1

Bonds (Debt)Characteristics and Valuation

What is debt?

What are bond ratings?

How are bond prices determined?

How are bond yields determined?

What is the relationship between bond prices and interest rates?

2

Debt Characteristics

Principal value, face value, maturity value, and par value

Interest payments—coupon rate of interest

Maturity date

Priority to assets and earnings

Control of the firm

3

Types of Debt—Short-Term

Treasury bills—U.S. government securities

Repurchase agreement—repo

Federal funds—loans from one bank to another

Banker’s acceptance—a “postdated check”

4

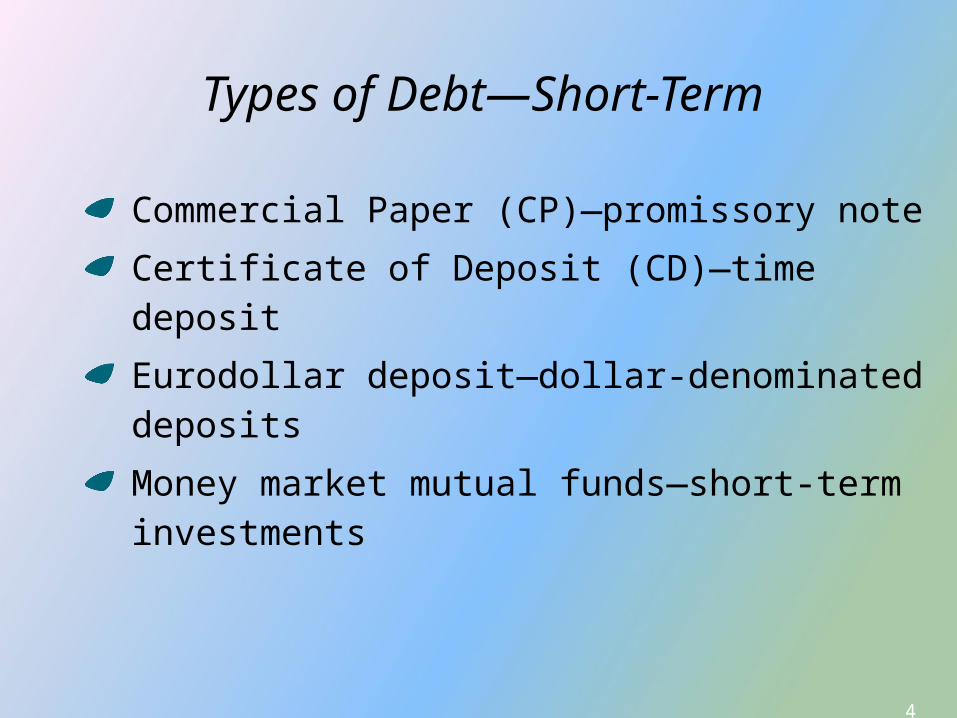

Types of Debt—Short-Term

Commercial Paper (CP)—promissory note

Certificate of Deposit (CD)—time deposit

Eurodollar deposit—dollar-denominated deposits

Money market mutual funds—short-term investments

5

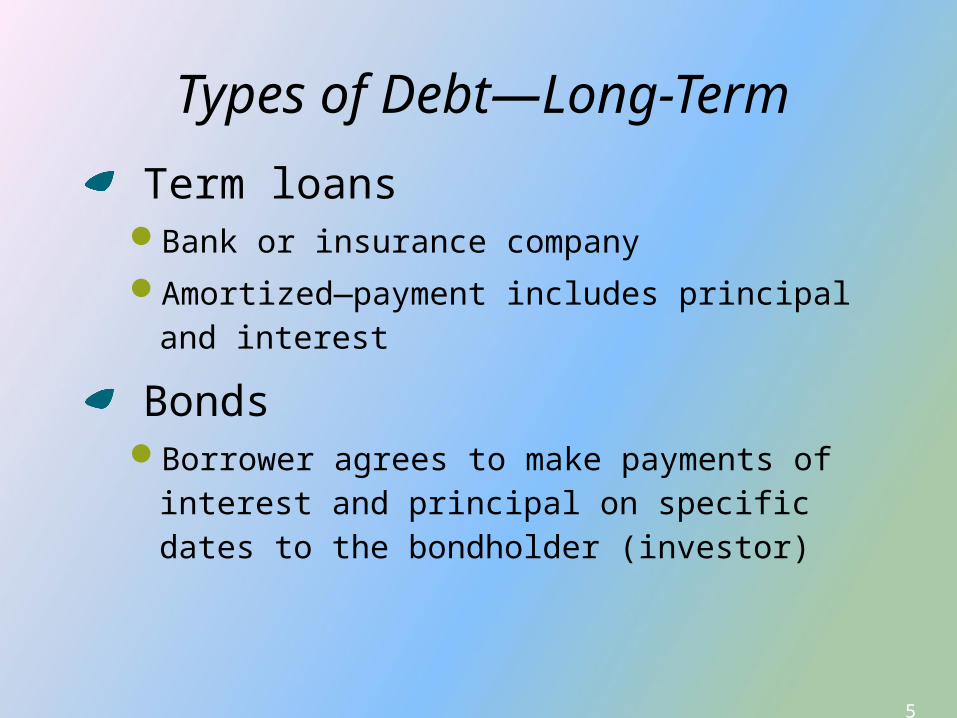

Term loansBank or insurance company

Amortized—payment includes principal and interest

Bonds Borrower agrees to make payments of

interest and principal on specific dates to the bondholder (investor)

Types of Debt—Long-Term

6

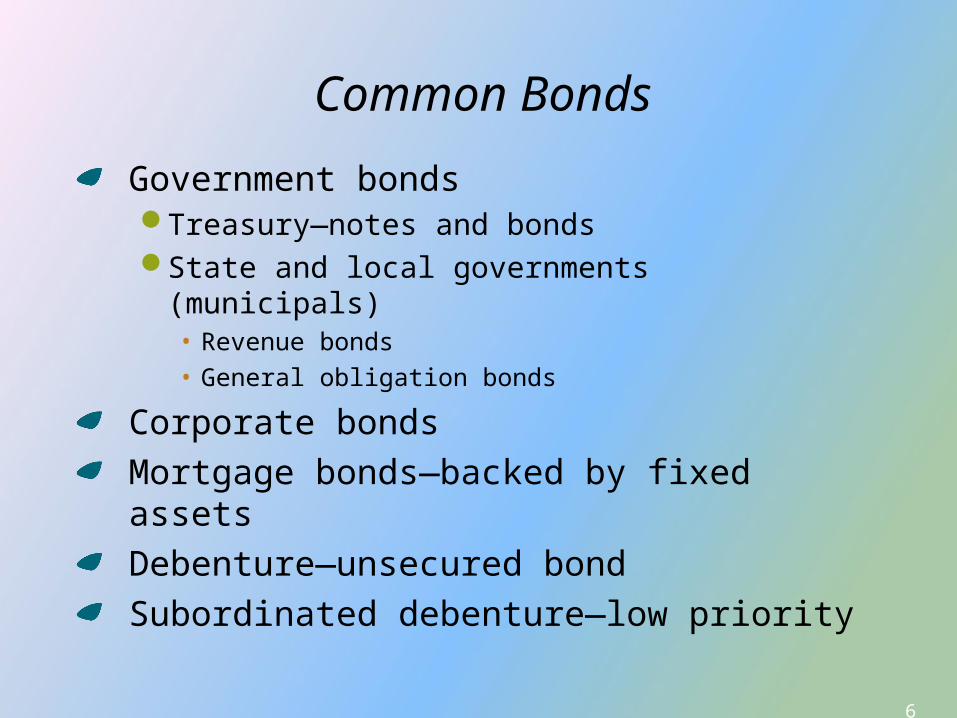

Common Bonds

Government bondsTreasury—notes and bondsState and local governments (municipals)

• Revenue bonds• General obligation bonds

Corporate bondsMortgage bonds—backed by fixed assetsDebenture—unsecured bondSubordinated debenture—low priority

