Regionality, customer proximity & sustainability

Solid core earnings based on sustainable business model

'HETA solution' positively impacts 2016 financial profitability

Substantial profit retention further strengthens already sound capitalisation

Continued significant growth in customer deposits

E | May 2017

HYPO NOE Investor Presentation

2

Section Slide

I. Group Business Strategy 3

II. Business Outlook for 2017 14

III. Financial Figures 15

IV. Funding 19

V. Contacts 26

Appendix Key Financial Statements and Further Details 27

Content

3

State of

Lower Austria

Vienna

I. Group Business Strategy HYPO NOE at a Glance

HYPO NOE Group: more than 125 years of track record and expertise

Regional market leader in Public Finance

Local banking partner for retail customers in Lower Austria and Vienna

Fully integrated service chain in the real estate business

Focused on Austria, Germany and on a selective basis EU-countries

in the neighbouring Danube region

Strong ratings

Issuer Rating: 'A/A-1' from Standard & Poor’s with stable outlook

Public Sector Covered Bonds: 'Aa1' from Moody’s

Mortgage Covered Bonds: 'Aa1' from Moody’s

Sustainability: 'C' from oekom research with status 'Prime'

Committed and reliable shareholder: State of Lower Austria owns 100 %

Leading issuer of Pfandbriefe in Austria

4

I. Group Business Strategy Recent Developments

Proposed Merger of HYPO NOE Landesbank AG and HYPO NOE Gruppe Bank AG

Schedule

June 29, 2016: Supervisory Board of HYPO NOE Gruppe Bank AG initiated a project to prepare a merger

with its 100 % subsidiary HYPO NOE Landesbank AG

Merger is scheduled for completion by autumn 2017 with retroactive effect from January 1st, 2017

Objective

Reintegration of the retail and housing finance businesses into the core universal bank

Primary purpose is an increase in efficiency of the banking group by lowering complexity of the

organisation and realising operational synergies

Process

Preparatory measures were started in 2016, and the merger progress is proceeding on schedule

Change management process has been initiated – with employee involvement and participation at the

heart of overall project success

5

I. Group Business Strategy Core Market: Competitive Economy

Austria

Positive GDP development

2016e + 1.5 % (EU19: 1.7 %)

2017f + 1.8 % (EU19: 1.6 %)

GDP per capita1 above average

2016e EUR 46,822 (EU19: EUR 38,986)

2017f EUR 48,617 (EU19: EUR 40,398)

One of the lowest unemployment rates within the EU

2016e 6.0 % (EU19: 9.9 %)

2017f 5.8 % (EU19: 9.4 %)

Public debt below EU average

2016e 84.6 % (EU19: 91.7 %)

2017f 82.4 % (EU19: 90.6 %)

Level of corporate and household indebtedness substantially

below Euro-zone average

Attractive yield spreads relative to Germany

Housing market: no oversized construction sector and low level of

household indebtedness

Lower Austria / Vienna

40 % of Austria‘s population live and work in

Lower Austria and Vienna

Region with highest population growth potential

2015-2075

41 % of Austrian GDP is generated in Lower Austria and Vienna

Highest gross income from employment

Lower Austria (# 1) EUR 33,118

Vienna (# 3) EUR 31,330

Highest purchase power per inhabitant

Lower Austria (# 1) EUR 21,048

Vienna (# 3) EUR 20,870

Fiscal equalisation scheme secures strong and prudent

framework for investors

Privileged access to international financial markets through

Federal Financing Agency (ÖBFA)

1 EIU, GDP per capita at purchase price parity; 03/2017

6

Issuer rating 'A/A-1' with stable outlook confirmed by Standard & Poor’s in August 2016

Strong capital position, GRE status, strong link to and important role for the State of Lower Austria as reliable owner

Public Sector Covered Bonds and Mortgage Covered Bonds both rated 'Aa1' by Moody’s – confirmed in October 2016

Credit strength of the issuer, credit quality of the assets, strength of the Austrian legal framework and OC level

On October 14th, 2016 Moody's Investors Service confirmed the 'Aa1' ratings for both mortgage covered bonds and public sector covered bonds issued by HYPO NOE

Gruppe Bank AG. Following the announcement by Kärntner Ausgleichszahlungs-Fonds ("KAF") on October 10th, 2016 that the required two-third acceptance rate for its tender

offer for Heta Asset Resolution AG's ("HETA") debt obligations was comfortably met (acceptance overall was 98.71%, of which 99.55% for senior debt and 89.42% for

subordinated debt), the rating agency has concluded the various rating reviews-of-Austrian-regional-mortgage-banks. On October 14th, 2016 the over-collateralisation can be

displayed as follows:

HYPO NOE Group’s public sector covered bonds have an over-collateralisation (OC) of 33.0% with a minimum OC level of 20.0%, of which 0% is on a "committed" basis.

HYPO NOE Group’s mortgage covered bonds have an over-collateralisation (OC) of 68.0% with a minimum OC level of 12.0%, of which 0% is on a "committed" basis.

In August 2016 Moody's upgraded the outlook for the Austrian banking system from negative to stable for the first time since 2009.

1 Unsolicited Rating

Issuer Type of Rating Standard & Poor’s Moody’s

Issuer Credit Rating 'A/A-1' (stable) -

Public Sector Covered Bond - 'Aa1'

Mortage Covered Bond - 'Aa1'

State of Lower Austria Issuer Credit Rating 'AA' (stable)1 'Aa1' (stable)

Republic of Austria Issuer Credit Rating 'AA+' (stable) 'Aa1' (stable)

I. Group Business Strategy Strong and Stable Credit Ratings

7

Sustainability ratings are an important evaluation with regards to corporate social responsibility performance and as such for a

holistic and future-orientated corporate governance. Therefore, sustainability ratings become an increasingly important aspect of

socially responsible investment decisions.

The corporate social responsibility performance of HYPO NOE Group is currently assessed by the sustainability rating agencies

oekom research, imug and rfu.

As part of a successful sustainability programme HYPO NOE Group was in 2015 awarded for

the first time a 'C' rating with the status of 'Prime' .

'Prime' is awarded for an above-average commitment in the areas of environmental and social

responsibility.

HYPO NOE Group was rated in 2016 by the Austrian rating agency rfu and awarded with the

status of "rfu qualified" (rating result: ba ). rfu is an Austrian company specialising in

sustainable investment and in particular sustainability analysis .

The best performing companies are awared with the status "rfu qualified“ and added to the rfu

sustainable investment universe.

I. Group Business Strategy Top Sustainability Ratings from oekom & rfu

8

HYPO NOE Group is in the upper quarter of all rated issuers of Public Pfandbriefe (Public Sector

Covered Bonds) .

