Embed Size (px)

Citation preview

DOCUMENT OF THE WORLD BANK

FOR OFFICIAL USE ONLY

' REPORTNO. 27627-MX

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

PROGRAM DOCUMENT

FOR A PROPOSED

PROGRAMMATIC LOAN

IN THE AMOUNT OF US$ 100 MILLION

TO THE

UNITED MEXICAN STATES FOR

AFFORDABLE HOUSING AND URBAN POVERTY

SECTOR ADJUSTMENT LOAN

APRIL 27,2004

FINANCE, PRIVATE SECTOR AND INFRASTRUCTURE MEXICO AND COLOMBIA COUNTRY MANAGEMENT UNIT LATIN AMERICA AND THE CARIBBEAN REGION

This document has a restricted distribution and may be used by recipients only in the performance of their official duties. I t s contents may not be otherwise disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

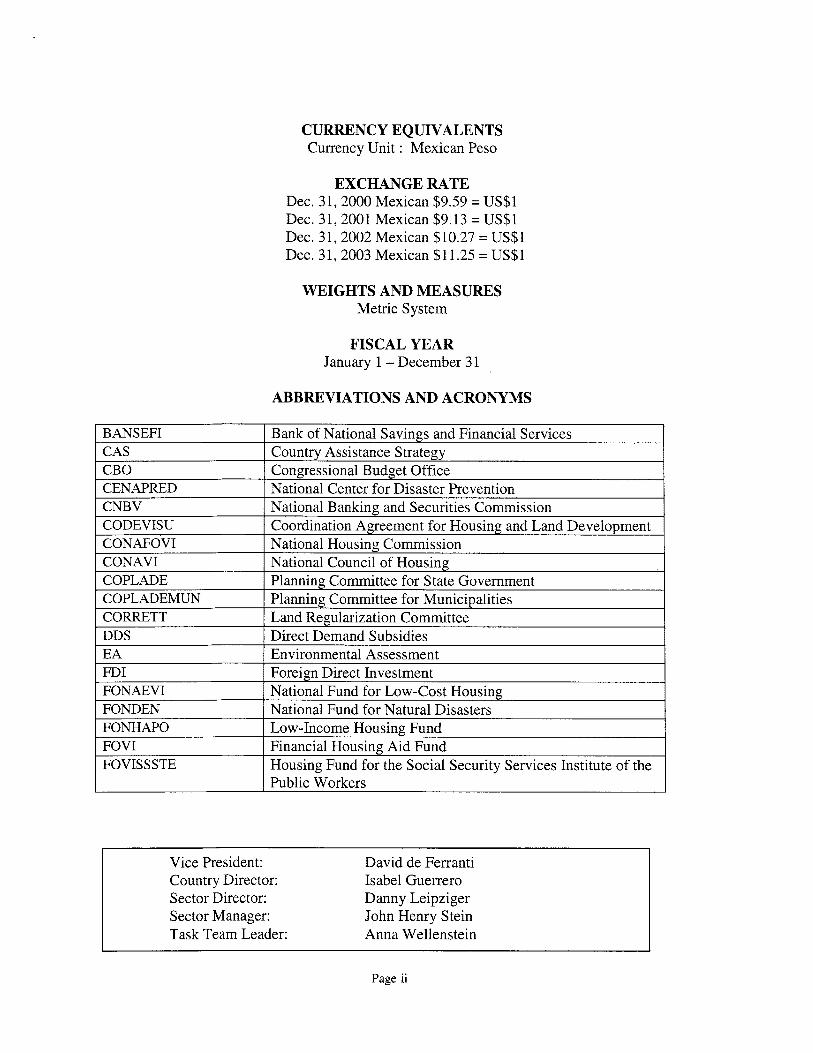

CURRENCY EQUIVALENTS Currency Unit : Mexican Peso

BANSEFI CAS CBO CENAPRED CNBV CODEVISU CONAFOVI CONAVI COPLADE COPLADEMUN CORRETT

EXCHANGE RATE Dec. 3 1,2000 Mexican $9.59 = US$1 Dec. 31,2001 Mexican $9.13 = US$1 Dec. 31,2002 Mexican $10.27 = U S $ l Dec. 31,2003 Mexican $1 1.25 = US$1

Bank o f National Savings and Financial Services Country Assistance Strategy Congressional Budget Office National Center for Disaster Prevention National Banking and Securities Commission Coordination Agreement for Housing and Land Development National Housing Commission National Council o f Housing Planning Committee for State Government Planning Committee for Municipalities Land Regularization Committee

WEIGHTS AND MEASURES Metric System

EA FDI FONAEVI FONDEN FONHAPO

FISCAL YEAR January 1 - December 31

Environmental Assessment Foreign Direct Investment National Fund for Low-Cost Housing National Fund for Natural Disasters Low-Income Housing Fund

ABBREVIATIONS AND ACRONYMS

FOVI FOVISS STE

Financial Housing Aid Fund Housing Fund for the Social Security Services Institute o f the Public Workers

1 DDS I Direct Demand Subsidies I

Vice President: Country Director: Sector Director: Sector Manager:

David de Ferranti Isabel Guerrero Danny Leipziger John Henry Stein

I Task Team Leader: Anna Wellenstein I Page ii

FOR OFFICIAL USE ONLY

GOM HUSAL

HUTAL

I GDP I Gross Domestic Product I Government o f Mexico Programmatic Affordable Housing and Urban Poverty Sector Adjustment Loan Housing. and Urban Technical Assistance Loan

IBRD IDB INDESOL INFONAVIT LICONS A

International Bank for Reconstruction and Development Inter- American Development Bank National Institute for Social Development Institute for National Housing Fund for Public Workers Industrial Milk ConasuDo

MW

NAFTA NGO OECD

I PROCEDE I Program for Ej ido and Urban Land Regularization

Minimum Wage (1MW= MX $1,20O/month = US$lOS)/month) North American Free Trade Agreement Non-Governmental Organization Organization for Economic CooDeration and DeveloDment

~

PROSAVI SEDESOL Social Development Ministry SHCP

Special Program for Housing Credit and Subsidies

Secretarv o f the Treasurv and Public Credit SHF SOFOLES UDI VIVAH WBI

This document has a restricted distribution and may be used by recipients only in the performance of their official duties. I t s contents may not be otherwise disclosed

' Federal Mortgage Corporation Financing Societies with Limited Purposes Investment Unit Savings and Subsidies Program for Housing World Bank Institute

/without W o r l d Bank authorization. I

TABLE OF CONTENTS PAGE

LOAN AND PROGRAM SUMMARY ................................................................................................................. v

1.

11.

111.

A. B. C. D. E. F. G.

Iv. A. B. C. D. E. F.

V.

VI.

VII.

VIII.

M.

RATIONALE AND OBJECTIVE ........................................................................................................... 1

HISTORICAL CONTEXT ....................................................................................................................... 2

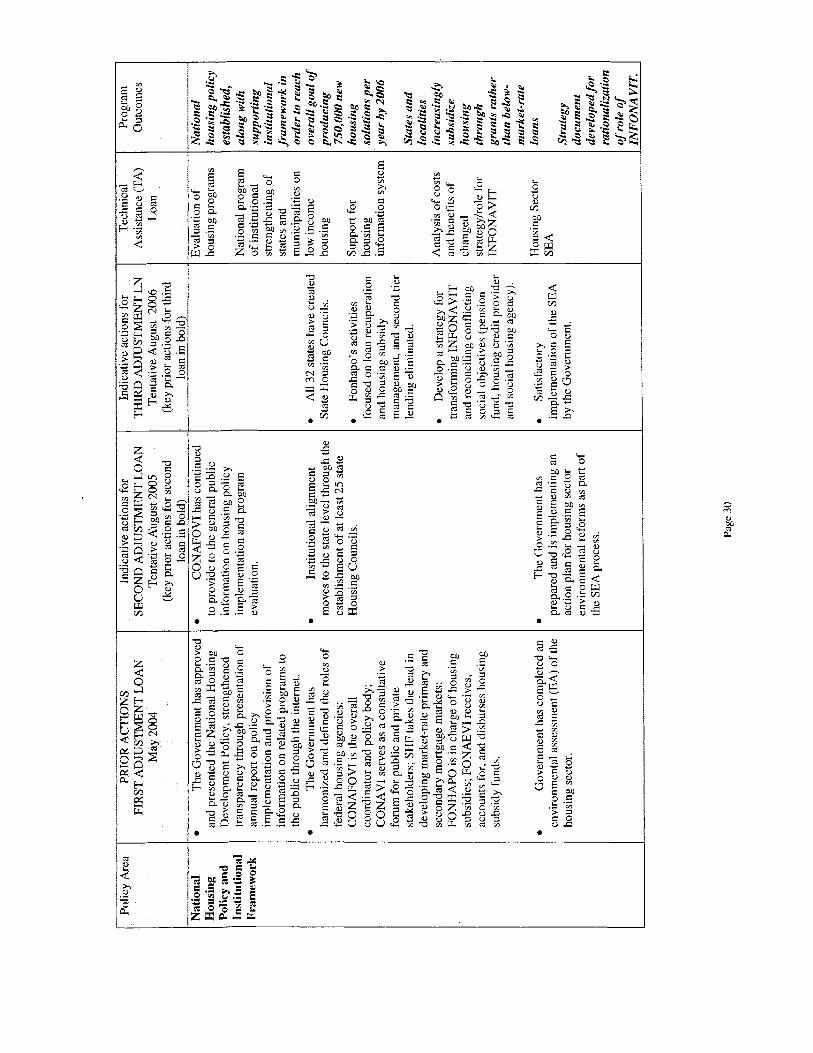

MEXICO’S HOUSING AND URBAN REFORM AGENDA 2001 - 2006 .......................................... 6

NATIONAL HOUSING POLICY AND INSTITUTIONAL FRAMEWORK.. ... ... ... . .. . ..... ... . ..... HOUSING SUBSIDIES. ............................................ 7 HOUSING CREDIT AN URBAN REAL PROPERTY REGISTRIE NATIONAL URBAN POLICY, S L U M UPGRADING AND INSTITUTIONAL STRENGTHENING 14 LOW AND MODERATE INCOME LAND DEVELOPMENT .............................................................. 15 DISASTER PREVENTION AND MANAGEMENT ....

