Embed Size (px)

Citation preview

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. 3332a-EGT

EGYPT

STAFF APPRAISAL REPORT

HADISOLB REHABILITATION PROJECT

May 1, 1981

Industrial Projects Department

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS(Used in the Appraisal Report)

US$1 = Egyptian Pound (LE) 0.69LE 1 = US$1.45

WEIGHTS AND MEASURES

1 metric ton (t) = I,OOO kilograms (kg) = 2,204 pounds (lb)1 meter (m) = 39.37 inches

1 kilometer (km) = 0.621 miles1 megawatt-hour (MwH) = 1,000 kilowatt-hours (kwh)

ABBREVIATIONS AND ACRONYMS USED

BOF - Basic Oxygen Furnace

CIF - FOB costs, Insurance and FreightCPE - Centrally Planned EconomiesCU - Coordinating Unit

EAF - Electric Arc FurnaceEC - European Community

EGITALEC - Egyptian-Italian Engineering and Construction CompanyFOB - Free on BoardERG - Federal Republic of GermanyGOFI - General Organization for IndustrializationHADISOLB - Egyptian Iron and Steel Company; from Arabic "Hadid"

(Iron) and "Solb" (Steel)ICB - International Competitive BiddingIMC - Executive Organization for the Industrial and Mining

Complexes (former ISC)KfW - Kreditanstalt fuer WiederaufbauLDC - Less Developed Country

OSC - Operating Steel Company (providing technical assistanceservices to HADISOLB)

PIU - Project Implementation UTnittpd - tons per day

tpy - tons per yearUEC - US Steel Engineers and Consultants

FISCAL YEAPR

Government and IIADISOLB: January 1 - December 31 until December 31, 1979January 1 - June 30 January 1 - June 30, 1980July 1 - June 30 after July 1, 1980

EGYPT FOR OFFICIAL USE ONLY

STAFF APPRAISAL REPORT

HADISOLB REHABILITATION PROJECT

TABLE OF CONTENTS

Page No.

I. StION ...................... ........................... U1

A. Theg Band ...... .......................................... r1B. Bank Grouep Involvement in the Egyptian Steel Industry 1. a

II. THE INDUSTRIAkL SECTOR AND THE STEEL INDUSTRY.......... 2

A. The Industrial Sector2 Departmt.B. Developmetnt of the Steel Industry in Egypt........ 4C. Structure and Organization of the Egyptian Steel

Industry.,......................... 4D. Issues arid Problems of the Steel Industry.......... 6

III. MARKET AND PRICE TRENDS FOR STEEL PRODUCTS.......... . 8

A. The Inter-national Steel Industry and Market........ 8

1. Historical World Steel Consumption and ProductionTrends......................... 8

2. Futurt e World Steel Demand and Supply Trends. .onl 103. Intescnational Price Trends for Steel Products .Ban 12

B. Egyptian Steel Demand and Production Trends ........ 13C. Comparison of Egyptian and International Prices for

Steel Products....................... 16

IV. THE COMPANY f........................... 18

A. Backgrounid and Ownership.................. 18B. Production Facilities and Performance............ 18C. Major Problem Areas .................... 19D. Financial. Performance ................... 22E. HADISOLB"s Stage I Rehabilitation Program ......... 23

V. THE PROJECT ~.......................... 26

A. Project Concept and Description .............. 26

1. Stage I Rehabilitation Program............. 262. The Bank Project.................... 27

This report was prepared by Messrs. D.T. Carpio, W. O'Neil, andW. Bertelsmefer of the Industrial Projects Department.

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

- ii -

TABLE OF CONTENTS (Cont'd)

Page No.

B. Production Program, Raw Materials and Utilities .......... . 28

1. Production Program ................................... 282. Raw Materials ...................................... .. . 293. Utilities ...... ..................... ......... 29

C. Ecological and Occupational Health Considerations ... ...... 30D. Project Implementation, Management and Training .......... 31

1. Project Engineering Assistance for the EquipmentPackage ............................... ................. 0...... 31

2. Technical Assistance from an Operating Steel Companyfor Improvements in Operations and Management ......... 32

3. Training .................... ....... .00.......................... 33

E. Organizational Improvements and Associated Risks ......... 34

VI. PROJECT COST AND FINANCING PLAN .............................. 35

A. Project Cost Estimate ...... .............................. 35B. Financing Plan ........ ................................... 36C. Procurement ..... 37D. Allocation and Disbursement of Bank Loan .............. ... 38

VII. FINANCIAL ANALYSIS ............................. .. .. .. ....... . 39

A. Production and Sales Forecasts ........ ................... 39B. Production Costs ...... ............... .................... 40C. Financial Projections ................ ..... i .............. 43D. Financial Rate of Return ............... .. ................ 44E. Major Risks .. 44F. Auditing and Reporting ................ .. ................. 45

VIII. ECONOMIC ANALYSIS ............................................ 45

A. Economic Costs and Benefits ..... ......................... 45B. Economics of HADISOLB's Operations . . . 46C. Economic Costs and Benefits of Stage I ................ ... 46D. Economic Rate of Return and Sensitivity Analysis ......... 47E. Other Benefits ........................................... 49

IX. AGREEMENTS .................................................. 49

- iii -

TABLE OF CONTENTS (Cont'd)

ANNEXES

1 Miscellaneous Terminology - HADISOLB Rehabilitation Project

3-1 World Stee:L Consumption Trends3-2 World Stee:L Capacity, Production, and Utili-

zation Rate Trends3-3 Percentage Share of Different

Technologies in the Steel Production ofSe:lected Countries

3-4 Projected .1985 Steel Prices3-5 Egypt - Historical Production, Imports and

Consumption of Steel Products3-6 Comparison of International and Egyptian Base

Prices for Steel Products

4 HADISOLB Steel Production Facilities

5-1 Flow Chart - Expected Production Levels After Completion of Stage I5-2 List of Project Facilities5-3 HADISOLB-s Production Plan (FY 1988 and later)5-4 Functional Organizational Chart for PIU and CU5-5 Project Imnplementation, Division of Functions

and Responsibilities5-6 Implementation Schedule

6-1 Capital Cost Estimate6-2 Disbursement Schedule for Bank Loan

7-1 Financial Projections (Without Rehabilitation)7-2 Financial Projections (With Rehabilitation)7-3 Assumptions Used in Financial Projections7-4 Production Cost Per Ton of Raw Steel Before

Rehabilitation7-5 Production Cost Per Ton of Raw Steel After

Rehabilitation (in constant prices)7-6 Production Cost Per Ton of Raw Steel After

Rehabilitation (including real term cost increases)7-7 Production Cost Per Ton of Raw Steel Without Rehabilitation (FY88)

(in constant prices)7-8 Production Cost Per Ton of Raw Steel Without Rehabilitation (FY88)

(including real term price increases)7-9 Financial Rate of Return: Cost and Benefit Streams8-1 HADISOLB 1.979 Operations in Financial and Economic Terms-8-2 Economic Value of HADISOLB's 1979 Sales8-3 Economic Rate of Return: Cost and Benefit Streams

- iv -

TABLE OF CONTENTS (Cont'd)

MAP

IBRD EGYPT: Project Location (IBRD Map No. 15272)

DOCUMENTS CONTAINED IN THE PROJECT FILE

1. Atkins Study (4 volumes) 19772. UEC - Operations Improvement Study March 19793. UEC - Market and Facility Study November 19794. UEC - Overall Management Study October 19785. UEC - Corporate Study and Organization Study November 19786. UEC - Development of Iron Ore Deposits7. Studies completed by EGITALEC December 1980

a. Review and update of capital costs.b. Estimation of capacities.c. Modification of one continuous

billet casting machined. Modification of the lime shaft kilns.

