Embed Size (px)

Citation preview

WS Atkins plcWoodcote GroveAshley RoadEpsomSurrey KT18 5BWEngland

Telephone +44 (0)1372 726140Fax +44 (0)1372 740055

The paper used in this report is sourced from sustainable forests, is totally chlorine free (TCF), and contains 50% recycled fibre. Designed and produced by College Design, London +44 (0)20 7457 2020

WS Atkins plcInterim Report 2003

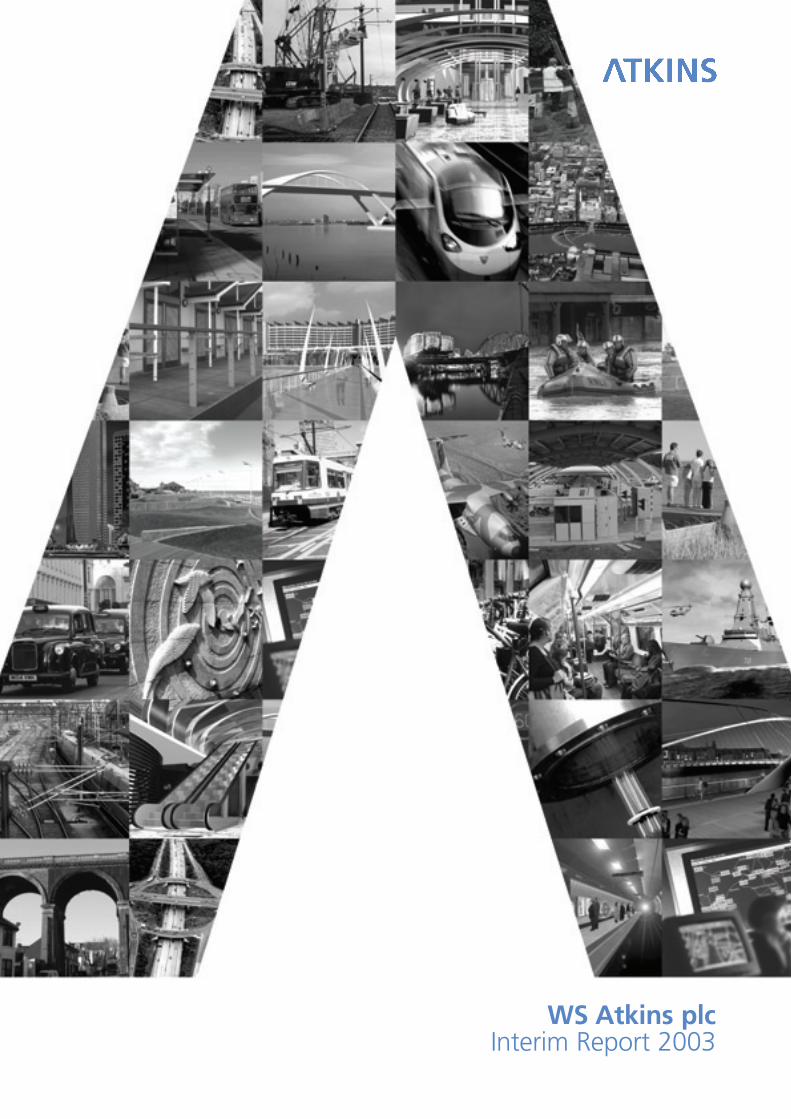

From left to right: Keith Clarke, Chief Executive, Stephen Billingham, Group Finance Director and Michael Jeffries, Chairman.

Segmental overview

Transport Equity InvestmentsDesign andEngineering Solutions

Management and Project Services

Turnover £131.3mOperating profit £5.0m

Design, Environment andEngineering (DE2)Industry

Turnover £194.9mOperating profit £12.4mJoint venture PBT £0.2m

RailHighways & Transportation

Turnover £109.3mOperating profit £3.0m

Management ConsultantsFaithful & GouldAsset ManagementProject Development

Turnover £26.5mOperating profit £0.2mJoint venture PBT £8.9m

MetronetLambert Smith Hampton Other joint ventures

Financial summarySix months to Six months to Year to30 Sept 2003 30 Sept 2002 31 March 2003

Turnover (excl Joint Ventures) £503.4m £449.2m £935.3m

Operating margin on continuing operations 4.5% (0.2)% 2.4%

Adjusted profit/(loss) before tax(a), (c) £23.8m £(2.5)m £18.7m

Operating profit/(loss) £26.6m £(11.6)m £(35.7)m

Profit/(loss) before tax £17.8m £(32.8)m £(61.6)m

Basic EPS 10.8p (36.2)p (58.7)p

Adjusted EPS(a) 17.6p (5.0)p 16.5p

Dividend 2.0p – 3.0p

Cashflow from operations £10.2m £(45.0)m £26.6m

Net debt(b) £26.1m £105.4m £71.9m

a) Before Metronet bid costs, amortisation of pension deficit/surplus, amortisation of goodwill, exceptional items and EBTs.b) Excluding cash held in the EBTs and on behalf of sub-contractors.c) The Directors consider that Adjusted Profit is a fairer reflection of the ongoing performance of the Group.

Front coverThese images reflect some of the range and diversity of projects undertaken by Atkins. They include refurbishment of London Underground; design of Glasgow’s newpedestrian footbridge; rejuvenation of the sea front at Hornsea; development of the Airbus A400M military transport plane; a revolutionary water treatment technology;design of the new M6 Toll Road; and creation of a state-of-the-art support centre for the Royal Navy.

01WS Atkins plc Interim Report 2003

OverviewI am pleased to report results for the Group that show a return tohealthier levels of profit and cash generation after the difficultiesof last year. Our focus on cost reduction, margin improvementand cash generation has produced good first half results. Adjustedprofit of £23.8m compares with a loss of £2.5m for the sameperiod last year. Better cash collection has enabled us to generatea cash inflow from operations in the first half of the year of£10.2m (2002 £45.0m outflow) against the Group’s historic trendof cash outflow and we expect this pattern to continue in thefuture. In addition, the disposal of Atkins Americas Holdings Inc(formerly Benham) and the reimbursement of Metronet bid costsand development fees enabled the Group to reduce net debt to£26.1m compared with £71.9m at 31 March 2003 and £105.4mat 30 September 2002.

Turnover from continuing operations rose from £399.9m to£462.0m. This was due to modest organic growth (5%), workgenerated from the Metronet PPP companies (3%), an increase inrevenues on existing framework contracts (5%) and the inclusionof a full half year’s turnover from Hanscomb (acquired in June2002) (3%).

We have continued to win new work on better terms which givesus confidence that we will be able to achieve our goal of a returnto historic margins. I would like to thank our clients for theirconfidence in the Group through the difficulties of last year. Thissupport, coupled with the expertise and commitment of our staff,has allowed the Group to re-establish its financial performance.

Adjusted profit before tax for the half year to 30 September 2003was £23.8m, an increase of £26.3m compared with the sameperiod last year. This turnaround reflects the strength of the Group’s core businesses, a reduction in the Group’s cost base andthe elimination of significant loss-making contracts and low margin activities. The Group’s operating margin on continuingoperations before Joint Ventures was 4.5% (2002: (0.2)%; full year 2002/03: 2.4%), an improvement upon last year and goodprogress towards achieving the Group’s margin objective.

We are also reporting for the first time results from the MetronetPPP companies which have performed broadly in line withexpectations. Included within adjusted profit before tax is theGroup’s interest in, and the results of the Group’s trading with, the Metronet PPP companies:

Metronet Six months to30 Sept 2003

£m

Metronet PPP companies 3.7Supply chain and other fees (including Trans4m Ltd ) 2.5Costs of letters of credit to support equity commitments (2.2)

4.0

During the first half of the year, the Group disposed of AtkinsAmericas Holdings Inc. We have also recently announced thedisposal of the Group’s interest in the Connect Roads PFIs andtoday announce the disposal of its interest in the companyestablished to undertake the Telkom South Africa facilitiesmanagement contract.

PensionsAn updated actuarial assessment of the principal defined benefitpension schemes was undertaken for the Group during the firsthalf of the year. This update indicated that the principal staffscheme had an actuarial deficit of approximately £65m at 30 September 2003. To take account of the change in thescheme’s position the pension charge for the half year includedwithin adjusted profit has increased by £1.8m and the credit toamortise the previous surplus (2002: £1.9m) has been replaced by a charge to amortise the estimated deficit (£1.6m). The Groupcontinues to account for pension costs under SSAP 24.

The actuaries indicated that additional annual cash contributions of £7m could be required from April 2004. The Group is reviewingways in which our cost can be reduced.

Financial performance

Six months to Six months to 30 Sept 2003 30 Sept 2002

£m £m

Turnover (excl Joint Ventures):– Continuing operations 462.0 399.9 – Discontinued operations 41.4 49.3

503.4 449.2 Turnover from Joint Ventures 99.0 37.8

602.4 487.0

Segmental operating profit/(loss) for the period:

– Continuing operations 20.6 (0.7)– Discontinued operations (1.1) (2.8)

19.5 (3.5)Share of Joint Ventures profit before tax 9.1 5.7 Net interest payable and financing charges (3.4) (1.4)PFI bid costs (excluding Metronet) (1.4) (3.3)

Adjusted profit/(loss) before tax 23.8 (2.5)Metronet bid costs – (3.5)Amortisation of pension (deficit)/surplus (1.6) 1.9 Amortisation of goodwill (3.4) (5.3)Exceptional items 0.9 (21.8)Employee Benefit Trusts (1.9) (1.6)

Profit/(loss) before tax 17.8 (32.8)

Cash flow from operations 10.2 (45.0)

Chairman’s statement

02 WS Atkins plc Interim Report 2003

CashThe Group has continued to focus on improving its cash position and has made substantial progress. The cashflow from operations in the first half year was a net inflow of £10.2m compared with anoutflow of £45.0m in the first half of last year.

Combined with the cash received from disposals (£13.0m) andreimbursement of Metronet bid costs and development fees(£20.1m), the Group has reduced net debt significantly since 31 March 2003. At 30 September 2003 net debt was £26.1m, down from £71.9m at 31 March 2003 and £105.4m at 30 September 2002.

Segmental reviewThe continuing businesses have been consolidated into the following major segments: Transport; Design and EngineeringSolutions; and Management and Project Services, supported byEquity Investments. This allows a smaller and more focused seniormanagement team to improve co-operation and skills transfer within Atkins and will improve the quality of service to our clients.Operating profits from the major segments have improvedsignificantly compared with the first half of last year.

