Results presentation for the

half year ended

27 June 2015

Half Year Results 2015

Kevin Lyons-Tarr CEO

David Seekings CFO

1. Background

2. Highlights

3. Financial review

4. Operational review

5. Outlook

2

• 4imprint is the leading direct marketer of promotional products in the USA,

Canada, the UK and Ireland

• 96% of revenue is generated in the USA and Canada from its headquarters

in Wisconsin, USA

• UK and Irish customers are served out of its base in Manchester, England.

• 4imprint’s strategy is to maximise organic revenue growth at broadly stable

operating margin percentage

• Group results now reported in US dollars; prior period comparatives restated

accordingly

Background

3

Highlights

4

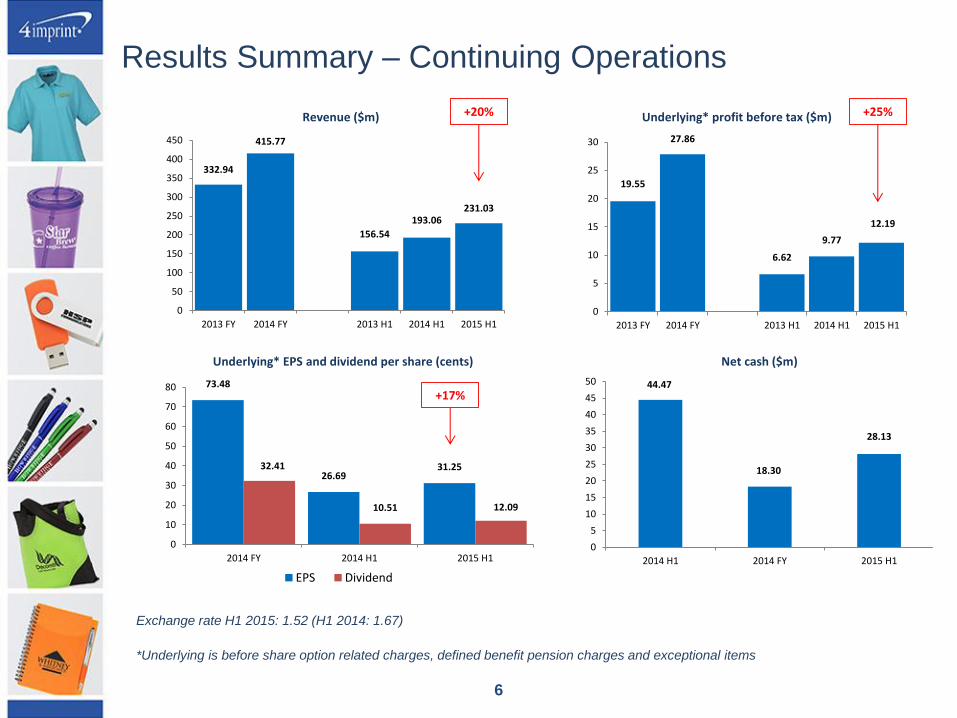

• Group revenue† up 20% to $231.03m

• Underlying* profit before tax † up 25% to $12.19m

• Underlying* basic EPS † up 17% to 31.25c

• Interim dividend 12.09c up 15%; 7.75p up 25%

• Net cash $28.13m

• US infrastructure investment of $9m on target for completion in September

2015

† Continuing operations

* Underlying is before share option related charges, defined benefit pension charges and exceptional items

Highlights

Financial Review

73.48

26.69 31.25 32.41

10.51 12.09

0

10

20

30

40

50

60

70

80

2014 FY 2014 H1 2015 H1

Underlying* EPS and dividend per share (cents)

EPS Dividend

332.94

415.77

156.54

193.06 231.03

0

50

100

150

200

250

300

350

400

450

2013 FY 2014 FY 2013 H1 2014 H1 2015 H1

Revenue ($m)

19.55

27.86

6.62

9.77

12.19

0

5

10

15

20

25

30

2013 FY 2014 FY 2013 H1 2014 H1 2015 H1

Underlying* profit before tax ($m)

6

Results Summary – Continuing Operations

Exchange rate H1 2015: 1.52 (H1 2014: 1.67)

*Underlying is before share option related charges, defined benefit pension charges and exceptional items

+20% +25%

+17% 44.47

18.30

28.13

0

5

10

15

20

25

30

35

40

45

50

2014 H1 2014 FY 2015 H1

Net cash ($m)