HYPO NOE Group is the best of all rated issuers of Public Pfandbriefe in the savings bank

sector .1

1 As an issuer HYPO NOE is assigned to the savings bank sector (incl. Landesbanks and mortgage banks).

HYPO NOE Group is in the upper quarter of all rated issuers of mortgage bonds (Mortgage

Covered Bonds).

HYPO NOE Group is the best of all rated issuers in the savings bank sector.1

HYPO NOE Group is in the upper quarter of all rated financial institutions (including development

banks).

HYPO NOE Group is the best of all rated issuers in the savings bank sector.1

I. Group Business Strategy Top Sustainability Ratings from imug

9

Public Finance

Corporate & Structured Finance

Religious Communities,

Special Interest

Groups & Agriculture

Real Estate Finance

Real Estate Services

Retail Customers

I. Group Business Strategy Competence and Experience Drive Business Focus

Strategic Business Units

Public Finance

Financing and leasing solutions for the public sector

Corporate & Structured Finance

Corporate and structured finance solutions

Project and infrastructure finance

Local SMEs

Religious Communities, Special Interest Groups &

Agriculture

Financing solutions

Ethical investments

Property & facility management

Real Estate Finance

Financing of commercial projects and housing developers

Real Estate Services

Project development and management

Property management

Facility management

Retail Customers

Experts on mortgages and housing for private customers

and special services for professionals

10

Business position

Partner of local and regional authorities, public agencies and

infrastructure companies

Public construction projects including leasing solutions and PPP

(Public-private-partnership)

Focus on Lower Austria and Vienna, active in selected countries

of Danube region

Long-standing cooperation with EIB, KfW, EBRD

Recent developments

Key revenue generator

Reference project Mistelbach-Gänserndorf State Hospital:

design-build general contractor solution that brought the project

in on budget and on schedule

Strategy

Remaining core business of HYPO NOE Gruppe

Reduction and diversification of Public Finance portfolio actively

promoted – resulting in a lower balance sheet total

Expanding market share in Austria

Syndications

1 Pro-forma analytical breakdown over all IFRS segments 2 Fee income + interest income

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2016 2015 2014 2013

Retail customers

Real Estate Finance

Corporate & Structured Finance

Public Finance

HYPO NOE Group – Total Assets1

29%

16% 29%

26% Public Finance

Corporate & Structured Finance

Real Estate Finance

Retail customers

HYPO NOE Group – Total Revenues2

I. Group Business Strategy Public Finance

11

Business position

Corporate and structured corporate finance solutions for the mid-cap

and large corporate segments

Regional focus Austria, Germany and defined markets of the Danube

region

International business focus on infrastructure and corporates of

strategic relevance.

Specialized team for target group religious communities, interest

groups and agriculture

Recent developments

Intense competition and subdued credit demand

Focus on SME business in core markets

Financing of the renovation of sacral buildings

Selective financing of renewable energy projects

Strategy

Structured corporate lending will remain a high priority

Drive Danube strategy forward by partnering with Austrian and local

businesses in the region

Build up a range of ethical investment products

1 SME business (33% of corporate portfolio) is part of HYPO NOE Landesbank

2 Pro-forma analytical breakdown over all IFRS segments 3 Fee income + interest income

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2016 2015 2014 2013

Retail customers

Real Estate Finance

Corporate & Structured Finance

Public Finance

HYPO NOE Group – Total Assets1

29%

16% 29%

26% Public Finance

Corporate & Structured Finance

Real Estate Finance

Retail customers

HYPO NOE Group – Total Revenues2

I. Group Business Strategy Corporate & Structured Finance1

12

Business position

Financing solutions for the asset classes:

office, logistics, warehouse and residential property, shopping

centers, retail parks, hotels, rental apartment properties/portfolios

Active in Austria, Germany and Danube region

Promoted housing developers (Wohnbaugenossenschaften) – low

risk business

Recent developments

Rising demand across all real estate categories due to low interest

rates

A number of early repayments, mainly as a result of early refinancing

or property disposals by customers

Strategy

Growth in Austria and Germany

Close watch on regional real estate trends

in Danube region

Maintaining strong relationships with

promoted housing developers in Austria

1 Promoted housing business (45% of real estate portfolio) is part of HYPO NOE Landesbank

2 Pro-forma analytical breakdown over all IFRS segments 3 Fee income + interest income

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2016 2015 2014 2013

Retail customers

Real Estate Finance

Corporate & Structured Finance

Public Finance

HYPO NOE Group – Total Assets1

29%

16%

29%

26% Public Finance

Corporate & Structured Finance

Real Estate Finance

Retail customers

HYPO NOE Group – Total Revenues2

I. Group Business Strategy Real Estate Finance and Promoted Housing1

13

Business position

Universal banking services for 70,000 customers

Branches in Lower Austria and Vienna

Strategic focus on finance & housing, saving & investment and

accounts & cards

Specialized services for professionals like doctors, pharmacists or

lawyers

Recent developments

Increases of retail deposits

Customer-focused efforts led to significant cut in the number of foreign

currency loans

Improved reachability via service centers

Roll out of user friendly homepage including new mobile services

Strategy

Focus on growth of the customer base and retail deposits

Efforts in the area of digitalisation will be further enhanced and

developed

1 Pro-forma analytical breakdown over all IFRS segments 2 Fee income + interest income

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2016 2015 2014 2013

Retail customers

Real Estate Finance

Corporate & Structured Finance

Public Finance

HYPO NOE Group – Total Assets1

29%

16% 29%

26% Public Finance

Corporate & Structured Finance

Real Estate Finance

Retail customers

HYPO NOE Group – Total Revenues2

I. Group Business Strategy Retail Customers and Professionals

14

Public Finance will remain core business

Reduction and diversification of the Public Finance portfolio actively promoted in coming years

Continued focus on real estate and infrastructure financing

in Lower Austria, Vienna and on a selective basis in the neighbouring Danube Region

Business in fee and commission based services is intended to be strengthened

in particular in the light of low interest rate environment

Diversification of available funding instruments

Customer deposits intended to remain a sustainable source of refinancing

Efforts in the area of digitalisation will be further enhanced and developed

Proposed merger with 100 % subsidiary HYPO NOE Landesbank AG

scheduled for completion in autumn 2017

II. Business Outlook for 2017

15

Key Facts (in EUR '000s) 2016 2015 2014 2013 2012

Total assets 15,392,051 15,895,645 15,926,960 14,209,746 14,861,697

Loans and advances to customers 10,854,932 11,557,287 11,194,066 10,590,574 10,735,077