8. List of Bid Packages, Preliminary January 19819. Status of Operation Improvements, HADISOLB December 198010. The Rehabilitation of the Egyptian Iron and

Steel Company's Helwan Plant prepared byDr. Samir Taher April 1980

11. Study on Actual Energy Consumption/Ton CrudeSteel and Applicable Recommendations forEnergy Conservation at HADISOLB prepared byEng. Fathalla Kamal April 1980

12. Combined Income Statements of Public SectorSteel Companies January 1981

13. Combined Balance Sheets of Public Sector SteelCompanies January 1981

14. Proportion of Flat and Non-Flat Finished SteelProducts in Production - 1978 (MarketEconomies) January 1981

15. HADISOLB Organization Chart December 198016. International Steel Situation, and Governmental

Intervention Mechanisms in the 1970's February 198117. List of Operations Improvement Schemes to be

implemented as part of the Bank Project February 198118. Worksheets for Calculation of Financial Projections

and Rates of Return March 1981

I. INTRODUCTION

A. Background

1.01 The Gcvernment of the Arab Republic of Egypt and the Egyptian Ironand Steel Companty (HADISOLB), a public sector enterprise, have requested Bankfinancing of US$;64 million equivalent to assist in implementing HADISOLB-s urgentlynecded `eg2 I rehabi' tation and debottlenecking program (Stage I) at its Helwanplant (IBRD Map No. 15272). The proposed Bank project (the Project) would be amajor component of Stage I. The second component will be implemented with financialassistance from Kreditanstalt fuer Wiederaufbau (KfW) of the Federal Republic ofGermany (FRG) arLd a third component with equipment supplied by the USSR. Stage Iis designed to take advantage of a substantial sunk investment which is onlyproducing at about 50% of design capacity at present. It will rehabilitate theold facilities and introduce better operating practices thereby increasing HADISOLB'sefficiency, particularly in terms of energy conservation, and its achievableoutput to about 75% of capacity by 1987. A subsequent Stage II program, which isexpected to be fully defined by early 1983 within the context of the proposedProject, would raise the achievable output to the full design capacity. In 1980,Egypt imported about one million tons of finished steel products at a cost ofabout US$385 million. The expected increase in HADISOLB's output as a result ofStage I will help reduce the import needs of the country as well as make theCompany profital:Je thereby eliminating the Government subsidies to one of itslargest public sector manufacturing enterprise.

1.02 The Project will involve financing of equipment, civil works and technicalassistance and provide the first significant step towards strengthening the organi-zation and operations of HADISOLB which are presently weak. The Project's successwill critically depend on meaningful progress in this area. A key aspect of theProject is the granting of sufficient autonomy to the Company regarding pricing,investments, procurement, personnel policies and remuneration levels adequate toattract and retain qualified employees as well as motivate them to perform well.

1.03 The Project is expected to cost about US$106 million equivalent includingabout US$76 million in foreign exchange. It will be financed with about 39% equity(US$42 million) from the Government and about 61% from the proposed Bank loan(US$64 million),,

1.04 Following preparatory missions in July 1979, October 1979 and April 1980,the Project was appraised in September 1980 and reviewed in December 1980 bya mission consisting of Messrs. D. Carpio (Chief), W. O'Neil and W. Bertelsmeierof the Industrial Projects Department and Mr. F. Kaps of the Country ProgramsDepartment I, EMIENA Region.

B. Bank Group Involvement in the Egyptian Steel Industry

1.05 Bank Group involvement in the Egyptian steel industry started with ametallurgical sector study undertaken as one of six industrial sub-sector reviewsfinanced under the Bank Group's Agricultural and Industrial Imports Project ofDecember 1974 (cr. No. 524-EGT and Ln. No. 1062-EGT). The study was carried outby Atkins Planning (UK) during 1976-77 and identified, among others, a highpriority rehabilitation/debottlenecking requirement for HADISOLB. On the basis

1J Annex I contains a glossary of technical terms used in this report.

- 2 -

of this study and subsequent discussions among the Government, HADISOLB, theExecutive Organization for Industrial and Mining Complexes (IMC) 1/ and ourselves,the Bank approved a US$2.5 million engineering loan in July 1977 (Iron Ore Benefi-cation and Engineering Project - Loan No. S5-EGT) to finance the foreign costs forthree consultancy tasks; namely: (i) a techno-economic evaluation of beneficiatingthe local iron ore used by HADISOLB which is very difficult to utilize due to itspoor quality; (ii) design and engineering, including the preparation of tenderdocuments, for an iron ore beneficiation project should the techno-economicevaluation identify an economically viable process; and (iii) a diagnostic studyof the technical, operating, managerial and organizational as well as marketingproblems of HADISOLB with recommendations for practical approaches towards solvingthese problems. The first and third tasks were undertaken by the US Steel Engineersand Consultants (UEC) and completed at the end of 1979. The recommendationscontained in UEC's diagnostic study formed the basis for HADISOLB-s Stage IRehabilitation Program and the proposed Bank Project. Likewise, on the basis ofUEC's iron ore beneficiation study, HADISOLB intends to build a semi-industrialpilot plant for washing the ore in order to develop the necessary technical andoperating data for a rigorous techno-economic evaluation.

1.06 HADISOLB, the three other small semi-integrated public sector steelcompanies, (para 2.06), and the El Nasr Coke Company were also beneficiaries underthe Bank's Second Industrial Import Loan of July 1977 (Ln. No. 1456-EGT) receivingfinancing for the import of equipment (US$10 million) and raw materials (US$18million). Finally, the Bank and IFC are considering participation in a major(US$800 million) joint venture integrated steel project (El Dikheila) between theEgyptian Government and a consortium of Japanese steel and trading companies.

II. THE INDUSTRIAL SECTOR AND THE STEEL INDUSTRY

A. The Industrial Sector

2.01 Industry 2/ has become a significant sector of the Egyptian economy withits share in GDP rising from 8% in 1946 to 13.5% in 1979. In that year industryemployed about 1.3 million persons, or nearly 12.4% of the civilian labor forcewhile industrial exports, valued at about LE 500 million (12.7% of the gross valueof industrial output) provided about 18% of commodity exports. The industrialstructure is weighted heavily in favor of industries producing consumer goodswhich account for about 58% of industrial gross value added; intermediate products(building materials, fertilizers, chemicals, and metals) account for about 34%;and capital goods, for only 8%.

2.02 As a result of the nationalizations of the early 1960s, the public sector,comprising some 200 enterprises, accounts for almost all large and medium scaleindustrial enterprises. It generates some two-thirds of the value added inindustry and mining and provides slightly more than half of total industrialemployment, mainly in four subsectors: textiles, food products, metal and engi-neering, and chemicals. Egypt-s basic industries are all in the public sector and

1/ IMC, a public sector agency within the Ministry of Industry, was responsiblefor supervising the installation of HADISOLB's newer production facilities,including the iron ore mining facilities at Bahariya (para 4.03).

2/ Manufacturing and mining excluding petroleum.

-3-

include iron and steel, aluminum and fertilizer. The private sector accounts forabout one-third of total value-added in industry and about half the sector-slabor force. Textiles, food products, leather, woodworking and furniture, andengineering are the important industries of private activity.

2.03 The industrial sector was characterized in 1973-74 by significant idleproductive capacities but rapialy improved during L975-77 iollowing theannouncement in 1973 of the "open door" policy which resulted in the relaxationof controls and greater availability of foreign exchange. This period wasfollowed by a temporary slowdown in the growth of industrial output in 1978(5.7%), but a subsequent recovery in 1979 (11.5%) pointing to the increasingimpact on producition of the investment efforts during the last few years.

2.04 Egyptian industry has significant long-term prospects to grow and broadenits base deriving primarily from the large and growing domestic market, adequatelocal energy resources and a strategic market location vis-a-vis the Middle Eastand Europe. An industrial structure and tradition already exist, as well as alarge and relatively low-cost labor force. Since development of agriculture isproceeding slowly and the service sector (mainly Government) is overstaffed, it isto industry that the Government looks to provide stimulus to growth as well as toabsorb the growing labor force through continued expansion, efficient importsubstitution emphasizing intermediate and capital goods, and expanded exports. Forexample, the sub-sector studies (para 1.05) point to the need to develop exportsand the capital goods and construction industries on a priority basis. The lattertwo subsectors will directly benefit from the Project, since they use HADISOLB'sproducts as a major input.

2.05 The Bank½s recent loans to industry include: (i) program loans toalleviate foreign exchange constraints and thereby improve capacity utilization;(ii) assistance to individual, large, high priority projects; (iii) attempts toaddress the principal issues affecting the productivity of major subsectors; and(iv) assistance no financial intermediaries to enable them to provide financialand technical asistance to private sector firms, including small scale industrialenterprises. The implementation experience of the Bank-s large industrialprojects in Egypti during the 1970's has been poor in terms of long constructiondelays and substantial cost overruns, primarily due to four factors:(i) the severe constraint in the capacity of the local civil works contractingindustry, includ.ng a chronic shortage of cement, rebars and other constructionmaterials due to foreign exchange constraints which limited imports; (ii) delaysin the release of local currency funds from the Government due to its difficultfiscal condition:; (iii) a cumbersome procurement procedure (including boycottprovisions) which prolonged the process of bid preparation, evaluation andaward; and (iv) some delays in filling the foreign exchange financing gapcreated by the suspension of disbursement by Arab co-financing sources followingthe Camp David Agreement in 1978. The more recent Bank industrial projects nowrequire international tendering of civil works contracts, where this is a majoritem, and also place emphasis on the establishment of strong project implementa-tion units as well as more efficient procurement arrangements to overcome someof the problems experienced in the past. The recent improvements in the fiscalsituation of the Government as well as in the balance of payments position arealso expected to ease some of the constraints on project implementation.

