Embed Size (px)

Citation preview

WS Atkins plc

Interim results for the six months ended

30 September 2009

25 November 2009

1

Summary

Results

Resilience

Growth

• Successful navigation of turbulent markets

• End market diversity

• Continuing investment in skills and capabilities

Heath Drewett

Group Finance Director

3

Financial highlights

30 Sep 2009 30 Sep 2008

Revenue £701.2 m £710.8 m (1)%

Operating profit £51.1 m £48.2 m 6 %

Operating margin 7.3 % 6.8 % 50 bp

Operating margin * 6.9 % 6.8 % 10 bp

Profit before tax * £40.9 m £47.5 m (14)%

Fully diluted eps * 31.6 p 36.4 p (13)%

Dividend per share 9.25 p 8.75 p 6 %

Work in hand 90 % 87 % Good

30 Sep 2009 31 Mar 2009

Headcount 16,235 18,017 (10)%

Net funds £230.6 m £234.2 m

* excluding pension gain in 2009 and JV disposal in 2008

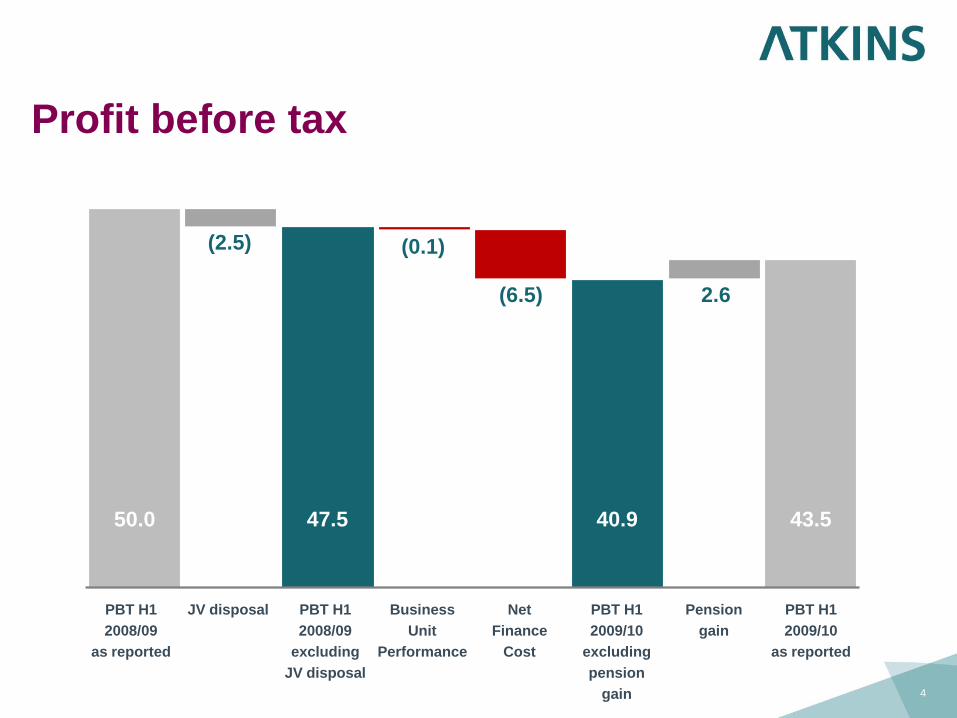

Profit before tax

4

PBT H1

2008/09

as reported

PBT H1

2009/10

as reported

Business

Unit

Performance

Net

Finance

Cost

PBT H1

2009/10

excluding

pension

gain

Pension

gain

50.0 40.9 43.5

2.6(6.5)

(0.1)

PBT H1

2008/09

excluding

JV disposal

JV disposal

47.5

(2.5)