7

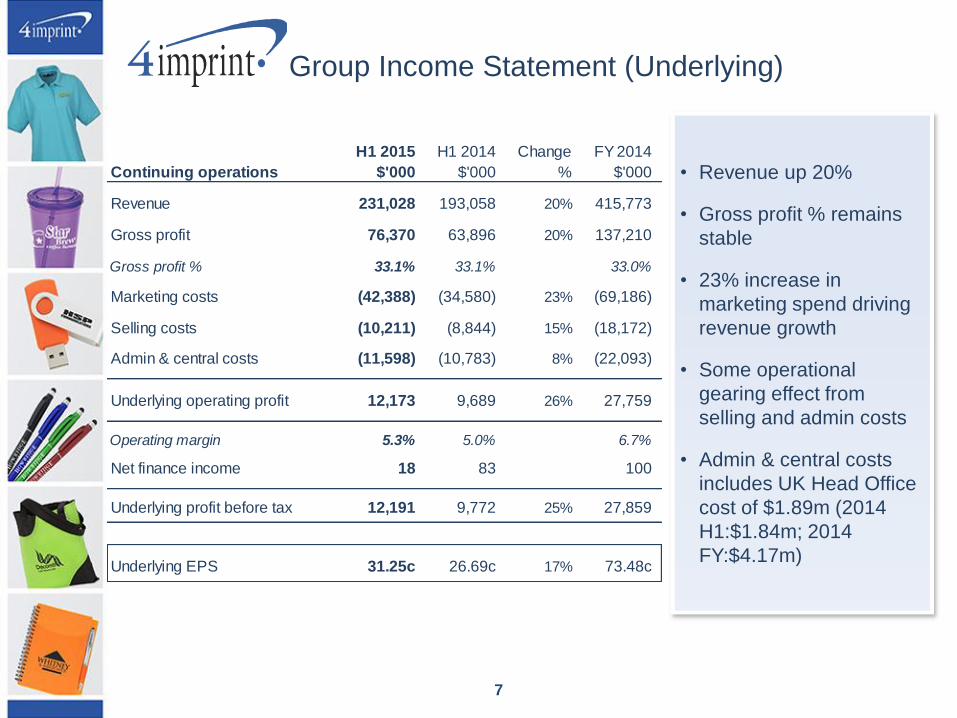

• Revenue up 20%

• Gross profit % remains

stable

• 23% increase in

marketing spend driving

revenue growth

• Some operational

gearing effect from

selling and admin costs

• Admin & central costs

includes UK Head Office

cost of $1.89m (2014

H1:$1.84m; 2014

FY:$4.17m)

Group Income Statement (Underlying)

H1 2015 H1 2014 Change FY 2014

Continuing operations $'000 $'000 % $'000

Revenue 231,028 193,058 20% 415,773

Gross profit 76,370 63,896 20% 137,210

Gross profit % 33.1% 33.1% 33.0%

Marketing costs (42,388) (34,580) 23% (69,186)

Selling costs (10,211) (8,844) 15% (18,172)

Admin & central costs (11,598) (10,783) 8% (22,093)

