Embed Size (px)

Citation preview

Document of

The World Bank

FOR OFFICIAL USE ONLY t tA

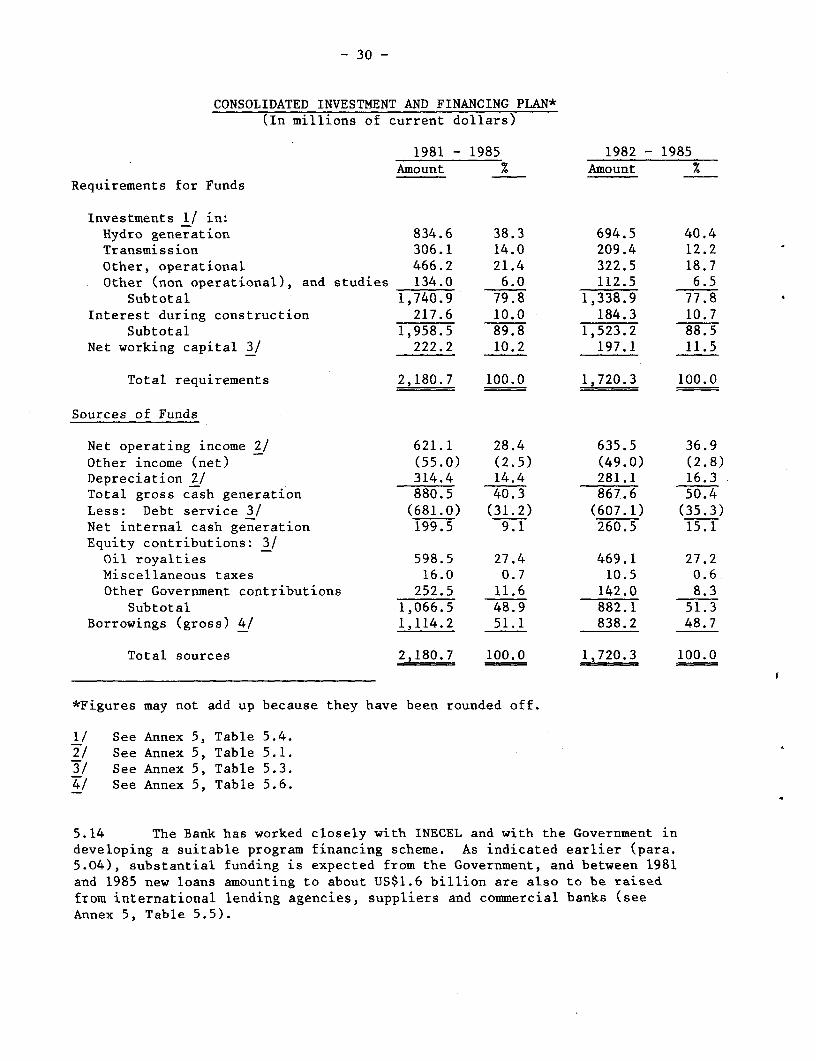

Report No. 3340b-EC

STAFF APPRAISAL REPORT

ECUADOR

INECEL POWER TRANSMISSION PROJECT

June 23, 1981

Projects DepartmentLatin America and the Caribbean Regional Office

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency unit Sucre (S/.)SI. 1.00 = 100 centavos = US$0.04S/. 1,000,000 = US$40,000US$1.00 = SI. 25.00 1/US$1,000,000 = SI. 25,000,000 1/US$ mill 1 = SI. 0.0250 1/

ACRONYMS

CENAFE Centro Nacional Franco-EcuatorianoCEPE Corporacion Estatal Petrolera EcuatorianaCONADE Consejo Nacional de DesarrolloEEQ Empresa Electrica de Quito S.A.EMELEC Empresa Electrica del Ecuador Inc.FONAPRE = Fondo Nacional de PreinversionIDB Inter-American Development BankIECO International Engineering Co. - U.S.A.INE Instituto Nacional de EnergiaINECEL Instituto Ecuatoriano de ElectrificacionMRNE Ministerio de Recursos Naturales y EnergeticosOLADE Organizacion Latinoamericana de EnergiaSNI Sistema Nacional Interconectado

ABBREVIATIONS, UNITS AND MEASURES

kcal kilocalorie (1,000 calories = 1.163 kWh)kW kilowattMw megawatt (1,000 kW)kWh kilowatt hourGWh gigawatt hour (1,000,000 kWh)kV kilovolt (1,000 volts)MVA megavolt-ampere (1,000 kVA)km2 kilometer (0.6214 mile)km square kilometer (0.386 sq. mi)ha hectare (0.01 km = 2.471 7acres)TOE = ton of oil equivalent (10 kcal)

FISCAL YEAR

INECEL's fiscal year ends December 31

1/ Commercial exchange rate as of March 31, 1981, which was used to computecurrency equivalents in this report.

FOR OFFICIAL USE ONLY

ECUADOR

STAFF APPRAISAL REPORT

INECEL Power Transmission Project

Table of ContentsPage No.

1. THE ENERGY SECTOR

Energy Resources ...................................... 1Energy Demand and Supply .............................. 1Hydroelectric Resources ............................... 2Hydrocarbons and other Fossil Fuels ................... 2Non-Conventional Sources of Energy .................... 3Energy Sector Organization ............................ 3Fuel Prices .......... ................................. 4Power Sector Organization ............................. 4Power Sector Regulation ............................... 5Existing Facilities ................................... 5Bank Group Participation in the Power Sector .... ...... 6Electricity Tariffs .................................... 6Marginal Cost Studies ................................. 8Constraints on Sector Development ..................... 8

2. THE BORROWER

Organization and Management ........................... 9Supervision of Electric Power Companies .... ........... 9Staffing ............ .................................. 10Training .............................................. 11Procurement .......... ................................. 11Accounting ........... ................................. 12Auditing ............ .................................. 13Insurance ........... .................................. 13Dam Safety ........... ................................. 14

3. THE POWER MARKET

The Present Power Market .............................. 14The Future Power Market ............................... 15Energy and Capacity Balances .......................... 17Distribution Losses ................................... 17

This report is based on the findings of an appraisal mission which visitedEcuador during November 1980. The mission comprised Messrs. Jorge Larrieu andRicardo Halperin. The report also draws on the findings of a sector mission(composed of Ms. Ursula Weimper and Messrs. Larrieu and Halperin) whichvisited Ecuador in July 1980.

This documnent has a restricted distribution and ray be used by recipients only in the Performance ofJtheir official duties. Its contents may not otherwise be disclosed without World Bank authorization,

TABLE OF CONTENTS (Continued)

Page No.

4. PROGRAM AND PROJECT

Background ............................................ 18Construction Program .................................. 18Generation Expansion Program .......................... 19Transmission Expansion Program ........................ 20Subtransmission and Distribution Expansion Programs ... 20Sector Investment Requirements ........................ 21The Project ........................................... 21Project Cost Estimates ................................ 22Project Financing Scheme .............................. 24Engineering and Consultants' Services .... ............. 24Procurement and Disbursements ......................... 25Project Execution ..................................... 25Environmental Aspects ................................. 26Project Risks ......................................... 26

5. FINANCE

Introduction .......................................... 26Financial History ..................................... 27Tariffs and Rate of Return ............................ 28Consolidated Investment and Financing Plan .... ........ 29Future Finances ....................................... 31Financial and Performance Indicators .... .............. 32

6. ECONOMIC ANALYSIS

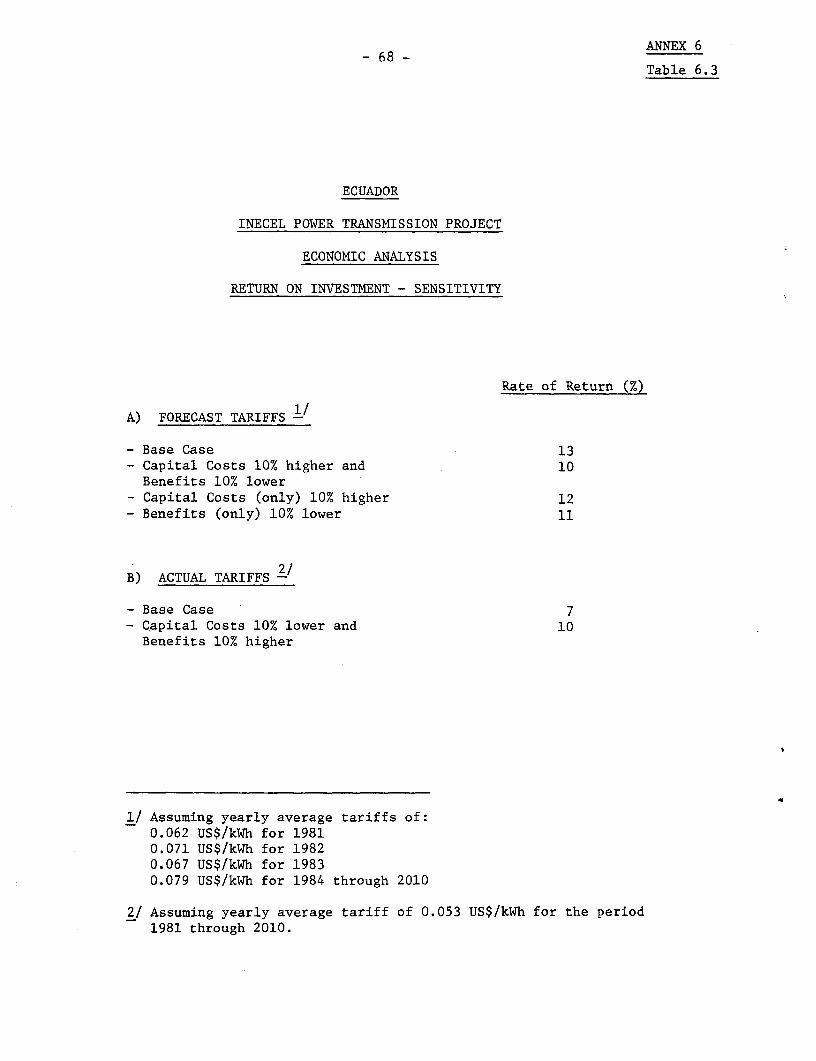

Least-Cost Solution ................................... 32Return on Investment ................................... 33Sensitivity Analyses .................................. 34

7. SUMMARY OF PROPOSED AGREEMENTS AND RECOMMENDATIONS .... 35

TABLE OF CONTENTS (Continued)

LIST OF ANNEXESPage No.

