Embed Size (px)

Citation preview

Document of The World Bank

FOR OFFICIAL USE ONLY

Report No. 54353-MN

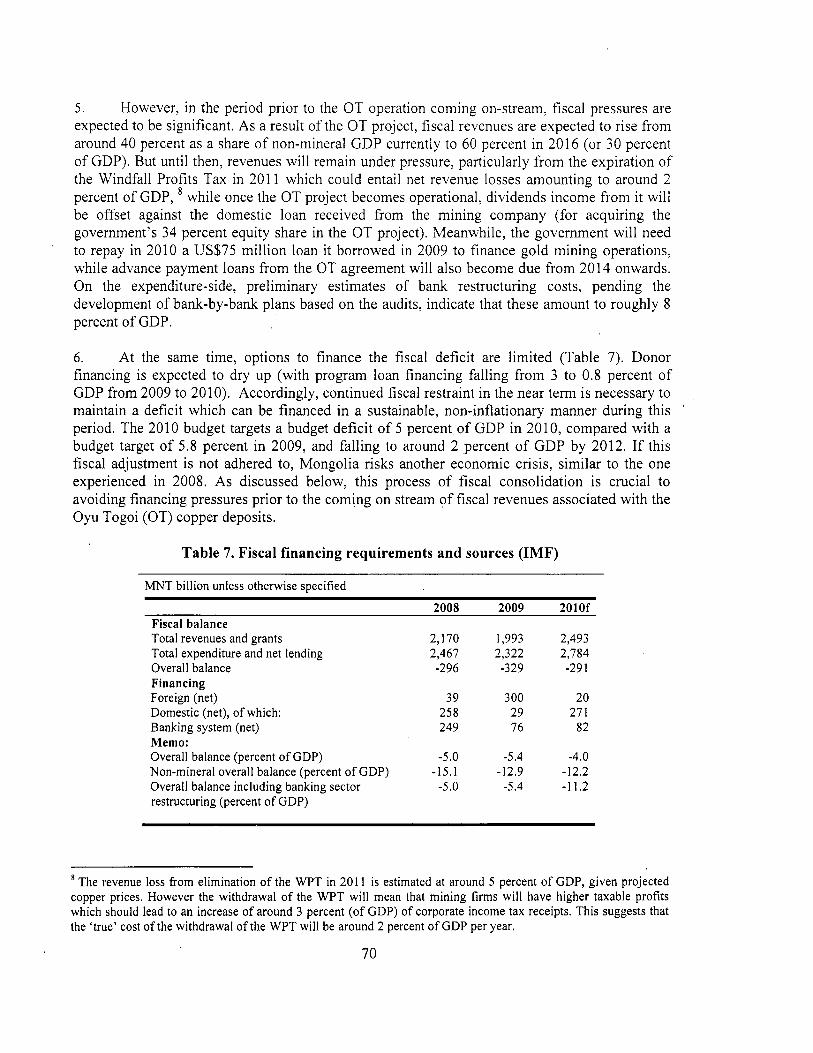

INTERNATIONAL DEVELOPMENT ASSOCIATION

PROJECT APPRAISAL DOCUMENT

FOR A PROPOSED CREDIT

IN THE AMOUNT OF SDR 8 MILLION (US$12 MILLION EQUIVALENT)

INCLUDING SDR 4.8 MILLION (US$7.2 MILLION EQUIVALENT)

IN PILOT CRISIS RESPONSE WINDOW RESOURCES

TO

MONGOLIA

FOR A MULTI-SECTORAL TECHNICAL ASSISTANCE PROJECT

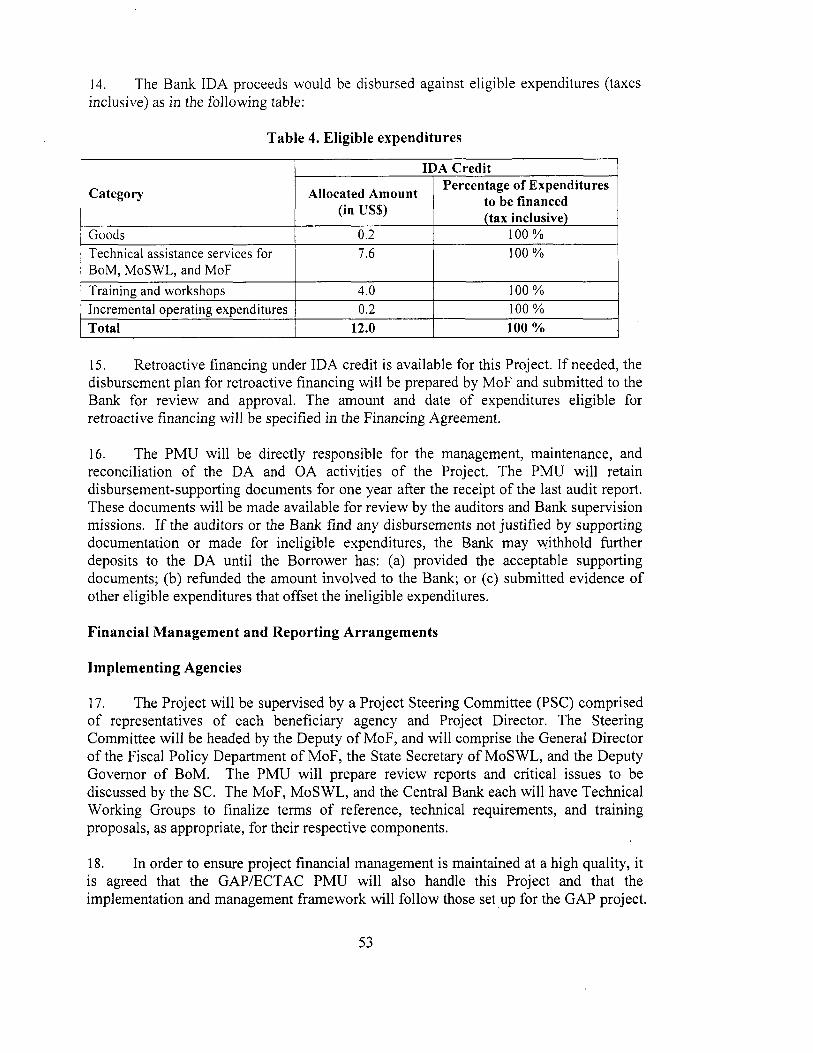

June 9,20 10

Poverty Reduction and Economic Management Department East Asia and Pacific Region

This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

MONGOLIA - GOVERNMENT FISCAL YEAR January 1 - December 3 1

CURRENCY EQUIVALENTS (Exchange Rate Effective as of March 3 1,201 0)

Currency Unit = Mongolian Tugrug US$I.OO = MNT1367

WEIGHTS AND MEASURES Metric System

Vice President: Country Director: Klaus Rohland, EACCF

Sector Director: Vikram Nehru, EASPR Country Manager: Arshad Sayed, EACMF

James W. Adams, EAPVP

Task Team Leader: Rogier van den Brink, EASPR

FOR OFFICIAL USE ONLY

ABBREVIATIONS AND ACRONYMS

AAA ADB Aimag BoM BP CFAA

CMP CPI

CPS CRW DA DCA DPC EBRD ECTAC

EITI

ESF FDI FMM FMSB FRC FSC GAP GFMlS

GDP

GoM GPF HDF IBL

IBRD

IDA IFAD

IFC IF1 IFR IMF ISN ISDS

Analytic and Advisory Services Asian Development Bank Province Bank of Mongolia Bank Procedures Country Financial Accountability Assessment Child Money Program Consumer Price Index

Country Partnership Strategy Crisis Response Window Designated Account Development Credit Agreement Development Policy Credit European Development Bank Economic Capacity and Technical Assistance Project Extractive Industries Transparency Initiative Exogenous Shock Facility Foreign Direct Investment Financial Management Manual Financial Management Sector Board Financial Regulatory Commission Financial Stability Council Governance Assistance Project Government Financial Management Information System Gross Domestic Product

Government of Mongolia Governance Partnership Facility Human Development Fund Integrated Budget Law

International Bank for Reconstruction and Development International Development Association International Fund for Agricultural Development International Finance Corporation International Financial Institution 1nterim.Financial Report International Monetary Fund Interim Strategy Note Integrated Safeguard Data Sheet

JlCA LSWSO MoF MoSWL MP MTAP

MTFF MTR

NDlC NPL OA OP OT PAD PCN

PEMFR

PIC PID PIP PMT PMU PPP PRGF PRSC

PSMFL

QBS QCBS OP ROSC

SBA

SBM SDR

SOE Soum TA TTL USAID WPT

Japan International Cooperation Agency Labor and Social Welfare Services Office Ministry of Finance Ministry of Social Welfare and Labor Member of Parliament Multi-sectoral Technical Assistance Project

Medium-Term Fiscal Framework Mid-Term Review National Development and Innovation Committee Non-performing Loan Operating Account Operations Policy Oyu Tolgoi Project Appraisal Document Project Concept Note

Public Expenditure and Financial Management Review Public Information Center Project Information Document Public Investment Program Proxy-means Test Project Management Unit Public-Private Partnership Poverty Reduction and Growth Facility Poverty Reduction Support Credit

Public Sector and Management of Finance Law Quality-Based Selection Quality and Cost-Based Selection Operations Policy Reports on the Observance of Standards and Codes Stand-By Arrangement

State Bank of Mongolia Special Drawing Rights

Statement of Expenditure District Technical Assistance Task Team Leader United States Agency for International Development Windfall Profit Tax

This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not be otherwise disclosed without World Bank authorization.

I . A . B . C .

I1 . A . B . C . D .

I11 . A . B . C . D . E . F .

IV . A . B . C . D . E . F . G .

