have been widely studied (Ashe and

Counsell 1990). In 1970 the UK moved to a system of self-regulation where

internal checks and monitoring were the responsibility of the institution.

However it was not until 1986 that the Financial Services Act was passed setting

out a regulatory system of acceptable practices and providing an external

monitoring body to oversea the functions.

The first regulating ‘Act’ created a statutory-based regulatory authority model

(the Securities Investment Board or SIB). This was a private company presiding

over a number of self-regulatory organisations (SRO’s) and assisting with

implementation and compliance with UK and European statutory rules,

regulations and directives. In October 1997 the UK established a new regulator.

The Financial Services Authority (FSA) were launched by the then Chancellor,

who promised that it would ‘be equipped with all the statutory functions and

powers needed to operate a single regime for authorisation and regulation of

financial services’ (Gilligan 1999). However, it appeared to lack the weapons to

engage in the promised combat and, following criticisms and concerns regarding

its efficiency and compliance with the present system, a joint committee of both

houses (Commons and Lords) was set up to examine the failings and make

proposals. They took oral and written evidence from a wide variety of sources

29

and ultimately produced the first joint report of the Joint Committee on Financial

Services and Markets 1999, which was later enacted as the Financial Services

and Markets Act 2000 (FSMA) (Penn and Moran 2012).

The Regulatory Framework

Since 2000 investment banking has been managed by the FSMA and the FSA,

with the Bank of England having operational policy responsibility and playing a

significant role in financial stability. This was amended slightly by the Banking

Act of 2009, making provision for the nationalisation of banks and amending the

insolvency provisions and financial services compensation schemes, following

the global financial crisis. Additionally, investment banks are subject to the same

directorial duties and responsibilities stipulated by the Companies Act 2006

which require them to honour their ‘fiduciary duties’ (responsibilities to

investors) and ‘director competencies’, by always acting with reasonable care,

skill, judgment and expertise in the management of the company. Investment

banks must have an organisational structure compliant with corporate

governance rules. ‘Good governance increases the probability that good

decisions will be made’ as it has been the regulators’ view that ‘poor governance

was a lead indicator of significant problems within the firm’ (Barker et al. 2013).

But this statement appears to have been continually revisited following crises

and scandals within the banking industry which have necessitated internal

investigation and external political review, and usually resulting in additional

regulation or a change of the way in which we regulate a business.

30

Following the global financial crisis commencing in 2008, the government

established a parliamentary banking select committee on banking standards,

with independent experts and consisting of cross party members and which was

to consider the present position with respect to the causation of the difficulties

and to make recommendations for policy change. The first report concerned

HBOS, a bank rescued by the Government and nationalised at the tax payer’s

expense; this was a ‘story of catastrophic failures of management, governance

and regulatory oversight’ (HL Paper 133 2013). But, to the surprise of the

committee, only one director, Peter Cummings, had faced regulatory sanction for

HBOS’ failures. This prompted criticisms that the FSA ‘had taken no steps to

establish whether the former leaders of HBOS are fit and proper persons to hold

the Approved Persons status’ (FSA para 83). Similar comments have been made

by criminologists studying failures to sanction reckless management (Reiman

1995). Research participants also commented on the lack of sanctioning in

general in relation to the core issues explored within the study, leading to the

creation of weaker environments within the schemes of control and deterrents

(See Tables 2b, 3b at pages 46 and 55). Poor management is not only an

indicator of a correlation with crime but is evidence within SAT of a contributor

to the causal process for establishing criminogenic settings and impacting

personal morality.

Parliamentary banking reviews

In June 2013 the Parliamentary Committee released their second report in two

volumes. This considered the changes necessary in the wake of their enquiry into

the LIBOR scandals and professional standards and culture in the UK banking

31

sector (Parliamentary Banking Commission 2013). The report exposed

‘shocking and widespread malpractice’, which ‘gravely damaged the reputation

of the financial sector … causing the public opinion and trust to fall to an all time

low’. The report found that the conduct failing had no shared causes with a single

resolution which would be able to restore the trust and repair the damage. But

they were concerned to report within their findings that ‘many junior staff who

may have done nothing wrong have been impugned by the actions of their

seniors’, a state of affairs which clearly had to end. Their report made a number

of recommendations which focused, surprisingly perhaps, not on more rules and

regulations to take control, but a better understanding of the way in which the

rules and controls were designed to act and what objectives they sought to

achieve. They too criticised the regulatory body responsible for management

and gave key guidance as to what actions would create a better environment.