Underlying operating profit 12,173 9,689 26% 27,759

Operating margin 5.3% 5.0% 6.7%

Net finance income 18 83 100

Underlying profit before tax 12,191 9,772 25% 27,859

Underlying EPS 31.25c 26.69c 17% 73.48c

8

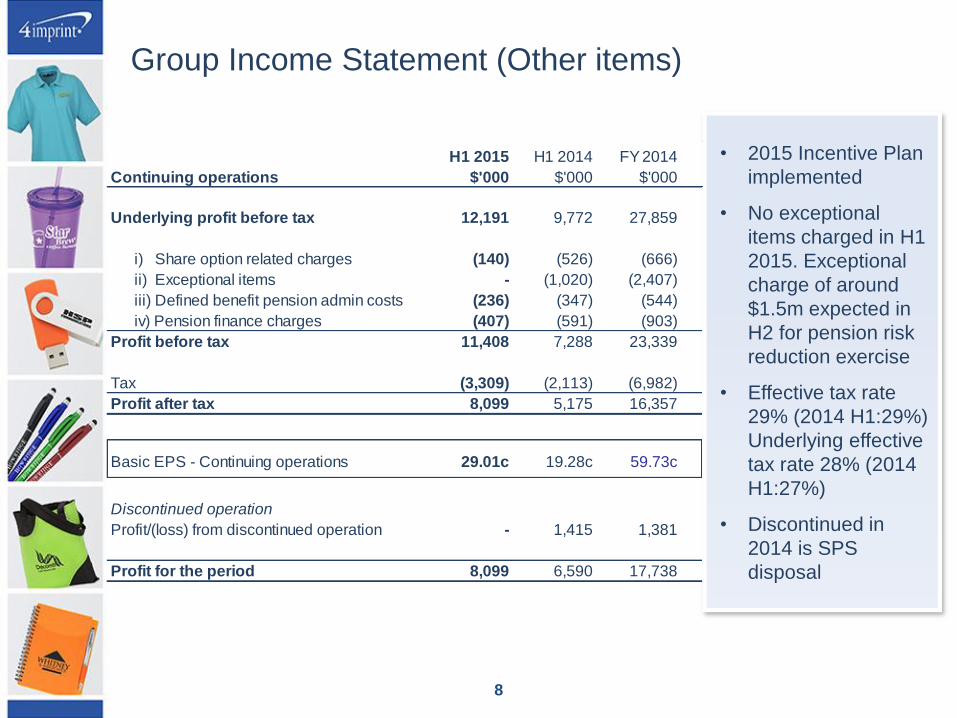

Group Income Statement (Other items)

• 2015 Incentive Plan

implemented

• No exceptional

items charged in H1

2015. Exceptional

charge of around

$1.5m expected in

H2 for pension risk

reduction exercise

• Effective tax rate

29% (2014 H1:29%)

Underlying effective

tax rate 28% (2014

H1:27%)

• Discontinued in

2014 is SPS

disposal

H1 2015 H1 2014 FY 2014

Continuing operations $'000 $'000 $'000

Underlying profit before tax 12,191 9,772 27,859

i) Share option related charges (140) (526) (666)

ii) Exceptional items - (1,020) (2,407)

iii) Defined benefit pension admin costs (236) (347) (544)

iv) Pension finance charges (407) (591) (903)

Profit before tax 11,408 7,288 23,339

Tax (3,309) (2,113) (6,982)

Profit after tax 8,099 5,175 16,357

Basic EPS - Continuing operations 29.01c 19.28c 59.73c

Discontinued operation

Profit/(loss) from discontinued operation - 1,415 1,381

Profit for the period 8,099 6,590 17,738

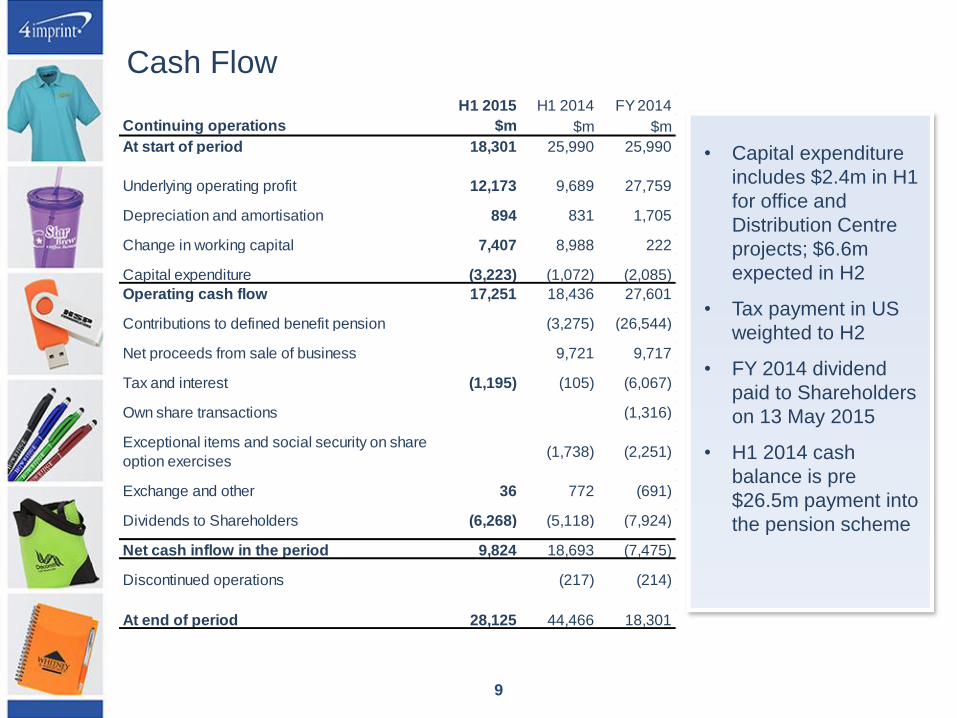

Cash Flow

• Capital expenditure

includes $2.4m in H1

for office and

Distribution Centre

projects; $6.6m

expected in H2

• Tax payment in US

weighted to H2

• FY 2014 dividend

paid to Shareholders

on 13 May 2015

• H1 2014 cash

balance is pre

$26.5m payment into

the pension scheme

9

H1 2015 H1 2014 FY 2014

Continuing operations $m $m $m

At start of period 18,301 25,990 25,990

Underlying operating profit 12,173 9,689 27,759

Depreciation and amortisation 894 831 1,705

Change in working capital 7,407 8,988 222

Capital expenditure (3,223) (1,072) (2,085)