MONGOLIA

MULTI-SECTORAL TECHNICAL ASSISTANCE PROJECT

TABLE OF CONTENTS

STRATEGIC CONTEXT AND RATIONALE .................................................. 1

Rationale for Bank involvement ............................................................................. 2 Higher level objectives to which the project contributes ........................................ 4

PROJECT DESCRIPTION ......................................................... 1 ........................ 4 Lending instrument ................................................................................................. 4 Project development objective and key indicators .................................................. 5 Project components ................................................................................................. 5 Lessons learned and reflected in the project design ................................................ 7

Partnership arrangements., ...................................................................................... 8 Institutional and implementation arrangements ...................................................... 9 Monitoring and evaluation of outcomes/results ...................................................... 9 Sustainability ......................................................................................................... 10 Critical risks and possible controversial aspects ................................................... 10 Credit conditions and covenants ........................................................................... 12

APPRAISAL SUMMARY .................................................................................. 13 Economic and financial analyses .......................................................................... 13 Technical ............................................................................................................... 13 Fiduciary ....................................................... ....................................................... 13

Environment .......................................................................................................... 14 Safeguard policies ................................................................................................. 15

Policy Exceptions and Readiness .......................................................................... 15

Country and sector issues ........................................................................................ 1

IMPLEMENTATION ........................................................................................... 8

. . .

Social ..................................................................................................................... 14

Annexes Annex 1 Country and Sector Background ................................................................................... 16 Annex 2 Major Related Projects Financed by the Bank and/or other Agencies .......................... 33 Annex 3 Results Framework and Monitoring .............................................................................. 34 Annex 4: Detailed Project Description ......................................................................................... 39 Annex 5 : Project Costs ................................................................................................................... 45

Annex 7: Financial Management and Disbursement Arrangements ............................................ 48 Annex 8: Procurement Arrangements ........................................................................................... 59 Annex 9: Economic and Financial Analysis ................................................................................. 62

Annex 11: Project Preparation and Supervision ........................................................................... 66 Annex 12: Documents in the Project File ..................................................................................... 67 Annex 13: Mongolia Joint IMF/World Bank Debt Sustainability Analysis ................................. 68 Annex 14: Mongolia at a Glance .................................................................................................. 72 Annex 15: Key Economic Indicators ............................................................................................ 75 Annex 16: List of References ........................................................ : .............................................. 76

Annex 6: Implementation Arrangements ...................................................................................... 46

Annex 10: Safeguard Policy Issues ............................................................................................... 63

Map IBRD 36948

Figures Figure 1 . Export concentration index* (right axis. bar). copper share in exports in 2007 (left axis.

17 Figure 2 . Changes in GDP growth 2008 to 2009 and non-mining fiscal balance in 2008 ........... 17 line) ...............................................................................................................................................

Figure 3 . Deteriorating fiscal balances ......................................................................................... 17 Figure 4 . Variable current account adjustments ........................................................................... 18

Figure 6: Recent macro-economic developments in Mongolia .................................................... 20 Figure 7 . Capital expenditures have expanded rapidly ................................................................. 24 Figure 8 . Parliament’s additions to the Public Investment Plan ................................................... 25

Figure 5 . Rising CPI inflation ....................................................................................................... 18

Figure 9 . Expenditures on capital repairs have been under-prioritized ........................................ 27 Figure 10 . Implementation arrangements for Multi-Sectoral TA Project ..................................... 47

Tables Table 1 . Selected policy actions through 20 10 and their expected impact ..................................... 2 Table 2 . Critical risks and possible controversial aspects ............................................................. 11 Table 3 . Mongolia selected economic indicators .......................................................................... 19 Table 4 . Eligible expenditures ...................................................................................................... 53

Table 7 . Fiscal financing requirements and sources (IMF) .......................................................... 70

Table 5 . Medium-term baseline projection ................................................................................... 69 Table 6 . Balance of payments outlook .......................................................................................... 69

Boxes Box 1 . How did other copper exporters experience the global downturn? ................................... 17

CREDIT AND PROJECT SUMMARY

Source BORROWEWRECIPIENT

Total: International Development Association (IDA)

MONGOLIA: MULTI-SECTORAL TECHNICAL ASSISTANCE PROJECT

Local Foreign Total 0.0 0.0 0.0 8.0 4.0 12.0 8.0 4.0 12.0

FY 2011 Annual 1 .o Cumulative 1 .O

2012 2013 2014 2015 3.0 3.0 3 .O 2.0 4.0 7.0 10.0 12.0

Project implementation period: Start July 1,2010 End: June 30, 2014 Expected effectiveness date: December 3 1,20 10 ExDected closing date: December 3 1. 2014

[ ]Yes [XINO

[ ]Yes [XINO [ ]Yes [XINO [ ]Yes [XINO

[XIYes [ ] No

Does the project depart from the CAS in content or other significant respects? Ref: PAD I. C. Does the project require any exceptions from Ban,k policies? Ref: PAD IK G. Have these been approved by Bank management? Is approval for any policy exception sought from the Board?

Does the project include any critical risks rated “substantial” or “high”? Ref: PAD III.E.

[XIYes [ ] N o Does the project meet the Regional criteria for readiness for implementation? Ref: PAD IK G. Project development objectives Ref: PAD II. C., Teclznical Annex 3 The Project’s development objectives are to support the Recipient’s efforts to enhance its capacity for policy making, regulation, and implementation in the fiscal, social, and financial sectors.

Project description Ref: PAD II.D., Teclinical Annex 4 The Project will provide technical assistance under four components as follows: (a) Enhancing capacity for fiscal management in the Ministry of Finance to better implement a budget that is

fiscallv sustainable and better linked to national. local, and sectoral Driorities.

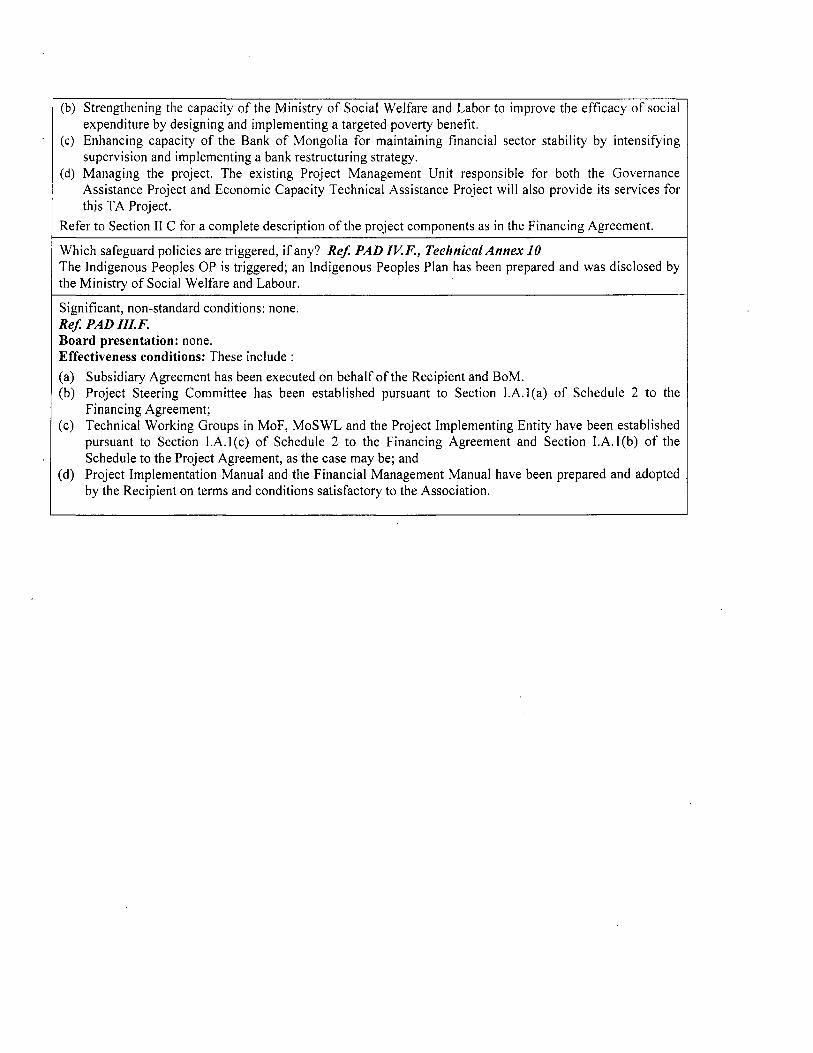

(b) Strengthening the capacity of the Ministry of Social Welfare and Labor to improve the efficacy of social expenditure by designing and implementing a targeted poverty benefit.

(c) Enhancing capacity of the Bank of Mongolia for maintaining financial sector stability by intensifying supervision and implementing a bank restructuring strategy.

(d) Managing the project. The existing Project Management Unit responsible for both the Governance Assistance Project and Economic Capacity Technical Assistance Project will also provide its services for this TA Project.

Refer to Section I1 C for a complete description of the project components as in the Financing Agreement.

Which safeguard policies are triggered, if any? Ref; PAD IKF., Teeknicnl Annex 10 The Indigenous Peoples OP is triggered; an Indigenous Peoples Plan has been prepared and was disclosed by the Ministry of Social Welfare and Labour.

Significant, non-standard conditions: none. Ref; PAD III. F. Board presentation: none. Effectiveness conditions: These include : (a) Subsidiary Agreement has been executed on behalf of the Recipient and BoM. (b) Project Steering Committee has been established pursuant to Section I.A.l(a) of Schedule 2 to the

Financing Agreement; (c) Technical Working Groups in MoF, MoSWL and the Project Implementing Entity have been established

pursuant to Section I.A.l(c) of Schedule 2 to the Financing Agreement and Section I.A.l(b) of the Scheduk to the Project Agreement, as the case may be; and

(d) Project Implementation Manual and the Financial Management Manual have been prepared and adopted by the Recipient on terms and conditions satisfactory to the Association.

IDA PROJECT DOCUMENT FOR A PROPOSED MULTI-SECTORAL TECHNICAL ASSISTANCE PROJECT

TO MONGOLIA

I. STRATEGIC CONTEXT AND RATIONALE A. Country and sector issues

1. The global downturn has hit Mongolia hard, most immediately through the collapse of mineral prices, in particular that of copper. Reliance on copper revenues in the budget (with mineral revenues accounting for more than one-third of the total budget revenues), the fiscal shock has been very large, causing the overall government balance to shift from a 2.9 percent of Gross Domestic Product (GDP) surplus in 2007 to a 5.4 percent deficit in 2009. Similarly, the external balance swung from a surplus into a deficit, as export proceeds fell by one quarter (about US$640 million) in 2009. And inflation, which had peaked at 34 percent in August of 2008, fueled by large increases in domestic spending, loose monetary policies and a de facto fixed exchange rate, turned negative for a brief period in the latter half of 2009, as the economy contracted sharply. Real GDP contracted by 1.6 percent in 2009, following growth of 8.9 percent in 2008.

