Embed Size (px)

Citation preview

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. 6786

PROJECT COMPLETION REPORT

PAKISTAN

FIRST SMALL INDUSTRIES PROJECT(CREDIT 1113-PAK)

May 19, 1987

Industrial Development and Finance DivisionSouth Asia Projects Department

T:iis document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS a/(annual averages)

Rs per US$1.00 US$ per Rs 1.00

FY82 10.55 0.095FY83 12.75 0.078FY84 13.50 0.074FY85 15.30 0.065FY86 16.90 0.059

a/ Since January 8, 1982, the exchange rate for the rupee has been managedwith respect to a weighted basket of currencies.

ABBREVIATIONS AND ACCRONYMS

ABL - Allied Bank of Pakistan LimitedBLGSC - Bannu Leather Goods Service CenterBLSMA - Bannu Leather and Shoe Manufacturers AssociationDSI - Directorate for Small IndustriesEPB - Export Promotion BureauGFMA - Gujrat Furniture Makers AssociationGOP - Government of PakistanGWSC - Gujrat Woodworking Service CenterHBL - Habib Bank LimitedIDBP - Industrial Development Bank of PakistanMCB - Muslim Commercial BankNBP - National Bank of PakistanNWFP - North West Frontier ProvincePBC - Pakistan Banking CouncilPCI - Participating Credit InstitutionPSIC - Punjab Small Industries CorporationSBP - State Bank of PakistanSIC - Small Industries CorporationSID - Small Industries DepartmentSIDB - Small Industries Development BoardSSI - Small Scale IndustriesSSI I - First Small Industries ProjectSSI II - Second Small IndusLries ProjectSSI III - Third Small Industries ProjectSSIC - Sind Small Industries CorporationUBL - United Bank Limited

FISCAL YEAR (FY)

Government of Pakistan: July 1 - June 30Commercial Banks : January 1 - December 31

FOR OFFICIAL USE ONLY

THE WORLD 8ANKWashington. DC 20431

U S A

Oice of oieeclno-enetalOpe..tawns Eajluit,n

May 19, 1987

MEMORANDUM TO THE EXECUTIVE DIRECTORS AND THE PRESIDENT

SUBJECT: Project Completion Report on Pakistan - First Small IndustriesProject (Credit 1113-PAK)

Attached, for information, is a copy of a report entitled "ProjectCompletion Report on Pakistan - First Small Industries Project (Credit1113-PAK)" prepared by the South Asia Projects Department. Under themodified system for project performance auditiag further evaluation of thisproject by the Operations Evaluation Department has not been made.

-''

Attachment

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

FOR OFFICIAL USE ONLY

PROJECT COMPLETION REPORT

PAKISTAN - FIRST SMALL INDUSTRIES EIA'JECT

(CREDIT 1113-PAK)

TABLE OF CONTENTS

Page No.

Preface .......................... .*iBasic Data Sheet .......................... .. . * iiHighlights .. iv

I. INTRODUCrION ........ 99....... 1

II. SECTORAL BACKGROUND

A. Economic Setting ... ............................. . 2B. The Industrial Sec t o r 2C. Financial Environment.i rn m... *... en t.... ... 3D. Small Scale Industries Sectore ct...o... or...... 4

III. PROJECT DESCRIPTION .......... 6

A. Orgn6B. Project Objectives............................... 6C. Project Components... .................... ..... . 7

IV. PROJECT IMPLEMETATION ... T....... 8

A. Subloan Compone m p....... 81. Stat-ua.r t.- u p.... ... 82. Timetable. .............. ......... 94.9. 9994 8

3. Subproject Apiaa i s a l 94. Supervision and Coliection Performance........ 95. Repotin*.,n.. 106. Procurements and Disbursements... 10

B. Technical Assistance Compponn ents................ 111. Gujrat Woodworking Service Center..*......... 112. Bannu Leather Goods Service Center..,.o .... *... 123. Export Promotion...o9.9 *.4.999 9 99 9 9 94.o 49 o 134. Project Development for Baluchistana.ech,...a...... 155. Fund for Subsector Studies and Project

Preparation.... .. ... *949.... ... **. 15

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

TABLE OF CONTENTS (Cont'd)

Page No.

V. PROJECT IMPACT ............................ .... ,.....*.. 16

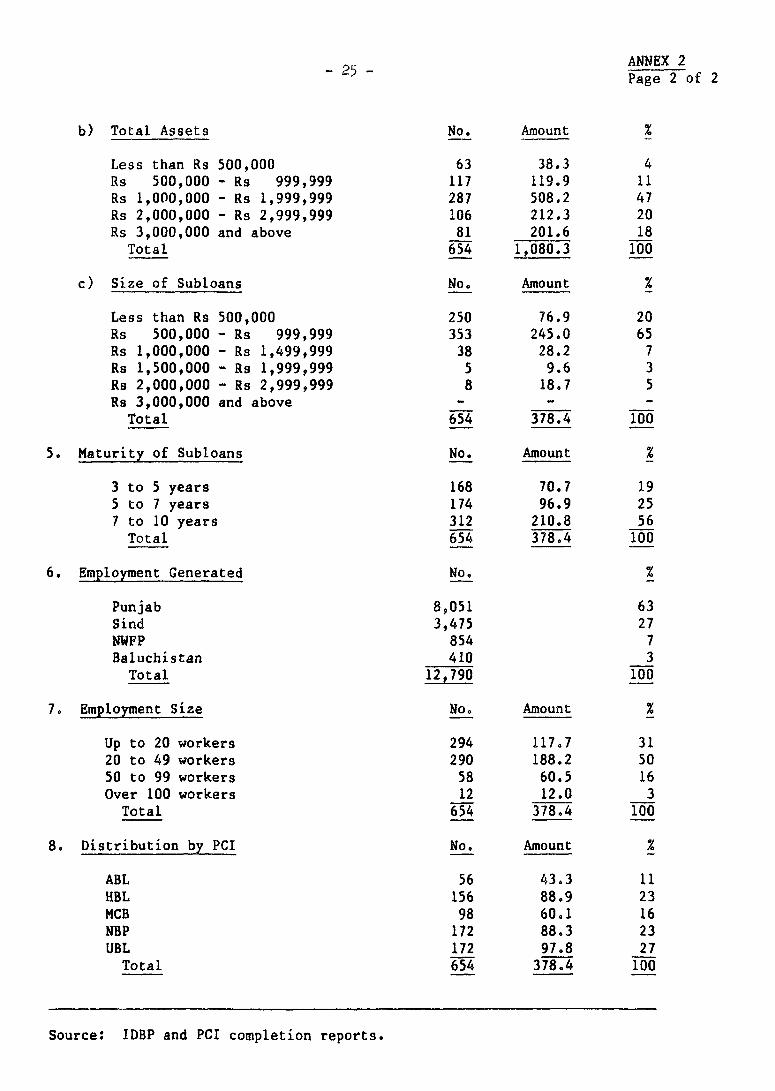

A. Subprojects Financed ............................... 16B. Institution Building *****@@@*o*O***¢ 18

VI. ROLE OF IDA . 20

VtI. CONCLUSIONS AND LESSONS LEARNED ..............., .......... 20

ANNEXES

1. Projected and Actual Cu' .lative Disbursements 23

2. Characteristics of Subprojects Financed .................... 24

3. Collection Performance of PCIs from FY82-86 .,....,......,... 264. Subloan Arrears 9999099 , 9 .............. ** * 27

ATTACHMENT I

Comments Received from the Industrial DevelopmentBank of Pakistan . . . 9 . . , . * , , . , , a ................. 28

-i -

PROJECT COMPLETION REPORT

PAKISTAN - FIRST SMALL INDUSTRIES PROJECT

(CREDIT 1113-PAK)

PREFACE

This report reviews the implementation of Credit 1113-PAK, which wasthe first small scale industry lending operation of the Bank Group inPakistan. The report covers the period from FY82 to FY86, during whichdisbursements under this Credit were made. The IDA Credit of SDR 23.6 mil-lion (US$30 million) was appraised in June 1980, approved in March 1981,declared effective in October 1981, and disbursed until December 27, 1985,within the original closing date of December 31, 1985. There was no cancel-lation since the full amount was disbursed. A second lending operation forSSI was approved on June 14, 1984 and is still being implemented. A proposedThird SSI Project has been appraised and is expected to be presented to theBoard in FY87. This PCR was prepared by the Industrial Development andFinance Division of the South Asia Projects Department based on informationcollected and processed for this purpose by the project implementingagencies.

Comments received from the Borrower have been taken into account infinalizing the report and are reproduced as an Attachment.

This project has not been audited by the Operations EvaluationDepartment.