THE PROPOSED LOANS ..................................................................................................................... 17

OBJECTIVES OF THE PROGRAM ... CONTENT OF THE! PROGRAM ........ ..................................................................................... 18 ANALYTICAL UNDERPINNINGS . . . ......... . . . .. . ........ .... . . .... .. ......... CONTENT OF THE LOANS ...... .. . ..... . . ... . . ... . .... . .... . .. . .... . . ..... . .. ......... . . . . .. .... . . . . ..... . ...... . ... . . .. ... . .... . ... . .. . .. . . 18 FINANCIAL ASSISTANCE & INSTITUTIONAL & IMPLEMENTATION ARRANGEMENTS. ... . .. 22 ENVIRONMENT AND RESETTLEMENT ...................................................................................... 23

THE MACROECONOMIC FRAMEWORK FOR THE PROPOSED OPERATION .................... 24

BANK STRATEGY ................................................................................................................................ 25

BENEFITS ............................................................................................................................................... 26

RISKS AND MITIGATION ................................................................................................................... 27

RECOMMENDATIONS ........................................................................................................................ 28

...............

TABLE 1: SUMMARY LEXICON OF AFFORDABLE HOUSING AND URBAN DEVELOPMENT IN MEXICO .............................................................................. .................................................................... 4

TABLE 2: OVERVIEW OF MEXICO HOUSING AND URBAN SECTOR ADJUSTMENT PROGRAM ....... 20 TABLE 3: MEXICO’S MAIN MACROECONOMIC INDICATORS ... . ..... . . ..... . ... . ... . .. . .. .... . .. ... . ... ... ... ... .. . . .. . .. . ... 24

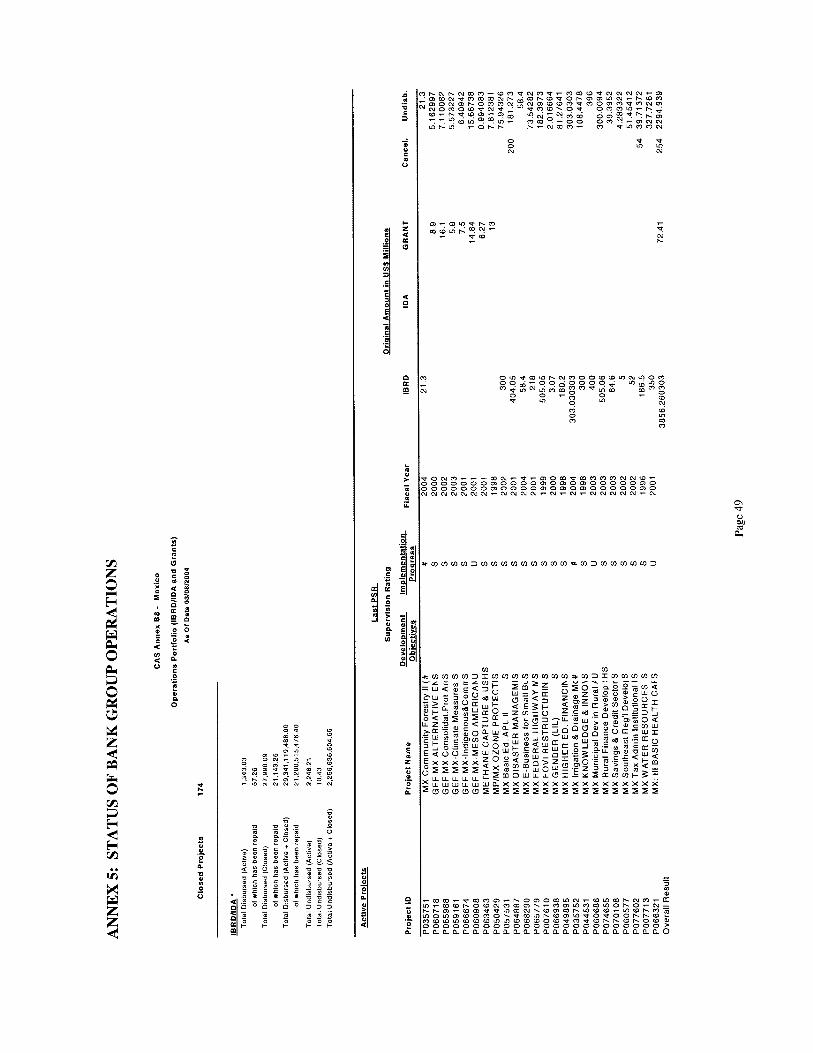

ANNEXES 29

Annex 1 : Policy Matrix Annex 2: Annex 3: Annex 4: Annex 5: Annex 6: Annex 7:

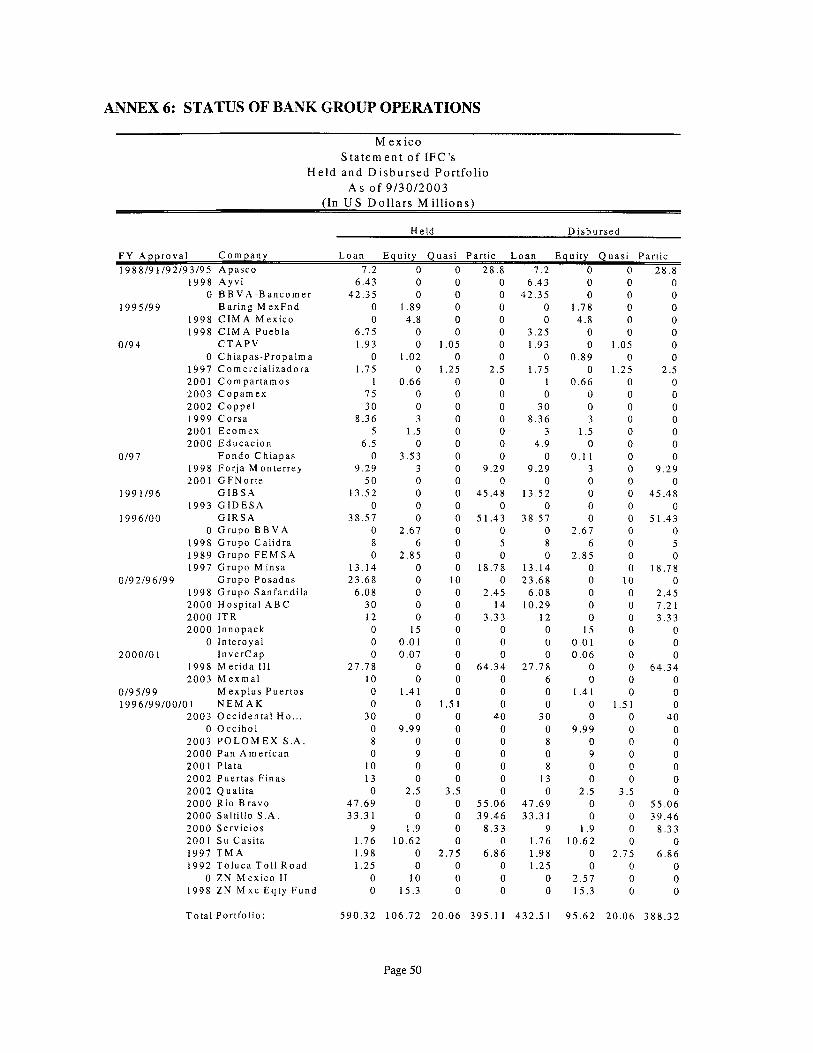

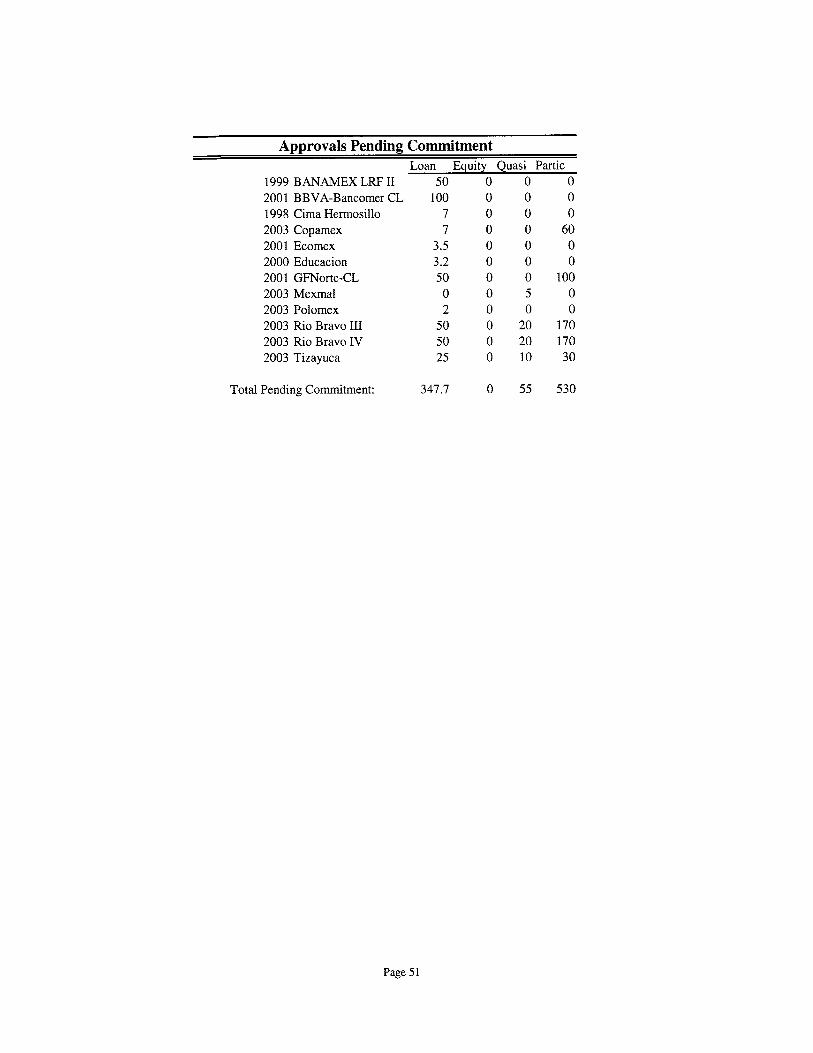

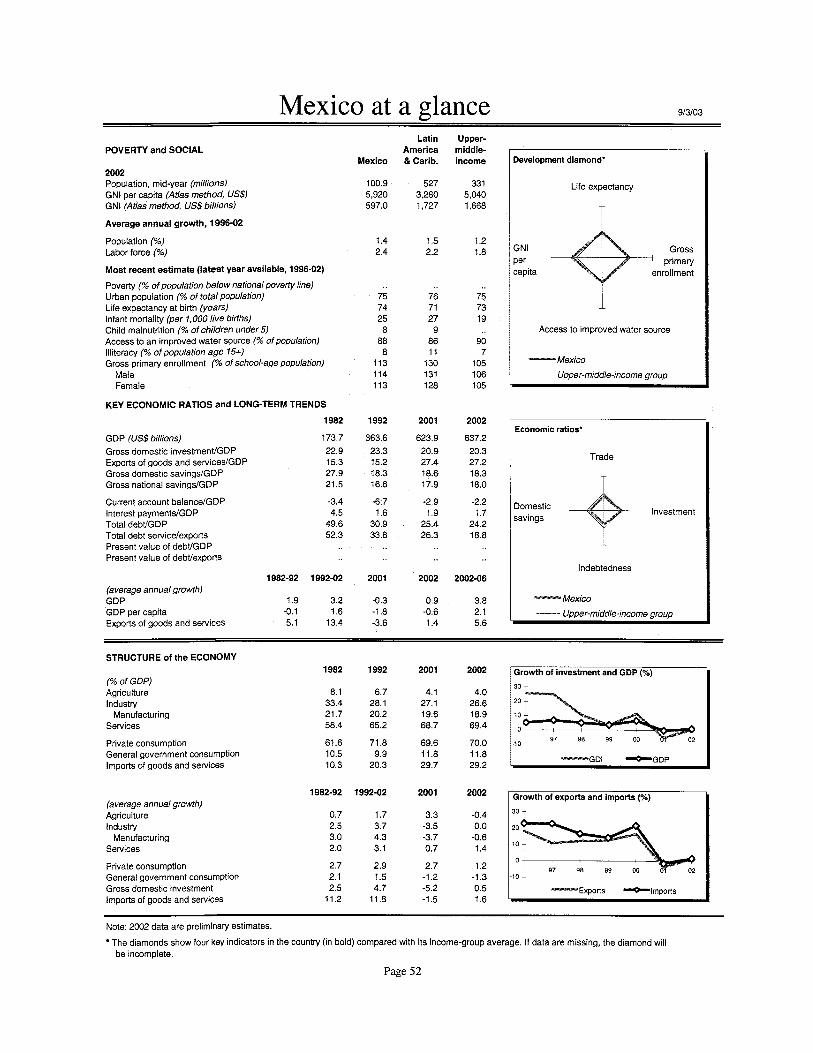

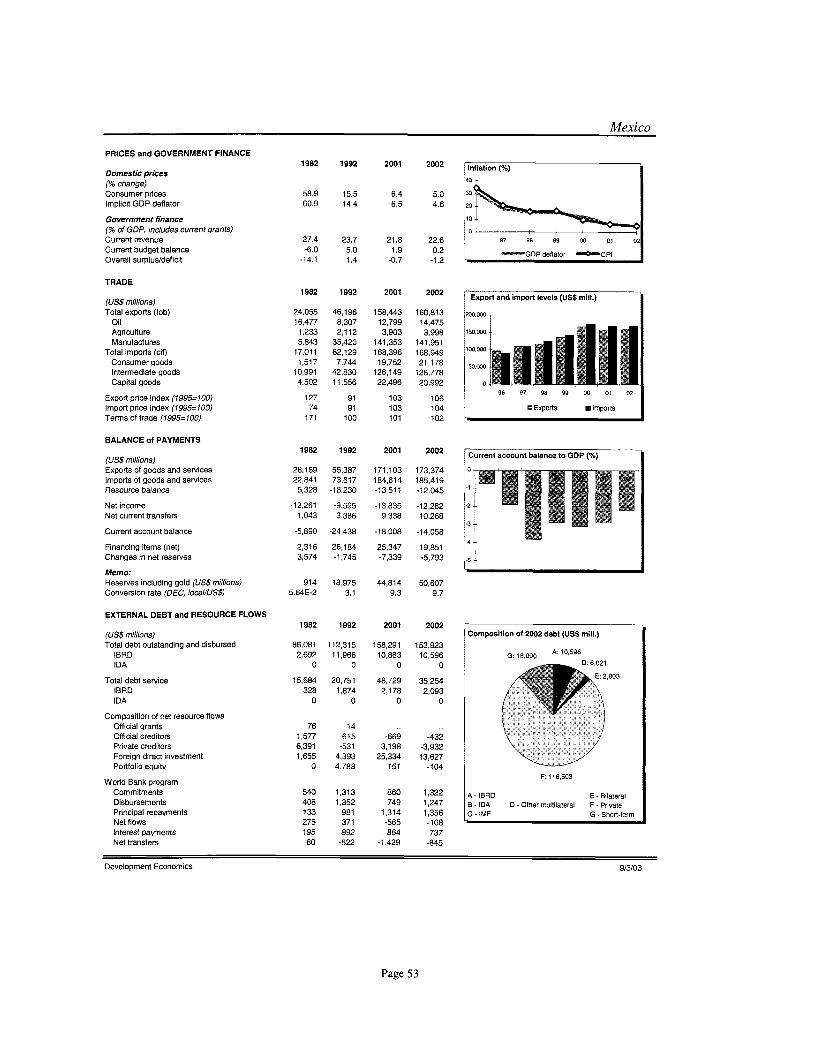

Letter o f Development Policy Environmental and Social Aspects of the HUSAL Mexico - Fund Relations Status o f Bank Group Operations Statement of IFC’s Held and Disbursed Portfolio Mexico at a Glance

29 38 44 48 49 50 52

Page iii

This operation was prepared by a World Bank team composed o f D. Bil ler, T. Campbell, R. Chavez, L. Chiquier, M. Freire, W. Gwinner, M. Hoek-Smit, E. Mosqueira, K. Oleson, C. Piedrafita, P. Pini, M. Sabella, V. Serra, T. Solo, J. Stein, C. Velazco-Weiss. The team was lead by A. Wellenstein and Bruce Ferguson. Peer Reviewers were Christine Kessides, Omar Razzaz, Jan Brzeski, Robert Buckley, and Wi l l i am Cobbett. The team worked under the general guidance of John Henry Stein (Sector Manager), Mar ia Emi l ia Freire (previous Sector Manager), Isabel Guerrero (Country Director), and Danny Leipziger (Sector Director).

Page i v

MEXICO AFFORDABLE HOUSING AND URBAN POVERTY PROGRAMMATIC SECTOR ADJUSTMENT LOAN

LOAN AND PROGRAM SUMMARY

Borrower

Implementing Agency

Poverty Category Amount Terms

Commitment Charge

Front-End Fee

Objectives, description, and benefits

United Mexican States

Secretary of the Treasury and Public Credit

Not Applicable US$ 100 million Standard IBRD Terms

0.85% on undisbursed loan balances for f i rst four years, standard charge o f 0.75% on undisbursed balances thereafter, beginning sixty days after signing, less any waiver.

1% of loan amount

The operation proposed in this Program Document represents the first of a series o f quick disbursing loans to support the Government o f Mexico’s (GoM) low- income housing and urban program. The proposed first Affordable Housing and Urban Poverty Sector Adjustment Loan (HUSAL I) in an amount of US$ 100 mill ion wi l l support initiatives already completed. The second HUSAL of US$ 100 million and third HUSAL o f US$ 200 mill ion wi l l follow 12 and 24 months later, depending on the pace o f reform implementation. A Housing and Urban Technical Assistance Loan (HUTAL) wi l l accompany this three-year adjustment program.

Mexico i s at a critical point in i t s demographic history where affordable housing and related urban development represent crucial challenges for the country’s socio-economic development. Although population growth rates have slowed dramatically, the formation of new families by the “baby boom” o f the 1970s and 1980s wi l l double the number o f total households and the resulting demand for housing and basic services between the years 2000 and 2030 as this group comes of age. The institutions and financial architecture necessary to serve about 60 percent o f families are largely in place. Low and moderate-income families, however generally lack formal-sector support. If this problem goes unaddressed, the resulting informal settlement, lack o f housing, and attendant social, economic, environmental, and health problems w i l l generate enormous private and public costs. The Government has committed to address this critical challenge by doubling formal-sector housing production to 750,000 housings solutions per year by 2006.

This operation furthers this goal in seven key areas, which compose the objectives o f the program:

Page v

Risks

Develop a sound national policy and institutional framework for housing and urban development; Design and put in place a unified housing subsidy policy that facilitates access of low/moderate-income families to housing and leverages household savings and private credit finance; Strengthen the housing credit and savings systems, and move these systems downmarket; Strengthen urban real property registries and rights; Increase the supply o f urban land and access by the poor and improve this market’s function; Coordinate and support physical and social investments to systematically upgrade poor neighborhoods; and Better prevent and manage the impacts o f natural disasters.

The cross-sectoral approach i s relatively ambitious, and -thus- may risk timely approval of the second and third loans. However, the natural synergies and complementarity among these areas require a comprehensive package to be effective. The GoM and the Bank address this risk through a well-designed, integrated strategy and a small number of key prior actions.

The project must also deal with several agencies to achieve the intended reform. The Program deals with this risk by relying on the leadership of the Ministry o f Finance (SHCP) -the key counterpart o f the loan - while worhng closely with the sectoral agencies in charge - CONAFOVI for housing policy, SHF for housing finance, and SEDESOL for urban development.

Net Present Value Not Applicable

Project PO7037 1 Identification Number

Page vi

IBRD PROGRAM DOCUMENT FOR A PROPOSED PROGRAMMATIC LOAN TO THE UNITED MEXICAN STATES FOR

AFFORDABLE HOUSING AND URBAN POVERTY SECTOR ADJUSTMENT

I. RATIONALE AND OBJECTIVE

1. Affordable housing and related urban development represent crucial challenges at this critical point in the Mexico’s demographic and socio-economic development. Population growth rates have decreased a percentage point every twenty years, going from 3% per annum in the 1960s to around 1% in 2002. However, the coming of age of the “baby boom” o f the 1970s and 1980s wi l l accelerate the pace of new household creation, doubling the number of total households and the resulting demand for housing and basic services between the years 2000 and 2030. This demand w i l l increase at even higher rates in cities as the country continues to urbanize. The institutional and financial architecture necessary to serve about two-thirds o f the families i s largely in place. However, low/moderate-income families generally lack formal-sector support. If this problem goes unaddressed, the resulting informal settlements, lack of housing, and attendant social, economic, environmental, and health problems w i l l generate enormous private and public costs. Housing and urban investment also account for around 10% of Mexico’s GDP and the construction sector consistently generates 9% of all employment. Finally, housing i s the main asset o f most families. GoM has responded by giving housing a high priority, setting a bold goal - to double production to match the rate o f new household formation (750,000 housing solutions per annum) - and putting in motion reforms to support housing and land markets, target assistance to the poor, and generate economic growth through housing investment.