2. The sudden economic downturn exposed the over-reliance of the budget on mineral revenues, causing the fiscal situation to become precarious. The downturn also exposed weaknesses in an overheated banking sector, eventually leading to two systemically important banks being placed into receivership, and a loss of confidence, as demonstrated by declining local currency deposits in late 2008 and early 2009. There has, however, been stabilization in the economic situation since the time of Board approval of the first DPC operation in June 2009.

3. Improving the policy environment is now the overriding priority for the government. Multilateral and bilateral donor activities in the form of budget support, technical assistance, and analytical work provide an important support for the government’s policy agenda. Considerable fiscal adjustment remains necessary over the next couple of years. Donor budget financing can play a crucial role in facilitating the process of fiscal adjustment, helping to protect key expenditures such as social protection and investment programs and limiting recourse to alternative, potentially destabilizing, financing options.

4. This Multi-Sectoral Technical Assistance Project (MTAP) of US$12 million is supporting, and is being processed together with, the second Development Policy Credit (DPC2) of US$30 million, following the US$40 million DPC 1 disbursed in 2009. The two DPCs support policy actions targeted towards the key crisis areas -- fiscal policy and management, social protection, and the financial sector -- as well as the mining sector, which is expected to lead the recovery. A follow-up series of three DPCs is planned to assist in the implementation of the medium-term policy agenda.

5. This MTAP is designed to improve fiscal policy and sustainability in a mineral-based economy, protect the poor and vulnerable, and restore confidence in the financial sector. Project activities include: (i) improving budget preparation and execution to ensure that resources are planned and spent in a sustainable, efficient, and transparent manner; (ii) protecting the poor by

retargeting existing social policies; and (iii) strengthening confidence in the financial sector by implementing best practice action plans for the resolution of the two failed banks and a wider banking sector restructuring strategy.

B. Rationale for Bank involvement

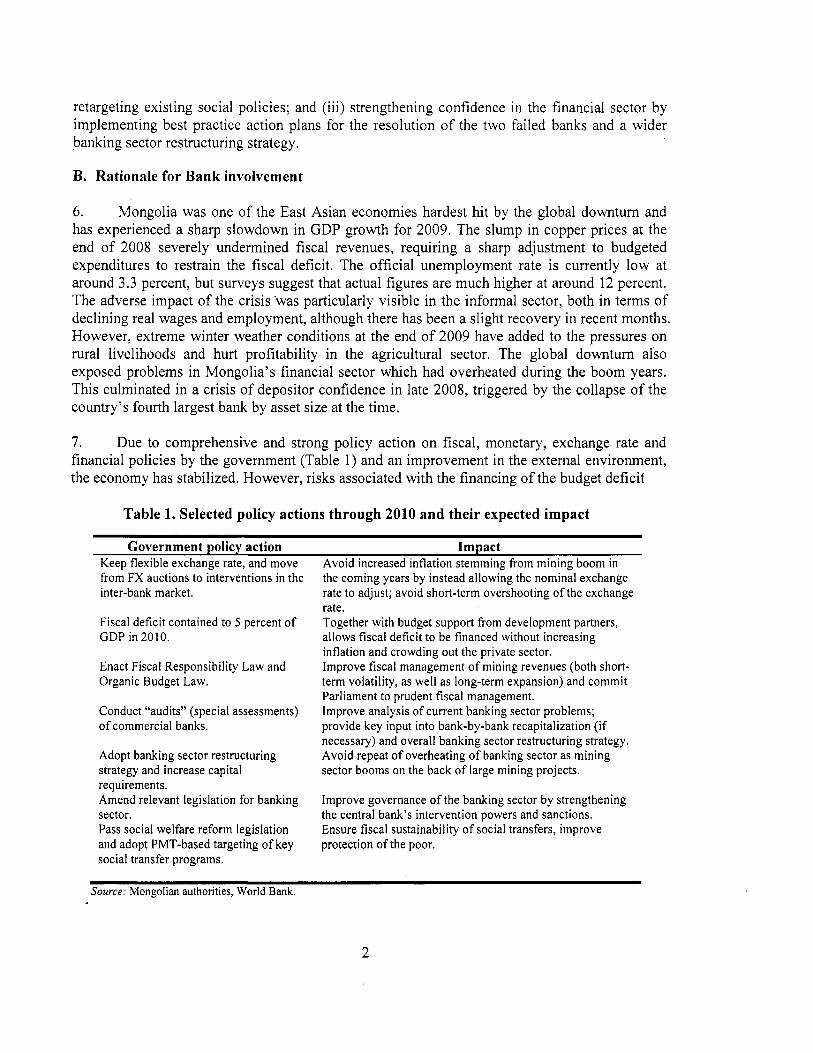

6. Mongolia was one of the East Asian economies hardest hit by the global downturn and has experienced a sharp slowdown in GDP growth for 2009. The slump in copper prices at the end of 2008 severely undermined fiscal revenues, requiring a sharp adjustment to budgeted expenditures to restrain the fiscal deficit. The official unemployment rate is currently low at around 3.3 percent, but surveys suggest that actual figures are much higher at around 12 percent. The adverse impact of the crisis ‘was particularly visible in the informal sector, both in terms of declining real wages and employment, although there has been a slight recovery in recent months. However, extreme winter weather conditions at the end of 2009 have added to the pressures on rural livelihoods and hurt profitability in the agricultural sector. The global downturn also exposed problems in Mongolia’s financial sector which had overheated during the boom years. This culminated in a crisis of depositor confidence in late 2008, triggered by the collapse of the country’s fourth largest bank by asset size at the time.

7. Due to comprehensive and strong policy action on fiscal, monetary, exchange rate and financial policies by the government (Table 1) and an improvement in the external environment, the economy has stabilized. However, risks associated with the financing of the budget deficif

Table 1. Selected policy actions through 2010 and their expected impact

Government policy action Impact Avoid increased inflation stemming from mining boom in Keep flexible exchange rate, and move

from FX auctions to interventions in the inter-bank market.

Fiscal deficit contained to 5 percent of GDP in 2010.

Enact Fiscal Responsibility Law and Organic Budget Law.

Conduct “audits” (special assessments) of commercial banks.

Adopt banking sector restructuring strategy and increase capital requirements. Amend relevant legislation for banking sector. Pass social welfare reform legislation and adopt PMT-based targeting of key social transfer programs.

the coming years by instead allowing the nominal exchange rate to adjust; avoid short-term overshooting of the exchange rate. Together with budget support from development partners, allows fiscal deficit to be financed without increasing inflation and crowding out the private sector. lmprove fiscal management of mining revenues (both short- term volatility, as well as long-term expansion) and commit Parliament to prudent fiscal management. lmprove analysis of current banking sector problems; provide key input into bank-by-bank recapitalization (if necessary) and overall banking sector restructuring strategy. Avoid repeat of overheating of banking sector as mining sector booms on the back of large mining projects.

Improve governance of the banking sector by strengthening the central bank’s intervention powers and sanctions. Ensure fiscal sustainability of social transfers, improve protection of the poor.

Source: Mongolian authorities, World Bank.

2

and the weak balance sheets in the banking sector remain (as evidenced by the failure of a second bank at the end of 2009), and the recovery in economic activity is at an early stage. The outlook, moreover, fundamentally depends on the degree of progress in a small number of major investment projects, in particular the Oyu Tolgoi (OT) investment agreement, and on whether the recovery in copper prices in recent months can be sustained. Any shock could therefore derail this nascent recovery.

8. The rationale behind the Bank’s involvement derives from the specific role the Bank has played in assisting the government in responding to the crisis, and its comparative advantage going forward. First, the Bank’s assistance strategy (as described in the Interim Strategy Note (ISN) of June 2009) exceptionally reallocated two-thirds of the IDA envelope to supporting policy reforms in key areas. International, as well as Mongolian experience, strongly suggests that the success and sustainability of these reforms is enhanced if they are accompanied by technical assistance and targeted capacity-building. This Multi-Sectoral TA Project (MTAP) therefore becomes a key pillar of the Bank’s assistance strategy.

9. Second, the two single-tranche DPCs (US$40 million in FYlO and US$30 million in FY 1 l), representing more than two-thirds of the notional IDA 15 envelope of US$90 million, both supported reforms in four critical areas: improving fiscal sustainability in a mineral-based economy, protecting the poor and vulnerable, restoring confidence in the financial sector, and encouraging transparent and prudent mining investments. Three out these four policy reform areas are covered in this MTAP. The fourth -- covering the mining sector -- is the focus of an already existing mining TA project and is not expected to need additional resources in the next few years.

10. Third, the three policy areas covered by this MTAP benefit from a rich portfolio of past and present Bank Analytic and Advisory (AAA) work. The TA Project draws from the same wealth of resources that was available for the first and second DPC on fiscal policy and management, social protection, and financial sector reform.

1 1. The fiscal policy and management agenda is underpinned by the 2009 World Bank Public Expenditure and Financial Management Review, the 2008 World Bank Governance Assessment Report, the 2008 ROSC Accounting and Auditing Report, a series of studies on improving medium-term program budgeting undertaken under an existing TA project (the ECTAC project), the 2008 IMF report on “Budget Preparation: A Roadmap for Institutional Strengthening”, the 2007 World Bank report “Foundation for Sustainable Development: Rethinking the Delivery of Infrastructure Services in Mongolia”, the ongoing Mongolia Policy Note of Public Investment Planning, and a draft report titled: “Challenges in Public Investment in a Resource Rich Country: A Political Economy Perspective.” These studies highlight the weaknesses in the budget formulation and public investment planning processes in Mongolia, including the political preference for funding new investments over maintaining the existing capital stock, leading to the chronic underfunding of maintenance; the significant discretion of Parliament to add new projects to the public investment plan without a formal appraisal process, including feasibility studies; and the institutional weaknesses and poor procedures throughout the project cycle. All these studies informed the fiscal prior actions on capital budgeting and maintenance. Other analytical work is addressing related issues in the broader agenda on improving fiscal

3

expenditure performance, for example a World Bank report on “Mongolia: Towards a High Performing Civil Service” published in June 2009.