7

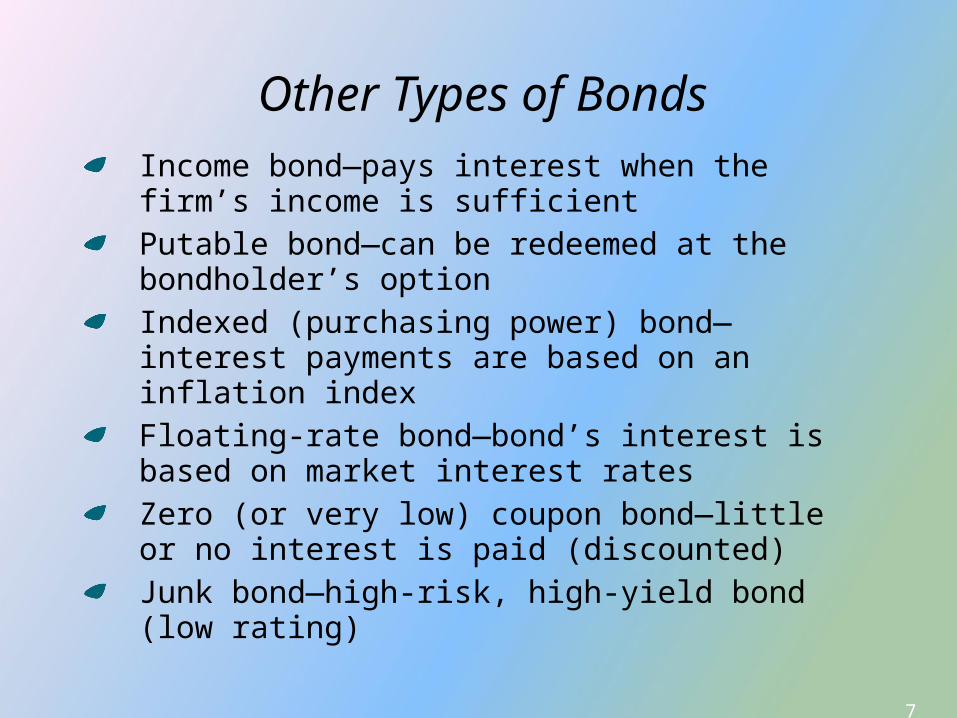

Other Types of BondsIncome bond—pays interest when the firm’s income is sufficient Putable bond—can be redeemed at the bondholder’s optionIndexed (purchasing power) bond—interest payments are based on an inflation indexFloating-rate bond—bond’s interest is based on market interest ratesZero (or very low) coupon bond—little or no interest is paid (discounted)Junk bond—high-risk, high-yield bond (low rating)

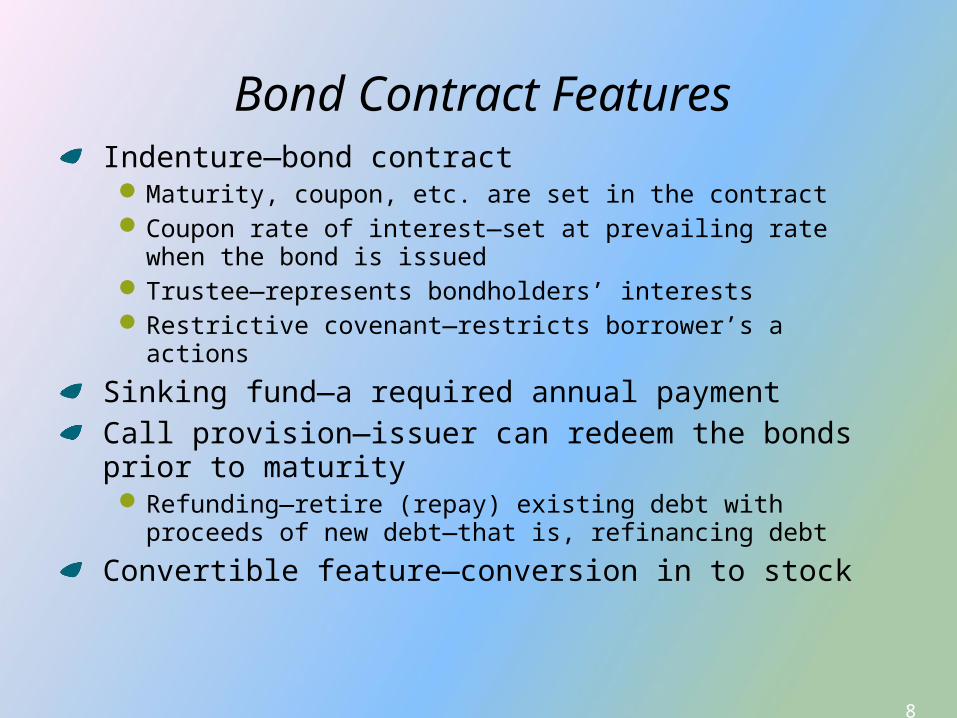

8

Bond Contract FeaturesIndenture—bond contractMaturity, coupon, etc. are set in the contractCoupon rate of interest—set at prevailing rate when the

bond is issuedTrustee—represents bondholders’ interestsRestrictive covenant—restricts borrower’s a actions

Sinking fund—a required annual paymentCall provision—issuer can redeem the bonds prior to maturityRefunding—retire (repay) existing debt with proceeds