-ii-

PROJECT COMPLETION REPORT

PAKISTAN - FIRST SMALL INDUSTRIES PROJECT

(CREDIT 1113-PAK)

BASIC DATA SHEET(Amounts in US$M)

CREDIT STATUS

As of 03/31/87

Borrower'sOriginal Disbursed Cancelled Repaid Obligation

Credit 1113-PAKSDR 23.6 23.6 0 - -

US$m 30.0 24.5 0 0 30.3

CUMULATIVE CREDIT DISBURSEMENT

FY81 FY82 FY83 FY84 FY85 FY86

(i) Planned G.5 8.7 21.9 28.5 30.0 30.0(ii) Actual - 0.1 2.8 22.1 29.6 30.0

(iii) (ii) as% of - 1.2% 12.8% 77.6% 98.7% 100%_ (iOTHER PROJECT DATA

Actual

Board Approval 03/17/81Credit Agreement 04/24/81Effectiveness 10/06/81Credit Closing 12/31/85

Borrower Government of the Islamic Republic of PakistanExecuting Agencies Industrial Development Bank of Pakistan

Nationalized Commercial BanksProvincial Small Industries CorporationsExport Promotion Bureau

Credit ComponentsSubloans US$26.0 millionTechnical Assistance US$ 4.0 million

-iii-

PROJECT COMPLETION REPORT

PAKISTAN - FIRST SMALL INDUSTRIES PROJECT

(CREDIT 1113-PAK)

MISSION DATA

Month/ Number of Number of Staff Date ofYear Weeks Persons Weeks Report

Appraisal 06/80 3 5 15 02/20/81Supervision 09/81 2 1/2 2 5 10/07/81Supervision 07/82 2 1 2 08/16/82Supervision 03/83 2 1 2 04/08/83Supervision 10/83 3 4 12 11/22/83Supervision 03/84 2 4 8 05/11/84Supervision 05/85 1 1/2 4 6 06/14/85Completion 09/85 1 3 3 10/31/86

STAFF INPUT(manweeks)

FY80 FY81 FY82 FY83 FY84 FY85 FY86 Total

Preparation 48.0 48.0Appraisal 15.0 15.0Negotiations 6.0 6.0Supervision 5.0 4.0 20.0 6.0 3.0 38.0

Totals 63.0 6.0 5.0 4.0 20.0 6.0 3.0 107.0

FOLLOW-ON PROJECT

Second Small Industries Project, Credit 1499-PAK, approved onJune 14, 1984 in the amount of SDR 47.0 miflion (US$50 million).

-iv-

PROJECT COMPLETION REPORT

PAKISTAN - FIRST SMALL INDUSTRIES PROJECT

(CREDIT 1113-PAK)

HIGHLIGHTS

1. Credit 1113-PAK, which was signed in April 1981, was the firstproject in Pakistan dealing exclusively with the small scale industry (SSI)sector. Previously, IDA assistance to SSI was part of general credit linesfor industry and was confined to financial assistance. Based on the findingsof studies, jointly undertaken by UNIDO and IDA, of five key SSI subsectors,the First SSI Project was designed to expand assistance to SSI by involvingthe five largest commercial banks in SSI financing and including projectcomponents that provided technical and marketing assistance.

2. The First SSI Project had the following specific objectives: (a) toencourage the development of SSI units that are export-oriented or are effi-cient in import-substitution by providing funds for term lending through thecommercial banks; (b) to assist in orienting the commercial banks toward alonger term project appraisal approach in their SSI lending; (c) to assisttwo provincial Small Industries Corporations (SIC) in providing selectedtechnical assistance, extension services and skills training in woodworkingand leather goods; (d) to expand the export promotion of SSI products; and(e) to initiate project development exercises in Baluchistan(paras. 3.03-3.05).

3. Overall, the project achieved its objectives satisfactorily. Theproject assisted the commercial banks in building their capability forproject lending by training staff in appraisal and supervision and bydeveloping appropriate systems and procedures for loan processing, procure-ment and disbursement, loan administration and end-use monitoring. WithSmall Industry Departments organized at their headquarters and operationallinkages established with their branches, the five participating creditinstitutions (PCI) fully disbursed the Credit to 654 subprojects on scheduie.These loans generated investments of about US$80 million, 45% higher than theappraisal estimate of US$54 million. Subsector distribution of subprojectswas basically as expected at appraisal, with concentration in agro-industries, light-engineering and textiles. Average subloan size was aboutUS$42,000, much lower than the maximum amount allowed of US$200,000, indicat-ing that adequate attention was given to smaller units. The subprojectsfinanced generated about 12,800 jobs at a cost per job of about US$6,000,compared with the appraisal estimate of 13,000 jobs. Annual incrementalvalue added is estimated to be about US$50 million. Ex-post financial ratesof return of fully operational subprojects ranged between 18 and 45%(paras. 5.01-5.05).

4. The project established the basis for the development of soundinstitutional arrangements for SSI financing. Using the commercial banks,with their branch network, close contact with SSI industrialists, ability tomobilize domestic resources and traditional role in working capitalfinancing, has proved to be a sound arrangement. With the additional skillsin project appraisal and supervision developed under the project, the commer-cial banks have a demonstrated capability for selecting subproject sponsors,

_v

appraising project proposals, disbursing subloans and supervising end-use.Given long term funds, the banks have prudently term transformed some oftheir own resources into long ter.n SSI subloans by cofinancing 20% of allsubloan3. With their close contact with clients through other bankingrelationships, subloan collection performance, after an initial problem, hasreached a ratio of 82% and is still improving. Overall, the SSI sector'saccess to institutional credit has i-acreased under the present financingsystem, with credit from the commercial banks accounting for about 40% of SSIinvestment needs, up from 30% in the past (paras. 5.06-5.10).

5. Implementation of the technical assistance (TA) components werecompleted on schedule despite start-up delays. The impact of the TA com-ponents has been less impressive than that of the subloan component but stillgenerally positive, resulting in the establishment of two service centerswhich have started to provide useful technical training and services to apre-identified clientele (paras. 4.13-4.19). The project preparation fundwas effective in assisting over 600 subloan applicants in preparing theirloan applications and feasibility reports for submission to the PCIs(paras. 4.29-4.31). Subsector studies and area development studies forBaluchistan have been prepared and are being utilized to improve projectpromotion and selection (paras. 4.26-4.28). The export promotion componentsucceeded in introducing several Pakistani exporters and products to the U.S.market (paras. 4.20-4.25).

6. Institution building for the technical assistance agencies has alsonot been as successful as for the PCIso The common problem has been §.he lackof qualified counterpart staff who could be trained on-the-job in the courseof project implementation. This problem was especially true of theGovernment of Baluchistan which could not provide counterpart staff and couldnot organize a unit for project promotion as envisioned at appraisal. To alesser degree, the same problem was encountered for the Bannu Leather GoodsService Center and the export promotion component. Transfer of technologyfrom consultants to counterpart staff was adequate only in the case of theGujrat Woodworking Service Center. Another major reason for weak institutionbuilding was the poor performance of some project advisors. This was espe-cially true of the export promotion component under which the advisors werenot only appointed late but apparently did not meet the qualificationsspecified in the terms of reference. Efforts by the consulting group toremedy the situation on the basis of feedback by the project agencies wereinsufficient, The problems dragged on until the project was completed(paras. 5.11-5.14)v

7. In summary, for the most part, the project objectives were achieved.The subloan components not only provided financial assistance to more SSIunits than expected at appraisal but established the basis for developing asound SSI credit delivery system. The TA components also achieved theirdirect objectives. However, institution building objectives implicit in theimplementation of these components was weak due to problems with some coun-terpart staff and advisors.

PROJECT COMPLETION REPORT

PAKISTAN - FIRST SMALL INDUSTRIES PROJECT

(CREDIT 1113-PAK)

I. INTRODUCTION

1.01 In the past, IDA assistance for small industry development inPakistan focused principally on the provision of investment funds to SSIunits through the development finance institution (DFI) which looked afterindustrial finance for the small and medium industries sector, i.e. theIndustrial Development Bank of Pakistan (IDBP). In 1977, UNIDO, with IDAassistance, undertook a study of five important SSI subsectors to assesstheir status, analyze problems and prospects, and recommend assistanceprograms for SSI development. Th,is study served as the basis for the designof the First Small Industries Project (SSI I), which proposed expansion ofSSI financing by involving the five nationalized commercial banks (NCB) andcomplementing financial assistance with project components addressing techni-cal and marketing problems blockis.g SSI growth and diversificaLion. Theproject was appraised in June 1980, was signed in April 1981 and becameeffective in October 1981.