-4-

B. Development of the Steel Industry in Egypt

2.06 Steel-making, as a modern industry in Egypt, began with the establishmentof the Delta Steel Company in 1947 and the National Metal Company in 1948, bothnear Cairo, and the Egyptian Copperworks in Alexandria, in 1952. These threefacilities use steel scrap as raw material utilizing mostly the open-hearthfurnace (OHF) and to a lesser extent the electric-arc furnace (EAF) steel-makingtechnologies and producing mostly concrete reinforcing bars (rebars) as well assome other non-flat products. Their combined production in 1980 was about 0.3million tons per year (tpy) of finished products. HADISOLB, in Helwan near Cairo,is the only integrated steel complex in the country; it started operation in1958 and had an initial capacity of about 0.3 million tpy of flat and non-flatsteel products based on iron ore mined locally near Aswan. With the assistanceof the USSR, HADISOLB in the mid-1960's began an expansion which increased productioncapacity to about 1.3 million tpy of finished products. There are also four smallpublic sector foundries and forges 1/ making castings and forgings with a capacityof about 0.1 million tpy of products. The present installed steel-making capacityin Egypt is about 1.7 million tpy of finished products 2/, but production has beenconstrained to about 55% of capacity due to the operating problems at HADISOLB.

2.07 The Egyptian steel industry accounted for about 2% of GDP in 1979 andemployed about 45,000 employees (3% of the industrial labor force); about 55%of these are in HADISOLB.

C. Structure and Organization of the Egyptian Steel Industry

2.08 Except for the few very small foundries still operated by the privatesector, the steel industry was nationalized in the early 1960's. The organizationof the public sector steel industry is shown on the following page and brieflydescribed below. With the Government as majority shareholder, the Ministry ofIndustry has prime responsibility for the industrial public sector enterprises.In this context, the General Shareholder's Assembly 3/ of each company is chairedby the Minister of Industry (or his representative) and the company chairmenreport directly to the Minister. Also directly under the Minister of Industryare the General Organization for Industrialization (GOFI), which is responsiblefor investment planning and procurement, and the Executive Organization forthe Implementation of Industrial and Mining Complexes (IMC) which is responsiblefor the actual implementation of some large scale industrial and mining projectsunder the Ministry of Industry. Finally, there is the High Council for theMetallurgical and Engineering Sector, which is chaired by the Minister of Industryand is composed of the chairmen of the various companies as well as experts in thesector. This High Council has about 45 members and has a technical secretariatwith about 30 employees essentially collecting statistical data. The High Counciloperates on an ad-hoc basis to discuss sectoral problems and development issuesand provides advice to the Minister of Industry. It is also a forum for coordi-nating plans and policies of the companies within the sector, but has no formalresponsibility for formulating development plans and strategies.

11 The- fout gublic sector foundries are Nasr Castings, Nasr Pipes andFittings, Nasr Forgings, and Helwan Iron Foundries.

2/ Equivalent to 2 million tpy of liquid steel.3/ The General Shareholder-s Assembly meets generally twice a year to

review and approve the annual financial statements and the budget, as wellas major capital investment projects and financing arrangements, and toreview operating results.

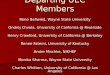

EGYPT - Organization of the Public Sector Steel Companies

| Minister of lIndustry & Mining_

High Council forthe Metallurgical& Engineering SectorChairman:Tht Minister

General Organizatiorn Executive Organizationfor Industrialization for Industrial & Mining

(GOFI) Complexes (IMC)

I.,Technical

I Secretariat for theMetallurgical &Engineering Sector

General Shareholders I /l Assembly of Each Company

Chairman: The Minister . /

Public Sector Metallurgical andEngineering Companies

NOTE: A solid line indicates a control function, a dotted line acoordinating or advisory function. On matters of capitalinvestment and procurement however, GOFI has a controlfunction in that it has to approve and recommend to theMinister the capital investment plans; also all procurementin excess of IS 0.75 million is done by the company inconjunction with GOFI and GOFI either signing or co-signing the ptrchase order/contract.

-6-

2.09 The operation of individual public sector enterprises is the responsibi-lity of an operating Board of Directors and the enterprise management within theframework of existing policies and legislation. The chairman of the board is alsothe company president; he and the top management members of the board are appointedby the Minister. The labor representatives on the board are elected by theemployees. The degree of enterprise autonomy (para 2.11) is heavily regulated bylaw and/or by ministerial policy which has effectively caused these enterprises tooperate like civil service agencies under a complex and restrictive system ofadministrative rules and regulations.

D. Issues and Problems of the Steel Industry

2.10 The Egyptian steel industry faces a number of serious problems whichaffect its present performance and future development prospects. The key problemareas relate to the: (i) institutional and policy framework for the public sectorenterprises; (ii) obsolete state of equipment and technology of existing steelmills and the need for upgrading the skills of management and workers; and (iii)poor financial situation of the steel companies.

2.11 Institutional and Policy Framework: Under existing legislation and policies,public sector enterprises are under a severe disadvantage relative to privatesector and joint venture companies due to restrictions on salary structure, numberof job grades, procurement, pricing, marketing, investments and retention ofprofits. Thus, these enterprises are finding it increasingly difficult to attractand retain qualified personnel as well as motivate employees to perform effectively,while being at the same time heavily overstaffed in the administrative and un-skilled labor groups because of the past Government practice of imposing employmentquotas. This has led to a gradual weakening in the management and organizationof most public sector enterprises, particularly those that have obsolete/inappro-priate facilities, or serious technical problems, or very low labor productivity.Many of these enterprises are not profitable and not in a position to offermeaningful production bonuses to reduce the large gap in total compensationbetween private sector and public sector pay levels.

2.12 The Government is now seriously considering specific legislative pro-posals to radically reform and liberalize the policies and regulations governingthe public sector enterprises, and thus lay the base for higher efficiency in thesector. In the meantime, several ad-hoc liberalization measures have been graduallyintroduced during the past three years: no employment quotas, an increase fromLE 0.5 million to LE 0.75 million in procurement contracts not requiring GOFIinvolvement, free dealings in foreign exchange including retention of all or partof foreign exchange export earnings, direct imports of capital goods, eliminationof the ceiling on bonus and incentive systems, unlimited participation of foreigncontractors in civil works, and selective increases in some industrial productprices (e.g. steel, textiles) which are about 80% to 105% of international levels.Also, as a result of the substantial improvement in the country's balance ofpayments as well as the Government's fiscal condition, the central Governmentnow has sufficient resources to invest in the rehabilitation/modernization ofpublic sector enterprises.

2.13 Obsolete or Inappropriate Equipment/Technology and Need for TrainingThe production facilities of the four public sector steel companies suffer froma variety of technical problems. In general, there is a combination of obsolete

or inappropriate t:echnology, old equipment, capacity imbalances and inefficientwork-flow patterns. The technical problems are exacerbated by poor to mediocreoperating practices and a shortage of highly skilled and qualified operators,further undermined by the financial attractiveness of working in nearby oilexporting countries. Consequently, production performance is poor -- in terms oflow capacity utilization relative to design capacity, low yield levels, and highconsumption rates of inputs, especially energy. The technical problems of thesteel companies can only be overcome through well-conceived rehabilitation programswhich are complemented by training of the labor force in new technologies as wellas improvements in operating procedures and upgrading of management skills andsystems. GOFI is expected to initiate a feasibility study for a modernization/rehabilitation project for the three smaller public sector steel companies in thenext few months. This effort, together with the implementation of HADISOLB'sStage I Program, and the proposed El Dikheila project, as well as the preparationof the Stage II Rehabilitation Program of HADISOLB, would cover the modernization/-expansion needs of the steel sector until the late 1980s.

2.14 Financial Situation: The profitability of the public sector enterprises,including the steel companies, is not satisfactory due to various technical andoperating problems and general inefficiencies, as well as the substantial finan-cial burden imposed by the past Government policy of: (i) fixing input and outputprices at relative levels that do not provide adequate profits; and (ii) causingsubstantial overemployment. The industry has suffered from a severe lack offinancial resources needed for adequate maintenance, rehabilitation/modernization,and working capital. The combined financial statements of the four public sectorsteel companies are sunmmarized below.