of new debt—that is, refinancing debt

Convertible feature—conversion in to stock

9

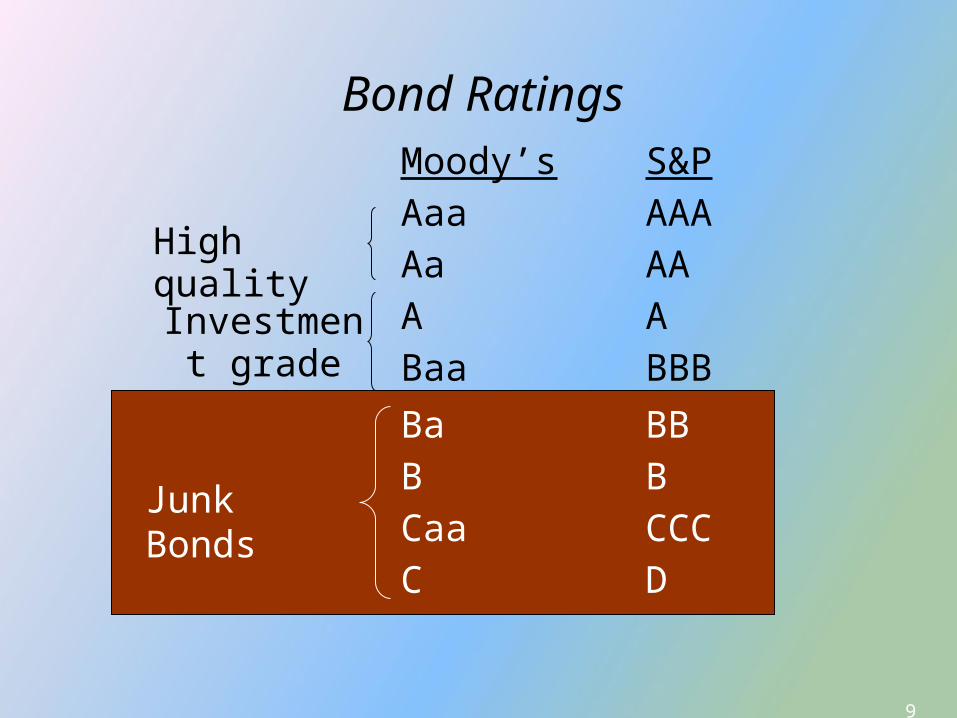

Bond RatingsMoody’s S&P Aaa AAA Aa AA A A Baa BBB Ba BB B B Caa CCC C D

High qualityInvestmen

t grade

Substandard

Speculative

Ba BB B B Caa CCC C D

Junk Bonds

10

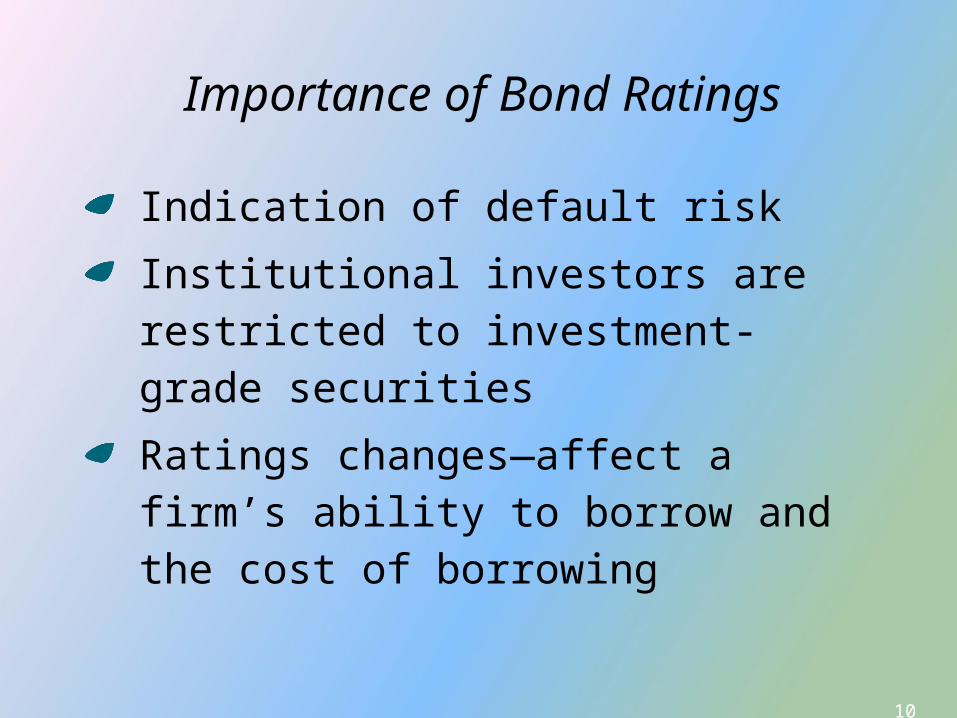

Importance of Bond Ratings

Indication of default risk

Institutional investors are restricted to investment-grade securities

Ratings changes—affect a firm’s ability to borrow and the cost of borrowing

11

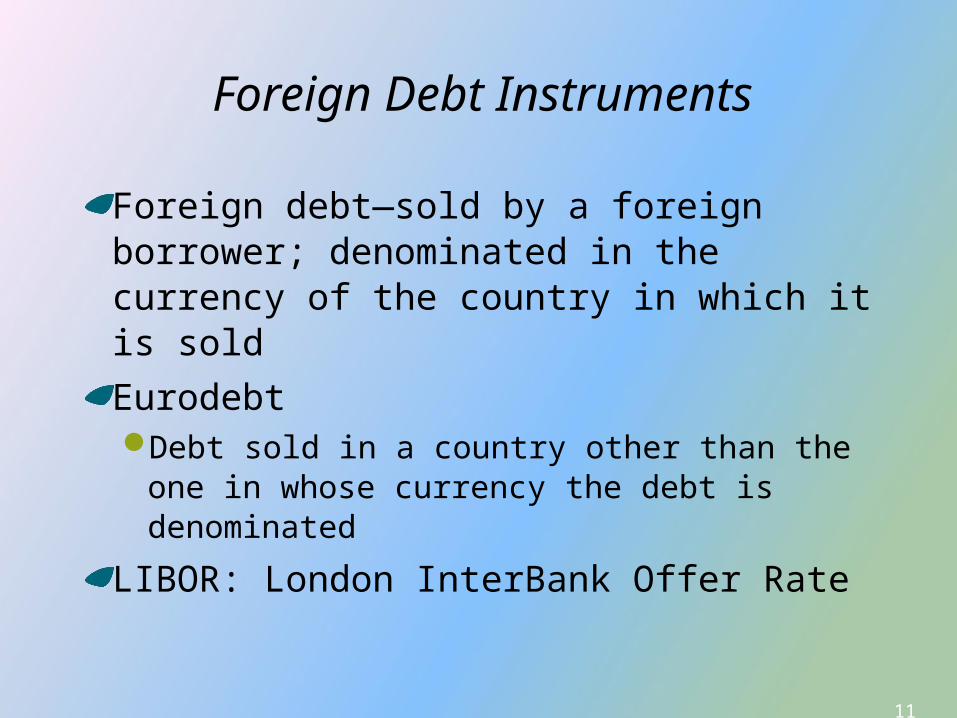

Foreign Debt Instruments

Foreign debt—sold by a foreign borrower; denominated in the currency of the country in which it is sold

EurodebtDebt sold in a country other than the one

in whose currency the debt is denominated

LIBOR: London InterBank Offer Rate

12

Basic Valuation

From “The Time Value of Money” we know that the value of an asset is based on the present value of the cash flows the asset is expected to produce in the future.