These include ‘making senior bankers personally responsible, reforming bank

governance, creating better functioning and more diverse markets, and

reinforcing the powers of regulators and making sure they do their job. It was

suggested that a new offence be created to cover senior persons engaging in

reckless misconduct in the management of a bank which would carry a custodial

sentence (Parliamentary Banking Commission 2013).

The government were quick to respond in July; they adopted many of the

recommendations, confirming their intention to ‘plan to review the collapse and

produce guidance following HBOS and RBS, set a new banking standards regime

governing the conduct of bank staff, introduce a criminal offence for reckless

misconduct by senior bank staff, and take further steps to improve competition

32

in the banking sector’ (H.M. Treasury Report, Department for Business

Innovation and Skills 2013). In advance of these reports the government had

already reformed the failing FSA by reshaping the regulatory management

systems around banks. The changes took effect in April 2013 and were

described as ‘the dawn of a new era’ (Cable, p6 in H.M Treasury Report 2013).

This followed the perfect storm between 2008 and 2012 which saw the industry

ravaged by scandal, corruption, and malpractice so that it appeared to be totally

out of control.

The current regulatory duties are split between 3 executive functions, the

Financial Policy Committee (FPC) under the control of the government and

formulates policy and guidance and makes recommendations. The Prudential

Regulatory Authority (PRA), a subsidiary of the Bank of England, is responsible

for promoting stability and prudent operation. The Financial Control Authority

(FCA) is responsible for the regulation of conduct in retail, wholesale and

financial markets and for the infrastructure that supports those markets.

One issue which until recently has appeared to be absent from banking culture,

is ethics. In a speech given by the director of the FCA, when talking of the future

direction of the industry he emphasised ‘the need for firms’ ethics to be built

around their customers…’, He stated that ‘the various investigations and reports

of regulators had concluded that the cause is usually not about failure to comply

with the specific rules but rather the fundamental flaw in the firms’ business

model, culture or business practices’ (FCA Press Release 2.12.13).

33

Economists have commented that ‘banks and financial institutions appeared to

believe and behave as if ethic were not relevant to their business’ (Koslowski

2009). The only principles they followed were mathematical with emphasis in

the way in which the business was contractually constructed. The industry

appeared sheltered by lawyers’ due diligence and contractual clauses and

schemes aiming to offer them ‘protection’ from recourse to their conduct.

Similar observations were made by the FCA who, when seeking to investigate the

banks in accordance with their duties, were met with non-cooperation, hostility

and the ‘harboring’ of employees whose conduct necessitated investigation (FCA

2012). The lack of focus on the moral context of these environments both

‘socially’ and ‘situationally’ has left the industry bereft of conscience, as

demonstrated by the findings of the regulators and parliamentary enquiries. So

much actuarial assessment was involved in the banking process that numerous

studies have shown there were ‘hidden perils’, for example a contagion of over-

estimation of products, which caused ‘herding trends in behaviour’ (Koslowski,

2009). If this has been the findings of economists regarding the financial

catastrophes, then one can consider that the ‘herding trends’ of behaviour within

these institutions may be producing similar criminogenic and propensity trends

in relation to white-collar criminal activity.

The very nature of these environments and the FSA manual promoting ‘high

level standards, principles of business, management, and system control, and

ensuring that individuals are ‘authorised’ and fit and proper people, who are

trained and competent’ (FSA Handbook, 2013) should lead us to focus rather on

the morality of these environments, and the ‘self and social selection’ which may

34

occur as part of the compliance and prevention strategy for better regulation. In

these high octane environments ‘where there is a great measure of influence and

power, there must also be a great measure of conscientiousness and moral

awareness, because power itself is a moral or ethical phenomenon’ (Koslowski,

2009).