Operating cash flow 17,251 18,436 27,601

Contributions to defined benefit pension (3,275) (26,544)

Net proceeds from sale of business 9,721 9,717

Tax and interest (1,195) (105) (6,067)

Own share transactions (1,316)

Exceptional items and social security on share

option exercises(1,738) (2,251)

Exchange and other 36 772 (691)

Dividends to Shareholders (6,268) (5,118) (7,924)

Net cash inflow in the period 9,824 18,693 (7,475)

Discontinued operations (217) (214)

At end of period 28,125 44,466 18,301

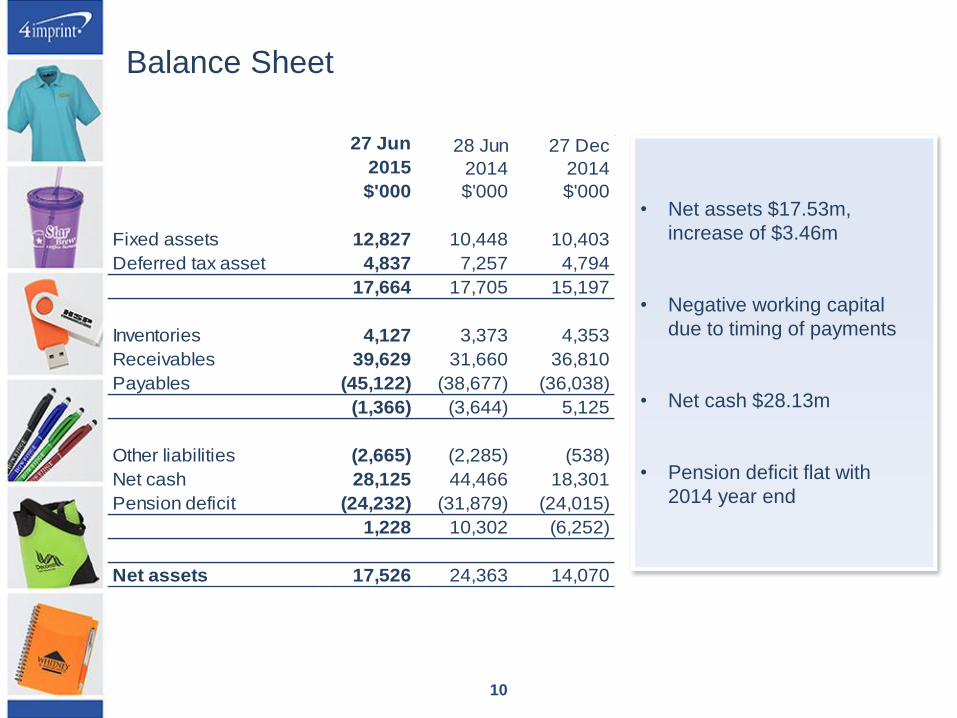

Balance Sheet

• Net assets $17.53m,

increase of $3.46m

• Negative working capital

due to timing of payments

• Net cash $28.13m

• Pension deficit flat with

2014 year end

10

$'000 $'000 $'000

Fixed assets 12,827 10,448 10,403

Deferred tax asset 4,837 7,257 4,794

17,664 17,705 15,197

Inventories 4,127 3,373 4,353

Receivables 39,629 31,660 36,810

Payables (45,122) (38,677) (36,038)

(1,366) (3,644) 5,125

Other liabilities (2,665) (2,285) (538)

Net cash 28,125 44,466 18,301

Pension deficit (24,232) (31,879) (24,015)

1,228 10,302 (6,252)