The results of Joint Ventures in which the Group has day to daymanagement involvement are included within the relevant business segment. Results of all other Joint Ventures are included as part of Equity Investments.

Discontinued operations include Education Services (principally theSouthwark contract) and the Group’s interest in Atkins AmericasHolding Inc.

TransportTransport now includes our specialist rail consultancy, AtkinsDanmark, which was previously included within the formerInternational segment.

Six months to Six months to30 Sept 2003 30 Sept 2002

£m £m

Turnover (excl Joint Ventures) 194.9 161.6Operating profit 12.4 3.2Operating margin 6.4% 2.0%Joint Venture profit before tax 0.2 –

RailThe Rail business has had a strong first half year. We continue tosupport Network Rail on a number of important projects includingthe West Coast Main Line. The recent announcement by NetworkRail to take maintenance activities back in house will not affect ourworkload as we do not undertake this type of contract.

In the first half of the year we have been awarded a number ofimportant contracts including the Manchester South Safety Case and Civil Engineering Consultancy for Midland Metro Phase 2.

Our Metronet supply chain contract continues to build momentumthrough the Trans4m Ltd supply chain Joint Venture. The focus inTrans4m Ltd has been on survey and design of the early stationrefurbishments. Work on site is due to commence early in 2004 and performance to date is broadly in line with expectations.

Highways & TransportationThis has been a good half year for Highways & Transportation. The Highways Agency’s £7bn acceleration of the roads programme is providing new opportunities. Working in partnership withInterserve, we have won the first Early Contractor Involvementpackaged scheme of its type.

The Somerset Highways Partnership between Atkins and SomersetCounty Council was launched in July. Our integrated highways services contract with Northamptonshire County Council wasexpanded to incorporate work from Northampton Borough Council.

Our Transport Planning business continues to lead the way intransport policy research and advice. An Atkins led consortium recently secured a three year commission to evaluate the impact of Local Transport Plans. We have also been appointed to the Scottish Executive’s five year framework contract covering the fullrange of services required to plan, design, procure and supervise trunk road improvement schemes.

Design and Engineering SolutionsThe Design and Engineering Solutions segment delivers design,environment and engineering services, engineering basedconsultancy and project management to a wide range of public and private clients.

Six months to Six months to30 Sept 2003 30 Sept 2002

£m £m

Turnover (excl Joint Ventures) 131.3 120.3Operating profit 5.0 (2.7)Operating margin 3.8% (2.2)%

Chairman’s statement continued

03WS Atkins plc Interim Report 2003

Design, Environment & EngineeringDesign, Environment & Engineering’s strategy of entering intonational framework contracts, increasing involvement in largerprojects and improving margins has been successful in the first half of the year.

We have been awarded the design of the North Liverpool CityAcademy which will be a significant feature when Liverpool becomes European City of Culture in 2008. Our work on major PFI projects continues with both consulting and design to in-houseand external PFI bidders. Our Environmental business is providingtechnical policy and strategic advice to the Environment Agency.Using our own NoiseMap software we are creating a noise map of London.

In mainland China we are involved in a number of development and regeneration plans. A landmark project has been the design ofThames Town, a new town development in Shanghai. Our businessin the United Arab Emirates is the leading provider of consultancy for high rise buildings. Complete design and site supervision services have been provided for the 21st Century Building justcompleted in Dubai which, at 269 metres, is the world’s tallest all-residential building.

IndustryIn the first half of the year Industry has focused on key clients in our core business areas and target markets. We have exited low margin and non-core business areas and significantly cut costs.The improvements to ongoing operating margins are alreadyreflected although the first half year has been impacted by one-offcosts, reducing the reported margin.

The Industry businesses are now all well positioned. Regulation and environmental pressures influence the markets in the Water and Power businesses. Expansion of our oil and gas consultancy activities based in Houston and Paris will create new opportunities.The developing relationships with clients such as the Ministry ofDefence and Airbus Industries are delivering growth in high valuespecialist engineering services.

Management and Project ServicesManagement and Project Services encompasses a range of activitiesdelivering management and IT consultancy, cost and programmemanagement and whole life cycle asset services to clients in thepublic and private sectors.

Six months to Six months to30 Sept 2003 30 Sept 2002

£m £m

Turnover (excl Joint Ventures) 109.3 82.8Operating profit 3.0 (3.2)Operating margin 2.7% (3.9)%

Management ConsultantsManagement Consultants provides clients with the skills andresources to manage complex programmes of business change. In the first half of the year the business has continued to focus on performance improvement and cost reduction resulting inimproved operating margins.

We have been awarded a three-year contract to provide a CorporateTraining Programme at the Defence Science and TechnologyLaboratory which will be delivered in partnership with the LeedsUniversity Business School.

Faithful & Gould (F&G)F&G has had a number of notable successes including projects for HM Prison Service, the 2012 Olympic Bid Team and Halifax Bank of Scotland (HBOS). The integration of the Hanscomb and F&Gbusinesses in the US provides greater support to selected clients and we expect steady growth in the US.

Cost consulting and associated services for the Group are nowmanaged by F&G, including Hanscomb Faithful & Gould in the US.

Asset ManagementProgress has been made to improve the performance of the AssetManagement business. Some unprofitable contracts have beenexited and improved margins have been negotiated on extensions to existing contracts.

We have won the facilities management contract for two newDiagnostic and Treatment Centres for the NHS, secured additionalwork on the commission for Cambridgeshire County Council and a major early works programme for Colchester Borough Council.

Project DevelopmentProject Development was previously included in our PFI division. The major bid teams will now function separately looking at a variety of procurement opportunities with and without equity investments.

Our focus in the first half of the year has been on achieving progresstowards financial close on Colchester Garrison and optimising thereturns from the current portfolio.

04 WS Atkins plc Interim Report 2003

Discontinued operationsOn 9 September 2003, we announced the sale of our USbusiness, Atkins Americas Holdings Inc. for $17.5m in cash. Underthe terms of the sale agreement the Group retained contingentliabilities in the form of performance bonds for two existingprojects. One project has now reached construction completionand the warranty period will expire by the end of November 2004.Construction completion on the second project is imminent andits warranty period will expire twelve months later.

Our involvement in Education Services (principally the LondonBorough of Southwark contract) ceased in August 2003.

DividendThe Board has declared an interim dividend of 2p per share whichwill be paid on 30 January 2004 to shareholders on the register on 5 January 2004. The Board has considered its dividend policyand, in particular, the importance of having earnings backed bycash. Earnings from Joint Ventures including the Metronet PPPcompanies and other material PFI/PPP type investments will,therefore, only be included in our calculation of dividend coverwhere they are matched by cash. Accordingly, the Board wishes to see a progression towards a dividend that is around 2.5 timescovered by cash-backed earnings before amortisation of goodwill.

Board I am pleased to report that Keith Clarke took up the post of Chief Executive on 1 October 2003.

OutlookCash generation and margin improvement remain our focus.Performance in the second half of the year continues in line withour expectations. The markets for our core services in the UKcontinue to be strong and are expected to remain so. We are now well placed to take advantage of these opportunities.

Michael JeffriesChairman 2nd December 2003

Chairman’s statement continued

Equity investmentsThe Equity Investments segment includes Lambert Smith Hamptonand holds the Group’s interests in our PFI/PPP investments and other associates.

Six months to Six months to30 Sept 2003 30 Sept 2002

£m £m

Turnover (excl Joint Ventures) 26.5 35.2Operating profit 0.2 2.0Operating margin 0.8% 5.7%Joint Venture profit before tax 8.9 5.7

Lambert Smith Hampton (LSH)The results of LSH were impacted by a difficult environment withinthe commercial property market. The outlook is more favourablewith signs of increased activity although conditions are expected to remain challenging in London and the South East.

MetronetSteady progress has been made to implement the changes necessary to achieve enhanced levels of performance. The MetronetPPP companies have operated broadly in line with expectations.

In the first six months Metronet has focused on improving theavailability of the railway systems through better maintenance and has put in place new contracts for the cleaning of trains andstations. The shareholder supply chain contracts for the multi billionpound capital investment programmes have been mobilised and we currently have c.300 staff across Atkins participating in this work. Construction is due to start in the new year of a number of stations for which we are currently undertaking the design,including Oxford Circus.

In recognition of the importance of Metronet to the Group, wereview and discuss progress at each Board meeting. Shortly, we will also be assigning a senior Atkins executive to a full time role overseeing the Group’s involvement in Metronet.

Other Joint VenturesThe results of other Joint Ventures included a strong performance in the first half year from our Connect Roads PFIs.

We have previously indicated that it is the Group’s intention to recycle capital invested in mature PFI investments at the appropriatetime and on 21 November 2003 the Group announced that it haddisposed of its interest in Connect Roads for £13.3m in cash.

The Group announced today that it has disposed of its interest inAtkins Rebserve (Proprietary) Ltd (‘AtReb’). AtReb has an interest in TFMC (Proprietary) Ltd, which was the company established toundertake the Telkom South Africa facilities management contract.