However we may be experiencing a paradigm shift in both prosecutions and

sanctions following the lack of previous lessons learnt. In July 2012 the FCA

brought proceedings for market-related offences against a proprietary trader at

Mizuho International. Having made findings against him they fined him

£175,000 and issued a prohibition order, preventing him from working within

the financial services industry. He appealed and the tax chamber hearing his

appeal allowed his appeal in relation to market abuse, ordering the FCA not to

take any further action, but in their judgment made a finding of fact that he had

lied to both the chamber and FCA. The FCA appealed this to the Court of Appeal

on the issue of the prohibition order, insisting that given the findings, even

though he had been cleared of the wrong-doing, the fact that they concluded he

had lied meant ‘he was not a fit and proper person’. The Court of Appeal agreed,

remitting the case to the Chamber who ruled that ‘in putting a false defence to

the FCA during the course of its investigation, and in maintaining that defence in

evidence before the Tribunal, he had exhibited a lack of integrity such that he is

not a fit and proper person’ (FCA v Hobbs 2013). The director of enforcement at

the FCA was quick to issue a statement stating that ‘[he] had failed to

demonstrate the standards of behaviour from a person in privileged position and

failed to act in his basic responsibility to act with integrity. If you cannot tell the

35

truth, there is no place for you in the financial services industry’. (FCA,

December 17 2013). This could see new ‘frictions’ emerging to combat the

phenomena of rule-breaking within investment banking and a strong basis for

the working of situational action theory in that setting.

CHAPTER V

Research Method

The research question was ‘moral contexts and rule-breaking in investment

banking: The application of Situational Action Theory

The purpose of the study was to analyse the moral contexts and types of rule-

breaking found in investment banking and to investigate whether there was any

support for the application of Situational Action Theory. With the research I

hope to gain an insight into the working environment in investment banks and to

consider and study the interplay between people’s criminal propensity and

criminogenic exposure using the framework of SAT, and to examine whether this

affected their involvement in crime and possible criminal careers.

The specific research questions for this research were:

1. To explore the moral context of the environment of investment banking.

2. To consider whether rule-breaking activity occurred.

3. To examine the application of the framework and mechanisms of SAT to

that environment.

4. To investigate the causal process and factors impacting individuals and

their environments and consider the implication for managing risk.

36

Participants and sample method

There were 20 participants in the study. 18 were interviewed, one pulled out on

the day of interview, and one withdrew consent following the interview.

Participants were selected using a targeted key informant, who then facilitated

with a semi-respondent-driven snowball sample of investment bankers who

were currently working or had previously worked within a primary trading

environment. Individuals linked to primary trading activities, i.e. traders, sales

representatives, analysts or management, were selected because their areas

were related to the area within which I had been employed and which I had

knowledge of. The environment was also selected because it is considered the

most volatile and stressful one in the banking business. This was relevant

because we know that stress and anxiety can impact the moral filtering process

(Wikström et al. 2012).

The snowball technique is often used for areas of research or for individuals that

are hard to identify or reach (Bachman and Schutt 2013). It is commonly used to

access and interview members of gangs and organised criminals (Wright and

Decker 1994; Decker and Van Winkle 1996). Unlike many others where

respondent-driven sampling was used, no rewards or gratuities were provided

for the respondent or peers. Each introduction produced successive waves into

the groups of interest. It was difficult to find willing participants from within

the targeted sample group. This was due to difficulty in accessing information

about suitable individuals, negative media press regarding the plethora of

banking scandals which has given rise to trust concerns, ongoing internal

enquiries and company sensitivities, and the general fears of individuals

37

regarding the confidentiality of their participation. There are, in my opinion,

some similarities between these two groups and the fears that they possess

regarding trust, disclosure, identification and investigation.

However it is not suggested that a completely random selection was made due to

the limitations of the study, outlined in the findings and discussion chapter. Due

to the difficulties experienced and the numbers approached, I used two strong

key informants who agreed to assist with contacting sample participants. Both

had in excess of thirty years experience within the banking industry and had

held global director positions within a public bank and a private equity business.

They agreed to provide an ongoing reference to other participants as necessary.

In seeking to recruit a suitable sample group it was necessary to use their

executive status in addition to the introduction for ongoing confirmation of my

identity and purpose of study, to validate the confidentiality agreement and the

issue of trust.