Net assets 17,526 24,363 14,070

27 Jun

2015

27 Dec

2014

28 Jun

2014

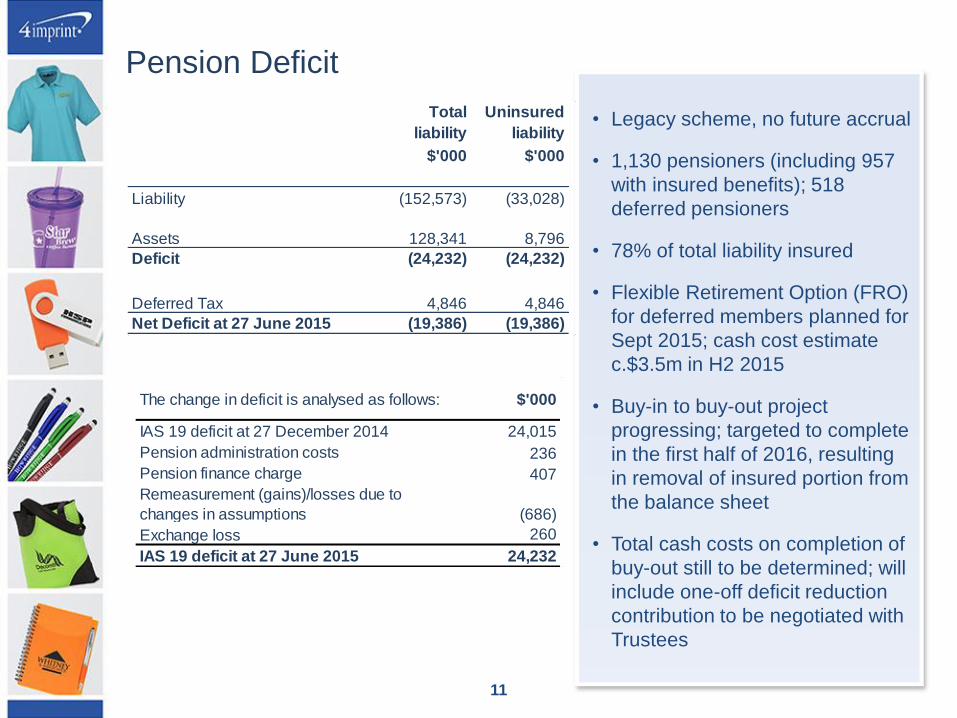

Pension Deficit

• Legacy scheme, no future accrual

• 1,130 pensioners (including 957

with insured benefits); 518

deferred pensioners

• 78% of total liability insured

• Flexible Retirement Option (FRO)

for deferred members planned for

Sept 2015; cash cost estimate

c.$3.5m in H2 2015

• Buy-in to buy-out project

progressing; targeted to complete

in the first half of 2016, resulting

in removal of insured portion from

the balance sheet

• Total cash costs on completion of

buy-out still to be determined; will

include one-off deficit reduction

contribution to be negotiated with

Trustees

11

Total

liability

Uninsured

liability

$'000 $'000

Liability (152,573) (33,028)

Assets 128,341 8,796

Deficit (24,232) (24,232)

Deferred Tax 4,846 4,846

Net Deficit at 27 June 2015 (19,386) (19,386)

The change in deficit is analysed as follows: $'000

IAS 19 deficit at 27 December 2014 24,015

Pension administration costs 236

Pension finance charge 407

Remeasurement (gains)/losses due to

changes in assumptions (686)