05WS Atkins plc Interim Report 2003

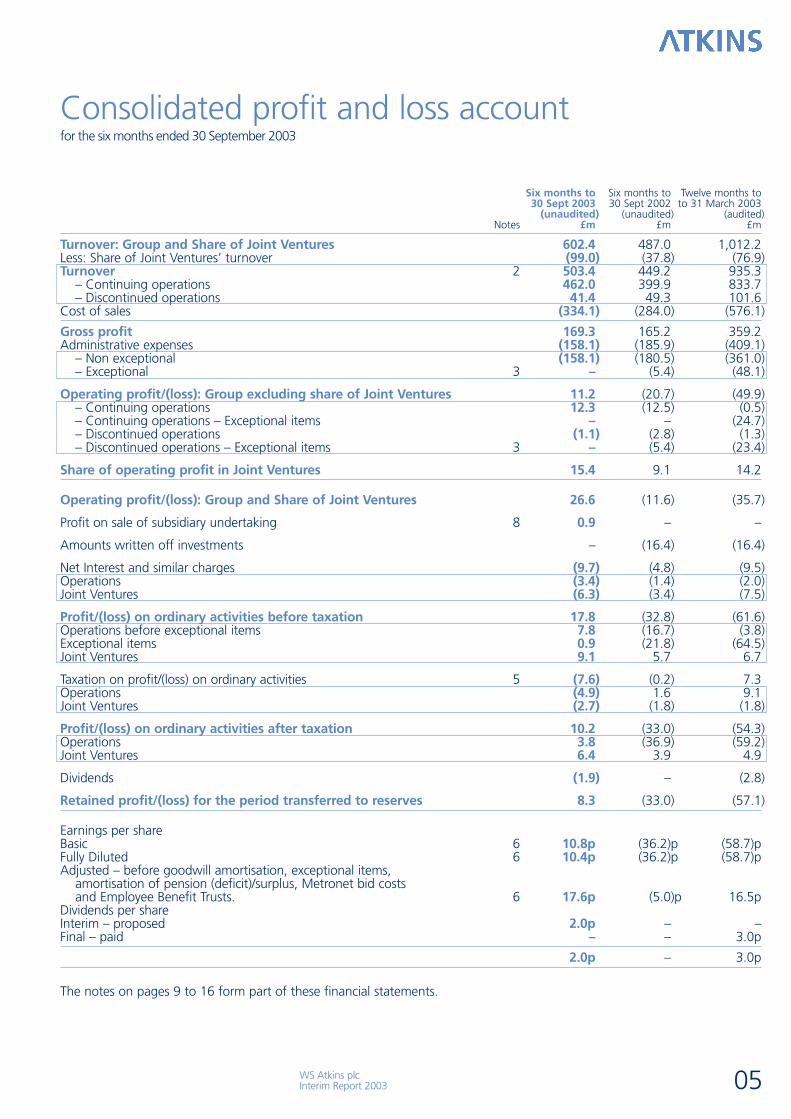

Consolidated profit and loss account for the six months ended 30 September 2003

Six months to Six months to Twelve months to 30 Sept 2003 30 Sept 2002 to 31 March 2003

(unaudited) (unaudited) (audited)Notes £m £m £m

Turnover: Group and Share of Joint Ventures 602.4 487.0 1,012.2Less: Share of Joint Ventures’ turnover (99.0) (37.8) (76.9)Turnover 2 503.4 449.2 935.3

– Continuing operations 462.0 399.9 833.7– Discontinued operations 41.4 49.3 101.6

Cost of sales (334.1) (284.0) (576.1)

Gross profit 169.3 165.2 359.2Administrative expenses (158.1) (185.9) (409.1)

– Non exceptional (158.1) (180.5) (361.0)– Exceptional 3 – (5.4) (48.1)

Operating profit/(loss): Group excluding share of Joint Ventures 11.2 (20.7) (49.9)– Continuing operations 12.3 (12.5) (0.5)– Continuing operations – Exceptional items – – (24.7)– Discontinued operations (1.1) (2.8) (1.3)– Discontinued operations – Exceptional items 3 – (5.4) (23.4)

Share of operating profit in Joint Ventures 15.4 9.1 14.2

Operating profit/(loss): Group and Share of Joint Ventures 26.6 (11.6) (35.7)

Profit on sale of subsidiary undertaking 8 0.9 – –

Amounts written off investments – (16.4) (16.4)

Net Interest and similar charges (9.7) (4.8) (9.5)Operations (3.4) (1.4) (2.0)Joint Ventures (6.3) (3.4) (7.5)

Profit/(loss) on ordinary activities before taxation 17.8 (32.8) (61.6)Operations before exceptional items 7.8 (16.7) (3.8)Exceptional items 0.9 (21.8) (64.5)Joint Ventures 9.1 5.7 6.7

Taxation on profit/(loss) on ordinary activities 5 (7.6) (0.2) 7.3Operations (4.9) 1.6 9.1Joint Ventures (2.7) (1.8) (1.8)

Profit/(loss) on ordinary activities after taxation 10.2 (33.0) (54.3)Operations 3.8 (36.9) (59.2)Joint Ventures 6.4 3.9 4.9

Dividends (1.9) – (2.8)

Retained profit/(loss) for the period transferred to reserves 8.3 (33.0) (57.1)

Earnings per share Basic 6 10.8p (36.2)p (58.7)pFully Diluted 6 10.4p (36.2)p (58.7)pAdjusted – before goodwill amortisation, exceptional items,

amortisation of pension (deficit)/surplus, Metronet bid costs and Employee Benefit Trusts. 6 17.6p (5.0)p 16.5p

Dividends per share Interim – proposed 2.0p – –Final – paid – – 3.0p

2.0p – 3.0p

The notes on pages 9 to 16 form part of these financial statements.

06 WS Atkins plc Interim Report 2003

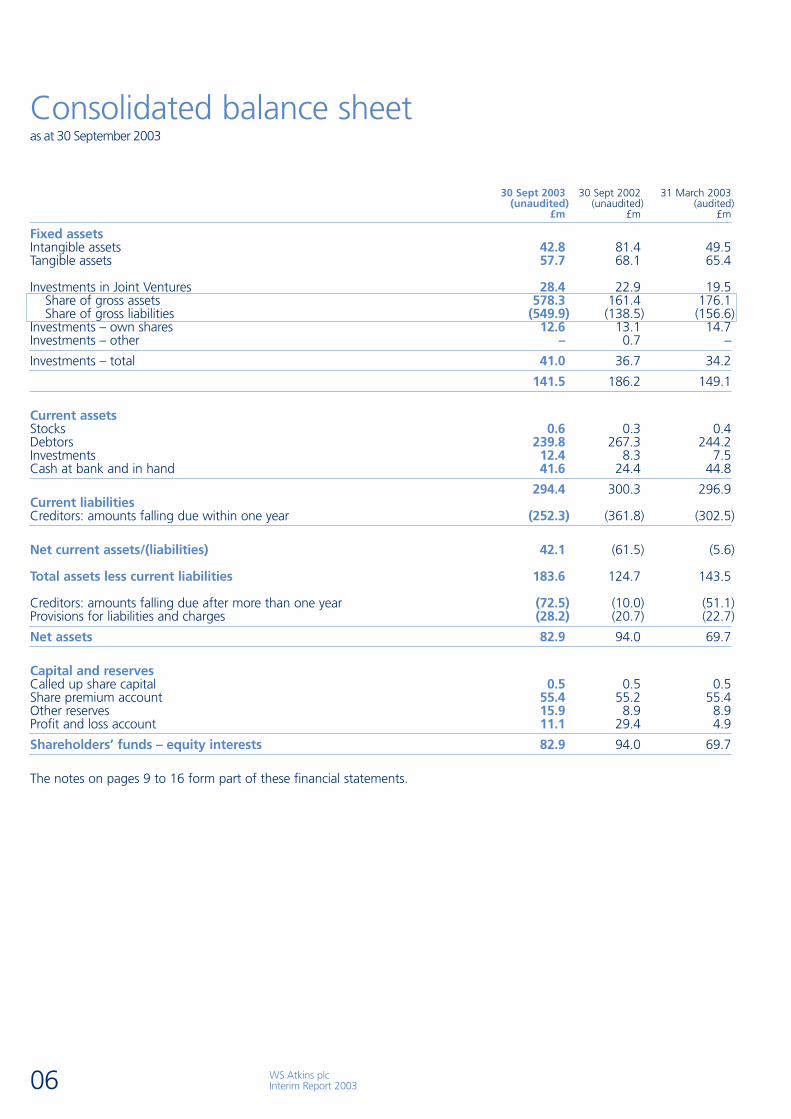

Consolidated balance sheet as at 30 September 2003

30 Sept 2003 30 Sept 2002 31 March 2003(unaudited) (unaudited) (audited)

£m £m £m

Fixed assetsIntangible assets 42.8 81.4 49.5 Tangible assets 57.7 68.1 65.4

Investments in Joint Ventures 28.4 22.9 19.5 Share of gross assets 578.3 161.4 176.1 Share of gross liabilities (549.9) (138.5) (156.6)

Investments – own shares 12.6 13.1 14.7 Investments – other – 0.7 –

Investments – total 41.0 36.7 34.2

141.5 186.2 149.1

Current assetsStocks 0.6 0.3 0.4 Debtors 239.8 267.3 244.2 Investments 12.4 8.3 7.5 Cash at bank and in hand 41.6 24.4 44.8

294.4 300.3 296.9 Current liabilitiesCreditors: amounts falling due within one year (252.3) (361.8) (302.5)

Net current assets/(liabilities) 42.1 (61.5) (5.6)

Total assets less current liabilities 183.6 124.7 143.5

Creditors: amounts falling due after more than one year (72.5) (10.0) (51.1)Provisions for liabilities and charges (28.2) (20.7) (22.7)

Net assets 82.9 94.0 69.7

Capital and reservesCalled up share capital 0.5 0.5 0.5 Share premium account 55.4 55.2 55.4 Other reserves 15.9 8.9 8.9 Profit and loss account 11.1 29.4 4.9

Shareholders’ funds – equity interests 82.9 94.0 69.7

The notes on pages 9 to 16 form part of these financial statements.

07WS Atkins plc Interim Report 2003

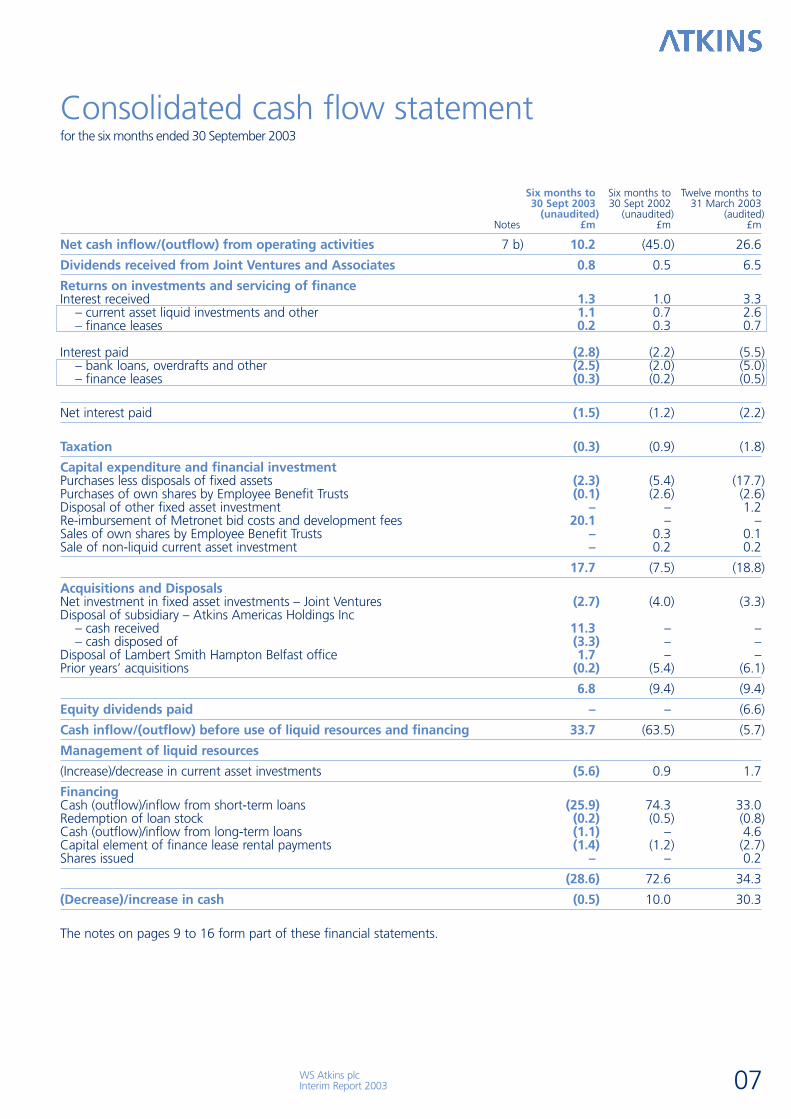

Consolidated cash flow statement for the six months ended 30 September 2003

Six months to Six months to Twelve months to30 Sept 2003 30 Sept 2002 31 March 2003