Following one of the interviews with a participant who was employed within an

institution under extreme scrutiny who then withdrew, I received threats of legal

action and was compelled to give undertakings to destroy data collected and

remove them from the study. Another participant who had been in regular

contact up until the day of proposed interview withdrew at short notice. The

peer who had provided the introduction received a hostile telephone call from

the participant’s managing director. He was accused of recklessness and

insensitivity towards their organisation for encouraging the employee to

participate in my research, hence compromising the organisation’s privacy.

38

These experiences lend weight to the propositions established in the study of

white-collar crime, that powerful corporations seek to misuse their ‘corporate

veils’ (a legal term used for allowing companies to operate privately) to allow

them to develop secretive, oppressive norms and operate beyond any public

scrutiny (Tombs and Whyte 2003).

Ethical Considerations

The study received approval from the Institute of Criminology Ethics Committee.

The research was conducted by asking participants to comment as ‘observers’ of

their environment. This provided safeguards against them specifically

implicating themselves or others in any criminal behaviour during the course of

their response to the questionnaire.

A participation information sheet was prepared (Annex A) setting out the nature

of the study, which was ‘to learn more about the working environment in

investment banks’. A statement was made explaining that I was seeking their

assistance as their knowledge and experiences were very important for a

complete and reliable picture to be obtained of what it is like working in

investment banking. I explained who I was and gave a brief summary of what I

was researching and the purpose of my study. I set out clearly how I would

communicate with them and what would happen with the information obtained.

Thorough transparency and detail was provided due to the fact that following

my short career within investment banking, I became a qualified criminal

barrister. I am presently on sabbatical from independent practice within a

common law set of Chambers, but I feared simple internet research of my

39

professional background could impact on participants trust and their willingness

to cooperate with my research. Therefore this information was provided at the

outset of the study.

Clear guidance was provided in the participation information sheet on how the

research would be conducted (via one-to-one interviews lasting approximately

30-40 minutes) and it was explained that the interviewees had the freedom to

participate and fill out the questionnaire to the extent they felt comfortable. The

need for participation consent together with their right to withdraw at any time

were included, together with a declaration stating that they had read the

participation information sheet and agreed to take part in the research. This was

designed to ensure that the maximum informed consent was obtained. I sought

permission to record the interviews advising that anonymous quotes might be

used unless they indicated otherwise. An additional binding confidentiality

clause was added to the consent form in order to reassure any participants who

raised concerns regarding the protection of their identity.