Annex 1 Power Sector Organization

Table 1.1 INECEL's Participation in the Capitalof the Electric Power Companies ............... - 38

Annex 2 Organization

h Table 2.1 INECEL's Organization Chart .39

Annex 3 The Power Market

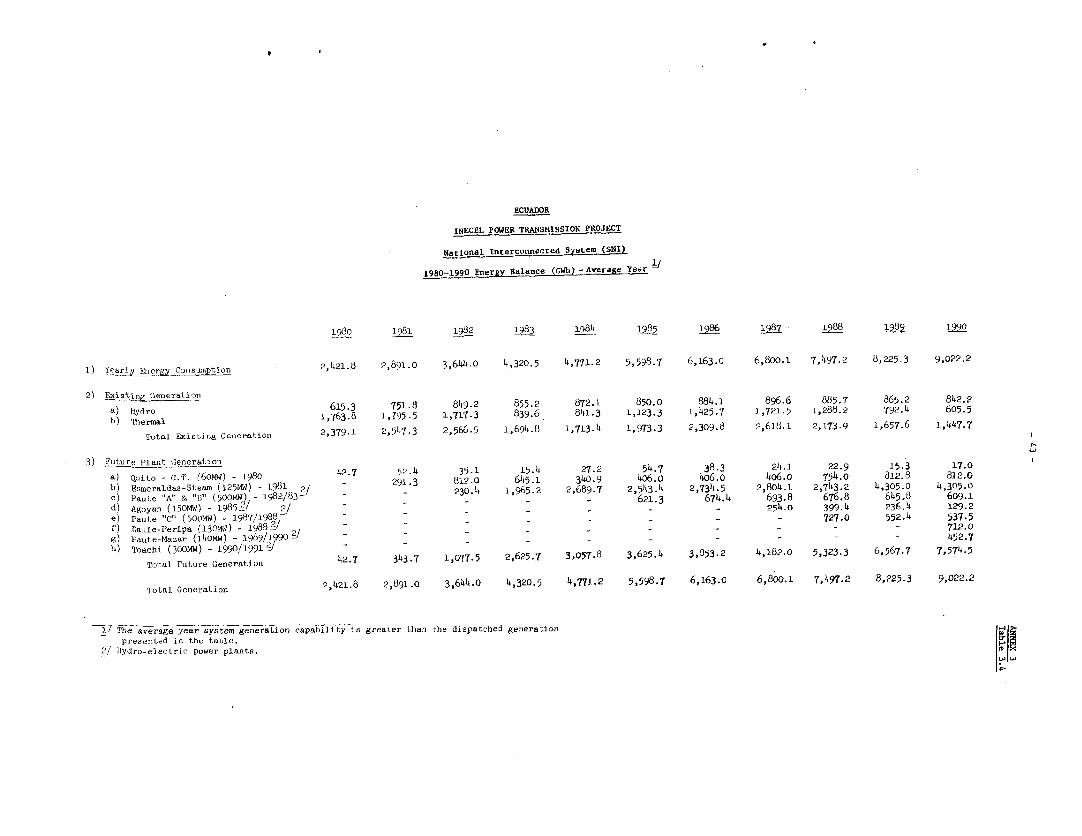

Table 3.1 National and SNI Energy Forecast (GWh) 40Table 3.2 National and SNI Demand Forecast (MW) 41Table 3.3 SNI 1980-1990 Power Balance (MW) .42Table 3.4 SNI 1980-1990 Energy Balance (GWh)-Average Year 43Table 3.5 SNI 1980-1990 Energy Balance (GWh)-Dry Year 44Table 3.6 1978 Gross Generation/Purchases,

Sales and Losses (GWh) .45

Annex 4 Program and Project

Attachment 4.1 Ongoing and Future Development Projects .46Table 4.1 Ecuador's Installed Capacity (MW) .47Attachment 4.2 Main Characteristics of Future Power Plants 48Attachment 4.3 Single Line Diagram .51Table 4.2 1980-1985 Investment Program .52Table 4.3 Summary of Project Cost Estimates .53Table 4.4 Estimated Loan Disbursement Schedule .54Attachment 4.4 Project Implementation Schedule .55Table 4.5 Performance Indicators ..... .................. 56

Annex 5 Finance

Table 5.1 Consolidated Income Statements, 1978-1985 .... 57Table 5.2 Consolidated Balance Sheet, 1978-1985 .... .... 58Table 5.3 Consolidated Sources and Applications of

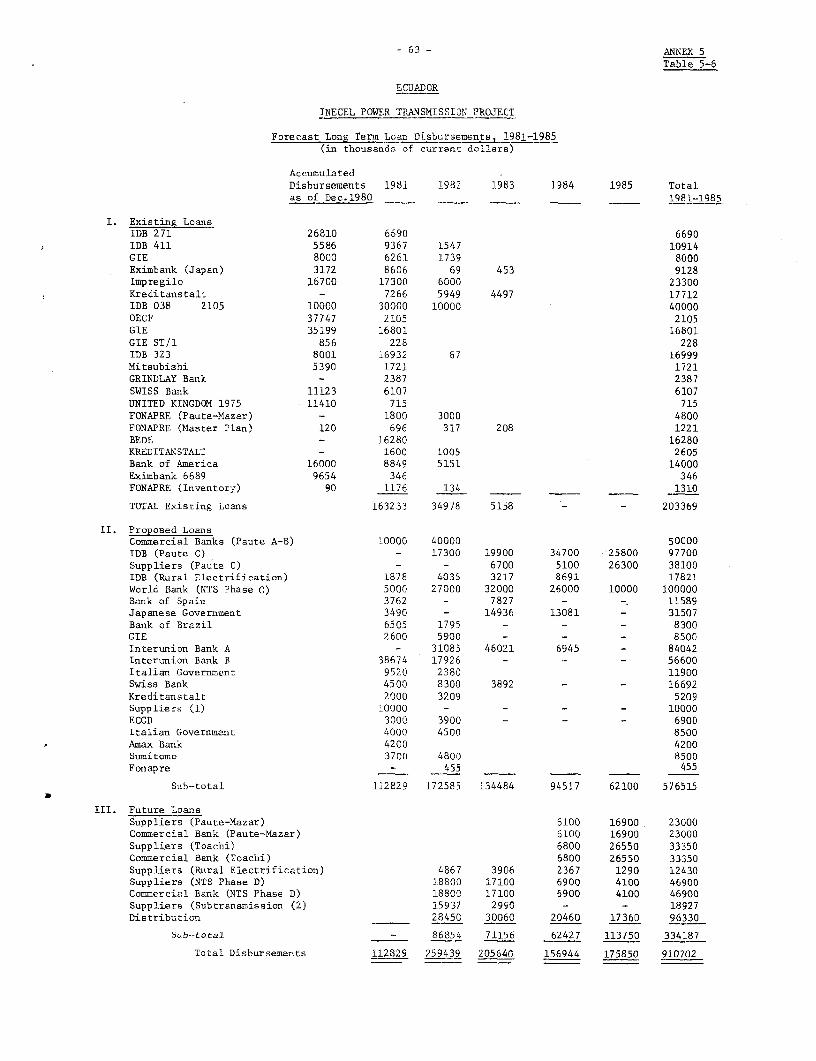

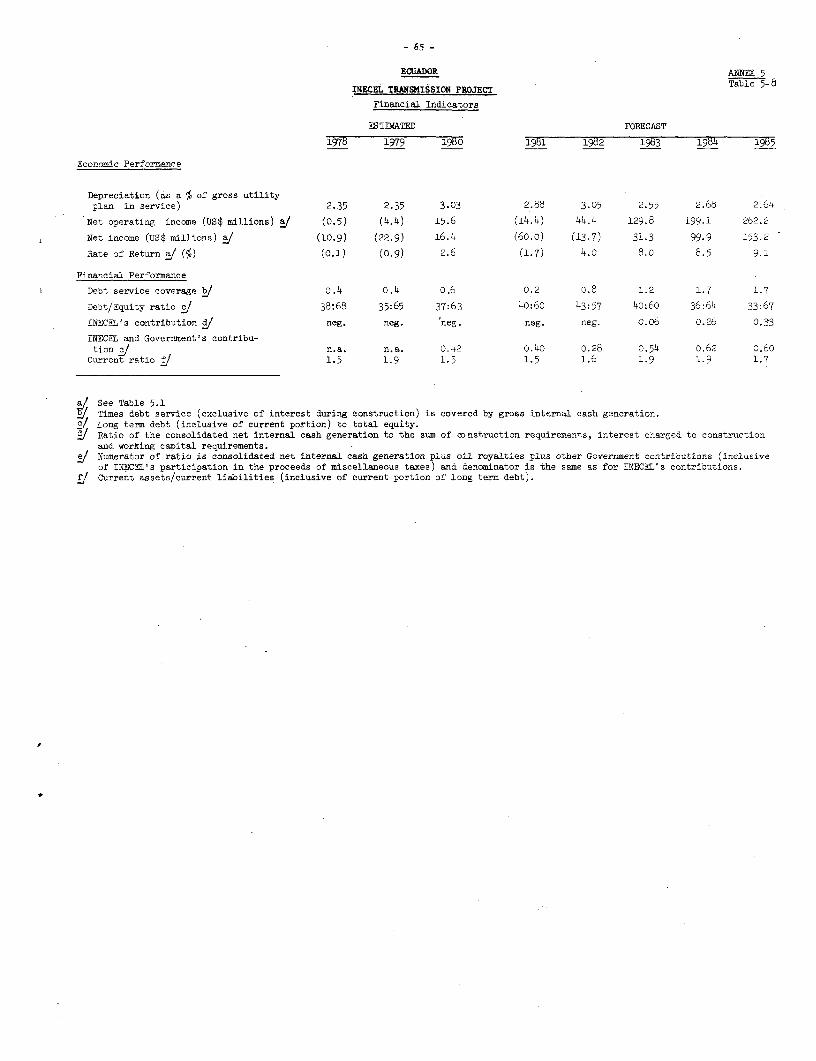

Funds Statements, 1980-1985 .... ............ 60Table 5.4 Construction Program, 1980-1985 .... .......... 61Table 5.5 Schedule of Existing and Proposed Long Term Debt 62Table 5.6 Forecast Long Term Loan Disbursement Schedule 63Table 5.7 Forecast Long Term Debt Amortization Schedule 64Table 5.8 Financial Indicators .65