Egypt - Public Sector Steel Companies Combined Financial Statements a/(LE Million)

1975 1976 1977 1978 1979

Gross Revenues 109 123 147 180 264Cost of Sales & Overhead 128 140 154 183 265Operating Profit (Loss) (19) (17) ( 7) ( 3) (1)

Interest & Other Expenses (Net) 3 5 5 5 6Income taxes Net Profit (Loss) (22) (22) (12) ( 8) 77)

Net Profit as % o.: Revenues (20) (18) ( 8) ( 4) ( 3)Current Ratio 1.1 1.1 1.1 1.1 1.1Debt/Equity Ratio 19:81 17:83 16:84 16:84 12:88

a/ HADISOLB, National Metal Company, Delta Steel Company,and Egyptian Copperworks.

2.15 The financial results are heavily influenced by HADISOLB's operations.For example, HADISOLB's revenues account for about 46% and 40% of the combinedrevenues of the four public sector steel companies for 1978 and 1979 respectively.HADISOLB's losses of about LE 10 million for 1978 and about LE 6 million for 1979

-8-

offset the profit of the three smaller steel companies of about LE 2 million in1978 and accounted for 86% of the combined losses for 1979 respectively. Theliquidity (current ratio) of the steel companies continues to be unsatisfactory.The capital structure (debt/equity ratio) however, has remained sound in spiteof cumulative losses because of the substantial additional equity capital thatthe Government has provided, primarily to HADISOLB, to cover both investmentsand increases in working capital requirements. The Government, as part of theproposed legislation to liberalize the public sector enterprises (para 2.12), isalso reviewing the financial aspects of their operations, especially the pricingof their outputs with the view to providing reasonable profits under conditionsof efficient operations.

2.16 The major problems facing the Egyptian steel industry can be overcomewith a strong commitment on the part of the Government especially for reformsin the way the public sector enterprises are managed and regulated. But theseproblems should not detract from the inherent comparative advantage in steel-making that Egypt possesses and ought to exploit. The country has a relat-ively substantial and growing market for steel which could take advantage ofeconomies of scale in production, a fairly well developed infrastructure, anindustrial tradition including steel-making, its own hydrocarbon energy resources,some iron ore deposits (para 4.03), and a relatively cheap and readily trainablelabor force. In addition, Egypt is at a stage of industrialization whereimportant linkages between the steel sub-sector and the capital goods/consumerdurables sub-sectors as well as the construction industry should be establishedas a means of broadening the industrial base and of employment creation. Thus,the efficient modernization of its steel industry should be among the highpriority programs of the Government, specially since there is already a largesunk investment in the steel industry that is not fully productive at presentbut whose output can be increased substantially at a much lower investment costper ton of incremental output compared to new (green-field) plants.

III. MARKET AND PRICE TRENDS FOR STEEL PRODUCTS

A. The International Steel Industry and Market

1. Historical World Steel Consumption and Production Trends

3.01 During the early 1970's, the world steel industry had an optimisticdemand outlook for the decade and substantial capacity 1/ additions were plan-ned and implemented. However, the recession of 1975 cut consumption by about20% in the industrial countries and 10% worldwide from their respective pre-vious peaks in 1973 and 1974 respectively. The subsequent recovery of demand

1/ Capacity is generally measured in terms of crude steel equivalent. There aretwo generally accepted definitions of capacity: "gross" or "normal" capacity,which is about equivalent to the engineering design capacity and alternatively,"effective" or "sustainable" capacity which can be achieved for sustained periodsunder normal working conditions. In this report, the second (i.e., "effective")definition is used. Effective capacity in the US and Japan is roughly 95% ofthe gross capacity; in the EC it is about 87% of the gross capacity.

- 9 -

was slower than expected, while firmly committed investments could not be delayedor cancelled. Thus, capacity increased faster than demand and capacity utiliza-tion rates in the industrial countries dropped drastically to between 75% and 82%during 1975-78, although the rates remained close to their practical achievablelevels in most developing countries. With the low capacity utilization rates inthe major historical steel producing areas, i.e. US, Japan and the European Com-munity (EC) -- which together account for about 53% of total world steel capacityand about 41% of world consumption, steel prices became severely depressed due toheightened ccrmpetition and the steel industry in the market economies was plungedinto disarray. The deteriorating situation of the industry in the developedmarket economies finally led to strong government intervention in the major steelproducing and. consuming areas such as the US, Japan and the EC. As a result, somedegree of ordler began to evolve after mid-1978. Historical (1970-80) world steelconsumption, production and capacity data by group of countries are shown inAnnexes 3-1 aLnd 3-2 and are summarized below:

World Steel Consumption and Production a/(In Million Tons of Crude Steel Equivalent)

1970 1973 1975 1977 1979

Industrial CountriesConsumption 355 403 314 333 369Production 384 443 370 377 416Degree of Self-Sufficiency (%) b/ 108 110 118 113 113

Developing CcuntriesConsumption 59 77 91 100 119Production 38 50 56 66 82Degree of Self-Sufficiency (%) 64 65 62 66 69

Centrally PlaLnned EconomiesConsumpticn 176 210 235 239 260Production 176 205 221 230 248Degree of Self-Sufficiency (%) 100 98 94 96 95

World TotalConsumption 590 690 640 672 748Production 598 698 647 673 746

a/ Apparent c onsumption.b/ Production as % of consumption.

3.02 While steel consumption declined in the industrial countries between1973 and 1979, it grew steadily in the developing countries, by about 7.5% peryear, and in the centrally planned economies (CPE) by close to 4% annuallyduring the same period. The developing countries as a group import (net) roughlyone-third of their steel consumption, although individually their degree ofself-sufficiency varies considerably. Between 1970 and 1979, self-sufficiencydeclined fronm 20% to 16% respectively for North Africa and the Middle Eastregion but increased for the Asia and the Pacific region from 54% to 72% and

- 10 -

for Latin America and the Caribbean region, from 72% to 82%. During the sameperiod the net imports of the developing countries increased from 21 to 37 milliontons and those of the CPE's from practically nothing to about 12 million tons.These increases in net imports were supplied primarily by Japan and the EC. Thus,even though steel-making capacity in the developing countries as a group increasedby about 98% from 46 to 91 million tpy during 1970-80, the group-s self-sufficiencyimproved only slightly from 64% to 68% as demand during 1970-80 grew from 59million tons in 1970 to an estimated 125 million tons in 1980 or by 212% (para3.05).

2. Future World Steel Demand and Supply Trends

3.03 Forecasts of steel demand are generally based on assumed growth ratesof GDP. Before the 1975 recession, the relationship between growth in steelconsumption and growth in GDP in the industrial countries had been stable 1/.However the extremely slow recovery in steel consumption after 1975, even whenGDP growth had recovered somewhat, led to an evolving consensus in the industrythat the basic relationship had changed during the mid-1970's. Three factors arethought to have caused this change: (i) about 30% to 40% of the steel deliveriesin industrial countries are consumed in sectors involving fixed capital formation;thus, as the growth in fixed capital formation continued to remain low relative toother sectors in the economy the growth in steel demand was also adversely affected;(ii) there has been a gradual decline in the usage of steel per unit of final pro-duct as substitution by other materials such as aluminum and plastics intensifiedafter the energy crisis of 1973/74, as energy conservation pressure led to smaller/lighter product designs (e.g. automobile) and as the quality of steel improved,thereby requiring less steel; and (iii) the increasing use of continuous castingtechnology (Annex 3-3) which, in addition to being less energy intensive, provideshigher steel yields than traditional production methods. In other words, a largerquantity of finished product is produced from each ton of crude steel when continuouscasting is used. Consequently, demand in terms of crude steel equivalent, whichis the generally accepted statistic for measuring steel demand and production,declined.

3.04 Forecasts of steel demand and production capacity for various regionshave been prepared for 1985. 2/ The forecasts assume that GDP growth rates inthe industrial countries would be depressed at an average of only 2.8% peryear during 1979-85 as a consequence of recent recessionary trends. In addi-ition, the continuing impact of the three factors mentioned in para 3.03 aboveis expected to further lower the GDP/steel consumption growth ratio for theindustrial countries to about 0.68 during 1979-85, compared to the historicalvalue of about 0.87 during 1960-74 and about 0.7 during 1974-79. On thisbasis, steel demand in the industrial countries is expected to grow at an

1/ The relationship is defined in terms of the ratio of the steel consumptiontina ' A& s of % tel e a½vat'tgowth rate to the Gipgrowth rate in real terms.

2/ The forecasts are based on a world steel market study (The International

Steel Market and the Outlook for Light Non-Flat Products, April 6, 1981)undertaken jointly by the Bank's Industrial Projects Department, the EconomicAnalysis and Projections Department and a specialized steel market consultingfirm.