2. This operation supports Mexico’s medium-term reform agenda in affordable housing and urban poverty. I t consists of a quick-disbursing loan (US$ 100 million) that w i l l be followed in the second and third years by quick-disbursing loans of an estimated US$ 100 mill ion and US$ 200 million, depending on reform progress. A Technical Assistance Loan w i l l accompany this three-year sector adjustment program in order to support the related policy changes.

3. The program’s overall objective i s to assist the Government’s efforts to improve the l iving conditions and access to real assets of low/moderate-income households. Specifically, the operation supports GoM to: (a) develop a sound national policy and institutional framework for housing and urban development; (b) design and put in place a unified federal housing subsidy system; (c) strengthen the housing credit and savings systems, and move these systems downmarket; (d) strengthen urban real property registries and rights; (e) coordinate physical and social investments to systematically upgrade poor neighborhoods; (f) increase the supply o f urban land and access by the poor and improve this market’s function; and (g) better prevent and manage the impacts o f natural disasters.

4. The program helps Mexico to achieve three objectives o f the CAS discussed by the Board on April 15, 2004: poverty reduction, competitiveness, and environmental sustainability. Most fundamental, the project wi l l improve affordable housing and basic services, and strengthen the real assets o f the poor. In addition, housing often serves as a key source o f capital accumulation and income generation for low/moderate-income households. Improving urban development enhances the efficiency o f cities, which account disproportionately for national economic growth. The project w i l l generate highly positive environmental impacts through upgrading existing slums and promoting formal-sector development on appropriate sites with rational layout.

5. The Government’s Letter of Development Policy (Annex 2) and the multi-year matrix of policy and institutional reforms for the proposed operation and potential subsequent loans (Annex 1) lay out the medium-term reforms supported by this program.

11. HISTORICAL CONTEXT

6. Access to housing and urban services strongly support both economic growth and poverty reduction. Mexico has a robust urban economy. About 66% of the population lives in urban centers and 80% of GDP originates in cities.’ Under previous administrations, many aspects o f housing and urban policy have clashed with attracting investment and reducing poverty. About 40% o f newly formed households (300,000 per year) earn less than 3 minimum wages (below US$ 327 per month) and cannot afford a finished house in a serviced neighborhood. National government has largely lacked the means to reach this group. Most federal programs and policy have, in effect, targeted moderate and higher income households, while financial institutions and developers have yet to reach the low/moderate-income market . 7. As a result, lowlmoderate-income families have mainly resorted to informal settlement and incremental building of their own units over five to fifteen years in order to afford homeownership. When unsupported and unguided by the private and public sector, such development generates enormous public and private costs; in the form of insecure tenure, poor construction, low quality, unhealthy environments, and inadequate and costly service provision. Roughly half o f all new housing production continues to occur informally without support from formal-sector institutions, prejudicing the country’s socio- economic development and these families’ l i fe prospeck2

8. The Government has committed to address this critical problem by doubling production of housing solutions and by promoting a sustainable expansion of the sector. To attain this goal, the administration i s taking measures to reform institutions and policies and to address the key bottlenecks in the sector. These actions include: (i) increase the efficiency and equity o f housing subsidy programs, harmonizing these efforts so that they provide comparable levels o f subvention for similar uses, and coordinating their administration; (ii) expand and diversify market-rate housing credit; and (iii) reform urban development, property rights, and land markets.

9. The operation proposed in this Program Document represents the f irst of a series o f quick disbursing loans to support the Government of Mexico’s (GoM) low-income housing and urban program. The proposed first Affordable Housing and Urban Poverty Sector Adjustment Loan (HUSAL I) in an amount o f US$ 100 million wi l l support initiatives already completed. The second HUSAL of US$ 100 mill ion and third HUSAL of US$ 200 mill ion w i l l follow 12 and 24 months later, depending on the pace of reform implementation. A Housing and Urban Technical Assistance Loan (HUTAL) wi l l accompany this three-year sector adjustment program.

10. Demand for Housing and Urban Services. New household formation - and, hence, demand for new housing and related urban services (basic infrastructure, and land) - runs at about 750,000 houses per year. According to CONAPO (National Population Council) the maturation o f Mexico’s “baby boom” of the 1970s and 1980s wi l l result in a doubling o f demand by the year 2030 by adding 23 mill ion new households to Mexico’s existing 22 mill ion households in the year 2000. About 40% o f this demand (300,000 per year) comes from families earning less than three minimum wages who in general cannot afford to purchase a market-financed commercially-built unit even with significant subvention. In

T h i s refers to the system of urban areas made up o f cities with populations over 15,000. Al l together, these cities account for 68,000,000 inhabitants. * Over the last decade, institutional mortgage finance has financed an average of around 325,000 units annually - roughly half of new household formation o f 750,000 families per year.

Page 2

comparison, current formal housing production financed by an institutional mortgage ran over 500,000 units in 2003.3

11. While rapid new household formation requires expanding new housing and urban services, improving existing homes and communities holds equal importance. Over 80% of Mexicans already have rights to the property in which they live.4 However, a large portion of these homes and attendant urban services and those of the surrounding communities are of poor quality. Approximately 2.5 mill ion houses require major improvements and 1 million need replacement. These less-expensive “housing solutions” cost a fraction o f the purchase of a new commercially-built home5 and - thus - represent the financially- sustainable alternative for most low/moderate-income families. In addition, surveys show that Mexican low-income households - as those in other countries - strongly prefer improving their existing home and their community to moving to a new unit in a social housing development far from work and critical social networks (friends, family - i.e. social capital). For various reasons, improving the existing housing stock and poor neighborhoods - in effect, support o f the progressive building and upgrading process - holds key importance for low-income households.

12. National housing policy and institutional framework. Until the last three years, the federal government lacked an effective vision for reform o f the housing sector. Similarly, the federal agencies involved in housing - FOVI (which has become SHF, and has lead responsibility for development of market-rate housing credit in Mexico), FONHAPO (a federal social housing agency), and INFONAVIT and FOVISSSTE (off-budget provident funds that receive mandatory contributions from, respectively, formally employed private-sector employees and federal-government employees) - operated with neither an overall strategy nor coordination. N o agency existed with responsibility for sector policy.

13. Housing subsidies. Over the last five years, Mexico has launched two small-scale (total funding of US$ 300 million in 2003) housing subsidy programs - Prosavi now operated by SHF (previously by FOVI), and Tu Casa (formerly called “Vivah”) now operated by FONHAPO. These two subsidy programs used wildly different levels and methods o f subvention. Until recently, the Prosavi program transferred a federal subsidy o f approximately US$ 6,000 (in 2002) for purchase o f an expandable unit built by private-sector developers and financed by private-sector financial institutions. In turn, Tu Casa operated by FONHAPO delivered a federal subsidy o f US$ 3,000 (matched by $3,000 from local government) for a core unit developed and financed by state and local housing institutes. These initial on- budget federal housing-subsidy programs have proved useful trials, but can be substantially improved - a pre-requisite for expansion of funding to a level necessary to have an important impact in reaching the government’s goal o f producing 750,000 housing solutions per year as intended. However, until the last three years, no plan or policy agency has existed for building on these subsidy programs to develop a unified national subsidy program - the mechanism that has proved most effective in Latin America.

For 2003, this included approximately: 291,400 units financed by INFONAVIT; 54,300 by SHFBOVI; 68,300 by FOVISSSTE; 23,000 by FONHAPO, and 63,000 by other sources. T h i s production covers new demand and some of the backlog in the above 3 minimum salary income household segment.

About 60% of these homeowners hold full legal title, while 40% have various degrees of para-legal rights to their property. The Mexican homeownership rate of over 80% compares to that of 67% in the US and in Canada, and an average of 61% in 16 Westem European countries.

The least expensive commercially produced unit costs US$ 16,000 and i s affordable only to families earning above five minimum salaries without subsidies. In contrast, major home improvement and/or expansion costs US$2,000 to US$4,000 and i s affordable to households earning 1.5 to 2.0 minimum salaries. Other relatively low-cost housing solutions include construction of a core unit on a lot already owned by a household (US$6,000 to US$ 8,000), and purchase of an existing unit in a low-income settlement (around US$ 10,000).

Page 3

Table 1 - Summary Lexicon of Affordable Housing and Urban Development in Mexico

BANSEFI. Th is federal institution was created in 2001 in order to promote household savings, help popular finance institutions adjust and prosper under the new Law for Popular Savings and Credit that phases in requirements between 2001 and 2004, and coordinate govemment support to financial institutions that focus on serving lowhnoderate-income households (“popular financial institutions”).

CONAFOVI. Formed in 2001. this federal institution - a dependency of SEDESOL that also reports to the President - develops housing policy and coordinates national housing institutions, particularly the federal housing institutions (SHF and FONHAPO), but also INFONAVIT and FOVISSSTE.

CONAVI. Created under the same law as that of CONAFOVI, this organization serves as a forum for public and private-sector input into housing policy and programs. and is managed by and reports to CONAFOVI.

CORETT. A dependency of SEDESOL, this organization has lead responsibility for regularizing informally-urbanized ejidos, and has operated on a massive scale. The process involves purchase of ejido land by the federal government (expropriation), regularizing title. and sale to the existing occupants.

Ejido land. Created by Article 27 of the Mexican Constitution, this form of communal property (often termed “social land”) was intended to protect rural farming communities and i s regulated by a complex set of federal laws and institutions. With urbanization, two-thirds of the land on the fringe of Mexico’s cities now consists of ejidos and constitutes the main source of developable parcels for new housing.

FONHAFW. Historically, this institution has served as the federal govemment’s main support to low-income housing. Poor repayment on below market-rate loans made by FONHAPO to state and local housing institutes that on-lent these funds to low-income households led to th is organization’s near bankruptcy, from which it has now recovered. A presidential decree has given the organization - along with FONAEVI - the mandate to develop a unified housing subsidy system. Currently, FONHAPOs main program is Tu Casa.

FONAEVI. A division of FONHAPO, this entity will receive, account for, and disburse funds under the unified housing subsidy system. and currently performs this function for Tu Casa.

FOVI. FOVI had the mandate to develop market-rate mortgage finance as a second-tier institution until the creation of SHF in 2002, which has assumed this role. FOVI continues as a trust within SHF with a number of specific functions mainly related to covering liabilities created during i t s former lending operation.

FOVISSSTE. This institution gets funding from a compulsory contribution of 5% of the salary of federal public-sector workers. I t then uses these resources to extend mortgage finance for housing at below-market interest rates graduated to favor lower-income households. FOVISSSTE accounts for around 14% of all mortgage finance. In addition to home lending, FOVISSSTE forms part of the pension fund for its contributing workers,

INFONAVIT. Governed by representatives of formally-employed workers, employers, and government, this institution gets funding from a governed compulsory contribution of 5% of the salary of private-sector workers and applies these monies to extend mortgage finance for housing at below. market interest rates graduated to favor lower-income households. INFONAVIT accounts for around 60% o f all mortgage finance. In addition tc home lending, INFONAVIT forms part of the pension system for i ts contributing workers.