Exchange loss 260

IAS 19 deficit at 27 June 2015 24,232

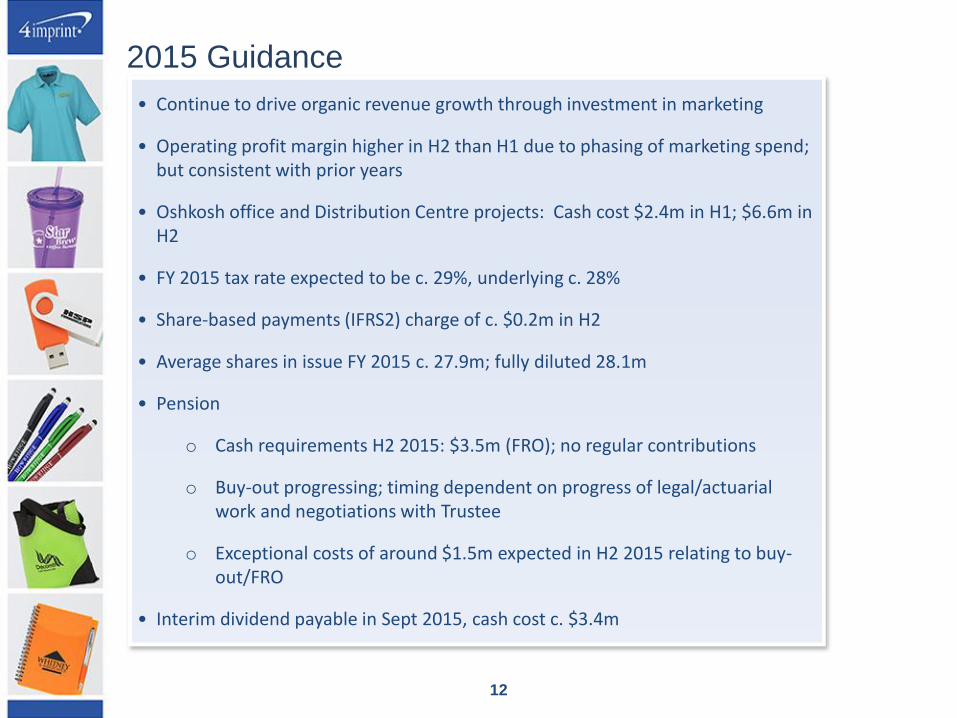

• Continue to drive organic revenue growth through investment in marketing

• Operating profit margin higher in H2 than H1 due to phasing of marketing spend; but consistent with prior years

• Oshkosh office and Distribution Centre projects: Cash cost $2.4m in H1; $6.6m in H2

• FY 2015 tax rate expected to be c. 29%, underlying c. 28%

• Share-based payments (IFRS2) charge of c. $0.2m in H2

• Average shares in issue FY 2015 c. 27.9m; fully diluted 28.1m

• Pension

o Cash requirements H2 2015: $3.5m (FRO); no regular contributions

o Buy-out progressing; timing dependent on progress of legal/actuarial work and negotiations with Trustee

o Exceptional costs of around $1.5m expected in H2 2015 relating to buy-out/FRO

• Interim dividend payable in Sept 2015, cash cost c. $3.4m

2015 Guidance

12

Operational Review

Direct Marketing Strategy

• Continue to deliver market share growth in large, highly fragmented market

• On target to double the business in five years (2011 – 2016) at stable operating profit margin %

• Equivalent to c.15% CAGR in sales

• Consistent with achievement in previous five years (2006 – 2011)

• Organic growth is driven through revenue investment in marketing as well as technology, resource and expertise

• High cash conversion, low fixed and working capital requirements

254.7

290.8

332.9

415.8

23.2 24.4

25.7 27.0

20

25

30

35

40

220240260280300320340360380400420440

2011 2012 2013 2014

Mar

ket

Size

($

bn

)

Re

ven

ue

($

m)

Growth History - 4imprint v Market

4imprint Group Revenue $m US, Canada & UK Market Size $bn

14

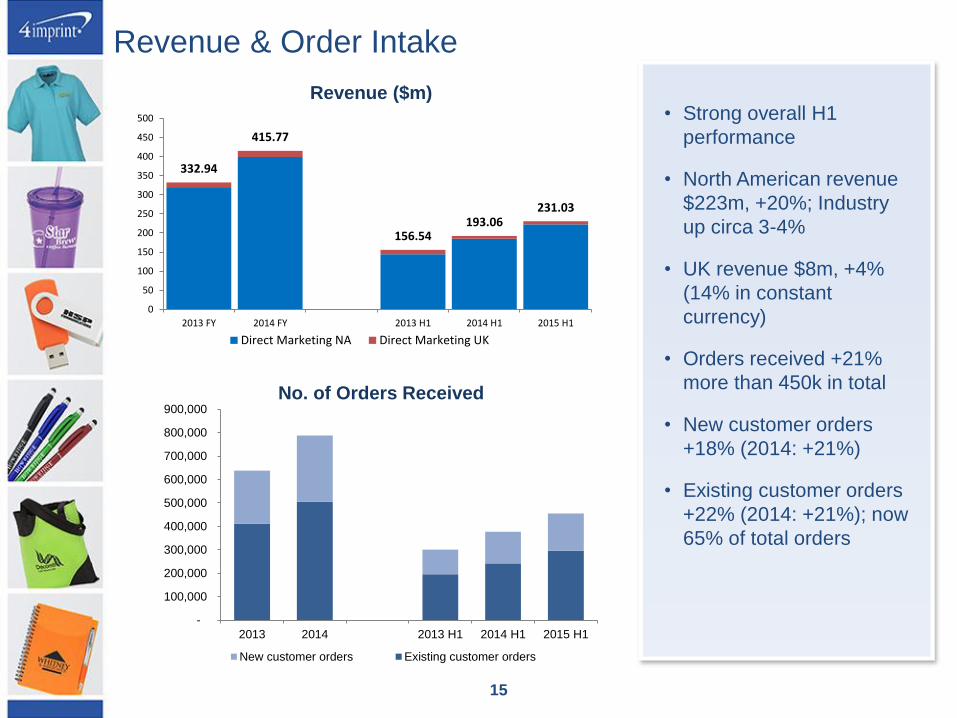

Revenue & Order Intake

• Strong overall H1

performance

• North American revenue

$223m, +20%; Industry

up circa 3-4%

• UK revenue $8m, +4%

(14% in constant

currency)