5

Design and Engineering Solutions

30 Sep 2009 30 Sep 2008

Revenue (£m) 197.1 202.6 (3)%

Operating profit (£m) 13.0 16.9 (23)%

Operating margin 6.6 % 8.3 % (170)bp

Work in hand 88 % 87 % Good

Average headcount 4,820 5,057 (5)%

30 Sep 2009 31 Mar 2009

Headcount 4,616 5,167 (11)%

• Defence, Nuclear and Oil & Gas markets good

• Challenges in Water and UK building design markets as expected

• Operating profit includes reorganisation/redundancy costs of c.£2m

• Near term outlook good following restructuring

6

Highways and Transportation

30 Sep 2009 30 Sep 2008

Revenue (£m) 143.4 138.0 4 %

Operating profit (£m) 12.0 8.4 43 %

Operating margin 8.4 % 6.1 % 230 bp

Work in hand 93 % 86 % Very Good

Average headcount 2,967 2,937 1 %

30 Sep 2009 31 Mar 2009

Headcount 2,935 3,075 (5 )%

• Good performance – M25 DBFO progressing well

• Secure workload in highways services – success in Somerset and Gloucester

• Strong demand in transport planning and design

• Full year outlook good

7

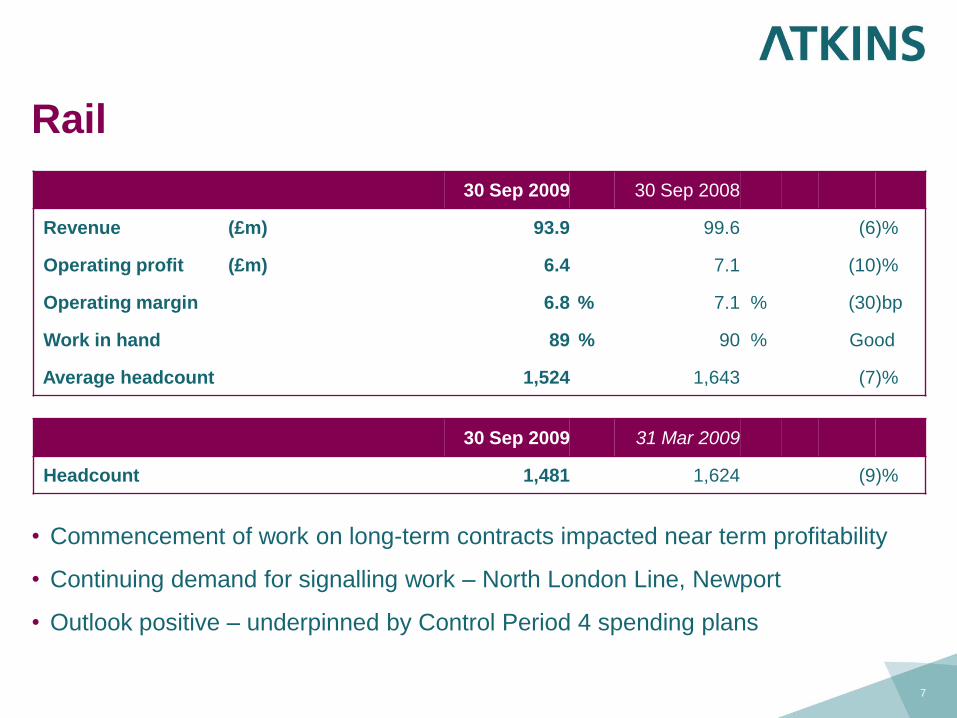

Rail

30 Sep 2009 30 Sep 2008

Revenue (£m) 93.9 99.6 (6)%

Operating profit (£m) 6.4 7.1 (10)%

Operating margin 6.8 % 7.1 % (30)bp

Work in hand 89 % 90 % Good

Average headcount 1,524 1,643 (7)%

30 Sep 2009 31 Mar 2009

Headcount 1,481 1,624 (9 )%

• Commencement of work on long-term contracts impacted near term profitability

• Continuing demand for signalling work – North London Line, Newport