12. Reforms in social protection are buttressed by the following studies: the 2009 World Bank Public Expenditure and Financial Management Review, the “Assessment of the Child Money Program and properties of its targeting methodology,” (Araujo, 2006), and “The making of a Modern Social Assistance System in Mongolia” (Ridao-Can0 and Cristobal, 2007).

13. Financial sector reforms draw on the 2008 World Bank-IMF Financial Sector Assessment Report, and more recent World Bank reviews and assessments of the banking sector and recent developments (undertaken in 2008 and 2009). The data for these studies will be updated but both the medium-term and long-term objectives of the studies that support the policy actions remain unchanged.

14. Finally, the three policy areas selected by this TA also reflect the Bank’s comparative advantage vis-a-vis the other development partners. On the fiscal side, the collaboration with the authorities and the IMF is very strong, and joint teams are working on the key policy issues together. Two existing Bank TA projects proved to be invaluable to support these efforts. The MTAP is designed to allow the Bank to continue its role in this collaboration. Similarly, with respect to social protection, the partnership between the government, the ADB, and the Bank is also strong, with the Bank being asked to help with the design and implementation of a targeted poverty benefit, given its comparative advantage in this area. And thirdly, the Bank is playing a leading role in the multi-donor partnership in the resolution of failed banks and in the design and implementation of the banking sector restructuring. The TA component of an existing project played a critical role in this. The MTAP will ensure the Bank’s continued engagement in these areas.

C. Higher level objectives to which the project contributes

15. Major mineral deposits, including prospects in the Gobi region, when developed, have the potential to significantly increase incomes and government revenues. But the risks of a mineral-dependent economy have also been underscored by deficiencies in Mongolia’s management of the recent boom, which made it more difficult to adjust to the impact of the global downturn. In addition, as in most mineral-rich economies, managing the resource revenues consistently and sustainably, puts a high premium on governance reforms. The adjustments needed will take place over the medium term, and include enhancing government capacities to improve public investment decisions, protect the poor, restructure the banking sector, and resolve key obstacles for mining and infrastructure development.

16. This TA Project supports key elements of the reform agenda in the above areas.

11. PROJECT DESCRIPTION A. Lending instrument

17. This Project will be an IDA Technical Assistance Credit in the amount equivalent to US$12 million. The project duration will be four years. The Project is aligned with the companion DPC2 operation as well as planned to support a Development Policy Credit series, to

4

improve capacity for fiscal policy formulation, social protection, and the management of the financial sector.

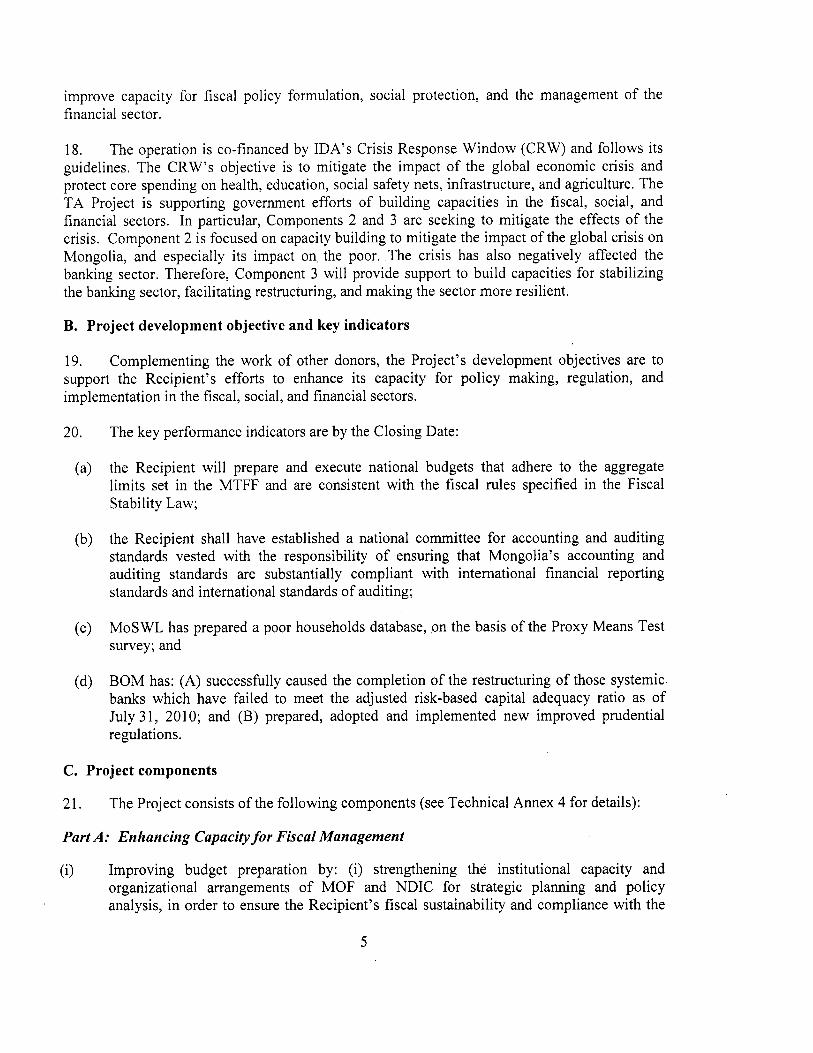

18. The operation is co-financed by IDA’S Crisis Response Window (CRW) and follows its guidelines. The CRW’s objective is to mitigate the impact of the global economic crisis and protect core spending on health, education, social safety nets, infrastructure, and agriculture. The TA Project is supporting government efforts of building capacities in the fiscal, social, and financial sectors. In particular, Components 2 and 3 are seeking to mitigate the effects of the crisis. Component 2 is focused on capacity building to mitigate the impact of the global crisis on Mongolia, and especially its impact on the poor. The crisis has also negatively affected the banking sector. Therefore, Component 3 will provide support to build capacities for stabilizing the banking sector, facilitating restructuring, and making the sector more resilient.

B. Project development objective and key indicators

19. Complementing the work of other donors, the Project’s development objectives are to support the Recipient’s efforts to enhance its capacity for policy making, regulation, and implementation in the fiscal, social, and financial sectors.

20. The key performance indicators are by the Closing Date:

(a) the Recipient will prepare and execute national budgets that adhere to the aggregate limits set in the MTFF and are consistent with the fiscal rules specified in the Fiscal Stability Law;

(b) the Recipient shall have established a national committee for accounting and auditing standards vested with the responsibility of ensuring that Mongolia’s accounting and auditing standards are substantially compliant with international financial reporting standards and international standards of auditing;

(c) MoSWL has prepared a poor households database, ,on the basis of the Proxy Means Test survey; and

(d) BOM has: (A) successfully caused the completion of the restructuring of those systemic banks which have failed to meet the adjusted risk-based capital adequacy ratio as of July 3 1 , 201 0; and (B) prepared, adopted and implemented new improved prudential regulations.

C. Project components

21. The Project consists of the following components (see Technical Annex 4 for details):

Part A: Enhancing Capacity for Fiscal Management

(i) Improving budget preparation by: (i) strengthening the institutional capacity and organizational arrangements of MOF and NDIC for strategic planning and policy analysis, in order to ensure the Recipient’s fiscal sustainability and compliance with the

5

Fiscal Stability Law; (ii) aligning the budgeting process to national, sectoral and local priorities, through the adoption of greater decentralization policies, and enhancing transparency and predictability in the apportionment, transfer and management of revenues and expenditures; (iii) improving inter-sectoral coordination; and (iv) improving public investment planning.

(ii) Improving the public financial management by: (i) revising and strengthening the existing legal framework for accounting and auditing; (ii) strengthening MOF’s and the Financial Regulatory Committee’s institutional capacity to ensure ’ compliance with international financial reporting standards and international standards on auditing; and (iii) strengthening MOF’s internal controls by improving its internal auditing capacity; and (iv) improving accounting and auditing professional education and training.

Part B: Supporting Government Efforts to Better Protect the Poor

Designing and piloting the implementation of a social benefit program for the provision of cash transfers to the poor households, including the determination of the amount of the benefits, frequency of transfers and/or any conditions attached thereto, and eventually devising the final structure of a permanent program.

Supporting the piloting and national roll-out of the Proxy Means Test targeting system for determining the eligibility of beneficiaries of the social benefit program, including, inter alia: (i) strengthening MoSWL’s and LSWSO’s capacity to develop and manage a social program beneficiaries database; (ii) developing and implementing a grievance redressal and appeals mechanism for social welfare programs, and a related information and communication campaign; (iii) strengthening the institutional and governance structures of MoSWL, LSWSO, MoECS, and MoH in order to improve their efficiency in the provision of welfare services; and (iv) developing and implementing an information, education and communication strategy regarding social welfare entitlements.

Monitoring and evaluating the cash transfer program performance by setting up a system of program audits and social accountability aimed at enhancing the program’s transparency in the allocation and payment of benefits, and assessing the impact of the reformed welfare system on the Recipient’s poverty rates and human development outcomes

Providing training to MoSWL’s and LSWSO’s staff for the implementation of the social welfare reform system, including the development and distribution of printed materialheference guides therefor, in order to ensure that social benefits are successfully delivered to the poor and vulnerable population.

Part C: Enhancing Capacity for Maintaining the Stability of the Financial Sector

(i) Strengthening the institutional capacity of BOM in order to: (i) finalize the liquidation of assets of the failed banks under the BOM’s receivership; (ii) finalize, adopt and implement a bank restructuring . strategy, including the effective operation and privatization of the State Bank of Mongolia; (iii) develop and implement a corporate debt restructuring in the mining and construction sectors; (iv) carry out targeted forensic audits

6

of financial institutions; and (v) provide on-the-job training to BOM’s staff in the above areas.