Deposits from customers1 3,847,855 3,260,856 2,305,056 2,149,698 2,717,286

Financial assets 1,987,488 2,108,456 2,249,653 1,805,667 1,840,271

Net interest income 124,439 130,840 129,9092 122,0522 131,6852

Net fee and commission income 13,458 13,850 13,979 13,294 11,985

Profit (+)/ Loss (-) before tax 93,430 11,659 -39,810 75,021 30,226

Profit (+)/ Loss (-) after tax 69,998 6,404 -30,988 53,695 22,808

Notes on major one-off effects:

2016: Significant non-recurring income from the sale of Carinthian Compensation

Payment Fund (KAF) zero-coupon bonds received under the swap for HETA

securities incl. unwinding: EUR 59.5 mn

2014-2015: Cumulated write-down (HETA): EUR 87.1 mn including impairment hedge

adjustment (35.85 % of face value EUR 225 mn)

2013: Reimbursement of penalty interests by FMA from 2010

based on Austrian Banking Act (EUR 58 mn)

Key Ratios (%) 2016 2015

Return on equity before tax 15.2 % 2.0 %

Return on equity before tax (operating)3 18.5 % 5.6 %

Cost income ratio 56.0 % 92.5 %

Cost income ratio (operating)4 46.3 % 77.3 %

Core Capital Ratio (CRR) 16.34 % 13.45 %

Equity Ratio (total, CRR) 17.10 % 15.16 %

Levies in respect of public authorities

Financial stability contribution (“bank tax”)

2016: EUR 14.9 mn (2015: EUR 14.7 mn)

Deposit insurance contribution and resolution fund

2016: EUR 8.1 mn

First-time endowment in 2015: EUR 6.6 mn

1 Including promissory notes placed with customers (2016: 521 EUR mn)

2 Adjusted net gains & losses on investments accounted for using the equity method disclosed in a separate line (Appendix:

Consolidated Statement of Comprehensive Income (I))

3 ROE before tax excl. financial stability contribution, contributions to resolution and deposit insurance funds, and regulatory costs/ave.

equity adjusted for financial stability contribution, contributions to resolution and deposit insurance funds, and regulatory costs

4 Cost/income ratio excl. financial stability contribution, contributions to resolution and deposit insurance funds, and regulatory costs

III. Financial Figures Key Facts and Ratios

16

Capitalisation

LCR > 100 %

Leverage ratio 4.48 %1

NSFR (indicative) 103 %

Equity Ratios phased-in vs. fully-loaded (CRR/CRD IV)

Difference between phased-in and fully loaded CET Ratios

predominantly due to 100% eligibility of AfS-reserve

Regulatory required core and total capital ratio of 4.5 % and

8.0 % again considerably exceeded

13.45% 14.05%

III. Financial Figures Solid Capitalisation

Basel III (CRR/CRD IV) Basel II (BWG)

17.10%

16.34%

phased-in

Capital base (EUR '000s) 2016 2015

Total eligible core capital 632,730 597,675

Capital requirement (CRR/CRD IV) 295,994 315,497

Surplus capital 336,736 282,178

1 with consideration of the approval by FMA (without consideration of IC transactions)

17.53%

16.78%

fully-loaded

Equity ratio (total)

Tier 1 capital ratio

17

90%

10 % <1%

EUR CHF GBP

Volume (in EUR '000s) 2016 NPL

Public sector customers 5,150,341 0.15 %

Business customers 1,778,604 8.19 %

Housing associations 1,540,216 0.02 %

Retail customers 2,325,131 2.30 %

Professionals 60,640 4.90 %

Total 10,854,932 1.94 %

III. Financial Figures Loan Portfolio and Risk Provisions

Industries

Leasing / Insurance companies 70 %

Retail 18 %

Corporates 12 %

States / Municipalities <1 %

Internal rating

1A-2E 78 %

3A-4E 20 %

5A-5E 2 %

Details on CHF loan portfolio

Breakdown of loans and advances to customers

89%

7% 4% <1%

Austria EU & CH

Germany Others

Waterfall of risk provisions in 2016

Breakdown by country Breakdown by currency

in E

UR

'0

00s

18

By Sectors

Banks 712,260,000

Sovereigns 796,105,010

International Organisations 55,000,000

Corporates 12,185,342

Sub-sovereigns and municipalities 83,000,000

Supranational banks 19,000,000

Insurance companies 4,000,000

Total 1,681,550,352

1 Based on nominal values (31.12.2016)

Regional Distribution

TOP 5 sovereign exposures in Austria, France, Poland, UK and

Belgium: approx. 60 %

100 % EUR denominated

Rest of portfolio well diversified within 21 countries

Average portfolio rating 'A1'

By Rating

52%

26%

21%

1% < 1%

Aaa - Aa2

A1 - A3

Baa1 - Baa3

Ba1

B1

43%

47%

3% 1%

5% 1% < 1% Banks

Sovereigns

International Organisations

Corporates

Sub-sovereigns and municipalities

Supranational banks

Insurance companies

III. Financial Figures Securities Portfolio1

19

IV. Funding Diversified Funding Base

Money Markets and Debt Capital Markets Funding

(as of December 2016, in EUR '000s)

Covered bonds 4,268,363 31 %

Senior unsecured bonds 3,430,202 25 %

Subordinated debt 202,647 1 %

Deposits from customers1 3,847,855 28 %

Deposits from banks 1,462,298 11 %

Promissory notes placed with banks 546,047 4 %

Repo / GC-Pooling 0 0 %

Total 13,757,412 100 %

1 including promissory notes placed with customers of EUR 521,249

Funding Strategy

Regular use of all available funding instruments

Solid track record as top tier Pfandbrief issuer

Frequent issuer of senior unsecured debt and promissory

notes

“tailor-made” private placements for institutional clients

HYPO NOE Landesbank generates retail deposits

through their branch network in Lower Austria and

Vienna

Highlights 2016

CHF 100 mn, senior unsecured benchmark

EUR 100 mn public sector covered bond private placement

Significant increase in customer deposits (+ ~ EUR 590 mn year-on-year)

Increased repurchase of own issues with final maturity 2017

Outlook 2017

Planned funding volume of around EUR 1,150 mn

Focus on public sector covered bond benchmark – EUR 500 mn public sector covered bond benchmark very successfully issued

on March 28, 2017 (first soft-bullet repayment structure in Austria)