• Outlook positive – underpinned by Control Period 4 spending plans

8

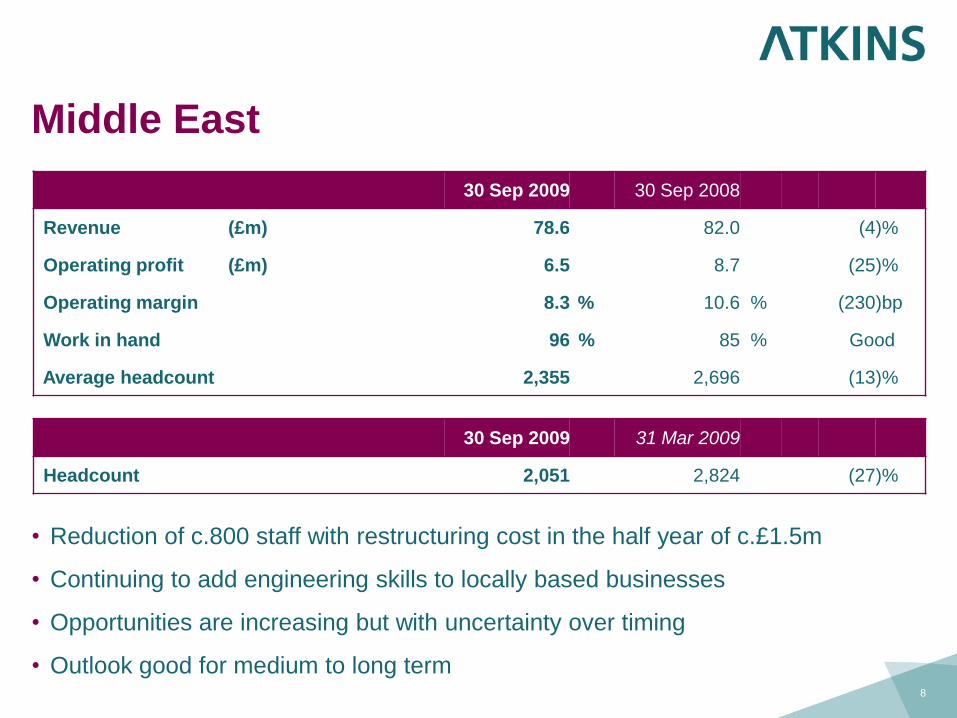

Middle East

30 Sep 2009 30 Sep 2008

Revenue (£m) 78.6 82.0 (4)%

Operating profit (£m) 6.5 8.7 (25)%

Operating margin 8.3 % 10.6 % (230)bp

Work in hand 96 % 85 % Good

Average headcount 2,355 2,696 (13)%

30 Sep 2009 31 Mar 2009

Headcount 2,051 2,824 (27 )%

• Reduction of c.800 staff with restructuring cost in the half year of c.£1.5m

• Continuing to add engineering skills to locally based businesses

• Opportunities are increasing but with uncertainty over timing

• Outlook good for medium to long term

9

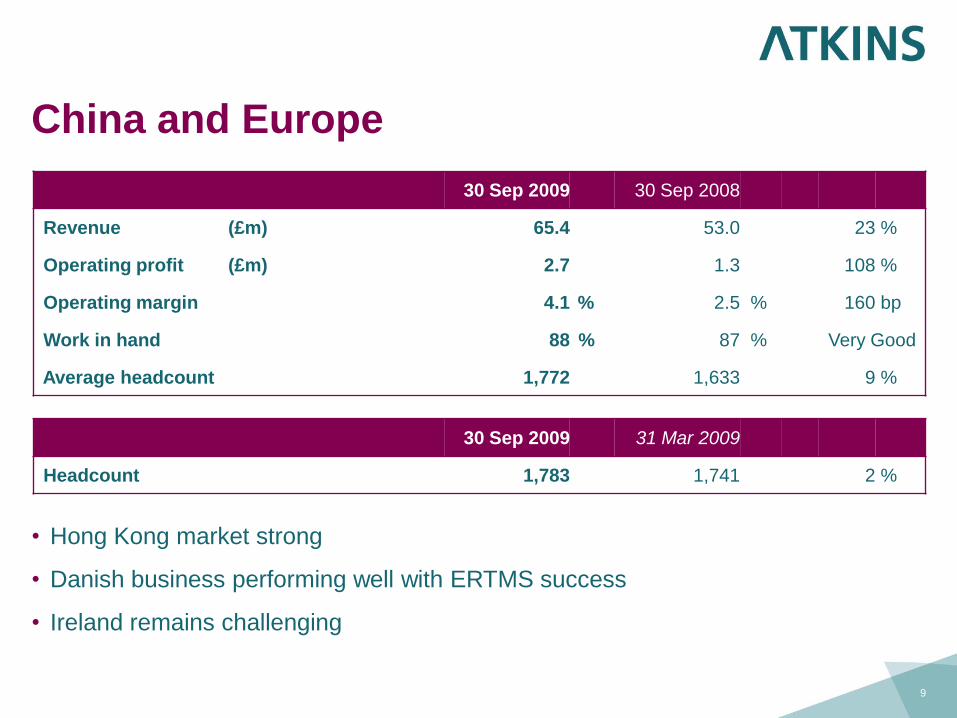

China and Europe

30 Sep 2009 30 Sep 2008

Revenue (£m) 65.4 53.0 23 %

Operating profit (£m) 2.7 1.3 108 %

Operating margin 4.1 % 2.5 % 160 bp

Work in hand 88 % 87 % Very Good

Average headcount 1,772 1,633 9 %

30 Sep 2009 31 Mar 2009

Headcount 1,783 1,741 2 %

• Hong Kong market strong

• Danish business performing well with ERTMS success

• Ireland remains challenging

10

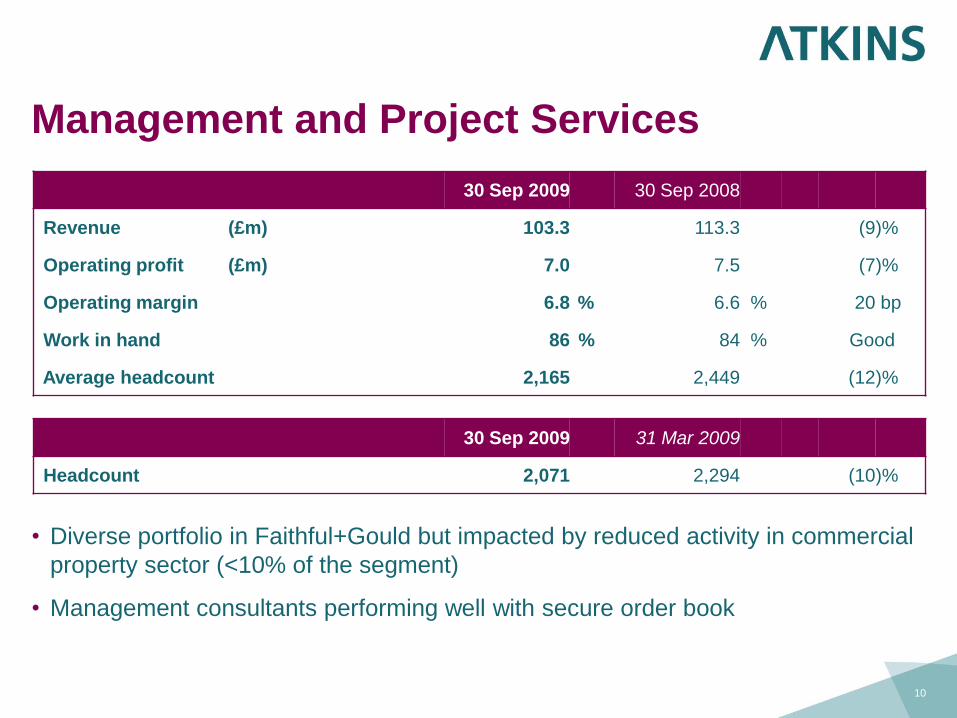

Management and Project Services

30 Sep 2009 30 Sep 2008

Revenue (£m) 103.3 113.3 (9)%

Operating profit (£m) 7.0 7.5 (7)%

Operating margin 6.8 % 6.6 % 20 bp

Work in hand 86 % 84 % Good

Average headcount 2,165 2,449 (12)%

30 Sep 2009 31 Mar 2009

Headcount 2,071 2,294 (10 )%

• Diverse portfolio in Faithful+Gould but impacted by reduced activity in commercial

property sector (<10% of the segment)