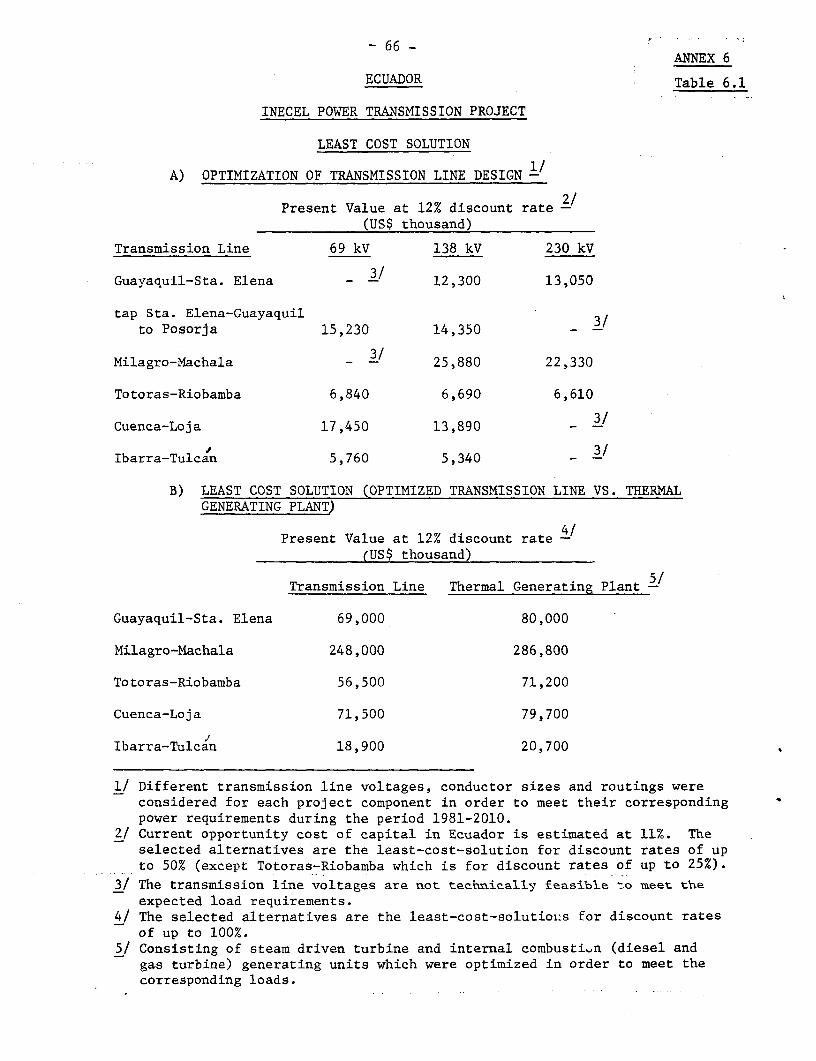

Annex 6 Economic Analysis

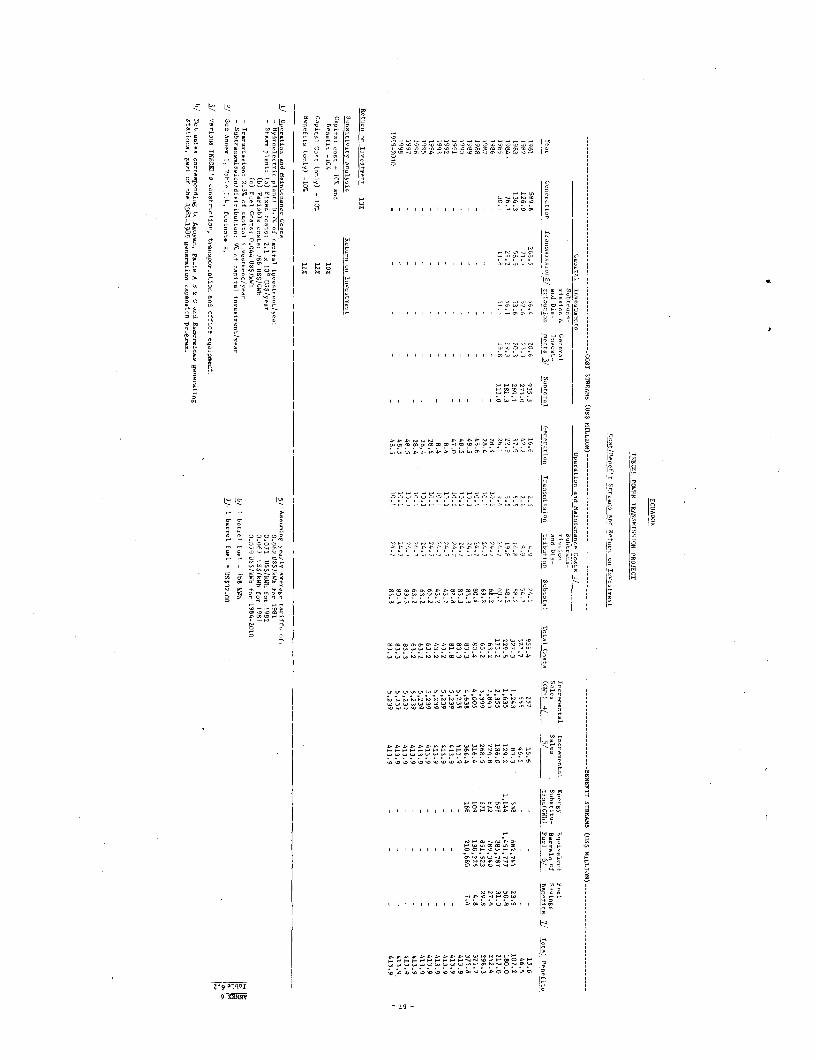

Table 6.1 Least Cost Solution .66Table 6.2 Cost/Benefit Streams and Rate of Return

on Investment .67Table 6.3 Return on Investment-Sensitivity .68

Annex 7 Selected Documents and Data Available in the Project File 69

MAP

- A

1. THE ENERGY SECTOR

Energy Resources

1.01 Ecuador has large reserves of hydrocarbons, significant hydro-electric resources and potential geothermal reservoirs. Hydrocarbons andhydroelectric energy are currently commercially exploited, while forestsand vegetable wastes (charcoal and sugarcane bagasse) are the main non-commercial sources of energy.

Energy Demand and Supply

1.02 Total output of primary energy has been adequate to meet domesticrequirements and has provided ample exportable surpluses of crude oil. Thetable below illustrates the 1978 structure of primary energy output.

Supply TOE x 10 1/

Primary energy output 10,752.3Imports 152.7Decrease in stocks 199.4

Total Supply 11,104.4

Demand

Exports 7,514.8Internal energy consumption:

- Petroleum and derivatives 2,162.5- Natural gas 2/ 31.6- Vegetable fuels (firewood,

sugarcane, bagasse) 693.9- Hydroelectricity 54.4 2,942.4

Own consumption and transformation losses 647.2

Total demand 11,104.4

The National Energy Institute (INE) is currently preparing Energy BalanceForecasts, including actual figures for 1979 and 1980.

Source: Mission estimates.

1/ TOE = ton of oil equivalent.

2/ Includes only the amount of liquified petroleum gas (LPG) produced fromnatural gas.

- 2 -

1.03 Between 1969 and 1978, commercial energy consumption 1/increasedat an average annual rate of about 11%, from 872,000 TOE in 1969 to 2,220,000TOE in 1978 and yearly energy consumption per capita doubled, from 0.15 TOEin 1969 to 0.29 TOE in 1978. In 1978, commercial energy consumption by sectorswas as follows: transportation and fishing, about 60%; commerce and households,23%; and industry, about 17%. About 97% of the total final commercial consump-tion was from hydrocarbon derivatives and 3% from hydroelectricity.

Hydroelectric Resources

1.04 The hydroelectric potential is estimated to be 22,000 MW, mainlycontained in the Pastaza, Santiago and Napo basins. If fully developed, thefirm energy would be about 90,000 GWh/year (which if thermally generated wouldrequire more than 150 million barrels of oil per year). It is presently esti-mated that about 12,000 MW could be economically developed (based on prevailinginternational fuel prices). At present, only about 2% of this potential hasbeen realized. The 1980-84 Development Plan has set as an objective theintensified development of hydroelectric resources, and by 1985 it is estimatedthat 72% of electricity requirements will be provided by this source, ascompared with about 25% at present.

Hydrocarbons and other Fossil Fuels

1.05 Sedimentary basins extend over an area of 17 million ha. In theseventies only limited new reserves were found, and the level of provenreserves decreased from about 1.6 billion barrels in 1972 to about 1.0 billionbarrels in 1980. Addition to proven reserves thus is of the highest priority.The national development plan forecasts a 730-million-barrel increase inreserves over the 1980-84 period, 570 million from secondary recovery and160 million from new fields. Current oil production amounts to about 220,000barrels/day, which covers all of the country's requirements, estimated atabout 75,000 barrels/day, and leaves a substantial balance for export.

1.06 Associated natural gas at the different oil fields is not availablefor power generation purposes. Currently, some gas is reinjected into thereservoirs to maintain field production conditions and the remainder is flared.By 1982, the gas now flared is to be processed at a new liquefaction plant(under construction at Shushufindi) and will be used for domestic consumptionat major centers. The Corporacion Estatal Petrolera Ecuatoriana (CEPE) ispresently evaluating the off-shore reserves at the gulf of Guayaquil. Con-siderable amounts of natural gas are expected to be available from this site.The Master Plan Studies (para. 3.04) will look into the use of gas forelectricity generation purposes.

1/ Includes only final consumption of petroleum and hydroelectricity.

- 3-

Non-Conventional Sources of Energy

1.07 Ecuador has favorable prospects for geothermal development. Super-ficial prospection surveys have detected geothermal activities in Tungurahua,Pichincha and Azuay. The Ecuadorean Electrification Institute (INECEL),the Borrower of the proposed loan, has undertaken the responsibility forevaluating the geothermal potential and in the first stage, presently inexecution, has received technical assistance from the Latin American EnergyOrganization (OLADE). A preliminary report, which includes the results ofthese prospects, is currently under preparation.

1.08 In rural areas, fuel-wood is an important source of energy.The country has important forestry resources, mainly in the Amazonas regionand in the province of Esmeraldas. However, the lack of a reforestationpolicy and the indiscriminate use of wood for industrial and energy purposeshas reduced considerably the forest area, and rural areas are facingshortages of fuel-wood. The National Energy Institute (INE) is attempting toaddress the problem through the development of improved wood-fueled cookingstoves.

1.09 The possible use of solar energy, windpower, and other non-conventional sources is being studied by INE. In addition, OLADE is promotingthe construction of biodigestors, in which animal and vegetable waste isconverted into methane. A demonstration plant has been built jointly with theProvincial Council of Pichincha and OLADE is also providing technical assis-tance to other provinces for similar purposes.

Energy Sector Organization

1.10 National economic planning is performed by the National DevelopmentCouncil (CONADE), which has prepared a National Development Plan for 1980-84.This plan, mandatory for public sector institutions, is intended to help ensurethe coherence in investment programs in all areas of the economy. It is to bereviewed each year.

1.11 The Ministry of Natural and Energy Resources (MRNE) is the executingand controlling agency for national energy policy. Under its jurisdictionare INECEL, CEPE (a public sector corporation through which the Governmentparticipates in the petroleum industry 1/), and INE, a research institutecreated in 1978 which is presently assessing Ecuador's energy resources,developing energy balances, and evaluating alternative energy technologies.

1.12 The present organization is satisfactory and results in a reasonablelevel of decentralization of decision making, while also generally ensuring thecoordination of the policies implemented by the respective executing agencies.However, there are some problems. MRNE is relatively poorly staffed and hasexperienced high personnel turnover, and CEPE has faced both organizational

1/ Several foreign oil companies also operate in Ecuador, in exploration,production and refining. The Government has recently developed newcontractual formulas which are expected to attract increased foreignparticipation in exploration activities.

- 4 -

strains as well as conflicts of authority with MRNE and of coordinationwith other agencies. This situation has been improving recently, and theproblems discussed are not expected to affect the proposed project.

Fuel Prices

1.13 Until early 1981, the prices of petroleum products in Ecuador wereamong the lowest in the world. In 1980 the implicit subsidy to consumers,given by the difference between internal and world market prices, representedan amount estimated to be close to 8% of GDP.

1.14 In the 1980-84 National Development Plan, the Government explicitlystated that it would adjust the prices of hydrocarbons, and some increases(for jet fuel and for fuel oil for ships) were approved in early 1980.Subsequently, a new "high test" gasoline was introduced at a price ofUS$0.73 per gallon (regular gasoline was then selling at US$0.19 per gallon)and in early 1981 the price of all petroleum products was increased, in somecases, such as regular gasoline, by over 200%. Present retail prices approxi-mately average 55%-60% of the wholesale prices in the Caribbean.

1.15 The retail prices of fuels used for electricity generation (mainlyBunker C and diesel) had in 1980 been at level which was 13% to 16% of theworld market, and this represented a hidden subsidy to power consumers thatexceeded US$100 million a year (roughly equivalent to the value of sectorbillings). These prices have now also been increased, and currently repre-sent 36% to 42% of prevailing world market levels. Agreement was reachedthat these prices will be periodically increased so that in 1984 theyrepresent not less than 50% of the world level then prevailing.

1.16 At present the prices for fuels used for electricity generation aresufficiently high to ensure that there is no waste, and that hydro generationis fully utilized while auto-generation is discouraged.

Power Sector Organization

1.17 Ecuador's 1961 Electricity Law establishes that the Government,through INECEL, has the monopoly on electricity generation, transmission anddistribution, but is empowered to authorize private operations. At presentthere is only one privately owned company: the Electric Company of Ecuador,Inc. (EMELEC), which operates in Guayaquil under a municipal concession.The contract expires in 1985, after which time the municipality of Guayaquilmay -- by first giving appropriate advance notice -- purchase at a fair

price the company's facilities. The other 14 power companies are organizedas private corporations, with INECEL as the largest shareholder and thebalance of shares owned mainly by the local municipalities. In a few cases,there are also individual private shareholders, who own very small participa-tions. Thus, whether in use of its regulatory powers (para. 1.19) or as amajority stockholder, INECEL has the ability to substantially control theactivities of all the power companies in the country. Annex 1, Table 1.1,shows INECEL's participation in the capital of each power company. In additionto these companies, INECEL also directly operates two small power systems and42 municipalities operate small local power installations.