Complementing senior unsecured funding

Continuous geographical expansion of investor base

20

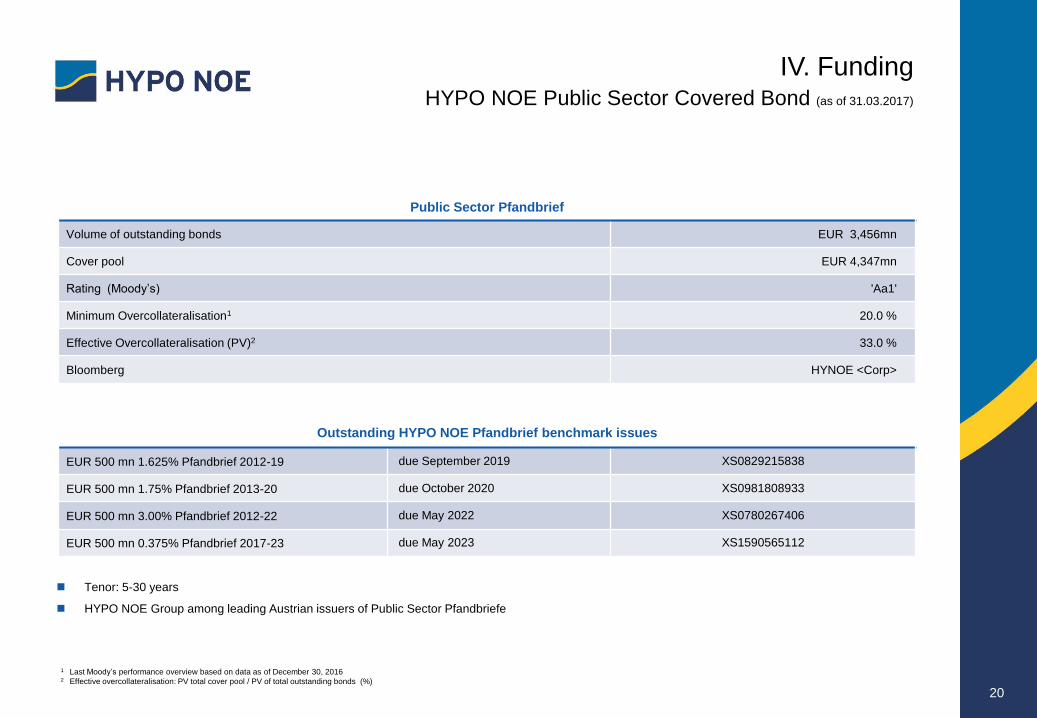

Public Sector Pfandbrief

Volume of outstanding bonds EUR 3,456mn

Cover pool EUR 4,347mn

Rating (Moody’s) 'Aa1'

Minimum Overcollateralisation1 20.0 %

Effective Overcollateralisation (PV)2 33.0 %

Bloomberg HYNOE <Corp>

Outstanding HYPO NOE Pfandbrief benchmark issues

EUR 500 mn 1.625% Pfandbrief 2012-19 due September 2019 XS0829215838

EUR 500 mn 1.75% Pfandbrief 2013-20 due October 2020 XS0981808933

EUR 500 mn 3.00% Pfandbrief 2012-22 due May 2022 XS0780267406

EUR 500 mn 0.375% Pfandbrief 2017-23 due May 2023 XS1590565112

Tenor: 5-30 years

HYPO NOE Group among leading Austrian issuers of Public Sector Pfandbriefe

1 Last Moody’s performance overview based on data as of December 30, 2016

2 Effective overcollateralisation: PV total cover pool / PV of total outstanding bonds (%)

IV. Funding HYPO NOE Public Sector Covered Bond (as of 31.03.2017)

21

Loans vs. Bonds (in EUR mn)

Loans 4,210 96.9 %

Bonds 137 3.1%

Total 4,347 100.0 %

Cover Pool by Geography (in EUR mn)

Austria 4,294 98.8 %

Slovakia 20 0.5 %

Poland 20 0.5 %

Czech Republic 13 0.2 %

Total 4,347 100 %

Average Size Cover Asset

EUR 9.5mn per debtor

EUR 3.4mn per loan

Types of Debtors and Guarantors (in EUR mn)

Guaranteed by federal states 2,118 49 %

Federal states 1,553 36 %

Municipalities 315 7 %

Guaranteed by municipalities 216 5 %

States 92 2 %

Guaranteed by states 53 1 %

Total 4,347 100 %

by Rating (in EUR mn)

Aaa 3,630 83.5 %

Aa 511 11.8 %

A 157 3.6 %

< A 49 1.1 %

Gesamt 4,347 100.0 %

IV. Funding HYPO NOE Public Sector Covered Bond (as of 31.03.2017)

49%

36%

7%

5% 2% 1%

Guaranteed by Federal States

Federal States

Municipalities

Guaranteed by Municipalities

States

Guaranteed by States

22

Research centre for cancer treatment

Client: EBG MedAustron

Facility: EIB-Loan

Amount: 100 mn Euro

Role: Arranger

Location: Wiener Neustadt, Lower Austria

Boat Terminal & World Heritage Centre

Client: Kremser Immobiliengesellschaft (KIG)

Facility: Loan

Amount: 2 mn Euro

Role: Lender & Project Manager

Location: Krems-Stein, Lower Austria

Copyright: Welterbezentrum

IV. Funding Examples: Classic and Social Infrastructure

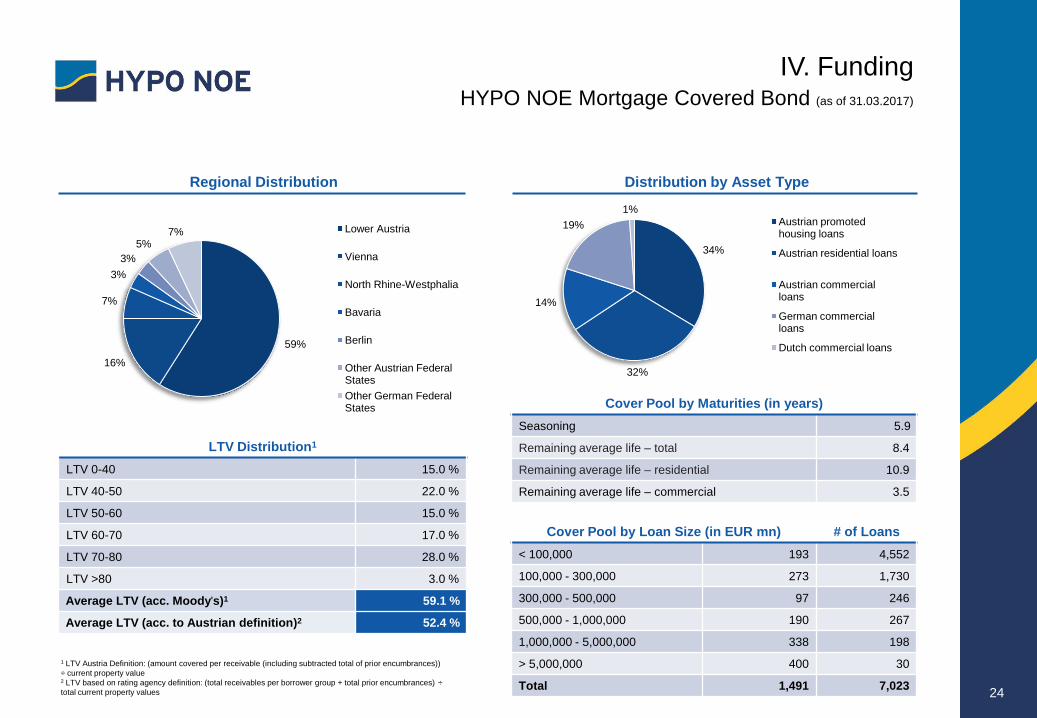

Mortgage Covered Bonds

Volume of outstanding bonds EUR 885 mn

Cover pool EUR 1,491 mn

Rating (Moody’s) 'Aa1'