- 11 -

average rate of only about 1.9% per year between 1979 and 1985 1/ and reach 390million tons in 1985. It should be remembered that steel consumption in theindustrial countries increased at an average annual rate of 5.3% during the1960's, and while it did not show any consistent growth pattern in the 1970's,the projected 1985 demand is still 3% lower than the peak recorded in 1973.This is a conservative forecast of steel consumption by 1985 assuming continuedsluggish growth in the economies of the industrial countries.

3.05 The sluggish economic performance in the industrial countries expectedduring 1980-85 will also dampen the economic growth of developing countries.Thus, steel demand in the developing countries is projected to grow by onlyabout 5.6% per year 2/ during 1979-85 and reach about 165 million tons in 1985.Steel demand in the CPE's is assumed to grow by about 2.5% per year during 1979-85. The followirtg table gives estimates and forecasts on consumption/demand,production, capacity and capacity utilization for 1980 and 1985 respectively forvarious regions and economic groupings.

Estimate and Forecast of World Steel Demand, Production and Capacity(In Million Tons of Crude Steel Equivalent)

1980 Estimate 1985 ForecastConsump- Produc- Capa- Rate Consump- Produc- Capa- Ratetion tion city (%) a/ tion tion city (%) a/

Industrial Countries

US 113 99 133 74 148 132 135 98EC 106 131 175 75 120 152 170 89Japan 78 112 138 81 83 123 138 89Others 33 37 39 95 39 43 44 98

Sub-Total 330 379 485 78 390 450 487 92

Developing Countries 125 85 91 93 165 115 123 93Total Market Economies 455 464 576 81 555 565 610 93

Centrally PlannedEconomies 265 255 270 b/ 94 300 290 305 b/ 95

World Total 720 719 846 85 855 855 915 93

a/ Capacity utilizzation rate.b/ Estimate assuming capacity utilization rate would be roughly 95%. For 1985,

it is also assumed that net steel imports of the CPE's will remain at 10million tpy.

l/ The average consumption for 1978, 1979 and 1980, has been used as the 1979 baseon which the projected average annual growth rate was applied to calculatethe 1985 consumption.

2/ This compares to an average growth in steel consumption in the developingcountries of about 9.7% per year during 1960-74 and 6.6% annuallyduring 1975-80.

- 12 -

3.06 Total world steel demand is expected to reach 855 million tons by 1985as against a world production capacity of 915 million tpy of crude steel equivalent.Developing countries are expected to account for nearly half of the increase incapacity between 1980-85 with the CPE's accounting for the remainder. The antici-pated absence of capacity additions in the industrial countries reflects thephase-out of obsolete capacity in the EC and the US, the weak market forecast, aswell as the emphasis on cost-saving and modernization investments to increaseprofitability rather than capacity. Under this scenario, capacity utilization in1985 will be about 93% in the market economies compared to an estimated 81% in1980, and 95% in 1970. This would be close to the effective steel-making capacitythat could be sustained over an extended period of time.

3.07 In the early 1980's, the basic steel supply and demand structure in theindustrial and developing countries will probably remain the same as in the1970's. In the developing countries, a larger proportion (about 60%) of steeldemand and production will continue to be non-flat products such as rebars, wirerods and light sections used in civil engineering construction activities with therest (40%) in flat products, such as tin plate, coils, sheets and plates, whichare used for equipment, pipes and consumer durables. As pointed out in a recentstudy 1/, non-flat steel products, particularly rebars, tend to be competitivelyproduced also by semi-integrated steel mills of smaller sizes and located close tothe market since the simplicity of the technology and small economic sizes,freight savings, and responsiveness to short-term market trends favor this typeof structure. Thus the developing countries are expected to increase capacityprimarily in non-flat steel products. On the other hand, flat steel productsrequire a more sophisticated technology and are in general more efficientlyproduced by large integrated mills mostly in the industrial countries.

3. International Price Trends for Steel Products

3.08 On the basis of the above discussions, it appears that during 1980-85,the steel industry in the market economies will be able to adapt better tomarket conditions and reestablish a healthy balance between demand and capacity.In addition to considerations of profitability, the capacity utilization rate isgenerally believed to be the most influential short-term determinant of steelprices. As capacity utilization rates approach 90% and a seller's market be-gins to develop, market pressures will start to push prices higher. Althoughit is difficult to generalize, past experience indicates significant priceincreases--and particularly so in the export markets--as the capacity utilizationrate exceeds 90%. Since the steel industry in the market economies is projectedto operate at about 93% capacity by the mid-1980's, prices -- and here againespecially export prices -- could therefore be expected to firm up and the pro-fitability of the industry should be satisfactory. Beyond the mid-1980½s, addi-tional capacity would be required to avoid a shortage situation and temporaryextreme price increases may occur if additional capacity is not added in time.Any steel shortage will particularly affect the developing countries, since thisgroup is always the first to suffer in terms of price as well as availabilitywhenever a tight demand/supply balance develops and since the group-s degreeof self-sufficiency is projected to improve only slightly from about 68% in1980 to about 70% in 1985.

1/ Hideo Hashimoto, "Prospects for Markets in Concrete Reinforcing Bars:1980-85, World Bank Division Working Paper No. 1980/5, July 1980.

- 13 -

3.09 The international prices of selected steel products have been projectedfor 1985 (Annex 3-4) taking into account price trends for iron ore and energy,the economic activity in various regions, and the expected average capacityutilization rate for the industry. The forecasts, together with historicalvalues are shown below. To arrive at the CIF price to most developing countries,ocean freight and related charges will at present generally add roughly betweenUS$40 to 50 per tona of product; by 1985 they are expected to be about US$50 to 60per ton (all in constant 1979 terms).

Historical and Projected Steel Prices - FOB (Antwerp) a/(In US$ per ton)

Rebars Hot-Rolled Strip/Coil(Current (Constant (Current (Constant

Year US$) 1979 US$) b/ US$) 1979 US$) b/

1970 116 346 131 3911972 105 217 128 2651974 311 517 298 4951975 207 298 223 3211976 227 321 246 3481978 234 265 272 3081980 311 276 337 3001985 (Forecast) - 320 - 355

aT Historical prices are the arithmetic average of the quarterly pricespublished by Metal Bulletin.

b/ Based on the Bank's index of international inflation.

3.10 The anticipated situation of the world steel industry by the mid-1980swould indicate opportunities for the developing countries to expand their ownsteel industries wihere efficient import substitution is possible. Thus, developingcountries with relatively large and growing markets, some industrial infrastructure,relatively low labor rates which more than offset their lower labor productivity 1/compared to industrialized countries, and domestic sources of iron ore and/orenergy (e.g. coal, natural gas etc.) would be in a good position to undertakean expansion of their steel industries. One such developing country is Egypt.

B. Egyptian Steel Demand and Production Trends

3.11 Egyptian apparent consumption of finished steel products 2/ was about1.64 million tons in 1980 compared to about 0.67 million tons in 1970 indicat-ing an average anniual growth of about 9.4% during that ten-year period. Incontrast, during 'i950-1970, consumption had grown by only about 4% per year.Domestic production, however, increased by only about 8.8% per year during1970-80, and in 1980 supplied only about 57% of consumption. HADISOLB pro-

1/ Although labor productivity in the developing countries, with the possibleexception of South Korea, is only 25% to 50% of that in industrial countries,wage rates are only 10% to 25% thereby providing some source of comparativeadvantage. Furthermore, steel production in some mills located in developingcountries (e.g. South Korea, Brazil) has now reached or exceeded design capa-city, thus making the equipment productivity of these mills comparable tochose Zn developed countrries.

2/ Finished flat and non-flat steel products respectively are assumed to beequivalent to about 75% and 90% of the crude steel weight. Thus the 1.64million tons of finished steel consumption in 1980 would be equivalent toroughly 1.92 million tons of crude steel.

- 14 -

duced about 0.36 million tons of flat products and 0.16 million tons ofnon-flat products in 1980 equivalent to 78% and 14% of the local consump-tion of these types of products respectively. The 1979-1980 consumption wasapproximately distributed as follows: rebars and rods - 50%; other non-flatproducts, including steel castings and forgings - 23%; and flat products -27%. The construction industry is the dominant market for steel products inEgypt at present, accounting for about one-half of steel consumption.Construction activity had grown at an average annual real rate of 6.5% during1971-76 and 14% during 1976-79, and the construction boom is expected tocontinue well into the 1980's due to strong housing demand and industrialinvestment activities.