• Management consultants performing well with secure order book

11

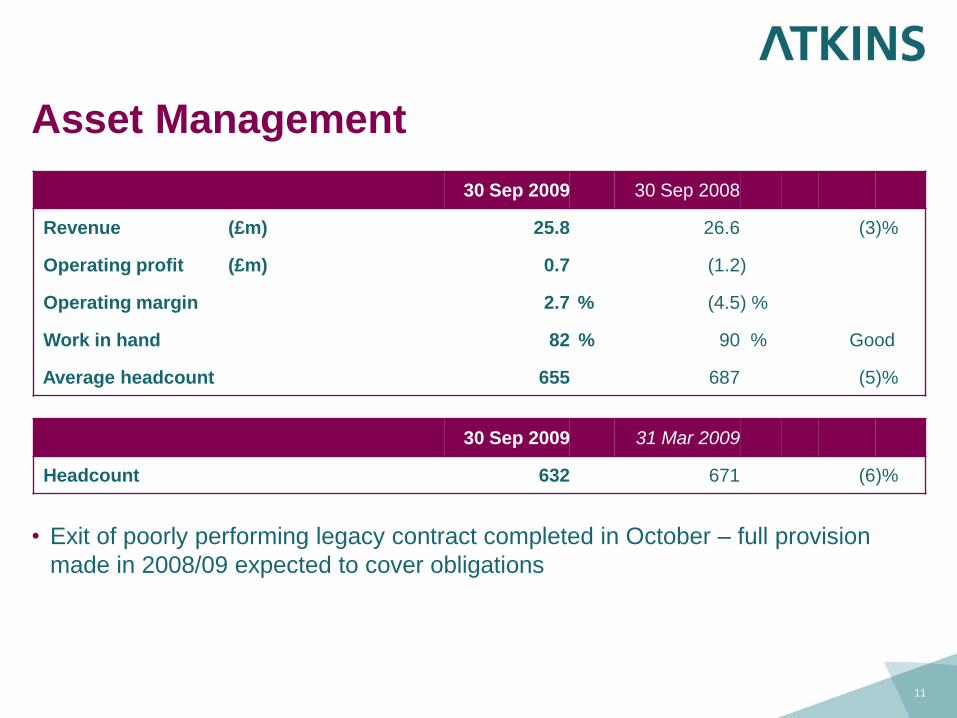

Asset Management

30 Sep 2009 30 Sep 2008

Revenue (£m) 25.8 26.6 (3)%

Operating profit (£m) 0.7 (1.2)

Operating margin 2.7 % (4.5) %

Work in hand 82 % 90 % Good

Average headcount 655 687 (5)%

30 Sep 2009 31 Mar 2009

Headcount 632 671 (6 )%

• Exit of poorly performing legacy contract completed in October – full provision

made in 2008/09 expected to cover obligations

12

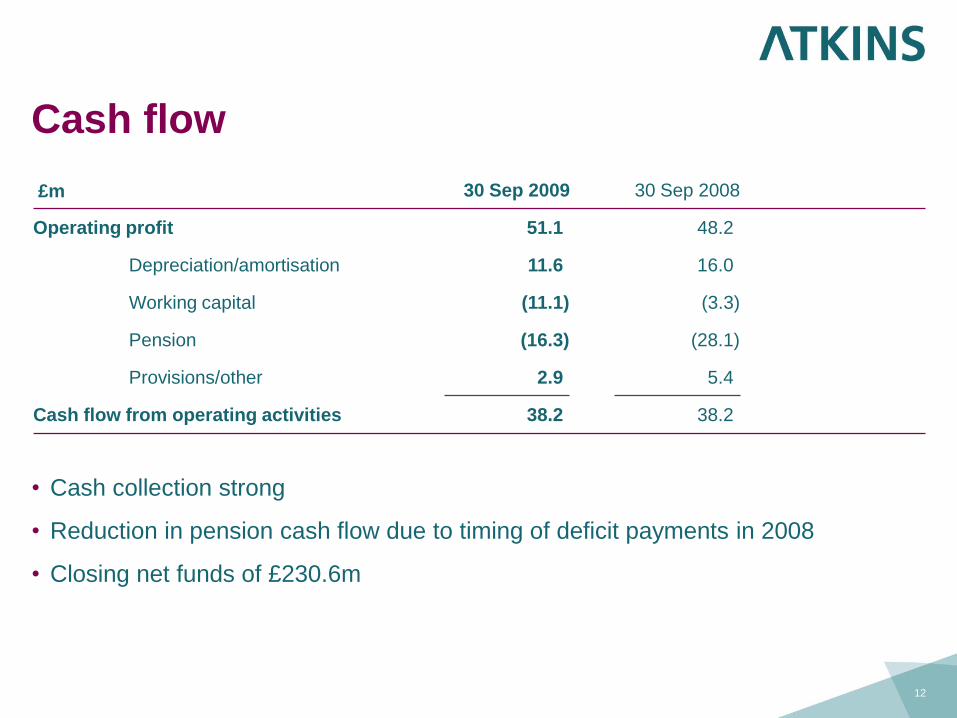

Cash flow

£m 30 Sep 2009 30 Sep 2008

Operating profit 51.1 48.2

Depreciation/amortisation 11.6 16.0

Working capital (11.1) (3.3)

Pension (16.3) (28.1)