- 5 -

1.18 The organization described above represents a considerable improve-ment over that which prevailed in 1961, when more than 100 companies werein operation. INECEL plans to continue the process of merging and consoli-dating the local power systems, by forming regional companies. This develop-ment is highly desirable as most of the power companies presently face signifi-cant diseconomies of scale. INECEL's present goal is to consolidate allelectric services now being provided by the 14 power companies it controls in10 regional companies. At negotiations, agreement was reached that this willbe done by December 31, 1984.

Power Sector Regulation

1.19 The Ministry of Natural and Energy Resources is responsible for theformulation of national electrification policy, while INECEL is responsiblefor power sector regulation and supervision. All power companies are requiredto submit their capital budgets to INECEL, inform INECEL about external bor-rowing plans, allow INECEL to inspect their facilities and audit theirrecords, and abide by the regulations INECEL's Board approves. INECEL'sregulatory performance is discussed in paragraphs 2.04 through 2.06.

Existing Facilities

1.20 Ecuador's installed power generating capacity (December 1979) isabout 924 MW, of which 700 MW, or 76% of the total, is thermal capacity; thebalance is hydroelectric. About 520 MW, or 56% of the total installedcapacity, are currently interconnected through the 230 kV Quito-Guayaquiltransmission line and the 69/34.5/22 kV Quito-Latacunga-Riobamba-Ambatosubtransmission network. Present public service supply (through INECEL, itssubsidiaries, EMELEC and municipalities), accounts for about 84% of totalpower supply. Private generation (self-producers, mostly industrial andagricultural undertakings) accounts for the remaining 16% (about 153 MWcapacity, of which 141 MW are diesel generators and 12 MW are hydroelectricplants). A summary description of these installations is shown in thefollowing table (see also Annex 4, Table 4.1).

Internal Oil-firedCombustion Steam Plant Hydro TotalGas

Turbines Diesel

Public Service 173.8 249.4 136.0 212.5 771.7

Self-Producers - 140.6 - 12.1 152.7

Total Ecuador 173.8 390.0 136.0 224.6 924.4

- 6 -

Bank Group Participation in the Power Sector

1.21 The Electric Company of Quito (EEQ) has been the main recipientof Bank Group funds within Ecuador's power sector. The first two Bank opera-tions (in 1956 and 1957) helped to finance the 40-MW Cumbaya hydroelectricproject, several diesel plants, and extensions of the distribution systems(these works were completed by the end of 1961 and have been operating satis-factorily).

1.22 IDA Credit 286-EC for US$6.8 million was approved in 1972 andcovered part of the foreign exchange costs of the 30-MW Nayon hydroplant,*an 18-MW diesel power station, transmission lines, and rural electrification.The PPAR (No. 3003, issued in May 1980) concluded that:

(a) the physical objectives of the project were met, albeit withdelays and cost overruns;

(b) progress towards the institutional objectives of the projectwas disappointing;

(c) most of the covenants related to the financial aspects of theinstitution were not met; and

(d) lack of cooperation adversely affected the effectiveness of IDAsupervision efforts, which, however, would also have required morefrequent field supervision than actually took place.

These lessons were kept in mind when outlining the conditions for the proposedproject, even though the proposed borrower is a different entity.

1.23 The only other financing provided by the Bank to the sector has beenthrough Loan S-006-EC to FONAPRE, for the Master Plan studies and thefeasibility study of the Paute-Mazar hydro-development which are currentlyunder way (para. 4.01).

Electricity Tariffs

1.24 The regulations governing electricity tariffs were approved bydecree in 1975 and are based on sound financial criteria. Essentially, theygive INECEL the power to set tariffs at a level that allows electric powercompanies to recover costs and make a reasonable profit, so that they mayenjoy a satisfactory financial situation and provide service efficiently.

1.25 To achieve this objective, the regulations authorize electricpower companies to achieve a rate of return of 8.5% on a rate base definedas the replacement cost, net of depreciation, of fixed assets in operationplus estimated working capital needs. Annual rate of return surpluses (ordeficits) over the 8.5% figure are to be registered in a stabilization accountand if surpluses or deficits occur in three consecutive years, tariffs shouldbe revised.

- 7 -

1.26 The regulations also establish a system of tariff adjustments dueto cost variations. Automatic adjustments are made when unit labor costs,unit electricity purchase costs, or unit fuel costs vary between 5% and 10%over the level used to determine the existing tariff levels. When the unitcosts mentioned above vary by more than 10%, adjustment must be approved byINECEL's Board.

1.27 For political reasons, the regulations were never implemented,which accounts for the financial difficulties faced by the sector (paragraphs5.01 to 5.04). None of the electric power companies revalued its assets inthe manner prescribed, nor were tariffs periodically adjusted in the mannerrequired to achieve the 8.5% rate of return. In this respect, it should benoted that INECEL's Board is controlled by the Government. Subsequent tothe fuel price increases implemented in early 1981 (para. 1.13), INECEL'sBoard approved a policy of monthly tariff increases averaging 3%. Atnegotiations, agreement was reached that these increases will remain inforce until the agreed rate of return targets are achieved. Failure toimplement these increases as agreed would be an event of default. Beforethe loan is declared effective, the Bank will seek confirmation that INECELis fulfilling its tariff increase commitments.

1.28 The tariff levels and tariff structures of the 15 companies inthe sector vary considerably. In 1979, the average sector tariff was US$mills 44/kWh; however, four systems (including the large EMELEC system and theLatacunga system, directly operated by INECEL) had average tariffs belowUS$ mills 40/kWh and, in one of these (Riobamba), the average tariff wasUS$ mills 28/kWh. In contrast, six systems had average tariffs exceedingUS$ mills 56/k.wh. The national development plan for 1980-84 sets as a policygoal the attainment of a uniform tariff structure for the national interconnectedsystem, and the 1980 tariff structure changes (para. 1.30) are a modest stepin this direction.

1.29 It should be noted that, with the present sector organization, theachievement of a national tariff structure will be a difficult goal to reach.This is because the cost structures of the different power companies differconsiderably; while some companies like EEQ and EMELEC operate in predominantlyurban areas, where population is heavily concentrated and industry has asignificant weight, others operate over larger territories, where popula-tion is dispersed, average income is low, and industrial demand is not signifi-cant. Thus, a mechanism would be required to transfer funds between companiesso as to allow them all to meet financing requirements and rate of returntargets. At negotiations, agreement was reached with INECEL that it willsubmit to the Bank, not later than September 30, 1981, a specific proposal(including main operational characteristics and target dates for implementation)for implementing this mechanism; discuss it with the Bank, and put it intooperation.

-8-

1.30 The tariff structure prevailing through 1979 encouraged electricityuse by establishing an inverse relationship between demand level and unitprices. In 1980 this was changed and, for the residential sector, thereare now lower rates for demands below 70 kWh per month and higher (constant)rates when consumption exceeds this figure. Furthermore, rates forresidential demands of 70 kWh per month or less are to remain unchanged fora period of three years, as part of the Government's incomes policy. In viewof its social objectives, this is justified; however, both the cut-off levelof 70 kWh and the rate level should be reviewed when tariff structures arerevised (para. 1.32). For commercial and industrial users, the rate structurestill favors the larger consumers. This, too, should be reviewed once themarginal cost studies are completed.

1.31 The above analysis and the financing problems faced by the powersector (discussed in Chapter 5) indicate that strong action in the tarifffield is required. Such action involves: (a) significantly increasingaverage tariff levels (para. 5.03), (b) further changing tariff structuresso as to bring them in line with true economic costs (para. 1.32), and(c) reducing the present tariff disparities between the various electricpower companies (paragraphs 1.28 and 1.29).

Marginal Cost Studies

1.32 As part of the Master Plan studies, INECEL's consultants' willprepare an analysis of the marginal cost of electricity generation. Atnegotiations, agreement was reached that INECEL would furnish to the Bank,no later than October 31, 1982, the results of the study, together withINECEL's own comments and proposals for a comprehensive marginal cost study,which will enable it to revise its structure of retail rates for the saleof electricity and would provide grounds for a review of the financial rateof return requirement, if and when future projects are brought for Bankconsideration.

Constraints on Sector Development

1.33 The Government has set ambitious goals for the power sector, aimingto substantially replace thermal generation and simultaneously significantlyincrease access to service. These goals are reflected in the 1982-85 consoli-dated investment program for INECEL and its subsidiaries (para. 5.13), whichresults in total financing requirements of about US$1.8 billion. The success-ful implementation of this program requires a major funding effort, whichincludes tariff increases, large amounts of Government equity contributionsand sizeable external borrowings. Failure to perform as required in any ofthese areas will, in all likelihood, result in program implementation delays.In view of the political difficulties associated with increasing tariffs andof the budgetary problems faced by the Government, the risk of such delaysshould not be underestimated.

1.34 While, as indicated above, the financial issues are presently themost serious ones faced by the sector, other matters of pressing concern arethe continuance of fuel subsidies, which distort resource allocation inducingexcessive consumption and waste, and the relatively weak control hithertoexercised by INECEL over the activities of the other power companies, which;s evidenced in poor coordination and in inefficiency. The remedies for theseissues involve, in the last instance, difficult political decisions, and, tortho extent that these are not implemented, present problems will continue.

1.35 To minimize the above risks, the Government and the Bank have been

engaged in a prolonged dialogue, which resulted in the implementation of

some significant measures (paragraphs 1.14 and 1.27) thus minimizing the

difficulties of meeting the loan covenants, once the loan becomes effective.

2. THE BORROWER

Organization and Management

2.01 The Borrower of the proposed loan would be INECEL, an autonomous

entity of the Government of Ecuador. INECEL was founded in 1961 and is

responsible for assessing national power resources, planning power sector

expansion, constructing and operating generation and transmission facilities,

supervising the other companies in the power sector, and approving tariffs

for the sale of electricity. INECEL also owns a major participation in 14 of

Ecuador's 15 electric public utilities and directly operates two small local

systems.

2.02 INECEL is governed by a Board of Directors presided by the Minister

of Natural Resources and Energy. Other board members are the Minister of

Finance, the Minister of Industry, the representative of the President of

CONADE, the Chief of the Joint Command of the Armed Forces, and one represen-

tative from each of the following: the other power companies, the Association

of Electrical Engineers, and the power sector workers. Responsibility for day

to day operations is delegated to the General Manager, who is assisted by six

operating managers.

2.03 INECEL's organization chart is shown in Annex 2, Table 2.1. Although

the organization structure is basically reasonable, INECEL faces management

problems. Some of these are caused by lack of qualified staff, notably in

finance, others by inadequate coordination between the various departments,

which operate with a considerable degree of autonomy. Furthermore, the number

of operating and staff units directly reporting to the General Manager is

high, probably placing excessive demands on his time and on his ability to

supervise them adequately. To address these problems, and also to assistINECEL in the upgrading of its information systems, evaluation of data process-

ing requirements and conciliation of budgetary and accounting data, the

proposed loan would finance consultant services for an organization study andformulation of a program of institutional improvements. Draft terms of

reference for this study have already been agreed upon. At negotiations,

agreement was reached with INECEL that it will engage the consultants no later

than December 31, 1981, will discuss the recommendations of the study with the

Bank, and will implement such recommendations as have been mutually agreed upon.

Supervision of Electric Power Companies

2.04 Through its Marketing and Distribution Department, INECEL supervises

the operations of the electric power companies. The Department's main func-

tions involve setting up standards for works and supervising the technical

aspects of the companies' operations and maintenance as well as their manag-

erial performance. These activities require seeing that norms instituted by

INECEL are properly applied and that the work of INECEL's representatives at

the subsidiaries' Boards of Directors is properly coordinated.