3.12 The historical (1970-80) production, imports and consumption of steelproducts in Egypt are shown in Annex 3-5 and summarized in the following pagefor 1977-80 together with the forecasts for 1985 and 1987. The production in1980 reflects the continuing increase which started in 1975, particularly atHADISOLB and National Steel Company, as the local steel companies improvedoperations and took advantage of the additional capacity that was installedin the early and mid-1970s. However beyond 1980, only minor increases inlocal production can be expected from the existing facilities without anymajor capital investments. The forecast for 1985 and 1987 assumes that HADISOLB'sStage I Program as well as the proposed El Dikheila project proceeds as scheduledthereby resulting in substantially higher production of rebars/rods, medium andheavy sections, as well as flat products. However, the forecast does not assumeany other major investment in the steel sector except for a small continuous bil-let casting facility at Delta Steel. HADISOLB's flat product output is expectedto reach 430 and 495 thousand tons during 1985 and 1987 respectively, compared to355 thousand tons in 1980. The Company's non-flat product output is likewise ex-pected to be 294 and 351 thousand tons during 1985 and 1987 respectively comparedto 160 thousand tons in 1980. The major increase in rebar/rod production willcome from the proposed El Dikheila project which is expected to start operationsin 1985 with an initial output of 200 thousand tons and to reach 790 thousand tonsby 1987. The three semi-integrated public sector steel companies are expected toinitiate feasibility studies for modernization/expansion projects but the scopeand timing of such investments can not be reliably assumed at present and are notshown in the production forecasts. It should suffice to point out that the scopewill take into account the types of non-flat products (e.g. rebars, drawn wire,and light sections) that would otherwise be imported by Egypt as indicated in theprevious table.

3.13 The projected domestic demand for steel products is expected to in-crease by an average of about 8.2% per year during the 1980s. As mentionedearlier, domestic steel consumption increased by an average of about 9.4% peryear during 1970-80. In general, steel demand in a developing economy that is onthe threshold of rapid industrialization, as is the case of Egypt, will grow atslightly more than the rate of growth of GDP. The Egyptian GDP has increased byabout 7.6% per year during 1970-80 and is expected to grow at an average rate ofabout 7% annually during 1980-87. 1/ In particular, the industrial sector isexpected to be the fastest growing sector during the early 1980s, increasing itsoutput by as much as 8% to 10% per year. Thus, an average growth rate in steelconsumption of 8% to 9% per year very reasonable and probably even somewhatconservative. 2/ Finally, demand during the mid-1980½s is expected to be

1/ Bank estimate.2/ During 1970-80, the implied steel consumption/GDP growth ratio averaged

about 1.24; for the forecast period (1980-87), the implied ratio wouldbe 1.17.

-15-

Egypt - Production and Imports of Finished Steel Products(In Thousand Tons)

Average AnnualActual Forecast Growth Rate (%)

1977 1978 1979 1980 1985 1987 1977-80 1980-85

Production a/

. Flat Steel Products 200 222 259 355 430 495 21.0 3.9b. Rebars & Rods b/ 283 288 317 300 550 1,140 2.0 12.9c. Other Non-Flat Products 181 203 215 270 380 430 14.2 7.0

Total Production 664 713 791 925 1,360 2,065 11.8 8.0

Impports

a. Flat Steel Products,Incl. Tubes & Pipes 125 167 191 157 285 350 7.9 12.6

b. Rebars & Rods 163 221 444 728 f/ 625 240 64.6 (3.1)c. Other Non-Flat Product:s 303 278 153 75 160 200 (60.0) 16.0d. Semi-Finished Products 37 47 34 40 80 100 2.0 15.0

Total Imports 628 713 822 1,000 1,150 890 17.8 2.8

Exports c/ 6 54 42 50 80 100 15. 0

Apparent Consumption d/

Flat Products 319 335 408 462 635 745 13.0 7.9Rebars & Rods 446 509 761 828 f/ 1,175 1,380 23.0 8.3Other Non-Flats 484 481 368 345 540 630 (12.0) 8.6

Total 1,249 1,325 1,537 1,635 2,350 e/ 2,755 e/ 9.4 8.2 e/

a/ Finished steel products excluding semi-finished or intermediate productsas well as steel pipes and tubes.

b/ The production forecast for 1985 and 1987 includes 200,000 and 790,000 tonsof rebars and rods respectively from the El Dikheila project.

c/ Egypt exports only flat steel products.dk/ Production plus imports (excluding semi-finished products) less exports without adjust-

ments for stock changes.e/ The forecast uses the- average consumption for 1979 and 1980 as the 1980 base and an

average increase of 8.2% per year for total steel consumption during 1980-87. The projecteddemand is assumed to be distributed as 27% flat, 50% rebars and rods, 23% other non-flats.

f/ Import duties on rebars were suspended in 1980 and international prices were low, prompt-ing a large import quantity to build-up local stocks. Although apparent consumption doesnot take into account stock changes, an adjustment is needed for 1980 to ensure a goodbase figure for the dlemand projections. It is assumed that only about 528,000 of the728,000 tons importedl were actually consumed in 1980 with the remainder carried over asstocks for 1981 (as of March 1981, Delta Steel had stocks of roughly 200,000 tons ofrebars and rods). Thus, 1980 rebar and rod consumption would be about 828,000 tonscompared to local production plus imports of about 1,028,000 tons.

-16-

distributed as follows: 50% rebars and rods, 27% flat products and 23% othernon-flat products as was the case during 1977-80.

3.14 A UNIDO-sponsored study completed in January 1979 estimated that Egyptiansteel demand in 1983 and 1987 would be about 2.1 and 3.1 million tons of finishedproducts respectively which implies a demand of about 2.4 million tons by 1985.The earlier (1978) market evaluation by UEC in connection with the HADISOLBdiagnostic studies (para 1.05) projected a consumption of about 2.3 million tonsand 3.3 million tons of finished products for 1985 and 1990 respectively. Theforecast above used in this report is in line with the UEC projections and slightlyless than that forecasted in the UNIDO-sponsored study.

3.15 On the basis of the above steel consumption forecasts, HADISOLB shouldhave no difficulties in selling the additional production from Stage I. Egyptwill still be importing some flat steel products included in the Stage I product-mixand could absorb the entire output of HADISOLB even if the Company chooses not toproceed with the small quantity of additional exports from 1985 onwards.

C. Comparison of Egyptian and International Prices for Steel Products

3.16 The Egyptian economy has a centralized structure and commodity pricesare still extensively controlled by the Government even after the "open-doorpolicy" was announced in 1973. Due to the complex industrial linkages as well assensitive socio-economic factors, only a gradual elimination or reduction ofconsumer and industrial non-food price subsidies can be expected for a largenumber of products and then only within the context of somewhat parallel increasesin wages and income. Nonetheless, a visible trend in increasing local pricescloser to international levels for a few industrial products, such as steel, hasemerged.

3.17 Domestic steel prices and distribution margins for steel products arecontrolled by the Government. Price changes have been infrequent though substantialwhen they occured. There were only three price increases since 1970: in November1973; in December 1977 (by 25% to 30%); and the most recent in March 1980 (by 20%to 30%). Prior to 1980, domestic ex-factory prices ranged from 85% to 100% of theFOB export prices from Europe and Japan or about 60% to 80% of the landed cost ofimports into Egypt (excluding duties). The recent (March 1980) price increases,however, brought the Egyptian price level reasonably in line with internationalprices. Local ex-factory prices are now 100% to 130% of the FOB export prices inEurope or Japan and about 80% to 105% of the landed cost of imports (Annex 3-6).l/For non-flat steel products, which constitute two-thirds of local steel consump-tion , domestic ex-factory prices are about 90% to 105% of the landed cost ofimports (excluding duties). Steel therefore is among the few commodities whosepresent local price approximates international levels. The present prices areshown below:

1/ The current domestic ex-factory prices range from roughly 90% to 110%of the US Trigger prices (1980, 4th quarter) for hot and cold-rolledsheets, heavy plate, galvanized sheets, rebars and some sections.

- 17 -

Egypt - I)omestic Steel Prices In Effect Since March 1980

Product LE/Ton US$/TonRange for Range for

Base a/ Extras b/ Base Extras

Pig Iron 125 - 181 -

Billets 135 - 196 -Hot Rolled Strip 211 12-27 306 17-39Hot Rolled Sheel 256 8-10 371 12-15Galvanized Sheet 391 25-90 567 36-131Plate 251 19-45 364 28-65Light Angles 291 17-33 422 25-48Heavy Sections 286 5-42 415 7-61Cold Rolled Sheet 266 13-39 386 19-57Cold Rolled Strip 286 20-88 415 29-128Rebars 269 n.a. 390 n.a.

a/ Includes LE 6 (US$9) per ton for packaging, inspection and loading,except in the case of pig iron and billets.

b/ In line wilth conventional systems elsewhere of charging extras accord-ing to width, thickness, grade and other typical specification options.