Minimum Overcollateralisation1 12.0 %

Effective Overcollateralisation2 68.0 %

Bloomberg HYNOE <Corp>

Outstanding HYPO NOE Pfandbrief benchmark issues

EUR 500 mn 0.75% Pfandbrief 2014-21 due September 2021 XS1112184715

EUR 300 mn 0.50% Pfandbrief 2015-20 due November 2020 XS1290200325

Cover Pool by Currencies (in EUR mn)

EUR 1,439 96.5 %

CHF 50 3.4%

JPY und USD 1 > 1.0 %

Gesamt 1,491 100.0 %

Cover Pool by Countries (in EUR mn)

Austria 1,191 79.9 %

Germany 283 19.0 %

Netherlands 17 1.1 %

Gesamt 1,491 100.0 %

1 Last Moody’s performance overview based on data as of December 30, 2016

2 Effective overcollateralisation: nominal value total cover pool / volume of bonds outstanding (%)

IV. Funding HYPO NOE Mortgage Covered Bond (as of 31.03.2017)

23

24

Distribution by Asset Type Regional Distribution

Cover Pool by Maturities (in years)

Seasoning 5.9

Remaining average life – total 8.4

Remaining average life – residential 10.9

Remaining average life – commercial 3.5

Cover Pool by Loan Size (in EUR mn) # of Loans

< 100,000 193 4,552

100,000 - 300,000 273 1,730

300,000 - 500,000 97 246

500,000 - 1,000,000 190 267

1,000,000 - 5,000,000 338 198

> 5,000,000 400 30

Total 1,491 7,023

LTV Distribution1

LTV 0-40 15.0 %

LTV 40-50 22.0 %

LTV 50-60 15.0 %

LTV 60-70 17.0 %

LTV 70-80 28.0 %

LTV >80 3.0 %

Average LTV (acc. Moody's)1 59.1 %

Average LTV (acc. to Austrian definition)2 52.4 %

IV. Funding HYPO NOE Mortgage Covered Bond (as of 31.03.2017)

59%

16%

7%

3%

3%

5% 7% Lower Austria

Vienna

North Rhine-Westphalia

Bavaria

Berlin

Other Austrian Federal States

Other German Federal States

1 LTV Austria Definition: (amount covered per receivable (including subtracted total of prior encumbrances))

÷ current property value 2 LTV based on rating agency definition: (total receivables per borrower group + total prior encumbrances) ÷

total current property values

34%

32%

14%

19%

1% Austrian promoted housing loans

Austrian residential loans

Austrian commercial loans

German commercial loans

Dutch commercial loans

25

Werderscher Markt

Client: Quartier am Auswärtigen Amt

Amount: 37 mn Euro

Size: 19,470 m²

Tenants: Arcotel (53%), Office + Retail (37%),

Residential (8%)

Location: Berlin, Germany

Promoted Housing in Lower Austria

Client: Siedlungsgenossenschaft Neunkirchen

Amount: 5.75 mn Euro

Size: 4,033 m²

Location: Neunkirchen, Lower Austria

Winner of the Lower Austrian Housing award 2011

IV. Funding Examples: Commercial and Promoted Housing

26

Treasury & ALM Investor Relations / Financial Institutions

Thomas Fendrich

Head of Group Treasury & ALM

+43 (0) 590 910 1233

Polina Christova

Head of Group Financial Institutions

& Business Support

+43 (0) 590 910 1225

Markus Payrits

Head of Liquidity Management

+43 (0) 590 910 1222

Martin Leppin

Head of Financial Institutions & Sovereigns

+43 (0) 590 910 1054

Peter Olsacher

Treasury Solutions Team

+43 (0) 590 910 1597

Agnieszka Feiler

Investor Relations Manager

+43 (0) 590 910 1489

Harald Klimt

Treasury Solutions Team

+43 (0) 590 910 1581

V. Contacts

27

Appendix

28

in EUR '000s 12/2016 12/2015 2015/2016

Δ absolut

Cash and balances at central banks 164,587 68,986 95,601

Loans and advances to banks 998,347 922,091 76,256

Loans and advances to customers 10,854,932 11,557,287 -702,355

Risk provisions -97,462 -100,423 2,961

Assets held for trading 555,293 586,811 -31,518

Positive fair value of hedges (hedge accounting) 483,215 509,458 -26,243

Available-for-sale financial assets 1,967,148 2,104,338 -137,190

Financial assets designated as at fair value through profit or loss 20,340 4,118 16,222

Investments accounted for using the equity method 29,922 20,937 8,985

Investment property 54,117 68,704 -14,587

Intangible assets 918 1,411 -493

Property, plant and equipment 77,525 80,159 -2,634

Current tax assets 20,333 19,653 680

Deferred tax assets 1,443 2,105 -662

Other assets 261,393 50,010 211,383

Total assets 15,392,051 15,895,645 -503,594

Appendix HYPO NOE Group Balance Sheet – Assets (consolidated)