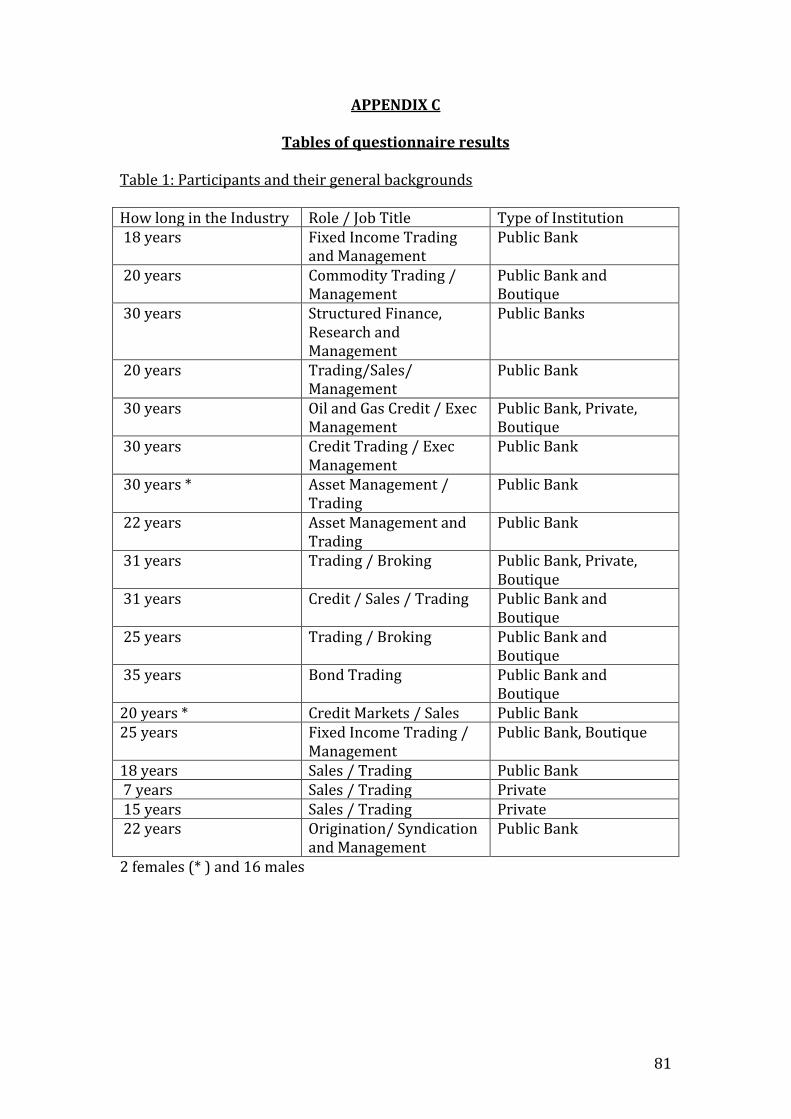

Participants and their general background

All participants emanated from a trading floor environment. This environment

was selected because I had worked within capital markets for three years at two

different American investment banks, and therefore, despite my experience

being historic, I had some appreciation of the business and its challenging

environment. SAT proposes that cognitive skills have a vital function in the

‘moral filtering process’ and the ability to properly evaluate perception choice

within its framework (Wikström and Treiber 2007). The trading floor is known

40

to be a volatile and stressful environment and, as is demonstrated in some of the

research findings, those individuals interviewed were insightful subjects in the

context of this issue. Several of the participants referred to the impact of

cognitive impairment due to ‘pressures’ such as stress, anxiety, exhaustion,

drugs, and alcohol. Despite my knowledge being outdated, I found the

participants were at ease when discussing my own history and I had a basic

comprehension of the general terminology used during the interview. This

proved essential both in conducting the interview and in evaluating the data.

The sample group had in the majority substantial experience within the banking

industry. Many of the individuals had held management positions in addition to

their core jobs. During the recruitment of the sample there was greater

reluctance to participate from those less experienced in the industry. Where

individuals had worked in more than one type of institution I asked them to

clarify the setting in response to some of their answers.

Procedure

Initial contact was made with a key informant with whom I had worked in the

City. He assisted with both the piloting of the questionnaire and the first wave of

snowball sampling. The snowball sampling process consisted of the participant

contacting a colleague and providing him or her with my participation

information sheet, together with confirmation that I was a known and trusted

individual. The new wave sample’s preferred contact details were then provided

to me and I made contact with the prospective participant. Contact was made by

phone and via my academic email; I provided a further copy of the participation

41

information and consent details and answered any further questions from the

individual. 75 people were contacted during a four month period to secure the

20 identified suitable for the final sample group. Recruiting the sample and

managing the interviews was a continual process for eight months. Many sought

additional reassurance and in order to secure participation I maintained contact

with them. I considered that the location and setting for the interview might

have an impact on the participants. I offered participants a choice of two venues

to meet at: a boardroom in Green Park or a private conference room in the Law

Society reading room. Some of the participants requested that the interview be

conducted within their working environment.

The interview was designed as a structured questionnaire, where the responses

could be measured using a uniform process. 16 of the 18 interviews were tape

recorded and fully transcribed. Two were transcribed from notes made during

the interview as they refused for the interview to be recorded. 16 were in the UK

and 2 were in the USA. All had worked in the US and UK investment banking.

The questionnaire was designed to capture quotes and insights suitable for

qualitative review rather than any complex quantitative data. This method was

used due to the size and selection of the sample group. The general approach of

‘thematic coding analysis’ was followed. Data was given labeling codes, data

themes collected and patterns considered using tables (Robson 2011).

The interview was conducted in a semi-structured way, allowing the participant

to reason their responses. Of the 18 interviews, 2 were conducted face-to-face in

a private office via Skype due to the respondents being in New York; all others

42

were in face- to-face interviews. 4 were conducted in a private boardroom, 5

were conducted on the trading floor, and 7 were conducted in other private

locations such as hotel lobbies, cafés, or private member club lounges. 3

participants were known to me from my time working in the industry, and the

other 15 were strangers.