Low-income household. A household earning 3 minimum wages (currently US$327 per month) and below

Minimum Wage. A measure used for social programs including housing programs. Currently, one minimum wage i s approximately US$ 109 pel month.

Moderate-income household. A household earning above 3 minimum wages to 6 minimum wages (currently US$ 327 to US$655 per month).

Prosavi. A subsidy program started by FOVI and now operated by SHF that provides an upfront grant (currently, about US$ 5,000). Households earning 4 to 6 minimum wages join this grant with a mortgage loan (currently from SOFOLES that receive their funding from SHF and that channe the Prosavi grant to specific projects) and a downpayment in order to purchase an expandable unit (around 40 m2; price: US$ 13,900) built b) developers.

SEDESOL. The Social Development Ministry holds overall responsibility for government action in urban development.

SHF. Created in 2002 as the successor to FOVI, the Federal Mortgage Society enjoys backing of the faith and credit of federal govemment for 1: years in order to lead the development of primary and secondary market-rate home lending. SHF operates as a second tier-finance institution tha provides liquidity and guarantees to first-tier lenders (currently, mainly the SOFOLES). SHF accounts for around 11% of total mortgage finance.

SOFOLES Hipotecarias. Following the withdrawal o f banks in 1995, these specialized lenders have become Mexico’s main source of private home lending. These institutions can make loans and raise debt on capital markets, but cannot accept deposits from the public.

Tu Casa (formerly “Vivah). A subsidy program operated by FONHAPO that delivers a federal grant (currently about US$3,000) that state and loca governments must match - typically with a serviced lot. The local government contracts the construction of a basic unit (up to 30 m2) that household: earning 2.5 minimum wages and below purchase by making a downpayment and, sometimes, their self-help labor in the construction.

Page 4

14. The bulk o f Mexico’s housing subsidies come in the form of below-market interest rates - off- budget subsidies mainly provided by INFONAVIT. In 2000, interest rate subsidies from INFONAVIT amounted to an estimated US$ 2.2 bi l l ion6 INFONAVIT and FOVISSSTE granted the highest subsidies on a per credit basis, near US$9,000 per borrower. Although all formally-employed households pay into these pension funds in principle, the interest-rate subsidies in these housing loans have gone mainly to the moderate-income households that can afford the mortgage payments necessary to purchase a finished, commercially-built unit. As low-income households cannot afford the finished housing financed by these subsidized mortgages, INFONAVIT has served these families far less than higher-income households.

15. Despite some advances in recent years, the credit finance system remains weak relative to other countries at a similar level o f socio-economic development. Outstanding mortgage loans represented 5.2% o f GDP in 2000, compared to over 10% in Colombia and Chile, and 35% to 40% on average for OECD countries. Below-market rate loans for the middle class via the provident funds for federal and private formal-sector employees (FOVISSSTE and INFONAVIT, respectively) s t i l l account for about 75% of all mortgages. The funding method o f INFONAVIT and FOVISSSTE - 5% of formal-sector payroll - has provided the cash flow for considerable housing production, even during times o f economic stagnation or/and instability. However, the heavy subvention embedded in these government loans has crowded out the private sector, hindered the mobilization o f private savings, reduced liquidity in the private housing market, and provided few housing options for low-income households.

Housing credit and household savings.

16. Mexico’s home-credit finance has been characterized by a narrow range of products and, while expanding, has yet to reach a large portion o f the potential market. The mortgage-finance industry focuses on lending for the purchase of new developer-built units affordable to a small share o f moderate- income people accompanied by a substantial subsidy and to the middle class and above at market rates. These mortgage institutions provide virtually no credit for the lower-cost housing solutions suited to the low/moderate-income majority, including home improvement, expansion, a serviced site, and purchase o f low-cost existing unit. Similarly, savings for housing i s quite low. Although those who save do so mainly for housing, 70% of Mexican families lack any type o f relation with a formal-sector financial institution, including a savings account. As a result of low savings, the family contribution necessary to leverage credit and subsidies i s small or missing.

17. The lack o f agreement on basic legal and administrative principles, operational inefficiency, and the antiquated and insecure information systems o f the great bulk o f Mexico’s 32 state property rights registries has helped make real private property ownership difficult and expensive. Widespread insecurity o f tenure and informal ownership has followed as low/moderate-income households opt out o f this costly, cumbersome system.

Urban real property registries and rights.

18. National urban policy, slum upgrading and institutional strengthening. Until recently, slum upgrading has occurred - if at all - in piecemeal fashion, without planning, neighborhood participation, sequencing o f investments, or integration of physical and social improvements. The fragmentation o f these functions within different areas o f SEDESOL - the government ministry in charge o f urban development - also impeded an integrated approach.

19. Low and moderate income land development. The supply o f urban land in Mexico represents a major problem for low/moderate-income households. According to the National Urban Development Program 2001-2006, an estimated 32,000 hectares o f land are currently available for urban use -

The estimate of total subsidies i s based on the net present value o f the implicit interest rate subsidy for the life of all INFONAVIT loans originated in 2000. The implicit interest rate subsidy was estimated as the difference between the rate offered on the mortgage and the conservative estimate o f 7.1% real interest rate on government funds.

Page 5

sufficient to meet only two years of demand. Myriad, complex and costly building and subdivision regulations have contributed to making low and moderate-income land development an uneconomic venture for the private sector. The bulk o f residential land development in urban areas occurs informally, at costs far higher than that o f formal-sector development.

20. The difficulties of developing ejido land have exacerbated this problem. About two-thirds o f the land on the periphery of medium and large towns consists o f ejidos, while high-end private-sector developers control most of the remainder. T h i s form o f communal landownership dating from the Mexican Revolution has had a complicated legal regimen that contributes to making private freehold ownership, assembly of parcels of significant size, and rational land development difficult and expensive. Since 1992, ejido lands can be privatized, but the process i s cumbersome and centralized under the federal government. Municipalities must then get the explicit authorization of the federal authorities - which i s often slow in coming - to intervene, raising the cost o f subsequent regularization. Many o f Mexico’s cities show discontinuous spatial patterns as formal development leap-frogs over ejido lands in search o f lower-cost parcels far from cities and employment centers, creating much higher costs for infrastructure provision and congestion (extra traffic, air pollution).

21. These problems have resulted in government provision of virtually all the parcels used in social housing projects, massive government purchase of informally-urbanized ejido land in order to subsequently regularize and transfer title o f these lots to their de-facto occupants, and the accumulation of land reserves by government - often, a problematic process in other countries - for these two other purposes (social housing projects and ejido regularization).

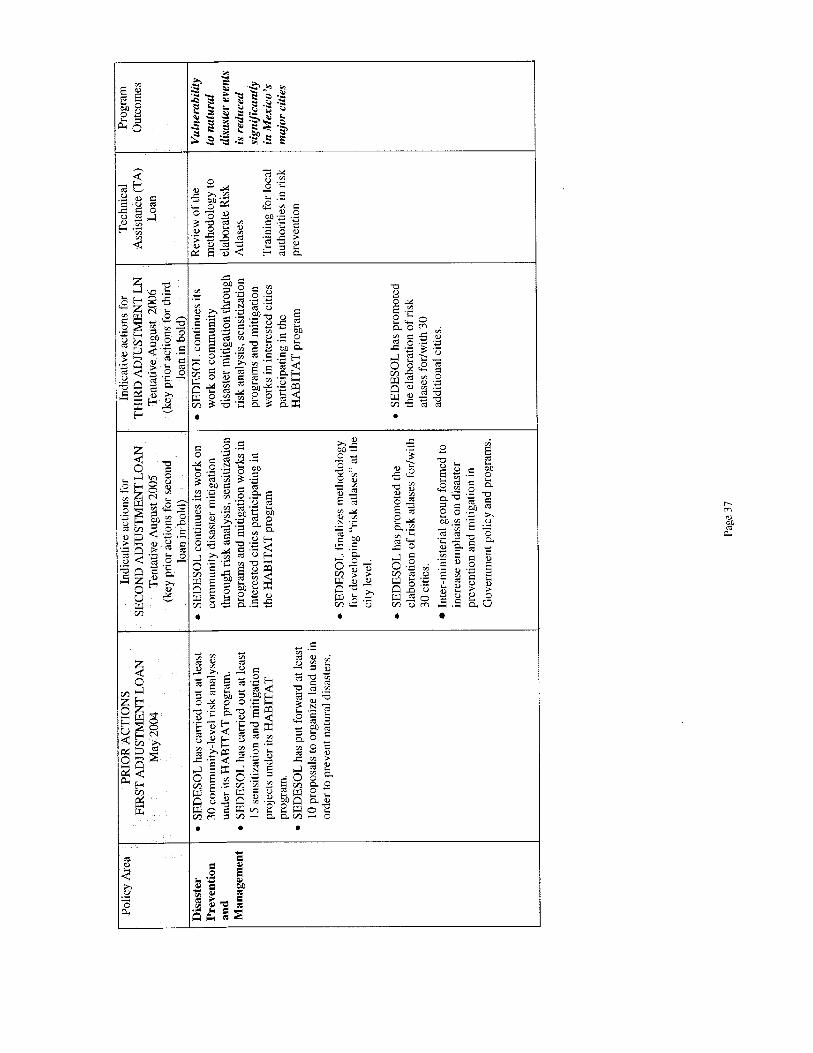

22. Disaster prevention and management. Vulnerable to earthquakes, hurricanes, and other natural disasters, Mexico has, until recently, assisted the victims post-event. In contrast, taking measures to prevent the damage from disasters can avoid immense suffering and cost. In response to the devastation caused by the earthquake of 1985, Mexico began to set aside reserves for emergency reaction and reconstruction after natural disasters. Recently, however, SEDESOL has focused on mitigating the vulnerability o f unplanned poor communities. The f irst step involves assessment based on GIS information. This assessment leads to mapping o f risk hazards and to the development o f mitigation measures and a community emergency plan. SEDESOL intends to take this process a step further by completing risk maps for 60 cities.

111. MEXICO’S HOUSING AND URBAN REFORM AGENDA 2001 - 2006

IMPLICATIONS FOR THE PROGRAM

23.

A.