13

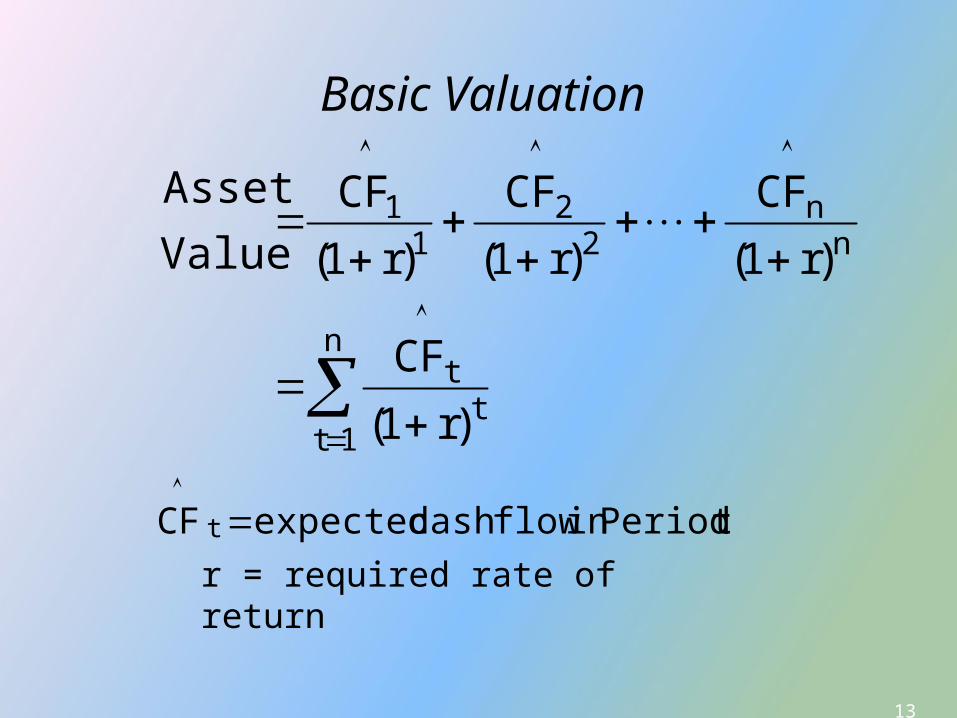

Basic Valuation

n

1tt

t

nn

22

11

)r1(

CF

)r1(

CF

)r1(

CF

)r1(

CF

Value

Asset

r = required rate of return

t Period inflow cash expected CFt

14

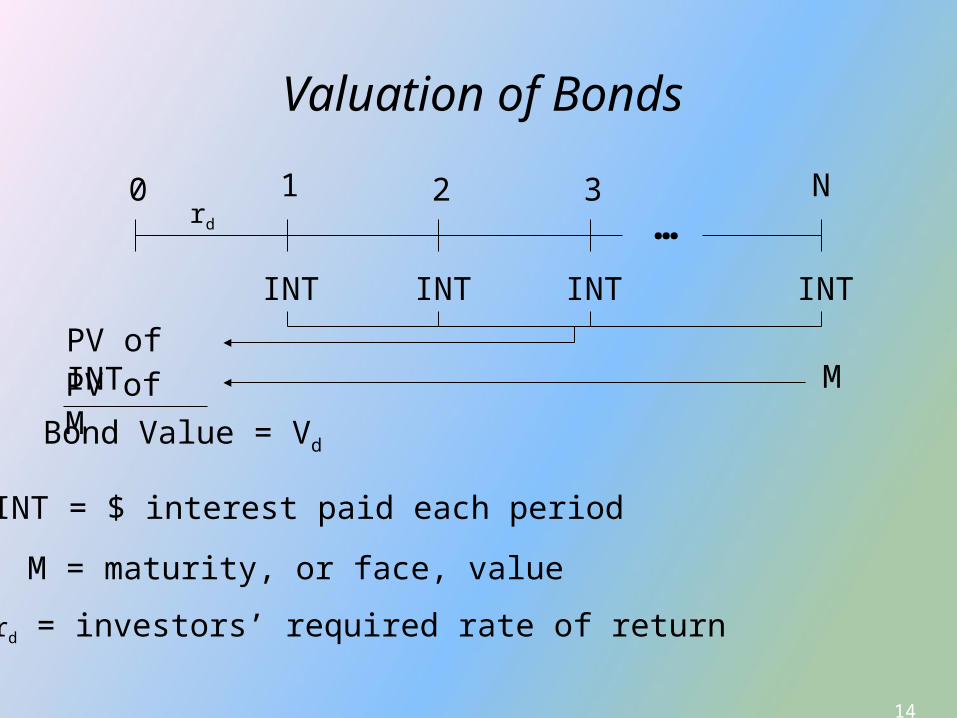

Valuation of Bonds

1…

0 2 3 N

INT

PV of INTPV of M

Bond Value = Vd

INT INT INT

M

INT = $ interest paid each period

M = maturity, or face, value

rd

rd = investors’ required rate of return

15

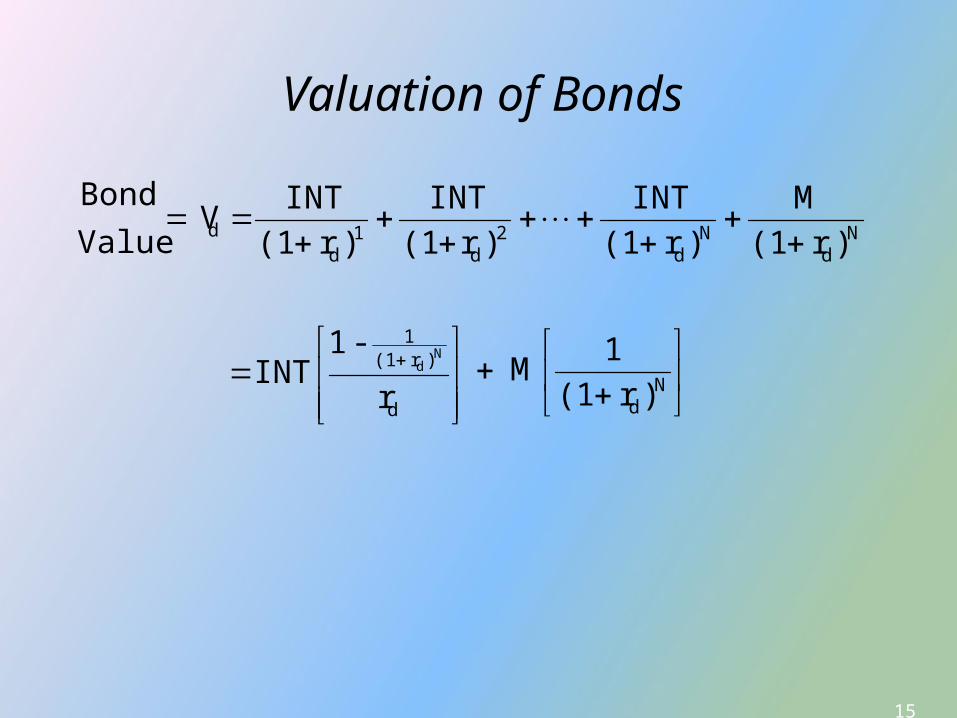

Valuation of Bonds

Nd

Nd

2d

1d

d )r (1M

)r (1INT

)r (1INT

)r (1INT

V Value

Bond

d

)r (11

r

- 1 INT

Nd

Nd)r (1

1 M

16

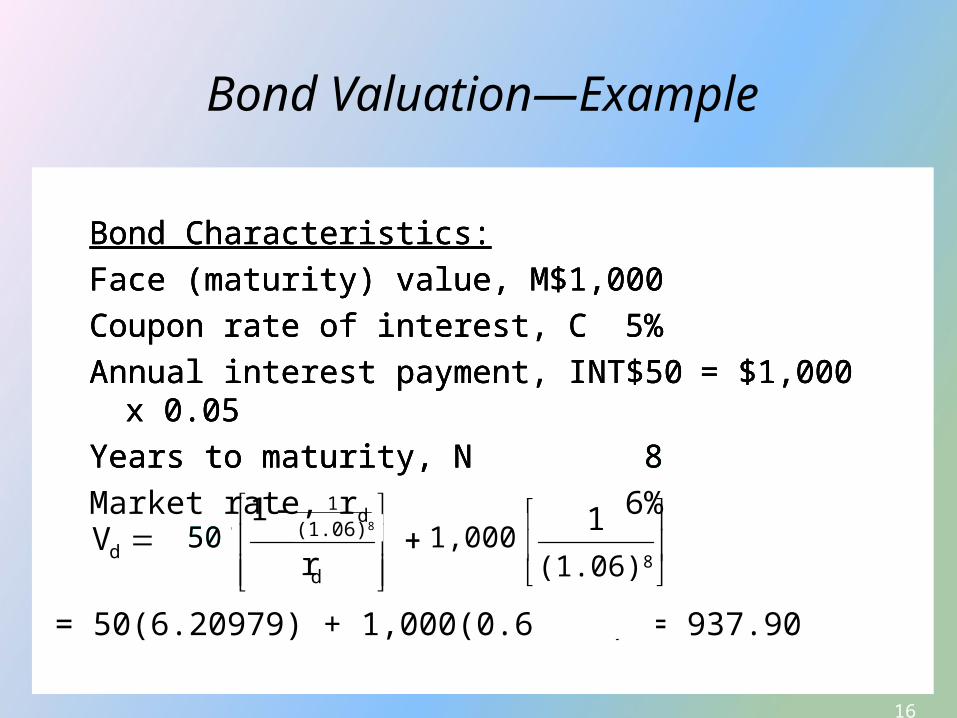

Bond Valuation—Example

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 5%Annual interest payment, INT $50 = $1,000 x

0.05Years to maturity, N 8Market rate, rd 6%

Ndd

)r (11

d )r (11

M r

- 1 INT V

N d

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 5%Annual interest payment, INT $50 = $1,000 x

0.05Years to maturity, N 8Market rate, rd 6%

1,000

= 50(6.20979) + 1,000(0.62741) = 937.90

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 5%Annual interest payment, INT $50 = $1,000 x

0.05Years to maturity, N 8Market rate, rd 6%

50 1,000

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 5%Annual interest payment, INT $50 = $1,000 x

0.05Years to maturity, N 8Market rate, rd 6%

50 (1 + rd)8

(1+rd)8

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 5%Annual interest payment, INT $50 = $1,000 x

0.05Years to maturity, N 8Market rate, rd 6%

(1.06)8

(1.06)8

Ndd

)r (11

d )r (11

M r

- 1 INT V

N d 1,00050 1,00050 (1 + rd)8

(1+rd)8

(1.06)8

(1.06)8

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 5%Annual interest payment, INT $50 = $1,000 x

0.05Years to maturity, N 8Market rate, rd 6%

17

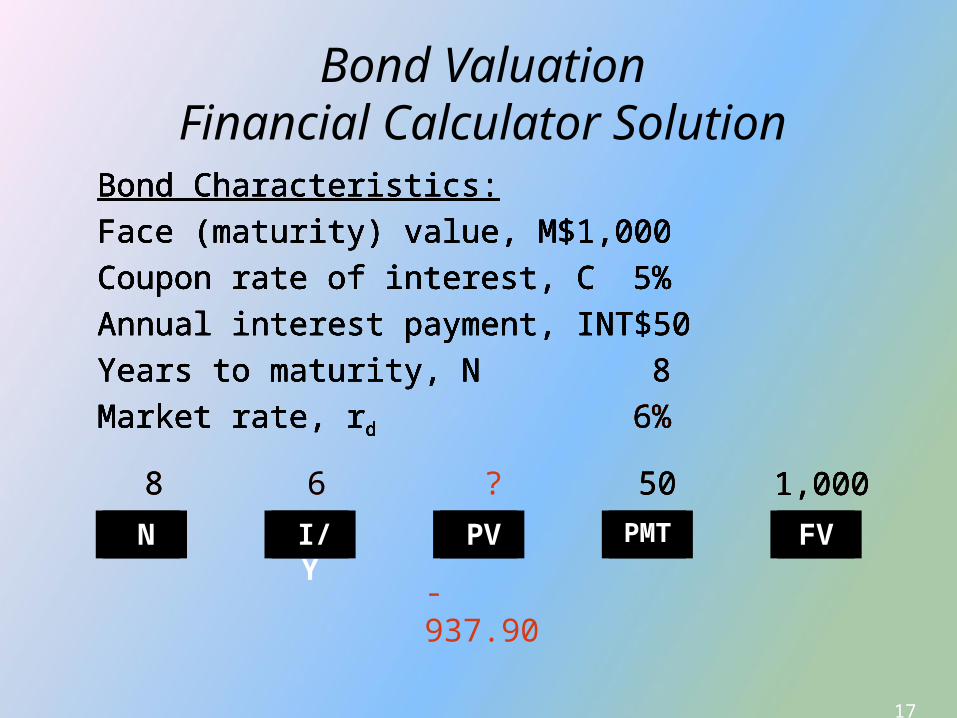

Bond ValuationFinancial Calculator Solution

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 5%Annual interest payment, INT $50Years to maturity, N 8Market rate, rd 6%

N I/Y PV PMT FV

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 5%Annual interest payment, INT $50Years to maturity, N 8Market rate, rd 6%

1,000

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 5%Annual interest payment, INT $50Years to maturity, N 8Market rate, rd 6%

1,00050

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 5%Annual interest payment, INT $50Years to maturity, N 8Market rate, rd 6%

1,000508

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 5%Annual interest payment, INT $50Years to maturity, N 8Market rate, rd 6%

1,000508 6

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 5%Annual interest payment, INT $50Years to maturity, N 8Market rate, rd 6%

1,000508 6 ?

-937.90

18

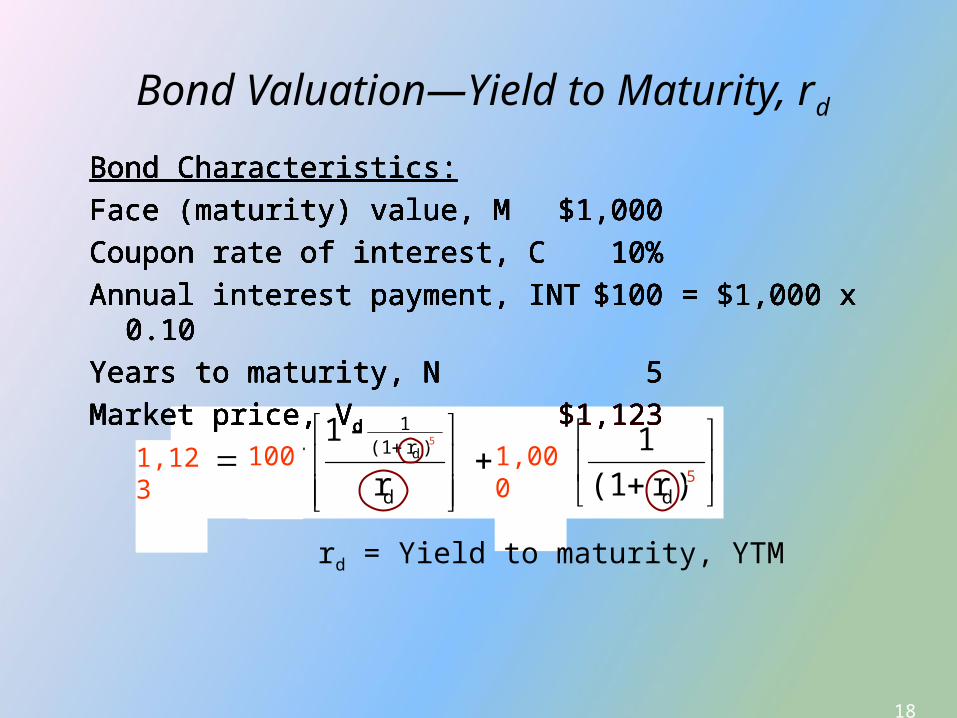

Bond Valuation—Yield to Maturity, rd

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 10%Annual interest payment, INT $100 = $1,000 x