3.18 There are tariffs on imported steel products 1/ ranging from 5%to 40% which further increase the difference in the final cost to the consumerbetweeen the imported product and the local steel. On the other hand, energyinputs (power, nLatural gas, and fuel oil) are priced throughout the economy atsubstantially less than their economic or international price equivalent (para8.01). 2 / In the case of HADISOLB, the Company also receives an indirectGovernment subsidy, equivalent to 33% of the price of coke purchased from ELNasr Coke Company (para 4.17). But the Government intends to progressivelyphase-out and eliminate the coke subsidy as HADISOLB's financial strengthimproves with increases in production, efficiency and/or selling prices.Thus, steel producers, though receiving somewhat less for their productscompared to the landed cost of imported steel, are also paying less for theirenergy inputs which constitute a substantial portion of steel productioncosts. Nonetheless, because of the obsolete and inefficient operations,coupled with the low productivity of the Egyptian steel industry, steelproducers in Egypt as a group were unprofitable until prices were raised inMarch 1980. Wit:h these new prices, the steel companies as a group areexpected to about break even or show a small profit.

1/ The 20% import duty on rebars has recently been suspended.2/ The Government has acknowledged the need for a more realistic energy pricing

structure. In the context of two recent Bank energy projects in Egypt(Power III and Cairo Gas Distribution) approved in FY 1980, the Governmenthas initiatedl a comprehensive petroleum product pricing study and thepreliminary results of the study are expected by the end of 1981 and willbe discussed with the Bank. In addition, some increases in the prices ofpetroleum products and natural gas mnay be announced before the end of 1981.

- 18 -

IV. THE COMPANY

A. Background and Ownership

4.01 The Egyptian Iron and Steel Company (HADISOLB), the project sponsor, isthe only integrated steel plant and the largest steel producer in Egypt. TheCompany was established in 1954 with the construction in Helwan, near Cairo, ofa 0.3 million tpy (finished products) integrated mill supplied by DEMAG (FRG).Commercial operations started in 1958. HADISOLB uses local iron ore from itsown mines as raw material for steel-making and buys its coke from the El NasrCoke Company, another public sector enterprise located adjacent to HADISOLB'sHelwan plant. The first iron ore mine, near Aswan, had a low quality ore (42%Fe and high phosphorus content) and was a relatively small-size deposit (25million tons); it was discontinued in 1975 (para 4.03).

4.02 HADISOLB's equity shareholdings have not changed significantly sincethe early 1960s. About 98% of the equity is held by the Government and otherpublic sector entities and the remaining 2% by private shareholders, includingDEMAG, the supplier of the original plant. Since nationalization in 1961/62,the private shareholders have been entitled to a minimum dividend of 4% on theface value of the shares. This dividend is guaranteed and has in fact been paidby the Government since HADISOLB has not been profitable for the last sevenyears. The equity shareholdings are shown below:

HADISOLB - Equity Shareholdings

Initial (1954) As of December 31, 1979LE Million % LE Million %

Ministry of Finance 2.00 95.2 199.5 62.1Banks and other Institutions a/ 0.04 1.9 12.3 3.8GOFI b/ 0.04 1.9 8.0 2.5IMC c/ - - 94.8 29.5

Sub-total Public Sector Shareholders 2.08 99.0 314.6 97.9

DEMAG 0.01 0.5 1.4 0.4Other Private Shareholders 0.01 0.5 5.3 1.7

Total 2.10 100.0 321.3 100.0

a/ Private sector prior to their nationalization in 1961-62.b/ General Organization for Industrialization.c/ Executive Organization for Industrial and Mining Complexes.

B. Production Facilities and Performance

4.03 In the early 1960's HADISOLB embarked on an expansion program. Atthe outset, it installed its first sinter plant and a light section mill in1964. In 1968 it signed an agreement for a USSR-designed and suppliedexpansion to be carried out in two phases. The first phase was started in1968 and mechanically completed in 1973; it involved primarily the additionof a 0.6 million tpy (liquid steel) integrated flat product plant. The secondphase, with an incremental capacity of also 0.6 million tpy (liquid steel)

- 19 -

involved an expansion/modernization of the non-flat products facilities. Itwas started in 1972/73 and mechanically completed in 1978, except for themedium section mill which was completed only in 1980. A new iron ore mine atBahariya, some 350 kms southwest of Cairo, was also developed with USSR tech-nology and started operations in 1973. The Bahariya iron ore, although bet-ter than the Aswan ore, is also of poor quality (para 4.08 - 4.10) but the orereserves of the mine are relatively large (250 million tons).

4.04 HADISOLB's major steel-related production facilities and their respectedrated capacities are shown in Annex 4 and summarized below together with therecent production performance.

HADISOLB - Capacity of Main Facilities and Production Performance(In Million Tons)

Facility Product 1975 1976 1977 1978 1979 1980

1. Iron Ore Mine Iron Ore Capacity a/ 2.5 2.5 2.5 2.5 2.5 2.5(Bahariya) Production 0.88 1.11 1.29 1.45 1.70 1.85

Util. Rate (%) 35 44 52 58 68 74

2. Sinter Plants Sinter Capacity 1.74 1.74 2.40 3.15 3.15 3.15Production 0.86 1.08 1.21 1.19 1.41 1.78Util. Rate (%) 49 62 50 38 45 54

3. Blast Furnaces Pig Iron Capacity 0.96 0.96 0.96 0.96 1.30 1.75Production 0.51 0.57 0.63 0.63 0.75 1.00Util. Rate (%) 53 59 66 66 58 57

4. Steel-Making Liquid Capacity 0.93 0.93 1.24 1.55 1.55 1.55Steel Production 0.34 0.43 0.51 0.52 0.58 0.84

Util. Rate (%) 37 46 41 34 37 54

5. Steel-Casting Crude Capacity 0.95 0.95 1.25 1.55 1.55 1.55Steel Production 0.19 0.28 0.36 0.38 0.51 0.76

Util. Rate (%) 20 29 29 24 33 49

6. Rolling Mills Finished Capacity 0.95 0.95 0.95 0.97 0.99 1.19Products Production 0.30 0.27 0.28 0.32 0.36 0.52

Util. Rate (%) 32 28 29 33 36 43C. Major Problem Areas

4.05 The periods 1974-77 and 1978-80 were the operational learning periods forHADISOLB-s first and second phase expansion projects respectively. The produc-tion performance of HADISOLB has slowly improved but is still low, with productionof the steel shops only at about 54% of design capacity in 1980. Under presentconditions, that is, without any major rehabilitation and operations improvementprojects, output can be expected to improve to at most only about 0.9 million

a/ The mining capacity is actually 3.3 million tpy but constraints in thetrain loading' facilities limit potential shipments to Helwan to not morethan 2.5 million tpy at present (assuming locomotives and wagons areavailable). This actual shipping capacity is adequate to serve thepresent requirements of HADISOLB as well as future requirements underthe proposed Project.

- 20 -

tpy of liquid steel or about 60% of liquid steel capacity by 1985 after somemore learning experience. The extremely poor production performance of HADISOLBat present and unfavorable future prospects without a substantial rehabilitationprogram are primarily due to three major problems: (i) a low quality rawmaterial (local iron ore) that is difficult to process; (ii) equipment whicheither embodies obsolete or inappropriate technology; and (iii) an organizationand management that is basically inadequate to operate and maintain a plant ofHADISOLB-s size, complexity and difficult technical conditions, coupled withoveremployment and an uncompetitive salary structure. Even a strong organizationand management would find the complexity of the operations and the technical andpersonnel problems of the Company a difficult challenge.

4.06 Several consulting firms have studied various aspects of the technicalproblems of HADISOLB since the mid-1970s. The latest and most comprehensivediagnostic studies were undertaken by US Steel Engineers and Consultants (UEC)under the Bank-s engineering loan (para 1.05). The UEC studies also developedpractical approaches for solving these problems and provided the basis forHADISOLB-s Stage I Rehabilitation Program (paras 4.18 - 4.23)

4.07 The three major problem areas (para 4.05) and the proposed solutionsare briefly described below:

4.08 Low Quality of the Bahariya Iron Ore: The local ore mined byHADISOLB at Bahariya has an average content of only 52% Fe, a rather low gradecompared to about 60% to 65% for the typical internationally traded iron ore.The most serious problem with the ore is however its relatively high contentof undesirable compounds such as salts (sodium chloride and potassium chloride),silica, alumina and manganese which make the operation and maintenance of thesinter plant and the blast furnaces very difficult. The use of high qualityimported ore or pellets for blending with the local ore would help significantlybut is not possible at present because there are no adequate port-handlingfacilities and local rail transport is also a serious bottleneck.