Provisions/other 2.9 5.4

Cash flow from operating activities 38.2 38.2

• Cash collection strong

• Reduction in pension cash flow due to timing of deficit payments in 2008

• Closing net funds of £230.6m

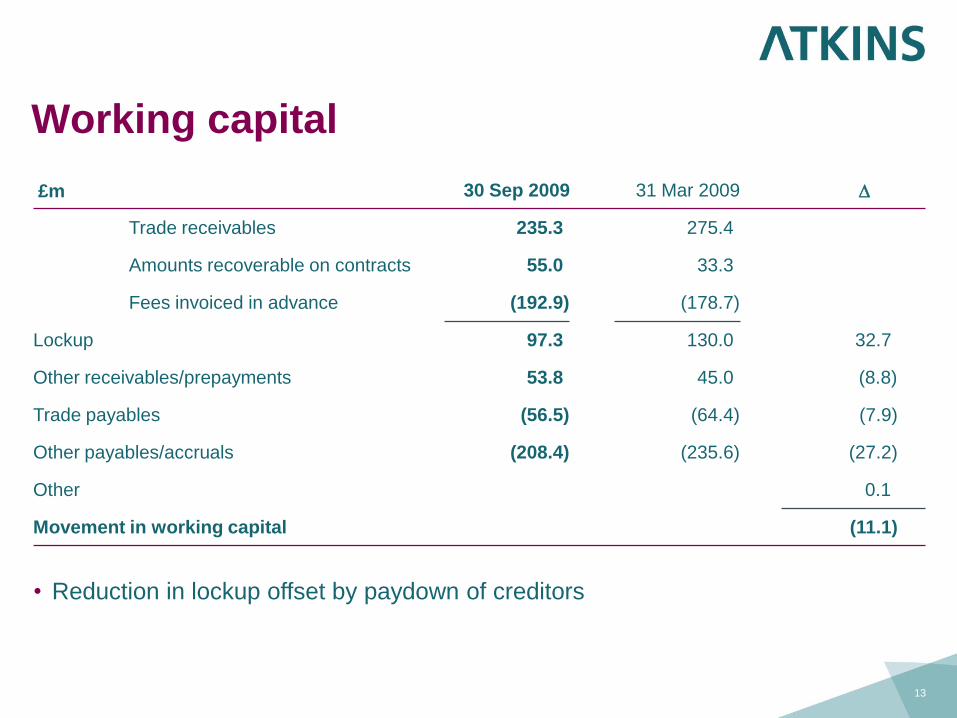

Working capital

13

£m 30 Sep 2009 31 Mar 2009 D

Trade receivables 235.3 275.4

Amounts recoverable on contracts 55.0 33.3

Fees invoiced in advance (192.9) (178.7)

Lockup 97.3 130.0 32.7

Other receivables/prepayments 53.8 45.0 (8.8)

Trade payables (56.5) (64.4) (7.9)

Other payables/accruals (208.4) (235.6) (27.2)

Other 0.1

Movement in working capital (11.1)

• Reduction in lockup offset by paydown of creditors

14

• IAS19 deficit increase due to decrease in discount rate from 6.3% to 5.3% despite

increase in value of scheme assets

• £16m deficit funding in first half year in line with agreed funding plan

• Next actuarial valuation due as at 1 April 2010

Pension

£m Gross Net of def tax

Net deficit at 1 April 2009 (298.4) (215.4)

Service cost (3.0)

Net finance cost (7.5)

Contributions 19.2

Actuarial loss (131.2)

Other 2.6

Net deficit at 30 September 2009 (418.3) (301.6)