The design of the questionnaire and the specific questions posed to bankers

were adapted from the collective efficacy model used by the PADS study.2 I

selected this model because it is an established measure for considering the

moral context of an environment. (Wikström, Trieber, Oberwittler and Hardy

2012). There has also been empirical support for the connection it makes

between structural characteristics and crime. The PADS model combines

residents’ reports of social cohesion and levels of informal social control in the

effort to intervene in cases of crime and disorder within a neighbourhood

setting. I saw the trading floor environment as analogous to this setting. Whilst

the PADS model focused on anti-social activity within the neighbourhood, my

questions were framed around known illegal acts perpetrated as white-collar

crime.

The four areas of illegal activity considered in this questionnaire were

‘illegitimate rate fixing’, ‘mismarking profit and loss within a trading account’,

‘insider trading’ and ‘misuse of company privileges’. After piloting the questions

and the potential problems with defining these activities, I included a definition

2 Peterborough Adolescent and Young Development Study

43

of what I understood each term to mean at the beginning of each of these

sections in order to clarify any ambiguity which might arise prior to addressing

each area. Illegitimate rate fixing was defined as ‘establishing the price of a

product or service illegitimately, exploiting knowledge or weakness, and acting

alone or collusively rather than allowing it to be determined naturally through a

free market’. Mismarking was defined as ‘valuation of a traders account at less

than the market rate by over or under inflation, or hiding assets that have been

bought or sold’. Insider trading was defined as ‘buying or selling securities by

someone who has access to material, non public information’. Misuse of

company privileges was defined as ‘using privileges preferred due to

employment in circumstances outside the permitted use, for personal gain’.

In addition to information about the four formal areas of specific actions, I

gathered very limited personal background data regarding how long the

interviewees had worked in investment banking, their role or the job titles that

they had had and the types of institutions that they had worked in. I applied

caution in seeking not to collect too much personal data in an attempt to

maximise cooperation in the main focus of the study as participants were

concerned that they should not be identifiable from the background information.

Members of the sample group were the exclusive ‘key informants’ in my data

collection. The PADS study sought access to education information, police

national computer records, conducted surveys, and had longer periods to gather

personal information. Due to limitations with time, data and the information

available the focus was on the moral context using their sole observations.

44

I grouped the type of institutions into public banks (large high street

institutions), private equity business (privately owned companies) and boutique

hedge funds (groups of individuals who are accredited to trade and manage

investments and private funds). All of these companies are subjected to identical

regulation but vary in their size, set-up, business model, operational activities

and management. This was designed to allow for analysis of whether there

were any variables or themes arising in the data collected from these different

groups. 16 had exposure to public banks, 4 to private equity companies and 6

boutique hedge funds. It balanced because many had worked in all types of

institutions and qualified their answers in relation to the responses to the

questionnaire.

The questionnaire in Annex B was amended following a pilot review of the

questions. After I had piloted them with a banker personally known to me, I

realised that participants would require reassurance as to why I was interested

in them, hence the short explanation was added regarding why I was asking

them to share their knowledge. I further noted from my pilot study that I needed

reassure them regarding confidentiality due to the topics being explored during

the interview. I therefore allowed a few minutes to converse, answering

questions about who I was and the study, before I embarked on tackling the main

core issues. Information regarding data protection and its destruction after the

study’s completion was reinforced for the same reasons. I collected simple

background data regarding their longevity in the business, job titles and types of

institutions experienced.

45

The four areas of known white-collar rule-breaking actions were then explored

so as to gather data in a uniform way regarding whether the respondents

believed the particular rule-breaking action had occurred, the prevalence of the

action, how many people were involved in committing the act, whether it would

be reported and, if so, to whom, what the typical consequences would be, and

what would promote or deter the action. Frequency and prevalence were not

fully capable of measurement due to lack of empirical data. Measurements used

for the responses were ‘most’, ‘some’, ‘few’, ‘almost never’ with regards to action

occurrence, and reporting colleagues for something was measured by ‘yes

always’, ‘yes sometimes’, ‘yes but rarely’, ‘no never’. I also sought to collect

frequency data for occurrence daily, weekly, monthly, annually. Additional types

of rule breaking not identified by the questionnaire were left as open-ended

questions at the end of the study. I also sought to solicit the participants’ views

as to whether people who broke rules in one area were more likely to break

rules in another. A copy of the questionnaire is included in appendix B.