4.09 Several studies have been undertaken concerning the possiblebeneficiation of the Bahariya ore. UEC-s technical evaluation, on thebasis of comprehensive laboratory tests and some pilot plant tests at USSteel½s facilities suggest that a leaching and washing beneficiation processwill reduce the salt content, in terms of chlorine equivalent, by about 85%.In this context HADISOLB is proposing to build a semi-industrial pilot oreleaching/washing plant to further evaluate the technical, financial as well asenvironmental aspects as a basis for a full feasibility study. The Bank isfinancing, under the engineering loan, the cost of consultants who will designand engineer the pilot plant. Any decision on a commercial scale beneficiationproject will probably be part of HADISOLB's Stage II Rehabilitation Program.In the meantime, as part of the Stage I Rehabilitation Program, HADISOLB willpartially compensate for the low quality iron ore by implementing the relevantoperations improvement schemes proposed by UEC, and by adding equipment toovercome the reduction in effective capacity as well as the process restrict-ions imposed by the low quality ore (paras 4.11 and 4.12). But productionefficiency at the sintering and blast furnace operations will continue tosuffer until a method for improving the quality of the iron ore rawmaterial is implemented.

4.10 Notwithstanding the low quality of the Bahariya iron ore, it is stillan economic raw material for HADISOLB because the cost of mining and transportis low (financial cost is US$10 per ton of ore delivered to the plant andeconomic cost is roughly about US$15 per ton) compared to the landed cost into

- 21 -

Egypt of high quality imported iron ore (at least US$40 per ton) 1/. The lowmining cost is due to the relatively easy mining conditions, the low capitalinvestment in the mine associated with the USSR-supplied equipment and techno-logy and the use of many items of salvaged heavy equipment from the Aswan HighDam construction project.

4.11 Equipment andJ Related Technical Problems: The technology and equipmentassociated with much of the original DEMAG plant is over 20 years old and hasalso suffered from inadequate maintenance practices in the past; and thus itis obsolete and must either be scrapped or rehabilitated given the technolo-gical developments during the last twenty years. Aside from the old DEMAG plant,the newer facilities supplied by the USSR are also experiencing technical andoperating problems. In general instrumentation in these facilities is unsatis-factory. Thus, of the roughly 17,000 instruments in the new facilities, about11,000 have been planned for replacement during the next three to five years.In the sintering plants, the high cloride content of the ore has caused saltdeposits to drastically reduce the effective sintering capacity and efficiency.With a modified grate bar design recommended by UEC, and better instrumentationand operating practices to be introduced as part of the proposed Bank Project,the existing sinter plants should be able to support the Stage I target productionof 1.2 million tpy of liquid steel equivalent. The fifth sinter machine (para4.20) included in the Stage I scope will raise sinter production to supportthe design production level of 1.6 million tpy of liquid steel equivalent.

4.12 The operations of the two new blast furnaces have been adversely affectedby several factors; the high salt (chloride) and silica content of the iron ore,the low blast temperatures caused by the low calorific value of the top gas, andthe use of poorly calcined fluxes (limestone and dolomite). The ultimateconsequences of these factors are: a coke consumption rate that is roughly 40%higher than the projected rate under Stage I; an effective capacity that isroughly 60% of the attainable capacity; a very short operating life for thefurnace refractory linings; and frequent and expensive maintenance work (anddowntime) to remove scales as well as to reline the furnaces. UEC has submittedseveral recommendations, particularly the use of an acidic slag in the blastfurnaces followed by external desulphurization, to minimize these operatingproblems and these recommendations have been incorporated in the Stage I scope.

4.13 The three new basic oxygen furnaces (BOF) in the steel-making shop alsohave problems which will be corrected under the Bank Project. The continuousslab casting shop has produced close to capacity but the yield is poor (e.g. toomany rejects) and the surface quality of the slab is also poor. Better instru-mentation and better operating practice should correct most of the slab-castingproblems. The three continuous billet-casters on the other hand, have producedat only one-third of capacity and are the most serious production bottlenecks atpresent. A major modification of the billet casters will be required to correctthe problems and the Project scope includes a major revamp of one billetcaster. The remaining billet casters will be modified in the Stage II Rehabili-tation Program to minimize the disruption of production during the Stage Iimplementation period as well as to confirm the level of improvement that couldbe achieved through the modification of the first billet caster.

1/ On an iron content basis, that is, per ton of Fe, the financial cost andthe economic cost of the Bahariya ore would be about UJS$19 and US$29 res-pectively compared to the landed cost of high quality imported ore ofabout US$62. These costs are in 1980 ITS$.

- 22 -

4.14 Finally, the iron ore storage and handling system at the Helwansite is limited and cannot support an output of more than roughly one milliontpy of liquid steel at present, especially not with the disruption in railwaytransportation from the Bahariya mines during the three-month sandstormseason. Again, Stage I is designed to overcome this problem. At theBahariya mine, mining capacity is adequate with the addition of five 70-tontrucks which were financed under the Bank's Second Industrial Import Loan (para1.06).

4.15 Management and Organizational Problems: As mentioned earlier (para2.11), the policies and regulations governing public sector enterprises areamong the major causes of the managerial and organizational problems ofHADISOLB. The Government has agreed however, to provide HADISOLB such degreeof autonomy in the areas of investment, procurement, pricing, and wages and man-agement policies to enable the Company to achieve its financial and operationalobjectives under the Project. Even now, HADISOLB is already taking advantageof the liberal regulations (para 2.12) introduced during the last few years.Thus, the Company has introduced a more innovative incentive system during thepast two years, and although it has several shortcomings and still leaves awide gap between salaries and wages paid in the private sector, the systemappears to have had a positive impact on overall performance. In addition,the top management of HADISOLB has began to recognize and take correctivemeasures with respect to the weak operating systems of the Company. Thus,UEC, under a separate UNIDO financed project, designed a computerized prevent-ive maintenance and spare parts control system which has been implementedalso with technical assistance from UNIDO. This UEC assignment recommended amuch broader set of computerized support functions for production such as aproduction planning system and a raw material control system; these have beenincluded in the scope of the Project. The Company has also established anenergy conservation unit and an industrial engineering unit to fill importantorganizational voids in the technical support staff. But much remains to bedone. For example, the employee turnover rates, specially among managers (20%-30%) and among engineers and skilled workers (10% - 15%) are still very high.Also, while the Company has a relatively well-conceived training program,implementation is not satisfactory. At present, the steel mill has no envi-ronmental protection standards nor does it have any pollution monitoringequipment. Finally, industrial safety is also not adequately emphasized.Under the Project, these shortcomings will begin to be corrected (para 5.05).

D. Financial Performance

4.16 The recent financial performance of HADISOLB is shown below, and the pro-jected situations with and without Stage I are discussed in Chapter VII.

- 23 -

HADISOLB - Historical Financial Performance(in Million of Current LE)

1974 1976 1976 1977 1978 1979 1980 a/(6 months)

Gross Revenues 35.0 56.5 58.9 62.8 83.0 106.7 78.0Cost of Sales & Overhead 34.6 74.6 81.3 74.7 90.0 110.3 76.4Operating Profit (Loss) 0.4 (18.1) (22.4) (11.9) (7.0) ( 3.6) 1.6Interest Expense 0.7 2.0 2.5 2.4 2.7 2.4 1.6

Net Profit (0.3) (20.1) (24.9) (14.3) (9.7) (6.0) 0.0Cash Generation 4.3 (9.7) (7.6) 4.6 9.9 18.5 13.3

Current Assets 58.5 84.5 101.4 124.5 152.4 180.7 214.4Fixed Assets 221.1 231.4 237.2 230.2 221.7 261.5 262.8Current L-iabilities 36.9 64.6 84.0 95.9 123.7 149.8 158.0Long-term Debt 55.8 48.8 43.5 3P.2 33.2 28.1 28.2Equity & Reserves 186.9 202.5 211.1 220.6 217.4 264.3 283.6

Net Profit as X

of Revenue (1) (36) (42) (23) (12) (2) 0Current Ratio 1.6 1.3 1.2 1.3 1.2 1.2 1.2Debt/Equity Ratio 23:77 19:81 17:83 15:85 13:87 10:90 9:91

a/ The fiscal year for HADISOLB was changed from calendar year to July-June startingin July 1980. A half-year statement was therefore prepared for January-June 1980.