(unaudited) (unaudited) (audited)Notes £m £m £m

Net cash inflow/(outflow) from operating activities 7 b) 10.2 (45.0) 26.6

Dividends received from Joint Ventures and Associates 0.8 0.5 6.5

Returns on investments and servicing of financeInterest received 1.3 1.0 3.3

– current asset liquid investments and other 1.1 0.7 2.6 – finance leases 0.2 0.3 0.7

Interest paid (2.8) (2.2) (5.5)– bank loans, overdrafts and other (2.5) (2.0) (5.0)– finance leases (0.3) (0.2) (0.5)

Net interest paid (1.5) (1.2) (2.2)

Taxation (0.3) (0.9) (1.8)

Capital expenditure and financial investmentPurchases less disposals of fixed assets (2.3) (5.4) (17.7)Purchases of own shares by Employee Benefit Trusts (0.1) (2.6) (2.6)Disposal of other fixed asset investment – – 1.2 Re-imbursement of Metronet bid costs and development fees 20.1 – – Sales of own shares by Employee Benefit Trusts – 0.3 0.1 Sale of non-liquid current asset investment – 0.2 0.2

17.7 (7.5) (18.8)

Acquisitions and DisposalsNet investment in fixed asset investments – Joint Ventures (2.7) (4.0) (3.3)Disposal of subsidiary – Atkins Americas Holdings Inc

– cash received 11.3 – – – cash disposed of (3.3) – –

Disposal of Lambert Smith Hampton Belfast office 1.7 – – Prior years’ acquisitions (0.2) (5.4) (6.1)

6.8 (9.4) (9.4)

Equity dividends paid – – (6.6)

Cash inflow/(outflow) before use of liquid resources and financing 33.7 (63.5) (5.7)

Management of liquid resources

(Increase)/decrease in current asset investments (5.6) 0.9 1.7

FinancingCash (outflow)/inflow from short-term loans (25.9) 74.3 33.0 Redemption of loan stock (0.2) (0.5) (0.8)Cash (outflow)/inflow from long-term loans (1.1) – 4.6 Capital element of finance lease rental payments (1.4) (1.2) (2.7)Shares issued – – 0.2

(28.6) 72.6 34.3

(Decrease)/increase in cash (0.5) 10.0 30.3

The notes on pages 9 to 16 form part of these financial statements.

08 WS Atkins plc Interim Report 2003

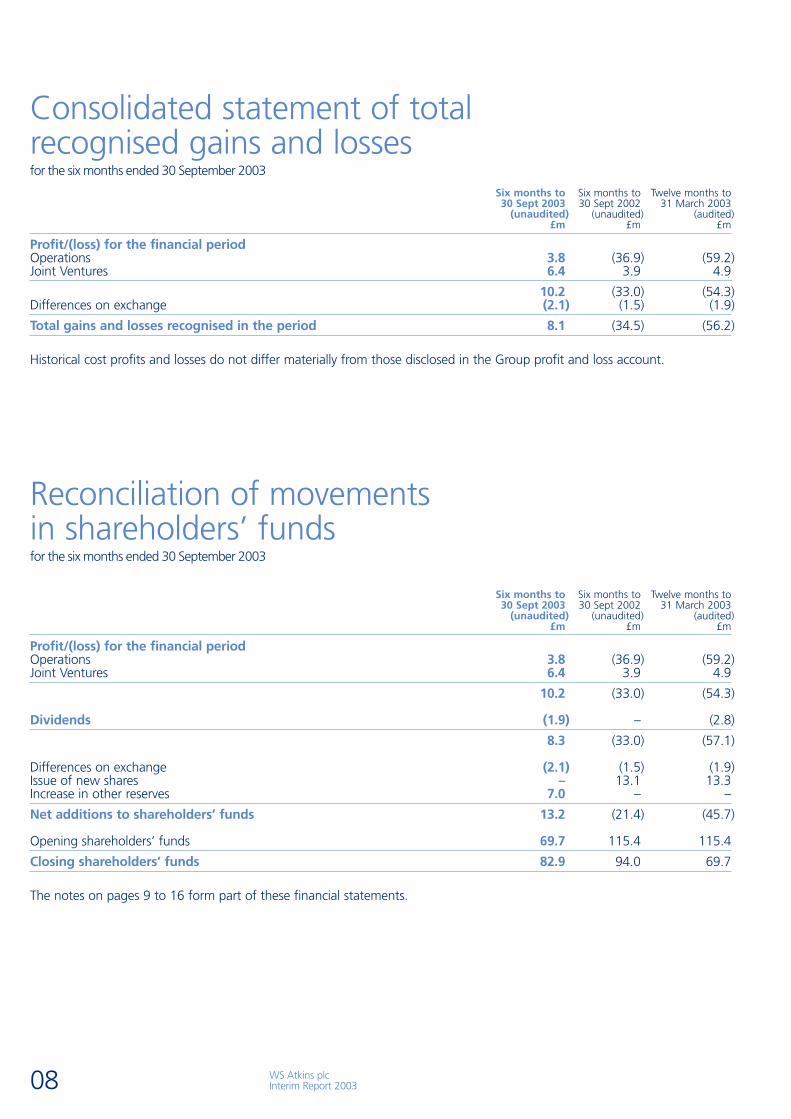

Consolidated statement of total recognised gains and losses for the six months ended 30 September 2003

Six months to Six months to Twelve months to30 Sept 2003 30 Sept 2002 31 March 2003

(unaudited) (unaudited) (audited)£m £m £m

Profit/(loss) for the financial periodOperations 3.8 (36.9) (59.2)Joint Ventures 6.4 3.9 4.9

10.2 (33.0) (54.3)Differences on exchange (2.1) (1.5) (1.9)

Total gains and losses recognised in the period 8.1 (34.5) (56.2)

Historical cost profits and losses do not differ materially from those disclosed in the Group profit and loss account.

Reconciliation of movements in shareholders’ funds for the six months ended 30 September 2003

Six months to Six months to Twelve months to30 Sept 2003 30 Sept 2002 31 March 2003

(unaudited) (unaudited) (audited)£m £m £m

Profit/(loss) for the financial periodOperations 3.8 (36.9) (59.2)Joint Ventures 6.4 3.9 4.9

10.2 (33.0) (54.3)

Dividends (1.9) – (2.8)

8.3 (33.0) (57.1)

Differences on exchange (2.1) (1.5) (1.9)Issue of new shares – 13.1 13.3 Increase in other reserves 7.0 – –

Net additions to shareholders’ funds 13.2 (21.4) (45.7)

Opening shareholders’ funds 69.7 115.4 115.4

Closing shareholders’ funds 82.9 94.0 69.7

The notes on pages 9 to 16 form part of these financial statements.

09WS Atkins plc Interim Report 2003

Notes to the financial statements

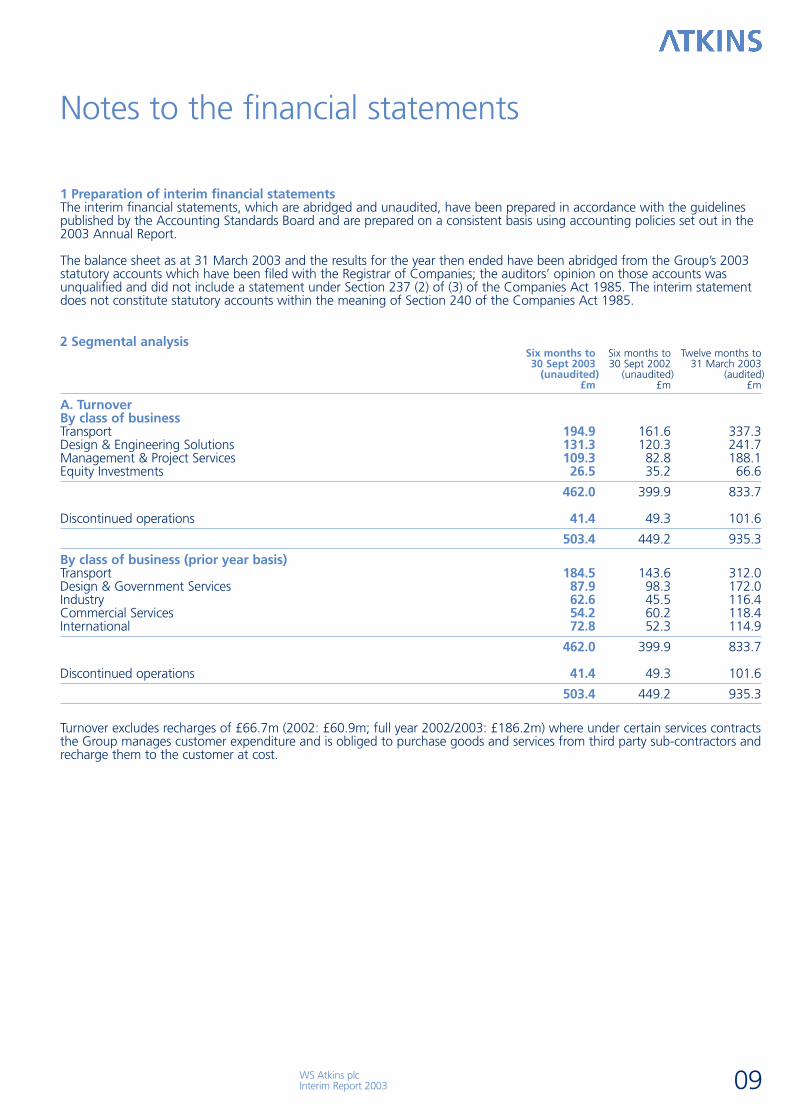

1 Preparation of interim financial statementsThe interim financial statements, which are abridged and unaudited, have been prepared in accordance with the guidelinespublished by the Accounting Standards Board and are prepared on a consistent basis using accounting policies set out in the2003 Annual Report.