29

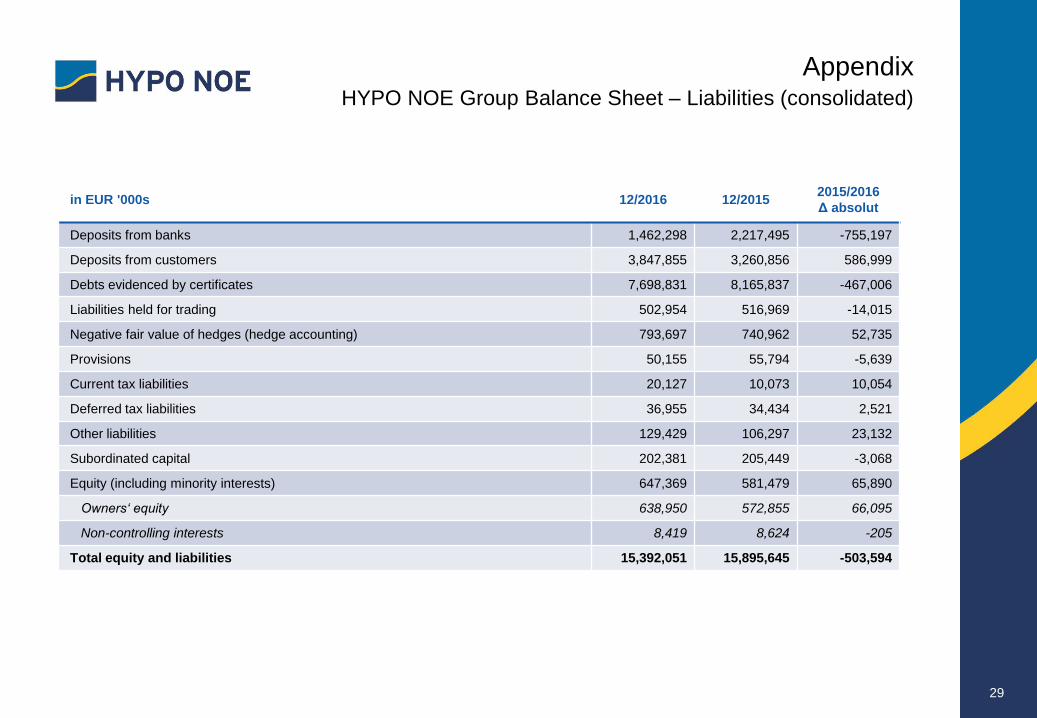

in EUR '000s 12/2016 12/2015 2015/2016

Δ absolut

Deposits from banks 1,462,298 2,217,495 -755,197

Deposits from customers 3,847,855 3,260,856 586,999

Debts evidenced by certificates 7,698,831 8,165,837 -467,006

Liabilities held for trading 502,954 516,969 -14,015

Negative fair value of hedges (hedge accounting) 793,697 740,962 52,735

Provisions 50,155 55,794 -5,639

Current tax liabilities 20,127 10,073 10,054

Deferred tax liabilities 36,955 34,434 2,521

Other liabilities 129,429 106,297 23,132

Subordinated capital 202,381 205,449 -3,068

Equity (including minority interests) 647,369 581,479 65,890

Owners‘ equity 638,950 572,855 66,095

Non-controlling interests 8,419 8,624 -205

Total equity and liabilities 15,392,051 15,895,645 -503,594

Appendix HYPO NOE Group Balance Sheet – Liabilities (consolidated)

30

in EUR '000s 12/2016 12/2015 2015/2016

Δ absolut

Interest and similar income 565,645 583,757 -18,112

Interest and similar expense -441,206 -452,917 11,711

Net interest income 124,439 130,840 -6,401

Credit provisions -7,789 1,171 -8,960

Net interest income after risk provisions 116,650 132,011 -15,361

Fee and commission income 16,534 16,638 -104

Fee and commission expense -3,076 -2,788 -288

Net fee and commission income 13,458 13,850 -392

Net trading income 665 3,242 -2,577

General administrative expenses -128,937 -129,111 174

Net other operating expenses 31,787 25,000 6,787

Results from deconsolidation 8,384 0 8,384

Income from investments accounted for using the equity method -4,813 -4,744 -69

Net gains or losses on available-for-sale financial assets 56,989 -27,825 84,814

Net gains or losses on financial assets designated as at fair value through profit or loss 249 -126 375

Net gains or losses on hedges -1,224 -1,887 663

Net gains or losses on other financial investments 222 1,249 -1,027

Profit (+)/ Loss (-) before tax 93,430 11,659 81,771

Income tax expense -23,432 -5,255 -18,177

Profit (+)/ Loss (-) after tax 69,998 6,404 63,594

Non-controlling interests -178 -252 74

Profit (+)/ Loss (-) for the year 69,820 6,152 63,668

Appendix Consolidated Statement of Comprehensive Income (I)

31

Other comprehensive income (in EUR '000s) 12/2016 12/2015 2015/2016

Δ absolut

Profit (+)/ Loss (-) for the year 69,820 6,152 63,668

Items not to be reclassified to profit or loss

Change in actuarial gains or losses (before tax) -1,455 824 -631

Other changes (before tax) 1 0 1

Change in deferred tax 364 -206 158

Items to be reclassified to profit or loss

Change in available-for-sale financial instruments (before tax) 1,407 4,987 -3,580

Exchange differences on translating foreign operations accounted for using the equity

method (before tax) 23 -13 10

Change in deferred tax -358 -1,243 885

Total other comprehensive income -18 4,348 -4,366

Total comprehensive income attributable to owners of the parent 69,802 10,500 59,302

Appendix Consolidated Statement of Comprehensive Income (II)

32

1.1.-31.12.2016 (in EUR '000s) Gruppe

Bank

Landes-

bank Leasing Other

Consoli-

dation Total 2016

Interest and similar income 89,268 39,307 4,815 -678 -8,274 124,439

Credit provisions -11,128 3,376 0 -37 0 -7,789

Net interest income after risk provisions 78,140 42,683 4,815 -715 -8,274 116,650

Net fee and commission income/expense 680 12,832 -14 -39 -1 13,458

Net trading expense 737 -72 0 0 0 665

Administrative expenses -72,688 -47,987 -4,327 -20,460 16,525 -128,937

Net other operating expense/income 21,620 4,931 3,341 16,736 -14,841 31,787

Net gains or losses on other financial investments 49,436 7,841 36 -21 -53 57,238

Net gains or losses on hedges -1,109 -115 0 0 0 -1,224

Net gains or losses on other financial assets 117 0 51 1,691 -1,637 222

Result from deconsolidation 0 0 0 8,384 0 8,384

Net gains or losses on investments accounted for using the equity method -5,063 0 -57 307 0 -4,813

Profit (+) / Loss (-) before tax 71,870 20,113 3,845 5,883 -8,280 93,430

Income tax -23,432

Profit for the year 69,998

Appendix Breakdown of Earnings Power by Segments

Highlights

Highest net interest income by segment Gruppe Bank

Highest profit before tax by segment Gruppe Bank

Significant positive profit contributions by all segments,

despite high statutory contributions

‘HETA solution’ achieved in 2016

October 2016: 98.71 % of HETA creditors accepted repurchase offer of

Carinthian Compensation Fund (KAF)

Creditors had the choice between a cash payment totalling around EUR

7.8bn or zero-coupon notes with a total nominal value of EUR 10.4bn

HYPO NOE Group accepted the exchange for a zero-coupon

bond with an abstract, explicit, unconditional and irrevocable

guarantee by the Federal Republic of Austria upon first demand

33

Pfandbriefe Fundierte

Bankschuldverschreibungen

Hypothekenbankgesetz

(Mortgage Banking Act 1899)

Pfandbriefgesetz

(Pfandbrief Act 1927)

Gesetz betreffend Fundierte

Bankschuldverschreibungen

(Covered Bond Act 1905)