0.10Years to maturity, N 5Market price, Vd $1,123

Ndd

)r (11

d )r (11

M r

- 1 INT V

Nd

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 10%Annual interest payment, INT $100 = $1,000 x

0.10Years to maturity, N 5Market price, Vd $1,123

1,000

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 10%Annual interest payment, INT $100 = $1,000 x

0.10Years to maturity, N 5Market price, Vd $1,123

100

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 10%Annual interest payment, INT $100 = $1,000 x

0.10Years to maturity, N 5Market price, Vd $1,123

5

5

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 10%Annual interest payment, INT $100 = $1,000 x

0.10Years to maturity, N 5Market price, Vd $1,123

rd = Yield to maturity, YTM

1,123

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 10%Annual interest payment, INT $100 = $1,000 x

0.10Years to maturity, N 5Market price, Vd $1,123

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 10%Annual interest payment, INT $100 = $1,000 x

0.10Years to maturity, N 5Market price, Vd $1,123

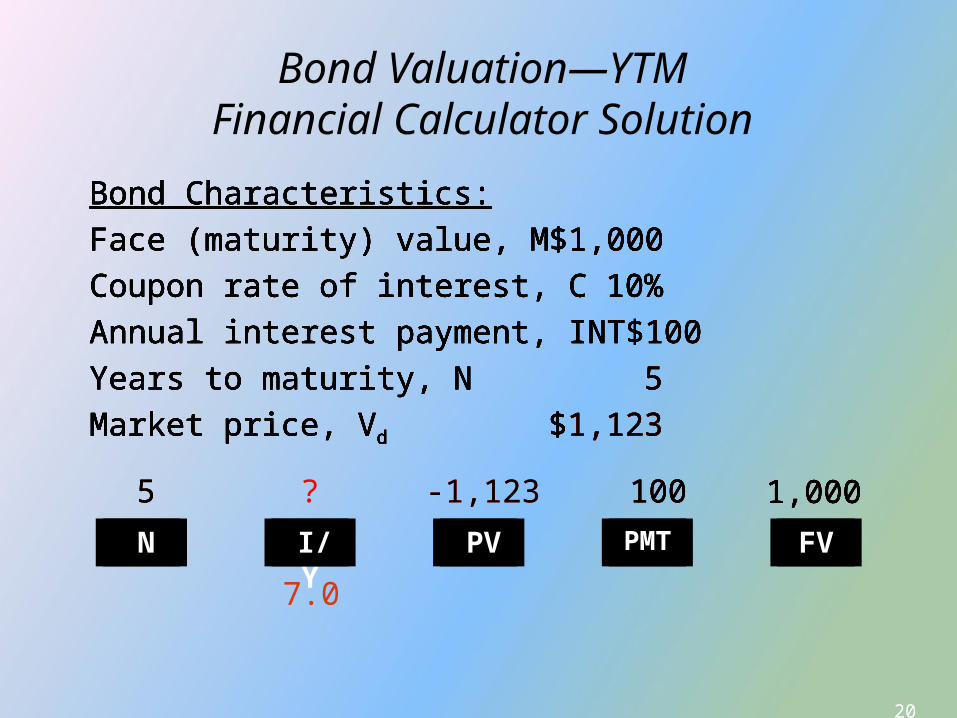

19

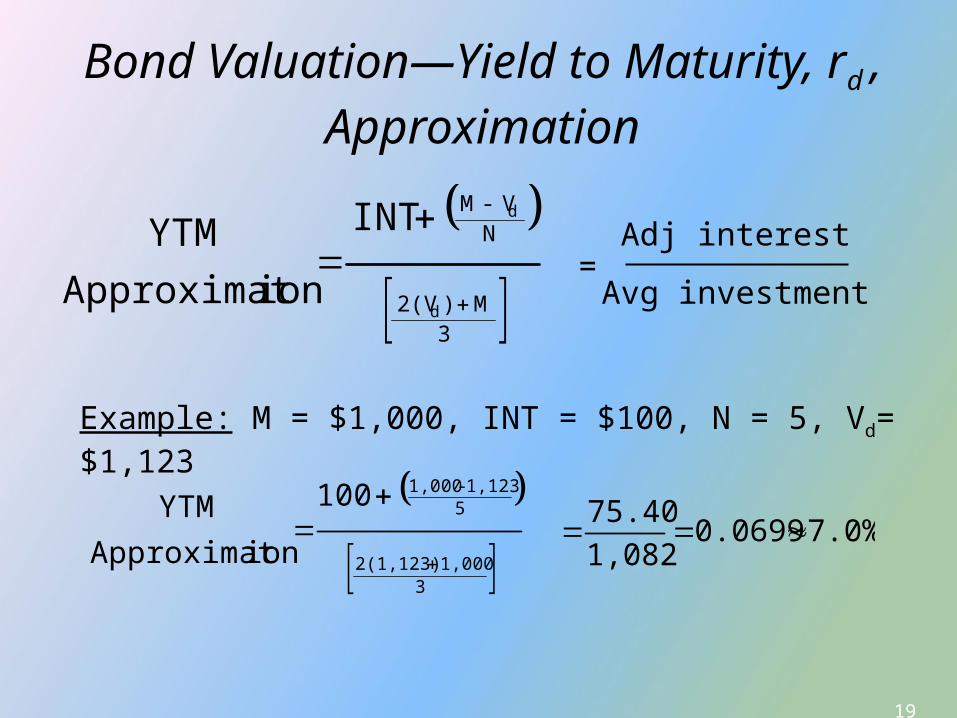

Bond Valuation—Yield to Maturity, rd , Approximation

3

M )2(V

N V- M

d

d INT

ionApproximat

YTM

Example: M = $1,000, INT = $100, N = 5, Vd= $1,123

31,000 2(1,123)

51,123 - 1,000 100

ionApproximat

YTM

7.0% 0.0699

1,08275.40

=Adj interest

Avg investment

20

Bond Valuation—YTMFinancial Calculator Solution

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 10%Annual interest payment, INT $100Years to maturity, N 5Market price, Vd $1,123

N I/Y PV PMT FV

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 10%Annual interest payment, INT $100Years to maturity, N 5Market price, Vd $1,123

1,000

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 10%Annual interest payment, INT $100Years to maturity, N 5Market price, Vd $1,123

1,000100

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 10%Annual interest payment, INT $100Years to maturity, N 5Market price, Vd $1,123

1,0001005

7.0

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 10%Annual interest payment, INT $100Years to maturity, N 5Market price, Vd $1,123

1,0001005 -1,123?

Bond Characteristics:Face (maturity) value, M $1,000Coupon rate of interest, C 10%Annual interest payment, INT $100Years to maturity, N 5Market price, Vd $1,123

1,0001005 -1,123

21

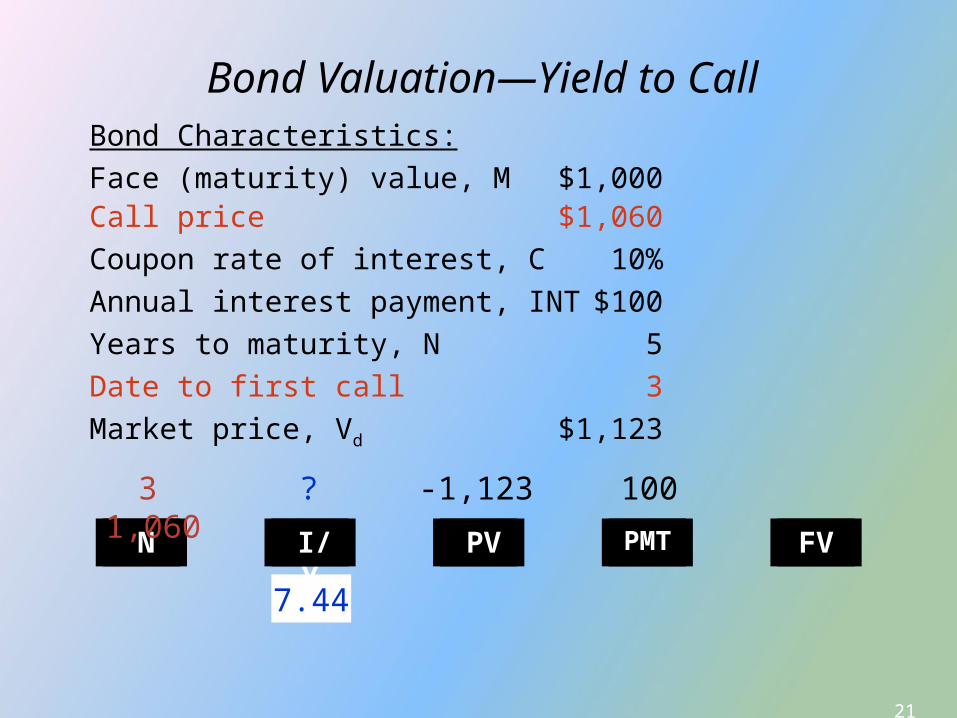

Bond Valuation—Yield to CallBond Characteristics:Face (maturity) value, M $1,000Call price $1,060Coupon rate of interest, C 10%Annual interest payment, INT $100Years to maturity, N 5Date to first call 3Market price, Vd $1,123