(ii) Supporting the implementation of the amended Central Bank Law and the new Banking Law by: (i) developing and adopting new financial reporting regimes for commercial banks; (ii) revising and streamlining existing bank regulations; (iii) strengthening BOM’s off-site supervision capabilities; and (iv) transitioning from a blanket deposit guarantee to a limited deposit insurance regime.

(iii) Strengthening BOM’ s human capital through: (i) developing regular training curricula for financial sector supervisors; and (ii) carrying out study tours and attending and/or hosting conferences and workshops.

Part D: Project Management

(i) Strengthening MOF’ s capacity for Project implementation, monitoring and evaluation, including, inter alia, audit arrangements, reporting requirements, procurement, disbursement and financial management activities.

D. Lessons learned and reflected in the project design

22. A number of important lessons have been learned by the implementation of past Bank projects as well as those of donor partners. The design of this operation draws on, and benefits from, these lessons:

Supporting the main policy areas with appropriate TA is important for the success and sustainability of critical policy reforms. This lesson from experience is drawn from both international, as well as Mongolian experience. For instance, the 2009 DPC benefited greatly from the work that had been undertaken under existing TA projects. The design of this Multi-Sectoral TA Project (MTAP) reflects this lesson. The four critical policy reform areas supported by the Bank each benefit from TA support. The MTAP supports three out of the four areas. The fourth (mining) was only excluded because it already benefited from a relatively recent TA project. If the crisis is to be turned into an opportunity, it is important to build targeted capacity to move from policy actions which quickly responded to the crisis to policy actions which build on the crisis response and constitute a medium-term agenda. In this regard, it is important to gauge from the beginning of an operation the capacity of the borrower or the implementing agency to implement the proposed reforms. The capacity of the borrower was sufficient enough to take the strong, and often painful, policy actions supported by the 2009 DPC when this was required. However, the more complicated reforms that are needed, for instance on social protection, will require developing more capacity. Similarly, as the weaknesses in the banking sector have turned out to be more severe than expected, additional capacity-building for banking sector supervision and restructuring is needed. The MTAP therefore includes targeted capacity building (including training) in each of the policy areas as one of its key activities. Donor coordination is key to avoid overlap and duplication. The intensive coordination necessitated by the crisis of 2009 resulted in a close collaboration between the donors.

7

The TA credit builds on the practical experience gained during this period in terms of joint work and the optimal division of labor in the Mongolian context. The selection of activities supported under this TA reflects that experience and understanding. The design of the MTAP needs to be selective and focused on the critical policy reforms, but flexible enough to accommodate the emerging policy agenda. This is particularly important in the case of Mongolia, where there is no clearly and explicitly defined policy agenda. Ownership is central to the success of the policy reform agenda. To gauge the existing ownership and strengthen it, the preparations for this Project (and the DPC series in general) have benefited from intensive dialogue with government, Parliament, the private sector, and academia. These consultations ranged from successful study tours to Chile and Washington, D.C. by members of Parliament, and targeted conferences and workshops, to increasing the frequency of the Bank’s Economic Updates from quarterly to monthly, seeking regular stakeholder input into these updates, and organizing public dissemination events.

E. Alternatives considered and reasons for rejection

23. An alternative of three single-sector TAs, one each for fiscal policy, social protection, and the banking sector was considered. Each single sector TA would have supported the policy reform in the DPC series. This was rejected in favor of a combined TA to increase efficiency, coordination, and to minimize transaction costs of three projects going to the Board at the same time. 24. A second alternative was to rely on other development partners to provide the technical assistance required. The close collaboration between the development partners during the crisis response provided a clear demonstration of “revealed” comparative advantage. The activities selected for this TA credit reflect the existing division of labor between the development partners and the existing gaps in the existing and planned TA support by other development partners.

’

111. IMPLEMENTATION A. Partnership arrangements

25. IDA’S catalytic platform services played a critical role in the development of the overall support program of the government’s policy reform agenda (balance of payments support, budget support, and technical assistance) by the development partners and its coordination. They included convening two donor meetings in 2009, in addition to the analytical work and advisory services described in Annex 1 (also see Annex 16 for references). This facilitation is a critical aspect of the effective and efficient use of the Crisis Response Window, which co-finances this operation.

26. This TA Project is funded by IDA. However, bilateral, parallel grant funding is being sought to complement this Project. As mentioned above, the partnership arrangements with the IMF on fiscal policy issues, with the ADB on social protection, and with the IMF, the ADB, USAID, and the EBRD on the financial sector, are the result of intensive collaboration and coordination during the crisis period and are reflected in the design of this TA Project. A list of ,

8

major related projects financed by the World Bank and/or other Agencies in these areas is included in Annex 2. B. Institutional and implementation arrangements

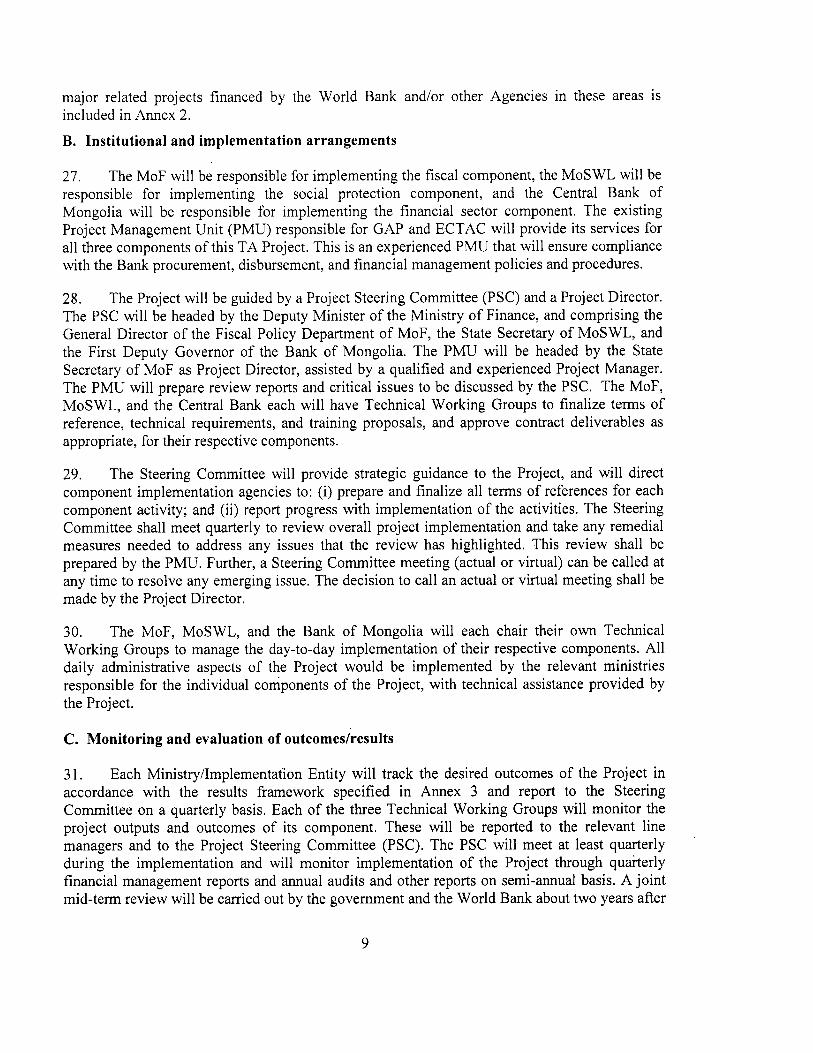

27. The MoF will be responsible for implementing the fiscal component, the MoSWL will be responsible for implementing the social protection component, and the Central Bank of Mongolia will be responsible for implementing the financial sector component. The existing Project Management Unit (PMU) responsible for GAP and ECTAC will provide its services for all three components of this TA Project, This is an experienced PMU that will ensure compliance with the Bank procurement, disbursement, and financial management policies and procedures.

28. The Project will be guided by a Project Steering Committee (PSC) and a Project Director. The PSC will be headed by the Deputy Minister of the Ministry of Finance, and comprising the General Director of the Fiscal Policy Department of MoF, the State Secretary of MoSWL, and the First Deputy Governor of the Bank of Mongolia. The PMU will be headed by the State Secretary of MoF as Project Director, assisted by a qualified and experienced Project Manager. The PMU will prepare review reports and critical issues to be discussed by the PSC. The MoF, MoSWL, and the Central Bank each will have Technical Working Groups to finalize terms of reference, technical requirements, and training proposals, and approve contract deliverables as appropriate, for their respective components.

29. The Steering Committee will provide strategic guidance to the Project, and will direct component implementation agencies to: (i) prepare and finalize all terms of references for each component activity; and (ii) report progress with implementation of the activities. The Steering Committee shall meet quarterly to review overall project implementation and take any remedial measures needed to address any issues that the review has highlighted. This review shall be prepared by the PMU. Further, a Steering Committee meeting (actual or virtual) can be called at any time to resolve any emerging issue. The decision to call an actual or virtual meeting shall be made by the Project Director.

30. The MoF, MoSWL, and the Bank of Mongolia will each chair their own Technical Working Groups to manage the day-to-day implementation of their respective components. All daily administrative aspects of the Project would be implemented by the relevant ministries responsible for the individual components of the Project, with technical assistance provided by the Project.

C. Monitoring and evaluation of outcomes/results

31. Each Ministry/Implementation Entity will track the desired outcomes of the Project in accordance with the results framework specified in Annex 3 and report to the Steering Committee on a quarterly basis. Each of the three Technical Working Groups will monitor the project outputs and outcomes of its component. These will be reported to the relevant line managers and to the Project Steering Committee (PSC). The PSC will meet at least quarterly during the implementation and will monitor implementation of the Project through quarterly financial management reports and annual audits and other reports on semi-annual basis. A joint mid-term review will be carried out by the government and the World Bank about two years after

9

the Project becomes effective (FY2011-12). This will provide an in-depth assessment of progress towards desired project outcomes and will recommend measures to reorient the project, if needed, to ensure that it will achieve its objectives. Two months before the Project closing date, the Steering Committee team will prepare and provide to IDA a report on the execution of the project, its costs and the current and future benefits to be derived from it, to be attached to IDA?S Implementation Completion Report (ICR) in accordance with IDA guidelines.