• Orders received +21%

more than 450k in total

• New customer orders

+18% (2014: +21%)

• Existing customer orders

+22% (2014: +21%); now

65% of total orders

15

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

2013 2014 2013 H1 2014 H1 2015 H1

No. of Orders Received

New customer orders Existing customer orders

332.94

415.77

156.54 193.06

231.03

0

50

100

150

200

250

300

350

400

450

500

2013 FY 2014 FY 2013 H1 2014 H1 2015 H1

Revenue ($m)

Direct Marketing NA Direct Marketing UK

Customers Acquired & Retention Percentage

• Strong new customer

growth - more than

100k customers

acquired

• Consistent customer

retention

• Marketing spend

+23% • Online spend

continues to

increase at faster

rate than offline

• Catalogue

circulation +5%

• Revenue per

marketing dollar

within acceptable

bandwidth

Revenue/Marketing $

16

6.08 6.01

5.62 5.58

5.45

5.10

5.20

5.30

5.40

5.50

5.60

5.70

5.80

5.90

6.00

6.10

6.20

2013 2014 H1 2013 H1 2014 H1 2015

0

10,000

20,000

30,000

40,000

50,000

60,000

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2

2007 2008 2009 2010 2011 2012 2013 2014 2015

Customers Acquired % Retained 12 Months % Retained 24 Months

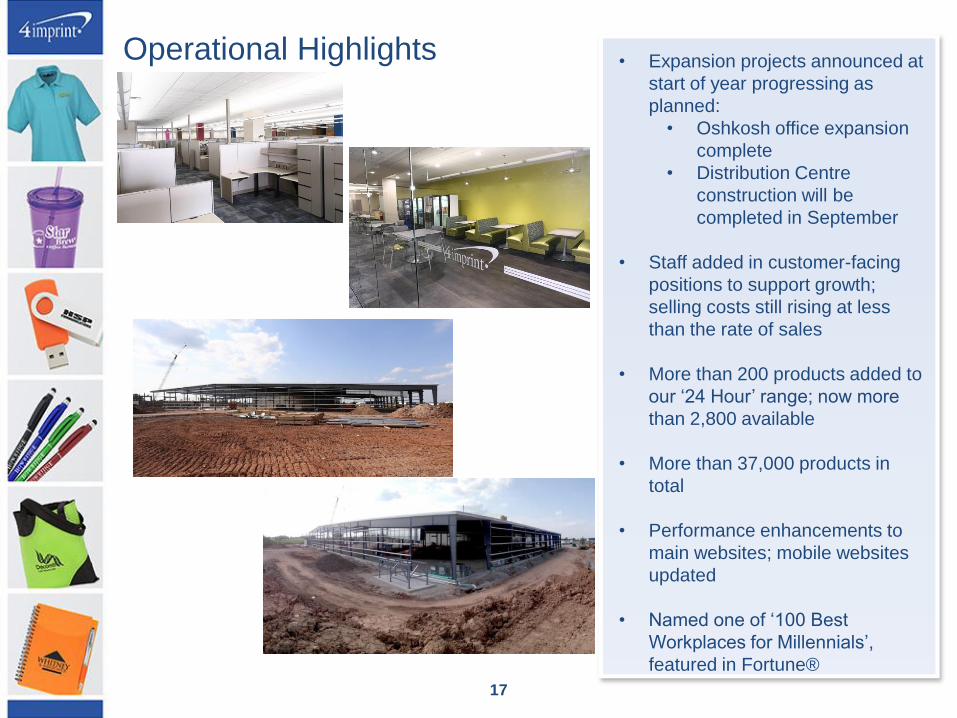

Operational Highlights • Expansion projects announced at

start of year progressing as

planned:

• Oshkosh office expansion

complete

• Distribution Centre

construction will be

completed in September

• Staff added in customer-facing

positions to support growth;

selling costs still rising at less

than the rate of sales

• More than 200 products added to

our ‘24 Hour’ range; now more

than 2,800 available

• More than 37,000 products in

total

• Performance enhancements to

main websites; mobile websites

updated

• Named one of ‘100 Best

Workplaces for Millennials’,

featured in Fortune®

17

Marketing Driving Growth – H2

Catalogue:

• Circulation growth continues at similar

pace with targeted increases driven

by data analytics/insights

Internet:

• Benefit of addition and acceleration of

new techniques in late H1 last year

now in the run rate; shift more to

optimisation than pure expansion

Retention:

• Blue Box® programme increased to

support larger customer file

18

Indications for the balance of the year are for a good

performance in keeping with our strategic growth objectives,

despite the strong growth comparator in the second half of 2014.

