Embed Size (px)

Citation preview

SBI Corporate Bond Fund

This product is suitable for investors who are seeking:

Investment in debt and money- market securities

Regular income for medium term

Low risk

Disclaimer: Investors should consult their financial advisors if in doubt whether this product is suitable for them.

SBI Corporate Bond Fund

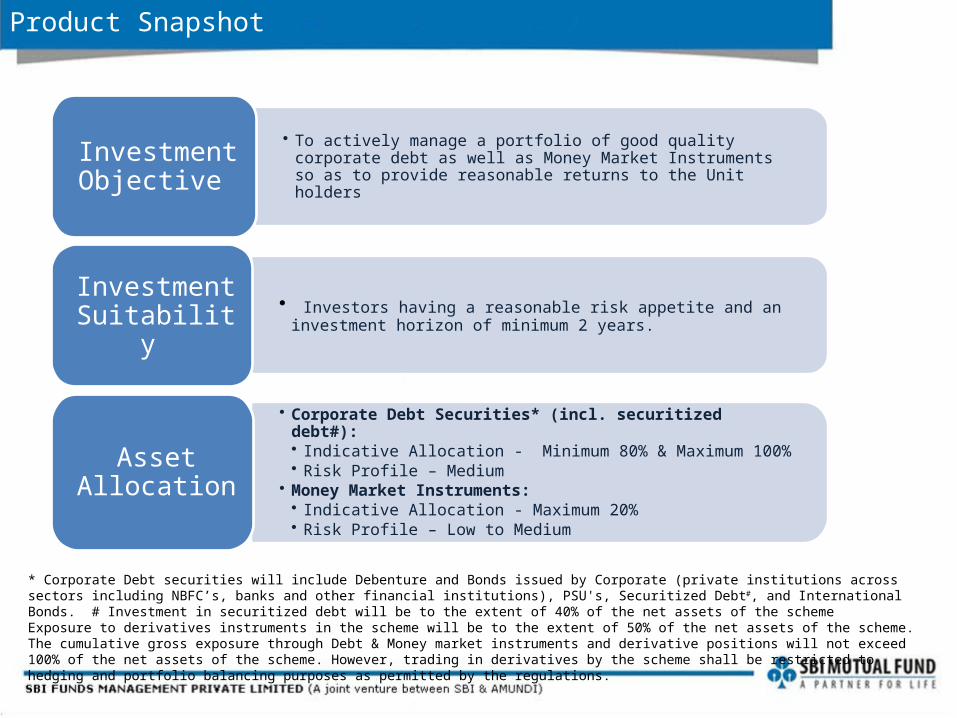

Product Snapshot

* Corporate Debt securities will include Debenture and Bonds issued by Corporate (private institutions across sectors including NBFC’s, banks and other financial institutions), PSU's, Securitized Debt#, and International Bonds. # Investment in securitized debt will be to the extent of 40% of the net assets of the scheme Exposure to derivatives instruments in the scheme will be to the extent of 50% of the net assets of the scheme. The cumulative gross exposure through Debt & Money market instruments and derivative positions will not exceed 100% of the net assets of the scheme. However, trading in derivatives by the scheme shall be restricted to hedging and portfolio balancing purposes as permitted by the regulations.

• To actively manage a portfolio of good quality corporate debt as well as Money Market Instruments so as to provide reasonable returns to the Unit holders

Investment Objective

• Investors having a reasonable risk appetite and an investment horizon of minimum 2 years.

Investment Suitability

• Corporate Debt Securities* (incl. securitized debt#):• Indicative Allocation - Minimum 80% & Maximum 100%• Risk Profile – Medium

• Money Market Instruments: • Indicative Allocation - Maximum 20% • Risk Profile – Low to Medium