- 10 -

2.05 Though the Electricity Law vests sector regulatory powers in INECEL(para. 1.19), in practice INECEL's subsidiaries have tended to operate with alarge degree of autonomy. Furthermore, despite the fact that INECEL holds thevoting power majority in each of the subsidiaries' Boards, it has seldom madeits presence felt; on the other hand, the minority Board members, whichrepresent the municipalities in which the subsidiaries operate, have carried adisproportionate weight in decision making, often introducing political con-siderations. This may help to explain some of the management problems whichmany of these subsidiaries face and which INECEL has had limited success insolving.

2.06 Currently, INECEL's management is striving to shape up its super-visory role. New staff have been appointed to key positions, meetings havebeen held with the subsidiaries' managers, and minimum periodic informationrequirements have been set up. The organizational and institutional improve-ments study included in the proposed project, would also look into INECEL'ssupervisory performance and provide recommendations for its improvement.However, since this study will require a long time to complete 1/, at nego-tiations agreement was reached with INECEL that it would submit to the Bank,an interim program--to be implemented at the earliest and monitored duringproject supervision--which would include the upgrading of periodic reportingby the subsidiaries, mechanisms for more frequent contact between INECEL'smanagement and those of its subsidiaries, closer evaluation and control ofthe subsidiaries' capital budgets, and assignment of increased responsi-bilities to INECEL's directors at the subsidaries' boards. That a satis-factory program had been submitted would be a condition of loan effectiveness.

Staffing

2.07 At present, INECEL employs about 2,400 people, 500 of whom haveprofessional degrees (nearly 400 of these are engineers, mainly civil andelectrical engineers) and has forecast that it will employ about 3,500people by 1985, which implies an annual growth rate of 8%. INECEL's subsid-iaries employ an additional 3,700 people, and this number would increase atapproximately the same rate as INECEL's own staff. It would presently appearthat, both in INECEL and in the subsidiaries, there are areas that are over-staffed. For this reason, the performance indicators which were agreed uponat negotiations, reflect a slower pace of growth in employment than INECEL'spresent forecasts. Furthermore, it has been agreed with INECEL that theorganizational and institutional improvements study will address this issue andidentify the specific areas that have an excess of personnel so that correctiveaction may be taken.

2.08 The salaries of INECEL's administrative staff are tied to thepublic administration structure. Workers are affiliated with several craftunions, each of which bargains separately, and the labor contracts usually run

1/ The first phase of the consultants' work would comprise an evaluationof INECEL's policy making role and control activities and informationflows from the subsidiaries. This phase would take about 18 months tobe completed.

- 11 -

for about two years. Labor relations are generally good and labor disputesnot frequent. Salary levels, supplemented by abundant fringe benefits, areadequate and generally competitive with those offered by the private sector.Salary increases are a function of merit and of seniority.

Training

2.09 INECEL has established an important and active Training Departmentwhich has, over the past seven years, developed a good, if somewhat central-ized, training system. Training services (oriented mainly to technicians andworkers in the operational and maintenance areas of the utilities) are avail-able to, and are widely used by, the staff of INECEL and of its subsidiaries.The training system is based upon sound principles and benefits from executivemanagement commitment and support. The following features of the system areindicative of the manner in which training services have been developed andare now being routinely provided.

(a) INECEL operates a well established residential training center(French-Ecuatorian National Center, CENAFE, with a present capa-city of 100 trainees), with competent staff and adequate facilities;

(b) an annual policy statement on workforce and training is updatedand circulated each year;

(c) regular workforce planning and forecasting for the complete sectoris undertaken as a corporate management exercise; and

(d) an annual program is issued to all regional utilities, detailingthe training programs to be offered at CENAFE and approved programsof education and training available in Ecuador and externally (forwhich grants are available).

2.10 The successful implementation of the sector development programand of the managerial and administrative reforms expected to be proposed bythe organization and institutional improvements study will require an intensivetraining effort, which should also include management training. To thisend, INECEL and the Bank have agreed to include as part of the proposedproject a training component, which would comprise an in-depth evaluation ofINECEL's training programs (to be carried out by external consultants whosequalifications and terms of reference are satisfactory to the Bank); specifictraining programs recommended by the consultants and agreed to by INECEL andthe Bank; and training equipment. The draft terms of reference for theseconsultants have already been agreed with the Bank. At negotiations agreementwas reached that these consultants will be hired no later than December 31,1981.

Procurement

2.11 INECEL's procurement procedures are governed by a national procure-ment law. The law's provisions have been found to be, by and large, reasonablethough restrictive interpretations sometimes cause excessive delays. To preventproblems in this area, agreement on the contents of the bidding documents forthe purchase of equipment and materials for the project has already been reached

- 12 -

and the draft documents have been submitted for review by the Bank, andfound satisfactory. During negotiations it was also agreed that theGovernment of Ecuador will take such actions as may be required to expediteprocurement authorizations and clearances as to avoid implementation delays.

Accounting

2.12 The quality of INECEL's financial statements is extremely poor be-cause of the lack of importance hitherto attached to such information,department head changes, old fashioned recording systems and absence ofcompetent staff. Contributing factors too, have been the insufficient attentiongiven to internal auditing and the delays of the Contraloria General's externalauditing interventions, which have limited their usefulness. INECEL is tryingto address this issue, and in 1980 it engaged additional qualified staff for itsinternal auditing unit, which is progressively increasing the scope of thework it carries out. The training programs proposed (para. 2.10) are expectedto address the needs of the internal auditing unit.

2.13 The main problems of INECEL's accounting systems and policies are:

(a) INECEL does not prepare consolidated financial statements, eventhough its participation in each of the subsidiaries' capital stockranges from 54% to 99%. This participation is shown as an invest-ments, at historic cost. Profits (or losses) earned by the subsid-iaries are not recognized, unless collected through dividends; and

(b) Fixed assets are shown at cost, despite legal provisions whichrequire their annual revaluation.

Other problems arise from the poor quality of some of the figures and fromthe excessive time taken to produce reports.

2.14 To address these problems, at negotiations agreement was reachedwith INECEL that it will:

(a) implement measures so that it may submit fully consolidatedfinancial statements for 1983, and on interim consolidationtargets for 1981 and 1982;

(b) revalue its fixed assets annually, and engage qualified experts, notlater than December 31, 1981, on terms of reference acceptable to theBank, to design recording systems such that future fixed asset inven-tories would be up to date and to fully inventory its fixed assetsand assess their replacement value, and (promptly upon the receipt ofthe valuation report) to reflect such valuation in its records andfinancial statements; and

(c) reflect a provisional revaluation 1/ of fixed assets in operationon the basis of inflation indices in the 1980 financial statements.

1/ Until replacement values have been assessed and agreed with the Bank.

- 13 -

2.15 Since the consolidation of financial statements requires thatINECEL's subsidiaries submit in time financial statements of satisfactoryquality (which at present most cannot do), at negotiations agreement wasreached with INECEL that it will furnish to the Bank its programs to achievethis goal in each subsidiary, as per an agreed schedule. The programs shouldidentify the accounting problems faced by each subsidiary, and should proposespecific measures to address them. Furthermore, since the asset valuationproblem (para. 2.13) is also applicable to INECEL's subsidiaries, atnegotiations agreement was reached that INECEL will cause each of its sub-sidiaries to revalue its fixed assets in the same manner as INECEL, per anagreed timetable, and would assist them and supervise them in this exercise.

2.16 The organization and institutional improvements study is to alsoaddress the operating problems of the accounting area, particularly dataprocessing and staffing.

Auditing

2.17 INECEL's financial statements are presently audited by theContraloria General de la Nacion, a specialized government agency. Due to theContraloria's lack of staff, the issuance of the audited statements has beenfrequently, and seriously, delayed. For instance, the 1978 and 1979 auditedstatements only became available in January 1981. Furthermore, the scope ofthe audit does not meet Bank requirements. It has therefore been agreed withINECEL that it will engage private external auditors. At negotiations, itwas also agreed that calls for bids would have been issued, and bids evaluated,as a condition of loan effectiveness and that actual engagement would takeplace not later than March 31, 1982.

2.18 INECEL's subsidiaries are organized as private corporations. Onlyone, EEQ, has private external auditors. The others are supposed to beaudited by the Contraloria, but this only happens in a limited number ofcases. Since, as indicated earlier, most of the subsidiaries have significantproblem's in their accounting systems, it is imperative that a major improvementeffort be made, if consolidated financial statements are to be produced.Thus, in addition to the measures listed in para. 2.15, at negotiations it wasagreed that INECEL will cause each of its subsidiaries to engage independentexternal auditors, by agreed dates.

Insurance

2.19 INECEL follows the practice of externally insuring its assets againstmajor risks, such as fire, explosion, hurricanes, tornadoes and flooding.As far as feasible, the insurance policies are based on estimated replacementvalues. These practices are acceptable and consistent with Bank requirements.At negotiations, agreement was reached to include the standard insurance clausein the loan agreement for the proposed project. Over the past 12 months,INECEL has set up an insurance division and this is already resulting insubstantial economies in insurance costs, which previously were too high.

- 14 -

Dam Safety

2.20 INECEL is currently completing construction of the Paute-Amaluzadam (one of the highest arch dams in the world). The successful operation ofthe facilities included in the proposed Bank project would be closely linkedto the adequate operation of the Paute hydroelectric development (para 4.07and Annex 4, Attachment 4.2). It has therefore been agreed with INECEL thatthe Paute-Amaluza dam will be monitored and inspected at least once a yearby qualified and experienced experts and that a copy of the inspection reportwould be submited to the Bank.

3. THE POWER MARKET

The Present Power Market

3.01 During the period 1970-78 Ecuador substantially improvedits electrification level as shown by the indicators below:

Year Capacity installed/ Consumption/ Electrificationinhabitant inhabitant Rate (%)

1970 51 watts 155 kWh/year 281975 74 watts 266 kWh/year 321978 122 watts 333 kWh/year 38

Despite this favorable trend, per capita installed capacity, energy consumptionand access to electricity are among the lowest in South America. 1/

3.02 Ecuador's electric public utilities (INECEL, its subsidiaries,EMELEC, and 42 small municipal systems) currently supply electricity to about622,000 customers, representing about 3,200,000 inhabitants. In 1978, totalelectricity sales amounted to 2,182 GWh, of which about 43% were sold to theGuayaquil area by EMELEC and about 29% to the Quito area by Empresa Electricade Quito, while INECEL's other subsidiaries and municipalities accounted forthe remaining 26.5% and 1.5% respectively.

3.03 Total electricity sales in Ecuador have increased steadily at anaverage annual rate of over 13%, from 791 GWh in 1970 to 2,182 GWh in 1978 (seeAnnex 3, Table 3.1). Simultaneously, maximum demand has increased from 224 MWin 1970 to 565 MW in 1978 (see Annex 3, Table 3.2), at an annual average rateof about 12%. Ecuador's 1978 total electricity generation and sales were asfollows:

1/ Consumption per capita and electrification rates of some other SouthAmerican countries are respectively: krgertina, 1,236 kWh and 800%; Brazii,912 kWh and 62%; Chile, 927 kWh and 87%; Colombia, 621 kWh and 62%; Peru,523 kWh and 35%; and Uruguay, 1087 kWh and 80%.