The Group expects a good outcome for the year as a whole.

Outlook

19

Appendices

• Sale of custom-printed merchandise, used to promote a brand, service or product

• Purchases by individuals within businesses and organisations of all sizes

• Product customised and shipped to customer directly from suppliers

• Investment in marketing, technology and people drives organic revenue growth

through new customer acquisition and consistent retention rates of customers

acquired:

• Marketing

• Innovative online and offline techniques including catalogues, email,

internet advertising, Blue Box® mailings

• Technology

• Customer-facing (web sites, mobile)

• Order processing technology to rapidly process hundreds of thousands of

customised orders

• Integrated supplier interfaces

• Complex database analytics to target marketing mix

• People

• Focus on the customer experience. Delivery time, satisfaction and service

guarantees

• Data analytics, marketing, merchandising technology expertise

• Favourable cash characteristics - minimal inventory, high proportion of orders paid by

credit card, ongoing capital investment broadly in line with depreciation

4imprint Direct Marketing Model

21

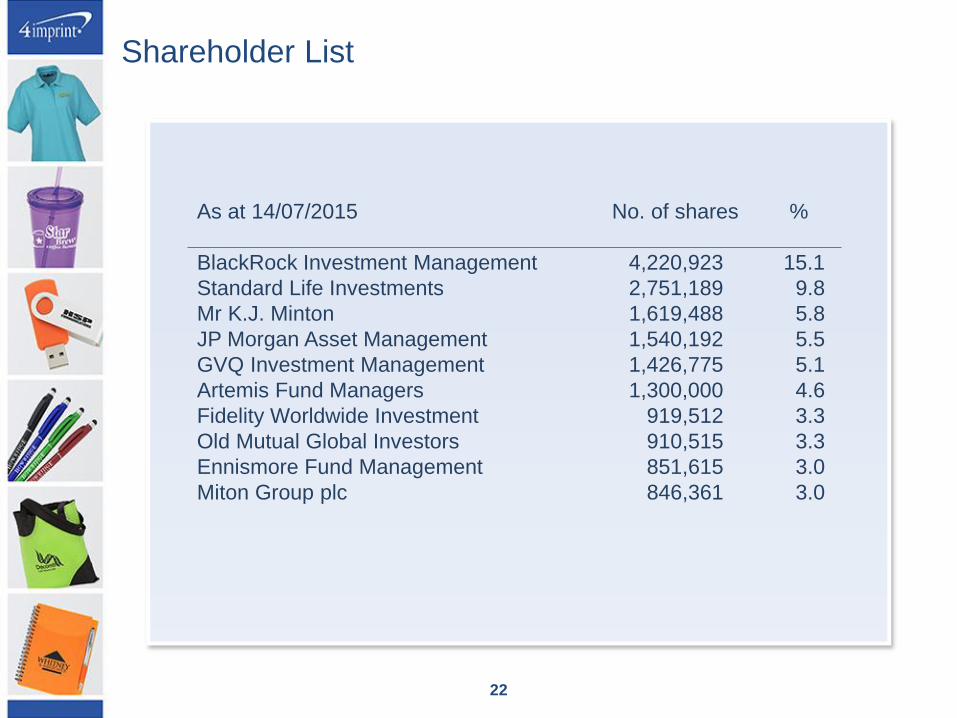

Shareholder List

As at 14/07/2015 No. of shares %

BlackRock Investment Management 4,220,923 15.1

Standard Life Investments 2,751,189 9.8

Mr K.J. Minton 1,619,488 5.8

JP Morgan Asset Management 1,540,192 5.5

GVQ Investment Management 1,426,775 5.1

Artemis Fund Managers 1,300,000 4.6

Fidelity Worldwide Investment 919,512 3.3

Old Mutual Global Investors 910,515 3.3

Ennismore Fund Management 851,615 3.0

Miton Group plc 846,361 3.0

22

Recommended