Asset Allocation

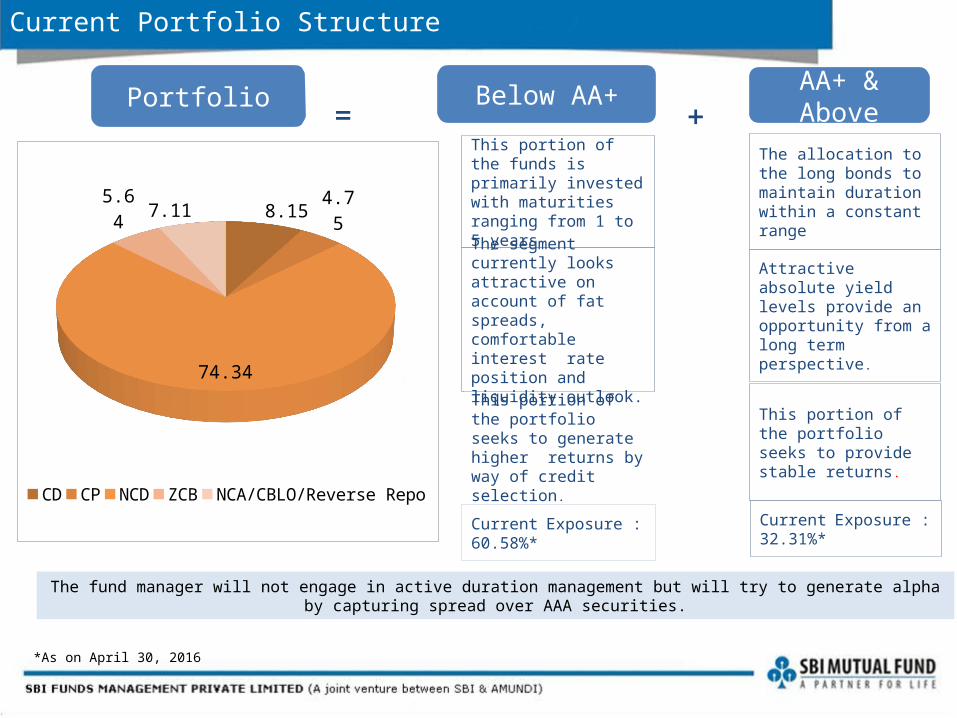

Current Portfolio Structure

Portfolio AA+ & AboveBelow AA+₌ ₊

The fund manager will not engage in active duration management but will try to generate alpha by capturing spread over AAA securities.

This portion of the funds is primarily invested with maturities ranging from 1 to 5 yearsThe segment currently looks attractive on account of fat spreads, comfortable interest rate position and liquidity outlook.This portion of the portfolio seeks to generate higher returns by way of credit selection.

The allocation to the long bonds to maintain duration within a constant range

Attractive absolute yield levels provide an opportunity from a long term perspective.

This portion of the portfolio seeks to provide stable returns.