The balance sheet as at 31 March 2003 and the results for the year then ended have been abridged from the Group’s 2003statutory accounts which have been filed with the Registrar of Companies; the auditors’ opinion on those accounts wasunqualified and did not include a statement under Section 237 (2) of (3) of the Companies Act 1985. The interim statementdoes not constitute statutory accounts within the meaning of Section 240 of the Companies Act 1985.

2 Segmental analysisSix months to Six months to Twelve months to30 Sept 2003 30 Sept 2002 31 March 2003

(unaudited) (unaudited) (audited)£m £m £m

A. Turnover By class of businessTransport 194.9 161.6 337.3 Design & Engineering Solutions 131.3 120.3 241.7 Management & Project Services 109.3 82.8 188.1 Equity Investments 26.5 35.2 66.6

462.0 399.9 833.7

Discontinued operations 41.4 49.3 101.6

503.4 449.2 935.3

By class of business (prior year basis)Transport 184.5 143.6 312.0 Design & Government Services 87.9 98.3 172.0 Industry 62.6 45.5 116.4 Commercial Services 54.2 60.2 118.4 International 72.8 52.3 114.9

462.0 399.9 833.7

Discontinued operations 41.4 49.3 101.6

503.4 449.2 935.3

Turnover excludes recharges of £66.7m (2002: £60.9m; full year 2002/2003: £186.2m) where under certain services contractsthe Group manages customer expenditure and is obliged to purchase goods and services from third party sub-contractors andrecharge them to the customer at cost.

10 WS Atkins plc Interim Report 2003

Notes to the financial statements

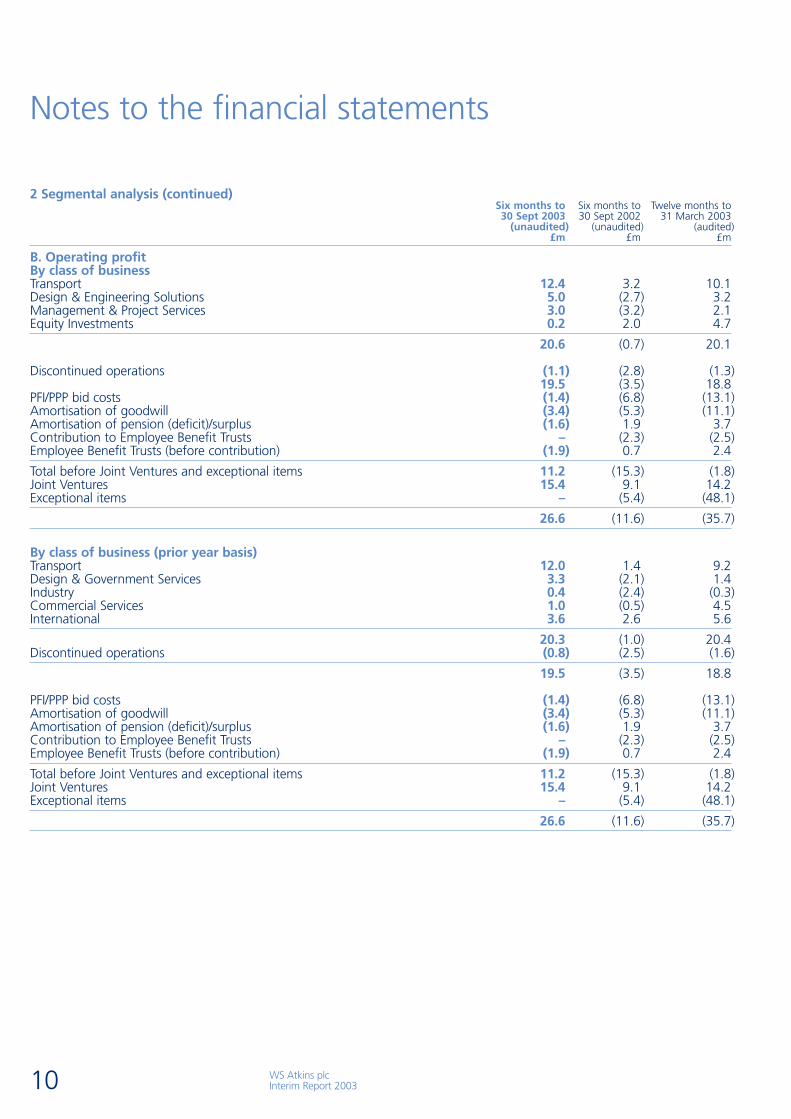

2 Segmental analysis (continued)Six months to Six months to Twelve months to30 Sept 2003 30 Sept 2002 31 March 2003

(unaudited) (unaudited) (audited)£m £m £m

B. Operating profit By class of businessTransport 12.4 3.2 10.1 Design & Engineering Solutions 5.0 (2.7) 3.2 Management & Project Services 3.0 (3.2) 2.1 Equity Investments 0.2 2.0 4.7

20.6 (0.7) 20.1

Discontinued operations (1.1) (2.8) (1.3)19.5 (3.5) 18.8

PFI/PPP bid costs (1.4) (6.8) (13.1)Amortisation of goodwill (3.4) (5.3) (11.1)Amortisation of pension (deficit)/surplus (1.6) 1.9 3.7 Contribution to Employee Benefit Trusts – (2.3) (2.5)Employee Benefit Trusts (before contribution) (1.9) 0.7 2.4

Total before Joint Ventures and exceptional items 11.2 (15.3) (1.8)Joint Ventures 15.4 9.1 14.2 Exceptional items – (5.4) (48.1)

26.6 (11.6) (35.7)

By class of business (prior year basis)Transport 12.0 1.4 9.2 Design & Government Services 3.3 (2.1) 1.4 Industry 0.4 (2.4) (0.3)Commercial Services 1.0 (0.5) 4.5 International 3.6 2.6 5.6

20.3 (1.0) 20.4 Discontinued operations (0.8) (2.5) (1.6)

19.5 (3.5) 18.8

PFI/PPP bid costs (1.4) (6.8) (13.1)Amortisation of goodwill (3.4) (5.3) (11.1)Amortisation of pension (deficit)/surplus (1.6) 1.9 3.7 Contribution to Employee Benefit Trusts – (2.3) (2.5)Employee Benefit Trusts (before contribution) (1.9) 0.7 2.4

Total before Joint Ventures and exceptional items 11.2 (15.3) (1.8)Joint Ventures 15.4 9.1 14.2 Exceptional items – (5.4) (48.1)

26.6 (11.6) (35.7)

11WS Atkins plc Interim Report 2003

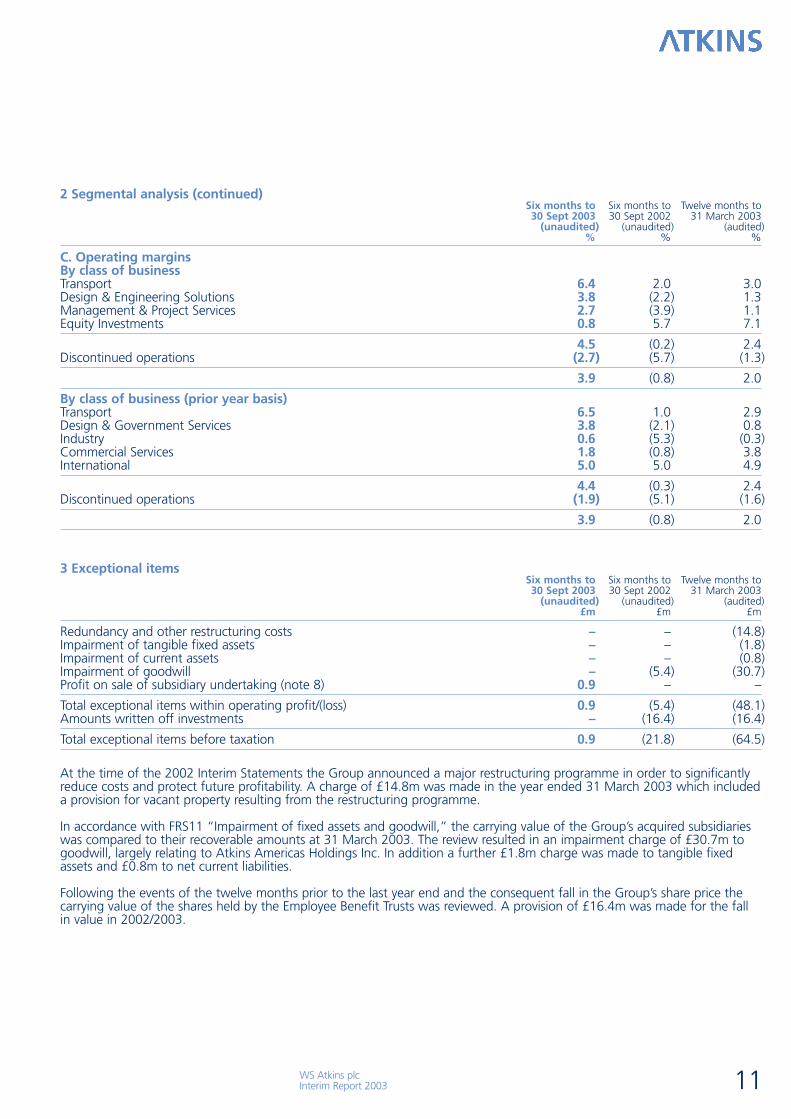

2 Segmental analysis (continued)Six months to Six months to Twelve months to30 Sept 2003 30 Sept 2002 31 March 2003

(unaudited) (unaudited) (audited)% % %

C. Operating margins By class of businessTransport 6.4 2.0 3.0Design & Engineering Solutions 3.8 (2.2) 1.3Management & Project Services 2.7 (3.9) 1.1Equity Investments 0.8 5.7 7.1

4.5 (0.2) 2.4Discontinued operations (2.7) (5.7) (1.3)

3.9 (0.8) 2.0

By class of business (prior year basis)Transport 6.5 1.0 2.9Design & Government Services 3.8 (2.1) 0.8Industry 0.6 (5.3) (0.3)Commercial Services 1.8 (0.8) 3.8International 5.0 5.0 4.9

4.4 (0.3) 2.4Discontinued operations (1.9) (5.1) (1.6)

3.9 (0.8) 2.0

3 Exceptional itemsSix months to Six months to Twelve months to 30 Sept 2003 30 Sept 2002 31 March 2003

(unaudited) (unaudited) (audited)£m £m £m

Redundancy and other restructuring costs – – (14.8)Impairment of tangible fixed assets – – (1.8)Impairment of current assets – – (0.8)Impairment of goodwill – (5.4) (30.7)Profit on sale of subsidiary undertaking (note 8) 0.9 – –

Total exceptional items within operating profit/(loss) 0.9 (5.4) (48.1)Amounts written off investments – (16.4) (16.4)

Total exceptional items before taxation 0.9 (21.8) (64.5)

At the time of the 2002 Interim Statements the Group announced a major restructuring programme in order to significantlyreduce costs and protect future profitability. A charge of £14.8m was made in the year ended 31 March 2003 which includeda provision for vacant property resulting from the restructuring programme.