1.02 After a slow start, due mainly to the new institutional set-up,project implementation quickly accelerated, with the Credit fully disbursedon schedule by December 31, 1985. The credit component financed 654subprojects, resulting in investments of about US$80 million. Financing wentmainly to growth SSI subsectors as expected during appraisal, with concentra-tion in agro-industries, light-engineering and textiles. Average subloansize was about US$42,000, much lower than the maximum allowable amount ofUS$200,000, indicating that adequate credit access was maintained for smallerunits. The subprojects financed generated about 12,800 jobs at a cost perjob of about US$6,000. Annual incremental value added is estimated to beabout US$50 million. Ex-post financial rates of return of fully operationalsubprojects ranged between 18% and 45%.

1.03 SSI I had a substantial impact on the NCBs' organization and staffingfor SSI lending. At the headquarters of each bank, a Small IndustriesDepartment (SIi) was created to undertake project appraisal. Training on SSIlending procedures was imparted to SID officers as well as over 400 branchofficers. Although appraisal initially was centralized at the banks'headquarters, the branches were made responsible for receiving and screeningapplications, loan disbursement and administration and project supervision.Emphasis on project financing, in addition to creditworthiness analysis,sharpened the NCBs' project selection capabilities and improved their systemsand procedures. Given matching maturity funds under the credit, the PCIsincreased their portfolio of SSI loans by blending their own short-termfunds. Overall, the project improved SSI's access to institutional creditsources.

1.04 Implementation of the technical assistance (TA) components of SSI Iwere also completed on schedule. The impact of the TA components was lessimpressive than that of the subloan component, but still generally positive.The project established two service centers which provide focussed technicaltraining and services to a pre-identified clientele. The project preparation

-2-

fund was effective in assisting over 600 subloan applicants prepare theirloan applications and feasibility reports for submission to the PCIs.Subsector studies and area development studies have been prepared and arebeing utilized to improve project promotion and selection. The export promo-Lion component succeeded in introducing several Pakistani exporters andproducts to the U.S. market. Institution building of the TA agencies,however, was weak due to leck of qualified counlterpart staff and the poorperformance of some project advisors.

11. SECTORAL BACKGROUND

A. Economic Setting

2.01 Beginning in the late 1970s, COP embarked on a program of reforms toachieve financial stability, high growth and a revival of private sectorconfidence. Progress during Lhe Fifth Plan period (FY79-FY83) was con-siderable despite adverse external factors, including the 1979 oil shock,a world recession, a 30% decline in the external terms of trade, and theAfghanistan crisis with its attendant requirements for defense and refugeeassistance expenditures. GOP restored financial discipline by reducingbudget deficits and bank borrowings and by enforcing stricter monetarypolicies. Improvements in financial management were combined with priceadjustments, aimed at correcting economic distortions and a program oflonger-term reforms in key productive sectors. As a result of these actiuns,the economy, expanded rapidly, growing at an average of over 6%; inflationrates declined gradually, private sector confidence increased, and a manage-able balance of payments situation was maintained. Growth performance wasgood in industry, agriculture, energy and exports.

2.02 Pakistan's steadily improving economic performance was interrupted inFY84, due to an unexpected downturn in agriculture and migrant remittances,and the carry-over of inflationary pressures built-up in the previous year.GDP growth in FY84 slowed to 3.5% and pressures on thc- balance of paymentsemerged as the slowdown in the Middle East began to be reflected on remit-tance flows and lower demand for Pakistan exports. FY85 was again a dif-ficult year for Pakistan's economy. Although economic growth recovered fromthe slump in FY84, with real CDP growing at 8.4%, the balance of paymentscontinued the deterioration begun in FY84, and the budgetary outcome worsenedconsiderably. The current account deticit increased due to lower remittancesand exports, forcing a larger than expected drawdown on reserves, reducingthem to about two months worth of imports. Increased budget deficits, equiv-alent to 3.9% of GDP, resulted in larger government borrowings from thebanking system. Although economic growth in FY86 is likely to remain high,there is considerable uncertainty over Pakistan's external position and thebudget deficit.

B. The Industrial Sector

2.03 Pakistan has a reasonably diversified industrial base. Textiles,which accounted for about 30% of manufacturing value added in the early19O0s, now constitute only 15%. Other important sectors include foodprocessing, engineering goods, cement and fertilizers. Manufactured andsemi-manufactured goods represented over 70% of total exports, although morethan half are cotton products. Other major exports consist of carpets,leather products, synthetic textiles and fish products. Since the lateseventies, the government has assigned a lead role to the private sector in

-3-

industrial development, reversing to some extent, the nationalizations of themid-seventies, opening up areas for private investment and reducing invest-ment in public sector enterprises. PrivaLe industrial investment grew by anaverage of 16.6% p.a. during FY79-FY85. The private sector, which in FY79accounted for only 27% of manufacturing investment, increased its share to70% in FY85. The improved policy environment, which has contributed to aresurgence of private sector confidence, has led to increased growth inoutput and investment. During FY79-FY84, the real growth of manufacturingvalue added averaged 10.4% p.a., compared to 3.3% p.a. in the preceding fiveyears. Sectoral pertormance in FY85 remained strong, but growth slowed to8.6%. A similar rate of growth is anticipated for FY86 in line with recentproduction trends and investmenL levels.

2.04 Although improved industrial performance in the eighties has beennoteworthy, sustained growth will depend on continued improvements in theincentive structure, further relaxation of government controls, increasedavailability of infrastructure and improved performance of publicenterprises. The industrial sector continues to be promoted in a protectedenvironment, largely sustained by import substitution policies. Exports ar2considered marginaL to most production and investment decisions and tend tofluctuate in response to short-run changes in incentives. The tariff struc-ture requires modification to provide a more uniform level of effectiveprotection and reduce the import substitution bias. Although industrialcontrols have been liberalized, industry is still hampered by governmentcontrols on investments, imports, access to foreign exchange, company forma-tion and pricing. Infrastructure deficiencies, especially in energy, are amajor cause of project delays and undermine capacity utilization. Publicenterprises affected by price controls operate under cost-plus arrangementswhich discourage operational efficiency.

C. Financial Environment

2.05 The Financial Sector. The financial system in Pakistan consists of:five nationalized commercial banks (NCBs); seventeen foreign commercialbanks; four specialized scheduled banks; nine development finance institu-tions (DFIs); several insurance companies; two leasing companies; two stockexchanges; and a housing finance corporation. The State Bank of Pakistan(SBP), the central bank, regulates and supports the banking system withinoverall policies set by COP. The Pakistan Banking Council (PBC) oversees andcoordinates the activities of the NCBs and fulfills many of the functionspreviously discharged by their former private shareholders. The Ministry ofFinance monitors the operations of the other financial institutions. Thecommercial banking sector is the most important part of the financial system,with total assets as of June 30, 1985 of Rs 320 billion, or about 90% of thetotal assets of the system. In turn, the NCBs account for 90% of the bankingbusiness in the country. NCBs are also important in terms of geographiccoverage, with 7,000 branches Lhroughout the country.

2.06 Two important developments have characterized the financial environ-ment recently. The first is the diversification of functions by the institu-tions in the system. Unlike in the past when the commercial banks wereengaged mainly in short-term lending and the development finance institutionsin long-term lending, the commercial banks now provide more long-term financ-ing to agriculture and industry while the development finance institutionsnow complement their term loans with short-term working capital loans. Theinvestment banks rely on the commercial banks to back up their .nderwritillgcommitments. Leasing companies are being established by commercial banks and

-4-

DFIs. With these developments, the system has acquired some flexibility, butthe general approach by GOP and the central bank is one of cautious andmeasured steps. A similar approach has characterized GOP's pursuit ofIslamization of the financial system. Initial but limited steps to abolish"riba", or interest, from the system were taken in 1981, but it was only fromJuly 1985 that all domestic currency transactions have been based on newfinancing modes consistent with Islamic principles. New financing arrange-ments include: (i) mark-up, a purchase and corresponding future re-purchaseof assets with a profit margin which varies according to the length of theinterval between the two transactions; (ii) Term Finance Certificates (TFCs),bonds with a risk premium; (iii) Musharika, loans designed to meet workingcapital needs on a profit sharing basis according to pre-agreed formula;(iv) K.odaraba companies, investment funds operating in accordance withIslamic tenets; and (v) hire-purchase and leasing.