- 15 -

Category C%n 7 of Total Generation

Residential 792 30.7Commercial 300 11.7Industrial 864 33.6Public Lighting and Others 226 8.8

Total Sales 2,182 84.8

Transmission and Distri-bution Losses 392 15.2

Total C-eneration 2,574 100.0

The Future Power Market

3.04 INFCFL, with the assistance of consultants (Lahmayer - Germany and-idroservice - Brazil), is currently preparing the National ElectrificationMaster Plan Studies, with Bank financing through Loan S-006-EC (para. 1.23).One of the main objectives of these studies has been the assessment of thefuture power market. The load forecast recently completed was developedafter an evaluation of alternative projection methodologies: extrapolationof historical consumption trends, correlation with macro-economic indicatorsand regionalized and national forecasts by sectors. Based on a detailedanalysis of the results obtained by using these different methods, INECEL, inconsultation with the Bank, decided to adopt the national load forecast bysectors.

3.05 Ecuador's total electric energy requirements, including transmissionand distribution losses, are expected to increase from 2,574 GCh in 1978 to5,600 GWh in 1985 at an average annual growth rate of about 11.7%. 1/ Maximumdemand is expected to increase from 565 MW in 1978 to 1,232 MW in 1985 at anaverage annual growth rate of about 11%. The generation system load factor(non-coincidental peak demand) is expected to improve from 50.5% in 1978 to51.87 in 1985. Details of the energy and power demand forecasts are given inAnnex 3, Tables 3.1 and 3.2.

1/ This growth is in line with Ecuador's economic projections, as out-lined in a Bank's country study of July 1979 (Ecuador: DevelopmentProblems and Prospects), and with the macroeconomic forecasts containedin the national five year development plan.

- 16 -

3.06 Specific components of projected 1985 aggregate demand and loadgrowth rates are as follows:

Category GWh 1978-85 Growth Rate (%)

Domestic 1,757 12.1Commercial 691 8.6Industrial 2,071 13.3Public Lighting and Others 403 8.6

Total Sales 4,922 12.3

Transmission and Distri-bution Losses 677 8.1

Total Generation 5,599 11.7

3.07 The structure of electricity consumption is not expected to changeconsiderably during the period 1978-85; the share of industrial consumptionis expected to increase from 34% in 1978 to 37% in 1985, and losses and powerstation use are expected to decrease by 3% from 15% in 1978 to 12% in 1985.It is reasonable to expect such reduction in energy losses and power stationuse as: (i) the bulk of the energy will be transferred through- high voltagelines (230 kV and 138 kV); (ii) existing subtransmission and distributionsystems are expected to be improved; (iii) INECEL and its subsidiaries areexpected to improve the existing methods of energy monitoring and theftcontrol (para. 3.11); (iv) power station use at thermal plants (which accountsfor the bulk of this item) is expected to be reduced substantially, as theNational Interconnected System's thermal generation requirements will decreaseonce the Paute hydro-development becomes operational (para. 4.07). Theremaining categories are expected to remain basically unchanged. The followingtable illustrates the structure of electricity consumption by categories:

Category % of Total Generation1978 1985

Residential 30.8 31.4Commercial 11.7 12.3Industrial 33.5 37.0Public Lighting and Others 8.8 7.2Losses and Power Station Use 15.2 12.1

Total 100.0 100.0

3.08 The analysis carried-out by INECEL and its consultants to determinethe sales forecast was comprehensive, and reflects well substantiated trends.The results were reviewed by the Bank and found adequate. The forecastsare consistent with: (i) the probable effect on the consumption pattern

- 17 -

of the proposed tariff increases (para. 5.03); (ii) the considerablereduction of electricity generation by auto-producers due to the increaseof internal fuel prices (para. 1.15); and (iii) the expected increase inthe numbers of consumers.

Energy and Capacity Balances

3.09 Based on the market requirements, existing power availability,and the future power development program, system simulation studies wereconducted for yearly power and energy allocations during dry (critical) andaverage precipitation year conditions. Results of these simulations are shownin Annex 3, Tables 3.3, 3.4 and 3.5.

3.10 The simulation studies were used to: (a) determine the commissioningdates of new power plant additions (a new power plant was added to the systemwhen a deficit in peaking capability and/or energy supply occurred; each powerplant was pre-selected based on optimization studies, and the generationprogram was determined using economic criteria and international fuel prices);(b) evaluate probable yearly generation from individual power plants; and(c) derive adequate margins of generation reserves (varying from 20% in 1983to 5% in 1986, according to system operational characteristics). The selected(least-cost) 1980-1995 expansion program consists only of hydroelectric powerschemes. The analysis carried out to define the energy and power balances wascomprehensive and based on adequate hypotheses; the premises, assumptions andresults of these studies are satisfactory.

Distribution Losses

3.11 In 1978, INECEL's subsidiaries' distribution losses (including theftand unaccounted) amounted to nearly 200 GWh, representing about 15% of theutilities' gross generation plus energy purchases. Some subsidiaries havereached unacceptable loss levels (up to 35% in the case of the Latacungaand Azogues utilities), mainly due to inadequacies of their distributionsystems and deficiencies of their recording methods. Information on losses bycompany is given in Annex 3,Table 3.6. During negotiations agreement wasreached with INECEL that it will: (a) engage consultants no later thanDecember 31, 1981 (under terms of reference acceptable to the Bank) to carryout a study to improve the overall efficiency of the subsidiaries' distributionsystems (including review and standardization of current distribution planning,construction and operational practices, improvement of existing distributionsystems, and measures to reduce theft); (b) discuss the conclusions and recom-mendations of the consultants with the Bank; and (c) implement such recommenda-tions as have been agreed upon with the Bank, per an agreed timetable.

- 18 -

4. PROGRAM AND PROJECT

Background

4.01 INECEL, with the assistance of consultants financed by LoanS-006-EC (para. 1.23), is currently preparing a National ElectrificationMaster Plan, designed to: (a) assess Ecuador's future power market;(b) select the least-cost program for power generation expansion based onhydroelectric, geothermal and conventional thermal developments; (c) optimizetransmission and distribution systems expansion; and (d) formulate theinvestment programs required to execute and implement the foregoing works.

4.02 The Master Plan studies are being developed in three stages: short-term (1978-85), medium-term (1985-92) and long-term (1992-2000). Thefollowing studies are also included under the Master Plan: (a) inventory ofEcuador's hydroelectric 1/ and geothermal 2/ resources, which will collectexisting information and will create new information banks containing carto-graphic, hydrological and geological data, as well as information regardingthe development stages of hydroelectric sites (identification, evaluation,prefeasibility, feasibility and detail design studies); and (b) developmentof an Integrated Planning System which will optimize the hydro/geothermalpower plants (identified in the inventory of hydro/geothermal resources) andtheir installation sequence.

4.03 The short-term (1978-85) Master Plan studies have already beencompleted and the draft reports were found to be adequate. The medium-termand long-term Master Plan studies are currently progressing satisfactorilyand draft reports are expected to be available from December 1981 to February1982.

Construction Program

4.04 The main objectives of INECEL's construction program are to:(a) meet the different regional systems' power requirements through theaddition of new generating capacity; (b) integrate all of INECEL's subsidiariesand some municipal systems to the National Interconnected System (SNI) througha new 230/138 kV transmission network in order to achieve fuel economies andincrease efficiency; and (c) provide electricity to an additional 1,500,000inhabitants (about 250,000 new customers) through the construction of new sub-transmission and distribution systems. The proposed Bank project wouldcontribute to the achievement of these objectives by: (a) delivering the

21/ The inventory is expected to cover about 225,000 km , or about 70% of

Ecuador's surface area, and about 80% of Ecuador's estimated hydro-electric potential. Only hydroelectric schemes larger than 30 MW areto be included.

2/ The inventory of geothermal resources, originally to be financed bythe Bank, is now being financed through a grant from OLADE.

- 19 -

hydroelectricity to be generated by the existing and proposed hydropower plantsto the different load centers; (b) incorporating the different isolated systemsto the SNI network; and (c) improving INECEL's management and staff skills throughcomprehensive training programs and assistance from consultants.

4.05 In order to meet energy and power capacity requirements during theperiod 1980-90, INECEL and its subsidiaries have prepared generation, trans-mission and distribution 1/ construction programs which are based on detailedanalyses of the capability of existing generation and transmission facilitiesand of facilities being added to the existing system and on the results of theshort-term Master Plan optimization studies.

4.06 The construction program includes the following major works:(a) about 940 MW and 1,220 MW of new generating capacity to be installedduring 1980-85 and 1986-90 respectively; (b) about 860 and 775 circuit-kilometers of 230 kV and 138 kV transmission lines to be commissioned during1980-82 and 1983-86 respectively; and (c) expansion of subtransmissionand distribution systems. Details of capacities and commissioning datesfor the different construction program works are given in Annex 4, Attachment4.1.

Generation Expansion Program

4.07 Currently, INECEL is constructing the following generating facilities,which are part of its 1980-85 expansion program:

(a) Paute (Phase A and B) hydroelectric power plant, which is expectedto be commissioned during 1982 (2 x 100 MW) and 1983 (3 x 100 MW);

(b) Esmeraldas thermal plant, consisting of I x 125 MW residualfuel-based steam turbine plant, to be commissioned during 1981;

(c) Guayaquil No.3 (73 MW) oil fired steam generator and Quito (60 MW)gas turbines, to be commissioned during 1981; and

(d) About 180 MW of small gas turbines and diesel engine generators,to be installed by the different INECEL subsidiaries during theperiod 1980-82 while the interconnected system becomes operational.

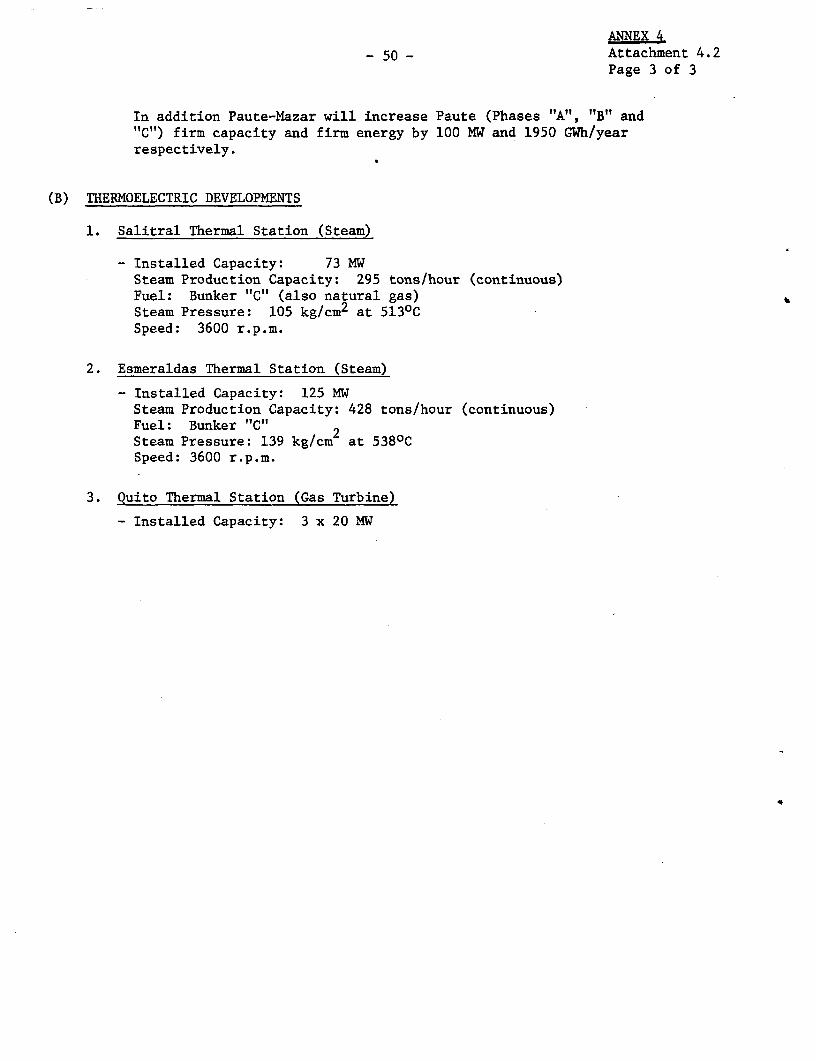

Details of these works are provided in Annex 4, Attachment 4.2.