In accordance with FRS11 “Impairment of fixed assets and goodwill,” the carrying value of the Group’s acquired subsidiarieswas compared to their recoverable amounts at 31 March 2003. The review resulted in an impairment charge of £30.7m togoodwill, largely relating to Atkins Americas Holdings Inc. In addition a further £1.8m charge was made to tangible fixedassets and £0.8m to net current liabilities.

Following the events of the twelve months prior to the last year end and the consequent fall in the Group’s share price thecarrying value of the shares held by the Employee Benefit Trusts was reviewed. A provision of £16.4m was made for the fall in value in 2002/2003.

Notes to the financial statements continued

12 WS Atkins plc Interim Report 2003

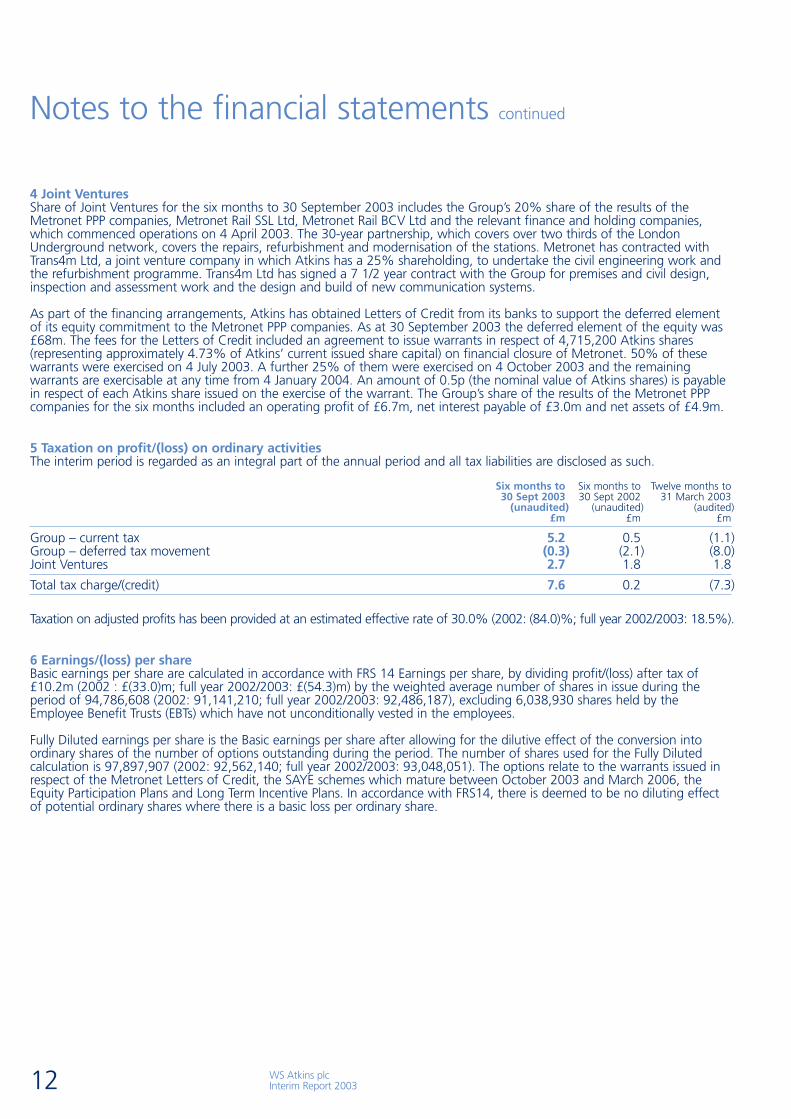

4 Joint VenturesShare of Joint Ventures for the six months to 30 September 2003 includes the Group’s 20% share of the results of theMetronet PPP companies, Metronet Rail SSL Ltd, Metronet Rail BCV Ltd and the relevant finance and holding companies,which commenced operations on 4 April 2003. The 30-year partnership, which covers over two thirds of the LondonUnderground network, covers the repairs, refurbishment and modernisation of the stations. Metronet has contracted withTrans4m Ltd, a joint venture company in which Atkins has a 25% shareholding, to undertake the civil engineering work andthe refurbishment programme. Trans4m Ltd has signed a 7 1/2 year contract with the Group for premises and civil design,inspection and assessment work and the design and build of new communication systems.

As part of the financing arrangements, Atkins has obtained Letters of Credit from its banks to support the deferred elementof its equity commitment to the Metronet PPP companies. As at 30 September 2003 the deferred element of the equity was£68m. The fees for the Letters of Credit included an agreement to issue warrants in respect of 4,715,200 Atkins shares(representing approximately 4.73% of Atkins’ current issued share capital) on financial closure of Metronet. 50% of thesewarrants were exercised on 4 July 2003. A further 25% of them were exercised on 4 October 2003 and the remainingwarrants are exercisable at any time from 4 January 2004. An amount of 0.5p (the nominal value of Atkins shares) is payablein respect of each Atkins share issued on the exercise of the warrant. The Group’s share of the results of the Metronet PPPcompanies for the six months included an operating profit of £6.7m, net interest payable of £3.0m and net assets of £4.9m.

5 Taxation on profit/(loss) on ordinary activitiesThe interim period is regarded as an integral part of the annual period and all tax liabilities are disclosed as such.

Six months to Six months to Twelve months to 30 Sept 2003 30 Sept 2002 31 March 2003

(unaudited) (unaudited) (audited)£m £m £m

Group – current tax 5.2 0.5 (1.1)Group – deferred tax movement (0.3) (2.1) (8.0)Joint Ventures 2.7 1.8 1.8

Total tax charge/(credit) 7.6 0.2 (7.3)

Taxation on adjusted profits has been provided at an estimated effective rate of 30.0% (2002: (84.0)%; full year 2002/2003: 18.5%).

6 Earnings/(loss) per shareBasic earnings per share are calculated in accordance with FRS 14 Earnings per share, by dividing profit/(loss) after tax of£10.2m (2002 : £(33.0)m; full year 2002/2003: £(54.3)m) by the weighted average number of shares in issue during theperiod of 94,786,608 (2002: 91,141,210; full year 2002/2003: 92,486,187), excluding 6,038,930 shares held by theEmployee Benefit Trusts (EBTs) which have not unconditionally vested in the employees.

Fully Diluted earnings per share is the Basic earnings per share after allowing for the dilutive effect of the conversion intoordinary shares of the number of options outstanding during the period. The number of shares used for the Fully Dilutedcalculation is 97,897,907 (2002: 92,562,140; full year 2002/2003: 93,048,051). The options relate to the warrants issued inrespect of the Metronet Letters of Credit, the SAYE schemes which mature between October 2003 and March 2006, theEquity Participation Plans and Long Term Incentive Plans. In accordance with FRS14, there is deemed to be no diluting effect of potential ordinary shares where there is a basic loss per ordinary share.

13WS Atkins plc Interim Report 2003

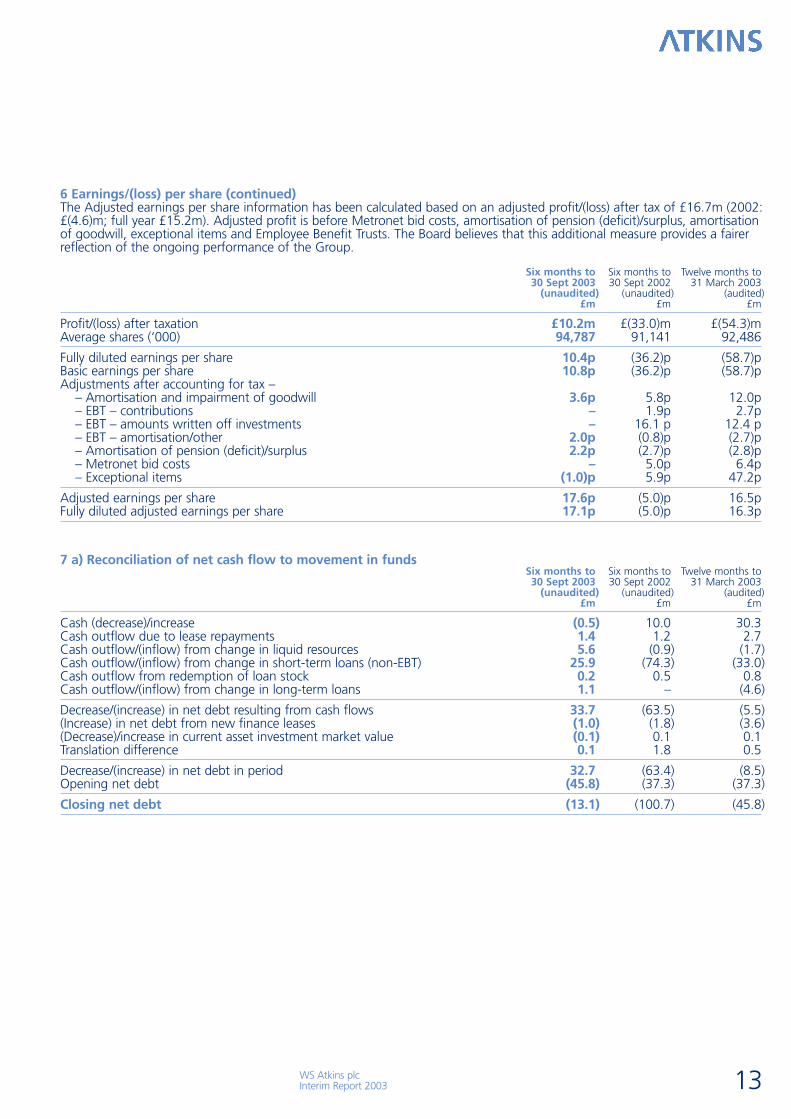

6 Earnings/(loss) per share (continued)The Adjusted earnings per share information has been calculated based on an adjusted profit/(loss) after tax of £16.7m (2002:£(4.6)m; full year £15.2m). Adjusted profit is before Metronet bid costs, amortisation of pension (deficit)/surplus, amortisationof goodwill, exceptional items and Employee Benefit Trusts. The Board believes that this additional measure provides a fairerreflection of the ongoing performance of the Group.