Current Exposure : 60.58%*

Current Exposure : 32.31%*

*As on April 30, 2016

8.154.75

74.34

5.64 7.11

CD CP NCD ZCB NCA/CBLO/Reverse Repo

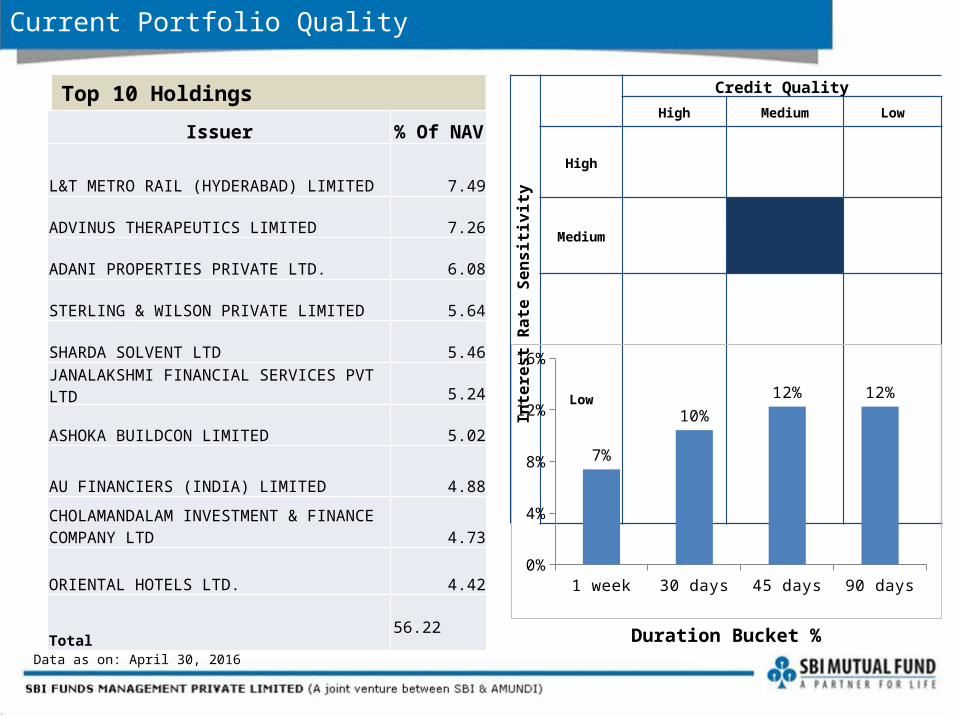

Current Portfolio Quality

Data as on: April 30, 2016

Rating Breakdown

Interest

Rate Sensitivity

Credit QualityHigh Medium Low

High

Medium

Low

Issuer % Of NAV

L&T METRO RAIL (HYDERABAD) LIMITED 7.49

ADVINUS THERAPEUTICS LIMITED 7.26

ADANI PROPERTIES PRIVATE LTD. 6.08

STERLING & WILSON PRIVATE LIMITED 5.64

SHARDA SOLVENT LTD 5.46JANALAKSHMI FINANCIAL SERVICES PVT LTD 5.24

ASHOKA BUILDCON LIMITED 5.02

AU FINANCIERS (INDIA) LIMITED 4.88

CHOLAMANDALAM INVESTMENT & FINANCE COMPANY LTD 4.73

ORIENTAL HOTELS LTD. 4.42

Total 56.22

Top 10 Holdings

Duration Bucket %

1 week 30 days 45 days 90 days0%

4%

8%

12%

16%

7%

10%12% 12%

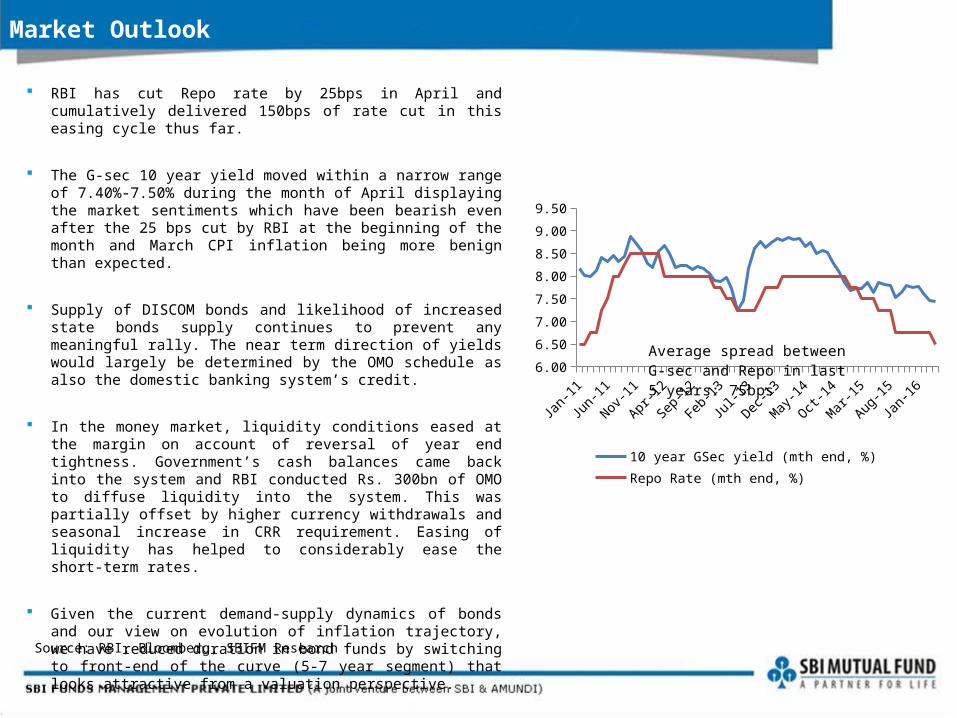

RBI has cut Repo rate by 25bps in April and cumulatively delivered 150bps of rate cut in this easing cycle thus far.

The G-sec 10 year yield moved within a narrow range of 7.40%-7.50% during the month of April displaying the market sentiments which have been bearish even after the 25 bps cut by RBI at the beginning of the month and March CPI inflation being more benign than expected.

Supply of DISCOM bonds and likelihood of increased state bonds supply continues to prevent any meaningful rally. The near term direction of yields would largely be determined by the OMO schedule as also the domestic banking system’s credit.

In the money market, liquidity conditions eased at the margin on account of reversal of year end tightness. Government’s cash balances came back into the system and RBI conducted Rs. 300bn of OMO to diffuse liquidity into the system. This was partially offset by higher currency withdrawals and seasonal increase in CRR requirement. Easing of liquidity has helped to considerably ease the short-term rates.

Given the current demand-supply dynamics of bonds and our view on evolution of inflation trajectory, we have reduced duration in bond funds by switching to front-end of the curve (5-7 year segment) that looks attractive from a valuation perspective.