D. Small Scale Industries Sector

2.07 Characteristics and Performance. GOP traditionally has attachedimportance to the SSI sector. Already in 1959, a committee was formed toexamine means to promote small industrial and agricultural activities and inthe sixties, institutions were established to serve the needs of smallenterprises. Following the separation of East Pakistan, Small IndustriesCorporations were formed at the provincial level to channel government assis-tance to the sector. Aside from the obvious social objectives of thesemeasures, considerations of industrial development also have been importantin GOP support of SSI. Generally, small firms are less affected by economicvariations, are less vulnerable and sensitive to political changes, generatea good portion of their capital needs from the informal capital markets andrequire less infrastructural support than do larger firms. These factorshelp explain why small scale industries continued to grow during the dif-ficult years of the seventies, while output from larger firms declined. Inthe 1980s, investments in small firms represented 18% to 27% of totalindustrial investments. In recent years, SSIs have constituted close to 4.7%of GDP, 27% of industrial value added, and 30% of manufactured exports. SSIsemploy about two million workers in about 100,000 establishments.

2.08 The majority of SSIs are located in the provinces of Punjab and Sind,with a smaller proportion in NWFP and Baluchistan. This geographic distribu-tion reflects population concentrations, availability of raw materials andinfrastructure, access to markets and local entrepreneurship. Traditionally,SSI units concentrated on processing local raw materials, such as cotton andother agricultural products. More recently, egpansion has been notable infood processing, engineering products and construction materials. Other keySSI activities focused on exports on the basis of adding value to importedraw material, and are characterized by carpets, sports goods, cutlery andsurgical instruments.

2.09 Policy Environment and Development Strategy. GOP's policies forindustrial development do not differentiate between large and small industry.Rather than protecting or subsidizing small firms, the Government has main-tained a strategy of increasing SSIs' access to credit and technicalservices. SSIs are allowed to set up and operate with little regulation,and market signals are the main determinants of SSI investments and theirviability. GOP's policy provides that all SSIs be in the private sector.Subsectors with strong potential, high value added, and limited economies ofscale are promoted. There is a push to develop SSIs in more remote urban andrural areas, but this objective again is pursued by promotion and provision

-5-

of services, rather than through subsidization. There is, however, a strongtendency to provide credit to SSI at rates lower than that for largeindustry.

2.10 Technical Assistance for SSI. The promotional and technicalassistance activities in support of SSI are a provincial governmentresponsibility, carried out by the Punjab Small Industries Corporation(PSIC), the Sind Small Industries Corporation (SSIC), the Small IndustriesDevelopment Board (SIDB) of NWFP, and the Directorate for Small Industries(DSI) in Baluchistan. 1/ These organizations used to be area offices of theWest Pakistan Small Industries Corporation, established in 1965 in Lahore anddivided along provincial lines in 1972. Consequently, their policies,outlook, organizational structure, and programs of assistance are similar,although PSIC is the best organized and has the largest technical staff.PSIC has directed most of its assistance to the organized small industrysector in the Lahore, Guiranwala, and Sialkot districts. The Punjab is thecenter for the manufacture of sport goods, cutlery, and surgical instrumentsand also has a large concentration of small manufacturers of other engineer-ing products.

2.11 To a large extent, the SICs have focused their assistance to thesector on providing physical facilities, developing industrial estates,building and equipping service centers, and establishing training and produc-tion centers for handicrafts. Insufficient attention has been given tobuilding effective programs to promote viable new enterprises and to provideextension services to existing firms. The project encouraged the SICs todevelop these services through subsector studies, project development, andpractical export promotion components. The SICs will need to continue tobuild their capabilities in these and other "soft-ware" aspects of SSIpromotion.

2.12 SSI Financing. With the introduction of the SSI lending programunder this project, GOP abolished the special credit schemes jointlyadministered by the provincial Small Industries Corporations (SIC) and theNCBs which proved to be ineffective. These schemes were not only small andfragmented due to the cumbersome institutional arrangements but also resultedin overlapping responsibilities, institutional frictions, delays in loanprocessing and finally, poor loan recovery performance. Moreover, concernswith lending drew the SICs away from the other important functions of SSIpromotion and extension services. The project succeeded in rationalizinginstitutional roles by assigning the lending function completely to thecommercial banks and reorienting the SICs toward technical assistance.

2.13 C.rrently, the NCBs have sole responsibility for the SSI lendingsystem. To ensure SSI's access to credit, annual targets for loans to thesector, expressed as net increments to the amount of outstanding SSI loans,are set by the State Bank of Pakistan based on COP's Annual Development Planprojections for SSI investments and value-added growth. These are thendivided among the five banks on the basis of deposit size. Achievement oftarget levels is monitored monthly; the targets themselves are revised duringthe year in reaction to actual credit demand from SSI for investment andworking capital. Since these targets have been quite conservative in rela-tion to SSI needs, contributing about 30% of SSI requirements, they have not

1/ The acronym SIC in this report refers to all of these agencies.

-6-

resulted in undt'e allocation to SSI. On the other hand, they do not repre-sent a constraint since they can be exceeded, as they have been in recentyears. Since IDA funds were made available in FY82, SSI loans by the commer-cial banks increased substantially, meeting about 40% of SSI investmentrequirements, up from about 30% in prior years. Moreover, with theavailability of long term funds from IDA, fixed investment loans haveincreased. IDA also assisted the NCBs in building their capabilities for SSIproject financing by improving subproject selection through better projectappraisal skills; improving systems and procedures to shorten loan processingtime; strengthening credit discipline to improve loan recovery; and expandingtraining and advisory services to reach more branches as decentralizationincreased.

III. PROJECT DESCRIPTION

A. Origin

3.01 In view of SSI's important role in achieving its economic and socialobjectives, GOP has placed high priority to assistance for the SSI sector.This role was particularly evident in the 1970s when SSIs continued to growwhiLe output from larger industrial enterprises declined in view ofnationalization, labor unrest and loss of private sector confidence. Toexpand its support for the SSI sector, GOP approached IDA for a credit tofinance SSI development. In February 1977, IDA undertook a project iden-tification mission which recommended preparation by the Ministry ofIndustries of a project focusing not only on financial assistance butbroadening the approach to include technical and marketing services for SSI.To assist the Ministry in preparing the project, UNIDO, with IDA assistanceon study design, undertook a study of five important SSI subsectors whichwas supposed to assess their status, analyze their problems and growthprospects and recommend policies and assistance programs for the sector. Thestudy was completed in mid-1979.

3.02 On the basis of findings of this study, project preparation andpre-appraisal missions were undertaken in November 1979 and February 1980,r.espectively, to develop project components and institutional -.rangements.With the assistance of two consultants, appraisal was undertaken in June1980. Negotiations were completed in January 1981. The credit was sub-sequently approved in February 1981, signed in April 1981 and became effec-tive in October 1981. The delay between signing and effectiveness was prin-cipally due to the fact that conditions of effectiveness affected six banksand four provincial agencies, only one of which had a prior relationship withIDA. All four conditions of effectiveness, however, were considered to beminimum requirements.

B. Proiect Objectives

3.03 Aside from the traditional objective of providing investment loansfor the establishment or expansion of SSI units, the project aimed at expand-ing SSI assistance beyond credit to include technical and marketing assis-tance and improving the effectiveness of the credit and technical assistancedelivery system by clarifying institutional roles and improving coordinationamong institutions. Specifically, the project aimed to: (a) encourage thedevelopment of SSI units that are export-oriented or are efficient in importsubstitution by providing funds for term lending through the commercialbanks; (b) assist in orienting the commercial banks toward a longer-term

-7-

project appraisal approach in their SSI lending; (c) assist two SICs inproviding selected technical assistance, extension services and skills train-ing in woodworking and leather goods; (d) expand the export promotion of SSIproducts; and (e) initiate project development exercises in Baluchistan.

3.04 In the past, SSI financing was carried out jointly by the commercialbanks and IDBP and the provincial Small Industries Corporations (SIC) underspecial schemes which had been developed in an ad hoc fashion. These schemeswere not only small and fragmented due to cumbersome institutional arrange-ments but also resulted in overlapping responsibilities, institutionalfriction, delays in loan processing and poor loan recovery performance.Under the project, GOP agreed to abolish these special credit schemes andassign full responsibility for SSI financing to the banks. Concomitantly,the project provided support to the SICs to reorient them toward technicalassistance and assisted some of their programs in which the SICs had beenmore effective.

3.05 T:ie project aimed at building on the State Bank of Pakistan's (SBP)program for SSI financing under which the NCBs were given annual targets forloans to the sector. While the institutional set-up was basically sound,some aspects of the system needed improvement. Most of the lending underthis program was in the form of short-term facilities and was carried outprincipally on the basis of creditworthiness analysis. The project aimed atincreasing the volume of investment financing by providing the NCBs withlong-term resources with which to blend their short-term funds to achieveprudent term transformation. Moreover, the project provided technical assis-tance to the NCBs to assist them in building their capability for SSI projectfinancing by improving subproject selection through better project appraisalskills; improving systems and procedures to shorten loan processing time andachieve satisfactory loan recovery performance and increase decentralizationto improve access of SSIs outside the main urban centers.