The Fox administration has responded in each o f these areas:

National Housing Policy and Institutional Framework

24. Strategy and Institutions. The recently formulated National Housing Policy for 2001-2006 state the importance of increasing access o f the poor to shelter. In line with the promises o f President Fox - who gives high priority to housing as a driver o f economic growth and social development - the Government has committed to doubling formal housing production by 2006 (to 750,000 housing solutions per year) through a decentralized and market-based approach. The pillars underlying this Administration’s housing strategy include: (i) targeting lowlmoderate-income households; (ii) a unified system of housing subsidies to be administered by a single agency complemented by credit and savings; (iii) expanding housing finance by putting in place the methods and institutions to develop primary and secondary markets, and by working with financial institutions experienced in serving low/moderate-

Page 6

income groups to develop products for financing low-cost housing solutions (improvement, expansion, purchase of existing housing); and (iv) strengthening property rights.

25. Institutionally, the Fox administration has taken bold steps to achieve these national priorities. B y harmonizing and defining the roles of federal housing agencies. CONAFOV17 - a new institution - now coordinates other federal housing agencies (SHF, FONHAPO, and - to some extent - the off-budget autonomous national institutions, INFONAVIT and FOVISSSTE) and defines policy for the sector. CONAVI - also new - serves as a consultative forum o f public and private stakeholders for CONAFOVI. GoM has created a new housing finance institution - SHF - to take the lead in developing market-rate primary and secondary mortgage markets. FONAEVI - a new institution that works in coordination with CONAFOVI and FONHAPO - receives, accounts for, and disburses housing subsidy funds.

26. Decentralized Execution. CONAFOVI has entered into coordination agreements (CODEVISU) with state governments that establish federal housing funding requirements and amounts, and policy goals. These agreements joined with the strengthening o f state housing institutes w i l l contribute to effectively decentralizing housing programs. FONHAPO wi l l assist municipal governments in assessing their needs, inventorying their resources, and developing a request for selected federal support programs best suited to local conditions. Eventually, this system could evolve into a housing block-grant program that flexibly allows a range o f program options and requires a local match - an approach with wide currency i n large federal countries with widely varying regional conditions (e.g. the U.S.).

27. While many aspects o f decentralization and local capacity building extend beyond the scope of this initiative, the HUSAL program supports government in the following measures: (a) FONHAPO wi l l develop models for the administration and programs o f state and local housing institutes; and b) CONAFOVI, SHF and SEDESOL wi l l enhance systems for data-collection and analysis of housing/housing finance and urban planning, to inform local decision-makers (see paragraph 46 for local capacity building efforts in support o f urban policy).

B. Housing Subsidies

28, New Subsidy Proposal. The GOM has committed to standardize federal housing subsidies across i t s previously-fragmented, uncoordinated programs by: (a) conveying comparable amounts for comparable uses; and (b) placing all on-budget federal housing subsidies under the control o f one operating fund, FONAEVI (a division of FONHAPO). The following basic principles w i l l help ensure the consistency o f this system and lay the basis for expansion to more significant scale:

a) Match objectives and instruments. A first step in the creation of a housing subsidy system consists o f defining and balancing objectives. The implicit objectives o f the housing subsidy structure in Mexico consist o f (i) helping low-income households acquire adequate shelter (e.g. Tu Casa); and (ii) teasing private housing development and lending down-market to serve moderate-income households that mainly require this extra purchasing power to afford a basic unit, and to develop financial and real estate markets (e.g. Prosavi). However, these two objectives require explicit definition and clear balancing in a unified subsidy system.

CONAFOVI has formulated a five-year housing policy/strategy for the country and has: (i) assessed housing requirements for different income groups; (ii) established a decentralized and participatory institutional architecture for the housing sector; (iii) formulated a general strategy for the four critical housing supply sectors - land, regulations/taxation, productiodinfrastructure and finance; (iv) prepared proposals for a unified housing subsidy system, and (v) started a well-orchestrated agenda of committee/commission meetings at the federal and state levels.

Page 7

b) Eficiency. The efficiency o f housing subsidy programs depends most on three factors: (i) type o f subvention; (b) per-unit amount and choice o f housing solution; and (iii) benefit versus cost.

Direct demand subsidies (“DDS”) have proved the most efficient type o f homeownership subvention for moderate and middle-income households in Latin America. Essentially, DDS are portable vouchers that bridge the gap between the amount households can afford (by joining an affordable mortgage, a downpayment, and the subsidy) and a housing solution. T h i s form o f subvention most effectively stimulates competition among supply agents (developers and financial institutions) and furthers development of the financial sector. Securitization o f accompanying market-rate home credit becomes feasible with DDS, whereas it i s generally unviable when subvention takes the form o f below-market interest rate loans. Once subsidy programs reach a significant size and continuity, they also develop important economies o f scale necessary for systemic improvement o f housing conditions as supply agents increase their knowledge o f and ability to use these programs. However, developers, financial institutions, and other formal-sector institutions (e.g. secondary mortgage markets, insurers, property registries etc.) often find serving low-income groups uneconomic if they have other options even if these families have direct demand subsidies.

Hence, countries with successful low-income subsidy programs have also facilitated supply through policy changes and through programs.* These supply bottlenecks - particularly the lack o f land and credit for low-income households - require direct action (e.g. assistance in development of housing microfinance and low-income housing credit, expanding independent mortgage insurance, reducing land development standards and streamlining the process, etc.)

Provision o f the lowest per-unit subvention feasible for the least costly type o f housing solution appropriate to the family constitutes a second important aspect of efficiency. Third, calculating the costs and benefits of the subsidy types that compose a system provides critical information for the creation of an overall strategy, a key measure o f efficiency, and the fiscal justification for expansion o f a subsidy system.

Mexico has partly met these efficiency criteria, but has considerable distance to go. Prosavi has operated on a small scale as a direct demand subsidy program for moderate income households - those earning up to 5 minimum wages (MW). Also on a minute scale relative to Mexico’s size, V i v a m u Casa has provided both a grant and assistance to supply in order to serve low-income groups -those earning up to 3 minimum salaries.

The experience o f these programs since their inception in 1998-99 provides part o f the basis for ramping up to more significant levels o f funding and impact. However, neither o f these programs has received a comprehensive evaluation nor incorporated important features that make similar programs work well in other countries. The available evidence, however, suggests two lines o f reform.

First, neither Prosavi or Tu Casa effectively address the two most critical supply barriers facing most low/moderate-income families in Mexico: (i) foremost in importance, access to an appropriately located serviced ∧ (ii) second, access to small loans to finance low-cost housing solutions (improvement, expansion, purchase o f a serviced site, etc.) In addition to mandating that local governments provide land to the project as the required match for the federal subsidy - the current approach o f Tu Casa - further efforts are need to improve the function of

~

* Here, direct federal govemment development and finance has generally worked poorly, whereas use o f NGOs and municipalities to organize poor households and get access to a parcel has worked better (Costa Rica).

Page 8

land markets. The Mexican Government has taken a first step in addressing this problem under Habitat through support of land reserves for the poor.

Second, the present subsidy level of both Tu Casa (including both federal and local subvention) and Prosavi i s quite high - about US$ 6,000 and US$ 5,000 respectively. Such high per-unit subsidies greatly l imit the reach o f the program. At the funding level o f US$ 300 mill ion per annum, Tu Casa and Prosavi served only about 33,700 households in 2002. In comparison, low- income household formation (a proxy for need) runs at about 300,000 families per annum and moderate-income household formation (a group also frequently unable to access minimally adequate market-rate housing unassisted) at an additional 245,000 per year. As more sustainable modes of housing finance (market-rate credit and household savings) expand, per-unit subsidy amounts should be lowered and favor less costly solutions, such as serviced sites and home improvement, as recommended by Mexico’s official national housing strategy. In addition, i t underlines the importance o f reforming these subsidy programs and quantifying their benefits (relative to their cost) in order to justify increasing the level o f on-budget housing subsidies towards international norms.

In summary, both Prosavi and Tu Casa could operate with a lower level o f subsidy per unit, and could focus more on lower-costs housing solutions for lower-income households than currently.

c) Equity. An equitable housing subsidy system typically has the following characteristics: (i) progressivity or neutrality in targeting o f subsidies to income groups; (ii) delivering comparable subsidy amounts to households in comparable situations; and (iii) regional adjustments for price/cost/income levels and local fiscal capacity.

“Progressivity” means targeting the subsidy system to lower-income families by either delivering more subvention per low-income family or by assigning more total resources to low-income groups. The first alternative - delivering a greater subsidy amount per family to low-income households - has proved difficult and, sometimes, impossible for many reasons. However, at a minimum, an equitable subsidy system assigns more resources to low-income groups, thus meeting the second criterion for progressivity. Taken as a whole, however, Mexico’s current housing subsidy system i s heavily regressive as INFONAVIT - the main source of subsidies - goes largely to moderate and middle-income families that are formally employed.

Mexico has made progress in harmonizing the levels o f subsidies across i t s on-budget programs (Prosavi and Vivah). These programs now deliver roughly comparable levels o f subsidy per family taking into account all sources of subvention. However, Mexico requires development o f regional housing cosdprice indices in order to adjust subsidy levels as well as other parameters to reflect local costlprice variations and fiscal capacity - a task recently begun by SHF and CONAFOVI.

d) Overcoming market and policy failures. In addition to neglecting credit and land bottlenecks, a number o f other market and policy failures hinder the creation o f a national subsidy program. Heavily subsidized lending by local governments as well as FONHAPO undermines development of credit markets for low/moderate-income households. Instead, FONHAPO and local housing institutes could usefully concentrate on the management o f an upfront grant program, rather than a subsidized credit system.

29. GoM i s planning the following reforms to deal with these issues:

4 FONHAPO and States w i l l withdraw from the credit market. Government (SHF) wi l l focus on measures to foster the capacity o f the Cajas de Ahorro y PrCstamo, credit unions, and

Page 9

other financial institutions to extend housing credit to low/moderate-income families for a range of low-cost housing solutions.

In tandem, Government (BANSEFI) w i l l develop and expand housing savings programs with the goal of increasing the household contribution that complements the housing subsidy provided by various programs (Tu Casa, Prosavi, INFONAVIT).

INFONAVIT wil l focus i t s subsidies increasingly on low-income households. GoM wi l l eliminate joining subsidy amounts from different programs - such as INFONAVIT and Tu Casa - to reach totals above those mandated for these programs separately (“double dipping”), or adjust the amounts for households receiving different sources o f subvention to correct for double dipping.

Government wil l conduct a comprehensive and coordinated evaluation o f all national subsidy programs, starting with Prosavi and Tu Casa, but also including those of INFONAVIT and FOVISSSTE. This evaluation wi l l include a quantitative analysis of the costs and benefits of these programs, and the fiscal, social, and economic implications of the expansion of Prosavi and Tu Casa once reformed.