Market Outlook

Source: RBI, Bloomberg, SBIFM Research

Jan-11

May-11

Sep-11

Jan-12

May-12

Sep-12

Jan-13

May-13

Sep-13

Jan-14

May-14

Sep-14

Jan-15

May-15

Sep-15

Jan-16

6.00

6.50

7.00

7.50

8.00

8.50

9.00

9.50

10 year GSec yield (mth end, %)Repo Rate (mth end, %)

Average spread between G-sec and Repo in last 5 years: 75bps

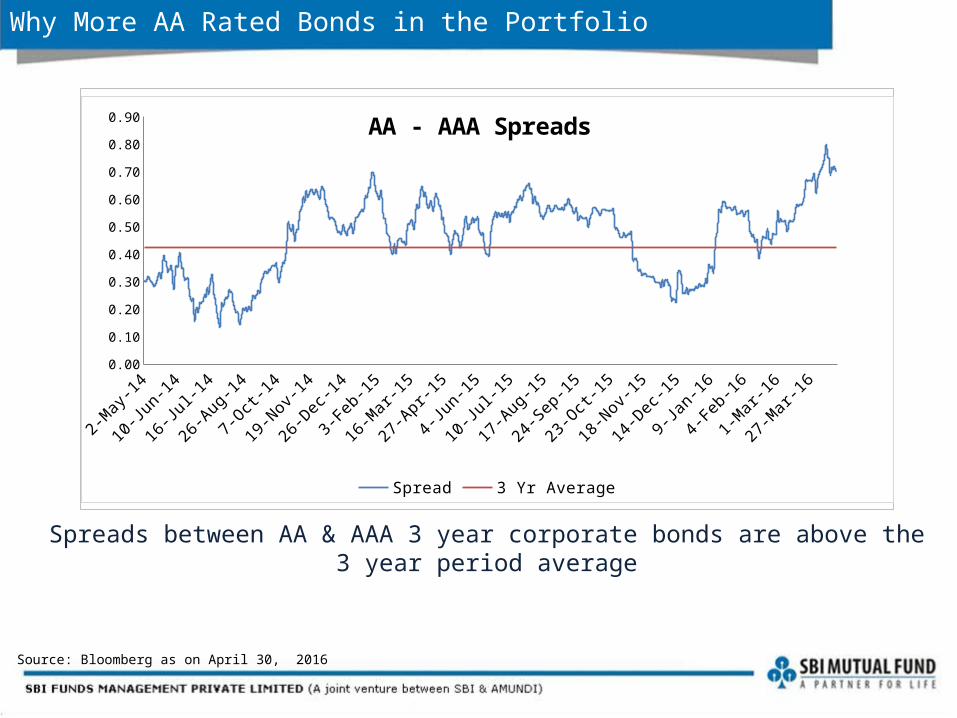

Why More AA Rated Bonds in the Portfolio

Source: Bloomberg as on April 30, 2016

AA - AAA Spreads

Spreads between AA & AAA 3 year corporate bonds are above the 3 year period average