C. Project Components

3.06 To achieve the above objectives the project had the followingcomponents:

(a) A credit component involving a line of credit onlent to the five NCBsfor investment financing of SSI units which met eligibility criteriaand were financially and economically viable;

(b) technical assistance for the NCBs in terms of training and advisoryservices in project promotion. appraisal and supervision;

(c) establishment of two service centers which would provide commonfacilities, training, demonstration and extension services to SSIunits in woodworking and leather goods;

(d) export promotion of selected handicrafts and SSI products in the U.S.market;

(e) project development assistance for the under-developed province ofBaluchistan; and

(f) a project preparation facility by which the SICs could assistprospective loan applicants in project preparation and loanapplication.

-8-

TV. PROJECT IMPLEMENTATION

A. Subloan Component

1. Start-jp

4.01 After the Credit became effective in October 1981, it took sevenmonths for subloan processing to start in earnest. The appraisal forecast ofthree months was too optimistic considering that the institutional set-up wasaltogether new, the loan processing procedures were different from thosewhich the banks were used to, the program had to be advertised and promotedintensively throughout the country and SSI officers of the PCIs had to bebriefed on the program and trained in project appraisal and supervision.

4.02 Training of SSI officers of the PCIs commenced in November 1981 andwas completed in March 1982 and comprised a five-week intensive trainingcourse on project appraisal and supervision for 15 key staff of the newlyestablished Small Industries Departments (SID) of the banks and severalthree-day orientation courses for 195 branch officers. To rEinforce thetraining courses, IDBP and the Pakistan Banking Council (PBC) prepared alending manual which spelled out lending policies and procedures as well asguidelines on project appraisal and supervision for the use of SSI officers.Application, appraisal and reporting formats were developed and standardizedto facilitate loan processing and ensure close monitoring of the project.

4.03 On completion of the training program, IDBP, PBC and the bankslaunched a nation-wide promotion campaign to inform the private sector of thenew lending program and develop a pipeline. In April 1982, a team of IDBP,PBC and bank personnel conducted information seminars for chami;rs of com-merce and industry in provincial capitals and other major cities. Newspaperadvertisements and other media coverage were also used. Brochures on ihescheme in English and the local language were distributed and posters wereposted in bank branches and other prominent places. The SICs conducted theirown promotion campaign through seminars and through contacts with industrialestate occupants and their other SSI clients. The Punjab Small IndustriesCorporation was the first to start performing its project preparation roleunder the project preparation facility to depelop a pipeline for the banks.

2. Timetable

4,04 After completion of all the preparatory work, subloan processingstarted in earnest in May 1982, seven months after Credit effectiveness.Nevertheless, the subloan component was fully committed by September 1983 orin about 18 months, half the time expected at appraisal. Thus while theappraisal report was too optimistic in estimating start-up time, it was tooconservative in estimating subloan commitment time. Rapid commitment ofsubloans was principally due to the existence of pent-up demand for credit bySSI which, up to then, had limited access to investment funds from institu-tional sources. Moreover, the NCBs proved to be more efficient in loanprocessing compared with our experience with SSI financing by the DFIs, withmuch shorter elapsed time between application and loan decision.

4.05 Disbursement on the subloans were expected at appraisal to be com-pleted in four years from Board date. Despite the delay in start-up,disbursements on subloans were completed on time or in ebout three and a half

-9-

years. This was accomplished despite lack of a revolving fund which madereimbursement procedures more cumbersome considering the large number ofsmall expenditures on a large number of small subloans. On the basis of thisexperience, a revolving fund was created for the Second SSI Project.

3. Subproject Apprasl

4.06 As envisaged at appraisal, two subproject appraisal procedures wereestablished, one for small subloans (free-limit subloans of less thanRs 800,000 or about US$75,000 equivalent) and one for larger subloans(Rs 800,000 up to Rs 3 milliton or US$280,000). For small subloans, appraisalreports were simplified focusing on financial analysis to determine financialviability and using eligibility criteria and project profiles to assesseconomic merit. For larger subloans and, particularly for new companies,appraisal reports were more detailed and were supposed to include financialand economic analyses.

4.07 In general, the quality of appraisals by the PCIs for small subloanswas satisfactory and appraisal procedures were established without majorproblems since the short-form appraisal was quite similar to what the PCIswere used to under their own lending program. The PCIs had more difficultieswith the long form appraisal for larger subloans and it took time and on-the-job counseling by IDBP before appraisal reports could meet requiredstandards. Difficulty with the long form appraisal was also a factor why thePCIs tended to concentrate on small subloans (para 5.01). Report presenta-tion was initially poor and analysis was particularly weak for the marketingand technica' aspects of subprojects. There were weaknesses also in assess-ing the availability of technical know-how and raw materials and in estimat-ing market demand. With additional training and counseling by IDBP, thequality of appraisals improved in the later part of project implementation.

4.08 Based on a 10% sample of subprojects visited, it was found that,despite weaknesses in appraisal reports, lending decisions were basicallysound. The quality of sponsor selection was high, with a good balancebetween existing and new clients and between traditional and newentrepreneurs. The PCIs ensured that, in cases of subprojects with complexprocesses, the sponsors were able to obtain the necessary technical knowhowthrough foreign collaboration or by employing techtnical personnel. However,there was a tendency to underestimate working capital requirements and toover-invest in buildings. These were corrected under SSI II by limitingeligibility for building expenditures and reviewing working capital calcula-tions more closely.

4. Supervision and Collection Performance

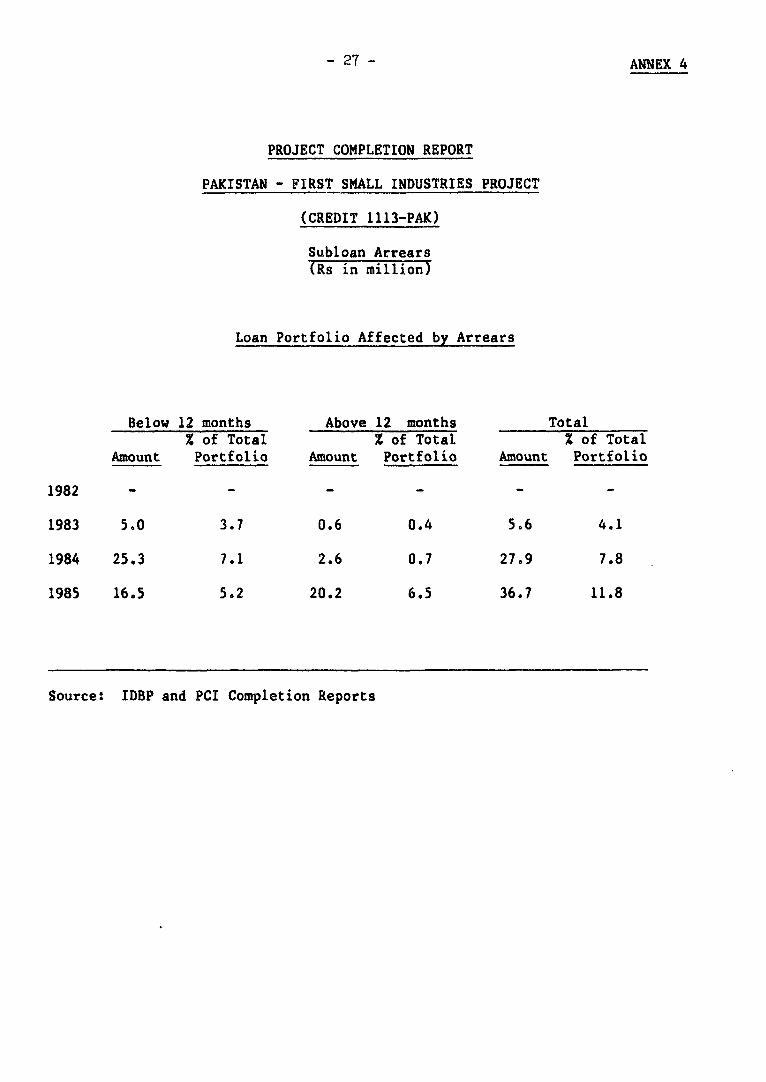

4.09 At the beginning, insti.ution building for the PCIs emphasizeddeveloping capability for subproject appraisal and installing systems forsubloan disbursements. Not enough attention was paid to project supervisionand end-use monitoring, resulting in an initially poor collectionperformance. In May 1984, when the first reports on collections weregathered and analyzed, the collection ratio of all the PCIs averaged only47%. A Bank mission highlighted this problem in its discussions with thePCIs and GOP and proposed several measures to address the problem before itdeteriorated. The banks responded by conducting an intensive collectiondrive during which all subprojects were visited, The collection ratioimproved to 64% by September 1984. By June 1986, the collection ratio fur-ther improved to 82%, as the banks continued to streamline their system and

-10-

procedures for collection, including timely billing of clients, moreorganized and frequent follow-up on defaulting borrowers and use of authorityto offset loan overdues with credit balance of borrowers. Also, the generalcredit environment improved as GOP supported the fluancial institutions intheir drive to improve overall portfolio quality. A major reason forimprovement in the overall credit system was the establishment of well func-tioning credit committees at several levels of management whereby defaultersare blacklisted and become unable to avail of new credit facilities.