CHAPTER VI

FINDINGS AND DISCUSSION

The presentation of this chapter shall broadly follow the specific research

questions for the research as set out at page 35, it also follows the structure of

the questionnaire posed to bankers and seeks to apply SAT under the

conventional headings.

46

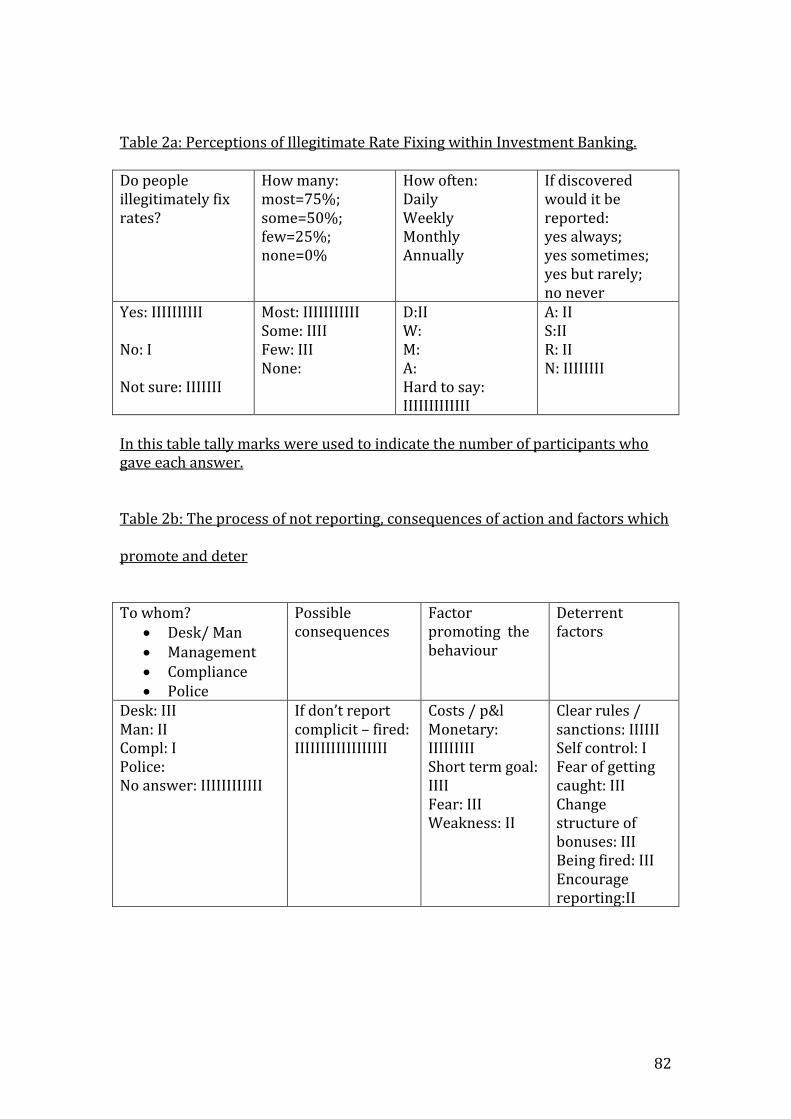

The moral context of investment banking

The study provided anecdotal insight from a group of very experienced bankers.

16 of the 18 had worked within the industry since the first rules relating to

securities and investments were implemented in 1986 and provided valuable

observation of the evolution of their environment and it’s morality. See Table 1

in Appendix C for the data collected.