May-14Jun-14

Jul-14

Aug-14

Sep-14

Oct-14

Nov-14

Dec-14Jan-15

Feb-15

Mar-15Apr-1

5

May-15Jun-15

Jul-15

Aug-15Se

p-15Oct-

15

Nov-15

Dec-15Jan-16

Feb-16

Mar-16Apr-1

6

May-16

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

Spread 3 Yr Average

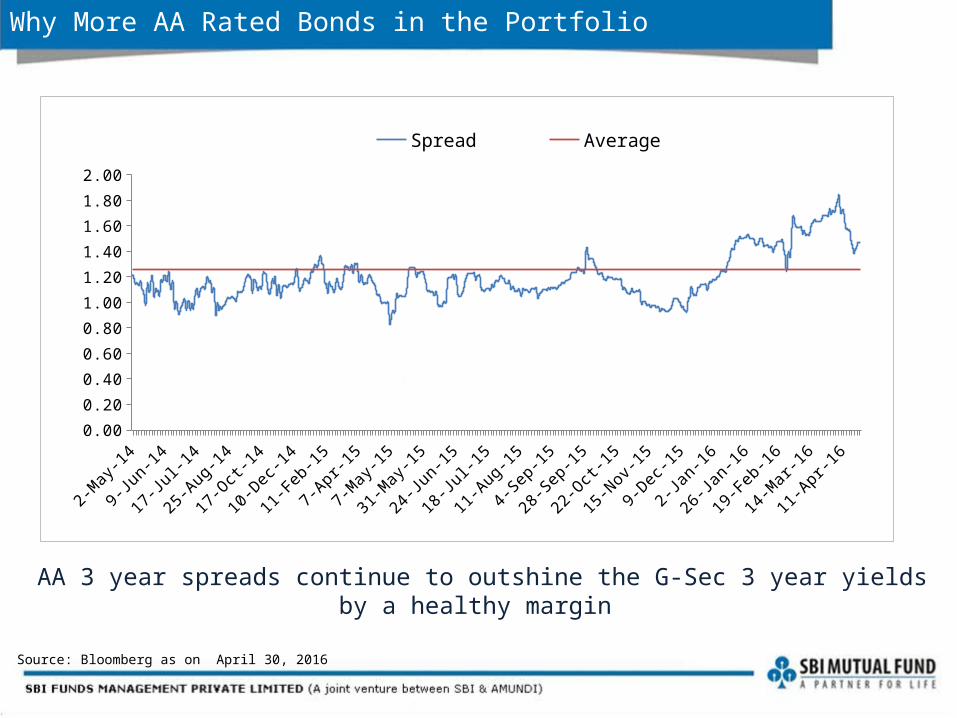

Why More AA Rated Bonds in the Portfolio

Source: Bloomberg as on April 30, 2016

AA 3 year spreads continue to outshine the G-Sec 3 year yields by a healthy margin

2-May-1

4

25-May-1

4

17-Jun-14

10-Jul-1

4

2-Aug-14

25-Aug-14

17-Sep-14

10-Oct-

14

2-Nov-1

4

25-Nov-1

4

18-Dec-1

4

10-Jan-15

2-Feb-15

25-Feb-15

20-Mar-1

5

12-Apr-15

5-May-1

5

28-May-1

5

20-Jun-15

13-Jul-1

5

5-Aug-15

28-Aug-15

20-Sep-15

13-Oct-

15

5-Nov-1

5

28-Nov-1

5

21-Dec-1

5

13-Jan-16

5-Feb-16

28-Feb-16

22-Mar-1

6

14-Apr-16

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

Spread Average

Investment Strategy

The fund aims to provide investors with yield spreads on corporate debt securities by cautiously managing the excess risk on its corporate investments. The fund will follow an active credit quality management strategy.

The scheme being open ended, some portion of the portfolio will be invested in money market instruments so as to meet the normal repurchase requirements. The remaining investments will be made in corporate debt securities which are either expected to be reasonably liquid or of varying maturities. However, the NAV of the Scheme may be impacted if the securities invested in are rendered illiquid after investment.

In line with the scheme objective we have deployed funds in 2 – 3 year corporate bonds with the primary focus on accrual. The portfolio average maturity is 2.96 years and the current weighted average portfolio yield is 9.26%.

Tactical exposure towards long AAA rated corporate bonds has been initiated with a positive bias on interest rates.

Credit Evaluation Mechanism

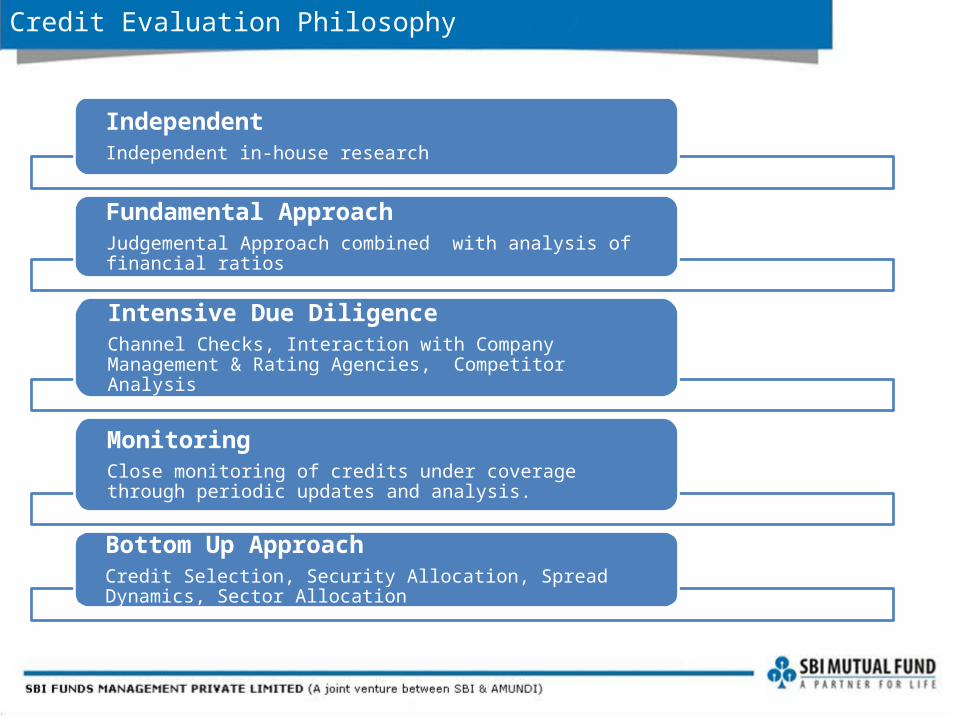

Credit Evaluation Philosophy

Independent Independent in-house research

Fundamental ApproachJudgemental Approach combined with analysis of financial ratios