32. A set of indicators defined in Annex 3 will be used to develop a monitoring baseline and for regular project monitoring. These indicators will be supplemented by information from other sources, including an independent assessment, audits of management, staff, facilities, human resource training, and records.

D. Sustainability

33. The government has taken strong policy actions over 2009 which have required bipartisan support and whi?ch demonstrate the currently strong political ownership of the reforms needed to address the impact of the crisis, to promote the recovery, and to put in place an improved policy framework for the medium-term. And the design of this operation has benefited from systematic dialogue with key government officials and representatives of both political parties. In addition, a series of outreach and consultation events to discuss key policy issues, along with the release of the regular economic updates, further helped raise awareness and ownership during project design. Endorsement from the MoF, MoSWL, and Central Bank of Mongolia is also an indicator of strong ownership.

34. Sustainability is further strengthened by the supporting policy framework currently provided by the IMF/ADB/JICA balance of payments and budget support operations to assist the government manage the crisis. A planned series of DPCs would ensure a continuation of such a mutually reinforcing link between policy conditionality and TA.

35. Targeted institutional capacity-building and training to be provided as part of this TA project will also improve the sustainability of the project by further deepening the institutional commitment and implementation capacity to the reform agenda.

36. Finally, this TA Project does not create any additional burden on government finances. On the contrary, the key actions in each of the components are targeted to generating cost- savings and efficiencies.

E. Critical risks and possible controversial aspects

37. Potential risks to the TA Project and the mitigating measures are identified in Table 2.

10

Table 2. Critical risks and possible controversial aspects

Rating of risk Description of risk Risk factors

Rating of residual

risk Mitigation measures

1. Country and/(

Adoption of new Organic Budget Law (IMF conditionality).

11. Strengthening Substantial

111. Social Protect

Prior action of the DPCs, Bank's analytical work and on-going technical assistance highlight this risk and explain the negative consequences. Intensive policy dialogue by all donors.

Sub-National Level Risks As the copper price revives, the perceived threat of imminent crisis recedes, and as the 20 12 elections draw nearer, political commitment to the reform process wanes.

Moderate

Moderate

Parliament does not approve government using a credit to finance TA, but insists on grant financing.

xal Policy and Public Financi; Continued politically motivated investment project selection, and lack of coordination between the Ministry of Finance and the NDIC on public investment planning due to bureaucratic rivalries Continued under- prioritization of capital '

maintenance due to low political visibility of these expenditures. Parliament failing to adopt the Fiscal Stability Law and the Organic Budget Law.

Substantial

Moderate

Management High

Substantial

Substantial

Adoption of prudent fiscal rules and macro management, anchored in a new legal framework (IMF performance criterion).

Agreement on DPC series.

Intensified IFI-supported outreach to policymakers, Parliament, academia, and civil society. Processing of DPC and TA as a package.

Obtaining commitment by other development partners to mobilize parallel financing.

Moderate

Low

Adoption of new social welfare reform law (conditionality of IMF, Failure to approve the

reformed Social Welfare

Lack of cauacitv within the

Ongoing technical assistance from ADB and World Bank.

Ministry oi. Social Welfare and Labor to design and implement the poverty

Moderate

Moderate

11

Failure to approve the Proxy Means Testing methodology by the National Statistical office.

Moderate Substantial DPC2 prior action.

Building up and High A sound and well-implemented maintaining political communication strategy targeted support, and managing various interest groups.

Weak capacity and busy work schedule. for weak capacity

directly at Parliament and the general public and carried out with support of international experts. Use of TA services to compensate

Training supported by the Project.

Substantial

Overall Risk Rating

F. Credit conditions and covenants

Substantial

Moderate

Moderate

Management approval conditions

38. None.

Effectiveness conditions

These include the :

Subsidiary Agreement has been executed on behalf of the Recipient and BoM;

Project Steering Committee has been established pursuant to Section I.A. l(a) of Schedule 2 to the Financing Agreement;

Technical Working Groups in MoF, MoSWL and BoM have been established pursuant to Section I.A.l(c) of Schedule 2 to the Financing Agreement and Section I.A.l(b) of the Schedule to the Project Agreement, as the case may be; and

Project Implementation Manual and the Financial Management Manual have been prepared and adopted by the Recipient on terms and conditions satisfactory to the Association.

Other Covenants 40. These include:

(a) Establishment and maintenance of the PSC and Technical Working Groups in MoF, MoLSW, and BoM, and the maintenance of the PMU established under the GAP within MoF;

(b) Preparation of annual implementation plans; and

12

(c) Screening of social sector activities in accordance with the Indigenous Peoples Planning Framework and the preparation, if necessary, of Indigenous Peoples Plan.

IV. APPRAISAL SUMMARY

A. Economic and financial analyses

41. The Project is not amenable to a cost-benefit analysis as the MoF, MoSWL, and Central Bank have hardly any significant cost recovery. The economic benefits from the Project will derive from two main sources. First, improvements in the efficiency of fiscal policy, social protection policy, and banking policy operations and agencies will result in a higher quality of policy formulation. Second, improved capacity will enhance decision-making, at policy, program, and project levels.

, 42. There can be a fiscal impact contributing to a better budgeting process and a potential increase in revenues due to better information and coverage.

B. Technical

43. not finance any works, a technical appraisal was not undertaken.

Since this operation is a technical assistance and capacity building operation, which does

C. Fiduciary

Financial Management Issues

44. The Financial Management team has conducted an assessment of the adequacy of the Project’s financial management system. The assessment, based on guidelines issued by Financial Management Sector Board on March 1, 20 10, has concluded that the Project meets the minimum Bank financial management requirements, as stipulated in BP/OP 10.02. In the FM team’s opinion, the Project will have financial management arrangements acceptable to the Bank and, as part of the overall arrangements that the borrower has in place for implementing the operation, provide reasonable assurance that the proceeds of the IDA credit will be used for the purposes for which they are provided. The main financial management risk is that World Bank credit proceeds will not be used for the purposes intended and is a combination of country-, sector-, and project-specific risk factors. Taking into account the risk mitigation measures proposed under the Project, a “moderate” FM risk rating was assigned to the Project at the appraisal stage.

Procurement Issues

45. Procurement for the Project would be carried out in accordance with the World Bank’s “Guidelines: Procurement Under IBRD Loans and IDA Credits” dated May 2004 (Revised October 2006); “Guidelines: Selection and Employment of Consultants by World Bank Borrowers” dated May 2004 (Revised October 2006), and the provisions stipulated in the Financing Agreement.

13

46. In accordance with the institutional arrangement, the PMU established for the on-going Bank-financed GAP and ECTAC projects would be responsible for project implementation. The procurement function rests with the same PMU. Based on the review of the capacity and experience of the PMU, technical support, and internal clearance procedures in general, the PMU is capable of managing procurement. The overall procurement risk is moderate.

47. An initial 12-month Procurement Plan was prepared and submitted to the Bank for clearance prior to credit negotiation and the format of the procurement monitoring report and procurement filing system was agreed.

48. The Project will be carried out in accordance with the provisions of the World Bank Guidelines on Preventing and Combating Fraud and Corruption in Projects Financed by IBRD Loans and IDA Credits and Grants, dated October 15, 2006.

D. Social

49. It is expected that the social protection component will lead to improved effectiveness of social services delivery to the population, in particular to the poor and vulnerable, through the implementation of a targeted poverty benefit. The fiscal policy component will improve fiscal sustainability and the efficiency of the public investment program. It would have an indirect, positive social impact. Stabilizing the financial sector would have a positive social impact by improving the access and efficient allocation of financial resources to clients, and minimizing the fiscal costs of future bank bailouts, if any. An Indigenous Peoples Planning Framework has been prepared and disclosed by the Ministry of Social Welfare and Labour to ensure that, within this reform process, the technical assistance provided through this Project will promote the inclusion and support to vulnerable households within indigenous communities.

.

E. Environment

50. The Project focuses on institutional reforms and capacity building of the fiscal policy system, social protection, and financial sector. It does not have any direct environmental impact, and the Project does not include any civil works. The TA will assist the government in designing national, poverty-targeted benefits. The “project area” is the nation, which consists of 30 ethnic groups. The Indigenous Peoples safeguard policy OP/BP 4.10 has been triggered because of a small ethnic group (about 400 Tsaatan reindeer herders) meets the Bank’s definition of “indigenous”. Therefore, an Indigenous Peoples Plan was prepared and disclosed by the Ministry of Social Welfare and Labour, and the Project rated as a Category B.