N I/Y PV PMT FV

3 ? -1,123 1001,060

7.44

22

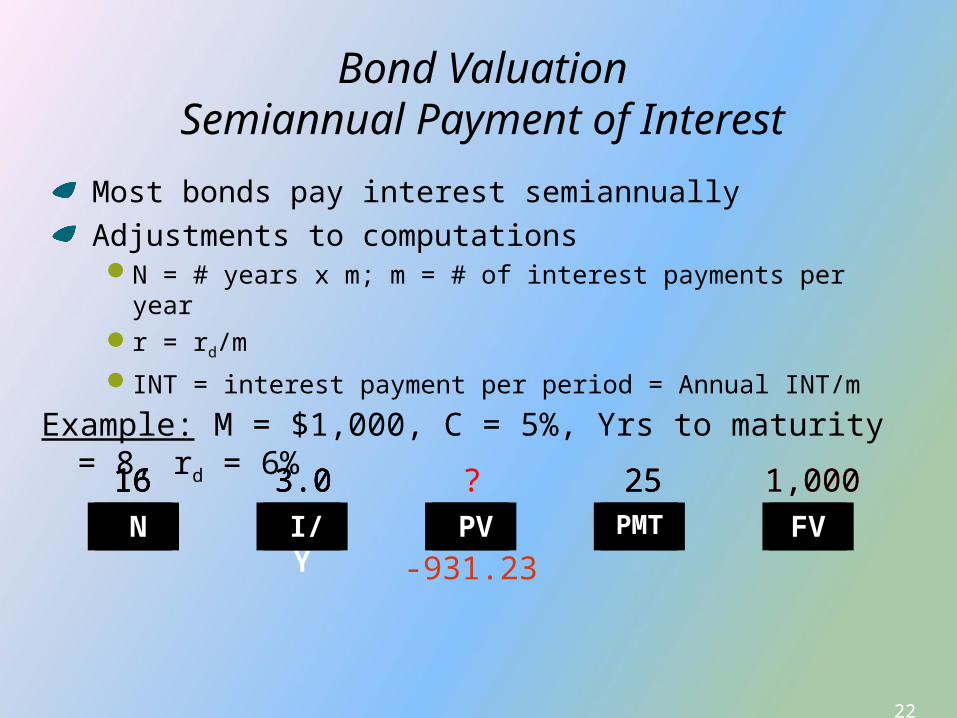

Bond ValuationSemiannual Payment of Interest

Most bonds pay interest semiannually Adjustments to computationsN = # years x m; m = # of interest payments per yearr = rd/m

INT = interest payment per period = Annual INT/m

Example: M = $1,000, C = 5%, Yrs to maturity = 8, rd = 6%

N I/Y PV PMT FV

1616 3.016 3.0 2516 3.0 25 1,000?16 3.0 25 1,000

-931.23

23

Changes in Bond Values Over Time

Whenever the going rate of interest, rd, equals the

coupon rate, a bond will sell at its par value

An increase (decrease) in interest rates will cause the price of an outstanding bond to fall (rise).

The market value of a bond will always approach its par value as its maturity date approaches, provided the firm does not go bankrupt.

24

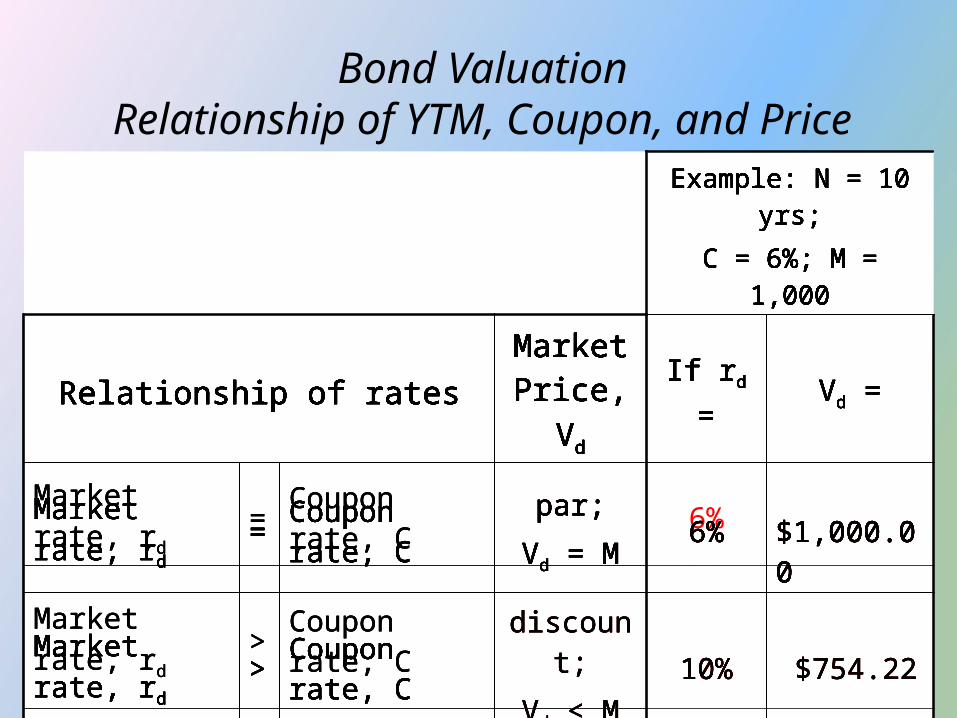

Bond ValuationRelationship of YTM, Coupon, and Price

Example: N = 10 yrs;

C = 6%; M = 1,000

Relationship of ratesMarket

Price, Vd

Market rate, kd

=Coupon rate, C

par;

Vd = M

Market rate, kd

>Coupon rate, C

discount;

Vd < M

Market rate, kd

<Coupon rate, C

premium

Vd > M

Example: N = 10 yrs;

C = 6%; M = 1,000

Relationship of ratesMarket

Price, Vd

Market rate, rd

=Coupon rate, C

par;

Vd = M

Market rate, rd

>Coupon rate, C

discount;

Vd < M

Market rate, rd

<Coupon rate, C

premium

Vd > M

Example: N = 10 yrs;

C = 6%; M = 1,000

Relationship of ratesMarket

Price, Vd

If rd = Vd =

Market rate, rd

=Coupon rate, C

par;

Vd = M

Market rate, rd

>Coupon rate, C

discount;

Vd < M

Market rate, rd

<Coupon rate, C

premium

Vd > M

Example: N = 10 yrs;

C = 6%; M = 1,000

Relationship of ratesMarket

Price, Vd

If rd = Vd =

Market rate, rd

=Coupon rate, C

par;

Vd = M6%

Market rate, rd

>Coupon rate, C

discount;

Vd < M

Market rate, rd

<Coupon rate, C

premium

Vd > M

Example: N = 10 yrs;

C = 6%; M = 1,000

Relationship of ratesMarket

Price, Vd

If rd = Vd =

Market rate, rd

=Coupon rate, C

par;

Vd = M6% $1,000.00

Market rate, rd

>Coupon rate, C

discount;

Vd < M

Market rate, rd

<Coupon rate, C

premium

Vd > M

Example: N = 10 yrs;

C = 6%; M = 1,000

Relationship of ratesMarket

Price, Vd

If rd = Vd =

Market rate, rd

=Coupon rate, C

par;

Vd = M6% $1,000.00

Market rate, rd

>Coupon rate, C

discount;

Vd < M

Market rate, rd

<Coupon rate, C

premium

Vd > M

Example: N = 10 yrs;

C = 6%; M = 1,000

Relationship of ratesMarket

Price, Vd

If rd = Vd =

Market rate, rd

=Coupon rate, C

par;

Vd = M6% $1,000.00

Market rate, rd

>Coupon rate, C

discount;

Vd < M10%

Market rate, rd

<Coupon rate, C

premium

Vd > M

Example: N = 10 yrs;

C = 6%; M = 1,000

Relationship of ratesMarket

Price, Vd

If rd = Vd =

Market rate, rd

=Coupon rate, C

par;

Vd = M6% $1,000.00

Market rate, rd

>Coupon rate, C

discount;

Vd < M10% $754.22

Market rate, rd

<Coupon rate, C

premium

Vd > M

Example: N = 10 yrs;

C = 6%; M = 1,000

Relationship of ratesMarket

Price, Vd

If rd = Vd =

Market rate, rd

=Coupon rate, C

par;

Vd = M6% $1,000.00

Market rate, rd

>Coupon rate, C

discount;

Vd < M10% $754.22

Market rate, rd

<Coupon rate, C

premium

Vd > M

Example: N = 10 yrs;

C = 6%; M = 1,000

Relationship of ratesMarket

Price, Vd

If rd = Vd =

Market rate, rd

=Coupon rate, C

par;