Erste Group Bank Bank Austria

Österreichische Landes-Hypothekenbanken

HYPO NOE Gruppe

BAWAG P.S.K Kommunalkredit Raiffeisenbanken

VOLKSBANK WIEN

Appendix Austrian Legal Framework for Covered Bonds

34

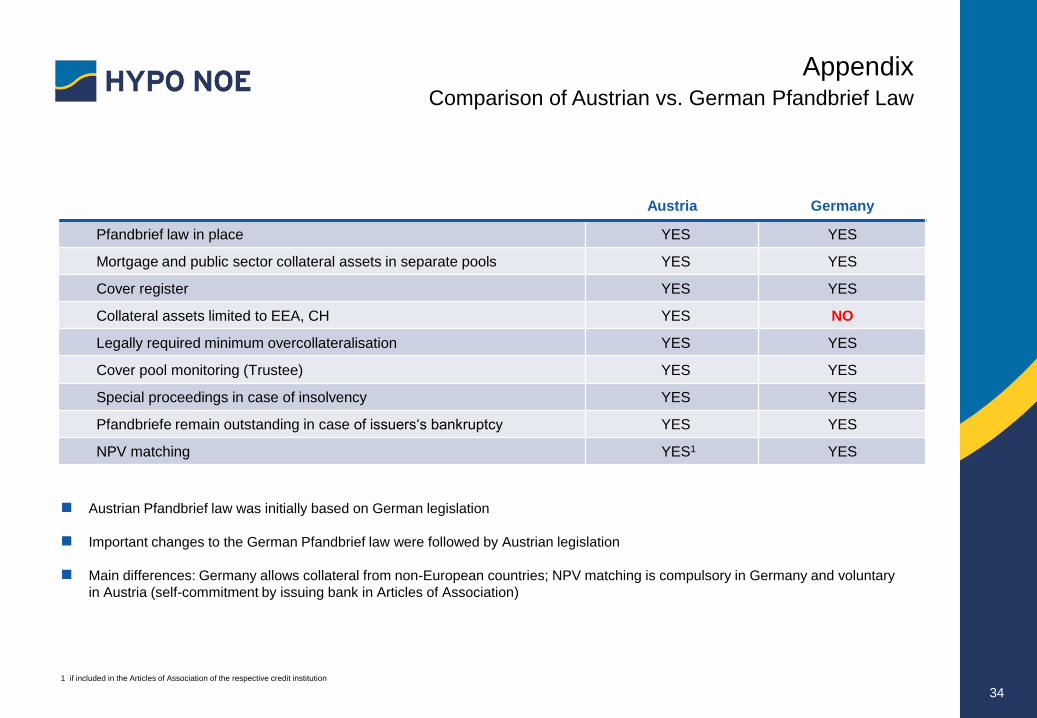

Austria Germany

Pfandbrief law in place YES YES

Mortgage and public sector collateral assets in separate pools YES YES

Cover register YES YES

Collateral assets limited to EEA, CH YES NO

Legally required minimum overcollateralisation YES YES

Cover pool monitoring (Trustee) YES YES

Special proceedings in case of insolvency YES YES

Pfandbriefe remain outstanding in case of issuers‘s bankruptcy YES YES

NPV matching YES1 YES

Austrian Pfandbrief law was initially based on German legislation

Important changes to the German Pfandbrief law were followed by Austrian legislation

Main differences: Germany allows collateral from non-European countries; NPV matching is compulsory in Germany and voluntary

in Austria (self-commitment by issuing bank in Articles of Association)

1 if included in the Articles of Association of the respective credit institution

Appendix Comparison of Austrian vs. German Pfandbrief Law

35

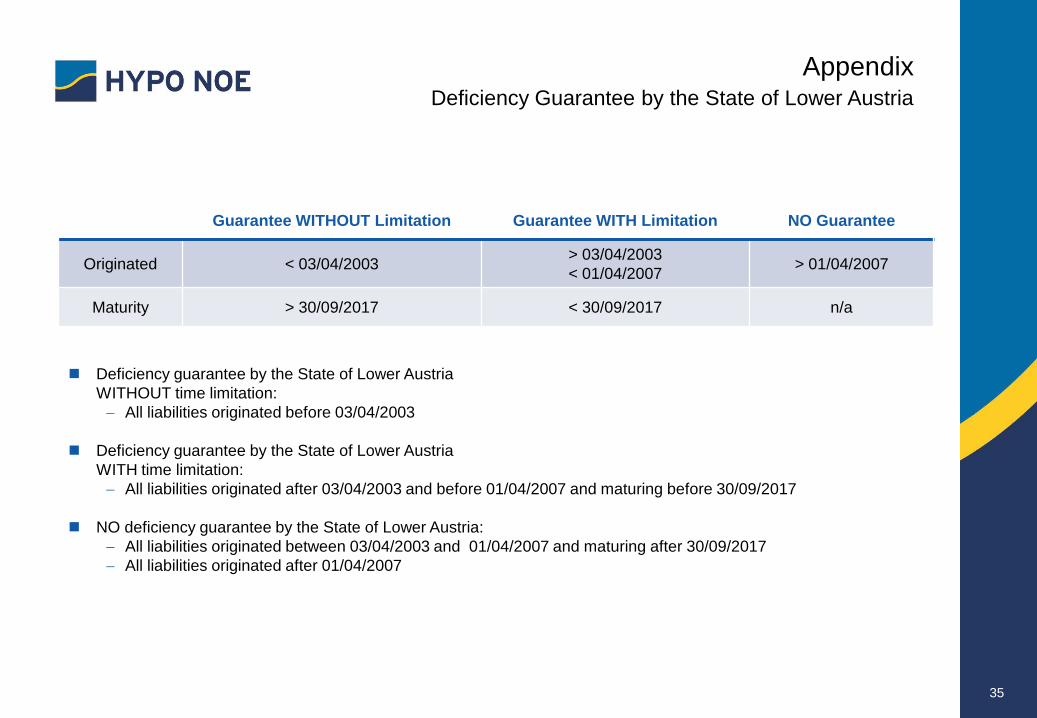

Deficiency guarantee by the State of Lower Austria

WITHOUT time limitation:

All liabilities originated before 03/04/2003

Deficiency guarantee by the State of Lower Austria

WITH time limitation:

All liabilities originated after 03/04/2003 and before 01/04/2007 and maturing before 30/09/2017

NO deficiency guarantee by the State of Lower Austria:

All liabilities originated between 03/04/2003 and 01/04/2007 and maturing after 30/09/2017