Both Prosavi and Tu Casa wi l l be changed to deliver a smaller per-unit subsidy for lower- cost housing solutions for lower-income households, as follows:

For Prosavi: (i) the federal government subsidy per unit w i l l decrease from i t s current level of around $5,000 per unit; (ii) local or state government w i l l be asked to contribute a modest amount in cash or in-kind (e.g. land) to these projects; and (iii) the total amount o f subsidy w i l l be progressive - that is, lower-income households w i l l receive more than higher-income families.

For Tu Casa: (i) the eligible solution w i l l change from the purchase o f a complete finished unit to a serviced lot joined with a small loan to assist the construction o f a basic unit; (ii) the subsidy amount o f both the federal and state/local governments (currently, about U S $3,000 each) wi l l decrease; (iii) local government wi l l facilitate land assembly for developers, NGOs, employers, and others to develop these projects and sell them to families.

A series o f studies w i l l further define the parameters o f the new Prosavi and Tu Casa, the project cycle of these new interventions, and the transition from the current programs to the new ones.

Government wi l l conduct quantitative studies o f the present value of subsidies embedded in INFONAVIT financing.

Capacity building for local governments aimed at dealing with supply constraints in urban land and property rights wi l l help deal with these structural issues unaddressed by housing subsidies.

Housing Credit and Household Savings

The Government views reform of the housing finance system as critical to meeting i t s goals in both the housing and urban sectors. GoM’s program builds on important structural reforms initiated under FOVI and continuing with SHF - the successor o f FOVI - and includes: (i) leveraging market-oriented private resources, mainly through guarantees o f private-sector debt on capital markets and elsewhere, rather than government borrowing directly to provide liquidity; and (ii) improving the efficiency and increasing the capacity o f the existing home lending institutions (banks, SOFOLES, SHF, and the

Page 10

provident fundshousing lenders INFONAVIT and FOVISSSTE). measures described in the rest of this section.

Future actions wi l l include the

3 1, Foreclosure and Transparency. All but three states have already modernized their legislation through c iv i l code proceedings on mortgage liens and foreclosure. In some instances, however, foreclosure remains ineffective due to judicial and political resistance. Congress has recently approved a financial transparency law to protect and better inform mortgage borrowers. The next step i s to build confidence o f lenders and investors in the enforceability o f mortgage contracts. The GoM i s moving forward on further judiciary reforms at the national level, including recent passage o f a new guarantee law that allows expedited foreclosure through a trust collateral instrument.

32. Development of secondary mortgage markets, SHF, and SOFOLES. The growth and diversification o f Mexican institutional investors provide ample opportunity for secondary market development.' Since i t s creation in 2001, SHF has successfully advanced the development o f primary and secondary Mexican mortgage markets. I t s contributions include: (i) steady access to long-term priced funding; (ii) revised actuarially-priced first-loss credit insurance products; (iii) improved risk management and pricing (refinancing and guarantees); (iv) consistent rating policy applied to SOFOLES; (v) stimulating access to private bond markets and funding diversification; and (vi) an acceleration in Prosavi execution. Additional key actions to be tackled in the near future with related milestones under the HUSAL program include the following: (i) expand SHF mortgage-related products (refinancing, guarantees) both in UDIs and pesos; (ii) design and expand the use o f products for the credit finance o f low-cost housing solutions such as home improvement, serviced sites, and purchase of existing housing; and (iii) develop rules (property appraisal and disclosure of lending costs) as required by the new financial transparency law.

33. Commercial banks, which had been the main market-rate home lenders, largely withdrew from the mortgage market after large losses from the 1994-95 peso crisis. Since then, 16 SOFOLES have become the main market-rate mortgage lenders and main clients o f SHF. SOFOLES currently get 90% of their funding from SHF. The lead SOFOLES, however, have begun to issue debt on domestic and international markets as planned under the SHF's broader mandate. The H U S K program wi l l support SHF's development o f and private-sector participation in a mortgage-risk database essential for secondary markets and mortgage insurance.

34. Subsidies and the Fideicomiso Fondo Nacional de Habitmiones Populares (FONHAPO). FONHAPO has acted as Government's lead institution in funding low-income housing. Over the last five years, the organization has recovered from i t s quasi-bankruptcy resulting from the subvention and high arrears o f on-lending to state housing institutes by recouping debt. Continued below-market rate lending to state institutes would not only jeopardize FONHAPO's hard-won financial solvency, but also undermine the Government's strategy to promote market-rate lending." Hence, this second-tier lending - which i s already at a low level'' - w i l l phase out during the program and be replaced by more financially sustainable approaches to supporting low income housing. Specifically, the funding o f social housing by FONHAPO from newly-budgeted monies w i l l occur in the form o f grants and not loans.

35. Rather than channel home credit - a function o f SHF - FONHAPO wi l l unify the federal govemment's housing subsidy programs for low-income households. In this regard, FONHAPO wi l l work with SHF to design and monitor Prosavi grants.

More than US$90 billion between mutual funds, provident funds, pension funds, and insurance companies. lo FONHAPO lends at minimum wage (MW) plus 4% to 6% to state housing institutes that provide state guarantees. '' Funded only by payments on FONHAPO's loan portfolio, which are small and shrinking fast in real value. In addition, most of the reflow from FONHAPO's loan portfolio goes to support this organization's administrative cost, leaving little for these below-market rate loans.

Page 11

36. In lieu o f FONAHPO’s second-tier lending to states, SHF wil l guarantee micro and mortgage housing credits to l o w and moderate-income loans originated by private financial institutions for both purchase and renovation of existing homes. Sustainable low-income housing finance requires strengthening o f the regulations and standards for this business, access to a range o f new SHF products, and institutional capacity building.

37. Redefining the role of the Znstituto del Fondo Nacional de la Vivienda para 10s Trabajadores. (INFONAVIT) has initiated an impressive array o f reforms under the current government. In 2003, INFONAVIT made a record of 291,000 loans. This high production has relied on: i) large inflows o f compulsory wage contributions of formal sector workers - many o f whom wi l l not receive a loan; ii) low servicing costs due to direct payroll deductions; and iii) less stringent capital and provisioning rules than for primary credit institutions. Improved management practices on the credit side have come from more transparent credit allocation, a better system for originating and managing loans; reformed internal organization, an active and out-sourced debt recovery program, improved management o f credit risk12 and operation risks,13 new minimum down-payment requirements, a simplified scoring system, extraordinary loan-loss provisions (US$ 2 billion in 2002) made for non-performing loans, and piloting the use of INFONAVIT savings to leverage private credits for higher-income members (article 43 bis). On the savings side, INFONAVIT expects to pay an annual return o f the minimum wage (“MW’) + 2.5% on i t s savings accounts, exceeding i t s minimum requirement and paying closer to private pension fund benchmarks (net o f management fees). After many years of poor performance, this trend reflects the increasing importance o f INFONAVIT’s role as a mandatory saving institution, in addition to i ts traditional home lender role. FOVISSTE - a providentiary institution that operates similarly to INFONAVIT but for federal public-sector employees - has also made important operational impr0~ements. l~

38. Despite this progress in improving i t s operation, INFONAVIT’s conflicting roles continue tc undermine the development of housing credit markets. INFONAVIT’s roles include functioning as: a) an efficient housing lender that provides loans to an ever higher proportion o f contributing members,15 achieving a better social match between the “taxed” contributors and borrowers, and leveraging more market-oriented credits with private lenders; b) a social housing agency contributing to the provision and targeting of subsidies; and c) a profitable pension fund increasing pension returns for retiring members and improving liquidity by permitting early withdrawals for housing investment purposes. These three roles create multiple contradictions. Most fundamental, the extension o f subsidized housing loans reduces the returns available to pay contributors’ pensions.

39. Over the medium term, the GoM aims to foster a transition to private market-rate housing finance and rationalize INFONAVIT’s conflicting roles. However, the Mexican housing finance system’s current dependency on INFONAVIT (which provides two-thirds o f all mortgages) and the institution’s complex governance structure complicate the transition. Hence, rationalization o f INFONAVIT’s role requires time and a clear plan in order to build broad support among stakeholders, avoid potentially devastating disruption of mortgage lending, and facilitate increased private lending. The challenges and path to reform of FOVISSSTE - an organization that operates similarly to INFONAVIT but for public-sector

Mostly when members become unemployed, or change jobs, notably to the informal sector where there i s no automatic payroll deduction. l3 Mostly due to improper payroll deduction by the employer. I4 FOVISSSTE has contracted SOFOLES as professional originators of i t s loans. Better management and credit recovery have resulted in accumulated liquidity and increased lending in 2002-2003. Non-performing loans are relatively low, at 3%. The proportion of members (public-sector employees) expected to receive a subsidized housing credit i s expected to rise from 26% to 40% by 2006. l5 With a current low “cover” ratio st i l l less than 20%.

Page 12

employees but at much smaller scale - parallel those o f the much larger institution and - hence - wi l l be subsumed under those of INFONAVIT in the program and the remainder of this document.

40. Savings products and BANSEFZ. In Mexico, over 60% of households that save in informal and formal-sector institutions dedicate these accumulated funds to housing, mainly to improvement o f their existing home. Hence, housing savings product are crucial for low-income households, particularly non- wage earners without bank accounts, in order to help them build equity, encourage financial discipline, achieve a “bankable” credit score, make use of formal financial institutions (go from “unbanked” to “banked”), and facilitate eligibility for housing subsidies. Larger savings can also reduce the cost of the subsidy program, which tries to compensate for miniscule downpayments (i.e. savings) for purchasing a house by increasing the level o f subvention. These higher downpayments also lower the credit risk of home lending by reducing loan-to-value ratios.

41. BANSEFI was created in April 2001 in order to promote household savings, help popular finance institutions adjust and prosper under the new Law for Popular Savings and Credit that phases in requirements between 2001 and 2004, and coordinate government support to financial institutions that focus on serving lowlmoderate-income households (“popular financial institutions”). In the last three years, the number of savers in BANSEFI’s 560 branches has grown from 800,000 to 1.7 million, and i s currently increasing by about 10,000 clients per month. BANSEFI has created a technical platform to connect i t s branches with those of several other popular finance institutions - the “people’s network.” BANSEFI has begun to partner separately with INFONAVR and FONHAPO to help households applying to these institutions for support by opening savings accounts that help them meet eligibility criteria. SHF and BANSEFI are poised to launch a similar savings initiative shortly. The HUSAL program has milestones for developing these savings links to credit and subsidies.