Results summary

• Improving margin

• Generating cash

• Increased interim dividend

15

Keith Clarke

Chief Executive

17

Overview

Results

Resilience

Growth

• Successful navigation of turbulent markets

• End market diversity

• Continuing investment in skills and capabilities

0%

1%

2%

3%

4%

5%

6%

7%

8%

0

20

40

60

80

100

120

140

2004 2005 2006 2007 2008 2009 2010

£m

Year ended 31 March

Full year operating profit

First half operating profit

Full year operating margin

Margin progression

18

19

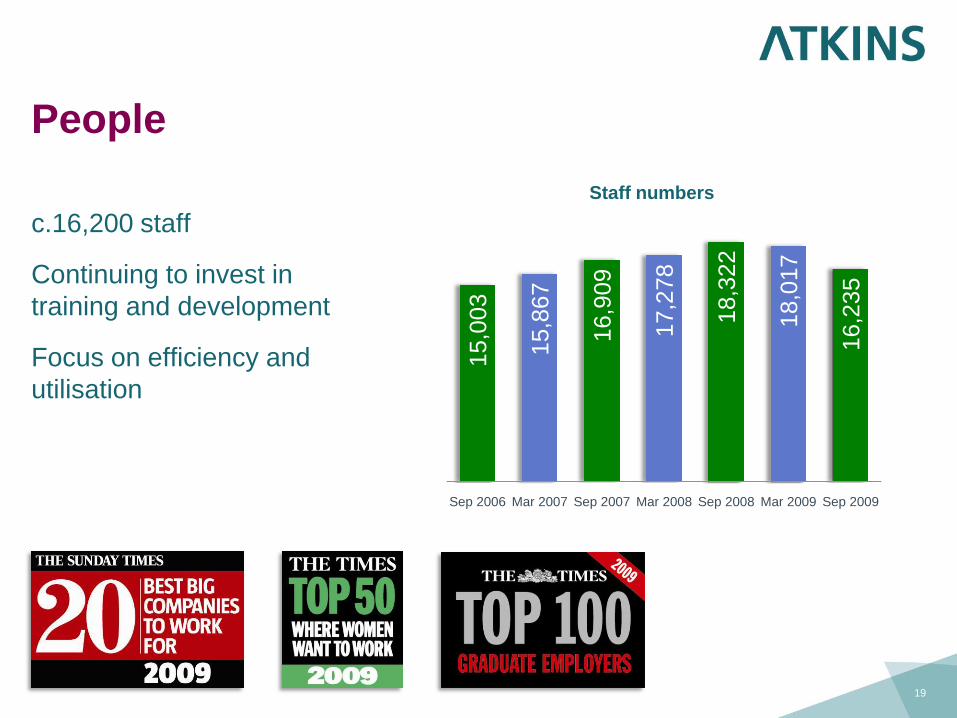

People

c.16,200 staff

Continuing to invest in

training and development

Focus on efficiency and

utilisation

15,0

03

15,8

67

16,9

09

17,2

78

18,3

22

18,0

17

16,2

35

Sep 2006 Mar 2007 Sep 2007 Mar 2008 Sep 2008 Mar 2009 Sep 2009

Staff numbers

88%93%

89%96%

88%86%

82%

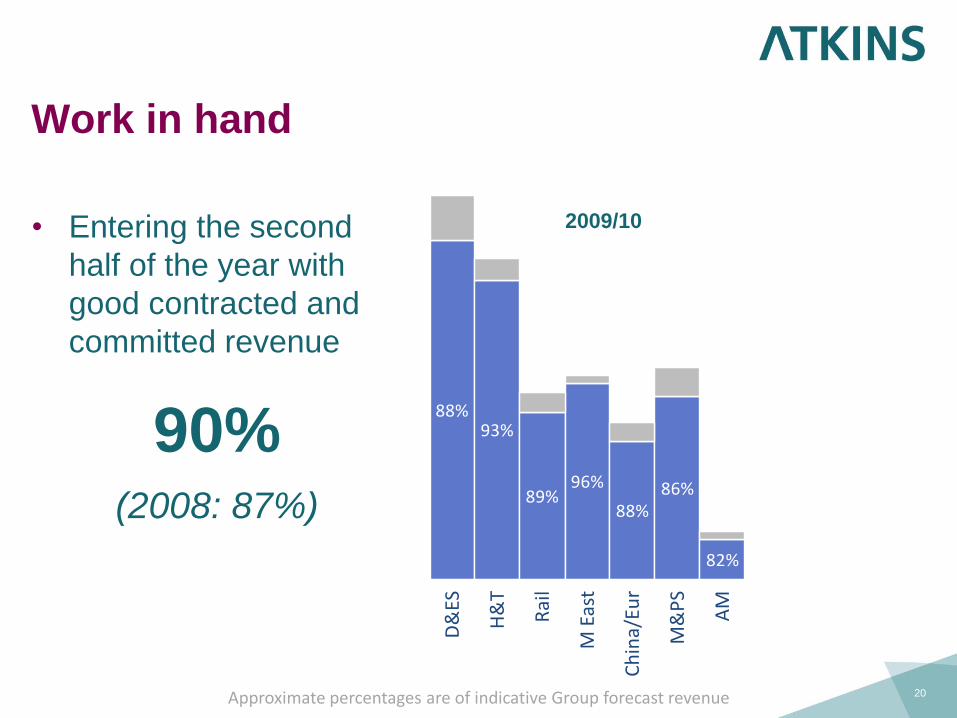

Work in hand

• Entering the second

half of the year with

good contracted and

committed revenue

20

D&

ES

H&

T

Rai

l

M E

ast

Ch

ina/

Eur

M&

PS

AM

2009/10

Approximate percentages are of indicative Group forecast revenue

90%(2008: 87%)