All liabilities originated after 01/04/2007

Guarantee WITHOUT Limitation Guarantee WITH Limitation NO Guarantee

Originated < 03/04/2003 > 03/04/2003

< 01/04/2007 > 01/04/2007

Maturity > 30/09/2017 < 30/09/2017 n/a

Appendix Deficiency Guarantee by the State of Lower Austria

36

HETA moratorium directly

Moratorium on HETA debt repayments imposed by the Austrian

Financial Market Authority on March 1, 2015

HYPO NOE held EUR 225mn of HETA debt securities on its own

portfolio

Cumulated write-down in 2014-2015 based on model calculations:

EUR 87.1 mn including impairment hedge adjustment

(35.85 % of face value EUR 225 mn)

Significant non-recurring income in 2016 from the sale of Carinthian

Compensation Payment Fund (KAF) zero-coupon bonds received

under the exchange for HETA securities incl. unwinding: EUR 59.5 mn

Pfandbriefbank (Österreich) AG – formerly Pfandbriefstelle

All eight member banks and their guarantors –

Austria’s federal states – bear joint and several liability

All members agreed on providing sufficient liquidity,

i.e. 1/8 each (= 12.5 % or approx. EUR 155mn)

HYPO NOE received explicit backing of the State of Lower Austria for

its part of joint and several liability for “Pfandbriefstelle“ issues,

therefore was no risk provisioning nor regulatory capital required

Appendix HETA moratorium – credit risk dimensions

37

Financial Market Authority (FMA)

The FMA issued a special notice imposing a moratorium on debt repayments by HETA until 31 May 2016.

By decision of 10 April 2016 a haircut was imposed by the FMA .

Tender & exchange offer and buy back offer

Tender offer for repurchase of HETA bonds at an envisaged discounted value (75% of face value) by Carinthian Compensation

Payment Fund (KAF) was denied by the creditors and did not reach a necessary two-third majority in March 2016.

On 18 May 2016, the Republic of Austria and a majority of HETA creditors underwent a MoU to create an out-of-court

settlement. A new tender offer of approx. 90% of the nominal value was expected to be disclosed in autumn 2016, which

required a significantly lower depreciation compared to the FMA haircut mentioned above.

Under the new tender offer which was announced by KAF on 6 September 2016, and which was valid until 7 October, creditors

had a choice between a cash payment totalling around EUR 7.8bn and an or zero-coupon notes with a total nominal value of

EUR 10.4bn.

Following the announcement by KAF on 10 October 2016 that the required two-third acceptance rate for its tender offer for

HETA Asset Resolution AG's debt obligations was comfortably met (acceptance overall was 98.71%, of which 99.55% for

senior debt and 89.42% for subordinated debt).

HYPO NOE Group accepted the exchange for a zero-coupon bond with an abstract, explicit, unconditional and irrevocable

guarantee by the Federal Republic of Austria upon first demand.

In December 2016, the zero-coupon bond was sold back to KAF for net proceeds of EUR 59.5 mn incl. unwinding.

HYPO NOE Group no longer holds any HETA or KAF bonds. Therefore, HYPO NOE Group is no longer subject to any

exposure-related risks with regards to HETA or KAF.

Appendix HETA moratorium – legal implications

38

This document does not constitute an offer to sell, or the solicitation of an offer to subscribe for or buy, any securities, investments or any other financial instruments, in or of HYPO

NOE Gruppe Bank AG, nor shall it or any part of it nor the fact of its distribution form the basis of, or be relied on in connection with, any contract or investment decision. This

document does not constitute an investment analysis or a recommendation to buy or to sell and is not intended to substitute any individual investment advice. Any such offers will

only be made when a prospectus in relation to the Offering is published in due course. This presentation will only be part of an offer, when it is explicitly referenced in the respective

offer.

No reliance may be placed for any purposes whatsoever on the information contained in this document or on its completeness. No representation or warranty, expressed or implied,

is given by or on behalf of HYPO NOE Gruppe Bank AG or the banks represented in this presentation or any of such institutions’ affiliates, directors, officers or employees, advisors

or any other person as to the accuracy or completeness of the information or opinions contained in this document and no liability whatsoever is accepted for any such information or

opinions or any use which may be made of them.

This document is intended for distribution in the United Kingdom only to persons who have professional experience in matters relating to investments falling within Article 19(5) of the

Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended, or to those persons to whom it may otherwise lawfully be distributed. Neither this document

nor any copy of it may be taken or transmitted in or into the United States or to any US person (as defined by Regulation S of the US Securities Act of 1933 (the “Securities Act”)) or

transmitted in or into Australia, Canada or Japan or to Australian, Canadian or Japanese persons. Securities of HYPO NOE Gruppe Bank AG have not been and – as of the date of

this presentation – will not be registered under the Securities Act and may not be offered or sold in the United States absent registration under the Securities Act or exemption from

the registration requirements thereof. There will be no public offer of securities of HYPO NOE Gruppe Bank AG in the United States. The distribution of this document in or into other

jurisdictions may be restricted by law and persons into whose possession this document comes should inform themselves about and observe, any such restrictions. Any failure to

comply with this restriction may constitute a violation of applicable securities law and regulations.

Certain market data and financial and other figures (including percentages) in this document were rounded in accordance with commercial principles. Figures rounded in this manner

may not in any and all cases add up to the stated totals or the statements made in the underlying sources. For the calculation of percentages used in the text, the actual figures,

rather than the commercially rounded figures, were used. Accordingly, in some cases, the percentages provided in the text may deviate from percentages based on rounded figures.

Certain statements in this presentation are forward-looking statements. By their nature, forward-looking statements involve a number of risks, uncertainties and assumptions that

could cause actual results or events to differ materially from those expressed or implied by the forward-looking statements. These risks, uncertainties and assumptions could

adversely affect the outcome and financial effects of the plans and events described herein. HYPO NOE Gruppe Bank AG does not undertake any obligation to update or revise any

forward-looking statements, whether as a result of new information, future events or otherwise. You should not place undue reliance on forward-looking statements, which speak as

only of the date of this presentation. Statements contained in this presentation regarding past trends or activities should not be taken as a representation that such trends or activities

will continue in the future.

Although due care has been taken in compiling this document it cannot be excluded that it is incomplete or contains errors.

HYPO NOE Gruppe Bank AG, its shareholders, advisors and employees are not liable for the accuracy and completeness of the statements, estimations and the conclusions

contained in this document. Possible errors or incompleteness do not constitute any grounds for liability, neither with regard to indirect nor direct damages. For the avoidance of

doubt HYPO NOE Gruppe Bank AG points out that it is not liable for any losses, damages or disadvantages including direct, indirect, financial, immaterial, special or consequential

loss or damage (whether for loss of profit or otherwise) due to this document or any of the statements contained therein.

By reading / downloading this presentation, you explicitly agree to be bound by the above.

NOT FOR DISTRIBUTION IN THE UNITED STATES OF AMERICA, AUSTRALIA, CANADA AND JAPAN.

DISCLAIMER

Recommended