Intensive Due Diligence Channel Checks, Interaction with Company Management & Rating Agencies, Competitor Analysis

Monitoring Close monitoring of credits under coverage through periodic updates and analysis.

Bottom Up Approach Credit Selection, Security Allocation, Spread Dynamics, Sector Allocation

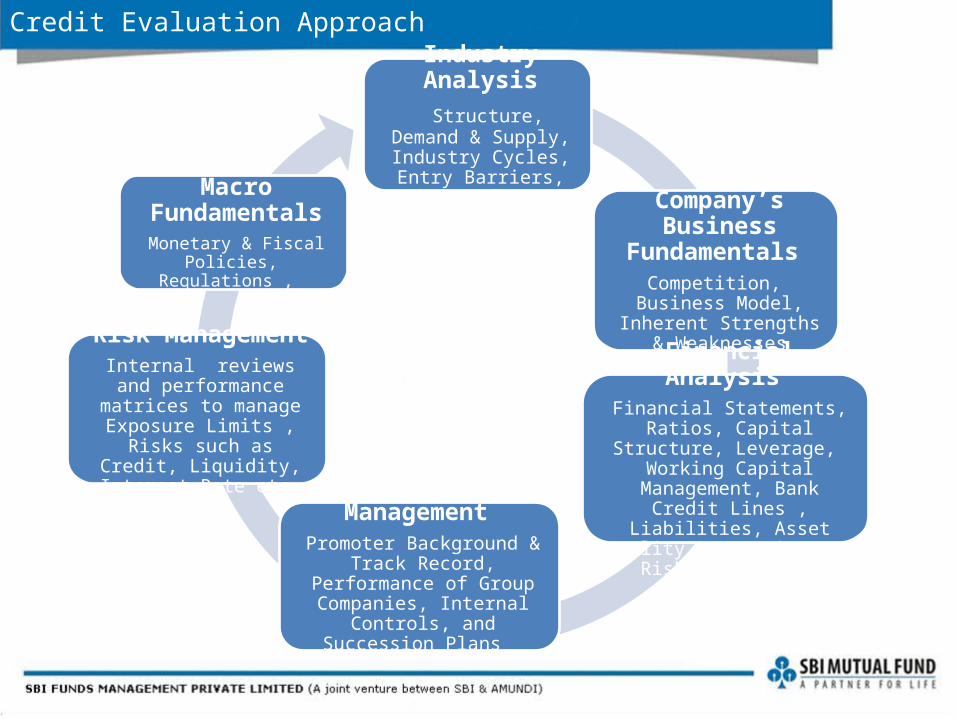

Industry Analysis Structure, Demand &

Supply, Industry Cycles, Entry Barriers, and

Outlook

Company’s Business Fundamentals

Competition, Business Model, Inherent Strengths

& Weaknesses

Financial Analysis Financial Statements, Ratios, Capital Structure, Leverage,

Working Capital Management, Bank Credit Lines , Liabilities, Asset Quality & Maturity and

Risk Management Management Promoter Background & Track Record, Performance of Group Companies, Internal Controls,

and Succession Plans

Risk ManagementInternal reviews and

performance matrices to manage Exposure Limits ,

Risks such as Credit, Liquidity, Interest Rate etc.