14

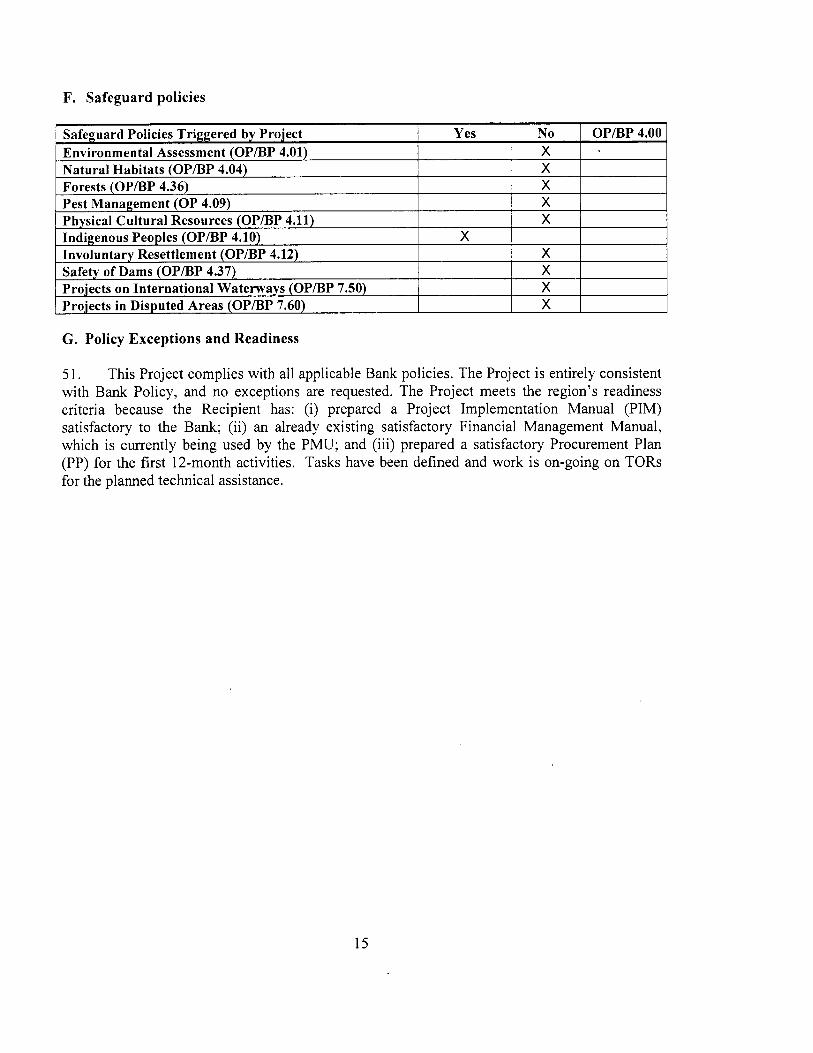

F. Safeguard policies

G. Policy Exceptions and Readiness

5 1. This Project complies with all applicable Bank policies. The Project is entirely consistent with Bank Policy, and no exceptions are requested. The Project meets the region’s readiness criteria because the Recipient has: (i) prepared a Project Implementation Manual (PIM) satisfactory to the Bank; (ii) an already existing satisfactory Financial Management Manual, which is currently being used by the PMU; and (iii) prepared a satisfactory Procurement Plan (PP) for the first 12-month activities. Tasks have been defined and work is on-going on TORS for the planned technical assistance.

15

Annex 1: Country and Sector Background

MONGOLIA: Multi-Sectoral Technical Assistance Project

I. Country Context

1. Mongolia has made tremendous political and economic progress since the transition that started in the 1990s. Five parliamentary elections were held in the period since, and all were deemed free and fair by international observers. Democratic laws and institutions were put in place, an active media developed, and a small, but vocal civil society increasingly engages on the political front. Similarly, in the past two decades, Mongolia has seen considerable success in moving from a centrally-planned to a market-based economy.

2. While Mongolia’s political environment is dynamic and open, this has also brought its own challenges to the process of governing, with three governments holding office in the last few years. A new bi-partisan coalition government was formed in the fall of 2008 following some short-lived disturbances after the June 2008 parliamentary elections. However, presidential elections held in May 2009 proceeded smoothly, with a junior member of the governing coalition defeating the incumbent. The recent political transition when the Prime Minister resigned due to health reasons in October 2009, was also smooth with the new Prime Minister asserting his continued support for the reform agenda. More generally, there is currently significant bi- partisan consensus on, and commitment to, the reform efforts needed to deal with the economic crisis. However, it is unclear how additional political pressures in the run-up to the next round of parliamentary elections, which are due in 201 2, may affect this commitment.

3. Major mineral deposits, including prospects in the Gobi region, when developed, have the potential to increase significantly incomes and government revenues. But the risks of a mineral-dependent economy have also been underscored by deficiencies in Mongolia’s management of the recent boom, which made it more difficult to adjust to the impact of the global downturn. In addition, as in most mineral-rich economies, managing the resource revenues consistently and sustainably, puts a high premium on governance reforms. The adjustments needed will take place over the medium term, and include reforms that protect the poor, maintain critical infrastructure, improve public investment decisions, restructure the banking sector, and resolve key obstacles for mining and infrastructure development.

A. Economic Context and Macroeconomic Outlook

4. Mongolia was one of the East Asian economies hardest hit by the global downturn. The principal transmission channel was the collapse in mineral prices, especially copper, from the middle of 2008. Mongolia’s budget relied heavily on mining revenues (30 percent of revenues in 2008) and, with the Central Bank pursuing a de facto peg of the local currency to the dollar, there was a direct transmission of the falling international copper prices to revenue losses. While the government did save part of its mining windfall during the “boom” years, it had also funded large increases in untargeted social expenditures, wages and salaries, and poorly-screened investment projects. When the “boom” turned into “bust”, the modest fiscal surplus quickly turned into a large deficit which the fiscal savings of the previous years proved insufficient to fund. At the same time, the external current account also swung into a large deficit, and the

16

financial sector, which had been overheating during the boom period, ran into serious problems, with a major bank having to be put under conservatorship. All the major copper producers in the world were affected by the collapse in copper prices, but, because of its particularly weak policy framework, Mongolia's experience was perhaps the most severe (see Box 1). The contrast with Chile is particularly striking: Chile's banking sector was unaffected due to prudent lending policies during the boom years, its exchange rate was flexible (so it absorbed part of the shock), and Chile was able to self-finance a large stimulus package to support its economy by drawing upon fiscal savings made during the boom years under its structural balance rule.

Figure 2. Changes in GDP growth 2008 to 2009 and

% change (GDP decline). % of GDP (balance) ice in 2008

Box 1. How did other copper exporters experience the global downturn?

Figure 3. Deteriorating fiscal balances % of GDP

'he largest copper exporters in the world, in terms of hare of copper to total exports, are Zambia, Chile, longolia (MNG), Papua New Guinea (PNG), and Peru Figure 1). These countries experienced the same global opper price collapse, but the impact on their economies /as different.

, I 1 five countries are facing GDP growth declines in 009, but Peru and Mongolia are facing the largest eclines (Figure 2 ) . All countries are projected to have a scal deficit in 2009. However, Chile and PNG had run irge fiscal surpluses during the boom times up to 2008, rhereas Mongolia and Zambia were already in deficit in 008 (Figure 3). And Mongolia's non-mining fiscal eficit was the largest of all (Figure 2 ) . The current :counts of all countries except PNG were also strongly npacted by the copper price collapse. However, Zambia i d Mongolia saw the largest deteriorations, and :quested external assistancea (Figure 4). CPI inflation 'as the highest in Mongolia since 2007, evidence of the irgest domestic boom, compared to the other four xmtries (Figure 5).

Figure 1 . Export concentration index* (right axis, bar), copper share in exports in 2007 (left axis, line) 1.0 1 . r 60

Nore: * Herfindahl index: sum of squares of % export shares across all commodities (range: 0-1 00).

non-mining fiscal balan

10 .... +... Chile Chile Peru PNG MNG Zambia

~ 1 &..>k*-.c - - - Peru / I I ' 1 I ' I I ' I I ' I I . r \. - +PNG

--I-- MNG \ - Zambia

17

Figure 4. Variable current account adjustments % of GDP

*o--oo--*

54 .......................

- . - . Peru -- +PNG \

-15 A --(-- MNG Zambia

~ -2006 2007 2008

2003 2004 2005 2006 2007 2008

I

Figure 5. Rising CPI inflation YO year-on-year change

--4-- Chile - . - . Peru 25 .. I I

20 ; -- +PNG *MNG / 1 . . .......

Copper export dependence, or a high export concentration, alone does not explain the differences in performance during the crisis. For example, Zambia and Chile are the most dependent on copper exports, but their expected drop in GDP is less than that of Mongolia and Peru. Zambia opened a major new copper mine in late-2008 (the only country to do so). The increase in copper output mitigated the downturn. Zambia also removed the windfall tax on mining to continue to attract new mining investments and prevent :xisting operations from being scaled down prematurely. It also benefited from debt relief as a result of good economic performance. Peru had accumulated sizeable fiscal surpluses for the previous three years, md used the mineral windfall largely by increasing savings and reducing public 'debt. Chile, finally, finds itself in a good position to weather the storm: it benefited from a fiscal rule which limited expenditure juring boom times, inflation targeting, a flexible exchange rate, a copper stabilization fund to help ensure :hat the fluctuations in copper prices do not spillover into the rest of the economy, and adequate access to Foreign financing.

Source: UN Comtrade database, Bank of PNG, IMF Article IV reports, World Bank. ' In response to the crisis, Zambia received a substantial increase in financing of its ongoing IMF poverty reduction program, although ts access to IMF financing is still only around 50 percent of its quota, whereas Mongolia received 300 percent under its SBA. For :ompleteness, Peru has had an IMF Stand-By Arrangement since early 2007, but this is considered precautionary with low access to MF resources, and Peru has not requested any increase in the loan amount.

B. Recent Economic Developments

5. Since the first DPC operation was approved by the Board in June 2009 there has been a substantial stabilization of the macroeconomic situation (see Table 3 and Figure 6). Two factors have contributed to this improvement. First, the government has taken comprehensive and strong policy action on fiscal, monetary, exchange rate and financial policies, supported by international and bilateral budget and balance of payments support, and technical assistance. The government was also able to conclude the major Oyu Tolgoi (OT) mining investment agreement. As a result of the signing of this agreement, positive sentiment has returned to the mining sector, and the overall economic outlook has improved significantly. GDP growth for 2010 is projected to rebound to over 7 percent of GDP, up from a slight decline in 2009 on the back of a huge increase in OT-related infrastructure spending.

~~

See discussion of key measures in Section IV. 1

18

6. Second, recent external sector developments have been supportive due to the sustained recovery in mineral prices and improvement in external demand. For instance, by the start of 2010, copper prices were only about a fifth below their peak in August 2008. Meanwhile, economic growth in China, Mongolia’s main export partner, continues to be strong, fueled by a massive fiscal and monetary stimulus package.