4.08 To meet estimated energy requirements through 1990 and to partiallysubstitute for thermal generation, INECEL prepared a generation expansionprogram which includes the installation of the following hydroelectric powerplants: Agoyan (150 MW), to be operational by 1986; extension of the Pautehydro development (500 MW), to be completed by 1987; the Daule-Peripa multipur-pose development (130 MW), to be commissioned by 1988; the Paute-Mazar (140 MW)

1/ The 1986-90 transmission, subtransmission and distribution work programshave not yet been defined and are not expected to be until February 1982,when the results of the medium-term Master Plan will become available.

- 20 -

hydro development, to be commissioned by 1989; and the Toachi (300 MW) hydro-electric plant, to be commissioned by 1990. The characteristics of theseplants are given in Annex 4, Attachment 4.2.

Transmission Expansion Program

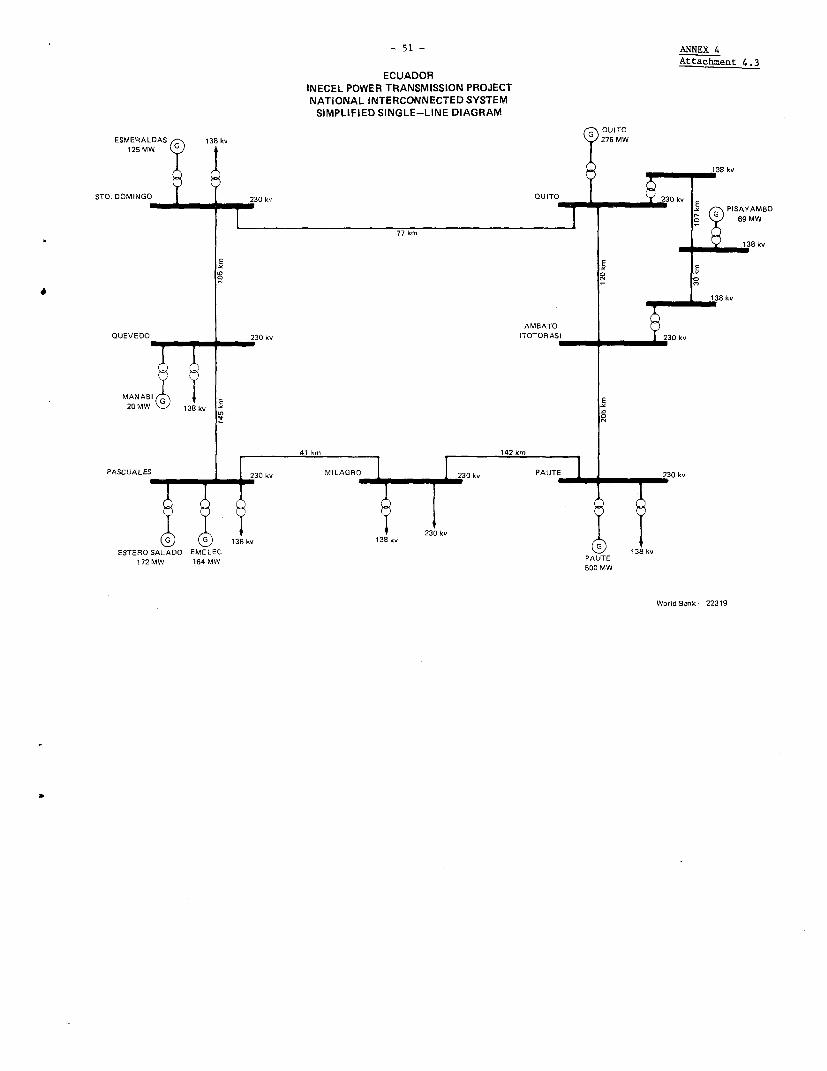

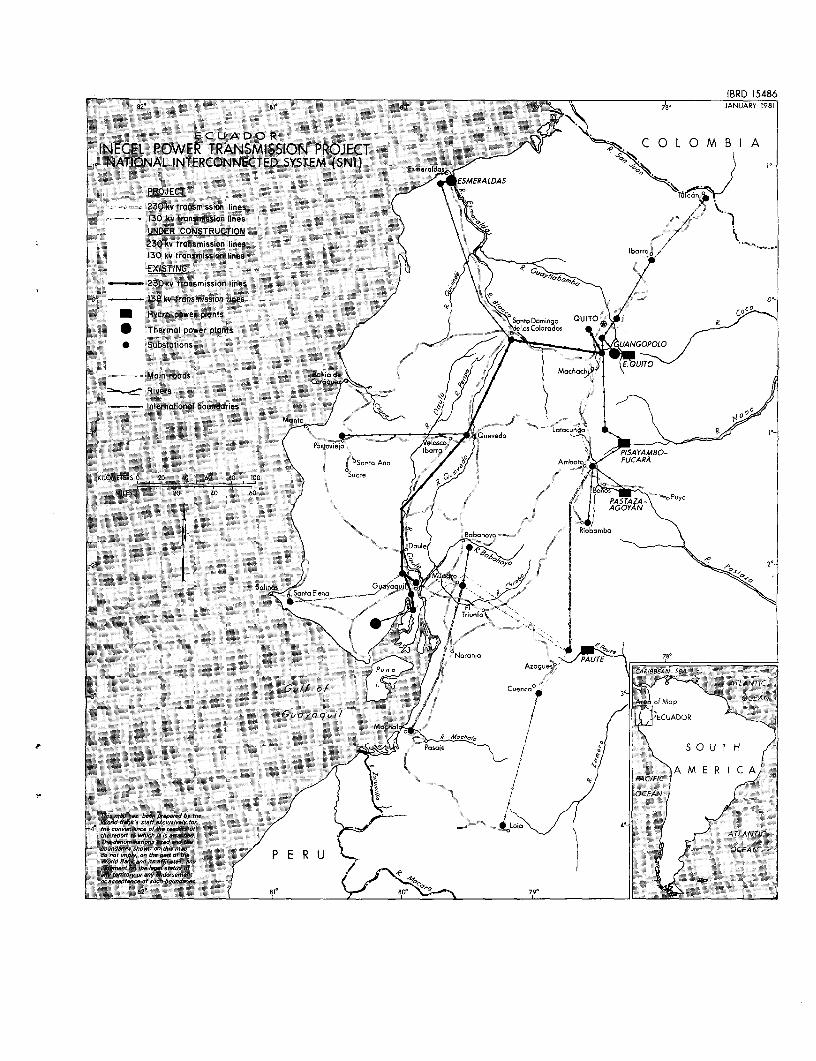

4.09 The existing transmission system is reduced to short links betweenmajor consumption centers and the nearby power generating stations. The firstNational Interconnected System major link was commissioned during August1980 and ties the two biggest consumption centers, Guayaquil and Quito,through a 654 circuit km - 230 kV transmission line. The following trans-mission lines, part of the 1980-85 expansion program, are currently underconstruction and are expected to be commissioned before the end of 1982:(a) 366 circuit km - 230 kV, Guayaquil-Paute; (b) 80 circuit km - 138 kVQuito-Ibarra; (c) 308 circuit km - 138 kV, Santo Domingo-Esmeraldas, and(d) 107 circuit km - 138 kV, Quevedo-Puertoviejo. Details of the NationalInterconnected System are shown in Annex 4, Attachment 4.3 and in the map.Furthermore, during the period 1982-85 INECEL would install and commissionabout 338 circuit kms of 230 kV transmission lines, 427 circuit kms of 138 kVtransmission lines and about 280 MVA step-up/down transformation capacity atdifferent substations (proposed transmission project to be financed by theBank).

Subtransmission and Distribution Expansion Programs

4.10 The majority of the isolated systems (all of INECEL's subsidiaries)would be integrated to the main SNI network through subtransmission lines (69kV and 34.5 kV). About 1,300 circuit kms of 69 kV and 34.5 kV subtransmissionlines and about 450 MVA step-up/down transformation capacity at differentsubstations are to be installed and commissioned during the period 1982-85.

4.11 Since successful completion of the subtransmission component affectsthe economics of the overall power development program and of the proposedproject, appropriate measures regarding work supervision and technical assistanceare required. INECEL has already submitted to the Bank a revised 1981-85subtransmission program, which defines which lines it would erect itselfand which would be erected by its subsidiaries and provides updated costestimates, bidding and implementation schedules and defines the financingarrangements proposed. During negotiations agreement was reached that INECELwill assume full responsibility for the adequate supervision and timelycommissioning of the subtransmission works and will submit periodic reportsto the Bank on the progress of these works.

4.12 During the period 1982-85, INECEL and its subsidiaries aim to provideelectricity to about 1,500,000 additional inhabitants in different areas ofEcuador (this represents about 250,000 new electricity consumer services).This would increase Ecuador's electrification rate from 38% in 1978 to 50% in1985. For this purpose, INECEL's subsidiaries plan to construct new lowvoltage distribution circuits and extend and improve existing distributionsystems. INECEL also plans to implement a two-stage rural electrificationprogram with assistance from IDB for the first stage. The projected electrifi-cation rate (13% for the period 1982-1985) is somewhat higher than historicaltrends (11.5% for the period 1972-1978), but INECEL and its subsidiaries havethe manpower and equipment capabilities to achieve the proposed target.

- 21 -

Sector Investment Requirements

4.13 INECEL has prepared a 1980-85 power sector investment program,which is in line with CONADE's five-year national development plan.The investment requirements for this period (see Annex 4, Table 4.2) areestimated at US$1,636 million, at 1980 price levels. About US$1,377 millionare to be invested by INECEL in: (a) SNI generation plants (US$782 million)(b) 138 kV and 230 kV SNI transmission lines (US$304 million); (c) 69 kVand 34.5 SNI subtransmission lines and rural electrification (US$164 million);and (d) studies and general investments (US$127 million). In addition,EMELEC and INECEL's subsidiaries are expected to invest about US$259 millionin their distribution systems. A summary of the investment program is givenin the following table:

Ongoing Works US$ Millions(1980 constant prices)

Generation 1/ 352Transmission 132Subtransmission and Rural Electrification 60INECEL Subsidiaries 2/ 120General Investments 3/ 27

Subtotal 691

Future Works

Generation 1/ 477Transmission 176Subtransmission and Rural Electrification 109INECEL's Subsidiaries 2/ 144General Investments 3/ 39

Subtotal 945

Total 1980-85 Investment Program 1,636

1/ Includes cost of studies (feasibility and detail design).2/ Includes investments by INECEL's subsidiaries in power generating plant

and distribution networks.3/ Includes general studies, buildings (US$20 million), office equipment,

transportation equipment, and the like.

The Project

4.14 The project proposed for Bank financing would consist of 230 kV and138 kV transmission lines and corresponding conversion (step-down) substations.It would also include training and institutional development programs, engineer-ing services for the design of a National Dispatch Center and engineering ser-vices for the supervision of the execution of the transmission/substation works.

- 22 -

4.15 Issuance of bidding documents for the purchase of equipment andmaterials is expected to start by January 1982 and construction by January1983. The physical works included in the project are expected to be completedby December 1984 and the studies by June 30, 1985.