Macro Fundamentals

Monetary & Fiscal Policies, Regulations ,

Credit Evaluation Approach

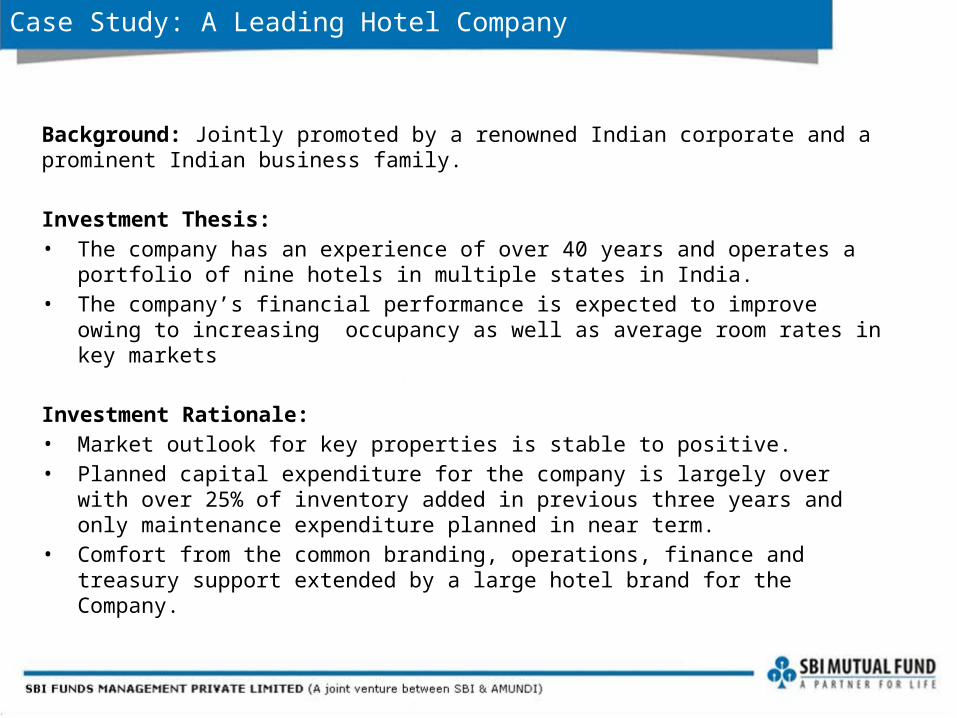

Case Study: A Leading Hotel Company

Background: Jointly promoted by a renowned Indian corporate and a prominent Indian business family.

Investment Thesis: • The company has an experience of over 40 years and operates a portfolio of nine hotels in

multiple states in India. • The company’s financial performance is expected to improve owing to increasing occupancy

as well as average room rates in key markets

Investment Rationale:• Market outlook for key properties is stable to positive. • Planned capital expenditure for the company is largely over with over 25% of inventory

added in previous three years and only maintenance expenditure planned in near term. • Comfort from the common branding, operations, finance and treasury support extended by a

large hotel brand for the Company.

Case Study: A Leading Infra Company

Background: • The company has a Build, Operate and Transfer (BOT) portfolio of 21 road projects

encompassing 5,000 lane km and spread across various states in India.

Investment Thesis: • 15 out of its portfolio of 21 projects are fully operational. • The company houses its road projects under two broad holding companies out of which one

was carved out with eight projects in its portfolio to enable a strategic stake sale to a fund sponsored by a PSU Bank.

• The PSU Bank Sponsored Fund holds around 35% in the said company.

Investment Rationale:• Key credit strengths are established track record in executing EPC contracts and BOT road

projects• Moderate financial leverage and working capital requirements and equity investment of Rs.

700 crore by the PSU Bank Sponsored Fund brings the holding company into the league of big BOT players being the exclusive platform for the Bank to bid for newer projects.

Synopsis

Attractiveness of AA & below securities in the improving credit situation. Sentiments in the bond markets have improved since the formation of a

stable and pro reform government at the centre.

Declining interest from foreign investors have been compensated by increasing interest from domestic institutions in the bond market. This inflow of funds will have an impact on the bond prices and may compress yields.

Declining inflation trajectory and the consistent rate cut by RBI. Its better to capitalise on the high corporate bond yields now.

About Us

17

Strong Indian Presence ; Extended International Reach

63% 37%

India’s premier and largest bank with over

200 years experience (Estd: 1806)

Asset base of USD 399 bn*

Pan-India network of ~22,635 branches and

~ 50,000 ATM’s as at end of June 2014

Servicing over 256 million customers

Only Indian bank in Fortune 500 list; ranked

among the top 100 banks in the world

Global leader in asset management

Backed by Credit Agricole and Société Générale

More than 2,000 institutional clients and distributors in

30 countries

Over 100 million retail clients via its partner networks

€ 866 bn AuM as at end of December 2014

Ranking N° 1 in Europe, Top 10 worldwide #

*Source: SBI Analyst Presentation as on end December 2014# Source : Amundi website as on end December 2014

18

Why SBIFM : Our Value Proposition

Group Advantage Process Expertise Risk Management

27 years of experience in asset management with a strong parentage

Leverage on strengths of both stakeholders to achieve qualitatively superior business

Extensive Distribution network and Strong Relationships with domestic and international investors