Resilience

• Diversified exposure to end markets

• Strong Group

– Scale

– Breadth

– Cash resources

– Higher end activity

– Adjacencies / skill transfer

• Market demands work on existing as well as new

infrastructure

21

22

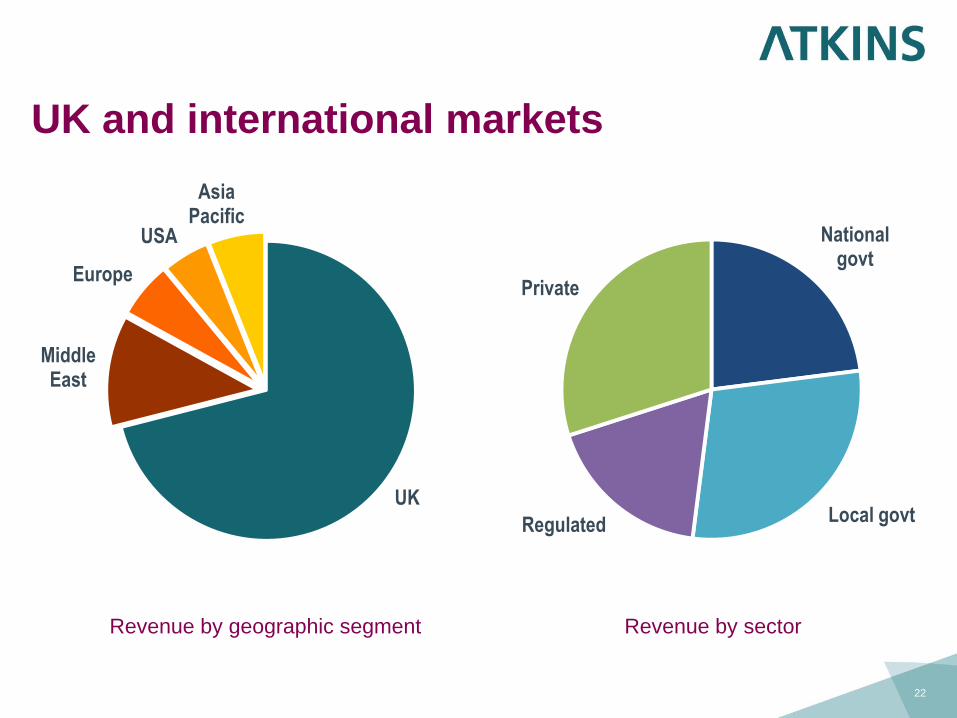

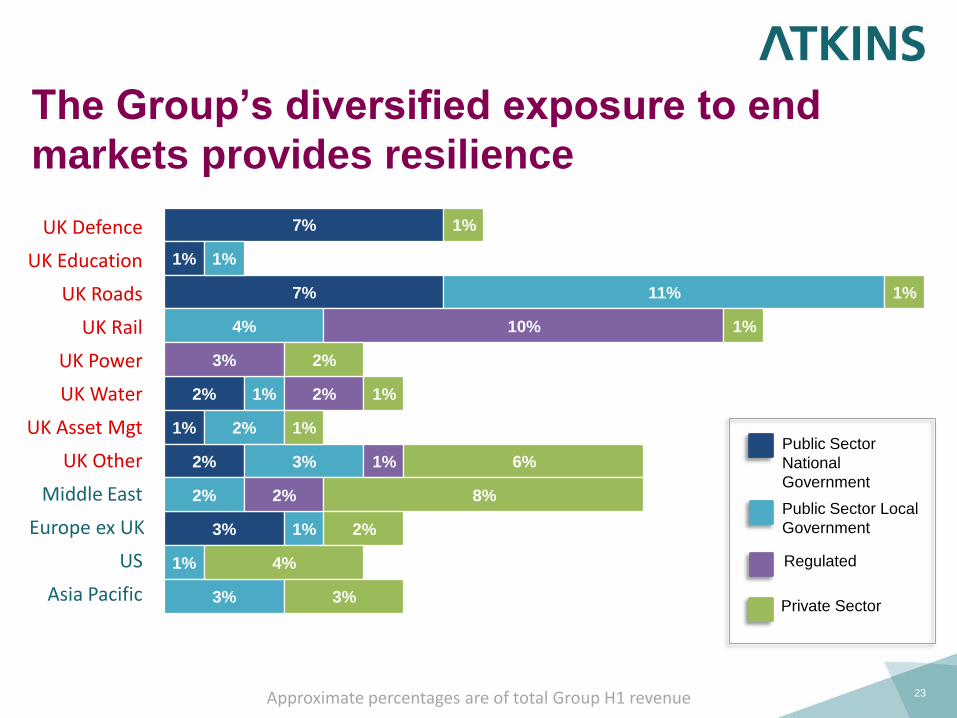

UK and international markets

UK

Middle East

Europe

USA

Asia Pacific

National govt

Local govtRegulated

Private

Revenue by geographic segment Revenue by sector

7%

1%

7%

2%

1%

2%

3%

1%

11%

4%

1%

2%

3%

2%

1%

1%

3%

10%

3%

2%

1%

2%

1%

1%

1%

2%

1%

1%

6%

8%

2%

4%

3%

The Group’s diversified exposure to end

markets provides resilience

23

Public Sector

National

Government

Public Sector Local

Government

Regulated

Private Sector

UK Roads

UK Rail

UK Power

UK Water

UK Defence

UK Education

UK Other

UK Asset Mgt

Middle East

Europe ex UK

US

Asia Pacific

Approximate percentages are of total Group H1 revenue

24

Middle East

• Confident liquidity slowly

returning

• Infrastructure opportunities

• Adding skills

• The region remains

attractive

Qatar

Dubai

Oman

Kuwait /

India

Revenue by market

Bahrain

Abu Dhabi

Sharjah

25

Rest of the world

Europe

• Expanding capabilities in Scandinavia

• Ireland remains challenging

USA

• Cost consulting stable

• Oil & Gas steady

Asia Pacific

• Hong Kong opportunities especially in transport

• Mainland China performing in line with expectations

Future development

• Exceptional people and management

• Focussing on quality

• Addressing attractive markets

– Renewables

– Nuclear

– Mass transit

• Taking advantage of opportunities by adding

technical/niche skills in good markets

26

27

Conclusion

Results

Resilience

Growth

• Successful navigation of turbulent markets

• End market diversity

• Continuing investment in skills and capabilities

Confidence in Group’s position and strategy

WS Atkins plc

Interim results for the six months ended

30 September 2009

25 November 2009

Appendices

UK End Market analysis

Net funds reconciliation

DEFENCE

UK Public Sector – National government

30

ROADS WATER

• M25, M74, A14

• Area 6 MAC (to 2013)

• Intelligent Transport

Systems

• Long term contracts

• RSME (to 2013)

• Environment Agency

• Carbon Agenda

7%7% 2%

Approximate percentages are of total Group H1 revenue

Roads

Rail

Power

Water

Defence

Education

Other

Asset Mgt

7%

7%

1%

1%

2%

2%

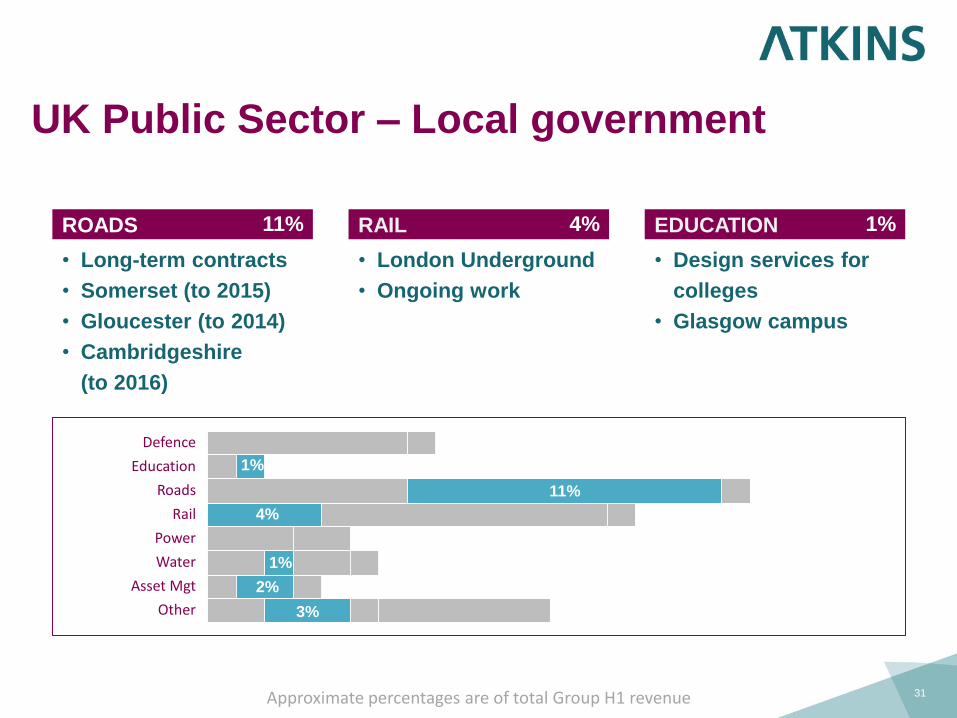

UK Public Sector – Local government

31

EDUCATION

• Design services for

colleges

• Glasgow campus

1%

Approximate percentages are of total Group H1 revenue

RAILROADS

• Long-term contracts

• Somerset (to 2015)