5. eporting

4.10 The DCA had required that the banks submit semi-annual progressreports on subloan commitments, disbursements, recoveries and arrears whichIDBP was supposed to consolidate for submission to IDA. In practice, whathappened was that banks submitted fcrtnightly status reports to the PBC andIDBP which were used to monitor implementation progress internally. Reportsfrom IDBP were prepared and submitted only for supervision missions ratherthan regularly on a semi-annual basis. While it did not meet the letter ofthe agreement, this practice was considered satisfactory since supervisionmissions were undertaken practically on a six-monthly basis and making reportsubmission coincide with supervision missions highlighted the importance ofthe report and ensured its review by Bank staff and feedback to theimplementing institutions. The reports were found to to be up-to-date,accurate and complete but were weak in analyzing policy issues and proposingmore medium-term strategies.

4,11 Audit reports of the banks were submitted regularly and on time asrequired by the DCA. Audit reports were prepared by the regular auditors ofthese banks which are local private auditing firms in Pakistan. Auditreports have been found satisfactory. However, they were deficient in thatthey did not contain a separate opinion by the auditors on the adequacy ofSOEs as required by the DCA. This deficiency was not identified during thecourse of project implementation. However, after the in-depth review ofcompliance with audit covenants carried out during a regional projectimplementation review (PIR), this deficiency was found and subsequentlycorrected under the Second SSI Project.

6. Procurements and Disbursements

4.12 Considering the large number and the small value of items to beprocured under many small subloans, IDA agreed to allow the banks to usetheir existing procurement procedures provided due care was taken to ensurethat prices were reasonable and competitive, taking into account relevantfactors such as time of delivery, quality and reliability of goods andavailability of maintenance facilities and spare parts. To ensure that theprocurement and disbursement procedures of the banks were sacisfactory andcontinued to be so, an intensive review of procurement and disbursementprocedures of sample bank branches was undertaken by a team consisting of arepresentative from the Bank's resident mission, as team leader, and of IDBP,PBC and the headquarters of concerned banks, as members. This review was.onducted twice during the project life and was able to ide.ntify weaknessesin the banks' procedures. Corrective measures were proposed and brought tothe attention of PBC and the management of the banks. These were quicklytransmitted back to the branches for implementation. Although the secondreview was able to identify other weaknesses in the system, it also found outthat most of the earlier weaknesses had been corrected by the banks. This

-11-

practice has been found very useful and should be extended to similar IDAoperations.

B. Technical Assistance Components

1. Gujrat Woodworking Service Center (GWSC)

4.13 Objectives. The Gujrat Woodworking Service Center was establishedto assist the traditional wooden furniture manufacturing industry in adaptingto changing technology and market conditions in order to improve viabilityand profitability. lo achieve this objective, the center was to provide thefollowing services to industry: (a) an extension program which would provideplanned in-plant advisory services to individual units to guide them inimproving technology and production methods; (b) common facilities for equip-ment which are not economic for each unit to acquire; (c) training of skilledworkers and machine operators on a two-year curriculum program for newrecruits and short-term evening sessions for existing industry workers;(d) design of standardized furniture which could be produced more efficientlyby the industry; and (e) commercial production, utilizing 60% of plantcapacity to provide demonstration of efficient production methods, laboratoryconditions for the extension progran. and actual factory situation for thetraining program. Income from the commercial production was to be used tocross-subs;dize the promotional aspects. The center was to be under theadministrative umbrella of the Punjab Small Industries Corporation (PSIC)but operate under a management committee including representatives from theprivate sector (Gujrat Furniture Makers Association-GFMA) to ensure continu-ing relevance with industry needs. The total cost of the center wasestimated at US$1.73 million of which IDA was to finance US$1.23 million.

4.14 Project Implementation. GWSC was completed and has been fully opera-tional since September 1984. There was an implementation delay of about9 months caused by the contractors for the buildings. After completing thestrucEure and receiving a major portion of the c)ntract price, the contractorlost interest in completing the work as he had taken up other contracts inthe area. However, the quality of the work done, when finally completed, wassatisfactory. Machinery was procu.ed without any problems on the recommenda-tion of the advisors of the project. The performance of the project advisorswhose assignment was completed in June 1985 was considered satisfactory byPSIC. The project was completed at a total foreign cost of US$1.08 millionand local cost of US$430,000 equivalent compared with the appraisal estimateof US$1.23 million plus US$500,000 equivalent in local currency, resulting insavings of US$220,000 equivalent. The savings came mainly from lower expen-ditures on consultant services and local currency devaluation.

4.15 The management committee with two private sector representatives fromCFAA was organized as envisioned at appraisal. This arrangement has ensuredparticipation of the private sector in policy formulation and management ofthe center and has improved communication between PSIC and the privatesector. This is manifested by the high demand for the center's training andextension facilities. Two batches of trainees for the two-year certificatecourse have started and will be completed in November 1986 and November 1987,respectively. Special courses of 4 to 6 weeks have been conducted for exist-ing industry workers to improve production skills on modern woodworkingmachinery. Common facilities comprising wood seasoning, hydraulic pressingof plastic laminations and plywood, sharpening of blades, saws and cuLtershave been extended to about 25 small woodworking units. Extension servicesrelating to productivity improvements and improvements in the quality and

-12-

design of products have been provided to 224 private woodworking units.iWSC's design and work preparation section is also fully operational and hasintroduced new designs, prepared production layouts and cost estimates whichwere then implemented by the production department. Production based on joborders worth Rs 1.2 million were executed in FY85. During FY86 orders worthRs 2.3 million have been executed while orders worth another Rs 8.2 millionwere pending. During FY87, GWSC is expected to become profitable by achiev-

ing full capacity utilization of Rs 8 million production per year.

4.16 The center is thus well on ics way to achieving all the objectivesset out at appraisal and will be a model of modern furniture manufacturingunit demonstrating use of up-to-date technology, machinery and productionmethods. It has stimulated the furniture manufacturing industry of the area

by demonstrating the benefits of utilizing modern technology, changing overto straight-line standardized designs suitable for mass production and use ofmodern machinery.

2. Bannu Leather Goods Service Centre (BLGSC)

4.17 Objectives. BLGSC was established with the objective of helpingtraditional shoe manufacturers in and around the Bannu area diversify intonon-footwear leather goods manufacture in response to changed marketconditions. The assistance to the target group through a multi-functional

service center was to consist of re-training of the labor force inappropriate skills; demonstration of the proper set-up and management of aleather goods unit; assistance in setting up individual workshops; and,through subcontracting, provision of the lead in developing domestic andexport markets. The initial emphasis of the center was to be on training.Further, a major element was subcontracting whereby the center would develop

the market and, concurrently, provide practical technical assistance to theindustry at the production end. Under this arrangement, the center wouldconcern itself with centralized functions such as securing orders accordingto the center's and the industry's capabilities; procuring and selecting rawmaterials according to market requirements; preparing initial proto-types andpatterns; undertaking preparatory processes to produce components ready forassembly by industry; distributing work among the subcontractors with in-plant technical guidance and training; and collecting products for furtherfinishing and marketing. The center was also to provide assistance to opera-tions of individual units outside the subcontracting scheme through provisionof common facilities in design preparation, pattern cutting and otherfacilities not available in individual units; and extension services throughregular plant visits by an extension unit to be run by the center. The total

cost of the center was estimated at US$1.47 million of which IDA was tofinance US$1.02 million.

4.18 Project Implementation. The project, although completed and partiallyoperational, has been faced with many implementation problems. Completionwas delayed by about one year due to the delay in hiring consultants.Moreover, the Small Industry Development Board (SIDB) faced procurementproblems since responses from suppliers to bids for machinery were notsatisfactory. The situation was rectified only after the advisor hadarrived, modified the specifications and used his personal contacts. The

project, being located in Bannu, an isolated and underdeveloped area, has

also suffered from staffing problems particularly at the senior levels. Thecenter, in effect, is being managed by the SIDB from Peshawar, the provincialcapital, and considering the distance and other communications problems inthe area, this arrangement has been a poor alternative. Finally, the project

-13-

faced serious problems with the building design and the civil contractors.The buildings were eventually completed only in early 1985 after many dis-putes with the contractors. Even now the main building is defective and doesnot provide sufficient protection agai.ist the extreme heat and cold in Bannu.SIDB is undertaking repairs of the buildings but the design is basicallydefective. The total cost of the center was US$0.97 million in foreita costand Rs 6.02 million in local costs compared with the appraisal estimate ofUS$1.02 million and Rs 4.5 million, respectively. The cost overrun in localcosts was mainly due to problems with the buildings.