4.16 The physical works and consulting services included in the proposedproject are described below (see Annex 4, Attachment 4.3 and map):

(a) Transmission Lines

(i) Construction of about 338 circuit km of 230 kV transmissionlines: (a) from the Paute hydroelectric plant to Totoras(near Ambato); and (b) from Milagro to Machala; and

(ii) Construction of about 427 circuit km of 138 kV transmissionlines: (a) from Guayaquil to Santa Elena; (b) from Cuenca toLoja; (c) from Ibarra to Tulcan; and (d) from Totoras to Ambato.

(b) Substations

Construction of substations and installation of step-down trans-formers at Machala (60 MVA), Riobamba (60 MVA), Santa Elena (40 MVA),Posorja (20 MVA), Tulcan (60 MVA) and Loja (40 MVA); and extensionof Ibarra substation.

(c) Training Program

Consultants' services for reviewing the existing training program andtraining facilities of INECEL and its subsidiaries; and costs ofspecific training programs, additional training facilities, purchaseof laboratory and training equipment, and scholarships for technicaland administrative staff.

(d) Institutional Development Program

Consultants' services for reviewing organizational, financial,commercial, and data processing matters and procedures of INECEL andits subsidiaries and purchase of computer software for accounting/commercial purposes.

(e) Engineering/Consultant Services

(i) Engineering services for the design (up to bidding documentsand their evaluation) and supervision of the installation ofthe National Dispatch Center, and (ii) consultant services forthe supervision of the proposed transmission project during theconstruction period.

Project Cost Estimates

4.17 Project cost is estimated at US$144 million, of which US$86 millionis the foreign exchange component. The project cost was estimated by INECEL'splanning and construction staff and reviewed and updated by the Bank. Thecost estimate is based on recent prices for equipment and materials and oncosts for installation and construction obtained from contracts recently

- 23 -

awarded by INECEL (230 kV Paute-Guayaquil and 138 kV Esmeraldas-Santo Domingotransmission lines) and from works recently commissioned (230 kV Guayaquil-Quito transmission line). The estimate is considered reasonable.

4.18 The project costs, which are detailed in Annex 4, Table 4.3, aresummarized in the following table:

Project Cost

US$ MillionLocal Foreign Total

Transmission Lines 13 34 47Substations 5 19 24Engineering and Administration 11 1 12Consultants' Services and Studies 1/ 1 5 6

30 59 89

Physical Contingencies 3 6 9Price Contingencies 25 21 46

Total Project Cost 58 86 144

1/ Includes Training Program (US$2.0 million), Institutional DevelopmentProgram (US$3.1 million) and Load Dispatch Center design (US$1.6 million).

Import duties are not included in these estimates as INECEL is exempt fromthese levies.

4.19 The project cost estimates are based on prices prevailing inJanuary 1980, escalated to reflect January 1981 price levels. Physicalcontingencies were calculated at a rate of 10% of direct costs on allproject components. In view of the nature of the works involved, thefigure is reasonable. Price contingencies were calculated using thefollowing annual escalation rates applied to basic costs and physicalcontingencies:

- 24 -

Percent (%)1981 1982 1983-85

Local Products and Services 20 15 15Foreign Products and Services 9 8.5 7.5

Project Financing Scheme

4.20 The financing scheme for the project would be as follows:

(a) local costs, amounting to US$57.9 million, would be financed fromINECEL's net internal cash generation and from Government contri-butions;

(b) foreign exchange costs which amount to US$86.2 million, includingindirect foreign exchange costs, and US$13.8 of financial chargeswould be financed by the proposed US$100 million Bank loan; and

(c) the balance of financial charges, amounting to US$11.2 million,would be financed from internally generated funds.

Engineering and Consultants' Services

4.21 INECEL's engineering staff is preparing the designs and specificationsfor equipment, materials and construction works, assisted when necessary byspecialized consultants (IECO-USA and individual consultants who are currentlyunder contract with INECEL). The same staff is also preparing the biddingdocuments for all project items.

4.22 INECEL will engage consultants under terms of reference andcontractual conditions acceptable to the Bank for the following tasks.

(a) training program, for which a total of 36 consulting staff-monthswere estimated to be required, at an average cost of US$12,000per staff-month 1/;

(b) institutional development program, expected to require about 126consulting staff-months at an average cost of US$12,000 perstaff-month 1/;

(c) load dispatch center, expected to require about 82 engineeringstaff-months at an average cost of US$12,400 per staff-month 1/;and

(d) supervision of project construction during the period June 1982-December 1984, which is expected to require about 80 consultantstaff-months at an average cost of US$5,000 per staff-month 1/.

1/ Excluding travel allowance costs.

- 25 -

Procurement and Disbursements

4.23 Most contracts for the supply of equipment and materials and theirinstallation (including civil works) to be financed with funds from theproposed loan will be procured through international competitive bidding(ICB) procedures in accordance with Bank guidelines. Competitive biddingin accordance with other procedures satisfactory to the Bank, such as interna-tional shopping, will be appropriate for a few contracts (such as laboratoryand training equipment, vehicles and computer software and hardware), each notexceeding US$100,000 and estimated not to exceed US$1,000,000 in total. Mostof the equipment and materials to be procured for the transmission lines andsubstations will be imported, as the local manufacturers either do not havethe production capability to meet the quantities required (aluminum conductors)or do not produce the specialized equipment and materials required for theproject. Therefore, preference for bid evaluation purposes to local manufac-turers and suppliers has not been requested by the Government.

4.24 The loan would be disbursed over a five-year period (see Annex 4,Table 4.4) against (a) 100% of foreign expenditures for imported goods and 85%of the local expenditures for locally manufactured materials; (b) 14% of thetotal expenditures on the contracts for civil works and for the installationof the corresponding equipment and materials, representing the estimated in-direct foreign exchange costs of the goods to be provided by the contractors(construction materials, transport, machinery, equipment, furniture);(c) consulting services and related expenses as follows: 100% of foreignexpenditures for supervision of project construction, 95% of total costs fortraining program, 70% of total costs for the institutional development programand load dispatch center studies; and (d) interest and other charges duringconstruction on the Bank loan through mid-1984 up to US$13.8 million. Allrequests for disbursements of funds from the loan account would be fullydocumented. Retroactive financing for up to US$1,000,000 is proposed forpayment of consultants' fees incurred and paid by the Borrower after June 1,1981 to cover advanced expenditures directly related to the training andinstitutional development programs and the design of the load dispatchcenter. The closing date for the proposed loan would be December 31, 1985.

Project Execution

4.25 INECEL will engage contractors for the civil works and for theinstallation of the equipment and materials of the transmission lines andcorresponding substations through international competitive bidding (ICB)in accordance with Bank guidelines. It is expected that these contracts wouldbe awarded to foreign firms with ample experience in similar undertakings.Invitations to bid are expected to be issued by January 1982 (see Annex 4,Attachment 4.4 for complete implementation schedule).

4.26 INECEL's engineering staff, with the assistance of consultantswhose experience, terms-of-reference and conditions of employment are accept-able to the Bank (and who will be responsible for the overall supervision ofthe construction) would be capable of executing the project adequately, asdemonstrated by the successful completion of the Quito-Guayaquil transmissionline, which was commissioned on schedule in August 1980. During negotiationsagreement was reached with INECEL that these consultants will be engaged bySeptember 30, 1982.

- 26 -

4.27 Project execution will be monitored against target dates shownin the project implementation schedule (Annex 4, Attachment 4.4). INECEL'soperational, financial and managerial performance will be monitored throughperformance indicators which were agreed during negotiations (Annex 4,Table 4.5). During negotiations agreement was reached that INECEL willsubmit such indicators regularly to the Bank.

Environmental Aspects

4.28 The proposed project does not present major environmental problems.Transmission line routes are considerably distant from urban centers.Furthermore, substations would be located at urban centers with due regardto environmental and aesthetic considerations and in accordance withurban regulations. INECEL would compensate property owners as required by thenational legislation. Clearing of rights-of-way would be kept to a minimumand natural drainage patterns are not expected to be affected.

Project Risks

4.29 The project faces no special physical risks. Sector issues orinsufficient action on financial matters could, however, negatively affectinstitutional performance or result in program and project delays (paragraphs1.33 to 1.35 and 5.02 to 5.04).

5. FINANCE

Introduction

5.01 Over the past 15 years, electricity sales have increased at anannual rate exceeding 12% (see Annex 3, table 3.1, for the sales statisticssince 1970), thus requiring significant investments in power facilities.Despite this, INECEL has followed a policy of low electricity tariffs,placing a substantial financing burden on the Government.

5.02 In the next five years, investment requirements are expected to beeven larger than in the preceding years, so that by 1985 total fixed assetswill approximately double their present value in real terms. To accomplishthis, a major financing effort will be needed. This will put to a severe testthe intentions of the Government and of INECEL to simultaneously reduce fuelsubsidies significantly, raise electricity tariffs to adequate levels, andprogressively reduce the sector's dependence on Government contributions.

5.03 To meet the consolidated financing requirements of INECEL and of itssubsidiaries, average retail electricity tariffs (inclusive of fuel clause)will have to increase from an equivalent of about US$0.05/kWh in 1980 toUS$0.154/kWh in 1985. This implies a nominal increase of about 200%; however,after adjusting for estimated domestic inflation the real increase would beabout 50%. To achieve this, INECEL has put into effect a policy of monthlytariff increases averaging 3% and has agreed to maintain these increases untilthe covenanted rates of return have been attained. This policy is expected to

- 27 -

result in a December 1981 retail tariff (inclusive of fuel clause) of S/1.74/kWh,which represents an increase of 32% over the December 1980 level. At negotia-tions, it was also agreed that cost increases in excess of those forecastwould be automatically reflected in additional tariff adjustments through theimplementation of existing legislation (para. 1.26).

5.04 At negotiations, the Government agreed to assign nearly US$900 millionequivalent (nearly 70% of which are expected from INECEL's participation inoil royalties) to the power sector between 1981 and 1985. Assurances werealso obtained that any shortfall in oil royalties would be made up throughother Government equity contributions. If such support were not to materialize,the financial viability of the investment program would disappear.

5.05 Annex 5, tables 5-1 through 5.8, show INECEL's historic and forecastconsolidated financial statements and complementary financial information.Since INECEL does not presently prepare consolidated financial statements,such consolidation was done by the appraisal mission. Analogously, fixedassets which had not been hitherto revalued (despite legal provisions which sorequire) were revalued, on an estimative basis, by the appraisal mission (seeTable 5.2, footnote b). For these reasons, and also because the originalstatements were not audited (paragraphs 2.17 and 2.18) the historic statementsshould be viewed as estimates. The mission forecasts are expressed in currentdollars (internal prices were assumed to increase at an annual rate of 15% andexternal prices at 9%; fuel price assumptions are discussed in Table 5.1,footnote f). A constant exchange rate of S/. 25 = US$1 was assumed.

Financial History

5.06 Though INECEL was legally constituted in 1961, in its early yearsits scope of activity was very limited and mainly concentrated in planningsector development and promoting the regional integration of the small localsystems. In 1973, INECEL commenced to invest in generating plants and itsfirst installations were commissioned in 1976. Investment in a major genera-tion project, Paute (500 MW), started in 1975 and only built up in recentyears.

5.07 Thus, INECEL's financial history is, for all relevant purposes, veryshort and provides little guidance as to its prospects for the future. Somesalient factors may, however, be noted:

(a) Net internal cash generation has been negative and financing needs(which were not only caused by INECEL's own expansion but also bythe requirements posed by INECEL's subsidiaries) were mainly fi-nanced through Government contributions (of which the main sourcewas INECEL's participation in oil royalties) and external loans.

(b) INECEL's debt-equity structure has evolved within conservativebounds, keeping well below a 50:50 ratio (based on fully revaluedfinancial statements, as estimated by the Bank mission), thussuggesting that increased reliance on long-term indebtness isviable, provided revenues are increased to ensure adequate debtservice coverage.

- 28 -