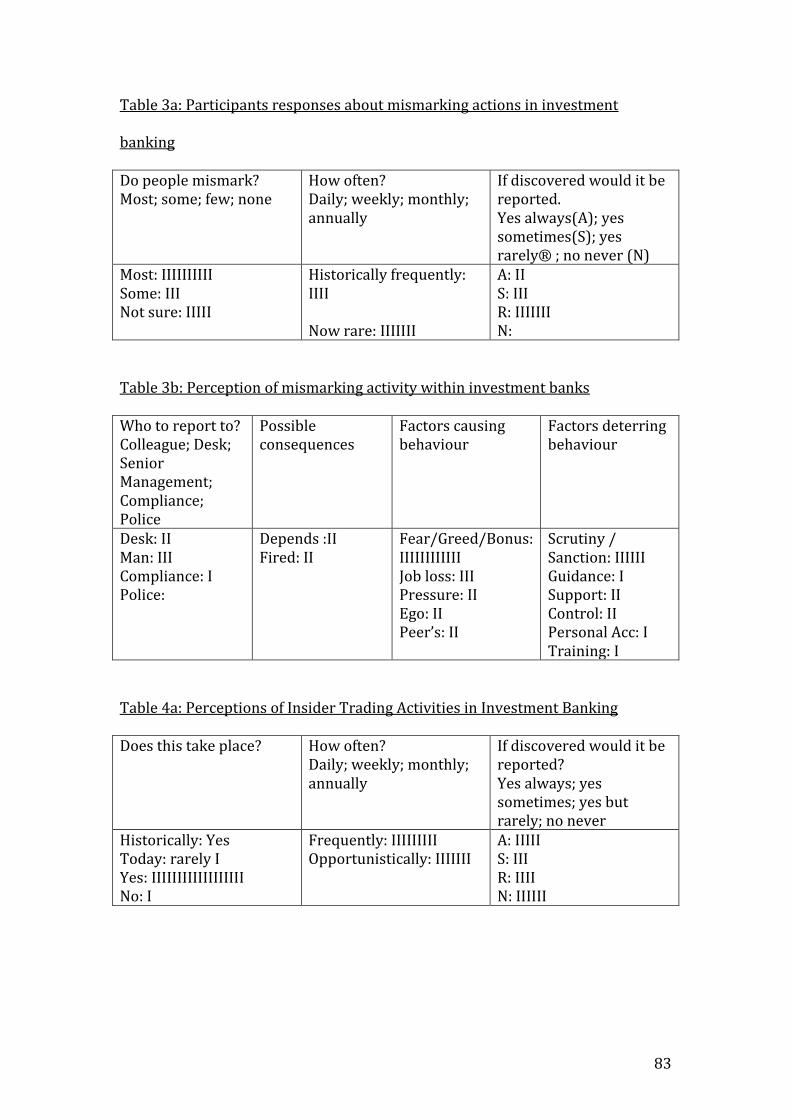

In many instances particularly in relation to illegitimate rate fixing and

mismarking of profit and loss responses questioned whether these acts were

rule-breaking at all. This is important in the context of considering the norms

created as the first proposition of SAT is to consider what is crime, SAT views

crime as moral actions, (Wikström 2010) if, as bankers reported they do not

believe that they are committing a crime, then their moral norm will be that it is

acceptable behaviour. Therefore where the rules are unclear moral levels are

unguided as to what is the right and wrong way to act. Some comments

demonstrating this are below.

“it’s difficult to define ‘illegitimate’ as the subject term often has a value judgment

which you decide whether its breaking the law or not ….”

“The problem is the ambiguity, sometimes it’s hard to know you’re breaking the

rules when you’re marking a volatile position …. You just find your own gut instinct’

… regarding rule-breaking “there won’t be a single trader of my era who hasn’t

done it…”

“the trouble is, none of the activities you’re mentioning used to be illegal… so it’s

hard for many old school to apply the new regime ..”

47

“many don’t see these actions (illegitimate rate fixing & mismarking) as wrong, it’s

just doing Bob a favor”.

Applying SAT to environments where opinions such as these are held is useful

because analysing crime as moral action doesn’t imply a moralistic approach, or

for an acceptance or rejection of the rule of law. To view crime as actions that

break rules doesn’t necessarily need laws, when you are considering crime as

moral actions it applies to all kinds of actions and equates them to rule breaking

or abidance, and not why they do an act but why they break the rules,

(Wikström, 2011), this was easier to explore as a concept during the interaction

with my bankers.

Many of the bankers stressed that there were compliance controls and training

regarding the correct procedures, but failed to relate this to their own moral

personal setting and thus appeared disconnected from the moral context. An

example illustrating this was provided by a trader regarding the contrast

experienced between a US and Japanese Bank. “I had been allowed to have large

positions at X and I was always trusted to operate my positions safely and

efficiently, the US were also flexible about my time keeping and how I chose to