D. Urban Real Property Registries and Rights

42. About 40% of those who say they own their property, in fact, lack full legal title. This problem arises not only from the complications o f the ejido system (see paragraph 20), but also from the cumbersome and costly procedures of the 32 state real property registries and an ineffective legal framework. With few exceptions, these state real property registries depend on manual data entry in paper books with entries arranged chronologically (rather than the modern standard o f electronic files for each property), involve 30 to 100 separate steps to register relatively simple transactions (a mortgage lien, for example), remain unlinked to the municipal cadastre (the other main source o f land information), and lack transparency.

43. Well aware of the importance of real (and housing) property rights for many markets and for social stability (including the development of housing finance, urban real estate taxation, extension and charging o f public utilities tariffs, safeguarding o f family relations, and general well-being o f housing dwellers), the GoM has initiated a project to strengthen the real property registries in two states through CONAFOVI. (i) analyze and reform the institutional and legal framework for property registrylrights; (ii) re-engineer the processes and work flow of the property registry in order to cut time, improve efficiency and accuracy, and reduce costs; (iii) shift from manual entry of transactions in chronological order to electronic folios of properties; (iv) digitize historical data as necessary in order to incorporate it into the electronic system; (v) permit remote consultation of the property registry; and (vi) link the state property registry to the municipal cadastre in order to unify land information. The HUSAL sets milestones for extending this project from the original two states to other states and for agreement on a legal framework.

CONAFOVI’s assistance matches each state’s counterpart resources in order to:

Page 13

E. National Urban Policy, Slum Upgrading and Institutional Strengthening

45. Strategy and Institutions. The recently formulated National Urban Development Plan for 2001- 2006 focuses on achieving sustainable and spatially-balanced urban development. The pillars o f the Government’s urban strategy include: (i) upgrading low-income communities through joining physical and social investments guided by planning and community participation; (ii) increasing land availability for the poor; and (iii) moving from mitigating the costs o f disasters to prevention. To support the achievement o f these goals, SEDESOL has joined control over the activities necessary for integrated slum upgrading - including both physical and social investments - in one division. In recognition of the growing importance of urban poverty, the Government has expanded Oportunidades - i t s major program of social support to the poor - from a rural focus to include urban areas.

46. The success of the GoM urban policy also largely depends on implementation capacity at the local level, particularly in land development and planning, community development, and property rights where local govemments have the main power and responsibility. The lack o f local planning agencies and financial capacity represents an important bottleneck to the implementation o f the GoM program. Over the last two decades, Mexican municipalities have gained increased political, administrative and financial autonomy, but many still lack the technical capacity and funds to perform their new roles. For example, while the reform o f constitutional article 115 decentralized responsibility for construction and operation of infrastructure and urban services to states and municipalities, federal transfers through Ramo 33 s t i l l fund the bulk o f local infrastructure investment. Proposals for fiscal reform and the government’s on-going decentralization program promise to further strengthen local and state governments. As previously mentioned, while many aspects o f decentralization extend beyond the scope of this program, the HUSAL wi l l provide support SEDESOL to launch a comprehensive program to build capacity of municipal and state governments on land management, local economic development, and community-based planning.

47. Slum Upgrading and the Habitat Program. Unable to access formal housing or land, about 100,000 poor families each year settle in marginal areas with overwhelming infrastructure deficits and without urban planning. The layout o f many Mexican barrios appears orderly in comparison to others in the region (e.g. those o f Venezuela or Brazil). However, location in hazardous or sensitive areas, scarcity of public facilities and goods, distance from infrastructure and services and the absence o f mechanisms for community input frequently damage these neighborhoods and raise the cost o f regularizing them to well above that of new formal-sector development. The cost to organize and provide public goods ex post exceeds the capacity o f households as well as communities and usually requires public support.

Decentralized Execution.

48. The GoM (SEDESOL) has developed an integrated program called Habitat to address precarious poor neighborhoods. Habitat provides support for neighborhood upgrading, access to land, and prevention o f natural disasters and includes initiatives to support community facilities, day-care centers for working mothers, and local development agencies that bring together community, private sector, and local government. Habitat channels federal funds (under Ramo 20) as matching grants to municipalities for programs that benefit families earning up to 3 MW.

49. The urban upgrading subprogram o f Habitat includes: (i) preparatory studies such as municipal urban-poverty diagnostics and action plans, comprehensive barrio upgrading plans, and detailed engineering for infrastructure projects; as well as (ii) investments in urbanization including water, sewerage, storm drainage, paved access roads, electricity and street lighting, rehabilitation or construction of community facilities, and improved solid waste management. The program has started in 60 medium and large cities, and invested around US$ 90 mill ion in 2003. HUSAL I includes as prior actions the integration of upgrading activities under Habitat and the programs approval and funding by Congress.

50. HABITAT includes several design innovations to improve targeting and program impact:

Page 14

Capacity. Habitat wi l l create local capacity among municipal authorities, NGOs and CBOs and related agencies. A capacity building program run by SEDESOL in proposed collaboration with the World Bank Institute (WBI) wi l l help strengthen local actors to implement the upgrading program. Poverty Targeting. SEDESOL has developed detailed geo-referenced poverty data down to the block level for eligible municipalities that allows for accurately allocating Ramo 20 funds. Neighborhoods must include at least 50% poor households, or 30% in special cases as specified in Habitat’s regulations, with federal government support matched by local government and beneficiaries’ contributions. Eligibility criteria for participating cities include the level o f poverty, city rate of growth, potential to generate wealth (per capita GDP), level o f inequality, and environmental sustainability (availability o f water). Based on the prioritization o f such criteria, appropriate blocks and neighborhoods are selected. Multiyear program of improvement. The program supports the development and execution o f multi-year plans for neighborhood improvement, helping to overcome some o f the transaction costs and capacity limitations o f progressive investment.

Although an important advance, the upgrading component of Habitat requires further action for the program to-fulf i l l i t s potential. The program design stipulates important procedures essential to i ts performance such as community participation, neighborhood investment plans, and an appropriate level and sequencing o f investment in each community. However, the rapid expansion o f the Program in i t s f irst year (2003) and the urgency o f meeting initial investment goals (the Program disbursed the budgeted amount of approximately US$ 90 mill ion in 2003) have sometimes taken precedence over these other aspects. SEDESOL i s fully committed to meeting these other milestones by the HUSAL Program’s second and third years o f operation.

F. Low and Moderate Income Land Development

52. In formal housing development, public goods such as environmental quality, green and community spaces, access, and storm drainage come at the beginning o f the development process. Middle-income families can afford to pay for these services upfront in the form o f the price of the new house and local taxes. Most low/moderate-income households, however, lack the financial ability to pay these sums upfront, and must stage them over time to make them affordable, thus reversing the process, which often starts with informal settlement.

53. Thus, most o f Mexico’s low/moderate-income residential land development occurs illegally, often on ejido lands. The dominant method of land supply for the poor consists o f an agile system o f illegal subdivisions, followed by a costly and time-intensive process o f expropriation and regularization by the Government through CORETT. When unassisted by the formal-sector - as i s usually the case -the incremental settlement and building process has one crucial virtue: it puts low-income households on the first rung o f the ladder o f homeownership. In the process, however, i t generates enormous public and private costs. From the families perspective, securing their property and building a house over many years involves a huge investment in time and labor, during which the family must live in inadequate and unhealthy environments. From a public-sector perspective, informal settlement leads to a broken settlement pattern that often costs two to three times the amount (generally o f government funds) to fix than planned formal-sector development (generally, private funds) would have initially.16 Hence, replacing informal settlement with low-cost formal sector land development holds crucial importance. Although some preliminary analysis has occurred in Mexico, the costs o f informal development and their

~~

l6 A Colombian study has calculated the costs of provision o f basic infrastructure to informal development at three times the cost of that to formal-sector development. A number of studies of land development in Mexico has reached a similar conclusion, but without quantification.

Page 15

impact on diverse participants in the process - households, landowners, local government, federal government - have yet to be quantified and publicized. In effect, the costs of the dominant approach to low/moderate-income land development in Mexico - informal urban settlement o f ejido land, regularization, and slum upgrading of many o f the resulting areas - remain undocumented, as do the costs and benefits o f other options.

54. In turn, formal-sector low/moderate-income land development represents a small fraction o f the total. Most formal-sector low/moderate-income land development occurs as part o f housing projects financed by federal agencies (INFONAVIT, FOVISSSTE, SHF, and FONHAPO) and local and state government housing institutes. Local and state government usually provides the land at discounted rates to the developers o f these federal and locally-assisted affordable housing projects. Most states and local governments, however, do not own substantial amounts o f developable land. Hence, in order to attract and make possible these low/moderate-income housing projects, most state and local governments purchase land to constitute “land reserves”. Here, too, however, no study has quantified the costs and benefits of land reserves, or o f the feasibility o f and changes necessary to improve profitability and spur formal private-sector involvement. Analysis o f successful experiences in Mexican states and other Latin American countries could shed light on options for low/moderate-income land development from deregulation to land readjustment.

55. In summary, the next steps in land are to: (a) quantify the costs and benefits o f informal vs. formal-sector development; and (b) analyze the experience o f selected Mexican states and other Latin- American countries in low/moderate-income settlement in order to develop viable options for reform. Based upon this analysis, GoM intends to put in place a pilot program. The HUSAL program supports these actions.

56. subsequent reform program:

A number o f factors require consideration in this analysis of costs, benefits, and options, and a

a) Rural-to- Urban Land ConversiodEjido System. Without an agile process for talung ejido land to the market, ejidatarios illegally parcel their land without attention to urban plans and regulations yielding unserviced plots and leapfrog development. The PROCEDE certificate was clearly an important step forward, but i t appears that the subsequent processes for conversion to full legal title or the development o f ejido real estate companies remain cumbersome and ~omplicated.’~ Thus, the next steps for reform are unclear and await definition.

b) Regulations and standards. SEDESOL has carried out studies to identify the incongruities and omissions in urban and standards and problems in compliance. An analysis of the costs and benefits o f informal vs. formal-sector development, and o f viable options for low/moderate-income development represent the missing complements to develop a program.

c) Govemment role in low/moderate-income land supply. In the face o f the pressing need for increased land supply, G o M continues to encourage and fund state and local governments to amass land reserves. In certain instances, this solution provides a short- term response but, as experiences in other countries have shown, has some important drawbacks: (i) increases in land prices; (ii) slowness o f the transactions under the reserve process; iii) inefficiency o f government in identifying the most desirable land offerings; iv) tendency o f the agencies handling land reserves to become large and inefficient; and v) a large percentage of the land reserves used for other than social purposes. SEDESOL

” PROCEDE i s a program to register and certify ejido property.

Page 16