• Gloucester (to 2014)

• Cambridgeshire

(to 2016)

• London Underground

• Ongoing work

4%11%

Roads

Rail

Power

Water

Defence

Education

Other

Asset Mgt

4%

11%

1%

2%

1%

3%

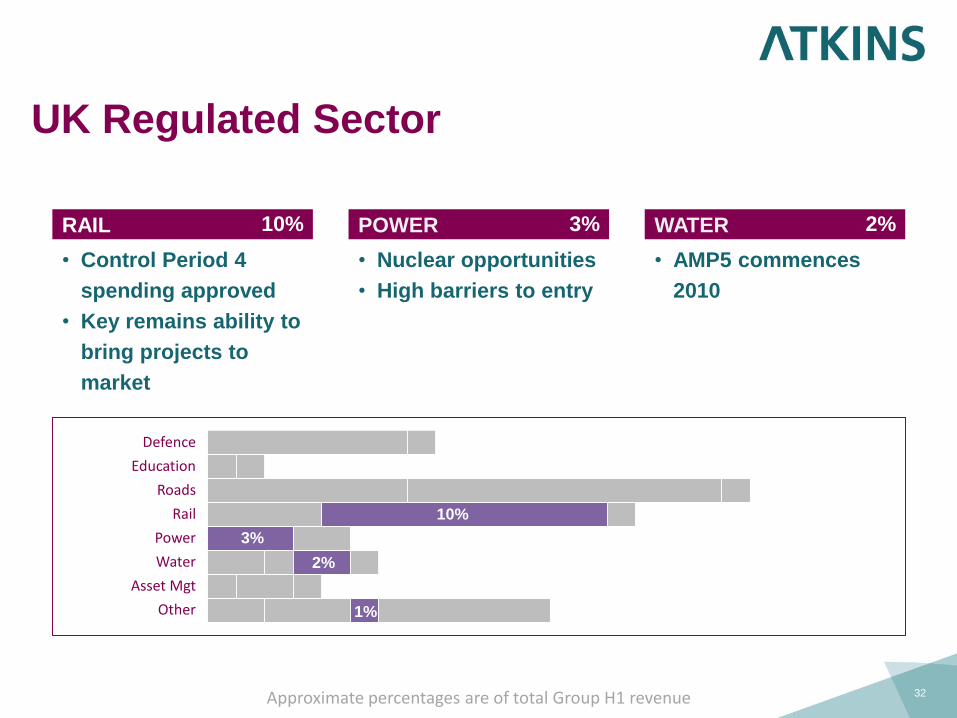

UK Regulated Sector

32

WATER

• AMP5 commences

2010

2%

Approximate percentages are of total Group H1 revenue

POWERRAIL

• Control Period 4

spending approved

• Key remains ability to

bring projects to

market

• Nuclear opportunities

• High barriers to entry

3%10%

Roads

Rail

Power

Water

Defence

Education

Other

Asset Mgt

10%

3%

2%

1%

UK Private Sector

33

OTHER

• Airbus programmes

in aerospace sector

• Cost management for

financial services /

pharma

6%

Approximate percentages are of total Group H1 revenue

ROADSPOWER

• Oil & gas portfolio of

clients and

continuing demand

• Technical support on

projects for private

sector clients

1%2%

Roads

Rail

Power

Water

Defence

Education

Other

Asset Mgt

1%

2%

1%

1%

1%

6%

1%

£m CashLoan notes

< 1yr

Loan notes

> 1yr

Financial

assets

Borrowings

< 1yr

Borrowings

> 1yr

Leases

< 1yr

Leases

> 1yrNet funds

Operating profit 51.1 51.1

Depreciation/amortisation 11.6 11.6

Working capital (11.1) (11.1)

Pension (16.3) (16.3)

Provisions / other 2.9 2.9

Cashflow from operating activities 38.2 38.2

Net interest 0.8 0.8

Tax (9.3) (9.3)

Net capital expenditure (3.5) (3.5)

26.2 26.2

Dividends (16.7) (16.7)

Net cash flow 9.5 9.5

Non-operating items Foreign Exchange (5.9) (13.1)

EBT share sales (7.2)

Financing - I Discount unwind - 0.2 (0.1) -

Transfer - 6.2 (6.2) (0.6) 0.6 (2.1) 2.1

New leases - (0.1)

Financing - II Investments (4.6) 4.6

Financial assets (8.4) 8.4 -

Borrowings - short term (0.4) 0.4

Leases : principal (2.9) 2.9

Movement (19.9) 6.2 (1.4) 8.4 (0.3) 0.6 0.7 2.1 (3.6)

Opening balance 209.7 - 12.9 28.7 (2.8) (0.6) (4.8) (8.9) 234.2

Closing balance 189.8 6.2 11.5 37.1 (3.1) - (4.1) (6.8) 230.6

Net funds reconciliation

35

Disclaimer

The information in this presentation pack which does not

purport to be comprehensive has been provided by Atkins,

and has not been independently verified. While this

information has been prepared in good faith, no representation

or warranty, express or implied, is or will be made and no

responsibility or liability is or will be accepted by Atkins, as to

or in relation to the accuracy or completeness of this

presentation pack or any other written or oral information

made available as part of the presentation and any such

liability is expressly disclaimed. Further, whilst Atkins may

subsequently update the information made available in this

presentation, we expressly disclaim any obligation to do so.