Six months to Six months to Twelve months to30 Sept 2003 30 Sept 2002 31 March 2003

(unaudited) (unaudited) (audited)£m £m £m

Profit/(loss) after taxation £10.2m £(33.0)m £(54.3)mAverage shares (‘000) 94,787 91,141 92,486

Fully diluted earnings per share 10.4p (36.2)p (58.7)pBasic earnings per share 10.8p (36.2)p (58.7)pAdjustments after accounting for tax –

– Amortisation and impairment of goodwill 3.6p 5.8p 12.0p– EBT – contributions – 1.9p 2.7p– EBT – amounts written off investments – 16.1 p 12.4 p– EBT – amortisation/other 2.0p (0.8)p (2.7)p– Amortisation of pension (deficit)/surplus 2.2p (2.7)p (2.8)p– Metronet bid costs – 5.0p 6.4p– Exceptional items (1.0)p 5.9p 47.2p

Adjusted earnings per share 17.6p (5.0)p 16.5pFully diluted adjusted earnings per share 17.1p (5.0)p 16.3p

7 a) Reconciliation of net cash flow to movement in fundsSix months to Six months to Twelve months to30 Sept 2003 30 Sept 2002 31 March 2003

(unaudited) (unaudited) (audited)£m £m £m

Cash (decrease)/increase (0.5) 10.0 30.3 Cash outflow due to lease repayments 1.4 1.2 2.7 Cash outflow/(inflow) from change in liquid resources 5.6 (0.9) (1.7)Cash outflow/(inflow) from change in short-term loans (non-EBT) 25.9 (74.3) (33.0)Cash outflow from redemption of loan stock 0.2 0.5 0.8 Cash outflow/(inflow) from change in long-term loans 1.1 – (4.6)

Decrease/(increase) in net debt resulting from cash flows 33.7 (63.5) (5.5)(Increase) in net debt from new finance leases (1.0) (1.8) (3.6)(Decrease)/increase in current asset investment market value (0.1) 0.1 0.1 Translation difference 0.1 1.8 0.5

Decrease/(increase) in net debt in period 32.7 (63.4) (8.5)Opening net debt (45.8) (37.3) (37.3)

Closing net debt (13.1) (100.7) (45.8)

Notes to the financial statements continued

14 WS Atkins plc Interim Report 2003

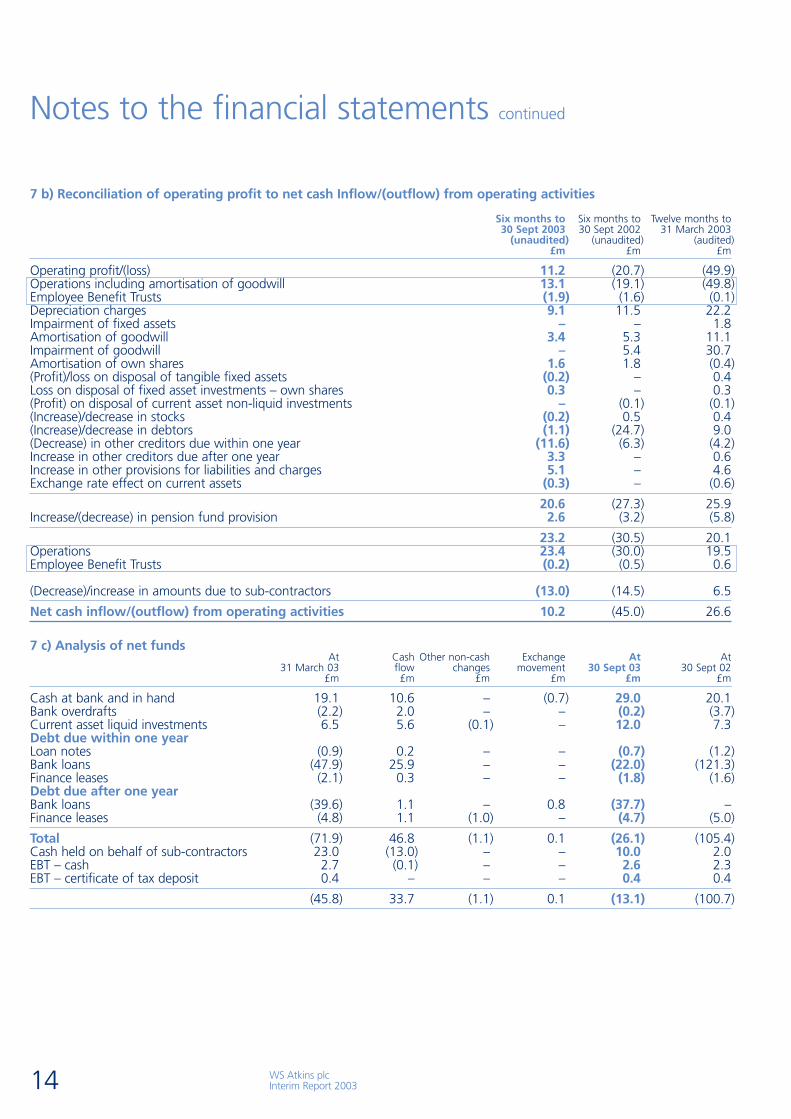

7 b) Reconciliation of operating profit to net cash Inflow/(outflow) from operating activities

Six months to Six months to Twelve months to30 Sept 2003 30 Sept 2002 31 March 2003

(unaudited) (unaudited) (audited)£m £m £m

Operating profit/(loss) 11.2 (20.7) (49.9)Operations including amortisation of goodwill 13.1 (19.1) (49.8)Employee Benefit Trusts (1.9) (1.6) (0.1)Depreciation charges 9.1 11.5 22.2 Impairment of fixed assets – – 1.8 Amortisation of goodwill 3.4 5.3 11.1 Impairment of goodwill – 5.4 30.7 Amortisation of own shares 1.6 1.8 (0.4)(Profit)/loss on disposal of tangible fixed assets (0.2) – 0.4 Loss on disposal of fixed asset investments – own shares 0.3 – 0.3 (Profit) on disposal of current asset non-liquid investments – (0.1) (0.1)(Increase)/decrease in stocks (0.2) 0.5 0.4 (Increase)/decrease in debtors (1.1) (24.7) 9.0 (Decrease) in other creditors due within one year (11.6) (6.3) (4.2)Increase in other creditors due after one year 3.3 – 0.6 Increase in other provisions for liabilities and charges 5.1 – 4.6 Exchange rate effect on current assets (0.3) – (0.6)

20.6 (27.3) 25.9 Increase/(decrease) in pension fund provision 2.6 (3.2) (5.8)

23.2 (30.5) 20.1 Operations 23.4 (30.0) 19.5 Employee Benefit Trusts (0.2) (0.5) 0.6

(Decrease)/increase in amounts due to sub-contractors (13.0) (14.5) 6.5

Net cash inflow/(outflow) from operating activities 10.2 (45.0) 26.6

7 c) Analysis of net fundsAt Cash Other non-cash Exchange At At

31 March 03 flow changes movement 30 Sept 03 30 Sept 02£m £m £m £m £m £m

Cash at bank and in hand 19.1 10.6 – (0.7) 29.0 20.1 Bank overdrafts (2.2) 2.0 – – (0.2) (3.7)Current asset liquid investments 6.5 5.6 (0.1) – 12.0 7.3 Debt due within one yearLoan notes (0.9) 0.2 – – (0.7) (1.2)Bank loans (47.9) 25.9 – – (22.0) (121.3)Finance leases (2.1) 0.3 – – (1.8) (1.6)Debt due after one yearBank loans (39.6) 1.1 – 0.8 (37.7) – Finance leases (4.8) 1.1 (1.0) – (4.7) (5.0)

Total (71.9) 46.8 (1.1) 0.1 (26.1) (105.4)Cash held on behalf of sub-contractors 23.0 (13.0) – – 10.0 2.0 EBT – cash 2.7 (0.1) – – 2.6 2.3 EBT – certificate of tax deposit 0.4 – – – 0.4 0.4

(45.8) 33.7 (1.1) 0.1 (13.1) (100.7)