Vd = M6% $1,000.00

Market rate, rd

>Coupon rate, C

discount;

Vd < M10% $754.22

Market rate, rd

<Coupon rate, C

premium

Vd > M4%

Example: N = 10 yrs;

C = 6%; M = 1,000

Relationship of ratesMarket

Price, Vd

If rd = Vd =

Market rate, rd

=Coupon rate, C

par;

Vd = M6% $1,000.00

Market rate, rd

>Coupon rate, C

discount;

Vd < M10% $754.22

Market rate, rd

<Coupon rate, C

premium

Vd > M4% $1,162.22

Example: N = 10 yrs;

C = 6%; M = 1,000

Relationship of ratesMarket

Price, Vd

If rd = Vd =

Market rate, rd

=Coupon rate, C

par;

Vd = M6% $1,000.00

Market rate, rd

>Coupon rate, C

discount;

Vd < M10% $754.22

Market rate, rd

<Coupon rate, C

premium

Vd > M4% $1,162.22

25

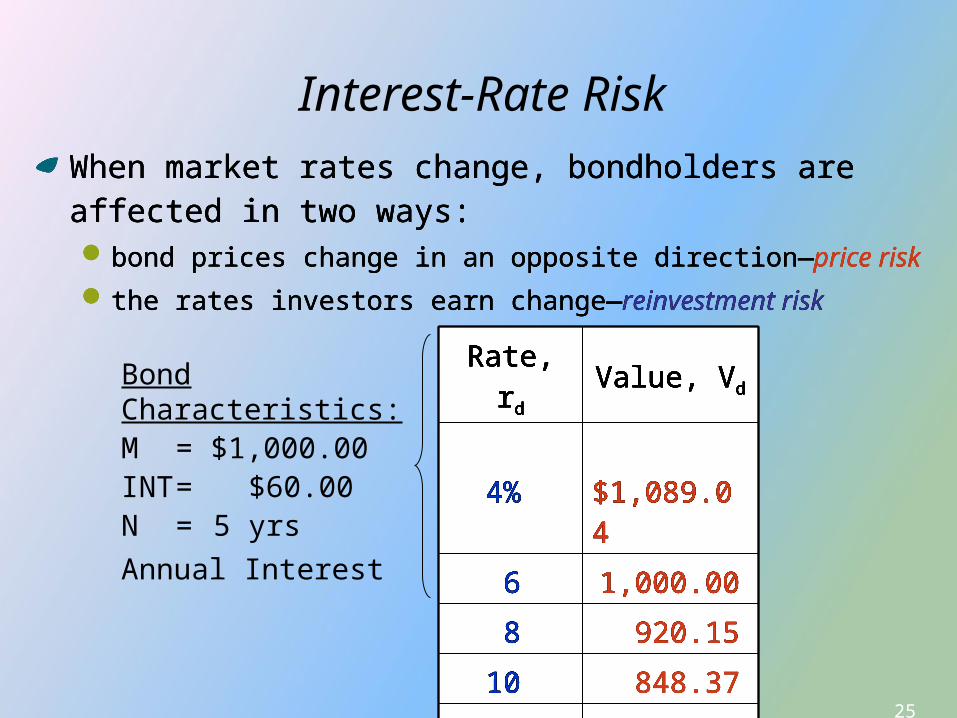

Interest-Rate Risk

Bond Characteristics: M = $1,000.00INT = $60.00N = 5 yrs

Annual Interest

Rate, rd Value, Vd

4% $1,089.04

6

8

10

12

Rate, rd Value, Vd

4% $1,089.04

6 1,000.00

8

10

12

Rate, rd Value, Vd

4% $1,089.04

6 1,000.00

8 920.15

10

12

Rate, rd Value, Vd

4% $1,089.04

6 1,000.00

8 920.15

10 848.37

12

Rate, rd Value, Vd

4% $1,089.04

6 1,000.00

8 920.15

10 848.37

12 783.71

Rate, rd Value, Vd

4% $1,089.04

6 1,000.00

8 920.15

10 848.37

12 783.71

Rate, rd Value, Vd

4% $1,089.04

6 1,000.00

8 920.15

10 848.37

12 783.71

When market rates change, bondholders are affected in two ways:bond prices change in an opposite direction—price risk

the rates investors earn change—reinvestment risk

When market rates change, bondholders are affected in two ways:bond prices change in an opposite direction—price risk

the rates investors earn change—reinvestment risk

When market rates change, bondholders are affected in two ways:bond prices change in an opposite direction—price risk