Structured and disciplined processes to ensure effective execution of strategies

Rigorous investment templates in place for each strategy

Flexibility to tailor solutions and advisory assignments

Proven expertise in managing strategies across asset classes

In-depth understanding of businesses and strong linkages with company managements and sell side analysts

Strong in-house research provides depth and breadth of coverage resulting in superior security selection

Strong six member independent team

Risk management aligned to international standards

Emphasis on coherence in risk monitoring

Mr. Navneet Munot - CIO Navneet Munot joined SBI Funds Management as Chief Investment Officer in December 2008. He brings

with him over 15 years of rich experience in Financial Markets. In his previous assignment, he was the Executive Director & Head - multi - strategy boutique with Morgan Stanley Investment Management. Prior to joining Morgan Stanley Investment Management, he worked as the CIO - Fixed Income and Hybrid Funds at Birla Sun Life Asset Management Company Ltd. Navneet had been associated with the financial services business of the group for over 13 years and worked in various areas such as fixed income, equities and foreign exchange. Navneet is a postgraduate in Accountancy and Business Statistics and a qualified Chartered Accountant. He is also a Charter holder of the CFA Institute USA and CAIA Institute USA. He is also an FRM Charter holder of Global Association of Risk Professionals (GARP).

Mr Rajeev Radhakrishnan – Head, Fixed Income Rajeev joined SBIFM as a fixed income portfolio manager in 2008. He currently heads the Fixed Income

desk at the AMC. Prior to joining SBIFM, Rajeev was Co-Fund Manager for Fixed Income with UTI Asset Management for seven years. Rajeev is an Engineering graduate and holds a Masters degree in finance from Mumbai University. He is also a charter holder of the CFA Institute, USA.

Mr. Dinesh Ahuja – Portfolio ManagerDinesh Ahuja joined SBIFM in 2010. Prior to joining SBIFM, Dinesh was a portfolio manager at L&T Asset Management and Reliance Group for four years. Dinesh started his career in 1998 as a fixed income dealer on the sell side. Thereafter he worked in leading broking outfits for eight years before moving on the buy side in 2006. Dinesh is a Commerce graduate and holds his Masters degree in Finance from Mumbai University.

Investments Team

Mr. Dinesh Balachandran - Head of Research Dinesh joined SBI FM in 2012 as a Senior Credit Analyst. He is now the Head of Research. Dinesh started

his career with Fidelity in Boston USA in 2001 where as an analyst he covered Structured Finance, and local US fixed income market over 10 years. Dinesh holds a B.Tech degree from IIT, Mumbai and M.S degree from Massachusetts Institute of Technology (MIT). He is also a Charter holder of the CFA Institute, USA.

Mr Lokesh Mallya - Credit Analyst Lokesh Mallya joined SBIFM in 2014. He brings along 9 years of experience in research in the Indian fixed

income market and fund management. Prior to joining SBIFM, Lokesh was working with Birla Sunlife Asset Management, Investment Team as fund manager for short term and ultra-short term funds. He is a Charter holder of the CFA Institute, USA and also a FRM charter holder of Global Association of Risk Professionals (GARP).

Ms Mansi Sajeja - Credit Analyst Mansi Sajeja joined SBIFM in 2009. Prior to joining SBIFM Mansi was a senior analyst at ICRA Ltd. for over

three years. Mansi holds bachelor’s degree in Financial & Investment analysis from Delhi University and has completed post graduation diploma in Business Management from MDI, Gurgaon. She is also a Charter holder of the CFA Institute, USA.

Credit Analysis Team

Disclaimer

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

This presentation is for information purposes only and is not an offer to sell or a solicitation to buy any mutual fund units/securities. These views alone are not sufficient and should not be used for the development or implementation of an investment strategy. It should not be construed as investment advice to any party. All opinions and estimates included here constitute our view as of this date and are subject to change without notice. Neither SBI Funds Management Private Limited, nor any person connected with it, accepts any liability arising from the use of this information. The recipient of this material should rely on their investigations and take their own professional advice

SBI Funds Management Private Limited(A joint venture between SBI and AMUNDI)

Registered Office:9th Floor, Crescenzo, C-38 & 39, ‘G’ Block,Bandra Kurla Complex, Bandra (E), Mumbai - 400 051

Board line: +91 22 61793000Fax: +91 22 67425687

Call: 1800 425 5425

SMS: “SBIMF” to 56161

Email: [email protected]

Visit us @ www.facebook.com/SBIMF

www.sbimf.com Website

Visit us @ www.youtube.com/user/sbimutualfund