15WS Atkins plc Interim Report 2003

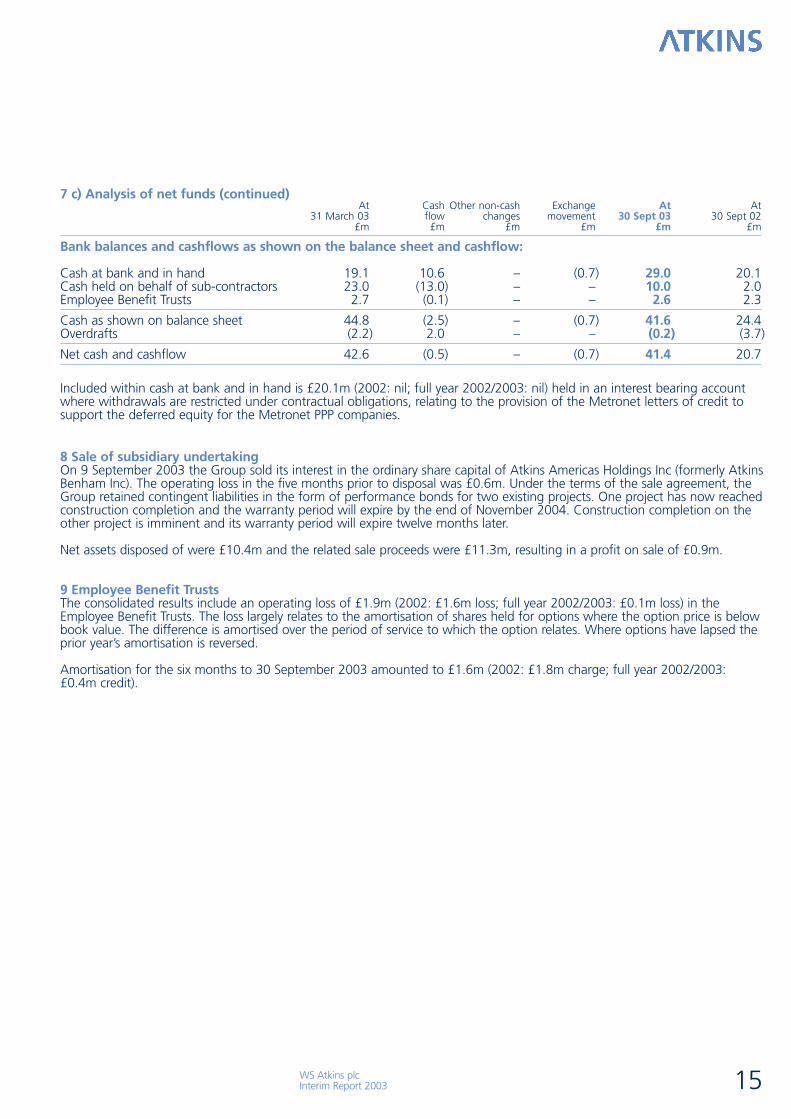

7 c) Analysis of net funds (continued)At Cash Other non-cash Exchange At At

31 March 03 flow changes movement 30 Sept 03 30 Sept 02£m £m £m £m £m £m

Bank balances and cashflows as shown on the balance sheet and cashflow:

Cash at bank and in hand 19.1 10.6 – (0.7) 29.0 20.1 Cash held on behalf of sub-contractors 23.0 (13.0) – – 10.0 2.0 Employee Benefit Trusts 2.7 (0.1) – – 2.6 2.3

Cash as shown on balance sheet 44.8 (2.5) – (0.7) 41.6 24.4 Overdrafts (2.2) 2.0 – – (0.2) (3.7)

Net cash and cashflow 42.6 (0.5) – (0.7) 41.4 20.7

Included within cash at bank and in hand is £20.1m (2002: nil; full year 2002/2003: nil) held in an interest bearing accountwhere withdrawals are restricted under contractual obligations, relating to the provision of the Metronet letters of credit tosupport the deferred equity for the Metronet PPP companies.

8 Sale of subsidiary undertakingOn 9 September 2003 the Group sold its interest in the ordinary share capital of Atkins Americas Holdings Inc (formerly AtkinsBenham Inc). The operating loss in the five months prior to disposal was £0.6m. Under the terms of the sale agreement, theGroup retained contingent liabilities in the form of performance bonds for two existing projects. One project has now reachedconstruction completion and the warranty period will expire by the end of November 2004. Construction completion on theother project is imminent and its warranty period will expire twelve months later.

Net assets disposed of were £10.4m and the related sale proceeds were £11.3m, resulting in a profit on sale of £0.9m.

9 Employee Benefit TrustsThe consolidated results include an operating loss of £1.9m (2002: £1.6m loss; full year 2002/2003: £0.1m loss) in theEmployee Benefit Trusts. The loss largely relates to the amortisation of shares held for options where the option price is belowbook value. The difference is amortised over the period of service to which the option relates. Where options have lapsed theprior year’s amortisation is reversed.

Amortisation for the six months to 30 September 2003 amounted to £1.6m (2002: £1.8m charge; full year 2002/2003:£0.4m credit).

Notes to the financial statements continued

16 WS Atkins plc Interim Report 2003

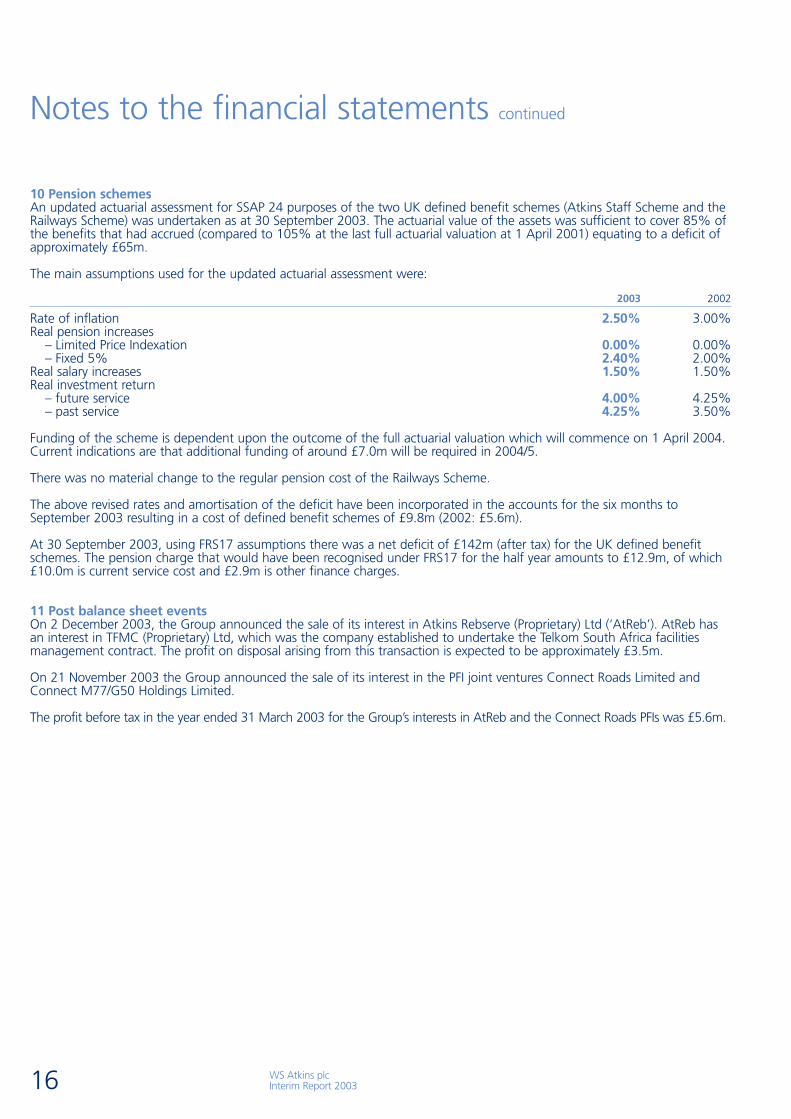

10 Pension schemesAn updated actuarial assessment for SSAP 24 purposes of the two UK defined benefit schemes (Atkins Staff Scheme and theRailways Scheme) was undertaken as at 30 September 2003. The actuarial value of the assets was sufficient to cover 85% ofthe benefits that had accrued (compared to 105% at the last full actuarial valuation at 1 April 2001) equating to a deficit ofapproximately £65m.

The main assumptions used for the updated actuarial assessment were:

2003 2002

Rate of inflation 2.50% 3.00%Real pension increases

– Limited Price Indexation 0.00% 0.00%– Fixed 5% 2.40% 2.00%

Real salary increases 1.50% 1.50%Real investment return

– future service 4.00% 4.25%– past service 4.25% 3.50%

Funding of the scheme is dependent upon the outcome of the full actuarial valuation which will commence on 1 April 2004.Current indications are that additional funding of around £7.0m will be required in 2004/5.

There was no material change to the regular pension cost of the Railways Scheme.

The above revised rates and amortisation of the deficit have been incorporated in the accounts for the six months toSeptember 2003 resulting in a cost of defined benefit schemes of £9.8m (2002: £5.6m).

At 30 September 2003, using FRS17 assumptions there was a net deficit of £142m (after tax) for the UK defined benefitschemes. The pension charge that would have been recognised under FRS17 for the half year amounts to £12.9m, of which£10.0m is current service cost and £2.9m is other finance charges.

11 Post balance sheet eventsOn 2 December 2003, the Group announced the sale of its interest in Atkins Rebserve (Proprietary) Ltd (‘AtReb’). AtReb hasan interest in TFMC (Proprietary) Ltd, which was the company established to undertake the Telkom South Africa facilitiesmanagement contract. The profit on disposal arising from this transaction is expected to be approximately £3.5m.

On 21 November 2003 the Group announced the sale of its interest in the PFI joint ventures Connect Roads Limited andConnect M77/G50 Holdings Limited.

The profit before tax in the year ended 31 March 2003 for the Group’s interests in AtReb and the Connect Roads PFIs was £5.6m.

Investor information

The Interim Report is being sent to all shareholders. Copies are available from the Company Secretary, WS Atkins plc, Woodcote Grove,Ashley Road, Epsom, Surrey KT18 5BW. The Company’s registered number is 1885586.

Shareholder servicesRegistrarAdministrative enquiries about the holding of WS Atkins plc shares should be directed in the first instance to the Registrar whose addressis The Registrar, Registration Department, The Registry, 34 Beckenham Road, Beckenham, Kent, BR3 4BR. Telephone: 0870 162 3100,Website: www.capitaregistrars.com.

Share dealing serviceDetails of a postal dealing service can be obtained from: WS Atkins plc Share Dealing Service, Cazenove & Co. Ltd, 20 Moorgate,London, EC2R 6DA. Telephone: 020 7155 5155, Website: www.cazenove.com

Dividend reinvestment plan (“DRIP”)The Company offers a dividend reinvestment plan to shareholders as a dividend alternative. Participation in the DRIP scheme is entirleyvoluntary and you may join or withdraw at any time. Should you wish to participate in the DRIP scheme please contact the Registrars on 0870 162 3100 to request a form of mandate and an explanatory booklet. Your completed mandate form must be received by theCompany’s Registrars by 9 January 2004.

Amalgamation of accountsShareholders who receive duplicate sets of Company mailings owing to multiple accounts in their name should write to the Registrar to have their accounts amalgamated.

Unsolicited mailThe Company is obliged by law to make its share register available to other organisations who may then use it for a mailing list. If you wish to limit the receipt of unsolicited mail you may do so by writing to: The Mailing Preference Service (MPS), Freepost 29 LON20771, London W1E 0ZT. MPS will then notify the bodies which support its service that you do not wish to receiveunsolicited mail.

WS Atkins plc Interim Report 2003