the rates investors earn change—reinvestment risk

Rate, rd Value, Vd

4% $1,089.04

6 1,000.00

8 920.15

10 848.37

12 783.71

26

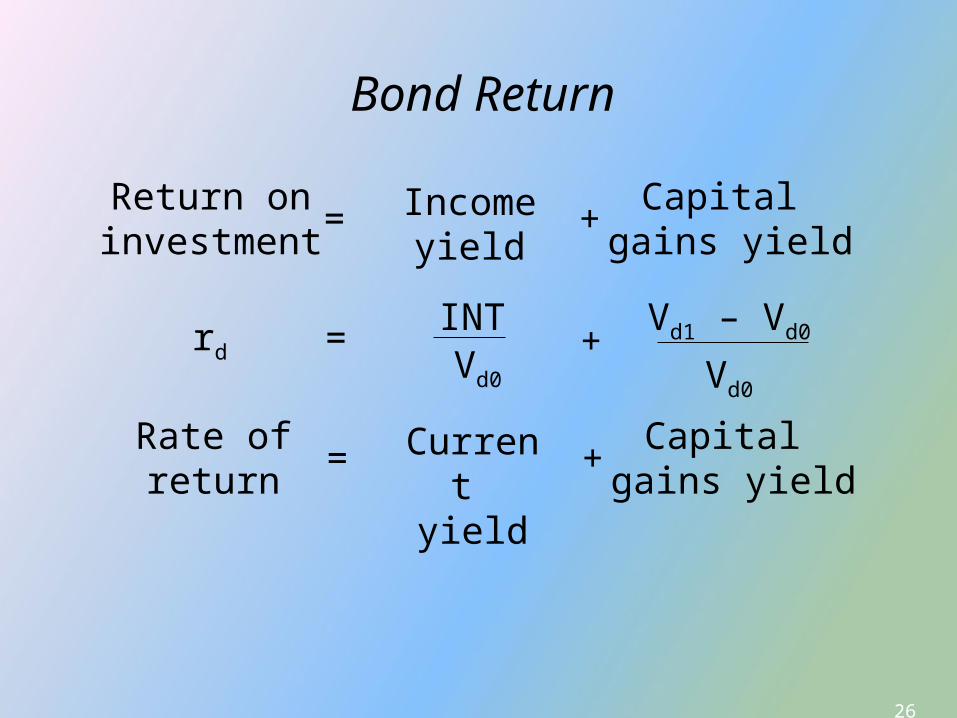

Bond Return

+=

Rate ofreturn

Current yield

= +Capital

gains yield

rd Vd0

INT Vd1 – Vd0

Vd0

Return oninvestment

Income yield

= +Capital

gains yield

27

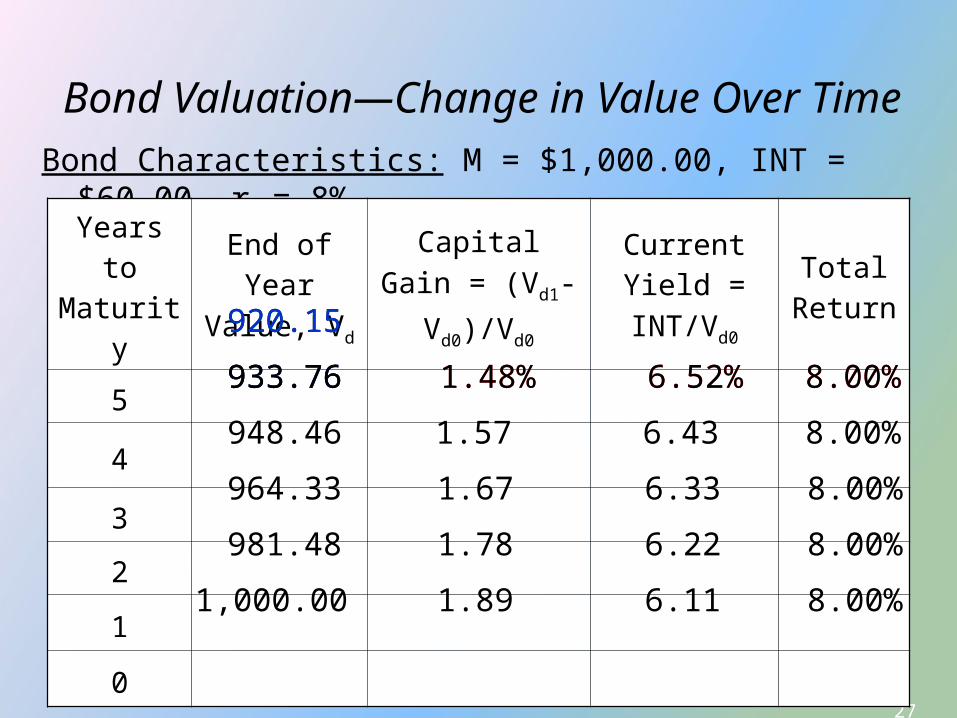

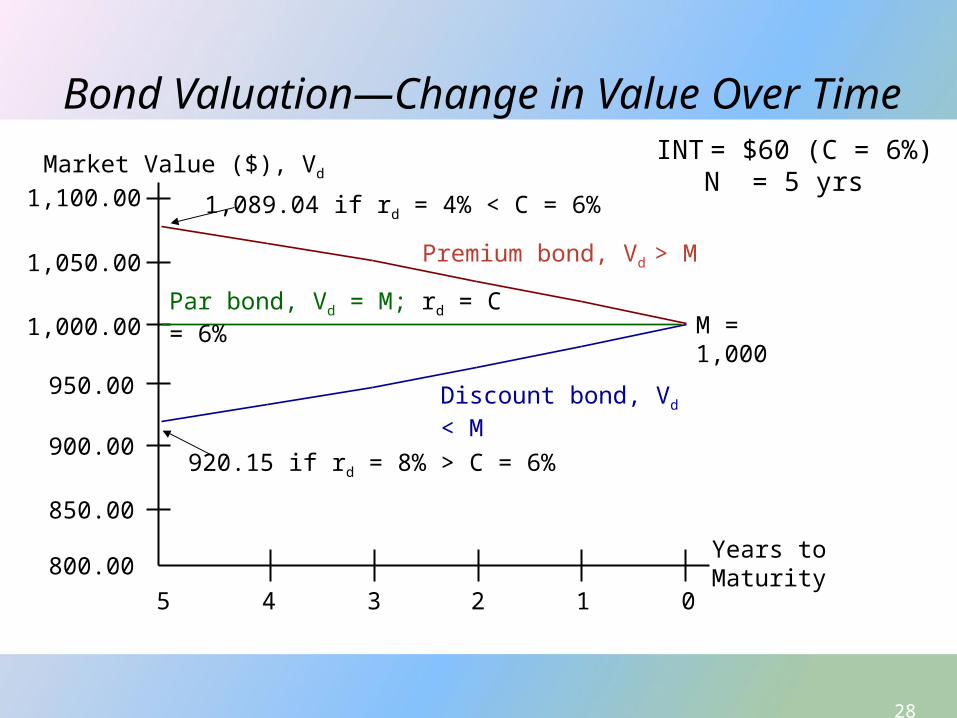

Bond Valuation—Change in Value Over Time

Bond Characteristics: M = $1,000.00, INT = $60.00, rd

= 8%Years to Maturity

End of Year

Value, Vd

Capital Gain = (Vd1-Vd0)/Vd0

Current Yield = INT/Vd0

Total Return

5

4

3

2

1

0

920.15

933.76

948.46

964.33

981.48

1,000.00

1.48% 6.52% 8.00%933.76

920.15

933.76 1.48% 6.52% 8.00%

1.57 6.43 8.00%

1.67 6.33 8.00%

1.78 6.22 8.00%

1.89 6.11 8.00%

28

Bond Valuation—Change in Value Over Time

800.00

850.00

900.00

950.00

1,000.00

1,050.00

1,100.00

5 4 3 2 1 0

Years toMaturity

Market Value ($), Vd

920.15 if rd = 8% > C = 6%

M = 1,000

Discount bond, Vd < M

Par bond, Vd = M; rd = C = 6%

Premium bond, Vd > M

1,089.04 if rd = 4% < C = 6%

INT = $60 (C = 6%) N = 5 yrs

29

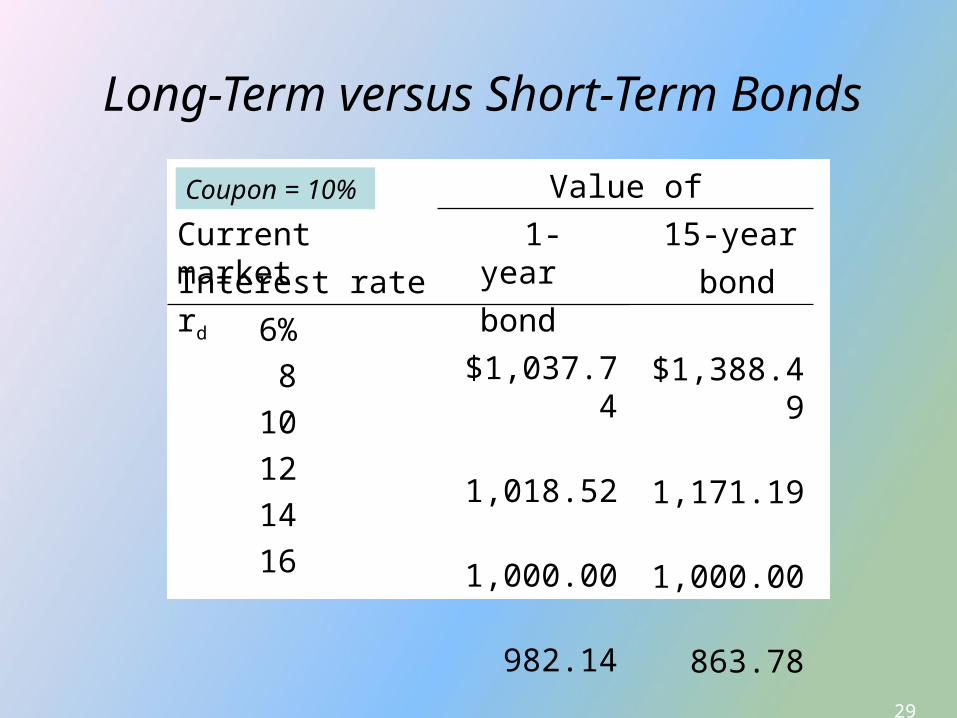

Long-Term versus Short-Term Bonds

$1,037.74

1,018.52

1,000.00

982.14

964.91

948.28

6%8

10121416

bondbond

Interest rate rd

15-year1-year

Current market

Value ofCoupon = 10%

$1,388.49

1,171.19

1,000.00

863.78

754.31

665.47

30

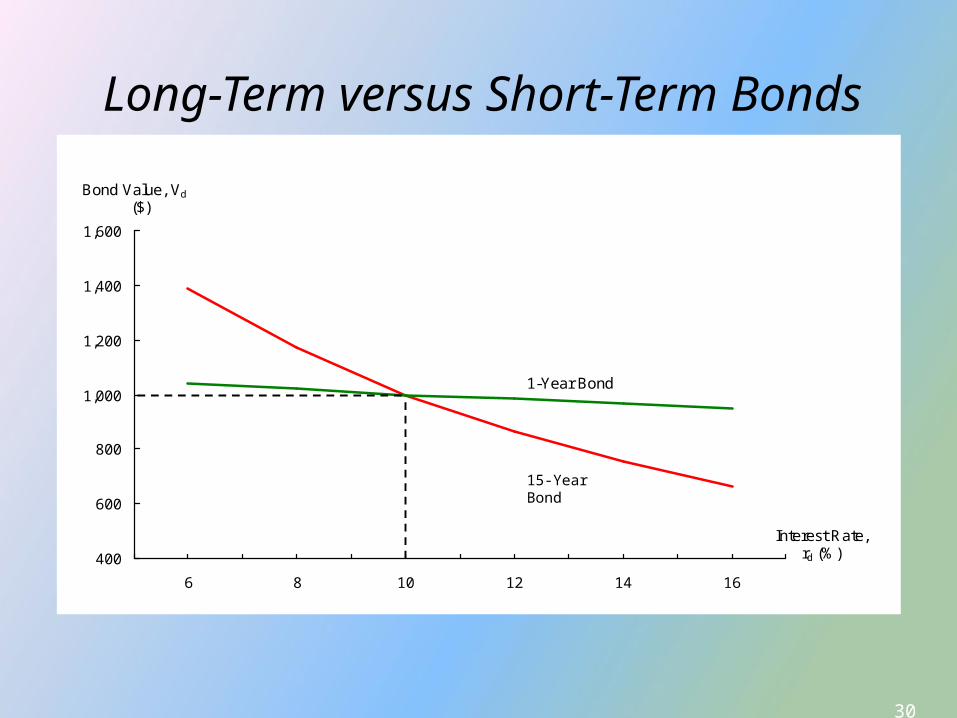

Long-Term versus Short-Term Bonds

400

600

800

1,000

1,200

1,400

1,600

6 8 10 12 14 16

Interest Rate, rd (%)

Bond Value, Vd

($)

1-Year Bond

14-Year Bond 15-Year Bond

31

What is debt? Debt represents a loan

What are bond ratings?Ratings give an indication of the default

risk associated with a bond

How are bond prices determined?Value = PV of the cash flows the bond is

expected to pay during its life

Bonds (Debt)Characteristics and Valuation

32

How are bond yields determined?YTM is the average annual rate of return that an

investor will earn if he or she buys the bond at the current market price and holds it until it matures

YTC is the average annual rate of return that an investor will earn if he or she buys the bond at the current market price and holds it until the first date the bond can be called

What is the relationship between bond prices and interest rates?When interest rates increase, bond prices decrease,

and vice versa

Bonds (Debt)Characteristics and Valuation

Recommended