4.19 The management committee including private sector representativesfrom the Bannu Leather and Shoe Manufacturers Association (BLSMA) is func-tioning satisfactorily. A basic training course for 20 trainees has alreadybeen completed and another batch of 20 is currently attending a similarcourse which includes pattern making, cutting, sewing and assembling.Specialized training in new designs and the operation of the machinery in thecenter was recently started. The center has so far produced and sold leathergoods worth Rs 6 million and Rs 1 million, respectively. The quality of thefinished goods produced by the center is high and has attracted manyinquiries from the local market. The management is also exploring exportpossibilities. The project has also made a beginning in providing the avail-able common facilities by providing skiving and splitting facilities to someof the shoe makers in the area. The center also plans to start providingassistance in setting up individual workshops as envisaged, as the needarises. However, it is likely to take about 2 years before the center canbecome a model of a well established, managed and financially viable leathergoods unit. The completion of the project and high quality of its productshave demonstrated that such centers can be set up in backward areas butimplementation problems can be many. Frequent supervision visits by Bankstaff were useful in minimizing implementation delays.

3. Export Promotion

4.20 Objectives. The export promotion component was designed to provide apractical dimension to the export promotion activities of the ExportPromotion Bureau (EPB) and the Sind Small Industries Corporation (SSIC), byfocusing on practical product adaptation exercises and marketing activitiesfor selected handicrafts and small industry products. Following a typicalmarketing cycle, all the activities from product selecting, pinpointing ofsuppliers, product designing/redesigning up to buyer matching and the holdingof specific marketing events were to be integrated for each product categoryin order to achieve sales in the short term and improve market access in thelong term. Marketing events were to include participation in single-countrytrade fairs, in multi-country, product-specific fairs and sales exposuretrips to the U.S., the target market, by promising SSI producers. Selectionof product candidates was to be made by EPB and SSIC, in consultation withthe private sector, based on export performance in the past and potential inthe market place. EPB was to implement the export promotion for manufacturedproducts and SSIC for handicrafts. Marketing and design consultants were tobe hired to assist EPB and SSIC in executing this component. The foreignexchange cost in terms of advisers and marketing events was estimated atUS$500,000 for SSIC and US$500,000 for EPB. The counterpart agencies were toprovide funds for counterpart staff and other local costs estimated atUS$200,000 equivalent.

4.21 Project Implementation. EPB and SSIC engaged a UN agency to provideconsultancy services in the fields of product design and marketing. In

-14-

addition, the agency also provided short-term (two-month duration)specialists for specific product lines such as lacquer craft, leather goodsand jewelry. Furthermore, it appointed the Pakistan Design Institute (PDI)in Karachi as consultant/advisor for onyx crafts and woolen durries. On thebasis of preliminary surveys, EPB and the advisors decided to concentrate onfive subsectors, namely, leather garments, leather goods, sports goods,surgical instruments and cutlery. Ninety one samples were sent to the U.S.A.for market tests of which 55 were found promising. Counter samples of theseand other products were produced and displayed in various exhibitions in theU.S.A. As a result, orders worth about US$750,000 were booked.

4.22 On the basis of local surveys and subsequent feedback on theirsamples from the marketing advisor, SSIC focused on onyx craft, wood craft,brass and copperware, silver jewelry, bone carvings and jewelry, glass beads,lacquer craft, woolen durries and shawls, ajrak (a Sindi cloth) and blockprinted cloth. Samples were displayed in the Dallas, Los Angeles and NewYork gift shows during 1986. At these shows the SSIC's handicraft shopobtained trial orders worth US$20,000 mainly for items made of onyx, brass,copper, wood, and white metal jewelrv. Six other participating exporters andmanufacturers booked some sample and triai orders.

4.23 Out of the US$500,000 IDA contribution towards EPB's export promotionproject, US$400,000 was used to pay the agency, resulting in a saving ofUS$100,000. The saving was due to slower than expected implementation of theproject caused mainly by agency's inability to appoint consultants on time.Total expenditure on SSIC's component was US$470,000 including expenditureincurred for follow-up marketing activities.

4.24 EPB and SSIC were generally dissatisfied with the performance of themarketing and product design advisors. The former never worked for anysustained period due to personal problems and the latter was a generalist andnot the specialist specified in the terms of reference. The consultingagency failed to replace the advisors for over a year resulting in delayedimplementation. Moreover, the advisor who was finally sent as a replacementdid not provide EPB with sufficient market feedback based on his marketsurvey as agreed. EPB found that the advisors were weak in developingappropriate marketing strategies for the product groups selected and inarranging participation in trade exhibitions. The performance of short-termexperts provided to EPB and SSIC on leather garments, lacquer craft andjewelry was considered satisfactory.

4.25 Due to the delay in project implementation and the weakness of theadvisors, the objectives of the export promotion component could not beachieved fully. However, the exporters who participated in this projectgained valuable experience in the U.S. market and acquired knowledge ofmarketing practices, attitudes and channels in the U.S. Useful leads havebeen provided through trial orders in some product areas which need to bepursued for further development. The consuLtants employed for this componentwere not very effective since they did not exactly have the right qualifica-tions for the job. Due to bureaucratic procedures, the consulting agencycould not quickly engage or replace consultants. It may be more appropriateto employ private sector advisors who have more flexibility and to compensatethem based on performance in the marketplace. Although the objectives of theexport components could not be fully realized, it has nevertheless providedvaluable initial exposure of Pakistani exporters and produrts to the U.S.market. A follow-up to this effort, modified to correct earlier weaknesses,is included under the proposed third project.

-15-

4. Project Development for Baluchistan

4.26 Objectives. Baluchistan is the least developed of the four provincesof Pakis_an with little industrial activity. This component was thereforeconceived with the objective of assisting the Government of Baluchistan inproject identification and promotion by preparing project proposals based onopportuinities in the province and promoting them to the private sector. IDAwas to finance a team of four iubsector specialists who would identify fiveto Len projects Laking into aLcounlt Baluchistan's resources; namely, animalskins, fruit and vegetables, marble (onyx), and wooL. The team was toanalyze the present production and market structures and develop projects ,pto the feasibility study stage, including formulation of financial plans.This component was to be carried out by a team of four over a three and ahalf month period. The total cost was estimated at US$110,000 of which IDAwas to finance the foreign exchange cost of about US$100,000.

4.27 Project Implementation. The Government of Baluchistan awarded theconsultancy work to a local consultancy companv based in Karachi. The workcompleted bv the consultants included the iollowing reports: (a) sectoralbackground providing sectoral analysis, industrial problems and prospects,pre-conditions lor development and area protile for the province ofBaluchistan; (b) subsectoral studies on fisheries, minerals, leather, wool,fruits and vegetables and agro-based industr:es; (c) general opportunitystudy summarizing findings of all the subsector studies and outlining astrategy for Baluchistan's industrial development; and (d) ten feasibilitystudies on projects selected by Government of Baluchistan. The entireallocation of US$100,000 was spent on the preparation of these studies and onsubsequent activities to promote these projects to the private sector.

4.28 While the consultants completed the preparation of studiessatisfactorily, they could not fully train counterpart staff and institution-alize the project preparation function within the Department of SmallIndustries of the Government of Baluchistan due to lack of counterpart staff.The government was unable to find qualified personnel and could not set up aunit for this purpose. Without this unit responsible for project promotionand development, the useful work done under this component remains largelyunutilized so far. Under the Second SSI Project now being implemented, aprovision was made for assisting the Government of Baluchistan in setting upsuch a unit.

5. Fund for Subsector Studies and Project Preparation

4.29 Objectives. One of the objectives of the project was to improve SSIlending and technical assistance operations by moving from a general approachto a subsector-specific approach. To extend the coverage of lending andtechnical services to more subsectors, funds were provided under the projectfor studies that would assess growth potential and estimate investment andcredit requirements of SSI subsectors, analyze technological choices, iden-tify geographic areas where subsectors should be promoted or expanded, iden-tify technical assistance needs and develop subsector norms to facilitate andimprove the banks project appraisals for lending. It was also expected thatsome prospective borrowers under the credit component, especially the smallerones, would be unable to prepare their own project proposals in a mannerrequired ly the banks for project appraisal purposes. For existing projects,a major problem a.rea was reconstructing operating performance from inadequaterecords. For net' projects, problems were foreseen in market research and

-16-

analysis and preparation of financial projections. Part of the fund there-fore was to be used to finance the costs of project preparation by the SICs.On requ?st by a borrower or a banker, the SICs would undertake projectpreparation free of charge and receive compensation from the fund accordingto a fixed schedule of fees and with proper screening and approvalprocedures. US$500,000 was allocated to the fund, with US$250,000 each forsubsector studies and project prepara.ion.