Table 3. Mongolia selected economic indicators

2004 2005 2006 2007 2008 2009 2010f Real GDP growth (percent yoy) 10.6 7.3 8.6 10.2 8.9 -1.6 7.3

10.9 9.6 5.9 14.1 23.2 1.9 7.5

(percent of GDP) -1.9 2.6 8.2 2.8 -4.9 -5.4 -4.0 Total expenditures (percent of GDP) 34.9 27.5 28.4 38.0 41.0 38:3 38.5

Consumer price index (end-period percent yoy change) Overall government balance including grants

Total revenues and grants (percent of GDP) 33.0 30.0 36.6 40.9 36.1 32.9 34.5

1.8 2.5 4.6 5 .O 3 .O 4.9 4.0 Gross FX reserves (months of imports of goods and services) Exchange rate (MNT/US$, eop) 1209 1221 1165 1170 1268 1447

Current account balance (percent of GDP) 1.3 1.3 7.0 6.7 -14.0 -5.6 -11.0

Note: Preliminary numbers for 2009. Source: Bank of Mongolia, IMF, and World Bank staff estimates

7. Together these factors have laid the grounds for a tentative recovery, as evident in the latest Q4 data for 2009. After three successive quarters of contraction, GDP growth in the final quarter came in at 3.9 percent year-on-year (yoy). Industrial production also rebounded at the end of 2009 while the bottoming out of the downturn was reflected in inflation turning positive after briefly dipping into negative territory between August and November 2009. The official unemployment rate stood at 3.3 percent since December 2009, down from 3.7 percent in June, although these numbers likely grossly underestimate actual unemployment levels. Meanwhile, fiscal retrenchment supported by a recovery in mining-related revenues resulted in deficit of 5.4 percent in 2009. This compares favorably with a full-year budget target of around 5.8 percent and is only slightly worse than the outturn in 2008 (see also discussion in Section I1 A. of this Annex).

8. On the external front, the exchange rate has stabilized since April after the central bank abandoned its de facto peg, introduced a transparent bi-weekly foreign exchange auctioning mechanism, and in order to restore confidence in the local currency, raised interest rates in March 2009 to 14 percent from 9.75 percent. This, combined with a narrowing of the trade deficit, has helped the central bank to rebuild reserves which reached record levels of US$1,145 million in December 2009. Reserves have also been boosted by the disbursement of the IMF SBA tranches, the OT prepayment loan, project funding from the International Fund for Agricultural Development (IFAD) and an SME Development Project from Japan, and deposits from commercial banks. The nominal depreciation and falling domestic inflation contributed to a roughly 20 percent fall in the real effective exchange rate over ,2009, unwinding an appreciation of similar magnitude in 2008 which was driven by rising inflation.

21t had initially been forecast in early 2009 that the 2009 budget deficit was heading for 12 percent of GDP if measures to control spending and to compensate for the revenue loss as copper prices fell were not taken.

19

Trade balances have improved significantly as the recovery in external demand and rising commodity prices have helped moderate the rate of contraction of Mongolia's exports. With imports falling faster than exports in 2009, the current account deficit narrowed to 4 percent of GDP in the final quarter of 2009, after peaking at 13 percent in Q1. It was primarily financed by net capital inflows in the financial account. Direct investment by foreign companies (FDI), mainly in the mining sector, also increased substantially over the course of the year, but remains slightly lower than 2008 levels. Net borrowing from abroad by both government and the private sector jumped in 2009, due to the donor disbursement and loans to the commercial banks.

Figure 6: Recent macro-economic developments in Mongolia

Recent external sector developments have been supportive.. . - Growth in China's real industrial value added (RHS)

----- International copper price (LHS)

- International gold price (LHS) Index Jan 2008=100 Change year-on- 140 7 year ; 30%

The exchange rate has stabilized and reserves are accumulating.

Official reserves (LHS) --- .......... Parallel market exchange rate (RHS)

- Official market exchange rate (RHS)

US$ million MNT per US$ 1,200 -

600 -

400 -

0 4 L 1,000

... and the trade deficit is shrinking as import compression exceeds that of exports. - Trade balance (rolling 12-month sum), RHS - Export growth (3-month moving average, 3mma), LHS - - - Import growth (3mma), LHS .

Change year-on-year

120% I \

US$ billion i- 2

l i

-80% 1 i I

-120% J L -2

There are tentative signs of an economic recovery.. .

CPI

+ RealGDP

- - - .......... Core price index

- Real industrial production (3mma) Change year-on-year

40% 1

30%

20%

10%

0%

-10%

-20%

-30%

20

... while the fiscal deficit lras improved reflecting expenditure restraint and a recovecv in mining receipts

Bank deposits have recovered but asset quality is deteriorating and credit availability remains tight. 0 NPLs including principal in arrears excluding Anod - NPLs due to Anod and Zoos (RHS)

and Zoos (RHS) - Fiscal balance excluding net lending (RHS)

- Total revenue and grants (LHS)

- - - Total expenditures (LHS)

..

.......... Deposits nominal value (LHS)

- Loans nominal value (LHS)

Percent of GDP, 12-month rolling sum Index J u n e 2008=100 Share of total loans 45% 1 I O

- 20%

15%

10% 85

30%

-6% -8% -10% 75

Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09

Sources: Bank of Mongolia, National Statistical Office, Ministry of Finance, Haver Analytics, World Bank

9. The authorities’ policy response since the beginning of 2009, including liquidity support for banks, a blanket deposit guarantee and a sharp increase in the policy rate, has led to a recovery in the level of deposits. However, weaknesses in the quality of banking sector balance sheets became increasingly apparent during 2009 in turn contributing to a sharp reduction in credit availability. NPLs and loans with principals in arrears currently amount to slightly more than a fifth of total outstanding loans, roughly double the levels in December 2008. Banks’ credit exposures also remain highly concentrated, with the top 50 borrowers by loan size accounting for around 30 percent of total loans at end 2009. Write-downs of loans are increasingly hitting bank capital, with a second bank, Zoos, failing at the end of 2009.3. The availability of credit also declined during the crisis period with banks increasingly choosing to use funds to purchase central bank bills for example, although there are currently signs of a tentative recovery in loan issuance.

10. Real interest rates continue to be extremely high, posing a constraint to the recovery of the private sector. Despite the Bank of Mongolia having cut its official policy rate three times since May 2009 from 14 percent to 10 percent in September, nominal interest rates on both local currency deposits and loans barely fell in 2009. On the deposit side, the search for funds by banks facing liquidity difficulties is likely an important driver of the high rates while the lending rates likely reflected concerns over credit quality, and high funding costs. With inflation falling sharply this has led to a surge in ex post real borrowing costs which rose to above 20 percent. Such high real rates also constrain the room the Bank of Mongolia has to raise rates, if macroeconomic conditions would seem to warrant this.

The first one, the Anod Bank, failed at the end of 2008. Both Zoos and Anod were placed into receivership at the 3

end of 2009.

21

11. Despite the improvement in the economic situation, there remain sizeable risks to the economic and policy outlook, in particular relating to banking sector solvency and to fiscal financing pressures in the next few years before mineral revenues associated with OT start to flow into the budget (around 2014/15). And, given the importance of the OT project to the economy, changes in the scale and timing of its progress would have large implications for macro outcomes in individual years. There is also uncertainty on the extent to which increased OT infrastructure-related investments will have positive spillovers for the domestic economy.

11. Sector Context

A. Fiscal Sector

Background

12. The slump in copper prices at the end of 2008 severely undermined fiscal revenues, requiring a sharp adjustment of budgeted expenditures to restrain the fiscal deficit. The collapse in copper prices at the end of 2008 led to a substantial weakening of Mongolia’s mining sector receipts, which account for roughly 40 percent of corporate income tax and 90 percent of dividend revenues. As part of the fiscal adjustment, the government has sharply reined in spending on infrastructure and goods and services. The budget for 2010, approved by Parliament in November 2009 targets a budget deficit of 5 percent of GDP in 2010, compared with an actual outturn of 5.4 percent in 2009. The budget deficit in the amended budget of April 2010 was 6.4 percent of GDP.

13. The fiscal deficit improved in late 2009 as the decline in revenues stabilized and as spending was curtailed. Overall, the fiscal balance in 2009 came in at MNT 328 billion (around 5.4 percent of GDP) compared with a full-year budget target of MNT 364 billion (around 5.8 percent of projected GDP) and not much worse than the deficit of 5.0 percent in 2008. The revenue intake in 2009 was some 7.5 percent lower than in 2008 in nominal terms mainly reflecting the drop in mining revenues due to the fall in copper prices. However, the recovery in copper prices helped to staunch the decline, with total revenues and grants increasing by 3 1 percent in the fourth quarter of 2009 quarter-on-quarter.

14. With the government also cutting back on spending in order to maintain fiscal sustainability and meet the fiscal deficit targets, total spending was some 5.7 percent lower in 2009 in nominal terms than in 2008. The largest cuts were made to capital expenditure and subsidies. Offsetting these was an increase in wages and salaries, unexpected repair expenditures due to flood damage and spending on containing the spread of swine flu and dzud relief efforts. There were also substantial fiscal costs associated with the blanket guarantee law and the failures in the banking sector.

15. However, significant fiscal financing pressures are expected in the near term. This is because government revenues will come under pressure from the expiration of the WPT in 20 1 1 , with net revenue losses estimated to be in the region of 2 percent of GDP. Bank restructuring costs, expected to be substantial, will also add to government spending. In this regard, it is therefore imperative to agree on the principles and conditions for the use of public funds for

22

possible bank bailout. Finally, with Mongolia rated as a sub-investment credit rating, borrowing on commercial terms is likely to be costly.

16. Given the limited financing options available, the next two to three years will require a continued fiscal effort to bring the budget back to a sustainable path. Over 2010 and 201 1 the availability of IF1 program financing is projected to decline. Increased domestic debt financing could further crowd out the private sector or there may be the risk of inflationary financing. Sustained fiscal effort will therefore be required to reduce further the deficit and avoid potential risks to debt sustainability through increased non-concessional external financing.

Challenges

17. As in the first DPC, the fiscal policy reforms supported under DPC2 focus on two areas: first, improving capital budget planning, and second, protecting the maintenance of key infrastructure.

18. Between 2002 and 2009, Mongolia went through a classic boom-and-bust cycle, exposing the poor fiscal framework in place. During the “boom” years, the budget became increasingly dependent on mining revenues, and the non-mining deficit, i.e. expenditures relative to non-mining revenues, rose substantially. The windfall mining revenues were used to massively increase (poorly planned) capital expenditures and to fund across the board wage increases and untargeted social transfers. When the “bust” came, the budget swung into a large deficit, which would have been impossible to finance without large expenditure cuts and donor assistance.

19. Going forward, the challenges are three-fold: how to insulate the budget from mineral price fluctuations, how to efficiently manage the massive increase in revenues starting in 201 6, and how to improve the efficiency of the locally invested part of the increased revenues.