4.30 Implementation. The Subsector and Project Preparation Fund wasestablished within IDBP which awarded the contract for subsector studies to aconsulting group which completed studies on the following subsecto.s: cook-ing and other household equipment; agricultural equipment and parts; automo-tive parts/accessories; marble products; agro-based industries; export-oriented vegetable and fruit processing and preservation; milk and milkproducts (dairy products); industries based on agricultural produce (cornproducts); furniture/wood-working products; surgical instruments; cutlery;sports goods; and ready-made garments. The studies assess the status,problems and prospects of these sectors and include project profiles inaccordance with the objectives agreed at appraisal. Due to the delay inselection of consultants the studies were delayed by about two years and werecompleted only in early 1986. As the credit component was already fullydisbursed by that time, the studies are being used by the PCIs for the secondproject.

4.31 In general, the quiality of the studies prepared was considered satis-factory by the banks. In addition, the consultants also prepared projectprofiles which the banks are using for project appraisal purposes. Under theproject preparation facility, over 600 small investors were assisted inpreparing their loan applications. Among the SICs, PSIC was the most activein providing the service followed by SSIC and SIDB. The DSJ of Baluchistan,as expected, could not provide this service due to lack of ql-alified staff.Assistance to build DSI was included in the second project.

V. PROJECT IMPACT

A. Subprojects Financed I/

5.01 Subloan Characteristics. The subloan component of the projectfinanced 654 units, about 40% more than the appraisal estimate of 475 units.This was because subloans were smaller than expected. The average subloansize was US$42,000, smaller thani appraisal estimates and much smaller thanthe maxirum amount allowed of US$200,000. Also, the breakdown between free-limit subloans (subloans of less than Rs 800,000) and above free-limit sub-loans was 85:15, compared to the DCA requirement that at least 50% should befree-limit subloans, indicating that a large percentage of subioans were forsmaller enterprises. While this pattern indicates that the PCIs paid suffi-cient attention to smaller borrowers, it is also due to the fact thatappraisal procedures were easier for smaller subloacis (para 4.07). Subloanshad an average maturity of 7 years and 3 months, showing the PCIs willingnessto increase loan maturities to match investment requirements given matchingfunds and sufficient margins. On average, subloans were applied to finance

1/ Annex 2 provides tables detailing the characteristics of the sub-projects financed under this Credit.

-17-

factory building constructions (20%), machinery and equipment (65%) andpermanent working capital (15%). Only 10% of subloan amounts were used inforeign exchange for direct imports by subborrowers; most subloans financedlocal goods as well as imported but locally available goods. Including theseindirect foreign costs, the foreign exchange application of subloans wasabout 30%, as expected at appraisal. The average equity contribution ofsponsors was 59%, much higher than expected at appraisal (40%) and the mini-mum equity requirement of 30%. This resulted in greater domestic resourcemobilization than expected and str ',er capital structuring of subprojects bythe PCIs. Overall, the financing .ttern was as follows: sponsor's equity59%, PCI financing of 8% and IDA financing of 33%. The subloan component ofUS$2t million equivalent thus generated investments of about US$80 millionequivalent, 45% higher than the appraisal estimate of US$54 millionequivalent.

5.02 Subsector Distribution. The subloan component financed 433 new and221 balancing, modernization, replacement and expansion (BMRE) subprojects,indicating that the PCIs stressed the financing of new businesses therebyexpanding credit access. Subsector distribution was as expected atappraisal. About a third of the subprojects financed belong to the fivesubsectors identified at appraisal as growth areas: light engineering,textiles and garments, surgical instruments, sports goods and leatherproducts. Agro-processing was the largest subsector financed, taking about39% of total subloans. This included activities such as ice and cold storageplants for the fishing and cash crop industry, oil extraction, cottonginning, rice and flour milling and fruit and vegetable processing.Considering the "rural" location of SSI units and the agricultural base ofthe economy, this subsector is expected to continue to be a growth area.

5.03 Geographical Distribution. About 90% of the subloans were for sub-projects located in the Punja'- (61%) and Sind (29%) provinces, with NWFPreceiving only 8% and Baluchistan 2% of IDA subloans. This distribution wassomewhat more lopsided than as expected at appraisal, but is reflective ofpopulation distribution and past patterns of commercial bank lending.Despite efforts at promoting projects in Baluchistan, problems with localentrepreneurship, availability of raw materials, access to markets andavailability of skilled workers limited their success (paras. 4.24 - 4.26).Suggestions for imposing credit targets by province were resisted since itwas correctly pointed out that credit alone would not develop projects. Moreintensive promotional and developmental work in the less-developed areas wasincluded in the Second SSI Project and should continue to be emphasized toprevent policy makers from taking the politically easy way out of credittargeting. The component under SSI II refers specifically to developingcapability within the SICs in the provinces to carry out project promotionprograms on a continuing basis.

5.04 Size of Subprojects. Most of the lending was for smaller subprojectswith total assets below Rs 2 million (US$125,000). Only about a quarter ofthe subprojects had total assets over Rs 2 million. The average subprojectsize was about Rs 625,000 in fixed assets excluding land and buildings, muchlower than size ceiling of Rs 3 million. This trend towards smaller sub-projects appears to be due to the fact that loan origination was mainly doneat the branches where borrowers are smaller.

5.05 Economic Impact. The 654 subprojects financed under the subloancomponent have generated about 12,800 new jobs at a cost per job of aboutUS$6,000. This is sightly lower than the appraisal estimate of about 13,000

-18-

new jobs created. However, about a quarter of the subprojects are onlypartially operational. Total employment generated is expected to exceed theoriginal appraisal estimate once all subprojects are full.y operational, butwill still fall far short of the PCI estimate of 18,900 at the subprojectappraisal stage. The subprojects financed under this project are almosttotally dependent on local raw materials (97%). Exports constitute a sig-nificant portion of subprojects in specific export-oriented subsectors suchas surgical instruments, sports goods, carpets and garments but, overall,constitute less than 5% of total output. The annual incremental value addedis estimated to be about US$50 million. Ex-post finan^ial rates of returnfor fully operational projects ranged between 18% and 45%. 1/

B. InstituLion Building

5.06 Participating Credit Institutions. One of the objectives of theproject was to develop the commercial banks into effective channels for SSIfinanzing by orienting them towards project-based lending methodology andusing their wide branch network to improve SSI's access to credit. Theproject included an allocation of US$150,000 to finance the training of keystaff of the commercial banks. Another US$250,000 was allocated to financethe preparation of subsector studies and project profiles which could be usedby the banks to facilitate project appraisal work (para 4.28-4.30).Moreover, a development bank, the Industrial Development Bank of Pakistan,was selected to be the refinancing and review agency for subloan processingin order to assist the commercial banks in acquiring proiect financingtechnology. Finally, a project preparation fund was inciuded to assistborrowers in preparing project proposals for bank appraisal, therebyfacilitating the banks' project appraisal task (para 4.28-4.30).

5.07 To prepare the banks for their role in project-based SSI financing,Small Industry Departments (SID) were created in their headquarters. Keyofficers of the SIDs were sent on an intensive five-week training with adevelopment bank in the Philippines. Subsequently, branch officers of about200 key branches were brought to headquarters for a series of three-dayorientation courses. To supplement the training coarses, a lending manualwas prepared and given to all SSI and other officers of the banks who wereexpected to play a role in the SSI lending program.

5.08 Due to the limited number of trained staff, initially, projectappraisal was centralized at the banks' headquarters. However, the brancheswere made responsible for preliminarily screening applicants, undertakingcredit analysis, forwarding applications to headquarters for appraisal,disbursing approved subloans and maintaining subloan accounts.

5.09 This set-up proved to be effective, particularly in the initialstages of project implementation. After all preparatory activities werecompleted, subloan processing picked up quickly and was completed in a yearand a half, quicker than expected at appraisal. Centralization, however,had its drawbacks, especially towards the later part of projectimplementation, since project supervision and end-use monitoring was weak.This weakness manifested itself in some problems with procurement and disbur-sement procedures and initially poor collection performance. As more

1/ Detailed information on financial and economic performance of eachsubproject is available in the project file.

-19-